Official Tumblr account of a leading fintech company with expertise in cards & payments.

Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by tpsworldwide-blog1 and here's what we found interesting.

Average Info

Notes Per Post

5

Likes Per Post

1

Reblog Per Post

4

Reply Per Post

0

Time Between Posts

1 month

Number of Posts By Type

Text

14

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a 66 index score for customer satisfaction in the US.

Text

CRAFTING A DELIGHTFUL MOBILE BANKING EXPERIENCE FOR CUSTOMERS

The banking industry is going through a huge upheaval with mobile experience expected to be at the forefront of attracting new customers. With smartphone usage on the rise all over the world, banks and financial must capitalize on associated opportunities and create superior experiences for the millenials.

With an average user having access to global businesses through their mobile phones, one has to stop and compare the differences in quality of services that are being offered. Unfortunately the local industry is still not treating mobile channel as a first-class citizen and this has to change sooner. It is evident when you look around and see the quality of mobile apps being published by local businesses. There are a few exceptions but overall the situation doesn't seem quite satisfactory. These apps are merely resized versions of their web counterparts with jumbled up user interface and confusing user experience. This is also true for mobile banking apps currently available.

Banking is already complex and confusing mobile experiences are not helping either. There is a huge change in mindset required to fix this situation and it is time for banks to understand the importance of turning things around. This is the age of design thinking and banks must either up their game on mobile innovation and design or trust their technology vendors to lead them to the right direction.

In this brief post, you are going to explore some key areas and I hope that by understanding them, you should be able to start considering things in a different perspective and start improving.

Embrace global design trends

It is said that having the right inspiration contributes a lot towards creating a beautiful design. A beautiful design doesn’t only mean using flashy color scheme or images, it also means having a cleaner, simpler design that doesn’t interfere with the user experience. In fact, a beautifully crafted app helps users achieve their goals quickly and seamlessly. There must be a lot of synergy between different elements of an application and you need to keep in mind the best practices of designs that are devised by industry leaders.

It is a fact that the quality of the apps created in Silicon Valley and the likes is top-notch and you should observe the patterns used in successful apps. You can take inspiration and learn from quality designs even if they don’t cater to the needs of the domain you are targeting. Apple and Google both regularly organize design awards for apps published on their respective stores. I highly recommend you to frequently check these apps for inspiration.

Another way to learn better design principles is to explore platform-specific guidelines. Apple follows a flat design philosophy and their guidelines can be found here while Google announced Material Design a couple years back which is the primary guideline for Android.

Material Design guidelines is something I encourage designers to explore in depth. The guidelines cover everything from overall theme, fonts and branding to individual controls. The best part of these guidelines is that they can be adapted on web, Android and iOS with only few platform-specific tweaks in design.

Improving the design process

To design better apps, you need to introduce some discipline in your design workflow. The most simplistic workflow could be:

1. First off, always start with a simple wireframe. You can sketch on a whiteboard or draw on a paper. Wireframes act as a tool to finalize the layout of screens without bringing in theming and branding concerns.

2. Get feedback on the wireframes and then move on to create mockups.

3. Create mid-fidelity mockups using tools such as Sketch, Figma or Gravit. You can also use Adobe Photoshop but that’s too complex for this phase.

4. Get feedback on the mockups as well to establish branding, color schemes and overall theme of the app and move on to create a prototype.

5. An interactive prototype helps a lot in getting the end-users’ feedback without jumping into code. This saves a lot of time and gives clarity to the developers and designers towards creating a better user experience. Some of the better prototyping tools are InVision and Marvel.

6. Get feedback from end-users on the interactive prototype and finalize the app UI and UX.

In addition to these steps, it’s always a good idea to do some user research and get a deeper understand of your users’ needs and problems.

There’s also an increasingly popular and effective way to design, prototype and test new and innovative ideas with customers. This is usually a five-day process and it is called Design Sprint. I introduced it in TPS last year and the stakeholders simply love it. I highly encourage you to try it out so you’re able to solve critical problems through this process.

Focusing on performance

Performance is one of the most important aspect of mobile apps in particular. It is hard to retain users if your app feel jittery and laggy. An app’s performance can be improved by simplifying the UI, displaying only necessary information, avoiding unnecessary animations and imagery, and selecting a good development tool. For example, hybrid apps perform worse compared to native apps.

Using platform features

Mobile platforms have been evolving with rapid pace. We get newer versions of these platforms every year with many exciting features. It is important to keep up with the pace and introduce these platform features into apps to create a pleasant user experience. Some of the features that can be used are:

· Fingerprint, Facial and Voice recognition for authentication.

· 3D touch (iOS 9 and above) and app shortcuts (Android 7.1.1 and above).

· Widgets for performing different tasks quickly

· Voice assistants (Siri, Google Assistant, Bixby, Cortana, Alexa).

Our mobile banking solution already has most of these features available and our team is on its toes to introduce other features in their next release.

About Asadullah Bin Yousuf:

Asadullah is a development manager and tech lead overlooking mobile and web development teams at TPS. He is generally seen as a technology advocate among his colleagues, and he has a knack for quickly coming to pace with latest trends in technology, and bringing them into practice. His current areas of interest are cross-platform mobile app development, mobile-first design thinking, mobile UI/UX, Material Design, Wearables, IoT, RESTful APIs and Cloud.

#mobilebanking#digitalbanking#mobileexperience#designthinking#tpsworldwide#tpspakistan#internetbanking

0 notes

Text

7 Million Heroes in 70 years

The spring locks of my grandma's attache case stretched like a cat, when I ordered them to open. Toiled by years of hard work, they had lost their recoil and sounded a warning for opening a treasure chest which did not belong to me. Neatly, stacked in there were separate stacks of letters from her six sons of whom my dad's were the most distinguishable. They were the blue aerogram letters that I had grown up seeing at my dad's desk. I immediately recognized them. It is difficult to understand how could one fill those leaves of paper without with an autocorrect featured software and printer, but with only a pen and ink of emotions.

Dad moved to Saudi Arabia in 1966 as a young pediatrician from his government job in a remote town in South Punjab. Those were the days when the King's Landing (overwhelmed by the GOT Season 7) was being built by hundreds of my fellow country men in the fields of medicine, engineering and education. Another of my uncle went to build the Queen's Landing in UK and another one to the Green's Landing posted as an army captain in the East Pakistan (fills me with grief on the 70th Independence day for what we lost only after 24 years of independence). The stories of my uncles are for another day when I unpack their letters.

Grandma had a lot reading to do. The boys treasured a great bond with their mother. The letters were old and many. Schooled by a great mom, almost all the letters were written in beautiful handwriting with cut nib pens. They were stocked neatly with grace into packs covered in a plastic envelop binded with a rubber band. The rubber band lay there now melted on the envelope, like a dutiful soldier with a sprawled hands protecting an unaffectionate intrusion into his motherland.

With teary eyes when I opened the first of my dad's scriptures, a tale of how my Rome was built unravelled infront of me. The struggle of defending Pakistani identity in a foreign land was bigger than the struggle of winning economic freedom. Month over month the hard earned money helped my aunts get married and the younger uncles complete their education. Like my father, there are more than 7 million expatriate heroes of Pakistan who go through this struggle everyday.

Our heroes keep our green lights blinking. Every year they send almost $19Bln home to their families home through banking channels

Even with the quick options of account/wallet credits using IBFT from 1Link powered by TPSWorldWide, the cash over counter is still the most in-demand transfer option for cross border remittances. As per industry insights, atleast 50% of the home remittances in the country are collected in cash from the bank branches or from the exchange company locations. The Agent banking/mobile money network though reaching 300,000+ locations in the country have not been able to contribute as a cashout access point for the home remittances. The reason is the average transaction size of ~USD300 per transaction.

The liquidity availability at the agent of PKR 25,000 - 30,000 is a challenge considering the only way to source the agent till is the funds from selling the merchandise. Also the 0.7-1% commission expectation of the agent (possible in a domestic remittance of average transaction size of ~Pkr 4300) against the disbursement is not viable for the MFS service provider.

The human centric operations for remittance payouts have not been productive. ATMs can prove to be a simpler and cost effective answer. Considering the impact of ATMs in financial inclusion and increasing the reach of financial service points, regulator is in a process of introducing regulations to license White Label ATM Operators.

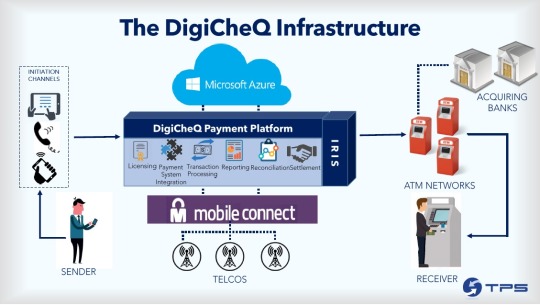

For remittance payouts through ATMs, the challenge is the KYC diligence of the beneficiary at the payout location. How can the beneficiary will be authenticated in the absence of a human agent. We have taken an attempt to crack the code with our #DigiCheQ service. (Read Just In Time remittances blog post ).

With our verified money transfer service built on GSMA's personal identity initiative Mobile Connect the beneficiary is able to withdraw funds from the ATM even without a formal bank account/wallet by authenticating herself from Teleco data (Read first blog in this series).

Using the Azure cloud hosted service the connected financial institution/exchange house can validate the beneficiary identity with a mobile number. The beneficiary is flashed with a USSD/SMS permission message to share her name and Citizen ID from the telco data. The One time Passcode is issued by the overseas correspondent to the sender for onward transmission to beneficiary.

The DigiCheQ is created from the in-coutry correspondent in the beneficiary name sent on her mobile number. With the two factor of authentication, the beneficiary can withdraw funds from the ATM of the acquirer institution connected to the DigiCheQ network. This is done with the help of Mobile Connect APIs of the connected telecom operator.

Mobile Connect is live with 52 mobile operators in 29 countries reaching East & South Asia, APAC, Europe, MENA and Latam. With our early deployments live with China Mobile, other operators including Mobilink, Telenor adoption is in progress. DigiCheQ is now expanding to integrate the Mobile Connect APIs of global operators to enable Just In Time Remittances.

About Mohsin Termezy:

Mohsin has rich experience across full cycle digital payments ecosystem with banks (retail, corporate, microfinance, agent banking), regulatory consulting and fintechs. He is a futurist with a belief in the power of two currencies: Data & Trust.

#tps worldwide#tps#tps pakistan#mobile connect#digicheq#two factor authentication#ibft#1link#payments#digital payments#mobile banking#agent banking#remittances#remittance processing solution#remittances in pakistan#financial inclusion

0 notes

Text

Just In Time Remittances

My left eye twitched. With my left hand on the phone and right hand reaching for my wallet in my back pocket, I picked the mobile on the first ring. Any happily married man would agreeably do the same when the dial screen flashes her name.

It was a little unusual for an early morning call at 0915. I heard my wife sobbing and I had to pull out of my Monday morning team meeting to attend to the emergency. Her favorite maid's son, a long haul driver had met an accident 1400 miles away from me. The savior had contacted our maid explaining how an immediate operation was deemed by the local hospital as necessary. In our part of the world where the public medical care system fails to reach the mark, such emergencies usually have to be dealt with-in the personal eco-system. This situation required me to transfer the basic operating expense to a town, the existence of which needed me to Google it. Bigger, however, was the challenge of remitting funds to this far off place, even though I work in the payments realm and know of many options.

Pakistan is completing 10 years of being introduced to the agent banking/branchless banking deployments. The country is the home to some of the world's best and fastest growing mobile money deployments. With 350,000+ agents covering the larger geo footprint of Pakistan (881,913 km2), the target of increasing and diversifying financial access points of agents, atm, pos and branches form the core of the National financial inclusion strategy. The banking agent network in aggregate performs more than 5 million P2P remittances per month with an average transaction size of ~$40. A Recent change in regulatory policy allows the cash out limit to be increased to ~$450 from the agent network. This opportunity can be seized but not without the challenge of having physical cash availability at all times.

Agent network seemed to be an obvious choice but I could not risk the availability of the cash at the location especially at 0915 when my beneficiary had to collect it in real time. It was not a case of financial access point but a challenge of making the cash available at the payout location. The same challenge has haunted the utilization of banking agents for cash payout of home remittances, where the average transaction size is about $350.

With the "war against cash', there is a debate on the longevity of the ATM business. The fact is that to date; ATMs have proved the cheapest 24x7 location for cash availability. Their deployments will slow down but we are going to have at least 4.3 Million ATMs globally by 2020. The banks are constantly looking at improving the utilization of these deployed ATM assets. Research shows improvement in operational cost per ATM i.e. cost per transaction and cost per replenishment when the number of transactions increase. A further improvement when these assets generate revenue from off-us transactions.

Before I talk about the famous cheque and bank relationship, I have a confession to make. Although I evangelize digital payments and make most of my payments digitally, I love the simplistic approach of a cheque and have butterflies in the stomach to think that they will soon be gone. When I saw, billionaire industrialist Linus Larrabee (Humphrey Bogart) baiting Chauffeur's daughter, Sabrina Fairchild (Audrey Hepburn) into leaving his playboy younger brother in my favorite classic 'Sabrina', I was introduced to cheques. A ‘bearer cheque’ is encashable to the amount written at the bank branch, after the writer's signature are verified. The cashier typically gets the bearer to sign at the back of the cheque and keep a copy of his photo id for record.

DigiCheQ our latest verified money transfer service closely emulates the experience. It leverages the magic of Mobile Connect (see my previous blog post) and allows money transfer from sender to a verified Mobile number instead of an account number. The sender is able to create a digital cheque from his internet/mobile banking and host the cheque in the cloud (DigiCheQ platform hosted on #Azure cloud). The receiver is notified of the issuance with a one-time password which can be input at a payout ATM along with a Citizen ID number to withdraw cash. Mobile Connect pairs the CitizenId and the receiver’s mobile for verification, at the time of withdrawal (in real-time). This addresses the challenges of fraud and AML reverberating in the agent banking cash-outs regime.

The fast growing 3G/4G mobile network is addressing the network challenge associated with ATM deployments beyond the metro towns. This has enabled Pakistan to commission the highest ATM in the world at 15,397 ft by National Bank of Pakistan. With a far reaching ATM network, high uptime, 24x7 operations and cash availability, the utilization of DigiCheQ is deemed to grow both for the payout of domestic and international remittances.

Since the past few years, I am seeing the mobile wallet teams in MFS providers focusing their innovation efforts to build adoption of mobile wallets both in the banked and unbanked world. The premise is simple, facilitate the banked customers to pay their domestic household workers and the recipients can transfer the money back home. Being a part of the same network is cheaper but the possibility of exchange between account-wallets or wallet-account is also enabled via IBFT (see earlier blogpost). When we envisaged DigiCheQ, we targeted the missing case of Connecting Banked to the Unbanked. Why are those who are yet to join the network be excluded from the digital transaction infrastructure? The power of DigiCheQ allows you to encash the cheque at an ATM with only your mobile number. Would you have a mobile wallet/account you also have the option of redeeming your DigiCheQ into your account, the option and more that I will be the subject of my next blog.

Domestic remittances using the agent network is typically a 3-5% fee income model for the mobile money provider where the revenues are split between the agents and the MM provider in a 60-40 split favoring the agents. Banks acting as Issuers and/or Acquirers in the DigiCheQ infrastructure will have the ability to utilize the ATM/CDM infrastructure for earning upto 0.5-1% from the fee income on DigiCheQ origination and withdrawal.

Mobile Connect is live with 52 mobile operators in 29 countries reaching East & South Asia, APAC, Europe, MENA and Latam. With our early deployments live with China Mobile, other operators including Mobilink, Telenor adoption is in progress. DigiCheQ is now expanding to integrate the Mobile Connect APIs of global operators to enable Just in Time remittances.

About Mohsin Termezy:

Mohsin has rich experience across full cycle digital payments ecosystem with banks (retail, corporate, microfinance, agent banking), regulatory consulting and fintechs. He is a futurist with a belief in the power of two currencies: Data & Trust.

#gsma#tps worldwide#tps karachi#mobile money#digicheq#remittances#home remittances#branchless banking

2 notes

·

View notes

Text

Taking it personal to build financial products with Mobile Connect

By: Mohsin Termezy

Telecom operators get ready to share the personal identity data with 3rd parties and help personalize products.

I wrote "Personalization" in a 72 font on a sticky note and put it up on my desk earlier this year. This was to constantly remind me of my communication and work engagement preferences. Data defines our personalization capability. For someone I know and have interacted with earlier (#LinkedIn is a great support with 3535 contacts to date and growing :) is easier for I can have a digital or mental trail with him or her. What about a new engagement for which i don't have a previous data trail ? Can someone share their engagement and credentials has always been a question?

Similar is the thought when we source new customers for our product or service especially for a digital engagement. Can you have the basic silhouette of the customer before you start your engagement? With 120+ million biometrically verified mobile subscribers in the country, the biggest source of customer data after national id registrar - Nadra is telecom operator data. I drooled long for the data to be available to utilize it for our products with options for demographic, location, usage, activity data.

Good news. The next wave of personalization is here... the mobile operators have federated a decision to share the customer data with 3rd parties under the GSMA global initiative of MobileConnect. Under the program the select attributes of the customer data would be available to be shared with 3rd parties. I know the watchdogs are giving me that look!!! Yes this is only with customer prior consent identifying the requesting party, purpose and individually for each request.

We jumped on the opportunity and established TPS Worldwide as the first Pakistani global sales service partner for GSMA to build new usecases for the financial services last year.

Its my pleasure to confirm that our first solution utilizing Mobile Connect is ready to be taken to market. DigiCheQ is a cardless remittance solution enabling customers to send money to a verified mobile number and the beneficiary will be able to collect the funds from the ATM.

This post is the series of 3-4 posts where I will introduce the product and the future roadmap of the solution. Keep watching!

About Mohsin Termezy:

Mohsin has rich experience across full cycle digital payments ecosystem with banks (retail, corporate, microfinance, agent banking), regulatory consulting and fintechs. He is a futurist with a belief in the power of two currencies: Data & Trust.

#digicheq#cardless remittance#gsma#tpsworldwide#tps#tps pakistan#mobileconnect#digital payments#payments#personalization

1 note

·

View note

Text

Social Banking – How Banks are enhancing customer experience by offering services on Social Networking Platforms.

For any business, customer relationship building is a top priority and even more so for banks as the competition is stiff and customers’ needs and wants are evolving. Banks, small or large, must keep pace with the speed of technological advancements. As Klaus Schwab, Founder and Executive Chairman of the World Economic Forum, said, “In the new world, it is not the big fish which eats the small fish, it's the fast fish which eats the slow fish.”

Millennials, the generation born between 1980 and 1994, now outnumber the Baby Boomers and the banks must understand this generational difference in order to stay competitive. Millennials have different preferences for communicating with the banks across multiple digital channels leading to the rise of alternate banking services such as mobile payments, Peer-to-Peer (P2P) payments, etc. They see value for convenience, mobile support and ease of use.

Since the onset of social media platforms such as Facebook & Twitter, Millennials’ expectations and their relationship with the banks have been changing rapidly. They increasingly expect the banks to offer services via these platforms. Realizing the need, banks are now making efforts to leverage these rapidly emerging platforms to offer a 21st century experience to their customers bringing a shift in the way customer relationship is managed.

Banks are opening their doors to new online payments via Facebook and Twitter. Some banks allow users to tweet money to each other using Twitter handles while others allow transfer of money through Facebook. In addition to funds transfer, banks are also offering more payment options including the ability to make payments to Facebook Events and gift payments to friends and family for special occasions such as birthdays.

Related Video: Social Platforms for Banking

youtube

From improving the face of customer service to integrating online payment services, social media is going to enable banks to transform the whole customer experience. Social media platforms will continue to integrate with banks and fintechs and eventually become the hub of digital banking.

TPS, a leading cards & payments solution partner, is working with over 130+ banks & telcos across the world and helping them adapt and prosper in a new “Millennial Age” of digital banking. With TPS’ digital banking solutions, banks are providing customer comprehensive banking services right at their fingertips. Using the features available, customers can avail banking services on social media platforms including:

P2P Payments

Split Bills

Crowd Funding

Request Money

Bills Payment

Donations

Balance Quest & much more.

As data adoption accelerates and customers move towards digitization, it is time for banks to transform the way they serve their customers and offer them a personalized social banking experience on social platforms.

About Zaka Haque:

Zaka is a fintech enthusiast currently associated with TPS Pakistan. He is responsible for designing fintech solutions and providing consultancy in areas including payment middleware, mobile money, international and domestic payment schemes, remittances, digital banking, etc. Zaka specializes in help setting up payments initiatives from concept creation to post execution.

#internet banking#mobile banking#tps prism#prism internet banking solution#internet banking solution#digital banking#digital banking solution#alternate delivery channels#banking on facebook#banking on twitter#funds transfer#bill payment#utility bills payment solution#facebook payments#tweet money#twitter payments

0 notes

Text

Benefits of PayPak - Pakistan’s First Domestic Payments Scheme

The world has increasingly come to expect faster payments. Even the thought of paying for items by a simple swipe of a watch no longer raises eyebrows. Meanwhile, the process of using payments through electronic means to curtail unregulated and free markets remains futile for decades in Pakistan due to the lack of any concrete road map and regulations on electronic payment usage.

The biggest hindrance to financial inclusion is the high cost of cards based on international schemes. This is the reason why a huge proportion of the population is unbanked and under-served. The unbanked population doesn’t have access to the banking services and can’t use electronic mediums to pay utility bills, obtain fast and easy credits, purchase goods, get government benefits and receive remittances etc.

Integrating digital payments into the economies of emerging and developing nations addresses crucial issues of broad economic growth and individual financial empowerment. Digital financial services tied up with domestic payment scheme will not only promote financial inclusion but also foster economic growth.

In line with State Bank of Pakistan Vision 2020 to enhance and promote financial inclusion, 1LINK (Guarantee) Limited launched Pakistan’s first domestic payment Scheme PayPak aimed at providing efficient, cost-effective, robust and ubiquitous payments solutions. With this launch, Pakistan became the 28th country in the world to have their own domestic payment scheme.

With a domestic payment scheme in place, the following benefits can be achieved in short term basis:

Benefits

Transforming the digital payments landscape in the country by ensuring digital financial access to both the un-served and underserved population while at the same time reducing the transaction cost and improving overall efficiency.

Provides interoperability in the domestic payment ecosystem.

Acceptability to instantly incorporate government programs at minimum cost.

Product offerings to expand payment services and broaden access to financial services in Pakistan.

Bringing up new innovations in technology, specific to domestic aspirations.

In built scalability capacity for future plans of launching e-Wallet/Pre-paid program.

Enablement of Person to Person transactions such as card to card based funds transfer by means of various payment instruments.

Highly cost effective card scheme program.

PayPak Adaption

With TPS as their trusted technology partner, the following banks have launched cards based on PayPak scheme:

Allied Bank

Allied PayPak Debit Card empowers the bank’s customers to carry out ATM withdrawals as well as retail/POS transactions anywhere within Pakistan, with no dependency on international payment schemes. With a domestic payment scheme in place, the bank provides cost-effective payment solutions to its customers.

Askari Bank

Askari PayPak cards holders have the ease of making cash withdrawals through all ATMs across Pakistan. Using PayPak, Askari Bank is able to provide efficient and cost-effective payments solutions to its customers.

Establishment of digital payments and adaption of robust methods for financial inclusion such as PayPak has enormous benefit for the poor population in the emerging markets. This also helps address concerns about the transparency and traceability of payments.

About Syed Kazim Raza

Syed Kazim Raza is an experienced payments professional. With several years of experience in the payments industry, Kazim provides technical and business consultancy to the banks and telecommunication companies across continents.

0 notes

Text

TECHNOLOGY PROCUREMENT IN FINANCIAL SERVICES INDUSTRY

By: Muhammad Faizan

The concept of a centralized procurement department in the banking and telecommunication sector began to fly by 2011. In the earlier days, the procurement functions were performed mostly by respective departments and teams themselves which included business development, technology, administration and others. The scope of procurement functions is far more diverse than the general impression. Understanding business requirements, shortlisting vendors, negotiating prices and concluding legal contracts are rather complex processes nowadays which fall under the umbrella of a procurement division. Not only confined to this, supporting organizational objectives and goals while working closely with other functional teams in a company nowadays define what an effective procurement department can achieve. Keeping all these factors in consideration, it can be safely said that the strength of a procurement department directly relates to the overall performance of a company.

Compared to traditional banks, procurement departments in telecommunication companies are way ahead in the race. They are more rigid and compliant when policies are concerned and are vividly able to grasp power and authority from within the company to execute procurement business. A substantial percentage of banks is still in the process of progression towards centralizing the procurement. Some banks have already sowed the seeds of a strong procurement department while others are striving to make their way. The banks where procurement divisions have already been empowered, may often come on strong in terms of price negotiations and contract dialogue, while the rest of the banks would rather be settling for routine clerical work. Witnessing this, the future of procurement in the banking industry can be foreseen as promising and growing.

Alongside procurement, a new term called vendor management is emerging in the arena. The functionalities of procurement and vendor management overlap at times in different companies while clear segregation can be spotted in few organizations. However, it should be noted that banks have started to take the procurement division very seriously over the course of time and many banks are progressing towards a centralized approach for procurement. The need for centralization is very high and budgets are accordingly being allotted to procurement departments along with proper yearly targets to be achieved.

Besides creating value for their customers, the main objective of any bank or telecommunication company for purchasing financial technology constantly revolves around sustaining and increasing profit in the face of growing competition. The developing synergy that can be seen between banks and telcos pin-points toward branchless banking, which is one of the most promising technologies in Pakistan at the moment.

Fortunately, TPS is blessed to have had the foresight to start developing such technologies at an early stage. Now as the banks and telecoms collaborate through creative business products, they are each empowered by seasoned and mature software developed by TPS for their specific needs.

As compared to other countries, the number of new, emerging banking institutions in Pakistan is rather limited. This can be considered as a great opportunity by the telecom sector, not only in terms of benefiting themselves from this relatively untapped market, but also benefiting the consumers with more varied, powerful and simple to use financial services.

About Muhammad Faizan:

Muhammad Faizan is a senior commercial and risk expert at TPS. He loves to solve business problems including complex contractual negotiations with procurement departments of banks and telcos.

0 notes

Text

Cardless Cash withdrawal through Digital Banking

With a varied number of payment methods available, the way we pay for everything is changing with more digital transactions taking place than ever before. This fiction story is about cardless cash withdrawal from ATM using a mobile banking app.

#prism internet banking solution#internet banking solution#internet banking#mobile banking#ATM#cardless cash#payments#fintech#tps#tps worldwide

0 notes

Text

NFC technology for contactless payments

Technological advancements in the payments industry is driving innovation in banking. Some of the recent developments in banking include branchless banking, online utility bills payment, EMV card issuance and acquiring system and much more. A new introduction to the banking industry is the NFC (Near Field Communications) technology that makes tap-and-pay services like Apple Pay, Samsung Pay and Google Wallet work.

So what exactly is NFC? If you have ever owned an NFC equipped phone, you probably already know what it is. Simply put, NFC is wireless, short-range communication between two compatible devices. This requires a transmitting device to transmit signals and another device to receive them. Just like infra-red technology, you bring the two devices close to transmit and receive signals. A range of devices can use the NFC standard and can be considered either active or passive depending on how they work.

Passive NFC devices include tags including other small transmitters that can send information to other NFC devices without the need for a power source of their own. However, they don't really process any information sent from other sources and can't connect to other passive components. These often take the form of interactive signs on walls or advertisements. Active devices are able to both send and receive data, and can communicate with each other as well as with passive devices. Smartphone's are by far the most common implementation of active NFC devices.

So, how is NFC making banking easier? Number of cash-based transactions are declining because customers are now using plastic cards to make purchases. Plastic cards are replacing cash because they are safer and more convenient. And you no longer have to wait for minutes if the shopkeeper doesn’t have change. NFC makes the process even faster. An example of NFC technology is the Chase Blink credit card which includes an NFC chip and enables users to wave their cards in front of an NFC-enabled point-of-sale terminal to make purchases.

NFC is paving the way for new payment opportunities and opening the door for new innovation. The technology is making it feasible for smartphone users to embrace mobile wallets. With a mobile wallet app in an NFC equipped smartphone, consumers can access their wallet (credit/debit card account, prepaid cards, loyalty programs, etc) by tapping their phone on a POS device and quickly and efficiently make payments.

Some of the major credit card companies, banks and cellular carriers have created an international mobile wallet standards consortium called ‘ISIS’ also known as ’Soft Card’. Smartphone manufacturers including Apple and Samsung have adopted NFC technology to drive innovation in payments. The advancements in this area led to the creation of products like Apply Pay, Samsung Pay & Google Wallet. Juniper Research, a UK based telecommunications research firm, has predicted that NFC based payments will total $180 billion by 2017. This number shows that NFC is going to shift the paradigm of retail payments. Let’s get ready for the paradigm shift in shopping and see the magic of NFC. About Malik Saad

Malik Saad is working as a Software Quality Assurance Lead at TPS. With solid experience in the area of core banking, he has worked on many projects related to IVR (Interactive Voice Response), Cardless & Talking ATM, Internet Banking, and Mobile Banking.

1 note

·

View note

Text

How to leverage lunchtime for learning through Brown Bag Sessions

Author: Asfand Ahmed

Training your employees in an industry as intensely competitive as the payments industry can give your competitors a run for their money! For a leading company that’s forging the way in a competitive industry, it’s very important to have a solid plan in place for developing their talent. Many companies are now investing in the continuous growth of their employees and taking steps to improve and enhance their knowledge capacity.

It has been observed that many companies design training programs for their employees on a yearly basis. The main problem with these training programs is that limited employees get to attend the training programs as even the most profitable companies in the world face time and budget constraints.

TPS, a leading cards & payments solution provider, had faced the same problem in the past. The human resources team at TPS came up with a very effective solution to tackle this problem. They introduced Brown Bag sessions. So, what is a Brown Bag session and how did these sessions help TPS solve the problem?

Brown Bag session is an informal meeting, training or presentation that occurs during a lunch period. These sessions can be conducted by any employee who has learned something new and interesting about any new technological advancement, updates, or transformational changes that are being done in the world. Employees who are willing to share their knowledge with others, request the HR team to arrange a session. The HR team then facilitates the session and ask interested employees to register for it. Employees can view a presentation or listen to a speaker discuss new concepts, innovation in upcoming projects, new initiatives, and technological improvements. Employees can cross train, dig deep into the topic, engage in continuous improvement, and create a learning environment within the session. But as the session has a limited number of seats, the issue remains there that how to make all the employees get benefit from the training. There comes TPSEDISON to the rescue, an online learning portal exclusively designed for the employees. Training sessions are recorded and uploaded on the portal along with relative material of the training so that employees who can’t attend the session can also benefit from it.

Brown Bag sessions are designed to provide any newly gained knowledge for employees from different work groups across the company. The sessions not only allow employees a real-time exchange of knowledge and experience but also helps employees socialize and get to know each other in a relaxed environment. The session also promotes learning and trusts building among employees. With Brown Bag sessions TPS encourages innovation, teamwork and employee engagement. Brown Bag Session leaps over the huge barriers that encumber external training. It also gives employees to get to know and share the real life problems that participants encounter every day at work and the solutions that can be used to tackle those problems, resulting in the production of high-quality products with fewer problems and flaws. Brown Bags sessions ensure that the employees who attend the training will experience support on their job as they attempt to apply the new concepts and ways to solve the issues faced by them at work. Trainers present topics in the language and terminology that participants can relate to and understand easily. The trainers not only develop skills of other employees but also cement their own knowledge on the topic. The best way to make sure that employees thoroughly understands a topic is to ask them to train others.

Brown Bag Session are the best way to retain, motivate, learn, unlearn, relearn, and reinforce the new technologies and methodologies for employees and TPS is proud to have such program implemented and encouraged by not just employees but the management too, to get the best possible outcome that helps the organization get better, productive and efficient.

About Asfand Ahmed

Asfand Ahmed is a Human Resource professional at TPS. Asfand has hands-on experience in areas like training & development, compensation and benefits, employee relation, and employee engagement. He is an enthusiastic social worker who also loves to paint and capture photos.

#brown bag#training and development#human resources#payments industry#employee engagement#learning and development

0 notes

Text

Step towards Mobile Banking

Author: Mubashira Yaqoob

Published in: Business Recorder

Over the past few years, the use of mobile banking has continued to increase in almost all parts of the world. The advent and rapid reach of smartphones to people belonging to different walks of life have played a significant role in promoting mobile banking. However, mobile banking is not restricted to a specific type of mobile phones. The main idea is use of mobility, away from traditional banking outlets and even computers. The mobile phone has evolved greatly from its initial purpose and has now become a rich channel for consumer interaction and data exchange. Mobile banking can include services as simple as balance inquiry over text messages or it can include more advanced transactions like bill payments and fund transfers. The challenges and risks are minimised by placing limits and smart new modes of authentication (RFID, NFC, tokenization, etc) to make sure that the ease of use that mobile technologies promise is not compromised. According to a survey conducted by Consumers and Mobile Financial Services, United States in March 2015, 59% of smartphone users had at least one bank account. 39% of mobile phone users with a bank account reportedly used mobile banking, a number which is continuously and convincingly climbing. It is suggested in the report that with the increased adoption and usage of smartphones, this trend should witness a hike in the coming years. Moreover, the recent launch of 3G/4G services by all mobile service providers will further contribute in adoption of mobile banking in Pakistan. Is Mobile Banking Secure? Technology innovators are exploring exciting new avenues for the provision of secure and reliable means for banking. However, there are still some rare yet highly publicised and/or ill-informed cases of fraudulent activities around the world that have made people skeptical of newer forms of payments. "How safe do you think people's personal information is when they use mobile banking?", a question asked by Consumers and Mobile Financial Services, United States in 2014. Out of a total of 2,603 respondents, 7 percent believed it was 'safe' to use mobile banking while 19 percent showed concerns and marked it 'very unsafe'. Spreitzenbarth, a blog run by Dr Michael Spreitzenbarth relating mobile security and forensics, has been working for public awareness for quite a long time now. According to the latest information published on the blog, there are more than 100 malicious android mobile apps presently, including financial apps as well. With such ill-natured programming entities active in the financial market, it is not only recommended to the users to steer clear of such apps but it is also the responsibility of the financial institutions to educate their market. The institutions can spread awareness by enlightening their consumers about company-registered mobile apps, how phishing scams work, and other related scenarios. All the aforementioned survey results suggest that a solid plan is required to make the mobile banking industry stronger than ever. The financial institutions trying to make a mark in mobile banking need to come up with secure financial solutions that minimise people's reservations. Working toward conversion to EMV can be one such step. EMV (Europay, MasterCard, VISA) may not be completely mobile specific, but it has helped reduce fraudulent transactions at the point-of-sales. EMV has planned to devise software approaches for online transactions involving interaction with the issuer bank or network's website (verified by MasterCard or VISA Securecode). Fingerprint authentication in the latest smart phones is another way to reduce and prevent identity theft, which can be serve as a great selling point for secure mobile banking. Replacing a traditional card number with an e-token is a practice which is under consideration and can play a significant role in masking real card information. As more of these advancements in providing secure means for mobile banking are being integrated in financial mobile apps and supporting systems, a growing number of consumers are expected to trust and become dependent on mobile banking for their day-to-day financial needs. PRISM Mobile Banking Solution TPS proudly offers PRISM as a comprehensive solution for internet banking, covering a wide spectrum of functionalities that banks can utilise to attract customers. PRISM's mobile app encompasses all the features which are available in the desktop version. The processes of beneficiary addition, funds transfer, bill payment, etc are all similar to execute. Wherever you go, your bank certainly follows you. Besides conventional features, PRISM's mobile app is capable of providing its customers with freedom to switch between multiple bank accounts through one platform. The app is designed and developed keeping in consideration the latest technology and security concerns. Deployed and working in a number of countries in Asia and Africa, PRISM has become a vital product, continually sensing your banking needs and coming up with comprehensive solutions. PRISM is determined to provide its customers with a mobile application that minimises the efforts and usage time and maximises availability and reliability.

About Mubashira Yaqoob

Mubashira Yaqoob is a Technical Author at TPS. When she’s not inscribing thoughts to paper at lightning speed, she’s seen boosting peer morale and spearheading new initiatives with the gumption of a thousand Spartans.

1 note

·

View note

Text

Banking Without Borders on Social Platforms

Author: Mubashira Yaqoob

Published in: Business Recorder (April 2016)

Social media has completely revamped how we interact with our social circles, without the inconvenience and cost of traditional socialisation. What was invented as a supplement to our day to day interactions has now become the norm, connecting us daily with people around and those away from us. The popularity of Facebook, in particular, can be accredited with initiating this movement. We can now interact with a lot more people, apply for more jobs, buy more items in less time with better product comparison, or even run an entire business from a social media web front. It has been a rapidly evolving phenomenon that is only set to dominate greater segments of our lives. 'We are social', an organisation that collects data relating social media usage world-wide, portrayed a not-so-surprising canvas of information in its 2016's report. There are about 7.395 billion humans walking on the planet earth at the moment, out of which 2.307 billion are already connected to social media actively. A growth rate of 46% was recorded this year as compared to the past reports, adding 219 million new active social media users since 2015. From Argentina to Vietnam, the survey involved 30 developed and underdeveloped countries. Facebook, with over 1500 million users secured first position among the most followed social networking websites on the globe. The aforementioned data and figures stress upon the fact that social media has gained such prominence which makes it unimaginable to skip social media integration in any kind of business. Where ecommerce industry is concerned, social media has already provided enough opportunities to merchants in order to make the most of their businesses by marketing their products to a plethora of communities world-wide. Marketing content on famous social platforms like Facebook and Twitter can boost the sales up to 70% if utilised smartly. Financial Institutions, unlike ecommerce businesses, are such entities that are directly or indirectly associated with the lives of a huge population either professionally or personally. In the present era when every other business is mobilised, it has now become the need of the time that the payment industry catches up to the imminent trends leading to a comprehensive social banking ecosystem. According to World Retail Banking Report 2015, 56% of the banks world-wide are still in the process of gathering information as to how can social banking be a part of the conventional banking without affecting the existing consumer base. When targeting social media in future prospects, banks should also consider the fact that millennials (people born between 1980s and 2000s) are the generation that are a predominant segment of the social cloth. On every popular social website, millennials are registered and actively participating in bigger numbers than generation X (people born before 1980). As they are more enthusiastic about social media, the demands and expectations also point towards a better, innovative and technologically diversified banking arena where they do not need to walk to a financial institution's physical branch for regular transactions. The report also highlighted the possibility of millennials leaving their primary banks in the next 6 months due to the unavailability of banking options that involve social media as compared to generation X. Financial barriers, security concerns and legal implications can be the underlined constraints that banks could face in the way of integrating social banking. At some level, these concerns are legitimate and demand a divergent analysis of the current and future aspects. For any organisation, adapting new technology and working in a completely different environment are not easy tasks to achieve. In order to begin with social banking, banks first need to take a number of steps, starting with increasing social presence and then moving on to the development of social banking features. Banks can put their first footstep in social banking by introducing basic functionalities on social media which do not require several levels of encryption. In the beginning, such a banking application would only facilitate customers in viewing their balance on any social media platform, be it Facebook or Twitter. Customers would also be able to view mini statement or request for a new card. Once the customers become accustomed to these features and get over the initial fear of security, banks can start introducing many innovative functionalities, the likes of which will redefine banking as we know it now. Having gained the confidence of their customers, banks can now launch features like transferring funds to friends through Facebook or Twitter; without knowing their account details, requesting money from friends or collecting funds for a social cause. All of these innovations use a key feature of social media which involves a person's social connections. On the other hand, online shopping has took a turn with social media, where merchants; small or large, showcase their products. The only ingredient missing is enabling customers to make payments directly from these platforms, where they can see the product, instead of elongating the process by asking customers to make a separate fund transfer to merchant's account; a cumbersome process that customers today follow grudgingly because of lack of other options. Allowing customers to make payments through social media will not only make life easier for the customer by giving them an option to pay right there and then but also help merchants in retaining and gaining more customers. These are just some future projections of how banks can not only win their estranged customers back, but can also make a difference in attracting new customers. Rest assured, only the banks which embrace social media today will survive this race of innovation. Today, people literally live on social media, then why don't banks do the same? TPS's Role In Social Banking TPS, with their goal of bringing the best and the most innovative to its customers, has now entered the arena of social banking, with prominent developments in two of its major products PRISM and Payaxis. PRISM, an internet banking solution deployed in a number of banks in Asia and Africa, has been working to bring versatile eBanking features for the world since its emergence. PRISM has now taken on a new turn by introducing applications for both Facebook and Twitter. Similarly Payaxis, a Payment Gateway solution deployed in both Pakistan and UAE has components and features carefully designed keeping in mind the current market trends and consumer needs. TPS envisions it as a flexible and transparent means of online purchasing to help increase user acceptance, merchant ease and the possibility of various web-store based products that can be launched by any central scheme operator. With the latest Hashtag Payments developed on Twitter, Payaxis has transcended one more milestone of providing diverse payment options to its customers anywhere in the world. At the same time, Payaxis's module of Facebook payments, enables merchants to market their products on Facebook and also receive payment using the same platform.

About Mubashira Yaqoob

Mubashira Yaqoob is a Technical Author at TPS. When she’s not inscribing thoughts to paper at lightning speed, she’s seen boosting peer morale and spearheading new initiatives with the gumption of a thousand Spartans.

0 notes

Text

Pakistan’s Position in Online Utility Bill Payments

Author: Mubashara Yaqoob (Technical Author at TPS)

Published in: Pakistan & Gulf Economist

Utility bill payment in physical bank branches is still a common practice in Pakistan. With all the exciting technologies surrounding us today, we might think that long queues in the sun should be a thing of the past, but they are not.

Conventional bills like power and gas utilities as well as bills for current day services like broadband internet are some mandatory and recurring expenditures that are still following archaic billing methods, including high cost physical branches, franchises and one stop shops, with insufficiently staffed offices and often poorly trained personnel. Much needs to be done to improve the customer experience and rather than seeing the short-term costs as a hurdle, the long term competitive advantage should be considered.

Unfortunately, in Pakistan, the consumers only receive a pile of papers with complicated financial figures, often with unclear hidden cost of services that consumers don’t fully understand and are hence unable to utilize. Even after completing the billing process, the consumers still need to maintain physical records for any future discrepancies, which are also a common occurrence given the inefficient billing systems and clerical errors.

What if this process could be simplified? What if the consumers didn’t have to add another series of tedious tasks to their monthly routine as the due date approaches? What if we could leverage the ongoing advancements in mobile payments and branchless banking for better customer experience? What would it take for not only the service providers to come on board with smart solutions but for the consumers as well to be educated and adaptive of such solutions?

These are some questions that need answers – answers that pledge that consumers will be able to receive and pay their utility bills online, through mobile phones, tablets and personal computers, while doing something more useful than standing in a queue.

These questions have been around for a while and are yet to be fully resolved. According to a commercial survey a couple of years back by Fiserv, paperless utility bills were not even common in a developed country like United States. Only 23 percent of the total number of consumers received electronic bills. However, the same report suggested that no less than 90 of consumers would like to witness improvement in this particular area of utility bill payment. When a majority consumer segment is willing to use a remote channel for bill payment that ensures ease of use, it is safe to say that with high-end, secure technology and swift internet speeds of today, people would prefer online and on-the-go methods for bill payment.

Why is it important for Pakistani utility companies and facilitating banks to focus on online bill payments facility today? It is because we as a nation have been making great progress in the field of information technology in recent years with an increasingly favorable local IT scene as well as foreign interest. The high-speed broadband services, especially in urban areas, have reached at least comparable levels to global standards. The exponentially increasing usage of mobile and smartphones also convincingly leads to the conclusion that online bill payment has an existing ecosystem at the user end.

The launch of (and existing competition in) 3G/4G services in Pakistan opened a lot of doors for improvement in almost all the sectors where technology can make a difference. By the end of January 2016, 128.042 million users made it to the list of mobile subscription in Pakistan. The number of 3G/4G users exceeded 24 million, implying that Pakistanis are hugely enthusiastic about using online facilities. If not 3G/4G, there is still a great number of population which is regular consumer of voice, SMS and USSD channels. If utility companies provide online payment facilities, it is highly likely that mobile user-base would include a lot of early adopters.

The utility consumers that are more proficient in using tablets/computers over mobile phones should also be considered. A good percentage of online payments in Pakistan are still operated through desktop computers and laptops, portraying the users as potential online billing consumer’s base. State Bank of Pakistan’s annual electronic banking statistics revealed that 1,370 thousand credit cards and 25, 024 thousand debit cards existed in the country by the end of 2015, summing eBanking transaction values as high as Rs. 35,848 billion. This is a massive user-base that still remains widely untapped and in need of simpler and more efficient online bill payment services.

Another aspect to consider is the lack of physical branches in rural areas of the country, where people may not be well educated but are regular customers of mobile services. Many areas also have access to merchant driven branchless banking, which has been a surprise success in recent years due to its ease of use. Banks and utility billers can also target these areas where people are willing to pay bills but are unable to do so at ease, many resorting to illegal local connectors that steal and redistribute power in one way or the other.

Another recent commercial survey by World Bank Group showcased the lack of digital financial instrument usage in Pakistan, revealing only 1 percent of the debit card holders are using it for online payments. However, at the same time, Pakistan has surpassed all other countries in South Asia in digital finance and branchless banking, standing at a position where 6 percent of the adults use mobile banking as compared to the 2 percent in rest of the South Asian countries.

The utility companies which have already stepped into the online bill payment circle do not completely meet the requirements and demands in a way the consumers want. A consumer will only prefer to pay online if the online bills are not complicated to spot and pay. Many banks that facilitate their customers with online and ATM based utility bill payment options, either have an interface which lacks flexibility and simplicity or is a mesh of a lot of different services that the consumers need to be educated about. Besides that, not all banks cater to all utility companies on all channels (ATMs, internet banking, mobile banking apps, etc.), which leads to a confusing mix of available/unavailable services that the consumers usually give up on after a few attempts.

There are a number of banks and utility companies which are willing and working in spreading the canvas of online bill payments in Pakistan. It is the time all banks and service providers to realize the need and aggregate such functionalities in their various channels, including ATMs, branchless banking, internet banking, mobile banking, etc.

Annual consumer bill volume in the world is estimated to be at least 330 billion, as per the research by a European company Billentis. This is a massive market where anyone with better services can come in and grab a bigger chunk of the business if only they can solve the pain points of the utility consumers.

The use of ecommerce websites has transformed from a non-reliable source to a preferred source of online shopping in the past decade. This has been made possible because companies strived to educate their market and worked hard to drag Pakistan out of the conventional store shopping arena. This has helped raise adoption and awareness levels of consumers that are ready for more similar solutions for their day-to-day needs.

There are also bill payment services provided by payment facilitators like 1Link, where they have installed bill payment solutions that work as central aggregators for payments. Before a central aggregator, each bank would have had to approach and acquire various service providers directly, meet their individual terms, and perform all settlement and maintenance operations on their own. But with the availability of such third party facilitators, the bank simply gets these services as a complete package without the need for a separate infrastructure.

If online payment system for utility bills could be streamlined in the next few years, it would significantly reduce the costs and expenditure of banks and utility companies as well as the cost (travel, time off from work, etc.) for the consumers. The utility companies will not necessarily need to dispatch snail mail dependent of paper bills, saving the costs of printing, delivery, etc. The banks would be investing less on physical branch banking facilities and customer services, leading to swift operations and better growth chances. People not only in Pakistan, but around the world would like to see advancement in this field in the form of mobile and desktop apps, ATM/POS bill payments, merchant assisted payment mechanisms, SMS/USSD based alerts and transaction services, IVR and Call Center assistance, etc.; hence covering the entire spectrum of bill payment possibilities for various customer preferences.

UBPS - Multi-Channel Electronic Bill Presentment & Payment Solution

UBPS is an electronic bill payment solution developed by TPS. The solution empowers the convenience of paying all your bills at one place. Using various channels such as ATM, internet banking, mobile banking, branchless banking or traditional branch banking, customers can pay bills with ease. Utility bills and payments such as electricity, telephone, gas, school fee, mobile top-ups, internet services, airline tickets, insurance payments, etc. can be paid with minimal effort from home, office or even on the go on mobile phones, tablets, etc.

About Mubashira Yaqoob

Mubashira Yaqoob is a Technical Author at TPS. When she’s not inscribing thoughts to paper at lightning speed, she’s seen boosting peer morale and spearheading new initiatives with the gumption of a thousand Spartans.

#internetbanking#mobilebanking#utilitybillpayments#utilitybillpaymentsoftware#tps#tpsworldwide#branchlessbanking#atm#fintech#payments#kesc#ssgc#ptcl

0 notes

Text

Escrow Services as a Trust Building Utility in Online Shopping

Author: Saqib Ahmed, Lead Technical Author, TPS

Published in Business Recorder (March 2016)

The world of online shopping brings millions of products and services at customers' fingertips. Window-shopping has been made so easy that you can browse and purchase products on your handheld devices, irrespective of the time or location. This means big business for retailers, wholesalers and manufacturers (as well as the central schemes/operators empowering them), who are willing to keep up with the technology and understand the challenges of such exponential business scaling. The escrow service is an important trust building utility, especially for new business acquisition. However, leveraging it for technology adoption in our day-to-day financial spending is yet to be fully capitalized.

Various central schemes and operators incorporate payment gateway applications to develop their online stores and register merchants within their virtual marketplace. This in turn enables merchants to sell their products online to various customers that are using different modes of payment through a single point of sale (for example an online shopping website that serves as a front end to the payment gateway). However, considering the various dynamics of customers' online purchasing needs, an escrow feature is required by the central schemes that operate such ecommerce stores. This helps the central scheme in maintaining control over the sales cycle, which includes verifying customer payments, monitoring merchant conduct and negotiating accordingly, pre-charging their fee from merchants, etc. Following are some cases where an escrow service can help ensure safeguarding the rights of customers as well as the merchants through dispute management controls, residing at the central scheme's back office.

1. An unregistered customer performs a purchase transaction after entering relevant card information. This card information is only used once for the transaction and no user data is saved. In this case the escrow facility is not available. The central scheme can use this opportunity to pitch the escrow facility as an incentive for the customer to sign up. This not only helps enhance the customer experience but also helps generate repeat business and monitoring of sales trends.

2. A registered customer can access the customer portal/website and login with their unique credentials to view previous purchase statuses and transaction history. He/she is presented with available transaction options, including a list of saved cards (if any). Once the customer performs a transaction, his/her account is charged and funds are placed into the escrow.

Successful merchant payments:

The payment gateway must safeguard a smooth payment mechanism for merchants to receive payments held in escrow after customers purchase their goods. Merchants commit a delivery date for each purchase, before which the purchased items must reach the customers. There is also the need for a system configured grace period after the delivery date has passed, during which disputes can be raised by customers.

Following are the available cases without any disputes raised:

1. If the customer receives goods before the delivery date has expired, he/she can confirm the receiving and payment is released from escrow to the merchant.

2. Merchants can also alert customers in case their own tracking systems show that goods have been delivered. Customers can then login to the web store to confirm goods received. This releases payment from escrow to the merchant, resulting in increased mutual goodwill.

3. If the delivery date as well as the dispute grace period have expired and the customer fails to update delivery status (whether or not the item was delivered), the payment is released from escrow to the merchant.

Dispute management:

Once the delivery deadline committed by the merchant has passed, there is a grace period during which registered customers can raise disputes against undelivered/faulty merchandise. Merchants can sign into the merchant portal to view payment statuses and history. They can also view available notifications in their inbox to review disputes and any related evidence attached by the customers. Disputes can result in the following cases:

1. The merchant fails to respond in time, the dispute is handled by the central scheme back office and, based on their discretion, customer payment is refunded from the escrow.

2. The merchant accepts the dispute, the payment is refunded back to the customer from the escrow.

3. The merchant rejects the dispute, it is handled by the central scheme and, based on their discretion (after reviewing the associated evidence records), either the payment is refunded from the escrow to the customer or it is released to the merchant.

Modes of payment:

It is also important to note that escrow services can be utilised by a payment gateway in various unlikely situations where offline payments fail to provide such security.

Over-the-counter: An exciting addition to ecommerce stores is over-the-counter payment. It is similar to adding goods to a virtual cart during online shopping, for which a voucher number is generated. This voucher number can be used later at a physical merchant counter to receive purchased items and pay in cash. This helps bring the convenience of online shopping to the offline world of cash purchases.

Payment Cards: A payment gateway can accept both debit and credit cards. Unregistered customers can perform quick transactions without the need to register. Registered customers can have a more personalized experience based on their saved profile, including a list of configured cards, so they can quickly select the desired card for a particular transaction. The payment gateway communicates with the respective bank switch (for debit cards) or the payment network (for credit cards) for verification and transaction completion.

Internet Banking: In direct debit transactions, the customer is asked to choose a favorite bank or institution for funds transfer. Once selected, the flow is transferred to the internet banking interface of the concerned bank. Customer enters the required authentication and transaction information using this interface. Upon validation and verification, the process is handed back to the payment gateway and then to the merchant to complete the sale.

Mobile Wallet: Mobile Wallet transactions require a registered mobile number from the customer. The mobile number is used to fetch customer information for the merchant, in order to authenticate the customer and complete the purchase.

Payaxis Application

Payaxis is a payment gateway application developed by TPS and is used to power ecommerce stores. It handles the authentication pre-requisites from the customer's bank and performs the transactions with the help of the respective payment switch/network to help complete the sale. Payaxis has been designed and developed considering the various scenarios and their challenges as discussed in this article.

About Saqib Ahmed

Saqib Ahmed is a Lead Technical Author at TPS. His main role is to ensure a seamless flow of Information Dissemination to our clients, partners, prospect customers and super-geeks in general.

#Escrow#internetbanking#mobilebanking#paymentgateway#ecommerce#tpsworldwide#tps#payments#fintech#mobilewallet

0 notes