#Data Center Monitoring Software Data Center Monitoring Software Market Data Center Monitoring Software Market 2022 Data Center Monitoring So

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a low social media market share in South America.

Text

Key Drivers and Market Share Analysis of Global ASCs Industry Through 2033

Astute Analytica stands out as a premier provider of comprehensive Ambulatory Surgical Centers market research reports specifically tailored for the healthcare sector. Our commitment lies in delivering valuable insights and research that empower healthcare organizations to navigate the complexities of this rapidly evolving industry.

By understanding the trends and opportunities within the healthcare market, businesses can strategically position themselves for success in an increasingly competitive environment. The integration of digital solutions, a focus on sustainability, and the adaptation to new care delivery models are essential components for enhancing patient care and ensuring the long-term viability of healthcare systems.

Vacuum blood collection tube market was valued at US$ 3.24 billion in 2024 and is projected to hit the market valuation of US$ 4.40 billion by 2033 at a CAGR of 3.45% during the forecast period 2025–2033.

A Request of this Sample PDF File@- https://www.astuteanalytica.com/request-sample/ambulatory-surgical-centers-market

The Essential Path of Digital Transformation in Healthcare

As we approach 2025, health system leaders across the globe are prioritizing efforts to drive efficiencies, boost productivity, and improve patient engagement. A significant factor influencing these initiatives is the accelerated digital transformation within healthcare, which has been identified as the most impactful issue for global health systems in the coming years. This emphasis on digitalization is not surprising, considering that healthcare has lagged behind other industries, such as retail and finance, in adopting advanced digital technologies.

According to recent surveys, approximately 70% of respondents believe that investing in technology platforms for digital tools and services will be crucial for their organizations. Furthermore, 60% of leaders highlighted the necessity of investing in core technologies, including electronic medical records (EMRs) and enterprise resource planning (ERP) software. Notably, around 90% of C-suite executives anticipate a significant acceleration in the use of digital technologies by 2025, with half expecting a profound impact on their operations.

The Rise of Consumer-Driven Digital Health Tools

The growing adoption of connected monitoring devices and digital tools among consumers is reshaping the healthcare landscape. In 2024, 43% of consumers are expected to utilize these technologies, up from 34% in 2022. This shift aligns with the highly personalized experiences that consumers have come to expect from industries such as banking, retail, and entertainment. Digital monitoring tools empower consumers by providing trending data that supports their health concerns, thereby enhancing their agency during patient-clinician interactions. This increased control and confidence is particularly vital in areas like maternal health, where timely and informed interactions can prevent adverse outcomes.

Mergers and Acquisitions in Healthcare Technology

The healthcare technology sector is poised for a surge in mergers and acquisitions (M&A) as we move into 2024. The COVID-19 pandemic has underscored the importance of health technology and healthcare delivery systems, prompting a renewed focus on consolidation within the industry. In 2023, biopharma M&A experienced a remarkable rebound, with an aggregate deal value increasing by 79% compared to 2022, reaching approximately $152 billion—the highest level since 2019. The average deal size has also shown an upward trend, approaching levels not seen since 2020. Several positive catalysts are expected to support this momentum in 2024, including emerging threats to growth, a fear of missing out on opportunities, and a resurgence of high-prevalence conditions that necessitate innovative solutions.

The U.S. Healthcare Market Landscape

The United States remains the world's largest healthcare market, with healthcare spending reaching $4.3 trillion in 2021, translating to about $12,900 per person. However, as consolidation continues and exposure to government payers increases, healthcare markets in other regions are anticipated to grow at a faster pace. Despite the substantial investment in healthcare, the outcomes do not always reflect this high expenditure, leading to significant disparities in access and quality of care. The U.S. healthcare system is evolving in response to these challenges, particularly the pressures of rising costs and an increasing number of uninsured individuals.

Navigating Political Changes and Regulatory Shifts

As the healthcare industry prepares for 2025, potential changes in political leadership could usher in new policy directions and regulatory shifts. Leaders within the healthcare space must remain agile, anticipating policy reforms that could reshape operational priorities, including resource allocation and shifts in care delivery models. Building collaborative ecosystems and staying informed about legislative developments will be crucial for organizations aiming to thrive in this dynamic environment.

For Purchase Enquiry: https://www.astuteanalytica.com/industry-report/ambulatory-surgical-centers-market

Market Segmentation and Analysis

In its quest for a granular understanding of the Ambulatory Surgical Centers market, the report segments the industry into various categories. This segmentation facilitates a more detailed analysis of the dynamics within each segment, allowing stakeholders to identify specific growth opportunities and challenges. By breaking down the market, the report aids in crafting targeted strategies tailored to the unique characteristics of each segment.

By Ownership

Physician Only

Hospital Only

Corporation Only

Physician & Hospital

Physician & Corporation

Hospital & Corporation

By Surgery Type

Dental

Otolaryngology

Endoscopy

Obstetrics / Gynecology

Opthalmology

Orthopedic

Cardiovascular

Neurology

Plastic Surgery

Podiatry

Others

By Specialty Type

Multi-specialty

Single specialty

By Service

Diagnosis

Treatment

By Region

North America

The U.S.

Canada

Mexico

Europe

Western Europe

The UK

Germany

France

Italy

Spain

Rest of Western Europe

Eastern Europe

Poland

Russia

Hungary

Rest of Eastern Europe

Asia Pacific

China

India

Japan

South Korea

Australia & New Zealand

ASEAN

Rest of Asia Pacific

Middle East

UAE

Saudi Arabia

Bahrain

Kuwait

Qatar

Rest of Middle East

Africa

Oman

Egypt

Nigeria

South Africa

Rest of Africa

South America

Argentina

Brazil

Rest of South America

Geographical Segmentation

The report further segments the market into geographical regions, including North America, South America, Asia, Europe, Africa, and Others. Each region is examined with a focus on key countries, providing insights into the current market size and forecasts extending until 2033. This geographical breakdown is critical for understanding regional market dynamics and tailoring strategies to meet local demands effectively.

Competitive Landscape

A significant portion of the report is dedicated to analyzing the competitive landscape within the global Ambulatory Surgical Centers market. This includes a comprehensive examination of leading Ambulatory Surgical Centers product vendors, highlighting their latest developments and market shares in terms of shipment and revenue. By profiling these major players, the report offers valuable insights into their product portfolios, technological capabilities, and overall market positioning.

The report identifies key players in the Ambulatory Surgical Centers market, providing a closer look at their contributions to the industry. This competitive profiling is essential for understanding the strengths and weaknesses of various companies, enabling stakeholders to make informed decisions and devise effective strategies in a crowded marketplace.

CHSPSC, LLC.

Eifelhöhen-Klinik AG

Edward-Elmhurst Health

Healthway Medical Group

Envision Healthcare Corporation

Nexus Day Surgery Centre

Pediatrix Medical Group

Prospect Medical Holdings, Inc.

Surgery Partners

SurgCenter

TH Medical

UNITEDHEALTH GROUP

Other Prominent Players

Download Sample PDF Report@- https://www.astuteanalytica.com/request-sample/ambulatory-surgical-centers-market

About Astute Analytica:

Astute Analytica is a global analytics and advisory company that has built a solid reputation in a short period, thanks to the tangible outcomes we have delivered to our clients. We pride ourselves in generating unparalleled, in-depth, and uncannily accurate estimates and projections for our very demanding clients spread across different verticals. We have a long list of satisfied and repeat clients from a wide spectrum including technology, healthcare, chemicals, semiconductors, FMCG, and many more. These happy customers come to us from all across the globe.

They are able to make well-calibrated decisions and leverage highly lucrative opportunities while surmounting the fierce challenges all because we analyse for them the complex business environment, segment-wise existing and emerging possibilities, technology formations, growth estimates, and even the strategic choices available. In short, a complete package. All this is possible because we have a highly qualified, competent, and experienced team of professionals comprising business analysts, economists, consultants, and technology experts. In our list of priorities, you-our patron-come at the top. You can be sure of the best cost-effective, value-added package from us, should you decide to engage with us.

Get in touch with us

Phone number: +18884296757

Email: [email protected]

Visit our website: https://www.astuteanalytica.com/

0 notes

Text

Price: [price_with_discount] (as of [price_update_date] - Details) [ad_1] SAMSUNG 990 PRO with Heatsink is designed for tech enthusiasts, hardcore gamers and heavy-workload professionals who want blazing fast speed. Compatible with PlayStation® 5, and integrated heatsink disperses heat to maintain speed, power, efficiency and thermal control, preventing downtime overheating on consoles and PCs. Experience sequential read/write speeds up to 7,450/6,900 MB/s.* *PCIe 4.0’s best theoretical sequential read is 8000 MB/s - 990 PRO reaches 7450 MB/s as of Q3, 2022. **Source: 2003-2022 OMDIA data: NAND suppliers' revenue market share. ***Sequential and random write performance was measured with Intelligent Turbo Write technology being activated. Intelligent Turbo Write operates only within a specific data transfer size. Performance may vary depending on SSD’s firmware, system hardware & configuration and other factors. For detailed information, please contact your local service center. 990 PRO reaches 7,450 MB/s based on test system configuration: AMD Ryzen 7 5800X 8-Core Processor [email protected], DDR4 3600MHz 16GBx2 (PC4-25600 Overclock), OS - Windows 10 Pro 64bit, Chipset - ASRock-X570 Taichi. To maximize the performance of the 990 PRO, please check whether your system supports PCIe 4.0 at the Intel or AMD website. ****PCI-SIG®D8 standard spec: 8.8mm. *****980 PRO Sequential Read/Write - 1,129/877 MB/Watt, 990 PRO Sequential Read/Write - 1380/1319 MB/Watt based on test result of 1TB capacity model. OUR ULTIMATE SSD: Reach near max performance with PCIe 4.0*; The in-house controller's smart heat control delivers our best power efficiency while maintaining ferocious performance that always keeps you at the top of your game MAXIMIZED PCIE 4.0 SPEED: Get random read/write speeds that are 40%/55% faster than 980 PRO; Experience up to 1400K/1550K IOPS and read/write speeds up to 7450/6900 MB/s for gaming, video editing, 3D modeling, data analysis and more** BREAKTHROUGH POWER EFFICIENCY: Get more performance while using less power; Enjoy up to 50% improved performance per watt over 980 PRO*** THERMAL CONTROL: Samsung's nickel-coated high-end controller delivers thermal control and prevents performance drops from overheating; 990 PRO with Heatsink is a perfect fit for PlayStation 5, desktops, laptops that meet the PCI-SIG D8 standard**** THE CHAMPION MAKER: A more than 55% improvement in random performance enables faster loads for an ultimate gaming experience on PS5 and DirectStorage PC games; With RGB LED lights, Heatsink’s futuristic design adds style to function***** SAMSUNG MAGICIAN SOFTWARE: Get the most out of your SSD with Samsung Magician's advanced yet intuitive optimization tools; Monitor drive health, protect valuable data, and receive important updates for your 990 PRO WORLD'S #1 FLASH MEMORY BRAND: Experience performance and reliability from the world's #1 brand for flash memory since 2003; All firmware & components, including Samsung's world-renowned DRAM & NAND, are produced in-house for quality you can trust****** [ad_2]

0 notes

Text

Interactive Video Wall Industry: Transforming Digital Engagement Across Sectors

The Interactive Video Wall Industry is rapidly evolving into a cornerstone of digital communication and visualization. Valued at USD 5.6 billion in 2022, this industry is projected to reach USD 13.2 billion by 2030, growing at a robust CAGR of 11.2%. From retail showrooms and educational institutions to command centers and healthcare facilities, interactive video walls are reshaping how organizations deliver immersive and responsive experiences.

Industry Dynamics

A Shift Toward Experience-Driven Environments

The industry is moving from static signage to intelligent, real-time visual interfaces. Interactive video walls provide tactile and gesture-responsive surfaces, enabling dynamic content interaction. This has fueled adoption across industries where engagement and visibility are paramount.

Convergence of AI, IoT, and Big Data

Next-generation video walls are increasingly integrated with artificial intelligence and IoT devices. This allows businesses to display data-rich dashboards, environmental updates, or customer behavior analytics—all updated in real time. These capabilities position the interactive video wall industry at the center of smart workspace and city initiatives.

Digital Transformation in Control and Command Centers

Security, defense, utility, and traffic monitoring centers are deploying large-scale video walls for situational awareness and multi-source data visualization. Real-time control room operations now rely on unified visual intelligence delivered through high-resolution displays.

Growth of Hybrid and Remote Workplaces

With remote collaboration becoming mainstream, enterprises are investing in interactive displays for high-quality video conferencing and cross-regional collaboration. Touch-enabled video walls allow simultaneous engagement from multiple devices and sources.

Industry Applications

Retail: Enhances customer engagement with real-time promotions, product demos, and brand storytelling in flagship stores and malls.

Education: Enables active learning and group collaboration in digital classrooms, auditoriums, and virtual labs.

Healthcare: Supports surgical planning, telemedicine visualization, and patient education in modern medical centers.

Government & Defense: Powers mission-critical decisions in emergency operations, surveillance hubs, and border control.

Corporate Sector: Transforms meeting rooms and common areas into data-driven, presentation-friendly spaces.

Transportation: Improves traveler experience through flight/train information systems, digital signage, and wayfinding.

Competitive Landscape

The Interactive Video Wall Industry includes a mix of global tech innovators and display specialists. Major industry players include:

Samsung Electronics

LG Display

Barco NV

Planar Systems

NEC Display Solutions

Christie Digital Systems

ViewSonic Corporation

Delta Electronics

These companies compete through innovation in screen resolution (4K/8K), ultra-thin bezels, brightness control, and software features such as remote management, modular scalability, and AI-enhanced user interfaces.

Strategic Moves:

Partnerships with AV integrators

Acquisitions of touch tech and signage software firms

Expansions into emerging markets

Development of energy-efficient, ultra-narrow bezel displays

Regional Highlights

North America leads due to enterprise innovation and control room integration.

Asia-Pacific is experiencing rapid adoption in smart cities, retail, and education.

Europe shows consistent demand driven by infrastructure modernization and public transit systems.

Future Outlook

As demand for smarter, more interactive environments grows, the Interactive Video Wall Industry is poised for exponential expansion. Investments in AR/VR integration, seamless multi-display interfaces, and AI-powered content delivery will drive future innovation. This sector will continue to redefine how institutions visualize, collaborate, and communicate information.

Trending Report Highlights

Discover other fast-evolving sectors aligned with visual and collaborative tech:

Automotive Manufacturing Equipment Market

Mid High Level Precision GP Market

RF Chip Inductor Market

Zoom Lens Market

Frame Grabber Market

0 notes

Text

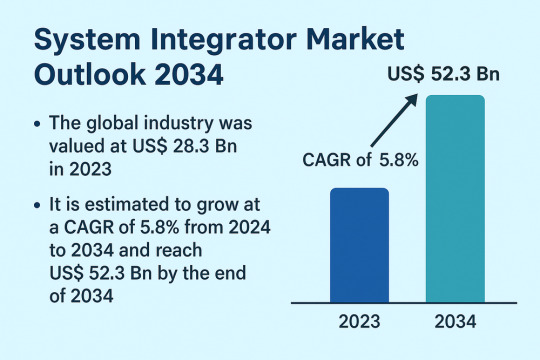

Automation and Integration Needs Power Robust Growth in System Integrator Market

The global System Integrator Market is poised for significant growth, projected to rise from US$ 28.3 Bn in 2023 to US$ 52.3 Bn by 2034, growing at a CAGR of 5.8% from 2024 to 2034. This growth is driven by the widespread adoption of industrial robots, technological advancements, and a pressing need among businesses to optimize operational efficiencies through connected systems.

System integrators play a pivotal role in designing, implementing, and maintaining integrated solutions that bring together hardware, software, and consulting services. These services support organizations in unifying internal and external systems, such as SCADA, HMI, MES, PLC, and IIoT, to enable seamless data flow and system interoperability.

Market Drivers & Trends: One of the primary market drivers is the rise in adoption of industrial robots. As industries accelerate automation, robotic system integrators have become vital in delivering customized, scalable, and high-performing solutions tailored to complex manufacturing needs.

Another major catalyst is the surge in technological advancements. Integrators are deploying cloud-based tools and platforms that provide real-time data insights, improve developer productivity, and support hybrid architectures. The increasing use of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) in integration solutions is fostering innovation and growth.

Latest Market Trends

Several emerging trends are shaping the system integrator landscape:

Cloud modernization platforms such as IBM’s Z and Cloud Modernization Center are enabling businesses to accelerate the transition to hybrid cloud environments.

Modular automation platforms are gaining popularity, allowing companies to rapidly deploy and scale integration solutions across multiple industry verticals.

Edge computing and cybersecurity solutions are increasingly being integrated to support secure, real-time decision-making on the production floor.

Digital hubs and scalable workflow engines are being adopted by integrators to support multi-specialty applications with high adaptability.

Key Players and Industry Leaders

The system integrator market is characterized by a strong mix of global leaders and regional specialists. Key players include:

ATS Corporation

Avanceon

Avid Solutions

Brock Solutions

JR Automation

MAVERICK Technologies, LLC

Burrow Global, LLC

BW Design Group

John Wood Group PLC

TESCO CONTROLS

These companies are actively investing in next-generation technologies, enhancing their product portfolios, and pursuing strategic acquisitions to strengthen market presence. For instance, in July 2023, ATS Corporation acquired Yazzoom BV, a Belgian AI and ML solutions provider, expanding their capabilities in smart manufacturing.

Recent Developments

Olympus Corporation launched the EASYSUITE ES-IP system in July 2023 in the U.S., offering advanced visualization and integration solutions for procedure rooms.

IBM introduced key updates in 2021 and 2022 to streamline mission-critical application modernization using cloud services and hybrid IT strategies.

Asia-Pacific companies have led the charge in deploying advanced integrated systems, reflecting the rapid industrial digitization in countries such as China, Japan, and South Korea.

Market Opportunities

Opportunities abound in both mature and emerging markets:

Smart factories and Industry 4.0 transformation offer immense potential for integrators to offer comprehensive solutions tailored to real-time analytics, predictive maintenance, and remote monitoring.

Government-led infrastructure modernization projects, particularly in Asia and the Middle East, are increasing demand for integrated control systems and plant asset management solutions.

The energy transition movement, including renewables and electrification of industrial processes, requires new types of integration across decentralized assets.

Future Outlook

As industries pursue digital transformation, the role of system integrators will evolve from traditional project implementers to long-term strategic partners. The future will see increasing demand for intelligent automation, cross-domain expertise, and real-time adaptive solutions. Vendors who can provide holistic, secure, and scalable services will dominate the landscape.

With continued advancements in AI, IoT, and robotics, the system integrator market will continue to thrive, transforming operations across diverse sectors, from automotive and food & beverages to oil & gas and pharmaceuticals.

Review critical insights and findings from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=82550

Market Segmentation

The market is segmented based on offering, technology, and end-use industry.

By Offering:

Hardware

Software

Service (Consulting, Design, Installation)

By Technology:

Human-Machine Interface (HMI)

Supervisory Control and Data Acquisition (SCADA)

Manufacturing Execution System (MES)

Functional Safety System

Machine Vision

Industrial Robotics

Industrial PC

Industrial Internet of Things (IIoT)

Machine Condition Monitoring

Plant Asset Management

Distributed Control System (DCS)

Programmable Logic Controller (PLC)

By End-use Industry:

Oil & Gas

Chemical & Petrochemical

Food & Beverages

Automotive

Energy & Power

Pharmaceutical

Pulp & Paper

Aerospace

Electronics

Metals & Mining

Others

Regional Insights

Asia Pacific leads the global system integrator market, holding the largest market share in 2023. This leadership is attributed to:

Rapid industrialization and digital transformation in China, Japan, and India.

Strong investments in smart manufacturing and Industry 4.0 initiatives.

Government support for infrastructure modernization, especially through Smart City programs and cybersecure IT frameworks.

North America and Europe also show strong demand, driven by the presence of established manufacturing facilities and a robust focus on sustainable operations and green automation.

Why Buy This Report?

Comprehensive Market Analysis: Deep insights into market size, share, and growth across all major segments and geographies.

Detailed Competitive Landscape: Profiles of leading companies with analysis of their strategy, product offerings, and key financials.

Actionable Intelligence: Understand technological trends, regulatory developments, and investment opportunities.

Forecast-Based Strategy: Develop long-term strategic plans using data-driven forecasts up to 2034.

Frequently Asked Questions (FAQs)

1. What is the projected value of the system integrator market by 2034? The global system integrator market is projected to reach US$ 52.3 Bn by 2034.

2. What is the current CAGR for the forecast period 2024–2034? The market is anticipated to grow at a CAGR of 5.8% during the forecast period.

3. Which region holds the largest market share? Asia Pacific dominated the global market in 2023 and is expected to continue leading due to rapid industrialization and technology adoption.

4. What are the key growth drivers? Key drivers include the rise in adoption of industrial robots and continuous advancements in integration technologies like IIoT, AI, and cloud platforms.

5. Who are the major players in the system integrator market? Prominent players include ATS Corporation, JR Automation, Brock Solutions, MAVERICK Technologies, and Control Associates, Inc.

6. Which industries are adopting system integrator services the most? High adoption is seen in industries such as automotive, oil & gas, food & beverages, pharmaceuticals, and electronics.

Explore Latest Research Reports by Transparency Market Research:

Multi-Mode Chipset Market: https://www.transparencymarketresearch.com/multi-mode-chipset-market.html

Accelerometer Market: https://www.transparencymarketresearch.com/accelerometer-market.html

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Advanced Marine Power Supply Market: https://www.transparencymarketresearch.com/advanced-marine-power-supply-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

From Local Speed to Global Reach: Why Indian Windows VPS Delivers More

As the demand for fast, secure, and reliable hosting grows, Indian businesses are turning toward Virtual Private Servers (VPS) for more control and flexibility. At CloudMinister Technologies, we understand that every second counts in the digital world — and our Indian Windows VPS hosting is engineered to deliver high performance, full customization, and unmatched reliability, right from Indian data centers.

Whether you're running enterprise applications, hosting a website, or managing remote desktops, CloudMinister's Windows VPS is the smart solution for modern businesses.

What is Windows VPS Hosting?

Windows VPS Hosting gives you a virtual server that mimics a dedicated physical server — but at a fraction of the cost. With the Windows operating system pre-installed, it’s ideal for running software and tools built for Microsoft platforms.

Each VPS is isolated, meaning you get:

Your own CPU, RAM, and disk space

Full administrative access

The freedom to install or remove applications as needed

This is a powerful alternative to shared hosting for businesses that need more speed, security, and flexibility.

Why Host Your VPS in India?

Hosting your server in India brings unique advantages, especially for businesses targeting local audiences:

Faster Access for Indian Users

When your server is located within India, your data reaches users faster. Whether it’s a website, app, or desktop service, you get low latency and quicker load times, resulting in improved user satisfaction.

Better Compliance with Local Laws

India is strengthening its data protection policies. Hosting within the country helps you comply with:

Sector-specific regulations (finance, health, government)

National data storage laws This reduces legal risks and enhances customer trust.

Enhanced SEO Performance

If you're targeting the Indian market, having a server with an Indian IP can boost your website ranking in local search results. Search engines often prioritize local servers for local searches.

Reliable Network Infrastructure

Indian data centers are now equipped with redundant power, cooling, and connectivity, offering uptime and stability that meet international standards.

Why Choose CloudMinister for Windows VPS in India?

CloudMinister Technologies has earned a strong reputation for delivering dependable, cost-effective, and future-ready VPS solutions. Here’s what makes our Indian Windows VPS offering stand out:

Enterprise-Class Hardware

Our infrastructure is powered by:

SSD/NVMe drives for lightning-fast data access

High-performance Intel/AMD CPUs

Secure Tier-III Indian data centers This ensures high availability, fast processing, and robust performance even during peak traffic.

Fully Licensed Windows Environment

We provide fully licensed versions of:

Windows Server 2016

Windows Server 2019

Windows Server 2022 No more compatibility headaches — you can run ASP.NET applications, MS SQL databases, and legacy Windows apps effortlessly.

Rapid Deployment

Your VPS is set up within minutes after signup. You’ll get:

Remote Desktop access

Full admin control

Quick configuration options via our user-friendly dashboard

This means you can start deploying your projects or applications without delay.

Scalable to Your Needs

Whether you're starting with a basic VPS or need multiple cores and high memory, CloudMinister offers plans that grow with your business. Scaling is seamless and can be done without downtime.

Managed and Unmanaged Options

Prefer to manage the server yourself? Go for our unmanaged VPS. Want us to take care of server updates, patching, and monitoring? Choose our managed VPS hosting — ideal for businesses without in-house IT.

24/7 Technical Assistance

Our experienced technical team is available round-the-clock to assist with:

OS installation

Troubleshooting

Security setup

Performance tuning We believe support should be proactive, not reactive.

Use Cases for Indian Windows VPS

CloudMinister’s Windows VPS is suitable for a wide range of applications:

Software Development: Host and test .NET, ASP.NET, and Windows-based projects

Database Hosting: Run secure, scalable Microsoft SQL Server databases

Forex Trading: Install MetaTrader and execute trades with low latency

Remote Desktop Services: Offer secure desktops for employees working remotely

Web Hosting: Deploy and manage business websites with high traffic

ERP & CRM Hosting: Run tools like Tally, Busy, or Microsoft Dynamics in a virtualized environment

Performance, Control, and Peace of Mind – All in One VPS

At CloudMinister Technologies, we believe in giving you more than just a server. We deliver:

Control through full admin access and configuration freedom

Performance with modern hardware and local Indian hosting

Reliability backed by 99.9% uptime and expert support

We help businesses transition from traditional hosting to VPS with ease, allowing them to scale and succeed in a competitive digital world.

Get Started with CloudMinister Today

Whether you’re a developer, a startup, or an established enterprise, CloudMinister’s Indian Windows VPS offers the power, performance, and support your business needs.

Visit www.cloudminister.com

Contact Us: [email protected]

Choose CloudMinister Technologies – because your business deserves a hosting partner, not just a provider.

0 notes

Text

Patient Management Software and Services Market Size, Share, Trends, Key Drivers, Demand and Opportunities

Patient Management Software and Services Market - Size, Share, Demand, Industry Trends and Opportunities

Global Patient Management Software and Services Market, By Component (Hardware, Software, Services), Delivery Mode (On–Premise Solutions, Cloud-Based Solutions, Web based), Size (Large Enterprises, Small and Medium-sized Enterprises), End User (Providers, Payers, Individual Users, and Others), Application (Health Management, Home Health Management, Social and Behavioural Management, Financial Health Management), Therapeutic Area (Chronic Diseases, Women’s Health, Fitness, Others), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, France, Italy, U.K., Belgium, Spain, Russia, Turkey, Netherlands, Switzerland, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, U.A.E, Saudi Arabia, Egypt, South Africa, Israel, Rest of Middle East and Africa) - Industry Trends

Patient management software and services market is expected to gain market growth in the forecast period of 2022 to 2029. Data Bridge Market Research analyses the market to grow at a CAGR of 8.6% in the above-mentioned forecast period.

Access Full 350 Pages PDF Report @

**Global Patient Management Software and Services Market Analysis**

The global patient management software and services market is a crucial sector within the healthcare industry. Patient management software helps healthcare providers streamline their operations, improve patient care, and enhance overall efficiency. The market has been witnessing significant growth in recent years, driven by factors such as the increasing adoption of electronic health records (EHRs), the growing demand for integrated healthcare solutions, and the rising focus on improving patient outcomes. According to recent data, the market was valued at nan in nan and is expected to reach nan by nan, growing at a CAGR of nan% during the forecast period.

**Segments**

The global patient management software and services market can be segmented based on the type of software, mode of delivery, end-user, and region. By type of software, the market can be divided into integrated software and standalone software. Integrated software solutions offer comprehensive patient management features, including EHR, practice management, and billing functionalities, while standalone software focuses on specific aspects of patient management. In terms of the mode of delivery, the market includes on-premise solutions and cloud-based solutions. Cloud-based solutions are gaining traction due to their scalability, cost-effectiveness, and ease of implementation. End-users of patient management software and services include hospitals, clinics, ambulatory care centers, and others.

**Market Players**

- Cerner Corporation - McKesson Corporation - Allscripts Healthcare, LLC - Athenahealth - Epic Systems Corporation - MEDITECH - NextGen Healthcare - eClinicalWorks - Greenway Health - Practice Fusion

The global patient management software and services market is highly competitive, with key players focusing on product innovation, strategic partnerships, and mergers and acquisitions to gain a competitive edge in the market. These market players offer a wide range of solutions tailored to meet the diverse needs of healthcare providers worldwide.

Market trends in the patient management software and services market include the increasing adoption of telemedicine and remote patient monitoring solutions, the integration of artificial intelligence and machine learning technologies to enhance patient care, and the rising demand for interoperable healthcare systems. Growth drivers for the market include government initiatives to promote the adoption of digital healthcare solutions, the need to reduce healthcare costs and improve operational efficiency, and the growing prevalence of chronic diseases driving the demand for advanced patient management solutions.

Challenges facing the global patient management software and services market include data security and privacy concerns, interoperability issues between different healthcare systems, and the complexity of integrating multiple software solutions within healthcare organizations. However, with ongoing technological advancements and increasing awareness about the benefits of patient management software, the market is poised for continued growth in the coming years.

For more detailed insights and market analysis, refer to https://www.databridgemarketresearch.com/reports/global-patient-management-software-and-services-market

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Global Patient Management Software and Services Market Landscape

Part 04: Global Patient Management Software and Services Market Sizing

Part 05: Global Patient Management Software and Services Market Segmentation by Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

Patient Management Software and Services Key Benefits over Global Competitors:

The report provides a qualitative and quantitative analysis of the Patient Management Software and Services Market trends, forecasts, and market size to determine new opportunities.

Porter’s Five Forces analysis highlights the potency of buyers and suppliers to enable stakeholders to make strategic business decisions and determine the level of competition in the industry.

Top impacting factors & major investment pockets are highlighted in the research.

The major countries in each region are analyzed and their revenue contribution is mentioned.

The market player positioning segment provides an understanding of the current position of the market players active in the Personal Care Ingredients

Browse Trending Reports:

Fox–Fordyce Disease Treatment Market Ultraviolet Currency Detector Market Agricultural Grow Bags Market Sialidosis Market Tantalum Carbide Coating for Graphite Market Foggy Guard Coating (FGC) Market Wood Packaging Materials Market Cathodic Protection Market Fuel Cards Market Hyaluronic Acid Based Dermal Fillers Market Woven Sacks Market Telehealth Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

North America In-Vitro Diagnostics Market Size, Share Insights 2025-2031

The North America in-vitro diagnostics market is expected to grow from US$ 21,207.07 million in 2022 to US$ 33,183.41 million by 2030. It is estimated to grow at a CAGR of 5.8% from 2022 to 2030.

North America In-Vitro Diagnostics Market Overview

North America region includes the US, Canada, and Mexico. It holds the largest share of the in-vitro diagnostics market by geography. All three countries in the region are witnessing considerable demand for in-vitro diagnostics. Certain factors, such as the increasing prevalence of chronic & infectious diseases, focus on efficient disease diagnosis, and a higher need for advanced healthcare systems are boosting the adoption of in-vitro diagnostics in the region. The US held the largest share of the North America in-vitro diagnostics market. Chronic diseases such as cancer and cardiovascular diseases are the major causes of disability and death in the US. Per the National Center for Chronic Disease Prevention and Health Promotion, 6 in 10 people in the country have at least one chronic disease.

Grab PDF To Know More @ https://www.businessmarketinsights.com/sample/TIPRE00022125

North America In-Vitro Diagnostics Market Revenue and Forecast to 2030 (US$ Million)

North America In-Vitro Diagnostics Market Segmentation

The North America in-vitro diagnostics market is segmented into product & services, technology, application, end user, and country.

Based on product & services, the North America in-vitro diagnostics market is segmented into reagents & kits, instruments, and software & services. The reagents & kits segment held the largest share of the North America in-vitro diagnostics market in 2022.

Based on technology, the North America in-vitro diagnostics market is segmented into immunoassay/ immunochemistry, clinical chemistry, molecular diagnostics, microbiology, blood glucose self-monitoring, coagulation & hemostasis, hematology, urinalysis, and others. The immunoassay/ immunochemistry segment held the largest share of the North America in-vitro diagnostics market in 2022.

Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

The List of Companies - North America In-Vitro Diagnostics Market

Abbott Laboratories

Becton Dickinson and Co

bioMerieux SA

Bio-Rad Laboratories Inc

Danaher Corp

F. Hoffmann-La Roche Ltd

Qiagen NV

Siemens AG

Sysmex Corp

Thermo Fisher Scientific Inc

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defence; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

0 notes

Text

Europe Microgrid Market Size, Share, Trends, Demand, Future Growth, Challenges and Competitive Analysis

"Europe Microgrid Market - Size, Share, Demand, Industry Trends and Opportunities

Europe Microgrid Market, By Connectivity (Off-Grid/Island/Remote, Grid Connected), Offering (Hardware, Software, Services), Pattern (Urban, Semi-Urban, Remote Island), Source (Diesel Generators, CHP, Solar Pv, Natural Gas, Others), Storage (Lithium-Ion, Lead Acid, Solar Batteries, Flywheel, Others), Grid Type (AC Microgrid, DC Microgrid, Hybrid Microgrid), Capacity (Less Than 5,000 MW, 5,001 – 10,000 MW, 10,001 – 15,000 MW, More Than 15,000 MW), Control (Primary (Local Control), Secondary, Tertiary (Optimization) Control), Application (Remote Location, Utility, Industrial, Campus, Military, Smart City, Data Center, Hospital, School, Others) - Industry Trends.

Get the PDF Sample Copy (Including FULL TOC, Graphs and Tables) of this report @

**Market Analysis of Europe Microgrid Market**

The Europe microgrid market is a dynamic and rapidly growing sector driven by factors such as increasing demand for reliable and secure power supply, rising focus on renewable energy integration, and the need for grid resilience against natural disasters. The market is expected to witness significant growth in the coming years, with countries across Europe adopting policies to promote clean energy and reduce carbon emissions. According to the latest data, the Europe microgrid market size was valued at nan in nan and is projected to grow at a CAGR of nan% during the forecast period.

**Segments**

The Europe microgrid market can be segmented based on components, grid type, end-user, and geography. In terms of components, the market can be divided into hardware, software, and services. Hardware components include generation units, energy storage systems, and control systems. Software components consist of energy management systems and control software. Services encompass engineering, procurement, and construction (EPC) services, operations and maintenance (O&M) services, and consulting services. Based on grid type, the market can be categorized into grid-connected microgrids and off-grid microgrids. End-users of microgrids include commercial and industrial sectors, utilities, and residential users.

**Market Players**

- Siemens AG - ABB - General Electric - Schneider Electric - Eaton - Honeywell International Inc. - Lockheed Martin Corporation - Power Analytics Corporation - S&C Electric Company - Toshiba Corporation

The Europe microgrid market is characterized by intense competition and the presence of key players who are actively involved in product development, partnerships, and strategic alliances to gain a competitive edge. These market players are focusing on enhancing their product portfolios, expanding their geographic presence, and investing in research and development to cater to the evolving needs of customers in the region. With technological advancements and the growing emphasis on sustainability, market players are also exploring opportunities in hybrid microgrid systems that combine multiple sources of energy for enhanced efficiency and reliability.

Market trends in the Europe microgrid market include the increasing deployment of smart grid technologies, the integration of Internet of Things (IoT) solutions for real-time monitoring and control, and the adoption of blockchain technology for secure and transparent transactions within microgrids. Furthermore, the rising investments in renewable energy projects, government initiatives to promote energy independence, and the emergence of microgrid-as-a-service (MaaS) models are driving the growth of the market.

Despite the positive outlook, the Europe microgrid market faces challenges such as high initial investment costs, regulatory constraints, and interoperability issues between different grid technologies. Market players need to address these challenges by developing cost-effective solutions, collaborating with regulatory bodies for policy support, and standardizing communication protocols to ensure seamless integration of microgrids into the existing grid infrastructure.

In conclusion, the Europe microgrid market presents lucrative opportunities for market players to capitalize on the growing demand for decentralized and sustainable energy solutions. With the increasing focus on energy security, grid reliability, and environmental sustainability, the market is poised for substantial growth in the coming years.

Access Full 350 Pages PDF Report @

Table of Content:

Section 01: Executive Summary

Section 02: Scope of The Report

Section 03: Research Methodology

Section 04: Introduction

Section 05: Market Landscape

Section 06: Market Sizing

Section 07: Five Forces Analysis

Section 08: Market by Product

Section 09: Market by Application

Section 10: Customer Landscape

Section 11: Market by End-User

Section 12: Regional Landscape

Section 13: Decision Framework

Section 14: Drivers and Challenges

Section 15: Market Trends

Section 16: Competitive Landscape

Section 17: Company Profiles

Section 18: Appendix

Critical Insights Related to the Europe Microgrid Market Included in the Report:

Exclusive graphics and Illustrative Porter’s Five Forces analysis of some of the leading companies in this market

Value chain analysis of prominent players in the market

Current trends influencing the dynamics of this market across various geographies

Recent mergers, acquisitions, collaborations, and partnerships

Revenue growth of this industry over the forecast period

Marketing strategy study and growth trends

Growth-driven factor analysis

Emerging recess segments and region-wise market

An empirical evaluation of the curve of this market

Ancient, Present, and Probable scope of the market from both prospect value and volume

Reasons to Buy:

Review the scope of the Europe Microgrid Market with recent trends and SWOT analysis.

Outline of market dynamics coupled with market growth effects in coming years.

Europe Microgrid Market segmentation analysis includes qualitative and quantitative research, including the impact of economic and non-economic aspects.

Europe Microgrid Market and supply forces that are affecting the growth of the market.

Market value data (millions of US dollars) and volume (millions of units) for each segment and sub-segment.

and strategies adopted by the players in the last five years.

Browse Trending Reports:

Middle East And Africa Indium Market North America Indium Market Europe Plant Based Milk Market Middle East And Africa Plant Based Milk Market Asia Pacific Plant Based Milk Market North America Plant Based Milk Market Australia And New Zealand Healthcare Logistics Market Europe Laminated Busbar Market Asia Pacific Laminated Busbar Market Middle East And Africa Laminated Busbar Market North America Laminated Busbar Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

Connected Care, Healthier Futures: Europe’s Digital Health Landscape

The Europe digital health market size is anticipated to reach USD 267.2 billion by 2030 and is projected to grow at a CAGR of 22.3% from 2024 to 2030, according to a new report by Grand View Research, Inc. Increasing aging population, rise in prevalence of chronic disorders in Europe, and growing demand for remote patient monitoring are among the major factors driving the market growth in this region. For instance , as per the Eurostat statistics, on 1 January 2023, the estimated population of the European Union was 448.8 million people, with 21.3% of the population being aged 65 years and over. In addition, improved IT infrastructure, growing digitalization of healthcare, and rising medical expenses are also anticipated to accelerate the market growth over the forecast period. Moreover, the shortage of healthcare professionals and overburdened healthcare facilities are also expected to increase the adoption of digital health platforms.

Growing internet and smartphone penetration in Europe and increasing adoption of mHealth platforms by medical professionals for better patient engagement is expected to boost market growth. In addition, the rise in government initiatives for the promotion and development of eHealth services also supports market growth.In 2019 , France implemented a new healthcare act based on the 'My Health 2022' plan, which aims to enhance the country's eHealth focus. The plan includes improving interoperability, implementing electronic health records (EHR) nationwide, utilizing AI in healthcare, creating a data hub for healthcare data sets, and investing in telemedicine introduced by the public health system.

In addition, the growing preference for healthcare platform upgrade services for better patient engagements in remote locations is driving the service segment growth. Moreover, training, staffing, maintenance, and resource allocation for pre- and post-installation of digital platforms to provide better remote healthcare services also support the market growth. Furthermore, growing market player’s initiatives to gain a competitive edge is driving the market growth. In April 2022, Amazon Web Services (AWS) in collaboration with University College London (UCL) established a digital innovation center at the IDEALondon technology hub. The center aims to help healthcare and education organizations expedite digital innovation and tackle worldwide challenges in their respective domains.

In addition, increasing prevalence of chronic diseases such as diabetes, cardiovascular, and respiratory diseases, among others are accelerating market growth. For instance , according to the European Society of Cardiology, cardiovascular disease (CVD) is responsible for causing 3.9 million deaths in Europe and over 1.8 million deaths in the European Union every year.

The major players operating in the market are adopting strategies such as collaborations, supply agreements, and partnerships with a major focus on enhancing the product formation and reach. For instance, in October 2021, Vodafone Group patterned with Deloitte to launch Vodafone Center for Health, a virtual care center, utilizing its connected health solutions and Deloitte’s healthcare consulting expertise to enhance healthcare accessibility across Europe. In August 2021, Lemonaid Health, an online healthcare company based in San Francisco, expanded its services internationally. The company has partnered with Boots UK to launch its services in the UK.

Europe Digital Health Market Report Highlights

Based on technology, the tele-healthcare segment held the market with the largest revenue share of 43.2% in 2023, owing to the increasing aging population and growing demand for remote patient monitoring

Based on component, the software segment is anticipated to grow at the fastest CAGR over the forecast period, owing to the rising need for efficient management of organizational workflows in healthcare organizations

Based on application, the diabetes segment held the market with the largest revenue share of 24.3% in 2023, owing to the rising cases of diabetes among the population

Based on end-use, the patients segment led the market with the largest revenue share of 34.1% in 2023, due to the growing preference for telehealth services among the population

Curious about the Europe Digital Health Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Europe Digital Health Segmentation

Grand View Research has segmented the Europe digital health market based on technology, component, application, end-use, and country:

Europe Digital Health Technology Outlook (Revenue, USD Million, 2018 - 2030)

Tele-healthcare

Tele-care

Activity Monitoring

Remote Medication Management

Tele-health

LTC Monitoring

Video Consultation

mHealth

Wearables & Connected Medical Devices

Vital Sign Monitoring Devices

Heart Rate Monitors

Activity Monitors

Electrocardiographs

Pulse Oximeters

Spirometers

Blood Pressure Monitors

Others

Sleep Monitoring Devices

Sleep Trackers

Wrist Actigraphs

Polysomnographs

Others

Electrocardiographs Fetal And Obstetric Devices

Neuromonitoring Devices

Electroencephalographs

Electromyographs

Others

mHealth Apps

Medical Apps

Women's Health

Menstrual Health

Pregnancy Tracking & Postpartum Care

Menopause

Disease Management

Others

Chronic Disease Management Apps

Diabetes Management Apps

Blood Pressure and ECG Monitoring Apps

Mental Health Management Apps

Cancer Management Apps

Obesity Management Apps

Other Chronic Disease Management Apps

Personal Health Record Apps

Medication Management Apps

Diagnostic Apps

Remote Monitoring Apps

Others (Pill Reminder, Medical Reference, Professional Networking, Healthcare Education)

Fitness Apps

Exercise & Fitness

Diet & Nutrition

Lifestyle & Stress

Services

mHealth Service, By Type

Monitoring Services

Independent Aging Solutions

Chronic Disease Management & Post-Acute Care Services

Diagnosis Services

Healthcare Systems Strengthening Services

Others

Digital Health Systems

EHR

E-prescribing Systems

Healthcare Analytics

Europe Digital Health Component Outlook (Revenue, USD Million, 2018 - 2030)

Software

Hardware

Services

Europe Digital Health Application Outlook (Revenue, USD Million, 2018 - 2030)

Obesity

Diabetes

Cardiovascular

Respiratory Diseases

Neurology

Others

Europe Digital Health End-use Outlook (Revenue, USD Million, 2018 - 2030)

Patients

Providers

Payers

Others

Europe Digital Health Country Outlook (Revenue, USD Million, 2018 - 2030)

UK

Germany

France

Italy

Spain

Denmark

Sweden

Norway

Key Players in the Europe Digital Health Market

Cerner Corporation

Veradigm LLC

Apple Inc

Telefonica S.A.

McKesson Corporation

Epic Systems Corporation

QSI Management, LLC

AT&T

Vodafone Group

Airstrip Technologies

Google, Inc

Samsung Electronics Co. Ltd

HiMS

Orange

Qualcomm Technologies, Inc

Softserve

Computer Programs and Systems, Inc

IBM Corporation

CISCO Systems, Inc

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Video Surveillance Market to Observe Strong Development by 2032

Allied Market Research, titled, “Video Surveillance Market by Component, Enterprise Size, System Type, Customer Type, and Application". The video surveillance market was valued at $61.8 billion in 2022 and is estimated to reach $204.5 billion by 2032, growing at a CAGR of 12.8% from 2023 to 2032.

A video surveillance system is a sophisticated and interconnected network of technological elements designed to observe, capture, and assess visual information within a specific setting. Consisting of surveillance cameras, devices for video recording and storage, and software for management, these systems serve diverse purposes, including security, safety, and operational optimization. Video surveillance systems provide real-time monitoring of the environment and people. This surveillance system is used to promote safety and security among the users. Next-generation video surveillance cameras are one of the most promising security solutions that have the capability of offering real-time surveillance and are superior compared to traditional surveillance systems. Video surveillance system helps end users to maintain flexible security solutions in the respective environment. These systems often feature advanced attributes such as motion detection, night vision, and pan-tilt-zoom capabilities to enhance monitoring capabilities. Through the integration of artificial intelligence and video analytics, these systems enable intelligent processing of visual data, facilitating functions such as facial recognition, object tracking, and behavior analysis. Video surveillance systems are widely employed in public areas, commercial establishments, critical infrastructure, and residential spaces, serving as a proactive tool for deterrence, incident response, and data-driven decision-making.

Video surveillance is witnessing wide acceptance and is expected to experience growth in the security service market in the future. Currently, this technology is in its growing stage; however, it is expected to gain a major position in the market owing to technological developments. Based on features offered by the video surveillance system, it is increasingly becoming popular among end users such as small and medium-scale enterprises. Advancements in technology are anticipated to help video surveillance cameras and accessories manufacturing companies reduce the overall cost of production of the system. The global video surveillance market is predicted to exhibit notable growth during the forecast period owing to the increased demand for enhanced security products. This is the major factor driving the growth of the global video surveillance market.

The versatile application of video surveillance systems is evident across numerous sectors, contributing significantly to heightened security, safety, and operational efficiency. In the security domain, these systems are widely utilized in public spaces, transportation centers, and commercial establishments to discourage potential threats, observe activities, and streamline responses to incidents using a security camera system. Retail environments leverage video surveillance for real-time monitoring and evidence collection to prevent losses. Critical infrastructure, including airports and power plants, relies on these systems to control access and ensure the uninterrupted operation of essential services.

However, the considerable obstacle to the growth of the video surveillance system market is the substantial investment cost associated with its implementation. Acquiring and installing advanced surveillance cameras, storage infrastructure, and analytics software entails significant initial expenses. Moreover, the requirement for skilled professionals for system integration and ongoing maintenance adds to the overall financial burden. This poses a challenge, particularly for small- and medium-sized enterprises, limiting their ability to embrace comprehensive video surveillance solutions. The continuous evolution of technology further demands regular upgrades, contributing to long-term financial commitments.

The global video surveillance market is segmented into system type, component, application, enterprise type, customer type, and region. By system type, the market is analyzed across analog surveillance, IP surveillance, and hybrid surveillance. By component, it is divided into hardware, software, and services. The hardware segment is further segmented into camera, monitor, storage, and accessories. In addition, the software segment is bifurcated into video analytics and video management software. Depending on application, the market is divided into commercial, military and defense, infrastructure, residential, and others. Based on enterprise type, the market is analyzed across small-scale enterprises, medium-scale enterprises, and large-scale enterprises. By customer type, it is divided into B2B and B2C. Region-wise, it is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

KEY FINDINGS OF THE STUDY

The video surveillance market size is expected to grow significantly in the coming years, driven by the integration of IoT in CCTV surveillance cameras.

The market is expected to be driven by the demand for video surveillance market share in the commercial segment for CCTV camera systems.

The market is highly competitive, with several major players competing for market share. The competition is expected to intensify in the coming years as new players enter the market.

The Asia-Pacific region is expected to be a major market for the video surveillance market growth owing to an increase in the adoption of advanced technologies in the region for security camera systems.

Competitive analysis and profiles of the major market players, in video surveillance industry such as Teledyne FLIR LLC, Verkada Inc., Eagle Eye Networks, Inc., Zhejiang Dahua Technology Co., Ltd, Canon Inc., BCD International, Inc., Panasonic Corporation, Infinova Corporation, HONEYWELL Commercial Security (HONEYWELL INTERNATIONAL INC.), and Motorola Solutions, Inc. are provided in this report. Product launch and acquisition business strategies were adopted by the major market players in 2022.

0 notes

Text

Artificial Intelligence in Drug Discovery Market 2025: Key Trends, Growth Drivers, and Industry Insights

Market Overview

AI in Drug Discovery: Pharmaceutical companies face numerous challenges during drug development, including extended timelines, high R&D investments, and stringent regulatory requirements. The increasing demand for advanced therapies has introduced new complexities such as large-scale data collection and analysis, a need for skilled professionals, and ensuring data security. Artificial Intelligence (AI), which mimics human intelligence processes, has become increasingly valuable in the pharmaceutical sector. AI applications span from research and development (R&D) and drug discovery to diagnostics, disease prevention, remote monitoring, and epidemic prediction. The integration of AI in drug discovery has led to improved success rates, faster delivery processes, and access to new biological insights.

The market for AI in drug discovery is growing due to the rising need to reduce drug discovery turnaround times, expanding applications of AI, the increasing prevalence of chronic diseases, and the high threat of emerging infectious diseases. Additionally, the adoption of machine learning (ML), the emergence of regional start-ups, and increased investments in R&D present growth opportunities for the market.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=5429

Chronic Diseases Drive AI Adoption in Drug Discovery

The prevalence of chronic diseases such as chronic obstructive pulmonary disease (COPD), diabetes, coronary artery disease, hepatitis, arthritis, and cancer continues to rise. According to the Centers for Disease Control and Prevention (CDC) data published in December 2022, six out of ten adults in the U.S. suffer from a chronic disease. Similarly, the European Commission reported in 2021 that over 35.2% of individuals in the European Union had chronic diseases.

The International Diabetes Federation reported that 502 million people worldwide had diabetes in 2020, with an estimated 23.4 million new cancer cases expected annually by 2032. Lung cancer remains the leading cause of cancer mortality in Asia-Pacific, underscoring the need for advanced therapies. The increasing burden of chronic diseases has amplified the demand for advanced therapies, boosting AI applications in drug discovery to accelerate the development of effective treatments.

Investment Surge in AI for Drug Discovery

The growing role of AI in drug discovery is reflected in increased investments and collaborations between pharmaceutical companies and AI firms. According to Stanford University’s Institute for Human-Centered Artificial Intelligence (HAI) 2020 report, investments in AI for drug discovery reached USD 13.8 billion. The trend continued in 2021 when Exscientia (U.K.), a clinical-stage pharma tech company, raised USD 225 million in a Series D funding round to enhance its proprietary pipeline and AI-driven drug discovery capabilities.

These investments enable pharmaceutical companies to leverage AI technologies to streamline drug discovery processes, reduce costs, and improve clinical outcomes. Partnerships between AI and pharmaceutical companies are also helping to integrate AI into drug research and development workflows more effectively.

Market Segmentation by Offering

In 2025, the software segment is expected to account for the largest share of the AI in drug discovery market. Software solutions are increasingly used in drug discovery for faster, more efficient, and cost-effective drug development processes. Pharmaceutical companies are particularly interested in AI-driven software due to its ability to enhance clinical trials and expedite novel therapy development.

Deployment Mode: Cloud-based Models on the Rise

The cloud-based deployment segment is projected to grow at the highest compound annual growth rate (CAGR) during the forecast period. Cloud-based models offer enhanced security, flexibility, and data storage capabilities. They also provide quick accessibility and cost-efficiency, which are critical for pharmaceutical companies managing vast amounts of data during drug discovery and clinical trials.

Applications: Lead Compound Identification Dominates

In 2025, the lead compound identification segment is expected to dominate the AI in drug discovery market. Lead compound identification is a critical phase in the drug discovery process, guiding which compounds advance to lead optimization and, eventually, clinical candidate development. AI technology accelerates this process by enabling the rapid screening of large chemical libraries, reducing both the time and costs associated with drug development.

Therapeutic Area: Focus on Oncology

Oncology is projected to hold the largest market share in the AI drug discovery market by 2025. Cancer remains a significant global health challenge, with pharmaceutical companies prioritizing oncology for drug discovery initiatives. The high incidence of cancer, along with substantial funding for oncology research, supports the adoption of AI in developing targeted cancer therapies. Additionally, numerous collaborations between pharmaceutical and AI companies in oncology drug development further enhance this segment's market share.

End User: Pharmaceutical & Biotechnological Companies Leading the Way

Pharmaceutical and biopharmaceutical companies are increasingly adopting AI to identify new drug candidates. These companies focus on minimizing operational costs and accelerating the introduction of innovative treatments to the market. The growing burden of chronic and infectious diseases puts pressure on pharmaceutical firms to develop new drugs quickly. By integrating AI into drug research, these companies can enhance drug discovery processes, reducing the time and costs required to bring new treatments to patients.

Get Full Report @ https://www.meticulousresearch.com/product/artificial-intelligence-in-drug-discovery-market-5429

Regional Insights: Asia-Pacific Leads Market Growth

Asia-Pacific is expected to be the fastest-growing regional market for AI in drug discovery. Factors such as developing AI and pharmaceutical research infrastructure in China, India, Singapore, and South Korea, increased funding for cancer research, and rising investments in AI contribute to this growth. Additionally, a surge in AI-based drug discovery startups in the region is further boosting market expansion.

Key Market Players

The competitive landscape of the AI in drug discovery market includes several prominent players:

Microsoft Corporation (U.S.)

Exscientia plc (U.K.)

NVIDIA Corporation (U.S.)

Schrödinger, LLC (U.S.)

Atomwise, Inc. (U.S.)

BenevolentAI Limited (U.K.)

Deep Genomics Incorporated (Canada)

InSilico Medicine (U.S.)

Cloud Pharmaceuticals, Inc. (U.S.)

Standigm Inc. (South Korea)

These companies are focused on developing advanced AI technologies and solutions for drug discovery, engaging in partnerships, and securing investments to enhance their market presence.

Scope of the AI in Drug Discovery Market

By Offering:

Software

Services

By Deployment Mode:

On-premises

Cloud & Web-Based Mode

By Application:

Target Discovery & Validation

Lead Compound Identification

De Novo Design and Drug Optimization

Preclinical & Clinical Testing

By Therapeutic Area:

Oncology

Neurodegenerative Diseases

Cardiovascular Diseases

Metabolic Diseases

Other Therapeutic Areas (including infectious and rare diseases)

By End User:

Pharmaceutical & Biopharmaceutical Companies

Contract Research Organizations (CROs)

Academic & Research Institutes

By Geography:

North America: U.S., Canada

Europe: Germany, U.K., France, Italy, Spain, Rest of Europe

Asia-Pacific: China, Japan, India, Rest of APAC

Latin America: Brazil, Mexico, Rest of Latin America

Middle East & Africa

The adoption of AI in drug discovery is transforming the pharmaceutical industry, offering new possibilities for developing advanced therapies to address the growing burden of chronic and infectious diseases. With continuous advancements and investments in AI technologies, the market for AI in drug discovery is poised for significant growth in the coming years.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=5429

0 notes

Text

Price: [price_with_discount] (as of [price_update_date] - Details) [ad_1] SAMSUNG 990 PRO with Heatsink is designed for tech enthusiasts, hardcore gamers and heavy-workload professionals who want blazing fast speed. Compatible with PlayStation® 5, and integrated heatsink disperses heat to maintain speed, power, efficiency and thermal control, preventing downtime overheating on consoles and PCs. Experience sequential read/write speeds up to 7,450/6,900 MB/s.* *PCIe 4.0’s best theoretical sequential read is 8000 MB/s - 990 PRO reaches 7450 MB/s as of Q3, 2022. **Source: 2003-2022 OMDIA data: NAND suppliers' revenue market share. ***Sequential and random write performance was measured with Intelligent Turbo Write technology being activated. Intelligent Turbo Write operates only within a specific data transfer size. Performance may vary depending on SSD’s firmware, system hardware & configuration and other factors. For detailed information, please contact your local service center. 990 PRO reaches 7,450 MB/s based on test system configuration: AMD Ryzen 7 5800X 8-Core Processor [email protected], DDR4 3600MHz 16GBx2 (PC4-25600 Overclock), OS - Windows 10 Pro 64bit, Chipset - ASRock-X570 Taichi. To maximize the performance of the 990 PRO, please check whether your system supports PCIe 4.0 at the Intel or AMD website. ****PCI-SIG®D8 standard spec: 8.8mm. *****980 PRO Sequential Read/Write - 1,129/877 MB/Watt, 990 PRO Sequential Read/Write - 1380/1319 MB/Watt based on test result of 1TB capacity model. ADOBE MEMBERSHIP: Get a two-month membership of Adobe Creative Cloud Photography plan on us when you purchase and register an eligible 1TB or 2TB Samsung SSD* HUGE SPEED BOOST: Get random read/write speeds that are 40%/55% faster than 980 PRO; Experience up to 1400K/1550K IOPS, while sequential read/write speeds up to 7,450/6,900 MB/s reach near the max performance of PCIe 4.0* BREAKTHROUGH POWER EFFICIENCY: Use less power and get more performance; Enjoy up to 50% improved performance per watt over 980 PRO, plus optimal power efficiency with max PCIe 4.0 performance** SMART THERMAL CONTROL: Samsung's own nickel-coated controller delivers effective thermal control; With its slim size, 990 PRO with Heatsink is a perfect fit for PlayStation 5, desktops and laptops that meet the PCI-SIG D8 standard*** THE CHAMPION MAKER: Up to 65% improvement in random performance enables faster loads for an ultimate gaming experience on PS5 and DirectStorage PC games;**** With RGB LED lights, Heatsink’s futuristic design adds style to function.SAMSUNG MAGICIAN SOFTWARE: Get the most out of your SSD with Samsung Magician's advanced yet intuitive optimization tools; Monitor drive health, protect valuable data, and receive important updates for your 990 PRO. Allowable Voltage: 3.3 V ± 5 % Allowable voltage [ad_2]

0 notes

Text

Digital Marketing Software Industry Outlook: AI, Big Data, Cloud Technologies Impact Analysis

The global digital marketing software market size is expected to reach USD 264.15 billion by 2030, registering a CAGR of 19.4% from 2023 to 2030, according to a new study conducted by Grand View Research, Inc. A growing focus on expanding customer reach globally and the quick digitization of many corporate sectors are driving the growth of the digital marketing software market. As the Internet, smartphones, social networking sites, and online marketing software become more widespread, and businesses increasingly use digital marketing strategies to study consumer behavior. Additionally, COVID-19 has benefited the sales of digital marketing products. During the COVID-19 pandemic, companies opt for digital marketing software to promote and market their products to a wider audience.

Digital Marketing Software Market Report Highlights

The adoption of marketing automation software is anticipated to gain traction over the forecast period it is widely used by marketing departments to effectively market their products on multiple online channels, such as websites, email, and social media, and to automate repetitive tasks.