#Microgrid Controller Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

Enabling Sustainable Energy: The Rise of Microgrid Controllers

The global microgrid controller market is witnessing significant growth as the world transitions toward resilient and sustainable energy infrastructure. According to recent research, the market was valued at USD 7.7 Bn in 2023 and is projected to reach USD 29.4 Bn by 2034, expanding at a robust CAGR of 12.8% from 2024 to 2034. Growing adoption of distributed energy resources (DERs), rising investments in smart grid technologies, and increasing government support for microgrid deployment are key factors propelling this growth.

Market Overview: Microgrid controllers play a pivotal role in managing and optimizing distributed energy systems. They act as intelligent platforms that coordinate energy generation, storage, and consumption in real-time, ensuring stability and reliability across the microgrid network. These systems are increasingly being deployed in campuses, hospitals, military bases, and remote communities to provide reliable, clean, and uninterrupted power.

As global energy systems evolve, microgrids and their control systems are becoming central to decentralization strategies, especially in areas with limited access to traditional grid infrastructure or where energy resilience is a priority.

Market Drivers & Trends

One of the primary drivers of the microgrid controller market is the rise in government funding for the development and integration of microgrids. These initiatives aim to improve energy resilience, reduce greenhouse gas emissions, and support renewable energy integration. Programs such as the Australian Renewable Energy Agency’s (ARENA) Regional Australia Microgrid Pilots Program (RAMPP) exemplify this trend.

Another significant driver is the increasing adoption of grid-connected smart microgrid controllers. These systems allow users to optimize energy consumption, reduce utility costs, and enhance energy reliability by connecting DERs like solar, wind, and battery storage to the grid. They also allow seamless transitions between on-grid and islanded modes, making them ideal for both urban and remote installations.

Latest Market Trends

A key trend reshaping the microgrid controller landscape is the development of smart microgrid communities. Companies such as SunPower Corp., Schneider Electric, and Southern California Edison are collaborating to create all-electric, solar-powered, battery-equipped communities with shared microgrid infrastructure, such as the Energy-Smart Connected Communities project in Menifee, California.

Moreover, digitalization and AI integration are gaining traction. Modern microgrid controllers are increasingly being equipped with machine learning capabilities for predictive analytics, energy forecasting, and autonomous decision-making.

Key Players and Industry Leaders

The global microgrid controller market is highly competitive and includes several prominent players focused on technological innovation and strategic partnerships. Notable companies include:

ABB

AutoGrid Systems, Inc.

Caterpillar

Cummins Inc.

Eaton

Emerson Electric Co

Encorp Powertrans

General Electric Company

Hitachi Energy Ltd.

Honeywell International Inc.

Power Analytics Corporation

S&C Electric Company

Schneider Electric

Schweitzer Engineering Laboratories, Inc.

Siemens

These companies are actively investing in R&D, product development, and regional expansions to strengthen their market presence.

Recent Developments

Key strategic moves are helping to shape the future of the microgrid controller market:

In March 2023, ABB announced a partnership with Direct Energy Partners to promote the adoption of Direct Current (DC) microgrids. ABB’s investment through its venture capital unit underscores the strategic importance of digital microgrid solutions.

Also in March 2023, Siemens Canada teamed up with Humber College to establish the Sustainable Microgrid and Renewable Technology Lab (SMART Lab). This initiative supports education, research, and workforce development in microgrid technologies.

Get a concise overview of key insights from our Report in this sample

Market New Opportunities and Challenges

As governments aim for carbon neutrality and grid modernization, new opportunities are emerging in:

Remote electrification projects in developing nations

Resilient infrastructure development in disaster-prone areas

Military and healthcare facility microgrids, ensuring energy independence and reliability

However, the market also faces challenges, such as:

High initial capital investment

Regulatory barriers and grid integration complexities

Cybersecurity concerns related to grid-connected digital systems

Overcoming these hurdles requires collaborative efforts between policymakers, utilities, and technology providers.

Future Outlook

Looking ahead, the global microgrid controller market is poised for transformative growth. As technologies mature and costs decline, microgrid solutions are expected to become more accessible and scalable. The integration of AI, IoT, and blockchain in microgrid controllers will further enhance performance, transparency, and operational efficiency.

Market Segmentation

The market can be segmented by offering, connectivity, and end-user:

By Offering

Hardware

Software

By Connectivity

On-grid

Off-grid

By End-user

Utilities

Renewable Energy

Traditional Energy

Commercial

Military and Defense

Healthcare

Industrial

Others (Automotive and Transportation, Telecommunications, etc.)

Hardware-based controllers currently dominate the market, but software-based platforms are gaining prominence due to their advanced analytics and remote control capabilities.

Regional Insights

Asia Pacific emerged as the leading region in 2023, driven by rapid industrialization, increased government investment in rural electrification, and a surge in microgrid projects across India and China.

North America follows closely, with strong demand for smart grid infrastructure, renewable energy, and energy security. Government initiatives aimed at improving grid reliability and electrifying off-grid communities are fostering regional growth.

Europe is witnessing increased adoption due to stringent decarbonization targets, especially in countries like Germany, the U.K., and France.

Other regions, including the Middle East & Africa and South America, are expected to experience moderate growth with rising awareness and energy access initiatives.

Why Buy This Report?

Purchasing the Microgrid Controller Market Report offers several advantages:

In-depth analysis of current market trends, growth drivers, and challenges

Quantitative and qualitative assessments including Porter’s Five Forces and value chain analysis

Forecasts up to 2034 with historical context and future projections

Detailed segmentation and regional breakdowns

Company profiles and competitive landscape insights

Recent developments and innovations driving market change

This report is ideal for:

Investors seeking high-growth opportunities in energy tech

Energy companies planning strategic expansions

Policy makers and regulators designing smart grid programs

Technology vendors exploring integration opportunities

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Want to know more? Get in touch now. - https://www.transparencymarketresearch.com/contact-us.html

0 notes

Text

Microgrid Controller Market by Connectivity (Grid-connected, Off-grid), Offering (Hardware, Software & Services), End User (Commercial & Industrial, Military, Government, Institutes & Campuses, Healthcare) and Region

0 notes

Text

High-Power Rectifiers Market Drivers: Industrial Expansion and Energy Demand Surge

The global high-power rectifiers market is experiencing significant momentum driven by the rapid expansion of industrial sectors, increasing electrification, and the growing demand for high-efficiency power conversion systems. As industries modernize and focus on energy-efficient operations, the deployment of robust rectification systems becomes a critical enabler of productivity and sustainability.

Surge in Industrialization Across Developing Economies

One of the most influential drivers of the high-power rectifiers market is the rapid industrialization occurring in emerging economies such as India, Brazil, Vietnam, and parts of Africa. As these countries focus on strengthening their manufacturing bases and infrastructure, there is a growing need for reliable and stable power supply systems. High-power rectifiers play a vital role in converting alternating current (AC) into direct current (DC) for use in a wide array of heavy industrial machinery, electrochemical processes, and smelting operations.

This demand is further amplified by government initiatives supporting industrial clusters and special economic zones (SEZs), which often include incentives for upgrading power systems. These developments are resulting in a sustained rise in procurement and implementation of high-power rectifier systems.

Renewable Energy Integration Requiring Efficient Power Conversion

As the energy mix shifts toward renewable sources like solar and wind, which inherently generate DC power or require DC transformation for efficient grid integration, high-power rectifiers become indispensable. These rectifiers help regulate and stabilize the fluctuating output from renewables, making them grid-compatible. The rise of hybrid energy systems and microgrids��especially in remote and off-grid locations—also bolsters the demand for advanced rectification technology.

Furthermore, utilities and energy providers are investing in smart grid infrastructure, where high-power rectifiers support voltage regulation, improve power quality, and ensure the seamless flow of energy between distributed energy resources (DERs) and the main grid.

Expansion of the Electrochemical Industry

Electrochemical industries—including aluminum smelting, electroplating, chlor-alkali production, and hydrogen generation—rely heavily on high-power DC supplies. These industries require a continuous, stable, and high-capacity power source for their chemical processes. With increasing global demand for lightweight metals (like aluminum in automotive and aerospace), the demand for efficient rectifier systems continues to rise.

The electrification of the chemical processing sector, driven by stricter environmental regulations and decarbonization efforts, is also expected to accelerate rectifier deployment. Companies are replacing outdated, inefficient power conversion units with modern rectifiers that offer better power factor correction, lower harmonic distortion, and improved thermal performance.

Technological Advancements Improving Efficiency and Reliability

Technological advancements in high-power rectifier design—such as the incorporation of silicon carbide (SiC) and gallium nitride (GaN) semiconductors—have significantly improved system performance. These new-generation rectifiers deliver higher switching speeds, better heat dissipation, and compact form factors, enabling their deployment in space-constrained and mission-critical environments.

Additionally, digital control systems and remote monitoring capabilities have made modern rectifiers more user-friendly, safer, and adaptable to diverse operational requirements. These innovations are particularly appealing to industries seeking to upgrade legacy systems for better control and energy efficiency.

Growing Investment in Infrastructure and Transportation

The construction and modernization of critical infrastructure—including railways, metros, airports, and ports—demand robust power solutions. High-power rectifiers are essential components in railway traction systems, substations, and urban transit power supplies. With increasing urbanization and mobility needs, governments worldwide are ramping up investments in public transportation networks, which directly contributes to the growing demand for high-performance rectifier systems.

The adoption of electrified rail and high-speed trains in countries such as China, France, Germany, and Japan further amplifies market potential. In addition, electric vehicle (EV) charging infrastructure development, especially for fast and ultra-fast chargers, indirectly drives the need for efficient rectification technologies.

Demand for Customization and Modular Solutions

Modern industries are increasingly looking for customized rectifier solutions that meet their specific voltage, current, and power quality requirements. This shift toward modular and tailor-made solutions is encouraging manufacturers to develop flexible product lines that are easily scalable and maintainable. As a result, companies offering high customization capability and aftersales support are gaining a competitive edge, fueling overall market growth.

Conclusion

The high-power rectifiers market is being propelled by a diverse range of drivers, from industrial expansion and renewable energy integration to advancements in semiconductor technology and infrastructure development. As industries continue to transition toward energy-efficient and automated systems, the demand for reliable, high-performance rectifiers is expected to grow steadily. Market players focusing on innovation, customization, and energy efficiency will be well-positioned to capitalize on these emerging opportunities.

0 notes

Text

From Fossil to Future: Building a Sustainable Energy System

The global energy crisis and climate challenge demand that we rethink how we design an energy system. Transitioning from fossil fuels to renewables, smart grids, and storage assurance is essential. This guide highlights key strategies and technologies to build a future-ready energies that supports sustainability, reliability, and decarbonization.

1. What Is an Energy System?

An energy system encompasses generation, storage, transmission, and distribution of power. A future sustainable energy integrates solar, wind, geothermal, nuclear, and other low‑carbon sources to minimize greenhouse gas emissions .

2. Renewable Energy Generation as the Backbone

Future energy systems must prioritize solar PV, wind turbines, hydropower, and geothermal––clean sources that deliver low‑carbon electricity. Advances in solar cell efficiency and wind turbine design are driving down costs and enhancing output .

3. Energy Storage: Essential for Grid Stability

Intermittent generation from renewables makes energy storage critical to any future energy. Technologies like lithium-ion batteries, flow batteries, pumped hydro, compressed air, and hydrogen storage ensure consistent supply and prevent curtailment .

4. Smart Grid Integration

Transforming the grid into a smart grid enables real-time control, two-way flows, demand management, and integration of distributed energy resources. A digital backbone is vital for optimizing the future energy .

5. Power‑to‑X for Sector Coupling

Energies flexibility improves through Power‑to‑X: converting surplus renewable electricity into hydrogen, synthetic fuels, or chemicals. This facilitates decarbonization across transport and industry .

6. Hybrid Power and Diverse Generation Mix

A resilient future energy systems often uses hybrid power solutions—combinations of solar, wind, battery, and backup generation—in storage‑balanced microgrids or community energy systems.

7. Emerging Technologies: AI, Blockchain & Diagnostics

AI and blockchain are enabling advanced operations in the system through predictive maintenance, decentralized energy markets, and real-time optimization. Prosumers (producer‑consumers) become active players in smart grid management.

8. Policy, Regulation & Finance

Supporting infrastructure and investments hinge on strong policy frameworks. Carbon pricing, renewable targets, incentives, and innovation funding are key to mobilizing capital for a sustainable energy systems .

9. Community‑Scale Energy Systems

Localized energy communities build decentralized future energy systems where generation, storage, and consumption are optimized at community scale. These systems boost resilience and social participation .

10. Roadmap: From Fossil to Future

To build a future energy systems, the roadmap includes:

Scaling renewables and low‑carbon generation

Deploying energy storage and smart grid tech

Leveraging Power-to-X and sector coupling

Fostering hybrid power microgrids and community systems

Innovating with AI, blockchain, and digital platforms

Advocating robust policy, regulation, and finance alignment

Vision & Benefits

A well-designed future energy systems delivers cleaner air, climate resilience, energy security, reduced fossil reliance, and inclusive economic growth. It enables a global shift to low‑carbon electricity systems and positions societies to adapt to future energy demands sustainably.

Stay informed on transforming energies systems for impact—follow IMPAAKT, your top business magazine, for strategic insights and sustainability-driven news.

0 notes

Text

Philippines Microgrid Market Size, Share, Demand, Key Drivers, Development Trends and Competitive Outlook

"Executive Summary Philippines Microgrid Market : Data Bridge Market Research analyses that the market is expected to reach the value of USD 620.14 million by 2029, at a CAGR of 17.6% during the forecast period

Philippines Microgrid Market report is sure to give new wings to the successful business. DBMR team uses new skills, new thinking, latest tools and innovative programs to help produce this report which aids clients achieve their goal. This is the most relevant, unique, fair and creditable global market research report which has been designed depending upon the business needs. Being an international market research report, it contains market research data from different corners of the globe. An experienced pool of language resources and integrated panel base carries out market research analysis across the world.

The Philippines Microgrid Market report brings together high quality global market research and wide-ranging multi-country industry specific knowledge of analysts. With a team of multi-lingual analysts and skilled project managers, the Philippines Microgrid Market report serve clients on every strategic aspect including product development, application modelling, exploring niche growth opportunities and new markets. With this report, it becomes easy to predict investment in an emerging market, expansion of market share or success of a new product with the help of global market research analysis. Sound facts and figures are represented well with graphs, and charts throughout the Philippines Microgrid Market report.

Discover the latest trends, growth opportunities, and strategic insights in our comprehensive Philippines Microgrid Market report. Download Full Report: https://www.databridgemarketresearch.com/reports/philippines-microgrid-market

Philippines Microgrid Market Overview

**Segments**

- By Type: - AC Microgrid - DC Microgrid - By Connectivity: - Grid Connected - Remote/Island

The Philippines microgrid market is witnessing significant growth, driven by the increasing demand for reliable and efficient power supply, especially in remote or island locations where the main grid infrastructure is unreliable or nonexistent. AC microgrids are popular in urban areas where there is a need to connect with the main grid, while DC microgrids are commonly used in off-grid settings for their efficiency. Grid-connected microgrids offer the advantage of energy sharing and stability, whereas remote/island microgrids provide self-sufficiency and independence from the main grid.

**Market Players**

- EnSync Energy Systems - Husk Power Systems - Schneider Electric - ABB - Siemens - Power Analytics Corporation - General Electric - Toshiba Corporation - Honeywell International Inc. - Lockheed Martin Corporation

The Philippines microgrid market is competitive and fragmented, with several key players competing for market share. Companies such as EnSync Energy Systems, Husk Power Systems, and Schneider Electric are focusing on innovative solutions and collaborations to expand their presence in the market. Larger corporations like ABB, Siemens, and General Electric are leveraging their global expertise and resources to offer comprehensive microgrid solutions tailored to the Philippines market. Emerging players such as Power Analytics Corporation and Lockheed Martin Corporation are also making their mark with cutting-edge technologies and strategic partnerships.

The Philippines microgrid market is poised for continued growth and development, spurred by the increasing focus on renewable energy sources and the need for reliable power supply solutions. One of the emerging trends in the market is the integration of advanced control systems and software solutions to optimize microgrid operations and enhance grid stability. Market players are increasingly investing in research and development to enhance the performance and efficiency of microgrid systems, driving innovation in energy storage technologies, smart grid solutions, and predictive maintenance tools.

Moreover, the growing awareness of the environmental impact of traditional energy sources is fueling the adoption of microgrid solutions in the Philippines. Companies are increasingly turning to microgrids powered by solar, wind, and other renewable energy sources to reduce their carbon footprint and meet sustainability goals. This shift towards cleaner energy sources is expected to drive the demand for microgrid systems in the coming years, creating new opportunities for market players to offer integrated solutions that combine renewable energy generation with advanced energy management technologies.

In addition, government initiatives and regulatory support are playing a crucial role in shaping the microgrid market landscape in the Philippines. Policies and incentives aimed at promoting renewable energy deployment and improving energy access in remote areas are driving investments in microgrid projects across the country. Market players are closely monitoring regulatory developments and collaborating with government agencies to align their strategies with the broader energy transition goals, ensuring compliance with emerging standards and regulations in the microgrid sector.

Furthermore, the advent of innovative financing models and partnerships is expected to accelerate the deployment of microgrid systems in the Philippines. Collaborations between technology providers, energy service companies, and financing institutions are facilitating project development and deployment, enabling easier access to capital and resources for microgrid projects. By leveraging these partnerships and investment mechanisms, market players can overcome financial barriers and scale up microgrid deployments to meet the growing energy demand in the Philippines.

Overall, the Philippines microgrid market is poised for robust growth, driven by a combination of technological advancements, policy support, and market dynamics. Market players that can offer tailored solutions, innovative technologies, and collaborative partnerships are well-positioned to capitalize on the emerging opportunities in the dynamic microgrid landscape of the Philippines.The Philippines microgrid market presents a compelling landscape for market players, with a strong emphasis on innovative solutions and sustainable energy sources. The country's focus on renewable energy and the need for reliable power supply solutions is driving the adoption of microgrid systems, particularly in remote or island locations. The market is characterized by a mix of established players like Schneider Electric, ABB, and Siemens, as well as emerging companies such as Power Analytics Corporation and Lockheed Martin Corporation. These players are vying for market share by offering comprehensive microgrid solutions that cater to the diverse needs of the Philippines market.

One of the key trends shaping the Philippines microgrid market is the integration of advanced control systems and software solutions to optimize microgrid operations. This trend underscores the importance of efficiency and grid stability in microgrid deployments, highlighting the growing emphasis on leveraging technology to enhance energy management. Market players are investing in research and development to drive innovation in energy storage technologies, smart grid solutions, and predictive maintenance tools, reflecting a commitment to advancing the capabilities of microgrid systems in the Philippines.

Moreover, the shift towards cleaner energy sources such as solar and wind power is driving the demand for microgrid systems in the Philippines. Companies are increasingly adopting renewable energy-driven microgrids to reduce their carbon footprint and align with sustainability goals. This transition towards sustainable energy sources not only addresses environmental concerns but also presents new business opportunities for market players to offer integrated solutions that combine renewable energy generation with advanced energy management technologies.

Government initiatives and regulatory support are also instrumental in shaping the microgrid market landscape in the Philippines. Policies aimed at promoting renewable energy deployment and improving energy access in remote areas are driving investments in microgrid projects. Market players are closely monitoring regulatory developments and collaborating with government agencies to align their strategies with energy transition goals, ensuring compliance with emerging standards and regulations in the microgrid sector.

Furthermore, the emergence of innovative financing models and partnerships is expected to accelerate the deployment of microgrid systems in the Philippines. Collaborations between technology providers, energy service companies, and financing institutions are facilitating project development and enabling easier access to capital for microgrid projects. By leveraging these partnerships and investment mechanisms, market players can overcome financial barriers and scale up microgrid deployments to meet the growing energy demand in the Philippines.

In conclusion, the Philippines microgrid market presents a dynamic and evolving landscape with ample opportunities for market players to drive growth and innovation. By focusing on tailored solutions, technological advancements, and strategic partnerships, companies can position themselves to meet the rising demand for reliable and sustainable energy solutions in the Philippines microgrid market.

The Philippines Microgrid Market is highly fragmented, featuring intense competition among both global and regional players striving for market share. To explore how global trends are shaping the future of the top 10 companies in the keyword market.

Learn More Now: https://www.databridgemarketresearch.com/reports/philippines-microgrid-market/companies

DBMR Nucleus: Powering Insights, Strategy & Growth

DBMR Nucleus is a dynamic, AI-powered business intelligence platform designed to revolutionize the way organizations access and interpret market data. Developed by Data Bridge Market Research, Nucleus integrates cutting-edge analytics with intuitive dashboards to deliver real-time insights across industries. From tracking market trends and competitive landscapes to uncovering growth opportunities, the platform enables strategic decision-making backed by data-driven evidence. Whether you're a startup or an enterprise, DBMR Nucleus equips you with the tools to stay ahead of the curve and fuel long-term success.

Reasons to Consider This Report

To understand the Philippines Microgrid Market landscape and identify market segments that are most likely to guarantee a strong return

Stay ahead of the race by comprehending the ever-changing competitive landscape for Philippines Microgrid Market

Efficiently plan M&A and partnership deals in Philippines Microgrid Market by identifying market segments with the most promising probable sales

Helps to take knowledgeable business decisions from perceptive and comprehensive analysis of market performance of various segments of cannabis seeds market

Obtain market revenue forecasts for the Philippines Microgrid Market by various segments in regions.

Browse More Reports:

Global Industrial Computed Tomography Market Middle East and Africa Personal Care Ingredients Market Asia-Pacific Footwear Market Global In-Vivo Imaging Market Global Food Grade Gases in Meat and Seafood Application Market Global Gaur Seed Market Global Perfusion Systems Market Global Rotomolding Market Asia-Pacific Food Bags Market Global Uveitis Drug Market Global Pet Oral Care Products Market Global Body Creams and Lotions Market Global Farber’s Disease Drug Market Asia-Pacific Laminated Busbar Market Middle East and Africa IoT Node and Gateway Market North America IoT Node and Gateway Market Global Contemporary Height-Adjustable Desk Market Global Silicone Adhesives Market Europe Potato Processing Market Global Regular Slotted Container Market Global Mine Ventilation System Market Global Polyphenylene Sulfide (PPS) Market Global Osteoarthritis Therapeutics Market Global Cloud Telephony Service Market Global Hair Straightener Market Asia-Pacific Weight Loss and Obesity Management Market Global Dermatitis Herpetiformis Treatment Market Global Rectal Catheters Market Asia-Pacific Network Test Lab Automation Market Global Digital Voice Recorder Market Global Filtration Cartridges Market Global Non Networked Sound Masking System Market Middle East and Africa Data Integration Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us: Data Bridge Market Research US: +1 614 591 3140 UK: +44 845 154 9652 APAC : +653 1251 975 Email:- [email protected]

"

0 notes

Text

Asia Pacific Battery Management System Market Report, Trends, Size, Share by 2025-2033

The Reports and Insights, a leading market research company, has recently releases report titled “Asia Pacific Battery Management System Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033.” The study provides a detailed analysis of the industry, including the Asia Pacific Battery Management System Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Asia Pacific Battery Management System Market Overview

The Asia Pacific battery management system market was valued at US$ 3.8 Billion in 2024 and is expected to register a CAGR of 19.8% over the forecast period and reach US$ 19.3 Billion in 2033.

Asia Pacific BMS Market for Battery is a part of electronics and energy industries that supply battery management systems the Asia Pacific BMS Market for Battery industry is heavily dependent on the development sector. A battery management system (BMS) is a technology that monitors, controls and manages the battery pack and battery cells. They are used to monitor the block battery or cell battery safety, error detection and overall optimal performance.

The Asia Pacific Battery Management System market is growing fast, due to adopting electric mobility and renewable energy solutions at a rapid rate in the region. China, Japan, South Korea, and India are the major contributors due to government rules to deploy clean energy systems and electric vehicles. The competition among the manufacturers for the EV battery market has pushed them to innovate productions like state-of-charge estimation, thermal management, and fault detection among others. The growth of industrial automation and consumer electronics sector also fuels the market growth.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2409

Asia Pacific Battery Management System Market Growth Factors & Challenges

The growth of the battery management system market in Asia Pacific is primarily attributed to the burgeoning demand for electric vehicles with incentives and regulations for lower carbon emissions. Progressive incorporation of large battery energies to integrate the intermittent renewable energy sources such as solar and wind technologies leads to augmenting the demand for advanced battery management systems. In addition, the development of battery technologies and the demand for better safety and operational efficiency across a range of applications is giving rise to uptake of smart BMS technologies.

The market has a bright future, but there are issues, including high costs linked to advanced battery management systems. These costs might restrict adoption, particularly in markets that are conscious of pricing. Diverse battery configurations and chemistries are creating technical complexities for integration. Moreover, and the lack of standards and interoperability between different BMS providers can slow down deployment and implementation. In addition, the market faces issues with supply chain disruptions as well as raw material price volatility.

Key suggestions for the report:

The Asia Pacific BMS market stationary battery segment is anticipated to hold the largest revenue share over the forecast period. These batteries are frequently utilized in grid-connected energy storage, commercial and residential systems, as well as off-grid applications like microgrids and telecom towers. The growth of the Market can be attributed to the large-scale energy storage projects and the growing focus energy management on energy efficiency in the various sectors.

The bonding wires segment is forecasted to show the greatest revenue share owing to its superior energy density, stability and life. As electric vehicles, storage of renewable energy and any consumer electronics depend heavily on the lithium-ion battery technology. Rising demand for them is due to their performance in high-demand applications such as electric aircraft and high-speed trains.

The market is led by centralized battery management systems because they are easy to integrate. Across industries, it will help better monitor and manage battery health and performance.

The telecom sector is expected to be the end user market for BMS as batteries provide important continuous power during operations. BMS technology has made it possible for telecom companies to lower their maintenance cost and enhance battery life as well as system reliability. As 5G becomes more common and more devices begin to be connected to the Internet, this demand is set to grow.

China, being the Asia Pacific country with a dominant market for BMS, generated wealth and displayed a high production volume. The demand for BMS in China has been accelerating because of its rapidly growing electronics manufacturing market and increasing energy storage demand.

The report presents information related to key drivers, restraints, and opportunities along with detailed analysis of the Asia Pacific Battery Management System market share.

Key Trends in Asia Pacific Battery Management System Industry

Emerging trends in the Asia Pacific Battery Management System Market are the use of artificial intelligence and machine learning algorithms to improve battery diagnostics and predictive maintenance capabilities. Manufacturers are resorting to wireless BMS solutions for easier installation and real-time monitoring as they develop solid-state batteries and next-generation chemistries, more advanced BMS designs are needed for new demands. Moreover, major automotive manufacturers, battery producers, and BMS developers are joining hands to innovate and reduce costs.

Asia Pacific Battery Management System Market Key Applications & Industry Segments

The Asia Pacific Battery Management System market is segmented by type, battery type, topology, end-user, and country.

By Type

Motive Battery

Stationary Battery

By Battery Type

Lithium-ion Batteries

Lead-acid Batteries

Nickel-based Batteries

Solid-State Batteries

Flow Batteries

By Topology

Centralized

Distributed

Modular

By End-User

Consumer Electronics/li>

Aerospace & Defense

Medical Devices

Telecommunication

Others

By Country

China

Japan

South Korea

India

Australia & New Zealand

Taiwan

Vietnam

Singapore

Rest of Asia Pacific

Leading Manufacturers in the Asia Pacific Battery Management System Market

Some of the key manufacturers which are included in the Asia Pacific Battery Management System market report are:

Sensata Technologies, Inc.

Analog Devices, Inc.

Renesas Electronics Corporation

Infineon Technologies AG

Maxwell Energy Services

Marelli Holdings Co., Ltd.

Eberspacher

Texas Instruments Incorporated

Panasonic Holdings Corporation

BMS PowerSafe

Key Attributes

Report Attributes

Details

No. of Pages

178

Market Forecast

2025-2033

Market Value (USD) in 2024

3.8 billion

Market Value (USD) in 2033

19.3 billion

Compound Annual Growth Rate (%)

19.8%

Regions Covered

Asia Pacific

View Full Report: https://www.reportsandinsights.com/report/asia-pacific-battery-management-system-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Asia Pacific Battery Management System Market share#Asia Pacific Battery Management System Market size#Asia Pacific Battery Management System Market trends

0 notes

Text

0 notes

Text

Global Data Concentrator Units (DCUs) Market | Key Trends, Emerging Opportunities, and Forecast to 2032

Global Data Concentrator Units (DCUs) Market size was valued at US$ 1.89 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 9.1% during the forecast period 2025-2032.

Data Concentrator Units are critical components in smart grid infrastructure that collect, process, and transmit data from multiple field devices to central management systems. These units serve as communication hubs between smart meters, sensors, and utility control centers, enabling real-time monitoring and advanced analytics. DCUs come in both wired (Ethernet, fiber optic) and wireless (RF, cellular) variants to accommodate diverse infrastructure requirements.

The market growth is driven by increasing investments in smart grid modernization, with utilities worldwide allocating over USD 300 billion annually for grid upgrades. However, cybersecurity concerns pose significant challenges to adoption rates. Major players like ZIV Automation and STMicroelectronics are addressing this through encrypted communication protocols, with recent product launches featuring advanced AES-256 encryption standards. The Asia-Pacific region currently leads market growth, accounting for 38% of global DCU deployments in 2023, fueled by China’s massive smart meter rollout program targeting 600 million installations by 2025.

Get Full Report with trend analysis, growth forecasts, and Future strategies : https://semiconductorinsight.com/report/global-data-concentrator-units-dcus-market/

Segment Analysis:

By Type

Wired DCUs Lead the Market Due to High Reliability in Industrial Applications

The global Data Concentrator Units (DCUs) market is segmented based on type into:

Wired DCUs

Subtypes: Ethernet-based, Serial Communication, and others

Wireless DCUs

Subtypes: Wi-Fi enabled, Cellular Network, and others

By Application

Smart Meter Management Dominates Due to Growing Smart Grid Deployments

The market is segmented based on application into:

Smart Meter Management

Network Monitoring

Powerline Communication Controller

Industrial Automation

Others

By End User

Utility Sector Accounts for Major DCU Adoption

The market is segmented based on end users into:

Utilities

Subtypes: Electricity, Water, Gas

Industrial

Commercial

Residential

By Technology

Advanced Metering Infrastructure (AMI) Integration Drives Market Growth

The market is segmented based on technology into:

Traditional DCUs

Advanced DCUs with IoT Capabilities

Cloud-connected DCUs

Edge Computing-enabled DCUs

Regional Analysis: Global Data Concentrator Units (DCUs) Market

North America The North American DCU market is characterized by advanced smart grid deployments and substantial investments in grid modernization. The U.S. leads with initiatives like the $3.5 billion Grid Resilience and Innovation Partnerships Program, driving demand for sophisticated DCUs that support bidirectional data flow and real-time monitoring. Canada follows closely, focusing on interoperability standards for microgrid applications. Regulatory pressures for AMI (Advanced Metering Infrastructure) adoption continue to push utilities toward high-performance DCU solutions, particularly in California and Texas where renewable integration is prioritized. Manufacturers like Curtiss-Wright and SCI Technology dominate with ruggedized units compliant with IEEE 1547-2018 standards.

Europe Europe’s DCU market thrives on stringent EU Directive 2019/944 mandates for smart meter rollouts, with countries like France and Spain targeting 100% penetration by 2027. The region shows strong preference for multi-protocol DCUs capable of handling DLMS/COSEM, IEC 61850, and Modbus communications. Germany’s E-Energy program has accelerated deployments of edge-computing enabled DCUs, while Nordic countries prioritize low-power wide-area network (LPWAN) compatible units. Environmental regulations favor energy-efficient designs, giving competitive edge to suppliers like Groupe Cahors and STMicroelectronics. However, complex certification processes and data privacy concerns under GDPR present adoption hurdles.

Asia-Pacific APAC represents the fastest-growing DCU market, projected to capture 42% of global share by 2027. China’s State Grid Corporation has deployed over 500 million smart meters, creating massive demand for DCUs with PLC (Power Line Communication) capabilities. India’s Revamped Distribution Sector Scheme (RDSS) allocates $40+ billion for smart grid components, spurring localization through players like Ami Tech India and Lekha. Japan and South Korea emphasize 5G-backhaul compatible DCUs for disaster-resilient grids. While cost sensitivity drives preference for wired solutions, wireless DCU adoption grows in Southeast Asia’s island grids. The region’s lack of unified standards, however, complicates cross-border interoperability.

South America Brazil dominates South America’s DCU market through its Energia + Program, with 30+ million smart meters slated for installation by 2031. Chilean utilities favor DCUs with dual SIM cellular connectivity for remote mining operations, while Argentina’s economic volatility constraints deployments to pilot projects. The region shows unique demand for anti-tampering DCUs due to high electricity theft rates. Though international players like ZIV Automation lead, local manufacturers are gaining traction through cost-optimized solutions. Infrastructure financing gaps and political instability remain key challenges, particularly in Andean nations.

Middle East & Africa MEA demonstrates divergent adoption patterns: Gulf Cooperation Council (GCC) countries deploy premium DCUs for smart cities like NEOM, while Sub-Saharan Africa relies on basic units for electrification projects. UAE’s DEWA has pioneered AI-integrated DCUs for predictive maintenance, whereas South Africa’s Eskom focuses on revenue protection features. North African utilities prefer French-standard compatible DCUs through partnerships with Groupe Cahors. Limited last-mile connectivity drives innovation in hybrid DCUs combining PLC and RF technologies. The region’s growth is tempered by budget constraints outside oil-rich economies and underdeveloped regulatory frameworks in emerging markets.

MARKET OPPORTUNITIES

Emerging Smart City Initiatives Create New Application Potential

Urban digital transformation projects worldwide are opening new possibilities for DCU applications beyond traditional utility networks. Smart city deployments increasingly incorporate DCUs for integrated management of street lighting, traffic systems, environmental sensors, and public infrastructure. This expansion into municipal applications provides growth avenues for DCU manufacturers to develop specialized solutions tailored to city management requirements.

The growing emphasis on data-driven decision making in urban planning further enhances the value proposition of advanced DCUs capable of processing and analyzing diverse data streams. Partnerships between technology providers and municipal authorities are expected to fuel innovation in this space, with pilot projects demonstrating the potential for DCUs to become fundamental components of comprehensive smart city ecosystems.

DATA CONCENTRATOR UNITS (DCUS) MARKET TRENDS

Smart Grid Modernization Driving Adoption of Advanced DCUs

The global push for smart grid modernization is significantly boosting demand for Data Concentrator Units (DCUs) as utilities seek more efficient ways to manage electricity distribution networks. DCUs serve as critical aggregation points for meter data collection in Advanced Metering Infrastructure (AMI) systems, with deployment rates increasing by approximately 18-22% annually in developed markets. Recent technological enhancements in DCUs include support for hybrid communication protocols (RF mesh, PLC, and cellular backhaul), enabling utilities to consolidate diverse meter populations into unified systems. This evolution aligns with global investments in smart grid infrastructure, estimated at $70 billion annually, where DCUs play a pivotal role in enabling real-time monitoring and demand response capabilities.

Other Trends

Edge Computing Integration

The integration of edge computing capabilities into DCUs represents a transformative shift, allowing localized data processing that reduces latency and bandwidth requirements. Modern DCUs now frequently incorporate processing power capable of running analytics algorithms at the network edge, with leading manufacturers embedding quad-core processors capable of handling over 50,000 meter endpoints. This trend responds to growing data volumes from smart meters, which generate 10-15 times more data points than traditional meters. Edge-enabled DCUs particularly benefit utilities managing large service territories, where centralized data processing would create unacceptable latency for time-sensitive applications like outage detection.

Cybersecurity as a Market Differentiator

With utilities facing increasing cyber threats, DCU manufacturers are emphasizing advanced security features as key competitive differentiators. Recent product launches showcase hardware-based security modules compliant with IEC 62351 standards, including secure boot mechanisms and encrypted communications that support AES-256 encryption. The market has seen a 40% increase in security-related DCU firmware updates since 2022, reflecting growing regulatory pressure from standards like NERC CIP. Furthermore, some manufacturers now offer over-the-air security patches, addressing vulnerabilities in deployed units without requiring physical access—a critical feature for utilities managing thousands of geographically dispersed DCUs.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Innovation Drive Market Competition

The global Data Concentrator Units (DCUs) market features a dynamic competitive landscape with both established players and emerging companies vying for market share. According to recent analysis, the market witnessed a valuation of $1.2 billion in 2023, with projected growth at a CAGR of 6.8% through 2030. This growth is fueled by increasing smart grid deployments and industrial automation.

ZIV Automation leads the market with its cutting-edge DCU solutions for energy utilities, capturing approximately 18% market share in 2023. The company’s dominance stems from its robust product portfolio and strategic acquisitions in Europe and Asia-Pacific. Meanwhile, STMicroelectronics has strengthened its position through innovative semiconductor solutions that enhance DCU performance in harsh industrial environments.

Asian manufacturers like Ami Tech India and Lekha are rapidly gaining traction, leveraging cost-competitive solutions tailored for developing markets. These players have collectively captured nearly 25% of the APAC market, challenging traditional Western manufacturers.

The competitive environment remains intense as companies focus on technological differentiation. Recent developments include Advanced Electronics Company’s launch of AI-powered DCUs with predictive maintenance capabilities and ASELSAN’s military-grade ruggedized units for defense applications.

List of Key Data Concentrator Unit Manufacturers

ZIV Automation (Spain)

Ami Tech India (India)

STMicroelectronics (Switzerland)

Advanced Electronics Company (Saudi Arabia)

Astronautics (U.S.)

Groupe Cahors (France)

SCI Technology (U.S.)

Curtiss-Wright (U.S.)

SANDS (South Korea)

ASELSAN (Turkey)

Nortex Technologies (Canada)

M B Control & Systems (U.A.E)

Learn more about Competitive Analysis, and Forecast of Global Data Concentrator Units (DCUs) Market : https://semiconductorinsight.com/download-sample-report/?product_id=95752

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Data Concentrator Units (DCUs) Market?

-> The global Data Concentrator Units (DCUs) market size was valued at US$ 1.89 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 9.1% during the forecast period 2025-2032.

Which key companies operate in Global DCUs Market?

-> Major players include ZIV Automation, STMicroelectronics, Advanced Electronics Company, ASELSAN, and Curtiss-Wright, collectively holding over 45% market share.

What are the key growth drivers?

-> Primary drivers include smart grid deployments (expected to grow at 12.3% CAGR), AMI adoption, and increasing investments in power infrastructure (USD 3.4 trillion projected by 2030).

Which region dominates the market?

-> Asia-Pacific accounts for 42% market share in 2024, while North America leads in technological innovation with 35% of patents.

What are the emerging trends?

-> Key trends include 5G-enabled DCUs, AI-powered predictive maintenance, and hybrid wired-wireless solutions gaining 28% adoption growth annually.

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 +91 8087992013 [email protected]

0 notes

Text

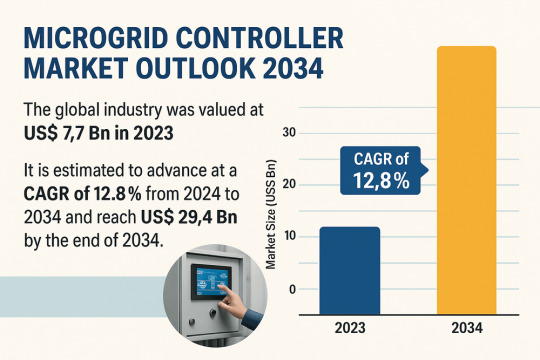

Global Microgrid Controller Market Set for 12.8% CAGR Growth Through 2034

The global microgrid controller market, valued at US$ 7.7 billion in 2023, is poised for robust growth over the next decade. Fueled by increasing government funding, rising demand for resilient power supply, and accelerated adoption of smart grid technologies, the market is projected to advance at a compound annual growth rate (CAGR) of 12.8% between 2024 and 2034, reaching US$ 29.4 billion by the close of 2034.

Market Overview

Microgrid controllers serve as the brain of microgrids localized energy systems that integrate distributed energy resources (DERs) such as solar panels, wind turbines, fuel cells, and energy storage systems. By continuously monitoring and optimizing power flows, controllers enable seamless switching between grid-connected and island modes, ensuring uninterrupted, high‑quality electricity for communities, campuses, military bases, and industrial parks. With advancements in digital communications and power electronics, modern controllers offer real‑time data analytics, predictive maintenance, and autonomous load‑shedding capabilities to enhance grid resilience and efficiency.

Market Drivers & Trends

Government Funding for Microgrid Development

Incentives and grants: Various governments are allocating significant budgets to pilot microgrid projects in remote and disaster-prone regions. For example, Australia’s Regional Australia Microgrid Pilots Program (RAMPP) launched in September 2021 earmarked funds to improve resilience in regional communities over six years.

Policy support: Electrification goals in India, China, and Southeast Asia have spurred nationwide rural electrification programs, with microgrid controllers playing a pivotal role in off-grid villages.

Adoption of Grid‑Connected Smart Controllers

Cost-effectiveness: Homeowners and small businesses increasingly favor grid‑tied microgrid controllers that balance self‑generation with utility draw, reducing energy bills and carbon footprints.

Community-scale projects: Collaborations like SunPower Corp., Schneider Electric, Southern California Edison, and KB Home’s Energy‑Smart Connected Communities in Menifee, California demonstrate scalable models for solar‑plus‑storage microgrids serving over 200 all‑electric homes.

Technological Advancements

AI and machine learning: Integration of advanced algorithms enables predictive load forecasting and autonomous fault detection, minimizing downtime.

Interoperability standards: Initiatives such as IEEE 2030.7 and IEC 61850 are fostering harmonized communication protocols, streamlining controller integration with diverse DER assets.

Latest Market Trends

Hybrid Microgrid Solutions: There is a growing preference for hybrid systems that combine renewable generation, diesel generators, and battery storage to guarantee reliability under all conditions.

DC‑Coupled Microgrids: Direct Current (DC) microgrids—championed by ABB’s investment in Direct Energy Partners—offer higher efficiency by minimizing conversion losses and simplifying integration of DC‑centric loads and DERs.

Edge Computing: Controllers with embedded edge‑computing capabilities enable decentralized decision-making, reducing latency and enhancing cybersecurity by keeping critical controls within the local network.

Download now to explore primary insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=66941

Key Players and Industry Leaders

ABB

AutoGrid Systems, Inc.

Caterpillar

Cummins Inc.

Eaton

Emerson Electric Co

Encorp Powertrans

General Electric Company

Hitachi Energy Ltd.

Honeywell International Inc.

Power Analytics Corporation

S&C Electric Company

Schneider Electric

Schweitzer Engineering Laboratories, Inc.

Siemens

Recent Developments

March 2023: ABB’s minority stake in Direct Energy Partners via ABB Technology Ventures accelerates development of DC microgrid solutions.

March 2023: Siemens Canada and Humber College inaugurate the SMART Lab, providing a real‑world testing ground for microgrid technologies and workforce training.

2024: Schneider Electric rolled out its X-Web control platform, which integrates predictive analytics and cybersecurity features for commercial microgrids.

Early 2025: AutoGrid Systems launched a SaaS‑based microgrid orchestration service, enabling remote monitoring and dynamic resource optimization for campus‑scale installations.

Market Opportunities and Challenges

Opportunities

Electrification of Remote Regions: UN Sustainable Development Goals and national rural electrification targets present vast untapped markets in Africa, Latin America, and Southeast Asia.

Corporate Sustainability Initiatives: Corporations targeting net-zero emissions are investing in on‑site microgrids to reduce Scope 2 emissions and ensure business continuity.

Resilience‑Driven Reconstruction: Post‑disaster rebuilding efforts in hurricanes‑ and wildfire‑affected zones in North America offer opportunities for rapid microgrid deployment.

Challenges

Regulatory Fragmentation: Divergent standards and interconnection requirements across jurisdictions complicate global product roll-outs.

High Capital Expenditure: Upfront costs of controller hardware, integration, and commissioning can deter smaller end users without financing support.

Cybersecurity Risks: As controllers become more connected, they face heightened threats from digital adversaries, necessitating continuous software updates and secure design practices.

Future Outlook

Analysts anticipate that ongoing declines in solar photovoltaic and battery storage costs will further boost controller adoption, particularly in hybrid configurations. The convergence of microgrids with electric vehicle (EV) charging networks and demand response programs is expected to unlock additional revenue streams. By 2034, enhanced interoperability, AI-driven autonomy, and modular hardware designs will drive market maturation, enabling plug‑and‑play deployments across residential, commercial, military, and utility segments.

Market Segmentation

By Offering

Hardware

Software

Connectivity (On‑grid, Off‑grid)

By End‑User

Utilities

Renewable Energy Companies

Traditional Energy Providers

Commercial & Industrial Facilities

Military & Defense

Healthcare

Others (Automotive, Transportation, Telecommunications)

By Geography

North America (U.S., Canada)

Europe (Germany, U.K., France, Italy, Spain)

Asia Pacific (China, India, Japan, South Korea, ASEAN)

Middle East & Africa (GCC, South Africa)

South America (Brazil, Argentina)

Regional Insights

Asia Pacific: Held the largest market share in 2023, driven by aggressive rural electrification, expansion of industrial parks, and government incentives in India and China.

North America: Rapid integration of smart grid initiatives, electrification of remote communities, and resilience programs post‑natural disasters have spurred steady growth.

Europe: Strong renewable mandates and EU funding for microgrid pilots under Horizon Europe have catalyzed projects in France, Germany, and the U.K.

Middle East & Africa: Off‑grid microgrid projects in GCC countries and Sub‑Saharan Africa address both energy access and power quality challenges.

South America: Brazil’s Amazon‑region pilot microgrids and Argentina’s Patagonia installations highlight growing interest in off‑grid solutions.

Why Buy This Report?

Comprehensive Analysis: Detailed market size, forecast, and growth drivers for 2024–2034.

Competitive Landscape: In‑depth profiles of 15+ key players, including recent strategic moves and financials.

Segment & Regional Breakdowns: Quantitative and qualitative insights across offerings, end‑users, and geographies.

Strategic Frameworks: Porter’s Five Forces, value chain, and trend analyses to inform market entry and investment decisions.

Data‑Rich Deliverables: Electronic PDF and editable Excel files containing historical data (2020–2022) and projections.

Explore Latest Research Reports by Transparency Market Research:

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Quantum Dot Sensor Market: https://www.transparencymarketresearch.com/quantum-dot-sensor-market.html

High Power RF Amplifier Module Market: https://www.transparencymarketresearch.com/high-power-rf-amplifier-module-market.html

3D Sensing Technology Market: https://www.transparencymarketresearch.com/3d-sensing-technology-market.html About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Microgrid Controller Market by Connectivity (Grid-connected, Off-grid), Offering (Hardware, Software & Services), End User (Commercial & Industrial, Military, Government, Institutes & Campuses, Healthcare) and Region

0 notes

Text

The Microgrid as a Service Market’s Growth Trajectory: Competitive Strategies and Future Projections (2025-2032)

A new qualitative research report from Fortune Business Insights (2025-2032) offers a comprehensive analysis of the Microgrid as a Service Market trend. This report is designed to provide industry leaders, investors, and decision-makers with data-driven insights for strategic planning and informed decision-making.

The global microgrid as a service market size was valued at USD 3.33 billion in 2024 and is projected to grow from USD 3.83 billion in 2025 to USD 9.35 billion by 2032, exhibiting a CAGR of 13.61% during the forecast period. Asia Pacific dominated the global market with a share of 40.54% in 2024. The Microgrid as a service market in the U.S. is projected to grow significantly, reaching an estimated value of USD 2.58 billion by 2032.

Key Highlights of the Microgrid as a Service Market Report:

Market Overview: The report provides a deep dive into key market trends, drivers, and challenges, along with a detailed analysis of market size, revenue, production, and Compound Annual Growth Rate (CAGR) using validated methodologies for accuracy.

Growth Projections: The Microgrid as a Service Market is projected to experience substantial growth from 2025 to 2032, with major players increasingly adopting strategic initiatives to drive expansion.

Competitive Landscape:

Detailed profiling of top companies, including financials (gross profit, sales volume, revenue, manufacturing costs), product benchmarking, and SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis.

Competitive analysis covers global players' revenue and sales volume rankings, average price by company, manufacturing base distribution, headquarters, product offerings, and strategic developments such as mergers, acquisitions, and expansions.

The report identifies key industry players, their innovations, and business strategies, highlighting the most promising long-term growth opportunities and advancements in processes and product development.

Get a Free Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/109975

Market Segmentation: Comprehensive segmentation by product type, application, end-user, region, and key competitors to identify market opportunities.

By Service Type:

Engineering & Design

Monitoring & Control

By Application:

Remote Areas

Industrial

By Region:

North America, Europe, Asia-Pacific

Geographical Analysis: Expert analysis of the Microgrid as a Service Market across key regions:

North America (U.S., Canada, Mexico)

Europe (Germany, U.K., France, Russia, Italy, Spain)

Asia-Pacific (China, India, Japan, Australia, Singapore, NZ)

South America (Argentina, Brazil)

Middle East & Africa (Saudi Arabia, Turkey, UAE, Africa)

Drivers and Trends: Discusses factors driving and restraining market growth, their impact on demand, emerging trends, challenges, limitations, and growth opportunities. It provides a forward-looking perspective on factors expected to boost overall market growth.

Research Methodology: Employs a robust methodology involving primary research (interviews with market influencers) and secondary research to provide accurate market predictions and insights into supply-demand dynamics.

Key Opportunities and Benefits: Identifies key opportunities, analyzes factors driving industry growth, and considers past development patterns and future trends. Benefits include quantitative analysis of market segments, Porter's Five Forces analysis for strategic decision-making, revenue mapping, and benchmarking of market players.

Actionable Insights: Delivers actionable insights derived from secondary research, direct stakeholder interviews, and expert validation leveraging Fortune Business Insights' extensive regional database.

This report serves as a crucial resource for businesses seeking to make informed, strategic moves by understanding technological innovations, pricing trends, consumer behavior, and investment potential within the Microgrid as a Service Market.

Get More Info: https://www.fortunebusinessinsights.com/microgrid-as-a-service-market-109975

About Us:

Fortune Business InsightsTM offers expert corporate analysis and accurate data, helping organizations of all sizes make timely decisions. We tailor innovative solutions for our clients, assisting them to address challenges distinct to their businesses. Our goal is to empower our clients with holistic market intelligence, giving a granular overview of the market they are operating in.

0 notes

Link

0 notes

Text

Low Voltage Cable Market Drivers Fueling Demand Across Infrastructure and Energy Sectors

The low voltage cable market is witnessing strong growth worldwide, powered by a combination of infrastructure development, renewable energy deployment, and industrial automation. These cables are essential in transmitting electricity at voltages up to 1,000 volts and are widely used in residential, commercial, and industrial applications. As global economies prioritize electrification and energy efficiency, the demand for reliable low voltage power distribution is intensifying.

Infrastructure Development Fuels Core Demand

One of the most prominent growth drivers for the low voltage cable market is the boom in infrastructure development. Countries across Asia-Pacific, Latin America, and the Middle East are investing heavily in housing, commercial spaces, smart cities, and transportation networks. These projects require robust electrical wiring systems, where low voltage cables serve as the backbone for lighting, HVAC, power sockets, and communication systems.

Urbanization trends are also fueling the demand for sustainable and energy-efficient buildings, further reinforcing the role of advanced low voltage cabling systems.

Renewable Energy Projects Accelerate Cable Usage

The shift towards renewable energy sources such as solar and wind is a major contributor to market growth. Solar photovoltaic (PV) farms and wind energy installations require extensive cabling networks to connect panels, turbines, inverters, and transformers. Low voltage cables are used extensively within renewable installations to manage internal electrical distribution, ensure safety, and support long-term reliability.

As governments ramp up their renewable capacity to meet climate targets, the need for specialized, weather-resistant low voltage cables is rising. Their role in low-voltage connections, including grounding and control wiring, makes them indispensable in energy transitions.

Electrification of Industrial Operations

Industries around the world are transitioning to electric-powered equipment and automated systems, replacing older mechanical and hydraulic systems. Manufacturing, oil and gas, mining, and processing sectors are implementing digital control systems and robotics, all of which require consistent low voltage power.

The use of low voltage cables in connecting machinery, sensors, and automation infrastructure ensures safe, uninterrupted operations. Additionally, the shift towards Industry 4.0 is bringing more data and control cables into industrial environments, expanding the application of low voltage cabling even further.

Regulatory Push for Safety and Efficiency

Governments and regulatory bodies are implementing stricter safety codes and energy efficiency standards for electrical installations. These mandates are pushing builders and engineers to use cables that meet fire-resistance, halogen-free, and low-smoke emission requirements. The demand for low voltage cables that comply with international certifications such as IEC, UL, and RoHS is on the rise.

As a result, manufacturers are developing eco-friendly and durable cable solutions that reduce power loss and environmental hazards. This aligns well with broader ESG (Environmental, Social, Governance) goals in the construction and manufacturing sectors.

Rural Electrification and Energy Access Initiatives

Electrification in remote and underserved areas is another area driving the adoption of low voltage cables. Governments, NGOs, and energy companies are rolling out grid extension programs and decentralized energy systems like solar microgrids. These initiatives depend on low voltage distribution networks for last-mile connectivity and power delivery in rural households.

Regions in Africa, Southeast Asia, and Latin America are especially active in such programs, with low voltage cable providers seeing a consistent rise in demand from these markets.

Smart Grids and Advanced Distribution Networks

The modernization of power grids into “smart” systems is another driver fueling the low voltage cable market. Smart grids rely on real-time communication, data analysis, and control systems to optimize energy flow and improve reliability. Low voltage cables are critical to connecting smart meters, control units, and distributed energy resources within these networks.

Advanced cable designs with integrated data transmission and increased shielding are gaining traction to support the digital needs of future power grids.

Technological Advancements in Cable Materials and Design

Innovation in cable materials, insulation, and design is expanding the application scope of low voltage cables. Cross-linked polyethylene (XLPE) insulation, thermoplastic compounds, and improved shielding technologies are making cables more efficient, flexible, and resistant to heat and moisture.

New manufacturing techniques are allowing cables to be lighter, more compact, and easier to install—meeting the evolving needs of contractors and system integrators across sectors.

Conclusion

The low voltage cable market is on a steady upward trajectory, driven by critical trends such as infrastructure expansion, renewable energy development, rural electrification, and the evolution of smart grids. As end-users seek safer, more efficient, and environmentally sound solutions, the demand for advanced low voltage cabling systems is expected to continue growing. Stakeholders investing in innovation, regulatory compliance, and diversified applications will be well-positioned to capitalize on these powerful market drivers.

0 notes

Text

0 notes

Text

Solar PV Inverters Market Drivers Push Equipment Demand Amid Infrastructure Boom Worldwide

As global infrastructure initiatives gain momentum, the Solar PV Inverters Market Trends are seeing significant uplift due to powerful market drivers. These catalysts are transforming how solar inverters are designed, integrated, and deployed across energy projects. From utility-scale solar plants to rooftop systems, increased demand for efficient, reliable, and grid-supportive inverters is being observed across both developed and emerging economies.

Infrastructure Boom: The Primary Catalyst

Worldwide, countries are making large-scale investments in infrastructure, particularly in clean energy. Nations like India, China, the United States, and several European Union members are driving major renewable energy projects to meet climate targets. This construction surge has directly influenced the demand for solar PV inverters as they are essential in converting DC power from solar panels into usable AC power for the grid. Governments are emphasizing decarbonization through solar energy, further propelling demand.

Additionally, the rollout of national electrification programs in Africa and Southeast Asia is expanding off-grid and microgrid applications. These setups rely heavily on string and central inverters, contributing to a healthy global demand.

Decentralization and the Rise of Rooftop Installations

Residential and commercial buildings are increasingly adopting rooftop solar solutions. As more prosumers seek energy independence and cost savings, there's a push for decentralized energy models. This shift supports the growth of single-phase and three-phase inverters suited for distributed energy systems. These compact and efficient inverters also offer greater flexibility for integration with battery energy storage systems (BESS).

In developed markets, policies like net metering and tax credits have further incentivized residential and small business owners to invest in solar, increasing the demand for high-efficiency inverters with smart features and grid support capabilities.

Grid Modernization and Smart Inverter Technologies

One of the strongest drivers reshaping the market is the global trend toward grid modernization. Smart grids need smart inverters—devices capable of voltage regulation, frequency control, reactive power compensation, and communication with the grid. These features not only stabilize the grid but also enable renewable penetration to rise without jeopardizing reliability.

Grid-forming inverters are becoming particularly vital in renewable-dominated energy systems. The push for inverters with advanced functionalities stems from their ability to offer grid support, helping utilities transition from traditional synchronous generation to inverter-based resources.

Demand for Energy Resilience and Storage Integration

Natural disasters, power outages, and rising energy prices are prompting industries and governments to improve grid resilience. Solar PV systems integrated with energy storage solutions are now considered essential infrastructure in regions prone to weather disruptions. Inverters that can seamlessly interact with batteries, manage peak loads, and operate during grid failures (islanding mode) are gaining traction.

This trend is especially visible in regions like California and Australia, where frequent blackouts and grid instability have encouraged users to adopt hybrid inverters with robust backup and storage capabilities.

Industrial Growth and Utility-Scale Solar Expansion