#finnext

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr posted its first advertisements in May 2012 and subsequently earned $13M in revenue.

Text

AI-Driven Personalization

AI-Driven Personalization: Redefining the Banking Landscape with Datavision’s Banking Software Solutions

In the fast-paced world of financial technology, the influence of Artificial Intelligence (AI) in shaping and driving the future of banking is undeniable. With its ability to analyze, learn from, and act on data, AI is transforming banking from a transaction-driven to an experience-driven sector.

Table of Contents Introduction to AI in Banking Transforming Customer Experience with AI AI in Risk Assessment and Fraud Detection Intelligent Automation with AI in Banking Data Analysis and Predictive Analytics with AI The Challenges of Implementing AI in Banking The Future of AI in Banking Conclusion FAQs How Can Datavision Help?

Introduction to AI in Banking In the fast-paced world of financial technology, the influence of Artificial Intelligence (AI) in shaping and driving the future of banking is undeniable. With its ability to analyze, learn from, and act on data, AI is transforming banking from a transaction-driven to an experience-driven sector.

Datavision, a leading banking software company, is spearheading the banking industry’s evolution with its world – class software solutions. Their AI-driven personalization platform is empowering banks to redefine the way they interact with customers, ensuring enhanced engagement, loyalty, and ultimately, a stronger bottom line.

Welcome to the world of advanced banking, where AI-driven personalization is reshaping the financial services landscape! Today, let’s delve into the transformative power of Datavision’s software solutions and their contributions to the banking industry.

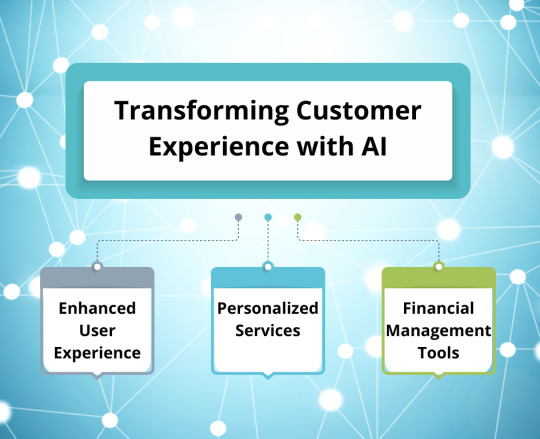

Transforming Customer Experience with AI Enhanced User Experience

Thanks to AI, banks can now provide a more personalized and seamless user experience. Imagine, instead of going through multiple menus, you can ask your banking app to transfer money to a friend. It’s like having a personal assistant tucked away in your pocket!

Personalized Services

From personalized product recommendations to custom-made financial advice, AI enables banks to tailor services to the unique needs of every individual. It’s no longer a one-size-fits-all approach but a bespoke service designed just for you!

Financial Management Tools

AI has also allowed banks to provide customers with tools to manage their finances effectively. These tools can analyze your spending habits, provide insights, and even offer suggestions on how to save more. Isn’t that like having your own financial advisor at your fingertips?

AI in Risk Assessment and Fraud Detection Accurate Risk Profiling

AI algorithms can sift through vast amounts of data to accurately assess a customer’s risk profile. It’s like an eagle-eyed detective spotting potential red flags that human analysts might miss.

Detecting Fraudulent Activities

Fraud detection has also seen a revolutionary shift with AI. The technology can identify patterns, anomalies, and trends in data that can help predict and prevent fraudulent activities. Think of it as your banking bodyguard, protecting your hard-earned money.

Intelligent Automation with AI in Banking

Process Automation

In banking, AI has resulted in more intelligent and faster automation of routine processes. This has improved efficiency and eliminated the chances of human error. Imagine a factory line where each piece of the process works in perfect harmony – that’s what AI brings to banking operations!

Improved Decision Making

AI’s data-driven insights aid in better decision-making in loan approval, investment strategies, or customer service. It’s like having a crystal ball that helps banks make informed choices and avoid pitfalls.

Data Analysis and Predictive Analytics with AI

Data-Driven Decisions

AI allows banks to tap into the gold mine of data they possess. These data insights allow precise decision-making, improving banking operations and customer experience. You can think of it as your GPS, guiding you to your destination with pinpoint accuracy!

Predicting Future Trends

AI’s ability to predict future trends based on past and present data is a game-changer. This can help banks strategize for the future and stay ahead of the curve. It’s like having a time machine giving you a peek into the future!

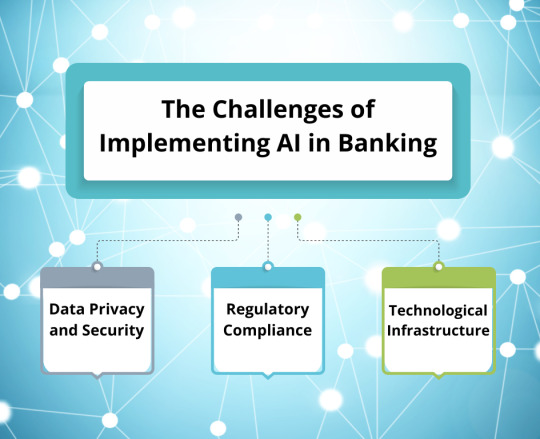

Despite the numerous advantages, AI implementation in banking comes with its own challenges. Ensuring data privacy and security is a paramount concern. After all, who wants their personal information to fall into the wrong hands?

Regulatory Compliance

Adherence to regulations is another major hurdle. How can banks ensure their AI systems comply with the ever-changing legal landscape? It’s like playing a never-ending game of catch-up!

Technological Infrastructure

Lastly, the need for robust technological infrastructure must be addressed. Implementing AI requires significant investment in technology and skilled personnel. So, how can banks strike a balance between innovation and cost-effectiveness?

The Future of AI in Banking Evolving Customer Expectations

As AI continues to evolve, so do customer expectations. Consumers demand instant, personalized, and seamless banking experiences. Will banks be able to keep up with these changing demands?

The Rise of Neobanks and Fintechs

The growth of neo banks and fintech with their AI-first approach poses a serious challenge to traditional banks. Will traditional banks be able to compete, or will they be left behind in the race?

Conclusion AI-driven personalization is redefining the banking landscape. AI’s potential in banking is vast, from transforming customer experience to detecting fraud. However, the journey to fully AI-powered banking is fraught with challenges. Nevertheless, the promise that AI holds is too vast to ignore. After all, who wants banking to be more complex than asking a question to your phone?

The future of banking is here, and it is exciting to witness the positive impact that AI-driven personalization is making on the financial industry. With Datavision’s software solutions leading the way, the possibilities for innovation are boundless, and the banking landscape is set to evolve like never before! So, let’s embrace this revolution and redefine the way we bank with AI-driven personalization. The future is bright, and the time to act is now!

FAQs

Q. What is AI-driven personalization in banking? AI-driven personalization in banking refers to using artificial intelligence to provide personalized banking services based on individual customer needs and preferences.

Q. How does AI improve customer experience in banking? AI improves customer experience in banking by providing personalized services, enhancing user experience with conversational interfaces, and offering intelligent financial management tools.

Q. AI improves customer experience in banking by providing personalized services, enhancing user experience with conversational interfaces, and offering intelligent financial management tools. AI helps in risk assessment by accurately profiling the risk associated with a customer. It aids in fraud detection by identifying patterns, anomalies, and trends that may signify fraudulent activities.

Q. AI helps in risk assessment by accurately profiling the risk associated with a customer. It aids in fraud detection by identifying patterns, anomalies, and trends that may signify fraudulent activities. The challenges of implementing AI in banking include ensuring data privacy and security, adhering to regulatory compliance, and investing in the necessary technological infrastructure and skilled personnel.

Q. How is AI shaping the future of banking? AI is shaping the future of banking by transforming customer experience, enabling accurate risk assessment, automating processes, aiding in data-driven decisions, and predicting future trends.

How Can Datavision help?

We assist various financial institutions and global banks on their digital transformation journey. Our one-of-a-kind approach, which combines people, process, and technology, expedites the delivery of superior results to our clients and drives excellence. Several reputed companies leverage our proprietary suite of business excellence tools and services to unlock new growth levers and unparalleled ROI.

Datavision is a leading Banking software solutions provider having operations in India. We at Datavision are the top retail and Corporate Banking Software provider as we serve our prestigious clients with cutting-edge core application software in Maharashtra and Karnataka, Delhi and Uttar Pradesh.

We provide the best banking software products to our clients in Rajasthan and Gujarat. Get in touch with us for customizable, scalable, and affordable banking software products and solutions.

Our portfolio of banking software product and services include:

Core Banking Solutions: | FinNext Core | Banking: | FinTrade | EasyLoan | MicroFin |

Digital Banking Solutions: | IBanc | MobiBanc | MBranch | FinTab | FinSight |

Payments: | FinPay |

Risk & Compliance: |FinTrust |

Want to know how our team of experts at Datavision provides customizable, scalable, and cost-effective banking software products and solutions to our esteemed clients? Visit us for more information.

#Core Banking Solutions: | FinNext Core | Banking: | FinTrade | EasyLoan | MicroFin |#Digital Banking Solutions: | IBanc | MobiBanc | MBranch | FinTab | FinSight |#Payments: | FinPay |#Risk & Compliance: |FinTrust |

0 notes

Photo

Старший управляющий директор Сбербанка Денис Фонов на FinNext 15 февраля выступит на тему «Будущее финансовых институтов в новой экономике на примере отрасли логистических услуг». Программа форума: http://finnext.ru/. Мероприятие в Facebook: https://www.facebook.com/events/310191266120039/. #fintech #tech #money #Russia #Moscow #Москва #Россия #форум #finnext #финтех #деньги #финансы #инвестиции #инновации #банки #технологии #онлайн #биометрия #Сбербанк #логистика #ДенисФонов (at Moscow, Russia)

#money#биометрия#техно��огии#финансы#денисфонов#moscow#tech#финтех#деньги#форум#russia#логистика#сбербанк#россия#онлайн#finnext#москва#инновации#инвестиции#fintech#банки

0 notes

Text

Will Digital Rupee Replace Your Bitcoin? | FinNext

Will Digital Rupee Replace Your Bitcoin? | FinNext

Updated: 12 Dec 2022, 04:37 PM IST Livemint The RBI’s pilot of India’s legal cryptocurrency ma… moreThe RBI’s pilot of India’s legal cryptocurrency makes everyone excited. But how would this new digital product stack up against your existing digital tokens? Watch a face-to-face comparison between the two in this video! #digitalrupee #cryptocurrency #bitcoin #mint Subscribe Now For Latest Updates-…

View On WordPress

0 notes

Text

Opportunities in the startup space

[ad_1]

IT is a fact that many businesses are crippled in the face of the current pandemic as companies struggle to keep business going. However, new opportunities are also emerging amidst the changing landscape, particularly in the tech startup space.If anything, the current crisis presents startups with a chance to relook their products and business models to cater to a new market.

“This is a good test bed and an opportunity for startups to pivot by being alert to what is happening on the ground and by responding to the real-time environment. Pivots are not new for startups. It is a part of their journey. They just need to ensure that they can sustain it, ” says Cyberview Sdn Bhd’s Siti Shafinaz Mohd Salim.

In a recent webinar organised by Cyberview titled “Startups: Navigating the new norm”, Shafinaz identifies artificial intelligence, Internet of Things (IoT), robotics and smart healthcare as among the upcoming segments that startups can tap into.

As more traditional companies look into digitalisation and automation, startups are primed to offer such solutions.

“We should be hungry at a time like this. Identify where the buying opportunity is in this space. Make use of this new normal and of the emerging technology that is out there.

“It is also a good time for those with ideas to roll out their products.

“If you are a new entrepreneur, I think this is a good time to start out, ” she says.

Her sentiments were echoed by Finnext Capital business director Aizat Rahim and TheLorry co-founder and managing director Nadhir Ashafiq.

Following the announcement of the movement control order (MCO) in March, TheLorry quickly rolled out a new service as it adapted to the changing needs of its customers.

It launched TheLorry Grocer within a week to help cover some of the revenue loss from its consumer business.

Amidst the challenging circumstances, Nadhir points out that there are steps that entrepreneurs can take to reduce some of the pain.

“There are a lot of things that we cannot control. But we can control our expenses. So map out your projections to know your cash position. And if there are ways to get cash in faster, explore that.

“This can include invoice financing or giving your customers a discount if they can pay up faster, ” he says.Nadhir opines that there are also opportunities to tap in the online grocery and food delivery services as well as e-learning, virtual collaboration and cybersecurity.

”Startups have limited resources and they need to pick business verticals that will give them the best return on investment. We are of the opinion that post-MCO, there will still be opportunities in these areas. I think they are long-term opportunities.

“Although some spaces may get crowded, like grocery for example, you can still make money if you have a certain value to offer and have the right database to leverage on, ” he says.

Meanwhile, Aizat notes that startups will also need time to recover once the current situation stabilises.

“Startups will take about 6-12 months to get back to their original projections. And it will be hard to get investments. But venture capitals and investors are still looking for investments.

“They are just more picky with what they invest in now, ” he says.

Aizat advises startups to focus on providing digital products and solutions and to remain flexible.

“Keep testing and trying out new solutions that people want. Also be mindful of your cash position, which is different from your revenue. And if you have a network of supporters like an angel investor, try to get a bridging loan instead of raising funds now because it will be harder to navigate valuations, ” he says.

In coming up with solutions, Aizat also urges startups to understand the needs of their users as much as possible.

“Pick products that serve your database. And be mindful of the user experience as well. That is important to keep users with you. There will be some players that will fall out during this time, but that happens in any industry.

“Keep an eye out on anything that impacts your direct stakeholders like your employees and your customers. “We also ask startups to look at their customers’ customers. You won’t be able to fix all the problems on your own so find partners that can help alleviate their pain points. If your customers’ customers are not doing well, then there’s a chance that your customers will also be in trouble, ” he shares.

Shafinaz adds that with more digital transactions taking place now, there is also a lot more data that can be obtained to help startups better evaluate the feasibility of their products and business plans. This will help them formulate better strategies and solutions as they adapt to the new normal.

“Stay agile. This is a time that startups can learn from, ” she says.That said, these are notably challenging times, even for agile startups. Entrepreneurs will have to remain steadfast in charging forward while keeping their teams and the business together.

“As entrepreneurs, we’re also affected. These are tough times and only tough guys will survive. I’ve had my own breakdowns as well. But do what you can to control what you can.

“Map out what you can and can’t control and work with it. And then find opportunities around you.

“I think there are many examples of entrepreneurs adapting to survive and this shows that entrepreneurs can do it. They are a special breed of people and they’ll find ways to get through, ” says Nadhir.

[ad_2] Source link

from WordPress https://ift.tt/2WWAqAB via IFTTT

0 notes

Text

DataFabric на FinNext-2018

15 февраля 2018 года в Москве с успехом прошел шестой форум финансовых инноваций FinNext. Генеральным продюсером и ведущим 4-й раз подряд выступил Олег Анисимов. Отчетный материал о форуме: http://bit.ly/2EXqwGI. Более 250 фотографий: http://bit.ly/2sKAjen. Следующий форум FinNext состоится в феврале. Подробности на сайте: http://bit.ly/2ETHQwh Форум в Facebook: http://bit.ly/2sEnNwU Форум в Twitter: https://twitter.com/finnextru/ Форум в Instagram: http://bit.ly/2eonAI9. Тег в соцсетях: #finnext DataFabric (информационные системы на основе семантических технологий) DataFabric на FinNext-2018

from DataFabric на FinNext-2018

0 notes

Text

FinNext-2018: итоги Битвы инноваторов

FinNext снова прошёл с грандиозным успехом. В Битве инноваторов победили проекты Arenza.ru (финансирование покупки оборудования для малого и среднего бизнеса), Platforma (площадка для инвестиций в судебные процессы), DataFabric (информационные системы на основе семантических технологий) и iDVP. Банки. Кредитные процессы (автоматизация выдачи кредитов). В Битве инноваторов также участвовали Sputnik (автоматизация финансовых бизнесов), MindScore (психологическая оценка личности заемщика), Конструктор документов FreshDOC.ru (составление договоров и других сложных документов для частных лиц и бизнеса), Penenza.ru (площадка для инвестиций физических лиц в займы бизнесу), Мои инвестиции (маркетплейс финансовых продуктов для начинающих инвесторов). Информация без задержки публикуется в телеграм-канале Финсайд.

http://finside.ru/1633 Источник Финсайд

0 notes

Photo

I beg una my people Make una thank this Woman for me, na she make me proud Man Today @finnext my Queen 👑 aka Sandilo aka Mamaray aka Lollipop 🍭 thank my Wife, all this pikin of today make una lean #showdonshow #daddyshowkey #lionclan #ghettosoldiers #ajegunle

0 notes

Photo

Our Demo Day for Finnext Capital. It's a wrap! (at Cyberjaya)

0 notes

Photo

6 Key Retail Payment Trends in 2022

Read our blog: https://www.datavsn.us/6-key-retail-payment-trends-in-2022/

0 notes

Photo

Руководитель калифорнийского представительства Finsight Ventures Максим Назаров на FinNext 15 февраля расскажет о последних мировых тенденциях в финтехе. Программа форума: http://finnext.ru/. Мероприятие в Facebook: https://www.facebook.com/events/310191266120039/. #fintech #tech #money #Russia #Moscow #Москва #Россия #форум #finnext #финтех #деньги #финансы #инвестиции #инновации #банки #технологии #онлайн #биометрия #finsight #vc #california (at Moscow, Russia)

#биометрия#финтех#форум#finsight#fintech#финансы#finnext#инновации#vc#банки#онлайн#россия#инвестиции#деньги#california#russia#москва#tech#moscow#технологии#money

0 notes

Photo

Команда Мое дело: Сергей Панов, председатель совета директоров, и Никита Семин, менеджер по партнерским программам. #моедело #finnext2015 #FinNext (в Мое Дело (moedelo.org))

0 notes

Text

4 Indian Companies That Are Launching Their Own NFTs | FinNext

4 Indian Companies That Are Launching Their Own NFTs | FinNext

Updated: 07 Dec 2022, 05:18 PM IST Livemint NFTs are driving everyone nuts! A few big companie… moreNFTs are driving everyone nuts! A few big companies want to capitalize on its potential too. So today, let’s go through some of them. #nfts #cryptocurrency #finance #mint Subscribe Now For Latest Updates- https://tinyurl.com/lbw8nze Source link

View On WordPress

0 notes

Text

6 Key Retail Payment Trends in 2022

6 Key Retail Payment Trends To Watch Out For In 2022

The pandemic and its effects have triggered a wave of innovative payment solutions for existing applications, which have benefited both consumers and businesses.

The resurgence of investments has resulted in the development of cutting-edge payment technology-based solutions. Priority has been given to data-driven offerings that provide value-added propositions, and distributed ledger technology has garnered interest in using digital currency solutions and enhancing operational competence.

Merchants and retailers are integrating payments into their value chains, whereas technology titans are stepping up their financial services game by integrating payments into their offerings.

We anticipate the following six trends to dominate the global retail payments market in 2022.

Social Commerce

Due to a large number of users of social media platforms and the potential payment opportunities they present, businesses must also pay attention to and capitalize on the convergence of payments and social media. Meta has implemented several dedicated product store features and store controls on its Facebook and Instagram platforms to create a destination of brand storefronts where customers can peruse offerings and make purchases.

This trend has already enticed numerous well-known and international brands to establish a presence on social media platforms to capitalize on the international customer base and visibility.

According to a report by Accenture, global social commerce sales reached USD492bn in 2021; this trade is projected to increase at a positive CAGR of 26% and surpass USD1.2tn in value by 2025. In addition to strategic partnerships, social platforms, brands, and retailers are anticipated to contribute significantly to the expansion of this market.

Digital Currencies

Digital currencies are seen as the next step in the evolution of digital payments. Simply put, a digital currency controlled by a central bank would function similarly to cash that can be stored and accessed digitally. Digital currencies would expedite financial inclusion and address deficiencies in the current payment infrastructure.

China has already implemented the e-renminbi, a digital version of its currency, allowing merchants and consumers to conduct business without an Internet connection, credit card, or bank account. In September 2021, Sweden joined the club by launching its digital currency (krona). South Korea, Australia, Singapore, and India also intend to join and are taking the necessary steps to expedite the launch of digital currencies.

Real-Time Transactions (RTT)

Due to the immediate availability of funds, convenience, ease of use, transparency, and safety, this method of payment is gaining significant traction among consumers worldwide. RTP delivers real-time alerts and provides features such as invoices with payments, payment requests, and account statements.

In addition, RTP's overall value proposition is enhanced by the incorporation of contemporary features such as support for all types of utility bill payments, In-app shopping, and P2P payments.

Financial institutions are investigating additional use cases to pave the way for innovative and seamless payment offerings for consumers and businesses. Fifty-four countries have adopted RTP systems, and several others are developing them. Existing systems are being modernized with innovations and interoperability for international transactions.

According to a recent article published by ACI Worldwide and Global Data, the number of real-time transactions in 2020 was 70,3 billion, up 41 percent from 2019; the value of transactions increased 33 percent y/y to USD69 trillion in 2020. In 2020, RTP accounted for 9.8 percent of all global electronic transactions, up from 7.6 percent in 2019; by 2025, this proportion is projected to reach 17.4 percent. India ranked first in the report, with 25,5 billion transactions, followed by China with 15,7 billion transactions.

Contactless Payments

The pandemic has accelerated the adoption of contactless payments. It acted as a catalyst for innovation: payment service providers such as Square and Adyen launched touch less payment checkout solutions in which merchants present a QR code to shoppers (via a POS terminal or printed form) that a link to complete the payment via smartphone. PayPal introduced comparable functionality in the United Kingdom, and other providers worldwide are expected to follow suit.

Near-field communication (NFC) payments technology for card-based payments holds a bright future due to its improved security standards and usability, allowing customers to tap or wave their mobile devices to pay.

The expansion of smartphone usage, Internet connectivity, and merchant networks would accelerate the growth of QR-based payment options and other contactless payment methods. According to the International Telecommunication Union, Internet users will reach 4,9 billion in 2021, up from 4.1 billion in 2019. (ITU).

From Electronic Wallets To Super Apps

Digital wallets have achieved great success in emerging markets such as China and India, and they appear to be evolving into payments super apps (e.g., We Chat and Paytm). Several companies in the United States are integrating services such as cryptocurrency purchases, banking services, wealth management, and insurance into a single app, thereby eliminating the need for separate apps and customer accounts.

For instance, Google Pay will enable users to open checking and savings accounts with traditional banks that can be managed through the app. Similarly, Square has added new features to its digital wallets, such as cryptocurrency trading and deposit services. To create an all-in-one digital wallet solution, PayPal has also announced some interesting new features, visibly in-app shopping tools, crypto trading, interest-earning savings accounts, direct deposits, and bill payments.

Buy-Now-Pay-Later (BNPL)

Globally, the BNPL payment option, a short-term credit product with no fees and interest, has spread rapidly. Due to its ability to offer installment products to consumers underserved by traditional financial institutions, its global adoption by merchants is growing. Its increasing popularity among consumers can be attributed to its straightforward pricing models, convenience, and user-friendliness (no credit history or other proof needed).

The BNPL option provides credit access in a decentralized, democratic, and inclusive manner, opening a market previously dominated by global credit card network providers and traditional financial institutions. Fintech and traditional financial institutions invested significant capital in strengthening their foothold; for example, Square acquired Afterpay for USD29 billion, and PayPal purchased Paidy for USD2.7 billion. Companies have collaborated (e.g., Klarna-Stripe and Amazon-Affirm) to take advantage of each other's expertise and geographic reach. It facilitates cross-pollination and accelerates business growth.

In this age of digitalization, customer preferences are rapidly changing, and technologies are becoming obsolete at an unprecedented rate. Companies must now innovate and invest in new payment solutions to remain competitive and increase their share of the volume and value of customer payments.

Governments and payment bodies/regulators are constructing the regulatory frameworks required to monitor the development of payment technology, combat fraud, and protect user interests.

How Can Datavision help?

On their digital transformation journey, we assist a variety of financial institutions and global banks. Our one-of-a-kind approach, which combines people, process and technology expedites the delivery of superior results to our clients and drives excellence. Several reputed companies leverage our proprietary suite of business excellence tools and services to unlock new growth levers and unparalleled ROI.

Datavision is a leading Banking software solutions provider having operations in Central American and Latin America like Mexico, Columbia Guatemala and Honduras. We at Datavision are the top retail and Corporate Banking Software provider as we serve our prestigious clients with cutting-edge core application software in Peru, Nicargua as well as High-performance ETF solution in Costa Rica and El Salvador. Also, we provide the best banking software products in Panama, Brazil and Belize . Get in touch with us for customizable, scalable, and affordable banking software products and solutions. Our portfolio of banking software product and services include:

Core Banking Solutions FinNext Core | FinNext Islamic Banking | FinTrade | EasyLoan | MicroFin

Digital Banking Solutions IBanc | MobiBanc | MBranch | FinTab | FinSight

Payments FinPay

Risk & Compliance FinTrust | InvestRite

Want to know how our team of experts at Datavision offer our reputed clients customisable, scalable and affordable banking software products and solutions? Visit us to know more.

0 notes

Photo

Retail Banking Trends

Read our blog: https://www.datavsn.us/retail-banking-trends/

0 notes

Text

Retail Banking Trends

Top 7 Retail Banking Trends: 2022

This blog post examines the top retail banking trends and projections for 2022, including the impact of financial technologies. AI, cloud, robotics, APIs, and cyber security. The latest technology enables companies to improve consumer experience and introduce new products and services.

The rise in digital banking, focus on innovation, new technologies, and changing industry dynamics are concerns that require management, but they also present opportunities in the banking sector. Every financial institution should build new business models, deploy new technology, and become customer-focused.

Transition To Cloud Computing

Most banks haven't moved their essential core systems to the cloud. Why? Because data control, governance, security, and various risks induce much anxiety in them. According to a recent survey in 2020, less than 10% of essential banking workloads have been moved to the cloud. Banks must improve their speed and scalability. Financial organizations should adopt cloud computing technologies. The bank's transition to core cloud computing would improve customer insights, innovation, efficiency, agility, and security and business continuity threats.

Cloud computing solutions boost staff productivity and deliver 360-degree insights. Over 80% of organizations report operational gains after using the technology. Most financial institutions' obsolete technology disappoints clients. It is not easy to update, expensive to maintain, and doesn't work well. Moving to the cloud is the best flexible choice for banks. Smaller banks can employ this technology to compete with larger ones.

Banking-as-a-service (BaaS)

Banking-as-a-service provides end-to-end financial services online. BaaS integrates digital banking services into non-banking products. An ECommerce website can offer loan payment services, mobile payment cards, and debit cards without obtaining a banking license. Banks can increase their revenue by adopting BaaS. A bank's goal is to reduce costs and increase revenue. BaaS also helps traditional banks build new income models. These models let banks commercialize their capabilities, data, and infrastructure.

Revenue-sharing agreements, one-time setup costs, and subscription fees are ways banks can boost their bottom line with BaaS. Getting a banking license is complex, and there are several regulatory requirements. Non-banking service companies will gladly partner with banks to avoid this hassle of regulatory compliance.

Embedded banking

Embedded Banking or Embedded finance integrates financial services with a non-financial service. For example, Uber is coupled with payroll automation software, allowing customers to make embedded payments. Embedded banking connects financial services with consumers. It strategically streamlines access to financial services. Embedded banking is the latest trend that has gained much traction these days.

Companies of all sizes are launching embedded financial services for individuals and enterprises. Most banks see it as an opportunity rather than a threat to existing banking rules. Consumers want to stay in an app throughout the buying cycle; therefore, embedded financial services are popular and have a promising future. Businesses implementing embedded solutions should either buy, partner, or license embedded finance technology as they will benefit from it.

Intelligent Process Automation (IPA)

IPA includes cognitive automation, computer vision, machine learning, robotic process automation, and the application of artificial intelligence.

IPA can automate the following:

Commercial lending

Trade finance

Bill discounting and financing

Letters of credit and guarantees

Anti-money laundering

Sanction screening

Banking regulations and compliance

Cash management operations

Besides the above, IPA also automates Import & export payments, payment operations, Payment investigations and Inward and outward payments.

Most banks struggle to implement intelligent automation despite knowing its benefits. It is recommended to start small with IPA and focus on the value each process will achieve once integrated across various financial systems. Without a computerized back office, the value of customer service deliverability can decline. Automating the strategies mentioned above will transform how customers view their banks. Most financial organizations will use IPA in 2022 to improve customer experiences.

Price Transformation

Since banks are cost-cutting measures to regain normalcy, they must engage in digital transformation to compete and meet online needs. Digital transformation would enable a remote workforce and preserve corporate continuity by 2022.

Today's banking institutions prioritize innovation. Financial institutions are cutting expenses by simplifying redundant IT systems, consolidating core platforms, decreasing contractor spending, offloading non-essential businesses, digitalizing additional services, and reducing office space.

Here are some cost-cutting measures banks took:

Barclays has reevaluated its office space use. Retail banks shall use their branch locations for tele-calling purposes and investment banking personnel.

Wells Fargo & Co unveiled a 4-year goal to reduce yearly spending by $8 billion. Their approach includes removing several layers in their management, reducing staff, and decreasing 20% of their office space by 2024.

Experiential Banking Experience

In Banking 4.0, financial organizations should offer customers contextual and lifestyle banking experiences. Banks should leverage data to build practical customer experiences. Banks have tons of data but can only be used as part of the value chain. Focusing on the customer experience requires employing several technologies and being adaptable.

Even though Agile has technical constraints, its early delivery and continuous development mindset can be the best. To offer experiential banking, banks must simplify and update their technological stacks using microservices, lightweight and reactive systems, analytics, AI, and machine learning.

Comprehending Gen Z's Preferences

Anyone born after 1996 is categorized as Gen Z. Millions of people become adults. All of them will need financial services at a certain point in time. They have different outlooks because they have a distinct perspectives on money and other topics. They're also the world's largest generation at 32% of its population. Freebies won't attract Gen Z'ers as they're well-informed and sensitive. They expect a fair banking user experience. Banks must carefully provide them with direction and financial liberty. Instead of a faceless relationship, banks can take advantage of social media platforms to offer financial knowledge and awareness. A rapport-building strategy is essential to connect with Gen Z. Application of personalized interfaces such as profile photos, incentive systems emojis, rewards and gamification seem more accessible.

Conclusion: Covid-19 caught banks unaware of the situation's severity. Even with more viral varieties, ambiguity remains. In retrospect, banks are better prepared for 2022.

Improving client experience is a top priority for banks. They'llThey'llcus on operational excellence to provide exceptional client service. While banks have found new models and revenue streams, they should embrace the latest technologies and processes to stay relevant. The last several months have reminded banks of the necessity of utilizing technology; now is the time to be innovative.

Technological advancement is leading FinTech development. Industry insiders have called 2022 "the year of value chain disruption" backed by AI and smart contracts (blockchain). Although technology has been disrupting the financial services value chain for a while, the attention will be more on such activities in 2022. As countries struggle to develop national regulatory norms, digital wallets are booming.

Technology is transforming the models, roles, and competitive environment of financial institutions and the markets and people they serve. Regulatory frameworks have been implemented globally post-crisis, and financial institutions have reshaped their business models. Accelerating digital innovation is the most creative and destructive factor in today's financial services ecosystem. It is safe to say that these new technology developments will drive banking and fintech innovation in 2022 and beyond.

If you are a financial institution looking for a technology partner for a complete digital transformation, you have come to the right place. Datavision prides itself on working with leading banking and financial services organizations, taking care of their technological needs, and improving their operational competency. Contact us to know more.

Datavision is a leading Banking software solutions provider having operations in Central American and Latin America like Mexico, Columbia Guatemala and Honduras. We at Datavision are the top retail and Corporate Banking Software provider as we serve our prestigious clients with cutting-edge core application software in Peru, Nicargua as well as High-performance ETF solution in Costa Rica and El Salvador. Also, we provide the best banking software products in Panama, Brazil and Belize . Get in touch with us for customizable, scalable, and affordable banking software products and solutions. Our portfolio of banking software product and services include:

Core Banking Solutions FinNext Core | FinNext Islamic Banking | FinTrade | EasyLoan | MicroFin

Digital Banking Solutions IBanc | MobiBanc | MBranch | FinTab | FinSight

Payments FinPay

Risk & Compliance FinTrust | InvestRite

Want to know how our team of experts at Datavision offer our reputed clients customisable, scalable and affordable banking software products and solutions? Visit us to know more.

0 notes