#fha $100 down program

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

US Tumblr user growth rate is estimated to slow down to 4.1%.

Text

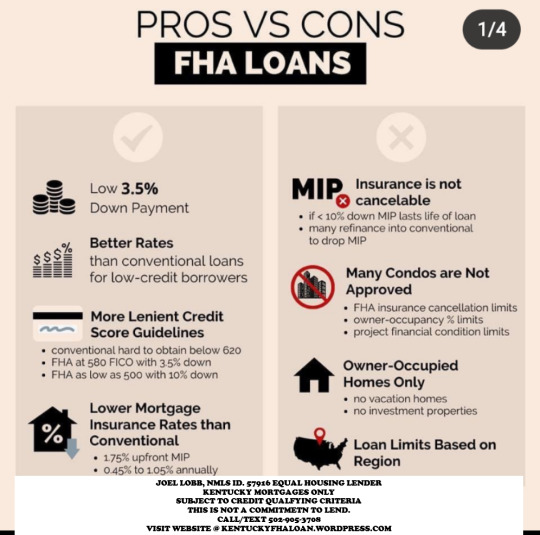

Best Kentucky FHA lenders to get an Approval to buy a house.

How to Qualify for a Kentucky FHA Loan Approval: If you’re looking to buy a home in Kentucky and are considering a Kentucky FHA loan, it’s essential to understand the qualifying criteria and the necessary steps. This article covers all the crucial aspects you need to know, from credit scores, bankruptcy, work history, collections, closing, home insurance, title, debt ratio , down payment and…

View On WordPress

#$100 Down FHA Mortgage#2020 Kentucky FHA Mortgage Guidelines#and work history requirements for Kentucky Mortgage loan approval for FHA#Credit score#FHA#fha $100 down program#fha 2014 fico score requirements#fha appraisals#FHA Approved Condos Louisville Kentucky#FHA Back to Work Program Ky#fha borrowers#FHA Co-signors#fha collections#fha credit score#First-time buyer#Kentucky#louisville#Mortgage#Mortgage loan#Zero down home loans

0 notes

Text

All Types of Home Loans (Conventional, FHA, Jumbo, VA, USDA Loans) in Dallas, TX

Buying a home in Dallas, TX, is an exciting milestone, but navigating the mortgage process can be overwhelming. With various loan options available, it’s essential to understand which one suits your financial situation best. At Edge Home Finance Inc, we specialize in helping borrowers secure the perfect home loan—whether it’s a Conventional, FHA, Jumbo, VA, or USDA loan. Each mortgage type has unique benefits, eligibility requirements, and ideal use cases. In this guide, we’ll break down all the major home loan options in Dallas, TX, so you can make an informed decision.

1. Conventional Loans: Flexible Financing for Strong Credit

Conventional loans are one of the most popular mortgage options in Dallas, TX, and are not backed by any government agency. These loans are ideal for borrowers with good to excellent credit (typically 620 or higher) and a stable income.

Key Features of Conventional Loans:

Down Payment Options: As low as 3% (with certain programs) but typically 5%-20%.

Loan Limits: Up to $766,550 in Dallas (conforming loan limits for 2024).

PMI (Private Mortgage Insurance): Required if the down payment is less than 20%.

Best For: Buyers with strong credit who want lower interest rates and flexible terms.

At Edge Home Finance Inc, we help clients compare conventional loan options to find the best rates and terms for their home purchase or refinance.

2. FHA Loans: Low Down Payment & Flexible Credit Requirements

If you have a lower credit score or limited savings for a down payment, an FHA loan (insured by the Federal Housing Administration) could be the perfect solution. These loans are designed to help first-time homebuyers and those with less-than-perfect credit.

Key Features of FHA Loans:

Down Payment: As low as 3.5% with a credit score of 580+.

Credit Score Requirements: Minimum 500 (with 10% down).

Mortgage Insurance: Upfront and annual MIP (Mortgage Insurance Premium) required.

Best For: First-time buyers, those with lower credit scores, or buyers with limited down payment funds.

Edge Home Finance Inc works with FHA-approved lenders in Dallas, TX, to help borrowers secure affordable financing.

3. Jumbo Loans: Financing High-Value Homes in Dallas

For luxury homes or properties that exceed conforming loan limits ($766,550 in 2024), a Jumbo loan is necessary. These loans are common in Dallas’s upscale neighborhoods, where home prices often surpass standard loan limits.

Key Features of Jumbo Loans:

Loan Amounts: Above $766,550 (varies by lender).

Down Payment: Typically 10%-20% or more.

Credit & Income Requirements: Stricter than conventional loans (usually 700+ credit score).

Best For: High-income buyers purchasing luxury homes.

At Edge Home Finance Inc, we connect borrowers with competitive jumbo loan lenders in Dallas, TX, ensuring seamless financing for high-value properties.

4. VA Loans: Zero Down Payment for Veterans & Military Members

Active-duty service members, veterans, and eligible spouses can benefit from VA loans, backed by the U.S. Department of Veterans Affairs. These loans offer unbeatable terms, including no down payment and no private mortgage insurance (PMI).

Key Features of VA Loans:

Down Payment: 0% required.

Credit Requirements: Varies by lender but generally more flexible than conventional loans.

Funding Fee: A one-time fee (can be rolled into the loan).

Best For: Military members and veterans looking for affordable home financing.

Edge Home Finance Inc proudly assists veterans and military families in Dallas, TX, in securing VA loans with favorable terms.

5. USDA Loans: Rural & Suburban Homebuying with No Down Payment

If you’re looking to buy a home in a rural or suburban area of Dallas, TX, a USDA loan (backed by the U.S. Department of Agriculture) could be an excellent choice. These loans offer 100% financing (no down payment) for eligible buyers.

Key Features of USDA Loans:

Down Payment: 0% required.

Income Limits: Must meet area-specific income caps.

Property Location: Must be in a USDA-eligible zone.

Best For: Low-to-moderate-income buyers in qualifying rural/suburban areas.

Edge Home Finance Inc helps Dallas homebuyers determine USDA eligibility and secure low-interest financing.

6. Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

Beyond loan types, borrowers must decide between fixed-rate mortgages (FRMs) and adjustable-rate mortgages (ARMs).

Fixed-Rate Loans: Interest rate stays the same for the entire loan term (15, 20, or 30 years). Ideal for long-term homeowners.

Adjustable-Rate Loans (ARMs): Lower initial rates that adjust periodically (e.g., 5/1 ARM). Best for short-term buyers or those expecting rising income.

Edge Home Finance Inc helps Dallas borrowers choose the right rate structure based on their financial goals.

7. How to Choose the Best Home Loan in Dallas, TX

Selecting the right mortgage depends on: ✅ Credit Score (Higher scores qualify for better rates) ✅ Down Payment Savings (FHA & VA allow low or no down payment) ✅ Loan Term (15-year vs. 30-year) ✅ Future Plans (Staying long-term? An ARM may not be ideal)

Our team at Edge Home Finance Inc provides personalized mortgage consultations to match you with the best loan option.

8. Why Choose Edge Home Finance Inc for Your Dallas Home Loan?

When securing a mortgage in Dallas, TX, working with a trusted lender makes all the difference. At Edge Home Finance Inc, we offer: 🔹 Expert Guidance: We explain all loan types in simple terms. 🔹 Competitive Rates: Access to multiple lenders for the best deals. 🔹 Fast Approvals: Streamlined process for quick closings. 🔹 Local Market Knowledge: Dallas-specific loan expertise.

Whether you need a Conventional, FHA, Jumbo, VA, or USDA loan, we’re here to help you every step of the way.

0 notes

Text

Mortgage Mondays with John V. Pinto:

Your Credit Score & Loan Qualifications—

What You Need to Know

🏡 **Struggling to move from renting to owning? Your credit score and loan options could be the key!**

When I take a listing, I don’t just market it for sale—I also introduce potential tenants to homeownership possibilities through **100% financing, VA loans, FHA loans, USDA loans, down payment assistance, and closing cost assistance programs**. While accumulating a down payment is a major challenge, **debt ratios and credit scores** play a critical role in determining whether buyers qualify for a loan—and at what interest rate.

💳 **What’s the minimum credit score you need?**

- **FHA Loans:** Starting at *580* (sometimes lower with higher down payments)

- **Conventional Loans:** Generally *620+*

- **VA Loans:** No minimum required (but lenders often look for *580–620*)

- **USDA Loans:** *640* recommended for smoother approvals

🎧 **Click the link to listen to my latest podcast episode!** Gain insights that could help make homeownership a reality.

🔗 Listen now

👉

https://open.spotify.com/episode/3p2UZujra3Whk8UNHgfAZz?si=2257_J4KSS-3Av8t7MKwhw

💬 **Have you run into credit score challenges when applying for a mortgage? Drop a comment below—I’d love to hear your experience!**

📞 Want expert guidance on navigating the path to homeownership? Call or text me directly at 408-829-4141—I’d love to help!

🔗 Know someone looking to buy a home? Tag them below!

📌

#MortgageMondays #HomeBuying #CreditScores #FinancingOptions #DownPaymentAssistance #HomeOwnershipGoals #RealEstateTips #FirstTimeHomeBuyer #JohnVPinto

0 notes

Text

Mortgage Pro Home Loan: Your Trusted Partner in Home Financing

Purchasing a home is one of the most significant financial decisions you will ever make. Whether you are a first-time buyer, upgrading to a larger property, or refinancing an existing mortgage, the process can be complex and overwhelming. That’s where Mortgage Pro Home Loan comes in—a reliable, client-focused mortgage service dedicated to helping individuals and families achieve their homeownership goals with confidence and clarity.

In this article, we’ll explore how Mortgage Pro Home Loan stands out in the lending industry, the range of services they offer, and how their expert guidance can simplify your journey toward owning your dream home.

Who Is Mortgage Pro Home Loan?

Mortgage Pro Home Loan is a full-service mortgage provider known for its personalized approach, competitive rates, and deep knowledge of the home loan industry. With a team of experienced professionals, they specialize in helping clients navigate various mortgage options and find the solution that best fits their financial profile and lifestyle.

The company prides itself on building long-term relationships with clients. Rather than simply securing a loan, Mortgage Pro takes the time to educate borrowers, address their concerns, and guide them through every step of the lending process—from application to closing.

Why Choose Mortgage Pro Home Loan?

There are plenty of mortgage lenders out there, but few combine the personalized service of a local provider with the resources and technology of a national lender. Here’s why more homeowners and buyers are choosing Mortgage Pro:

✅ Personalized Service

No two borrowers are the same, and Mortgage Pro understands that. They take a consultative approach, getting to know each client's unique financial situation and housing goals before recommending loan options.

✅ Wide Range of Loan Programs

Whether you need a conventional loan, FHA, VA, USDA, jumbo, or refinancing, Mortgage Pro has access to a wide variety of loan products from multiple lenders—giving you more flexibility and better rates.

✅ Fast Pre-Approvals

In a competitive housing market, speed matters. Mortgage Pro provides fast and accurate pre-approvals, helping buyers make strong offers with confidence.

✅ Transparent Communication

Throughout the mortgage process, communication is key. Mortgage Pro Home Loan keeps clients informed every step of the way with clear timelines, updates, and answers to all your questions.

✅ Local Expertise

Understanding regional real estate trends, taxes, and laws is critical when securing a mortgage. Mortgage Pro brings the advantage of local knowledge to help you make smarter financial decisions.

Loan Options Available with Mortgage Pro Home Loan

One of the standout features of Mortgage Pro is the variety of loan programs they offer. No matter your income, credit score, or property type, there’s likely a solution that fits your needs.

🏡 Conventional Loans

These are the most common types of mortgages and are ideal for borrowers with good credit and stable income. Conventional loans can offer competitive rates and flexible terms.

🪖 VA Loans

For veterans, active-duty service members, and eligible military spouses, VA loans offer zero down payment options and favorable rates. Mortgage Pro has VA loan specialists to guide you through the process.

🏘️ FHA Loans

FHA loans are designed for first-time homebuyers or those with lower credit scores. They offer a lower down payment and more flexible qualification criteria.

🌾 USDA Loans

Living in a rural or suburban area? You may qualify for a USDA loan, which provides 100% financing with low interest rates for eligible properties and borrowers.

💼 Jumbo Loans

If you’re purchasing a high-value property that exceeds conforming loan limits, a jumbo loan may be the right solution. Mortgage Pro offers competitive jumbo loan programs for qualified buyers.

🔄 Refinancing

Looking to lower your rate, reduce monthly payments, or tap into home equity? Mortgage Pro Home Loan offers refinancing solutions tailored to your current financial goals.

The Mortgage Process: What to Expect

Mortgage Pro Home Loan makes the lending process smooth, efficient, and stress-free. Here’s a quick breakdown of how it works:

Initial Consultation – You’ll meet with a loan specialist to discuss your financial goals and review loan options.

Pre-Approval – Provide basic financial documents to get pre-approved and determine your buying power.

Home Search & Offer – With your pre-approval letter in hand, you can start house hunting and make offers with confidence.

Loan Processing – Once you have an accepted offer, the team will begin the full loan application and underwriting process.

Closing – After approval, you’ll review and sign final documents, and officially become a homeowner!

Client-Centered Values

Mortgage Pro Home Loan was founded on the belief that every client deserves honesty, transparency, and trust. This client-first philosophy has earned them a reputation for going the extra mile to support homeowners through each phase of the lending journey.

They understand that buying or refinancing a home is a major life event, not just a transaction. That’s why they stay in touch even after closing, providing ongoing support, market updates, and refinancing opportunities when the time is right.

Customer Testimonials

Mortgage Pro Home Loan has helped hundreds of families and individuals reach their homeownership goals. Here’s what some of their happy clients have to say:

"The team at Mortgage Pro was responsive, professional, and truly cared about getting us the best loan for our situation. We closed faster than expected and felt supported the whole way." – Sarah T., First-Time Buyer

"I’ve worked with other lenders before, but Mortgage Pro was hands down the best. Clear communication, competitive rates, and no surprises." – Jason M., Home Refinance

Conclusion: Let Mortgage Pro Help You Open the Door to Homeownership

Whether you're buying your first home, upgrading, or refinancing, choosing the right mortgage partner is critical. Mortgage Pro Home Loan offers the expertise, resources, and personal service you need to make confident financial decisions and move forward with peace of mind.

Don't let mortgage myths or confusing jargon hold you back. Reach out to Mortgage Pro Home Loan today—and take the first step toward turning your homeownership dreams into reality.

0 notes

Text

💸 FHA 0% Down Payment – 100% Financing with No Strings Attached

Body: Thinking about buying your first home but worried about saving for a down payment? You’re not alone — and now, you don’t have to wait.

🏠 With Shop Rates, you may qualify for FHA-backed financing with 0% down — yes, truly 100% financing for qualified buyers.

✨ Low credit score? ✨ Not a first-time buyer? ✨ Need help navigating programs?

We’ve got you covered.

📍 Serving Nashville and beyond. 🔗 Read how it works: https://shoprates.com/fha-0-down-payment/

#mortgagetips #fha #zerodown #homebuyer #firsttimehomebuyer #realestate #mortgageloan #shoprates #nashvillehomes

#shoprates#dscr loans#nashville#real estate investing#hardmoneyloans#propertyinvestment#realestateinvesting#investmentopportunity#hardmoney

0 notes

Text

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Navigate benefits, myths, hidden rules, and pitfalls for maximum advantage.

The VA home loan program, guaranteed by the U.S. Department of Veterans Affairs, stands as one of the most significant and advantageous benefits available to eligible active-duty personnel, veterans, National Guard members, Reserve members, and certain surviving spouses. While often lauded for its well-known features, a deeper understanding reveals nuances, lesser-known opportunities, and potential pitfalls that can dramatically impact a homebuyer& experience. This guide delves into the comprehensive landscape of VA loans, from core benefits to hidden guidelines critical for success.

Highlights: Key VA Loan Advantages

No Down Payment & No PMI: Qualified borrowers can often finance 100% of a home& purchase price without needing Private Mortgage Insurance (PMI), offering substantial upfront and monthly savings compared to conventional or FHA loans.

Lifelong, Reusable Benefit: Eligibility for a VA loan isn& a one-time deal. Veterans can use the benefit multiple times throughout their lives, potentially even holding more than one VA loan simultaneously under certain entitlement conditions.

Flexible Guidelines & Competitive Terms: The program features competitive interest rates, often lower than conventional options, flexible credit requirements, and limits on allowable closing costs, making homeownership more accessible. Sellers can also contribute significantly towards closing costs.

Core Features: The Foundation of VA Loan Power

Understanding the fundamental benefits of VA loans is the first step towards leveraging this powerful program.

VA loans provide significant advantages for eligible veterans and service members seeking homeownership.

Financial Advantages

Zero Down Payment

Perhaps the most celebrated feature, VA loans typically do not require a down payment, provided the home& sales price doesn& exceed its appraised value and the loan amount is within the borrower& entitlement limits. This removes a major barrier to entry for many homebuyers.

No Private Mortgage Insurance (PMI)

Even without a down payment, VA loans do not require PMI. This contrasts sharply with conventional loans (where PMI is usually required for down payments under 20%) and FHA loans (which have upfront and annual mortgage insurance premiums). Eliminating PMI can save borrowers hundreds of dollars monthly.

Competitive Interest Rates

Due to the VA& guarantee reducing risk for lenders, VA loans often feature interest rates that are as low as, or even lower than, conventional mortgage rates. This translates to lower monthly payments and less interest paid over the life of the loan.

Limits on Closing Costs & Seller Concessions

The VA limits the types and amounts of closing costs that lenders can charge veteran borrowers. Furthermore, VA guidelines

0 notes

Text

Unlocking the Full Power of VA Home Loans

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Navigate benefits, myths, hidden rules, and pitfalls for maximum advantage.

The VA home loan program, guaranteed by the U.S. Department of Veterans Affairs, stands as one of the most significant and advantageous benefits available to eligible active-duty personnel, veterans, National Guard members, Reserve members, and certain surviving spouses. While often lauded for its well-known features, a deeper understanding reveals nuances, lesser-known opportunities, and potential pitfalls that can dramatically impact a homebuyer& experience. This guide delves into the comprehensive landscape of VA loans, from core benefits to hidden guidelines critical for success.

Highlights: Key VA Loan Advantages

No Down Payment & No PMI: Qualified borrowers can often finance 100% of a home& purchase price without needing Private Mortgage Insurance (PMI), offering substantial upfront and monthly savings compared to conventional or FHA loans.

Lifelong, Reusable Benefit: Eligibility for a VA loan isn& a one-time deal. Veterans can use the benefit multiple times throughout their lives, potentially even holding more than one VA loan simultaneously under certain entitlement conditions.

Flexible Guidelines & Competitive Terms: The program features competitive interest rates, often lower than conventional options, flexible credit requirements, and limits on allowable closing costs, making homeownership more accessible. Sellers can also contribute significantly towards closing costs.

Core Features: The Foundation of VA Loan Power

Understanding the fundamental benefits of VA loans is the first step towards leveraging this powerful program.

VA loans provide significant advantages for eligible veterans and service members seeking homeownership.

Financial Advantages

Zero Down Payment

Perhaps the most celebrated feature, VA loans typically do not require a down payment, provided the home& sales price doesn& exceed its appraised value and the loan amount is within the borrower& entitlement limits. This removes a major barrier to entry for many homebuyers.

No Private Mortgage Insurance (PMI)

Even without a down payment, VA loans do not require PMI. This contrasts sharply with conventional loans (where PMI is usually required for down payments under 20%) and FHA loans (which have upfront and annual mortgage insurance premiums). Eliminating PMI can save borrowers hundreds of dollars monthly.

Competitive Interest Rates

Due to the VA& guarantee reducing risk for lenders, VA loans often feature interest rates that are as low as, or even lower than, conventional mortgage rates. This translates to lower monthly payments and less interest paid over the life of the loan.

Limits on Closing Costs & Seller Concessions

The VA limits the types and amounts of closing costs that lenders can charge veteran borrowers. Furthermore, VA guidelines

0 notes

Text

Unlocking the Full Power of VA Home Loans

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Navigate benefits, myths, hidden rules, and pitfalls for maximum advantage.

The VA home loan program, guaranteed by the U.S. Department of Veterans Affairs, stands as one of the most significant and advantageous benefits available to eligible active-duty personnel, veterans, National Guard members, Reserve members, and certain surviving spouses. While often lauded for its well-known features, a deeper understanding reveals nuances, lesser-known opportunities, and potential pitfalls that can dramatically impact a homebuyer& experience. This guide delves into the comprehensive landscape of VA loans, from core benefits to hidden guidelines critical for success.

Highlights: Key VA Loan Advantages

No Down Payment & No PMI: Qualified borrowers can often finance 100% of a home& purchase price without needing Private Mortgage Insurance (PMI), offering substantial upfront and monthly savings compared to conventional or FHA loans.

Lifelong, Reusable Benefit: Eligibility for a VA loan isn& a one-time deal. Veterans can use the benefit multiple times throughout their lives, potentially even holding more than one VA loan simultaneously under certain entitlement conditions.

Flexible Guidelines & Competitive Terms: The program features competitive interest rates, often lower than conventional options, flexible credit requirements, and limits on allowable closing costs, making homeownership more accessible. Sellers can also contribute significantly towards closing costs.

Core Features: The Foundation of VA Loan Power

Understanding the fundamental benefits of VA loans is the first step towards leveraging this powerful program.

VA loans provide significant advantages for eligible veterans and service members seeking homeownership.

Financial Advantages

Zero Down Payment

Perhaps the most celebrated feature, VA loans typically do not require a down payment, provided the home& sales price doesn& exceed its appraised value and the loan amount is within the borrower& entitlement limits. This removes a major barrier to entry for many homebuyers.

No Private Mortgage Insurance (PMI)

Even without a down payment, VA loans do not require PMI. This contrasts sharply with conventional loans (where PMI is usually required for down payments under 20%) and FHA loans (which have upfront and annual mortgage insurance premiums). Eliminating PMI can save borrowers hundreds of dollars monthly.

Competitive Interest Rates

Due to the VA& guarantee reducing risk for lenders, VA loans often feature interest rates that are as low as, or even lower than, conventional mortgage rates. This translates to lower monthly payments and less interest paid over the life of the loan.

Limits on Closing Costs & Seller Concessions

The VA limits the types and amounts of closing costs that lenders can charge veteran borrowers. Furthermore, VA guidelines

0 notes

Text

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Navigate benefits, myths, hidden rules, and pitfalls for maximum advantage.

The VA home loan program, guaranteed by the U.S. Department of Veterans Affairs, stands as one of the most significant and advantageous benefits available to eligible active-duty personnel, veterans, National Guard members, Reserve members, and certain surviving spouses. While often lauded for its well-known features, a deeper understanding reveals nuances, lesser-known opportunities, and potential pitfalls that can dramatically impact a homebuyer& experience. This guide delves into the comprehensive landscape of VA loans, from core benefits to hidden guidelines critical for success.

Highlights: Key VA Loan Advantages

No Down Payment & No PMI: Qualified borrowers can often finance 100% of a home& purchase price without needing Private Mortgage Insurance (PMI), offering substantial upfront and monthly savings compared to conventional or FHA loans.

Lifelong, Reusable Benefit: Eligibility for a VA loan isn& a one-time deal. Veterans can use the benefit multiple times throughout their lives, potentially even holding more than one VA loan simultaneously under certain entitlement conditions.

Flexible Guidelines & Competitive Terms: The program features competitive interest rates, often lower than conventional options, flexible credit requirements, and limits on allowable closing costs, making homeownership more accessible. Sellers can also contribute significantly towards closing costs.

Core Features: The Foundation of VA Loan Power

Understanding the fundamental benefits of VA loans is the first step towards leveraging this powerful program.

VA loans provide significant advantages for eligible veterans and service members seeking homeownership.

Financial Advantages

Zero Down Payment

Perhaps the most celebrated feature, VA loans typically do not require a down payment, provided the home& sales price doesn& exceed its appraised value and the loan amount is within the borrower& entitlement limits. This removes a major barrier to entry for many homebuyers.

No Private Mortgage Insurance (PMI)

Even without a down payment, VA loans do not require PMI. This contrasts sharply with conventional loans (where PMI is usually required for down payments under 20%) and FHA loans (which have upfront and annual mortgage insurance premiums). Eliminating PMI can save borrowers hundreds of dollars monthly.

Competitive Interest Rates

Due to the VA& guarantee reducing risk for lenders, VA loans often feature interest rates that are as low as, or even lower than, conventional mortgage rates. This translates to lower monthly payments and less interest paid over the life of the loan.

Limits on Closing Costs & Seller Concessions

The VA limits the types and amounts of closing costs that lenders can charge veteran borrowers. Furthermore, VA guidelines

0 notes

Text

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Unlocking the Full Power of VA Home Loans: Beyond the Basics

Navigate benefits, myths, hidden rules, and pitfalls for maximum advantage.

The VA home loan program, guaranteed by the U.S. Department of Veterans Affairs, stands as one of the most significant and advantageous benefits available to eligible active-duty personnel, veterans, National Guard members, Reserve members, and certain surviving spouses. While often lauded for its well-known features, a deeper understanding reveals nuances, lesser-known opportunities, and potential pitfalls that can dramatically impact a homebuyer& experience. This guide delves into the comprehensive landscape of VA loans, from core benefits to hidden guidelines critical for success.

Highlights: Key VA Loan Advantages

No Down Payment & No PMI: Qualified borrowers can often finance 100% of a home& purchase price without needing Private Mortgage Insurance (PMI), offering substantial upfront and monthly savings compared to conventional or FHA loans.

Lifelong, Reusable Benefit: Eligibility for a VA loan isn& a one-time deal. Veterans can use the benefit multiple times throughout their lives, potentially even holding more than one VA loan simultaneously under certain entitlement conditions.

Flexible Guidelines & Competitive Terms: The program features competitive interest rates, often lower than conventional options, flexible credit requirements, and limits on allowable closing costs, making homeownership more accessible. Sellers can also contribute significantly towards closing costs.

Core Features: The Foundation of VA Loan Power

Understanding the fundamental benefits of VA loans is the first step towards leveraging this powerful program.

VA loans provide significant advantages for eligible veterans and service members seeking homeownership.

Financial Advantages

Zero Down Payment

Perhaps the most celebrated feature, VA loans typically do not require a down payment, provided the home& sales price doesn& exceed its appraised value and the loan amount is within the borrower& entitlement limits. This removes a major barrier to entry for many homebuyers.

No Private Mortgage Insurance (PMI)

Even without a down payment, VA loans do not require PMI. This contrasts sharply with conventional loans (where PMI is usually required for down payments under 20%) and FHA loans (which have upfront and annual mortgage insurance premiums). Eliminating PMI can save borrowers hundreds of dollars monthly.

Competitive Interest Rates

Due to the VA& guarantee reducing risk for lenders, VA loans often feature interest rates that are as low as, or even lower than, conventional mortgage rates. This translates to lower monthly payments and less interest paid over the life of the loan.

Limits on Closing Costs & Seller Concessions

The VA limits the types and amounts of closing costs that lenders can charge veteran borrowers. Furthermore, VA guidelines

0 notes

Text

Kentucky FHA Loan Requirements

Kentucky FHA Mortgage Loan Lender Guidelines Kentucky FHA Loan Requirements The requirements for Kentucky FHA loans are set by HUD. Borrowers must have a steady employment history of the last two years within the same industry or line of work. Recent college graduates can use their transcripts to supplant the 2-year work history rule as long as it makes sense. Self-Employed will need a 2-year…

View On WordPress

#Appraisers FHA#bad credit fha loan#collections fha loan#credit scores fha loan#FHA#fha $100 down program#fha appraisals#FHA Approved Condos Louisville Kentucky#FHA Back to Work Program Ky#fha borrowers#FHA Co-signors#fha collections#fha credit score#fha foreclosure#FHA Guidelines#First-time buyer#Kentucky

0 notes

Text

All Types of Home Loans (Conventional, FHA, Jumbo, VA, USDA Loans) in Dallas, TX

Buying a home in Dallas, TX, is an exciting journey, but navigating the various home loan options can be overwhelming. Whether you're a first-time homebuyer or looking to refinance, understanding the different types of home loans available—including Conventional, FHA, Jumbo, VA, and USDA loans—can help you make the best financial decision. At Edge Home Finance Inc, we specialize in guiding borrowers through the mortgage process, ensuring they secure the best loan for their needs. In this guide, we’ll break down each loan type, their benefits, and how they can help you purchase your dream home in Dallas.

1. Conventional Loans: Flexible Financing for Strong Credit

Conventional loans are one of the most popular mortgage options, backed by private lenders rather than government agencies. These loans are ideal for borrowers with good to excellent credit (typically 620 or higher) and a stable income.

Key Features of Conventional Loans in Dallas:

Down Payment Options: As low as 3% for qualified buyers (though 20% avoids PMI).

Loan Limits: Up to $766,550 for 2024 in Dallas (conforming loan limits).

Flexible Terms: 15-, 20-, or 30-year fixed-rate or adjustable-rate options.

If you have strong credit and want to avoid mortgage insurance or secure competitive interest rates, a Conventional loan from Edge Home Finance Inc may be the best choice.

2. FHA Loans: Low Down Payment & Lenient Credit Requirements

For buyers with lower credit scores or limited savings, an FHA loan (insured by the Federal Housing Administration) provides an accessible path to homeownership.

Why Choose an FHA Loan in Dallas?

Low Down Payment: Just 3.5% with a credit score of 580+ (or 10% for 500-579).

Easier Credit Approval: More forgiving of past financial challenges.

Competitive Rates: Often lower than Conventional loans for buyers with lower credit.

Edge Home Finance Inc helps many first-time buyers and those with limited funds secure FHA loans with minimal hassle.

3. Jumbo Loans: Financing High-Value Dallas Homes

If you’re looking to buy a luxury home in Dallas that exceeds conforming loan limits, a Jumbo loan is the solution. These loans finance properties above $766,550 (as of 2024) and require strong financial credentials.

Jumbo Loan Highlights:

Higher Loan Amounts: Covers luxury homes in Dallas’s upscale neighborhoods.

Strict Requirements: Excellent credit (700+), low debt-to-income ratio, and significant reserves.

Competitive Terms: Fixed or adjustable rates available.

Edge Home Finance Inc works with high-net-worth buyers to secure Jumbo loans with favorable terms.

4. VA Loans: Zero Down Payment for Veterans & Military

Active-duty service members, veterans, and eligible spouses can benefit from VA loans, backed by the U.S. Department of Veterans Affairs.

Advantages of VA Loans in Dallas:

No Down Payment Required: 100% financing available.

No PMI: Lower monthly payments compared to Conventional loans.

Flexible Credit Guidelines: Easier approval for qualified borrowers.

At Edge Home Finance Inc, we honor veterans by helping them secure VA loans with unbeatable benefits.

5. USDA Loans: Affordable Rural & Suburban Homeownership

The USDA loan program supports low-to-moderate-income buyers in eligible rural and suburban areas around Dallas.

Why Consider a USDA Loan?

Zero Down Payment: 100% financing for qualified buyers.

Low Mortgage Insurance: Lower costs than FHA loans.

Income & Location Eligibility: Must meet USDA property and income limits.

Edge Home Finance Inc helps buyers explore USDA loan options in Dallas’s qualifying areas.

6. Comparing Home Loan Options in Dallas, TX

Choosing the right loan depends on your financial situation, credit score, and homebuying goals. Here’s a quick comparison:Loan TypeDown PaymentCredit ScoreBest ForConventional3%-20%620+Buyers with strong creditFHA3.5%-10%500+First-time buyers, lower creditJumbo10%-20%+700+Luxury home purchasesVA0%VariesVeterans & militaryUSDA0%640+Rural/suburban buyers

7. Why Choose Edge Home Finance Inc for Your Dallas Home Loan?

At Edge Home Finance Inc, we simplify the mortgage process by:

Offering personalized loan recommendations based on your needs.

Providing competitive rates and fast approvals.

Guiding you through pre-approval to closing with expert support.

Whether you need a Conventional, FHA, Jumbo, VA, or USDA loan, we’re here to help you secure the best financing in Dallas.

8. Get Started on Your Dallas Home Loan Today!

Ready to buy a home in Dallas? Edge Home Finance Inc makes it easy with tailored loan solutions. Contact us today to explore your options and get pre-approved for the perfect mortgage!

By understanding the different types of home loans in Dallas, TX, you can confidently choose the best financing path. Let Edge Home Finance Inc be your trusted partner in homeownership!

0 notes

Text

Manufactured Home Loans in Texas: A Complete Guide to Financing Your Dream Home

Manufactured homes have become an affordable and practical housing solution for many Texans. Whether you're a first-time homebuyer or looking for a cost-effective alternative to traditional site-built homes, manufactured homes provide a range of benefits, including lower costs, energy efficiency, and quicker construction timelines. However, financing a manufactured home differs from securing a conventional mortgage. This guide explores Manufactured Home Loans in Texas, covering available loan options, eligibility criteria, benefits, and tips for securing the best financing.

Understanding Manufactured Homes and Loan Types

A manufactured home is a factory-built home constructed after June 15, 1976, adhering to the HUD (Department of Housing and Urban Development) code. These homes are often confused with modular homes, but the key distinction is that manufactured homes are built on a permanent chassis and can be transported, while modular homes are assembled on-site in sections.

Financing a manufactured home requires specialized loan programs that accommodate their unique structure and ownership status. Below are the most common loan options available:

1. FHA Manufactured Home Loans

The Federal Housing Administration (FHA) loan is a government-backed option that provides lower down payment requirements and flexible credit criteria. To qualify, the manufactured home must be permanently affixed to the land and classified as real property.

Minimum Down Payment: 3.5% (with a credit score of at least 580)

Loan Term: Up to 30 years

Occupancy Requirement: Must be the borrower’s primary residence

Foundation Requirement: Must be placed on a permanent foundation

2. VA Manufactured Home Loans

For veterans, active-duty service members, and eligible surviving spouses, the VA loan program offers a great opportunity to finance a manufactured home with zero down payment and no private mortgage insurance (PMI).

No Down Payment Required (for qualified applicants)

Competitive Interest Rates

No Private Mortgage Insurance (PMI)

Must Meet VA Standards for Permanent Foundation

3. USDA Manufactured Home Loans

If you’re looking to purchase a manufactured home in a rural area of Texas, the USDA loan program offers 100% financing with favorable terms.

Zero Down Payment Required

Low Interest Rates

Income Limits Apply

Home Must Meet USDA Property Standards

4. Chattel Loans

A chattel loan is a personal property loan that finances the home itself but not the land. This option is suitable for buyers who plan to place their home on leased land, in a mobile home park, or on family property.

Shorter Loan Terms (15-20 years)

Higher Interest Rates than Traditional Mortgages

No Land Ownership Required

5. Conventional Loans for Manufactured Homes

Some lenders offer conventional mortgage loans for manufactured homes that meet Fannie Mae and Freddie Mac requirements.

Minimum Credit Score of 620

Down Payment of at Least 5%

Home Must Be Titled as Real Property

Must Meet HUD Construction and Safety Standards

Eligibility Requirements for Manufactured Home Loans in Texas

Securing a manufactured home loan in Texas requires meeting specific eligibility criteria. These requirements vary depending on the type of loan but generally include factors related to property classification, credit score, down payment, foundation, home age, and land ownership. Below is a detailed breakdown of these essential qualifications:

Property Classification: For most loan types, the manufactured home must be classified as real property. This means the home must be permanently affixed to a foundation and owned along with the land it sits on. If the home is classified as personal property, financing options may be more limited.

Minimum Credit Score: Lenders assess borrowers based on their credit history. Typical credit score requirements include:

FHA Loans: Minimum 580

Conventional Loans: Minimum 620

Chattel Loans: Often require a higher credit score

A higher credit score can improve loan approval chances and lead to more favorable interest rates.

Down Payment Requirements: The required down payment varies depending on the loan program:

VA and USDA Loans: 0% down payment (for eligible borrowers)

FHA Loans: As low as 3.5%

Conventional Loans: Typically 5%-20%

Chattel Loans: Often require 20% or more due to the perceived risk of financing personal property

Foundation Type: Most mortgage-backed loans require the manufactured home to be installed on a permanent foundation that complies with federal and state regulations. A non-permanent foundation may limit financing options to chattel or personal property loans.

Age of the Home: Manufactured homes must meet the HUD (U.S. Department of Housing and Urban Development) standards established on June 15, 1976. Homes built before this date may not qualify for most loan programs due to outdated construction codes and safety concerns.

Land Ownership: Some loan programs, particularly FHA, VA, and conventional loans, require borrowers to own the land where the manufactured home is placed. However, chattel loans can finance a manufactured home located on leased land, such as in mobile home parks.

Meeting these eligibility requirements is crucial for securing the right financing option for a manufactured home in Texas. Consulting with lenders who specialize in manufactured home loans can help determine the best loan program based on individual financial situations and property conditions.

Benefits of Manufactured Home Loans in Texas

Affordability – Manufactured homes cost significantly less than site-built homes, making homeownership more accessible.

Flexible Financing Options – Various loan programs cater to different financial situations, including zero-down payment loans for eligible borrowers.

Quick Home Setup – Since these homes are factory-built, construction and delivery take much less time than traditional homes.

Energy Efficiency – Many modern manufactured homes come with energy-efficient features, reducing utility costs.

Customization – Buyers can choose from various layouts, finishes, and features to suit their needs.

Tips for Securing the Best Manufactured Home Loan

Improve Your Credit Score – A higher credit score can help you secure better interest rates and loan terms.

Save for a Down Payment – While some loans offer no-down-payment options, having a larger down payment can reduce monthly mortgage costs.

Shop Around for Lenders – Not all lenders offer the same loan terms. Compare different lenders specializing in manufactured home loans in Texas.

Ensure the Home Meets HUD Standards – Homes that comply with HUD safety and construction standards have a higher chance of qualifying for favorable loan terms.

Consider Land Ownership – If you plan to finance both the home and the land, you may qualify for better mortgage options.

Work with a Mortgage Specialist – A lender experienced in manufactured home loans can guide you through the process and help you secure the best financing option.

Why Choose Clear Lending for Manufactured Home Loans in Texas?

When it comes to securing financing for a manufactured home in Texas, choosing the right lender is crucial. Clear Lending stands out as a top choice for borrowers looking for flexible loan options, competitive rates, and exceptional customer service. Here’s why Clear Lending should be your preferred partner for manufactured home loans:

Expertise in Manufactured Home Financing Clear Lending specializes in providing tailored loan solutions for manufactured homes. Unlike traditional lenders who may have limited experience with these properties, Clear Lending understands the unique requirements, challenges, and financial nuances associated with manufactured home financing. This expertise allows borrowers to navigate the loan process smoothly.

Diverse Loan Programs Whether you’re looking for an FHA, VA, USDA, conventional, or chattel loan, Clear Lending offers multiple financing options to suit different needs and budgets. The availability of diverse loan programs ensures that borrowers can find the best fit based on their financial situation, home type, and land ownership status.

Competitive Interest Rates & Flexible Terms One of the most important factors in choosing a lender is affordability. Clear Lending provides competitive interest rates and flexible loan terms to make homeownership more accessible. With low down payment options and customized repayment plans, borrowers can secure loans that align with their long-term financial goals.

Streamlined Application & Fast Approvals Time is valuable, and Clear Lending understands the importance of a quick and hassle-free loan process. The application process is designed to be straightforward, with fast pre-approvals and efficient loan processing. This ensures that borrowers can move forward with their home purchase without unnecessary delays.

Personalized Customer Service At Clear Lending, every borrower receives personalized attention. The team takes the time to understand each client’s financial situation, homeownership goals, and concerns, providing tailored guidance throughout the process. From explaining loan options to assisting with paperwork, Clear Lending prioritizes a smooth and stress-free experience.

Lenient Eligibility Criteria Manufactured home financing often comes with strict requirements, but Clear Lending offers flexible eligibility criteria to help more buyers qualify. Whether it’s lower credit score thresholds, alternative documentation acceptance, or accommodating self-employed borrowers, Clear Lending works to make homeownership accessible to a wider range of applicants.

Assistance for First-Time Homebuyers Purchasing a manufactured home can be overwhelming, especially for first-time buyers. Clear Lending provides step-by-step guidance to help new homeowners understand loan terms, eligibility requirements, and repayment structures. The team also assists with down payment options and special programs designed to support first-time buyers.

Transparency & Trust Clear Lending is committed to transparency in all dealings. There are no hidden fees or surprises—borrowers receive clear information about loan terms, closing costs, and interest rates upfront. This honesty builds trust and ensures borrowers make informed decisions.

Serving Borrowers Across Texas Whether you’re purchasing a manufactured home in Houston, Dallas, Austin, San Antonio, or any other part of Texas, Clear Lending provides state-wide coverage. The lender’s deep understanding of Texas-specific housing regulations ensures borrowers receive loans that comply with local and federal guidelines.

Ongoing Support Even After Closing Clear Lending doesn’t just stop at loan approval. The team provides ongoing support, answering any questions borrowers may have post-closing. Whether it’s understanding refinancing options, handling payment schedules, or managing loan modifications, Clear Lending remains a reliable partner throughout homeownership.

Secure Your Manufactured Home Loan with Clear Lending

Choosing the right lender makes all the difference in achieving homeownership with ease. With its extensive experience, flexible loan options, competitive rates, and commitment to customer satisfaction, Clear Lending is a trusted partner for securing manufactured home loans in Texas. Contact Clear Lending today to explore your options and take the next step toward owning a manufactured home!

Conclusion

Purchasing a manufactured home in Texas is a great way to achieve homeownership at an affordable price. With multiple financing options available, including FHA, VA, USDA, conventional, and chattel loans, buyers can find a program that fits their financial situation. Understanding the eligibility criteria, benefits, and key requirements will help ensure a smooth loan approval process. By taking the right steps—improving credit scores, saving for a down payment, and working with experienced lenders—self-employed and first-time buyers alike can successfully finance their dream home.

For more details on Manufactured Home Loans in Texas, visit Clear Lending.

0 notes

Text

Trade-Up Tuesday:

Your Path to Homeownership

with John V. Pinto, Realtor!"

🏡 Exciting first-time homebuyer opportunity alert! Join me, John V. Pinto, Realtor, for this week's **Trade-Up Tuesday** as we explore an incredible chance for renters to become homeowners!

Check out this charming **2-bedroom, 1-bath condo** located at **900 Cambridge Dr. #56 in Benicia**, listed for just **$374,888**! With **1,087 sq. ft.** of comfortable living space, this second-level gem features bamboo laminate floors, a spacious living room, a private balcony, and a beautifully remodeled kitchen. Plus, it comes with essential appliances including a refrigerator, washer, and dryer, along with a convenient one-car carport and ample guest parking.

🌟 Renters, this is your moment! Take advantage of **100% financing**, down payment assistance, and closing cost assistance programs available to help make your homeownership dreams a reality.

Enjoy the best of Benicia with easy access to charming downtown, the vibrant farmers market, and the Vallejo ferry to San Francisco. You’re also just a short drive away from the beautiful wine country of Napa and Sonoma, with quick access to freeways and airports.

👉 Don’t miss this chance! Click to watch my **2½-minute walk-through video** of the condo:

https://youtube.com/shorts/2-2yowjqVho?feature=share

📞 Ready to make the leap? DM me today!

For more information on financing options and assistance programs, DM me at **408-829-4141** so I can connect you with my lender and see what federal, state, municipal, county, and nonprofit down payment assistance programs and closing cost assistance programs you qualify for.

Let’s turn your renting dreams into homeownership reality!

#Benicia #CondoForSale #RealEstate #HomeOwnership #RentersToOwners #FinancingOptions #DownPaymentAssistance #ClosingCostAssistance #VA #FHA #CaliforniaRealEstate #Napa #Sonoma #WineCountry #CharmingDowntown #FarmersMarket #VallejoFerry #SanFrancisco #HomeSweetHome #RealEstateOpportunity #JohnVPintoRealtor #RealtorLife #HouseHunting #NewHome #InvestmentProperty #HomeBuyer #RealEstateInvesting #DreamHome #CondoLiving #HomeGoals #CaliforniaLiving #RealEstateVideo #WalkthroughTour #PropertyListing #HomeForSale

📞 Ready to make the leap? DM me today!

0 notes

Text

Content writing project: MoneyGeek

From November 2021 to April 2023, I worked with MoneyGeek, a U.S.-based personal finance company and wrote more than 100 articles about housing, loans, credit cards, and insurance.

If you want to avoid clicking away, I've copied a segment from an article I've written:

What Is a First-Time Homebuyer Program & How Can It Help?

Before you even purchase a home, it’s wise to look at the expenses you need to anticipate. One of the largest costs you need to consider is your mortgage down payment.

A mortgage down payment is an important aspect of the homebuying process, especially since it can affect your monthly expenses. For example, having a higher down payment upfront can lower your monthly payments since you’ll pay less interest.

The down payment is usually 20% of your home’s total cost, which can be a bit expensive for some. Hence, homebuyer assistance programs are worth looking into if you need a more affordable rate.

Generally, there are zero-down-payment programs (USDA and VA loans) and low-down-payment programs (conventional, FHA and FHA 203(k) loans). Alaska has several statewide loan programs, including the Closing Cost Assistance loan program.

While there are many options, the best homebuyer program for you depends on your financial background and needs. For example, a government-backed loan doesn’t typically require homebuyers to have a down payment.

––––––

Other writing projects include:

0 notes

Text

Single Mother Grants Texas

Navigating the world of homeownership can be daunting, especially for single mothers and fathers. In Texas, numerous resources and programs exist to help make this dream a reality. Whether you're seeking financial assistance or favorable loan terms, understanding your options is crucial. This guide will explore various home loans designed specifically for single parents, including FHA, VA, USDA loans and state-run programs. Discover how grants can lighten your load while ensuring you find a safe haven for your family in the Lone Star State.

Understanding home loans for single moms and dads

Home loans for single parents are tailored to meet unique financial needs. With various options available, understanding the different types can empower you in your search for a home. Programs like FHA and VA loans offer lower down payments and more lenient credit requirements, making them accessible. Additionally, USDA loans focus on rural properties and support families with limited income. State-run home loan programs often provide even more benefits specifically designed for residents of Texas, ensuring that single moms and dads have the resources needed to secure safe housing.

FHA loans

FHA loans are government-backed mortgages designed to support low-to-moderate-income borrowers, including single mothers. They require a lower down payment—often as little as 3.5%—making homeownership more accessible for those with limited savings. These loans come with flexible credit score requirements, which can be advantageous for single parents who may have faced financial challenges. With the FHA's backing, lenders are more willing to take risks on applicants who might not qualify for conventional loans. This makes FHA loans a popular option among single moms seeking stable housing in Texas and beyond.

VA loans

VA loans are a fantastic option for eligible veterans and active-duty service members, including single parents in Texas. These loans offer competitive interest rates and require no down payment, making homeownership more accessible. Additionally, VA loans do not mandate private mortgage insurance (PMI), resulting in lower monthly payments. The flexibility of credit requirements further enhances the appeal for single mothers seeking stable housing solutions. Understanding these benefits can help navigate the path to securing your dream home with ease.

USDA loans

USDA loans are designed to assist low- and moderate-income families in rural areas. These loans offer 100% financing, meaning no down payment is required, making homeownership more accessible for single parents. Eligibility typically depends on income levels and property location. The program aims to improve the quality of life in rural communities by promoting homeownership. Single mothers can benefit significantly from this opportunity, as it opens doors to affordable housing solutions while fostering stable living conditions for their children.

State-run home loan programs

State-run home loan programs are tailored specifically for residents, including single mothers and fathers. These initiatives often provide favorable terms such as lower interest rates, reduced down payments, or even grants to help cover closing costs. Programs vary widely by state, so researching local options is essential. In Texas, the Texas Department of Housing and Community Affairs (TDHCA) offers several assistance programs. They aim to make homeownership more achievable for families with limited income. Many of these resources focus on empowering single parents through financial stability and housing security.

Types of home loans for single moms

Single moms have various home loan options tailored to their needs. Programs like Good Neighbor Next Door offer substantial discounts for eligible public servants, while the National Homebuyers Fund provides down payment assistance. These initiatives can ease the financial strain of buying a home. Additionally, single mothers may benefit from programs such as the Housing Choice Voucher Program and Homeownership for Public Housing Residents. State and local grants also present opportunities for financial aid. Organizations like Habitat for Humanity and Operation Hope further support single parents in securing stable housing through affordable financing solutions.

Good Neighbor Next Door

The Good Neighbor Next Door program offers substantial benefits for eligible single mothers. This initiative is designed to help law enforcement officers, teachers, firefighters, and EMTs buy homes in revitalization areas at a steep discount—50% off the listing price. To qualify, participants must commit to living in the home for 36 months after purchase. The properties often require some renovation but provide an excellent opportunity for affordable housing. Single moms working in these fields can take advantage of this unique chance to invest in their future and secure stable housing for their families.

National Homebuyers Fund

The National Homebuyers Fund (NHF) offers assistance to first-time homebuyers, including single mothers. This program provides down payment and closing cost assistance, making homeownership more accessible. The NHF’s grants can cover up to 5% of the loan amount. Eligible applicants can use these funds with various mortgage types, including FHA and conventional loans. The support is designed to empower families by easing financial burdens associated with buying a home. This initiative helps single parents create stable living environments for their children while investing in their futures.

Housing Choice Voucher Program

The Housing Choice Voucher Program, administered by the U. S. Department of Housing and Urban Development (HUD), assists low-income families, including single mothers, in affording safe housing. Participants receive vouchers to help cover a portion of their rent in privately-owned homes or apartments. Eligible applicants can find landlords willing to accept these vouchers, which makes it easier for them to secure affordable housing options. The program emphasizes tenant choice while ensuring that recipients live in decent conditions without exceeding their financial limits on rent payments.

Homeownership for Public Housing Residents

Homeownership for Public Housing Residents is a program designed to assist families living in public housing achieve their dream of owning a home. This initiative allows eligible residents the opportunity to buy their homes at a reduced price, fostering stability and community growth. Participants can benefit from various resources such as financial education, counseling services, and access to favorable mortgage rates. These support systems are aimed at preparing families for the responsibilities of homeownership while ensuring they can transition smoothly from renting to owning without overwhelming financial burden.

State and local grants

State and local grants provide vital support for single mothers seeking homeownership. Various programs are available, tailored to help families achieve stability through housing assistance. These grants often cover down payments or closing costs, making home purchases more feasible. Eligibility requirements vary by location and program, ensuring that those in need receive the necessary financial aid. Prospective homeowners should research specific state and local options to find the best fit for their situation. Many states also offer resources online to assist with applications and eligibility checks.

Habitat for Humanity

Habitat for Humanity is a nonprofit organization dedicated to providing affordable housing solutions. They partner with families in need, including single mothers, to build and renovate homes. Through volunteer labor and donations, they help create safe living environments. Eligible applicants can benefit from low-interest loans or sweat equity programs. Families actively participate in the construction process, ultimately gaining ownership of their home. This initiative not only fosters community but also empowers individuals by giving them a hand up rather than a handout. It’s an excellent option for those seeking stability and security in their housing situation.

Operation Hope

Operation Hope is a nonprofit organization dedicated to providing financial education and support for individuals in need, including single mothers. They offer various programs designed to empower families through economic opportunities and homeownership assistance. Single moms can access resources such as credit counseling, budgeting workshops, and even down payment assistance. By focusing on personal finance skills, Operation Hope aims to help families achieve sustainable financial stability while navigating the challenges of home buying. Their services are tailored to meet the unique needs of single parents striving for a better future.

Eligibility Criteria

Eligibility criteria for single mother grants can vary widely based on the specific program. Generally, applicants must demonstrate financial need, which may involve income limits and household size considerations. Many programs require proof of residency in Texas. Additionally, some grants target specific groups such as military veterans or public housing residents. Applicants might also need to show a good credit history or meet employment requirements to qualify for certain home loans or grant opportunities tailored for single mothers seeking assistance. Always check individual program guidelines for precise eligibility details.

Documents Required

When applying for single mother grants in Texas, several documents are essential. You’ll typically need proof of income, such as pay stubs or tax returns, to demonstrate your financial situation. Other vital papers include identification documentation like a driver’s license or Social Security card. Additionally, lenders may request bank statements and monthly expense records. If you’re applying through specific programs, eligibility letters from local agencies might also be necessary. Be prepared with all requested information to streamline the application process effectively and increase your chances of approval.

Application Process

Applying for single mother grants in Texas involves several key steps. First, gather all necessary documents, such as proof of income, identification, and residency status. Completing the application form accurately is crucial to avoid delays. Next, submit your application through the appropriate channels—either online or in person at designated offices. Be prepared for any follow-up interviews or additional documentation requests. Always keep copies of everything you send out. Staying organized will help ensure a smoother process as you seek financial assistance for housing needs.

Oraganizations that provide assistance

Numerous organizations offer assistance to single mothers seeking housing. The United Way is a nonprofit that helps families access resources, including housing support and financial literacy programs. They often partner with local agencies to provide targeted help. Another valuable resource is the National Low Income Housing Coalition, which advocates for affordable housing solutions and connects renters with various assistance options. Local nonprofits like Interfaith Ministries can also guide single parents through available grants and services tailored to their needs. Reaching out to these organizations can open doors to vital support systems.

Conclusion

Single parents in Texas have access to various resources aimed at easing the burden of homeownership. From federal loan programs to local grants, there are multiple pathways to secure financial assistance. Exploring these options can lead you toward fulfilling your dream of owning a home. Staying informed about single mother grants and other support systems is crucial. By understanding eligibility criteria and application processes, you're better equipped to take the next steps toward securing housing for yourself and your family. Your journey begins with knowledge and determination, leading you closer to stability and success.

FAQs

Navigating the world of home loans and grants can be overwhelming for single parents in Texas. However, numerous resources are available to assist you on this journey. What grants are available specifically for single mothers in Texas? Single mothers in Texas can access various grants such as those from the National Homebuyers Fund or state-specific initiatives aimed at helping low-income families buy homes. How do I qualify for FHA loans? To qualify for an FHA loan, borrowers typically need a credit score of at least 580 with a 3.5% down payment or 500-579 with a 10% down payment while meeting income requirements. Are there any special programs for veterans who are single parents? Yes! VA loans offer specialized benefits to veterans which include no down payment options and lower interest rates making them ideal even for single-parent households. How long does the application process take? The application process varies by program but generally takes about 30-45 days once all necessary documentation is submitted properly. Can I combine different types of assistance? Yes! Many applicants successfully combine several programs like state-run grants with federal loan options enhancing their chances of securing affordable housing solutions.

0 notes