#Microprocessor Market size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

CNC development history and processing principles

CNC machine tools are also called Computerized Numerical Control (CNC for short). They are mechatronics products that use digital information to control machine tools. They record the relative position between the tool and the workpiece, the start and stop of the machine tool, the spindle speed change, the workpiece loosening and clamping, the tool selection, the start and stop of the cooling pump and other operations and sequence actions on the control medium with digital codes, and then send the digital information to the CNC device or computer, which will decode and calculate, issue instructions to control the machine tool servo system or other actuators, so that the machine tool can process the required workpiece.

1. The evolution of CNC technology: from mechanical gears to digital codes

The Beginning of Mechanical Control (late 19th century - 1940s)

The prototype of CNC technology can be traced back to the invention of mechanical automatic machine tools in the 19th century. In 1887, the cam-controlled lathe invented by American engineer Herman realized "programmed" processing for the first time by rotating cams to drive tool movement. Although this mechanical programming method is inefficient, it provides a key idea for subsequent CNC technology. During World War II, the surge in demand for military equipment accelerated the innovation of processing technology, but the processing capacity of traditional machine tools for complex parts had reached a bottleneck.

The electronic revolution (1950s-1970s)

After World War II, manufacturing industries mostly relied on manual operations. After workers understood the drawings, they manually operated machine tools to process parts. This way of producing products was costly, inefficient, and the quality was not guaranteed. In 1952, John Parsons' team at the Massachusetts Institute of Technology (MIT) developed the world's first CNC milling machine, which input instructions through punched paper tape, marking the official birth of CNC technology. The core breakthrough of this stage was "digital signals replacing mechanical transmission" - servo motors replaced gears and connecting rods, and code instructions replaced manual adjustments. In the 1960s, the popularity of integrated circuits reduced the size and cost of CNC systems. Japanese companies such as Fanuc launched commercial CNC equipment, and the automotive and aviation industries took the lead in introducing CNC production lines.

Integration of computer technology (1980s-2000s)

With the maturity of microprocessor and graphical interface technology, CNC entered the PC control era. In 1982, Siemens of Germany launched the first microprocessor-based CNC system Sinumerik 800, whose programming efficiency was 100 times higher than that of paper tape. The integration of CAD (computer-aided design) and CAM (computer-aided manufacturing) software allows engineers to directly convert 3D models into machining codes, and the machining accuracy of complex surfaces reaches the micron level. During this period, equipment such as five-axis linkage machining centers came into being, promoting the rapid development of mold manufacturing and medical device industries.

Intelligence and networking (21st century to present)

The Internet of Things and artificial intelligence technologies have given CNC machine tools new vitality. Modern CNC systems use sensors to monitor parameters such as cutting force and temperature in real time, and use machine learning to optimize processing paths. For example, the iSMART Factory solution of Japan's Mazak Company achieves intelligent scheduling of hundreds of machine tools through cloud collaboration. In 2023, the global CNC machine tool market size has exceeded US$80 billion, and China has become the largest manufacturing country with a production share of 31%.

2. CNC machining principles: How code drives steel

The essence of CNC technology is to convert the physical machining process into a control closed loop of digital signals. Its operation logic can be divided into three stages:

Geometric Modeling and Programming

After building a 3D model using CAD software such as UG and SolidWorks, CAM software “deconstructs” the model: automatically calculating parameters such as tool path, feed rate, spindle speed, and generating G code (such as G01 X100 Y200 F500 for linear interpolation to coordinates (100,200) and feed rate 500mm/min). Modern software can even simulate the material removal process and predict machining errors.

Numerical control system analysis and implementation

The "brain" of CNC machine tools - the numerical control system (such as Fanuc 30i, Siemens 840D) converts G codes into electrical pulse signals. Taking a three-axis milling machine as an example, the servo motors of the X/Y/Z axes receive pulse commands and convert rotary motion into linear displacement through ball screws, with a positioning accuracy of up to ±0.002mm. The closed-loop control system uses a grating ruler to feedback position errors in real time, forming a dynamic correction mechanism.

Multi-physics collaborative control

During the machining process, the machine tool needs to coordinate multiple parameters synchronously: the spindle motor drives the tool to rotate at a high speed of 20,000 rpm, the cooling system sprays atomized cutting fluid to reduce the temperature, and the tool changing robot completes the tool change within 0.5 seconds. For example, when machining titanium alloy blades, the system needs to dynamically adjust the cutting depth according to the hardness of the material to avoid tool chipping.

3. The future of CNC technology: cross-dimensional breakthroughs and industrial transformation

Currently, CNC technology is facing three major trends:

Combined: Turning and milling machine tools can complete turning, milling, grinding and other processes on one device, reducing clamping time by 90%;

Additive-subtractive integration: Germany's DMG MORI's LASERTEC series machine tools combine 3D printing and CNC finishing to directly manufacture aerospace engine combustion chambers;

Digital Twin: By using a virtual machine tool to simulate the actual machining process, China's Shenyang Machine Tool's i5 system has increased debugging efficiency by 70%.

From the meshing of mechanical gears to the flow of digital signals, CNC technology has rewritten the underlying logic of the manufacturing industry in 70 years. It is not only an upgrade of machine tools, but also a leap in the ability of humans to transform abstract thinking into physical entities. In the new track of intelligent manufacturing, CNC technology will continue to break through the limits of materials, precision and efficiency, and write a new chapter for industrial civilization.

#prototype machining#cnc machining#precision machining#prototyping#rapid prototyping#machining parts

2 notes

·

View notes

Text

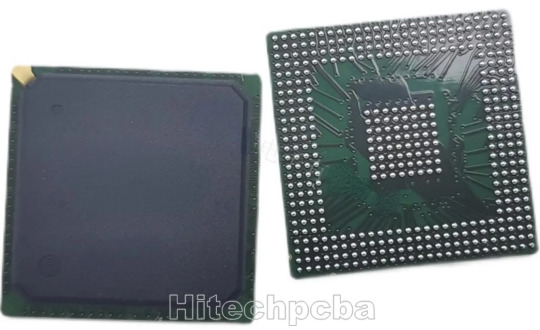

BGA PCB Assembly

What’s BGA PCB?

BGA PCB is Printed Circuit Boards with Ball Grid Array. We use various sophisticated techniques for making BGA PCBs. Such PCBs have a small size, low cost, and high packaging density. Hence, they are reliable for high-performance applications.

What’s BGA PCB Assembly?

Ball Grid Array (BGA) assembly technology is a surface mount packaging technology applied to integrated circuits, which is often used to permanently fix devices such as microprocessors. BGA assembly can accommodate more pins than other packages such as Dual in-line packages or Quad Flat Packages, and the entire bottom surface of the device can be used as pins , instead of only peripherals available, and also have a shorter average wire length than peripheral-limited package types for better high-speed performance.

Our BGA assembly services cover a wide range, including BGA prototype development, BGA PCB assembly, BGA component removal, BGA replacement, BGA rework and reballing, BGA PCB assembly inspection, and so on. Leveraging our full-coverage services, we can help customers streamline the supply network and accelerate product development time.

Benefits of BGA PCB Assembly

Efficient Use of Space – BGA PCB layout allows us to efficiently use the available space, so we can mount more components and manufacture lighter devices.

Better Thermal Performance – For BGA, the heat generated by the components is transferred directly through the ball. In addition, the large contact area improves heat dissipation, which prevents overheating of components and ensures long life.

Higher Electrical Conductivity – The path between the die and the circuit board is short, which results in better electrical conductivity. Moreover, there is no through-hole on the board, the whole circuit board is covered with solder balls and other components, so vacant spaces are reduced.

Easy to Assemble And Manage – Compared to other PCB assembly techniques, BGA is easier to assemble and manage as the solder balls are used directly to solder the package to the board.

Less Damage to Leads – We use solid solder balls for manufacturing BGA leads. Hence, there is a lesser risk that they will get damaged during the operation.

In a word, BGA PCB assembly, have these advantages, high density, better electrical conductivity, lower thermal resistance, easy to assembly & manage are some of the advantages of BGA PCB.

Stringent BGA PCB Assembly Testing Process

To achieve the highest quality standards for BGA assembly, we use a variety of inspection methods throughout the process including optical inspection, mechanical inspection, and X-ray inspection. Among them, the inspection of BGA solder joints must use X-rays. X-rays can pass through the components to inspect the solder joints below them, so as to check the solder joint position, solder joint radius, and solder joint thickness.

Inspection of BGA PCB

We mostly use X-ray inspection for analyzing the features of BGA PCBs. This technique is known as XRD in the industry and relies on X-rays for unveiling the hidden features of this PCB. This kind of inspection reveals.

* Solder Joint Position

* Solder Joint Radius

* Change in Circular shape

* Solder Joint Thickness

The Hitechpcba advantage lies in a whole range of aspects, beginning from the fact that we have the proven technology available at our disposal. With over 15 years of experience in a wide range of PCB Fabrication and Assembly techniques, what we also have is trained manpower and importantly, robust industry experience and best practices that you can benefit from.

Our unstinting devotion to quality and customer satisfaction means that once you partner with us, you can rest assured that you will get nothing but the best. The customer-oriented approach also shows up in your commitment to delivery times. With quick turnaround times, you can reap the benefit of quick time-to-market, which, in turn, can be a major source of competitive advantage.

Whether your requirement is BGA PCB design, BGA PCB, BGA PCB layout, BGA PCB Assembly or BGA rework, you can rest assured that you will get superior quality and performance, that will in turn, positively impact the performance of your final product.

With our efficient network of component suppliers and the many economies of scale that we enjoy, that you will get optimal costs, is a given.

Please feel free to contact us ([email protected]) if you have any other special request on the BGA pcb assembly.

3 notes

·

View notes

Text

Costa Power offers ups battery backup solution with the highest space and cost benefits. The Delta UPS INX series is an Delta ups online double-conversion providing consistent sine wave power to your critical equipment. The Delta UPS INX series features an input power factor corrector and best-in-class AC-DC efficiency of up to 90% resulting in greater energy savings. The Delta UPS INX series leads the industry in combining compact size, availability, flexibility and best total cost of ownership.

Costa Power is Top Delta ups suppliers in India chain of Delta ups manufacturers in Bangalore, Delta ups battery Suppliers in Mumbai of ups distributors such as delta industrial ups suppliers, delta line interactive online ups suppliers, Delta single phase ups in Mumbai, Delta digital ups, delta modular ups dealers in Pune,Delta three phase ups systems, delta online ups dealers in Mumbai, delta offline ups suppliers, etc. Costa power provides ups battery system with customized solutions and Delta ups amc services, ups amc nationwide with a strong presence in the thane, Mumbai, Mumbai Suburbs, Maharashtra interior parts and in India.

Costa power design, build Delta ups systems and Delta ups amc service in India for Data centers, Communication networks, Commercial and industrial applications We support today with a portfolio of ups battery systems, thermal and infrastructure management ups battery backup solutions by help of principal Company Delta. Costa Power offer unsurpassed global scale and broad expertise, built from our heritage as top Delta ups distributors in Mumbai and providing Delta ups suppliers in India.

Costa Power offers Delta UPS systems, product line, the Agilon Delta ups family are Delta single phase UPS systems for power rating requirements under Delta 1.5 kVA ups, that can support PC products, peripherals and small POS systems. The word Agilon (Agile + on), denotes agility and precision, which describe the features of this Delta UPS system – small yet efficient; they are the perfect power management and ups battery backup solution for residential users, SOHO workers or small enterprises. The Agilon Delta ups family, Delta VX line-interactive UPS designed with microprocessor control offers reliable and cost effective delta ups distributors power protection for PCs, laptops, POS, and other sensitive electronics used in home offices and small businesses..

#Upsbattery#Upsbatterydealers#Upsbatterydistributor#Upsbatterysuppliers#Upsamc#Upsapc#Microtekinverter#Quatabattery#Luminousups#Emersonups#Onlineups#Digitalups#Offlineups#Bestups#Bestbattery#Servostabilizer#Vertivups#Exidebattery#Luminousinverter#Upsdealers#Upssuppliers#Upsdistributors

0 notes

Text

Nanotechnology Market Estimated to Experience a Hike in Growth By 2030

Allied Market Research, titled, “Nanotechnology Market By Type, and Application: Global Opportunity Analysis and Industry Forecast, 2021–2030,” the global nanotechnology market size was valued at $1.76 billion in 2020, and is projected to reach $33.63 billion by 2030, registering a CAGR of 36.4% from 2021 to 2030.

The nanotechnology market analysis is currently in its growth stage and is expected to register substantial growth in the near future, owing to the high investment in R&D activities by market players and increase in focus toward Internet of Things (IoT). Other factors that drive the market growth include increase in demand for automobile & electronics and development of smart devices.

According to nanotechnology market trends, emerging technologies, such as artificial intelligence (AI) and quantum computing, require nanotechnology to achieve full commercialization. The UK has a rich heritage of microprocessor design, with companies such as ARM and Imagination Technologies, and new start-up companies designing AI processors, such as Bristol-based Graphcore, which creates lucrative opportunities for its market growth globally.

North America is the second largest region, in terms of revenue generation, in the global nanotechnology market. The consumer electronics industry is well-established in North America, which has led to increased adoption of nanotechnology. In addition, rapid growth in the sales of consumer electronic products supplements the market growth. Moreover, increase in defense expenditure and widespread use of nanotechnology in healthcare, consumer electronics, and automotive industries drive the nanotechnology market growth globally.

Intel has created a 14-nanometer transistor and IBM has created the first 7-nanometer transistor recently. In addition, ultra-high definition displays and televisions are now being sold that use quantum dots to produce more vibrant colors while being more energy efficient. Furthermore, nanotechnology and nanotech devices are used to develop computing and electronic products, which include flash memory chips for smartphones and thumb drives, ultra-responsive hearing aids, antimicrobial/antibacterial coatings on keyboards and cell phone casings, conductive inks for printed electronics for RFID, smart cards and smart packaging, and flexible displays for e-book readers.

Various nanodevices and nanosensors are used for offshore oil & gas extractions to detect any faulty working conditions. Furthermore, researchers are developing wires containing carbon nanotubes that will have much lower resistance than the high-tension wires currently used in the electric grid, thus reducing transmission power loss. In addition, nanotechnology can be incorporated into solar panels to generate electricity more efficiently, promising inexpensive solar power in the future.

Nanostructured solar cells could be cheaper to manufacture and easier to install, since they can use print-like manufacturing processes and can be made in flexible rolls rather than discrete panels. Furthermore, the number of energy efficiency and energy saving products are increasing and also its types of application. Nanotechnology is enabling more efficient lighting systems, lighter and stronger vehicle chassis materials for the transportation sector, lower energy consumption in advanced electronics, and light-responsive smart coatings for glass.

The emergence of COVID-19 has significantly impacted the smart display industry. The delays caused by partial or complete lockdowns in various regions of the world for construction projects have significantly reduced demand for nanotechnology during the pandemic. However, the rise in demand for signage display in the sport & entertainment sectors has grown during the pandemic. Hence, the sport & entertainment sector is expected to witness prominent growth post-pandemic for the nanotechnology industry.

Key Findings of the Study

In 2020, the nanodevice segment generated the highest revenue and is projected to grow at a notable CAGR of 38.5% during the forecast period.

The healthcare segment is projected to grow by 36.2% from 2021 to 2030 in the nanotechnology market.

North America contributed a major share to the nanotechnology market analysis, accounting for more than 32.11% share in 2020.

The key players profiled in the report include Altair Nanotechnologies Inc., Applied Nanotech Holdings Inc., Thermo Fisher Scientific, Imina Technologies SA, Bruker AXS, Kleindiek Nanotechnik GmbH, eSpin Technologies Inc., Advanced Nano Products, Biosensor International, and Nanoics Imaging Ltd. These Market players have adopted various strategies such as product launch, collaboration & partnership, joint venture, and acquisition to expand their foothold in the nanotechnology market.

0 notes

Text

Automatic Defrost Controller Market: Global Key Trends & Industry Forecast to 2032

Global Automatic Defrost Controller Market size was valued at US$ 345.8 million in 2024 and is projected to reach US$ 634.9 million by 2032, at a CAGR of 9.21% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China’s market is anticipated to grow at a faster 7.1% CAGR through 2032.

Automatic Defrost Controllers are electronic devices designed to optimize defrost cycles in refrigeration systems by monitoring temperature differentials and ice buildup. These intelligent controllers utilize sensors and algorithms to initiate defrost cycles only when necessary, significantly improving energy efficiency compared to traditional timer-based systems. Modern variants incorporate smart features like remote monitoring and adaptive learning capabilities.

Market growth is driven by tightening energy efficiency regulations worldwide and the rapid expansion of cold chain logistics. The commercial refrigeration segment currently dominates applications, particularly in supermarkets and food service, where energy savings directly impact operational costs. Leading manufacturers are focusing on IoT integration, with recent product launches featuring cloud connectivity for predictive maintenance.

Get Full Report : https://semiconductorinsight.com/report/automatic-defrost-controller-market/

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Refrigeration Solutions to Accelerate Market Growth

The global push toward energy efficiency in refrigeration systems is driving significant adoption of automatic defrost controllers. Modern units can reduce energy consumption by up to 35% compared to traditional defrost methods, creating substantial cost savings for commercial and industrial users. With commercial refrigeration accounting for approximately 40% of total energy usage in supermarkets, the demand for intelligent defrost management continues to rise. The circulating defrost segment, in particular, is witnessing rapid adoption due to its ability to maintain consistent temperatures while preventing ice buildup.

Expansion of Cold Chain Logistics to Boost Market Expansion

The global cold chain market size surpassed $280 billion in 2024, creating parallel demand for advanced refrigeration control technologies. Automatic defrost controllers play a critical role in maintaining product integrity across pharmaceutical, food logistics, and chemical storage applications. The emergence of precise temperature-controlled transportation solutions has increased deployment of these controllers in mobile refrigeration units. Their ability to prevent temperature fluctuations during the defrost cycle makes them indispensable for sensitive cargo. Recent technological integrations with IoT platforms further enhance real-time monitoring capabilities.

Furthermore, stringent regulatory requirements regarding food and pharmaceutical storage conditions are compelling upgrades to existing refrigeration infrastructure.

➤ For instance, the FDA’s current good manufacturing practice (CGMP) regulations require precise temperature maintenance for biologics storage, creating mandatory demand for reliable defrost control systems.

The industrial sector is projected to represent the fastest-growing application segment through 2032, driven by expanded cold storage facility development across emerging economies.

MARKET RESTRAINTS

High Initial Investment Costs for Advanced Systems to Limit Market Penetration

While automatic defrost controllers offer long-term operational savings, their premium pricing creates adoption barriers in price-sensitive markets. Commercial-grade units can cost 4-6 times more than conventional defrost timers, making retrofit projects economically challenging for small businesses. The sophisticated sensor technology and microprocessor components account for nearly 60% of the total system cost. This financial hurdle is particularly pronounced in developing regions where refrigeration systems often operate on thin margins.

Other Restraints

Interoperability Challenges Integration with legacy refrigeration equipment remains problematic, as many older systems lack compatible control interfaces. Retrofitting often requires additional component replacements, increasing total project costs beyond initial estimates.

Technical Complexity Modern controllers require specialized installation and calibration, creating dependence on qualified technicians. The current shortage of HVAC-R professionals adds service delays and increased maintenance costs for end users.

MARKET CHALLENGES

Component Shortages and Supply Chain Disruptions to Impact Market Stability

The semiconductor crisis continues to affect production lead times for automatic defrost controllers, with some manufacturers reporting 8-12 week delays on microcontroller units. These critical components represent approximately 25% of the bill of materials for advanced defrost controllers. The situation is compounded by fluctuating raw material prices, particularly for copper and specialty plastics used in sensor housings.

Additionally, the global shift toward localized manufacturing creates logistical complexities for multinational suppliers. Lead times for complete systems have increased by 30-45% compared to pre-pandemic levels, forcing distributors to maintain higher inventory levels. These operational challenges come at a time when demand is growing at 6-8% annually across developed markets.

Small and medium manufacturers face particular difficulties securing stable component supplies, potentially leading to market consolidation as larger players leverage their purchasing power.

MARKET OPPORTUNITIES

Integration with Smart Building Ecosystems to Generate New Revenue Streams

The emergence of connected refrigeration systems presents a $1.2 billion opportunity for advanced defrost controllers with IoT capabilities. Modern units can now interface with building management systems, providing predictive maintenance alerts and energy optimization recommendations. This functionality is particularly valuable for supermarket chains managing hundreds of refrigeration units across multiple locations.

The commercial sector shows strong adoption potential, with an estimated 45% of new refrigeration installations now specifying networked defrost controllers. Cloud-based analytics platforms enable centralized performance monitoring, reducing service costs and minimizing downtime. Major manufacturers are responding with strategic partnerships – recent collaborations between HVAC controls specialists and IoT platform providers aim to standardize communication protocols.

Emerging applications in medical cryogenic storage and laboratory refrigeration are creating specialized niches that command premium pricing. The pharmaceutical cold chain segment alone is projected to require nearly 200,000 new controller installations annually through 2030.

AUTOMATIC DEFROST CONTROLLER MARKET TRENDS

Energy Efficiency Standards Driving Market Innovation

The global push for energy-efficient refrigeration systems is accelerating demand for advanced automatic defrost controllers. Regulatory frameworks such as the EU Ecodesign Directive and U.S. Department of Energy appliance standards now mandate stricter energy consumption limits, pushing manufacturers to develop smarter defrost cycle management. Modern controllers utilizing adaptive defrost algorithms have demonstrated energy savings of 15-25% compared to traditional timer-based systems, making them essential for compliance. The commercial refrigeration segment accounts for approximately 40% of total market adoption, with supermarkets increasingly retrofitting units to meet sustainability targets.

Other Trends

Smart Connected Defrost Systems

Integration with IoT platforms is transforming automatic defrost controllers into predictive maintenance tools. Wireless-enabled controllers now represent 28% of new installations, allowing real-time frost accumulation monitoring through cloud-based dashboards. Major players are embedding machine learning to analyze compressor run times, door openings, and ambient humidity – enabling defrost cycles only when actually needed. This connectivity also facilitates remote troubleshooting, reducing service costs by an estimated 30-40% in commercial applications. The home appliance segment is gradually adopting these smart features, with premium refrigerators increasingly offering app-controlled defrost management.

Material Science Advancements in Frost Detection

Innovations in sensor technologies are eliminating dependence on simplistic temperature differential methods. New capacitive and optical ice detection sensors achieve 98% accuracy in frost layer measurement, preventing unnecessary defrost cycles that waste energy. Some advanced controllers now incorporate dual-sensor validation systems, combining ultrasonic thickness measurement with thermal conductivity analysis. These developments are particularly crucial for cold chain logistics, where precise humidity control prevents both ice buildup and product dehydration. Medical refrigeration applications are adopting these high-precision controllers at a 22% CAGR, as pharmaceutical storage demands tighter temperature tolerances.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Efficiency Drive Market Competition in Automatic Defrost Controllers

The global automatic defrost controller market demonstrates a moderately consolidated structure, dominated by established players while allowing space for regional specialists and emerging innovators. RODGERS stands out as a market leader, commanding significant share through its comprehensive product range spanning both circulating and non-circulating defrost technologies. Their dominance stems from decades of refrigeration control expertise and strong distribution networks across North America and Europe.

ICM Controls and Emerson follow closely, together accounting for approximately 30% of the 2024 market revenue. These companies differentiate themselves through precision-engineered solutions for commercial refrigeration applications, particularly in supermarket display cases and cold storage facilities. Their growth trajectories benefit from increasing demand for energy-efficient defrosting systems in food retail chains.

Meanwhile, Honeywell and Gems Sensors & Controls are making strategic inroads into the industrial segment, developing robust controllers capable of handling extreme temperature ranges down to -40°F. Recent investments in IoT-enabled defrost solutions position these companies for accelerated growth as smart refrigeration gains traction.

The competitive intensity spurs continuous product enhancements across the board. Industry players recognize that automatic defrost controllers constitute mission-critical components in refrigeration systems, where reliability directly impacts operational costs. This understanding drives substantial R&D budgets, averaging 5-7% of revenue among top manufacturers.

List of Key Automatic Defrost Controller Manufacturers

RODGERS (U.S.)

ICM Controls (U.S.)

PENN (U.S.)

HB Products (Denmark)

Manik Engineers (India)

Emerson Electric Co. (U.S.)

Honeywell International Inc. (U.S.)

Hansen Technologies (U.S.)

Gems Sensors & Controls (U.S.)

Download A Sample Report : https://semiconductorinsight.com/download-sample-report/?product_id=97999

Segment Analysis:

By Type

Circulating Defrost Segment Leads Due to Energy Efficiency and Faster Ice Removal

The market is segmented based on type into:

Circulating Defrost

Subtypes: Electric heating elements, hot gas bypass systems

Non-circulating Defrost

Subtypes: Time-based controllers, temperature-initiated systems

Hybrid Systems

Others

By Application

Commercial Segment Dominates Owing to High Adoption in Refrigerated Storage Facilities

The market is segmented based on application into:

Commercial

Subtypes: Supermarkets, cold storage warehouses, food processing plants

Industrial

Home

Transportation Refrigeration

By Technology

Smart Controllers Segment Grows Rapidly with IoT Integration Trends

The market is segmented based on technology into:

Traditional Timers

Temperature Sensors

Smart Controllers

Subtypes: Wi-Fi enabled, cloud-based monitoring

Hybrid Systems

By Installation Type

New Installations Segment Maintains Majority Share in Developing Markets

The market is segmented based on installation type into:

New Installations

Retrofit/Replacement

Upgrade Systems

Regional Analysis: Automatic Defrost Controller Market

North America The North American market demonstrates strong demand for automatic defrost controllers, driven by rigorous appliance manufacturing standards and the widespread adoption of energy-efficient HVAC & refrigeration systems. The U.S. leads the region, accounting for approximately 65% of regional revenue, propelled by commercial refrigeration modernization and stringent EPA regulations on appliance efficiency. Industries such as food retail and cold storage are increasingly integrating smart defrost controllers to minimize energy waste and comply with sustainability mandates. Canada follows closely, with growth tied to cold-chain logistics expansion. However, supply chain disruptions and semiconductor shortages occasionally hinder production schedules for key manufacturers like Emerson and Honeywell.

Europe Europe’s market thrives on electromechanical defrost controller innovations and the rapid phase-out of legacy systems under the EU’s Ecodesign Directive. Germany and France collectively dominate over 50% of regional sales, prioritizing precision-controlled defrost cycles in industrial freezers and heat pumps. The shift toward IoT-enabled controllers (growing at ~12% CAGR) reflects the broader Industry 4.0 adoption. Scandinavian countries emphasize low-temperature applications, particularly in seafood processing and pharmaceutical storage. Despite robust demand, pricing pressures from Asian competitors and complex recycling regulations under WEEE directives pose challenges for mid-sized suppliers.

Asia-Pacific APAC represents the fastest-growing market, with China and Japan contributing 70% of regional volume. China’s booming cold storage infrastructure (projected to exceed 35 million cubic meters by 2027) fuels demand for high-capacity defrost controllers. Meanwhile, Japan’s precision-focused manufacturers drive advancements in miniaturized controllers for compact refrigeration units. India’s market remains price-sensitive, favoring non-circulating defrost systems, though urbanization and FDI in food processing are gradually elevating standards. Southeast Asia emerges as a production hub, with Thailand and Vietnam attracting investments from global players like ICM Controls to serve cost-conscious OEMs.

South America Market growth here is uneven, with Brazil accounting for 60% of regional demand—mainly for commercial refrigeration in supermarkets and breweries. Argentina’s economic instability restricts imports of advanced controllers, favoring refurbished units. Chile and Colombia show promise in wine and agricultural cold chains, adopting modular defrost systems for export-grade storage. However, unreliable grid infrastructure in rural areas limits the deployment of energy-intensive defrost technologies, pushing vendors to develop battery-compatible controllers. Currency fluctuations further complicate long-term contracts with international suppliers.

Middle East & Africa The GCC nations spearhead growth through large-scale HVAC projects (e.g., UAE’s Dubai Expo legacy infrastructure), deploying AI-optimized defrost controllers in smart buildings. Saudi Arabia’s Vision 2030 drives cold storage investments for pharmaceutical imports, while South Africa’s food processing sector adopts frost detection sensors to reduce spoilage. Sub-Saharan Africa remains underserved due to low electrification rates, though off-grid solar chillers present niche opportunities. The region’s reliance on European and Chinese imports persists, but local assembly initiatives in the UAE and Turkey aim to reduce lead times by 20–25% by 2030.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automatic Defrost Controller markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 128.7 million in 2024 and is projected to reach USD 185.4 million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Circulating Defrost, Non-circulating Defrost), application (Commercial, Home, Industrial), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America (USD 42.3 million in 2024), Europe, Asia-Pacific (fastest-growing at 6.8% CAGR), Latin America, and the Middle East & Africa.

Competitive Landscape: Profiles of leading market participants including RODGERS (12.5% market share), ICM Controls, Emerson, and Honeywell, covering their product portfolios and strategic developments.

Technology Trends & Innovation: Assessment of smart defrost technologies, IoT integration, and energy-efficient solutions driving market evolution.

Market Drivers & Restraints: Evaluation of refrigeration industry growth, energy efficiency regulations, and supply chain challenges affecting component availability.

Stakeholder Analysis: Strategic insights for HVAC manufacturers, component suppliers, and investors regarding emerging opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory bodies and trade associations to ensure accuracy.

Customization of the Report In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

Related Reports :

Contact us:

+91 8087992013

0 notes

Text

Europe Server Microprocessor Market : SWOT Analysis and Competitive Leadership Insights

This report presents a comprehensive analysis of the , providing stakeholders with valuable insights into its growth trajectory, opportunities, and challenges. The study explores key market dynamics, trends, competitive landscape, and future projections to assist decision-makers in strategic planning. Europe Server Microprocessor Market Overview Some of the major players covered in the market research report are: Intel Corporation Advanced Micro Devices (AMD) Inc. Texas Instruments Incorporated Qualcomm Technologies Inc. Applied Micro Circuits Corporation IBM Corporation Mediatek Inc. Toshiba Corporation NVIDIA Corporation and Hisilicon Technologies Co. Ltd. Get a free sample of the report:https://www.prophecymarketinsights.com/market_insight/Insight/request-sample/936 Industry Insights Current market status and key drivers shaping the industry. Emerging trends and innovations impacting market evolution. Economic and regulatory factors influencing market performance. Europe Server Microprocessor Market Scope & Segmentation By Design: X86, ARM, Power, and Others By Type: Integrated Graphics, Discrete Graphics, Analog-To-Digital and Digital-To-Analog Converter, and Others By Application: Smart Phones, Servers, Personal Computers, Tablets, and Others By End User: Large Enterprises, Medium Enterprises, and Small Enterprises Competitive Landscape Key Players & Market Positioning Analysis of major competitors, including market share, business strategies, and innovations. SWOT analysis of key industry participants. Market entry barriers and opportunities for new entrants. Request a PDF Brochure of the Report:https://www.prophecymarketinsights.com/market_insight/Insight/request-pdf/936 Europe Server Microprocessor Market Dynamics Drivers Factors fueling market demand and expansion. Technological advancements influencing growth. Challenges & Restraints Potential risks, barriers, and regulatory constraints. Economic fluctuations and supply chain disruptions. Opportunities Untapped market potential and emerging consumer needs. Strategic investment areas and growth prospects. Regional Analysis Europe Server Microprocessor Market Performance by Region Regional demand variations and economic impact. Key players and competitive environment in each region. Infrastructure, policies, and trade regulations affecting market growth. Get Flat 30% OFF on Europe Server Microprocessor Market:https://www.prophecymarketinsights.com/market_insight/Insight/request-discount/936 Consumer Insights & Behavioral Trends Shifting customer preferences and purchasing patterns. Influence of digital transformation on market demand. Impact of sustainability and ethical sourcing on buying decisions. Future Outlook & Forecast Potential disruptions and innovations shaping the industry. Strategic recommendations for stakeholders. Conclusion & Strategic Recommendations Summary of key findings and takeaways. Actionable insights for investors, businesses, and policymakers. Recommendations for capitalizing on emerging trends. About Us: Prophecy Market Insights is a leading provider of market research services, offering insightful and actionable reports to clients across various industries. With a team of experienced analysts and researchers, Prophecy Market Insights provides accurate and reliable market intelligence, helping businesses make informed decisions and stay ahead of the competition. The company's research reports cover a wide range of topics, including industry trends, market size, growth opportunities, competitive landscape, and more. Prophecy Market Insights is committed to delivering high-quality research services that help clients achieve their strategic goals and objectives.

0 notes

Text

What Are the Latest Innovations Transforming the Prosthetic Limbs Market in 2024?

The global Prosthetic Limbs Market Size was valued at USD 1.95 billion in 2023 and is projected to reach USD 3.07 billion by 2032, growing at a compound annual growth rate (CAGR) of 5.18% during the forecast period of 2024–2032. This impressive growth reflects the increasing demand for advanced prosthetics, improvements in healthcare infrastructure, and greater awareness about mobility restoration technologies. As the population ages and the number of amputations due to diabetes and traumatic injuries continues to rise, the prosthetics industry is rapidly evolving to meet these new challenges with smart, efficient, and customized solutions.

https://www.snsinsider.com/assets/images/report/1731997958-709192537.png

Market Dynamics and Key Drivers

The rise in limb loss cases due to road accidents, diabetes-related complications, and vascular diseases has significantly increased the demand for prosthetic limbs globally. In addition, ongoing R&D in materials such as lightweight carbon fiber and AI-integrated components has resulted in more functional and comfortable prosthetic limbs, further accelerating market adoption.

Healthcare professionals and patients alike are placing higher value on customizable and user-friendly prosthetic devices that restore near-natural movement. Countries with aging populations, especially in North America, Europe, and parts of Asia-Pacific, are leading the charge in prosthetic limb demand, thanks to supportive healthcare reimbursement policies and government initiatives.

Technology Paving the Way for Market Expansion

The introduction of myoelectric prosthetics and bionic limbs powered by microprocessors is transforming patient outcomes and daily usability. These innovations not only improve mobility and dexterity but also enhance the quality of life for amputees. Manufacturers are investing heavily in AI and sensor technologies to produce smarter, responsive prosthetics capable of real-time movement correction and muscle signal detection.

Regional Outlook

North America continues to dominate the prosthetic limbs market due to its advanced healthcare ecosystem, favorable insurance coverage, and significant investments in innovation. Meanwhile, the Asia-Pacific region is expected to witness the fastest growth, with countries such as India, China, and Japan focusing on improving access to prosthetic care and expanding orthopedic services in rural areas.

Competitive Landscape

Key players in the prosthetic limbs market include Össur, Ottobock, Blatchford, Steeper Group, WillowWood Global, and Fillauer LLC. These companies are pursuing strategic partnerships, new product launches, and regional expansion to stay competitive in a rapidly advancing industry.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us: Jagney Dave – Vice President of Client Engagement 📞 +1-315 636 4242 (US) | +44- 20 3290 5010 (UK) 📧 [email protected]

#prosthetic limbs market#prosthetics industry growth#medical device market trends#prosthetic limb technology#global prosthetic limbs forecast

0 notes

Text

Automotive Chipset Market Growth and Development Insight - Size, Share, Growth, and Industry Analysis - MarkNtel Advisors

According to Markntel Advisors Report, Automotive Chipset Market is expected to grow at a significant growth rate, and the analysis period is 2024-2030, considering the base year as 2023.Consistent monitoring and evaluating of market dynamics to stay informed and adapt your strategies accordingly. As a market research and consulting firm, we offer market research reports that focus on major parameters including Target Market Identification, Customer Needs and Preferences, Thorough Competitor Analysis, Market Size & Market Analysis, and other major factors. At the end, we do provide meaningful insights and actionable recommendations that inform decision-making and strategy development.

Automotive chipsets are specialized integrated circuits designed for vehicle applications to provide essential functionalities like control, processing, and connectivity for systems such as infotainment and Advanced Driver-Assistance Systems (ADAS). These chipsets are engineered to meet the rigorous reliability and performance requirements of automotive environments and ensure safe & efficient operation in vehicles.

Global Automotive Chipset Market Research Report & Summary:

The Global Automotive Chipset Market size is estimated to grow at a CAGR of around 12.5% during the forecast period, i.e., 2024-30.

Time Period Captured in the Report:

Historical Years: 2019-22

Base Years: 2023

Forecast Years: 2024-30

Who are the Key Players Operating in the Automotive Chipset Market?

The top companies of the Automotive Chipset Market ruling the industry are:

NXP Semiconductors, Analog Devices, Inc., Renesas Electronics Corporation, Toshiba Corporation, Robert Bosch GmbH, ROHM Co., Ltd., Infineon Technologies AG, Texas Instruments Incorporated, STMicroelectronics, Samsung Electronics, NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., Microchip Technology, Inc., SK Hynix Inc., and among others

Our Latest Reports Now Include In-Depth Supply Chain Ecosystem Analysis, Enabling Businesses to Navigate Tariff Challenges with Greater Agility Get Sample Report - https://www.marknteladvisors.com/query/request-sample/automotive-chipset-market.html

("Kindly use your official email ID for all correspondence to ensure seamless engagement and access to exclusive benefits, along with prioritized support from our sales team.")

✅In case you missed it, we are currently revising our reports. Click on the below to get the latest research data with forecast for years 2025 to 2030, including market size, industry trends, and competitive analysis. It wouldn’t take long for the team to deliver the most recent version of the report.

What is Included in Automotive Chipset Market Segmentation?

The Automotive Chipset Market explores the industry by emphasizing the growth parameters and categorizes including geographical segmentation, to offer a comprehensive understanding of the market dynamic. The further bifurcations are as follows:

-By Chip Type

-Analog ICs- Market Size & Forecast 2019-2030F, USD Million

-Logic ICs- Market Size & Forecast 2019-2030F, USD Million

-Microcontrollers & Microprocessors- Market Size & Forecast 2019-2030F, USD Million

-Others (Memory ICs, Interface ICs, etc.)- Market Size & Forecast 2019-2030F, USD Million

-By Vehicle Type

-Passenger Vehicles- Market Size & Forecast 2019-2030F, USD Million

-Commercial Vehicles- Market Size & Forecast 2019-2030F, USD Million

-Light Commercial Vehicles- Market Size & Forecast 2019-2030F, USD Million

-Medium & Heavy Commercial Vehicles- Market Size & Forecast 2019-2030F, USD Million

-By Propulsion

-ICE- Market Size & Forecast 2019-2030F, USD Million

-Electric or Hybrid Vehicles- Market Size & Forecast 2019-2030F, USD Million

-By Application

-Safety System- Market Size & Forecast 2019-2030F, USD Million

-Body Electronics- Market Size & Forecast 2019-2030F, USD Million

-Chassis- Market Size & Forecast 2019-2030F, USD Million

-Telematics & Infotainment- Market Size & Forecast 2019-2030F, USD Million

-Powertrain- Market Size & Forecast 2019-2030F, USD Million

-Others (Advance Driver Assistance System (ADAS), Autonomous Driving, etc.) - Market Size & Forecast 2019-2030F, USD Million

-By Region

-North America

-South America

-Europe

-The Middle East & Africa

-Asia-Pacific

Explore the Complete Automotive Chipset Market Analysis Report – https://www.marknteladvisors.com/research-library/automotive-chipset-market.html

Global Automotive Chipset Market Driver:

Rapid Expansion of Automotive Chips in Response to Vehicle Electrification & Intelligence – The rapid expansion of automotive chips is closely related to the increasing use of electric vehicles. As automobiles advance into the smart era, automotive chips are becoming fundamental to this transition. They serve as the backbone of the technological revolution in vehicles, particularly within smart terminals, which act as central control centers for these innovations. Various chips, including primary control, power, memory, communication, and interface chips, are experiencing swift development to meet the growing demands of electric vehicles.

Moreover, the ongoing refinement of autonomous driving technology is further fueling the expansion of automotive chips, requiring a significantly higher number of different chip types, compared to traditional automobiles. Moreover, as manufacturing facilities are being built & expanded in the US, American companies are still reliant on manufacturers in Asia for high-quality and economical chipsets for vehicle..

Need personalized insights? Click here to customize this report- https://www.marknteladvisors.com/query/request-customization/automotive-chipset-market.html

Why Markntel Advisor Report?

MarkNtel Advisors is a leading consulting, data analytics, and market research firm that provides an extensive range of strategic reports on diverse industry verticals. We being a qualitative & quantitative research company, strive to deliver data to a substantial & varied client base, including multinational corporations, financial institutions, governments, and individuals, among others.

We have our existence across the market for many years and have conducted multi-industry research across 80+ countries, spreading our reach across numerous regions like America, Asia-Pacific, Europe, the Middle East & Africa, etc., and many countries across the regional scale, namely, the US, India, the Netherlands, Saudi Arabia, the UAE, Brazil, and several others.

For Further Queries:

Contact Us

MarkNtel Advisors

Email at [email protected]

Corporate Office: Office No.109, H-159, Sector 63, Noida, Uttar Pradesh - 201301, India

0 notes

Text

0 notes

Text

IoT Chips Market is Driven by Explosive Connectivity Demand

Internet of Things (IoT) chips are specialized microprocessors, system-on-chips (SoCs), and connectivity modules designed to enable seamless data exchange among sensors, devices, and cloud platforms. These chips incorporate ultra-low-power architectures, embedded security protocols, and advanced signal processing capabilities that support a broad spectrum of IoT applications—from smart homes and wearable gadgets to industrial automation and connected vehicles. Advantages include reduced latency through edge computing, optimized energy efficiency for battery-operated devices, and streamlined integration into existing network infrastructures.

As businesses pursue digital transformation, there is a growing need for reliable, scalable chipsets capable of handling massive device connectivity, real-time analytics, and robust encryption. Continuous innovation in semiconductor fabrication processes has driven down production costs and boosted performance metrics, enabling smaller startups and established market players alike to introduce competitive products. Meanwhile, evolving market trends such as 5G rollout, AI-enabled analytics, and smart city initiatives are creating new IoT Chips Market opportunities and shaping the industry landscape. Comprehensive market research highlights expanding market segments in healthcare monitoring, agricultural sensors, and asset tracking.

The IoT chips market is estimated to be valued at USD 620.36 Bn in 2025 and is expected to reach USD 1415.005 Bn by 2032, growing at a compound annual growth rate (CAGR) of 15.00% from 2025 to 2032. Key Takeaways

Key players operating in the IoT Chips Market are:

-Intel Corporation

-Samsung Electronics Co. Ltd

-Qualcomm Technologies Inc.

-Texas Instruments Incorporated

-NXP Semiconductors NV

These market companies have established strong footholds through diversified product portfolios that span microcontrollers, application processors, short-range wireless SoCs, and AI inference engines. Their strategic investments in R&D, partnerships with tier-one automotive and industrial firms, and capacity expansions in fabrication plants are instrumental in driving market share growth. Robust alliances and licensing agreements help these players accelerate time-to-market for next-generation solutions, while continuous performance enhancements maintain their competitive edge. As major players optimize supply chains and strengthen IP portfolios, they contribute significantly to the overall market dynamics and industry size. The growing demand for IoT chips is fueled by accelerated digitalization across verticals such as automotive, healthcare, consumer electronics, and manufacturing. Automotive OEMs are integrating IoT chips for connected car features—remote diagnostics, vehicle-to-everything (V2X) communication, and advanced driver-assistance systems (ADAS)—driving substantial market growth. In healthcare, remote patient monitoring and telemedicine solutions rely on miniaturized, power-efficient chips to ensure continuous data transmission and secure access. Additionally, smart agriculture applications leverage low-cost sensors and communication modules to optimize resource usage and crop yields. As enterprises embrace Industry 4.0, the deployment of IoT solutions for predictive maintenance and asset tracking has become a critical business growth strategy. These evolving market trends underscore the importance of high-performance, cost-effective IoT chips to sustain long-term expansion.

‣ Get More Insights On: IoT Chips Market

‣ Get this Report in Japanese Language: IoTチップ市場

‣ Get this Report in Korean Language: IoT칩시장

0 notes

Text

Box Compression Tester Price in West Bengal

Unlocking Packaging Strength: Box Compression Tester Price in West Bengal – LabZenix

Introduction

In the fast-paced packaging industry of India, especially in West Bengal, manufacturers are continuously seeking reliable ways to ensure product safety and structural integrity during transit and storage. One of the most essential tools in this process is the box compression tester. This sophisticated testing equipment plays a vital role in evaluating the compressive strength of corrugated and packaging boxes. For businesses in the region, understanding the Box Compression Tester Price in West Bengal is crucial for budgeting and procurement.

LabZenix, a trusted name in the testing equipment industry, delivers premium solutions backed by innovation, accuracy, and cost-effectiveness. In this article, we’ll explore the factors affecting the box compression tester price in West Bengal, LabZenix’s product offerings, applications, benefits, and frequently asked questions.

What is a Box Compression Tester?

A box compression tester is a precision instrument used to measure the maximum compressive force a packaging box can withstand before it deforms or collapses. It simulates the pressure boxes face when stacked or transported, thereby helping manufacturers guarantee packaging quality and performance.

Whether it's for corrugated boxes, folding cartons, or other rigid containers, the box compression tester is an essential quality control instrument for packaging industries, e-commerce, food and beverage sectors, logistics companies, and more.

Why West Bengal Needs Reliable Box Compression Testing

West Bengal has emerged as a growing hub for packaging, FMCG, and industrial logistics due to its strategic location and vibrant manufacturing base. Businesses in cities like Kolkata, Durgapur, Siliguri, and Asansol are increasingly relying on accurate packaging testing equipment.

As demand rises, so does the curiosity about the box compression tester price in West Bengal. LabZenix addresses this need by offering highly competitive pricing without compromising on performance, reliability, or support.

Factors Affecting Box Compression Tester Price in West Bengal

Understanding what determines the box compression tester price in West Bengal can help businesses make informed buying decisions. Key factors include:

1. Machine Capacity

LabZenix offers machines in various capacities ranging from 500 kgf to 5000 kgf, depending on the box type and industry. Higher capacities come at a higher price but offer broader testing applications.

2. Digital or Computerized Model

Digital models display results on a screen, while computerized variants offer detailed graphs, test reports, and connectivity with analysis software. Computerized models naturally influence the final box compression tester price in West Bengal.

3. Platform Size

Box sizes vary greatly. LabZenix offers customized platform sizes, and this customization can also slightly alter the overall box compression tester price in West Bengal.

4. Automation and Features

Advanced features like overload protection, automatic report generation, or programmable test cycles can increase the cost. However, these features also enhance accuracy and operational efficiency.

5. Brand and After-Sales Service

Choosing a trusted brand like LabZenix ensures you receive quality products with local service support in West Bengal, making your investment worthwhile.

LabZenix: Your Partner for Box Compression Testers in West Bengal

LabZenix is known across India for its premium quality lab testing equipment. With a focus on customer-centric pricing, LabZenix offers some of the most affordable and durable box compression testers in the market.

Key Features of LabZenix Box Compression Testers:

Precision load cells for accurate measurements

Microprocessor-based digital display or computerized controls

Rigid frame construction with safety features

Customizable platform dimensions

Compliance with global standards (ASTM, ISO, IS)

Local service support across West Bengal

If you're exploring the box compression tester price in West Bengal, LabZenix provides full quotations, demo availability, and end-to-end installation support.

Price Range of Box Compression Testers in West Bengal

While actual costs depend on specifications and features, here’s a general price range: Model TypeApprox. Price (INR)Digital Manual Model (Basic)₹85,000 – ₹1,20,000Digital Auto Model (Standard)₹1,50,000 – ₹2,00,000Computerized High-End Model₹2,25,000 – ₹3,50,000Customized Heavy-Duty Model₹3,75,000 – ₹5,00,000+

Note: These prices are indicative for West Bengal and may vary depending on shipping, customization, and installation costs.

Applications of Box Compression Tester

Corrugated box manufacturing

FMCG packaging

E-commerce packaging evaluation

Textile and garment box testing

Pharmaceutical packaging

Logistics and warehousing

Reliable packaging is not just a quality concern—it’s a brand reputation issue. LabZenix helps brands maintain consistency and prevent product damage during shipment.

Benefits of Investing in LabZenix Box Compression Tester

Accurate strength evaluation of packaging

Reduces transit damage complaints

Compliance with international testing standards

Boosts client confidence in product safety

Available at a fair box compression tester price in West Bengal

Durable build and low maintenance

Prompt support and training from local service teams

FAQs – Box Compression Tester Price in West Bengal

Q1: What is the average box compression tester price in West Bengal?

A: The average price ranges from ₹85,000 to ₹3,50,000 depending on the model and features. LabZenix offers competitive pricing with exceptional after-sales support.

Q2: Can I get a customized box compression tester in Kolkata?

A: Yes. LabZenix provides full customization on platform size, capacity, and features. Delivery and installation are available across Kolkata and other West Bengal cities.

Q3: Do LabZenix machines comply with testing standards?

A: Absolutely. All LabZenix box compression testers comply with ASTM, ISO, and BIS standards to ensure accurate and globally acceptable results.

Q4: How do I get a price quote for a box compression tester in West Bengal?

A: Simply contact LabZenix through their website or customer helpline. Their sales team will guide you through the selection and provide a customized quote based on your needs.

Q5: Is training provided during installation?

A: Yes. LabZenix provides full operational training and maintenance guidance with every machine installation in West Bengal.

Conclusion

If you’re looking to invest in quality packaging control tools, understanding the box compression tester price in West Bengal is the first step. LabZenix, with its legacy of precision and trust, offers the perfect balance of technology, durability, and affordability.

From basic digital models to advanced computerized testers, LabZenix provides everything a packaging unit in West Bengal needs to ensure consistent box quality. With reliable support, local service, and budget-friendly options, LabZenix is your go-to partner for all box compression testing needs.

Choose wisely. Choose LabZenix

#labzenix#industrial#technology#labzenix box compression tester#box compression strength tester#box compression tester

0 notes

Text

Microprocessor and GPU Market Size, Strategic Trends, End-Use Applications

The microprocessor and GPU market was valued at USD 88.02 billion in 2022 and is expected to reach USD 178.25 billion by 2030, growing at a CAGR of 9.45% during the forecast period. The growth is driven by increasing demand for high-performance computing, AI acceleration, data centers, autonomous systems, and enhanced graphic processing needs across industries.

Overview

Microprocessors and graphics processing units (GPUs) serve as the core computational engines of modern digital devices. Microprocessors are designed for general-purpose processing, managing operating systems, and running applications. GPUs, originally developed for rendering graphics, are now widely used in parallel processing, machine learning, and real-time data analysis.

As digital transformation accelerates across the globe, the need for faster, more efficient, and specialized processors continues to rise. Applications ranging from cloud computing, gaming, and automotive electronics to edge AI and IoT devices are fueling demand. Moreover, the emergence of new technologies such as 5G, AI, and metaverse platforms is reinforcing the market’s long-term growth potential.

Market Segmentation

By Type

Microprocessor (CPU)

Graphics Processing Unit (GPU)

By Architecture

x86

ARM

MIPS

PowerPC

SPARC

RISC-V

By Application

Consumer Electronics

Automotive

Industrial Automation

Healthcare

Aerospace and Defense

Telecommunications

Data Centers

Gaming

By End-User

Enterprises

Government

Individuals

Cloud Service Providers

OEMs

Key Trends

Rise of heterogeneous computing combining CPU and GPU cores

Expansion of AI workloads, pushing GPU development in edge and cloud environments

Increasing integration of GPU-based accelerators in autonomous vehicles and smart devices

Growth in ARM-based microprocessors, especially for mobile and embedded applications

Miniaturization and energy efficiency trends in IoT devices and wearables

Segment Insights

Type Insights: Microprocessors dominate in traditional computing, smartphones, and embedded systems. However, GPUs are witnessing exponential demand due to their superior parallel processing capabilities, especially in AI training, inference engines, and 3D modeling.

Architecture Insights: x86 architecture leads the market due to widespread use in PCs and servers. ARM architecture is gaining traction in mobile, automotive, and low-power devices. RISC-V is emerging as an open-source alternative in academia and next-gen chip research.

Application Insights: Consumer electronics such as smartphones, tablets, and PCs remain the largest application segment. However, the fastest-growing sectors are automotive (for ADAS and autonomous driving), healthcare (for imaging and diagnostics), and telecommunications (for 5G infrastructure and network slicing).

End-User Insights

Enterprises: Rely on high-performance CPUs and GPUs for servers, data centers, and enterprise applications.

Cloud Providers: Heavily invest in GPU-based infrastructure for AI, machine learning, and virtual computing.

Government and Defense: Utilize advanced processors for simulation, encryption, and real-time intelligence.

OEMs: Integrate customized processors into devices such as AR/VR headsets, drones, and robots.

Individuals: High consumer demand for gaming PCs, laptops, and graphic-intensive applications.

Regional Analysis

North America: Leads in R&D, chip manufacturing (especially GPUs), and cloud computing infrastructure.

Europe: Focused on industrial automation, automotive processors, and green computing.

Asia-Pacific: Fastest-growing region, driven by electronics production in China, South Korea, Taiwan, and India.

Latin America: Rising demand for mobile devices, smart home electronics, and gaming consoles.

Middle East & Africa: Emerging applications in smart cities, telecom, and security analytics.

Key Players

Leading companies in the microprocessor and GPU market include Intel Corporation, AMD (Advanced Micro Devices), NVIDIA Corporation, Qualcomm Technologies, Samsung Electronics, Apple Inc., MediaTek, IBM Corporation, ARM Holdings, and Imagination Technologies.

These players are investing in chiplet design, advanced process nodes (like 3nm and below), AI accelerators, and integrated system-on-chip (SoC) platforms. Collaborations with cloud providers, automotive OEMs, and software developers are also driving performance-specific innovation and ecosystem expansion.

Future Outlook

The market for microprocessors and GPUs will remain a critical pillar of global digital infrastructure. Future growth will be shaped by quantum computing research, AI-native chipsets, neuromorphic processors, and photonic integration. Sustainable semiconductor manufacturing and energy-efficient chip designs will also gain strategic importance as environmental concerns intensify.

Trending Report Highlights

Beam Bender Market

Depletion Mode JFET Market

Logic Semiconductors Market

Semiconductor Wafer Transfer Robots Market

US Warehouse Robotics Market

0 notes

Text

0 notes

Text

Semiconductor Ceramic Components Market 2025-2032

The global Semiconductor Ceramic Components Market size was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 5.23 billion by 2032, at a CAGR of 5.9% during the forecast period 2025-2032

Semiconductor Ceramic Components Market Overview:

Semiconductor ceramics refer to electronic ceramics that incorporate semiconductor grains and grain boundaries. These ceramics can efficiently convert physical signals into electrical signals, making them essential in advanced electronic applications such as sensors, actuators, and communication devices.

Global Semiconductor Market Outlook (2022–2029)

Market Size in 2022: US$ 579 billion

Projected Market Size by 2029: US$ 790 billion

CAGR (2022–2029): 6%

Key Segment Growth in 2022

Despite overall modest growth, several segments showed double-digit year-over-year (YoY) growth in 2022:

Analog ICs: +20.76%

Sensors: +16.31%

Logic Devices: +14.46%

Memory Segment: Declined by −12.10% YoY

Microprocessor (MPU) and Microcontroller (MCU) Market Trends

Growth Status: Stagnant

Reasons:

Decline in notebook and desktop shipments

Weaker investments in standard computing devices

However, the rising adoption of IoT-enabled devices is creating new opportunities for hybrid processors.

Grab Your Complimentary Sample Report-https://semiconductorinsight.com/download-sample-report/?product_id=97953

Impact of IoT on Semiconductor Growth

IoT Electronics demand powerful processing and control capabilities.

Hybrid MPUs and MCUs are becoming essential for:

Real-time embedded processing

Efficient control systems in IoT applications

This trend is boosting demand in both consumer and industrial sectors.

Analog Integrated Circuit (IC) Segment Insights

Growth Trend: Gradual

Key Demand Drivers:

Signal Conversion (e.g., ADC/DAC)

Automotive Analog Applications (e.g., sensors, braking systems)

Power Management (e.g., voltage regulation and efficiency)

However, networking and communication sectors show limited demand currently, slightly slowing overall Analog IC momentum.

Discrete Power Devices: Rising Demand

Analog circuit developments also drive the need for discrete power devices, essential in:

Power supply units

Electric vehicle systems

Renewable energy applications

Semiconductor Ceramic Components Key Market Trends :

Rising Use in Advanced Wafer Applications Increasing adoption in 300mm and 200mm wafer production is driving the demand for high-performance ceramic components.

Integration with IoT-Based Electronics The growth of IoT devices is pushing demand for hybrid MPUs and MCUs, boosting the need for reliable semiconductor ceramics.

Growth of Analog and Sensor Devices Analog IC and sensor components are witnessing high growth rates, fueling market expansion for ceramic parts.

Focus on Energy Efficiency and Miniaturization The trend toward energy-efficient and compact electronics is promoting innovation in ceramic semiconductor materials.

Increased R&D in Smart Materials Development of photosensitive, gas-sensitive, and pressure-sensitive ceramics supports the growth of smart applications and sensors.

Semiconductor Ceramic Components Market Segmentation :

Global Semiconductor Ceramic Components market, by Type, 2020-2025, 2026-2032 ($ millions) & (K Units) Global Semiconductor Ceramic Components market segment percentages, by Type, 2024 (%)

Photosensitive

Heat Sensitive

Pressure Sensitive

Moisture Sensitive

Gas Sensitive

Global Semiconductor Ceramic Components market, by Application, 2020-2025, 2026-2032 ($ Millions) & (K Units) Global Semiconductor Ceramic Components market segment percentages, by Application, 2024 (%)

300mm Wafer

200mm Wafer

Others

Competitor Analysis The report also provides analysis of leading market participants including:

Key companies Semiconductor Ceramic Components revenues in global market, 2020-2025 (estimated), ($ millions)

Key companies Semiconductor Ceramic Components revenues share in global market, 2024 (%)

Key companies Semiconductor Ceramic Components sales in global market, 2020-2025 (estimated), (K Units)

Key companies Semiconductor Ceramic Components sales share in global market, 2024 (%)

Further, the report presents profiles of competitors in the market, key players include:

KYOCERA China

NGK Insulators

Applied Ceramics

CoorsTek

Ferrotec

Suzhou Kematek

SeaTools Corporation

Svenska Kullagerfabriken

SHANGHAI COMPANION PRECISION CERAMICS

TOCHANCE TECHNOLOGY

XIDE Technology

JAPAN FINE CERAMICS

COREWAY OPTECH

Hangzhou Semiconductor Wafer

Electronics Notes

Maruwa

NGK Spark Plug

SCHOTT Electronic Packaging

NEO Tech

AdTech Ceramics

Ametek

ECRI Microelectronics

SoarTech

Semiconductor Enclosures Inc(SEI)

Claim Your Free Sample Report-https://semiconductorinsight.com/download-sample-report/?product_id=97953

FAQs

Q1. What are the key driving factors and opportunities in the Semiconductor Ceramic Components market? A: Key drivers include the rising use in advanced wafer production and IoT electronics. Opportunities exist in smart sensors and clean energy applications.

Q2. Which region is projected to have the largest market share? A: Asia-Pacific is expected to dominate the market due to strong semiconductor manufacturing bases in China, Japan, and South Korea.

Q3. Who are the top players in the global Semiconductor Ceramic Components market? A: Leading players include Kyocera, Murata, CoorsTek, NGK Insulators, and CeramTec.

Q4. What are the latest technological advancements in the industry? A: Recent advancements involve smart ceramics with gas, pressure, and photosensitive properties for high-end sensor applications.

Q5. What is the current size of the global Semiconductor Ceramic Components market? A: The market size was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 5.23 billion by 2032.

0 notes

Text

Global Extreme Ultraviolet Lithography (EUVL) Market Outlook 2025–2032

The global Extreme Ultraviolet Lithography (EUVL) market was valued at US$ 507.7 million in 2023 and is projected to reach US$ 1468.9 million by 2030, at a CAGR of 16.0% during the forecast period.Market size in 2023US$ 507.7 MillionForecast Market size by 2030US$ 1468.9 MillionGrowth RateCAGR of 16.0%Number of Pages200+ Pages

“Extreme ultraviolet lithography (EUVL)” is a leading next-generation lithography (NGL) technology used to print lines as small as 30nm and develop microprocessors and microchips. This technology may replace optical lithography, which is currently used to create microcircuits. The EUVL system operates by directing strong beams of ultraviolet light reflected from a circuit design pattern onto a silicon wafer.

EUVL systems utilize extremely short wavelength technology, which can be applied down to the 10nm node. However, three significant challenges must be addressed before mass production can occur: a light power source, resistance, and mask infrastructure.

EUVL is a forefront NGL technology capable of printing lines as small as 30nm, crucial for developing microprocessors and microchips. This method has the potential to supplant optical lithography, which is used for current microcircuits. The system functions by projecting intense beams of ultraviolet light, reflected from a circuit design pattern, onto a silicon wafer.

EUVL systems feature extremely short wavelength technology, applicable down to the 10nm node. However, for this approach to reach mass production, three key concerns must be resolved: a light power source, resistance, and mask infrastructure.

EUVL, one of the foremost next-generation lithography technologies, prints lines as narrow as 30nm to develop advanced microprocessors and microchips. This technology could replace the optical lithography used in today’s microcircuits. The EUVL system burns strong ultraviolet light beams reflected from a circuit design pattern onto a silicon wafer.

This research report provides a comprehensive analysis of the Extreme Ultraviolet Lithography (EUVL) market, focusing on the current trends, market dynamics, and future prospects. The report explores the global Extreme Ultraviolet Lithography (EUVL) market, including major regions such as North America, Europe, Asia-Pacific, and emerging markets. It also examines key factors driving the growth of Extreme Ultraviolet Lithography (EUVL), challenges faced by the industry, and potential opportunities for market players.