#Automotive Plastics Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Users from the US are the majority of Tumblr visitors.

Text

Automotive Plastic Compounding Market: Innovations in Lightweight and High-Performance Materials

Global Automotive Plastic Compounding Market size and share is currently valued at USD 3.30 billion in 2024 and is anticipated to generate an estimated revenue of USD 6.17 billion by 2034, according to the latest study by Polaris Market Research. Besides, the report notes that the market exhibits a robust 6.5% Compound Annual Growth Rate (CAGR) over the forecasted timeframe, 2025 – 2034 Market…

#Automotive Plastic Compounding Market#Automotive Plastic Compounding Market 2025#Automotive Plastic Compounding Market Share#Automotive Plastic Compounding Market Size#Automotive Plastic Compounding Market Trends

0 notes

Text

Plasticizers Market Poised to Reach $26.9 Billion by 2032 – Growth, Trends, and Forecast

Meticulous Research®—leading global market research company, published a research report titled ‘Plasticizers Market—Global Opportunity Analysis and Industry Forecasts (2025–2032)’. According to this latest publication from Meticulous Research®, the plasticizers market is expected to reach $26.9 billion by 2032, at a CAGR of 5.4% from 2025 to 2032.

The growth of this market can be attributed to several factors, including the increasing construction and infrastructure development projects in developing countries and the growing adoption of plasticizers in the consumer goods and automotive industries. However, the fluctuating prices of raw materials restrain market growth.

Additionally, the rising need for eco-friendly plasticizers and the increasing demand for plasticizers in packaging materials manufacturing are expected to create market growth opportunities. However, stringent regulations for plastic products are a major challenge for the players operating in this market.

Key Players:

The plasticizers market is moderately competitive due to the presence of many large and small-sized global, regional, and local players. The key players operating in the plasticizers market are UPC Technology Corporation (Taiwan), Exxon Mobil Corporation (U.S.), BASF SE (Germany), Evonik Industries AG (Germany), Eastman Chemical Company (U.S.), Aekyung Chemical (South Korea), LG Chem, Ltd. (South Korea), DIC Corporation (Japan), Kao Corporation (Japan), Avient Corporation (U.S.), Polynt S.p.A. (Italy), KLJ Group (India), Arkema Group (France), Perstorp AB (Sweden), The Dow Chemical Company (U.S.), and Nan Ya Plastics Corporation (Taiwan).

The plasticizers market is segmented by type and end-use industry. This study also evaluates industry competitors and analyzes the plasticizers market at the regional and country levels.

Among the plasticizer types studied in this report, in 2025, the phthalate plasticizers segment is expected to dominate the plasticizers market with the largest share of over 47%. Phthalate plasticizers’ popularity due to their relatively lower costs, low volatility, and ability to create very elastic materials supports the segment’s dominant position in the plasticizers market. Additionally, phthalate plasticizers’ effectiveness in improving the flexibility, durability, and workability of plastics, the growing use of phthalate plasticizers in products such as vinyl flooring, coatings, pipes, and wiring insulation, and the extensive application of Diisononyl Phthalate (DINP) and Diethylhexyl Phthalate (DEHP) in PVC products also contribute to the segment’s large share.

Among the end-use industries studied in this report, in 2025, the building & construction segment is expected to dominate the plasticizers market with the largest share of over 35%. In building & construction applications, plasticizers are used as reducers and added to concrete to make it softer, improve its workability and strength, and reduce its water requirements. Rapid urbanization and infrastructure development and the growing use of plasticizers to enhance the flexibility, durability, and workability of construction materials support the segment’s large share in the plasticizers market.

Among the geographies studied in this report, in 2025, Asia-Pacific is expected to dominate the plasticizers market with the largest share of over 53%, followed by North America, Europe, Latin America, and the Middle East & Africa. Ongoing industrialization in APAC countries, including China, South Korea, and India, the increasing use of plasticizers to enhance the performance and flexibility of products, growing construction activities across APAC countries, and the increasing adoption of advanced packaging solutions among food processors support the region’s large market share.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6022

Key Questions Answered in the Report:

Which are the high-growth market segments based on type, end-use industry, and geography?

What was the historical market size for plasticizers globally?

What are the market forecasts and estimates for the period 2025–2032?

What are the major drivers, restraints, opportunities, and challenges in the plasticizers market?

Who are the major players, and what shares do they hold in the plasticizers market?

What is the competitive landscape like in the plasticizers market?

What are the recent developments in the plasticizers market?

What are the growth strategies adopted by major players in the plasticizers market?

What are the key geographic trends, and which are the high-growth countries?

Who are the local emerging players in the plasticizers market, and how do they compete with the other players?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#The Plasticizers Market is projected to grow significantly#reaching $26.9 billion by 2032. This report analyzes market size#share#trends#and forecasts by type (phthalate#non-phthalate#bio) and end-use industries#including building & construction (wires & cables#flooring#roofing)#automotive#and packaging.

0 notes

Text

#Automotive Plastics Market Market#Automotive Plastics Market Market Share#Automotive Plastics Market Market Size#Automotive Plastics Market Market Research#Automotive Plastics Market Industry#What is Automotive Plastics Market?

0 notes

Text

#Automotive Plastics Market#Automotive Plastics Market size#Automotive Plastics Market share#Automotive Plastics Market trends#Automotive Plastics Market analysis#Automotive Plastics Market forecast#Automotive Plastics Market outlook#Automotive Plastics Market overview

0 notes

Text

Flame Retardants Market demand analysis and regional outlook across key end use industries

The Flame Retardants Market is expanding rapidly due to its essential role across sectors like construction, electronics, automotive, and textiles. With growing safety regulations, fire prevention measures, and technological developments, demand patterns vary notably across regions and end-use applications.

Rising Global Demand and Key Drivers

Flame retardants are crucial in preventing fire-related hazards and are increasingly used in products that require compliance with fire safety standards. Their demand is primarily driven by strict building codes, growing awareness about safety, and the rising use of electronic devices globally. Regions such as North America, Asia Pacific, and Europe are showing consistent growth, but with distinct trends and preferences.

In North America, the growth is linked to infrastructure development and industrial safety compliance. Europe shows preference for non-halogenated and eco-friendly retardants, while Asia Pacific leads in manufacturing volume, driven by strong electronics and construction markets in China, India, and Southeast Asia.

Industry-Specific Growth Patterns

Construction is a leading end-use sector for flame retardants, especially in residential and commercial buildings. Flame retardant materials like insulation, wires, cables, and structural plastics are essential for fire prevention. Demand in this sector is increasing in urbanizing regions such as Asia Pacific and the Middle East due to rising construction activities.

Electronics is another significant segment where flame retardants are used in circuit boards, housings, and connectors. As global demand for smartphones, smart TVs, and electronic vehicles grows, so does the use of flame retardants. Asia Pacific, being the hub of electronics manufacturing, is the biggest contributor here.

Automotive applications include upholstery, engine components, and electrical systems. With electric vehicles becoming mainstream, manufacturers are increasingly using flame-retardant materials to ensure passenger safety and battery protection.

Textiles represent a niche but fast-growing sector, especially for specialized garments, furniture fabrics, and industrial uniforms. The demand is rising in both developed and developing economies where fire-resistant clothing is mandated.

Regional Outlook and Market Hotspots

North America remains a mature market but shows steady demand due to regulations like the National Fire Protection Association (NFPA) codes and strong construction activity. The U.S. dominates the region’s share, followed by Canada.

Europe focuses on sustainability and safety, with strict REACH regulations and increased use of non-toxic flame retardants. Germany, France, and the UK are the leading contributors. There's a growing preference for phosphorous-based and mineral-based retardants due to environmental concerns.

Asia Pacific is the fastest-growing region, supported by expanding electronics, automotive, and textile industries. China leads in production and consumption, with India and Southeast Asia catching up rapidly. Governments in the region are also tightening fire safety norms, which is fueling further demand.

Latin America and the Middle East & Africa are emerging markets. Although smaller in size, infrastructure growth and industrial development are increasing the demand for flame retardant materials, especially in commercial real estate and energy projects.

Market Challenges and Demand Constraints

Despite the growing demand, the market faces a few constraints. Halogenated flame retardants are under scrutiny for their potential health and environmental effects, prompting stricter regulation and replacement with alternatives. Also, regional disparities in enforcement of safety standards sometimes slow market penetration in emerging areas.

Another issue is raw material volatility, which can impact pricing and production planning. For instance, supply chain disruptions in Asia Pacific or geopolitical instability in Europe may lead to fluctuating costs.

Future Outlook and Regional Forecast

The future of the flame retardants market is rooted in innovation and regional adaptability. Demand is expected to grow significantly over the next decade, with Asia Pacific continuing to dominate in volume and Europe and North America setting trends in sustainability. Emerging economies in Africa and Latin America are projected to witness stronger growth as infrastructure and industrial development accelerate.

Growth will likely be supported by rising R&D in eco-friendly compounds and a growing emphasis on safety standards across all industries. Companies that align their offerings to regional preferences—like halogen-free products in Europe or cost-effective solutions in Asia—will have a competitive edge.

Conclusion

The global flame retardants market shows strong regional diversity in demand, influenced by regulations, industrial activities, and consumer preferences. Each major end-use industry—construction, electronics, automotive, and textiles—offers unique growth opportunities that vary by region. Companies looking to succeed in this space must adapt to regional market dynamics, invest in sustainable alternatives, and align with evolving safety standards.

#FlameRetardants#ConstructionSafety#ElectronicsIndustry#FireProtection#MarketTrends#AsiaPacificGrowth#SustainableMaterials#FireSafety#MarketAnalysis#GlobalExpansion

3 notes

·

View notes

Text

Zero Friction Coatings Market: Charting the Course for Enhanced Performance and Sustainable Solutions

The global zero friction coatings market size is estimated to reach USD 1,346.00 million by 2030 according to a new report by Grand View Research, Inc. The market is expected to expand at a CAGR of 5.6% from 2022 to 2030. Growth can be attributed to the fact that these coatings reduce friction and wear resulting in low fuel consumption and less heat generation. According to the European Automobile Manufacturers' Association, 79.1 million motor vehicles were produced across the globe in 2021 which was up by 1.3% as compared to 2020. Zero friction coatings can extend the time between component maintenance and replacement, especially for machine parts that are expensive to manufacture.

Zero Friction Coatings Market Report Highlights

In 2021, molybdenum disulfide emerged as the dominant type segment by contributing around 50% of the revenue share. This is attributed to its properties such as low coefficient of friction at high loads, electrical insulation, and wide temperature range

The automobile & transportation was the dominating end-use segment accounting for a revenue share of more than 35% in 2021 due to the rapid growth of the automotive industry across the globe

The energy end-use segment is anticipated to grow at a CAGR of 5.7% in terms of revenue by 2030, owing to the excessive wear on the drill stem assembly and the well casing during the drilling operations in the oil and gas sector

In Asia Pacific, the market is projected to witness the highest CAGR of 5.8% over the predicted years owing to the presence of car manufacturing industries in the countries such as Japan, South Korea, and China

For More Details or Sample Copy please visit link @: Zero Friction Coatings Market Report

Several applications in the automobile industry use wear-resistant plastic seals that require zero tolerance for failure and lifetime service confidence. Increasing demand for the product from the automotive industry across the globe for various applications including fuel pumps, automatic transmissions, oil pumps, braking systems, and others is expected to drive its demand over the forecast period.

Low friction coatings can be used in extreme environments comprising high pressure, temperatures, and vacuums. These coatings can provide improved service life and performance thereby eliminating the need for wet lubricants in environments that require chemicals, heat, or clean room conditions. The product containing molybdenum disulfide (MoS2) are suitable for reinforced plastics while those free from MoS2 are suitable for non-reinforced plastics.

Zero friction coatings are paint-like products containing submicron-sized particles of solid lubricants dispersed through resin blends and solvents. The product can be applied using conventional painting techniques such as dipping, spraying, or brushing. The thickness of the film has a considerable influence on the anti-corrosion properties, coefficient of friction, and service life of the product. Its thickness should be greater than the surface roughness of the mating surfaces.

ZeroFrictionCoatingsMarket #FrictionlessTechnology #CoatingInnovations #IndustrialEfficiency #ZeroFrictionSolutions #AdvancedMaterials #SurfaceCoatings #ManufacturingAdvancements #GlobalIndustryTrends #InnovativeCoatings #PerformanceOptimization #MechanicalSystems #SustainableTechnology #IndustrialApplications #FutureTech #InnovationInMaterials #EfficiencySolutions #ZeroFrictionMarket #TechnologyInnovation #EngineeringMaterials

#Zero Friction Coatings Market#Frictionless Technology#Coating Innovations#Industrial Efficiency#Zero Friction Solutions#Advanced Materials#Surface Coatings#Manufacturing Advancements#Global Industry Trends#Innovative Coatings#Performance Optimization#Mechanical Systems#Sustainable Technology#Industrial Applications#Future Tech#Innovation In Materials#Efficiency Solutions#Zero Friction Market#Technology Innovation#Engineering Materials

2 notes

·

View notes

Text

Blow Molded Plastics Market Global Industry Share Size Future Demand Emerging Trends Region By Forecast To 2034

Understanding the Dynamics of the Blow Molded Plastics Market

Introduction

The Blow Molded Plastics Market is a dynamic sector witnessing steady growth owing to its diverse applications across various industries. This article delves into the intricacies of the market, exploring its dynamics, key segments, applications, and regional influences.

Market Overview

The Global Blow Molded Plastics Market is expected to witness substantial growth, with a projected valuation of USD 89.6 billion in 2023 and an estimated rise to USD 149 billion by 2032, exhibiting a CAGR of 5.6% during the forecast period (2023-2032).

VISIT For a Free PDF Sample Request@ https://dimensionmarketresearch.com/report/blow-molded-plastics-market/request-sample

Understanding Blow Molding

Blow molding stands as a pivotal method for crafting hollow plastic items using thermoplastic materials. The process entails heating and inflating a plastic tube, known as a preform, positioned between molds tailored to the desired product. Subsequently, air is introduced to inflate the tube, shaping its walls to match the mold's contours. Following the blowing stage, the product undergoes cooling, ejection, trimming, and preparation for subsequent processes.

Basic Steps in Blow Molding

Market Dynamics

The demand for blow-molded plastics is primarily driven by the packaging and automotive sectors. Plastic containers, bottles, and various packaging materials find extensive use in packaging food, beverages, personal care items, and household chemicals. Additionally, blow-molded plastics are favored in the automotive industry for crafting lightweight components such as air ducts, fuel tanks, and interior trims.

Environmental Concerns

Despite their advantages, blow-molded plastics have raised concerns regarding their environmental impact, particularly regarding plastic waste and pollution. Heightened awareness of plastic pollution has led to a shift toward more sustainable alternatives, prompting regulatory actions and consumer preferences for eco-friendly options.

Recent Developments in the Blow Molded Plastics Market (2023-2024)

Here are some noteworthy developments in the Blow Molded Plastics Market, along with the years they occurred:

Growth and Trends:

Grab This Report Here@ https://dimensionmarketresearch.com/checkout/blow-molded-plastics-market

Research Scope and Analysis

By Type

Extrusion blow molding holds a significant share of the market, creating durable and lightweight plastic products ideal for packaging applications. The lightweight nature of these products reduces transportation costs and environmental impact while maintaining structural integrity.

By Resin

Polyethylene leads the market in resin categories, owing to its widespread utilization in electrical, electronics, and packaging sectors. Polyethylene terephthalate (PET) also sees extensive use in packaging, particularly for beverages and food items.

By Application

The packaging segment dominates the blow-molded plastics market, driven by high consumer spending in developing countries. Additionally, the automotive and transport sector exhibits significant growth, fueled by the increasing use of plastics in car parts and the surge in e-car manufacturing.

Regional Analysis

The Asia-Pacific region emerges as a dominant force in the global blow molded plastics market, securing a substantial share of global revenue. The region's rapid urbanization has led to increased demand for plastic items in construction, contributing to market growth.

Prominent Players in the Market

Several key players contribute to the growth and development of the Blow Molded Plastics Market, including:

FAQs

1. What is blow molding, and how does it work?

Blow molding is a method used to craft hollow plastic items from thermoplastic materials. It involves heating and inflating a plastic tube, known as a preform, between molds to shape the desired product.

2. What are the primary drivers of demand for blow-molded plastics?

The demand for blow-molded plastics is primarily fueled by the packaging and automotive sectors due to their versatility and lightweight properties.

3. How do environmental concerns impact the blow molded plastics market?

Heightened awareness of plastic pollution has led to a shift toward more sustainable alternatives, prompting regulatory actions and consumer preferences for eco-friendly options.

4. Which resin category leads the blow molded plastics market?

Polyethylene holds the maximum share in resin categories, owing to its widespread utilization in various sectors such as electrical, electronics, and packaging.

5. Which region dominates the global blow molded plastics market?

The Asia-Pacific region secures a substantial share of global revenue in the blow molded plastics market, driven by rapid urbanization and increased demand in construction.

Conclusion

The Blow Molded Plastics Market exhibits promising growth prospects, fueled by its diverse applications across packaging, automotive, and construction sectors. Despite environmental concerns, advancements in sustainable materials and manufacturing processes are expected to drive market expansion in the forecast period.

#BlowMoldedPlastic#PlasticManufacturing#PackagingSolutions#PlasticContainers#InjectionMolding#PlasticIndustry#SustainablePackaging#ManufacturingTechnology#PlasticProducts#IndustrialDesign

1 note

·

View note

Text

Top 15 Market Players in Global N-Butanol Market

Top 15 Market Players in Global N-Butanol Market

The global N-Butanol market is highly competitive, shaped by key players operating across North America, Europe, Asia-Pacific, and the Middle East. These companies focus on production capacity, supply chain strength, and end-user engagement.

BASF SE

Dow Inc.

Eastman Chemical Company

Mitsubishi Chemical Corporation

OXEA GmbH

Sasol Limited

PetroChina Company Limited

Formosa Plastics Corporation

Grupa Azoty

INEOS Group Holdings S.A.

KH Neochem Co., Ltd.

Elekeiroz S.A.

LG Chem Ltd.

Andhra Petrochemicals Limited

Perstorp Holding AB

These firms play a crucial role in the value chain of N-Butanol, serving various industries such as paints and coatings, adhesives, textiles, and plastics.

Request report sample at https://datavagyanik.com/reports/n-butanol-market/

Top Winning Strategies in N-Butanol Market

Market leaders adopt diverse strategies to enhance their market share and secure long-term profitability in the evolving N-Butanol landscape. Here are the most prominent tactics:

1. Strategic Expansions & Plant Modernization

Several companies are investing in expanding their production capacity, particularly in Asia and the Middle East, to meet rising demand and reduce logistical costs.

2. Sustainability Integration

Major players are exploring bio-based alternatives and environmentally friendly production methods to align with global sustainability goals and reduce their carbon footprint.

3. Joint Ventures & Strategic Alliances

Collaborations between regional and global chemical firms enable technological exchange, market penetration, and shared infrastructure.

4. Vertical Integration

Firms are integrating upstream and downstream operations to control costs, improve margins, and ensure raw material availability.

5. R&D and Product Innovation

Investment in research and development helps companies improve product quality, explore new applications, and comply with regulatory standards.

6. Geographic Diversification

Establishing a presence in emerging markets allows firms to tap into new customer bases, diversify risk, and adapt to local regulatory frameworks.

7. Customer-Centric Solutions

Customized formulations and flexible delivery models strengthen relationships with end users in the coatings, automotive, and construction sectors.

Request a free sample copy at https://datavagyanik.com/reports/n-butanol-market/

0 notes

Text

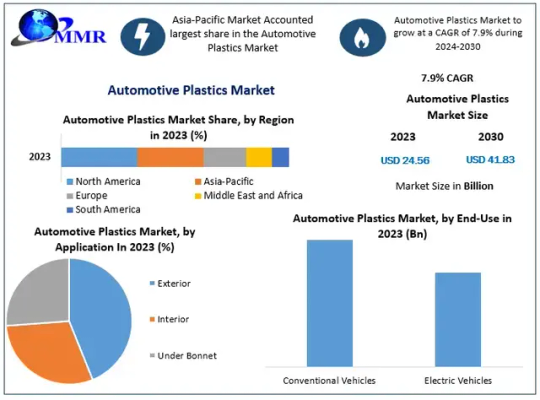

Driving Efficiency: Market Outlook and Demand Drivers for Automotive Plastics

Automotive Plastics Market size was valued at US$ 24.56 Bn. in 2023 and the total Automotive Plastics revenue is expected to grow at 7.9 % through 2024 to 2030, reaching nearly US$ 41.83 Bn.

Automotive Plastics Market Overview:

Maximize Market Research is a Business Consultancy Firm that has published a detailed analysis of the “Automotive Plastics Market”. The report includes key business insights, demand analysis, pricing analysis, and competitive landscape. The analysis in the report provides an in-depth aspect at the current status of the Automotive Plastics Market.

Download your sample copy of this report today!https://www.maximizemarketresearch.com/request-sample/16392/

Automotive Plastics Market Scope and Methodology:

The Automotive Plastics Market requires a mix of both qualitative and quantitative research methods. Automotive Plastics Market information is gathered through different research methods including expert advice, primary and secondary research, both qualitative and quantitative. Primary research gathers important data from interviews, surveys, questionnaires, and input from industry experts, customers and other sources either in person or over the phone.

The report provides in-depth analysis on different strategies used by leading companies, such as partnerships, mergers, acquisitions, and collaborations. The report conducted a SWOT analysis to evaluate the company's market position through identifying its strengths, weaknesses, opportunities, and threats. Analytical techniques, such as examining investment returns, conducting a feasibility study, and using Porter's five forces analysis, were employed to assess the Automotive Plastics market. The bottom-up approach was used to determine the global and regional Automotive Plastics market sizes.

Automotive Plastics Market Regional Insights:

The Automotive Plastics Market report is segmented into various key countries. Countries such as North America (United States, Canada, Mexico), Europe (United Kingdom, Germany, France, Spain, Italy, Rest of Europe), Asia Pacific (China, India, Japan, Australia, South Korea, ASEAN countries, other APAC countries), South America (Brazil), and the Middle East and Africa.

Secure your sample copy of this report immediately!https://www.maximizemarketresearch.com/request-sample/16392/

Automotive Plastics Market Segmentation:

by Product Type

Polypropylene Polyurethanes Polyvinyl Chloride Acrylonitrile butadiene styrene High-density polyethylene Polycarbonates Polymethyl methacrylate Polyamide Polyethylene terephthalate

the PP segment held the greatest market share in 2023. Polypropylene (PP) is another name for polypropene. Polypropylene is a thermoplastic polymer that can be easily molded into almost any shape. Polypropylene is widely utilized in passenger automobiles for a variety of purposes including interior, exterior, and underbody components. Polypropylene, being a commodity plastic is less expensive than other engineered plastics and therefore preferred by engineers over other plastics. Polypropylene is commonly used by engineers to meet the low-cost vehicle design criteria. These variables account for PP's substantial proportion of the automotive plastics market for passenger cars.

by Application

Exterior Interior Under Bonnet

by End-Use

Conventional Vehicles Electric Vehicles

Automotive Plastics Market Key Players:

North America 1. Magna International Inc. 2. Lear Corporation 3. Flex-N-Gate Corporation 4. Faurecia 5. ABC Technologies 6. Algonquin Automotive 7. Celanese

Europe 8. Valeo 9. Forvia Hella 10. Webasto Group 11. ElringKlinger 12. Gestamp Automocion 13. Novares Group 14. HEXPOL

Obtain your sample copy of this report now!https://www.maximizemarketresearch.com/request-sample/16392/

Key questions answered in the Automotive Plastics Market are:

What is Automotive Plastics ?

What is the growth rate of the Automotive Plastics Market?

Which are the factors expected to drive the Automotive Plastics Market growth?

What are the upcoming opportunities and trends for the Automotive Plastics Market?

Who are the leading companies and what are their portfolios in Automotive Plastics Market?

What are the recent industry trends that can be implemented to generate additional revenue streams for the Automotive Plastics Market?

Who are the key players in the Automotive Plastics Market?

What are the different segments of the Automotive Plastics Market?

Which is the fastest growing region in the Automotive Plastics Market?

What growth strategies are the players considering to increase their presence in Automotive Plastics ?

What is the CAGR at which the Automotive Plastics Market will grow during the forecast period?

What segments are covered in the Automotive Plastics Market?

To learn more about the findings of this research, please check:https://www.maximizemarketresearch.com/market-report/global-automotive-plastics-market/16392/

Key Offerings:

Past Market Size and Competitive Landscape

Past Pricing and price curve by region

Market Size, Share, Size & Forecast by different segment

Market Dynamics – Growth Drivers, Restraints, Opportunities, and Key Trends by Region

Market Segmentation – A detailed analysis by segment with their sub-segments and Region

Competitive Landscape – Profiles of selected key players by region from a strategic perspective

Competitive landscape – Market Leaders, Market Followers, Regional player

Competitive benchmarking of key players by region

PESTLE Analysis

PORTER’s analysis

Value chain and supply chain analysis

Legal Aspects of Business by Region

Lucrative business opportunities with SWOT analysis

Recommendations

Our Trending Related Report :

Global Fresh Cherries Market https://www.maximizemarketresearch.com/market-report/global-fresh-cherries-market/96291/ Foldable Display Market https://www.maximizemarketresearch.com/market-report/global-foldable-display-market/65149/

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

+91 96071 95908, +91 9607365656

#Automotive Plastics Market Analysis#Automotive Plastics Market Share#Automotive Plastics Market Growth#Automotive Plastics Market Demand#Automotive Plastics Market Trends#Automotive Plastics Market Forecast

0 notes

Text

0 notes

Text

AI Image Generator Market to be Worth $1093.1 million by 2032

Meticulous Research®—leading global market research company, published a research report titled ‘Plasticizers Market—Global Opportunity Analysis and Industry Forecasts (2025–2032)’. According to this latest publication from Meticulous Research®, the plasticizers market is expected to reach $26.9 billion by 2032, at a CAGR of 5.4% from 2025 to 2032.

The growth of this market can be attributed to several factors, including the increasing construction and infrastructure development projects in developing countries and the growing adoption of plasticizers in the consumer goods and automotive industries. However, the fluctuating prices of raw materials restrain market growth.

Additionally, the rising need for eco-friendly plasticizers and the increasing demand for plasticizers in packaging materials manufacturing are expected to create market growth opportunities. However, stringent regulations for plastic products are a major challenge for the players operating in this market.

Key Players:

The plasticizers market is moderately competitive due to the presence of many large and small-sized global, regional, and local players. The key players operating in the plasticizers market are UPC Technology Corporation (Taiwan), Exxon Mobil Corporation (U.S.), BASF SE (Germany), Evonik Industries AG (Germany), Eastman Chemical Company (U.S.), Aekyung Chemical (South Korea), LG Chem, Ltd. (South Korea), DIC Corporation (Japan), Kao Corporation (Japan), Avient Corporation (U.S.), Polynt S.p.A. (Italy), KLJ Group (India), Arkema Group (France), Perstorp AB (Sweden), The Dow Chemical Company (U.S.), and Nan Ya Plastics Corporation (Taiwan).

The plasticizers market is segmented by type and end-use industry. This study also evaluates industry competitors and analyzes the plasticizers market at the regional and country levels.

Among the plasticizer types studied in this report, in 2025, the phthalate plasticizers segment is expected to dominate the plasticizers market with the largest share of over 47%. Phthalate plasticizers’ popularity due to their relatively lower costs, low volatility, and ability to create very elastic materials supports the segment’s dominant position in the plasticizers market. Additionally, phthalate plasticizers’ effectiveness in improving the flexibility, durability, and workability of plastics, the growing use of phthalate plasticizers in products such as vinyl flooring, coatings, pipes, and wiring insulation, and the extensive application of Diisononyl Phthalate (DINP) and Diethylhexyl Phthalate (DEHP) in PVC products also contribute to the segment’s large share.

Among the end-use industries studied in this report, in 2025, the building & construction segment is expected to dominate the plasticizers market with the largest share of over 35%. In building & construction applications, plasticizers are used as reducers and added to concrete to make it softer, improve its workability and strength, and reduce its water requirements. Rapid urbanization and infrastructure development and the growing use of plasticizers to enhance the flexibility, durability, and workability of construction materials support the segment’s large share in the plasticizers market.

Among the geographies studied in this report, in 2025, Asia-Pacific is expected to dominate the plasticizers market with the largest share of over 53%, followed by North America, Europe, Latin America, and the Middle East & Africa. Ongoing industrialization in APAC countries, including China, South Korea, and India, the increasing use of plasticizers to enhance the performance and flexibility of products, growing construction activities across APAC countries, and the increasing adoption of advanced packaging solutions among food processors support the region’s large market share.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6022

Key Questions Answered in the Report:

Which are the high-growth market segments based on type, end-use industry, and geography?

What was the historical market size for plasticizers globally?

What are the market forecasts and estimates for the period 2025–2032?

What are the major drivers, restraints, opportunities, and challenges in the plasticizers market?

Who are the major players, and what shares do they hold in the plasticizers market?

What is the competitive landscape like in the plasticizers market?

What are the recent developments in the plasticizers market?

What are the growth strategies adopted by major players in the plasticizers market?

What are the key geographic trends, and which are the high-growth countries?

Who are the local emerging players in the plasticizers market, and how do they compete with the other players?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#AIImageGenerator#GenerativeAI#MarketForecast#ArtificialIntelligence#TechTrends2032#AIInDesign#CreativeTech#DigitalTransformation#ContentAutomation#MachineLearning#MarketGrowth#InnovationInAI#EmergingMarkets

1 note

·

View note

Text

What’s Shaping the Global Plasticizers Price Trend? Market Analysis, Forecast & Insights

The Plasticizers Price Trend has become a critical element for stakeholders spanning construction, automotive, packaging, medical devices, and consumer goods industries. Plasticizers—primarily phthalate esters, non‑phthalate alternatives, and bio‑based variants—are additives that enhance flexibility, durability, and workability in polymer matrices. Their price behaviour is dictated by feedstock cost fluctuations, regulatory shifts, supply–demand dynamics, and emerging sustainability requirements.

Prices: Latest Price, News, Market Insights

While actual prices are excluded here per instructions, market intelligence providers like IMARC Group, Procurement Resource, and ICIS consistently publish comprehensive data on spot, Ex‑Works, FOB and CIF price levels across major regions such as North America, Europe, and Asia‑Pacific . Latest news highlights include freight rate impacts on feedstock like phthalic anhydride during early‑2025, geopolitical tensions affecting Red Sea shipping routes, and U.S. anti‑dumping investigations into European and Asian DOTP exports leading to duty impositions .

Market Analysis & News

Procurement Resource reports indicate that Q1 2025 experienced stable plasticizer supply and moderate end‑use demand from construction and automotive sectors, resulting in only modest fluctuations . However, periods of elevated freight costs and regional supply chain disruptions triggered short‑lived price spikes, followed by rapid correction as distribution logistics normalized. ICIS commentary echoes these observations and underscores the need for real‑time data access to capitalize on market volatility . In Europe, pricing for key plasticizer DOTP saw modest increases in early 2024 and then declined as demand softened and feedstock prices eased .

Historical Data & Forecast

Historical trends show plasticizers price movements aligning closely with phthalic anhydride and 2‑Ethylhexanol feedstock behaviour. In 2023, weak downstream demand in the U.S. building and construction sectors slowed inventory turnover, dragging prices downward . Asia‑Pacific inventory buildup amid pandemic recovery in 2022 also pressured prices before stabilization later in the year .

Growth forecasts vary by source: Lucintel projects market CAGR of 5–7 % for 2021–2026 driven by urbanisation and automotive demand . Market data from Market Research Future and Fortune Business Insights anticipates industry value rising from ~USD 18 billion in 2024–25 to ~$26–34 billion by early 2030s, with CAGR estimates between 4.1 % and 5.2 % across different horizons . The eco‑friendly plasticizers segment, including bio‑based and non‑phthalate alternatives, is forecast to grow faster—approx. 7 % CAGR over 2024‑2030—spurred by sustainability trends and regulations .

Chart, Historical & Forecast Data & Database Access

Market intelligence platforms such as IMARC Group deliver detailed historical data, time‑series price charts, spot price indices, and future projections (PDF + Excel) across regions and product types (e.g. U.S., China, Germany) . Procurement Resource offers integrated database tools featuring interactive charts, regional surveillance, downloadable datasets, price indices, and forecast modeling—enabling procurement analysts to track pricing patterns, benchmark suppliers, and simulate cost scenarios .

Regional Insights & Analysis

In Asia‑Pacific, particularly China and India, plasticizer demand continues to grow due to rapid urbanisation, infrastructure development, and expansion in vinyl flooring, wire & cable and flexible PVC usage. This region accounted for ~59 % market share in 2022 and is expected to maintain the highest growth rate (~6 % CAGR) through 2030 . However, regional feedstock oversupply and low-cost output from China can moderate price spikes, especially for DOTP .

In North America, the plasticizer market was valued at over USD 5 billion in 2023; strong automotive and construction infrastructure spending has supported demand, although high interest rates and housing softness weighed on volumes in H2 2024 . U.S. protectionist actions—especially anti‑dumping duties on DOTP imports from Turkey and Poland—are reshaping supply‑side dynamics and creating pricing insulation for domestic producers like Eastman and BASF .

In Europe, demand challenges persist, with the building sector sluggish and 2‑EH feedstock oversupply leading to downward pressure on plasticizer margins. The increase in energy costs, particularly natural gas, has added cost pressure to European producers while supply from Asia remains competitively priced .

Market Insights & Demand Drivers

Demand for plasticizers is largely driven by the construction sector (e.g. flooring, roofing membranes, cables), automotive interiors and sealants, consumer goods (footwear, toys), and medical applications (gloves, tubing). The shift from traditional phthalate plasticizers to eco‑friendly, non‑phthalate and bio‑based options is accelerating due to regulatory restrictions and consumer safety concerns . Phthalate plasticizers (e.g. DEHP, DINP) still command ~47 % share in 2025, though alternatives are gaining rapidly .

Key price drivers include phthalic anhydride and 2‑EH feedstock price shifts, energy and freight costs, trade tariffs, regulatory changes (e.g. anti-dumping duties), and macroeconomic shifts in construction and automotive industries.

Procurement Resource as Sourcing Intelligence

Procurement Resource serves as a strategic procurement resource for sourcing professionals by delivering granular analysis on the Plasticizers Price Trend, along with database access, supplier benchmarking, price indices, regional breakdowns, and sustainability-driven category intelligence. Their platform enables deep dive into price drivers, future forecasts, and historical charts—helping procurement teams align purchasing strategy with market conditions.

Using Procurement Resource, buyers can evaluate Ex‑Works vs CIF pricing, compare plasticizer types (phthalate, non‑phthalate, bio‑based), assess supplier reliability, and plan inventory or contracts effectively.

Request for the Real Time Prices

Real-time price updates enable industry stakeholders to make faster and more informed procurement decisions, especially in volatile market conditions.

https://www.procurementresource.com/resource-center/plasticizers-price-trends/pricerequest

Access to live price tracking allows manufacturers and supply chain managers to adjust purchase schedules, renegotiate contracts, and stay ahead of cost changes affecting product margins.

Market Insights for Procurement Professionals

Procurement leaders must monitor multiple dimensions: price trend charts, feedstock indexes, tariffs, regional supply changes, and emerging eco‑friendly formulations. Leveraging real‑time market insights and forecast tools enables timing procurement cycles, negotiating better terms, and avoiding exposure to price spikes. Accessing historical data, demand forecasts, regional analysis, and news-linked pricing through a central database supports smarter strategy in volatile markets such as plasticizers.

Contact Information

Company Name: Procurement Resource

Contact Person: Ashish Sharma (Sales Representative)

Email: [email protected]

Location: 30 North Gould Street, Sheridan, WY 82801, USA

Phone:

UK: +44 7537171117

USA: +1 307 363 1045

Asia‑Pacific (APAC): +91 1203185500

0 notes

Text

Electric Vehicle Plastics Market: An In-Depth Exploration and its Contribution to a Circular Automotive Industry

The global electric vehicle plastics market size was estimated at USD 13.33 billion in 2030 and is anticipated to grow at a compound annual growth rate (CAGR) of 28.0% from 2024 to 2030. The industry is projected to witness significant growth in terms of consumption, on account of high application scope and increasing demand from the growing population. The Polypropylene (PP) resin demand in the Asia Pacific region is estimated to grow at the fastest CAGR over the forecast period. Strong government support & initiatives regarding emissions and increasing investment by manufacturers are propelling the growth of the region.

Electric Vehicle Plastics Market Report Highlights

The Asia Pacific region is estimated to grow at the fastest CAGR from 2022 to 2030. Increasing demand from the growing population coupled with environmental concerns among others are anticipated to drive market growth in the region

The battery segment is anticipated to register the fastest CAGR from 2022 to 2030. Batteries are one of the significant components of an EV and, in comparison to combustion engines, battery vehicles do not produce any emissions and are eco-friendly. The growing demand for EVs has promising growth for EV batteries

The exterior application segment accounted for the largest revenue share in 2021 and is estimated to continue its dominance over the forecast period due to the high demand in aesthetics

The BEV vehicle type segment led the industry in 2021 and it is anticipated to continue growing over the forecast period as PHEVs have higher maintenance costs than BEVs

For More Details or Sample Copy please visit link @: Electric Vehicle Plastics Market Report

Furthermore, EVs are efficient and require less maintenance as compared with traditional vehicles. These factors are expected to boost the demand for EVs, which is expected to drive the demand for plastics over the forecast period. Increasing utilization of plastics in EVs is anticipated to boost industry growth positively over the forecast period. Plastics have proven to perform well under harsh conditions through their resistance to shock, moisture, oxidation, and further maintaining their chemical and mechanical properties. Plastics will be crucial material for manufacturing lightweight and energy-efficient EVs. Based on resin type, PP is expected to witness major demand during the projected years.

Polypropylene is used in many components of the vehicle including bumpers, carpet fibers, cable insulation, and others. Properties, such as good heat, chemical & fatigue resistance, and others, are anticipated to drive the demand for PP in the industry. Major manufacturers are adopting expansion strategies, such as new product development, production facility expansions, mergers & acquisitions, and joint ventures. For instance, in October 2021, DuPont launched a new extension of its existing Zytel HTN range, named as Zytel 500 series. These products are developed to provide enhanced retention properties in e-mobility oils, electrically friendly characteristics, and a high Comparative Tracking Index (CTI).

EVPlastics #ElectricVehicles #SustainableDriving #EcoFriendlyCars #ElectricVehicleTech #CleanTransportation #GreenMobility #EVInnovation #PlasticsInEVs #FutureOfTransport #SustainableMaterials #EcoAutoDesign #EVManufacturing #PolymerInnovation #ZeroEmissionVehicles #GreenTechAuto #CleantechPlastics #EVDesign #EcoFriendlyPlastics #CircularAutoEconomy

#EV Plastics#Electric Vehicles#Sustainable Driving#Eco-Friendly Cars#Electric Vehicle Tech#Clean Transportation#Green Mobility#EV Innovation#Plastics In EVs#Future Of Transport#Sustainable Materials#Eco Auto Design#EV Manufacturing#Polymer Innovation#Zero Emission Vehicles#Green Tech Auto#Cleantech Plastics#EV Design#Eco-Friendly Plastics#Circular Auto Economy

2 notes

·

View notes

Text

Bio-Based Engineering Plastics on the Rise

The global engineering plastic market is poised for significant expansion, with its valuation estimated at USD 165.4 billion in 2025 and projected to reach a substantial USD 359.2 billion by 2035, exhibiting a robust Compound Annual Growth Rate (CAGR) of 8.1%. This impressive growth is primarily driven by the escalating need for lightweight materials and enhanced durability across critical industries such as automotive, electronics, and construction.

Engineering plastics, renowned for their superior thermal stability, mechanical properties, and chemical resistance, have become indispensable substitutes for metals and conventional polymers in numerous applications. The rapid growth of industrial automation and the accelerating shift towards electric mobility are significantly contributing to this market surge. For electric vehicles, these plastics offer crucial benefits, including reducing component weight, improving fuel economy, and enhancing design flexibility, while their increasing application in metal replacement in under-the-hood automotive parts supports global sustainability objectives by reducing carbon emissions.

To Gain More Insights about this Research, Visit! https://www.futuremarketinsights.com/reports/engineering-plastics-market

Key Drivers and Market Dynamics:

Automotive and Electronics Demand: The automotive and transportation sector is the largest application segment, accounting for 34% of the market share in 2025, followed by electrical and electronics at 25%. Engineering plastics are preferred for their low weight, mechanical strength, and ability to meet stringent safety, flame retardancy, and insulation requirements in high-performance equipment.

Miniaturization and Performance: The consumer electronics industry is increasingly adopting engineering plastics for housings, connectors, and display components, driven by the demand for miniaturized, high-performing devices like smartphones, tablets, and wearables.

Healthcare Opportunities: The healthcare industry presents new opportunities for high-performance plastics in diagnostic equipment, drug delivery systems, and surgical instruments, leveraging their biocompatibility and sterilization standards.

Sustainability Focus: A growing emphasis on circular economy values is driving innovations in recycling technology and the production of sustainable materials, including bio-based and recyclable engineering plastics.

Segmental Dominance:

By Product Type, Polyamides (PA) will lead the industry in 2025 with a 23.5% share, followed by Polycarbonates (PC) at 15%. Polyamides, particularly PA6 and PA66, are favored for their excellent mechanical strength and thermal stability in automotive and industrial applications. Polycarbonates are prized for their clarity, impact resistance, and heat resistance, making them ideal for automotive lamps, electronic housings, and medical devices.

Request Your Sample and Stay Ahead with Our Insightful Report! https://www.futuremarketinsights.com/checkout/1881

Regional Outlook and Competitive Landscape:

The engineering plastic market is witnessing strong growth across various countries:

China will dominate the market with a 6.2% CAGR, driven by massive production capacity and needs from its construction, automotive, and electronics industries, along with government policies encouraging green technology.

The USA (5.4% CAGR) is fueled by strong demand from automotive, aerospace, and electrical sectors, and increasing investments in high-performance thermoplastics.

Germany (4.9% CAGR) benefits from robust vehicle exports and advanced manufacturing infrastructure, with a focus on additive manufacturing and green raw materials.

South Korea (5.1% CAGR) is driven by rapid technology developments and extensive integration with its electronics and semiconductor sectors.

Japan (4.6% CAGR) sees stable industrial demand and precision manufacturing technology development, with increasing use in robotics and medical equipment.

The UK (4.7% CAGR) and France (4.5% CAGR) are underpinned by increasing demand from automotive and electrical industries, and a focus on recyclable and lightweight materials.

Italy (4.3% CAGR), Australia (4.2% CAGR), and New Zealand (3.9% CAGR) also contribute to market growth, driven by their respective industrial and infrastructure demands.

The industry is intensely competitive, dominated by multinational chemical corporations. BASF SE (15-19% market share), DuPont (12-16% share), and Covestro (10-14% share) hold strong footholds due to their extensive product portfolios and technological advances. Asian manufacturers like LG Chem (8-12% share) and Mitsubishi Engineering-Plastics Corporation are spearheading demand in consumer electronics and automotive components.

Key strategies adopted by prominent players include:

Heavy investment in R&D to develop high-performance polymers with improved durability, thermal resistance, and mechanical strength.

Focus on sustainable alternatives, including bio-based and recyclable plastics, to comply with circular economy trends.

Strategic acquisitions and collaborations to expand footprint in industrial and medical engineering plastics.

The engineering plastic market is poised for a dynamic future, driven by continuous material innovation, evolving performance requirements, and a strong global push towards lightweight, durable, and sustainable solutions across critical industries.

𝐀𝐛𝐨𝐮𝐭 𝐅𝐮𝐭𝐮𝐫𝐞 𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬 (𝐅𝐌𝐈)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

𝐂𝐨𝐧𝐭𝐚𝐜𝐭 𝐅𝐌𝐈:

Future Market Insights Inc. Christiana Corporate, 200 Continental Drive, Suite 401, Newark, Delaware - 19713, USA T: +1-347-918-3531 For Sales Enquiries: [email protected] Website: https://www.futuremarketinsights.com LinkedIn| Twitter| Blogs | YouTube

0 notes

Text

Top 15 Market Players in Global Butanol Market

Top 15 Market Players in Global Butanol Market

The global butanol market is dominated by several major players who influence market dynamics through production capacity, geographic reach, and innovation. Below are 15 prominent companies driving growth in this sector:

BASF SE

The Dow Chemical Company

Sasol Limited

Eastman Chemical Company

Mitsubishi Chemical Corporation

Oxea GmbH (part of OQ Chemicals)

Formosa Plastics Corporation

PETRONAS Chemicals Group Berhad

Andhra Petrochemicals Ltd.

China National Petroleum Corporation (CNPC)

KH Neochem Co., Ltd.

LyondellBasell Industries

Grupa Azoty Zakłady Azotowe Kędzierzyn S.A.

Saudi Kayan Petrochemical Company (SABIC affiliate)

Celanese Corporation

These companies contribute significantly to the production of various types of butanol, including n-butanol, isobutanol, and tert-butanol, which are used across industries such as paints and coatings, textiles, pharmaceuticals, and automotive.

Request report sample at https://datavagyanik.com/reports/butanol-market/

Top Winning Strategies in Butanol Market

To maintain competitive advantage and respond to evolving market demands, leading firms in the butanol sector have adopted several high-impact strategies:

1. Strategic Partnerships and Joint Ventures

Companies are forming alliances to combine technical expertise, expand market presence, and share investment burdens. These collaborations also facilitate access to new geographical markets.

2. Capacity Expansion

To meet growing global demand, especially from emerging economies in Asia-Pacific, several players are increasing their production capacity through greenfield and brownfield projects.

3. Vertical Integration

By integrating operations from raw material sourcing to end-product manufacturing, companies enhance cost efficiency, supply chain control, and profit margins.

4. Focus on Bio-Based Butanol

With sustainability gaining traction, there is a notable pivot toward the development and commercialization of bio-butanol. This eco-friendly alternative offers reduced carbon emissions and appeals to environmentally conscious markets.

5. Geographic Diversification

To mitigate regional risks and capture untapped markets, firms are expanding their operations across multiple continents, especially into Latin America, Africa, and Southeast Asia.

6. R&D and Process Innovation

Continuous investment in research is enabling companies to improve yield, reduce energy consumption, and develop specialty butanol grades tailored for niche applications.

7. Mergers and Acquisitions

Several players are consolidating their market positions through strategic M&A activities, which help streamline operations and access new technologies or customer bases.

Request a free sample copy at https://datavagyanik.com/reports/butanol-market/

0 notes

Text

Wafer Packaging Materials Market: Innovations Shaping the Future of Authentication, 2025-2032

Wafer Packaging Materials Market, Trends, Business Strategies 2025-2032

Wafer Packaging Materials Market size was valued at US$ 4.23 billion in 2024 and is projected to reach US$ 7.67 billion by 2032, at a CAGR of 8.9% during the forecast period 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=108071

MARKET INSIGHTS

The global Wafer Packaging Materials Market size was valued at US$ 4.23 billion in 2024 and is projected to reach US$ 7.67 billion by 2032, at a CAGR of 8.9% during the forecast period 2025-2032. This growth trajectory reflects increasing semiconductor demand across consumer electronics and automotive applications, despite macroeconomic challenges in 2022-2023 that temporarily slowed the broader semiconductor industry’s expansion to 4.4% annually.

Wafer packaging materials encompass specialized components essential for protecting and interconnecting semiconductor die after wafer dicing. These materials include lead frames, ceramic packages, bonding wires (gold, copper, aluminum), and advanced epoxy molding compounds that ensure thermal stability and electrical performance. The packaging process involves precisely mounting die onto substrates, creating electrical connections through wire bonding or flip-chip techniques, and encapsulating the assembly for mechanical protection.

Market growth is primarily driven by 5G infrastructure deployment requiring advanced packaging solutions, along with automotive semiconductor demand increasing 20.8% annually as vehicles incorporate more electronics. However, supply chain constraints and material cost fluctuations pose challenges, particularly for gold bonding wires which account for approximately 30% of packaging material costs. Leading players like Shin-Etsu Chemical and Henkel are investing in copper wire bonding alternatives and low-temperature cure encapsulants to address these cost pressures while meeting performance requirements for AI chips and high-power devices.

List of Key Wafer Packaging Materials Companies Profiled

Henkel (Germany)

Shin-Etsu Chemical (Japan)

Sumitomo Chemical Company (Japan)

KYOCERA (Japan)

Hitachi Chemical (Japan)

BASF SE (Germany)

DuPont (U.S.)

Dow Corning (U.S.)

Alent (U.K.)

IBIDEN (Japan)

SEMCO (South Korea)

MITSUI HIGH-TEC (Japan)

Heraeus (Germany)

Guangdong Wabon Technology (China)

ETERNAL MATERIALS (Taiwan)

Segment Analysis:

By Type

Packaging Substrate Segment Leads Due to High Demand for Advanced Semiconductor Packaging Solutions

The market is segmented based on type into:

Lead Frame

Package Substrate

Ceramic Packaging Materials

Bonding Wires

Die Bonding Materials

By Application

Consumer Electronics Segment Dominates Owing to Growing Demand for Smart Devices

The market is segmented based on application into:

Consumer Electronics

Automobile Industry

Industrial Applications

Healthcare Electronics

By Material

Organic Substrates Hold Major Share Due to Cost-Effectiveness and Versatility

The market is segmented based on material into:

Organic Substrates

Ceramic Substrates

Metal Alloys

Thermoset Plastics

By Packaging Technology

Flip Chip Technology Gains Traction for High-Performance Applications

The market is segmented based on packaging technology into:

Wire Bonding

Flip Chip

Wafer-Level Packaging

3D Packaging

Regional Analysis: Wafer Packaging Materials Market

North America The North American wafer packaging materials market is driven by strong demand from the semiconductor industry, particularly in the U.S., which accounted for over 40% of the regional market share in 2023. The presence of major semiconductor players like Intel, Micron, and Texas Instruments fuels innovation in advanced packaging solutions. The region leads in adopting cutting-edge materials for 3D IC packaging and fan-out wafer-level packaging (FOWLP) due to extensive R&D investments. However, stringent environmental regulations on materials like lead-based solders present challenges for manufacturers. The U.S. CHIPS Act, allocating $52 billion for domestic semiconductor production, is expected to significantly boost wafer packaging material demand through 2030.

Europe Europe maintains a strong position in specialty wafer packaging materials, particularly in ceramic packaging and advanced bonding wires, with Germany and France being key markets. The region benefits from leading material science companies like BASF and Heraeus. European semiconductor packaging emphasizes sustainability and recycling initiatives, driving demand for eco-friendly materials. The European Chips Act aims to double the region’s global market share to 20% by 2030, which will create significant opportunities for packaging material suppliers. However, higher production costs compared to Asian manufacturers remain a challenge for widespread adoption of European-made packaging solutions.

Asia-Pacific As the dominant region with over 60% market share, Asia-Pacific is the powerhouse of wafer packaging material production and consumption. Taiwan, South Korea, China, and Japan collectively host the world’s largest OSAT (outsourced semiconductor assembly and test) providers. China’s rapid expansion in domestic semiconductor production has increased demand for all packaging material types, though it relies heavily on imports for advanced substrates. Southeast Asian nations like Malaysia are emerging as important packaging hubs due to lower labor costs. The region shows particular strength in lead frame and bonding wire production, but faces challenges in achieving self-sufficiency in high-end packaging substrates.

South America The South American market remains small but shows gradual growth, primarily serving local electronics manufacturing needs in Brazil and Argentina. The region’s wafer packaging material market is characterized by import dependency, particularly for advanced packaging substrates and specialty bonding materials. Some local production exists for basic lead frames and plastic encapsulation compounds serving consumer electronics applications. While economic fluctuations have limited market expansion, increasing investments in automotive electronics manufacturing may drive future demand for packaging materials. The market however lacks significant domestic material innovation capabilities.

Middle East & Africa This emerging region shows potential due to strategic investments in semiconductor test and packaging facilities, particularly in Israel and UAE. Israel’s strong position in semiconductor design creates niche demand for advanced packaging solutions. Countries like Saudi Arabia are making initial moves to establish local semiconductor ecosystems as part of economic diversification plans. However, the market remains constrained by limited local material production capabilities and reliance on imports. Some growth is expected in basic packaging materials for consumer electronics assembly, but the region will likely remain a minor player in the global wafer packaging materials landscape through 2030.

MARKET DYNAMICS

The emergence of chiplet-based architectures presents significant opportunities for advanced wafer packaging materials. Heterogeneous integration requires specialized die-attach materials and thermally conductive interfaces that can maintain stability across multiple thermal cycles. The chiplet packaging market is projected to require over $2 billion in new material solutions by 2026, with particular demand for ultra-low-loss dielectric materials and fine-pitch bonding solutions.

Growing interest in glass and silicon-based substrates for high-performance computing applications is opening new avenues for material innovation. These alternatives offer superior dimensional stability for advanced packaging, with glass substrates showing particular promise for optical interconnects. Early adopters report 30% improvements in signal integrity versus organic substrates in high-frequency applications, though material costs remain 2-3X higher currently.

As power densities in advanced packages continue to increase, thermal management becomes critical. Next-generation thermal interface materials capable of maintaining stable performance at >300W/cm² are seeing rapidly growing demand. Metal-based TIMs and graphene-enhanced compounds are emerging as potential solutions, with the high-end TIM market expected to grow at 18% CAGR through 2030.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108071

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wafer Packaging Materials Market?

Which key companies operate in Global Wafer Packaging Materials Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 [+91 8087992013] [email protected]

0 notes