#Biodegradable Films Market Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was attacked by a cross-site scripting worm deployed by the Internet troll group GNAA on Dec 3, 2012.

Text

Sustainable Packaging Revolution: The Growth of the Biodegradable Films Market

Rising Demand for Sustainable Packaging and Eco-Friendly Materials Drives Growth in the Biodegradable Films Market.

The Biodegradable Films Market size was USD 1.3 billion in 2023 and is expected to reach USD 2.3 billion by 2032 and grow at a CAGR of 6.7% over the forecast period of 2024-2032.

The Biodegradable Films Market is driven by increasing environmental concerns and regulatory support for sustainable packaging solutions. Biodegradable films, derived from renewable sources such as starch, polylactic acid (PLA), and polyhydroxyalkanoates (PHA), are gaining traction in industries like food packaging, agriculture, pharmaceuticals, and consumer goods. As governments worldwide enforce strict regulations on plastic waste, the demand for eco-friendly alternatives like biodegradable films is expected to surge.

Key Players in the Biodegradable Films Market

BASF SE (Ecovio, Soil biodegradation)

Taghleef Industries (Nativia, Biofilm)

Kingfa Sci. & Tech. Co., Ltd. (Eco-Friendly Biodegradable Films, Kingfa PLA Film)

BioBag Americas, Inc. (BioBag, BioBags for Food Storage)

Avery Dennison Corporation (Eco-friendly Label Films, Biodegradable Packaging Films)

Bi-Ax International Inc. (Biodegradable Film Rolls, Bioplastics)

Cortec Corporation (Eco-Corr Films, VpCI Biodegradable Films)

Clondalkin Group (Compostable Packaging Films, Flexible Packaging Solutions)

Paco Label (Biodegradable Label Films, Eco-Friendly Packaging Solutions)

Layfield Group (Biodegradable Mulch Film, Layfield BioFilms)

Future Scope of the Market

The future of the biodegradable films market looks promising, with:

Expanding applications in food packaging, agriculture, and healthcare.

Stronger government regulations against plastic pollution fueling market demand.

Technological advancements improving the durability and cost-effectiveness of biodegradable films.

Rising consumer awareness driving demand for sustainable packaging solutions.

Increased investment in research and development for innovative biodegradable film solutions.

Emerging Trends in the Biodegradable Films Market

The market is witnessing a shift toward plant-based and compostable packaging materials, particularly in food and beverage applications where sustainability is a key selling point. Companies are focusing on developing high-performance biodegradable films with enhanced barrier properties to extend product shelf life. The agricultural sector is also seeing a rise in the adoption of biodegradable mulch films, reducing plastic waste in farming. Additionally, major brands are incorporating biodegradable films into their packaging strategies to align with their corporate sustainability goals.

Key Points:

Growing demand for eco-friendly packaging solutions in various industries.

Stricter government regulations supporting the adoption of biodegradable films.

Innovations in bio-based materials enhancing film durability and performance.

Expanding applications in food packaging, agriculture, and healthcare.

Increased investment in research & development for cost-effective biodegradable alternatives.

Conclusion

The Biodegradable Films Market is set to witness strong growth, fueled by sustainability trends, regulatory pressure, and increasing consumer awareness. As industries move away from traditional plastic films, biodegradable alternatives will play a critical role in reducing plastic waste and promoting a circular economy. Companies that focus on innovation, material efficiency, and scalable production methods will be at the forefront of this rapidly evolving market.

Read Full Report: https://www.snsinsider.com/reports/biodegradable-films-market-1454

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Biodegradable Films Market#Biodegradable Films Market Size#Biodegradable Films Market Share#Biodegradable Films Market Report#Biodegradable Films Market Forecast

0 notes

Text

Global Mulch Film Market: Biodegradable Focus

Global Mulch Film Market: Biodegradable Focus

Mulch film, a plastic sheet laid over soil, plays a vital role in agriculture. It suppresses weeds, conserves moisture, regulates soil temperature, and improves crop yields. However, traditional plastic mulch film presents a growing environmental concern. This blog post, based on insights from Mordor Intelligence's market research report, dives into the Global Mulch Film Market: Biodegradable Focus. Here, we'll explore the rise of biodegradable mulch films, analyze the factors driving its adoption, and examine the potential benefits it holds for sustainable agriculture.

A Growing Concern: The Environmental Impact of Traditional Mulch Film

Conventional plastic mulch film, while effective, has a significant drawback – it's not biodegradable. This leads to:

Plastic Pollution: Discarded plastic mulch ends up in landfills or pollutes the environment, harming wildlife and ecosystems.

Soil Contamination: Microplastics from degraded plastic film can contaminate soil, potentially affecting plant health and food safety.

Waste Management Challenges: Removing and disposing of used plastic mulch film can be expensive and logistically challenging for farmers.

These concerns are driving the search for more sustainable solutions, and biodegradable mulch film is emerging as a promising alternative.

A Sustainable Solution: The Rise of Biodegradable Mulch Film

Biodegradable mulch film is composed of materials like plant starches, cellulose, or synthetic polymers designed to break down naturally in the soil. This offers several advantages:

Reduced Environmental Impact: Biodegradable mulch film decomposes into organic matter, eliminating plastic pollution and microplastic concerns.

Improved Soil Health: Decomposition of the mulch film enriches the soil with organic matter, promoting beneficial microbial activity and long-term soil health.

Convenience for Farmers: Biodegradable mulch film eliminates the need for removal and disposal, simplifying agricultural practices.

Potential Yield Benefits: Improved soil health and moisture retention with biodegradable mulch film can potentially lead to increased crop yields.

The growing environmental awareness and the advantages offered by biodegradable mulch film are driving its adoption in the global market.

Cultivating a Sustainable Future: Opportunities in the Biodegradable Mulch Film Market

The biodegradable mulch film market presents exciting opportunities for a more sustainable agricultural future:

Innovation in Materials: Research and development of new biodegradable materials and improved film performance can further enhance market growth.

Government Support: Government policies promoting sustainable agricultural practices and offering incentives for biodegradable mulch film adoption can accelerate market expansion.

Consumer Preferences: The increasing demand for sustainable food production creates a market for farmers to adopt biodegradable mulch film and cater to environmentally conscious consumers.

Education and Awareness: Educating farmers about the benefits of biodegradable mulch film and overcoming adoption barriers is crucial for market growth.

By addressing these opportunities, the biodegradable mulch film market can play a significant role in creating a more sustainable and environmentally friendly agricultural system.

Conclusion

Mordor Intelligence's market research report paints a promising picture for the future of biodegradable mulch film. Driven by environmental concerns, the demand for sustainable solutions, and potential benefits for farmers and consumers, the market is expected to witness continued growth. By embracing innovation, promoting sustainable practices, and fostering awareness, the biodegradable mulch film industry can cultivate a greener future for agriculture, one film at a time.

#Biodegradable Mulch Film Market#Biodegradable Mulch Film Market size#Biodegradable Mulch Film Market share#Biodegradable Mulch Film Market trends#Biodegradable Mulch Film Market research reports#Biodegradable Mulch Film Market analysis#Biodegradable Mulch Film Market forecast#Biodegradable Mulch Film Market growth drivers

0 notes

Text

Cohesive Packaging Solutions 📦: Market Set to Hit $2.13B by 2034

Cohesive Packaging Solutions Market is on an upward trajectory, projected to grow from $1.41 billion in 2024 to $2.13 billion by 2034, reflecting a compound annual growth rate (CAGR) of 4%. This market includes packaging materials that self-adhere, eliminating the need for additional adhesives. The surge in online shopping, a greater focus on sustainable materials, and demand for efficient packaging in sectors like healthcare and consumer goods are key growth drivers. From cohesive films to wraps and tapes, these solutions streamline packaging processes, reduce waste, and enhance product security.

Market Dynamics

Rapid industrialization, increased environmental awareness, and evolving consumer preferences are reshaping packaging priorities. Companies are adopting cohesive solutions to minimize environmental impact while maintaining cost-efficiency. E-commerce continues to lead demand, with retailers needing fast, protective, and eco-friendly packaging. Meanwhile, the healthcare industry is prioritizing sterile, tamper-evident cohesive solutions. Technological advances such as smart packaging and automation are improving supply chain management and boosting operational efficiencies. However, the market faces hurdles including rising raw material costs, complex regulatory frameworks, and challenges in adapting to emerging technologies.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS33073

Key Players Analysis

Several major players are driving innovation and expansion in the cohesive packaging market. Amcor, Sealed Air Corporation, Mondi Group, and Smurfit Kappa are at the forefront, investing in eco-friendly technologies and strategic partnerships. These companies are expanding globally, acquiring smaller firms, and launching new product lines to meet the growing demand for sustainable and customizable packaging. Emerging players such as Ranpak and Packsize International are also making their mark with niche solutions focused on e-commerce and sustainable logistics. The competitive landscape is shaped by ongoing R&D, M&A activity, and a race to develop recyclable and biodegradable alternatives.

Regional Analysis

North America dominates the cohesive packaging market, led by the U.S., which benefits from advanced logistics infrastructure and high e-commerce penetration. Europe follows, with countries like Germany and the UK driving growth through stringent sustainability regulations and a robust retail sector. Asia-Pacific is the fastest-growing region, driven by booming e-commerce markets in China and India, as well as favorable government initiatives supporting manufacturing. Latin America, led by Brazil and Mexico, is seeing steady growth due to rising industrial activities. Meanwhile, the Middle East & Africa are witnessing expansion fueled by urbanization, retail growth, and economic diversification.

Recent News & Developments

Recent developments highlight the market’s dynamic nature. Amcor has partnered with a tech firm to enhance sustainable packaging technologies, while Mondi rolled out a new eco-friendly cohesive packaging line aimed at the European market. Sealed Air Corporation strengthened its position through a key acquisition, and Smurfit Kappa launched innovative packaging lines optimized for e-commerce logistics. Additionally, DS Smith invested heavily in production upgrades to meet the rising global demand. These strategic moves reflect the sector’s focus on innovation, efficiency, and environmental responsibility.

Browse Full Report : https://www.globalinsightservices.com/reports/cohesive-packaging-solutions-market/

Scope of the Report

This report provides a comprehensive analysis of the Cohesive Packaging Solutions Market, offering insights into market forecasts, trends, competitive strategies, and segment growth across type, product, material, technology, application, and region. It identifies key drivers, restraints, and opportunities, examining both current dynamics and future potential. The scope also includes PESTLE and SWOT analyses, detailed company profiles, and evaluations of market strategies such as mergers, product launches, and R&D investments. From local market trends to global supply chain assessments, the report serves as a strategic tool for stakeholders aiming to navigate and capitalize on this growing industry.

Discover Additional Market Insights from Global Insight Services:

Polylactic Acid Market : https://www.globalinsightservices.com/reports/polylactic-acid-market/

Adsorbents Market : https://www.globalinsightservices.com/reports/adsorbents-market/

Ceiling Tiles Market : https://www.globalinsightservices.com/reports/ceiling-tiles-market/

Compressor Oil Market : https://www.globalinsightservices.com/reports/compressor-oil-market/

Flame Retardants Market : https://www.globalinsightservices.com/reports/flame-retardants-market/

#cohesivepackaging #packagingsolutions #sustainablepackaging #ecofriendlypackaging #ecommercegrowth #logisticsinnovation #smartpackaging #packagingindustry #supplychainmanagement #biodegradablematerials #flexiblepackaging #packagingtrends #packagingdesign #greenpackaging #recyclablepackaging #retailpackaging #healthcarepackaging #custompackaging #futureofpackaging #marketforecast #globalmarket #packagingtechnology #environmentalregulations #packagingefficiency #onlinecommerce #packagingnews #industrialpackaging #packaginginnovation #packagingautomation #packagingstrategy #regionalanalysis #ecoawareness #sustainablematerials #zerowastepackaging #industrialgrowth #carbonfootprint #circulareconomy #materialscience #consumerpackaging #marketgrowth

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700

Website: https://www.globalinsightservices.com/

1 note

·

View note

Text

Global Medicine Blister Market Forecast: Growth & Opportunities 2032

The global medicine blister packaging market is experiencing remarkable growth, primarily driven by increasing demand for secure, tamper-evident, and user-friendly pharmaceutical packaging solutions. With the market valued at USD 15.6 billion in 2023, projections indicate it will expand at a CAGR of over 5.2% from 2024 to 2032, eventually surpassing USD 25.4 billion by the end of the forecast period. This growth is closely tied to the rising consumption of prescription and over-the-counter (OTC) medications, the need for more advanced drug packaging technologies, and the increasing regulatory requirements for safety and sustainability in pharmaceutical packaging.

The global medicine blister packaging market benefits from several key trends such as the increasing aging population, the prevalence of chronic diseases, and innovations in packaging technology. From smart blister packs that improve medication adherence to eco-friendly, biodegradable materials, the market is poised for continued transformation as it adapts to both consumer demand and regulatory pressures. This article provides a detailed examination of these trends, as well as a breakdown of the market's key segments, regional developments, and the competitive landscape.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40618-global-medicine-blister-market

Medicine Blister Packaging Market Dynamics and Key Drivers

1. Rising Demand for Secure and User-Friendly Packaging

The growing demand for tamper-evident, secure, and easy-to-use medicine packaging is one of the most significant drivers of the blister packaging market. Blister packs offer unparalleled advantages in ensuring that pharmaceuticals are protected against tampering, contamination, and damage, thus safeguarding patient safety.

Moreover, blister packaging simplifies the process for unit-dose packaging, making it more convenient for both patients and healthcare providers. As consumers increasingly prioritize convenience, transparency, and accuracy in dosing, this demand continues to accelerate.

2. Increasing Prevalence of Chronic Diseases and Aging Population

Aging populations worldwide, particularly in developed regions such as North America and Europe, are driving up the demand for medication adherence solutions. As people live longer, they require long-term treatments for chronic diseases such as cardiovascular conditions, diabetes, and cancer. Blister packaging is particularly valuable in this context, as it improves medication compliance by clearly labeling dosage instructions and offering single-dose compartments.

3. Technological Advancements in Packaging

Technological innovation is a critical factor shaping the market's future. Smart blister packs, which include features like QR codes, NFC-enabled reminders, and tamper-proof tracking systems, are gaining significant traction. These solutions offer not only patient adherence benefits but also data-driven insights for healthcare providers to monitor patient progress and compliance. Furthermore, advancements in active packaging—including moisture-absorbing and oxygen-scavenging films—help improve the shelf life and stability of sensitive drugs.

4. Environmental and Sustainability Considerations

The global shift towards sustainable packaging is also a key market driver. Environmental concerns, including the growing ecological impact of non-recyclable plastic and aluminum packaging, have led to increased demand for biodegradable and recyclable blister packs. Packaging manufacturers are focusing on producing lightweight materials, reducing their carbon footprints, and adopting eco-friendly designs without compromising on product safety or efficacy.

5. Regulatory Pressures and Compliance

Regulatory frameworks, particularly in North America and Europe, have become more stringent in recent years. The pharmaceutical industry is under constant pressure to adhere to increasingly demanding compliance standards. As a result, packaging solutions must be robust, tamper-proof, and capable of maintaining drug integrity throughout their shelf life. Additionally, the increasing regulation of child-resistant packaging has led to the widespread adoption of senior-friendly and child-resistant blister pack designs.

Get up to 30% Discount: https://www.statsandresearch.com/check-discount/40618-global-medicine-blister-market

Segmental Analysis of the Global Medicine Blister Packaging Market

The global medicine blister packaging market is divided into various segments based on material type, technology, application, and end-user. Below is a comprehensive breakdown of these segments, highlighting key trends and market dynamics.

By Material Type:

Plastic: Holding the largest market share of approximately 49% in 2023, plastic blister packaging is widely preferred for its cost-effectiveness, flexibility, and transparency, which allows users to easily view the medications inside. The segment is projected to grow at a CAGR of 5.8% through 2032.

Aluminium: Known for its superior barrier properties, aluminium-based blister packs are widely used for medications sensitive to moisture and oxygen. As a result, they are expected to continue seeing steady demand.

Paper & Paperboard: As eco-friendly packaging solutions gain popularity, paper-based blister packs are emerging as a sustainable alternative to plastic and aluminum packaging. The growth of this segment aligns with green packaging trends.

Cold Form Foil: This material type, which offers high moisture and oxygen barrier properties, is growing steadily and is ideal for highly sensitive drugs, particularly biologics.

By Technology:

Thermoforming: The thermoforming segment dominates the market, accounting for 68% of the total share in 2023. This technology is preferred for its cost efficiency, transparency, and lightweight nature.

Cold Forming: Cold forming is becoming increasingly popular due to its superior barrier properties. This technology is especially suited for drugs that require high moisture protection and is projected to grow at a CAGR of 5.1%.

By Application:

Tablets: The tablet segment holds the largest share of the market, accounting for 55% in 2023. Blister packs for tablets are convenient, cost-effective, and provide tamper resistance, making them the most widely used in the industry.

Capsules: Growing demand for capsules packaged in blister packs is expected to continue, particularly with the rise in biologic therapies and prescription drugs.

Ampoules & Vials: The rise in demand for injectable medications has led to increased use of ampoules and vials in blister packaging. This segment is expected to grow at a CAGR of 6.2%.

Syringes: As injectable drugs and vaccines become more prevalent, there is increasing demand for secure and reliable syringe packaging solutions.

By End-User:

Pharmaceutical Companies: The pharmaceutical sector holds the largest share, accounting for 49% of the market in 2023. This segment continues to expand due to the increasing need for compliance-ready and cost-effective packaging solutions.

Biotechnology Firms: With the rise in personalized medicine and biologic drugs, biotechnology firms are expected to grow at the fastest rate, achieving a CAGR of 6.3%.

Hospitals & Clinics: Hospitals and clinics represent a critical segment due to their demand for safe and reliable unit-dose packaging.

Contract Manufacturing Organizations (CMOs): CMOs are increasingly adopting blister packaging as they expand production capabilities for various pharmaceutical products.

By Distribution Channel:

Direct Sales: The largest segment, direct sales, accounts for 39% of the market share. Manufacturers prefer bulk sales to packaging suppliers.

Online Pharmacies: Online pharmacies are experiencing the fastest growth, driven by the increasing popularity of e-commerce and digital healthcare platforms.

By Region:

North America: North America holds the largest share of the market at 43%, driven by the region's advanced pharmaceutical infrastructure and regulatory environment.

Asia-Pacific: The Asia-Pacific region is experiencing the fastest growth, with a CAGR of 6.5%, as demand for pharmaceutical products and innovative packaging solutions increases in countries such as China, India, and Japan.

Competitive Landscape

The global medicine blister packaging market is highly competitive, with several key players striving to maintain or grow their market positions through product innovation, strategic partnerships, and sustainability initiatives. Leading companies in the market include:

Amcor Plc

WestRock Company

Constantia Flexibles

Sonoco Products Company

Honeywell International Inc.

ACG Pharmapack Pvt. Ltd.

Tekni-Plex, Inc.

Huhtamki Oyj

These companies are investing heavily in next-generation packaging solutions, such as recyclable and biodegradable materials, and integrating smart features to enhance security, medication adherence, and patient safety.

Noteworthy Industry Developments

Amcor Plc introduced a recyclable PET-based blister packaging solution in 2022, significantly reducing plastic waste while maintaining high protective barriers for medications.

WestRock Company unveiled an all-paper blister pack in 2023, aiming to eliminate plastic waste from pharmaceutical packaging. The Folding Carton Blister Pack is made from sustainable paperboard and complies with child safety regulations.

Key Takeaways:

Innovation in Technology and Design: The increasing use of smart blister packs, which integrate tamper-proof features, QR codes, and NFC-enabled reminders, plays a pivotal role in improving medication adherence and patient safety.

Sustainability Concerns: As consumer demand for eco-friendly packaging grows, there is a marked shift towards the adoption of biodegradable and recyclable materials. The industry is working to reduce its reliance on plastic and aluminum, making the market more eco-conscious.

Growing Need for Secure Packaging: With the rising prevalence of chronic diseases and the increasing use of unit-dose prescriptions, there is a heightened need for secure, tamper-evident packaging to ensure patient safety.

Rising Adoption of Child-Resistant and Senior-Friendly Designs: The market is witnessing the development of child-resistant blister packs and senior-friendly packaging solutions, meeting regulatory demands and enhancing patient safety.

Regional Growth Opportunities: North America remains the largest market for blister packaging due to its advanced pharmaceutical infrastructure and regulatory environment. However, the Asia-Pacific region, with its rapid healthcare advancements and growing pharmaceutical manufacturing capabilities, represents the fastest-growing market.

Market Forecast and Growth Projections (2024-2032)

The global medicine blister packaging market is expected to experience robust growth over the next decade. By 2032, the market is projected to exceed USD 25.4 billion, driven by factors such as:

The increasing demand for secure packaging solutions due to the rise in prescription medications and OTC drugs.

The shift towards smart packaging technologies that integrate digital health tools and patient compliance features.

The growing importance of eco-friendly packaging options, including biodegradable, recyclable, and sustainable materials.

The rising prevalence of chronic diseases, particularly in aging populations, which drives the need for medication adherence solutions.

Future Trends to Watch:

Smart Packaging Solutions: The incorporation of QR codes, NFC, and IoT-based tracking systems to monitor medication adherence and enhance patient outcomes will be a major trend in the coming years. As the healthcare industry continues to digitalize, expect a significant increase in the demand for smart blister packs.

Biodegradable and Recyclable Materials: As sustainability becomes a priority across all industries, manufacturers will continue developing eco-friendly packaging solutions. The adoption of biodegradable films and recycled paper-based blister packs will see accelerated growth.

Active Packaging Technologies: New active packaging solutions—such as moisture-absorbing and oxygen-scavenging films—will play a key role in enhancing the stability and shelf life of sensitive drugs, especially biologics and vaccines.

Customized and Personalized Packaging: With the rise of personalized medicine, the demand for customized blister packaging that caters to individual patient needs will grow. This includes packaging solutions designed for biologic drugs, injectables, and tailored pharmaceutical products.

E-commerce Growth and Direct-to-Consumer Distribution: The rise of online pharmacies and direct-to-consumer healthcare platforms is expected to drive the demand for durable, tamper-evident, and easy-to-ship blister packaging. This will be particularly relevant in regions experiencing rapid growth in e-commerce, such as Asia-Pacific.

Conclusion: A Medicine Blister Packaging Market in Transformation

The global medicine blister packaging market is on a transformative journey, driven by advancements in technology, sustainability, and patient-centric design. As pharmaceutical companies continue to innovate and adapt to regulatory standards, the market will likely experience significant growth and diversification.

The shift towards biodegradable and smart packaging, along with the growing demand for medication adherence solutions, presents immense opportunities for companies in the blister packaging industry. Key players in the market are focused on developing eco-friendly, secure, and patient-friendly packaging that meets both consumer and regulatory needs.

As the global healthcare landscape evolves, so too will the packaging solutions designed to deliver safe, convenient, and effective medications to patients around the world.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40618-global-medicine-blister-market

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

#Medicine Blister Market#blister packaging#pharmaceutical packaging#market trends#medicine packaging#global blister market#pharmaceutical market#blister packaging trends#medicine blister forecast#blister market analysis#marketresearch#marketresearchreport#news#technologyresearch

1 note

·

View note

Text

U.S. Packaging Coating Market: Trends Shaping the Industry

The global packaging coating market has been instrumental in ensuring product safety, enhancing visual appeal, and extending the shelf life of packaged goods. Traditionally, this market has been dominated by well-established technologies like epoxy, acrylic, and polyester coatings. These materials serve crucial functions such as barrier protection against moisture, grease, oxygen, and light—factors that can degrade the quality and safety of food, pharmaceuticals, and consumer goods. However, as regulatory scrutiny increases and consumer demand for safer and more sustainable packaging grows, a silent transformation is underway. One of the most groundbreaking developments, though still underrepresented in mainstream discussions, is the rise of nano-coatings in packaging applications.

According to Future Market Insights, the packaging coating market is projected to grow from USD 5.9 billion in 2025 to USD 9.9 billion by 2035, at a CAGR of 5.3% during the forecast period.

Request the Report Sample: https://www.futuremarketinsights.com/reports/sample/rep-gb-19541

Nano-coatings, or nanostructured barrier layers, are ultra-thin films engineered at the molecular or atomic scale to provide enhanced protective properties without increasing packaging weight or compromising recyclability. Unlike conventional coatings, which rely heavily on thickness and multi-layer laminations to offer barrier functions, nano-coatings leverage material science innovations to create high-performance barriers using significantly less material. This makes them not only efficient in function but also environmentally favorable, as they often eliminate the need for complex multilayer composites that are difficult to recycle.

In food packaging, nano-coatings are increasingly being investigated for their ability to prevent microbial growth and oxidation. These coatings can be embedded with silver nanoparticles or zinc oxide, both known for their antimicrobial properties. The result is a packaging surface that actively reduces microbial contamination, thereby extending the shelf life of perishable goods such as dairy, meat, and ready-to-eat meals. Companies like Tetra Pak and Amcor have been testing nano-enhanced packaging films that are both compostable and capable of reducing spoilage. For instance, a recent pilot study in Germany demonstrated that fresh cheese packaged with nano-silver embedded polymer coatings retained freshness for nearly 30 percent longer compared to traditional PE-coated film.

The pharmaceutical packaging industry is also witnessing the potential of nano-coatings. In this sector, maintaining the chemical stability of medicines is paramount. Moisture-sensitive drugs, such as antibiotics and hormone treatments, require airtight packaging solutions. Nano-coatings can be engineered to deliver ultra-low water vapor transmission rates, enabling the development of lightweight and flexible blister packs or vials that can replace glass or aluminum without compromising efficacy. Moreover, their application in cold chain logistics offers additional benefits, including thermal stability and condensation resistance—factors that play a critical role in global vaccine distribution.

Browse the Complete Report: https://www.futuremarketinsights.com/reports/packaging-coating-market

What sets nano-coatings apart from other innovative technologies is their ability to fuse functionality with environmental responsibility. Many conventional coatings rely on petroleum-based resins and require solvents or chemical additives that pose risks to both human health and the environment. In contrast, several nano-coating solutions are being developed using biodegradable polymers or water-based dispersions, significantly reducing their ecological footprint. For instance, nanocellulose-based coatings derived from plant fiber waste are now being researched as a renewable substitute for fluorinated compounds traditionally used in grease-resistant packaging. These coatings not only perform on par with their chemical counterparts but also align with circular economy goals.

Despite these advantages, widespread adoption of nano-coatings in the packaging coating market is still limited due to regulatory ambiguity and technical challenges. Health concerns surrounding nanoparticle migration, particularly in food-contact applications, have prompted stringent review processes by agencies like the FDA and EFSA. Manufacturers must prove that these particles do not leach into food or medicine under various conditions. Additionally, scale-up challenges remain, especially when it comes to uniformly applying nano-coatings on high-speed production lines without altering existing packaging formats or machinery.

Nevertheless, the packaging coating market is beginning to see a shift. As major brands commit to sustainability targets—such as eliminating unrecyclable packaging by 2035—nano-coatings offer a pathway to reduce material use while maintaining or even enhancing performance. This shift is also being supported by increased R&D funding and collaborations between packaging manufacturers and nanotechnology firms. For example, a joint initiative in South Korea between a packaging company and a university research center recently resulted in a biodegradable nano-coating that resists both oil and oxygen, ideal for snack and pet food applications.

Printing Technology Industry Overview: https://www.futuremarketinsights.com/industry-analysis/printing-technology

0 notes

Text

Polylactic Acid Prices Index: Trend, Chart, News, Graph, Demand, Forecast

The Polylactic Acid (PLA) market experienced diverse price movements across global regions during the first quarter of 2025, shaped by a complex interplay of supply-demand dynamics, sustainability trends, regulatory developments, and economic pressures. PLA, a biodegradable and bio-based polymer derived primarily from renewable sources such as corn starch or sugarcane, has gained increasing importance across industries including packaging, agriculture, textiles, and 3D printing due to rising environmental concerns and the global shift toward eco-friendly materials. In North America, the PLA price trend during Q1 2025 reflected volatility stemming from seasonal changes, logistical issues, and evolving trade dynamics. At the beginning of January, PLA prices remained relatively stable as balanced supply and demand conditions post-holiday helped maintain equilibrium. Sufficient domestic production levels and steady raw material availability, particularly lactic acid and lactide, supported market fundamentals. However, mid-January brought a slight downturn in prices due to competitive pressure, reduced industrial activity, and a typical seasonal dip in consumption. Despite this, demand from core sectors such as compostable packaging and agriculture provided a cushion against steeper declines.

Get Real time Prices for Polylactic Acid: https://www.chemanalyst.com/Pricing-data/polylactic-acid-1275

By February, prices in the North American PLA market weakened further, impacted by oversupply, economic uncertainty, and growing competition from conventional petrochemical-based plastics as well as alternative biodegradable polymers. Rising import volumes, especially from Asia, began to saturate the market, while logistical inefficiencies, particularly at East Coast ports, disrupted supply chains and added downward pressure on prices. However, a shift occurred in March when market sentiment turned more optimistic. Growing demand for sustainable packaging materials, supported by changing consumer preferences and policy initiatives favoring compostable products, led to a 3.7% increase in PLA prices. Innovations such as Ingeo Extend, designed to enhance the performance of PLA across broader applications, contributed to renewed industry confidence. By the end of March 2025, PLA prices in North America closed at USD 2800 per metric ton on a FOB US Gulf Coast basis. Still, when compared to the previous quarter, the prices reflected a marginal decline of around 2%, underscoring the market’s sensitivity to both domestic developments and international competition.

In Europe, the PLA market showed a more consistent upward price trend throughout the first quarter of 2025, driven largely by strong demand, supportive regulatory policies, and rising operational costs. The quarter opened with stable price levels sustained by continued interest from packaging, textile, and 3D printing industries. Regulatory support played a pivotal role in the European market, with new amendments under the EU Packaging and Packaging Waste Regulation (PPWR) and the inclusion of PLA mulch films under the Fertilising Products Regulation driving demand, especially from the agriculture and food packaging sectors. As the quarter progressed, inflationary pressures and elevated energy prices pushed up production and transportation costs across the Eurozone. These rising costs were soon reflected in PLA pricing, especially as supply chains encountered further strain from severe congestion at critical logistics hubs like the Port of Rotterdam in March. Concurrently, feedstock prices, particularly for lactic acid and lactide, saw incremental increases, compounding upward pricing trends across the region. Despite some market resistance to price volatility, the strong regulatory push toward a circular bioeconomy and intensified efforts to curb microplastic pollution continued to support PLA’s long-term market position. By the end of March, PLA prices in Europe reached USD 2490 per metric ton on a FOB Amsterdam basis. Though prices increased throughout the quarter, they ultimately showed no significant change from the previous quarter, indicating that the market had reached a temporary stabilization point after the surge in late 2024.

In the Asia-Pacific region, and particularly in China, the PLA market experienced a mixed pricing trend during Q1 2025, reflecting alternating periods of growth and contraction influenced by demand patterns, production changes, and competitive dynamics. The start of the quarter saw a firm price increase due to post-holiday inventory replenishment and robust demand from packaging, agriculture, and additive manufacturing industries. Maintenance shutdowns at several Chinese PLA production units and rising raw material costs added to supply tightness, supporting the initial price surge. However, by mid-January, prices softened slightly as downstream industries resumed normal operations and new production capacities were introduced, easing the earlier strain on supply. February brought another round of price increases, bolstered by continued interest in bio-based solutions amid growing sustainability awareness and government incentives promoting green materials. Nonetheless, this upward trajectory was short-lived as March saw a gradual price decline.

By the end of Q1 2025, a combination of weakened demand from consumer goods and packaging sectors, improved logistics, increased domestic output, and a rise in available inventories led to downward price adjustments across the Chinese market. Competitive pressures from petroleum-based plastics and other biodegradable alternatives also challenged PLA’s short-term growth. PLA prices in China fell to USD 2300 per metric ton, spot Ex-Qingdao, by the end of March, marking an 8% decrease from the previous quarter. While the short-term outlook revealed signs of market saturation and economic headwinds, long-term prospects for PLA in the Asia-Pacific region remained promising, given the region’s strong manufacturing base, environmental initiatives, and increasing adoption of sustainable packaging solutions.

Overall, the global PLA price landscape during Q1 2025 revealed region-specific trends but shared underlying themes of sustainability-driven demand, raw material cost volatility, logistical hurdles, and regulatory influence. As global markets continue to push for circular economy models and environmentally friendly alternatives to conventional plastics, PLA is expected to retain a critical position in the bio-based polymer space. Price movements going forward will likely depend on raw material availability, production scalability, government policies, and the pace of adoption across various industrial sectors.

Get Real time Prices for Polylactic Acid: https://www.chemanalyst.com/Pricing-data/polylactic-acid-1275

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Polylactic Acid Price#Polylactic Acid Prices#Polylactic Acid Pricing#Polylactic Acid News#Polylactic Acid Price Monitor#Polylactic Acid Database

0 notes

Text

Cosmetic Laminated Tube Packaging Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

The global Cosmetic Laminated Tube Packaging market was valued at 1351 million in 2024 and is projected to reach US$ 2106 million by 2032, at a CAGR of 6.5% during the forecast period.

The global cosmetic laminated tube packaging market is experiencing significant growth, fueled by the evolving demands of the beauty and personal care industry. As consumers increasingly prioritize convenience, hygiene, and sustainability, laminated tubes have emerged as the packaging solution of choice for a wide range of cosmetic products including skincare creams, facial cleansers, hair treatments, and sunscreens. Offering superior barrier properties, aesthetic appeal, and enhanced product protection, these tubes are rapidly replacing traditional containers in both premium and mass-market segments. In addition, rising environmental awareness is prompting manufacturers to develop recyclable, biodegradable, and lightweight tube materials, further accelerating market expansion. With growing investments in packaging innovation and the surge of e-commerce and direct-to-consumer beauty brands, the laminated tube packaging market is poised for robust growth across both developed and emerging economies.

Industry Driver

Rising Demand for Sustainable and Eco-Friendly Packaging

As sustainability becomes a core focus for consumers and brands alike, the cosmetic industry is shifting toward eco-conscious packaging solutions. Laminated tubes made from recyclable and biodegradable materials are gaining traction due to their reduced environmental impact compared to traditional plastic containers. Major brands like L’Oréal and Unilever have launched recyclable laminated tubes to align with their sustainability goals, while startups are adopting PCR (post-consumer recycled) content and bio-based materials. According to industry insights, over 65% of consumers in North America and Europe now consider sustainability a deciding factor when purchasing beauty products, propelling manufacturers to invest in green packaging technologies

Growth in Skincare and Personal Care Product Consumption

The global surge in skincare routines, fueled by rising beauty consciousness, social media influence, and self-care trends, is significantly boosting the demand for cosmetic packaging, especially laminated tubes. These tubes offer superior product protection, extended shelf life, and a premium look ideal for creams, lotions, and serums. The Asia-Pacific region, led by countries like China, South Korea, and India, is witnessing rapid growth in personal care consumption, which directly drives the laminated tube market.

Industry Restraint

High Cost of Raw Materials and Production Complexity

One of the major restraints affecting the growth of the cosmetic laminated tube packaging market is the high cost of raw materials such as aluminum foils, specialized polymer films (like EVOH), and eco-friendly alternatives (such as sugarcane-based plastics). Laminated tube production involves multiple layers to ensure barrier protection, printability, and durability, making the manufacturing process more technically complex and capital-intensive compared to conventional packaging formats. This raises the overall unit cost particularly challenging for small and medium cosmetic brands operating on tight margins. In addition, fluctuations in raw material prices, especially petroleum-based components, further exacerbate cost unpredictability. According to a 2024 packaging industry report, material costs accounted for nearly 55–60% of total laminated tube production expenses, limiting widespread adoption in price-sensitive markets.

Limited Recycling Infrastructure and End-of-Life Challenges

Despite advances in eco-friendly laminated tube designs, recycling remains a major bottleneck due to the multi-layered composition of materials such as plastic, aluminum, and barrier films. Many municipal recycling systems, especially in emerging markets, lack the capability to separate and process these complex structures efficiently. As a result, even tubes labeled as "recyclable" often end up in landfills. This creates a disconnect between sustainable branding and actual environmental impact, drawing criticism from environmentally conscious consumers and watchdog organizations. For instance, a 2023 survey by the Ellen MacArthur Foundation found that less than 30% of laminated cosmetic tubes are effectively recycled worldwide, highlighting a critical gap between innovation and infrastructure.

Industry Opportunity

Expansion of E-commerce and Direct-to-Consumer (DTC) Beauty Brands

The rapid rise of e-commerce and DTC cosmetic brands is creating a strong opportunity for laminated tube packaging. These tubes are lightweight, tamper-evident, and leak-proof, making them ideal for online shipping. Their ability to retain product integrity over long distances and diverse climates makes them a preferred choice for digitally native brands. With more beauty consumers shopping online particularly for skincare, haircare, and wellness products packaging that ensures both performance and shelf appeal is in high demand. Global B2C ecommerce revenue is expected to grow to USD$5.5 trillion by 2027 at a steady 14.4% compound annual growth rate

Technological Advancements in Digital Printing and Customization

Advances in digital printing technologies are enabling high-quality, cost-effective customization of laminated tubes, allowing brands to rapidly prototype and personalize packaging. This is especially valuable for limited editions, influencer collaborations, and seasonal product lines. With consumer demand shifting toward unique, premium, and visually appealing products, brands are leveraging digitally printed tubes to enhance shelf impact and brand recall. Furthermore, new flexographic and hybrid printing methods reduce lead time and waste, aligning with sustainability goals. According to Smithers Pira, the global digitally printed packaging market is expected to grow at a CAGR of 13% through 2026, directly benefiting laminated tube adoption in the cosmetics sector.

Industry Challenges

Balancing Sustainability with Functional Performance

One of the foremost challenges in laminated tube packaging is maintaining barrier integrity and durability while making the packaging sustainable. Laminated tubes typically consist of multiple layers (plastic, aluminum, EVOH, etc.) designed to protect sensitive cosmetic formulations from air, light, and contamination. However, replacing these layers with recyclable or bio-based alternatives often compromises performance leading to reduced shelf life or aesthetic quality. Striking a balance between eco-friendliness and product protection is technically demanding and often expensive. According to industry research, over 70% of packaging developers cite sustainability-performance trade-offs as their top innovation challenge in 2024.

Regulatory Compliance and Evolving Labeling Standards

With the global cosmetic industry facing increasing scrutiny from regulators, laminated tube manufacturers must navigate a complex web of compliance requirements related to material safety, labeling, recyclability, and chemical migration. For example, the European Union’s Packaging and Packaging Waste Regulation (PPWR) and new Extended Producer Responsibility (EPR) laws in countries like Canada and India are pushing brands toward standardized, transparent, and recyclable packaging formats. Adapting to these evolving norms requires frequent design revisions and documentation, which can delay product launches and increase development costs. According to Packaging Europe, compliance costs for cosmetic packaging firms are expected to rise by 15–20% globally between 2024 and 2026.

Competative Analysis

The global cosmetic laminated tube packaging market is characterized by a blend of well-established global leaders and emerging regional players, all competing on innovation, sustainability, and customization capabilities. Key players such as Albéa Group, EPL Ltd. (formerly Essel Propack), Huhtamaki Oyj, Montebello Packaging, Amcor plc, and ALLTUB Group dominate the market with their expansive manufacturing footprints and strong relationships with top-tier cosmetic brands like L’Oréal, Colgate-Palmolive, and Unilever. Albéa has been a frontrunner in sustainable packaging innovation, notably through its recyclable Greenleaf® tube, while EPL Ltd. has launched its recyclable Platina™ tube certified by global recycling bodies.

Meanwhile, Montebello Packaging and Amcor have differentiated themselves by offering advanced digital printing and post-consumer recycled (PCR) content solutions, catering to the rising demand for personalization and eco-conscious branding. Huhtamaki continues to expand its laminated tube portfolio in emerging markets such as India and Southeast Asia. New entrants from China, such as CTLP Packaging, are disrupting the landscape with cost-competitive offerings, although they often face regulatory and sustainability certification hurdles in developed markets. Recent developments between 2023 and 2025 include strategic collaborations (e.g., EPL with Colgate), plant expansions in Europe and Asia, and new recyclable or mono-material tube launches. As brands increasingly focus on ESG compliance and e-commerce-friendly designs, companies with strong R&D and agility in production are gaining a clear competitive edge.

July 2024, Albéa Tubes has launched local production of its Greenleaf™ recycle-ready laminated tube web in North America at its Ontario plant. Certified by APR and RecyClass, this marks a major step in sustainable packaging, with Greenleaf™ expected to comprise 70% of Albéa’s North American tube mix by 2025.

June 2025, TUBEX announced the launches of its 100% recycled aluminium applicator tube, The MonoSense applicator tube is available in multiple sizes with either aluminium or plastic caps. TUBEX says it has high dispensing efficiency for optimal product use and ‘outstanding’ barrier properties.

EPL Ltd. and Colgate-Palmolive strengthened their collaboration by deploying recyclable laminated tubes across Colgate’s product portfolio globally, continuing into 2025. List of Key Amines Flash Rust Inhibitor Companies Profiled

Albea

Essel-Propack

Berry

BeautyStar

Kimpai

Neopac

SUNA

Rego

Abdos

Kyodo Printing

DNP

Montebello

Bell Packaging Group

LeanGroup

Segment Analysis:

By Material Type

The market is segmented based on Material Type into:

Plastic Barrier Laminates (PBL).

Aluminum Barrier Laminates (ABL)

Hybrid Laminates (PCR or Bio-based Layers)

By Capacity

The market is segmented based on Capacity into:

Less than 50 ml

50 ml to 100 ml

More than 100 ml

By Printing Technology

The market is segmented based on Printing Technology into:

Flexographic Printing

Offset Printing

Digital Printing

By Application

The market is segmented based on Application into:

Skin Care

Hair Care

Oral Care

Makeup and Beauty Cosmetics

Body Care & Wellness

Others

Regional Analysis

The Asia-Pacific region currently dominates the global cosmetic laminated tube packaging market, driven by rapid urbanization, increasing disposable incomes, and a booming beauty and personal care industry. Countries like China, India, South Korea, and Japan are at the forefront, with rising skincare consumption and e-commerce penetration fueling demand for cost-effective, visually appealing, and protective packaging formats. This region accounted for the largest market share in 2024 and is expected to register the fastest CAGR through 2030.

Europe follows as a key market, bolstered by stringent environmental regulations, such as the EU’s Packaging and Packaging Waste Regulation (PPWR), which are pushing brands toward recyclable and mono-material tube solutions. Consumers in Western Europe increasingly favor sustainable and premium cosmetic packaging, while countries like France, Germany, and the UK serve as innovation hubs for green beauty packaging.

North America also holds a significant share, with the U.S. leading in demand for eco-friendly laminated tubes, particularly among DTC and luxury skincare brands. The region is witnessing a surge in digital printing and customized packaging to meet evolving consumer preferences for personalized beauty products.

Latin America is emerging as a growth market, particularly in Brazil and Mexico, where rising grooming awareness and expanding cosmetic retail infrastructure are boosting demand for affordable, durable, and hygienic laminated tubes. Although price sensitivity remains a factor, demand for innovative packaging is rising with regional market maturity.

Lastly, the Middle East and Africa (MEA) region, while relatively smaller in size, is growing steadily due to increasing urbanization, premium beauty brand adoption, and the rise of local halal and natural cosmetic brands. The UAE and Saudi Arabia, in particular, are key contributors, with consumer preference shifting toward attractive, functional, and travel-friendly tube formats.

Report Scope

This market research report provides a comprehensive analysis of the global amines flash rust inhibitor market for the forecast period 2025–2032. It delivers accurate and actionable insights based on primary and secondary research methodologies.

Key Coverage Areas:

✅ Market Overview

Global and regional market size (historical & forecast)

Growth trends and value/volume projections

✅ Segmentation Analysis

By product type (Compound Amine Salt, Organic Acid Amine Salt, Others)

By application (Power Generation, Oil & Gas, Pulp & Paper, Metal & Mining, Others)

By end-user industry

✅ Regional Insights

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Country-level analysis for key markets

✅ Competitive Landscape

Company profiles and market share analysis

Key strategies: M&A, partnerships, expansions

Product portfolio analysis

✅ Technology & Innovation

Emerging technologies in corrosion inhibition

Sustainability initiatives in rust prevention

✅ Market Dynamics

Key growth drivers and restraints

Supply chain analysis

✅ Opportunities & Recommendations

High-growth application segments

Strategic recommendations for stakeholders

✅ Stakeholder Insights

Target audience includes manufacturers, suppliers, and end-users

FREQUENTLY ASKED QUESTIONS:

▶ What is the current market size of global Cosmetic Laminated Tube Packaging market ?

Global amines flash rust inhibitor market was valued at USD 1351 million in 2024 and is projected to reach USD 2106 million by 2032.

▶ Which key companies operate in global Cosmetic Laminated Tube Packaging market ?

Key players include Albea, Essel-Propack, Berry, BeautyStar, Kimpai, Neopac, among others.

▶ What are the key growth drivers?

Growth is driven by Rising Demand for Skincare and Personal Care Products Globally.

▶ Which region dominates the market?

Asia-Pacific leads in market share due to rapid industrialization, while North America shows significant technological advancements.

▶ What are the emerging trends?

Emerging trends include Surge in Demand for Digital Printing and Personalizationhttps://www.intelmarketresearch.com/download-free-sample/977/cosmetic-laminated-tube-packaging-2025-2032-932

0 notes

Text

Americas Plastic Bags And Sacks Market Size, Trends, Innovations & Growth Insights

Americas Plastic Bags And Sacks Market Overview The Americas plastic bags and sacks market is a significant segment of the global flexible packaging industry. In 2024, the market is estimated to be valued at USD 10.3 billion and is projected to reach approximately USD 13.5 billion by 2030, growing at a CAGR of 4.5% during the forecast period. This growth is driven by increasing demand from retail, food and beverage, healthcare, and consumer goods sectors. Plastic sacks are particularly favored for their lightweight nature, cost-efficiency, and barrier properties. The rising consumption of packaged and processed food, along with the e-commerce boom, is supporting the expansion of the plastic bags and sacks market across North and South America. However, regulatory pressure around single-use plastics and growing environmental awareness are prompting a shift toward recyclable and biodegradable alternatives. Key players are investing in the development of compostable, bio-based, and reusable bags to align with sustainability trends and regulations. Americas Plastic Bags And Sacks Market Dynamics Market Drivers: Increasing urbanization, retail sector growth, and a surge in online shopping have amplified the demand for flexible packaging solutions. Additionally, advancements in polymer processing and extrusion technologies are enhancing the production efficiency and product variety in plastic sacks. Restraints: Environmental concerns and the implementation of strict regulations on plastic usage—especially in countries like the U.S., Canada, and parts of Latin America—are restricting market growth. Public sentiment against single-use plastics and the push for zero-waste policies are also challenging traditional plastic bag consumption. Opportunities: Opportunities lie in the production of sustainable plastic bags, including oxo-biodegradable, compostable, and recycled-content options. With growing demand for green packaging and circular economy initiatives, companies that innovate in material science and waste management will see long-term growth. Technology and sustainability are playing transformative roles, with manufacturers exploring bio-polymers, improved recycling processes, and digital printing for brand customization. Regulatory support for eco-friendly materials is further catalyzing this shift. Download Full PDF Sample Copy of Americas Plastic Bags And Sacks Market Report @ https://www.verifiedmarketresearch.com/download-sample?rid=514917&utm_source=PR-News&utm_medium=387 Americas Plastic Bags And Sacks Market Trends and Innovations Emerging trends in the Americas plastic bags and sacks industry include the integration of smart packaging technologies, antimicrobial bags for healthcare use, and advanced multilayer film structures for improved strength and durability. Bioplastic and starch-based sack production is witnessing a surge, especially for retail and agricultural applications. Innovations in lightweight, high-tensile plastic sacks are reducing material usage without compromising quality. Collaborative efforts among manufacturers, recyclers, and regulatory bodies are driving material recovery systems. Automation in bag manufacturing lines is increasing production speed and precision, thereby enhancing supply chain efficiencies. Americas Plastic Bags And Sacks Market Challenges and Solutions The market faces several challenges including volatile raw material prices, tightening government policies on plastic usage, and fragmented recycling infrastructure. Supply chain disruptions, particularly for virgin and recycled polymers, have impacted production timelines and cost structures. Solutions involve diversifying raw material sources, investing in closed-loop recycling systems, and forming public-private partnerships to enhance waste collection and segregation. Leveraging digital technologies like AI and blockchain can also optimize logistics and improve traceability in plastic lifecycle management. Americas Plastic Bags And Sacks Market Future Outlook

The Americas plastic bags and sacks market is poised for moderate yet resilient growth over the next decade. The market's future will be shaped by the transition toward sustainable and smart packaging solutions, greater consumer awareness, and evolving legislative landscapes. With continued investments in green technologies, biodegradable material development, and compliance with extended producer responsibility (EPR) regulations, the industry will gradually pivot from traditional plastic bags to circular economy-aligned alternatives. By 2030, North America is expected to lead in innovation, while Latin America offers growth potential through infrastructure upgrades and policy adoption. Americas Plastic Bags And Sacks Market Competitive Landscape The Americas Plastic Bags And Sacks Market competitive landscape is characterized by intense rivalry among key players striving to gain market share through innovation, strategic partnerships, and expansion initiatives. Companies in this market vary from established global leaders to emerging regional firms, all competing on parameters such as product quality, pricing, technology, and customer service. Continuous investments in research and development, along with a focus on sustainability and digital transformation, are common strategies. Mergers and acquisitions further intensify the competition, allowing companies to broaden their portfolios and geographic presence. Market dynamics are influenced by evolving consumer preferences, regulatory frameworks, and technological advancements. Overall, the competitive environment fosters innovation and drives continuous improvement across the Americas Plastic Bags And Sacks Market ecosystem. Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount?rid=514917&utm_source=PR-News&utm_medium=387 Americas Plastic Bags And Sacks Market Segmentation Analysis The Americas Plastic Bags And Sacks Market segmentation analysis categorizes the market based on key parameters such as product type, application, end-user, and region. This approach helps identify specific consumer needs, preferences, and purchasing behavior across different segments. By analyzing each segment, companies can tailor their strategies to target high-growth areas, optimize resource allocation, and improve customer engagement. Product-based segmentation highlights variations in offerings, while application and end-user segmentation reveal usage patterns across industries or demographics. Regional segmentation uncovers geographical trends and market potential in emerging and developed areas. This comprehensive analysis enables stakeholders to make informed decisions, enhance competitive positioning, and capture new opportunities. Ultimately, segmentation serves as a critical tool for driving focused marketing, innovation, and strategic growth within the Americas Plastic Bags And Sacks Market. Americas Plastic Bags And Sacks Market, By Type Americas Plastic Bags And Sacks Market, By Application Americas Plastic Bags And Sacks Market, By End User Americas Plastic Bags And Sacks Market, By Geography • North America• Europe• Asia Pacific• Latin America• Middle East and Africa For More Information or Query, Visit @ https://www.verifiedmarketresearch.com/product/americas-plastic-bags-and-sacks-market/ About Us: Verified Market Research Verified Market Research is a leading Global Research and Consulting firm servicing over 5000+ global clients. We provide advanced analytical research solutions while offering information-enriched research studies. We also offer insights into strategic and growth analyses and data necessary to achieve corporate goals and critical revenue decisions. Our 250 Analysts and SMEs offer a high level of expertise in data collection and governance using industrial techniques to collect and analyze data on more than 25,000 high-impact and niche markets. Our analysts are trained to combine modern data collection techniques,

superior research methodology, expertise, and years of collective experience to produce informative and accurate research. Contact us: Mr. Edwyne Fernandes US: +1 (650)-781-4080 US Toll-Free: +1 (800)-782-1768 Website: https://www.verifiedmarketresearch.com/ Top Trending Reports https://www.verifiedmarketresearch.com/ko/product/foundry-additives-market/ https://www.verifiedmarketresearch.com/ko/product/coherent-optical-equipment-market/ https://www.verifiedmarketresearch.com/ko/product/polypropylene-random-copolymer-market/ https://www.verifiedmarketresearch.com/ko/product/high-performance-polyamides-market/ https://www.verifiedmarketresearch.com/ko/product/plastic-packaging-market/

0 notes

Text

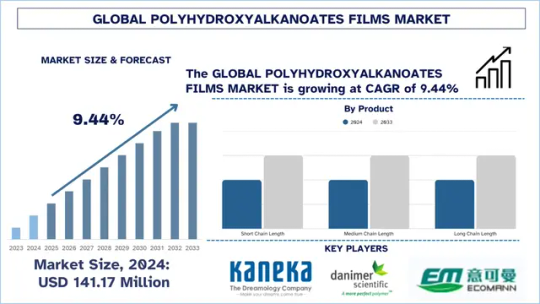

Polyhydroxyalkanoates Films Market Report, Trends, Analysis & Forecast

According to the UnivDatos, as per their “Polyhydroxyalkanoates Films Market” report, the global market was valued at USD 141.17 million in 2024, growing at a CAGR of about 9.44% during the forecast period from 2025 - 2033 to reach USD million by 2033.

The global polyhydroxyalkanoates (PHA) films market is now gaining momentum as the industries around the world are moving into materials that are equally functional yet responsible for the environment. PHA films are biodegradable films processed using microbial fermentation processes utilizing renewable feedstocks, thus posing as a sustainable alternative to traditional petroleum-based plastics. This is due to their properties such as biodegradability, compostability, and performance. These films are used in a wide range of applications in various sectors such as food packaging, agriculture, and biomedical devices. With increasing concerns over plastic waste and tightening regulations all over the world, PHA films are becoming the next generation of sustainable material solutions.

Stringent Environmental Regulations Drive Market Growth

One of the major reasons behind the rapid growth of PHA films is the rapid increase due to a slew of rigid environmental regulations put into place in various countries all over the world. Some areas in Europe, North America, and Asia are taking measures to reduce, restrict, or outright ban single-use plastics. Countries are implementing regulations such as the EU Single-Use Plastics Directive and California's Plastic Pollution Prevention and Packaging Producer Responsibility Act are effectively building an inescapable demand for compostable and marine-degradable packaging materials. For instance, the Plastic Waste Management Rules, 2016, as amended, provide the statutory framework and the prescribed authorities for enforcement of the rules, including a ban on single-use plastic items. The country has implemented a complete ban on single-plastic items from the 1st to the 31st of July 2022. Therefore, the demand for polyhydroxyalkanoate films increases. As these films find themselves in an excellent position to meet these requirements, they offer a closed-loop alternative that can biodegrade through soil, marine, and home-composting environments. For that very reason, PHA is an apt candidate for consumer goods and packaging firms wanting to meet EPR laws and sustainability reporting requirements. Companies would thus accelerate the adoption of PHA films in retail, food service, and agriculture by reviewing their packaging portfolio to include bioplastics.

Latest Trends in the Polyhydroxyalkanoates Films Market

Shift Toward Multi-Functional Bioplastics

As the bio-based materials market grows older, a strong melody around multifunctional bioplastics gains popularity. Hence, the PHA films trail the innovation curve. The earlier generation of bioplastics did offer biodegradation but at the expense of performance; next-gen PHA films are being engineered for applications with varying demands, being oxygen barriers, antimicrobial, UV-protective, and mechanically strong. This trend is strong in food-packaging applications, where materials have to maintain shelf life while having an eco-label attached. Likewise, in medical sectors, PHA films are being studied as wound dressings and drug-delivery systems, whereby biodegradability after use gives them advantages. This trend is further pushed by the ongoing active R&D investments and collaborative effort among biopolymers startups, academics, and global packaging brands are the main driving forces behind these advancements. As performance catches up with ecological benefits, PHA films have begun transformation into competitive, high-performing material solutions.

Access sample report (including graphs, charts, and figures): https://univdatos.com/reports/polyhydroxyalkanoates-films-market?popup=report-enquiry

Emerging Opportunities in Asia-Pacific and Latin America

The growing plastic waste awareness is growing, along with government support, and this has opened up new opportunities in emerging markets in Asia and Latin America. Landed with rapid urbanization and growing consumer demand for sustainable packaging, countries like India, China, Brazil, and Mexico offer fertile grounds for bio-based solutions such as PHA films. Policy-backed pathways for adoption are being forged by government-led initiatives such as India's ban on various single-use plastic items and Chile's extended producer responsibility laws. Simultaneously, climate financing and development partnerships at the international level are financing PHA production at the local level with Agri-waste as feedstock, embedding the circular economy concept. This, therefore, creates a very lucrative opportunity for firms to expand manufacturing and distribution activities in these regions. Also, adoption of eco-certification schemes and sustainable public procurement programs further promotes demand for compostable packaging and agricultural films, giving manufacturers a front-runner advantage in establishing brand equity and local supply chains.

PHA films drive sustainable progress as the future of high-performance, biodegradable materials

As the world economy is inclined more and more toward low-carbon and circular solutions, PHA films stand out for their sustainability and performance. PHA films deliver full biodegradability without compromising on utility has making them an important thrust for the substitution of fossil-fuel-based plastics. While challenges concerning scalability and costs remain, regulatory push, technological progress, and new market opportunities are setting forth a strong path for the growth of the industry. From food protection to wound healing and nurturing, PHA films are no longer just nature-friendly alternatives- they are the materials of the future, weaving a world where performance and planet meet side by side.

Contact Us:

UnivDatos

Contact Number - +1 978 733 0253

Email - [email protected]

Website - https://univdatos.com/

Linkedin- https://www.linkedin.com/company/univ-datos-market-insight/mycompany/

0 notes

Text

Startups & Biorefineries Tackle Fossil Dependency with Green Chemistry

The Global Bio Plasticizer market is projected to grow at a CAGR of 7.2% during the forecast period 2024–2031, driven by rising demand across pharmaceuticals, packaging, consumer goods, automotive, and construction sectors. Derived from renewable sources, bio plasticizers offer eco-friendly alternatives to traditional phthalates without compromising performance. Growing regulatory pressure, environmental concerns, and market shifts toward sustainable materials are fueling adoption. Competitive dynamics are intensifying with key players like Evonik, Lanxess AG, and Solvay S.A. actively shaping the market landscape.

Unlock exclusive insights with our detailed sample report :

Key Market Drivers

1. Regulatory Pressure Against Phthalates

The global push against DEHP, DBP, BBP, and other toxic phthalates has accelerated demand for bio-based plasticizers. Regulatory bans in the U.S., EU, and Japan are reshaping material sourcing in industries such as childcare, healthcare, and construction.

2. Sustainability in Packaging and Consumer Goods

Consumer demand for eco-friendly packaging, especially for food and beverages, is fostering the adoption of biodegradable and compostable plasticizers that are safe and do not leach harmful chemicals.

3. Green Building and Construction Codes

Green construction norms including LEED, BREEAM, and national building codes now encourage or mandate the use of non-toxic and sustainable materials. Bio plasticizers are thus replacing fossil-based alternatives in flooring, cables, and wall coverings.

4. Automotive Light-Weighting and Interior Health

As automakers seek lightweight, flexible, and non-volatile interior materials, bio plasticizers enable PVC flexibility while reducing VOC emissions, contributing to better cabin air quality and recyclability.

5. Biopolymer Expansion in Packaging

Bio plasticizers are critical for enhancing the flexibility and durability of PLA, PHA, and other biopolymers used in packaging films, wraps, and single-use items. Their addition improves processing and final product properties.

Regional Trends

United States

The U.S. market is witnessing rapid growth due to:

Phthalate bans by the Consumer Product Safety Commission (CPSC) in toys and childcare articles.

Adoption of citrate and soybean-based plasticizers in healthcare and food-grade packaging.

Investment by chemical firms in green chemistry initiatives.

Integration into BPA- and phthalate-free medical devices, a key growth area post-COVID-19.

Japan

Japan is a frontrunner in:

R&D on castor oil-based and epoxidized soy oil plasticizers for high-specification electronics and industrial films.

Applications in automotive, consumer electronics, and elder-care medical devices.

Collaborations between companies like Kaneka Corporation, DIC Corporation, and academic institutes to develop non-toxic, biodegradable plasticizers.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

Material & Application Insights

By Material Type:

Epoxidized Soybean Oil (ESBO)

Citrate Esters

Sebacates

Castor Oil Derivatives

Palm Fatty Acid Esters

Starch Derivatives

By Application:

Consumer Goods (Toys, Footwear)

Medical Devices (Tubes, Blood Bags)

Packaging (Flexible Films, Labels)

Automotive Interiors

Construction (Flooring, Cables, Adhesives)

By End-Use Industry:

Healthcare

Packaging

Construction

Automotive

Agriculture Films

Textiles and Coatings

Latest Industry Trends

Bio Plasticizer-Enabled Flexible Electronics Flexible OLEDs and wearable electronics now use bio plasticizer-modified films to enhance flexibility and biodegradability.

Rapid Growth in Medical Applications Post-Pandemic Hospitals are transitioning to phthalate-free devices, driving demand for bio plasticizers in tubing, masks, IV bags, and gloves.

Startups and Innovators Using Waste Oils Firms are turning used cooking oils, algae oils, and agricultural byproducts into high-performance, cost-effective plasticizers.

Digital Twin and AI in Formulation R&D Companies use AI tools to model bio plasticizer–polymer interactions, reducing development time for customized blends.

Partnerships in Biorefineries for Raw Material Supply Major chemical players are securing long-term contracts with palm and soy oil producers, enhancing supply chain security and scalability.

Buy the exclusive full report here:

Growth Opportunities

Expansion in Emerging Markets with infrastructure and healthcare investment driving flexible PVC usage.

Integration with PLA and Other Bioplastics to boost mechanical performance for compostable packaging.