#Remote Monitoring Software Remote Monitoring Software Market Remote Monitoring Software Market 2022 Remote Monitoring Software Market Analys

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

BuzzFeed published a report claiming that Tumblr was utilized as a distribution channel for Russian agents to influence American voting habits during the 2016 presidential election in Feb 2018.

Text

Subprime gadgets

I'm on tour with my new, nationally bestselling novel The Bezzle! Catch me THIS SUNDAY in ANAHEIM at WONDERCON: YA Fantasy, Room 207, 10 a.m.; Signing, 11 a.m.; Teaching Writing, 2 p.m., Room 213CD.

The promise of feudal security: "Surrender control over your digital life so that we, the wise, giant corporation, can ensure that you aren't tricked into catastrophic blunders that expose you to harm":

https://locusmag.com/2021/01/cory-doctorow-neofeudalism-and-the-digital-manor/

The tech giant is a feudal warlord whose platform is a fortress; move into the fortress and the warlord will defend you against the bandits roaming the lawless land beyond its walls.

That's the promise, here's the failure: What happens when the warlord decides to attack you? If a tech giant decides to do something that harms you, the fortress becomes a prison and the thick walls keep you in.

Apple does this all the time: "click this box and we will use our control over our platform to stop Facebook from spying on you" (Ios as fortress). "No matter what box you click, we will spy on you and because we control which apps you can install, we can stop you from blocking our spying" (Ios as prison):

https://pluralistic.net/2022/11/14/luxury-surveillance/#liar-liar

But it's not just Apple – any corporation that arrogates to itself the right to override your own choices about your technology will eventually yield to temptation, using that veto to help itself at your expense:

https://pluralistic.net/2023/07/28/microincentives-and-enshittification/

Once the corporation puts the gun on the mantelpiece in Act One, they're begging their KPI-obsessed managers to take it down and shoot you in the head with it in anticipation of of their annual Act Three performance review:

https://pluralistic.net/2023/12/08/playstationed/#tyler-james-hill

One particularly pernicious form of control is "trusted computing" and its handmaiden, "remote attestation." Broadly, this is when a device is designed to gather information about how it is configured and to send verifiable testaments about that configuration to third parties, even if you want to lie to those people:

https://www.eff.org/deeplinks/2023/08/your-computer-should-say-what-you-tell-it-say-1

New HP printers are designed to continuously monitor how you use them – and data-mine the documents you print for marketing data. You have to hand over a credit-card in order to use them, and HP reserves the right to fine you if your printer is unreachable, which would frustrate their ability to spy on you and charge you rent:

https://arstechnica.com/gadgets/2024/02/hp-wants-you-to-pay-up-to-36-month-to-rent-a-printer-that-it-monitors/

Under normal circumstances, this technological attack would prompt a defense, like an aftermarket mod that prevents your printer's computer from monitoring you. This is "adversarial interoperability," a once-common technological move:

https://www.eff.org/deeplinks/2019/10/adversarial-interoperability

An adversarial interoperator seeking to protect HP printer users from HP could gin up fake telemetry to send to HP, so they wouldn't be able to tell that you'd seized the means of computation, triggering fines charged to your credit card.

Enter remote attestation: if HP can create a sealed "trusted platform module" or a (less reliable) "secure enclave" that gathers and cryptographically signs information about which software your printer is running, HP can detect when you have modified it. They can force your printer to rat you out – to spill your secrets to your enemy.

Remote attestation is already a reliable feature of mobile platforms, allowing agencies and corporations whose services you use to make sure that you're perfectly defenseless – not blocking ads or tracking, or doing anything else that shifts power from them to you – before they agree to communicate with your device.

What's more, these "trusted computing" systems aren't just technological impediments to your digital wellbeing – they also carry the force of law. Under Section 1201 of the Digital Millennium Copyright Act, these snitch-chips are "an effective means of access control" which means that anyone who helps you bypass them faces a $500,000 fine and a five-year prison sentence for a first offense.

Feudal security builds fortresses out of trusted computing and remote attestation and promises to use them to defend you from marauders. Remote attestation lets them determine whether your device has been compromised by someone seeking to harm you – it gives them a reliable testament about your device's configuration even if your device has been poisoned by bandits:

https://pluralistic.net/2020/12/05/trusting-trust/#thompsons-devil

The fact that you can't override your computer's remote attestations means that you can't be tricked into doing so. That's a part of your computer that belongs to the manufacturer, not you, and it only takes orders from its owner. So long as the benevolent dictator remains benevolent, this is a protective against your own lapses, follies and missteps. But if the corporate warlord turns bandit, this makes you powerless to stop them from devouring you whole.

With that out of the way, let's talk about debt.

Debt is a normal feature of any economy, but today's debt plays a different role from the normal debt that characterized life before wages stagnated and inequality skyrocketed. 40 years ago, neoliberalism – with its assaults on unions and regulations – kicked off a multigenerational process of taking wealth away from working people to make the rich richer.

Have you ever watched a genius pickpocket like Apollo Robbins work? When Robins lifts your wristwatch, he curls his fingers around your wrist, expertly adding pressure to simulate the effect of a watchband, even as he takes away your watch. Then, he gradually releases his grip, so slowly that you don't even notice:

https://www.reddit.com/r/nextfuckinglevel/comments/ppqjya/apollo_robbins_a_master_pickpocket_effortlessly/

For the wealthy to successfully impoverish the rest of us, they had to provide something that made us feel like we were still doing OK, even as they stole our wages, our savings, and our futures. So, even as they shipped our jobs overseas in search of weak environmental laws and weaker labor protection, they shared some of the savings with us, letting us buy more with less. But if your wages keep stagnating, it doesn't matter how cheap a big-screen TV gets, because you're tapped out.

So in tandem with cheap goods from overseas sweatshops, we got easy credit: access to debt. As wages fell, debt rose up to fill the gap. For a while, it's felt OK. Your wages might be falling off, the cost of health care and university might be skyrocketing, but everything was getting cheaper, it was so easy to borrow, and your principal asset – your family home – was going up in value, too.

This period was a "bezzle," John Kenneth Galbraith's name for "The magic interval when a confidence trickster knows he has the money he has appropriated but the victim does not yet understand that he has lost it." It's the moment after Apollo Robbins has your watch but before you notice it's gone. In that moment, both you and Robbins feel like you have a watch – the world's supply of watch-derived happiness actually goes up for a moment.

There's a natural limit to debt-fueled consumption: as Michael Hudson says, "debts that can't be paid, won't be paid." Once the debtor owes more than they can pay back – or even service – creditors become less willing to advance credit to them. Worse, they start to demand the right to liquidate the debtor's assets. That can trigger some pretty intense political instability, especially when the only substantial asset most debtors own is the roof over their heads:

https://pluralistic.net/2022/11/06/the-end-of-the-road-to-serfdom/

"Debts that can't be paid, won't be paid," but that doesn't stop creditors from trying to get blood from our stones. As more of us became bankrupt, the bankruptcy system was gutted, turned into a punitive measure designed to terrorize people into continuing to pay down their debts long past the point where they can reasonably do so:

https://pluralistic.net/2022/10/09/bankruptcy-protects-fake-people-brutalizes-real-ones/

Enter "subprime" – loans advanced to people who stand no meaningful chance of every paying them back. We all remember the subprime housing bubble, in which complex and deceptive mortgages were extended to borrowers on the promise that they could either flip or remortgage their house before the subprime mortgages detonated when their "teaser rates" expired and the price of staying in your home doubled or tripled.

Subprime housing loans were extended on the belief that people would meekly render themselves homeless once the music stopped, forfeiting all the money they'd plowed into their homes because the contract said they had to. For a brief minute there, it looked like there would be a rebellion against mass foreclosure, but then Obama and Timothy Geithner decreed that millions of Americans would have to lose their homes to "foam the runways" for the banks:

https://wallstreetonparade.com/2012/08/how-treasury-secretary-geithner-foamed-the-runways-with-childrens-shattered-lives/

That's one way to run a subprime shop: offer predatory loans to people who can't afford them and then confiscate their assets when they – inevitably – fail to pay their debts off.

But there's another form of subprime, familiar to loan sharks through the ages: lend money at punitive interest rates, such that the borrower can never repay the debt, and then terrorize the borrower into making payments for as long as possible. Do this right and the borrower will pay you several times the value of the loan, and still owe you a bundle. If the borrower ever earns anything, you'll have a claim on it. Think of Americans who borrowed $79,000 to go to university, paid back $190,000 and still owe $236,000:

https://pluralistic.net/2020/12/04/kawaski-trawick/#strike-debt

This kind of loan-sharking is profitable, but labor-intensive. It requires that the debtor make payments they fundamentally can't afford. The usurer needs to get their straw right down into the very bottom of the borrower's milkshake and suck up every drop. You need to convince the debtor to sell their wedding ring, then dip into their kid's college fund, then steal their father's coin collection, and, then break into cars to steal the stereos. It takes a lot of person-to-person work to keep your sucker sufficiently motivated to do all that.

This is where digital meets subprime. There's $1T worth of subprime car-loans in America. These are pure predation: the lender sells a beater to a mark, offering a low down-payment loan with a low initial interest rate. The borrower makes payments at that rate for a couple of months, but then the rate blows up to more than they can afford.

Trusted computing makes this marginal racket into a serious industry. First, there's the ability of the car to narc you out to the repo man by reporting on its location. Tesla does one better: if you get behind in your payments, your Tesla immobilizes itself and phones home, waits for the repo man to come to the parking lot, then it backs itself out of the spot while honking its horn and flashing its lights:

https://tiremeetsroad.com/2021/03/18/tesla-allegedly-remotely-unlocks-model-3-owners-car-uses-smart-summon-to-help-repo-agent/

That immobilization trick shows how a canny subprime car-lender can combine the two kinds of subprime: they can secure the loan against an asset (the car), but also coerce borrowers into prioritizing repayment over other necessities of life. After your car immobilizes itself, you just might decide to call the dealership and put down your credit card, even if that means not being able to afford groceries or child support or rent.

One thing we can say about digital tools: they're flexible. Any sadistic motivational technique a lender can dream up, a computerized device can execute. The subprime car market relies on a spectrum of coercive tactics: cars that immobilize themselves, sure, but how about cars that turn on their speakers to max and blare a continuous recording telling you that you're a deadbeat and demanding payment?

https://archive.nytimes.com/dealbook.nytimes.com/2014/09/24/miss-a-payment-good-luck-moving-that-car/

The more a subprime lender can rely on a gadget to torment you on their behalf, the more loans they can issue. Here, at last, is a form of automation-driven mass unemployment: normally, an economy that has been fully captured by wealthy oligarchs needs squadrons of cruel arm-breakers to convince the plebs to prioritize debt service over survival. The infinitely flexible, tireless digital arm-breakers enabled by trusted computing have deprived all of those skilled torturers of their rightful employment:

https://pluralistic.net/2021/04/02/innovation-unlocks-markets/#digital-arm-breakers

The world leader in trusted computing isn't cars, though – it's phones. Long before anyone figured out how to make a car take orders from its manufacturer over the objections of its driver, Apple and Google were inventing "curating computing" whose app stores determined which software you could run and how you could run it.

Back in 2021, Indian subprime lenders hit on the strategy of securing their loans by loading borrowers' phones up with digital arm-breaking software:

https://restofworld.org/2021/loans-that-hijack-your-phone-are-coming-to-india/

The software would gather statistics on your app usage. When you missed a payment, the phone would block you from accessing your most frequently used app. If that didn't motivate you to pay, you'd lose your second-most favorite app, then your third, fourth, etc.

This kind of digital arm-breaking is only possible if your phone is designed to prioritize remote instructions – from the manufacturer and its app makers – over your own. It also only works if the digital arm-breaking company can confirm that you haven't jailbroken your phone, which might allow you to send fake data back saying that your apps have been disabled, while you continue to use those apps. In other words, this kind of digital sadism only works if you've got trusted computing and remote attestation.

Enter "Device Lock Controller," an app that comes pre-installed on some Google Pixel phones. To quote from the app's description: "Device Lock Controller enables device management for credit providers. Your provider can remotely restrict access to your device if you don't make payments":

https://lemmy.world/post/13359866

Google's pitch to Android users is that their "walled garden" is a fortress that keeps people who want to do bad things to you from reaching you. But they're pre-installing software that turns the fortress into a prison that you can't escape if they decide to let someone come after you.

There's a certain kind of economist who looks at these forms of automated, fine-grained punishments and sees nothing but a tool for producing an "efficient market" in debt. For them, the ability to automate arm-breaking results in loans being offered to good, hardworking people who would otherwise be deprived of credit, because lenders will judge that these borrowers can be "incentivized" into continuing payments even to the point of total destitution.

This is classic efficient market hypothesis brain worms, the kind of cognitive dead-end that you arrive at when you conceive of people in purely economic terms, without considering the power relationships between them. It's a dead end you navigate to if you only think about things as they are today – vast numbers of indebted people who command fewer assets and lower wages than at any time since WWII – and treat this as a "natural" state: "how can these poors expect to be offered more debt unless they agree to have their all-important pocket computers booby-trapped?"

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/03/29/boobytrap/#device-lock-controller

Image: Oatsy (modified) https://www.flickr.com/photos/oatsy40/21647688003

CC BY 2.0 https://creativecommons.org/licenses/by/2.0/

#pluralistic#debt#subprime#armbreakers#mobile#google#android#apps#drm#technological self-determination#efficient market hypothesis brainworms#law and political economy#gadgets#boobytraps#app stores#curated computing#og app#trusted computing

230 notes

·

View notes

Text

"In the age of smart fridges, connected egg crates, and casino fish tanks doubling as entry points for hackers, it shouldn’t come as a surprise that sex toys have joined the Internet of Things (IoT) party.

But not all parties are fun, and this one comes with a hefty dose of risk: data breaches, psychological harm, and even physical danger.

Let’s dig into why your Bluetooth-enabled intimacy gadget might be your most vulnerable possession — and not in the way you think.

The lure of remote-controlled intimacy gadgets isn’t hard to understand. Whether you’re in a long-distance relationship or just like the convenience, these devices have taken the market by storm.

According to a 2023 study commissioned by the U.K.’s Department for Science, Innovation, and Technology (DSIT), these toys are some of the most vulnerable consumer IoT products.

And while a vibrating smart egg or a remotely controlled chastity belt might sound futuristic, the risks involved are decidedly dystopian.

Forbes’ Davey Winder flagged the issue four years ago when hackers locked users into a chastity device, demanding a ransom to unlock it.

Fast forward to now, and the warnings are louder than ever. Researchers led by Dr. Mark Cote found multiple vulnerabilities in these devices, primarily those relying on Bluetooth connectivity.

Alarmingly, many of these connections lack encryption, leaving the door wide open for malicious third parties.

If you’re picturing some low-stakes prank involving vibrating gadgets going haywire, think again. The risks are far graver.

According to the DSIT report, hackers could potentially inflict physical harm by overheating a device or locking it indefinitely. Meanwhile, the psychological harm could stem from sensitive data — yes, that kind of data — being exposed or exploited.

A TechCrunch exposé revealed that a security researcher breached a chastity device’s database containing over 10,000 users’ information. That was back in June, and the manufacturer still hasn’t addressed the issue.

In another incident, users of the CellMate connected chastity belt reported hackers demanding $750 in bitcoin to unlock devices. Fortunately, one man who spoke to Vice hadn’t been wearing his when the attack happened. Small mercies, right?

These aren’t isolated events. Standard Innovation Corp., the maker of the We-Vibe toy, settled for $3.75 million in 2017 after it was discovered the device was collecting intimate data without user consent.

A sex toy with a camera was hacked the same year, granting outsiders access to its live feed.

And let’s not forget: IoT toys are multiplying faster than anyone can track, with websites like Internet of Dongs monitoring the surge.

If the thought of a connected chastity belt being hacked makes you uneasy, consider this: sex toys are just a small piece of the IoT puzzle.

There are an estimated 17 billion connected devices worldwide, ranging from light bulbs to fitness trackers — and, oddly, smart egg crates.

Yet, as Microsoft’s 2022 Digital Defense Report points out, IoT security is lagging far behind its software and hardware counterparts.

Hackers are opportunistic. If there’s a way in, they’ll find it. Case in point: a casino lost sensitive customer data after bad actors accessed its network through smart sensors in a fish tank.

If a fish tank isn’t safe, why would we expect a vibrating gadget to be?

Here’s where the frustration kicks in: these vulnerabilities are preventable.

The DSIT report notes that many devices rely on unencrypted Bluetooth connections or insecure APIs for remote control functionality.

Fixing these flaws is well within the reach of manufacturers, yet companies routinely fail to prioritize security.

Even basic transparency around data collection would be a step in the right direction. Users deserve to know what’s being collected, why, and how it’s protected. But history suggests the industry is reluctant to step up.

After all, if companies like Standard Innovation can get away with quietly siphoning off user data, why would smaller players bother to invest in robust security?

So, what’s a smart-toy enthusiast to do? First, ask yourself: do you really need your device to be connected to an app?

If the answer is no, then maybe it’s best to go old school. If remote connectivity is a must, take some precautions.

Keep software updated: Ensure both the device firmware and your phone’s app are running the latest versions. Updates often include critical security patches.

Use secure passwords: Avoid default settings and choose strong, unique passwords for apps controlling your devices.

Limit app permissions: Only grant the app the bare minimum of permissions needed for functionality.

Vet the manufacturer: Research whether the company has a history of addressing security flaws. If they’ve been caught slacking before, it’s a red flag.

The conversation around sex toy hacking isn’t just about awkward headlines — it’s about how we navigate a world increasingly dependent on connected technology. As devices creep further into every corner of our lives, from the bedroom to the kitchen, the stakes for privacy and security continue to rise.

And let’s face it: there’s something uniquely unsettling about hackers turning moments of intimacy into opportunities for exploitation.

If companies won’t take responsibility for protecting users, then consumers need to start asking tough questions — and maybe think twice before connecting their pleasure devices to the internet.

As for the manufacturers? The message is simple: step up or step aside.

No one wants to be the next headline in a tale of hacked chastity belts and hijacked intimacy. And if you think that’s funny, just wait until your light bulb sells your Wi-Fi password.

This is where IoT meets TMI. Stay connected, but stay safe."

https://thartribune.com/government-warns-couples-that-sex-toys-remain-a-tempting-target-for-hackers-with-the-potential-to-be-weaponized/

#iot#I only want non-smart devices#I don't want my toilet to connect to the internet#seriously#smart devices#ai#anti ai#enshittification#smart sex toys

26 notes

·

View notes

Text

Top 10 Companies Shaping the Future of Fuel Management Systems

The global fuel management systems (FMS) market was valued at US$ 624.4 million in 2023 and is expected to reach US$ 1.0 billion by 2034, growing at a CAGR of 4.6% from 2024 to 2034. As fuel expenses continue to dominate operational costs in fleet-heavy industries, the demand for effective, secure, and intelligent fuel management solutions has surged.

What is a Fuel Management System (FMS)?

A fuel management system is a combination of hardware and software technologies designed to track, monitor, and control fuel usage across vehicles and industrial equipment. These systems are essential in industries that depend on road, rail, air, or marine transportation, enabling businesses to minimize fuel waste, detect theft, and boost operational efficiency.

Analyst Viewpoint: A Growing Need for Fuel Intelligence

Two main trends are fueling the rise of FMS:

For example, in early 2022, petroleum/fuel accounted for 12% of recorded cargo thefts in the U.S., emphasizing the need for robust tracking mechanisms.

Technological Advancements in FMS

Modern FMS solutions increasingly incorporate IoT sensors, telematics, GPS, cloud integration, and AI algorithms to give fleet operators a detailed view of fuel consumption across sites and vehicles. These technologies offer real-time alerts, fuel trend analysis, and remote diagnostics.

Key technological advancements include:

For instance, in 2021, Fuel Me launched a mobile platform offering fuel purchasing and emergency services for the commercial transportation and construction sectors. Similarly, Aeris partnered with Omnicomm to combat fuel theft in India through smart monitoring solutions.

Regional Outlook: Asia Pacific Takes the Lead

Asia Pacific held the largest share of the global FMS market in 2023. The region's rapid industrialization, increasing fleet sizes, and efforts to optimize fuel consumption have contributed to this dominance.

Key factors contributing to regional growth include:

As companies in Asia Pacific continue to adopt cutting-edge solutions to minimize fuel costs, the region is expected to maintain its leading position through 2034.

Key Players and Market Landscape

Prominent players in the FMS market are developing customized, integrated, and modular solutions to meet the growing needs of fleet operators. Key companies include:

These players are focusing on R&D investments, strategic partnerships, and region-specific launches to expand their customer base. For instance, Shell Fleet Solutions offers localized services in India tailored to reduce the total cost of fleet ownership.

Market Segmentation Overview

The FMS market can be segmented by process, application, end-user, and geography:

Future Outlook

With the rising emphasis on fuel efficiency, cost control, and security, the FMS market is well-positioned for steady growth through 2034. Companies across sectors—from logistics and mining to aviation and construction—are likely to continue investing in FMS as part of their digital transformation and sustainability strategies.

In the coming years, we can expect to see further integration of AI and machine learning, greater use of predictive analytics, and scalable SaaS platforms that cater to businesses of all sizes.

0 notes

Text

Data, Distribution, and Detection: Smart Water Tech Growth

Meticulous Research®—a leading global market research company, published a research report titled, ‘Smart Water Management Market by Offering (Hardware, Software, Services), Application (Water Management, Leak Detection, Water Quality & Quantity Monitoring, Others), End User (Residential, Commercial, Industrial), & Geography - Global Forecast to 2030.’ According to this latest publication from Meticulous Research®, in the past few years, we have seen a real shift in how utilities and governments are thinking about water. The days of simply patching leaks and replacing broken pipes are fading. Now, there’s real momentum behind smarter water systems — ones that can predict issues before they become crises. The market for smart water management reflects that change. By 2030, it is expected to reach around $69.6 billion, growing at a steady 14.7% annually from 2023. What is fueling this? A few things stand out: First, the massive problem of non-revenue water. That is water that never gets billed because it is lost in the system — through leaks, theft, or poor metering. Then there is the infrastructure itself. Much of it is decades old, and retrofitting is not optional anymore. Governments, especially in places focused on smart cities, are pushing for innovation. But this shift does not come cheap. The cost of implementation and the challenge of merging new tech with outdated systems are real roadblocks. Despite that, one thing is clear: smart water meters are catching on fast. They are not just about data — they are about using that data to manage water more responsibly.

Smart Water Systems by Offering – Where the Market Stands in 2023

Smart water management tends to get broken down into three main areas: hardware, software, and services. Last year, hardware came out on top — and honestly, that makes sense. Smart meters, sensors, and wireless transmitters are everywhere now. Utilities are using them not just to read usage remotely, but to spot leaks, reduce waste, and make billing more accurate without sending someone out in a truck. A solid example? Sardinia. The island rolled out smart meters in early 2023 to help curb water loss and improve efficiency. It is a good example of how regions with aging infrastructure are leaning on tech to modernize their systems without starting from scratch. But there is a shift happening. While hardware still holds the biggest share, software is catching up — fast. What I am seeing is that utilities are no longer just collecting data; they are starting to act on it. Software platforms now help operators monitor systems in real-time, detect anomalies, and even predict where a pipeline failure might happen next. Trimble’s eRespond is a case in point — it tracks incidents from the first report all the way to resolution and documentation. That kind of integration is making software less of a support tool and more of a core part of how utilities operate day-to-day.

Application-Based Insights into the Smart Water Management Market

The range of applications under smart water management is growing wider every year. Today, it includes everything from water quality monitoring and asset lifecycle management to stormwater prediction systems, real-time analytics, and leak detection platforms. In 2023, the water qualityand quantity monitoring segment take the lead — and for good reason. Utilities are under pressure to meet stricter water safety standards and ensure supply reliability, especially as climate risks grow. Smart sensors that can detect changes in pH, temperature, or microbial presence are now essential in identifying issues before they turn into emergencies. One example of this shift is Brunei’s 2022 rollout of a networked smart water monitoring system. It now serves as an early-warning tool for floods and infrastructure strain. Beyond Brunei, places like Singapore, California, and parts of Western Europe are scaling similar tech for monitoring drinking water pipelines and wastewater treatment facilities, tying the data into centralized dashboards for faster response. That said, the fastest-growing application is not monitoring alone — it is smart water management and distribution. As cities expand, outdated infrastructure struggles to keep up. Distribution losses remain a massive issue, particularly in regions where nearly a third of treated water goes unaccounted for. Smart water management platforms are being used to reduce that gap. They automate system responses, reroute flows during disruptions, and identify leak-prone zones long before a pipe bursts. Dubai's DEWA system is a great case study — it remotely monitors citywide water flows, enabling near-instant control adjustments, and supports predictive maintenance. Other global utilities are now benchmarking against similar systems, as governments invest heavily in water sustainability and urban resilience.

End-user Insights into Global Smart Water Management Adoption

In many industries, water usage is not just about cost — it is tied directly to performance, compliance, and sustainability. That is why the industrial sector is currently the biggest user of smart water technologies. Manufacturers, energy companies, and chemical plants are adopting tools that help them understand how water flows through their systems. These setups offer real-time tracking, highlight inefficiencies, and support environmental goals, all while helping companies stay within regulatory limits. A case in point: Saint-Gobain upgraded its plant in Social Circle, Georgia, back in 2022 with smart water meters and modernized equipment. The move helped the company get better control over water use in its production processes. On a different note, equipment providers are also evolving — Grundfos recently rolled out smart-connected pumps in Singapore that can track performance data and notify teams when maintenance is needed. Still, it is not just factories making the switch. The residential sector is catching up fast, especially as water leaks and overuse become bigger concerns. According to the U.S. Environmental Protection Agency, about 10% of homes have leaks that waste nearly 100 gallons a day. That is not just water lost — it is money, too. This has led to a spike in smart meter installations in homes, where people want accurate billing and leak detection alerts. With smart homes becoming more mainstream, smart water tools are naturally following.

Exploring the Global Surge in IoT-Driven Water Monitoring Systems

Across the globe, how we manage water is undergoing a real transformation. In 2023, North America led the smart water management market, driven by cities and utilities upgrading to digital systems that can detect leaks, monitor flow, and reduce waste without needing manual intervention. Tools using smart water technology and IoT water management are becoming the new norm — not just to cut costs, but to improve day-to-day reliability. Meanwhile, the Asia-Pacific region is growing rapidly in this space. As urban populations rise and fresh water becomes scarcer, the region is doubling down on digital tools for smarter water monitoring. Cities are deploying intelligent water management systems for everything from irrigation in agriculture to metering water use in high-density housing. What is interesting is how this tech is being localized — adapted for both urban slums and upscale developments alike. Also worth noting is how private industries are adopting smart water commercial solutions. From manufacturing facilities to real estate developers, more are choosing smart systems to gain better visibility over consumption, catch leaks early, and automate billing processes. These shifts show that modern water management is not just a public sector responsibility anymore — it is a shared priority.

Key Players:

Some of the key players operating in the global smart water management market are IBM Corporation (U.S.), ABB Ltd. (Switzerland), Honeywell International Inc. (U.S.), Schneider Electric SE (France), Cisco Systems, Inc. (U.S.), Sensus (U.S.), Mueller Water Products, Inc. (U.S.), Trimble Inc. (U.S.), Arad Group (Israel), Oracle Corporation (U.S.), Badger Meter, Inc. (U.S.), Landis+Gyr Group AG (Switzerland), Kamstrup A/S (Denmark), SUEZ SA (France), HydroPoint (U.S.), Siemens AG (Germany), Itron, Inc. (U.S.), Endress+Hauser AG (Switzerland) and Neptune Technology Group Inc. (U.S.).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5198

Key questions answered in the report:

What is the projected value of the global smart water management market by 2030?

What is the estimated CAGR of the smart water management market between 2023 and 2030?

Which offering segment—hardware, software, or services—held the largest share of the market in 2023?

Why is hardware still dominating the smart water management market?

Which application area led the market in 2023, and why?

What role does water quality and quantity monitoring play in smart utilities today?

Why does the industrial segment account for the largest share in the market?

What benefits do manufacturing companies gain from smart water management tools?

Why did North America lead the global smart water management market in 2023?

What factors are driving Asia-Pacific to register the highest CAGR during the forecast period?

How are IoT and AI transforming the landscape of water management?

In what ways are utilities shifting from data collection to data action through software?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

Agriculture Drones Market Impact of IoT and AI Technologies

The global agriculture drones market was valued at approximately USD 2.74 billion in 2024 and is projected to reach USD 10.26 billion by 2030, reflecting a compound annual growth rate (CAGR) of 25.0% from 2025 to 2030. The increasing demand for precision farming is a key driver behind the growing adoption of agriculture drones. These techniques aim to maximize crop yields while minimizing resource usage, such as water, fertilizers, and pesticides.

Drones equipped with high-resolution cameras, multispectral sensors, and GPS technology enable farmers to collect detailed data on crop health, soil conditions, and moisture levels. This real-time information empowers farmers to make informed, data-driven decisions regarding the application of inputs, thereby optimizing crop production and reducing waste. As the agricultural sector faces increasing pressure to enhance efficiency and sustainability, the demand for precision farming solutions, including drones, continues to rise. Data from the U.S. Department of Agriculture (USDA) indicate that the top five states adopting precision agriculture technologies—North Dakota, Nebraska, Iowa, South Dakota, and Illinois—accounted for nearly half of the U.S. cash receipts for field crops in 2022. This trend highlights a significant opportunity for the compact tractor market, as sales of advanced machinery supporting precision farming practices grow in these regions.

The growing integration of IoT (Internet of Things) and big data analytics in agriculture further enhances the utility of drones. When combined with IoT devices and data analytics platforms, drones offer a more comprehensive view of farm operations. They collect data in real time, analyze it, and transmit findings to farmers via cloud-based platforms. This connectivity allows for precise and timely monitoring of crops and soil conditions, enabling farmers to take immediate action to enhance productivity and crop health. The convergence of drones with IoT and big data solutions is driving the digital transformation of agriculture, significantly boosting the adoption of drone technology.

Key Market Trends & Insights

• North America agriculture drones market held a significant share of around 33.7% in 2024. The growing popularity of remote sensing technologies is a key factor influencing the agriculture drone market. Drones with various sensors, such as multispectral and thermal imaging, enable farmers to gather detailed information about their crops from above.

• The U.S. agriculture drones market is growing due to the growing movement toward sustainable agriculture. Farmers increasingly seek ways to minimize their ecological impact as consumers demand more environmentally friendly products.

• Based on component, the market is segmented into hardware, software, and services. The hardware segment dominated the market with a revenue share of 50.0% in 2024. The growing demand for longer flight times and increased payload capacities drive the segment growth.

• Based on farming environment, the component is divided into indoor farming and outdoor farming. The outdoor farming segment dominated the market in terms of revenue, with a revenue share of 82.5% in 2024. The increasing need for large-scale outdoor agricultural operations is driving the market growth.

Order a free sample PDF of the Agriculture Drones Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

• 2024 Market Size: USD 2.74 Billion

• 2030 Projected Market Size: USD 10.26 Billion

• CAGR (2025-2030): 25.0%

• North America: Largest market in 2024

• Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Some of the key players in the agriculture drones market include DJI, Sentera, and Trimble Inc., among others.

DJI is a Chinese technology company renowned for its civilian drones and aerial imaging technology. Its primary offerings encompass drones designed for photography, filmmaking, agriculture, and various hardware and software systems applicable to other industries. DJI has expanded its product range to include handheld gimbals, action cameras, and camera stabilizers, all featuring advanced imaging and stabilization technology. Due to their versatility and precision, DJI's products are widely utilized in sectors such as film production, agriculture, mapping, and law enforcement.

Parrot Drone SAS and DroneDeploy are notable emerging players in this market.

Parrot Drone SAS is a French manufacturer that initially focused on wireless products before shifting its focus to drones. The company's product lineup includes a variety of consumer drones, such as the Parrot Anafi and Parrot Mambo, which often feature high-quality cameras and advanced functionalities like automated flight modes, making them popular among hobbyists and photography enthusiasts. In the professional domain, Parrot offers robust solutions such as the Parrot Bluegrass and Parrot Disco, tailored for agricultural and surveying applications. These drones are equipped with specialized sensors and software designed to facilitate crop analysis, mapping, and aerial inspections.

Key Players

• DJI • Parrot Drone SAS • AgEagle Aerial Systems Inc. • AeroVironment, Inc. • PrecisionHawk • Trimble Inc. • DroneDeploy • Autel Robotics • Draganfly Inc. • Pix4D SA • Sky-Drones Technologies Ltd • Sentera

Conclusion

The agriculture drones market is on a robust growth trajectory, driven by the rising demand for precision farming and advancements in technology. As farmers increasingly seek efficient and sustainable methods to enhance crop yields, the integration of drones with IoT and big data analytics will play a crucial role in revolutionizing agricultural practices. This trend not only presents significant opportunities for market players but also contributes to the broader transformation of the agricultural landscape towards greater efficiency and sustainability.

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

#Agriculture Drones Market#Agriculture Drones Industry#Agriculture Drones Market Growth#Agriculture Drones Market Analysis#Agriculture Drones Market Forecast#Agriculture Drones Market Size

0 notes

Text

Exploring the Global Telemetry Market: Trends, Innovations, and Growth Opportunities

The Global Telemetry Market size is anticipated to exceed USD 512.25 Billion by 2032, growing at a CAGR of 8.9% from 2022 to 2032.

Telemetry Market Insights

Telemetry enables remote data collection and monitoring through automated wireless communication, using various sensors like temperature, pressure, and voltage. It is essential in sectors such as energy, healthcare, agriculture, and oil and gas. Market growth is fueled by cloud adoption, smart devices, big data integration, government support, and rising R&D. In healthcare, especially, its use in monitoring cardiac conditions is expanding due to the increasing prevalence of cardiovascular diseases.

This study gives a detailed analysis of drivers, restrains, opportunities and challenges limiting the market expansion of Telemetry market. The survey included a diverse set of players, including a balance of leading and growing manufacturers for business profiling, such as;

Cobham Limited, L3Harris Technologies Inc., Siemens AG, AstroNova Inc., General Electric Company, Honeywell International Inc., International Business Machines Corporation (IBM Corp.), Koninklijke Philips N.V., Rogers Communications Inc, Schneider Electric SE, Others.

Our expert team is consistently working on updated data and information on the key player's related business processes that value the market for future strategies and predictions

Get Access to a Free Copy of Our Latest Sample Report - https://www.sphericalinsights.com/request-sample/2300

Market Segmentation:

By Technology

Wire-Link

Wireless Telemetry Systems

Data Loggers

Acoustic Telemetry

Digital Telemetry

By Component

Hardware

Software

Covered in this Report:

1. Go-to-market Strategy. 2. Neutral perspective on the market performance. 3. Development trends, competitive landscape analysis, supply side analysis, demand side analysis, year-on-year growth, competitive benchmarking, vendor identification, QMI quadrant, and other significant analysis, as well as development status. 4. Customized regional/country reports as per request and country level analysis. 5. Potential & niche segments and regions exhibiting promising growth covered. 6.Analysis of Market Size (historical and forecast), Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM), Market Growth, Technological Trends, Market Share, Market Dynamics, Competitive Landscape and Major Players (Innovators, Start-ups, Laggard, and Pioneer).

Buy this report now:- https://www.sphericalinsights.com/checkout/2300

Industry Developments:

In April 2023, Mezmo, a leading observability data platform, has announced a free trial of Mezmo Telemetry Pipeline as well as a free community plan. Companies can now utilise the power of their data while reaping the cost savings and control benefits of a telemetry pipeline all without making a large upfront investment.

Regional Analysis for Telemetry Market:

✫ North America: (U.S., Canada, Mexico) ✫ Europe: (U.K., Italy, Germany, Russia, France, Spain, The Netherlands and Rest of Europe) ✫ Asia-Pacific: (India, Japan, China, South Korea, Australia, Indonesia Rest of Asia Pacific) ✫ South America: (Colombia, Brazil, Argentina, Rest of South America) ✫ Middle East & Africa: (Saudi Arabia, U.A.E., South Africa, Rest of Middle East & Africa)

Benefits of the Report:

⏩ A descriptive analysis of demand-supply gap, market size estimation, SWOT analysis, PESTEL Analysis and forecast in the global market. ⏩ Top-down and bottom-up approach for regional analysis ⏩ Porter’s five forces model gives an in-depth analysis of buyers and suppliers, threats of new entrants & substitutes and competition amongst the key market players. ⏩ By understanding the value chain analysis, the stakeholders can get a clear and detailed picture of this Market

Insightful inquiry before buying:- https://www.sphericalinsights.com/inquiry-before-buying/2300

Frequently asked questions:

➥ What is the market size of the Telemetry market? ➥ What is the market growth rate of the Telemetry market? ➥ What are the Telemetry market opportunities and threats faced by the vendors in the global Telemetry Industry? ➥ Which application/end-user or product type may seek incremental growth prospects? What is the market share of each type and application? ➥ What focused approach and constraints are holding the Telemetry market? ➥ What are the different sales, marketing, and distribution channels in the global industry?

Unlock the full report now! @ https://www.sphericalinsights.com/reports/telemetry-market

About the Spherical Insights

Spherical Insights is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

Contact Us:

Company Name: Spherical Insights

Email: [email protected]

Phone: +1 303 800 4326 (US)

Follow Us: LinkedIn | Facebook | Twitter

#Telemetry Market#Global Telemetry Market#Telemetry Market Size#Telemetry Market Share#Telemetry Market Analysi

0 notes

Text

A Hotelier’s Guide to Choosing the Best Management Software in the Philippines

Southeast Asia is fast becoming one of the hottest hospitality markets in the world—and right at its heart is the Philippines. With a booming tourism sector, growing demand for digital guest experiences, and a tech-savvy workforce, the country is ripe for innovation in hotel operations. Central to this transformation is the rise of hotel software in the Philippines, revolutionizing how properties are managed, guests are served, and revenues are maximized.

In this article, we’ll explore why hotel technology matters more than ever, why Southeast Asia (especially the Philippines) is in focus, and how hotel management software in the Philippines is reshaping the future of hospitality.

Why Southeast Asia—and Why Now?

Southeast Asia has emerged as a global tourism magnet. In 2023, the region recorded over 100 million international arrivals, with Thailand, Vietnam, and the Philippines leading the charts. By 2025, the figure is projected to hit 160 million tourists.

Here’s why the region is booming:

A young, digital-native population.

A surge in budget and midscale travel.

Heavy investment in infrastructure and smart tourism by governments.

Growing adoption of mobile, cloud, and AI-powered solutions in the hospitality sector.

The Philippines, in particular, has seen a 140% rise in inbound tourism from 2022 to 2024, with domestic travel also recovering strongly. The Department of Tourism projects 8 million international arrivals in 2025, supported by the “Love the Philippines” campaign and digitalization of travel services.

The Hidden Cost of Manual Hotel Management

Many independent hotels in the Philippines still run on spreadsheets, legacy tools, or manual check-in systems. While these may have worked in the past, today’s market dynamics make them a liability.

Problems hotels face without proper software:

Double bookings and poor inventory control.

Delayed check-ins and poor guest satisfaction.

Lack of data on guest preferences or behavior.

Inability to distribute rooms efficiently across OTAs.

Lost revenue from poor rate management.

In a study by Statista, 67% of travelers in Southeast Asia say they will not return to a hotel that has slow check-in or digital unfriendliness. In short, hospitality today is digital-first—and hotels need to catch up.

Hotel Software in the Philippines: A Game-Changer

Enter cloud-based hotel management software in the Philippines—platforms that help automate bookings, housekeeping, billing, marketing, guest communications, and more, all in one interface.

Key Benefits of Hotel Software:

Real-time room management: No more overbookings or lost reservations.

Multi-channel distribution: Sell rooms across Agoda, Booking.com, Airbnb, and your website simultaneously.

Guest personalization: Store guest preferences and deliver tailored experiences.

Mobile check-ins: Empower guests to check-in from their phone, skip the queue, and head straight to their room.

Revenue optimization: Use AI tools to analyze demand trends and auto-adjust rates.

Case Study: The Blue Orchid Resort, Cebu

After switching to a cloud-based hotel PMS, The Blue Orchid Resort in Moalboal saw increase in direct bookings within 4 months and reduced OTA commissions. Their front desk team now spends 50% less time on manual tasks, focusing more on delivering memorable guest experiences.

Top Features to Look For in Hotel Software in the Philippines

Whether you run a boutique hotel in Palawan, a business hotel in Makati, or a beach resort in Siargao, here’s what you should expect from modern hotel software:

Cloud-Based Accessibility: Work from anywhere, on any device—ideal for remote monitoring and multi-property chains.

Channel Manager: Sync room availability and rates across OTAs and your booking engine in real time.

Integrated POS: For F&B, spa, or gift shop billing—everything connects back to the guest folio.

Local Tax Compliance: The best hotel software Philippines platforms support VAT, withholding tax, and BIR-compliant invoicing.

Multilingual & Multi-currency

Handle both domestic and international guests without hassle.

The Business Case: ROI in Less Than a Year

A typical hotel in the Philippines using digital hotel management software can expect:

20–30% improvement in staff productivity

15–25% higher RevPAR (Revenue per Available Room)

20–40% reduction in human errors and operational delays

30–50% more direct bookings when combined with a smart booking engine

The payback period? Often less than 6–12 months, especially for mid-sized properties.

Tech Trends Shaping Hotel Software in 2025

Hotel software isn’t just about automation anymore—it’s about intelligence and personalization. Here are three trends to watch:

AI-Powered Guest Profiling

Using AI, software can build behavioral profiles based on past stays, preferences, and booking behavior. This enables predictive personalization—offering the right room, upsells, or services at the right time.

Contactless Everything

From mobile check-in to QR-code menus and chat-based concierge, the demand for low-touch experiences continues to rise.

Sustainability Tracking

New tools help hotels monitor water, energy, and waste metrics in real time, aligning with eco-conscious travelers and government incentives.

🇵🇭 Why Local Matters: Choosing a Hotel Software Partner in the Philippines

Global platforms are powerful—but not always tailored to local needs. Here’s why choosing a hospitality software provider in the Philippines makes sense:

Local support during Philippine business hours.

Built-in compliance with local tax laws and BIR guidelines.

Experience working with resorts, hostels, and boutique hotels in local destinations.

Integration with local payment gateways (e.g., GCash, Maya).

“We tried an international PMS before, but they couldn’t support our VAT invoicing or local currency setup. Switching to a local provider saved us a lot of time and stress.” – Operations Manager, Boutique Hotel, Baguio

How to Get Started with Hotel Software in the Philippines

If you’re ready to modernize your operations, follow these steps:

Assess your needs – size of property, number of rooms, departments, booking channels.

Book a demo – leading platforms offer free walkthroughs.

Trial the system – look for free trials to test compatibility.

Train your team – ensure all departments are aligned.

Go live and measure – track KPIs like ADR, RevPAR, and booking sources.

Final Thoughts: Digital-First is Guest-First

The hospitality industry is no longer just about beds and breakfasts—it’s about seamless, tech-enabled experiences. With tourism bouncing back stronger than ever in Southeast Asia, Filipino hotels that embrace technology will be best positioned to attract, retain, and delight modern travelers.

By investing in the right hotel management software in the Philippines, properties can do more than survive—they can thrive.

Ready to Digitize Your Hotel? Look for cloud-based, user-friendly, and locally supported hotel software that meets the evolving expectations of today’s guests. Schedule a free demo today and get 30 days free trial.

0 notes

Text

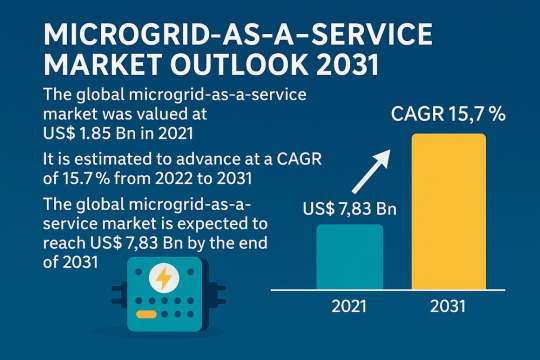

Microgrid-as-a-Service: A High-Growth $7.8B Market by 2031

The global Microgrid-as-a-Service (MaaS) market, valued at US$ 1.85 Bn in 2021, is projected to advance at a CAGR of 15.7% from 2022 to 2031 and reach a valuation of US$ 7.83 Bn by the end of 2031, according to recent market intelligence. The rapid shift toward decentralized, renewable energy and the growing need for uninterrupted power supply are major contributors to this robust growth.

Market Overview: Microgrid-as-a-Service (MaaS) is an emerging model that enables institutions, industries, and residential consumers to deploy microgrids with minimal upfront investment. MaaS provides energy security and enhances grid resilience, offering a reliable solution to frequent outages and natural disasters. It is increasingly becoming a preferred option in both developed and emerging markets for its ability to deliver cost-effective, clean, and locally sourced energy.

Market Drivers & Trends

The global MaaS market is being driven by:

Surge in renewable energy adoption: The growing installation of solar and wind energy systems is propelling the demand for intelligent microgrid solutions.

Government incentives and modernization programs: Initiatives like the U.S. Department of Energy’s Smart Grid Investment Grant Program and subsidies for clean energy projects are fostering microgrid deployments.

Growth in smart devices and grid digitization: Countries are rapidly adopting smart meters and automated transmission systems, reducing outages and improving energy efficiency.

Need for energy independence and resiliency: Particularly in disaster-prone or remote regions, microgrids provide critical backup and localized power supply.

Advancements in peer-to-peer energy trading and blockchain integration, enabling real-time, decentralized energy exchanges.

Key Players and Industry Leaders

The global MaaS market is consolidated, with a few major players commanding substantial market share. Leading companies include:

Schneider Electric – Offers Energy-as-a-Service and microgrid operation tools.

ABB – Provides turnkey solutions with digitized microgrid control platforms.

Siemens AG – Known for its intelligent energy management systems and consultancy services.

Eaton Corporation – Specializes in islanded and grid-tied microgrid operations.

Aggreko, ENGIE, Tech Mahindra, General Electric, and AIO Systems Ltd. also play significant roles in global deployments.

Emerging players such as Green Energy Corp. and Spirae, LLC are also gaining traction by focusing on software innovation and scalable energy management.

Recent Developments

In December 2021, Schneider Electric and Temasek launched GreeNext, a joint venture to deliver hybrid solar-battery microgrids to commercial and industrial clients.

In February 2021, ABB partnered with DEIF, combining control technologies to accelerate renewable energy integration in marine and land-based microgrid applications.

Numerous R&D initiatives are exploring virtual microgrids and blockchain-based energy trading, marking the next phase of energy decentralization.

Access key findings and insights from our Report in this sample -

Latest Market Trends

Growing preference for grid-connected microgrids due to their ability to trade unused energy and operate in hybrid or islanded modes.

Rising demand for monitoring and optimization services, ensuring efficient grid operation, reduced peak loads, and real-time energy analytics.

Surge in corporate ESG commitments, with companies seeking low-carbon and self-reliant energy systems.

Market Opportunities

The market is ripe with opportunities, particularly in:

Remote and underserved areas, where microgrids can deliver energy access.

Urban applications, as falling costs of solar panels and batteries make microgrids viable even in densely populated settings.

Commercial and industrial sectors, which demand reliable power for continuous operations.

Training and software services, as the need for skilled microgrid operators grows.

Future Outlook

Analysts predict a bright future for the MaaS industry:

Strong growth expected post-2030, driven by increased electrification, climate targets, and global energy transition goals.

The convergence of AI, IoT, and cloud computing with microgrid infrastructure will create new revenue streams in predictive maintenance and real-time grid management.

Hybrid energy systems (combining renewables, storage, and diesel) are anticipated to dominate deployments, offering cost, reliability, and environmental benefits.

Market Segmentation

The global microgrid-as-a-service market can be segmented as follows:

By Type:

Islanded Microgrid

Grid Connected Microgrid (Dominant segment with 78% share in 2021)

By Service:

Monitoring & Optimization

System Maintenance & Operations

Infrastructure Upgradation (Software & Others)

Training

Others

By End-user:

Government & Utility

Commercial

Industrial

Residential

Regional Insights

North America leads the global MaaS market, holding around 38% share, supported by:

Early adoption of renewable technologies

Government funding and incentives

Strong presence of key players

Asia Pacific is emerging as a high-growth region, driven by:

Rapid urbanization and industrialization

Government regulations promoting grid modernization

Growing demand from countries like India, China, Japan, and ASEAN nations

Europe continues to support the market with strong environmental regulations and sustainability goals.

South America and the Middle East & Africa are exhibiting steady progress, with South America showing the fastest CAGR owing to increasing renewable energy penetration and microgrid adoption in rural areas.

Why Buy This Report?

This comprehensive report offers:

In-depth analysis of current and future market dynamics

Insights into technological innovations and deployment strategies

Detailed profiling of key market players, including product portfolios and strategies

Regional and segment-wise breakdown of market share and growth rates

Strategic recommendations for stakeholders, investors, policymakers, and industry participants

0 notes

Text

U.S. Internet of Things (IoT) Market Size to Hit USD 118.24 Bn by 2030

The U.S. Internet of Things (IoT) market share remains one of the most mature and dynamic ecosystems globally. Valued at USD 98.09 billion in 2022, the market is projected to grow from USD 118.24 billion in 2023 to USD 553.92 billion by 2030, registering a compound annual growth rate (CAGR) of 24.7% during the forecast period. The U.S. Internet of Things (IoT) market refers to the ecosystem of interconnected physical devices, sensors, software, and network infrastructure that enables the collection, exchange, and analysis of data across a wide range of industries. These devices are embedded with computing technology that allows them to monitor environments, automate processes, and communicate with other systems and users in real-time.

Key Market Highlights: • Market Size (2022): USD 98.09 billion • Projected Size (2030): USD 553.92 billion • CAGR (2023–2030): 24.7% • Growth Drivers: Technological maturity, innovation leadership, and extensive IoT adoption across industries.

Leading U.S. Companies in the IoT Space: • Cisco Systems, Inc. • Amazon Web Services (AWS) • Microsoft Corporation • Intel Corporation • Qualcomm Technologies, Inc. • Hewlett Packard Enterprise (HPE) • IBM Corporation • Google LLC • Oracle Corporation • PTC Inc.

Request For Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-internet-of-things-iot-market-107392

Market Dynamics:

Strategic Market Drivers: • Expansion of smart city infrastructure supported by federal and state governments. • Increasing deployment of industrial IoT (IIoT) for manufacturing automation and predictive maintenance. • Growth in consumer IoT, including connected homes, wearables, and personal health tracking devices. • Advancements in 5G, AI, and edge computing fueling real-time, decentralized data processing.

Major Opportunities: • Healthcare IoT for remote patient monitoring, smart diagnostics, and hospital asset management. • Smart grid and energy optimization systems led by clean energy policies. • Transportation and mobility solutions such as connected vehicles and V2X communication. • Federal funding for infrastructure modernization and cybersecurity in IoT environments.

Market Applications: • Smart manufacturing • Connected healthcare and telemedicine • Smart homes and consumer IoT • Fleet and supply chain management • Environmental and agricultural monitoring • Retail automation and customer behavior tracking

Deployment Models & Connectivity: • Deployment Types: Cloud-based, on-premises, hybrid, and edge-enabled solutions • Connectivity: 5G, Wi-Fi 6, LPWAN (LoRa, NB-IoT), Bluetooth, Zigbee, and satellite IoT

Key Market Trends: • Surging interest in cybersecure IoT ecosystems and zero-trust architecture. • Integration of artificial intelligence (AI) with IoT for autonomous decision-making. • Proliferation of IoT-as-a-Service (IoTaaS) and managed IoT platforms. • Increased focus on sustainability and green IoT solutions for emissions tracking and resource efficiency.

Speak to Analyst: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-internet-of-things-iot-market-107392

Recent Industry Developments: May 2023 – Amazon Web Services (AWS) expanded its IoT TwinMaker platform, enabling faster digital twin deployment for industrial and logistics enterprises across the U.S.

August 2023 – Cisco launched its U.S.-focused IoT Operations Dashboard for real-time device tracking, configuration management, and anomaly detection at enterprise scale.

About Us: Fortune Business Insights delivers powerful data-driven insights to help businesses navigate disruption and capitalize on emerging trends. We specialize in delivering sector-specific intelligence, customized research, and strategic consulting across a wide range of industries. Our team empowers organizations with clarity, foresight, and a competitive edge in a fast-moving technological landscape.

Contact Us: US: +1 833 909 2966 UK: +44 808 502 0280 APAC: +91 744 740 1245 Email: [email protected]

#U.S. Internet of Things Market Share#U.S. Internet of Things Market Size#U.S. Internet of Things Market Industry#U.S. Internet of Things Market Driver#U.S. Internet of Things Market Growth#U.S. Internet of Things Market Analysis#U.S. Internet of Things Market Trends

0 notes

Text

Military RAS Supply Chain: Challenges, Opportunities, and Global Players

Military robotic and autonomous system (RAS) comprises minimally of a platform, software, and a power source. Military RAS consists of three platforms, namely, unmanned aircraft system, unmanned ground & robotic system, and unmanned maritime system. An unmanned aircraft system (UAS), commonly known as a drone, is an aircraft without any human pilot, crew, or passengers on board. UAVs are a component of an unmanned aircraft system, which includes adding a ground-based controller and a system of communications with the UAS. An unmanned ground and robotic system (UGRS) is a vehicle that operates while in contact with the ground and without an onboard human presence. UGRSs can be used for many applications where it may be inconvenient, dangerous, or impossible to have a human operator present. Unmanned maritime system (UMS) refers to all systems, subsystems, associated components, vehicles, equipment, and logistics for the operation of UAVs. These vehicles can be operated on the surface or underwater and may be remotely operated, partially or fully autonomous.

The Military Robotic and Autonomous System (RAS) market, with a base year of 2024, is projected to grow at a CAGR of 3.9% from 2025 to 2035.

Key Market Trends

The modernization of military forces and rising geopolitical tensions have increased demand for autonomous defensive platforms.

To lessen human exposure, armed forces are increasingly using RAS solutions in complicated and high-risk contexts.

Military RAS are gradually transitioning from tethered and remote-controlled systems to completely autonomous platforms thanks to technological developments.

Investment in RAS capabilities is increasing as the importance of rapid response and cost-effective combat grows.

Military strategy is increasingly dependent on RAS platforms' capacity to carry out precision strikes, logistical assistance, and continuous monitoring.

Leading Nations in RAS Development and Deployment

North America (U.S., Canada)

Europe (U.K., France, Russia, Germany, Italy, Spain, Sweden, Norway, Netherlands, Rest of Europe)

Asia-Pacific (China, India, Japan, South Korea, Rest of Asia-Pacific)

The military RAS market is expected to be dominated by North America.

Recent Developments

December 2022: The U.K. Ministry of Defense awarded a $158 million (£129 million) contract for 99 Stalker UAVs and 15 Indago UAVs to support troop operations.

August 2022: Kratos Defense & Security Solutions secured a $14 million contract to supply its tactical jet drone systems—including the XQ-58A Valkyrie, UTAP-22 Mako, and X-61A Gremlin—to the U.S. Air Force.

October 2022: Garuda Aerospace signed an MoU with Lockheed Martin Canada CDL Systems to integrate India-made drones with advanced unmanned aircraft systems software for defense and commercial use.

July 2021:Shield AI acquired Martin UAV to integrate its combat-proven autonomy software, Hivemind, with the V-BAT platform, strengthening its position in military edge autonomy and AI-driven applications.

Types of Military Robotic Systems

Unmanned Aircraft Systems (UAS)

Medium Altitude Long Endurance (MALE) UAVs

High Altitude Long Endurance (HALE) UAVs

Unmanned Combat Aerial Vehicles (UCAVs)

Unmanned Helicopters

Small UAVs

Loitering Munition UAVs

Unmanned Ground and Robotic Systems

Unmanned Ground Vehicles (UGVs)

Robots

Humanoid Robots

Unmanned Maritime Systems

Autonomous Maritime Surface Vehicles

Autonomous Maritime Underwater Vehicles

Key Industry Players

Northrop Grumman

Lockheed Martin

BAE Systems

General Dynamics

Elbit Systems

Anduril Industries

Kratos Defense & Security Solutions

Take a Deep Dive: Access Our Sample Report to Understand How the market Drive the Military Robotic and Autonomous System Market!

Learn more about Robotics and Automation Vertical. Click Here!

Conclusion

Advances in AI, autonomy, and systems integration are driving the worldwide military RAS market into a revolutionary era. Nations are quickly using unmanned systems as force multipliers in response to growing security concerns and increased global defense spending. North America's strong defense environment, significant R&D spending, and savvy acquisitions have allowed it to maintain its market dominance. Military RAS will be crucial in redefining modern combat as autonomous technologies advance, allowing for quicker, safer, and more intelligent operations on the battlefield. Even if there are still issues like high costs and operational complexity, the military RAS industry is well-positioned for long-term development and resilience thanks to continuous innovation, changing battle plans, and supporting defense policies.

#Military Robotic and Autonomous System (RAS) market#Military Robotic and Autonomous System (RAS) industry#Military Robotic and Autonomous System (RAS) report#automation

0 notes

Text

Interactive Video Wall Industry: Transforming Digital Engagement Across Sectors

The Interactive Video Wall Industry is rapidly evolving into a cornerstone of digital communication and visualization. Valued at USD 5.6 billion in 2022, this industry is projected to reach USD 13.2 billion by 2030, growing at a robust CAGR of 11.2%. From retail showrooms and educational institutions to command centers and healthcare facilities, interactive video walls are reshaping how organizations deliver immersive and responsive experiences.

Industry Dynamics

A Shift Toward Experience-Driven Environments

The industry is moving from static signage to intelligent, real-time visual interfaces. Interactive video walls provide tactile and gesture-responsive surfaces, enabling dynamic content interaction. This has fueled adoption across industries where engagement and visibility are paramount.

Convergence of AI, IoT, and Big Data

Next-generation video walls are increasingly integrated with artificial intelligence and IoT devices. This allows businesses to display data-rich dashboards, environmental updates, or customer behavior analytics—all updated in real time. These capabilities position the interactive video wall industry at the center of smart workspace and city initiatives.

Digital Transformation in Control and Command Centers

Security, defense, utility, and traffic monitoring centers are deploying large-scale video walls for situational awareness and multi-source data visualization. Real-time control room operations now rely on unified visual intelligence delivered through high-resolution displays.

Growth of Hybrid and Remote Workplaces

With remote collaboration becoming mainstream, enterprises are investing in interactive displays for high-quality video conferencing and cross-regional collaboration. Touch-enabled video walls allow simultaneous engagement from multiple devices and sources.

Industry Applications

Retail: Enhances customer engagement with real-time promotions, product demos, and brand storytelling in flagship stores and malls.

Education: Enables active learning and group collaboration in digital classrooms, auditoriums, and virtual labs.

Healthcare: Supports surgical planning, telemedicine visualization, and patient education in modern medical centers.

Government & Defense: Powers mission-critical decisions in emergency operations, surveillance hubs, and border control.

Corporate Sector: Transforms meeting rooms and common areas into data-driven, presentation-friendly spaces.

Transportation: Improves traveler experience through flight/train information systems, digital signage, and wayfinding.

Competitive Landscape

The Interactive Video Wall Industry includes a mix of global tech innovators and display specialists. Major industry players include:

Samsung Electronics

LG Display

Barco NV

Planar Systems

NEC Display Solutions

Christie Digital Systems

ViewSonic Corporation

Delta Electronics

These companies compete through innovation in screen resolution (4K/8K), ultra-thin bezels, brightness control, and software features such as remote management, modular scalability, and AI-enhanced user interfaces.

Strategic Moves:

Partnerships with AV integrators

Acquisitions of touch tech and signage software firms

Expansions into emerging markets

Development of energy-efficient, ultra-narrow bezel displays

Regional Highlights

North America leads due to enterprise innovation and control room integration.

Asia-Pacific is experiencing rapid adoption in smart cities, retail, and education.

Europe shows consistent demand driven by infrastructure modernization and public transit systems.

Future Outlook

As demand for smarter, more interactive environments grows, the Interactive Video Wall Industry is poised for exponential expansion. Investments in AR/VR integration, seamless multi-display interfaces, and AI-powered content delivery will drive future innovation. This sector will continue to redefine how institutions visualize, collaborate, and communicate information.

Trending Report Highlights

Discover other fast-evolving sectors aligned with visual and collaborative tech:

Automotive Manufacturing Equipment Market

Mid High Level Precision GP Market

RF Chip Inductor Market

Zoom Lens Market

Frame Grabber Market

0 notes

Text

North America Edge Computing Market Demand, Supply, Growth Factors, Latest Rising Trends and Forecast (2022-2028)

The North America edge computing market is expected to grow from US$ 16,212.71 million in 2022 to US$ 52,976.45 million by 2028. It is estimated to grow at a CAGR of 21.8% from 2022 to 2028.

North America Edge Computing Market

Edge computing operates through a highly distributed network, a design specifically crafted to eliminate the time-consuming round trip to the cloud. This core principle leads to reduced latency and real-time responsiveness, which are essential for enhancing user experience and supporting customer satisfaction in numerous applications. The acceleration of data transmission has become a critical business objective. From online meetings to mission-critical cloud-hosted computation applications, low latency ensures smooth and fast operation. Cumulative small improvements in latency across applications in sectors like healthcare, air traffic control, and combat situations can yield significant network performance improvements.

Low latency underpins a reliable and robust connection, effectively reducing connection loss, delays, lags, and buffers. This capability is vital for many businesses and industries that depend on real-time applications or live streaming, such as banking, diagnostic imaging, navigation, stock trading, weather forecasting, collaboration, research, ticket sales, video broadcasting, and online gaming. Thus, low latency enhances the operational speed at the edge, boosting the demand for edge computing. While all networks have limited bandwidth, particularly wireless communication, edge computing distributes data computation through on-premise smart devices, helping to alleviate these constraints.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/BMIRE00028905

North America Edge Computing Strategic Insights