#asia-pacific cyber security market growth

Link

Asia Pacific Cybersecurity Market is poised to grow at a CAGR of 18.3 % by 2027. Factors driving the Asia Pacific Cybersecurity Market are increasing severity of these attacks and strict government laws.

#apac cyber security market#social media security market growth#asia-pacific cyber security market#asia pacific cyber security#social media security market#industrial cyber security market share#asia-pacific cyber security market growth

0 notes

Text

IoT Security Market Expansion Insights: Forecasting Growth from USD 22.3 Billion to USD 85.5 Billion by 2030

The IoT security market is poised for significant growth, with projections indicating an increase from USD 22.3 billion in 2023 to USD 85.5 billion by 2030, reflecting a compound annual growth rate (CAGR) of 21.2% during this period. This remarkable expansion is driven by the increasing prevalence of IoT devices and the corresponding rise in cyber threats targeting these interconnected systems.

Overview of the IoT Security Market

The Internet of Things (IoT) refers to the network of physical devices connected to the internet, enabling them to collect and exchange data. As IoT technology proliferates across various sectors, including healthcare, manufacturing, and smart homes, the need for robust security measures becomes paramount. IoT security encompasses a range of practices and technologies designed to protect these devices and the data they generate from unauthorized access and cyberattacks.

Access Full Report @ https://intentmarketresearch.com/latest-reports/iot-security-market-3033.html

Market Dynamics

Several factors are contributing to the growth of the IoT security market:

Rising Cyber Threats: The increasing number of cyberattacks targeting IoT devices has heightened awareness regarding the need for effective security solutions. Reports indicate a 400% increase in IoT-targeted cyberattacks in recent years, with manufacturing being one of the most affected sectors.

Regulatory Compliance: Governments worldwide are establishing stricter regulations regarding IoT security. For instance, the UK has mandated cybersecurity standards for IoT devices, and similar regulations are being considered in other regions.

Technological Advancements: Innovations in technologies such as artificial intelligence (AI), machine learning (ML), and advanced encryption methods are enhancing the capabilities of IoT security solutions, making them more effective against evolving threats.

Market Segmentation

The IoT security market can be segmented based on various criteria:

By Component

Solutions: This segment includes endpoint security, network security, application security, and cloud security.

Services: Managed services and professional services that support the implementation and maintenance of IoT security solutions.

By Deployment Type

Cloud-based Solutions: These offer flexibility and scalability, making them suitable for businesses with fluctuating needs.

On-premises Solutions: These provide a higher level of control and security but may require more resources for maintenance.

By Enterprise Size

Large Enterprises: Typically have more resources to invest in comprehensive security solutions.

Small and Medium Enterprises (SMEs): Often seek cost-effective solutions tailored to their specific needs.

By End-user Industry

Consumer IoT: Includes smart home devices like thermostats and security cameras.

Industrial IoT: Encompasses manufacturing equipment, supply chain logistics, and smart infrastructure.

Regional Analysis

North America

North America currently holds a significant share of the IoT security market due to its advanced technological infrastructure and high adoption rates of connected devices. The region is home to several key players in the cybersecurity space, including Cisco Systems and IBM.

Asia-Pacific

The Asia-Pacific region is expected to witness the highest growth rate during the forecast period. Countries like China, India, and Japan are investing heavily in smart city projects and industrial automation, driving demand for robust IoT security solutions. The region's rapid economic growth coupled with increasing awareness of cybersecurity threats further fuels this demand.

Europe

Europe is also experiencing substantial growth in its IoT security market as organizations across various sectors recognize the importance of securing their connected devices. The European Union's regulatory framework promoting cybersecurity standards is expected to bolster market growth further.

Key Players in the Market

Several notable companies are leading the charge in the IoT security market:

◘ Allot

◘ Check Point

◘ Cisco

◘ Fortinet

◘ IBM

◘ Intel

◘ Microsoft

◘ Palo Alto

◘ Thales

◘ Trend Micro

◘ Afero

◘ Bastille Networks

◘ Claroty

◘ Cybeats

◘ Nozomi Networks

◘ Nubeva Technologies

◘ SAM Seamless Network

◘ Xage Security

Download Sample Report @ https://intentmarketresearch.com/request-sample/iot-security-market-3033.html

Challenges Facing the Market

Despite its promising growth trajectory, the IoT security market faces several challenges:

Complexity of Security Solutions: Implementing comprehensive security measures can be complex due to the diverse nature of IoT devices and networks.

Cost Constraints for SMEs: Smaller enterprises may struggle to allocate sufficient budgets for robust security solutions.

Rapidly Evolving Threat Landscape: Cybercriminals are continuously developing new tactics to exploit vulnerabilities in IoT systems, necessitating constant updates to security protocols.

Future Trends

Looking ahead, several trends are likely to shape the future of the IoT security market:

Increased Adoption of AI and ML: These technologies will play a crucial role in enhancing threat detection capabilities and automating responses to potential breaches.

Focus on Data Privacy: As data breaches become more common, organizations will prioritize privacy protection measures alongside traditional security protocols.

Integration with Other Technologies: The convergence of IoT with blockchain technology could provide enhanced data integrity and transparency, further securing connected systems.

Conclusion

The IoT security market is at a pivotal point, characterized by rapid growth driven by increasing device connectivity and rising cyber threats. With projections indicating an increase from USD 22.3 billion in 2023 to USD 85.5 billion by 2030 at a CAGR of 21.2%, stakeholders across industries must prioritize securing their IoT ecosystems. As technological advancements continue to evolve alongside regulatory pressures, organizations must remain vigilant and proactive in implementing robust security measures to safeguard their operations against emerging threats.The future landscape will likely be shaped by innovations that enhance connectivity while ensuring that robust cybersecurity practices are integrated into every layer of IoT deployment.

About Us

Intent Market Research (IMR) is dedicated to delivering distinctive market insights, focusing on the sustainable and inclusive growth of our clients. We provide in-depth market research reports and consulting services, empowering businesses to make informed, data-driven decisions.

Our market intelligence reports are grounded in factual and relevant insights across various industries, including chemicals & materials, healthcare, food & beverage, automotive & transportation, energy & power, packaging, industrial equipment, building & construction, aerospace & defense, and semiconductor & electronics, among others.

We adopt a highly collaborative approach, partnering closely with clients to drive transformative changes that benefit all stakeholders. With a strong commitment to innovation, we aim to help businesses expand, build sustainable advantages, and create meaningful, positive impacts.

Contact Us

US: +1 463-583-2713

0 notes

Text

The Power of Biometrics: Exploring Advanced Sensor Technologies

According to the report, the global biometric sensors market is projected to grow at a compound annual growth rate (CAGR) of 11% over the forecast period of 2022-2028. The market, which was valued at around USD 4,400 million in 2022, is expected to reach nearly USD 8,300 million by 2028, showcasing significant growth potential.

What Are Biometric Sensors?

Biometric sensors are advanced technologies that capture and analyze biological data to authenticate individuals based on unique physical characteristics. These sensors are widely used for applications such as fingerprint recognition, facial recognition, iris scanning, voice recognition, and vein pattern detection. They play a critical role in enhancing security, identity verification, and access control across various industries, including healthcare, finance, government, and consumer electronics.

Get Sample pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/877

Market Dynamics and Growth Drivers

The biometric sensors market is being driven by several key factors:

Increasing Demand for Secure Authentication: With the rise of cyber threats and data breaches, there is a growing demand for more secure authentication methods. Biometric sensors provide enhanced security by offering unique, non-replicable identification methods, making them crucial for industries such as banking, healthcare, and government services.

Expansion of Consumer Electronics: The widespread adoption of biometric sensors in smartphones, laptops, and wearable devices is fueling market growth. Consumers increasingly rely on biometric authentication for unlocking devices, making payments, and accessing personal data, boosting demand for these sensors in the consumer electronics sector.

Growth in Contactless Solutions: The COVID-19 pandemic accelerated the need for contactless solutions, further boosting the demand for biometric sensors, particularly in facial recognition and iris scanning technologies. As hygiene and safety remain a priority, these solutions are becoming more prevalent in public spaces, offices, and healthcare settings.

Government Initiatives and Regulations: Government initiatives around the world aimed at improving national security and implementing biometric-based identification systems, such as e-passports and national identity programs, are contributing to the market's growth.

Regional Analysis

North America: North America holds a significant share of the biometric sensors market, driven by technological advancements, widespread adoption in the healthcare and financial sectors, and government initiatives. The U.S. is a key contributor, with increasing use of biometric sensors in border control, law enforcement, and consumer electronics.

Europe: Europe is another prominent market for biometric sensors, with major countries such as the U.K., Germany, and France implementing biometric identification systems in public and private sectors. The region is also seeing strong growth in contactless biometric applications in response to the pandemic.

Asia-Pacific: The Asia-Pacific region is expected to witness the fastest growth, driven by the expanding adoption of biometric technologies in emerging markets such as China, India, and Japan. Government initiatives in India, such as the Aadhaar program, which relies on biometric authentication, are contributing to the market’s expansion.

Latin America, Middle East & Africa: These regions are gradually embracing biometric technologies, with applications ranging from secure banking to national identity verification systems. The growing focus on improving security in these regions will provide opportunities for market growth.

Competitive Landscape

The biometric sensors market is competitive, with several leading companies contributing to the sector’s growth. Key players include:

Apple Inc.: Known for incorporating biometric sensors into its range of consumer electronics, including iPhones and iPads, Apple is a significant player in the market.

NEC Corporation: A global leader in biometric solutions, NEC provides a range of biometric identification systems, including fingerprint and facial recognition technologies.

Thales Group: Thales offers a comprehensive suite of biometric solutions, with a focus on secure identification for government and law enforcement agencies.

Synaptics Incorporated: Specializes in biometric sensors for the consumer electronics market, with applications in smartphones, tablets, and laptops.

Fingerprint Cards AB: A major player in the fingerprint sensor market, Fingerprint Cards AB offers innovative solutions for smartphones, tablets, and access control systems.

Report Overview : https://www.infiniumglobalresearch.com/reports/global-biometric-sensors-market

Challenges and Opportunities

While the biometric sensors market holds great potential, it faces certain challenges:

Privacy Concerns: The collection and storage of biometric data raise privacy concerns among users, which could hinder market growth. Governments and organizations must address these concerns through robust data protection regulations.

High Implementation Costs: The initial cost of implementing biometric systems, especially in developing regions, can be a barrier to market growth. However, advancements in technology and increased adoption will likely drive down costs in the future.

On the other hand, the market offers several opportunities for growth:

Technological Advancements: Continued advancements in artificial intelligence (AI) and machine learning are improving the accuracy and efficiency of biometric sensors, leading to wider adoption across industries.

Expanding Applications: Beyond security and identification, biometric sensors are finding new applications in areas such as healthcare, where they can be used for patient identification, and in retail, where they enable personalized customer experiences.

Conclusion

The global biometric sensors market is on a steady growth trajectory, driven by increasing demand for secure authentication, the expansion of consumer electronics, and the growing adoption of contactless solutions. With a projected value of nearly USD 8,300 million by 2028, the market offers substantial opportunities for innovation and investment across various industries. As technological advancements continue to improve the capabilities of biometric sensors, the market is set to play a critical role in shaping the future of security and identification.

0 notes

Text

Distributed Denial-of-Service (DDoS) Protection Market: Competitive Landscape and Key Players

Introduction to Distributed Denial-of-Service (DDoS) Protection market

The Distributed Denial-of-Service (DDoS) Protection market is witnessing rapid growth as cyber threats escalate across industries. As businesses increasingly digitize, the demand for advanced security solutions to mitigate DDoS attacks is surging. DDoS attacks, which aim to disrupt service availability, have evolved in complexity and frequency, driving the need for multi-layered defense systems. Key players offer solutions ranging from cloud-based protection to on-premise services, catering to the diverse needs of enterprises, governments, and critical infrastructure sectors.

The Distributed Denial-of-Service (DDoS) Protection Market is Valued USD 4.1 billion in 2024 and projected to reach USD XX billion by 2030, growing at a CAGR of 14.3% During the Forecast period of 2024-2032. As global internet use and connected devices proliferate, industries face higher risks from sophisticated DDoS attacks. The market comprises cloud, hardware, and software solutions, designed to detect, absorb, and mitigate attacks in real time. Major sectors deploying these solutions include telecom, banking, healthcare, and e-commerce. Increasing awareness of cybersecurity, growing cloud adoption, and regulatory pressure propel market demand.

Access Full Report :https://www.marketdigits.com/checkout/113?lic=s

Major Classifications are as follows:

By Component

Hardware Solutions

Software Solutions

Mitigation Techniques

Network Layer

Null Routing

Sinkholing

Scrubbing

Application Layer

Domain Name System (DNS) routing

Border Gateway Protocol (BGP) routing

Services

Professional Services

Design and Implementation

Consulting and Advisory

Training and Education

Support and Maintenance

Managed Services

By Deployment Mode

On-Premises

Cloud

Hybrid

By Organization Size

Large Enterprises

SME’s

By Application

Network

Application

Database

Endpoint

By Vertical

BFSI

IT & Telecommunication

Education

Government and Defense

Retail

Healthcare

Manufacturing

Others

Key Region/Countries are Classified as Follows:

◘ North America (United States, Canada,)

◘ Latin America (Brazil, Mexico, Argentina,)

◘ Asia-Pacific (China, Japan, Korea, India, and Southeast Asia)

◘ Europe (UK,Germany,France,Italy,Spain,Russia,)

◘ The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South

Key Players of Distributed Denial-of-Service (DDoS) Protection market

NetScout, Akamai, Radware, Huawei Technology, Fortinet, Link11, Imperva, Cloudflare, BT, A10 Networks, Fastly, Nexusguard, Corero, RioRey, PhoenixNAP, Allot, StrataCore, Sucuri, Verisign, StackPath, Seceon, Haltdos, DDoS-Guard, Indusface, Activereach, Mlytics, and Others.

Market Drivers in Distributed Denial-of-Service (DDoS) Protection Market:

Several factors are propelling the growth of the DDoS Protection market:

Increased Cyber Threats: The rise in large-scale DDoS attacks targeting businesses of all sizes necessitates robust protection systems.

Digital Transformation: With cloud adoption accelerating, the need for secure, scalable protection has grown.

Government Regulations: Increasing regulatory requirements for data security encourage businesses to adopt DDoS protection solutions.

Market Challenges in Distributed Denial-of-Service (DDoS) Protection Market:

The DDoS protection market faces several key challenges:

Evolving Threat Landscape: Attackers continuously adapt, developing more sophisticated and varied attack strategies that make protection solutions complex.

Cost of Implementation: High initial costs and ongoing maintenance of DDoS protection solutions can deter smaller businesses from adopting them.

False Positives: DDoS protection systems must balance security and access, but overly aggressive filters can block legitimate traffic, negatively affecting user experience.

Market Opportunities in Distributed Denial-of-Service (DDoS) Protection Market:

Cloud-based Protection Solutions: Cloud-based DDoS protection offers scalability and flexibility, attracting companies with dynamic workloads and decentralized operations.

AI and Machine Learning: Integrating AI-driven analytics into DDoS protection can improve real-time detection and response to emerging threats.

SME Adoption: As DDoS solutions become more affordable, small and medium-sized enterprises (SMEs) represent a vast untapped market for vendors.

Conclusion:

The Distributed Denial-of-Service (DDoS) Protection market is positioned for robust growth, driven by increasing cyber threats and the expanding digital economy. Companies must continuously innovate to stay ahead of attackers, offering scalable, cost-effective solutions that meet regulatory and operational needs. Challenges such as cost and technical complexity remain, but advancements in AI, cloud solutions, and the growing awareness of cybersecurity's critical role present ample opportunities for vendors and businesses alike.

0 notes

Text

Automotive Cyber Security Market — Forecast(2024–2030)

Global automotive cyber security market size was valued at USD 3,090.6 million in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 20.93% from 2023 to 2030.

Download Sample

1. Introduction

The automotive industry is undergoing a significant transformation with the rise of connected vehicles, autonomous driving, and electric vehicles (EVs). This transformation brings a heightened risk of cyber threats, making automotive cybersecurity a critical area of focus. Automotive cybersecurity encompasses technologies and strategies designed to protect vehicles from hacking, data breaches, and other cyber threats.

2. Market Size and Growth

The automotive cybersecurity market has seen rapid growth due to increasing concerns over vehicle safety and data privacy. According to recent reports, the global automotive cybersecurity market is expected to grow from approximately $4.5 billion in 2023 to around $10 billion by 2028, at a compound annual growth rate (CAGR) of over 18%.

3. Key Drivers

Rise of Connected Vehicles: The increasing number of connected vehicles with internet access and in-vehicle networks heightens the risk of cyberattacks.

Autonomous Vehicles: The development of autonomous driving technologies requires robust cybersecurity measures to ensure safe operation and prevent malicious interference.

Regulatory Compliance: Governments and regulatory bodies are implementing stricter cybersecurity regulations for automotive manufacturers, pushing the industry towards enhanced security measures.

Growing Data Privacy Concerns: With vehicles collecting vast amounts of data, protecting this information from unauthorized access has become a priority.

Enquiry Before Buying

4. Major Threats

Remote Attacks: Hackers can exploit vulnerabilities in vehicle communication systems to gain unauthorized access remotely.

Vehicle-to-Everything (V2X) Attacks: Threats targeting the communication between vehicles and their environment can disrupt traffic systems and endanger safety.

Software Vulnerabilities: Flaws in vehicle software or firmware can be exploited to gain control over critical vehicle functions.

Data Breaches: Unauthorized access to personal and sensitive data collected by vehicles can lead to privacy violations and identity theft.

Schedule a Call

5. Key Technologies

Intrusion Detection Systems (IDS): Monitors vehicle networks and systems for suspicious activity.

Encryption: Protects data transmitted between the vehicle and external entities by encoding it to prevent unauthorized access.

Secure Communication Protocols: Ensures that data exchanged between vehicle components and external networks is secure.

Hardware Security Modules (HSMs): Provides physical and logical protection against tampering and unauthorized access to cryptographic keys and sensitive data.

6. Market Segmentation

By Security Type: Network Security, Endpoint Security, Application Security, and Cloud Security.

By Vehicle Type: Passenger Cars, Commercial Vehicles, and Electric Vehicles.

By Technology: Encryption, Intrusion Detection Systems, Firewall, and Public Key Infrastructure (PKI).

By Region: North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa.

7. Regional Insights

North America: Leads the market due to early adoption of connected and autonomous vehicles, along with stringent cybersecurity regulations.

Europe: Significant growth driven by regulatory standards such as the General Data Protection Regulation (GDPR) and the European Union’s cybersecurity initiatives.

Asia-Pacific: Rapid growth due to increasing vehicle production and adoption of advanced automotive technologies, with notable developments in China and Japan.

Buy Now

8. Key Players

Autotalks: Specializes in V2X communication solutions and automotive cybersecurity.

Harman International (Samsung Electronics): Provides end-to-end cybersecurity solutions for connected and autonomous vehicles.

Vector Informatik: Offers a range of automotive security products, including intrusion detection and prevention systems.

NXP Semiconductors: Focuses on secure hardware solutions for automotive applications.

McAfee: Provides cybersecurity solutions tailored for automotive systems.

9. Challenges

Complexity of Automotive Systems: The increasing complexity of vehicle architectures makes it challenging to implement comprehensive cybersecurity measures.

Evolving Threat Landscape: The rapid evolution of cyber threats requires continuous updates and improvements in security technologies.

Cost Considerations: Implementing advanced cybersecurity solutions can be expensive, especially for smaller manufacturers and suppliers.

10. Future Outlook

The automotive cybersecurity market is poised for significant advancements with the integration of artificial intelligence (AI) and machine learning (ML) for predictive threat detection and response. As vehicles become more connected and autonomous, the need for robust and adaptive cybersecurity solutions will continue to grow.

To get more information about this Click Here

#reseach marketing#marketing#digital marketing#automotive#cybersecurity#security#data security#car accessories

0 notes

Text

Cloud Discovery Market – Forecast 2024-2030

Cloud Discovery Market Overview:

Cloud Discovery Market size is estimated to reach US$4.1 billion by 2030, growing at a CAGR of 16.4% during the forecast period 2024-2030. Growing adoption of multi-cloud environments and increasing need for compliance and security are expected to propel the growth of Cloud Discovery Market.

Additionally, one prominent trend in the cloud discovery market is the integration of artificial intelligence (AI) and machine learning (ML) technologies. AI and ML algorithms are being incorporated into cloud discovery solutions to enhance automation, intelligence, and predictive capabilities. These technologies enable more accurate identification of cloud assets, real-time monitoring of cloud environments, and proactive threat detection. By analyzing large datasets and patterns, AI-powered cloud discovery tools can provide actionable insights, streamline workflows, and improve the efficiency of cloud management processes. Another significant trend shaping the cloud discovery market is the increasing focus on hybrid and multi-cloud optimization. As organizations adopt hybrid and multi-cloud strategies to leverage the strengths of different cloud platforms, optimizing resource allocation, performance, and costs across these environments becomes essential. Cloud discovery solutions are evolving to provide comprehensive visibility and control over hybrid and multi-cloud architectures, enabling organizations to identify redundant resources, optimize workloads, and maximize cost-efficiency.

Request Sample

Cloud Discovery Market - Report Coverage:

The “Cloud Discovery Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Cloud Discovery Market.

AttributeSegment

By Organization Size

● Large Enterprises

● Small & Medium Enterprises

By Component

● Solutions

Application Discovery

Infrastructure Discovery

● Services

Professional Services

Managed Services

By Industry Vertical

● BFSI

● Healthcare & Life Sciences

● Telecommunications & ITs

● Retail & Consumer Goods

● Government & Public Sector

● Media & Entertainment

● Manufacturing

● Transportation & Logistics

● Others

By Geography

● North America (U.S., Canada and Mexico)

● Europe (Germany, France, UK, Italy, Spain, Netherlands and Rest of Europe),

● Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific),

● South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

● Rest of the World (Middle East and Africa).

COVID-19 / Ukraine Crisis - Impact Analysis:

● The COVID-19 pandemic has accelerated the adoption of cloud technologies as businesses shifted to remote work environments. This transition heightened the need for cloud discovery solutions to manage and secure cloud assets effectively. Organizations faced increased cybersecurity threats and compliance challenges as remote work expanded the attack surface. Consequently, demand for cloud discovery tools surged, driving market growth. Additionally, the pandemic underscored the importance of digital transformation and resilient IT infrastructures, further propelling investments in cloud discovery solution.

● The conflict in Ukraine has had complex effects on the cloud discovery market. Geopolitical tensions and cybersecurity threats have intensified, leading to increased vigilance and investment in cloud security measures. Companies are prioritizing robust cloud discovery tools to safeguard their data and infrastructure against potential cyber-attacks and disruptions. Additionally, the conflict has prompted reassessments of data sovereignty and compliance requirements, driving further demand for comprehensive cloud discovery solutions.

Key Takeaways:

● Services Dominated the Market

According to the Cloud Discovery Market analysis, in the Cloud Discovery market share, Services is analyzed to hold a dominant market share of 55% in 2023. As organizations increasingly migrate their operations to the cloud, they face complex challenges related to visibility, security, and compliance. Cloud discovery services address these challenges by providing comprehensive solutions for discovering, mapping, and managing cloud resources across multiple environments. In February 2023, Cisco introduces new cloud services in IoT Operations Dashboard to increase industrial asset visibility, securely manage assets from anywhere and provide Industrial Internet of Things (IoT) customers with a seamless path to cloud automation for Operational Technology (OT) teams. The dominance of services in this market is the expertise and specialized knowledge required to effectively manage cloud infrastructures. The services help organizations understand their cloud footprint, identify unauthorized usage, and ensure that all cloud resources comply with regulatory requirements. As businesses utilize multiple cloud platforms (e.g., AWS, Microsoft Azure, Google Cloud), managing these diverse environments becomes increasingly complex. Service providers facilitate seamless integration and management across different cloud services, offering a unified view and control over the entire cloud ecosystem. The continuous evolution of cloud technologies and the associated security threats necessitate ongoing support and updates, which are effectively managed through service engagements.

Inquiry Before Buying

● Telecommunications & ITs is the fastest growing segment

In the Cloud Discovery Market forecast, Telecommunications & ITs segment is estimated to grow with a CAGR of 8.2% during the forecast period. The telecommunications industry is undergoing a significant transformation with the rollout of 5G technology. The deployment of 5G networks requires robust cloud infrastructure to handle the increased data traffic and provide enhanced services such as low-latency applications, IoT integration, and advanced mobile services. Cloud discovery tools are essential for telecom operators to manage and optimize their multi-cloud environments, ensuring seamless operations, compliance, and security. ITs companies, which include IT services, business process outsourcing (BPO), and managed services providers, are increasingly adopting cloud-based solutions to improve operational efficiency and reduce costs. These organizations handle vast amounts of sensitive data and require comprehensive cloud discovery solutions to ensure data integrity, compliance with regulatory standards, and protection against cyber threats. The need for visibility into cloud resources and the ability to control and secure these assets is paramount, making cloud discovery tools indispensable. Additionally, the pandemic has accelerated the digital transformation across both telecommunications and ITs sectors. Remote work, increased reliance on digital communication tools, and the shift towards virtualized environments have amplified the demand for cloud services. As a result, there is a heightened need for effective cloud discovery and management solutions to support these transitions.

● North America to Hold Largest Market Share

According to the Cloud Discovery Market analysis, North America region is estimated to hold the largest market share of 33% in 2023. The region has a high concentration of major cloud service providers, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, which dominate the global cloud infrastructure landscape. These companies not only offer extensive cloud services but also continually innovate, driving demand for cloud discovery solutions that help organizations manage and optimize their cloud environments effectively. North America's robust technological infrastructure and advanced IT ecosystem support the adoption of cloud discovery tools. The presence of numerous tech-savvy enterprises and startups accelerates the implementation of multi-cloud and hybrid cloud strategies, necessitating sophisticated discovery tools to maintain visibility and control over diverse cloud resources. Additionally, North America's strong emphasis on cybersecurity and regulatory compliance fuels the need for cloud discovery solutions. Enterprises are increasingly required to ensure data security and compliance with regulations such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), which mandate stringent controls over cloud data management and reporting. The high adoption rate of emerging technologies such as artificial intelligence (AI), Internet of Things (IoT), and big data analytics in North America propels the need for advanced cloud discovery solutions.

Schedule a Call

● Growing Adoption of Multi-Cloud Environments

As businesses increasingly leverage multiple cloud service providers to achieve diverse objectives such as redundancy, cost optimization, and access to specialized services, the complexity of managing these environments escalates. Cloud discovery solutions play a crucial role in addressing this complexity by providing comprehensive visibility and control across various cloud platforms. These solutions enable organizations to identify, map, and manage their cloud assets effectively, regardless of the underlying infrastructure. Multi-cloud adoption enhances flexibility and mitigates the risk of vendor lock-in, empowering organizations to choose the best-fit solutions for their specific needs. However, managing disparate cloud environments requires sophisticated tools capable of integrating and harmonizing data from different sources. Cloud discovery solutions offer centralized management capabilities, allowing businesses to streamline operations, optimize resource utilization, and enhance security across their entire cloud footprint. Therefore, the growing adoption of multi-cloud environments drives the demand for cloud discovery solutions by addressing the challenges associated with managing diverse cloud infrastructures and enabling organizations to harness the full potential of their multi-cloud strategies.

● Increasing Need for Compliance and Security

As businesses migrate their operations to the cloud, they face stringent regulatory requirements and escalating cybersecurity threats. Compliance standards such as GDPR, HIPAA, SOC 2, and others mandate strict data protection measures, making it imperative for organizations to ensure the security and integrity of their cloud environments. Cloud discovery solutions play a crucial role in meeting these compliance needs by offering comprehensive visibility into cloud assets, configurations, and activities. These tools enable organizations to monitor and audit their cloud infrastructure continuously, identify unauthorized access or configurations, and enforce compliance controls effectively. Moreover, with the escalating frequency and sophistication of cyber-attacks targeting cloud environments, organizations are increasingly investing in cloud discovery solutions to bolster their security posture. By providing real-time insights, threat detection, and remediation capabilities, cloud discovery tools empower businesses to proactively mitigate risks and safeguard their sensitive data, thereby driving the adoption of these solutions in the cloud market landscape.

● The Lack of Standardized Approaches and Tools for Cloud Discovery

With the rapid proliferation of cloud services and architectures, organizations face challenges in achieving consistent and comprehensive visibility into their cloud environments. The absence of standardized methodologies and tools complicates the process of discovering and managing cloud resources effectively. One of the primary issues stemming from this constraint is the lack of interoperability between different cloud platforms and services. Without standardized approaches, organizations struggle to integrate disparate cloud environments seamlessly, leading to inefficiencies and gaps in visibility. Additionally, the lack of standardized tools hampers collaboration and knowledge sharing among industry stakeholders. Without commonly accepted frameworks and best practices, organizations may resort to ad-hoc or proprietary solutions, further exacerbating fragmentation and hindering innovation in the cloud discovery space. Addressing this constraint requires concerted efforts from industry players, standardization bodies, and regulatory authorities to develop and promote consistent methodologies, frameworks, and tools for cloud discovery. By establishing common standards and practices, organizations can streamline cloud management processes, enhance interoperability, and foster a more robust and dynamic cloud discovery market ecosystem.

Buy Now

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Cloud Discovery Market. The top 10 companies in this industry are listed below:

ServiceNow

Amazon Web Services, Inc.

Microsoft

McAfee, LLC

IBM

Cisco Systems, Inc.

Oracle

Google LLC (Alphabet Inc.)

Netskope

Qualys, Inc.

Scope of Report:

Report MetricDetails

Base Year Considered

2023

Forecast Period

2024–2030

CAGR

16.4%

Market Size in 2030

$4.1 billion

Segments Covered

Organization Size, Component, Industry Vertical

Geographies Covered

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Colombia and Rest of South America), Rest of the World (Middle East and Africa).

Key Market Players

ServiceNow

Amazon Web Services, Inc.

Microsoft

McAfee, LLC

IBM

Cisco Systems, Inc.

Oracle

Google LLC (Alphabet Inc.)

Netskope

Qualys, Inc.

#Cloud Discovery Market#Cloud Discovery Market Share#Cloud Discovery Market Size#Cloud Discovery Market Forecast#Cloud Discovery Market Report#Cloud Discovery Market Growth

0 notes

Text

Biometric Sensors Market to Record an Exponential CAGR by 2030

Allied Market Research, titled, “Biometric Sensors Market by Type and Application: Global Opportunity Analysis and Industry Forecast, 2021–2030”, the global biometric sensors market size was valued at $1.15 billion in 2020, and is projected to reach $3.31 billion by 2030, registering a CAGR of 11.8% during the forecast period. The North America region is expected to be the leading contributor to the global market during the forecast period, followed by Asia-Pacific and Europe.

A biometric sensor is an identification and authentication device that uses automated methods of verifying or recognizing the identity of a living person, based on the physical attribute. These attributes include fingerprints, facial images, Iris and voice recognition. Generally, the sensor reads or measures light, temperature, speed, electrical capacity, and other types of energies. Different technologies are applied to get the conversation using sophisticated combinations, networks of sensors and digital cameras.

Many physical characteristics of a person, such as face, iris, fingerprints, are scanned by a biometric sensor and are converted to a digital image using an analog to digital converter. This digital information is stored in a memory and is used to verify or authenticate identity of person.

In the current modernized digital world, security threats are on a rapid rise. The global financial and banking sectors are interconnected via the Internet and the data related to consumers is highly confidential and prone to cyber-attacks. The current security systems implemented by organizations have multiple loopholes and are unsecure against high level cyber-attacks. Further, surge in demand for touchless fingerprint technology drives the biometrics sensors market.

Prominent factors that impact the biometric sensors market growth include the rise in number of identity threats, emergence of touch less fingerprint technology, and growth in popularity of wearable devices, such as smart watches and smart bands. However, high cost of biometric technology and easy availability of alternative cheap non-biometric technologies restricts the market growth. On the contrary, the growing concerns related to privacy breaches is expected to create lucrative opportunities for the market. Therefore, these factors are expected to definitely affect the biometric sensors industry during the forecast period.

On the basis of region, the biometric sensors market trends are analyzed across North America (U.S., Canada, and Mexico), Europe (Germany, France, UK, Italy, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, and Rest of Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa). North America is dominating the market, due to increase in demand for smart weapons, and most of the smart weapons use biometric sensors technology, which further stimulates the demand for biometric sensors. The overall biometric sensors market analysis is determined to understand the profitable trends to gain a stronger foothold.

Covid-19 Impact Analysis

The COVID-19 pandemic has significantly impacted global economies, resulting in workforce & travel restrictions, supply chain & production disruptions, and reduced demand & spending across many sectors. Sudden decline in infrastructure development is expected to hamper the growth of the market share.

The biometric sensors market revenue witnessed a decline in its growth rate, owing to delayed projects, which led to a substantial impact. Furthermore, market players are investing in R&D of biometric sensors, owing to increase in governmental initiatives globally. Therefore, the biometric sensors market size is anticipated to gain momentum by the end of 2022.

Key Findings Of Study

In 2020, the voice scan segment accounted for the maximum revenue and is projected to grow at a notable CAGR of 13.9% during the forecast period.

The thermal sensors segment is expected to witness highest growth rate during the forecast period.

Germany was the major shareholder in the Europe biometric sensors market, accounting for approximately 25% share in terms of revenue in 2020.

The key players profiled in the report include CROSSMATCH Technologies Inc., Fujitsu, Fulcrum Biometrics, Thales Group, IDEX ASA, Infineon, NEC Corporation, Precise Biometrics AB, SAFRAN S.A. and ZKTECO Inc. These players have adopted various strategies, such as partnership, agreement, collaboration, and product launch to expand their foothold in the biometric sensors industry.

0 notes

Text

VPN Market Insights: Growth Drivers and Emerging Technologies

Market Definition

The Virtual Private Network (VPN) market refers to the industry encompassing products and services that provide secure, encrypted connections over the internet. VPNs create private, protected pathways for users to access networks and data remotely, often used to enhance online privacy, circumvent geographic content restrictions, and secure data transmissions. This market includes various types of VPN solutions, such as consumer VPN services, enterprise VPNs, and VPN hardware, catering to different needs from individual privacy to organizational network security.

Market Overview

The market overview provides a snapshot of the current state and dynamics of a specific industry or sector. It includes an analysis of key trends, growth drivers, market size, competitive landscape, and major players. This overview helps stakeholders understand the market's potential, emerging opportunities, and challenges. For instance, in the VPN market, the overview would cover factors like increasing demand for online privacy, technological advancements, and the competitive positioning of leading VPN providers.

[PDF Brochure] Request for Sample Report:

Market Dynamics:

The VPN market is propelled by rising concerns over data security and privacy, driven by increasing cyber threats and the proliferation of remote work. However, high costs and potential performance issues can restrain market growth. Opportunities are emerging in expanding markets and advancements in technology, while challenges include intense competition and navigating complex regulatory environments.

Market Trends:

The VPN market is experiencing a surge in consumer adoption driven by heightened privacy concerns and remote work trends. Key trends include the integration of VPNs with broader cybersecurity solutions, a focus on advanced encryption technologies, and the push for multi-platform compatibility. Additionally, there's a notable shift towards user-friendly, scalable solutions that cater to both personal and business needs.

Top Key Players in Virtual Private Network (VPN) market:

GmbH

CyberGhost S.A.

Nord VPN

Microsoft Corporation

Private Internet Access

NortonLifeLock Inc.

Golden Frog

Buffered VPN

NetGear INC.

Regional Analysis in Virtual Private Network (VPN) market:

The VPN market varies significantly by region, with North America leading due to high cybersecurity awareness and advanced technological infrastructure. Europe follows closely, driven by stringent data protection regulations like GDPR. The Asia-Pacific region is rapidly growing, fueled by increasing digitalization and a rising middle class. Latin America and the Middle East & Africa are emerging markets with expanding demand, though they face challenges such as regulatory complexities and varying levels of technological adoption.

Strategic recommendations for stakeholders:

Stakeholders in the VPN market should focus on enhancing product innovation to stay ahead of emerging cybersecurity threats and user demands. Investing in advanced encryption technologies and multi-platform support can attract a broader user base. Forming strategic partnerships and exploring opportunities in expanding markets can drive growth. Additionally, addressing regulatory compliance proactively and emphasizing cost-effective, scalable solutions can improve market positioning and customer satisfaction.

Browse In-depth Market Research Report:

0 notes

Text

Exploring the Regulatory Landscape for AIoT Platforms Market: Compliance and Standards

Introduction to AIoT Platforms Market

AIoT (Artificial Intelligence of Things) platforms integrate AI capabilities with IoT (Internet of Things) devices, creating smart, interconnected systems that can analyze and act on data in real-time. The AIoT platforms market is rapidly growing as industries seek to enhance operational efficiency, improve decision-making, and create innovative applications. These platforms combine data collection, machine learning, and advanced analytics to enable smart cities, industrial automation, and connected healthcare. Key players in the market include tech giants and specialized startups, driving competition and innovation. The market’s expansion is fueled by increasing demand for automation, data-driven insights, and the proliferation of IoT devices.

Market overview

The AIoT Platforms Market is Valued USD 5.1 billion in 2024 and projected to reach USD 92.0 billion by 2032, growing at a CAGR of 37.9% During the Forecast period of 2024–2032.This rapid growth is driven by advancements in AI technology, increasing adoption of IoT devices across various sectors, and the demand for data-driven insights and automation solutions.

Access Full Report : https://www.marketdigits.com/checkout/677?lic=s

Major Classifications are as follows:

By Component

Platform

Application Management

Connectivity Management

Device Management

Software

Data Management

Network Bandwidth Management

Real-time Streaming Analytics

Remote Monitoring

Security

Edge Solution

By Services

Managed Services

Professional Services

By End-user

Manufacturing

Healthcare

Retail

BFSI

Transportation & Logistics

Energy & Utilities

Others

Key Region/Countries are Classified as Follows:

◘ North America (United States, Canada, and Mexico)

◘ Europe (Germany, France, UK, Russia, and Italy)

◘ Asia-Pacific (China, Japan, Korea, India, and Southeast Asia)

◘ South America (Brazil, Argentina, Colombia, etc.)

◘ The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South Africa)

Major players in AIoT Platforms Market:

Amazon Web Services, Autoplant System India Pvt. Ltd., Axiomtek, Cisco, Cognosos, Falkonry, Google, Hitachi, HPE, IBM, Intel, Microsoft, Nxp, Oracle, Relayr, Sap, Sas Institute Inc., Semifive, Sharp Global, Sight Machine, Tencent Cloud, Terminus Group, Uptake Technologies Inc., Wiliot & others.

Market Drivers in AIoT Platforms Market:

Advancements in AI and Machine Learning: Improvements in AI and machine learning algorithms enhance the capabilities of IoT devices, enabling more sophisticated data analysis and decision-making.

Increasing AloT Device Adoption: The proliferation of IoT devices across industries — such as manufacturing, healthcare, and smart cities — creates a growing need for AIoT platforms market to manage and analyze vast amounts of data.

Demand for Automation: Organizations seek to automate processes to improve efficiency, reduce costs, and enhance productivity, which drives the adoption of AIoT solutions.

Enhanced Data Analytics: AIoT platforms market provide advanced analytics capabilities, offering valuable insights that help businesses make informed decisions and optimize operations.

Market challenges in AIoT Platforms Market:

Data Privacy and Security: Ensuring the security and privacy of data collected from IoT devices is a major concern. The integration of AI with IoT increases the complexity of protecting sensitive information from cyber threats.

Interoperability Issues: Diverse IoT devices and platforms often lack standardization, leading to challenges in ensuring seamless integration and communication between different systems.

Complexity of AI Models: Developing and managing sophisticated AI models can be complex and resource-intensive, requiring specialized skills and significant computational power.

Market opportunities in AIoT Platforms Market:

Expansion in Emerging Markets: Growing industrialization and technological adoption in emerging markets offer new opportunities for AIoT platforms market, particularly in sectors like agriculture, manufacturing, and logistics.

Smart Cities Development: Increasing investments in smart city projects create demand for AIoT platform market to enhance urban infrastructure, traffic management, and public safety.

Collaboration with 5G Networks: The rollout of 5G networks offers opportunities for AIoT platforms market to leverage higher data speeds and lower latency for more effective and scalable solutions.

Future trends in AIoT Platforms Market:

Edge AI Integration: The shift towards edge computing allows AIoT platforms to process data locally on IoT devices, reducing latency and improving real-time decision-making and analytics.

Enhanced AI Algorithms: Advances in AI algorithms, such as more sophisticated machine learning and deep learning models, will improve the accuracy and capabilities of AIoT applications.

5G and Connectivity: The widespread adoption of 5G networks will enable faster data transmission and more reliable connections for IoT devices, enhancing the performance and scalability of AIoT solutions.

AIoT for Sustainability: There will be a growing focus on using AIoT platforms market for environmental sustainability, including energy management, waste reduction, and monitoring of environmental conditions.

Conclusion:

The AIoT platforms market is poised for significant growth, driven by advancements in AI, expanding IoT adoption, and the push for automation and data-driven insights. While challenges such as data security, interoperability, and high costs persist, opportunities in smart cities, healthcare, and industrial automation offer promising prospects. Future trends, including edge computing, 5G integration, and enhanced AI algorithms, will further shape the market, leading to more efficient and innovative solutions. As AIoT technology continues to evolve, it will unlock new possibilities and drive transformative changes across various industries, positioning itself as a critical component of the digital future.

#AIoT platforms market demand#AIoT platforms market share#AIoT platforms market trend#AIoT platforms market size

0 notes

Text

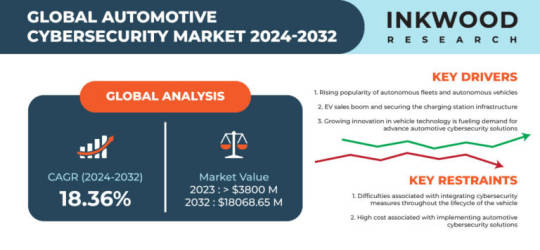

Escalating EV Sales to Aid Automotive Cybersecurity Market Growth

As per Inkwood Research, the Global Automotive Cybersecurity Market is expected to grow at a CAGR of 18.36% in terms of revenue over the forecasting period of 2024-2032.

VIEW TABLE OF CONTENTS

Automotive cybersecurity focuses on protecting vehicles from digital threats and unauthorized access. As vehicles increasingly incorporate advanced technology and connectivity, safeguarding against cyberattacks is crucial to ensure safety and privacy.

REQUEST FREE SAMPLE

This field addresses vulnerabilities in onboard systems, communication networks, and external interfaces to prevent malicious exploitation and ensure secure operation.

Rising EV Sales to Propel Automotive Cybersecurity Market Growth

The surge in electric vehicle (EV) sales is driving significant growth in the global automotive cybersecurity market. As EVs integrate sophisticated technologies and extensive connectivity features, they become more vulnerable to cyber threats, necessitating robust security measures. The increasing reliance on software and data communication in EVs amplifies the need for advanced cybersecurity solutions to protect against hacking and unauthorized access. This heightened demand for security is prompting automakers and technology providers to invest heavily in cybersecurity innovations. Consequently, the expanding EV domain is fueling rapid advancements and growth in the automotive cybersecurity sector, ensuring safer and more secure vehicle operations.

Connected Vehicle Security is Estimated to be the Leading Security Type

Connected network security is crucial for protecting a vehicle’s connections to external networks, such as cellular and Wi-Fi, from threats like man-in-the-middle attacks. This involves securing the Telematics Unit (TMU), which transmits sensitive data, through encryption and authentication methods to ensure secure communication. Proactive vulnerability management, including identifying and patching software and firmware weaknesses, is also essential. Additionally, Security Information and Event Management (SIEM) systems play a key role by analyzing real-time data to swiftly detect and address threats. Advanced diagnostics and remote monitoring by automotive manufacturers further enhance security by providing early detection and insights for effective response to potential cyberattacks.

In 2023, Asia-Pacific was the Largest Region in the Automotive Cybersecurity Market

The APAC, with major automotive markets like China, Japan, and India, demands strong cybersecurity for its growing fleet of connected and autonomous vehicles. China leads the global automotive market, driving high demand for automotive cybersecurity due to extensive production, electric vehicle adoption, and advanced infotainment systems, supported by government initiatives. Japan also faces rising cybersecurity risks, prompting the government to enhance protections through bodies such as JAMA and JAPIA, addressing threats to vehicles and associated IT/OT systems.

The global automotive cybersecurity market is highly competitive, with numerous players striving to innovate and secure advanced vehicle systems against evolving cyber threats. Key industry rivals include established tech giants and specialized cybersecurity firms, all vying for dominance in an expanding sector driven by increasing vehicle connectivity and regulatory demands. Some of the leading companies operating in the market include Infineon Technologies AG, NXP Semiconductors NV, Robert Bosch GmbH, etc.

Request for Customization

Related Reports:

AUTONOMOUS VEHICLE MARKET

CYBER SECURITY MARKET

ELECTRIC VEHICLE MARKET

About Inkwood Research

Inkwood Research specializes in syndicated & customized research reports and consulting services. Market intelligence studies with relevant fact-based research are customized across industry verticals such as technology, automotive, chemicals, materials, healthcare, and energy, with an objective comprehension that acknowledges the business environments. Our geographical analysis comprises North & South America, CEE, CIS, the Middle East, Europe, Asia, and Africa.

Contact Us

1-(857)293-0150

0 notes

Text

IoT Security Market: Your Guide to the Booming Industry of 2024 and Beyond

The Internet of Things (IoT) is reshaping industries and everyday life with its rapid growth and expanding applications. As more devices become interconnected, the need for robust security measures becomes increasingly critical. The IoT security market is at the forefront of addressing these concerns, and its trajectory is nothing short of impressive.

According to recent forecasts, theIoT security market is expected to grow from USD 22.3 billion in 2023 to USD 85.5 billion by 2030, reflecting a remarkable compound annual growth rate (CAGR) of 21.2% during the forecast period. This surge highlights the escalating importance of securing IoT devices and networks as they become integral to various sectors, including healthcare, manufacturing, transportation, and smart homes.

Key Drivers of Growth

Several factors are propelling the growth of the IoT security market. First and foremost is the increasing number of IoT devices being deployed globally. As businesses and consumers alike embrace smart technologies, the volume of connected devices has skyrocketed, creating a larger attack surface for potential cyber threats. This explosion in device connectivity necessitates advanced security solutions to safeguard sensitive data and ensure operational integrity.

Another significant driver is the rising frequency and sophistication of cyber-attacks targeting IoT systems. From data breaches to ransomware attacks, the security risks associated with IoT are becoming more complex and damaging. In response, organizations are investing heavily in comprehensive security strategies and technologies to protect their IoT ecosystems.

Download Sample Report @ https://intentmarketresearch.com/request-sample/iot-security-market-3033.html

Innovations and Solutions

The IoT security market is characterized by continuous innovation as companies develop new solutions to tackle emerging threats. These include advanced encryption techniques, threat intelligence platforms, and AI-driven security tools that offer real-time monitoring and response capabilities. Additionally, the integration of blockchain technology is gaining traction as a means to enhance the security and integrity of IoT transactions and communications.

Major Key Players

◘ Allot

◘ Check Point

◘ Cisco

◘ Fortinet

◘ IBM

◘ Intel

◘ Microsoft

◘ Palo Alto

◘ Thales

◘ Trend Micro

◘ Afero

◘ Bastille Networks

◘ Claroty

◘ Cybeats

◘ Nozomi Networks

◘ Nubeva Technologies

◘ SAM Seamless Network

◘ Xage Security

◘ Zscaler

Regional Insights

The growth of the IoT security market is not uniform across the globe. North America, particularly the United States, is currently the largest market due to its early adoption of IoT technologies and stringent regulatory requirements. However, other regions, such as Europe and Asia-Pacific, are also experiencing significant growth driven by increasing IoT deployment and heightened awareness of cybersecurity risks.

Access Full Report @ https://intentmarketresearch.com/latest-reports/iot-security-market-3033.html

The Road Ahead

Looking ahead, the IoT security market is poised for continued expansion. As the number of connected devices grows and cyber threats evolve, the demand for innovative and effective security solutions will only increase. Organizations must stay ahead of the curve by investing in cutting-edge technologies and adopting best practices to protect their IoT infrastructures.

In conclusion, the IoT security market's projected growth from USD 22.3 billion in 2023 to USD 85.5 billion by 2030 underscores the critical need for advanced security solutions in an increasingly connected world. As the market evolves, stakeholders must remain vigilant and proactive to address the ever-changing landscape of IoT security threats.

Contact Us

US: +1 463-583-2713

0 notes

Text

IoT Microcontroller Market Poised to Witness High Growth Due to Massive Adoption

The IoT microcontroller market is expected to enable connectivity of various devices used in applications ranging from industrial automation to consumer electronics. IoT microcontrollers help in building small intelligent devices that collect and transmit data over the internet. They offer benefits such as compact design, low-power operation and integrated wireless communication capabilities. With increasing connectivity of devices and growing demand for remote monitoring in industries, the adoption of IoT microcontrollers is growing significantly.

Global IoT microcontroller market is estimated to be valued at US$ 6.04 Bn in 2024 and is expected to reach US$ 14.85 Bn by 2031, exhibiting a compound annual growth rate (CAGR) of 13.7% from 2024 to 2031.

The burgeoning need for connected devices across industries is one of the key factors driving the demand for IoT microcontrollers. Various industries are rapidly adopting IoT solutions to improve operational efficiency and offer enhanced customer experience through remote monitoring and management. Additionally, technology advancements in wireless communication standards such as Bluetooth 5, WiFi 6, and LPWAN are allowing development of low-cost IoT devices with extended range, which is further fuelling market growth.

Key Takeaways

Key players operating in the IoT microcontroller are Analog Devices Inc., Broadcom Inc., Espressif Systems (Shanghai) Co., Ltd., Holtek Semiconductor Inc., Infineon Technologies AG, Integrated Device Technology, Inc.,and Microchip Technology Inc.

Key opportunities in the market include scope for integrating advanced features in microcontrollers to support new wireless technologies and opportunity to develop application-specific microcontrollers for niche IoT markets and applications.

There is significant potential for IoT Microcontroller Market Growth providers to expand globally particularly in Asia Pacific and Europe owing to industrial digitalization efforts and increasing penetration of smart homes and cities concept in the regions.

Market drivers

Growing adoption of connected devices: Rapid proliferation of IoT across various industries such as industrial automation, automotive, healthcare is fueling demand for microcontroller-based solutions. IoT devices require microcontrollers to perform essential tasks like data processing and wireless communication.

Enabling technologies advancements: Improvements in low-power wireless technologies, Embedded Systems, and sensors are allowing development of advanced yet affordable IoT solutions leading to new applications for microcontrollers.

Market restraints

Data privacy and security concerns: Use of IoT microcontrollers makes devices vulnerable to cyber-attacks and privacy breaches raising concerns among users. Addressing security issues remain a challenge restricting broader adoption.

Interoperability issues: Lack of common communication protocols results in devices inability to communicate with each other smoothly restricting large-scale IoT deployments.

Segment Analysis

The IoT Microcontroller Market Regional Analysis is segmented based on product type, end-use industry, and geography. Within product type, 8-bit microcontrollers dominate the segment as they are cheaper and suit basic IoT applications requiring low power consumption. Based on their wide usage in wearable devices, home automation systems, and smart appliances, 8-bit microcontrollers capture over 50% market share. 32-bit microcontrollers are gaining popularity for complex industrial, automotive and networking applications.

The end-use industry segments of IoT microcontroller market include consumer electronics, automotive, industrial automation, healthcare, and others. Consumer electronics captures a major share owing to exponential increase in number of smart devices. Wearable fitness bands and smartwatches incorporate IoT microcontrollers to track vitals and connect to networks. Furthermore, incorporation of microcontrollers in smart home appliances like refrigerators, air conditioners, and washing machines are supporting the consumer electronics segment growth.

Global Analysis

In terms of regions, Asia Pacific dominates the IoT microcontroller market led by rising electronics production in India and China. counties like China, Japan and South Korea are major manufacturing hubs for smart appliances and wearable devices, driving the regional market. North America follows Asia Pacific in terms of market share led by growing industrial automation and presence of automotive giants in the US and Canada adopting connected car technologies. Europe captures a significant market share with growing penetration of IoT across industry verticals in major countries like Germany, UK and France. Middle East and Africa offer lucrative opportunities for embedded software development and IoT services companies eying untapped markets.

Get more insights on Iot Microcontroller Market

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)

#Coherent Market Insights#Iot Microcontroller Market#Iot Microcontroller#Internet Of Things#Iot Devices#Embedded Systems#Smart Devices#Iot Development#Microcontroller Unit#MCU#Low-Power Microcontroller

0 notes

Text

"Outsourced Investigative Resources: Critical Support or Just Another Expense?"

Introduction

Outsourced investigative resources have become a crucial component for businesses and law enforcement agencies worldwide. These services include background checks, forensic investigations, surveillance, and fraud detection, providing organizations with the expertise and tools needed to navigate complex legal and security challenges. The rising need for specialized investigative capabilities, cost-effectiveness, and the demand for rapid response to incidents are driving the growth of this market. This report delves into the market dynamics, regional trends, segmentation, competitive landscape, and future outlook of outsourced investigative resources.

Market Dynamics

Drivers

Increasing Security Concerns: The rise in cybercrimes, corporate fraud, and workplace misconduct has heightened the demand for outsourced investigative services. Companies seek specialized expertise to protect their assets and reputation, driving market growth.

Cost Efficiency: Outsourcing investigative tasks allows organizations to access expert services without the need to maintain an in-house team. This cost-effective approach is particularly appealing to small and mid-size companies.

Regulatory Compliance: Stricter regulations across various industries necessitate thorough investigative processes. Outsourced investigative resources help companies meet these compliance requirements efficiently.

Challenges

Data Privacy Issues: Handling sensitive information during investigations can raise data privacy concerns. Ensuring compliance with data protection laws is a significant challenge for service providers.

Dependence on External Providers: Relying on external agencies for critical investigations can be risky if the provider lacks reliability or thoroughness, potentially leading to compromised results.

Opportunities

Technological Advancements: The integration of advanced technologies such as artificial intelligence, machine learning, and data analytics in investigative processes offers significant growth opportunities. These technologies enhance the accuracy and speed of investigations.

Expanding Market in Emerging Economies: The growing awareness and adoption of outsourced investigative resources in emerging markets present opportunities for service providers to expand their footprint.

Sample Pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/41139

Regional Analysis

North America: The North American market is the largest for outsourced investigative resources, driven by stringent regulatory environments, high demand for corporate investigations, and the presence of key industry players.

Europe: Europe follows closely, with a strong focus on compliance and data protection. The region's demand is fueled by increasing corporate governance requirements and the need for fraud detection.

Asia-Pacific: The Asia-Pacific region is experiencing rapid growth, driven by the expanding corporate sector, rising cyber threats, and the need for regulatory compliance in countries like India and China.

Latin America: In Latin America, the market is growing due to rising crime rates and the need for robust investigative solutions to address security concerns.

Middle East and Africa: The Middle East and Africa are seeing gradual growth as governments and corporations increasingly adopt outsourced investigative services to combat crime and fraud.

Market Segmentation

By Service Type:

Background Checks

Fraud Detection

Forensic Investigations

Surveillance

By End-User:

Corporate

Government

Law Enforcement

Financial Institutions

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Competitive Landscape

Market Share of Large Players: Large players such as Control Risks, Pinkerton, and Kroll dominate the market, holding significant shares due to their established reputation, global presence, and comprehensive service offerings.

Price Control: Big players often influence pricing through their advanced technology and wide-ranging service portfolios, but competition remains intense with smaller firms offering specialized services at competitive rates.

Challenges from Small and Mid-Size Companies: Small and mid-size companies challenge the larger firms by focusing on niche markets, providing tailored services, and leveraging local expertise.

Key Players:

Control Risks

Pinkerton

Kroll

International Investigators, Inc.

Bishop Investigations

Report Overview: https://www.infiniumglobalresearch.com/reports/global-outsource-investigative-resource-market

Future Outlook

New Product Development: Continuous development of new investigative technologies, such as AI-powered analytics and advanced cybersecurity tools, is essential for companies to stay competitive and meet evolving client needs.

Sustainable Practices: The focus on ethical and sustainable investigative practices is growing. Companies that emphasize data privacy, compliance, and ethical standards are more likely to gain and retain client trust.

Conclusion

The outsourced investigative resources market is expanding rapidly due to increasing security concerns, the need for cost-effective solutions, and the rising complexity of corporate environments. While challenges such as data privacy and dependence on external providers persist, technological advancements and opportunities in emerging markets offer significant growth potential. Companies that innovate and adhere to ethical standards are well-positioned to thrive in this evolving landscape.

0 notes

Text

Distributed Denial-of-Service (DDoS) Protection Market Growth Drivers

Introduction to Distributed Denial-of-Service (DDoS) Protection Market

The Distributed Denial-of-Service (DDoS) Protection Market is expanding rapidly due to the rising frequency and complexity of cyberattacks. DDoS protection solutions safeguard networks from malicious traffic aimed at disrupting services. Market growth is fueled by increasing digital transformation, stringent data protection regulations, and heightened awareness of cyber threats. Key segments include on-premise, cloud-based, and hybrid solutions. Challenges include evolving attack methods and high costs, but opportunities arise from advancements in AI, expanding cloud services, and managed service models. Overall, the market is set to grow as organizations prioritize robust cybersecurity measures.

Market overview

The Distributed Denial-of-Service (DDoS) Protection Market is Valued USD 4.1 billion in 2024 and projected to reach USD XX billion by 2030, growing at a CAGR of 14.3% During the Forecast period of 2024-2032. The Distributed Denial-of-Service (DDoS) Protection Market focuses on solutions designed to prevent, mitigate, and respond to DDoS attacks, which flood a network with excessive traffic to disrupt services. The market has seen robust growth due to the increasing frequency and sophistication of DDoS attacks. Key segments include on-premise solutions, cloud-based solutions, and hybrid models. As organizations worldwide recognize the importance of cybersecurity, the demand for DDoS protection solutions continues to rise, driven by evolving threats and regulatory requirements.

Access Full Report :https://www.marketdigits.com/checkout/113?lic=s

Major Classifications are as follows:

By Type

Hardware Solutions

Software Solutions

Mitigation Techniques

Network Layer

Null Routing

Sinkholing

Scrubbing

Application Layer

Domain Name System (DNS) routing

Border Gateway Protocol (BGP) routing

Services

Professional Services

Design and Implementation

Consulting and Advisory

Training and Education

Support and Maintenance

Managed Services

By Application

Network

Application

Database

Endpoint

Key Region/Countries are Classified as Follows:

◘ North America (United States, Canada,)

◘ Latin America (Brazil, Mexico, Argentina,)

◘ Asia-Pacific (China, Japan, Korea, India, and Southeast Asia)

◘ Europe (UK,Germany,France,Italy,Spain,Russia,)

◘ The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South

Major players in Distributed Denial-of-Service (DDoS) Protection Market:

NetScout, Akamai, Radware, Huawei Technology, Fortinet, Link11, Imperva, Cloudflare, BT, A10 Networks, Fastly, Nexusguard, Corero, RioRey, PhoenixNAP, Allot, StrataCore, Sucuri, Verisign, StackPath, Seceon, Haltdos, DDoS-Guard, Indusface, Activereach, Mlytics, and Others.

Market Drivers in the Distributed Denial-of-Service (DDoS) Protection Market

Rising Cyber Threats: Increased frequency and complexity of DDoS attacks drive the demand for advanced protection solutions

Digital Transformation: Growing adoption of digital technologies and cloud services increases exposure to potential attacks

Regulatory Compliance: Stringent data protection regulations necessitate robust security measures, including DDoS protection.

Enhanced Awareness: Increasing awareness about the financial and reputational impacts of DDoS attacks leads to higher investment in protection solutions. Market Challenges in the Distributed Denial-of-Service (DDoS) Protection Market:

Evolving Attack Techniques: Constantly evolving DDoS attack strategies require continuous updates to protection mechanisms.

High Costs: Advanced DDoS protection solutions can be expensive, posing a challenge for small to mid-sized enterprises.

Complex Integration: Integrating DDoS protection with existing IT infrastructure can be complex and resource-intensive.

False Positives: DDoS protection systems may sometimes generate false positives, impacting legitimate traffic and user experienceMarket Opportunities in the Distributed Denial-of-Service (DDoS) Protection Market: