#Industrial Refrigeration Systems Market Trends

Text

What Are Most-Significant Applications of Industrial Refrigeration Systems?

The ongoing COVID-19 pandemic has put the spotlight on the global healthcare ecosystem, as many of the myths about how advanced the medical infrastructure around the world is were busted. With the case and death counts rising, the industry was caught gasping for breath (metaphorically), while the patients were literally gasping for breath (COVID is a lung infection). During this time, the number of research studies being conducted in the pharmaceutical and healthcare sectors on virology skyrocketed, as a vaccine was to be the leader of the charge against the pandemic.

Therefore, the number of clinical trials being conducted for viral vaccines rose massively, as did the worldwide trade of vaccines, aided by several such products getting regulatory approvals. With the healthcare and pharmaceutical sectors expected to not drop their guard for many years to come, the industrial refrigeration systems market size, as calculated by P&S Intelligence, is predicted to increase to $41.1 billion in 2030 from $26.8 billion in 2019, at a 5.0% CAGR between 2020 and 2030.

This is because an efficient, unbroken cold chain is essential for drug development and trade. Refrigerators are not only used to store and transport the final pharmaceutical products but also for the storage and transportation of the raw materials. Pharmaceuticals, biosimilars, excipients, active ingredients, tissues, and blood products are extremely sensitive to heat; therefore, effective cooling is necessary to protect them from damage and make them viable for use over a long time.

Another sector where refrigeration is important for the same reason is food and beverage. Most agricultural products spoil in the heat, which is why keeping them in cool conditions is paramount. Several of the processed food packages carry the directions “store in a cool and dry place”. In food processing factories, the ingredients, intermediate goods, and final products must be refrigerated to increase their shelf life. Thus, with the rising disposable income allowing people in developing countries to purchase processed food, the demand for industrial-grade refrigerators among food and beverage companies is surging.

Other industries where refrigeration is vital are oil and gas, construction, and manufacturing. Since, the food and beverage sector has been the largest user of such systems, their sales have been the highest in Asia-Pacific (APAC). Home to the largest number of people in the world, APAC has the most-productive food and beverage industry. India is already home to the fifth-largest processed food industry, which continues to garner extensive government support. “…the food processing sector in India has received around US$ 7.54 billion worth of Foreign Direct Investment (FDI) during the period April 2000-March 2017.”, says the India Brand Equity Foundation (IBEF).

Moreover, recently, the Indian government announced plans to establish 40 mega food parks, which are essentially integrated manufacturing districts for the food and beverage sector. With this, the industrial refrigeration systems market is poised for strong growth, with such equipment being important in this industry. Moreover, Invest India expects the country’s food processing sector to value more than $500 billion by 2025, which reflects a consistently growing demand for processing equipment.

Hence, with the pharmaceutical and food and beverage production growing, the procurement of industrial-grade refrigerators will escalate too.

#Industrial Refrigeration Systems Market Share#Industrial Refrigeration Systems Market Size#Industrial Refrigeration Systems Market Growth#Industrial Refrigeration Systems Market Applications#Industrial Refrigeration Systems Market Trends

1 note

·

View note

Text

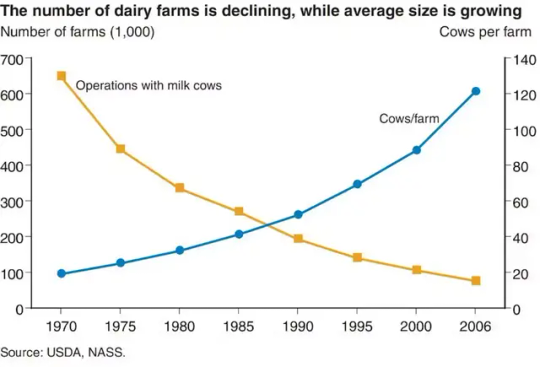

Milton Orr looked across the rolling hills in northeast Tennessee. “I remember when we had over 1,000 dairy farms in this county. Now we have less than 40,” Orr, an agriculture adviser for Greene County, Tennessee, told me with a tinge of sadness.

That was six years ago. Today, only 14 dairy farms remain in Greene County, and there are only 125 dairy farms in all of Tennessee. Across the country, the dairy industry is seeing the same trend: In 1970, more than 648,000 US dairy farms milked cattle. By 2022, only 24,470 dairy farms were in operation.

While the number of dairy farms has fallen, the average herd size—the number of cows per farm—has been rising. Today, more than 60 percent of all milk production occurs on farms with more than 2,500 cows.

This massive consolidation in dairy farming has an impact on rural communities. It also makes it more difficult for consumers to know where their food comes from and how it’s produced.

As a dairy specialist at the University of Tennessee, I’m constantly asked: Why are dairies going out of business? Well, like our friends’ Facebook relationship status, it’s complicated.

The Problem with Pricing

The biggest complication is how dairy farmers are paid for the products they produce.

In 1937, the Federal Milk Marketing Orders, or FMMO, were established under the Agricultural Marketing Agreement Act. The purpose of these orders was to set a monthly, uniform minimum price for milk based on its end use and to ensure that farmers were paid accurately and in a timely manner.

Farmers were paid based on how the milk they harvested was used, and that’s still how it works today.

Does it become bottled milk? That’s Class 1 price. Yogurt? Class 2 price. Cheddar cheese? Class 3 price. Butter or powdered dry milk? Class 4. Traditionally, Class 1 receives the highest price.

There are 11 FMMOs that divide up the country. The Florida, Southeast, and Appalachian FMMOs focus heavily on Class 1, or bottled, milk. The other FMMOs, such as Upper Midwest and Pacific Northwest, have more manufactured products such as cheese and butter.

For the past several decades, farmers have generally received the minimum price. Improvements in milk quality, milk production, transportation, refrigeration, and processing all led to greater quantities of milk, greater shelf life, and greater access to products across the US. Growing supply reduced competition among processing plants and reduced overall prices.

Along with these improvements in production came increased costs of production, such as cattle feed, farm labor, veterinary care, fuel, and equipment costs.

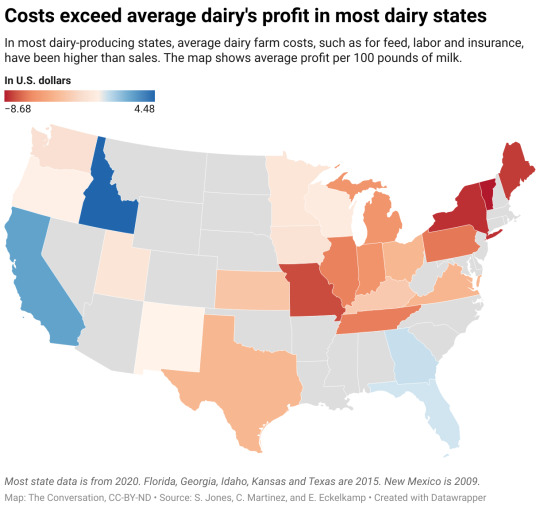

Researchers at the University of Tennessee in 2022 compared the price received for milk across regions against the primary costs of production: feed and labor. The results show why farms are struggling.

From 2005 to 2020, milk sales income per 100 pounds of milk produced ranged from $11.54 to $29.80, with an average price of $18.57. For that same period, the total costs to produce 100 pounds of milk ranged from $11.27 to $43.88, with an average cost of $25.80.

On average, that meant a single cow that produced 24,000 pounds of milk brought in about $4,457. Yet, it cost $6,192 to produce that milk, meaning a loss for the dairy farmer.

More efficient farms are able to reduce their costs of production by improving cow health, reproductive performance, and feed-to-milk conversion ratios. Larger farms or groups of farmers—cooperatives such as Dairy Farmers of America—may also be able to take advantage of forward contracting on grain and future milk prices. Investments in precision technologies such as robotic milking systems, rotary parlors, and wearable health and reproductive technologies can help reduce labor costs across farms.

Regardless of size, surviving in the dairy industry takes passion, dedication, and careful business management.

Some regions have had greater losses than others, which largely ties back to how farmers are paid, meaning the classes of milk, and the rising costs of production in their area. There are some insurance and hedging programs that can help farmers offset high costs of production or unexpected drops in price. If farmers take advantage of them, data shows they can functions as a safety net, but they don’t fix the underlying problem of costs exceeding income.

Passing the Torch to Future Farmers

Why do some dairy farmers still persist, despite low milk prices and high costs of production?

For many farmers, the answer is because it is a family business and a part of their heritage. Ninety-seven percent of US dairy farms are family owned and operated.

Some have grown large to survive. For many others, transitioning to the next generation is a major hurdle.

The average age of all farmers in the 2022 Census of Agriculture was 58.1. Only 9 percent were considered “young farmers,” age 34 or younger. These trends are also reflected in the dairy world. Yet, only 53 percent of all producers said they were actively engaged in estate or succession planning, meaning they had at least identified a successor.

How to Help Family Dairy Farms Thrive

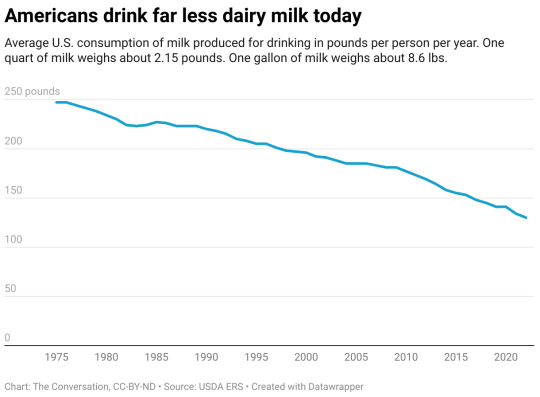

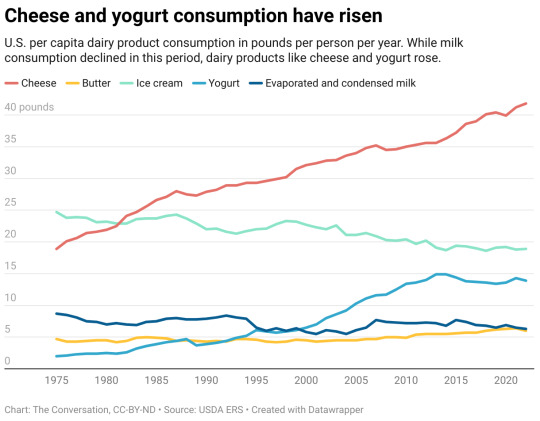

In theory, buying more dairy would drive up the market value of those products and influence the price producers receive for their milk. Society has actually done that. Dairy consumption has never been higher. But the way people consume dairy has changed.

Americans eat a lot, and I mean a lot, of cheese. We also consume a good amount of ice cream, yogurt, and butter, but not as much milk as we used to.

Does this mean the US should change the way milk is priced? Maybe.

The FMMO is currently undergoing reform, which may help stem the tide of dairy farmers exiting. The reform focuses on being more reflective of modern cows’ ability to produce greater fat and protein amounts; updating the cost support processors receive for cheese, butter, nonfat dry milk, and dried whey; and updating the way Class 1 is valued, among other changes. In theory, these changes would put milk pricing in line with the cost of production across the country.

The US Department of Agriculture is also providing support for four Dairy Business Innovation Initiatives to help dairy farmers find ways to keep their operations going for future generations through grants, research support, and technical assistance.

Another way to boost local dairies is to buy directly from a farmer. Value-added or farmstead dairy operations that make and sell milk and products such as cheese straight to customers have been growing. These operations come with financial risks for the farmer, however. Being responsible for milking, processing, and marketing your milk takes the already big job of milk production and adds two more jobs on top of it. And customers have to be financially able to pay a higher price for the product and be willing to travel to get it.

30 notes

·

View notes

Text

Frozen Food Market - Forecast (2022 - 2027)

Frozen Food market Overview:

According to the Food and Agriculture Organization of United Nations, nearly one third of the food produced every year amounting to roughly $680 billion (approximately 1.3 billion tons) gets either wasted, or lost[1]

. The issue of food wastage has given birth to the frozen food market which is experiencing a colossal growth with an increase in disposable income, and accentuated refrigeration technology. According to the analyst at Industry ARC, the global frozen food market size in 2018 stood between $225 billion to $228 billion. The market is estimated to grow steadily with a normal CAGR of 3.5%-5% during the forecast period of 2019-2025. Geographically, Europe led the frozen food market with a regional share of 30%-32% in 2018 owing to an increase in mergers and acquisitions between vendors and hypermarkets. On-the-go consumption of food is also driving the European frozen food market.

Frozen Food Market Outlook:

The prospect for frozen food market has never seemed brighter. With a growing awareness in food trends, consumers are resorting to cooking fresh meals at home which are free from any preservatives. For this, they require frozen foods which come in extensive categories these days, some of which are dairy-free, vegan, gluten-free, sugar-free, low fat, etc. Availability of high quality frozen foods makes market growth easier, and less prone to negative fluctuation. Recent trends in technology have introduced cryogenic freezing which prevents addition of any artificial preservatives, while maintaining negligible growth of microorganisms at the same time. Ready meals, a key segment of the frozen food market, is expected to grow at a standard CAGR of 2.5%-4%. It is a convenient, and accessible option for the working class society which is perpetually busy, and consistently short on time.

Request Sample

Frozen Food Market Growth Drivers:

An Increasing Demand for Preservative Free Food

With an increase in organic produce demand, consumers are incessantly on the lookout for fresh vegetables, seafood, and fruits that do not have a short shelf life. Since most of the organic produce expires quickly, hypermarkets are resorting to freezing of frozen foods which customers are interested in buying. Cryogenic freezing of food items extends their shelf lives, and makes them free from any added preservatives. Consumers flock towards these products, and help frozen food market in attaining noticeable growth.

The Shopping Trends of Millennials

Contrary to popular beliefs on millennials being irresponsible buyers, frozen food market heavily relies on their purchasing trends. Millennials are ready to experiment, and invest on novel things unlike the generation before them. They also tend to buy products that preserve their time, and are easy to handle. These traits fuel the market growth of frozen foods as they are convenient, and ready to use, exactly how millennials might prefer. This generation, which drowns in student debts, and underpaying jobs relies majorly on the frozen food market for their nutritional needs.

Frozen Food Market Challenges:

One of the basic challenges faced by the frozen food market is the lack of a proper supply chain system, and the consistent fear of cold chain systems failing. Since frozen foods require a set optimum temperature around -18°C, even the slightest failure in cold chain system can result in massive wastage. A thoroughly functioning power backup, and consistent vigilance is required for assuring negligible frozen food loss.

Inquiry Before Buying

Frozen Food Market Key Players Perspective:

According to the analyst at IndustryArc, some of the key players in the frozen food market are Nestle SA, Unilever, Kellogg Company , General Mills Inc, Conagra Brands, Inc., Grupo Bimbo S.A.B. de C.V., McCain Foods Limited , Kraft Heinz Company, and Associated British.

In 2018, after recognizing the frozen food preference patterns of millennials, and losing out to rivals like LeanMeals, Nestle increased production in its US factories, and introduced a plethora of items in its lineup like frozen coconut chickpea curry, and sweet earth lover’s veggie pizza[2]

Frozen Food Market Trends:

Improved Supply Chain Management

In order to make sure that the frozen food market continues to grow, and is not obstructed by food wastage, companies are employing an ameliorated supply chain management system. Reefer trucks are being used to consistently maintain an optimum environment for frozen foods to stay fresh. These trucks are now being fitted with third party GPS technologies for timely deliveries. This being a primary market disruption, is driving the growth of frozen food market in a positive direction.

The Rise Of IQF Food

IQF stands for ‘individually quick frozen’ which implies that all the items in a frozen food packet are frozen individually, and not as a block. The method involves passing of every individual piece of food through a blast chiller on a conveyor belt. This assures freshness in the food items even after thawing. An amount of peas for example, if frozen using IQF technique and packed in a carton, lidded tray, or crystallized PET tray will sell faster owing to its freshness as compared to the one frozen using ordinary refrigerant technique.

Schedule a Call

Frozen Food Market Research Scope:

The base year of the study is 2018, with forecast done up to 2025. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. It also provides information on unit shipments. These provide the key market participants with the necessary business intelligence and help them understand the future of the frozen food market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats. The key areas of focus include the types of cheese in the frozen food market, and their specific applications in different areas.

Buy Now

Frozen Food market Report: Industry Coverage

Frozen food market can be segmented on the basis of type, and distribution channels. Based on distribution channels, the market can be divided into supermarkets, hypermarkets, online stores, and convenience stores. On the basis of type, the market can be bifurcated into ready to eat meals, seafood, vegetables, fruits, etc.

The frozen food market report also analyzes the major geographic regions for the market as well as the major countries for the market in these regions. The regions and countries covered in the study include:

North America: The U.S., Canada, Mexico

South America: Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, Costa Rica

Europe: The U.K., Germany, Italy, France, The Netherlands, Belgium, Spain, Denmark

APAC: China, Japan, Australia, South Korea, India, Taiwan, Malaysia, Hong Kong

Middle East and Africa: Israel, South Africa, Saudi Arabia

For more Food and Beverage Market related reports, please click here

#frozen food market price#frozen food market size#frozen food market share#frozen food market forecast#frozen food market report

2 notes

·

View notes

Text

The global Pharmaceutical Logistics Market is projected to grow from USD 99,675 million in 2024 to USD 189,329 million by 2032, registering a compound annual growth rate (CAGR) of 8.35%. The pharmaceutical logistics market plays a critical role in the global healthcare sector, ensuring that medicines, vaccines, and other healthcare products are delivered safely and efficiently from manufacturers to end-users. This market has seen rapid growth due to the increasing demand for pharmaceuticals, the expansion of healthcare services, and the need for specialized logistics services to handle sensitive medical products. However, the sector faces several challenges, including stringent regulatory requirements, temperature control management, and supply chain disruptions. This article will delve into the key trends, drivers, and challenges of the pharmaceutical logistics market.

Browse the full report at https://www.credenceresearch.com/report/pharmaceutical-logistics-market

Key Trends in Pharmaceutical Logistics

1. Growing Demand for Biologics and Vaccines

The rise in biologics, vaccines, and complex therapies has spurred the need for specialized logistics services. These products are highly sensitive and require strict temperature control, often within cold chains, to maintain their efficacy. As more biologic-based drugs enter the market, pharmaceutical companies are investing in advanced logistics solutions that can meet the needs of these delicate products.

2. Advancement in Cold Chain Logistics

Cold chain logistics, which refers to the transportation of temperature-sensitive products, has become a significant segment in pharmaceutical logistics. With the rising demand for vaccines, particularly in the wake of the COVID-19 pandemic, the focus on maintaining appropriate temperature conditions during transportation has intensified. Innovations like real-time monitoring systems, temperature-controlled packaging, and advanced refrigeration technologies are helping to ensure that products reach their destinations without compromise.

3. Automation and Digitalization

Technology is transforming the logistics landscape, and the pharmaceutical sector is no exception. Automation, artificial intelligence (AI), and the Internet of Things (IoT) are being increasingly used to enhance operational efficiency, optimize routes, and provide real-time tracking of shipments. Digital platforms are streamlining the supply chain, reducing human error, and ensuring compliance with strict regulations.

4. Increased Regulatory Scrutiny

The pharmaceutical industry is highly regulated due to the critical nature of its products. Regulatory bodies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) impose stringent guidelines on how drugs should be stored, transported, and delivered. Compliance with these regulations is essential for pharmaceutical companies and their logistics partners. As a result, logistics providers must stay updated with changing regulations to avoid penalties and ensure the safety of pharmaceutical products.

Key Drivers of Market Growth

1. Global Demand for Pharmaceuticals

The growing global population, rising life expectancy, and increasing prevalence of chronic diseases are driving the demand for pharmaceuticals. This growth, in turn, creates a higher demand for reliable logistics services that can ensure the timely and safe delivery of healthcare products to various regions worldwide. Emerging markets, particularly in Asia-Pacific, Latin America, and Africa, are seeing an increase in healthcare expenditure, further fueling market expansion.

2. COVID-19 Pandemic Impact

The COVID-19 pandemic highlighted the importance of efficient pharmaceutical logistics. The global rollout of COVID-19 vaccines required complex logistics arrangements, including cold chain management, transportation to remote areas, and real-time tracking of vaccine deliveries. The pandemic underscored the need for resilient supply chains and innovative logistics solutions to meet the challenges of distributing medical products on a massive scale.

3. Outsourcing Trends

Many pharmaceutical companies are increasingly outsourcing their logistics functions to third-party logistics (3PL) providers. By outsourcing, companies can focus on their core competencies while leveraging the expertise and infrastructure of specialized logistics firms. This trend is driving growth in the pharmaceutical logistics market, as more companies seek cost-effective and efficient logistics solutions.

Challenges in the Pharmaceutical Logistics Market

1. Temperature Sensitivity and Cold Chain Failures

One of the most significant challenges in pharmaceutical logistics is maintaining the correct temperature during transportation. Temperature excursions can lead to product spoilage, resulting in financial losses and potentially putting patients at risk. Cold chain failures are particularly costly, and ensuring that logistics systems are reliable and robust is essential.

2. Supply Chain Disruptions

Global supply chain disruptions, such as those caused by natural disasters, geopolitical tensions, or pandemics, can significantly impact the pharmaceutical logistics market. These disruptions can delay the delivery of life-saving medications, leading to shortages and potentially harming patients. Logistics providers must have contingency plans in place to mitigate the effects of such disruptions.

3. High Operational Costs

Managing the logistics of pharmaceutical products, especially cold chain products, comes with high operational costs. Specialized packaging, real-time monitoring systems, and the need for constant temperature control contribute to these expenses. Logistics providers are under pressure to balance cost efficiency with quality and compliance.

Key Player Analysis:

Top Key Players

DHL Supply Chain & Global Forwarding

Kuehne + Nagel International AG

FedEx Corporation

United Parcel Service (UPS), Inc.

DB Schenker

AmerisourceBergen Corporation

SF Express

Ceva Logistics

Panalpina Group

XPO Logistics

Segmentations:

By Type

Cold Chain Logistics

Non-cold Chain Logistics

By Component

Storage

Warehouse

Refrigerated container

Transportation

Sea freight Logistics

Airfreight Logistics

Overland Logistics

Monitoring components

Hardware

Sensors

RFID Devices

Telematics

Networking Devices

Software

By Application

Bio Pharma

Chemical Pharma

Speciality Pharma

By Procedure

Picking

Storage

Retrieval Systems

Handling Systems

By Region

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/pharmaceutical-logistics-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Exploring the Europe HVAC Industry: Trends, Challenges, and Future Prospects

The Heating, Ventilation, and Air Conditioning (HVAC) industry in Europe is undergoing a significant transformation, driven by technological advancements, sustainability initiatives, and changing consumer demands. The Europe HVAC Market is estimated to reach USD 28.67 billion in 2024 and is projected to grow to USD 38.75 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.20% during the forecast period. As Europe focuses on reducing carbon emissions and improving energy efficiency, the HVAC market is poised for robust growth. In this blog, we will delve into the current landscape of the European HVAC industry, key trends shaping its future, and the challenges it faces.

Current Landscape of the Europe HVAC Industry

The European HVAC market encompasses a wide range of systems and technologies designed for heating, cooling, and ventilation in residential, commercial, and industrial applications. The industry's growth is primarily fueled by the increasing demand for energy-efficient and sustainable HVAC solutions, spurred by regulatory frameworks aimed at reducing greenhouse gas emissions.

Recent market research indicates that the European HVAC industry is expected to experience significant growth over the next few years, driven by advancements in technology, increased awareness of indoor air quality, and a growing emphasis on sustainable building practices.

Key Trends in the European HVAC Market

Focus on Energy Efficiency: Energy efficiency is a top priority in the European HVAC market, with regulations such as the Energy Performance of Buildings Directive (EPBD) encouraging the adoption of high-efficiency systems. Manufacturers are developing innovative products that reduce energy consumption and operating costs, catering to both residential and commercial sectors.

Integration of Smart Technologies: The rise of smart homes and buildings has led to the integration of advanced technologies in HVAC systems. Smart thermostats, IoT-enabled devices, and automation solutions are enhancing user comfort and energy management, allowing consumers to monitor and control their HVAC systems remotely.

Emphasis on Indoor Air Quality (IAQ): The COVID-19 pandemic has heightened awareness of indoor air quality, prompting consumers and businesses to prioritize ventilation and air purification systems. The demand for HVAC solutions that improve IAQ, such as advanced filtration systems and air purifiers, is on the rise.

Sustainability and Green Solutions: With the European Union's commitment to achieving carbon neutrality by 2050, the HVAC industry is increasingly focused on sustainable practices. Manufacturers are investing in eco-friendly refrigerants, heat pumps, and renewable energy integration to align with sustainability goals.

Challenges Facing the Europe HVAC Industry

While the European HVAC market presents numerous opportunities, it also faces several challenges:

Regulatory Compliance: The HVAC industry must navigate complex regulations and standards related to energy efficiency, emissions, and refrigerants. Staying compliant while innovating can be a daunting task for manufacturers.

Supply Chain Disruptions: Recent global events, including the COVID-19 pandemic, have exposed vulnerabilities in supply chains, affecting the availability of critical components and materials needed for HVAC systems. Addressing these disruptions is essential for maintaining production and meeting market demands.

Skill Shortages: As the HVAC industry evolves with new technologies, there is a growing need for skilled professionals. The shortage of trained technicians and engineers poses a challenge for companies looking to implement and maintain advanced HVAC systems.

Outlook

The future of the European HVAC industry looks promising, with strong growth potential driven by increasing consumer awareness, regulatory support, and technological advancements. As the market evolves, companies that prioritize innovation, sustainability, and customer-centric solutions will likely emerge as leaders in the industry.

Investments in research and development will be crucial for manufacturers to create cutting-edge products that meet the evolving needs of consumers while adhering to stringent environmental standards. The integration of smart technologies and a focus on energy efficiency will continue to shape the industry's landscape.

Conclusion

The European HVAC industry is at a pivotal moment, influenced by a myriad of factors including regulatory changes, technological advancements, and a growing emphasis on sustainability. As the market continues to evolve, stakeholders must navigate the complexities while capitalizing on emerging opportunities. By embracing innovation and sustainability, the European HVAC industry can contribute significantly to the region's energy efficiency goals and enhance the comfort of indoor environments.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence https://www.mordorintelligence.com/industry-reports/europe-hvac-equipment-market

#marketing#europe hvac market#europe hvac market size#europe hvac market share#europe hvac market trends#europe hvac market growth#europe hvac market report#europe hvac market analysis

0 notes

Text

Industry Outlook of Fuel Cell Market 2023 Trends to 2030

Fuel Cell Industry Overview

The global fuel cell market size was estimated at USD 7.35 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 27.1% from 2024 to 2030. Increasing demand for unconventional energy sources is one of the key factors driving the growth. Growing private-public partnerships and reduced environmental impact are expected to propel the demand. Governments across the globe are anticipated to supplement the developments by offering support in different forms, including funding R&D activities and funding suitable financing programs. Building a robust regulatory framework is vital as government enterprises need to provide an environment that is favorable for investment.

Gather more insights about the market drivers, restrains and growth of the Fuel Cell Market

Most of the U.S. states, such as California and New York, have set mandates to limit the carbon emissions from commercial and industrial end users in the country. This has resulted in end users opting for clean energy technologies to comply with the mandate and limit their carbon footprint. Bloom Energy, one of the major fuel cell vendors in the U.S., provides its bloom energy servers for power generation application to aid commercial and industrial end users limit their carbon footprint.

For instance, in September 2023, FuelCell Energy, Inc. and Toyota Motor North America announced the completion of Tri-gen system at Toyota's Port of Long Beach operations. Tri-gen is an example of FuelCell Energy's ability to scale hydrogen-powered fuel cell technology. Such innovative ideas is expected to foster the demand of fuel cell market over forecast period.

Fuel cell market is a rapidly growing sector with a wide range of potential opportunities. The technology is constantly improving, with new materials and designs leading to increased efficiency and performance. This is making fuel cells more attractive for a wider range of applications. Transportation sector is one of the largest markets for fuel cells. Fuel cell electric vehicle (FCEVs) offer several advantages over battery-electric vehicles (BEVs), such as longer range and faster refueling times. As the cost of FCEVs comes down and the hydrogen infrastructure grows, the market for fuel cell vehicles is expected to boom. Companies operating in the market continuously launch new products in order to pace up with the growing fuel cell technology. For instance, in January 2024, Nikola Corporation launched 42 and wholesaled 35 Class 8 Nikola hydrogen-powered fuel cell electric vehicles (FCEVs) under HYLA brand for U.S. and Canada customers. The trucks are featured to run with a range of 500 miles with an estimated fueling time as low as 20 minutes.

Browse through Grand View Research's Power Generation & Storage Industry Research Reports.

• The global battery market size was estimated at USD 118.20 billion in 2023 and is projected to grow at a CAGR of 16.1% from 2024 to 2030. The market is experiencing rapid growth, driven primarily by the increasing adoption of electric vehicles (EVs) and the expansion of renewable energy infrastructure.

• The global refrigerant market size was estimated at USD 14.26 billion in 2023 and is projected to grow at a CAGR of 4.7% from 2024 to 2030.The industry is experiencing growth due to increased demand from various end-use sectors, particularly the commercial & industrial refrigeration industry.

Fuel Cell Market Segmentation

Grand View Research has segmented the global fuel cell market report based on product, components, fuel, size, application, and end-use, and region:

Fuel Cell Product Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• PEMFC

• PAFC

• SOFC

• MCFC

• AFC

• Others

Fuel Cell Components Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• Stack

• Balance of Plant

Fuel Cell Fuel Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• Hydrogen

• Ammonia

• Methanol

• Ethanol

• Hydrocarbon

Fuel Cell Size Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• Small-scale

• Large-scale

Fuel Cell Application Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• Stationary

• Transportation

• Portable

Fuel Cell End-use Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• Residential

• Commercial & Industrial

• Transportation

• Data Centers

• Military & Defense

• Utilities & Government

Fuel Cell Regional Outlook (Volume, Units; Capacity, MW, Revenue, USD Million, 2018 - 2030)

• North America

o US

o Canada

o Mexico

• Europe

o Germany

o France

o UK

o Italy

o Spain

• Asia Pacific

o China

o Japan

o South Korea

o India

o Taiwan

o Australia

• Central & South America

o Brazil

o Argentina

• Middle East & Africa

o Saudi Arabia

o UAE

o South Africa

Order a free sample PDF of the Fuel Cell Market Intelligence Study, published by Grand View Research.

Key Companies profiled:

• Ballard Power Systems

• Bloom Energy

• Ceres Power Holdings PLC

• Doosan Fuel Cell America, Inc.

• FuelCell Energy, Inc.

• Hydrogenics Corporation

• Nedstack Fuel Cell Technology B.V.

• Nuvera Fuel Cells LLC

• Plug Power, Inc.

• SFC Energy AG

Key Fuel Cell Company Insights

• In November 2023, Honda in association with General Motors displayed a prototype of its next-generation hydrogen fuel cell system at European Hydrogen Week in Brussels. The company is planning to expand its portfolio in fuel cell technology.

• In December 2023, General Motors and Komatsu announced to develop a hydrogen fuel cell power module for the Japanese construction machinery maker's 930E electric drive mining truck.

• In January 2023, Cochin Shipyard Limited initiated research activities for the development of a hydrogen-fueled electric vessel based on low-temperature proton exchange membrane technology.

• In January 2023, Advent Technologies collaborated with Alfa laval to explore the application of high-temperature proton exchange membrane fuel cells in marine applications.

0 notes

Text

2024-2030: Air Conditioning Compressor for New Energy Vehicle Market Trend And Analysis

On 2024-9-24 Global Info Research released【Global Air Conditioning Compressor for New Energy Vehicle Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030】. This report includes an overview of the development of the Air Conditioning Compressor for New Energy Vehicle industry chain, the market status of Consumer Electronics (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), Household Appliances (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), and key enterprises in developed and developing market, and analysed the cutting-edge technology, patent, hot applications and market trends of Air Conditioning Compressor for New Energy Vehicle.

The air-conditioning compressor for new energy vehicles is a key component designed specifically for electric vehicles and other new energy vehicles. It is the power source of the vehicle's air-conditioning refrigeration system and promotes the circulation of refrigerant in the system.

The global Air Conditioning Compressor for New Energy Vehicle market size is expected to reach $ million by 2030, rising at a market growth of %CAGR during the forecast period (2024-2030).

This report studies the global Air Conditioning Compressor for New Energy Vehicle production, demand, key manufacturers, and key regions.

This report is a detailed and comprehensive analysis of the world market for Air Conditioning Compressor for New Energy Vehicle and provides market size (US$ million) and Year-over-Year (YoY) Growth, considering 2023 as the base year. This report explores demand trends and competition, as well as details the characteristics of Air Conditioning Compressor for New Energy Vehicle that contribute to its increasing demand across many markets.

Market segment by Type: <34cc、34-45cc、>45cc

Market segment by Application:Passenger Car、Commercial Vehicle

Major players covered: Toyota Industries、Hanon Systems、Valeo、MAHLE、Sanden、Brose、Denso、Highly Marelli、Aotecar、Suzhou Zhongcheng New Energy、Shanghai Highly、Zhengzhou Yuebo New Energy、Welling Auto Parts、Shanghai Velle Automobile Air Conditioner、Songz Automobile Air Conditioning、Panasonic Corporation、Mitsubishi、Huaqiang Electric

Market segment by region, regional analysis covers: North America (United States, Canada and Mexico), Europe (Germany, France, United Kingdom, Russia, Italy, and Rest of Europe), Asia-Pacific (China, Japan, Korea, India, Southeast Asia, and Australia),South America (Brazil, Argentina, Colombia, and Rest of South America),Middle East & Africa (Saudi Arabia, UAE, Egypt, South Africa, and Rest of Middle East & Africa).

The content of the study subjects, includes a total of 15 chapters:

Chapter 1, to describe Air Conditioning Compressor for New Energy Vehicle product scope, market overview, market estimation caveats and base year.

Chapter 2, to profile the top manufacturers of Air Conditioning Compressor for New Energy Vehicle, with price, sales, revenue and global market share of Air Conditioning Compressor for New Energy Vehicle from 2019 to 2024.

Chapter 3, the Air Conditioning Compressor for New Energy Vehicle competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast.

Chapter 4, the Air Conditioning Compressor for New Energy Vehicle breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030.

Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030.

Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Air Conditioning Compressor for New Energy Vehicle market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030.

Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis.

Chapter 13, the key raw materials and key suppliers, and industry chain of Air Conditioning Compressor for New Energy Vehicle.

Chapter 14 and 15, to describe Air Conditioning Compressor for New Energy Vehicle sales channel, distributors, customers, research findings and conclusion.

Data Sources:

Via authorized organizations:customs statistics, industrial associations, relevant international societies, and academic publications etc.

Via trusted Internet sources.Such as industry news, publications on this industry, annual reports of public companies, Bloomberg Business, Wind Info, Hoovers, Factiva (Dow Jones & Company), Trading Economics, News Network, Statista, Federal Reserve Economic Data, BIS Statistics, ICIS, Companies House Documentsm, investor presentations, SEC filings of companies, etc.

Via interviews. Our interviewees includes manufacturers, related companies, industry experts, distributors, business (sales) staff, directors, CEO, marketing executives, executives from related industries/organizations, customers and raw material suppliers to obtain the latest information on the primary market;

Via data exchange. We have been consulting in this industry for 16 years and have collaborations with the players in this field. Thus, we get access to (part of) their unpublished data, by exchanging with them the data we have.

From our partners.We have information agencies as partners and they are located worldwide, thus we get (or purchase) the latest data from them.

Via our long-term tracking and gathering of data from this industry.We have a database that contains history data regarding the market.

Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provides market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Phase Change Material Market Size, Share, Trends & Forecast

According to a new report by Univdatos Market Insights, the Global Phase Change Material Market is expected to reach USD 6,934.49 million in 2032, growing at a CAGR of 20.45%. The market is driven by the rising application in building and construction, increasing demand for HVAC systems, and the growing need for energy-efficient solutions in various industries.

Demand:

The PCM market is growing globally, which can be attributed to several factors increasing the demand for PCM. Firstly, the market has been highly affected by the demand to embrace energy efficiency and sustainability in the construction of buildings. Enhancing the use of PCM in building materials has the following benefits: It enables the control of indoor temperatures, thus espousing heating and cooling, leading to energy conservation. This corresponds to the worldwide practice of promoting sustainable building to maintain green certifications.

Also, with the increasing reliability of the electronics and transport sector, the need for enhanced thermal management has increased. PCMs can be utilized in electronics where miniaturization may lead to the generation of heat and thus aid in reducing heat and possibly improving the efficiency and durability of the devices. In the case of automobiles, the PCMs can be employed in batteries and the climate control of cabins and car interiors to make them more energy-friendly.

Applications:

The market for PCMs is active due to their versatility and ability to be used across many industries. In the building and construction field, they are incorporated into the wallboards, floor, and ceiling to act as thermal mass control of internal environment temperatures. Some benefits of this application include the ability to minimize energy expenses while improving occupant comfort.

In the heating refrigeration and ventilation industry, PCMs are utilized in refrigeration systems by depositing and liberating thermal energy in air conditioning. PCMs render cold chain logistics a convenient way of transferring temperature-sensitive commodities like pharmaceuticals and foods to their intended destinations while maintaining the set temperatures.

In the construction sector, they are used for HVAC systems, building insulation, and energy storage, as well as thermal management solutions applied in electronics like laptops, smartphones, and data centers. Furthermore, in the automobile segment, PCMs are also employed in battery thermal management and cabin thermal regulation, which leads to fuel productivity and a cozy climate for the passengers.

Request Free Sample Pages with Graphs and Figures Here https://univdatos.com/get-a-free-sample-form-php/?product_id=63882

Technological Advancements:

There is increased research on the PCM market and the development of technologies by many industry players for new, innovative, and green products. The following are some of the new directions that are worth mentioning: bio-based and non-toxic PCMs. Industry players are using funds to work on PCMs that are bio-based. This is in a bid to meet sustainable development goals.

For instance, Rubitherm Technologies recently launched an enhanced PCM range made from natural oils, a better option than petroleum-based PCMs. These bio-based PCMs have thermal characteristics comparable to those of more conventional materials but with much regard for the environment.

Conclusion:

PCM industry remains highly promising for considerable growth in the future because of the growing requirements for energy-saving and efficient solutions in various sectors. The increasing demand for better thermal management in building and construction, electronics, and automotive industries will drive the growth of the PCM market. Manufacturers are still focusing on new opportunities and increasing their product offerings to better serve the needs of these sectors. The growth of new technologies and the invention of environmentally friendly PCMs also continue to fuel product demand in line with global progress.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

0 notes

Text

Refrigerated Warehousing And Storage Market 2024-2033 : Demand, Trend, Segmentation, Forecast, Overview And Top Companies

The refrigerated warehousing and storage global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Refrigerated Warehousing And Storage Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size -

The refrigerated warehousing and storage market size has grown strongly in recent years. It will grow from $172.31 billion in 2023 to $187.87 billion in 2024 at a compound annual growth rate (CAGR) of 9.0%. The growth in the historic period can be attributed to globalization of the food supply chain, consumer demand for fresh products, e-commerce and online grocery shopping, pharmaceutical supply chain requirements.

The refrigerated warehousing and storage market size is expected to see strong growth in the next few years. It will grow to $262.9 billion in 2028 at a compound annual growth rate (CAGR) of 8.8%. The growth in the forecast period can be attributed to population growth and urbanization, sustainability and energy efficiency, economic growth in emerging markets, climate change and extreme weather events. Major trends in the forecast period include technology integration, energy efficiency and sustainability, e-commerce and last-mile delivery, cold storage for e-pharmacies.

Order your report now for swift delivery @

https://www.thebusinessresearchcompany.com/report/refrigerated-warehousing-and-storage-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers -

Warehouses are increasingly using mobile technologies to efficiently monitor warehouse operations. Mobile technology includes the use of tablets, smartphones, mobile printers, and other handheld devices for communication and information. These devices make use of GPS, RFID, VoIP, digital imaging, and voice technology. Technicians operating forklifts and automated material handling equipment in a warehouse are using mobile technologies to obtain information on troubleshooting, repairs, and work orders. This gives warehouse managers access to equipment status and performance reports and enables them to track warehouse operations around the clock. Wearable technology such as smart glasses is being integrated with warehouse management systems to improve hands-free mobility for workers. According to a report by MHI, a material handling, logistics, and supply chain association, 22% of the respondents use mobile technologies in warehouses, and the adoption rate is expected to reach 45% in the next two years.

The refrigerated warehousing and storage market covered in this report is segmented –

1) By Type: Cold Storage, Frozen Storage

2) By Ownership: Private Warehouses, Public Warehouses, Bonded Warehouses

3) By Application: Fruits and Vegetables, Bakery and Confectionery, Milk and Dairy Products, Meat, Seafood, Beverages, Other Applications

Get an inside scoop of the refrigerated warehousing and storage market, Request now for Sample Report @

https://www.thebusinessresearchcompany.com/sample.aspx?id=2256&type=smp

Regional Insights -

Asia-Pacific was the largest region in the refrigerated warehousing and storage market in 2023. North America was the second largest region in the refrigerated warehousing and storage market. The regions covered in the refrigerated warehousing and storage market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, and Africa.

Key Companies -

Major companies operating in the refrigerated warehousing and storage market include AmeriCold Logistics, Nichirei Corporation, Lineage Logistics Holdings LLC, Henningsen Cold Storage Co., Burris Logistics, Toyo Suisan Kaisha Ltd., Agro Merchants North America Holdings LLC, Nippon Suisan Kaisha Ltd., Snowman Logistics Ltd., Lineage Logistics, Americold Reality Trust Inc., United States Cold Storage Inc., NewCold Cooperatief U.A., Nichirei Logistics Group Inc., Emergent Cold LatAm Management LLC, Interstate Warehousing Inc., Frialsa Frigorificos S.A. De C.V., Constellation Cold Logistics, Superfrio Logistica Frigorificada, FreezPak Logistics, Conestoga Cold Storage Limited, Congebec Logistics Inc., METCOLD Supply Network Management Limited, RLS Logistics, Friozem Armazens Frigorificos Ltda., Magnavale Ltd., Confederation Freezers, Trenton Cold Storage Inc., Nor-Am Cold Storage, Burris Logistics, Agri-Norcold A/S, Vertical Cold Storage, ColdPoint Logistics, Hanson Logistics Ltd., Cloverleaf Cold Storage Co., Henningsen Cold Storage Co., Gruppo Marconi Logistica Integrata, Zero Mountain Inc.

Table of Contents

1. Executive Summary

2. Refrigerated Warehousing And Storage Market Report Structure

3. Refrigerated Warehousing And Storage Market Trends And Strategies

4. Refrigerated Warehousing And Storage Market – Macro Economic Scenario

5. Refrigerated Warehousing And Storage Market Size And Growth

…..

27. Refrigerated Warehousing And Storage Market Competitor Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

30. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www

0 notes

Text

Global Green Hydrogen Market: Growth Opportunities and Technological Barriers

According to a new report published by Allied Market Research, the green hydrogen market size was valued at $2.5 billion in 2022, and is estimated to reach $143.8 billion by 2032, growing at a CAGR of 50.3% from 2023 to 2032.

Green hydrogen, also known as renewable hydrogen, is a form of hydrogen produced using renewable energy sources, such as solar, wind, or geothermal power. Furthermore, the demand for proton exchange membrane electrolyzer is anticipated to witness growth during the forecast period, owing to economic growth in emerging markets continues to surge.

In 2023, Asia-Pacific accounts for the largest green hydrogen market share, followed by Europe and North America.

Major Companies

Green Hydrogen Systems, Air Liquide, Shell plc, Enapter S.r.l., Plug Power Inc., Ballard Power Systems, Linde plc, Reliance Industries, GAIL (India) Limited and Adani Green Energy Ltd.

The green hydrogen market is expected to be driven by factors such as the promising growth of the food and beverages, medical, chemical, and petrochemical industries.

Demand for power generation has escalated due to global population growth, coupled with urbanization and industrialization, leading to increase electricity consumption.

The food and beverage segment are projected to manifest a CAGR of 51.6% from 2023 to 2032, and has significant proportion in green hydrogen market size. Rise in the food and beverage industry significantly influences the green hydrogen market, primarily due to intensive energy demand of the industry.

Food and beverage production requires substantial energy for processing, packaging, refrigeration, and transportation. Green hydrogen presents a sustainable solution to meet these escalating energy demands, especially in processes were direct electrification not efficient.

Rise in living standards and technological advancements also contribute to higher energy needs, especially in emerging economies where electricity access has expanded rapidly.

Ongoing R&D efforts focus on enhancing electrolyzer efficiency, durability, and scaling up production, leading to cost reductions and improved performance. This trend aligns with ambitious governmental targets and corporate commitments aimed at fostering the green hydrogen industry, spurring innovation and market growth.

Increasingly stringent regulations and carbon pricing mechanisms incentivize to transition of industries into low-carbon alternatives, propelling its market penetration. These converging green hydrogen market trends collectively position green hydrogen as a pivotal player in the sustainable energy landscape, driving a fundamental shift toward cleaner, more resilient energy systems across the globe.

the electrification of transportation and heating sectors, driven by the push for cleaner energy sources, further amplifies the demand for power generation. This growth in demand provides a significant opportunity for the green hydrogen market.

Green hydrogen emerges as a versatile solution as traditional energy sources struggle to meet these escalating demands while maintaining environmental sustainability.

This symbiotic relationship between the rise in demand for power generation and the need for clean energy solutions positions green hydrogen as a key player in meeting the escalating energy needs sustainably.

The push toward decarbonization and the reduction of greenhouse gas emissions in the transportation sector amplifies the appeal of green hydrogen market opportunities.

Carbon Solutions, a greenhouse gas reduction consultancy, in May 2023, stated that less than 1% of the 10 million metric tons of hydrogen produced in the U.S. at present counts as green hydrogen. Instead, 76% is derived from natural gas or coal, and 23% is a by-product of petroleum refining or other chemical processes.

Globally, the hydrogen market is about 96 million metric tons per year. The report from Carbon Solutions puts number of electrolyzers operating in the U.S. at just 42, with a combined hydrogen production capacity of about 3,000 tons per year.

The U.S. Department of Energy (DOE) aims to have 10 million tons of clean hydrogen flowing per year by 2030, 20 million tons by 2040, and 50 million tons by 2050. About half that production is expected to come from renewably powered electrolysis. The U.S. government is projected to invest $8 billion in several hydrogen hubs across the country by 2026 and produce about 250 times as much hydrogen per day.

Trending Reports in Energy and Power Industry:

Electrolyzer Market Trend Analysis Report, by Application, by Capacity, by Product : Global Opportunity Analysis and Industry Forecast, 2023-2032

Renewable Energy Market Trend Analysis Report, by Type, by End Use : Global Opportunity Analysis and Industry Forecast, 2024-2033

Clean Energy Infrastructure Market Size, Share, Competitive Landscape and Trend Analysis Report, by Infrastructure Type, by End-Use : Global Opportunity Analysis and Industry Forecast, 2024-2033

About Us

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "Market Research Reports" and "Business Intelligence Solutions." AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

Pawan Kumar, the CEO of Allied Market Research, is leading the organization toward providing high-quality data and insights. We are in professional corporate relations with various companies and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

#energy#power#business#news#solar#green hydrogen#clean energy#renewableenergy#renewablepower#hydrogen electrolyzer market#electrolysis

0 notes

Text

The Future of Home Appliances: A Glimpse into 2030

As we approach the year 2030, the home appliance industry is poised for a transformative shift, driven by advancements in technology, sustainability, and personalization. Here's a glimpse into the exciting future of home appliances:

Smart Home Integration: The New Standard in 2030

By 2030, smart home integration will be the norm, with appliances seamlessly connecting to home automation systems. Imagine a refrigerator that not only tracks inventory but also suggests recipes based on available ingredients, sending instructions to a smart oven that preheats itself to the perfect temperature. Voice-activated controls and remote access via smartphones will make daily tasks effortless.

Advanced Features of Smart Appliances

- Inventory Management: Fridges will track what’s inside and suggest meals.

- Voice Control: Manage appliances hands-free with voice commands.

- Remote Access: Control your home devices from anywhere using your smartphone.

Energy Efficiency and Sustainability: A Green Future

Sustainability will be a key focus in the home appliances of the future. Eco-friendly materials, such as bamboo countertops and recycled glass backsplashes, will become increasingly popular. Energy-efficient appliances will be the standard, featuring innovations like solar-powered devices and advanced water filtration systems.

Eco-Friendly Living: Growing Your Own Food

Homeowners will be able to grow their own herbs and vegetables year-round using indoor gardens or hydroponic systems, promoting fresh, home-grown ingredients.

Personalization and AI: Tailoring Home Appliances to You

Artificial intelligence (AI) will revolutionize the way we interact with our home appliances. Smart ovens will suggest optimal cooking settings based on user preferences, while AI-driven thermostats will adjust temperatures to balance comfort with energy savings.

Healthier Living Through AI

- Personalized Recipes: Get suggestions tailored to your dietary needs.

- Health Monitoring: Appliances will help track and improve your health.

Compact and Multifunctional Designs: Maximizing Urban Living Spaces

As urban living spaces continue to evolve, compact and multifunctional appliances will become increasingly popular. Combination microwave-ovens and washer-dryer units will maximize functionality while minimizing space requirements.

The Rise of Minimalist Aesthetics

Minimalist aesthetics with clean lines and concealed storage solutions will create a sense of calm and organization in increasingly smaller living spaces.

Appliance Repair and Longevity: Ensuring Durability in High-Tech Homes

As home appliances become more advanced, the importance of reliable repair services will grow. Companies will offer extended warranties and specialized repair services to ensure that high-tech appliances remain functional for longer periods.

The Role of Repair in Sustainability

The ability to easily repair appliances will contribute to sustainability by reducing waste and extending their lifespan.

Smart Home Appliances Market Growth (2023-2030): What to Expect

The future of home appliances is an exciting prospect, with smart integration, sustainability, personalization, and compact designs shaping the industry. By embracing these trends, homeowners can create living spaces that are not only efficient and convenient but also aligned with their individual lifestyles and environmental values.

Read the full article

0 notes

Text

India's Dairy Industry Sees Surge in Milk Production Amid New Challenges

The dairy industry has always been a vital part of India’s agricultural sector, and recent developments indicate that it is poised for even more growth. With increasing demand for milk and dairy products both domestically and globally, the industry is taking significant steps to boost production and ensure sustainability. India remains the largest producer of milk in the world, with its dairy sector contributing significantly to the livelihoods of millions of farmers across the country. However, as the market continues to grow, new challenges are emerging that require attention from policymakers and industry leaders.

One of the most notable trends in dairy industry news is the increase in Indian milk production over the past year. According to recent reports, India’s milk output has grown by nearly 6% annually, reaching approximately 220 million metric tons in 2023. This surge is largely attributed to the adoption of advanced dairy farming techniques, improved animal husbandry, and better feed management practices. The government has also played a crucial role by introducing schemes aimed at modernizing dairy infrastructure, enhancing cold chain facilities, and providing financial assistance to small and marginal farmers.

Despite the increase in Indian milk production, the industry faces several challenges. One pressing issue is the rising cost of fodder and feed, which has put pressure on the profitability of dairy farmers. Climate change is another growing concern, as unpredictable weather patterns and extreme temperatures are affecting livestock health and milk yields. Furthermore, the industry is grappling with the need for more efficient logistics and distribution systems, especially in rural areas where access to quality refrigeration and storage facilities remains limited.

In response to these challenges, industry stakeholders are advocating for greater investment in research and development to enhance dairy farming practices and make them more resilient to climate change. Additionally, there is a growing focus on expanding export opportunities for Indian dairy products, particularly in Southeast Asia and the Middle East, where demand for high-quality milk products is on the rise.

Overall, while the Indian dairy industry continues to experience impressive growth, addressing these challenges will be critical to ensuring its long-term sustainability. As the sector evolves, it remains a crucial component of India’s economic fabric, supporting the livelihoods of millions and contributing to the nation’s food security.

0 notes

Text

Future Trends in Pet Care Products Market: Global Forecast

Overview of the Pet Care Products Market

In 2023, the pet care products market was estimated to be worth USD 216.73 billion. The market for pet care products is expected to expand at a compound annual growth rate (CAGR) of 6.31% between 2024 and 2032, from an estimated USD 228.44 billion in 2024 to USD 372.68 billion by 2032.

The global air conditioner (AC) market has experienced significant growth in recent years, driven by rising global temperatures, increasing urbanization, and growing consumer demand for energy-efficient cooling solutions. As consumers seek enhanced comfort and cooling technologies, the air conditioning industry is evolving to meet the changing needs of residential, commercial, and industrial sectors. This blog post explores key trends, drivers, and projections for the air conditioner market, with forecasts extending to 2030.

Key Drivers of Growth

Rising Global Temperatures: One of the most significant drivers of the air conditioner market is the rise in global temperatures due to climate change. As extreme heat events become more frequent, the demand for cooling solutions has surged, particularly in regions that experience prolonged periods of high temperatures. Countries in the Asia-Pacific region, the Middle East, and North America have witnessed increased demand for air conditioning units in both residential and commercial settings.

Urbanization and Infrastructure Development: The global trend of urbanization is contributing to the increased adoption of air conditioners. As more people move to cities and urban areas expand, there is a growing need for infrastructure that includes cooling systems. The rise in high-rise buildings, commercial complexes, and industrial facilities has led to a surge in demand for HVAC (heating, ventilation, and air conditioning) systems, including air conditioners. This trend is expected to continue as more emerging markets urbanize.

Energy Efficiency and Sustainability: Consumers and governments alike are placing greater emphasis on energy-efficient and eco-friendly cooling solutions. Air conditioning units are notorious for high energy consumption, but technological advancements have led to the development of energy-efficient models that comply with stricter energy regulations. In particular, smart air conditioners with advanced features like automated temperature control, energy-saving modes, and IoT (Internet of Things) integration are gaining popularity. These models not only reduce energy consumption but also lower operational costs for consumers.

Government Regulations and Incentives: Governments worldwide are implementing regulations and incentives to promote energy-efficient and environmentally friendly air conditioning systems. For example, the use of eco-friendly refrigerants, which have a lower impact on the ozone layer and global warming, is becoming more widespread. Additionally, governments are offering subsidies and tax incentives for individuals and businesses that invest in energy-efficient cooling systems, further boosting the market.

Market dynamics for Pet Care Products

Important market forces

Consumer spending on pet care goods is increasing due to the rising incidence of diseases in pets. The hygiene of the pets is maintained by the pet care items. These are high-quality products that safeguard the pet's skin, coat, and overall wellness. The demand is ultimately rising due to the increased knowledge of the need to prevent pet ailments. It is a key factor propelling the market expansion for pet care products over the predicted period. Additionally, pet adoption rates have gone up in a number of areas. These days, adopting a little pet is quite common. Another important element driving the growth of the pet care products market overall is the rising rate of pet adoption. The need for pet grooming, cleanliness, and care goods increases with pet adoption.

Opportunities for market expansion

Services for pet owners are developing in a number of areas. More people than ever are using mobile pet care services. Online pet care services allow owners with busy schedules to provide for their dogs. These quick examinations assist pet owners in selecting high-quality items for their animals. There are additional prospects for market expansion as people become more aware of pet care online services. Additionally, it is anticipated that in the projected year, the majority of pet owners will favor these mobile pet services. The market for pet care items is growing due to the rising incidence of automated products.

The limitations of the market

Pets benefit greatly from pet care items. They protect pets' hygienic conditions and well-being. These high-quality goods are pricey, too. The majority of pet owners believe that these supplies for pet care can be overpriced. Pet care supplies are still available at reasonable prices. Nonetheless, there is more advertising for pricey pet care items. Most pet owners are subjected to excessively expensive pet supplies. One of the main market restraints is cost. In addition, not enough people are aware of the advantages of pet care products. These things are not considered necessities for pets in many areas. Pets who use pet care products have healthier, longer lives. But many people are unaware of this advantage.

The difficulties in the market

Only in developed areas are pet care products seen as essential expenses. The developed area is aware of the various applications and advantages of pet care goods. The developing world is not aware of these products, though. One major issue facing the market is the underdeveloped region's lack of understanding about pet items. It is an important market challenge since it slows down the rate of market expansion. Additionally, during the projected period, it is a factor that may lower the market's total demand for pet care products.

Analysis of cumulative growth

In 2030, the market for pet care goods will rise steadily. During the projected period, the market as a whole will develop due to the critical drivers of the industry. The key factors driving the market are the rise in pet illnesses and consumer awareness. Nonetheless, a number of restrictions may prevent the industry from expanding. The market may be significantly impacted by the high cost of production. Another aspect that would impact market expansion is the underdeveloped region's lack of understanding regarding pet care goods. The factors driving market expansion will outweigh the effects of market limitations. As a result, the market's overall growth analysis appears favorable.

Market Trends

Shift Towards Smart Air Conditioners: Smart air conditioners are becoming a dominant trend in the market. These units offer remote control via smartphones, voice-activated commands, and integration with smart home ecosystems. They provide convenience, flexibility, and better energy management, allowing users to monitor and adjust their cooling systems even when they are away from home. This trend aligns with the broader shift towards smart home technology and connected devices.

Expansion of the Inverter AC Segment: Inverter air conditioners have gained popularity due to their energy efficiency and ability to maintain stable temperatures. Unlike traditional AC units that constantly turn on and off to regulate temperature, inverter ACs adjust the compressor speed according to the room’s cooling requirements. This results in lower energy consumption and longer-lasting performance, making them a preferred choice for consumers seeking energy savings and reduced electricity bills.

Growing Demand in Developing Economies: The demand for air conditioning systems is expanding rapidly in developing economies, particularly in the Asia-Pacific region, Africa, and Latin America. Rising disposable incomes, improving standards of living, and increasing access to electricity are key factors driving this trend. Countries such as India, China, Brazil, and Indonesia are expected to witness strong growth in air conditioner sales in the coming years as more households and businesses install cooling systems.

Environmentally Friendly Refrigerants: With increased focus on environmental sustainability, the market is seeing a shift toward the use of natural and eco-friendly refrigerants. Traditional refrigerants, such as hydrofluorocarbons (HFCs), have a high global warming potential. As a result, manufacturers are developing and adopting refrigerants like R-32 and R-290, which have a lower environmental impact. The adoption of these environmentally friendly refrigerants is anticipated to gain traction as consumers and governments prioritize green technologies.

Regional Analysis of the Pet Care Products Market

The markets for pet care goods are divided into the Middle East, South America, Asia Pacific, Europe, and North America. Over the course of the projection period, North America will dominate the rest of the market. The main motivator is awareness of veterinary health. Additionally, the areas have significant levels of consumer spending on pet supplies. The majority of the pet supplies in the area are pricey. Europe is renowned for having sizable marketplaces for pet supplies. The market for pet care items is diverse and offers a large selection of goods. During the projection period, the market growth is anticipated to reach its maximum rate. The third-largest market in the world, Asia Pacific, has a lot of promise.

For more information: https://www.marketresearchfuture.com/sample_request/842

Key Players of The Pet Care Product Market

PetSmart Inc. (US)

Petco Animal Supplies, Inc. (US)

General Mills, Inc. (US)

Mars, Incorporated (US)

Nestle S.A.(Switzerland)

Petmate Holdings Co. (US)

KONG Company (US)

Champion Petfoods LP (US)

Blue Pet Products, Inc. (US)

Colgate-Palmolive Company (US)

Unicharm Corporation (Japan)

About Market Research Future: