Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by simplifinances and here's what we found interesting.

Average Info

Notes Per Post

0

Likes Per Post

0

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

14 days

Number of Posts By Type

Photo

9

Text

7

Link

1

Last Seen Tumblr Blogs

Fun Fact

Premium Tumblr themes are available from anywhere between $9 to $49.

Photo

Are you scared to invest in the stock market right now because it’s been so volatile? Are you worried about purchasing real estate because the next crash could be around the corner? If you’re currently feeling this way, you’re not alone! Things are obviously crazy and no one really knows what’s going to happen. Here are 6 places you can consider placing your cash for the time being. 💵 Some places are definitely better than others. Click the link in my bio to learn about the best places to stash your cash. https://www.instagram.com/p/CAVWWRyHZiq/?igshid=tmdgb7btfj4c

0 notes

Photo

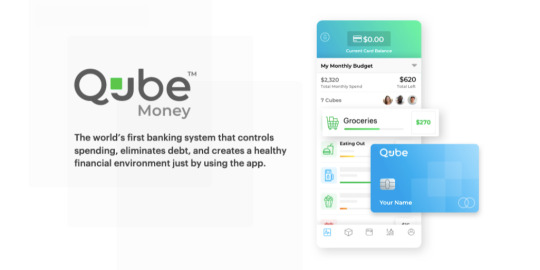

Hey guys! I wanted to let you know that my new company is offering lifetime memberships to the revolutionary budgeting app before it launches. Learn more about the Utah-based company Qube Money by clicking the link in my bio! #personalfinance #budgeting #moneymanagement #fintech #siliconslopes https://www.instagram.com/p/B6IpUkhHBfk/?igshid=tqr9nf9md1w8

0 notes

Text

[BIG NEWS!] I DECIDED TO JOIN THE QUBE MONEY TEAM!

I mentioned two weeks ago that I quit my job as a financial planner. I had a bunch of people reach out and ask me what was happening!

I’m excited to share the new chapter of our lives with you!

The new opportunity is with a fin-tech start-up company based out of Utah called Qube Money (formerly ProActive Budget).

Qube is rebranding and relaunching in spring 2020. I’ve been watching this company since meeting them at FinCon 2018 in Orlando. This past FinCon 2019, I learned they were relaunching and adding new features. So I wanted to find a way to be a part of it!

WHY I MADE THE SWITCH

“85% of people who need help financially can’t afford it.”

This is a quote from Alan Moore of the XY Planning Network at a conference in San Diego two years ago. This has driven me crazy and is one reason why I became a financial counselor.

“Many of the people who most need financial planning services and investment advice can’t afford to pay for either. To be in a position to hire someone to advise you on how to build wealth, you first have to build some wealth,” says Rick Kahler of Brightscope

Seeds of doubt have been planted in my mind for many years. Things like, you can’t make money helping people that don’t have money. But I’ve wanted to find a way to help as many everyday individuals and families with their finances as I can. One of the reasons I started a financial coaching business and this blog.

I’ve worked in academia and helped people in their 20’s. I’ve worked as a financial planner helping clients with their investments. And, I started a financial coaching practice and helped clients pay off debt and start saving. These have all been great opportunities. But it kept coming back to one problem that was hard to solve. Cash flow management.

This is one of the biggest things keeping people from reaching their financial goals and becoming financially independent. I’ve taught people the jar’s money management system with success but it was missing something.

WHY THIS ALIGNS WITH MY PURPOSE

I’ve been interested in the new financial apps that have released over the years like Robinhood, Acorns, Simple, and Varo. They’ve all experienced rapid growth addressing needs for younger people and lowering fees. I’ve thought it would be cool to work for a new company like one of these.

Most would require us to move to San Francisco if I went that route. But this won’t require us to do that. Utah is experiencing insane growth and it’s largely driven by financial service and fin-tech companies.

What’s been done in the past to help people is moving online and I don’t think that will change anytime soon.

MORE ABOUT QUBE MONEY

Qube first launched as ProActive Budget two years ago and did well. They experienced issues with their processor and shut down operations. They’re now with a better processor and rebranding. When you google proactive budget you could probably guess what kept showing in up the search results. Skincare. Which is a big-budget item for a lot of women, apparently!

This video explains what it is:

Qube money requires you to be intentional with your spending. Most people have heard of the cash envelope system because it’s powerful and it helps with spending behavior. The problem is cash is a hassle and writing down each transaction sucks.

Qube is like digital cash envelopes. If you don’t have money in your qube for a certain purchase it will decline the transaction.

No other financial app makes you think before you buy, changes behavior and is effective long-term.

I believe this has the potential to impact millions and help them live healthier financial lives.

I can’t share everything yet but a lot is happening behind the scenes that make this super exciting!

WHAT’S GOING TO HAPPEN TO SIMPLIFINANCES?

Don’t worry, Simplifinances isn’t going anywhere. I’m still trying to figure out what my plan is for 2020. I will most likely scale back on how much I write. For two years, I’ve published one article a week and at times that can be a lot. Especially on top of a full-time job, school, family, church, etc. I may write once or twice a month or whenever I feel like I have something to share.

I’m excited about the new opportunity and feel grateful to be a part of it! This is something I would have never had the opportunity for if I wouldn’t have decided to start Simplifinances.

I don’t write a ton about blogging and growing an online business because that was never my intent from the beginning. But this week I’m going to share a course with you if blogging has been something you’ve wanted to try. I am an affiliate for the course and I think it will give you a great starting point.

Make sure you join my mailing list and look out for an email in the next couple of days.

If you’d like to learn more about Qube and be a part of the launch join the waiting list at www.goqube.io.

0 notes

Text

MY STRUGGLES GETTING INTO THE FINANCIAL SERVICES INDUSTRY

From a young age, I knew I would work in the financial services industry. I wanted to become a writer, a coach, a speaker, or a financial planner. I had a BIG desire to help people, most likely because of the pain I experienced in my childhood.

In high school, my brother and I were into making videos. I decided to venture out on my own and create a video for a contest on a topic that interested me. Financial literacy.

Here it is:

https://youtu.be/eQL2tXw3D7w

I wanted to know why schools weren’t teaching financial literacy early on. Rich Dad Poor Dad convinced me I was better off acquiring assets than sitting in class. Financial literacy was something I knew was practical and important to learn from a young age. However, it certainly didn’t keep me from making financial mistakes.

This video I created was entered into the Utah State High School Film Festival in my senior year. It ended up taking second place. And I received a scholarship of $2,750 to attend any college.

I was stoked! After I graduated, I went to Utah Valley University just down the road from where I lived. I had no idea what to study.

As I completed general college courses, I was working two jobs — car detailing and installing fireplaces. This covered my living expenses and I was able to save some money.

As an elective, I decided to take “intro to personal finance.” UVU was one of the few colleges in the country that offered a degree in personal financial planning which made me think every university must offer a similar degree. I was wrong.

MY FIRST 4 ATTEMPTS TO START WORKING IN THE FINANCIAL SERVICES INDUSTRY

I wanted to find a job in the financial services industry. I first met with an independent financial planner (I didn’t even know what that meant). He said to pass the health and life insurance exam and then I could start selling life insurance. It seemed like a good idea. I studied for the test and failed it. I studied some more and failed again. Health insurance wasn’t interesting and I didn’t care to learn all the rules. So I gave up.

The second time I tried, I was living at my mom’s. A few guys knocked on our door calling themselves “financial planners.” I asked them if I could learn more about what they do. So they brought me into their office and introduced me to their team. The only thing everyone talked about was how many variable life insurance policies they had sold that included investments in gold. I had a bad feeling so I got out of there.

Let me note, I have no problem with sales if it’s something I believe in. I love sales and marketing.

On the third try, I had a good friend who knew I was interested in becoming a financial planner. He took me under his wing and said come to one of our events and I will show you how to become a “financial planner.” He worked for a company called Primerica. I got close to joining their team but decided I didn’t have a good feeling about that either.

Lastly, I met with someone from Transamerica. He said, “the first thing we’ll do is create a list of friends and family and we’ll just start calling them.” I walked out the door.

I NEVER GOT STARTED

It felt like everyone was more concerned about selling products than impacting lives. Too much time was spent figuring out how to start working in the financial services industry but none of these felt right.

So I gave up.

And went back to cleaning cars.

I PURSUED MORE EDUCATION

My dream was to one day be able to graduate from the University of Utah. I finished my associate’s degree at UVU and headed up to Salt Lake City. They had a degree in financial planning but it was suffering from low enrollment. This is when I found out UVU had one of the best programs in the country.

I was kicking myself but decided to pursue a finance degree through the business school. That way if I decided to go into investment banking or private equity I could. I found out quickly I didn’t like corporate finance. My grades suffered and I didn’t get into the finance program. So I gave up and graduated with a degree in Business Administration.

I TRIED TWO MORE TIMES

This drove me, even more, to help people with their finances. Sitting in some fancy office on Wall Street is never what I envisioned. I thought it would be time to finally start working as a financial planner. My buddy worked for North Western Mutual and he set up an interview. I came close to joining them but again, it didn’t feel right to me.

So I thought, “why not work for a company like Fidelity?” No products to push and I can help people. I applied for their Financial Representative position and went through two grueling interviews. I wanted this job. They wanted me to work graveyard shifts and Sundays and I was willing to do it.

A few weeks went by and they told me I didn’t get the job.

I was devastated.

Then I went back to cleaning cars.

I began to think I would never work in the financial services industry.

I BECAME A PEER MENTOR IN COLLEGE

On-campus one day, I came across a program called the Personal Money Management Center. That sparked my curiosity. I could help younger people with basic personal finance and I didn’t have to sell products. The pay was fairly low but I started working there six hours a week and supplemented my income detailing cars to support me and my wife.

I stuck around and became an Accredited Financial Counselor. I helped so many people and was there for almost three years.

Even though so many great opportunities came from being there, my plan was never to stay their long term. It was a great job to have during college but I wanted to become a financial planner. Because I didn’t want to be a financial salesman like all of the others I had met with, I decided to further my education and pursue a master’s degree. I learned that Texas Tech had one of the best programs in the country for financial planning and so I applied.

I PURSUED EVEN MORE EDUCATION

About the same time I decided to pursue my master’s degree, I decided to start a financial coaching business which also turned into this blog. I wanted to reach more people and help them reach financial independence by simplifying their finances. It’s been an incredible journey and I’ve been able to build so many solid relationships with my coaching clients. But I’m not going to lie, it’s been hard at times.

I honestly didn’t know what I was trying to do when I started this but I knew I didn’t want another year or two go by without getting out of my comfort zone and trying something new. I’ve been amazed at how many opportunities have come because of it, even though none of them have allowed me to quit my job.

My purpose in going to Texas was to get my master’s degree. Before packing up the moving truck, I came across a company that was recommended by a faculty member of the program. One of the financial planners was in my home town of Lehi, Utah who completed the same program I was enrolled in. He gave me the chance to work under him and learn from him for a few months before heading to Texas.

I didn’t need a master’s degree to be a financial planner and some questioned my decision. But I didn’t care because I had a strong feeling that this is what I was supposed to do.

I STARTED WORKING FOR A FEE-BASED FINANCIAL PLANNING FIRM

While pursuing my master’s, I worked part-time for this RIA. This was the first time in my life that I felt like I was working in the financial services industry. Something that had taken me years to do. This was a fee-based financial planning firm and I got to experience working with clients, managing money and helping people with their investments.

This was it and I felt like I was going to be there for a long time. But something didn’t feel right. I started to question if being a financial planner was the type of work I wanted to do. I thought, “no Scott, you’ve invested too much time and energy to give up on this.”

Later, I started working full-time but the problem was I didn’t feel like I was helping anyone the way they needed help. I wasn’t having an impact on people’s lives that I thought I would back when I was younger. There’s certainly a need for financial planning and it’s nothing against the firm that I worked with I just felt a disconnect with what I was doing and what I felt my purpose was.

CONCLUSION

So like I mentioned last week, I quit my job as a financial planner and I’m excited to share with you the next chapter of my life. This aligns with my purpose and it’s something I know will have a positive impact on individuals and families all across the country.

0 notes

Text

I Just Quit My Job

Today’s blog post will be short and sweet.

For the past year and a half, I’ve been working for a Registered Investment Advisor as a Financial Planner in Lubbock, Texas.

Today, I’m announcing that I recently just quit my job. It wasn’t an easy decision to quit because I’ve put a lot of time and energy into the company I’ve been working for.

The firm I’ve been working for is a great company and I’ve been able to create some solid relationships and learn a ton in the meantime!

As many of you know I’m still in the process of completing my master’s degree. I started my Master’s in Personal Financial Planning at Texas Tech University in the Fall of 2018. I will still complete it this spring.

Perhaps you’re wondering why I quit my job and what my plan is.

I’ll give you two hints: 1) It’s not financial planning and 2) it doesn’t require me to stay in Texas.

Let’s just say that I’m super excited and will be filling you all in soon.

Stay tuned! :]

0 notes

Text

WHERE TO STASH YOUR CASH

Each dollar of yours is like an employee. If you let them sit around and do nothing, it will hurt your business. If you “employ” them, which means to put to work or make use of, it will benefit your company. Is every dollar of yours benefiting your personal finances or are there lazy dollars sitting around doing nothing for you?

Below I’m going to show you 5 places to stash your cash based on goals that are one to five years away to get the maximum value from each of your green employees.

Depending on your financial goals, where you stash your cash will determine if you reach those goals. If you plan to spend the money within one year, be safe with it. If you plan to spend it in one to five years, go for a higher rate of return.

Where I save my money depends on the goal. I’m willing to invest my savings for something like a vacation fund because the cost of a vacation varies and when we go is flexible. On the other hand, if I’m going to put money down on a house soon I don’t want to lose any of that money.

SHORT-TERM VS. LONG-TERM GOALS

Let’s use three examples of goals:

Saving for a vacation

A down payment on a house

And building an emergency fund

Using these three examples, where is the best place to stash your cash if your goal is one to five years out for each of these?

When it comes to long-term goals like saving for retirement I would look at different options than what is mentioned below.

1. CASH

Some people suggest you keep cash somewhere in your house. Other than the internet disappearing or banks seizing to exist, it doesn’t do you good to have cash under your mattress because those are lazy dollars that need to wake up!

Some people like cash because it’s tangible. If you’re new to budgeting or teaching your kids to manage money, using cash is powerful!

Read: The Jars Money Management System

Cash is good for teaching. It’s a powerful tool because you can hold it and feel it. And let’s be honest who doesn’t love holding a wad of cash! We live in a world where money is more of an abstract idea than a physical object.

Cash is good for changing behavior. I used cash for years as a teenager to manage my money. Now, I don’t have more than $5 – $10 of cash on me unless I am traveling (No thief would be happy to rob me).

If you struggle with spending, cash is harder to spend than swiping a card. According to a study, people spend 17% more money when using a credit card than if they were to use cash.

Other than for behavior change or teaching purposes, I think you’re better off doing something else with your dollars in place of using cash.

Read: Don’t Like Using Cash to Manage Your Money? Try This…

2. SAVINGS ACCOUNT

My bank is my central hub for my money and everything else flows from it. This allows me to transfer money easily to savings, investments or paying bills. The best part is I can track exactly where I spend my money unlike using cash.

Some people don’t like having their money sit in a savings account because most banks pay an interest rate of 0.000Nothing%. I don’t blame them with the average interest rate on savings being 0.06%. But, having money in your savings accounts could be good for a few reasons:

Liquidity – It’s easy to get to when you need it

Security – Your money is FDIC insured up to $250,000

Safety – Essentially no risk (except for one major risk below)

Although the peace of mind of having your money in a savings account is nice, you run a risk of leaving it there. That risk is called purchasing power risk. $100 today will buy you less in 10 years due to inflation. Inflation can fall between 2-4% per year. So if you’re not earning at least enough interest to keep up with inflation, the value of your dollar decreases over time. It’s not a good idea to leave too much money in a savings account.

3. HIGH-YIELD ONLINE SAVINGS ACCOUNT

Many online banks now are willing to pay a higher interest rate to keep up with inflation. Online banks have lower overhead costs because they don’t have to pay for physical branches. That means they can pass the savings to the consumer by offering higher rates. The interest rate is important when you’re looking for a place to keep your money, but it’s not the most important thing. Other things to consider are:

Your savings rate

The credibility of the bank

Terms and conditions

One of the downsides of a high-yield savings account is not having all of your money in one place. If you need to transfer money into your primary bank quickly it could take a couple of days. Don’t put your everyday spending money in one of these accounts. I’ve looked into savings accounts that offer up to 3% APY (Annual Percentage Yield) which is changing all the time. Let me know if you know of any good ones!

BANKS VS. CREDIT UNIONS

When deciding where to stash your cash should you use a bank or a credit union? There are pros and cons to both.

Banks are for-profit enterprises, while credit unions are nonprofits. Credit unions also offer higher interest rates on deposits, lower rates on loans and lower fees.

WHY CHOOSE A BANK?

More branches in the region or across the country

Typically quicker to roll out new apps and new tech

WHY CHOOSE A CREDIT UNION?

Typically has lower fees and higher interest rates on deposits

Emphasis on customer service

I go for the best of both worlds and use USAA for my personal banking and Wells Fargo for my business banking. I’m happy with USAA and would recommend them to anyone. Think of it as an online credit union with low fees, great customer service and always at the front of technology. They were the first bank to introduce biometric sign in. I was using my face to log in to my account back in 2014.

Although I’m happy with USAA, I’m always looking for something better.

4. MONEY MARKET ACCOUNTS (MMA)

Money market accounts are federally insured short-term interest-bearing instruments that generate a variable yield while preserving principal. They tend to have interest rates that are higher than savings accounts, but they often require a higher minimum deposit.

The difference between a savings account and an MMA is what the bank can do with your money. The bank is restricted in how they can loan your money. With an MMA the bank may put your money in a CD, low-risk mutual fund or government securities. Many people have an MMA already and don’t realize it. That’s because in your investment account there is typically cash waiting to be invested that is stored in an MMA. I wouldn’t be too concerned about these accounts for your goals.

5. CERTIFICATE OF DEPOSIT (CD)

A certificate of deposit (CD) acts as a savings account and has a fixed interest rate. It also has a fixed date of withdrawal, known as the maturity date. I call these certificates depression:). If you want to invest your money for the long run the interest rate is measly. Although it’s higher than a typical savings account or money market account your money is going to be locked up for a period of time. For example, at my local credit union the terms of a CD are:

2.00% 1-year CD

2.50% 4-year CD

3.15% 5-year CD

I don’t use CDs anymore because I had a bad experience. I deposited $5,000 into a 2.5 year CD back when I was 19 and made $50 in interest after two years. My car broke down and I needed to access the money early and paid a $25 fee. Then, I had to pay taxes on that $50 which was $7.50. So my $50 return went to $17.50 which is a 0.0035% return. Basically the same as if I would have left it in the bank.

I could have found a better CD and I could not have pulled it out early but either way, I’m not a fan of CDs. I want control over my money and I’m willing to take more risk if I’m going to be saving that money for a few years.

However, CDs seem to fit some people very well and there are many reasons why they may make sense for you. Something that seems to be effective with CDs is called a CD ladder. You open multiple CDs to have access to your money at different times in the future without locking all of your money into one long-term account. I still think there is better places to stash your cash.

BOTTOM LINE

To be honest I don’t use high-yield savings accounts (I may if I find a good one), money market accounts or CDs. I use traditional savings accounts and any other amount of money above that I invest it.

Hopefully, you’ll be able to take away information from this article and apply it to your situation. I didn’t talk about investing. If you would like to read an article I wrote about that:

Read: I Don’t Know How to Invest and I’m Scared I’ll Make a Mistake

These are simply a few ways you can employ your dollars and stash your cash. But, more important than getting the highest interest on your savings is how much money you save.

If you’re having trouble saving money I recommend you set it up automatically. You can set this up with your bank or you could use a tool like Qapital or Digit to do it automatically for you. They don’t have a high APY but they can help you consistently save. I love personal finance technology that helps change behavior!

Where do you stash your cash!?

0 notes

Photo

The newest personal finance/financial independence just released October 1st! This is a book I've been anticipating for quite some time and I'm excited to share it with you. I've had the chance to get to know all three authors and they've put together something that is life-changing. ChooseFI: Your Blueprint To Financial Independence 📘 The ChooseFI book gives you a clear framework on how to live a financially independent life. It begins with the “Stages of FI” which can be compared to the Dave Ramsey “Baby Steps.” Except these are far from baby steps. These are big boy/girl steps. In my opinion, they’re way more difficult. It’s not simply a matter of becoming debt-free, it’s becoming debt-free AND getting to the point where working is optional. Once you reach financial independence, you’ll never have to work another day in your life if you decide not to. Click the link in my bio to read my review of the book! https://www.instagram.com/p/B3mxk94n1Tq/?igshid=180c8tygrzff6

0 notes

Text

ChooseFI Book Review: Your Blueprint to Financial Independence

I remember the first time I learned the difference between an asset and a liability. Sitting on the couch in the living room as a young teenager, I wanted to share my new-found knowledge with my mother. I explained to her the difference between the two knowing that she would be proud of me. She wanted to make good financial decisions so I didn’t make the same mistakes as her.

My mom introduced me to personal finance at a young age because she wanted me to free myself from the poverty cycle we were in. And I couldn’t do that without making solid financial decisions.

She went through two divorces, bankruptcy, and many other financial challenges that could turn anyone into a victim. My father walked out and later committed suicide for a number of reasons (one being financial obligations). But my mom never became a victim and she found a way to improve her situation. We went from being homeless and broke to living a fulfilled and rich life.

I knew what it was like growing up with nothing, I became obsessed with learning how to equip myself with the right tools to one day become financially free. I read books like the Total Money Makeover, Rich Dad Poor Dad and Secrets of the Millionaire Mind which all helped build a foundation and are all great books.

However, after reading many books, I felt like I was learning all there was to know about personal finance. How much is there out there on the topic?

I WAS MISSING SOMETHING

I was missing two things: (1) a community of like-minded people and (2) a way to optimize what I knew. Every book kept telling me that if I just save and invest a small percentage I would be financially free. But financial freedom felt so arbitrary and it didn’t feel like I would ever obtain it.

Then one day, in December of 2017, I was just finishing up college, I came across a podcast of a guy that had just quit his job as a pharmacist. I listened to that episode because I had just joined the Millennial Money Man Facebook group and it was around the time he was on the ChooseFI podcast.

I realized there was a living and breathing community of people interested in the exact same things as me. Two podcast episodes later and decided to start from the very beginning on the ChooseFI podcast. I’m glad that I did because my life will never be the same.

I FOUND MY TRIBE

Along with being a book review, this post is also an inside look and review of the FI community as a whole.

I’ve since had the chance to meet Brad and Jonathan a few times at FinCon as well as get to know Chris Mamula very well who is a fellow Utahn. (Utah is home even though we currently live in Texas).

I was excited to read the new book they were putting together that gives a great overview of this new movement and what a superpower financial independence can be. This stuff is life-changing.

Before I get into sharing what I love about the ChooseFI book, it’s worth noting that soon after I found the FI community, my mom decided to jump on the bus with me. We’re now currently on this path to financial independence together. She introduced me to personal finance, and I introduced her to financial independence.

HERE’S WHAT I LOVE ABOUT THE CHOOSEFI BOOK

The ChooseFI book gives you a clear framework on how to live a financially independent life. It begins with the “Stages of FI” which can be compared to the Dave Ramsey “Baby Steps.” Except these are far from baby steps. These are big boy steps. In my opinion, they’re way more difficult. It’s not simply a matter of becoming debt-free, it’s becoming debt-free and getting to the point where working is optional. Once you reach financial independence, you’ll never have to work another day in your life if you decide not to.

This is what was missing from the idea of becoming financially free. To me, that meant crushing it and buying an island which is something almost no one can achieve.

After telling one of my friends about this online community of people working toward the same goal, he told me was how he liked the idea because it’s something anyone can do.

Reaching financial independence is driven by what your annual expenses are. It forces you to be frugal. What they mention in the book a “Valuist,” which is someone who spends money on what they value and cuts back ruthlessly on the things they don’t.

MINIMALISM AND SIMPLE LIVING

I appreciate how these guys discuss minimalism and simple living at great length. For me, life was never about making as much money as possible, it was about living a meaningful and intentional life. For years I was promised all of these opportunities to make a bunch of money and was sold this lavish lifestyle that never really appealed to me. My desire was to one day live a life of simplicity and independence like Henry David Thoreau.

One of the biggest advantages of reading this book is the fact that they don’t shy away from the nitty-gritty details. Something most financial books, podcasts, and financial planners stay away from because it doesn’t relate to the masses or they want to hold on to the information themselves.

ADVANCED PERSONAL FINANCE TOPICS

I couldn’t believe the education I was getting from reading and listening to the podcast was free. I was learning more practical and applicable information than in business school or a master’s program in personal financial planning. Things like tax optimization, mega backdoor Roth, sequence of return risk, and different investment strategies. They go into a lot of advanced strategies. But at the same time, they keep it simple and easy for anyone to understand.

I couldn’t get enough of it because it was all geared toward helping me make more money, spend less and enjoy the journey. My wife and I were on a date one night (she was sick of me talking about this), and I told her “I found my tribe, these people get it.”

“I FOUND MY TRIBE, THESE PEOPLE GET IT.”

Even though I’m still getting started in my career and I have faced a lot of challenges in my younger years, I can honestly say I feel very grateful to have learned these things at such a young age because I know what kind of impact it will have on me and my family. These are all principles I want to instill in my son, Everett. Which will hopefully one day become 3rd generation FI.

GET YOUR BLUEPRINT TO FINANCIAL INDEPENDENCE TODAY

If the ChooseFI book is a book you already know you want to purchase, you can go ahead and get it on Amazon by clicking the link below! Plus, the holidays are right around the corner and this could be a great gift for someone you think could benefit from the book.

Purchase the ChooseFI Book

0 notes

Text

DON’T LIKE USING CASH TO MANAGE YOUR MONEY? TRY THIS…

After people learn about the money jars system, I get a few who say, “I like the idea of dividing my money up into different jars but I hate using cash.

I’m not a big fan of using cash either. To be honest, I don’t.

After the first two years of using cash, I changed my jars to digital jars. I opened up a few bank accounts when I was 18 years old (it was more like six), but it has been extremely effective in helping me reach my goals. The banker was probably like, “what is this 18-year old doing opening up a bunch of bank accounts? This can’t be good.”

Here’s how to get started.

OPEN ONE CHECKING ACCOUNT

I encourage you to first start out using actual jars — even if you don’t like using cash. You can get started dividing up $100 or less. Physically doing the act is very powerful.

I also encourage you to get the jars if you have kids to teach them how to be smart with money. This is such a simple thing to teach your kids that when they understand it, you’ll be doing a great job as a parent raising money-savvy kids.

After you’ve mastered the physical jars go to your bank and open up a checking account. I imagine most of you reading this will already have a checking account so you really don’t need to do anything here.

OPEN FIVE SAVINGS ACCOUNTS

If you don’t like using cash, it’s time to transition everything online. You need at least five savings accounts (not checking accounts). Most people only have one saving account so you’re most likely going to have to speak to your bank about this.

Once those are set up, divide the money up into the bank accounts just like you would the jars. You’re WAY less likely to transfer the money out of your savings account and spending it than you would if the funds were sitting in your checking account.

Most people are terrible savers because they try to keep a running tab in their head and then at the end of the month they tell themselves that whatever is leftover they will transfer it to savings. And guess which account never grows? Yep, you guessed it. You have to learn how to pay yourself first!

It’s important to note that legally you cannot treat a savings account as a checking account. Federal law prohibits you from withdrawing from a savings account more than six times in one month. So if you transfer the money into a savings account don’t be buying stuff out of that account.

Think of your checking account like the hub and everything else stems from it. The checking account is like the trunk of a tree and the savings accounts are like branches. Your money comes into your checking account and the first thing you do is divide 10% here and 10% there.

I’ve never run into an issue of having to withdraw money from a savings account more than six times in one month. But it’s worth mentioning.

FIND A BANK THAT DOESN’T CHARGE FEES

This next idea is extremely important. If you have a bank that will let you open five savings accounts with no problems, you’ve got a great bank. But if you’re bank tells you, “sorry, we’re going to have to charge you to open up more than one bank,” I want you to switch banks.

What you might be thinking:

“First Scott tells me to use this budgeting system for the rest of my life, and now he’s telling me I need to change banks, is this guy crazy?” Yes, most of the “BIG” banks, Wells Fargo, Chase, Bank of America may charge you additional fees for having additional savings accounts if you don’t maintain a minimum balance, or set up automatic transfers.

I hate paying fees. You should never have to pay a fee for having a savings account. The interest rate on savings accounts is already horrific.

Here’s your script when you go to sit down with your banker and they tell you they have to charge you a fee for more than one savings account:

Mr. Banker: We will have to charge you a fee for more than one savings account. You: Thank you mister banker, but it’s important that I have five savings accounts and pay no fees. A bank down the road said they would do it so I guess I will have to take my business there.

Mr. Banker: I will see what I can do.

THE BANK WANTS YOUR BUSINESS

The bank wants to keep your business and I’ve heard they will wave the fees in many cases. But, if they say, “sorry we cannot change that,” I promise there are hundreds of other banks that will. I’ve never heard of a credit union not willing to do that for you.

I asked my credit union how many bank accounts I could open without paying fees, and they said, “as many as you would like.” I said, “really?” She said, “we have a customer who has 63 bank accounts with us and that’s totally fine.”

My bank is USAA and I’ve had a great experience paying no fees and having multiple savings accounts. I would highly encourage you to open your accounts with them if you have access to them. Most people don’t unless you or a family member is or has been in the military.

The bottom line is DO NOT PAY FEES.

THIS WORKS IF YOU SPEND LESS

I already know many of you are thinking, “this isn’t possible in my situation because I don’t make enough money.” You can read ways to make more money here. However, the most overlooked way to make this system work is by spending less.

If you’re serious about financial independence, not only do you need to make more money, you need to keep as much of it in your wallet as possible.

We’re constantly bombarded with marketing messages telling us we need to spend money to be happy. This is not true! Live simply and be grateful for what you have and you’ll be amazed how much you can save.

Read: 8 Ways Minimalism and Personal Finance Are Related

People only spend less when they have to. Be content with what you have and look for ways to save money, you can make this system work.

So, if you don’t like using cash, this is what I did to transition everything to digital jars.

0 notes

Photo

3/4th of the way through the year and 75% contributed to the good ole Roth! 🙌🏽 We decide to max out the Roth IRA each year because the contributions are after-tax dollars. Which means when we go to withdraw the funds we won’t have to pay taxes on the back-end. I like to think of it like paying taxes on the seed instead of the harvest.📈 There’s certainly advantages to a deferred compensation plan like a 401k like tax deferral which allows compounding interest to do it’s thang! Sadly, I don’t have that benefit through work and my wife is self-employed. So if you have a 401(k) or 403(b) plan, you should definitely be taking full advantage of that and any employer match you may get. For those that don’t have that, we’ve got the Roth IRA. If you would like to learn every investing mistake that I’ve made since I started a Roth IRA many years ago, click the link in my bio!👆🏼 If you haven’t started a Roth IRA, maybe it’s time you look into it! https://www.instagram.com/p/B3Nlwl9H1Ct/?igshid=qd0da14ommj6

0 notes

Text

USING THE MONEY JARS SYSTEM TO MANAGE YOUR MONEY

Let’s be honest, there are hundreds of ways to manage your money. But today, I’m going to tell you why the money jars system that I use to manage my money is the most effective.

I tried the cash envelope system (which became messy), I tried saving everything in one savings account (which felt like deprivation), and I even tried not managing my money at all.

None of these things worked for me.

WHEN I LEARNED ABOUT THE MONEY JARS SYSTEM

We were poor growing up. And I never wanted to be poor again. I knew I needed to change things to make sure I never had money problems.

When I was 16, I learned the importance of managing my money over a long period of time so I could reach financial freedom one day. Luckily, I applied what I learned with a simple money jars system to manage my money.

This set the foundation for the rest of my life. I have successfully used the money jars system to manage my money for over 10 years. I’m well on my way to becoming financially independent by simply using the money jars system I’m about to share with you.

WHAT IS THE MONEY JARS SYSTEM?

After learning about the jar's money system, I purchased 5 mason jars and used a random popcorn box because Walmart didn’t sell mason jars in packs of 6. To get started you’ll need 6 physical mason jars.

MONEY JAR #1

The first money jar is for necessities. Each time you get paid, 50% of your money will go into this first money jar. This money will be used for things like housing, transportation, and food. Spending that takes up 70 – 80% of people’s budget. You’re going to learn how to get this spending down to 50% of what you make.

This requires decreasing your expenses and spending money on things you absolutely have to. This will require major discipline on your end.

Even after trying new things, you can only cut so far on your expenses. And in some cases, it requires increasing your income at your job or through a side hustle.

Learn more about how to increase your income if you feel you don’t make enough money.

Read: The Ultimate Guide to Making Side Income

MONEY JAR #2

The second money jar is your financial independence jar. 10% of every dollar you make no matter what goes into your financial independence jar. Even if it’s a small amount of money, this will help you build the habit of saving money each time you get paid.

Should you save or pay off debt? The answer depends. I don’t think that you shouldn’t save money until all of your debt is paid off and you have an emergency fund of 3 to 6 months. I think you should be doing both. Saving while paying off debt?

Once you understand compound interest, this will make more sense. The more money you can save early in life the better off you will be. So get started saving 10% of your income no matter what even if you have student loans or a car payment.

MONEY JAR #3

The third jar of money is long-term savings of 10%. What’s the difference? Financial independence money will be spent when you become financially independent. That money will sustain your lifestyle.

Long-term savings has two functions: save for a down-payment on a house, pay cash for a car or to build up assets like starting a business. The second purpose this money jar serves is it can act as an emergency fund.

I’ve discovered setting money aside in a savings account labeled “emergency fund” doesn’t work. Because guess what happens? An emergency! And the money gets spent.

I building an emergency fund over and over again and the money always gets spent. The only thing that allowed me to actually have money in case of an actual emergency was if the money was going towards something else like a down payment on a house. In case of an actual emergency, the money was there and it meant we had to delay when we would buy a house.

MONEY JAR #4

The fourth money jar is tithing/give. I believe in paying a 10% tithe to my church. It goes a lot deeper than simply giving 10% to my church. I truly believe that when you have the mentality to give, you’re looking at life with an abundance mentality. This will spill over into other things.

I don’t want you to have a scarcity mindset. That’s no way to live! 10% doesn’t have to go to a church, it could go to your favorite charity or you could even use the money for birthday and Christmas gifts. Either way, when you give, you look at life in a different lens.

MONEY JAR #5

The 5th money jar is play money to blow. 10% of your income will be set aside and spent on whatever your heart desires. This is non-guilty spending and it will help you to maintain balance in your life.

10% of your money should be going toward things you love to spend money on and if you could choose to spend more, you would totally do it. Things like weekend getaways, expensive date nights, massages, concerts, fairs, whatever you want.

“Life is meant to be enjoyed, not just endured.”

If you’re paying more than 5 – 7% interest on any debt, you should be paying that off and not spending money on play. This is about priorities and you can’t afford to be flushing money down the drain each money on high-interest debt. Pay off that high-interest debt, then you’ll be able to start spending more money on things that you value.

MONEY JAR #6

The last money jar is for education and is probably the most flexible jar. Invest 10% in yourself and your skills. Pay for college, buy courses, books or anything that will help you increase your skills.

“The best investment with the highest ROI is an investment in yourself.”

Setting aside money for education could do more for you than any other jar. You should be doing this if you’re able to master all of the money jars above.

However, If you’re unable to live off 50% of your income or you’re paying off a lot of high-interest debt, you should be using the money from your education jar to pay for those things.

CONCLUSION

If you’ve tried managing your money in the past and it didn’t work, what do you have to lose by giving the money jar system a try?

This will help you build a foundation for financial wellness and allow you to live the life you’ve always wanted to live.

Using cash can be difficult for a lot of people and I get the question, “how can I use this money jars system digitally?” And my answer is you absolutely don’t have to use physical jars. I recommend it starting out but you can do the exact same time with your bank accounts.

I will be sharing an article next week about what to do if you don’t like using cash to manage your money.

You can also sign up for the free course on learning how to manage your money with the money jars system where I give you the step-by-step guide you need to get started in 7 days.

Sign up HERE! You’ll be glad you did!

0 notes

Photo

[NEW BLOG POST] Here’s the money management system that will get you to financial independence if you follow it. It will also help you enjoy the journey along the way! Click the link in my bio to learn more and get your free PDF on how to start using this money management system!!! 👉🏼 Follow @simplifinances for more!

https://www.instagram.com/p/B3HhRMBHd28/?igshid=1m2ydx9iz70xd #moneymanagement #managemoney #manageyourmoney #money #budget #budgetsystem #budgetingsystem #moneyjars #jarssystem #jarsmoneymanagement #thejarsmoneymanagementsystem #moneymanagementsystem #jarsofmoney #jars #cashinjar #jarmethod #moneyjarsystem #simplifinances #financialindependence #financialfreedom #ficommunity #firecommuity #debtfree #debtfreecommunity #frugal #minimalism #teachmykidsmoney #financialwellness #enjoylife #personalfinance

0 notes

Link

Are you tired of feeling like you have no control over your spending? Do you look at your money at the end of the month and wonder where it went?

If you answered yes to one of those questions, maybe it's time to get serious about managing your money! This article covers what I believe to be one of the most effective money management techniques.

Don't let another day go by without doing something to get a little better with your money!

#moneymanagement #moneyjars

0 notes

Photo

👉🏼GIVEAWAY!!!👈🏼 To build awareness for my new course I’m giving away two $25 Apple store gift cards to two individuals! Here’s how to win: 1. Make sure you are following @simplifinances 2. Like this post 3. Tag 3 people in separate comments 4. Click the link in my bio and sign up for the FREE 7 day Transform Your Finances email course! Optional for more entries - Share this post in your story and tag us! That’s it! Winner will be announced randomly on Monday, Sept. 30 here on this post. You must be signed up for the course to win! https://www.instagram.com/p/B26p7-DnKJ6/?igshid=9kxpewun6a35

0 notes

Photo

Personal finance is 80% behavior and 20% numbers. For most people tax optimization and maximizing your savings rate isn’t necessarily going to get you where you want to be. It’s a simple matter of living on less than you make. Tag a friend! Follow @simplifinances for more! https://www.instagram.com/p/B2y3msEH7fG/?igshid=vbfozdiaoq7j

0 notes

Photo

5 years go today, I asked for my wife’s hand @m__kenzie in marriage. What was she thinking!? I must have had her under some spell because she was crazy enough to say yes! If you’re curious how I proposed to my wife 5 years ago click the link in my bio. You’ll be able to see the video and read about our story. It’s hard to believe our proposal video has over 3.5 million views! #proposal #marriage #5years #proposalvideo #happilymarried #marriageproposal #married #marriedlife #marriedliferocks #moneymanagement #managemoney #manageyourmoney #money #budget #budgetsystem #budgetingsystem #moneyjars #jarssystem #jarsmoneymanagement #thejarsmoneymanagementsystem #moneymanagementsystem #jarsofmoney #jars #cashinjar #jarmethod #moneyjarsystem #simplifinances https://www.instagram.com/p/B2wPAFDniwX/?igshid=wkde6zw9jdhm

#proposal#marriage#5years#proposalvideo#happilymarried#marriageproposal#married#marriedlife#marriedliferocks#moneymanagement#managemoney#manageyourmoney#money#budget#budgetsystem#budgetingsystem#moneyjars#jarssystem#jarsmoneymanagement#thejarsmoneymanagementsystem#moneymanagementsystem#jarsofmoney#jars#cashinjar#jarmethod#moneyjarsystem#simplifinances

0 notes

Photo

BOOM! The new website is live and along with it I’m officially dropping the new 7 day transform your finances email course! Is all you have to do is head over to www.simplifinances.com and sign up for the new course for free. Let me know what you think of the new website, my team and I have been putting a lot of work into the new changes and I’m excited for what’s in store. Sorry for anyone that has tried to visit the website in the past day or two. It did experience some down time getting things switched over. Go sign up for the course! You’ll be glad you did! https://www.instagram.com/p/B2nQGtaHOeu/?igshid=nf1wm79hvpz8

0 notes