#national guard va home loan

Text

VA Mortgage Transfer: Understanding the Process and Benefits

Transferring a VA mortgage can be a significant decision for both veterans and active service members. Whether you are moving to a new home or seeking better loan terms, understanding the VA mortgage transfer process can help you make informed choices. At Thelivelead, we aim to provide you with all the necessary information to navigate this process smoothly.

What is a VA Mortgage Transfer?

A VA mortgage transfer, also known as a VA loan assumption, allows a borrower to transfer their existing VA home loan to another eligible veteran or service member. This process can be beneficial for both the current homeowner and the new borrower. The original borrower is relieved of the mortgage obligation, while the new borrower benefits from the favorable terms of the existing VA loan.

Benefits of a VA Mortgage Transfer

1. No Down Payment for the New Borrower

One of the primary advantages of a VA loan assumption is that the new borrower can take over the loan without needing to make a down payment. This benefit makes homeownership more accessible for veterans and active-duty service members who may not have significant savings.

2. Lower Interest Rates

VA loans often come with lower interest rates compared to conventional mortgages. By assuming an existing VA loan, the new borrower can potentially secure a lower rate than what is currently available in the market, leading to significant savings over the life of the loan.

3. Simplified Qualification Process

The qualification process for a VA loan assumption can be less stringent than applying for a new mortgage. The new borrower may find it easier to qualify based on the original loan's terms and conditions, which can expedite the home-buying process.

4. Avoiding Closing Costs

In many cases, the closing costs associated with assuming a VA loan are lower than those for obtaining a new mortgage. This reduction in costs can make the transaction more affordable for the new borrower.

The VA Mortgage Transfer Process

1. Determine Eligibility

Before proceeding with a VA mortgage transfer, it's essential to determine if the new borrower is eligible for a VA loan. Eligibility is typically extended to veterans, active-duty service members, and certain members of the National Guard and Reserves. The new borrower must also obtain a Certificate of Eligibility (COE) from the Department of Veterans Affairs.

2. Contact the Lender

The current homeowner should contact their lender to discuss the possibility of a VA loan assumption. The lender will provide information on the specific requirements and documents needed for the process. It is crucial to ensure that the lender approves the assumption before proceeding.

3. Submit Required Documentation

The new borrower will need to submit various documents to the lender, including proof of income, credit history, and the COE. The lender will review these documents to assess the new borrower's ability to assume the loan.

4. Credit and Income Verification

The lender will perform a credit and income verification to ensure that the new borrower can meet the loan's obligations. This step is essential to protect both the lender and the borrower from potential financial difficulties.

5. Assumption Agreement

Once the lender approves the assumption, an assumption agreement is drafted. This legal document outlines the terms and conditions of the loan transfer. Both the current homeowner and the new borrower must sign this agreement to finalize the process.

6. Transfer of Property Title

The final step in the VA mortgage transfer process is the transfer of the property title. This step ensures that the new borrower becomes the legal owner of the property and is responsible for the mortgage payments moving forward.

Important Considerations

1. Remaining Entitlement

When a VA loan is assumed, the original borrower's VA loan entitlement may remain tied to the property unless the new borrower is a veteran and substitutes their entitlement. This situation can impact the original borrower's ability to obtain another VA loan in the future.

2. Due-on-Sale Clause

Some VA loans include a due-on-sale clause, which means the loan must be paid in full if the property is sold or transferred. It's crucial to review the original loan agreement and consult with the lender to understand any potential implications.

3. Negotiating Terms

The terms of the VA loan assumption, such as the interest rate and loan duration, may be negotiable. It's advisable for both parties to discuss and agree on these terms to ensure a mutually beneficial arrangement.

Conclusion

Transferring a VA mortgage can be an excellent option for both current homeowners and prospective buyers. With benefits like no down payment, lower interest rates, and a simplified qualification process, a VA loan assumption can make homeownership more accessible and affordable. At Thelivelead, we are committed to helping veterans and service members navigate the VA mortgage transfer process with ease. If you have any questions or need assistance, our team of experts is here to support you every step of the way.

#business leads#commercial#leads#leads generation#debt settlement leads#debt settlement#startup#best debt settlement leads#b2b leads#united states

2 notes

·

View notes

Text

Hard money North Carolina

Understanding Real Estate Loans: A Comprehensive Guide

Real estate loans, also known as mortgages, are fundamental financial instruments that facilitate the purchase of property. These Hard money North Carolina are essential for most individuals and businesses, allowing them to acquire residential, commercial, or investment properties without paying the full purchase price upfront. This article provides an overview of real estate loans, their types, processes, and key considerations for borrowers.

Types of Real Estate Loans

Conventional Loans:

Conventional loans are not insured by the federal government and typically require a higher credit score and a substantial down payment. They come in two forms: conforming loans, which adhere to the guidelines set by Fannie Mae and Freddie Mac, and non-conforming loans, which do not meet these criteria.

FHA Loans:

Insured by the Federal Housing Administration, FHA loans are designed for low-to-moderate-income borrowers who may have lower credit scores. They offer lower down payment requirements and are popular among first-time homebuyers.

VA Loans:

Available to veterans, active-duty service members, and certain members of the National Guard and Reserves, VA loans are guaranteed by the Department of Veterans Affairs. These loans often require no down payment and offer competitive interest rates.

USDA Loans:

These loans are backed by the U.S. Department of Agriculture and are aimed at rural property buyers. USDA loans typically require no down payment and offer favorable terms to promote homeownership in rural areas.

Jumbo Loans:

Jumbo loans exceed the conforming Hard money North Carolina loan limits set by Fannie Mae and Freddie Mac. They are used to finance luxury homes or properties in high-cost areas and require a higher credit score and larger down payment.

The Loan Process

The process of obtaining a real estate loan involves several key steps:

Pre-Approval:

Before house hunting, potential buyers should seek pre-approval from a lender. This involves an evaluation of their credit score, income, debts, and assets to determine how much they can borrow.

House Hunting and Offer:

With pre-approval in hand, buyers can search for homes within their budget. Once they find a suitable property, they make an offer, which, if accepted, leads to a purchase agreement.

Loan Application:

The formal loan application involves submitting detailed financial information to the lender, including proof of income, tax returns, and details of the property being purchased.

Underwriting:

During underwriting, the lender assesses the borrower’s financial health and the property’s value to ensure they meet the loan criteria. This step may involve an appraisal and further documentation.

Closing:

If the loan is approved, the closing process begins, involving the signing of documents, payment of closing costs, and transfer of property ownership. The borrower receives the loan funds to complete the property purchase.

Key Considerations for Borrowers

Borrowers should consider several factors when applying for a real estate loan:

Interest Rates:

The interest rate affects the overall cost of the loan. Fixed-rate mortgages offer stability with a consistent interest rate, while adjustable-rate mortgages may start with lower rates that can change over time.

Loan Term:

Common loan terms are 15, 20, and 30 years. Shorter terms usually have higher monthly payments but lower total interest costs.

Down Payment:

A larger down payment reduces the loan amount and may eliminate the need for private mortgage insurance (PMI).

Credit Score:

A higher credit score typically results in better loan terms and lower interest rates.

Debt-to-Income Ratio (DTI):

Lenders evaluate the DTI ratio to ensure borrowers can manage their monthly payments alongside other debts.

In conclusion, Hard money North Carolina loans are crucial for enabling property ownership, and understanding the types, process, and key considerations can help borrowers make informed decisions. By carefully evaluating their financial situation and loan options, borrowers can secure favorable terms and successfully navigate the complex real estate market.

0 notes

Text

Navigating the Path to Homeownership: Residential Home Loans and the Role of a Local Mortgage Company

The dream of owning a home is a significant milestone for many individuals and families. However, the journey to homeownership often involves navigating the complex world of residential home loans. Working with a local mortgage company can simplify this process, providing personalized service and local market expertise that can make all the difference in securing the right mortgage.

Understanding Residential Home Loans

Residential home loans, commonly known as mortgages, are financial instruments that allow individuals to purchase homes without paying the full purchase price upfront. These loans are repaid over a set period, typically 15 to 30 years, with interest. Understanding the types of residential home loans available and their respective terms is crucial for prospective homeowners.

Fixed-Rate Mortgages: These loans have a constant interest rate for the duration of the loan term, providing predictable monthly payments. Fixed-rate mortgages are ideal for buyers who plan to stay in their homes for a long time and prefer the stability of consistent payments.

Adjustable-Rate Mortgages (ARMs): ARMs have an interest rate that adjusts periodically based on market conditions. These loans often start with a lower interest rate compared to fixed-rate mortgages, making them attractive for buyers who may move or refinance before the rate adjusts.

FHA Loans: Insured by the Federal Housing Administration, FHA loans are designed for low-to-moderate-income buyers. They offer lower down payment requirements and are more forgiving of lower credit scores.

VA Loans: Available to veterans, active-duty service members, and certain members of the National Guard and Reserves, VA loans offer competitive interest rates and do not require a down payment or private mortgage insurance (PMI).

USDA Loans: These loans are aimed at rural homebuyers and are backed by the United States Department of Agriculture. They offer low interest rates and require no down payment for eligible buyers.

Jumbo Loans: For properties that exceed the conforming loan limits set by the Federal Housing Finance Agency, jumbo loans provide financing for luxury homes and high-priced real estate markets.

The Importance of a Local Mortgage Company

Choosing a local mortgage company for securing a residential home loan can offer several advantages over larger, national lenders. A local mortgage company provides personalized service, deep knowledge of the local real estate market, and a community-focused approach.

Personalized Service: A local mortgage company can offer a more personalized experience. They take the time to understand your financial situation, homeownership goals, and preferences, tailoring their services to meet your needs. This personalized approach ensures that you receive the most suitable mortgage product for your circumstances.

Local Market Expertise: Local mortgage companies have a deep understanding of the local real estate market. They are familiar with neighborhood trends, property values, and local regulations, which can be invaluable in securing the best loan terms and conditions. This expertise can also help in navigating any regional nuances that may affect the loan process.

Accessibility and Communication: Working with a local mortgage company often means easier access and more direct communication. You can meet with your mortgage advisor in person, which can simplify the application process and provide peace of mind. This direct interaction can lead to quicker responses and more efficient problem-solving.

Community Focus: Local mortgage companies are invested in their communities. They build relationships with local real estate agents, appraisers, and other professionals, which can facilitate a smoother homebuying process. Their reputation in the community depends on providing excellent service, which can translate into a better experience for you.

Steps to Securing a Residential Home Loan with a Local Mortgage Company

Securing a residential home loan involves several steps, each of which can be made smoother with the help of a local mortgage company:

Pre-Approval: The first step is to get pre-approved for a mortgage. This involves a thorough review of your financial situation, including your credit score, income, and debt. A pre-approval letter from a local mortgage company shows sellers that you are a serious and qualified buyer.

Home Search: With pre-approval in hand, you can start your home search with confidence. Your local mortgage advisor can provide insights into neighborhoods and help you understand how different properties might fit within your budget.

Loan Application: Once you find your dream home, you will complete a formal mortgage application. Your local mortgage company will guide you through the necessary paperwork and documentation, ensuring everything is in order.

Processing and Underwriting: The mortgage company will then process your application and submit it to underwriting. This step involves verifying your financial information and assessing the property’s value. Local knowledge can expedite this process, as the mortgage company is familiar with local appraisers and property values.

Approval and Closing: After underwriting, you will receive final loan approval. The local mortgage company will coordinate with all parties involved to schedule the closing, where you will sign the final documents and take ownership of your new home.

Benefits of Residential Home Loans

Securing a residential home loan offers numerous benefits, making homeownership accessible to a broader range of people:

Build Equity: Homeownership allows you to build equity over time as you pay down your mortgage and property values appreciate.

Tax Benefits: Mortgage interest and property taxes may be tax-deductible, reducing your overall tax burden.

Stability: Fixed-rate mortgages provide payment stability, making it easier to budget and plan for the future.

Personalization: Owning a home gives you the freedom to personalize your space, making it truly your own.

1 note

·

View note

Text

The Art of Crafting an Explanatory Letter for Mortgage: Understanding Different Home Loan Types

In the world of real estate, understanding the different types of mortgages is crucial for prospective homebuyers. Securing a mortgage can be complex, and individuals may face various challenges. One such challenge is the need to write an explanatory letter for a mortgage, commonly known as a “letter of explanation for a mortgage loan.” This letter plays a significant role in the loan approval process, providing lenders valuable insights into a borrower’s financial situation and decision-making. In this article, we will explore the importance of a letter of explanation for a mortgage loan and delve into the different types of mortgages available in the market.

The Significance of an Explanatory Letter for Mortgage

When applying for a mortgage, lenders carefully evaluate the financial stability and creditworthiness of potential borrowers. A letter of explanation for a mortgage loan is a vital component of this evaluation process, and it serves several essential purposes:

Clarification: Sometimes, there may be irregularities or discrepancies in a borrower’s financial history or application. An explanatory letter can provide an opportunity to clarify these issues and explain any negative marks on the credit report.

Mitigating Risk: Lenders aim to minimize risk when approving mortgages. By providing a well-written letter of explanation, borrowers can demonstrate their commitment to meeting their financial obligations, even if they have faced challenges.

Building Trust: An explanatory letter can help establish trust between the borrower and the lender. It shows transparency and a willingness to communicate openly about financial circumstances.

Types of Mortgages

Before delving into the details of crafting an effective explanatory letter for a mortgage, it is crucial to have a comprehensive understanding of the different types of mortgages available. Knowing the various options allows prospective homebuyers to make informed decisions about the type of loan that best suits their needs. Here are some of the most common mortgage types:

Fixed-Rate Mortgage

A fixed-rate mortgage is one of the most straightforward and traditional mortgage options. With this type of loan, the interest rate remains constant throughout the life of the loan. Borrowers can choose from various term lengths, such as 15, 20, or 30 years. Fixed-rate mortgages provide stability and predictability, making them an excellent choice for those who prefer consistent monthly payments.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage, on the other hand, features an interest rate that can fluctuate over time. Typically, ARMs have a fixed initial period when the interest rate remains constant, followed by periodic adjustments based on prevailing market rates. While ARMs often offer lower initial interest rates, they can become less predictable, potentially leading to higher payments in the future.

FHA Loans

Federal Housing Administration (FHA) loans are government-backed mortgages designed to assist first-time homebuyers and individuals with lower credit scores. FHA loans require a smaller down payment and offer competitive interest rates. They are an attractive option for those not qualifying for conventional mortgages.

VA Loans

VA loans are exclusively available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. The U.S. Department of Veterans Affairs backs these loans and offers favorable terms, including no down payment requirements and competitive interest rates.

USDA Loans

The U.S. Department of Agriculture (USDA) provides USDA loans to eligible rural and suburban homebuyers. These loans offer low interest rates and require no down payment. They are ideal for individuals looking to purchase a home in areas designated as eligible by the USDA.

Jumbo Loans

Jumbo loans are used for financing higher-priced homes that exceed the conforming loan limits set by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. These loans often come with stricter credit requirements and higher interest rates due to the more significant loan amounts.

Crafting a Letter of Explanation for Mortgage

Now that we’ve explored the importance of a letter of explanation for a mortgage loan and gained insight into various home loan types let’s delve into the key elements of crafting a practical explanatory note:

Clarity and Brevity: Your letter should be clear and concise. Address the issues you must explain directly and avoid unnecessary details or lengthy narratives.

Honesty and Transparency: Be honest about your financial situation and any challenges you’ve faced. Transparency is critical to building trust with your lender.

Organization: Organize your letter in a logical and structured manner. Start with a brief introduction, then a clear explanation, and conclude with a summary of your resolution or plan to address the problem.

Language and Tone: Use professional and respectful language in your letter. Avoid making excuses and maintain a positive tone throughout.

Conclusion

In real estate, securing a mortgage is a significant milestone in the journey to homeownership. Understanding the different types of mortgages and being prepared to craft an explanatory letter for your mortgage application can make the process smoother and more successful. Whether you opt for a fixed-rate mortgage, an adjustable-rate mortgage, or one of the specialized government-backed loans, your letter of explanation can play a pivotal role in demonstrating your financial responsibility and addressing any issues that may arise during the application process.

In the end, Paul Mitchell Houston, a prospective homebuyer, is better equipped to navigate the diverse landscape of different home loan types and confidently pen an explanatory letter that communicates their financial history, addresses any concerns, and moves them one step closer to achieving their homeownership dreams.

Mitchell Mortgage Group a Division of Aspire Home Loans

24285 Katy Fwy, Katy, TX 77494

(713) 714–0220

https://www.paulmitchellmortgage.com

1 note

·

View note

Text

U.S. Department of Veterans Affairs Definition

What Is the U.S. Department of Veterans Affairs?

The U.S. Department of Veterans Affairs (VA) is a federal government agency that provides a wide range of services and benefits to eligible veterans, their families, and survivors. Established in 1930, the VA's primary mission is to care for and support veterans of the United States Armed Forces. Here are some key aspects of what the VA does:

Healthcare Services: The VA operates one of the largest healthcare systems in the world, providing medical care, mental health services, and rehabilitative support to veterans. This includes a network of hospitals, clinics, and other healthcare facilities across the United States.

Disability Compensation: Veterans who are disabled due to injuries or illnesses that occurred during active military service may be eligible for disability compensation. The VA provides financial assistance and support to these veterans.

Education Benefits: The VA administers several education assistance programs, such as the GI Bill, which provides financial support for veterans' education and training. This can be used for college, vocational training, and other educational pursuits.

Home Loans: The VA offers home loan guaranty programs to help veterans, active-duty service members, and certain members of the National Guard and Reserves purchase, build, repair, retain, or adapt a home for personal occupancy.

Life Insurance: The VA provides life insurance options for veterans and their families, including Service-Disabled Veterans Insurance, Veterans’ Group Life Insurance, and Family Servicemembers' Group Life Insurance.

Burial Benefits: The VA operates national cemeteries where eligible veterans, their spouses, and dependents can be buried. The VA also provides burial allowances to help cover burial and funeral costs.

Support for Homeless Veterans: The VA runs programs to assist homeless veterans by providing housing, healthcare, job training, and other essential support services.

Research and Innovation: The VA conducts research to improve healthcare services for veterans. This research often focuses on areas such as post-traumatic stress disorder (PTSD), traumatic brain injuries, and other conditions commonly affecting veterans.

The VA plays a crucial role in honoring the nation's commitment to its veterans by ensuring they receive the care, support, and benefits they have earned through their military service.

Understanding the U.S. Department of Veterans Affairs

Certainly, understanding the U.S. Department of Veterans Affairs (VA) involves recognizing its multifaceted role in supporting veterans and their families. Here are some key points to comprehend about the VA:

1. Mission and Commitment:

The VA's primary mission is to provide comprehensive healthcare services, benefits, and support to veterans who served in the U.S. military and to their families.

The agency is committed to fulfilling President Lincoln's promise to care for veterans and their families.

2. Healthcare Services:

The VA operates a vast network of medical facilities, including hospitals, clinics, and nursing homes, providing healthcare services to eligible veterans.

Services encompass a wide range, from general medical care to specialized services like mental health and rehabilitation.

3. Disability Compensation and Pensions:

Veterans who incurred disabilities or illnesses during military service may be eligible for disability compensation, ensuring financial support based on the severity of their disability.

Pensions are provided for wartime veterans with limited income who are permanently and totally disabled or are 65 years or older.

4. Education and Training Benefits:

The VA administers education programs like the GI Bill, offering financial assistance for veterans' education, including college, vocational, and technical training.

5. Home Loans and Housing Assistance:

VA-backed home loans are available to veterans, active-duty service members, and certain members of the National Guard and Reserves, promoting homeownership.

Housing assistance programs aid homeless veterans by providing shelter, counseling, and access to essential services.

6. Life Insurance and Burial Benefits:

Various life insurance programs are offered to veterans and their families, ensuring financial security.

Burial benefits include interment at national cemeteries, headstones, markers, and burial flags to honor veterans' service.

7. Support for Special Groups:

Specialized support is provided for women veterans, homeless veterans, those with PTSD, and veterans with specific service-related issues.

8. Research and Innovation:

The VA conducts research to enhance healthcare services, focusing on areas like PTSD, traumatic brain injury, and other conditions prevalent among veterans.

9. Claims and Appeals:

The VA assists veterans in filing claims for benefits, ensuring they receive the compensation and services they are entitled to.

Understanding the VA involves recognizing its dedication to improving the lives of veterans, ranging from healthcare to housing and education, and its ongoing efforts to honor their service to the nation.

Veterans Health Administration

The Veterans Health Administration (VHA) is one of the largest components of the U.S. Department of Veterans Affairs (VA). It operates the nation's largest integrated healthcare system, providing comprehensive medical services to eligible military veterans. Here are key points about the Veterans Health Administration:

1. Integrated Healthcare System:

The VHA operates a vast network of hospitals, clinics, nursing homes, and other healthcare facilities across the United States.

It provides a wide range of services, including primary care, specialized care (such as cardiology, orthopedics, and mental health), surgery, and rehabilitation.

2. Focus on Veterans' Health:

The VHA is specifically designed to meet the unique healthcare needs of veterans, including services tailored to conditions that may arise due to military service, such as combat-related injuries, post-traumatic stress disorder (PTSD), and exposure to environmental hazards.

3. Preventive Care and Wellness Programs:

VHA emphasizes preventive care, health screenings, and wellness programs to improve the overall health and well-being of veterans.

It offers programs to help veterans quit smoking, manage weight, and address issues like diabetes and hypertension.

4. Mental Health Services:

The VHA provides extensive mental health services, including counseling, therapy, and support for issues like PTSD, depression, and substance abuse.

Specialized programs exist for veterans dealing with military sexual trauma and traumatic brain injuries.

5. Telehealth Services:

VHA has embraced telehealth services, allowing veterans to consult with healthcare providers remotely, which is especially valuable for those in rural areas or with limited mobility.

6. Research and Innovation:

The VHA is a leader in medical research, conducting studies to improve healthcare for veterans and the general population.

It fosters innovation in medical treatments and technologies.

7. Training and Education:

The VHA plays a role in training healthcare professionals, including doctors, nurses, and therapists, ensuring a high standard of care for veterans.

It collaborates with medical schools and universities for research and education.

8. Collaboration and Partnerships:

The VHA collaborates with other federal agencies, private healthcare providers, and non-profit organizations to enhance services and outreach to veterans.

The Veterans Health Administration plays a vital role in honoring the nation’s commitment to provide healthcare for those who have served in the military, ensuring that veterans receive high-quality medical services tailored to their unique needs.

Veterans Benefits Administration

The Veterans Benefits Administration (VBA) is another key component of the U.S. Department of Veterans Affairs (VA). While the Veterans Health Administration (VHA) focuses on healthcare services, the VBA primarily deals with providing a variety of benefits and services to veterans, their dependents, and survivors. Here are the key aspects of the Veterans Benefits Administration:

1. Disability Compensation:

VBA administers disability compensation, providing tax-free financial benefits to veterans with disabilities that are a result of or were worsened by their active military service.

2. Pensions:

The VBA offers pensions to wartime veterans with limited income who are permanently and totally disabled or are 65 years or older. Surviving spouses and children of deceased veterans may also be eligible for pensions.

3. Education and Training Benefits:

The VBA oversees education programs such as the GI Bill, which provides financial assistance for veterans' education and training, including college degrees, vocational and technical training, licensing and certification tests, and more.

4. Vocational Rehabilitation and Employment (VR&E) Program:

VR&E assists veterans with service-connected disabilities to prepare for, find, and maintain suitable employment. The program provides services such as job training, resume development, and job-seeking skills coaching.

5. Home Loan Guaranty Program:

VBA guarantees loans made to veterans to buy, build, repair, retain, or adapt a home for personal occupancy. This program helps veterans secure affordable home loans with favorable terms.

6. Life Insurance:

VBA administers life insurance programs, including Service-Disabled Veterans Insurance (S-DVI), Veterans' Group Life Insurance (VGLI), and Family Servicemembers' Group Life Insurance (FSGLI), providing various life insurance options to veterans and their families.

7. Dependents and Survivors Benefits:

VBA provides benefits to eligible dependents and survivors of veterans, including compensation, education assistance, home loan guarantees, and vocational rehabilitation services.

8. Burial Benefits:

VBA offers burial benefits, including interment at national cemeteries, headstones, markers, burial flags, and financial reimbursement for eligible veterans' burials.

9. Claims Assistance and Appeals:

VBA assists veterans in filing claims for benefits and provides support for appeals if claims are denied.

The Veterans Benefits Administration plays a crucial role in ensuring that veterans and their families receive the financial, educational, and other support they are entitled to, honoring their service to the nation.

National Cemetery Administration

The National Cemetery Administration (NCA) is an important branch of the U.S. Department of Veterans Affairs (VA) responsible for managing the country's national cemeteries and providing burial and memorial benefits for veterans and eligible family members. Here are key aspects of the National Cemetery Administration:

1. National Cemeteries:

NCA maintains and administers national cemeteries across the United States. These cemeteries are reserved for the burial of veterans, their spouses, and dependent children.

2. Burial Benefits:

NCA provides burial benefits to eligible veterans, including a gravesite in a national cemetery, a headstone or marker, a burial flag, and a Presidential Memorial Certificate. Some veterans may also be eligible for burial allowances to assist with funeral costs.

3. Eligibility and Pre-Need Burial Determination:

NCA determines eligibility for burial in national cemeteries. Veterans and their families can also make pre-need burial arrangements, ensuring that their wishes are honored when the time comes.

4. State Veterans Cemeteries:

NCA provides grants to states for establishing, expanding, or improving state veterans cemeteries. These cemeteries operate under the guidelines of the VA and provide burial options for veterans in addition to national cemeteries.

5. Memorial Services and Honors:

NCA conducts memorial services, including military funeral honors, to honor veterans during their burial ceremonies. This can include the playing of Taps, the folding and presenting of the U.S. flag, and the presence of a rifle detail.

6. Maintenance and Preservation:

NCA is responsible for the maintenance and preservation of national cemeteries, ensuring they are kept in a dignified and respectful condition.

7. Commemorative Events:

NCA organizes and participates in commemorative events and ceremonies, such as Memorial Day and Veterans Day observances, to honor and remember veterans and their sacrifices.

8. Veterans Legacy Program:

NCA operates the Veterans Legacy Program, which engages students, educators, and the public in the research and preservation of veterans' legacies, promoting a greater understanding of their service and contributions.

The National Cemetery Administration plays a significant role in honoring veterans by providing them with a final resting place that reflects the nation's gratitude for their service. Through its services and programs, NCA ensures that veterans and their families are remembered and respected for their sacrifices.

billion

I see that you mentioned "billion." How can I assist you further with this term? Are you looking for information about a specific topic related to a billion, such as its numerical value, its significance in various contexts, or something else? Please provide more details so I can provide you with the most relevant information.

History of the U.S. Department of Veterans Affairs

The history of the U.S. Department of Veterans Affairs (VA) is closely intertwined with the history of veterans' care and benefits in the United States. Here is an overview of the key developments in the history of the VA:

1. Post-Revolutionary War Era:

After the American Revolution, the U.S. government recognized the need to support veterans. The Continental Congress passed pension laws to provide financial assistance to disabled veterans.

2. Civil War and Post-Civil War Era:

The federal government established national soldiers' homes and hospitals to care for disabled veterans. The National Asylum for Disabled Volunteer Soldiers, established in 1865, was an early form of government-sponsored veterans' care.

3. World War I and the Veterans Bureau:

After World War I, the Veterans' Bureau was created in 1921 to consolidate various veterans' programs. It was the first federal agency dedicated entirely to veterans' services.

4. Great Depression and World War II:

The Great Depression and World War II increased the need for veterans' services. The Veterans Administration (VA) was established as a federal cabinet-level agency in 1930 to replace the Veterans' Bureau. It integrated various veterans' programs under one administration.

5. Post-World War II Era:

The Servicemen's Readjustment Act of 1944, also known as the GI Bill of Rights, provided a range of benefits to veterans, including education, loans for homes, and unemployment benefits. This legislation had a profound impact on the American middle class and veterans' prosperity.

6. Modern Era and Department of Veterans Affairs:

In 1989, President Ronald Reagan elevated the VA to a cabinet-level department, renaming it the Department of Veterans Affairs. This change reflected the importance of veterans' issues in the federal government.

7. Recent Developments:

The VA has seen continuous evolution to meet the changing needs of veterans. It has expanded services for female veterans, enhanced mental health care, and developed programs to address issues like post-traumatic stress disorder (PTSD) and traumatic brain injuries.

8. Challenges and Reforms:

The VA has faced challenges, including long wait times for medical appointments and issues with the disability claims process. Various administrations and Congress have worked on reforms to improve efficiency, accessibility, and quality of care for veterans.

Throughout its history, the VA has been dedicated to honoring the nation's commitment to its veterans, providing them with the care, benefits, and support they need and deserve after their military service.

Read more: https://computertricks.net/u-s-department-of-veterans-affairs-definition/

0 notes

Text

What are the types of home loan?

There are several types of home loans available to borrowers, each with its own features and benefits. Here are some common types of home loans:

Fixed-Rate Mortgage (FRM): A fixed-rate mortgage is one where the interest rate remains constant throughout the entire loan term. This provides borrowers with predictability and stability in their monthly payments, as the principal and interest portions of the payment remain the same. Fixed-rate mortgages are available in various terms, such as 15, 20, or 30 years.

Adjustable-Rate Mortgage (ARM): An adjustable-rate mortgage has an interest rate that starts off lower than the prevailing market rate for a certain period (often 5, 7, or 10 years), after which the rate adjusts periodically based on an index. These adjustments can result in either higher or lower monthly payments. ARMs are riskier because of potential rate fluctuations, but they can be beneficial if interest rates remain relatively stable.

FHA Loan: Backed by the Federal Housing Administration, FHA loans are designed to help borrowers with lower credit scores and smaller down payments. These loans require mortgage insurance premiums (MIP) and have more lenient qualification criteria compared to conventional loans.

VA Loan: Available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves, VA loans are guaranteed by the Department of Veterans Affairs. They often require no down payment and offer favorable terms, including competitive interest rates and no private mortgage insurance (PMI) requirement.

USDA Loan: The United States Department of Agriculture (USDA) offers loans to help low- to moderate-income borrowers in eligible rural and suburban areas purchase homes. These loans often require no down payment and have lower interest rates.

Reference:

Types of home loan

0 notes

Text

VA loan Texas

VA loan Texas

A VA loan in Texas is a lasting home loan financing to American Experts and army family members. VA Loans in Texas are released by government certified personal loan providers as well as are ensured by the united state Department of Veterans Affairs. The United State Department of Veterans Matters determines eligibility and also problems a certificate of qualification (COE). The certification of eligibility allows Armed force Service candidates to submit to their home loan lender of choice. For servicemen and ladies, it is generally simpler to get a VA funding request than conventional car loans. If you are an active-duty solution military personnel, a present National Guard or Book member, discharged participant of a chosen book, or a retired veteran, this sort of lending program is for you. Below we will certainly go over the Texas VA lending procedure

Additional information regarding a Texas VA loan is available; contact The Texas Mortgage Pros

Texas VA loan process.

Right here is how a Texas VA Financing works:

Military Solution applicants as well as their qualified partners to get the Loan Benefit. A VA financing charge of 0 to 2.15% (this charge may be funded) of the loan quantity is paid to the VA . When buying a residence, veterans may borrow up to 100% of the sales price or practical worth of the house, whichever is less. When re-financing a house, veterans may borrow up to 90% of affordable worth in order to re-finance where state law allows. The house needs to be made use of as a primary home just, should be occupied within 60 days after closing on the funding, and need to remain the professional's main residence for at least 3 years.

Advantages of a Texas VA Finance

Here are the benefits of a Texas VA Loan:

VA Loans reward eligible experts as well as active-duty service member members for their sacrifice as well as contributions. VA Loans use really reduced as well as competitive interest rates contrasted to conventional loans. VA Loans are assured by the VA and also secure the lending institution against loss if the customer defaults on the financing. VA Loans do not need a deposit. VA Loans do not require mortgage insurance add-on on month-to-month settlements as well as no minimal credit report. The seller can likewise pay for a few of the closing sets you back approximately 4% of the lending quantity.

There are great advantages for Texas VA loans for experts, solution participants and armed forces family members. Below we will certainly go over just how VA Loans can be made use of in Texas. VA finance housing options

VA Loans in Texas can be utilized for the following:

To acquire a house or a apartment (as long as the condo remains in a VA-approved growth area). To develop a home. To make improvements to the house. To re-finance lendings of an existing VA finance. To cash-out Refinance

Texas VA Loans can be made use of for lots of types of purposes if the service participant fulfills the qualification requirements below. apply for a home mortgage online Certifications for a VA finance

A Armed force Solution Application can receive a VA Car loan to aid in buying a single-family home ensured by the United States Division of Veterans Matters. The US Department of Veterans Affairs offers a complete 100 percent financing to qualifying active-duty service, qualified servicemen and also females, together with their eligible spouses and armed forces households.

Eligibility for VA financing

Right here is a listing of people qualified for a VA Finance in Texas:

US professionals of the USA Army, Navy, Flying Force, Coastline Guard, Public Health Service, Marine Corps, or Texas National Guard Participants of the routine military Reservists National Guard The spouses of dead solution members that passed away while at work or as a result of a service-connected special needs

Also, it could be valuable to get in touch with a trusted VA lender to recognize your VA eligibility Below are the Service Needs for a VA Finance in Texas.

Texas VA loan certificate of eligibility.

The Certification of Eligibility (COE) plays a significant part in your finance application. The Certification of Eligibility verifies that you have met the minimum service needs, such as service history and obligation status.

Right here are the means to get a Certification of Eligibility (COE)."

Apply via a VA-approved lending institution. Apply by email with VA Type 26-1880. Apply online with the VA's eBenefits portal.

For privilege reconstruction, complete the VA Kind 26-1880 as well as send it to the VA local finance center of your state.

VA finances Texas FAQs.

What is the optimum VA financing quantity in Texas? To obtain an accurate maximum VA lending quantity for your certain needs, you can get in touch with our VA-approved lenders so you can contact them your qualification for a VA financing and neighborhood financing limits. Every situation is different due to the fact that every person's situation is various. The mortgage quantity, sort of residential property, credit rating, and solution backgrounds, funding qualification, are completely different from person to person.

What are the property needs for a VA car loan? The Minimum Residential Or Commercial Property Requirements (MPRs) in Texas are set by the Department of Veterans Affairs. The Department of Veterans Affairs Minimum Residential Property Requirements for VA Loans make certain that expert borrowers and also their households have a risk-free. The Minimum Home Needs are analyzed by an independent VA evaluator. The independent VA appraisers evaluate residential properties for security, cleanliness, as well as architectural stability of the residence.

Here are the Minimum Home Requirements for a VA Financing in Texas:.

The residential or commercial property needs to be a Residential Home as well as not an investment property. The residential property must be made use of as a primary residence. The property must have Architectural Infrastructure. The home needs to be architecturally sound, from roofing systems to crawlspaces to basements. The residential property needs to have comfortable space. The residential property has to permit the residence customer and also his household to live, cook and also rest. The residential or commercial property must have sanitation. Financed buildings must offer clean alcohol consumption water as well as ample sewage disposal.

What are VA finance demands in Texas? Right here are the VA Financing Needs in Texas:.

The surviving spouse of a professional is qualified for a VA lending as long as the partner remains solitary till age 57; they can remarry after age 57. Partners of some entirely impaired experts who died from a service-connected special needs may likewise be qualified. Experts as well as the eligible partner are required to have a copy of their DD-214. Credit report. Certification of Eligibility.

What are the VA car loan armed forces service needs in Texas? Here are the VA Financing Solution Requirements in Texas:.

You have actually provided 90 successive active duty days of service throughout wartime. You have actually done 181 days of active service during peacetime. You have made over 6 years of service or even more in the National Guard or Reserves or your dead spouse that passed away while on active duty.

The Texas Mortgage Pros

Social Profile Links:

https://twitter.com/Mrloanapproval

https://www.linkedin.com/in/jasonturnerthrive

1 note

·

View note

Text

Unlocking the Benefits of VA Loans in Texas: A Guide for Eligible Veterans

VA loans are a great opportunity for eligible veterans and their families to become homeowners in Texas. VA loans offer many benefits such as low-interest rates, no down payment requirements, and no private mortgage insurance (PMI). With these benefits, it's no surprise that VA loans are a popular choice for veterans who want to purchase a home. In this guide, we will explore the benefits of VA loans in Texas and how eligible veterans can take advantage of this opportunity.

One of the biggest benefits of VA loans in Texas is the low-interest rates. VA loans have competitive interest rates that are often lower than conventional loans. This means that veterans can save a significant amount of money over the life of the loan. With lower monthly mortgage payments, veterans can use their money for other important expenses such as healthcare or education.

Another advantage of VA loans is that they do not require a down payment. This is a significant benefit for veterans who may not have enough money saved up for a down payment. With a VA loan, veterans can purchase a home without having to worry about the financial burden of a down payment. This allows veterans to focus on finding the perfect home for themselves and their families.

In addition to no down payment requirements, VA loans also do not require private mortgage insurance (PMI). PMI is a monthly fee that is added to a mortgage payment when a borrower puts less than 20% down on a home. With a VA loan, veterans do not have to worry about this additional expense. This can save veterans thousands of dollars over the life of the loan.

To be eligible for a VA loan in Texas, veterans must meet certain criteria. First, veterans must have served in the United States military for at least 90 consecutive days during wartime or 181 consecutive days during peacetime. Veterans who have served for at least 6 years in the National Guard or Reserves are also eligible for a VA loan. In addition, veterans must have received an honorable discharge. VA loans Texas

Once veterans have determined their eligibility for a VA loan, they can begin the application process. The first step is to obtain a Certificate of Eligibility (COE) from the Department of Veterans Affairs (VA). The COE verifies a veteran's eligibility for a VA loan and is required by lenders to approve a loan. Veterans can apply for a COE online through the VA's eBenefits portal or by submitting a VA Form 26-1880.

After obtaining a COE, veterans can begin searching for a lender. It's important to choose a lender who has experience with VA loans and understands the unique benefits and requirements. Veterans can use the VA's lender search tool to find a lender who specializes in VA loans in their area.

Once a lender has been chosen, veterans will need to provide documentation such as income verification, tax returns, and bank statements. The lender will also order an appraisal of the property to ensure that it meets VA standards. Once the loan is approved, veterans can move forward with closing on the home and becoming homeowners.

In conclusion, VA loans in Texas offer many benefits to eligible veterans and their families. From low-interest rates to no down payment requirements and no PMI, VA loans can make homeownership more accessible and affordable for veterans. If you are a veteran and are interested in purchasing a home in Texas, be sure to explore the benefits of a VA loan and take advantage of this opportunity.

It's worth noting that VA loans are not only limited to purchasing homes. They can also be used for other purposes, such as refinancing an existing mortgage. Veterans can use a VA loan to refinance their current mortgage, which can result in lower monthly payments or a shorter loan term. This can save veterans money over the life of the loan and allow them to pay off their mortgage sooner.

Another benefit of VA loans in Texas is that they are often easier to qualify for than conventional loans. VA loans have less strict credit score and debt-to-income ratio requirements, which means that veterans with less-than-perfect credit or high levels of debt may still be able to qualify for a VA loan. This can make homeownership a possibility for veterans who may have been turned down for a conventional loan.

It's important to note that while VA loans offer many benefits, there are also some potential drawbacks to consider. For example, VA loans often have stricter property standards than conventional loans, which means that certain types of properties may not be eligible for a VA loan. In addition, VA loans may have higher closing costs than conventional loans, although veterans can negotiate with lenders to try to reduce these costs.

Overall, VA loans in Texas are an excellent opportunity for eligible veterans to become homeowners. With competitive interest rates, no down payment requirements, and no PMI, VA loans can make homeownership more accessible and affordable for veterans. If you are a veteran and are interested in purchasing a home in Texas, be sure to explore the benefits of a VA loan and take advantage of this opportunity.

1 note

·

View note

Text

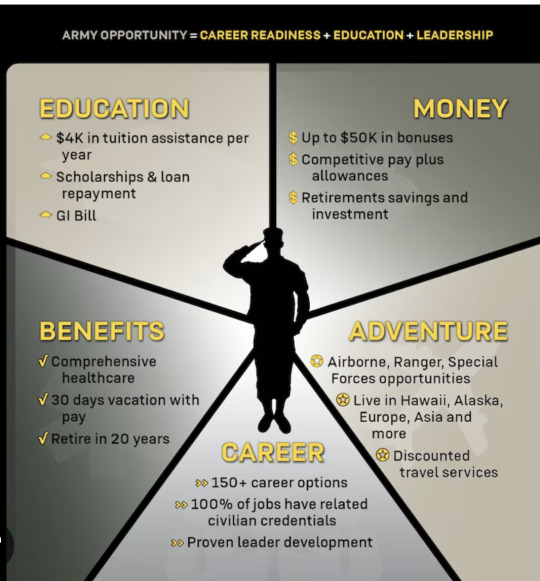

5 Things I Love About Being in the Service

With recruiting as one of the biggest focuses right now when it comes to the service, I decided I’ll do two separate blogs about the 5 things I love about being in the service and 5 major considerations anyone should think about before joining which will come at a later time. I want to start by expressing that everyone experience in the service is different and I can only share things from my view from my career. I am currently an Army Officer with 17 years of service where I hold the rank of Major. I started my career in 2006 by enlisting in the Army Reserves to help pay for school and had no idea it would be my first professional career after college. In 2008 I switched over to the Louisiana National Guard where I was able to respond to various state emergencies such as Hurricane Gustav (2008) and other events within Louisiana. In 2010 I graduated from Northwestern State and commissioned as a 2nd Lieutenant where I have been an active-duty Soldier since. I’ve been deployed to Afghanistan and had a chance to see the world throughout my time of being in.

Educational Benefits

Since graduating high school, I completed 5 college degree programs where the military financially contributed to. During my undergraduate years I served in the Army Reserves for 2 years and the National Guard for 2 years. I took advantage of every opportunity that was available for education and was able to collect on benefits such tuition assistance, the GI Bill, the addition $350/monthly kicker, along with my monthly drill pay. As an undergraduate student, my educational benefits alone were able to fund my monthly bills. When I started my professional career in the Army after graduation, I was able to collect tuition assistance to fund my 1st graduate degree. When going for my Doctorate I was able to use my GI Bill and when I completed my last degree in Kansas the Army paid all the costs since it was a part of the course I was attending. Because of all my years in the service I qualified for programs where any loans I took out were forgiven. My advice to anyone whether you go to college or a trade school is to have the service support whatever goals you have in mind

Financial Stability, Retirement, and Career Potential

The Army gave me that experience of graduating college and immediately working in a career where I could support myself financially. I didn’t know it at the time but the annual salary for an officer who started their career fell within the top 19% in the US at the time. Because I served 4 years as Reservist/National Guard Soldier before starting my active-duty career I was making an additional $1,000 monthly compared to my peers who were just starting. In 2010 as a 2nd Lieutenant, I made $60K and by 2015 I was clearing 100K. The other benefit I is that with more rank that is earned and with every year of just serving we get a raise to help us keep up with the economy. Also, based on the cost of living in certain areas could determine increased benefits such as a higher housing allowance. The base pay of all service members along with benefits is public knowledge online and allows predictably in the future. The Army also have one of the best retirement systems where you can earn a percentage of your salary for the rest of your life at the 20-year mark along with collecting on VA benefits. Also, when getting out and starting my next career it’s 6 figure jobs that I qualify for so the potential of having 3 checks monthly and a financially comfortable lifestyle is possible in my post military career. It can also help when wanting to start my own business or wanting to go to law school which is still a goal of mine.

Medical Benefits

During my time of being in service, I never had to pay for a medical or dentist appointment. I also never had to pay for any prescription medicine. Anytime I had a medical emergency when being away from home, the Army worked with me to get help from the hospital that was close by so I could be seen. I had various procedures conducted and get annual checkups where doctors help me monitor various conditions that run in my family. With highly blood pressure and glaucoma as things I should look out for, I am able to get some of the best resources and information on things I should be on the lookout for to better take care of myself. Because of my benefits I am to get free therapy sessions which really supported me mentally and helped me adjust throughout the years. I was also able to help peers out who were in the service too by sharing resources.

Relationships and Comradery

Being in I’ve been able to come across some great people and build relationships that will last for the rest of my life. It’s a great feeling knowing that I have friends all over the world and people that would help me in time of need when I’m not living close to my family in Louisiana. With moving so much I’ve been able to improve my interpersonal skill and blend in with all types of people. I’ve been able to work with people from all walks of life and gain valuable insight of their story. I’ve also been able use my various networks such as being in a fraternity and had it grow times 10 along with my membership in other organizations. I been able to connect with community leaders and be of services in places that I’ve lived along with impacting the lives of those I served with. If yall talk to any veterans most of them would probably tell you that one of the best things they enjoyed about being in is the people.

Travel & Experiences

Before joining the Army, I never been on a plane or had travels outside the south. The only times I would ever leave Louisiana would be to either to visit my mom side of the family in Mississippi or attend family reunions. Since joining I had the chance to travel all over the world and experience other cultures. I’ve also had a chance to travel all over the United States. Since going active duty in 2010 I’ve moved a total of 7 times and took advantage of every move. Also, with joining the military came unforgettable experiences. I’ve shot and trained with weapons that others could only dream about. I’ve had the opportunity to jump out of planes and helicopter over 20 times, and participate in training that was just downright fun. I was also able to make the best of time in service by attending various military schools that included learning how to jump from planes, packing parachutes, and repelling from helicopters.

Life: Currently I’m supporting training in California but I look forward to coming home to Shreveport at the end of the month for a few days before going back over seas. I l cant wait to just eat good food and catch up with my parents and friends. One thing I’m learning is that other states have decent food but nothing comes close to the food or feelings of just being home 😊.

.

0 notes

Text

Can a reservist get a va loan?

If you are a reservist and you are planning to buy a house and you do not have enough budget to buy a house. So you have a very good option v a loan. Yes friends VA loan is one such loan given to active-duty service members, veterans, and eligible surviving spouses to buy a home, but the question arises whether reservists can take a VA loan or not.

Today in our blog Kabbage Loan Guide, we will discuss this in detail. In the previous article, we told you that Can you buy land with a VA loan? Today we will tell you in this article of ours can an army reservist get a VA loan.

Can a reservist get a VA loan?

Yes, reservists may be eligible for a VA loan if they meet certain eligibility requirements. To be eligible for a VA loan, a reservist must have served for at least six years in the Selected Reserve. National Guard, or another military branch. Reservists must also meet certain credit and income requirements.

Thanks

Please like & share.

0 notes

Text

VA Mortgage Transfer

What is a VA Mortgage?

A VA mortgage is a home loan program established by the U.S. Department of Veterans Affairs (VA) to assist veterans, active-duty service members, and certain members of the National Guard and Reserves in obtaining home loans with favorable terms. These loans are provided by private lenders, such as banks and mortgage companies, but are partially guaranteed by the VA, reducing the risk for lenders.

What is a VA Mortgage Transfer?

A VA mortgage transfer, often referred to as an assumption, allows another qualified individual to take over the existing VA loan, assuming the terms and conditions of the original mortgage. This process can be beneficial for both the seller and the buyer, as it allows the buyer to take advantage of the existing interest rates and terms, which might be more favorable than current market conditions.

Benefits of VA Mortgage Transfer

Lower Interest Rates: If the original loan was taken out during a period of lower interest rates, the new borrower could benefit from these historically low rates, potentially saving thousands over the life of the loan.

No Down Payment: One of the major advantages of a VA loan is the ability to purchase a home with no down payment. This benefit can transfer to the new borrower, making homeownership more accessible.

No Need for New Appraisal: In many cases, a new appraisal is not required during the transfer process, which can save time and money.

Avoiding the Hassle of New Loan Approval: The assumption process is often simpler and faster than applying for a new loan, as it involves fewer steps and less paperwork.

Key Considerations

Eligibility Requirements: The person assuming the VA loan must be a qualified veteran or active-duty service member who meets the VA’s eligibility requirements. They must also have a Certificate of Eligibility (COE).

Creditworthiness: The new borrower must meet the lender’s credit and income requirements to ensure they can take over the mortgage payments.

Release of Liability: The original borrower should seek a release of liability from the lender, ensuring they are no longer responsible for the loan after the transfer. This step is crucial to protect their financial interests.

Funding Fee: The new borrower may be required to pay a VA funding fee, which is a one-time payment made to the VA to help cover the costs of the loan program. This fee varies based on the type of service and the down payment amount.

The Transfer Process

Contact the Lender: The original borrower must first contact their lender to inquire about the assumption process. The lender will provide specific instructions and requirements.

Submit Application: The new borrower must submit an application to assume the loan, along with proof of eligibility and financial documentation.

Review and Approval: The lender will review the application, ensuring the new borrower meets all requirements. This process includes a credit check and verification of income.

Sign Assumption Agreement: Once approved, both parties will sign an assumption agreement, transferring the mortgage from the original borrower to the new borrower.

Finalize the Transfer: The lender will finalize the transfer, updating their records to reflect the new borrower as the responsible party for the mortgage.

Conclusion

A VA mortgage transfer can be an excellent opportunity for qualified veterans and active-duty service members to take advantage of favorable loan terms and conditions. By understanding the benefits, key considerations, and the transfer process, both sellers and buyers can navigate this option effectively. Always consult with a knowledgeable lender or financial advisor to ensure a smooth and successful VA mortgage transfer.

#business leads#commercial#leads#leads generation#best debt settlement leads#debt settlement leads#debt settlement#startup#united states#b2b leads

1 note

·

View note

Photo

The VA says you can apply for a VA loan if you meet the minimum service requirement. According to the VA, you meet the requirement if:

✨Active-duty service members: You’ve served at least 90 continuous days of active duty

✨Surviving spouses: Your spouse is a service member who is missing in action or who died while in service or from a service-related disability.

✨For veterans, National Guard members, or Reserve members: You meet the active-duty requirements for your dates of service

Ready to buy that dream home?💫🏡 Don't miss out on the VA Loan benefit, call us today!

✨📥

Michael Wolff

U Mortgage-Branch Manager

NMLS #239403

NC SC CA FL TN SD AK

.

.

.

.

.

#michaelthebroker #fortbragg #camplejeune #realestate #raleighNC #raleighrealestate #northcarolinaliving #mortgagepro #VAloan #veteransloan #homebuying #homebuyingprocess #firsttimehomebuyers #veterans #military #dreamhome #northcarolina #buyhome #requirements #valoanexpert

0 notes

Text

All you need to know about VA home loans in California

Are you aware about VA home loan? If not, you can read this blog to know all the important points associated with this type of loan. It is a specific type of mortgage offered by the U.S department of veterans Affairs (VA) and is given to qualified borrowers and comes with modest credit. Down payment and debt to income requirement in comparison to conventional loans. VA home loan in California is preferred by first time home buyers who require additional support in housing market. VA home loans are offered by government agencies who join hands with private lenders and lenders are assured that they won’t lose all the money even in a difficult situation.

It is worth noting that VA home loan can only be utilized for purchasing a house if you are going to spend most of your time there. One cannot use this loan to buy vacation, outing or investment property. It can be used to renovate or repair a house or for adding services that benefit people with service-related disabilities.

Common types of VA home loans

VA home loans are of many types and advice from trusted professional mortgage brokers can help in getting ahead with the most suitable loan type. Some common types are mentioned below:

VA home purchase loan

It is a standard mortgage backed by the US department of veteran affairs.

VA jumbo loans

It is a VA home loan in California which exceeds conforming loan limits.

VA renovation loan

It is a VA loan which funds a purchase of a home along with the cost required to renovate the property.

VA cash-out refinance

It is a VA home loan in California that convert’s a home’s equity into cash.

VA rate or term refinance

It allows eligible clients who are not in a VA loan to refinance for the purpose of lowering their rate and changing the terms of their mortgage.

VA interest rate reduction refinance loan (IRRRL)

It works for people who already have a VA loan. The aim is to decrease the monthly interest rate. It requires less documentation and lower VA funding fee. It is also termed as VA streamlined.

VA home loan – know how it works

VA home loans are not issued by US department of veteran affairs. They only determine who qualifies for the loan and associate with private lenders who can issue them. VA home loans in California are considered less risky because they are backed by government body.

Not everyone who has served for the armed forces qualifies for a VA loan. Meeting any of the below mentioned criteria is important:

181 days of active service during peacetime.

90 days of consecutive service during wartime.

6 years of services with National Guard or 90 days of service under Title 32 with at least 30 of those days being consecutive.

You are the spouse (who didn’t remarry) of the service member who lost his or her life during the line of duty or due to service connected disability.

There are additional requirements too and the definition of wartime and peacetime varies as per service tenure. At 4LoanInfo, we provide best advice associate with VA home loan in California.

1 note

·

View note

Text

VA Loan: National Guard VA Loan qualifications 2022 update

Featured photo credit: https://ift.tt/KtJzfbU The VA loan is one of the most powerful home buying tools available to those who qualify. A few benefits of the VA home loan are an option for ZERO down payment, no Private Mortgage Insurance, and lenient credit qualifications. There are specific criteria to qualify for the VA home loan, …

The post VA Loan: National Guard VA Loan qualifications 2022 update appeared first on Benchmark.

The post VA Loan: National Guard VA Loan qualifications 2022 update appeared first on John Seville.

via https://ift.tt/JNFM2oR

0 notes

Text

5 best Tips About national guard va home loan

5 best Tips About national guard va home loan

5 Tips About national guard va home loan You Can Use Today

Below we break down co-borrower necessities and supply popular situations close to co-borrowing and joint VA loans.

6 creditable a long time during the National Guard so you had been discharged honorably or placed on the retired listing

The value of this expanded usage of VA home loans for National Guard associates? It

offers National…

View On WordPress

0 notes

Text

How You Can Get a Low Interest VA Home Loan?

How You Can Get a Low Interest VA Home Loan?

The Veterans Administration of the United States makes it easy for veterans who have served or are serving in all branches of the U.S. military to buy the homes they need with the VA home loan program. This program is a government backed lending program designed to put veterans and their families in the homes they need and want.

The Military home loan is not issued or written by the United States…

View On WordPress

0 notes

Last Seen Blogs