#Solar Encapsulation Market Revenue

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile Tumblr US users spend an average of 4.04 minutes per session on the app.

Text

Solar Encapsulation Market Size, Trends, Growth and Analysis 2034

Global solar encapsulation plays a vital role in enhancing the durability, efficiency, and performance of solar photovoltaic (PV) modules. Encapsulation involves using protective materials, typically ethylene-vinyl acetate (EVA), polyvinyl butyral (PVB), or thermoplastic polyolefin (TPO), to safeguard solar cells from environmental factors such as moisture, UV radiation, and mechanical damage. This protective layer not only increases the lifespan of solar panels but also ensures consistent energy output over time. These encapsulation materials are critical for maintaining the structural integrity and electrical performance of solar modules throughout their operational life. These materials contribute significantly to the reliability and the long-term sustainability of solar power systems across the whole globe.

According to SPER Market Research, “Global Solar Encapsulation Market Growth, Size, Trends Analysis - By Material, By Technology, By Application - Regional Outlook, Competitive Strategies and Segment Forecast to 2034” states that Global Solar Encapsulation Market is estimated to reach 11.72 USD billion by 2034 with a CAGR of 8.26%.

Drivers:

One of the main developments in the solar encapsulation industry is the worldwide movement towards renewable energy, particularly solar electricity. The market for solar power is growing quickly as long as businesses continue to prioritize investments in renewable energy. EVA (ethylene vinyl acetate) sheets and other solar encapsulants are essential for shielding solar cells from mechanical stress, moisture, and ultraviolet light. The expansion of the solar encapsulation market is also being driven by advancements in the manufacture of solar modules, such as bifacial and high-efficiency solar cells. These increase solar panels' longevity and energy yield, which necessitates the use of encapsulants that can withstand greater temperatures and exposure to UV light.

Request a Free Sample Report: https://www.sperresearch.com/report-store/solar-encapsulation-market?sample=1

Restraints: Solar PV recycling is rather complicated. In terms of size, technology, composition, and condition, the EoL solar PV module flow is not uniform. Furthermore, current solar PV panels were not made to be recycled; performance and durability criteria have resulted in sandwich-like, sealed, and encapsulated constructions that make it challenging to separate the constituent parts. During recycling, solar encapsulating materials like polyvinyl butyral (PVB) and ethylene-vinyl acetate (EVA) can be challenging to separate. It is more difficult to separate and recover these materials since they are made to be strong and resilient to environmental influences. Long-term exposure to sunlight and other environmental conditions can cause encapsulation materials to deteriorate over time. China held the biggest revenue share in the Global Solar Encapsulation Market. This dominance is driven by factors such as substantial investment in renewable energy and the presence of leading solar panel manufacturers. Focus on infrastructure development and increasing infrastructure projects also contributes to the growing demand for solar encapsulation materials. Some of the key market players are First Solar, H.B. Fuller Company, Dow, DuPont, Exxon Mobil Corporation and LG Chem.

For More Information, refer to below link: –

Solar Encapsulation Market Share

Related Reports:

Crystalline Solar PV Backsheet Market Growth

Electrical Conduit Market Growth

Follow Us –

LinkedIn | Instagram | Facebook | Twitter

Contact Us:

Sara Lopes, Business Consultant — USA

SPER Market Research

+1–347–460–2899

#Solar Encapsulation Market#Solar Encapsulation Market Growth#Solar Encapsulation Market Share#Solar Encapsulation Market Size#Solar Encapsulation Market Revenue#Solar Encapsulation Market Demand#Solar Encapsulation Market Analysis#Solar Encapsulation Market Segmentation#Solar Encapsulation Market Future Outlook#Solar Encapsulation Market Scope#Solar Encapsulation Market Challenges#Solar Encapsulation Market Competition#Solar Encapsulation Market forecast#solarencapsulation#solarindustry#solarenergy#sustainability

0 notes

Text

M-Toluidine Market Growth Analysis 2025

The global M-Toluidine market was valued at US$ 44.28 million in 2023 and is anticipated to reach US$ 52.43 million by 2030, witnessing a CAGR of 3.57% during the forecast period 2024-2030.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/414/m-toluidine-market

Europe market for M-Toluidine is estimated to increase from $ 10.01 million in 2023 to reach $ 11.96 million by 2030, at a CAGR of 2.14% during the forecast period of 2024 through 2030.

China market for M-Toluidine is estimated to increase from $ 23.23 million in 2023 to reach $ 25.82 million by 2030, at a CAGR of 4.87 % during the forecast period of 2024 through 2030.

M-Toluidine, also known as meta-toluidine, is an aromatic amine compound with the chemical formula C7H9N. It is a colorless liquid with a pungent odor and is used in a variety of industrial and chemical applications, including the production of dyes, pesticides, pharmaceuticals, and other organic compounds.

The major global manufacturers of M-Toluidine include Lanxess, Deepak Nitrite, Aarti Industries, Jiangsu Huaihe Chemicals, Shandong Tsaker Dongao Chemical, Hubei Kecy Chemical, Jiangsu John Kei Chemical, etc. in 2023, the world's top three vendors accounted for approximately 45.18% of the revenue.

This report aims to provide a comprehensive presentation of the global market for M-Toluidine, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding M-Toluidine.

The M-Toluidine market size, estimations, and forecasts are provided in terms of output/shipments (K MT) and revenue ($ millions), considering 2023 as the base year, with history and forecast data for the period from 2019 to 2030. This report segments the global M-Toluidine market comprehensively. Regional market sizes, concerning products by Type, by Application, and by players, are also provided.

For a more in-depth understanding of the market, the report provides profiles of the competitive landscape, key competitors, and their respective market ranks. The report also discusses technological trends and new product developments.

The report will help the M-Toluidine manufacturers, new entrants, and industry chain related companies in this market with information on the revenues, production, and average price for the overall market and the sub-segments across the different segments, by company, by Type, by Application, and by regions.

Market Segmentation By Company

Lanxess

Deepak Nitrite

Aarti Industries

Jiangsu Huaihe Chemicals

Shandong Tsaker Dongao Chemical

Hubei Kecy Chemical

Jiangsu John Kei Chemical

Segment by Type

Pharmaceutical Grade

Industrial Grade

Others

Segment by Application

Dye Intermediate

Pesticide Intermediate

Pharmaceutical Intermediate

Others

Production by Region

Europe

China

India

Consumption by Region

Europe

Germany

France

U.K.

Italy

Russia

Rest of Europe

Asia

China

India

Drivers

Rising Demand in Packaging ApplicationsEBA copolymers are widely used in the packaging industry due to their excellent flexibility, impact resistance, and sealing properties. With the growing demand for flexible and durable packaging solutions, especially in the food and beverage sector, the market for EBA is expanding.

Growing Use in Construction and Building MaterialsEBA’s strong adhesive properties and chemical resistance make it an essential material in construction, particularly for adhesives, sealants, and waterproofing membranes. The increasing focus on infrastructure development globally is driving its adoption in this sector.

Surge in Renewable Energy ApplicationsEBA is used as an encapsulant material in photovoltaic (PV) solar modules due to its durability and resistance to environmental factors. The global shift towards renewable energy sources has boosted the demand for solar energy, creating a significant market for EBA.

Versatility in Polymer ModificationEBA copolymers are increasingly used as modifiers to enhance the flexibility, toughness, and impact strength of other polymers, such as polyolefins. This versatility has driven its adoption across various industries, including automotive and electronics.

Environmental Advantages over Traditional PolymersEBA copolymers exhibit better recyclability and lower emissions during production compared to other polymers. This aligns with global initiatives to adopt eco-friendly materials, further enhancing market growth.

Increased Demand for High-Performance AdhesivesEBA copolymers are gaining traction in the adhesives industry due to their strong adhesion to a wide range of substrates. Their application in industries such as automotive, electronics, and consumer goods is contributing to market growth.

Restraints

Fluctuating Raw Material PricesThe production of EBA relies on ethylene and butyl acrylate, both of which are derived from crude oil and natural gas. Price volatility in these raw materials can impact production costs and market stability.

Competition from Alternative MaterialsEBA faces competition from other copolymers and resins, such as ethylene-vinyl acetate (EVA) and low-density polyethylene (LDPE), which may offer similar properties at a lower cost. This competition could limit its market growth in price-sensitive applications.

Regulatory ChallengesThe production and use of acrylates are subject to stringent environmental regulations due to potential health and safety concerns. Compliance with these regulations can increase production costs and complicate market entry.

Limited Awareness in Emerging MarketsIn some developing regions, the benefits and applications of EBA copolymers are not well-known, limiting their adoption in industries that could otherwise benefit from their properties.

Opportunities

Expansion in Emerging EconomiesRapid industrialization and urbanization in regions like Asia-Pacific, Latin America, and Africa present untapped opportunities for EBA applications in packaging, construction, and energy sectors.

Innovation in Renewable Energy ApplicationsWith increasing investment in renewable energy, there is significant potential for EBA as a critical material in solar panel encapsulation. Continuous advancements in solar technology could further boost its demand.

Development of Bio-Based EBAThe development of bio-based EBA copolymers can address environmental concerns associated with petrochemical-based production. Bio-based variants can open new avenues for growth, particularly among eco-conscious consumers and industries.

Growing Automotive IndustryThe use of EBA as a modifier for polymers in automotive applications, such as bumpers, interior components, and protective coatings, is expanding. With the growth of electric vehicles (EVs), the demand for lightweight and durable materials is expected to rise.

Increased Focus on Sustainable PackagingAs industries prioritize sustainable packaging solutions, EBA’s recyclable properties make it an attractive material. Innovations in flexible packaging designs and eco-friendly laminates provide opportunities for market expansion.

Advancements in Polymer Blending TechnologiesNew blending technologies that enhance the performance characteristics of EBA copolymers are creating opportunities for their application in high-performance products across multiple industries.

Challenges

Technological Barriers to AdoptionSome industries may face challenges in adapting their production processes to utilize EBA copolymers effectively, especially in regions lacking advanced manufacturing infrastructure.

Environmental Concerns Related to AcrylatesDespite being more sustainable than some alternatives, the environmental impact of butyl acrylate production and its potential emissions remain concerns for stakeholders advocating for stricter regulations.

Economic Instability in Key MarketsEconomic fluctuations in regions heavily dependent on industries like construction or automotive could impact the demand for EBA copolymers, leading to market uncertainties.

High Initial Costs for AdoptionThe transition from traditional materials to EBA copolymers may involve higher upfront costs for manufacturers, including equipment upgrades and process modifications, deterring some potential adopters.

Competition from Emerging AlternativesWith the rise of new materials and polymers offering similar or superior properties, maintaining a competitive edge will require continuous innovation and marketing efforts.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/414/m-toluidine-market

https://imimmigrant.ca//read-blog/13764

https://imimmigrant.ca//read-blog/13765

https://imimmigrant.ca//read-blog/13767

https://imimmigrant.ca//read-blog/13768

0 notes

Text

0 notes

Text

Low Viscosity Epoxy Resin Market Price, Sales Volume, Demand and Revenue Report by 2032

Low Viscosity Epoxy Resin Market Overview

The Low Viscosity Epoxy Resin Market is experiencing growth due to its wide range of applications across various industries, including automotive, aerospace, construction, electronics, and marine. Low viscosity epoxy resins are known for their ease of application, excellent wetting properties, and ability to penetrate intricate molds and surfaces, making them highly desirable in both industrial and consumer applications.

The Low Viscosity Epoxy Resin Market was valued at USD 8.17 billion in 2023. It is projected to grow from USD 8.75 billion in 2024 to approximately USD 15.2 billion by 2032. The market is expected to expand at a Compound Annual Growth Rate (CAGR) of 7.14% during the forecast period from 2024 to 2032.

Drivers

Increasing Demand in Electronics and Electrical Applications: Low viscosity epoxy resins are used extensively in electronics and electrical components for encapsulation, insulation, and as adhesive materials. The rise in electronic devices and advancements in technology are driving the demand for these resins.

Download Report Sample Copy of Low Viscosity Epoxy Resin Market

Growth in Automotive and Aerospace Industries: The automotive and aerospace sectors are incorporating low viscosity epoxy resins for lightweight, high-strength composite materials and repair applications. Their properties enhance the performance and longevity of components in these high-demand industries.

Advancements in Composite Materials: Low viscosity epoxy resins are critical in the production of advanced composite materials used in sports equipment, construction materials, and wind turbine blades. The growth in these sectors fuels the demand for these resins.

Construction and Infrastructure Development: With increased infrastructure development globally, low viscosity epoxy resins are used in coatings, adhesives, and repair materials due to their durability and resistance to environmental factors.

Challenges

High Raw Material Costs: The cost of raw materials for producing low viscosity epoxy resins can be high, which impacts the overall cost of the end products. Fluctuations in prices of chemicals and resins can affect market stability.

Read Full Report Summary Click Here: Global Low Viscosity Epoxy Resin Market

Key Companies Profiled

JLM Industries Inc. ,Shandong Jufeng Chemical Co. Ltd ,Nanjing Tianfu Chemical Co. Ltd ,AOC RESINS Inc. ,Evonik Industries AG. ,Solvay S.A. ,PPG Industries, Inc. ,Kyocera Chemical Corporation ,BIP Chemicals Ltd ,DIC Corporation ,Hexion Inc. ,Huntsman Corporation ,Kukdo Chemical Co., Ltd. ,Chang Chun Group Co., Ltd

Environmental and Health Concerns: There are concerns about the environmental impact and health risks associated with epoxy resins, including issues related to VOCs (Volatile Organic Compounds) and the potential for hazardous emissions during curing. Regulatory pressures are increasing to address these concerns.

Competition from Alternative Materials: The market faces competition from alternative materials like polyurethanes and silicones, which can offer similar or enhanced performance characteristics in certain applications.

Opportunities

Growth in Renewable Energy Sector: The expansion of the renewable energy sector, particularly wind and solar power, presents opportunities for low viscosity epoxy resins in the manufacturing of turbine blades and solar panels.

Innovation in Epoxy Resin Formulations: Ongoing research and development in epoxy resin formulations aim to enhance performance characteristics, such as reducing curing times, improving mechanical properties, and developing eco-friendly variants. These innovations can open new market opportunities.

Emerging Markets: Rapid industrialization and infrastructure development in emerging markets, especially in Asia-Pacific and Latin America, provide growth opportunities for the low viscosity epoxy resin market.

Key Applications

Automotive: Used in automotive repair and manufacturing for bonding, coating, and sealing applications.

Aerospace: Employed in aerospace components for lightweight, high-strength composites and structural adhesives.

Electronics: Utilized in encapsulation, potting, and insulation of electronic components and circuit boards.

Construction: Applied in coatings, adhesives, and repair materials for both residential and commercial construction.

Marine: Used in marine applications for coatings and repairs due to its resistance to water and harsh environmental conditions.

addressing environmental concerns are well-positioned to capitalize on the market's growth opportunities.

Browse Related Report:

Silver Solder Paste Market -Global Silver Solder Paste Market and Forecast 2024-2032

Ceramic Zirconia Ferrule Market -Global Ceramic Zirconia Ferrule Market and Forecast 2024-2032

0 notes

Text

Global Top 5 Companies Accounted for 85% of total PV Modules market (QYResearch, 2021)

An encapsulant is used to provide adhesion between the solar cells, the top surface and the rear surface of the PV module. The encapsulant should be stable at elevated temperatures and high UV exposure. It should also be optically transparent and should have a low thermal resistance. EVA (ethyl vinyl acetate) is the most commonly used encapsulant material. EVA comes in thin sheets which are inserted between the solar cells and the top surface and the rear surface. This sandwich is then heated to 150 °C to polymerize the EVA and bond the module together.

Encapsulant materials used in photovoltaic (PV) modules serve multiple purposes; it provides optical coupling of PV cells and protection against environmental stress. Polymers must perform these functions under prolonged periods of high temperature, humidity, and UV radiation. When PV panels were first developed in the 1960s and the 1970s, the dominant encapsulants were based on polydimethyl siloxane (PDMS). Ethylene-co-vinyl acetate (EVA) is currently the dominant encapsulant chosen for PV applications, not because it has the best combination of properties, but because it is an economical option with an established history of acceptable durability. Getting new products onto the market is challenging because there is no room for dramatic improvements, and one must balance the initial cost and performance with the unknowns of long-term service life. Recently, there has been renewed interest in using alternative encapsulant materials with some significant manufacturers switching from EVA to polyolefin elastomer-based (POE) alternatives.

According to the new market research report “Global PV Modules Market Report 2023-2029”, published by QYResearch, the global PV Modules market size is projected to reach USD 7.38 billion by 2029, at a CAGR of 11.2% during the forecast period.

Figure. Global PV Modules Market Size (US$ Million), 2018-2029

Figure. Global PV Modules Top 5 Players Ranking and Market Share(Based on data of 2021, Continually updated)

The global key manufacturers of PV Modules include First, Sveck, HIUV, Bbetter, Cybrid Technologies, 3M, Hanwha, Lucent CleanEnergy, Vishakha Renewables, Tianyang, etc. In 2021, the global top five players had a share approximately 85.0% in terms of revenue.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

For more information, please contact the following e-mail address:

Email: [email protected]

Website: https://www.qyresearch.com

0 notes

Text

U.S. Solar Films Market Expansion: Exploring Market Penetration and Regional Opportunities

The U.S. solar films market size is anticipated to reach USD 1,404.5 million by 2030, growing at a CAGR of 6.3% from 2023 to 2030, according to a new report by Grand View Research, Inc. The U.S. market has increasing adoption of solar films across various industries and applications, including residential, commercial, and industrial sectors. This expansion is propelled by the growing awareness of renewable energy's significance in reducing carbon emissions and addressing climate change. In addition, favorable government incentives and policies, such as tax credits and rebates, continue to incentivize solar energy adoption, making solar films an attractive investment. Technological advancements in solar film materials and manufacturing processes have also improved efficiency and reduced costs, making them more accessible to a wider range of consumers. Furthermore, heightened environmental concerns, coupled with the desire to reduce energy costs and enhance energy security, are further propelling the adoption of solar films in the U.S. These factors collectively contribute to the robust and sustainable growth of the market.

U.S. Solar Films Market Report Highlights

Based on type, the encapsulation film segment held the largest revenue share of over 65% in 2022, due to its crucial role in protecting solar cells from environmental factors, ensuring the long-term durability and reliability of solar panels. Encapsulation films safeguard against moisture ingress and physical damage, making them an essential component in solar installations

Based on polymer type, the fluoropolymer film segment held over 64% revenue share in 2022, due to the exceptional durability and resistance to environmental stressors offered by fluoropolymers, making them well-suited for the demanding outdoor environment of solar panels

Based on thickness, the less than 100 mm segment held over 45% revenue share in 2022, due to the practicality and versatility of thinner solar films, which are lightweight, flexible, and cost-effective, making them a preferred choice for a wide range of solar applications

Based on film type, the clear (Non-reflective) segment held over 30% revenue share in 2022, due to its ability to seamlessly integrate into architectural elements while minimizing glare and maintaining aesthetic appeal, making it an ideal choice for building-integrated photovoltaic (BIPV) applications and urban environments

In terms of application, the construction industry segment held over 56% revenue share in 2022, and the segment growth is driven by the construction industry’s growing focus on sustainability and energy efficiency. Solar films offer a versatile and cost-effective solution for energy generation and aesthetic enhancement, aligning with these industry priorities

Based on end-use, the commercial segment held over 39% revenue share in 2022, and the segment growth is driven by the commercial sector's increasing emphasis on sustainability, energy efficiency, and long-term cost savings. Solar films offer a practical and eco-friendly solution for businesses to achieve these goals while generating clean, renewable energy

In June 2023, First Solar launched the world's first advanced thin-film semiconductor bifacial solar panel, initiating a limited production run. This pioneering technology will be showcased at Intersolar Europe in Munich, Germany, through the pre-commercial Series 6 Plus Bifacial solar module.

For More Details or Sample Copy please visit link @: U.S. Solar Films Market Report

Based on type, the encapsulation solar film segment was a highly penetrated segment accounting for over 65% of the U.S. market share in 2022, due to its critical role in safeguarding solar cells from environmental factors. Encapsulation films provide essential protection against moisture ingress and physical damage, ensuring the long-term durability and reliability of solar panels. As the solar industry continues to expand, the demand for high-quality encapsulation materials remains strong, underscoring their significant market presence.

Based on polymer type, the Fluoropolymer segment held over 64% revenue of the U.S. market in 2022, due to its exceptional durability and resistance to environmental stressors. Fluoropolymers, such as polyvinyl fluoride (PVF) and ethylene-tetrafluoroethylene (ETFE), are well-suited for the demanding outdoor environment of solar panels, withstanding prolonged exposure to factors like UV radiation, extreme temperatures, and moisture. This durability ensures the long lifespan and reliability of solar installations, making fluoropolymer-based solar films the preferred choice for maximizing energy generation and ensuring the sustained success of solar projects in the U.S.

Based on thickness, the less than 100 mm segment dominated the market in 2022 with a revenue share of over 45%, due to the practicality and versatility of thinner solar films. These films are lightweight, flexible, and easier to install and integrate into various applications, including building-integrated photovoltaics (BIPV). Their adaptability to different surfaces, such as windows, facades, and roofing materials, allows for seamless integration without compromising the aesthetics or functionality of structures. Thinner films are cost-effective and space-efficient, appealing to both residential and commercial solar projects, where maximizing energy generation and cost savings are paramount.

Clear (Non-reflective) was a highly penetrated film type segment due to its aesthetic appeal and suitability for various applications. Unlike reflective films, clear solar films are designed to maintain the appearance of architectural elements like windows, facades, and building surfaces while harnessing solar energy. This seamless integration into existing structures without altering their visual aesthetics makes clear solar films an attractive choice for building-integrated photovoltaic (BIPV) applications. In addition, they mitigate issues related to glare and light pollution, particularly in urban areas, contributing to their preference for regulatory compliance and community acceptance, further bolstering their dominance in the U.S. market.

#SolarFilmsMarketAnalysis#RenewableEnergy#SolarPower#EnergyEfficiency#CleanEnergy#GreenTechnology#SolarEnergy#EnvironmentalImpact#InvestmentOpportunities#EnergyTransition#FutureOfEnergy

0 notes

Text

Navigating the Future: Unleashing the Potential of SOC Containers Market

In the ever-evolving landscape of cybersecurity, Security Operations Center (SOC) containers emerge as the avant-garde solution, poised to revolutionize the way organizations combat cyber threats. As the digital realm becomes increasingly intricate, the SOC Containers Market has become a focal point for businesses seeking robust and scalable security frameworks. This article delves into the dynamic landscape of SOC containers, exploring their significance, potential, and the transformative impact they bring to the cybersecurity ecosystem.

Understanding SOC Containers:

SOC containers represent a paradigm shift in cybersecurity architecture, encapsulating security operations within isolated, lightweight, and portable containers. These containers encapsulate security processes, allowing for seamless deployment, integration, and management of security protocols across diverse environments. The modular nature of SOC containers enables organizations to scale their security infrastructure without compromising agility or efficiency.

Gate Full Info: https://www.econmarketresearch.com/industry-report/soc-containers-market/

Key Drivers of SOC Containers Market Growth:

Flexibility and Scalability: SOC containers empower organizations to scale their security infrastructure seamlessly. Whether in on-premises, cloud, or hybrid environments, SOC containers provide a uniform security framework, adapting to the evolving needs of modern businesses.

Rapid Deployment and Automation: The containerized nature of SOC solutions facilitates rapid deployment, reducing the time required to fortify digital landscapes against emerging threats. Automation capabilities embedded within SOC containers streamline repetitive tasks, enabling cybersecurity teams to focus on strategic threat mitigation.

Interoperability and Integration: SOC containers break down silos by fostering interoperability and integration with existing security ecosystems. This ensures a cohesive defense strategy, allowing organizations to leverage their current investments while enhancing overall cybersecurity posture.

Cost-Efficiency: By optimizing resource utilization, SOC containers contribute to cost efficiency. Organizations can allocate resources more judiciously, mitigating the need for extensive hardware investments, and reducing operational overhead.

Other Report:

HVAC Chillers Market Size

Digital Brain Health Market Analysis

Cognitive Robotics Market Trends

Industrial IoT Display Market Share

Edible Offal Market Application

Potato and Yam Derivatives Market

Surgical Booms Market Overview

Marine Application Market Opportunities

Wind Power Parks Market Revenue

Aluminum Slug Market Development

Floor Adhesive Market Sales

Pet Fitness Care Market Technology

Axial Flux Motor Market Drivers

Audio and Video Equipment Market Types

Self Stabilizing Spoon Market Challenges

Solar Backsheet Films Market Outlook

Marine Sensors Market Analysis

Dry Shipping Container Market Segmentation

Blood Stream Infection Testing Market Size

Ethyl Vanillin Market Growth

Prebiotic Fiber Market Future

Solar Watch Market Trends

Industrial and Commercial Floor Scrubbers Market Analysis

Electro-Mechanical Brake Market Share

Fiber-Reinforced Plastics Recycling Market Segmentation

Closed Cell Foam Market Drivers

Perfume Ingredient Chemicals Market Technology

Bucket Wheel Excavator Market Revenue

Female Fragrance Market Sales

Yard Crane Market Outlook

Fuel Cells In Aerospace And Defense Market Size

0 notes

Text

Ethylene Vinyl Acetate Market Poised to Grow on Back of High Demand from Solar Panel Manufacturing Industry

Ethylene vinyl acetate (EVA) is a copolymer of ethylene and vinyl acetate which finds extensive usage as an encapsulant in photovoltaic (PV) module manufacturing. As an encapsulant, EVA protects PV cells from moisture and helps in improving their performance. It provides excellent adhesion to both front glass as well as back sheet. The global solar panel market has been growing rapidly over the past few years owing to supportive government policies and initiatives encouraging the adoption of renewable energy. With increasing deployment of solar panels worldwide, demand for EVA from this application segment is projected to surge substantially. The global ethylene vinyl acetate market is estimated to be valued at US$ 1710.66 Mn in 2024 and is expected to exhibit a CAGR of 3.4% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: The high demand from solar panel manufacturing is one of the major drivers propelling the growth of ethylene vinyl acetate market. Solar panel encapsulants account for over 40% of the overall EVA consumption. The government targets to increase usage of renewable sources of energy along with falling prices of solar panels have boosted the solar energy market size significantly. According to the International Renewable Energy Agency (IRENA), globally over 100 GW of solar PV was added in 2021 alone. This rising deployment of solar panels directly translates to increased consumption of EVA. Apart from this, EVA finds wide applications in hot melt adhesives, packaging, and cables. The growth in end-use industries is further augmenting demand. SWOT Analysis Strength: Ethylene Vinyl Acetate (EVA) is used as an effective polymer in several end use industries such as solar panels, medical devices, and footwear. EVA provides excellent flexibility, transparency, and reliability in production processes. EVA products show consistent performance even in extreme temperatures due to their durable nature. Weakness: Fluctuating raw material prices impact the cost of EVA production. Rising crude oil prices increase the commodity prices of ethylene and vinyl acetate, making EVA slightly expensive. EVA has poor mechanical properties and low melting point in comparison to other polymers. Opportunity: Surging demand for renewable energy sources is driving the solar PV industry. EVA encapsulants protect photovoltaic cells from moisture and UV damage, thereby enhancing module efficiency. Growing medical devices market especially for implants and prosthetics boosts EVA usage. Threats: Strict regulations regarding toxic emissions can adversely impact manufacturing units. Intense competition from substitute polymers may reduce EVA consumption gradually. Key Takeaways The global ethylene vinyl acetate market size is expected to witness high growth backed by increasing solar installations and growing medical device industry. The global ethylene vinyl acetate market is estimated to be valued at US$ 1710.66 million in 2024 and is expected to exhibit a CAGR of 3.4% over the forecast period 2024 to 2031.

Asia Pacific dominates the global market due to large solar PV sector and rapidly expanding construction industry in China and India. Key regional players are expanding their production capacities to meet local demand. Key players operating in the ethylene vinyl acetate market are DuPont, ExxonMobil, FPC, Hanwha Group, LyondellBasell, Sipchem, and Formosa Plastics. They are focusing on developing novel EVA grades with enhanced properties to strengthen their market position. Technological innovation and partnerships remain crucial for gaining competitive edge. New product launches with optimized performance characteristics could boost revenues. Collaboration with end users aids in developing customized polymer solutions.Get more insights on this topic:https://www.newswirestats.com/ethylene-vinyl-acetate-market-size-and-outlook/

#Ethylene Vinyl Acetate#Ethylene Vinyl Acetate Market#Ethylene Vinyl Acetate Market size#Ethylene Vinyl Acetate Market share#Coherent Market Insights

0 notes

Text

US Solar Inverter Market Types and Applications, Drivers, Ongoing Trends, Future Demand, Challenges, Top Companies & Forecast 2030

The “US Solar Inverter Market” forecast 2030 report analyses the present and future competitive scenario of the analytics industry. US Solar Inverter Market report offers an in-depth analysis on segments including top companies, products, applications, revenue and regions. a number of topics including likewise market share, drivers, trends and methods. This report additionally offers insights into the latest growth and trends. It encapsulates key aspects of the market, with focus on leading key player’s areas that have witnessed the highest demand, leading regions and applications.

The US Solar Inverter market size is expected to grow from US$ 825.86 million in 2022 and is expected to reach US$ 2,773.99 million by 2030; it is estimated to record a CAGR of 12.8% from 2022 to 2030.

The report covers an in-depth analysis of the key market players within the market

GoodWe Technologies Co Ltd, Delta Electronics Inc, CyboEnergy Inc, Yaskawa America Inc, Danfoss AS, SMA Solar Technology AG, SolarEdge Technologies Inc, Power Electronics SL, Ginlong Technologies Co Ltd, Chicago Digital Power Inc, Sungrow Power Supply Co Ltd, Caterpillar Inc.

Key Market Segments

Based on phase type, the US Solar Inverter market analysis is segmented into single phase, and three phase. Single phase is commonly utilized in cases where typical loads are heating, instead of large electric motors. This type of phase generates single phase power from the PV modules and is capable to connect power to single phase equipment or the grid itself. The single phase comes under a less than 5 kW of capacity. The single phase power produces electricity for the residential houses and power supplies which might be utilized domestically. Various appliances need small level of power to make televisions, lights, and heaters functional. Due to generation of power for using appliances, single phase inverter is ideal for residential purpose.

Market Analysis and Insights: US Solar Inverter Market

US Solar Inverter Market report elaborates the market size, market characteristics, and market growth of the US Solar Inverter Market industry, and breaks down according to the type, application, and consumption space of US Solar Inverter Market. The report also conducted a PESTEL analysis of the industry to check the most influencing factors and entry barriers of the industry.

Customize Your Report: Don't miss out on the chance to talk to our analyst and know more insights concerning this market report. Our analysts can also assists you customize this report according to your needs. Our analysts and industry experts will work directly with you to understand your requirements and provide you with custom made information during a short quantity of your time

0 notes

Text

Encapsulants Market: Global Industry Size, Share, Regional Outlook, Segmentation and Opportunity Analysis

Encapsulants are materials that are used to shield and insulate semiconductor devices. They are typically applied in the form of a liquid or paste and cured to form a protective layer around the semiconductor. Encapsulants are used to protect semiconductors from damage caused by environmental factors such as moisture, chemicals, or dust. They also provide electrical insulation and reduce the…

View On WordPress

#Covid 19 Impact on Encapsulants Market#electronic potting#electronic potting epoxy#electronic potting silicone#encapsulant solar panel#Encapsulants Industry#Encapsulants Market#Encapsulants Market Analysis#Encapsulants Market Forecast#Encapsulants Market Growth#Encapsulants Market Outlook#Encapsulants Market Research#Encapsulants Market Revenue#Encapsulants Market Share#Encapsulants Market Size#Encapsulants Market Trends#epoxy encapsulant#Europe Encapsulants Market#fiberlock mold encapsulant#glob top encapsulant#silicone encapsulant#solar cell encapsulant#thermally conductive encapsulant#UK Encapsulants Market#US Encapsulants Market

1 note

·

View note

Text

The encapsulants market is estimated to be USD 1.26 billion in 2017 and is projected to reach USD 1.64 billion by 2022, at a CAGR of 5.5% from 2017 to 2022. The growth of advanced electronic packaging technique is driving the encapsulants market in different end-use industries. The growing use of encapsulants in consumer electronics and transportation is also fueling the growth of the encapsulants market across the globe. Medical and energy & power are some of the end-user industries of encapsulants.

Expansion and new product development/launch accounted for the major share of all growth strategies adopted by the leading players in the encapsulants market between January 2013 and September 2017. Dow Corning (US), Henkel (Germany), LORD Corporation (US), Shin-Etsu Chemicals (Japan), and H.B. Fuller (US) are some of the leading players operating in the encapsulants market.

Besides expansions and new product launches, the leading players also adopted agreements and mergers as key strategies to enhance their market shares and strengthen their presence in the encapsulants market between January 2013 and September 2017.

Henkel is the leading manufacturer of encapsulants, globally. The company carries out its business operations through its semiconductor assembly product lines. In September 2015, Henkel acquired The Bergquist Company, a privately-held leading supplier of thermal management solutions to the global electronics industry. This acquisition helped the company strengthen its position as a global leader in adhesives technology, catering to the emerging electronics industry of the Asia Pacific and South American regions.

#Encapsulants Market#electronic potting#electronic potting epoxy#silicone encapsulant#solar cell encapsulant#glob top encapsulant#encapsulant solar panel#electronic potting silicone#epoxy encapsulant#thermally conductive encapsulant#fiberlock mold encapsulant#Encapsulants Industry#Covid 19 Impact on Encapsulants Market#Encapsulants Market Size#Encapsulants Market Share#Encapsulants Market Analysis#Encapsulants Market Revenue#Encapsulants Market Trends#Encapsulants Market Growth#Encapsulants Market Research#Encapsulants Market Outlook#Encapsulants Market Forecast#US Encapsulants Market#UK Encapsulants Market#Europe Encapsulants Market#Encapsulants Major Players

0 notes

Text

Thermally Conductive Polymers Market 2023 Brief Analysis by Trends, Growth and Revenue Estimations till 2030

Thermally conductive polymers are a type of polymer material that possess high thermal conductivity, allowing them to efficiently transfer heat. Unlike traditional polymers, which are generally poor thermal conductors, thermally conductive polymers are designed or modified to have improved thermal properties for specific applications where heat management is crucial. These polymers are used in a wide range of industries, including electronics, automotive, aerospace, and energy.

There are several ways to achieve thermal conductivity in polymers. One approach is to incorporate thermally conductive fillers, such as metal particles, carbon fibers, or ceramic materials, into the polymer matrix. These fillers create a conductive network within the polymer, facilitating the transfer of heat through the material. Another approach is to modify the chemical structure of the polymer itself to enhance its thermal properties.

Thermally conductive polymers offer several advantages in various applications. For example, in the electronics industry, they can be used as heat sinks, helping to dissipate heat generated by electronic components, such as transistors and LEDs, which can improve their performance and reliability. In the automotive and aerospace industries, thermally conductive polymers can be used in thermal management systems to improve the efficiency and safety of engines, brakes, and other high-temperature components. In the energy sector, they can be used in batteries, fuel cells, and heat exchangers to enhance their thermal performance.

The thermally conductive polymers market has been witnessing significant growth in recent years due to the increasing demand for efficient heat management solutions across various industries, such as electronics, automotive, aerospace, and energy. The market for thermally conductive polymers is expected to continue to expand in the coming years, driven by advancements in material science and growing applications in emerging industries.

One of the key drivers of the thermally conductive polymers market is the rapidly growing electronics industry. As electronic devices become smaller and more powerful, the need for effective heat dissipation solutions has become critical to prevent overheating and ensure optimal performance. Thermally conductive polymers are increasingly being used in applications such as heat sinks, thermal interface materials, and encapsulation materials in electronic devices, including smartphones, laptops, and electric vehicles, to improve their thermal management capabilities.

The automotive and aerospace industries are also significant contributors to the thermally conductive polymers market. With increasing focus on lightweighting and improving fuel efficiency in vehicles, thermally conductive polymers are being used in applications such as engine components, braking systems, and thermal management systems to enhance heat dissipation and reduce weight.

Furthermore, the growing demand for renewable energy sources, such as solar panels and wind turbines, is driving the adoption of thermally conductive polymers in energy applications. These polymers are used in components such as heat exchangers, thermal storage systems, and battery housings, to improve their thermal performance and efficiency.

Geographically, the thermally conductive polymers market is witnessing growth across regions, including North America, Europe, Asia-Pacific, and Rest of the World. Asia-Pacific, in particular, is expected to witness significant growth due to the presence of major electronics manufacturers and automotive industries in countries like China, Japan, and South Korea.

Key companies covered as a part of this study include RTP Company, PolyOne Corporation, Celanese Corporation, SABIC, Covestro AG, Royal DSM, Mitsubishi Engineering-Plastics Corporation, HELLA GmbH & Co., and Torray Industries, Inc.

The demand for thermally conductive polymers is driven by various factors, including the increasing need for efficient heat management solutions in industries such as electronics, automotive, aerospace, and energy. The demand for thermally conductive polymers is influenced by several key factors, including:

➢ Electronics Industry: The demand for thermally conductive polymers in the electronics industry is driven by the growing use of electronic devices, such as smartphones, laptops, tablets, and electric vehicles. These devices generate significant amounts of heat during operation, and effective heat dissipation is crucial for optimal performance and reliability. Thermally conductive polymers are used in applications such as heat sinks, thermal interface materials, and encapsulation materials to improve the thermal management capabilities of electronic devices.

➢ Automotive and Aerospace Industries: The demand for thermally conductive polymers in the automotive and aerospace industries is driven by the need for lightweighting and improved fuel efficiency. Thermally conductive polymers are used in applications such as engine components, braking systems, and thermal management systems to enhance heat dissipation and reduce weight, thereby improving the overall performance and efficiency of vehicles.

➢ Energy Industry: The demand for thermally conductive polymers in the energy industry is driven by the growing adoption of renewable energy sources, such as solar panels and wind turbines. Thermally conductive polymers are used in components such as heat exchangers, thermal storage systems, and battery housings to improve their thermal performance and efficiency.

➢ Emerging Industries: Thermally conductive polymers are finding increasing applications in emerging industries such as 5G telecommunications, electric vehicles, and wearable devices, where efficient heat management is critical for performance and reliability. The demand for thermally conductive polymers in these industries is expected to grow as these technologies continue to advance and become more widely adopted.

Thermally conductive polymers find a wide range of applications across various industries due to their unique properties of both thermal conductivity and polymer characteristics. Some of the key applications of thermally conductive polymers include:

✦ Electronics and Electrical: Thermally conductive polymers are extensively used in the electronics and electrical industry for applications such as heat sinks, thermal interface materials, encapsulation materials, and printed circuit boards (PCBs). They help in managing heat generated by electronic devices and ensure their efficient operation and reliability. These polymers are used in various electronic devices, including smartphones, laptops, tablets, servers, LED lighting, power modules, and electric vehicle components.

✦ Automotive and Aerospace: Thermally conductive polymers are used in the automotive and aerospace industries for applications such as engine components, braking systems, thermal management systems, battery housings, and power electronics. They help in dissipating heat from critical components, reducing weight, and improving the overall performance and efficiency of vehicles.

✦ Energy: Thermally conductive polymers are used in the energy industry for applications such as heat exchangers, thermal storage systems, and battery thermal management. They help in improving the thermal performance and efficiency of renewable energy sources such as solar panels and wind turbines, as well as energy storage systems such as batteries.

✦ Industrial: Thermally conductive polymers are used in industrial applications such as heat sinks for power electronics, thermal management in industrial processes, and encapsulation of sensitive components in harsh environments. They help in managing heat generated during industrial processes and ensuring reliable operation of industrial equipment.

✦ Medical and Healthcare: Thermally conductive polymers are used in medical and healthcare applications such as medical devices, drug delivery systems, and wearable devices. They help in managing heat generated by medical equipment, maintaining drug stability, and improving the comfort and safety of wearable devices.

✦ Consumer Goods: Thermally conductive polymers are used in consumer goods applications such as appliances, sporting goods, and consumer electronics. They help in managing heat generated by consumer goods, improving their performance, and enhancing user comfort and safety.

The use of thermally conductive polymers in various applications offers several benefits, which contribute to their growing market demand. Some of the key benefits of thermally conductive polymers include:

★ Enhanced Heat Dissipation: Thermally conductive polymers are designed to efficiently dissipate heat, making them ideal for managing heat generated by electronic devices, automotive components, industrial equipment, and other applications. They help in preventing overheating, reducing the risk of thermal damage, and improving the performance and reliability of components and systems.

★ Lightweight and Design Flexibility: Thermally conductive polymers are generally lightweight compared to traditional metal-based heat dissipation materials, making them suitable for weight-sensitive applications such as automotive, aerospace, and portable electronic devices. Moreover, they offer design flexibility due to their ability to be molded into complex shapes and integrated into various forms, allowing for innovative and space-efficient designs.

★ Electrical Insulation: Thermally conductive polymers are typically electrically insulating, which makes them suitable for applications where electrical insulation is required along with thermal conductivity. This property allows for the use of thermally conductive polymers in electronic devices and electrical components without the risk of short-circuits or other electrical issues.

★ Corrosion Resistance: Many thermally conductive polymers exhibit excellent corrosion resistance, making them ideal for use in harsh environments where corrosion can degrade the performance and reliability of components. This makes them suitable for applications in industries such as automotive, aerospace, and industrial equipment, where exposure to moisture, chemicals, and other corrosive agents is common.

★ Cost-effective: Thermally conductive polymers can offer cost advantages over traditional heat dissipation materials, such as metals, due to their lower raw material costs, ease of processing, and potential for reduced manufacturing and assembly costs. They can also contribute to weight and space savings, leading to improved overall system efficiency and cost-effectiveness.

★ Versatility: Thermally conductive polymers can be formulated to exhibit a wide range of thermal conductivity values, allowing for customization to meet specific application requirements. This versatility enables their use in various industries and applications, including electronics, automotive, aerospace, energy, medical, and consumer goods.

★ Environmental Sustainability: Thermally conductive polymers can offer environmental sustainability benefits, as they can be designed to be recyclable or biodegradable, reducing their impact on the environment compared to traditional heat dissipation materials. Additionally, the use of thermally conductive polymers in lightweighting applications can contribute to reducing energy consumption and greenhouse gas emissions associated with transportation.

Overall, the benefits of thermally conductive polymers, such as enhanced heat dissipation, lightweight and design flexibility, electrical insulation, corrosion resistance, cost-effectiveness, versatility, and environmental sustainability, make them attractive for a wide range of applications across various industries, driving their market demand.

0 notes

Text

Growth of Solar EV Charging Market Share Report Till 2031

Solar EV Charging Market Overview

The solar EV charging market was valued at $159.6 million in 2021, and is estimated to reach $330.9 million by 2031, growing at a CAGR of 8.1% from 2022 to 2031.

Some of the major players in the solar EV charging market include iSun, Inc., Bharat Heavy Electricals Limited, Zhejiang Benyi New Energy Co., Ltd. , PowerFlex, EmPower Solar, HES Solar., Paired Power, KEBA, Brightfield Transportation Solutions., and ChargePoint, Inc.

Download Report Sample: https://www.alliedmarketresearch.com/request-sample/54125

Asia-Pacific region held major share in terms of revenue and is anticipated to grow at a CAGR of 8.4% from 2022 to 2031. Future developments in China solar product industry are projected to drive the growth of the solar EV charging market in the country.

Europe holds the CAGR of 8.2% during the forecast period.

Utilization of solar energy for charging electric vehicles is an evolving idea which has taken ground over the past few years.

Solar PV has proven to be an excellent solution for localized electricity generation, even for large-scale applications.

Over the past ten years, researchers have tried to include solar energy for charging stations to ensure energy autonomy and reduced emissions.

A solar panel harnesses the solar radiation and into electrical energy which is used to charge EV batteries with clean energy. Solar energy is one of the cleanest options for fueling the electric cars. The main advantage for solar EV charging to operate for a long time is the extended life span of solar panels.

Improvement in technology is enabling solar EV charging to create new records in terms of power generation and capacity which is boosting the global EV charging market size in future.

Surge in awareness and promotion of using green energy solution are expected to drive the global solar EV charging market growth in anticipated period.

Solar EV charging has several advantages such as energy-saving, durable, affordable, safe and eco-friendly which is expected to fuel the global solar EV charging market share in near future.

Buy This Report (305 Pages PDF with Insights, Charts, Tables, and Figures): https://bit.ly/3nLVwl0

The demand for solar EV charging is already high in the residential sector as solar EV charging lowers the expense on charging EV battery.

As per the solar EV charging market forecast, global trends indicate that both the EV and solar industry has been witnessing an exponential growth over the recent past. The challenges are coming in the way to make EVs as the mainstream for transportation.

In the near future, there will be a solar EV charging market opportunities such as the growing adoption of EVs in developing countries and improvement in the energy storage systems.

For instance, U.S. has approximately 250,000 EVs and about 500,000 solar rooftops, and both industries are still growing exponentially.

On the basis of charging level, the level 2 segment held the market share of more than 60.0% in 2021 in terms of revenue

On the basis of system, the off grid segment held the market share of around 70.0% in 2021 in terms of revenue

Read More Information: https://www.alliedmarketresearch.com/solar-ev-charging-market-A53650

On the basis of application, the private EV charger segment held three-fourths market share in 2021 in terms of revenue.

Related Reports:-

About Us

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "Market Research Reports" and "Business Intelligence Solutions." AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

Pawan Kumar, the CEO of Allied Market Research, is leading the organization toward providing high-quality data and insights. We are in professional corporate relations with various companies and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

Contact:

David Correa 5933 NE Win Sivers Drive #205, Portland, OR 97220 United States USA/Canada (Toll Free): +1-800-792-5285, +1-503-894-6022 UK: +44-845-528-1300 Hong Kong: +852-301-84916 India (Pune): +91-20-66346060 Fax: +1(855)550-5975 [email protected]

Web: www.alliedmarketresearch.com

Allied Market Research Blog:

Follow Us on | Facebook | LinkedIn | YouTube

0 notes

Text

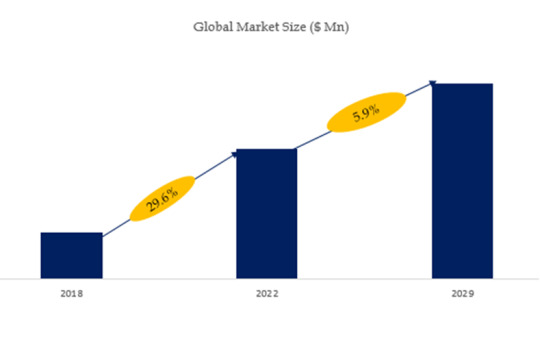

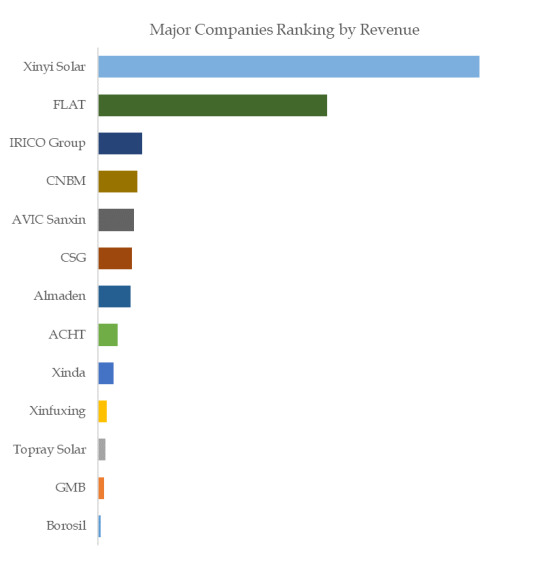

Global Top 5 Companies Accounted for 82% of total Glass for Solar Cells market (QYResearch, 2021)

Glass for solar cells is generally used as an encapsulation sheet for solar modules to protect solar cells. After the solar cell is installed in the solar panel, the conversion efficiency will be reduced because the encapsulating glass absorbs and reflects sunlight. Therefore, in order to minimize the reflection and absorption of sunlight so that more sunlight can pass through the protective glass and hit the solar cell, the quality of the encapsulation glass is very important. Because of this unique feature, as the global use of solar energy continues to rise and the installation of solar modules and panels increases, there is an even greater demand for specialized, high-quality and high-transparency solar glass products.

According to the new market research report “Global Glass for Solar Cells Market Report 2023-2029”, published by QYResearch, the global Glass for Solar Cells market size is projected to reach USD 6.75 billion by 2029, at a CAGR of 5.9% during the forecast period.

Figure. Global Glass for Solar Cells Market Size (US$ Million), 2018-2029

Figure. Global Glass for Solar Cells Top 13 Players Ranking and Market Share(Based on data of 2021, Continually updated)

The global key manufacturers of Glass for Solar Cells include Xinyi Solar, FLAT, IRICO Group, CNBM, AVIC Sanxin, CSG, Almaden, ACHT, Xinda, Xinfuxing, etc. In 2020, the global top five players had a share approximately 82.0% in terms of revenue.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

For more information, please contact the following e-mail address:

Email: [email protected]

Website: https://www.qyresearch.com

0 notes