#Melexis sensors

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 27% of US Tumblr users had an annual household income of over $100,000.

Text

youtube

Melexis Redefines the Market with 3D Magnetic Position Sensors

https://www.futureelectronics.com/resources/featured-products/infineon-psoc-4100s-max-for-home-automation. Melexis expands its portfolio of 3D magnetic position sensing solutions with the introduction of the MLX9042x series. These sensors are intended for cost-conscious automotive customers who need to measure absolute position accurately and safely in harsh and noisy environments over an extended temperature range. https://youtu.be/MhrNCdwdnJY

#Melexis#3D Magnetic Position Sensors#Magnetic Position Sensors#Melexis 3D magnetic position sensor#Melexis magnetic position sensor#MLX9042#sensors#automotive#absolute position#Melexis MLX9042#Melexis sensors#Youtube

2 notes

·

View notes

Text

youtube

Melexis Redefines the Market with 3D Magnetic Position Sensors

https://www.futureelectronics.com/resources/featured-products/infineon-psoc-4100s-max-for-home-automation. Melexis expands its portfolio of 3D magnetic position sensing solutions with the introduction of the MLX9042x series. These sensors are intended for cost-conscious automotive customers who need to measure absolute position accurately and safely in harsh and noisy environments over an extended temperature range. https://youtu.be/MhrNCdwdnJY

#Melexis#3D Magnetic Position Sensors#Magnetic Position Sensors#Melexis 3D magnetic position sensor#Melexis magnetic position sensor#MLX9042#sensors#automotive#absolute position#Melexis MLX9042#Melexis sensors#Youtube

0 notes

Text

Sensors, Temperature Sensors, MLX90640ESF-BAA-000-TU, Melexis

MLX90640 32x24 Thermal Array sensor 3 Volt 120 Degree Total FOV

0 notes

Text

https://www.futureelectronics.com/p/semiconductors--analog--sensors--temperature/mlx90640esf-baa-000-tu-melexis-5097624

Coolant temperature sensors, Digital sensor, oven temperature sensors air

MLX90640 32x24 Thermal Array sensor 3 Volt 120 Degree Total FOV

#Melexis#MLX90640ESF-BAA-000-TU#Sensors#Temperature Sensors#coolant temperature sensors#Digital sensor#oven temperature sensors air#Remote#tire pressure sensor#Sensor module#Water pressure sensors#chip#indoor air quality monitors

1 note

·

View note

Text

Automotive Gesture Recognition Market Share, Size, Segmentation Analysis, Key segments and Forecast 2026

The global automotive gesture recognition market, valued at US$ 1.4 billion, is projected to grow significantly at a CAGR of 17.8% through 2026. By the end of 2026, the market is expected to reach US$ 2.7 billion in revenue.

Multimedia, infotainment, and navigation applications are anticipated to collectively represent over 60% of the global market share by 2026.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚���� 𝐚 𝐒𝐚𝐦𝐩𝐥𝐞 𝐂𝐨𝐩𝐲 𝐨𝐟 𝐓𝐡𝐢𝐬 𝐑𝐞𝐩𝐨𝐫𝐭: https://www.factmr.com/connectus/sample?flag=S&rep_id=20

Key Players:

Cognitec Systems GmbH

Harman International Industries

Eyesight Technologies

Visteon Corp.

NXP Semiconductors

Synaptics Incorporated

Continental AG

Delphi Automotive PLC

Renesas

Gestigon GmbH

Melexis

Softkinetic

Neonode Inc.

Qualcomm Inc.

Navtek Solutions

Country-wise Insights

Germany is expected to be a pivotal market for automotive gesture recognition in Europe, driven by the presence of leading luxury car brands like BMW, Mercedes, and Audi. As customer preferences shift towards enhanced human-technology interaction, German automakers are increasingly incorporating advanced gesture recognition systems into luxury vehicles.

Rising investments in autonomous vehicle development within the country are anticipated to further boost demand for automotive gesture recognition technologies in the coming years. The adoption of advanced automotive technologies is likely to continue fueling the growth of the automotive gesture recognition market in Germany through 2026.

Category-wise Insights

The global automotive gesture recognition market is segmented into touch-based and touchless systems based on component type.

Touch-based systems require users to physically interact with a screen, which can divert a driver's attention from the road, potentially leading to accidents. To mitigate these risks, touchless systems are being increasingly adopted. These systems offer enhanced safety by minimizing the need for physical interaction, allowing drivers to operate functions through body movements and gestures.

Touchless systems utilize motion-sensing technology to detect specific gestures, providing a more intuitive and safer user experience. Due to these advantages, touchless systems are expected to dominate the market throughout the forecast period.

Competitive Landscape

Leading companies in the automotive gesture recognition market are enhancing their sales potential through the development of innovative products. To strengthen their global market presence, these providers are also pursuing strategic acquisitions and mergers.

In August 2022, Renesas Electronics Corporation, a prominent player in the semiconductor sector, announced its acquisition of Steradian Semiconductors Private Limited, a Bengaluru-based start-up specializing in radar technology. This acquisition is expected to enhance Renesas’s capabilities in human-machine interface (HMI) systems, including gesture recognition.

Additionally, in August 2022, STMicroelectronics, a major semiconductor manufacturer, introduced its new FlightSense Time-of-Flight (ToF) multi-zone sensors. These sensors use ToF technology to map and gather data without requiring a camera, making them suitable for applications such as gesture recognition, user detection, and intruder alert systems.

Automotive Gesture Recognition Industry Research Segments

By Component Type:

Touch-based Systems

Touchless Systems

By Authentication Type:

Hand

Fingerprint

Leg

Face

Vision

Iris

By Application:

Multimedia

Infotainment

Navigation

Lighting

Others

By Region:

North America

Latin America

Europe

APAC

MEA

𝐂𝐨𝐧𝐭𝐚𝐜𝐭:

US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

Motion Capture Sensors Market : Regulatory Developments and Compliance Outlook 2025–2032

Motion Capture Sensors Market, Global Outlook and Forecast 2025-2032

The global Motion Capture Sensors Market was valued at US$ 1.73 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 9.12% during the forecast period 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=88024

MARKET INSIGHTS

The global Motion Capture Sensors Market was valued at US$ 1.73 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 9.12% during the forecast period 2025-2032.

Motion Capture Sensors are specialized devices used to record and analyze human or object movements in three-dimensional space. These sensors include inertial measurement units (IMUs), optical markers, depth cameras, and mechanical exoskeletons, which track position, orientation, and acceleration data. The technology enables precise motion tracking for applications ranging from animation and gaming to sports science and medical rehabilitation.

The market growth is driven by increasing demand in entertainment industries for realistic CGI animation and virtual production, which accounts for over 35% of current applications. Furthermore, advancements in sensor miniaturization and AI-powered motion analysis algorithms are creating new opportunities in healthcare and industrial training simulations. Key players like Microsoft Corporation and Rokoko are expanding their product portfolios with wireless sensor solutions, while emerging markets in Asia-Pacific show accelerated adoption rates above the global average.

List of Key Motion Capture Sensor Companies Profiled

Inertia (U.S.) – Leader in inertial motion capture systems

Rokoko (Denmark) – Innovator in affordable mocap solutions

Technaid (Spain) – Specializes in biomechanical applications

Honeywell (U.S.) – Industrial motion sensing leader

ASUSTeK Computer (Taiwan) – Consumer motion tracking solutions

Cognex Corporation (U.S.) – Machine vision specialists

LMI Technologies (Canada) – 3D scanning innovators

Melexis (Belgium) – MEMS sensor specialists

Microchip Technology (U.S.) – Expanding mocap portfolio

Microsoft Corporation (U.S.) – Kinect platform developer

Regional differences create varied competitive dynamics. While North America remains the innovation hub with numerous startups, Chinese players like Navgnss and Norinco Group are rapidly gaining share through cost-effective solutions tailored for Asian markets.

The market’s projected 12.4% CAGR through 2031 will likely intensify competition further. Companies are already shifting strategies – some focusing on vertical-specific solutions while others pursue horizontal platform approaches. The coming years will test players’ abilities to balance precision, affordability, and scalability as motion capture becomes mainstream across industries.

Segment Analysis:

By Type

Inertial Sensors Segment Leads Due to High Demand in Consumer Electronics and Gaming Applications

The market is segmented based on type into:

Inertial sensors

Subtypes: Accelerometers, gyroscopes, and magnetometers

Measurement sensors

Subtypes: Optical sensors, force sensors, and others

Other sensors

Subtypes: Acoustic, pressure, and environmental sensors

By Application

Entertainment Segment Dominates Owing to Growing Animation and Virtual Production Needs

The market is segmented based on application into:

Entertainment

Subcategories: Film production, gaming, and virtual reality

Life science

Subcategories: Biomechanics research and medical rehabilitation

Sports

Industrial

Others

By End-User Industry

Media & Entertainment Industry Shows Strong Adoption Due to Rising Demand for High-Quality Animation

The market is segmented based on end-user industry into:

Media & entertainment

Healthcare

Education & research

Manufacturing

Others

Regional Analysis: Motion Capture Sensors Market

North America North America remains a dominant force in the motion capture sensors market, driven largely by technological advancements and a thriving entertainment industry. The U.S. contributes significantly to the region’s market share, with major studios and research institutions leveraging motion capture for animation, gaming, and biomechanics. Key players like Microsoft Corporation and Cognex Corporation continually innovate, pushing the adoption of high-precision inertial and optical sensors. Additionally, increasing applications in healthcare—such as rehabilitation tracking and sports science—are creating new growth avenues. While regulatory frameworks ensure data accuracy and security, the high cost of advanced systems remains a limiting factor for smaller enterprises.

Europe Europe’s motion capture sensors market is characterized by robust demand from both entertainment and life sciences sectors. Countries like the U.K. and Germany are frontrunners, thanks to their well-established gaming and animation industries, alongside cutting-edge medical research facilities. Stricter data protection laws, such as GDPR, encourage the use of compliant, high-quality sensor technologies. The region also witnesses growing adoption of wearable motion capture solutions for athlete performance monitoring. However, market expansion is somewhat restricted by budget constraints in smaller economies and competition from established North American and Asian manufacturers.

Asia-Pacific Asia-Pacific is the fastest-growing region in the motion capture sensors market, primarily due to rapid urbanization and increasing investments in entertainment and healthcare technologies. China leads the charge, supported by government initiatives in digital content creation and robotics. India and Japan follow closely, with emerging gaming studios and automotive companies integrating motion capture for ergonomic testing. While cost-effective alternatives dominate the lower-tier markets, premium sensor adoption is rising in urban hubs. Challenges include fragmented regulatory standards and intellectual property concerns, though innovation in AI-powered motion analytics offers substantial future potential.

South America The South American market for motion capture sensors is still in its nascent stages, with growth primarily concentrated in Brazil and Argentina. The region’s film and gaming industries show gradual adoption of motion tracking, but limited funding and infrastructure slow widespread deployment. Local manufacturers focus on affordability, which restricts the uptake of high-end systems. Despite these hurdles, rising interest in virtual production and sports analytics hints at opportunities for market players willing to navigate the region’s economic volatility and import dependency.

Middle East & Africa The Middle East & Africa exhibit sporadic but promising growth in motion capture sensor adoption. Wealthier Gulf nations, such as the UAE and Saudi Arabia, invest in immersive entertainment and smart healthcare, while Africa’s progress is constrained by infrastructural gaps. Public-private partnerships aim to boost local technology ecosystems, but market penetration remains low outside of niche applications. Long-term prospects hinge on digital transformation initiatives and rising disposable incomes, though geopolitical instability and currency fluctuations continue to pose challenges for sustained growth.

MARKET DYNAMICS

The development of lightweight, low-power motion capture sensors presents significant opportunities in consumer wearables. Fitness trackers and smart garments incorporating basic motion capture capabilities could create a new market segment worth an estimated $3.4 billion by 2026. Current innovations focus on MEMS-based sensors that offer reasonable accuracy while consuming minimal power. Manufacturers exploring this opportunity prioritize comfort and discretion, with some prototypes resembling ordinary athletic apparel while capturing comprehensive movement data.

Factories implementing collaborative robotics and human-machine interfaces present a growing market for industrial-grade motion capture systems. These applications require sensors that withstand vibration, electromagnetic interference, and harsh environmental conditions while maintaining precision. The industrial sector’s motion capture market is projected to grow at 14.2% CAGR as manufacturers seek safer, more efficient ways to automate processes involving human workers. Recent advancements include explosion-proof variants certified for use in hazardous locations.

The combination of motion capture data with artificial intelligence creates opportunities for predictive analytics and behavior modeling. Advanced algorithms can now detect subtle movement patterns that elude human observers, enabling applications ranging from early disease detection to sports performance optimization. The sports analytics segment alone is projected to generate $1.8 billion in annual revenue by 2025, with motion capture forming a critical data source for these AI-driven systems. Manufacturers investing in platform-agnostic data outputs will be best positioned to capitalize on this trend.

The motion capture industry currently lacks universal standards for data formats and communication protocols. This fragmentation forces users to commit to single-vendor ecosystems or undertake costly integration projects. Proprietary file formats create particular challenges for researchers requiring long-term access to motion capture data. While industry groups have proposed standardization initiatives, adoption remains inconsistent across manufacturers.

Magnetic interference and signal occlusion continue to pose challenges for motion capture implementations. In environments with metal structures or electronic equipment, inertial systems may experience drift while optical systems suffer from marker occlusion. These limitations currently prevent reliable motion capture in settings like operating rooms or manufacturing plants where such conditions prevail. Recent developments in sensor fusion algorithms show promise but haven’t yet achieved perfect reliability.

As motion capture becomes more prevalent in consumer applications, questions arise about appropriate handling of sensitive movement data. Some jurisdictions are considering classification of kinematic data as protected health information when used in medical contexts. These evolving regulations could significantly impact business models that rely on aggregating or monetizing motion data, particularly in regions with strict privacy laws like the GDPR. Compliance will become increasingly important as the technology expands into new markets.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=88024

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Motion Capture Sensors Market?

Which key companies operate in Global Motion Capture Sensors Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 [+91 8087992013] [email protected]

0 notes

Text

Global Miniature Thermopile Detectors Market | New Developments, Current Growth Status, & Forecast to 2032

Global Miniature Thermopile Detectors Market was valued at US$ 97.4 million in 2024 and is projected to reach US$ 151.2 million by 2032, at a CAGR of 5.67% during the forecast period 2025-2032.

Miniature thermopile detectors are infrared sensors that convert thermal energy into electrical signals through the thermoelectric effect. These compact devices feature micro-sensor solutions, sensitive chips, and small optical windows, with integrated thermistors for ambient temperature compensation. They are widely used for non-contact temperature measurement across various industries due to their small form factor, high sensitivity, and fast response times.

The market growth is driven by increasing demand for miniaturized thermal sensors in medical devices, automotive applications, and consumer electronics. Advancements in MEMS technology have enabled cost-effective production, while the growing adoption of IoT devices creates new opportunities. However, competition from alternative technologies like pyroelectric detectors presents challenges. Key players such as Honeywell, Excelitas, and Hamamatsu Photonics are investing in product innovations to maintain market share, with recent developments focusing on improved accuracy and reduced power consumption for battery-operated applications.

Get Full Report with trend analysis, growth forecasts, and Future strategies : https://semiconductorinsight.com/report/global-miniature-thermopile-detectors-market/

Segment Analysis:

By Type

Square Window Format Dominates Due to Higher Compatibility with Compact Device Integration

The market is segmented based on type into:

Circular Window Format

Square Window Format

By Application

Medical Industry Leads Through Extensive Use in Non-contact Temperature Measurement Devices

The market is segmented based on application into:

Medical Industry

Construction Industry

Automobile Industry

Electronic Products

Others

By Detection Range

Medium Range Detectors (0°C to 300°C) Show Maximum Adoption Across Industries

The market is segmented based on detection range into:

Low Range (-40°C to 100°C)

Medium Range (0°C to 300°C)

High Range (up to 600°C)

By Output Signal

Analog Output Remains Preferred Choice for Most Legacy Systems

The market is segmented based on output signal into:

Analog Output

Digital Output

Regional Analysis: Global Miniature Thermopile Detectors Market

North America The North American miniature thermopile detectors market is driven by advanced manufacturing capabilities and strong demand from medical and industrial automation sectors. The U.S. accounts for over 60% of regional market share, with leading manufacturers like Honeywell and TE Connectivity focusing on high-precision sensors for healthcare diagnostics and smart home applications. Strict FDA regulations for medical-grade thermopiles are accelerating R&D investments in miniaturization and IoT integration. However, supply chain disruptions and semiconductor shortages have temporarily constrained production volumes in 2022-2023. The Canadian market shows promising growth in automotive thermal sensing applications, particularly for EV battery monitoring systems.

Europe Europe’s market thrives on stringent industrial safety standards (EN ISO 13849) and growing adoption of thermopiles in building automation. Germany dominates with 35% of regional revenues, driven by its robust automotive sector’s demand for occupant detection systems. The EU’s EcoDesign Directive has pushed manufacturers like Melexis and Hamamatsu Photonics to develop energy-efficient detector solutions. While Western Europe shows maturity with steady 5-7% annual growth, Eastern Europe presents untapped potential – particularly in smart meter applications across Poland and Czech Republic. Brexit-related trade complexities continue to impact UK supply chains, creating minor logistical challenges.

Asia-Pacific As the fastest-growing region, APAC is projected to capture 42% of global market share by 2025, led by China’s electronics manufacturing boom and India’s healthcare expansion. Japanese firms (Hamamatsu, Panasonic) lead in precision thermopile production, while Chinese manufacturers like SK-Advanced are gaining ground with cost-competitive alternatives. The proliferation of consumer electronics and government initiatives like India’s “Make in India” are accelerating adoption. However, quality standardization remains inconsistent across Southeast Asia, creating both opportunities and challenges for international suppliers. Temperature screening needs post-pandemic have spurred demand in public infrastructure projects throughout the region.

South America South America presents a developing market with growth concentrated in Brazil and Argentina’s industrial sectors. While economic volatility limits large-scale investments, the automotive aftermarket and food processing industries show 12% annual demand increase for basic thermopile solutions. Local production remains limited with 85% of detectors being imported, primarily from China and the U.S. Regulatory frameworks are evolving, with Brazil’s INMETRO certification gaining importance for quality compliance. The region’s renewable energy sector is emerging as a potential growth avenue for thermopiles in solar thermal monitoring applications.

Middle East & Africa MEA’s market is nascent but shows strategic growth in oil/gas infrastructure monitoring and healthcare modernization. The UAE and Saudi Arabia account for 70% of regional demand, driven by smart city projects and hospital expansions. African adoption is largely limited to South Africa’s mining sector, though telecommunications infrastructure development is creating new opportunities. Pricing sensitivity dominates procurement decisions, favoring mid-range Asian imports over premium Western products. Lack of local testing facilities and technical expertise remains a market restraint, though regional partnerships with European and Chinese firms are gradually improving technical capabilities.

MARKET OPPORTUNITIES

Emerging Medical Applications Open New Revenue Streams

The healthcare sector presents transformative opportunities for miniature thermopile detectors beyond traditional thermometry applications. Researchers are developing novel diagnostic tools that utilize thermal imaging for early detection of conditions ranging from vascular disorders to breast cancer. Recent clinical trials have demonstrated the potential for thermopile-based systems to reduce screening costs while improving accessibility in low-resource settings. The global medical infrared imaging market is projected to grow at a 9% CAGR through 2030, driven by these innovative applications.

Industrial IoT Integration Creates Scalable Deployment Models

The convergence of miniature thermopile detectors with industrial IoT platforms enables continuous equipment monitoring at scale. Predictive maintenance systems incorporating thermal sensors can identify overheating components before failure, reducing downtime in manufacturing facilities. Energy management applications are particularly promising, with thermopile arrays providing granular temperature data for optimizing HVAC systems in large commercial buildings. Manufacturing plants implementing these solutions have reported energy savings of 15-25%, demonstrating the compelling ROI for industrial users.

Advancements in MEMS Technology Enable Cost Reduction

Breakthroughs in microelectromechanical systems (MEMS) fabrication are lowering the production costs of miniature thermopile detectors while improving performance characteristics. New wafer-level packaging techniques and integrated signal conditioning circuits are reducing bill-of-materials costs by up to 40% for certain sensor configurations. These advancements are making thermopile solutions economically viable for consumer electronics applications that were previously cost-prohibitive. The MEMS sensor market is forecast to exceed $30 billion by 2028, with thermal detectors representing one of the fastest-growing segments.

GLOBAL MINIATURE THERMOPILE DETECTORS MARKET TRENDS

Integration of IoT and AI Driving Demand for Miniature Thermopile Detectors

The rapid advancement of Internet of Things (IoT) and Artificial Intelligence (AI) technologies has significantly increased the adoption of miniature thermopile detectors across various industries. These compact infrared sensors are becoming indispensable in smart home automation, industrial monitoring, and wearable health devices due to their ability to provide non-contact temperature measurements with high accuracy. The global market is projected to grow at a compound annual growth rate (CAGR) of approximately 6.5% from 2023 to 2028, fueled by increasing automation across sectors. Manufacturers are now incorporating advanced signal processing algorithms and machine learning capabilities into thermopile detectors, enabling real-time analytics and predictive maintenance applications.

Other Trends

Healthcare and Medical Applications

The healthcare sector’s growing emphasis on non-invasive patient monitoring is creating substantial opportunities for miniature thermopile detectors. Recent advancements in thermal imaging for fever detection, particularly in the post-pandemic era, have accelerated their adoption in hospitals and public spaces. These detectors are being integrated into portable medical devices for measuring body temperature, blood flow monitoring, and even early detection of certain medical conditions. The medical applications segment is expected to account for over 25% of the total market share by 2025, driven by increasing healthcare expenditure worldwide.

Automotive Industry Adoption Accelerating

The automotive sector is witnessing surging demand for miniature thermopile detectors, particularly for advanced driver-assistance systems (ADAS) and cabin comfort applications. Modern vehicles incorporate these sensors for occupant detection, climate control optimization, and pedestrian detection in night vision systems. With the global automotive infrared sensor market projected to exceed $2.5 billion by 2026, thermopile detectors are becoming a critical component in next-generation vehicles. Leading automakers are increasingly partnering with sensor manufacturers to develop customized solutions that meet stringent automotive safety and reliability standards while maintaining compact form factors.

Energy Efficiency Regulations Shaping Market Dynamics

Stringent energy efficiency regulations worldwide are prompting increased adoption of miniature thermopile detectors in building automation and smart infrastructure. These regulations, such as the EU’s Energy Performance of Buildings Directive (EPBD), have created strong demand for smart HVAC systems utilizing thermal sensors for optimized energy consumption. Building automation currently represents nearly 30% of the total miniature thermopile detector applications, with commercial buildings leading the adoption curve. Sensor manufacturers are responding with ultra-low power consumption designs that can operate on energy harvesting systems, further expanding their application potential in green building initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Miniaturization and Precision to Gain Competitive Edge

The global miniature thermopile detectors market exhibits a mix of established players and emerging competitors, with key manufacturers focusing on miniaturization, energy efficiency, and multi-spectral detection capabilities. Honeywell International Inc. dominates a significant portion of the market, leveraging its decades of experience in sensor technology and strong distribution networks across industrial sectors.

Hamamatsu Photonics and Excelitas Technologies have emerged as important players, particularly in medical and industrial applications where high-precision temperature measurement is critical. These companies continue to invest heavily in MEMS-based thermopile technology to maintain their market positions.

Recent industry trends show that competition is intensifying through strategic acquisitions and patent developments. TE Connectivity strengthened its market position by acquiring First Sensor AG in 2020, gaining access to advanced thermopile technologies for automotive applications. Similarly, Melexis continues to expand its portfolio of contactless temperature sensors for automotive and industrial markets.

Smaller specialized manufacturers like Heimann Sensor GmbH and LASER COMPONENTS are carving out niches in specific applications, particularly in HVAC and consumer electronics, through customized solutions and rapid prototyping capabilities.

List of Key Miniature Thermopile Detector Manufacturers

Honeywell International Inc. (U.S.)

Excelitas Technologies Corp. (U.S.)

Thorlabs, Inc. (U.S.)

Newport Corporation (U.S.)

Hamamatsu Photonics K.K. (Japan)

LASER COMPONENTS GmbH (Germany)

TE Connectivity Ltd. (Switzerland)

PerkinElmer, Inc. (U.S.)

International Light Technologies (U.S.)

SK-Advanced Co., Ltd. (South Korea)

Heimann Sensor GmbH (Germany)

Electro Optical Components, Inc. (U.S.)

Melexis NV (Belgium)

Fluke Corporation (U.S.)

Jotrin Electronics Ltd. (China)

Learn more about Competitive Analysis, and Forecast of Global Miniature Thermopile Detectors Market : https://semiconductorinsight.com/download-sample-report/?product_id=44629

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Miniature Thermopile Detectors Market?

-> Miniature Thermopile Detectors Market was valued at US$ 97.4 million in 2024 and is projected to reach US$ 151.2 million by 2032, at a CAGR of 5.67% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Honeywell, Excelitas, Hamamatsu Photonics, Thorlabs, TE Connectivity, and Melexis among others.

What are the key growth drivers?

-> Growth is driven by increasing automation, demand for contactless temperature measurement, and expanding applications in medical devices and automotive systems.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (38% in 2024), while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include MEMS-based detectors, integration with IoT platforms, and development of ultra-miniature sensors for wearable devices.

Browse Related Reports :

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 +91 8087992013 [email protected]

0 notes

Text

Non-contact Infrared Temperature Sensor Market - Trends, Growth, including COVID19 Impact, Forecast

Global Non-contact Infrared Temperature Sensor Market Research Report 2025(Status and Outlook)

The global Non-contact Infrared Temperature Sensor Market size was valued at US$ 847.2 million in 2024 and is projected to reach US$ 1.42 billion by 2032, at a CAGR of 7.38% during the forecast period 2025-2032.

Non-contact infrared temperature sensors detect thermal radiation emitted by objects to measure surface temperature without physical contact. These sensors utilize thermopile technology that converts infrared energy into electrical signals, with key components including optical systems, detectors, and signal processing circuits. The technology finds applications across medical devices, industrial processes, automotive systems, and smart home appliances.

The market growth is driven by increasing demand for contactless temperature measurement in healthcare (especially post-pandemic), industrial automation trends, and stringent safety regulations. Recent technological advancements in sensor accuracy (±0.1°C tolerance) and miniaturization (chip-scale packaging) are expanding application possibilities. Key players like Melexis and TE Connectivity have introduced innovative MEMS-based sensors with digital outputs and IoT compatibility, while companies such as Excelitas Technologies and Hamamatsu Photonics continue to dominate the high-precision industrial sensor segment.

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis.https://semiconductorinsight.com/download-sample-report/?product_id=95914

Segment Analysis:

By Type

Through Hole Thermopile Infrared Sensor Segment Maintains Strong Market Share Due to Wide Industrial Applications

The market is segmented based on type into:

Through Hole Thermopile Infrared Sensor

SMD Thermopile Infrared Sensor

Other advanced variants

By Application

IoT Smart Home Segment Shows Rapid Growth With Increasing Adoption of Automation Technologies

The market is segmented based on application into:

IoT Smart Home

Industrial Use

Healthcare

Automotive

Others

By Technology

Advanced MEMS-based Sensors Gain Traction Due to Miniaturization and Higher Accuracy

The market is segmented based on technology into:

MEMS-based sensors

Thin film thermopiles

Traditional thermopile sensors

By End-User Industry

Manufacturing Sector Remains Key Consumer With Growing Automation Needs

The market is segmented based on end-user industry into:

Manufacturing

Healthcare

Consumer Electronics

Automotive

Others

Regional Analysis: Global Non-contact Infrared Temperature Sensor Market

North America The North American market for non-contact infrared temperature sensors is driven by stringent healthcare and industrial safety regulations, particularly in the U.S., where demand surged during the COVID-19 pandemic. The FDA-approved use of these sensors in medical diagnostics and their adoption in smart building automation systems contribute to steady growth. The region’s focus on Industry 4.0 integration and IoT applications in manufacturing further accelerates demand. Major players like Excelitas and TE Connectivity dominate the market, leveraging advanced thermopile sensor technology. However, high production costs and competition from alternative sensing technologies pose challenges.

Europe Europe maintains a strong position in the market, supported by strict workplace safety standards under EU directives and the widespread adoption of energy-efficient building management systems. Germany and the UK lead in industrial applications, while France emphasizes healthcare integrations. The region’s emphasis on automotive manufacturing (e.g., thermal imaging for EVs) and intelligent HVAC systems drives innovation. However, GDPR compliance for data collection via sensors adds complexity. Leading manufacturers like Melexis and Heimann Sensor have intensified R&D to meet these regulatory and technical demands.

Asia-Pacific As the fastest-growing regional market, China accounts for over 40% of global production due to its electronics manufacturing ecosystem. The pandemic-driven demand for fever screening devices led to exponential growth, with domestic players like Winson and Senba Sensing expanding capacity. India and Southeast Asia are emerging markets, fueled by smart city initiatives and increasing industrial automation. While cost-effective SMD thermopile sensors dominate, Japan and South Korea focus on high-accuracy applications in robotics and automotive sectors. The region’s challenge lies in balancing affordability with precision requirements.

South America Market growth in South America has been slower due to economic volatility and limited local manufacturing capabilities. Brazil represents the largest market, primarily for industrial equipment maintenance applications, while Argentina sees growing use in food processing temperature monitoring. The lack of standardized regulations compared to North America or Europe results in fragmented adoption patterns. Nonetheless, increasing foreign investments in mining and oil/gas sectors are creating new opportunities for infrared temperature sensing solutions in hazardous environments.

Middle East & Africa The MEA market shows potential with rising smart infrastructure projects in the UAE and Saudi Arabia, where non-contact sensors are deployed in building automation and oil refinery safety systems. Africa’s adoption is constrained by limited technical expertise and infrastructure, though South Africa and Nigeria are emerging as key markets for industrial and medical applications. The region benefits from government initiatives to modernize healthcare facilities but struggles with reliance on imports due to underdeveloped local manufacturing ecosystems.

List of Key Non-Contact Infrared Temperature Sensor Manufacturers

Excelitas Technologies Corp. (U.S.)

Orisystech (South Korea)

Heimann Sensor GmbH (Germany)

Melexis NV (Belgium)

Amphenol Advanced Sensors (U.S.)

TE Connectivity Ltd. (Switzerland)

Semitec Corporation (Japan)

Hamamatsu Photonic KK (Japan)

Nicera Co., Ltd. (Japan)

KODENSHI Corporation (Japan)

Winson Electronics (Taiwan)

Senba Sensing Technology (China)

Sunshine Technologies (China)

San-U (South Korea)

The global non-contact infrared temperature sensor market is witnessing substantial growth due to increasing adoption across healthcare facilities. These sensors have become indispensable tools for mass fever screening, particularly in hospitals, airports, and public spaces – a trend accelerated by recent global health crises. Medical-grade infrared thermometers now account for over 35% of total market revenue, with demand consistently growing at 12% annually. Their ability to provide rapid, hygienic temperature readings without physical contact makes them ideal for infection control protocols. Furthermore, technological advancements have improved accuracy to ±0.2°C, making them suitable for critical medical applications.

Industrial sectors are increasingly incorporating infrared temperature sensors into automation systems, driving market growth. Manufacturing facilities utilize these sensors for equipment monitoring, predictive maintenance, and quality control processes where traditional contact sensors are impractical. The Industry 4.0 revolution has particularly boosted adoption, with smart factories deploying these sensors across production lines. Recent data shows that industrial applications now represent 28% of the market share, growing at 9% year-over-year. Their durability in harsh environments and ability to measure moving objects make them invaluable for modern manufacturing operations.

The proliferation of IoT-enabled devices is further amplifying demand, as infrared sensors can be seamlessly integrated into wireless monitoring systems. This integration reduces downtime by enabling real-time temperature tracking of critical machinery components.

The rapid expansion of smart home ecosystems offers significant opportunities for non-contact infrared temperature sensor manufacturers. Integration with home automation systems for climate control, appliance monitoring, and energy management represents a growing market segment projected to grow at 18% CAGR over the next five years. Advanced sensors capable of multi-point temperature mapping are particularly in demand for next-generation HVAC systems.

Additionally, the development of compact, low-power consumption sensors compatible with IoT platforms enables new use cases in residential security and eldercare applications. Major technology companies are actively seeking partnerships with sensor manufacturers to develop integrated solutions for the connected home market.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=95914

Key Questions Answered by the Non-contact Infrared Temperature Sensor Market Report:

What is the current market size of Global Non-contact Infrared Temperature Sensor Market?

Which key companies operate in Global Non-contact Infrared Temperature Sensor Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Browse More Reports:

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

0 notes

Text

North America Automotive Sensors Market, Size, Segment and Growth by Forecast Period: (2021-2031)

North America Automotive Sensors Market Poised for Steady Growth, Reaching US$2.66 Billion by 2027

The North America automotive sensors market was valued at US$1.63 billion in 2018 and is projected to grow at a CAGR of 5.7% from 2019 to 2027, reaching US$2.66 billion by 2027. This growth is driven by increasing demand for electric vehicles (EVs) and connected cars, alongside advancements in automotive safety and performance technologies. 📚Download Full PDF Sample Copy of Market Report @ https://wwcw.businessmarketinsights.com/sample/TIPRE00005047

Electric Vehicles Fueling Sensor Demand

Automakers like Tesla, BMW, Nissan, Ford, and Volkswagen are heavily investing in EVs, which rely on a wide array of sensors to enhance reliability, safety, and performance. These sensors are integrated into critical systems, including:

Battery management

Braking systems

Induction motors

Dashboard and infotainment systems

The shift toward electrification is further accelerated by environmental concerns and stringent regulations like the Worldwide Harmonized Light Vehicles Test Procedure (WLTP). As EV adoption grows, so does the demand for advanced semiconductors and sensor technologies.

Connected Cars Driving Innovation

Consumer demand for smart, connected vehicles is pushing automakers to integrate advanced sensors and embedded computing systems. Key growth factors include:

Technological advancements in vehicle connectivity

Consumer preference for connected features

Competitive pricing and cost optimization

Enhanced safety and performance through sensor integration

The rise of connected cars is expected to significantly boost the automotive sensors market, as manufacturers focus on developing robust, high-performance sensor solutions.

U.S. Leads Market Growth

The United States dominates the North American automotive sensors market, home to major automakers like General Motors, Ford, and Fiat-Chrysler, as well as leading semiconductor companies such as Intel, Texas Instruments, and ON Semiconductor. The U.S. accounts for nearly 20% of global automotive R&D investments, driven by demand for:

Advanced infotainment systems

Enhanced vehicle safety features

Improved communication and comfort technologies

Canada also contributes to the regional market, with steady growth expected in the coming years.

Future Outlook

With rising EV production, connected car adoption, and continuous technological advancements, the North America automotive sensors market is set for strong growth. Innovations in semiconductor and sensor technologies will play a pivotal role in shaping the future of automotive safety, efficiency, and performance.

Companies Mentioned

• Analog Devices Inc.

• Continental AG

• DELPHI TECHNOLOGIES PLC

• Denso Corporation

• Infineon Technologies

• Melexis

• NXP Semiconductors NV

• ON Semiconductors

• Robert Bosch GmbH

• Texas Instruments Incorporated

Strategic Insights for North America's Automotive Sensors Market

This analysis delivers a data-driven assessment of the North American automotive sensors industry, examining current trends, competitive dynamics, and regional variations. By uncovering high-growth opportunities and unmet market needs, these insights empower businesses to craft differentiated strategies and strengthen their market position.

Through advanced analytics, stakeholders—including investors, manufacturers, and suppliers—can anticipate evolving demand, regulatory shifts, and technological disruptions. A forward-looking perspective ensures long-term resilience, enabling companies to align their investments and innovations with future market demands.

Ultimately, these strategic insights equip decision-makers with the intelligence needed to optimize profitability, mitigate risks, and secure a competitive edge in North America’s rapidly evolving automotive sensors sector. About Us: Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Défense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications Author's Bio Akshay Senior Market Research Expert at Business Market Insights

0 notes

Text

youtube

Melexis: Introducing Induxis (Fully Integrated Inductive Switch)

https://www.futureelectronics.com/m/melexis . Discover the first Induxis® switch, an inductive switch that fully integrates the coils. Contact-less, magnet-less, and stray field immune, this solution simply detects any conductive target (e.g. metal). It is ideal for safety applications in the area of electrification. https://youtu.be/ilXKkf_K30U

#Induxis#Melexis#Fully Integrated Inductive Switch#Melexis Induxis#Inductive switch technology#Sensor innovation#Automotive electronics#Inductive sensing technology#contactless#magnetless#stray field immune#Youtube

0 notes

Text

⚡ Tiny Sensors, Huge Growth: Current Sensor Market to Reach $7.8B by 2034

Current Sensor Market is on an impressive upward trajectory, expected to surge from $3.1 billion in 2024 to $7.8 billion by 2034, growing at a strong CAGR of 9.7%. This growth mirrors the increasing demand for current measurement in smart technologies, electric vehicles, renewable energy systems, and advanced industrial machinery. Current sensors play a crucial role in monitoring and regulating electric currents to enhance system efficiency, safety, and energy savings. From managing battery systems in electric cars to powering smart grid infrastructure, their role is more vital than ever.

Market Dynamics

The market is being driven by a combination of technological innovations, rising renewable energy adoption, and the global transition to electric mobility. The demand for Hall Effect sensors, due to their reliability and cost-effectiveness, remains dominant across several sectors. Shunt-based sensors, gaining ground due to their versatility, are widely used in energy management and automation.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS20825

On the flip side, challenges such as the rising cost of raw materials, integration complexities with IoT, and regulatory compliance across geographies could hinder short-term growth. Yet, the ongoing miniaturization of sensors and increased investment in AI-driven monitoring systems are expected to unlock new opportunities.

Key Players Analysis

Some of the major players steering the current sensor industry include Allegro MicroSystems, Infineon Technologies, Honeywell International, LEM Holding, and Melexis NV. These companies are setting benchmarks through innovation, mergers, and partnerships aimed at improving sensor accuracy, energy efficiency, and real-time data capabilities. Emerging names like Volt Guard, Sense Stream, and Electra Sense are also entering the competitive arena, bringing niche innovations and disrupting traditional sensor models. Strategic moves by these players — especially toward sustainable manufacturing and smart applications — are reshaping the competitive landscape.

Regional Analysis

The Asia-Pacific region continues to lead the current sensor market, driven by rapid industrial growth and tech innovation in countries like China, Japan, and India. Smart city initiatives and the boom in EV adoption have further accelerated sensor deployment. North America follows closely, where focus on IoT, energy-efficient infrastructure, and robust automotive markets — especially in the United States — are fueling demand. Europe, led by Germany and France, maintains strong growth through regulatory pushes for sustainability and automation. Meanwhile, Latin America, the Middle East, and Africa are emerging as high-potential markets, thanks to infrastructure development and increasing renewable energy projects.

Recent News & Developments

Recent years have seen an evolution in sensor pricing and design, with costs ranging from $1 to $50 per unit, depending on type and functionality. Innovations like wireless current sensors, non-invasive technologies, and AI-integrated systems are redefining application scopes. Companies such as Aceinna and Analog Devices have introduced advanced sensor models supporting real-time analytics and predictive maintenance. Moreover, global supply chain challenges and trade policy shifts are prompting businesses to invest in localized manufacturing and sustainable sourcing. Regulatory developments, especially around energy efficiency and data security, are also shaping R&D focus.

Browse Full Report : https://www.globalinsightservices.com/reports/current-sensor-market/

Scope of the Report

This report offers a detailed snapshot of the current sensor industry, spanning segmentation by type, technology, material, and application. It analyzes both quantitative trends — such as unit sales and CAGR — and qualitative dynamics, including SWOT, PESTLE, and competitive strategies. It highlights regional performance, emerging market entrants, and key development strategies like partnerships, acquisitions, and R&D investment. From OEMs to aftermarket trends, and from analog to digital sensor tech, the report lays out a comprehensive roadmap for stakeholders. With detailed insights into cross-segmental opportunities, demand-supply analysis, and local regulatory landscapes, it empowers strategic decision-making for sustainable and profitable growth in this evolving market.

Discover Additional Market Insights from Global Insight Services:

Asset Integrity Management Market : https://www.globalinsightservices.com/reports/asset-integrity-management-market/

Printed Circuit Board Market : https://www.globalinsightservices.com/reports/printed-circuit-board-market/

Medical Sensors Market : https://www.globalinsightservices.com/reports/medical-sensors-market/

Fiber Optic Cables Market : https://www.globalinsightservices.com/reports/fiber-optic-cables-market/

Smart Factory Market : https://www.globalinsightservices.com/reports/smart-factory-market/

#currentmarkettrends #currentsensormarket #iotdevices #energyefficiency #automotivesensors #smartgridtech #hallfx #digitalsensors #industryautomation #techdriven #renewableenergygrowth #electricvehicles #embeddedtech #standaloneelectronics #asiapacificgrowth #europetechmarket #northamericainnovation #industrialsolutions #automotiveinnovation #sensorfusion #smartdevices #powersystems #futuretech #sensorinnovation #aiintegration #minisensors #costefficienttech #energymanagement #techtrends2025 #sensorrevolution #microelectronics #semiconductortechnology #globaltechmarket #batterymanagement #cleantech #sustainablesolutions #iotintegration #powersensing #currentmeasurement #smartmobility

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

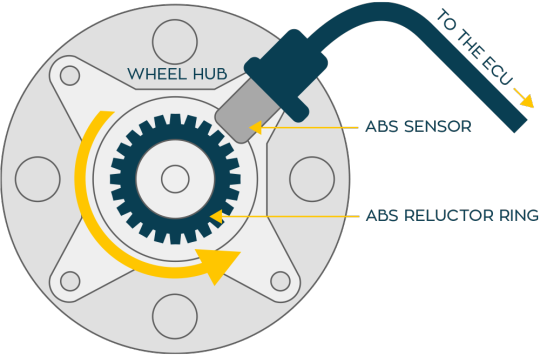

Automotive Wheel Speed Sensor Market Size, Analyzing Trends and Projected Outlook for 2025-2032

Fortune Business Insights released the Global Automotive Wheel Speed Sensor Market Trends Study, a comprehensive analysis of the market that spans more than 150+ pages and describes the product and industry scope as well as the market prognosis and status for 2025-2032. The marketization process is being accelerated by the market study's segmentation by important regions. The market is currently expanding its reach.

The Automotive Wheel Speed Sensor Market is experiencing robust growth driven by the expanding globally. The Automotive Wheel Speed Sensor Market is poised for substantial growth as manufacturers across various industries embrace automation to enhance productivity, quality, and agility in their production processes. Automotive Wheel Speed Sensor Market leverage robotics, machine vision, and advanced control technologies to streamline assembly tasks, reduce labor costs, and minimize errors. With increasing demand for customized products, shorter product lifecycles, and labor shortages, there is a growing need for flexible and scalable automation solutions. As technology advances and automation becomes more accessible, the adoption of automated assembly systems is expected to accelerate, driving market growth and innovation in manufacturing. Automotive Wheel Speed Sensor Market Size, Share & Industry Analysis, By Type (Magneto Resistive Wheel Speed Sensor, Hall Effect Wheel Speed Sensor), By Application (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles)and Regional Forecast, 2021-2028

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/102499

Dominating Region:

North America

Fastest-Growing Region:

Asia-Pacific

Major Automotive Wheel Speed Sensor Market Manufacturers covered in the market report include:

The major companies in the global Automotive Wheel Speed Sensor market include Robert Bosch GmbH, Continental AG, Denso Corporation, NXP Semiconductors, WABCO, ZF Friedrichshafen AG, Hitachi Metals Ltd., Melexis, Delphi Automotive, etc.

Increasing automobile production and rising demand for enhancement of safety features is fueling the growth of WSS. Increased number of driving accidents, emphasis on reforming road safety protocols, and strict regulations regarding vehicle safety have boosted the adoption of the automobile monitoring devices. This, in turn, has propelled the demand for wheel speed sensors.

Geographically, the detailed analysis of consumption, revenue, market share, and growth rate of the following regions:

The Middle East and Africa (South Africa, Saudi Arabia, UAE, Israel, Egypt, etc.)

North America (United States, Mexico & Canada)

South America (Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, etc.)

Europe (Turkey, Spain, Turkey, Netherlands Denmark, Belgium, Switzerland, Germany, Russia UK, Italy, France, etc.)

Asia-Pacific (Taiwan, Hong Kong, Singapore, Vietnam, China, Malaysia, Japan, Philippines, Korea, Thailand, India, Indonesia, and Australia).

Automotive Wheel Speed Sensor Market Research Objectives:

- Focuses on the key manufacturers, to define, pronounce and examine the value, sales volume, market share, market competition landscape, SWOT analysis, and development plans in the next few years.

- To share comprehensive information about the key factors influencing the growth of the market (opportunities, drivers, growth potential, industry-specific challenges and risks).

- To analyze the with respect to individual future prospects, growth trends and their involvement to the total market.

- To analyze reasonable developments such as agreements, expansions new product launches, and acquisitions in the market.

- To deliberately profile the key players and systematically examine their growth strategies.

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2025 to 2032?

► What are the key market dynamics influencing growth in the Global Automotive Wheel Speed Sensor Market?

► Who are the prominent players in the Global Automotive Wheel Speed Sensor Market?

► What is the consumer perspective in the Global Automotive Wheel Speed Sensor Market?

► What are the key demand-side and supply-side trends in the Global Automotive Wheel Speed Sensor Market?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Automotive Wheel Speed Sensor Market?

FIVE FORCES & PESTLE ANALYSIS:

In order to better understand market conditions five forces analysis is conducted that includes the Bargaining power of buyers, Bargaining power of suppliers, Threat of new entrants, Threat of substitutes, and Threat of rivalry.

Political (Political policy and stability as well as trade, fiscal, and taxation policies)

Economical (Interest rates, employment or unemployment rates, raw material costs, and foreign exchange rates)

Social (Changing family demographics, education levels, cultural trends, attitude changes, and changes in lifestyles)

Technological (Changes in digital or mobile technology, automation, research, and development)

Legal (Employment legislation, consumer law, health, and safety, international as well as trade regulation and restrictions)

Environmental (Climate, recycling procedures, carbon footprint, waste disposal, and sustainability)

Points Covered in Table of Content of Global Automotive Wheel Speed Sensor Market:

Chapter 01 - Automotive Wheel Speed Sensor Market for Automotive Executive Summary

Chapter 02 - Market Overview

Chapter 03 - Key Success Factors

Chapter 04 - Global Automotive Wheel Speed Sensor Market - Pricing Analysis

Chapter 05 - Global Automotive Wheel Speed Sensor Market Background or History

Chapter 06 - Global Automotive Wheel Speed Sensor Market Segmentation (e.g. Type, Application)

Chapter 07 - Key and Emerging Countries Analysis Worldwide Automotive Wheel Speed Sensor Market.

Chapter 08 - Global Automotive Wheel Speed Sensor Market Structure & worth Analysis

Chapter 09 - Global Automotive Wheel Speed Sensor Market Competitive Analysis & Challenges

Chapter 10 - Assumptions and Acronyms

Chapter 11 - Automotive Wheel Speed Sensor Market Research Methodology

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

US:+18339092966

UK: +448085020280

APAC: +91 744 740 1245

0 notes

Text

High-speed optical communications

My experience these past few years has been focused on;Melexis, MLX90614ESF-ACF-000-TU, Sensors, Temperature Sensors, Optical Sensors and High-speed optical communications.

0 notes

Text

Automotive Magnetic Sensor Market : Cost Analysis and Pricing Strategies 2025–2032

Global Automotive Magnetic Sensor Market Research Report 2025(Status and Outlook)

Automotive Magnetic Sensor Market size was valued at US$ 3.67 billion in 2024 and is projected to reach US$ 7.84 billion by 2032, at a CAGR of 9.1% during the forecast period 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=95806

MARKET INSIGHTS

The global Automotive Magnetic Sensor Market size was valued at US$ 3.67 billion in 2024 and is projected to reach US$ 7.84 billion by 2032, at a CAGR of 9.1% during the forecast period 2025-2032.

Automotive magnetic sensors are electronic components that detect magnetic fields to measure position, speed, direction and current in vehicles. These sensors utilize different technologies including AMR (Anisotropic Magnetoresistance), GMR (Giant Magnetoresistance), and TMR (Tunnel Magnetoresistance) effects. They play critical roles in various automotive applications such as anti-lock braking systems (ABS), electronic power steering, transmission systems, and electric vehicle battery management.

The market growth is driven by increasing vehicle electrification, stricter safety regulations mandating advanced driver assistance systems (ADAS), and rising electric vehicle production. Major players like NXP Semiconductors and Infineon Technologies are expanding their product portfolios through strategic partnerships – for instance, in 2023, NXP introduced a new TMR-based wheel speed sensor with improved accuracy for EV applications. However, pricing pressures and complex integration requirements in modern vehicles pose challenges to market expansion.

List of Key Automotive Magnetic Sensor Companies Profiled

NXP Semiconductors (Netherlands)

Infineon Technologies (Germany)

TDK Corporation (Japan)

Magnetic Sensors Corporation (U.S.)

Melexis (Belgium)

Allegro MicroSystems (U.S.)

LEM Holding SA (Switzerland)

Honeywell International (U.S.)

Sensitec GmbH (Germany)

Sanken Electric (Japan)

Segment Analysis:

By Type

TMR Sensors Lead the Market Due to High Sensitivity in Advanced Automotive Applications

The global automotive magnetic sensor market is segmented based on sensor type into:

AMR (Anisotropic Magnetoresistance)

Applications: Position sensing, speed detection, and angle measurement

GMR (Giant Magnetoresistance)

Applications: Steering angle sensing, transmission systems

TMR (Tunnel Magnetoresistance)

Applications: Advanced ADAS systems, brake position sensing

Hall Effect Sensors

Other Emerging Technologies

By Application

ADAS Systems Drive Growth With Increasing Safety Regulations Worldwide

The market is segmented based on application into:

Advanced Driver Assistance Systems (ADAS)

Engine and Powertrain Management

Transmission Systems

Braking Systems

Other Vehicle Systems

By Vehicle Type

Electric Vehicles Emerging as Key Growth Segment for High-Precision Magnetic Sensors

The market is segmented based on vehicle type into:

Passenger Vehicles

Commercial Vehicles

Electric Vehicles (BEVs, PHEVs, HEVs)

Off-Road Vehicles

By End-User

OEMs Remain Primary Consumers for Integrated Automotive Solutions

The market is segmented based on end-user into:

OEMs (Original Equipment Manufacturers)

Aftermarket

Tier-1 Suppliers

Regional Analysis: Global Automotive Magnetic Sensor Market

North America North America remains a dominant force in the automotive magnetic sensor market, largely due to technological advancements and robust demand for electric vehicles (EVs). The United States, in particular, leads with stringent safety regulations and federal mandates promoting ADAS (Advanced Driver Assistance Systems), which heavily rely on magnetic sensors for functions like position detection and speed monitoring. Canada’s focus on sustainable mobility, backed by investments exceeding $300 million in EV infrastructure, further drives adoption. Major players like Honeywell International and Allegro MicroSystems continue to innovate, particularly in high-accuracy TMR sensors. However, supply chain disruptions and semiconductor shortages have occasionally slowed production, creating opportunities for localized component manufacturing.

Europe Europe’s automotive magnetic sensor market thrives on its strong automotive OEM base and strict emissions regulations pushing electrification. Germany, the region’s manufacturing hub, sees high demand for GMR and TMR sensors in luxury vehicles and industrial automation. The EU’s planned phase-out of internal combustion engines by 2035 accelerates investments in EV sensor technologies, with companies like Infineon and NXP Semiconductors leading R&D. Eastern European nations are emerging as cost-competitive manufacturing centers, though adoption lags in price-sensitive markets. A notable challenge is the region’s reliance on third-party suppliers for raw materials, which could impact pricing stability in the long term.

Asia-Pacific Asia-Pacific dominates global market share, accounting for over 40% of demand, driven by China’s massive automotive production and India’s growing electric rickshaw market. Chinese manufacturers prioritize cost-efficient AMR sensors for mass-market EVs, while Japan and South Korea focus on high-end TMR solutions for hybrid and autonomous vehicles. Tier-1 suppliers like TDK and Sensitec are expanding production capacities in Southeast Asia to cater to regional OEMs. However, inconsistent quality standards and intellectual property concerns in certain markets pose risks. The region’s rapid urbanization and government subsidies for EV adoption (e.g., China’s NEV policy) ensure sustained growth, though competition keeps profit margins thin.

South America South America’s market is nascent but shows promise, particularly in Brazil and Argentina where local production incentives are boosting automotive part manufacturing. Magnetic sensor adoption is primarily driven by aftermarket demand for vehicle safety upgrades and emission control systems. Economic volatility and currency fluctuations, however, hinder large-scale investments in advanced sensor technologies. Most sensors are imported, making the region sensitive to global supply chain bottlenecks. Fleet modernization programs in mining and agriculture sectors offer niche opportunities for robust sensor solutions, but widespread electrification remains distant due to inadequate charging infrastructure.

Middle East & Africa The Middle East demonstrates selective growth, with UAE and Saudi Arabia investing in smart mobility projects like autonomous taxis, creating demand for precision sensors. Africa’s market is largely untapped, though South Africa’s automotive hubs show potential for basic magnetic sensor integration in commercial vehicles. The region faces challenges like low consumer awareness, limited local expertise, and dependency on imports. Long-term opportunities lie in infrastructure-linked projects, such as Dubai’s Autonomous Transportation Strategy, but political instability in parts of Africa slows market penetration. Partnerships with global distributors are crucial to bridge technology gaps.

Market Dynamics

The automotive magnetic sensor supply chain involves over 150 individual components sourced from specialized suppliers worldwide. Recent geopolitical tensions and logistics disruptions have pushed typical order fulfillment times from 12 weeks to over 24 weeks for some sensor varieties. Many manufacturers are now carrying 40-50% higher inventory buffers to mitigate these risks. Lag Creates Integration Hurdles

The lack of industry-wide standards for magnetic sensor interfaces and communication protocols continues to create integration challenges. Vehicle manufacturers report spending 15-20% of sensor implementation time on compatibility testing and software adaptation rather than value-added features.

The global automotive magnetic sensor market is experiencing robust growth, primarily driven by the rapid electrification of vehicles and advancements in autonomous driving technologies. With electric vehicles projected to account for over 30% of new car sales by 2030, magnetic sensors have become critical components for motor position sensing, battery management systems, and current monitoring applications. Simultaneously, autonomous vehicle development demands high-precision position and speed sensing capabilities, where Anisotropic Magnetoresistance (AMR) and Tunnel Magnetoresistance (TMR) sensors deliver superior performance in harsh automotive environments.

Automotive manufacturers are increasingly demanding smaller, more accurate magnetic sensor solutions to accommodate space constraints while improving system reliability. Recent innovations have reduced sensor package sizes by 40% compared to previous generations while maintaining or enhancing measurement precision. This trend is particularly evident in electric power steering systems, where compact magnetic angle sensors enable precise torque measurement with minimal space requirements. Furthermore, the integration of digital signal processing within sensor ICs has reduced system complexity while improving noise immunity by up to 70% in some applications.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=95806

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Magnetic Sensor Market?

Which key companies operate in Global Automotive Magnetic Sensor Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/global-extreme-ultraviolet-euv_2.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-industrial-force-sensor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-smart-temperature-monitoring.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-extreme-ultraviolet-euv.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-non-tactile-membrane-switches.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-semiconductor-alcohol-sensors.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-healthcare-biometric-systems.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-class-d-audio-power-amplifiers.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-usb-31-flash-drive-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-optical-fiber-development-tools.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-3d-chips-3d-ic-market-regional.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-3d-acoustic-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-wired-network-connectivity-3d.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-lens-antenna-market-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-millimeter-wave-antennas-and.html

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 [+91 8087992013] [email protected]

0 notes

Text

3D Sensor Companies - Infineon Technologies AG (Germany) and Microchip Technology Inc. (US) are the Key Players

The global 3D sensor market is expected to be valued at USD 6.1 billion in 2024 and is projected to reach USD 12.8 billion by 2029 and grow at a CAGR of 16.3% from 2024 to 2029. Market players ' major growth strategies are product launches, acquisitions, collaborations, partnerships, agreements, and expansions. These strategies have enabled them to fulfill the growing demand for 3D sensor from different verticals and expand their global footprint by offering products in all the major regions.

Key players operating in the 3D sensor market are Infineon Technologies AG (Germany), Microchip Technology Inc. (US), Sony Group Corporation (Japan), KEYENCE CORPORATION (US), STMicroelectronics (Switzerland), LMI TECHNOLOGIES INC. (US), ifm electronic gmbh (Germany), Qualcomm Technologies, Inc (US), NXP Semiconductors (Netherlands), OMNIVISION (US), SICK AG (Sweden), Velodyne Lidar, Inc. (US), Leuze electronic GmbH + Co. KG (US), ams-OSRAM AG (Austria), Melexis (Belgium), Pepperl+Fuchs (Germany), Teledyne Technologies Incorporated (US), Orbbec Inc. (China), Micro-Epsilon (Germany), Banner Engineering Corp. (US), wenglor (Germany), OMRON Corporation (Japan), Asahi Kasei Microdevices Corporation (Japan), Semiconductor Components Industries, LLC (US), SmartRay GmbH (Germany).

Major 3D Sensor companies include:

Infineon Technologies AG (Germany)

Infineon Technologies AG provides semiconductor and system solutions. It operates through the following segments: Automotive, Green Industrial Power, Power and Sensor systems, Connected Secure Systems, and Other Operating Segments. The Automotive segment designs, develops, manufactures, and markets semiconductors for automotive applications. The Green Industrial Power segment involves the design, development, manufacture, and marketing of semiconductors for electrical energy generation, transmission, and economy. The Power and Sensor systems segment includes the design, development, manufacture, and marketing of semiconductors for energy-efficient power supplies, mobile devices, and mobile phone network infrastructures. Connected Secure Systems designs, develops, manufactures, and markets semiconductor-based security products for card applications and network systems.

The company markets its products to the automotive, industrial, communications, and consumer and security electronics sectors worldwide, including the Americas, Europe, the Middle East, and Asia Pacific. It has 21 manufacturing units and 54 R&D centers in these regions.

Microchip Technology Inc. (US)

Microchip technology develops, manufactures, and sells intelligent, connected, and secure embedded control solutions used by customers for various applications. It sells its products globally through its sales and distribution network. The company’s product portfolio includes microcontrollers, amplifiers, memories, motor drivers, sensor, wireless connectivity products, safety & security products, power management, thermal management, and high-speed communication devices. The company’s synergistic product portfolio empowers disruptive growth trends, including 5G, artificial intelligence and machine learning, Internet of Things (IoT), advanced driver assist systems (ADAS) and autonomous driving, and electric vehicles, in key end markets such as automotive, aerospace and defense, communications, consumer, data centers and computing, and industrial.

The company has a patented 3D sensor technology called GestIC. This technology uses an electric field for proximity sensing and developing 3D gesture controllers. It enables users to interact with the device using hand or finger movement. These sensor have a detection range of 0–20 cm and operate at low power, which makes them energy-efficient. GestIC technology-based 3D sensor are not affected by surrounding light and sound; they use thin, low-cost sensing electrodes. These gesture controllers are used in smartphones, computer peripherals, electronic readers, game controllers, and consumer electronics products.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=248537071

Sony Group Corporation (Japan)