#Air Quality Monitoring System Market Analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s website traffic is steadily declining.

Text

Air Quality Monitoring System Market Innovations, Smart Sensors and IoT Integration

The global air quality monitoring system market was estimated at USD 5.80 billion in 2024 and is projected to reach USD 8.89 billion by 2030, growing at a CAGR of 7.5% from 2025 to 2030. The market is being propelled by advancements in technologies such as the Internet of Things (IoT) and sensor innovations, which are transforming how air quality data is collected, analyzed, and applied. These advancements are enabling more proactive, data-driven responses to air pollution and its effects on human health and the environment.

IoT technology allows physical devices, such as air quality sensors, to connect and communicate through the internet, forming dynamic networks capable of real-time data sharing. This connectivity turns traditional air quality monitoring systems into intelligent, integrated infrastructures. These networks provide detailed insights into pollution levels and patterns, contributing to smart city development. They can be synchronized with other smart systems—such as traffic control and public health networks—to generate timely and coordinated responses to environmental issues.

For example, real-time air quality data can inform traffic management systems, prompting them to reduce vehicle flow during periods of high pollution. Additionally, the widespread adoption of IoT in air monitoring is fueling innovation in sensor development. Modern sensors are now more compact, energy-efficient, and capable of detecting a wider range of pollutants at lower concentrations. This not only allows for broader deployment across various environments but also enhances the accuracy and reliability of air quality assessments.

Key Market Trends & Insights

North America led the global air quality monitoring system market with a revenue share of over 36% in 2024. This dominance is largely due to increasing acid rain incidents, which have led to widespread acidification of regional lakes. In response, regulatory bodies have enforced strict air quality monitoring mandates. The market also benefited from initiatives like NASA’s Tropospheric Emissions: Monitoring of Pollution (TEMPO) satellite mission launched in April 2023.

By product type, the outdoor air quality monitoring segment dominated with over 65% of global revenue in 2024. This growth is driven by urbanization, rising personal spending, and increased industrial activities. Technological innovations are further enhancing these monitoring systems, making them more reliable and efficient.

By pollutant type, the chemical segment accounted for the largest market share in 2024. The demand for systems capable of measuring hazardous chemicals such as volatile organic compounds (VOCs), sulfur oxides (SOx), nitrogen dioxide (NO₂), and particulate matter (PM) has risen significantly due to growing health concerns.

By component, the hardware segment captured the largest share of market revenue in 2024. This is attributed to the growing number of system integrators who procure components like sensors and display units from hardware manufacturers, supporting the proliferation of integrated systems.

By end-use, the commercial segment led the market in 2024. With the integration of IoT, commercial facilities can now monitor and adjust their ventilation and filtration systems in real time. Smart buildings use these technologies to maintain indoor air quality efficiently, reduce energy consumption, and create healthier work environments.

Order a free sample PDF of the Air Quality Monitoring System Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 5.80 billion

2030 Projected Market Size: USD 8.89 billion

CAGR (2025-2030): 7.5%

Leading Region (2024): North America

Key Companies & Market Share Insights

Major players in the market include General Electric, Aeroqual, Emerson Electric Co., Siemens, Merck KGaA, and Teledyne Technologies Incorporated. These companies are leveraging mergers, acquisitions, collaborations, and advanced technologies—particularly artificial intelligence—to improve product offerings and maintain competitive advantage.

General Electric (GE) delivers sophisticated air quality monitoring systems integrated with IoT and analytics. These systems are widely used in emissions-intensive sectors like manufacturing and energy, offering real-time data and actionable insights. GE’s AI-driven platforms not only monitor pollution but help optimize operations to meet environmental standards and reduce emissions.

Aeroqual designs a wide range of air quality monitors, from portable devices to fully integrated systems for both indoor and outdoor use. Known for precision and usability, Aeroqual’s solutions support research, regulatory compliance, and industrial monitoring. The company also invests in AI-based technologies to enhance data accuracy and deliver predictive analytics, enabling proactive air quality management across sectors.

Key Players

3M

General Electric

HORIBA Scientific

Aeroqual

Emerson Electric Co.

Siemens

Merck KGaA

Teledyne Technologies Incorporated.

Testo SE & Co. KGaA

Thermo Fisher Scientific Inc.

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global air quality monitoring system market is experiencing strong growth, driven by rapid advancements in IoT, sensor technology, and AI-based analytics. Rising awareness of public health risks, tightening environmental regulations, and the need for real-time pollution control are encouraging widespread adoption across commercial, industrial, and governmental sectors. North America continues to lead the market due to stringent policies and technological adoption, while innovations in hardware and system integration are setting new standards for efficiency and reliability. As smart cities and sustainable infrastructure initiatives gain momentum globally, air quality monitoring systems will play an increasingly critical role in ensuring environmental and public health outcomes.

#Air Quality Monitoring System Market#Air Quality Monitoring System Industry#Air Quality Monitoring System Market Growth#Air Quality Monitoring System Market Analysis#Air Quality Monitoring System Market Forecast#Air Quality Monitoring System Market Size

0 notes

Text

Explore the Indonesia Air Quality Monitoring System Market growth, challenges, and top players with forecasts up to 2028. Gain insights into revenue trends, market outlook, and key developments shaping the industry's future.

#Indonesia Air Quality Monitoring System Market research report#Indonesia Air Quality Monitoring System Market report#Indonesia Air Quality Monitoring System Market size#Indonesia Air Quality Monitoring System Market trends#Indonesia Air Quality Monitoring System Market share#Indonesia Air Quality Monitoring System Market revenue#Indonesia Air Quality Monitoring System Market outlook#Indonesia Air Quality Monitoring System Future Market#Indonesia Air Quality Monitoring System Market insights#Indonesia Air Quality Monitoring System Market forecast#Indonesia Air Quality Monitoring System Market analysis#Indonesia Air Quality Monitoring System Market top players#Indonesia Air Quality Monitoring System Market major players#Indonesia Air Quality Monitoring System Market leading players#Indonesia Air Quality Monitoring System Market emerging players#Indonesia Air Quality Monitoring System Market players#Indonesia Air Quality Monitoring System Market competitors#Indonesia Air Quality Monitoring System Market growth#Indonesia Air Quality Monitoring System Market growth factors#Indonesia Air Quality Monitoring System Market development#Indonesia Air Quality Monitoring System Market challenges

0 notes

Text

Ambient Air Quality Monitoring System Market May Set New Growth Story

Advance Market Analytics published a new research publication on "Ambient Air Quality Monitoring System Market Insights, to 2028" with 232 pages and enriched with self-explained Tables and charts in presentable format. In the Study you will find new evolving Trends, Drivers, Restraints, Opportunities generated by targeting market associated stakeholders. The growth of the Ambient Air Quality Monitoring System market was mainly driven by the increasing R&D spending across the world.

Get Free Exclusive PDF Sample Copy of This Research @ https://www.advancemarketanalytics.com/sample-report/10614-global-ambient-air-quality-monitoring-system-market Some of the key players profiled in the study are: Thermo Fisher Scientific (United States), Emerson Electric (United States), General Electric (United States), Siemens AG (Germany), Teledyne Technologies (United States), PerkinElmer, Inc. (United States), Agilent Technologies, Inc. (United States), Spectris plc (United Kingdom), 3M Company (United States), Honeywell International Inc (United States). Scope of the Report of Ambient Air Quality Monitoring System Ambient air quality monitoring is required to determine the existing quality of air, evaluation of the effectiveness of control programme and to identify areas in need of restoration and their prioritization. Ambient air quality monitoring system is the device designed for realizing monitoring function. Ambient Air Quality Monitoring Systems or AAQMS monitors the level of pollutants. From a single analyzer to complete turnkey systems (Both Mobile and Fixed) with shelters, hard wired or wireless data transfer to the pollution boards. Chemtrols provides a wide range of solutions to meet much of the Ambient Air Quality Monitoring demands. The titled segments and sub-section of the market are illuminated below:

by Type (Portable Monitoring System, Stationary Monitoring System), Application (Indoor Monitoring System, Outdoor Monitoring System), Pollutant (Gas, VOC, Particulate Matter, Biological), End user (Government, Petrochemical, Commercial) Market Trends: Fast adoption of new advanced air quality monitoring technologies,

Opportunities: Ongoing technological advancements in the field of gas analyzers & particulate sensors

Market Drivers: Supportive government regulations for effective air pollution monitoring and control

Increasing public-private funding for effective air pollution monitoring Region Included are: North America, Europe, Asia Pacific, Oceania, South America, Middle East & Africa Country Level Break-Up: United States, Canada, Mexico, Brazil, Argentina, Colombia, Chile, South Africa, Nigeria, Tunisia, Morocco, Germany, United Kingdom (UK), the Netherlands, Spain, Italy, Belgium, Austria, Turkey, Russia, France, Poland, Israel, United Arab Emirates, Qatar, Saudi Arabia, China, Japan, Taiwan, South Korea, Singapore, India, Australia and New Zealand etc. Have Any Questions Regarding Global Ambient Air Quality Monitoring System Market Report, Ask Our Experts@ https://www.advancemarketanalytics.com/enquiry-before-buy/10614-global-ambient-air-quality-monitoring-system-market Strategic Points Covered in Table of Content of Global Ambient Air Quality Monitoring System Market:

Chapter 1: Introduction, market driving force product Objective of Study and Research Scope the Ambient Air Quality Monitoring System market

Chapter 2: Exclusive Summary – the basic information of the Ambient Air Quality Monitoring System Market.

Chapter 3: Displayingthe Market Dynamics- Drivers, Trends and Challenges & Opportunities of the Ambient Air Quality Monitoring System

Chapter 4: Presenting the Ambient Air Quality Monitoring System Market Factor Analysis, Porters Five Forces, Supply/Value Chain, PESTEL analysis, Market Entropy, Patent/Trademark Analysis.

Chapter 5: Displaying the by Type, End User and Region/Country 2015-2020

Chapter 6: Evaluating the leading manufacturers of the Ambient Air Quality Monitoring System market which consists of its Competitive Landscape, Peer Group Analysis, BCG Matrix & Company Profile

Chapter 7: To evaluate the market by segments, by countries and by Manufacturers/Company with revenue share and sales by key countries in these various regions (2023-2028)

Chapter 8 & 9: Displaying the Appendix, Methodology and Data Source finally, Ambient Air Quality Monitoring System Market is a valuable source of guidance for individuals and companies. Read Detailed Index of full Research Study at @ https://www.advancemarketanalytics.com/reports/10614-global-ambient-air-quality-monitoring-system-market

Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Middle East, Africa, Europe or LATAM, Southeast Asia. Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global Ambient Air Quality Monitoring System Market#Ambient Air Quality Monitoring System Market Demand#Ambient Air Quality Monitoring System Market Trends#Ambient Air Quality Monitoring System Market Analysis#Ambient Air Quality Monitoring System Market Growth#Ambient Air Quality Monitoring System Market Share#Ambient Air Quality Monitoring System Market Forecast#Ambient Air Quality Monitoring System Market Challenges

0 notes

Text

Exhaust Gas Induction Sensor Market - Latest Study with Future Growth, COVID-19 Analysis

Exhaust Gas Induction Sensor Market, Trends, Business Strategies 2025-2032

The global Exhaust Gas Induction Sensor Market size was valued at US$ 567.89 million in 2024 and is projected to reach US$ 834.56 million by 2032, at a CAGR of 5.67% during the forecast period 2025–2032.

Exhaust gas induction sensors are critical components designed to detect and measure the concentration of harmful emissions, including carbon monoxide, nitrogen oxides, and hydrocarbons, in automotive and industrial environments. These sensors play a vital role in monitoring air quality and ensuring compliance with stringent environmental regulations, particularly in the automotive sector where emission standards continue to evolve.

The market is witnessing steady growth driven by increasing regulatory pressure to reduce vehicle emissions, coupled with rising demand for fuel-efficient combustion systems. While automotive applications dominate the sector, industrial adoption is growing as manufacturing facilities prioritize emission monitoring. Key technological advancements focus on enhancing sensor accuracy and durability under extreme conditions. Major players like Bosch, Denso, and Continental are investing in next-generation sensor technologies to address emerging requirements in electric and hybrid vehicle platforms.

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis. https://semiconductorinsight.com/download-sample-report/?product_id=103239

Segment Analysis:

By Type

Portable Device Segment Dominates Due to Rising Demand for Flexible Gas Monitoring Solutions

The market is segmented based on type into:

Portable Device

Fixtures

By Application

Automated Industry Leads Due to Stringent Emission Regulations in Manufacturing Sector

The market is segmented based on application into:

Automated Industry

Biomedical Science

Aerospace

Others

By Technology

Electrochemical Sensors Dominate Due to High Accuracy in Toxic Gas Detection

The market is segmented based on technology into:

Electrochemical

Infrared

Semiconductor

Catalytic

Regional Analysis: Exhaust Gas Induction Sensor Market

North America The North American exhaust gas induction sensor market is driven by stringent emission regulations, particularly in the U.S., where the Environmental Protection Agency (EPA) mandates strict monitoring of pollutants. The automotive sector remains a key adopter, with major manufacturers like Denso and Delphi Automotive integrating advanced sensors to comply with Tier 3 and LEV III standards. Additionally, increasing investments in industrial automation and smart infrastructure—such as the U.S. government’s allocation of $1.2 trillion for infrastructure modernization—are accelerating demand for high-accuracy sensors. The region is also witnessing a shift toward IoT-enabled solutions, with sensor manufacturers focusing on real-time data analytics capabilities.

Europe Europe leads in environmental sustainability initiatives, with the EU’s stringent Euro 6 and Euro 7 norms pushing automotive OEMs to adopt precise exhaust gas sensors. Countries like Germany and France are at the forefront, leveraging their strong automotive and industrial bases to drive innovation. The region’s emphasis on circular economy principles has also spurred R&D in low-power, recyclable sensor materials. However, high manufacturing costs and competition from Asian suppliers remain challenges. Recent collaborations between Bosch and Infineon for next-gen sensor technologies highlight Europe’s commitment to maintaining its competitive edge.

Asia-Pacific The Asia-Pacific region dominates global sensor demand, accounting for over 40% of market share, fueled by rapid industrialization in China and India. China’s “Blue Sky” policy and India’s BS-VI emission standards are major growth drivers. While cost sensitivity keeps demand high for mid-range sensors, Japanese and South Korean manufacturers are pivoting toward high-sensitivity OEM solutions for premium automotive and aerospace applications. The region’s expanding electronics manufacturing ecosystem and government-backed smart city projects further contribute to long-term growth. However, inconsistent regulatory enforcement in Southeast Asia poses a hurdle for uniform market expansion.

South America South America’s market remains nascent but shows potential, particularly in Brazil and Argentina, where industrial emissions monitoring is gaining traction. The automotive aftermarket represents a key segment due to aging vehicle fleets requiring retrofit solutions. However, economic instability and fluctuating raw material prices hinder large-scale deployments. Recent trade agreements focusing on environmental technology transfer could open doors for international sensor suppliers, though local manufacturing limitations persist.

Middle East & Africa This emerging market is characterized by disparate growth patterns. Gulf Cooperation Council (GCC) countries, led by the UAE and Saudi Arabia, are investing heavily in smart infrastructure and refining operations, creating demand for industrial-grade sensors. In contrast, African markets face challenges due to limited technical expertise and funding. The region’s focus on oil & gas and mining operations, however, presents opportunities for ruggedized exhaust monitoring systems. Long-term prospects look promising as governments gradually align with global emission reduction goals.

List of Key Exhaust Gas Induction Sensor Companies Profiled

Denso Corporation (Japan)

Continental AG (Germany)

Delphi Automotive PLC (UK)

Hitachi Ltd. (Japan)

Robert Bosch GmbH (Germany)

Hella KGaA Hueck & Co. (Germany)

Infineon Technologies AG (Germany)

NGK Spark Plug Co., Ltd. (Japan)

Sensata Technologies Holding NV (Netherlands)

Tightening emission regulations worldwide are accelerating demand for exhaust gas induction sensors. Governments are implementing stricter Euro 7 and China 6B standards, requiring real-time monitoring of vehicle emissions. These sensors play a critical role in detecting pollutants like nitrogen oxides (NOx), carbon monoxide (CO), and hydrocarbons to ensure compliance. The automotive sector accounts for over 65% of sensor demand as manufacturers integrate advanced detection systems to meet these evolving standards while avoiding heavy penalties.

While electric vehicles reduce tailpipe emissions, hybrid models still require exhaust monitoring during combustion cycles. The rising popularity of plug-in hybrid electric vehicles (PHEVs), expected to grow at 15% CAGR through 2030, creates sustained demand for gas sensors. These vehicles operate in dual modes, necessitating sensitive detection systems that can switch between monitoring battery efficiency and traditional exhaust analysis. This technological crossover is driving innovations in multi-functional sensor designs.

Beyond automotive uses, industrial facilities are increasingly deploying exhaust sensors to monitor workplace safety and environmental compliance. Chemical plants, refineries, and manufacturing sites now integrate these sensors as part of smart factory initiatives. The industrial segment is projected to account for 22% of market revenue by 2027 as corporations prioritize employee health and regulatory adherence. Continuous emissions monitoring systems (CEMS) incorporating advanced sensors are becoming standard in high-risk environments.

The integration of artificial intelligence with exhaust gas sensors enables predictive failure detection and maintenance scheduling. Machine learning algorithms analyzing sensor data can identify performance deterioration patterns with 90% accuracy, allowing preventative action before system failures occur. This innovation is particularly valuable for mission-critical industrial applications where unplanned downtime can cost over $10,000 per hour. Major players are investing heavily in these smart monitoring solutions, anticipating 40% revenue growth in AI-enabled sensors by 2026.

Urban air quality monitoring networks present significant growth potential, with cities worldwide deploying sensor grids to track pollution hotspots. These systems require rugged, low-power sensors capable of continuous operation in diverse weather conditions. The municipal monitoring segment is projected to grow at 18% annually as environmental consciousness rises and IoT infrastructure expands. Next-generation sensors with wireless connectivity and solar power options are well-positioned to capture this emerging market.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103239

Key Questions Answered by the Exhaust Gas Induction Sensor Market Report:

What is the current market size of Global Exhaust Gas Induction Sensor Market?

Which key companies operate in Global Exhaust Gas Induction Sensor Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Browse More Reports:

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

0 notes

Text

Air Handling Units Market Report: Unlocking Growth Potential and Addressing Challenges

United States of America – Date – 17/07/2025 - The Insight Partners is proud to announce its newest market report, "Air Handling Units Market: An In-depth Analysis of the Air Handling Units Market " The report provides a holistic view of the Air Handling Units market and describes the current scenario as well as growth estimates for Air Handling Units during the forecast period.

Overview of Air Handling Units Market

There has been some development in the Air Handling Units market, such as growth and decline, shifting dynamics, etc. This report provides insight into the driving forces behind this change: technological advancements, regulatory changes, and changes in consumer preference.

Get the Sample of The Report: - https://www.theinsightpartners.com/sample/air-handling-units-market

Key findings and insights

Market Size and Growth

Historical Data: The Air Handling Units market is estimated to reach US$ XX million by 2031, with a CAGR of XX%. These estimates provide valuable insights into the market's dynamics and can inform future projections.

Here's a detailed analysis of the key factors, market segmentation, emerging trends, and growth opportunities within the Air Handling Units (AHU) market:

Key Factors Affecting the Air Handling Units Market

The Air Handling Units (AHU) market is a crucial segment of the HVAC (Heating, Ventilation, and Air Conditioning) industry, driven by several interconnected factors:

Drivers:

Stringent Regulations on Energy Efficiency and Indoor Air Quality (IAQ): Governments worldwide are implementing stricter building codes and regulations aimed at reducing carbon emissions, energy consumption, and improving indoor air quality. This directly mandates the adoption of highly efficient AHUs with advanced filtration and energy recovery systems. Post-pandemic, the focus on IAQ has intensified, further boosting demand.

Rapid Urbanization and Industrialization, Especially in Emerging Economies: The accelerated pace of urban development and industrial expansion in regions like Asia-Pacific (China, India, Southeast Asia) is leading to massive construction activities in commercial, residential, and industrial sectors. Each new building requires sophisticated HVAC systems, with AHUs being a central component.

Increasing Awareness of Indoor Air Quality (IAQ) and Health Impacts: Growing public and institutional awareness about the detrimental effects of indoor air pollutants on health (e.g., respiratory issues, allergies) is driving demand for AHUs with superior filtration capabilities (HEPA filters, UV-C light technology) to ensure healthier indoor environments.

Growth in Commercial and Industrial Construction: The construction of new office buildings, shopping malls, hotels, hospitals, data centers, educational institutions, and manufacturing facilities globally is a primary driver. These large-scale establishments require robust and efficient AHUs for optimal climate control and air circulation.

Technological Advancements in AHUs: Continuous innovation in AHU design, including the integration of smart controls, IoT, AI, variable speed drives (VSDs), and advanced heat recovery systems, is enhancing energy efficiency, improving performance, and enabling predictive maintenance, thereby increasing their appeal.

Spotting Emerging Trends

Technological Advancements:

The Air Handling Units (AHU) market is undergoing significant technological evolution, driven primarily by demands for energy efficiency, superior indoor air quality, and intelligent operation:

Smart AHUs and IoT Integration: This is a dominant trend. AHUs are increasingly equipped with a multitude of sensors (temperature, humidity, CO2, VOCs, particulate matter) and integrated with IoT platforms. This enables:

Remote Monitoring and Control: Facility managers can monitor performance, adjust settings, and receive alerts from anywhere.

Predictive Maintenance: AI/ML algorithms analyze operational data to predict potential failures, allowing for proactive maintenance and reducing downtime.

Optimized Energy Management: Real-time data allows for dynamic adjustments to airflow, fan speed, and coil temperatures based on occupancy, weather, and air quality, leading to significant energy savings.

Integration with Building Management Systems (BMS): Seamless communication with wider building automation systems for centralized control and holistic building performance optimization.

Advanced Energy Recovery Systems: Beyond traditional heat wheels and plate exchangers, innovations include:

Desiccant-Based Dehumidification: AHUs integrating desiccant wheels or liquid desiccant systems for highly efficient humidity control, especially crucial in hot and humid climates or specific industrial processes.

Thermodynamic Heat Pump AHUs: AHUs that incorporate integrated heat pump technology for simultaneous heating and cooling, offering high energy efficiency and reduced reliance on fossil fuels.

Phase Change Materials (PCMs): Integration of PCMs into AHU components (e.g., coils) to store and release thermal energy, reducing peak load demands and improving efficiency.

Changing Consumer Preferences:

"Consumer preferences" in the Air Handling Units market primarily refer to the evolving demands and priorities of building owners, facility managers, architects, contractors, and, indirectly, the occupants of buildings. These preferences have shifted significantly:

Strong Emphasis on Energy Efficiency and Sustainability: This is perhaps the most significant shift. Building owners and operators are keenly aware of escalating energy costs and their carbon footprint. They actively seek AHUs with high energy efficiency ratings (e.g., higher IEER, SEER2), variable speed drives (VSDs), and integrated heat/energy recovery systems to reduce operational expenses and meet green building certifications (e.g., LEED, BREEAM). The drive for decarbonization also influences choices, favoring electric heat pump-integrated AHUs.

Prioritization of Indoor Air Quality (IAQ) and Health: The COVID-19 pandemic dramatically heightened awareness of IAQ. Occupants and building managers now demand AHUs with advanced filtration (HEPA, UV-C), efficient ventilation strategies, and even air purification capabilities to ensure healthier and safer indoor environments, reducing the spread of airborne pathogens and allergens.

Regulatory Changes:

Regulatory changes play a pivotal role in shaping the Air Handling Units (AHU) market, primarily driven by environmental concerns, energy conservation mandates, and public health initiatives.

Energy Efficiency Standards and Building Codes:

Impact: Governments and regulatory bodies globally (e.g., Department of Energy (DOE) in the US, Ecodesign Directive in the EU, ASHRAE standards, local building codes) are continuously updating and tightening minimum energy efficiency requirements for HVAC equipment, including AHUs. This includes metrics like Seasonal Energy Efficiency Ratio (SEER2), Integrated Energy Efficiency Ratio (IEER), and specific energy consumption limits.

Consequence: Forces manufacturers to invest heavily in R&D to develop more energy-efficient AHU components (e.g., EC motors, advanced heat recovery systems, improved coil designs, better insulation) and entire units. It also accelerates the replacement cycle for older, less efficient units and promotes the adoption of technologies like VSDs and demand-controlled ventilation. Non-compliant products face market exclusion.

Growth Opportunities of the Air Handling Units Market

The Air Handling Units (AHU) market is ripe with growth opportunities, driven by evolving global needs and technological innovation:

Sustainable Building and Energy Efficiency Imperative: The global push towards net-zero buildings and stringent energy efficiency regulations (e.g., tightening SEER2, IEER, and new building codes) creates a sustained and growing demand for high-efficiency AHUs. Opportunities lie in:

Advanced Heat/Energy Recovery Systems: Developing and integrating more efficient heat wheels, plate exchangers, and desiccant-based systems.

Integrated Heat Pumps: Offering AHUs with integrated heat pump technology for highly efficient heating and cooling, aligning with electrification and decarbonization trends.

Optimized Fan and Motor Technologies: Further enhancing the efficiency of EC motors and fan designs.

Indoor Air Quality (IAQ) Enhancement: The heightened awareness of IAQ post-pandemic presents massive opportunities:

Advanced Filtration Solutions: Increased demand for AHUs incorporating HEPA/ULPA filters, UV-C light, bipolar ionization, and advanced chemical filtration for superior pathogen and pollutant removal.

Demand-Controlled Ventilation (DCV): Expanding the adoption of DCV systems that optimize fresh air intake based on real-time occupancy and CO2 levels, balancing IAQ with energy efficiency.

Integrated Air Purification: Opportunities for AHUs that go beyond filtration to actively purify air from odors, VOCs, and other gaseous contaminants.

Get The Infographics of Report:- https://in.pinterest.com/pin/869335534328439853

Conclusion

The Air Handling Units Market: Global Industry Trends, Share, Size, Growth, Opportunity, and Forecast Air Handling Units 2023-2031 report provides much-needed insight for a company willing to set up its operations in the Air Handling Units market. Since an in-depth analysis of competitive dynamics, the environment, and probable growth path are given in the report, a stakeholder can move ahead with fact-based decision-making in favor of market achievements and enhancement of business opportunities.

About The Insight Partners

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

0 notes

Text

Liquefied Natural Gas (LNG) Production Cost Analysis Report by Procurement Resource

Procurement Resource, a globally recognized leader in procurement intelligence and market research, is pleased to unveil its latest Liquefied Natural Gas (LNG) Production Cost Report. This exhaustive report offers a complete analysis of cost structures, market dynamics, production methodologies, and investment considerations associated with LNG production. Designed for investors, energy companies, and policymakers, the report provides essential tools for strategic decision-making and operational planning in the global LNG sector.

Liquefied Natural Gas: A Key Component in the Global Energy Transition

Liquefied Natural Gas (LNG) is natural gas (predominantly methane) that has been cooled to approximately -162°C (-260°F) to transform it into a liquid state. This liquefaction process reduces the gas’s volume by around 600 times, making it easier and more economical to transport across long distances where pipelines are not feasible.

LNG plays a crucial role in:

Energy diversification and security

Cleaner-burning fuel alternatives to coal and oil

Power generation and industrial heating

Transportation fuel for ships and heavy-duty vehicles

With increasing global demand for cleaner fuels and the push toward decarbonization, LNG is seen as a vital bridge in the transition to renewable energy.

Global LNG Market Dynamics

Expanding Demand and Infrastructure

The LNG market has experienced significant growth over the past decade, with key demand centers including:

Asia-Pacific: Led by China, Japan, South Korea, and India

Europe: Due to reduced reliance on Russian pipeline gas

North America: Both as a major exporter and domestic user

Emerging markets in Africa and Latin America

LNG is also gaining prominence in floating storage regasification units (FSRUs), small-scale LNG applications, and marine bunkering.

Key Market Drivers

Increased focus on energy diversification

Decline in domestic gas production in several countries

Global push for decarbonization and replacement of coal

Emergence of spot LNG trading and hub-based pricing

Production Process Overview

LNG production involves several stages of processing and cooling. The major components of the LNG supply chain include:

1. Natural Gas Pre-Treatment

Removal of impurities such as water vapor, hydrogen sulfide, carbon dioxide, and heavy hydrocarbons

These contaminants must be eliminated to prevent freezing and ensure product quality

2. Liquefaction

The purified gas is cooled in stages using refrigeration cycles (e.g., mixed refrigerant, cascade, or expander cycles)

Key technologies: APCI (C3MR), Shell DMR, and ConocoPhillips Optimized Cascade

3. Storage and Shipping

The LNG is stored in cryogenic tanks and transported via LNG carriers

Advanced insulation systems are used to reduce boil-off gas losses during transit

The report breaks down these stages and provides cost-per-unit analysis for each segment.

Technical Infrastructure and Equipment Needs

Establishing an LNG facility requires complex and capital-intensive infrastructure:

Gas treatment units

Heat exchangers and refrigeration compressors

Liquefaction trains

Cryogenic storage tanks

Boil-off gas handling systems

Marine loading terminals and pipelines

The report details equipment specifications, supplier benchmarks, and investment requirements for small-, mid-, and large-scale LNG plants.

Utilities and Operational Inputs

The LNG process is energy-intensive, requiring:

High electricity consumption for compression and cooling

Refrigerants such as propane, ethylene, or mixed hydrocarbons

Cooling water or air for heat exchange systems

Instrumentation and control systems for temperature and pressure monitoring

Procurement Resource’s report includes utility consumption tables and region-specific energy cost analysis.

Raw Material and Feedstock Cost Evaluation

Natural Gas as Feedstock

The cost of natural gas represents a major component of LNG production expenses.

Prices vary significantly depending on the region, supply agreements, and market benchmarks (e.g., Henry Hub, TTF, JKM).

The report provides a detailed cost trajectory of natural gas over recent years, analyzes the impact of global supply-demand shifts, and compares pipeline gas vs. LNG import economics.

Manpower and Human Resource Requirements

Running an LNG plant involves a multidisciplinary team, including:

Process and mechanical engineers

Plant operators and control room technicians

Maintenance crews

Safety and environmental compliance personnel

Marine terminal operators

The report provides estimates on manpower needs and salary structures based on plant size and location, ensuring compliance with global labor and safety regulations.

Quality Standards and Regulatory Compliance

Given LNG’s flammable and cryogenic nature, rigorous safety and quality protocols are essential:

Adherence to standards such as ISO 16903, NFPA 59A, and API guidelines

Monitoring of methane purity, calorific value, and impurity levels

Compliance with local environmental laws, emission caps, and GHG reporting frameworks

The report outlines mandatory certifications and testing procedures to ensure safe handling and global market eligibility.

Financial Overview and Cost Estimation

Capital Investment (CAPEX)

Depending on scale and technology, LNG plant investment ranges:

Small-scale LNG plants: $100–500 million

Mid-scale facilities: $500 million–$1.5 billion

Large-scale export terminals: $3–15 billion+

CAPEX includes land acquisition, engineering, procurement, construction (EPC), and commissioning.

Operating Cost (OPEX)

Ongoing expenses include:

Natural gas feedstock

Power and utilities

Refrigerant replenishment

Labor and maintenance

Transportation and shipping

Carbon compliance costs (in some jurisdictions)

The report provides a breakdown of OPEX on a $/MMBtu and $/ton basis.

Profitability Metrics

The report presents:

Return on Investment (ROI)

Net Present Value (NPV)

Internal Rate of Return (IRR)

Payback period under various market price scenarios

Sensitivity analysis for feedstock and energy price volatility

Sustainability and Decarbonization in LNG

The LNG sector is increasingly focused on reducing carbon intensity and adopting cleaner technologies:

Integration of carbon capture and storage (CCS)

Use of renewable-powered liquefaction units

Production of e-LNG using green hydrogen and captured CO₂

Certifications for carbon-neutral LNG cargoes

The report examines global trends in green LNG, regulatory incentives, and the long-term viability of decarbonized LNG pathways.

Regional Insights and Market Opportunities

The report evaluates cost drivers and investment potential across key regions:

North America: Abundant shale gas and export infrastructure

Qatar and Middle East: Low-cost LNG due to rich natural gas fields

Africa: Emerging export capacity (Mozambique, Nigeria)

Asia-Pacific: Rising demand and potential for small-scale LNG in island nations

Europe: LNG as a strategic substitute for pipeline gas

Request a Free Sample: https://www.procurementresource.com/production-cost-report-store/liquified-natural-gas/request-sample

Why Choose Procurement Resource?

Procurement Resource delivers value through:

Detailed cost modeling and benchmarking

Market-based production analysis

Customized feasibility and profitability studies

Real-time procurement intelligence and supplier analysis

Our expertise spans energy, chemicals, and industrial sectors, enabling clients to optimize procurement, reduce risk, and enhance ROI.

Contact Information

Company Name: Procurement Resource Contact Person: Ashish Sharma (Sales Representative) Email: [email protected] Location: 30 North Gould Street, Sheridan, WY 82801, USA Phone: UK: +44 7537171117 USA: +1 307 363 1045 Asia-Pacific (APAC): +91 1203185500

Connect With Us Online:

https://x.com/procurementres

https://www.linkedin.com/company/procurement-resource-official/

https://www.pinterest.com/procurementresource/

0 notes

Text

How to Improve the Purity of Recycled PET Flakes: Best Practices

Recycled PET flakes are a crucial resource in the circular economy. They are used in packaging, textiles, and other industries. However, the quality and purity of these flakes affect their usability and market value. Impurities such as labels, adhesives, dirt, and mixed plastics can reduce performance and limit applications.

Improving the purity of recycled PET flakes is crucial for manufacturers seeking to meet industry standards and produce high-quality products. This article shares best practices for enhancing flake purity, from collection to final processing.

Start with Clean and Sorted Input Materials

The first step in producing high-quality recycled PET flakes is ensuring that the input materials, which are PET bottles, are clean and properly sorted.

Best practices:

Source from reliable collection systems: Bottles collected through organized recycling programs tend to be cleaner and better sorted.

Remove caps and labels early: These are often made from different plastics and can contaminate the flakes.

Avoid mixing with other plastics: Keep PET separate from HDPE, PVC, and other materials to prevent cross-contamination.

Proper sorting at the beginning reduces the burden on downstream cleaning and separation processes.

Use Advanced Washing and Cleaning Systems

Washing is a critical stage in improving the purity of recycled PET flakes. It removes dirt, glue, food residues, and other contaminants.

Recommended washing techniques:

Hot water washing: Helps dissolve adhesives and remove stubborn residues.

Friction washers: Scrub the flakes to eliminate surface contaminants.

Chemical cleaning: In some cases, mild detergents or alkali solutions are used to enhance cleaning.

Multiple rinse cycles: Ensure thorough removal of cleaning agents and residues.

A well-designed washing line can boost the quality of recycled PET flakes.

Invest in Optical and Density-Based Sorting

Even after washing, some impurities may remain. Advanced sorting technologies help separate PET flakes from unwanted materials based on colour, density, and composition.

Sorting technologies to consider:

Optical sorters: Use cameras and sensors to detect and remove coloured or contaminated flakes.

Air classifiers: Separate light contaminants such as paper or film.

Float-sink tanks: Separate PET from other plastics based on density differences.

These systems are useful in large-scale recycling operations where manual sorting is not feasible.

Monitor and Control Contamination Levels

To maintain consistent quality, it’s important to test and monitor the purity of recycled PET flakes. This helps identify issues early and adjust processes accordingly.

Quality control measures:

Visual inspection: Check for colour consistency and visible contaminants.

Intrinsic viscosity (IV) testing: Measures polymer strength and degradation.

Contaminant analysis: Use lab tests to detect non-PET materials or chemical residues.

Batch tracking: Keep records of input sources and processing conditions.

Regular monitoring ensures that recycled PET flakes meet industry standards and customer expectations.

Train Staff and Maintain Equipment

Human error and poorly maintained equipment can lead to contamination. Training and maintenance are key to ensuring high-purity output.

Operational best practices:

Train workers on sorting and handling procedures

Schedule regular equipment cleaning and maintenance

Calibrate sensors and sorting machines periodically

Enforce safety and hygiene protocols in the facility

A well-managed recycling plant produces cleaner and better quality recycled PET flakes.

Conclusion: Clean flakes ensure better products

Improving the purity of recycled PET flakes is not just about meeting technical standards; it’s about creating better products, reducing waste, and supporting sustainability. By following best practices in sorting, washing, and quality control, manufacturers can produce flakes that are suitable for high-end applications, such as food-grade packaging and premium textiles.

0 notes

Text

Residential Air Purifier Market Regional Analysis and Growth Forecast By 2032

The worldwide residential air purifier market reached a valuation of US$ 3.8 billion in 2021. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.3% from 2022 to 2032, with an anticipated global market value of US$ 7.44 billion by the end of 2032.

In an age where indoor air quality has become a growing concern, residential air purifiers have emerged as essential appliances for improving the health and well-being of homeowners. With pollutants such as dust, allergens, and volatile organic compounds (VOCs) posing risks to respiratory health, the demand for effective air purification solutions continues to rise. As consumers prioritize clean and healthy indoor environments, the residential air purifier market is experiencing significant growth and innovation.

Understanding Residential Air Purifiers:

Residential air purifiers are devices designed to remove contaminants and pollutants from indoor air, including dust, pollen, pet dander, smoke, and airborne pathogens. These purifiers utilize various technologies such as High-Efficiency Particulate Air (HEPA) filtration, activated carbon filtration, ultraviolet (UV) sterilization, and ionization to capture and neutralize airborne particles and odors, ensuring cleaner and healthier indoor air.

Market Dynamics:

Several factors are driving the growth of the residential air purifier market:

Growing Awareness of Indoor Air Quality:With increasing awareness of the health effects of indoor air pollution, consumers are seeking proactive solutions to improve indoor air quality and reduce exposure to pollutants. Residential air purifiers offer an effective means of removing contaminants and allergens, providing relief for individuals with respiratory conditions such as asthma and allergies.

Rising Concerns About Allergens and Asthma Triggers:Allergens such as dust mites, pollen, and pet dander are common triggers for allergies and asthma attacks. Residential air purifiers equipped with HEPA filtration and other advanced technologies can effectively capture and remove these allergens from indoor air, providing relief for allergy sufferers and improving respiratory health.

Impact of Environmental Factors:Environmental factors such as wildfires, pollution, and urbanization contribute to poor outdoor air quality, which can infiltrate indoor environments. Residential air purifiers serve as a barrier against outdoor pollutants, ensuring that indoor air remains clean and safe for occupants.

Technological Advancements:Ongoing advancements in air purification technologies, including the development of smart and connected devices, sensor-based air quality monitoring, and multi-stage filtration systems, are driving innovation in the residential air purifier market. These advancements enhance the performance, efficiency, and user experience of air purifiers, meeting the evolving needs of consumers.

Market Segmentation and Regional Analysis:

The residential air purifier market can be segmented based on technology, type, application, and region. Key technologies include HEPA filtration, activated carbon filtration, UV sterilization, ionization, and ozone generation. Common types of residential air purifiers include portable air purifiers, whole-house air purifiers, and in-duct air purifiers. Applications of residential air purifiers range from residential homes and apartments to offices, schools, and healthcare facilities.

Regionally, North America dominates the residential air purifier market, driven by growing concerns about indoor air quality, increasing prevalence of respiratory conditions, and stringent regulations on indoor air pollutants. Asia Pacific is also a significant market for residential air purifiers, fueled by rising urbanization, pollution levels, and consumer awareness of health and wellness.

Future Outlook and Opportunities:

The future of the residential air purifier market looks promising, with several opportunities for growth and innovation:

Integration of Smart and Connected Features:Smart and connected residential air purifiers equipped with Wi-Fi connectivity, mobile app control, and voice assistant compatibility are gaining popularity among consumers. These features offer convenience, remote monitoring, and personalized control over indoor air quality, driving demand for smart home solutions.

Focus on Energy Efficiency and Sustainability:Manufacturers are increasingly focusing on developing energy-efficient and eco-friendly residential air purifiers that minimize energy consumption and environmental impact. Features such as low-power consumption, eco-friendly filtration materials, and recyclable components appeal to environmentally conscious consumers and support sustainable living practices.

Expansion into Emerging Markets:Emerging economies in regions such as Asia Pacific, Latin America, and the Middle East offer significant growth opportunities for residential air purifier manufacturers. Rapid urbanization, rising disposable incomes, and increasing awareness of health and wellness are driving demand for air purification solutions in these markets.

Get More Info: https://www.factmr.com/connectus/sample?flag=S&rep_id=7103

In conclusion, the residential air purifier market is poised for steady growth and innovation, driven by growing awareness of indoor air quality, rising concerns about allergens and pollutants, technological advancements, and expanding applications across various industries. As consumers prioritize clean and healthy indoor environments, residential air purifiers will continue to play a critical role in improving indoor air quality and enhancing the well-being of occupants.

Contact: US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

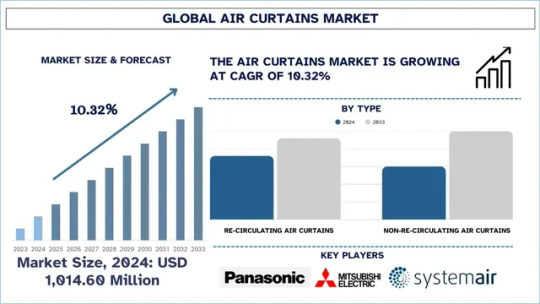

Air Curtains Market Trends, Size, Growth, Analysis and Forecast to 2033

An air curtain is a system placed above or next to a door to form a barrier of strong air movements. They protect the cleanliness of your home by not allowing air from outside to enter and mix with the air inside your home. The installation of air curtains in commercial and industrial areas helps businesses maintain greater energy efficiency. They make spaces cleaner and more comfortable where foot traffic is regular. In some cases, air curtains run all the time, but in others, they are controlled by sensors on the door. They can also be heated to suit the requirements of the space where they are installed. According to the UnivDatos analysis, the rising demand for energy-efficient HVAC solutions, growing indoor air quality and hygiene awareness, and expanding commercial spaces like malls, hospitals, and airports are the major factors driving the growth of the air curtains market worldwide. As per their “Air Curtains Market” report, the global market was valued at USD 1,014.60 million in 2024, growing at a CAGR of about 10.32% during the forecast period from 2025 - 2033 to reach USD million by 2033.

1. Adoption of Sensor-Based & Automated Air Curtains

Businesses are increasingly choosing sensor-based and automated air curtains because they offer efficient and smarter ways to maintain indoor comfort and air quality. They have motion sensors, door-position sensors, or are integrated with BAS systems, so they activate only when there is a need, which helps reduce both energy use and running costs. Additionally, automated air curtains operating in commercial spaces like retail stores, hospitals, and airports are well-suited because they handle many door openings and closings without the need for manual help. Moreover, adjusting to the environment on the fly ensures they use less energy and support the long-life operation of the HVAC systems.

For instance, in January 2023, Berner International, New Castle, Pa., which is the leading manufacturer and innovator of air curtains, introduced the Industrial “Intelliswitch™”. This product is North America’s first digital controller platform for the shipping dock and door industrial air curtain market. The Industrial Intelliswitch enables building managers to control and monitor air curtains individually or in groups via additional options such as the Berner AIR™ smart controller/app and BACnet.

Access sample report (including graphs, charts, and figures): https://univdatos.com/reports/air-curtains-market?popup=report-enquiry

2. Hybrid Air Curtains (Hot & Cold Air)

As hybrid air curtains can use both hot and cold air, these systems are becoming popular for their flexibility in meeting various climate control needs throughout the year. Because of this, these systems are most useful in places where the weather shifts a lot by season, so consumers are always warm during winter and cool during summer. Because of its combined features, hybrid air curtains cut the need for extra HVAC repairs at entry points, making operations more energy efficient and less complex. As hospitality, healthcare, and retail businesses need to stabilize their indoor air quality to ensure comfort, cleanliness, and compliance with rules, air curtains play a major role in helping to fulfill these needs.

3. Growth in Vertical Air Curtains

Vertical air curtains are used when a standard horizontal air curtain is not possible to place. Majorly, conventional overhead air curtains are mounted above doorways, whereas vertical air curtains are used for places such as warehouses, factories, and large shops with high or open entrances. Additionally, these systems have a strong air barrier covering the entire doorway, so very little air, dust, or contaminants can leak in or out, regardless of door measurements. Moreover, several factories are starting to use these systems because they are both flexible and provide high performance in busy logistics and big commercial areas.

Related Reports:

Air Pollution Control Systems Market

Air Handling Units Market

Air Suspension Market

Air Purifier Market

Air-Borne Wind Turbine Market Future Trends Fueling the Growth of the Air Curtains Market

The air curtains market is set to grow because of ongoing future trends such as the adoption of sensor-based & automated air curtains, hybrid air curtains (Hot & Cold Air), and the growth in vertical air curtains. These trends are accelerating the air curtains market globally and promoting the adoption of these technologies across industries.

Contact Us:

UnivDatos

Email - [email protected]

Website - www.univdatos.com

#Air Curtains Market#Air Curtains Market Report#Air Curtains Market Segments#Air Curtains Market Growth#Air Curtains Market Analysis

0 notes

Text

Asia Pacific Industrial Air Filtration Market Size, Trends, Forecast by 2025-2033 | Reports and Insights

The Reports and Insights, a leading market research company, has recently releases report titled “Asia Pacific Industrial Air Filtration Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033.” The study provides a detailed analysis of the industry, including theAsia Pacific Industrial Air Filtration Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Asia Pacific Industrial Air Filtration Market Overview

The Asia Pacific industrial air filtration market was valued at US$ 5.1 Billion in 2024 and is expected to register a CAGR of 4.9% over the forecast period and reach US$ 7.8 Billion in 2033.

The Industrial Air Filtration market of Asia Pacific is important for ensuring that air quality is maintained and that regulatory framework compliance is achieved for manufacturing and processing industries. As the industrial production is increasing and the awareness about the environment is also increasing, the need for the control of hazardous emission, dust, and other airborne pollutants is needed. The regional demand for industrial air filtration systems, is powered by sectors such as pharmaceuticals, food & beverages, cement, chemicals, electronics, and others.

Unquestionably, the growing concerns over safety of workers, indoor air quality and strict environmental regulations have expanded the market rapidly. Countries such as China, India, Japan, South Korea and Indonesia are tightening emissions standards and workplace safety regulations, forcing industries to upgrade filtering systems. The advancement of filters materials and smart monitoring systems is improving the efficiency and reliability of these systems. The market will grow due to investments in industrial automation and the setting up of new production facilities.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2465

Asia Pacific Industrial Air Filtration Market Growth Factors & Challenges

Rapid industrialization, growing health awareness, and more vigorous implementation of air pollution control policies, are key growth drivers. To comply with air quality standards, Asian and Pacific governments are increasingly implementing incentives and penalties sparking industries to invest in effective filtration technologies. The market is further propelled by the rising demand from the automotive, electronics and metalworking sectors. To this end, companies are installing sophisticated air purifying technology as there is an international push to cut back carbon footprint and increase workplace safety.

The market has positive momentum, but all is not well. The high initial investment and maintenance costs can prevent small and medium sized enterprises from adopting an Advanced Filtration System. Manufacturers that operate across nations face difficulties due to the inconsistent regulatory regime across nations. Need for constant innovation due to the technical limitation of filter performances with ultra-fine particles and corrosive gases. Inefficient maintenance of system and lack of trained people can lower its operational efficiencies and effectiveness.

Key suggestions for the report:

The dust collectors’ segment is projected to experience the highest sales growth in the Asia Pacific industrial air filtration market. The increasing demand for dust collectors in these industries is due to the heightened need to control atmospheric dust. Dust control is essential to comply with regulations for dust emissions.

According to the report, the online sales channel will be the most lucrative segment. This is due to the rising trend of buying online due to convenience, more options, and faster delivery. This change can help businesses grow, if they switch to online sales.

Among using industries, cement industry is expected to dominate due to dispersal of dust in high volume during production. As emissions must be reduced to comply with environmental standards and protect workers, advanced air filtration systems are in demand.

The report presents information related to key drivers, restraints, and opportunities along with detailed analysis of the Asia Pacific industrial air filtration market share.

Key Trends in Asia Pacific Industrial Air Filtration Industry

Market is averting towards eco-friendly and easy-to-handle filtration technologies. Systems that can monitor air in real-time and maintain predictively are getting popular. There is an ever-increasing focus on creating modular and scalable systems which can be applied to a range of industries. The increasing use of nanofiber material and hybrid filtration technology enhances the performance and life of filters. Eco-friendly materials and recyclable filter components are seeing demand on sustainability concerns.

Asia Pacific Industrial Air Filtration Market Key Applications & Industry Segments

The Asia Pacific industrial air filtration market is segmented by product, sales channel, end-use industry, and country.

By Product

Dust Collectors

Mist Collectors

HEPA Filters

Cartridge Collectors, Filters

Baghouse Filters

Others

By Sales Channel

Direct Sales

Online Sales

OEM Sales

Others

By End-Use Industry

Food & Beverage

Cement Industry

Pharmaceutical

Chemicals & Petrochemical

Electronics

Power Plants

Others

By Country

China

Japan

South Korea

India

Australia & New Zealand

Taiwan

Vietnam

Singapore

Rest of Asia Pacific

Leading Manufacturers in the Asia Pacific Industrial Air Filtration Market

Some of the key manufacturers which are included in the Asia Pacific industrial air filtration market report are:

3M Company

ACDelco Inc.

CAMFIL Group

Clarcor

Cummins Inc.

Denso corporation

Donaldson company inc

Filtration Group Corporation

Honeywell International inc

K&N Engineering Inc.

KAYSER FILTERTECH GmbH

Mahle GmbH

MANN+HUMMEL Group

Nordic Air Filtration

Parker Hannifin Corporation

Hubei Clean

Panasonic

Toray Industries

AAF India Pvt Ltd

KLC

Thermax Limited

Others

Key Attributes

Report Attributes

Details

No. of Pages

191

Market Forecast

2025-2033

Market Value (USD) in 2024

5.1 billion

Market Value (USD) in 2033

7.8 billion

Compound Annual Growth Rate (%)

4.9%

Regions Covered

Asia Pacific

View Full Report: https://www.reportsandinsights.com/report/asia-pacific-industrial-air-filtration-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Asia Pacific Industrial Air Filtration Market share#Asia Pacific Industrial Air Filtration Market size#Asia Pacific Industrial Air Filtration Market trends

0 notes

Text

Global Sample Digestion Market Expands Rapidly

Rising demand from sectors like environmental monitoring, pharmaceuticals, food, agriculture, mining, and petrochemicals is putting the global sample digestion equipment market on track to grow from USD 150.7 million in 2024 to USD 209.3 million by 2033 — a projected 4.5% CAGR.

Environmental analysis leads growth areas.

Environmental testing is one of the strongest application areas for digestion equipment. Tighter environmental rules combined with growing attention on pollution and waste management require reliable digestion systems that can break down complex matrices and deliver consistent, interference-free results.

Food and agriculture is another importantdigestion equipment market driver. As food chains become more global and regulations become more complex, quality assurance and safety testing now require consistent elemental analysis of fertilizers, livestock feed, and processed foods to detect contaminants at very low concentrations.

North America leads, Asia Pacific catching up fast.

Geographically, North America is expected to hold the largestdigestion equipment market share over the forecast period. The region benefits from advanced regulatory systems and the presence of major industry players. But Asia Pacific is catching up quickly — industrial growth, infrastructure development, and stronger investment in research activities are fueling demand across emerging markets in the region.

ColdBlock pushes beyond microwave speeds.

While microwave digestion remains central to the market, ColdBlock Technologies Inc. is pushing boundaries further.

ColdBlock’s digestion system offers cycle times of just 10 to 40 minutes — much quicker than both microwave and hot plate methods. With fewer upkeep demands and straightforward controls, it helps labs work faster without complicating their workflow. One person can install the system in under 30 minutes, and weekly maintenance takes less than 10 minutes.

Productivity and safety gains drive adoption.

ColdBlock's digestion equipment technology not only boosts lab productivity by reducing digestion time but also cuts costs. Labs have reported savings of 10% to as much as 30% compared to microwave and hot block systems.

On the safety front, ColdBlock eliminates the need for perchloric acid and functions safely in open-air environments using a vent hood. Its cooling zone keeps handling safe, with no need for pressurization.

ColdBlock is ensuring its system reaches new customers efficiently by working closely with regional partners. The company is expanding globally by partnering with local distributors and sales teams, positioning itself in labs around the world. If you are interested in becoming a distributor and accessing more product information, visit ColdBlock.ca or email [email protected].

0 notes

Text

Smart Cities Market Size, Share & Growth Report 2031

Meticulous Research®—a leading global market research company, published a research report titled, Smart Cities Market—Global Opportunity Analysis and Industry Forecast (2024-2031). According to this latest publication from Meticulous Research®, the smart cities market is projected to reach $3,967.7 billion by 2031, at a CAGR of 26.9 from 2024 to 2031.

The growth of the smart cities market is underpinned by several key factors. These include the increasing demand for effective resource management and sustainable development and several initiatives taken by government agencies globally to address the needs of the growing urban population. However, the high capital and operating expenditures may restrain the growth of this market.

The integration of AI and the expanding applications of IoT technology is expected to create growth opportunities for market players. However, the rising cases of data theft, the integration of different systems and technologies from multiple vendors, and the reluctance to upgrade existing infrastructure to accommodate new smart technologies pose challenges to the growth of the smart cities market.

Key Players

The smart cities market is characterized by a moderately competitive scenario due to the presence of many large- and small-sized global, regional, and local players. The leading players operating in the smart cities market are Cisco Systems, Inc. (U.S.), Huawei Technologies Co., Ltd. (China), IBM Corporation (US.), Siemens AG (Germany), Cognizant Technology Solutions Corporation (U.S.), Schneider Electric SE (France), Intel Corporation (U.S.), Qualcomm Technologies, Inc. (U.S.), Fujitsu Ltd. (Japan), Robert Bosch GmbH (Germany), Atos SE (France), Foxconn Electronics Inc. (Hon Hai Precision Industry Co. Ltd.) (China), LTIMindtree Limited (India), General Electric Company (U.S.), Capgemini SE (France), Microsoft Corporation (U.S.), ABB Ltd. (Switzerland), Oracle Corporation (U.S.), Honeywell International, Inc. (U.S.), and NEC Corporation (Japan).

The smart cities market is segmented by solution (smart citizen services {smart public safety, smart governance, smart street lighting, smart education, smart healthcare}, smart environment {climate monitoring, smart waste management, air quality monitoring, noise mapping & monitoring}, smart buildings {solution, type}, smart transportation {solution, application}, smart utilities {smart energy management, smart water management, smart distribution management, smart waste management}, other smart cities solutions), component (hardware, {endpoint devices, processing devices, network devices, and other devices}, software {IoT device software, gateway software, cloud software, computing device software, and other software}, services {consulting services, system integration & deployment services, infrastructure monitoring & management services, network services, and other services}), technology (IoT, artificial intelligence, cloud computing, machine learning, machine-to-machine communications, and other technologies).

By solution, the smart citizen services segment is anticipated to hold the dominant market share of over 48.0% of the smart cities market in 2024. The segment's significant market share is primarily attributed to the increasing demand for economic & extensible public services, government initiatives for smart city projects aimed at enhancing infrastructure, sustainability, and quality of life, and the advancements in IoT, artificial intelligence, and big data analytics.

By component, the hardware segment is anticipated to hold the dominant market share of over 40.0% in 2024. The segment's significant market share is primarily attributed to the growing need for real-time data collection & analytics, rising R&D investments, the key focus on hardware-centric capabilities, and the increasing demand for innovative & reliable hardware for advanced IoT sensors in applications like air quality monitoring, traffic management, and environmental sensing.

By technology, the IoT segment is anticipated to hold the dominant market share of over 37.0% in 2024. The segment's significant market share is primarily attributed to the increasing demand for IoT solutions in intelligent traffic management, smart parking, and connected vehicles; the growing adoption of IoT-enabled smart grids, energy meters, and building management systems; and the rising need for IoT-enabled surveillance cameras, emergency alert systems, and predictive policing technologies.

By geography, APAC is anticipated to hold the dominant market share of over 30.8% in 2024. The presence of prominent smart city players, including Fujitsu Ltd. (Japan), Huawei Technologies Co., Ltd. (China), and NEC Corporation (Japan), is expected to contribute to the dominant market share of this region. Moreover, the rising population density in APAC cities, the growing concerns about public safety & security, and the increasing government initiatives & funding for smart city projects are driving demand in the region.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5087

Key Questions Answered in the Report:

Which are the high-growth market segments in terms of solution, component, and technology?

What was the historical market size for smart cities globally?

What are the market forecasts and estimates for 2024–2031?

What are the major drivers, restraints, opportunities, challenges, and trends in the smart cities market?

Who are the major players in the smart cities market, and what are their market shares?

What is the competitive landscape like?

What are the major market trends geographically, and which are the high-growth countries?

Who are the local emerging players in the smart cities market, and how do they compete with other players?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Smart Cities Market#Smart Cities#Smart Citizen Services#Smart Transportation#Smart Buildings#Smart Utilities#Smart Environment#Smart Waste Management

0 notes

Text

Desktop Air Samplers Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

According to a new report from Intel Market Research, the global Desktop Air Samplers market was valued at USD 161 million in 2024 and is projected to reach USD 215 million by 2032, growing at a steady CAGR of 4.0% during the forecast period (2025-2032). This growth is driven by increasing regulatory requirements across pharmaceutical and food industries, technological advancements in sampling devices, and expanding quality control measures in emerging markets.

What are Desktop Air Samplers?

Desktop Air Samplers are precision instruments designed for collecting and analyzing airborne contaminants including microbial particles, dust, and chemical pollutants. These compact devices employ either active (pump-assisted) or passive (gravity-based) sampling methods to deliver accurate air quality assessments. Primarily used in pharmaceutical cleanrooms, food processing facilities, and environmental monitoring stations, these tools have become essential for compliance with international standards like ISO 14644-1 and GMP regulations.

The latest generation of samplers now incorporates real-time particle counting, wireless connectivity, and automated reporting features, transforming them from basic monitoring tools into intelligent air quality management systems. Leading manufacturers are focusing on portable designs that maintain laboratory-grade accuracy while offering field deployment capabilities.

📥 Download Sample Report: Desktop Air Samplers Market - View in Detailed Research Report

Key Market Drivers

1. Stringent Regulatory Compliance Across Industries

The pharmaceutical sector's strict adherence to Good Manufacturing Practices (GMP) represents the single largest growth driver, accounting for 42% of total market demand. Recent FDA crackdowns on manufacturing facilities have increased adoption rates, with over 60% of major pharmaceutical companies now implementing continuous monitoring systems. The food industry shows parallel growth, where post-pandemic hygiene concerns have boosted adoption by 28% since 2020.

2. Technological Advancements Expanding Applications

Innovations in sensor technology and data analytics have significantly enhanced sampler capabilities. The 2023 introduction of multi-parameter devices capable of simultaneous viable/non-viable particle detection has been particularly impactful. These advancements have reduced sampling times by 40-60% while improving detection accuracy, making the technology accessible to smaller laboratories and production facilities.

3. Pharmaceutical Industry Expansion in Emerging Markets

Asia's booming pharmaceutical sector has triggered 19% year-over-year demand increases for compact sampling solutions. Countries like India and Vietnam are experiencing rapid growth in regulated manufacturing, driven by both domestic needs and export requirements. This expansion coincides with increased WHO prequalification standards, mandating sophisticated environmental monitoring systems.

Market Challenges

While growth prospects remain strong, several obstacles warrant consideration:

High Ownership Costs: Premium units range from $5,000-$15,000, with annual calibration adding $500-$1,200 to operating expenses - representing 18-25% of typical quality control budgets

Operational Complexity: 31% of facilities report staff shortages for proper sampler operation, with audit findings showing 15-20% procedural variance between technicians

Competition from Alternative Technologies: IoT-based continuous monitoring systems offer real-time data at 60-70% lower cost, though with reduced precision