#Motion Sensor Market Applications

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 411 employees.

Text

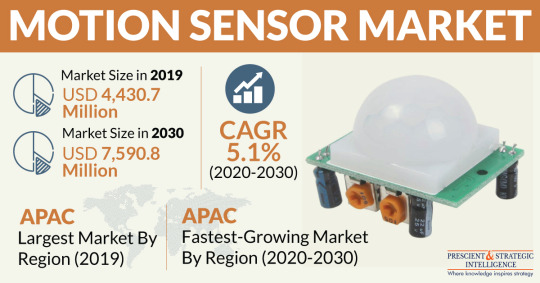

Burgeoning Sales of Consumer Electronics Driving Motion Sensor Market

The global motion sensor market was valued at $4,430.7 million in 2019, and it is predicted to reach a revenue of $7,590.8 million by 2030. According to the estimates of the market research company, P&S Intelligence, the market will progress at a CAGR of 5.1% from 2020 to 2030 (forecast period). The market is being driven by the surging demand for consumer electronics, such as smartphones, laptops, and tablets. Motion sensors are heavily used in heart rate monitors, which are used in smart wearable devices and to control the orientation of smartphone screens.

The ballooning need for smartphones and wearable devices among young individuals, particularly the millennials, is fueling the demand for motion sensors. In addition, the surging population of people across the globe is also propelling the demand for consumer electronic devices, which is, in turn, driving the expansion of the motion sensor market. Besides, the growing use of internet of things (IoT)-connected devices is also creating immense growth opportunities for the players operating in the industry.

According to the Institute of Electrical and Electronics Engineers (IEEE), around 27 billion IoT devices were in use all over the world in 2017, and this number will surge to 125 billion by 2030. With the integration of IoT capabilities, motion sensors can easily monitor and track the physical status of a device remotely. Further, these devices can enhance several building automation applications, such as lighting and heating, ventilation, and air conditioning (HVAC) systems.

The other major motion sensor market growth driver is the booming automotive industry across the world. In this industry, motion sensors are extensively used for applications, such as airbag systems, vehicle alarm systems, and wheel alignment systems. As per the International Organization of Motor Vehicle Manufacturers (OICA), 95.1 million automobiles, including passenger and commercial vehicles, were sold all over the world in 2018, thereby registering a CAGR of 1.8% between 2014 and 2018. Furthermore, the growing deployment of electric vehicles is expected to fuel the expansion of the automotive industry.

Depending on type, the motion sensor market is divided into combo sensor, ultrasonic, infrared, accelerometer, tomographic sensor, and gyroscope categories. Out of these, the combo sensor category is predicted to demonstrate the highest growth rate in the market in the coming years. This is ascribed to the microfabrication of several types of motion sensors into a single device, which results in higher accuracy in detecting motion. Moreover, in consumer electronic devices, especially smartphones, combo sensors are heavily used wherein a single MEMS system integrates magnetometer, gyroscope, and accelerometer.

Globally, the Asia-Pacific (APAC) region contributed the highest revenue to the industry during the last few years. This was because of the high requirement for motion sensors, especially in China, on account of the country’s dominance in the worldwide manufacturing sector. China and the U.S. are the major countries in which the sales of motion sensors are skyrocketing. This is attributed to the booming automobile and consumer electronic industries in these countries. Additionally, the growing sales of smartphones are also positively impacting the industry, especially in China.

Hence, it can be safely said that the demand for motion sensors will surge sharply in the coming years, primarily because of the mushrooming sales of consumer electronics across the world.

Source: P&S Intelligence

#Motion Sensor Market Share#Motion Sensor Market Size#Motion Sensor Market Growth#Motion Sensor Market Applications#Motion Sensor Market Trends

1 note

·

View note

Text

Is the MEMS Accelerometer & Gyroscope Market Set to Skyrocket? Here's What You Need to Know

Introduction

The global MEMS Accelerometer and Gyroscope Market is experiencing rapid growth, largely driven by the increasing demand for motion-sensing technology across various high-tech industries. This growth is evident in sectors such as consumer electronics, automotive, aerospace, and healthcare. MEMS sensors, which include accelerometers, gyroscopes, and Inertial Measurement Units (IMUs), are integral to technologies requiring precise motion detection, navigation, and stability control.

As we move further into the 21st century, the adoption of MEMS accelerometers and gyroscopes in advanced devices such as smartphones, wearables, autonomous vehicles, and drones is expanding the market's reach. From a technological perspective, MEMS sensors have become more efficient, smaller in size, and significantly more power-efficient, which contributes to the growth of this market.

The MEMS accelerometer and gyroscope market is projected to grow at a robust compound annual growth rate (CAGR) of 10.5% from 2025 to 2032, a clear indication of the potential and importance of MEMS technology across a wide range of industries.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40601-global-mems-accelerometer-and-gyroscope-market

Market Dynamics: Forces Shaping the MEMS Accelerometer and Gyroscope Market

Increasing Demand Across Key Industries

The primary driver of the MEMS accelerometer and gyroscope market's rapid expansion is the increasing demand for motion-sensing technology across a variety of industries:

Consumer Electronics: MEMS sensors are widely used in smartphones, wearables, and gaming devices. The increasing reliance on touch-based interfaces, augmented reality (AR), and virtual reality (VR) applications drives the demand for high-precision motion sensors.

Automotive: The automotive industry is another major contributor to the growth of MEMS accelerometers and gyroscopes. These sensors are essential in advanced driver-assistance systems (ADAS), autonomous vehicles, and stability control systems, where accurate motion detection is crucial.

Aerospace: In aerospace applications, MEMS sensors are used in navigation systems, stability control, and flight systems for precision and reliability.

Healthcare: The healthcare industry has also seen an uptick in MEMS adoption, particularly in medical devices such as wearable health trackers, implantable devices, and diagnostic equipment.

The continued innovation in these sectors, alongside the integration of MEMS sensors into next-generation devices, will drive sustained growth in the coming years.

Get up to 30% Discount: https://www.statsandresearch.com/check-discount/40601-global-mems-accelerometer-and-gyroscope-market

Technological Advancements

Recent advancements in MEMS technology have significantly enhanced the functionality, miniaturization, and energy efficiency of sensors. The trend towards sensor fusion—integrating accelerometers, gyroscopes, and magnetometers into single units—has led to more versatile motion sensors. These sensors are capable of providing highly accurate real-time data processing for a variety of complex applications, including industrial automation, robotics, and AR/VR experiences.

Moreover, the growing demand for low-power MEMS sensors to support energy-efficient applications across industries such as wearables and automotive systems has spurred further innovation.

Rise of Emerging Technologies

The MEMS accelerometer and gyroscope market is also benefiting from the rise of emerging technologies, notably:

Internet of Things (IoT): MEMS sensors are key enablers in the development of smart devices and systems that form the backbone of IoT networks. Their compact size and low power consumption make them ideal for IoT devices in homes, factories, and healthcare settings.

Artificial Intelligence (AI): AI-powered systems require high-performance sensors that enable precise motion tracking, which is where MEMS technology plays a crucial role.

Autonomous Systems: Drones, autonomous vehicles, and robots rely heavily on MEMS sensors for navigation, motion detection, and flight control.

These emerging technologies continue to open up new applications for MEMS sensors and will drive future growth.

Challenges in the MEMS Accelerometer and Gyroscope Market

Despite the promising outlook, there are several challenges that could hinder the growth of the MEMS accelerometer and gyroscope market:

High Manufacturing Costs: MEMS technology can be expensive to produce due to the complexity of the fabrication process. This could make it challenging for smaller companies or developing markets to afford high-precision MEMS sensors.

Supply Chain Disruptions: The MEMS industry relies heavily on specific semiconductor materials and components, which makes it vulnerable to supply chain disruptions, especially in a global market where raw material prices fluctuate.

Calibration Complexity: High-precision MEMS sensors require intricate calibration processes, which can be resource-intensive and time-consuming.

However, technological advancements and efforts to streamline production and calibration are expected to mitigate these challenges over time.

MEMS Accelerometer and Gyroscope Market Segmentation: Detailed Breakdown

By Product Type

The MEMS accelerometer and gyroscope market can be segmented into several product categories, each contributing to the overall growth of the market:

MEMS Accelerometers: MEMS accelerometers hold the largest share of the market in 2024, valued at approximately USD 2.5 billion. These sensors are crucial in applications like automotive stability control, consumer electronics, and industrial automation. Their high accuracy, compact size, and integration capabilities make them indispensable in modern motion-sensing technologies.

MEMS Gyroscopes: MEMS gyroscopes, which measure rotational movement, are used in applications requiring precise orientation control, such as drones, robotics, and wearables.

MEMS Inertial Measurement Units (IMUs): IMUs, which integrate accelerometers and gyroscopes, are primarily used in more complex systems like drones, aerospace navigation, and robotics. They offer the advantage of multi-dimensional sensing, allowing for more accurate motion tracking in dynamic environments.

By Application

The MEMS accelerometer and gyroscope market can also be segmented by application, with several industries showing significant demand for motion-sensing technologies:

Consumer Electronics: As the leading application segment, consumer electronics accounted for over USD 3.0 billion in 2024. This includes smartphones, wearables, and gaming devices, all of which require high-precision motion sensors for features like touch detection, gaming controls, and fitness tracking.

Automotive: The automotive industry is increasingly adopting MEMS sensors, particularly in autonomous vehicles, ADAS, and vehicle navigation systems. With the growing focus on safety and self-driving technology, the automotive segment is expected to grow at a CAGR of 11.4% through 2032.

Aerospace & Defence: MEMS accelerometers and gyroscopes are used extensively in navigation systems for aircraft and spacecraft, offering enhanced accuracy in flight control and positioning.

By Region

The MEMS accelerometer and gyroscope market is geographically diverse, with significant regional growth patterns:

Asia-Pacific: Expected to dominate the MEMS market by 2024, Asia-Pacific's growth is largely attributed to the booming consumer electronics sector in countries like China, Japan, and South Korea. The region is projected to grow at the highest CAGR of 12.0% through 2032.

North America and Europe: Both regions show steady demand, driven by automotive, aerospace, and healthcare applications. The U.S. and European countries are significant players in the MEMS market, with robust research and development activities.

South America and Middle East: These regions are expected to experience slower growth but will see increasing adoption of MEMS technology as industrial automation and IoT applications expand.

Competitive Landscape: Key Players and Strategic Insights

The MEMS accelerometer and gyroscope market is highly competitive, with several key players pushing the boundaries of innovation to capture market share. These companies focus on advancing sensor accuracy, power efficiency, and miniaturization. Notable companies in the market include:

Robert Bosch GmbH: A leader in MEMS sensor technology, Bosch offers a wide range of accelerometers and gyroscopes for automotive, consumer electronics, and industrial applications.

STMicroelectronics N.V.: Known for its innovations in MEMS sensors, STMicroelectronics provides highly integrated solutions that cater to automotive, consumer electronics, and industrial markets.

Analog Devices: Specializes in high-precision MEMS sensors for a variety of applications, including aerospace, automotive, and healthcare.

Honeywell: A key player in the consumer electronics sector, Honeywell offers next-generation MEMS gyroscopes for applications in AR/VR and wearables.

These companies are continuously investing in R&D to introduce more cost-effective and high-performance MEMS sensors, positioning themselves for long-term growth in a rapidly evolving market.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40601-global-mems-accelerometer-and-gyroscope-market

Conclusion

The MEMS accelerometer and gyroscope market is on a strong growth trajectory, driven by the increasing demand for motion-sensing technologies in various high-tech industries. With continued innovation in miniaturization, sensor fusion, and power efficiency, MEMS sensors are poised to play a crucial role in shaping the future of consumer electronics, automotive systems, healthcare devices, and beyond.

The increasing integration of MEMS sensors in emerging technologies such as AI, IoT, and autonomous systems ensures that this market will continue to experience robust growth through the next decade. As key players innovate and expand their offerings, the MEMS accelerometer and gyroscope market will remain a key enabler of technological advancement and digital transformation across industries.

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

#MEMS Accelerometer and Gyroscope Market#MEMS sensors#accelerometer market#gyroscope market#MEMS technology#market trends#sensor market#MEMS accelerometer#MEMS gyroscope#sensor industry#wearable sensors#automotive sensors#MEMS applications#MEMS devices#motion sensors#sensor technology#market analysis#MEMS sensor market growth#IoT sensors#MEMS sensor applications#MEMS market forecast#MEMS sensor suppliers#MEMS accelerometer applications#MEMS gyroscope applications#MEMS market demand#MEMS in automotive#MEMS in wearable devices#MEMS market research

1 note

·

View note

Text

Crew-8 Astronauts Return to Earth

After seven months of living and working onboard the International Space Station (ISSInternational Space Station), astronauts of NASA’s eighth rotational SpaceX crew mission (Crew-8) splashed down safely off the coast of Florida. The mission, which is part of NASA’s Commercial Crew Program, included NASANational Aeronautics and Space Administration astronauts Matthew Dominick, Michael Barratt, and Jeanette Epps, as well as Roscosmos cosmonaut Alexander Grebenkin. During their mission on station, the three NASA astronauts supported dozens of research investigations sponsored by the ISS National Laboratory®.

These investigations spanned many areas, including in-space production applications(Abbreviation: InSPA) InSPA is an applied research and development program sponsored by NASA and the ISS National Lab aimed at demonstrating space-based manufacturing and production activities by using the unique space environment to develop, test, or mature products and processes that could have an economic impact., life and physical sciences, and technology development, all aimed at bringing value to humanity and enabling a robust market in low Earth orbit(Abbreviation: LEO) The orbit around the Earth that extends up to an altitude of 2,000 km (1,200 miles) from Earth’s surface. The International Space Station’s orbit is in LEO, at an altitude of approximately 250 miles. (LEO).

Below highlights a few of the ISS National Lab-sponsored projects the Crew-8 NASA astronauts worked on during their mission.

Several investigations focused on in-space production applications, an increasingly important area of emphasis for the ISS National Lab and NASA.

A project from Cedars Sinai Medical Center aims to establish methods to support the in-space manufacturing of stem cells, which can be matured into a wide variety of tissues. These methods will be used for future large-scale in-space biomanufacturing of stem cell-derived products, which could lead to new treatments for heart disease, neurodegenerative diseases, and many other conditions.

Redwire Corporation partnered with Eli Lilly and Company and Butler University on a series of investigations leveraging Redwire’s Pharmaceutical In-space Laboratory (PIL-BOX), a platform to crystallize organic molecules in microgravityThe condition of perceived weightlessness created when an object is in free fall, for example when an object is in orbital motion. Microgravity alters many observable phenomena within the physical and life sciences, allowing scientists to study things in ways not possible on Earth. The International Space Station provides access to a persistent microgravity environment.. Results from this research could lead to improved therapeutics to treat an array of conditions. These projects continue Eli Lilly’s space journey, as the company has launched multiple investigations to the orbiting laboratory over the years for the benefit of patient care on Earth.

The astronauts supported the third experiment in a series of projects from the University of Notre Dame to improve ultra-sensitive biosensors. The biosensors can detect trace substances in liquids, including early cancer biomarkers. By using laser heating to control bubble formation in microgravity, the team improved particle collection—a key step in boosting sensor sensitivity. This research, funded by the U.S. National Science Foundation, could transform early and asymptomatic cancer detection and other medical diagnostics.

The crew conducted phase two of a technology development project from Sphere Entertainment to test Big Sky—the company’s new ultra-high-resolution, single-sensor camera—on the space station. In the first phase of the project, which launched in November 2022, astronauts tested a commercial off-the-shelf camera on the ISS to collect baseline information. During the second phase, the astronauts tested Big Sky to validate the camera’s function, operations, and video downlink capabilities in microgravity. Big Sky is being developed by Sphere Entertainment to capture content for Sphere, the next-generation entertainment medium in Las Vegas.

In the final days before their departure from the space station, the Crew-8 astronauts supported projects that recently launched on NASA’s ninth rotational crew mission (Crew-9).

One is a student-led project from Isabel Jiang, a recent high school graduate from Hillsborough, CA, who is now in her first year at Yale. Jiang is the winner of the 2023 Genes in Space student research competition, founded by Boeing and miniPCR bio and supported by the ISS National Lab and New England Biolabs. Jiang’s experiment investigates the effect of radiation and the space environment on mechanisms for gene editing. Results could help develop methods to better protect astronauts and shed light on genetic risks for certain diseases during spaceflight.

Another is an investigation from the U.S. Air Force Academy and Rhodium Scientific to compare the root growth of Arabidopsis plants, a member of the mustard family, at two different orbital altitudes. Plants grown on the space station in LEO for four to six days will be compared with similar plants grown on the recent Polaris Dawn mission, which flew in the same type of vehicle at a higher orbit for approximately the same amount of time. Results could provide insights into the production of crops for long-duration space missions and in high-radiation environments.

IMAGE: SpaceX Crew-8 astronauts (top to bottom) NASA's Jeanette Epps, Mike Barratt & Matthew Dominick, and Roscosmos cosmonaut Alexander Grebenkin onboard the ISS. Credit NASA

5 notes

·

View notes

Text

Motion Control Market Revenue, Size, Segment by Type, Application, Key Companies 2033

According to the latest analysis by Fact.MR, the global motion control market is projected to reach US$ 35.52 billion by 2033, growing at a CAGR of 5.1% from 2023 to 2033.

The market's steady expansion is driven by several key factors, including the increasing demand for automation and industrialization across various industries. Businesses are continuously seeking ways to enhance productivity, efficiency, and quality in manufacturing operations. Motion control systems play a crucial role by enabling precise positioning, speed regulation, and machinery synchronization, allowing industries to automate processes and optimize production lines effectively.

For more insights into the Market, Request a Sample of this Report – https://www.factmr.com/connectus/sample?flag=S&rep_id=335

Advancements in motion control technologies, including motor design, sensor technology, and control algorithms, have expanded application possibilities and increased the adoption of motion control systems. These innovations have enhanced performance, reliability, and integration capabilities, driving widespread acceptance across industries globally.

The integration of motion control systems with emerging technologies such as the Industrial Internet of Things (IIoT) and Industry 4.0 is further fueling market growth. By connecting motion control systems to networks, industries can collect and analyze data, implement predictive maintenance, and achieve real-time monitoring and control. This connectivity enhances operational efficiency, reduces downtime, and optimizes overall productivity.

Key Takeaways from Market Study

In 2023, the global motion control market was valued at US$ 21.60 billion.

Driven by increasing demand, the market is projected to grow at a CAGR of 5.1% over the next decade, reaching US$ 35.52 billion by 2033.

The motion control market in China is expected to attain a valuation of US$ 7.74 billion by 2033.

Meanwhile, demand for AC servo motors is forecasted to expand at a CAGR of 5.8% during the study period.

“Motion control systems are becoming more popular as the demand for automation and industrialization grows across industries. Companies are seeking ways to increase efficiency, productivity, and quality in their production processes, which has led to a growth in the use of motion control systems. Furthermore, expanding industries in emerging economies and favourable government measures to boost automation are driving market expansion,” says a Fact.MR analyst.

Competitive Landscape

Competition in the global motion control market is intensifying as companies strive to strengthen their market presence and gain a competitive edge. Leading players are heavily investing in product development and new launches to expand their customer base and differentiate themselves in the industry.

For instance:

In January 2021, Microsoft Corporation introduced the Pulse Red wireless controller, designed to seamlessly switch between Xbox consoles, PCs, and Android devices without requiring repeated setup. The controller retains memory of multiple devices, enabling quick and effortless transitions.

In April 2021, Performance Motion Devices, Inc. (PMD) launched the ION/CME N-Series Digital Drives, an extension of its ION Digital Drive family. These new digital drives offer high-performance motion control, network connectivity, and amplification, catering to the growing demand for advanced motion solutions.

Key Companies Profiled

Siemens AG

ABB Group

Schneider Electric

Rockwell Automation Inc

STM Microelectronics

Eaton Corp. Plc

Galil Motion Control

Kollmorgen Corp.

Mitsubishi Electric Corp.

Moog Inc

Regional Analysis

The Asia Pacific region, led by China, India, and South Korea, is experiencing substantial growth in the global motion control market.

China’s rapid industrialization, strong government support for automation, and expanding manufacturing sector are key drivers of motion control system adoption.

Japan, known for its technological expertise, is another major market in the region. The country’s advanced manufacturing industries, particularly in automotive and electronics, require high-precision motion control, driving demand for these systems. Similarly, South Korea’s strong presence in the electronics and robotics industries is further contributing to market expansion.

Overall, the Asia Pacific region remains a critical growth hub for the global motion control market, driven by industrial advancements, technological innovation, and the increasing shift toward automation across various sectors.

𝐂����𝐧𝐭𝐚𝐜𝐭:

US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

The Rise of 3D Printing in Prosthetics and Orthotics Market

The global prosthetics and orthotics market plays a vital role in improving quality of life for millions worldwide. Worth an estimated $7.2 billion in 2024, the market facilitates mobility for those with limb differences or injuries through highly customized external limb replacements and braces. The market introduces prosthetics and orthotics—Medical devices that enhance or assist impaired body parts and mobility. Orthotics are braces or supports for joints, spine, and limbs; prosthetics externally replace missing limbs. Together they improve functionality and quality of life for users. Major players in the prosthetics and orthotics space utilizing advanced manufacturing include Ossur, Steeper Group, Blatchford, Fillauer, Ottobock, and WillowWood Global. These industry leaders increasingly deploy cutting-edge 3D printing and customized design software to produce state-of-the-art prosthetics and braces. Current trends in the prosthetics and orthotics market include growing utilization of 3D printing and advanced manufacturing techniques. 3D printing enables on-demand production of complex, customized devices. It reduces manufacturing costs and wait times while improving fit and comfort. Expanding material options also allow more lifelike prosthetics. As technology evolves, the market is positioned for continued growth through 2031 in facilitating mobility worldwide. Future Outlook The prosthetics and orthotics market is expected to witness significant advancements in the coming years. Manufacturers are constantly focusing on developing innovative technologies such as 3D printed prosthetics that provide a better fit, enhanced comfort, and unrestricted movement. There is also a rising trend of using lightweight, highly durable and comfortable materials like carbon fiber and thermoplastics to manufacture prosthetic devices. Advancements in myoelectric prosthetics with touch and motion sensors are making them more dexterous and responsive. Using pattern recognition and machine learning techniques, next-gen prosthetics could gain functionality approaching that of natural limbs.

PEST Analysis Political: Regulations regarding clinical trials and approvals of new prosthetic technologies may affect market growth. Favorable reimbursement policies for prosthetic devices can boost adoption. Economic: Rising disposable incomes allow more individuals to opt for higher-end prosthetics. Emerging markets present abundant opportunities for growth. Inflation and economic slowdowns can hinder market profitability. Social: Increasing incidence of amputations and disabilities due to aging population, accidents, war injuries etc. drive market demand. Growing awareness regarding prosthetics and orthotics aids adoption. Stigma associated with limb loss poses challenges. Technological: Advancements in materials, manufacturing techniques like 3D printing, sensors, computing power and battery technologies are enhancing functionality and usability of prosthetics/orthotics. Myoelectric and robotic prosthetics have vastly improved in recent years. Opportunity Rising aging population presents a huge opportunity for prosthetics and orthotics targeting mobility issues and disabilities. Over 630,000 amputations occur annually in the U.S. due to dysvascular conditions like diabetes, presenting a sizable patient pool. Expanding applications of prosthetics and orthotics beyond mobility impairment into sports and military could drive significant growth. Growing incidence of trauma and injuries globally increases the number of patients relying on these devices. Emerging markets like Asia Pacific and Latin America offer immense opportunities owing to increasing disposable incomes, expanding healthcare infrastructure and rising medical tourism. Technological advancements are constantly improving functionality and usability of prosthetic devices, fueling adoption rates. The lightweight, durable and comfortable characteristics of newer materials expand addressable indications and patient acceptance. Key Takeaways Growing demand from aging population: The rapid increase in aging population worldwide who are prone to mobility issues, disabilities and chronic diseases like diabetes is a key driver spurring sales of orthotic and prosthetic devices. Global expansion into emerging markets: Emerging markets like Asia Pacific, Latin America, Eastern Europe and the Middle East offer immense opportunities owing to their large population bases and improving healthcare penetration. Technological advancements: Constant R&D bringing advancements in areas such as 3D printing, lightweight materials,

4 notes

·

View notes

Text

Gear Motor Market Size, Share & Growth 2025-2034

The gear motor market is a crucial part of the industrial automation and mechanical power transmission ecosystem. A gear motor combines an electric motor with a gearbox, which reduces speed and increases torque output. These systems are widely used in industries like mining, automotive, food and beverage, wind power, and material handling due to their durability and ability to handle heavy loads. Growing industrialization, advancements in automation, and rising investments in infrastructure projects worldwide are driving the demand for efficient gear motors. Manufacturers are constantly innovating to enhance energy efficiency, reduce operational costs, and meet evolving industry standards.

Expert Market Research: Insights on Gear Motor Market

Backed by detailed insights from Expert Market Research, the gear motor market is projected to maintain its strong momentum due to rapid industrialization and technological innovations. Their extensive data and strategic forecasts help companies identify growth pockets and adapt to dynamic market conditions. By leveraging these actionable insights, businesses can gain a competitive edge, optimize production, and expand globally. As industries prioritize energy efficiency and advanced automation, Expert Market Research highlights the critical role gear motors will continue to play in powering industrial equipment worldwide.

Gear Motor Market Size

The global gear motor market reached an impressive value of approximately USD 27.89 Billion in 2024, highlighting its vital role across diverse industries. The market’s robust size reflects the widespread application of gear motors in machinery and equipment that require controlled motion and high torque output. With the rising adoption of automated material handling equipment and the push for energy-efficient industrial solutions, the demand for gear motors is on an upward trajectory. Small and large manufacturers alike rely on these systems for smooth, reliable operations, ensuring the gear motor market maintains its strong foothold in the global industrial landscape.

Gear Motor Market Trends

One of the significant gear motor market trends includes the shift towards compact, high-efficiency gear motors that deliver better performance with lower energy consumption. Industries are increasingly seeking sustainable and smart solutions, which has led to innovations like integrated gear motors with smart sensors for predictive maintenance. Another key trend is the rising use of gear motors in renewable energy sectors, especially in wind power generation. The surge in electric vehicle production also contributes to demand for advanced gear motor technologies. Furthermore, manufacturers are focusing on customization to cater to diverse application requirements across various sectors, boosting market dynamism.

Gear Motor Market Opportunities and Challenges

The gear motor market presents numerous opportunities, particularly with the rise in automation across industries such as mining, automotive, and food and beverage. The expansion of the renewable energy sector, especially wind power, further enhances growth potential. However, the market also faces challenges, including the high initial costs associated with advanced gear motors and the need for continuous maintenance. Fluctuations in raw material prices and global supply chain disruptions can also impact production and pricing. Nonetheless, with advancements in manufacturing technologies and digitalization, companies can overcome these barriers and tap into emerging market opportunities.

Gear Motor Market Segmentation

By Product Type:

Gearbox

Gear Motor

By Gear Type:

Helical-Bevel

Worm

Helical

Planetary

Others

By Rated Power:

Up to 7.5 kW

7.5 kW to 75 kW

Above 75 kW

By Torque:

Up to 10,000 Nm

Above 10,000 Nm

By End Use:

Metals and Mining

Material Handling

Wind Power

Food and Beverage

Cement and Aggregates

Automotive

Others

By Region:

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Gear Motor Market Growth

The gear motor market is poised for steady growth driven by rapid industrial expansion and technological advancements in manufacturing processes. Between 2025 and 2034, the market is projected to grow at a healthy CAGR of 5.00%, reaching about USD 45.43 Billion by 2034. This growth is attributed to increasing adoption of automation in heavy industries and a robust demand for renewable energy systems. As more industries invest in smart manufacturing and advanced machinery, the need for efficient and compact gear motors will rise. Emerging economies in Asia Pacific and Latin America are expected to play a significant role in driving future market expansion.

Gear Motor Market Forecast

Forecasts indicate that the gear motor market will continue to expand steadily over the next decade. The consistent demand for gear motors in material handling, wind power, and automotive sectors will underpin this growth. Moreover, the transition towards Industry 4.0 and smart factories will boost the deployment of intelligent gear motors integrated with IoT-enabled sensors for real-time monitoring. Companies will increasingly focus on developing modular and highly customizable gear motor solutions to meet specific industrial needs. By 2034, the market’s estimated worth of USD 45.43 Billion will reflect the sector’s resilience and adaptability to evolving technological and regulatory landscapes.

Gear Motor Market Competitor Analysis

Siemens AG: Global leader providing innovative gear motor solutions, enhancing industrial automation, energy efficiency, and smart manufacturing worldwide.

Eaton Corporation plc: Specializes in sustainable power management and gear motors, delivering reliable performance and energy-saving solutions for industrial applications.

Emerson Electric Co.: Develops advanced gear motors and drives, supporting efficient operations in diverse industries with cutting-edge automation technologies.

Johnson Electric Holdings Limited: Offers precision motion systems and gear motors, serving automotive, industrial, and consumer markets with high-quality engineered solutions.

Bosch Rexroth AG: Renowned for robust drive and control technologies, supplying high-performance gear motors that optimize heavy-duty industrial machinery.

0 notes

Text

North America Building Automation Systems (BAS) Market Size Paving the Way for Smart, Sustainable Infrastructure

As cities grow smarter and energy efficiency becomes a global imperative, Building Automation Systems (BAS) are transforming how residential, commercial, and industrial spaces are operated. BAS integrates various building systems—HVAC, lighting, fire safety, and security—into a unified, intelligent framework that reduces energy consumption and enhances operational efficiency.

The North America Building Automation Systems Market is witnessing robust growth as governments and enterprises push for sustainable infrastructure, improved building performance, and smarter urban development.

What Are Building Automation Systems?

Building Automation Systems (BAS) are centralized, networked systems that monitor and control various building functions such as:

Heating, Ventilation, and Air Conditioning (HVAC)

Lighting and energy management

Security and access control

Fire and life safety systems

Elevators and smart shading systems

These systems allow facilities managers to optimize performance, reduce costs, and improve occupant comfort through real-time data analytics and remote monitoring.

Key Market Drivers

Rise in Smart Cities and Green Buildings

Urbanization is fueling the growth of smart city initiatives. Governments across North America are investing in green buildings, which require automated systems to meet energy compliance and efficiency goals.

Emphasis on Energy Efficiency

With rising energy costs and sustainability regulations, BAS plays a pivotal role in reducing building energy consumption by automating temperature, lighting, and power usage.

Demand for Real-Time Monitoring

Facility managers are increasingly adopting BAS for remote monitoring, predictive maintenance, and centralized control—enhancing asset longevity and reducing operational downtime.

Enhanced Security Requirements

Modern BAS integrates security systems, including surveillance, motion detection, and biometric access, which is particularly crucial for commercial and government buildings.

Market Applications

Commercial Buildings – Office towers, retail malls, and hotels leverage BAS for lighting, climate control, and energy optimization.

Industrial Facilities – BAS manages utilities, environmental control, and safety compliance in factories and warehouses.

Healthcare & Education – Hospitals and schools use BAS for air quality management, safety, and energy saving.

Residential Complexes – Smart homes and condominiums are increasingly adopting scalable BAS for luxury, security, and efficiency.

Technology Trends Shaping the BAS Market

IoT Integration Internet of Things (IoT) sensors collect and analyze real-time data to automate responses and enhance decision-making.

Cloud-Based BAS Platforms Cloud-enabled BAS offers better scalability, remote access, and system integration across multiple buildings or campuses.

AI & Machine Learning Predictive algorithms improve system efficiency, detect faults early, and optimize energy usage dynamically.

Wireless BAS Networks Wireless connectivity enables easier installation and upgrades, especially in retrofitting older buildings.

Challenges

High Initial Investment: Installing a fully integrated BAS requires upfront capital, though the long-term savings outweigh the costs.

Cybersecurity Concerns: As BAS systems become more connected, they must be protected from hacking and data breaches.

Integration Complexity: Ensuring interoperability between legacy systems and new technologies can pose technical challenges.

Trending Report Highlights

Explore more market insights across automation, electronics, and IT sectors:

Barcode Scanner Market

United States Managed Services Market

SEA Robotic Process Automation Market

US Graphics Processing Unit Market

SEA Led Lighting Market

Hand Tools Market

India Electromechanical Components Market

PC Peripherals Market

India Mobile Components Market

Restaurant POS Systems Market

United States LED Light Emitting Diode Market

Asia Pacific Battery Energy Storage System Market

Middle East & Africa Smart Cities Market

Wearable AI Market

Model Based Enterprise Market

The North America Building Automation Systems (BAS) Market is poised for substantial growth driven by the demand for energy-efficient, intelligent, and secure buildings. Whether it’s a towering commercial complex or a smart residential hub, BAS is no longer a luxury—it’s a necessity. Stakeholders investing in advanced BAS solutions today are not only reducing costs but also contributing to a more sustainable and future-ready urban ecosystem.

0 notes

Text

Solar lights Global Demand, Renova Pulse Energy's Bestselling Solar Lights for Mumbai

According to Renovapulse energy global solar lights market is projected to reach $14.2 billion by 2032, growing at a CAGR of 6.2% from 2022 to 2032. Solar lights are changing the way India lights its homes, streets, and villages. More and more people are using solar lights because electricity costs are going up and people are becoming more aware of clean energy. Solar lights are no longer only for remote villages. They are now used in cities, industries, farms, and public places.

For more Info visit our site: https://www.renovapulseenergy.com

• More than 4 million solar street lights have been put up as part of government-funded programs. • They help save electricity, lower power bills, and make people less reliant on the grid.

• Solar lights also help cut down on pollution by using less diesel in rural areas. •Solar lights are now cheaper than ever because the prices of solar panels and batteries are going down.

• By 2030, solar power, including solar lights, should help bring electricity to most rural areas that don't have reliable power lines or any at all. •Big government projects like the Smart City Mission and the Saubhagya Yojana are putting in more solar street lights in cities and villages to make public places safer and brighter.

Choose ReNova Pulse Energy as your trusted partner for solar lighting! We sell high-quality solar lights from well-known brands in India and around the world at ReNova Pulse Energy. These lights can be used for a wide range of lighting needs, from small homes to big commercial and outdoor projects. Our selection includes everything from 3W solar lanterns to 120W streetlights, so they're great for homes, gardens, communities, industrial areas, and public spaces.

Our solar lamps outdoor have advanced features like built-in lithium batteries, energy-efficient LED technology, and IP65 designs that are weatherproof, so they will work reliably in all seasons. We can install lights that last a long time and don't cost any electricity, whether you need them for safety, decoration, or everyday use. Study Coverage: This study gives a brief overview of the most important products in the global lamp solar light market, as well as an overview of the most important segments and their benefits. It also talks about the different types of growth rates in the industry and how they are used. Types of Solar Lights: Solar Street Lights

Bright lights for roads, paths, parks, and communities outside. They turn on at night and off in the morning. Some have motion sensors.

Bollard lights and solar garden attractive lights for parks, gardens, and walkways. Solar flood lights are simple to install and add safety and aesthetic appeal to your outdoor area. For open spaces like parking lots, warehouses, events, and security purposes, strong, bright lights are necessary. Some also have motion sensors.

Wall Lights with Solar Motion Sensors For gates, doors, and building entrances, tiny wall lights with sensors that activate when someone walks by are ideal.

Renova Pulse Energy is a government-approved vendor that offers genuine products with subsidy support under approved schemes, as certified by MNRE, BIS, and IEC. This is one of the benefits of installing solar lighting with them.

✅ Full Installation Service — We take care of everything, saving you trouble, from site inspection to final setup. ✅ Assistance with Subsidies & Documents — Complete support for submitting applications for government subsidies and necessary documentation. ✅ Reliable, high-quality products — long-lasting, low-maintenance lights that function in any weather. ✅ After-Sales Service & Support — We provide routine maintenance, support, and service when required. ✅ Reasonably priced with savings — Lower long-term expenses and electricity bills

About us:

ReNova Pulse Energy isIndia’s next-generation solar startup, committed to delivering sustainable, reliable, and affordable solar solutions across the nation to every corner of India especially rural communities especially to rural communities. Go solar with us and enjoy the benefits of government subsidies and hassle-free installation!

Call or Schedule a Visit with us today!

Address:

A-216, Kailas Business Park,

Veer Savarkar Marg,

Vikhroli West, Mumbai, 400079

Email us: [email protected]

Instagram Facebook LinkedIn

0 notes

Text

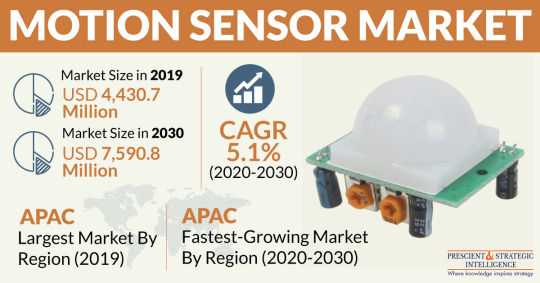

Growing Adoption of Electric Vehicles Fueling Motion Sensor Sales

The burgeoning need for consumer electronics, such as laptops, wearable devices, and smartphones, is driving the demand for motion sensors. This is because motion sensors are heavily used in heart rate monitors, which are extensively used in smart wearable devices, and also to control the orientation of smartphone screens. Owing to this factor, the soaring demand for smartphones and wearable devices among the youth, particularly the millennials, is positively impacting the demand for motion sensors.

Additionally, with the rise in the worldwide population, the demand for consumer electronics is expected to shoot up, which will also fuel the expansion of the motion sensor market. P&S Intelligence estimates that the value of the market will grow from $4,430.7 million in 2019 to $7,590.8 million by 2030. Furthermore, the market is expected to demonstrate a CAGR of 5.1% from 2020 to 2030. The growing use of internet of things (IoT)-enabled devices is also expected to create lucrative growth opportunities for motion sensor developers across the world.

According to the Institute of Electrical and Electronics Engineers (IEEE), there were around 27 billion IoT devices in use all over the world in 2017, and this share is expected to surge to 125 billion by 2030. The integration of IoT will enable motion sensors to monitor a device’s physical status from remote locations. Moreover, these devices can improve several building automation applications, such as lighting systems and heating, ventilation, and air conditioning (HVAC) controls.

Infrared (IR), tomographic sensors, ultrasonic, gyroscopes, accelerometers, and combo sensors are the most widely used types of motion sensors. Out of these, the demand for combo sensors is expected to rise at the fastest pace in the coming years. This will be because of the fact that the microfabrication of different types of motion sensors into a single device will enable the device to detect motion more accurately. In various consumer electronic devices, such as smartphones, combo sensors are preferred wherein a magnetometer, gyroscope, and accelerometer is incorporated in one microelectromechanical system (MEMS).

Besides consumer electronics, the other major application areas of motion sensors are automobiles, building automation systems, medical devices, and industrial equipment. Out of these, the incorporation of motion sensors was observed to be the highest in automobiles in the past. This was because of the fact that motion sensors enhance the autonomous driving experience by improving the functioning of the navigation system and battery and assisting in electronic device stability detection.

Because of this factor, the surging sales of automobiles, especially autonomous and electric vehicles, pushed up the global demand for motion sensors. Geographically, the sales of motion sensors are expected to rise rapidly in the Asia-Pacific (APAC) region in the forthcoming years. This will be because of their skyrocketing demand in Japan, India, China, South Korea, and Indonesia, owing to the large-scale manufacturing of smartphones, tablets, gaming consoles, lighting systems, building automation equipment, and electronic medical devices.

Thus, the sales of motion sensors will shoot up in the near future, mainly because of the surging demand for consumer electronics and electric and autonomous vehicles.

#Motion Sensor Market Share#Motion Sensor Market Size#Motion Sensor Market Growth#Motion Sensor Market Applications#Motion Sensor Market Trends

1 note

·

View note

Text

Top Companies Leading the Kinetic Footfall Energy Harvesting Market Revolution

Unleashing the Future of Energy: A New Paradigm in Sustainable Power Generation

The global Kinetic Footfall Energy Harvesting and Security market is undergoing a revolutionary transformation. With an anticipated compound annual growth rate (CAGR) of 54.1% from 2024 to 2031, this sector is poised to redefine how urban ecosystems generate and manage energy. Leveraging advanced technologies like piezoelectric systems, electromagnetic induction, and triboelectric nanogenerators (TENGs), the market is rapidly expanding into diverse applications ranging from smart cities to high-traffic public venues.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40424-global-kinetic-footfall-energy-harvesting-market

Kinetic Footfall Energy Harvesting Market Forecast: Explosive Growth Through 2031

In 2023, the kinetic footfall energy harvesting market was valued at USD 318.78 million, and is projected to surpass USD 630 million by 2031. This exponential growth is driven by increasing global emphasis on sustainable energy, carbon neutrality, and smart infrastructure integration.

Key growth catalysts include:

Expanding urbanization and smart city initiatives

Public and private investment in renewable technologies

Technological advancements in micro-energy generation

Growing demand for decentralized and autonomous energy systems

Get up to 30%-40% Discount: https://www.statsandresearch.com/check-discount/40424-global-kinetic-footfall-energy-harvesting-market

Regional Outlook: Strategic Growth Across Global Kinetic Footfall Energy Harvesting Markets

North America

North America is at the forefront of kinetic energy adoption, particularly the United States and Canada, which are investing heavily in smart city infrastructure and sustainable public transportation systems.

Europe

Countries like Germany, UK, and France lead the region with widespread integration in urban transport hubs, commercial complexes, and green building developments.

Asia-Pacific

Emerging economies such as China, India, Japan, and South Korea are driving robust adoption fueled by rapid urban expansion, government-backed clean energy initiatives, and population density.

Middle East and Africa

With increasing focus on renewable energy to reduce dependence on oil, countries like UAE and South Africa are integrating kinetic energy harvesting into new smart city projects.

South America

Nations including Brazil and Chile are gradually adopting these systems within public spaces and transit systems, driven by environmental policies and energy cost reduction strategies.

Technology Landscape: The Core of Energy Harvesting Innovation

Piezoelectric Technology

Piezoelectric systems dominate the market due to their high-frequency responsiveness and compact design, ideal for high-traffic locations such as airports, stadiums, and urban crosswalks. These materials convert pressure from footsteps into electrical energy, which can power lighting, sensors, and low-consumption devices.

Electromagnetic Induction

Utilizing the relative motion between magnetic fields and coils, electromagnetic induction is suitable for moderate foot traffic areas. These systems are reliable, durable, and cost-efficient, particularly in transportation hubs and shopping malls.

Triboelectric Nanogenerators (TENGs)

As a cutting-edge solution, TENGs harness friction-based mechanical movement to generate electricity. With their lightweight, flexible design, TENGs are becoming increasingly prevalent in educational institutions, healthcare facilities, and public walkways.

Application Spectrum: Cross-Sector Adoption Driving Market Momentum

Urban Infrastructure

Smart pavements, energy-harvesting crosswalks, and public lighting systems are transforming cities into self-powered environments, improving operational efficiency while lowering environmental impact.

Commercial Buildings

Integrated energy-harvesting flooring systems are being used to reduce energy bills and achieve sustainability certifications (e.g., LEED, BREEAM).

Transportation Hubs

Airports, train stations, and metro systems are prime locations for harvesting energy from massive foot traffic, powering LED displays, ticketing systems, and surveillance cameras.

Sports & Entertainment Venues

Stadiums and event spaces employ kinetic floors that convert audience movement into electricity for real-time lighting effects and digital engagement.

Educational Institutions

Universities and schools are early adopters, using kinetic energy to promote environmental awareness and power smart classroom equipment.

Healthcare Facilities

Hospitals utilize harvested energy for emergency lighting, monitoring systems, and automated sanitization devices, especially in off-grid or backup scenarios.

Residential Complexes

Innovative flooring technologies are integrated into lobbies and gyms to contribute to overall building energy efficiency.

Public Spaces

Parks, plazas, and sidewalks are being redesigned to include kinetic harvesting systems that enhance lighting and safety using human activity.

End-User Segmentation: Stakeholders Leading the Green Transition

Municipalities and Governments

Municipal investments are fueling widespread deployment of kinetic energy in public services such as smart street lighting, traffic management, and environmental monitoring systems.

Commercial Enterprises

Retail giants and corporate campuses are integrating footfall energy systems to demonstrate corporate social responsibility and reduce energy expenditure.

Educational Institutions

Adoption is driven by both functional energy benefits and the desire to create interactive, educational demonstrations of sustainability in action.

Healthcare Providers

Hospitals and care centers are embedding these technologies to ensure uninterrupted operation of critical systems in high-traffic zones.

Property Developers

Footfall energy solutions are enhancing property value and contributing to certification targets for net-zero buildings.

Event Organizers

Temporary installations at festivals, marathons, and concerts are enabling energy-independent event management, improving sustainability credentials.

Competitive Landscape: Kinetic Footfall Energy Harvesting Market Leaders and Innovators

The global kinetic footfall energy harvesting marketis shaped by both well-established companies and emerging players offering niche technologies. Leading participants include:

Pavegen – A pioneer in human-powered smart flooring

EnOcean GmbH – Specializing in self-powered IoT sensor solutions

Energy Floors – Creators of interactive kinetic floors for public engagement

Freevolt Technologies Limited – Innovators in RF and kinetic energy hybrid solutions

POWERleap Inc. – Known for energy-generating floor tiles

EnOcean Alliance – A collective promoting interoperability standards for energy harvesting tech

Piezoelectric Technology Inc. – Advanced materials for high-output footfall applications

Voltree Power Inc. – Specializing in alternative renewable sources including kinetic applications

Strategic Outlook: Accelerating Toward Smart, Self-Powered Environments

The global Kinetic Footfall Energy Harvesting and Security market is transitioning from experimental deployment to mainstream integration. With the convergence of urban planning, environmental responsibility, and smart technology, this market will serve as a foundation for decentralized, responsive, and intelligent energy systems of the future.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40424-global-kinetic-footfall-energy-harvesting-market

Conclusion

We are entering a transformative era where energy from human movement is no longer a conceptual novelty but a critical component of sustainable infrastructure. With advanced technology, strategic applications, and unwavering global demand, the kinetic footfall energy harvesting market stands as a cornerstone in the renewable energy revolution. The next generation of smart cities will not just be powered by the sun or wind���but by the very steps we take.

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

1 note

·

View note

Text

Resolver Interface Module Market : Size, Trends, Opportunities, Demand, Growth Analysis and Forecast

Resolver Interface Module Market, Trends, Business Strategies 2025-2032

The global Resolver Interface Module Market size was valued at US$ 145.67 million in 2024 and is projected to reach US$ 234.89 million by 2032, at a CAGR of 7.23% during the forecast period 2025–2032.

A Resolver Interface Module (RIM) is a critical component in industrial automation systems that processes signals from resolver sensors – specialized rotary transformers measuring position, speed, and direction in rotating machinery. These modules act as intelligent bridges between analog resolver outputs and digital control systems, performing signal conditioning, analog-to-digital conversion, and often incorporating advanced features like fault diagnostics and temperature compensation.

The market growth is driven by increasing industrial automation adoption, particularly in manufacturing and energy sectors, where precision motion control is paramount. While North America currently leads with 38% market share due to advanced manufacturing infrastructure, Asia-Pacific is witnessing the fastest growth at 9.1% CAGR, fueled by China’s aggressive industrial modernization. Key players including AMETEK, Schneider Electric, and Rockwell Automation are expanding their RIM portfolios to support Industry 4.0 applications, with multi-channel variants gaining traction for complex robotic systems.

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis. https://semiconductorinsight.com/download-sample-report/?product_id=103242

Segment Analysis:

By Type

Single Channel Modules Lead Due to Cost-Effectiveness in Small-Scale Applications

The market is segmented based on type into:

Single Channel

Subtypes: Standard resolution, High-resolution

Multi-channel

Subtypes: Dual channel, Quad channel, Modular systems

By Application

Industrial Automation Dominates Owing to Wide Usage in Motor Control Systems

The market is segmented based on application into:

Industrial Automation

Subtypes: Robotics, CNC machines, Servo drives

Aerospace & Defense

Automotive

Subtypes: EV systems, Steering angle measurement

Energy & Power

By End User

OEMs Account for Majority Demand Due to System Integration Requirements

The market is segmented based on end user into:

Original Equipment Manufacturers (OEMs)

System Integrators

Maintenance & Repair Organizations

Regional Analysis: Resolver Interface Module Market

North America North America represents a major hub for the Resolver Interface Module (RIM) market, driven by robust industrial automation and the presence of key manufacturers like AMETEK and Rockwell Automation. The U.S. alone accounts for a significant market share, supported by high adoption rates in aerospace, defense, and automotive sectors, where resolver-based motion control systems are critical. Technological advancements, such as Industry 4.0 adoption and increasing demand for high-precision control systems, further propel market growth. However, stringent regulatory standards for electromagnetic compatibility (EMC) and signal integrity impose compliance challenges on manufacturers.

Europe Europe stands as a high-maturity market for RIM solutions, primarily due to its well-established industrial automation ecosystem and advancements in robotics. Countries like Germany and France lead the demand, fueled by strong manufacturing and automotive industries. The EU’s emphasis on energy-efficient motor control systems has accelerated the adoption of resolvers and accompanying interface modules. Schneider Electric and other regional players dominate here, offering multi-channel and fault-tolerant solutions. Despite steady demand, the market faces pressure from alternative sensing technologies like encoders, requiring continuous innovation to maintain growth.

Asia-Pacific The fastest-growing region for RIM adoption, Asia-Pacific benefits from rapid industrial automation in China, Japan, and India. China’s dominance in manufacturing and its push for smart factories under the “Made in China 2025” initiative drive demand for resolver-based systems. Japan remains a leader in precision robotics, while India’s expanding automotive sector presents untapped opportunities. Price sensitivity remains a challenge, often favoring single-channel RIM solutions over high-end products. Nevertheless, with increasing investments in industrial IoT (IIoT), the region is poised for long-term expansion.

South America A developing market, South America exhibits gradual growth for RIMs, largely concentrated in Brazil’s automotive and heavy machinery sectors. Limited industrial automation penetration and economic instability hinder rapid adoption, although localized manufacturing efforts show promise. Rockwell Automation and Schneider Electric maintain a presence, focusing on cost-competitive solutions. Infrastructure modernization projects, particularly in mining and energy, could unlock future demand, but progress remains uneven due to currency fluctuations and regulatory unpredictability.

Middle East & Africa The RIM market here is nascent but growing, with demand primarily tied to oil & gas and defense applications. Countries like Saudi Arabia and the UAE invest in automation for industrial diversification, though adoption lags behind other regions. High dependence on imports and lack of local manufacturing capabilities limit market scalability. However, rising interest in smart infrastructure and renewable energy projects signals potential for gradual uptake, particularly in multi-channel resolver modules for large-scale machinery.

List of Key Resolver Interface Module Manufacturers

AMETEK (U.S.)

Advanced Micro Controls (AMCI) (U.S.)

Data Device Corporation (U.S.)

United Electronic Industries (UEI) (U.S.)

Schneider Electric (France)

Rockwell Automation (U.S.)

The global push toward Industry 4.0 and smart manufacturing is creating unprecedented demand for precision motion control systems. Resolver Interface Modules (RIMs) serve as critical components in industrial automation by providing reliable position and speed feedback for motors and actuators. Manufacturing sectors are increasingly adopting these modules to enhance operational efficiency, with the industrial automation market projected to grow at nearly 9% CAGR through 2030. This sustained growth directly correlates with increased RIM deployments across automotive, aerospace, and heavy machinery applications where resolver-based systems offer superior reliability in harsh environments compared to optical encoders.

The automotive industry’s rapid transition to electric vehicles represents a significant growth driver for resolver interface technology. Modern EV powertrains require highly accurate rotor position sensing for optimal motor control and energy efficiency. Premium automotive manufacturers are increasingly specifying resolver-based systems due to their electromagnetic interference immunity and durability. With global EV production volumes expected to exceed 40 million units annually by 2030, the demand for automotive-grade RIMs with enhanced temperature tolerance and vibration resistance is seeing corresponding growth.

Military modernization initiatives across major economies are driving adoption of resolver-based systems in defense applications. The inherent reliability of resolver technology makes it ideal for critical systems such as radar positioning, weapon turret control, and aircraft flight surfaces. Defense contractors are specifying ruggedized RIM solutions that meet stringent MIL-STD-810 standards for shock and vibration resistance. Recent contract awards for next-generation military platforms indicate accelerating replacement of older synchro systems with modern resolver interface solutions, creating a $300 million+ annual opportunity for specialized defense-grade modules.

The global transition to renewable energy creates significant opportunities for resolver technology in power generation applications. Wind turbine pitch control systems increasingly utilize resolver-based position feedback due to the technology’s reliability in harsh outdoor environments. With wind capacity installations projected to grow at 7% annually through 2030, turbine manufacturers are driving demand for customized RIM solutions that can withstand extreme temperature cycles and provide decades of maintenance-free operation.

The convergence of industrial IoT and advanced motion control presents opportunities for next-generation RIM products. Manufacturers are developing modules with integrated Industry 4.0 capabilities including predictive maintenance algorithms and remote diagnostics. These smart modules can monitor resolver health indicators such as signal degradation, enabling condition-based maintenance strategies that reduce unplanned downtime. Early adopters in automotive manufacturing have demonstrated 15-20% improvements in equipment availability through these intelligent monitoring features.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103242

Key Questions Answered by the Resolver Interface Module Market Report:

What is the current market size of Global Resolver Interface Module Market?

Which key companies operate in Global Resolver Interface Module Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Browse More Reports:

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

0 notes

Text

Motion Capture Sensors Market : Regulatory Developments and Compliance Outlook 2025–2032

Motion Capture Sensors Market, Global Outlook and Forecast 2025-2032

The global Motion Capture Sensors Market was valued at US$ 1.73 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 9.12% during the forecast period 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=88024

MARKET INSIGHTS

The global Motion Capture Sensors Market was valued at US$ 1.73 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 9.12% during the forecast period 2025-2032.

Motion Capture Sensors are specialized devices used to record and analyze human or object movements in three-dimensional space. These sensors include inertial measurement units (IMUs), optical markers, depth cameras, and mechanical exoskeletons, which track position, orientation, and acceleration data. The technology enables precise motion tracking for applications ranging from animation and gaming to sports science and medical rehabilitation.

The market growth is driven by increasing demand in entertainment industries for realistic CGI animation and virtual production, which accounts for over 35% of current applications. Furthermore, advancements in sensor miniaturization and AI-powered motion analysis algorithms are creating new opportunities in healthcare and industrial training simulations. Key players like Microsoft Corporation and Rokoko are expanding their product portfolios with wireless sensor solutions, while emerging markets in Asia-Pacific show accelerated adoption rates above the global average.

List of Key Motion Capture Sensor Companies Profiled

Inertia (U.S.) – Leader in inertial motion capture systems

Rokoko (Denmark) – Innovator in affordable mocap solutions

Technaid (Spain) – Specializes in biomechanical applications

Honeywell (U.S.) – Industrial motion sensing leader

ASUSTeK Computer (Taiwan) – Consumer motion tracking solutions

Cognex Corporation (U.S.) – Machine vision specialists

LMI Technologies (Canada) – 3D scanning innovators

Melexis (Belgium) – MEMS sensor specialists

Microchip Technology (U.S.) – Expanding mocap portfolio

Microsoft Corporation (U.S.) – Kinect platform developer

Regional differences create varied competitive dynamics. While North America remains the innovation hub with numerous startups, Chinese players like Navgnss and Norinco Group are rapidly gaining share through cost-effective solutions tailored for Asian markets.

The market’s projected 12.4% CAGR through 2031 will likely intensify competition further. Companies are already shifting strategies – some focusing on vertical-specific solutions while others pursue horizontal platform approaches. The coming years will test players’ abilities to balance precision, affordability, and scalability as motion capture becomes mainstream across industries.

Segment Analysis:

By Type

Inertial Sensors Segment Leads Due to High Demand in Consumer Electronics and Gaming Applications

The market is segmented based on type into:

Inertial sensors

Subtypes: Accelerometers, gyroscopes, and magnetometers

Measurement sensors

Subtypes: Optical sensors, force sensors, and others

Other sensors

Subtypes: Acoustic, pressure, and environmental sensors

By Application

Entertainment Segment Dominates Owing to Growing Animation and Virtual Production Needs

The market is segmented based on application into:

Entertainment

Subcategories: Film production, gaming, and virtual reality

Life science

Subcategories: Biomechanics research and medical rehabilitation

Sports

Industrial

Others

By End-User Industry

Media & Entertainment Industry Shows Strong Adoption Due to Rising Demand for High-Quality Animation

The market is segmented based on end-user industry into:

Media & entertainment

Healthcare

Education & research

Manufacturing

Others

Regional Analysis: Motion Capture Sensors Market

North America North America remains a dominant force in the motion capture sensors market, driven largely by technological advancements and a thriving entertainment industry. The U.S. contributes significantly to the region’s market share, with major studios and research institutions leveraging motion capture for animation, gaming, and biomechanics. Key players like Microsoft Corporation and Cognex Corporation continually innovate, pushing the adoption of high-precision inertial and optical sensors. Additionally, increasing applications in healthcare—such as rehabilitation tracking and sports science—are creating new growth avenues. While regulatory frameworks ensure data accuracy and security, the high cost of advanced systems remains a limiting factor for smaller enterprises.

Europe Europe’s motion capture sensors market is characterized by robust demand from both entertainment and life sciences sectors. Countries like the U.K. and Germany are frontrunners, thanks to their well-established gaming and animation industries, alongside cutting-edge medical research facilities. Stricter data protection laws, such as GDPR, encourage the use of compliant, high-quality sensor technologies. The region also witnesses growing adoption of wearable motion capture solutions for athlete performance monitoring. However, market expansion is somewhat restricted by budget constraints in smaller economies and competition from established North American and Asian manufacturers.

Asia-Pacific Asia-Pacific is the fastest-growing region in the motion capture sensors market, primarily due to rapid urbanization and increasing investments in entertainment and healthcare technologies. China leads the charge, supported by government initiatives in digital content creation and robotics. India and Japan follow closely, with emerging gaming studios and automotive companies integrating motion capture for ergonomic testing. While cost-effective alternatives dominate the lower-tier markets, premium sensor adoption is rising in urban hubs. Challenges include fragmented regulatory standards and intellectual property concerns, though innovation in AI-powered motion analytics offers substantial future potential.

South America The South American market for motion capture sensors is still in its nascent stages, with growth primarily concentrated in Brazil and Argentina. The region’s film and gaming industries show gradual adoption of motion tracking, but limited funding and infrastructure slow widespread deployment. Local manufacturers focus on affordability, which restricts the uptake of high-end systems. Despite these hurdles, rising interest in virtual production and sports analytics hints at opportunities for market players willing to navigate the region’s economic volatility and import dependency.

Middle East & Africa The Middle East & Africa exhibit sporadic but promising growth in motion capture sensor adoption. Wealthier Gulf nations, such as the UAE and Saudi Arabia, invest in immersive entertainment and smart healthcare, while Africa’s progress is constrained by infrastructural gaps. Public-private partnerships aim to boost local technology ecosystems, but market penetration remains low outside of niche applications. Long-term prospects hinge on digital transformation initiatives and rising disposable incomes, though geopolitical instability and currency fluctuations continue to pose challenges for sustained growth.

MARKET DYNAMICS

The development of lightweight, low-power motion capture sensors presents significant opportunities in consumer wearables. Fitness trackers and smart garments incorporating basic motion capture capabilities could create a new market segment worth an estimated $3.4 billion by 2026. Current innovations focus on MEMS-based sensors that offer reasonable accuracy while consuming minimal power. Manufacturers exploring this opportunity prioritize comfort and discretion, with some prototypes resembling ordinary athletic apparel while capturing comprehensive movement data.

Factories implementing collaborative robotics and human-machine interfaces present a growing market for industrial-grade motion capture systems. These applications require sensors that withstand vibration, electromagnetic interference, and harsh environmental conditions while maintaining precision. The industrial sector’s motion capture market is projected to grow at 14.2% CAGR as manufacturers seek safer, more efficient ways to automate processes involving human workers. Recent advancements include explosion-proof variants certified for use in hazardous locations.