#Advanced Driver Assistance System (ADAS) Advanced Driver Assistance System (ADAS) Market Advanced Driver Assistance System (ADAS) Market siz

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Total funding amounts to $125.3M.

Text

0 notes

Text

Advanced Driver Assistance Systems (ADAS) Market Size | Analysis, Trends 2024 - 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Advanced Driver Assistance Systems (ADAS) Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2031.” The study provides a detailed analysis of the industry, including the global Advanced Driver Assistance Systems (ADAS) Market Share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Advanced Driver Assistance Systems (ADAS) Market?

The advanced driver assistance system (ADAS) market was US$ 28.1 Billion in 2022. Furthermore, the advanced driver assistance system (ADAS) market to register a CAGR of 17.1% which is expected to result in a market forecast value for 2031 of US$ 116.3 Billion.

What are Advanced Driver Assistance Systems (ADAS)?

Advanced Driver Assistance Systems (ADAS) are electronic systems embedded in vehicles to improve safety and convenience by aiding drivers in various tasks. Using technologies like sensors, cameras, radar, and lidar, ADAS offer real-time data for features such as adaptive cruise control, lane departure warnings, automatic emergency braking, and parking assistance. These systems aim to minimize human error, prevent accidents, and enhance the overall driving experience by providing alerts, automation, and control support. As a crucial element in the evolution of autonomous vehicles, ADAS significantly advance road safety and driving efficiency.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2068

What are the growth prospects and trends in the Advanced Driver Assistance Systems (ADAS) industry?

The advanced driver assistance systems (ADAS) market growth is driven by various factors and trends. The advanced driver assistance systems (ADAS) market is rapidly expanding due to the increasing demand for enhanced vehicle safety and automation. This market includes various technologies such as adaptive cruise control, lane departure warnings, automatic emergency braking, and parking assistance, all designed to improve driving safety and convenience. Key growth drivers are heightened consumer awareness of safety features, stringent government road safety regulations, and advancements in sensor and camera technologies. The movement towards autonomous vehicles also boosts the ADAS market, as these systems are vital for self-driving technology. Consequently, the ADAS market is crucial in the automotive industry’s progress towards safer and more efficient driving experiences. Hence, all these factors contribute to advanced driver assistance systems (ADAS) market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Type:

Parking Assist System

Adaptive Front-lighting

Night Vision System

Blind Spot Detection

Advanced Automatic Emergency Braking System

Collision Warning

Driver Drowsiness Alert

Traffic Sign Recognition

Lane Departure Warning

Adaptive Cruise Control

By Technology:

Radar

Lidar

Camera

By Vehicle Type:

Passenger Cars

Commercial Vehicles

By Applications:

Transportation and Logistics

Agriculture

Construction

Mining

Public Transportation

Security

By Region

North America

United States

Canada

Europe

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

Benelux

Nordic

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East & Africa

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Renesas Electronics Corporation

NXP Semiconductors

Panasonic Holdings Corporation

Valeo SA

Denso Corporation

Robert Bosch GmbH

Continental AG

Texas Instruments Incorporated

Magna International Inc.

AUTOLIV INC.

Infineon Technologies AG

View Full Report: https://www.reportsandinsights.com/report/Advanced Driver Assistance Systems (ADAS)-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Advanced Driver Assistance Systems (ADAS) Market share#Advanced Driver Assistance Systems (ADAS) Market size#Advanced Driver Assistance Systems (ADAS) Market trends

0 notes

Text

Advanced Driver Assistance System (ADAS) Market is Rising with Higher CAGR by 2028

“Global Advanced Driver Assistance System (ADAS) Market Size Report | Industry & Analysis – 2028 Year” is the latest market research offered by The Insight Partners and is now out for purchase. Dive into the future of the Advanced Driver Assistance System (ADAS) market with our meticulous research report. In this report, we have analyzed various platforms for accurate market-based insights. This…

View On WordPress

#Advanced Driver Assistance System (ADAS)#Advanced Driver Assistance System (ADAS) Market#Advanced Driver Assistance System (ADAS) Market News

0 notes

Text

How is AI transforming every aspect of human life?

AI is transforming every aspect of human life by revolutionizing the way we work, communicate, learn, and live. Here are some key areas where AI is making a significant impact:

What is Artificial Intelligence?

Artificial Intelligence (AI) refers to the simulation of human intelligence in machines that can perform tasks requiring human-like cognitive abilities. It involves machine learning, natural language processing, computer vision, and other advanced techniques.

How does it impact every industry?

AI has the potential to revolutionize every industry by automating processes, analyzing vast amounts of data, and making intelligent predictions. It improves efficiency, enhances decision-making, and drives innovation across sectors such as healthcare, finance, manufacturing, and transportation.

How does it impact every individual?

AI impacts individuals by providing personalized experiences, virtual assistants, and smart devices. It enhances daily life through voice recognition, recommendation systems, and virtual customer support. AI-powered technologies make our lives easier, more convenient, and efficient.

AI is transforming every aspect of human life by revolutionizing the way we work, communicate, learn, and live. Here are some key areas where AI is making a significant impact:

1. Healthcare:

AI is enhancing medical diagnosis, drug discovery, and personalized treatment plans. It helps analyze vast amounts of patient data, identify patterns, and provide accurate predictions for disease prevention and early intervention.

According to Accenture, AI in healthcare could potentially save up to $150 billion annually for the U.S. healthcare economy by 2026.

The global AI in healthcare market is projected to reach $45.2 billion by 2026, growing at a compound annual growth rate (CAGR) of 44.9% from 2019 to 2026.

2. Education:

AI is revolutionizing education by enabling personalized learning experiences, adaptive tutoring, and intelligent assessment systems. It helps tailor educational content to individual student needs, track progress, and provide timely feedback for better learning outcomes.

The global AI in education market is expected to reach $3.68 billion by 2025, with a CAGR of 38.17% from 2018 to 2025.

A study by the American Institutes for Research found that AI-powered tutoring systems have a positive impact on student learning outcomes, resulting in an average percentile gain of 28 points.

3. Transportation:

AI is driving advancements in autonomous vehicles, optimizing traffic management systems, and improving transportation efficiency and safety. It enables self-driving cars, real-time navigation, and predictive maintenance, revolutionizing the way we commute and travel.

The global autonomous vehicle market is projected to reach $556.67 billion by 2026, with a CAGR of 39.47% from 2019 to 2026.

According to the National Highway Traffic Safety Administration, AI-powered advanced driver-assistance systems (ADAS) have the potential to reduce traffic fatalities by up to 94%.

4. Communication:

AI-powered language translation, natural language processing, and speech recognition technologies are transforming communication. Chatbots, virtual assistants, and language translation tools facilitate seamless cross-cultural communication and enhance accessibility.

The global AI in communication market is expected to reach $3.5 billion by 2026, growing at a CAGR of 34.7% from 2019 to 2026.

AI-powered language translation technologies have advanced significantly, with Google Translate handling more than 100 billion words daily in over 100 languages.

Virtual assistants like Siri, Alexa, and Google Assistant leverage AI to understand and respond to user commands, making voice-based communication more convenient and efficient.

5. Entertainment:

AI is reshaping the entertainment industry with personalized content recommendations, virtual reality experiences, and computer-generated imagery. It enhances user experiences, facilitates content curation, and enables immersive storytelling.

The global AI in the entertainment market is projected to reach $5.5 billion by 2026, with a CAGR of 25.4% from 2019 to 2026.

AI algorithms are used in content recommendation systems of streaming platforms like Netflix and Spotify, which account for a significant portion of their user engagement and revenue.

AI-powered computer-generated imagery (CGI) has transformed the visual effects industry, enabling the creation of realistic and immersive experiences in movies, video games, and virtual reality.

6. Finance:

AI is revolutionizing the financial industry with automated trading, fraud detection, risk assessment, and personalized financial advice. It enables efficient data analysis, real-time market insights, and improved decision-making processes.

A report by PwC estimates that AI could contribute up to $15.7 trillion to the global economy by 2030, with the financial sector being one of the largest beneficiaries.

AI-driven automated investment platforms, also known as robo-advisors, managed over $1 trillion in assets globally in 2020.

7. Smart Homes:

AI-powered smart home devices and virtual assistants, such as voice-activated speakers and smart thermostats, make our daily lives more convenient and efficient. They automate tasks, provide personalized recommendations, and create a connected and intelligent living environment.

The global smart home market is expected to reach $246.97 billion by 2027, with a CAGR of 11.6% from 2020 to 2027.

Voice-activated smart speakers, powered by AI assistants like Amazon Alexa and Google Assistant, have seen widespread adoption. As of 2021, there were over 200 million smart speakers in use worldwide.

8. Manufacturing:

AI-driven robotics and automation technologies optimize manufacturing processes, increase productivity, and improve product quality. AI-enabled machines and robots perform complex tasks, enhance precision, and enable predictive maintenance.

The global AI in manufacturing market is expected to reach $16.7 billion by 2026, growing at a CAGR of 49.5% from 2019 to 2026.

According to Deloitte, companies that invest in AI and advanced automation technologies in manufacturing can experience productivity gains of up to 30%.

AI-powered predictive maintenance can reduce equipment downtime by up to 50% and maintenance costs by up to 10-40%.

9. Agriculture:

AI is transforming agriculture by optimizing crop management, monitoring soil conditions, and predicting weather patterns. It enables precision farming techniques, reduces resource waste, and improves agricultural productivity.

The global AI in agriculture market is projected to reach $4 billion by 2026, with a CAGR of 22.5% from 2021 to 2026.

AI-powered agricultural robots and drones are expected to reach a market value of $1.3 billion by 2026.

The use of AI in agriculture can increase crop yields by up to 70%, according to a study by the International Data Corporation (IDC).

10. Cybersecurity:

AI is strengthening cybersecurity measures by detecting and preventing cyber threats, identifying anomalous behavior, and improving data protection. AI algorithms analyze large datasets to detect patterns and anomalies, enhancing security measures.

According to Gartner, by 2022, 90% of security budgets will be allocated to addressing AI-powered cyber threats.

The global AI in cybersecurity market is projected to reach $38.2 billion by 2026, growing at a CAGR of 23.3% from 2021 to 2026.

In summary:

AI is transforming every aspect of human life, from healthcare and education to transportation, communication, entertainment, finance, and beyond. Its applications are vast and diverse, revolutionizing industries, improving efficiency, and enhancing the overall human experience. As AI continues to advance, it holds immense potential to shape a future where intelligent technologies seamlessly integrate into our daily lives, making them more convenient, productive, and enriching.

#aiinnovation#artificialintelligence#airevolution#futuretechnology#transformativetech#aiadvancements#ai applications#aiprogress#aiinsociety#emergingtech#techtrendsin2023#aiimpact#aiintegration#aiforgood

15 notes

·

View notes

Text

Notchback Market Set to Reach New Heights: Market Overview, Key Trends, Porter's Analysis, and Key Takeaways

Notchback Market

Market Overview: The global Notchback Market is estimated to be valued at US$78.49 billion in 2023, with a projected compound annual growth rate (CAGR) of 5% from 2023 to 2030. A notchback refers to a car body style with a distinct rear deck lid that is positioned higher than the trunk. These vehicles offer valuable advantages to consumers, including spaciousness, practicality, and improved aerodynamics. Notchbacks cater to the needs of various consumers who prioritize functionality and efficiency without compromising on style. These vehicles provide ample cargo space while maintaining an elegant and sleek design. With the growing demand for versatile vehicles that combine form and function, the notchback segment is expected to witness substantial growth in the coming years. Market Key Trends: One key trend shaping the Notchback Market is the focus on sustainability and electric mobility. As environmental concerns rise and governments push for stricter emission regulations, automakers are increasingly investing in electric vehicles (EVs) within the notchback segment. For instance, key players like Volkswagen Group, BMW Group, and Mercedes-Benz are launching electric notchback models to meet evolving consumer demands and contribute to a sustainable future. The integration of advanced technologies is another significant trend driving the notchback market. Features such as advanced driver-assistance systems (ADAS), connectivity solutions, and enhanced safety features are becoming increasingly prevalent in notchback vehicles. These technological advancements enhance the driving experience and provide a competitive edge to automakers. Porter's Analysis: - Threat of New Entrants: The threat of new entrants in the notchback market is relatively low due to significant capital requirements, established brand presence of key players, and complex manufacturing processes.

- Bargaining Power of Buyers: Buyers in the notchback market have moderate bargaining power as they have access to various options from different manufacturers. However, their power is somewhat limited due to the innovation and brand loyalty associated with established automakers.

- Bargaining Power of Suppliers: Suppliers who provide key components such as engines, transmissions, and electronics have moderate bargaining power due to the presence of multiple automakers as their potential customers. - Threat of New Substitutes: The threat of new substitutes for notchback vehicles is low, as no alternative body style offers the same combination of style, functionality, and aerodynamics.

- Competitive Rivalry: Competitive rivalry among key players in the notchback market is intense, as established automakers constantly strive to innovate, offer unique features, and expand their market presence. Key Takeaways: 1: The global notchback market is expected to witness high growth, exhibiting a CAGR of 5% over the forecast period, fueled by increasing consumer demand for spacious, practical, and aerodynamically efficient vehicles. This growth will be driven by the emphasis on sustainability and electric mobility. 2: The fastest-growing and dominating region in the notchback market is likely to be North America, with rising consumer preferences for vehicles that balance functionality and elegance, as well as stringent emission regulations driving the adoption of electric notchback cars. 3: Key players operating in the global notchback market include Volkswagen Group, BMW Group, Mercedes-Benz (Daimler AG), Audi (Volkswagen Group), Ford Motor Company, General Motors, Toyota Motor Corporation, Honda Motor Co. Ltd., Hyundai Motor Group, Kia Motors Corporation, Nissan Motor Co. Ltd., Mazda Motor Corporation, Subaru Corporation, Volvo Cars, and Peugeot SA. These industry leaders are at the forefront of innovation, investing in electric mobility and incorporating advanced technologies to meet consumer expectations. In conclusion, the notchback market is poised for significant growth as automakers focus on sustainability, integrate advanced technologies, and cater to consumer demands for spacious and aerodynamically efficient vehicles. With key players leading the way, the notchback segment promises to offer consumers a perfect blend of practicality, style, and sustainable mobility options in the years to come.

#Notchback Market Market Overview#Notchback Market Market Key Trends#Notchback Market Porter's Analysis#Notchback Market Key Takeaways

2 notes

·

View notes

Text

Auto Parts Manufacturer: The Backbone of the Automotive Industry

The automotive industry is often recognized for the brands that manufacture cars, bikes, and trucks. But behind every vehicle on the road is a network of skilled and innovative companies—the auto parts manufacturers—that build the components enabling these machines to function reliably.

From engines and transmissions to lights and sensors, auto parts manufacturers form the backbone of India’s mobility ecosystem.

What Does an Auto Parts Manufacturer Do?

An auto parts manufacturer is responsible for designing, engineering, and producing individual components or assemblies that are used in the manufacturing or maintenance of automobiles. These can include:

Engine parts (pistons, crankshafts, valves)

Brake systems and clutches

Electrical components (alternators, batteries, sensors)

Body parts (doors, bumpers, mirrors)

Suspension and steering systems

Interior components (dashboard panels, seats, infotainment)

These parts are either supplied directly to Original Equipment Manufacturers (OEMs) or sold in the aftermarket for vehicle servicing and upgrades.

India as a Global Hub for Auto Parts Manufacturing

India is one of the leading countries in the global auto components market. With a large pool of skilled labor, competitive costs, and a growing domestic automobile industry, Indian auto parts manufacturers have made a strong impact both locally and globally.

Key facts:

The Indian auto component industry is projected to reach USD 200 billion by 2026.

Over 25% of the industry’s revenue comes from exports to markets like the US, Europe, and Southeast Asia.

Tier 1 and Tier 2 suppliers in India are investing heavily in automation and EV-compatible parts.

Challenges and Innovations

The modern auto parts manufacturer is navigating a fast-changing landscape marked by:

Electrification: Shifting from traditional IC engine parts to EV components like battery packs, electric drive units, and controllers.

Sustainability: Using recycled materials, energy-efficient processes, and adhering to global emissions standards.

Smart Technology: Incorporating sensors, ADAS (advanced driver-assistance systems), and connectivity solutions.

Companies that adapt to these changes with R&D investments and advanced manufacturing technologies are emerging as leaders.

Choosing the Right Auto Parts Manufacturer

Whether you're an OEM, a dealer, or a garage owner, selecting a reliable auto parts manufacturer is crucial. Key criteria include:

Quality Certifications (ISO, TS16949)

On-time delivery track record

Customization capabilities

Post-sale support

Strong R&D and innovation focus

In India, many manufacturers are offering a full spectrum of services—from design to distribution—with digital support and export readiness.

Conclusion

The role of an auto parts manufacturer extends far beyond assembly lines—they are engineers of reliability, safety, and performance. As India's automotive industry enters a new era of electric, connected, and sustainable mobility, the auto parts manufacturing sector will be at the center of this transformation.

0 notes

Text

IoT Chips Market is Driven by Explosive Connectivity Demand

Internet of Things (IoT) chips are specialized microprocessors, system-on-chips (SoCs), and connectivity modules designed to enable seamless data exchange among sensors, devices, and cloud platforms. These chips incorporate ultra-low-power architectures, embedded security protocols, and advanced signal processing capabilities that support a broad spectrum of IoT applications—from smart homes and wearable gadgets to industrial automation and connected vehicles. Advantages include reduced latency through edge computing, optimized energy efficiency for battery-operated devices, and streamlined integration into existing network infrastructures.

As businesses pursue digital transformation, there is a growing need for reliable, scalable chipsets capable of handling massive device connectivity, real-time analytics, and robust encryption. Continuous innovation in semiconductor fabrication processes has driven down production costs and boosted performance metrics, enabling smaller startups and established market players alike to introduce competitive products. Meanwhile, evolving market trends such as 5G rollout, AI-enabled analytics, and smart city initiatives are creating new IoT Chips Market opportunities and shaping the industry landscape. Comprehensive market research highlights expanding market segments in healthcare monitoring, agricultural sensors, and asset tracking.

The IoT chips market is estimated to be valued at USD 620.36 Bn in 2025 and is expected to reach USD 1415.005 Bn by 2032, growing at a compound annual growth rate (CAGR) of 15.00% from 2025 to 2032. Key Takeaways

Key players operating in the IoT Chips Market are:

-Intel Corporation

-Samsung Electronics Co. Ltd

-Qualcomm Technologies Inc.

-Texas Instruments Incorporated

-NXP Semiconductors NV

These market companies have established strong footholds through diversified product portfolios that span microcontrollers, application processors, short-range wireless SoCs, and AI inference engines. Their strategic investments in R&D, partnerships with tier-one automotive and industrial firms, and capacity expansions in fabrication plants are instrumental in driving market share growth. Robust alliances and licensing agreements help these players accelerate time-to-market for next-generation solutions, while continuous performance enhancements maintain their competitive edge. As major players optimize supply chains and strengthen IP portfolios, they contribute significantly to the overall market dynamics and industry size. The growing demand for IoT chips is fueled by accelerated digitalization across verticals such as automotive, healthcare, consumer electronics, and manufacturing. Automotive OEMs are integrating IoT chips for connected car features—remote diagnostics, vehicle-to-everything (V2X) communication, and advanced driver-assistance systems (ADAS)—driving substantial market growth. In healthcare, remote patient monitoring and telemedicine solutions rely on miniaturized, power-efficient chips to ensure continuous data transmission and secure access. Additionally, smart agriculture applications leverage low-cost sensors and communication modules to optimize resource usage and crop yields. As enterprises embrace Industry 4.0, the deployment of IoT solutions for predictive maintenance and asset tracking has become a critical business growth strategy. These evolving market trends underscore the importance of high-performance, cost-effective IoT chips to sustain long-term expansion.

‣ Get More Insights On: IoT Chips Market

‣ Get this Report in Japanese Language: IoTチップ市場

‣ Get this Report in Korean Language: IoT칩시장

0 notes

Text

Ceramic Bonding Tool Market: Investments and Technological Advances

MARKET INSIGHTS

The global Ceramic Bonding Tool Market size was valued at US$ 123 million in 2024 and is projected to reach US$ 167 million by 2032, at a CAGR of 4.3% during the forecast period 2025-2032. The U.S. market accounted for approximately 28% of global revenue in 2024, while China is expected to exhibit the fastest growth rate at 7.9% CAGR through 2032.

Ceramic bonding tools are precision components used in semiconductor packaging and microelectronics manufacturing. These tools primarily include capillaries for wire bonding and wedge bonding tools for specialized applications. The ceramic materials (typically alumina or zirconia) provide superior wear resistance, thermal stability, and electrical insulation compared to metal alternatives, making them essential for advanced packaging technologies.

The market growth is driven by increasing semiconductor production, particularly for IoT devices and 5G infrastructure, which require high-reliability packaging solutions. The capillaries segment dominates with over 65% market share in 2024 due to widespread use in gold and copper wire bonding. Key players like Kulicke & Soffa and Adamant Namiki are investing in advanced ceramic formulations to meet the demands of finer pitch bonding in next-generation chips.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Semiconductor Packaging to Accelerate Market Growth

The ceramic bonding tool market is experiencing robust growth due to the increasing demand for advanced semiconductor packaging solutions. As consumer electronics become more compact and powerful, manufacturers require higher precision bonding tools for chip assembly. The global semiconductor packaging market, valued at over $40 billion in 2024, continues to expand with ceramic bonding tools playing a critical role in wire bonding applications. These tools offer superior thermal and electrical properties compared to metal alternatives, making them indispensable for high-frequency and high-power applications. With the semiconductor industry projected to grow at nearly 7% annually, ceramic bonding tool manufacturers are scaling production to meet rising demand from fabless semiconductor companies and OSAT providers.

Expansion of 5G Infrastructure Creates New Demand for Ceramic Bonding Solutions

The global rollout of 5G networks is creating significant opportunities for ceramic bonding tool manufacturers. 5G infrastructure requires advanced RF components that utilize ceramic packages for their excellent high-frequency performance and thermal management properties. Bonding tools with ceramic capillaries are essential for assembling these sensitive components, as they provide the precision required for fine-pitch bonding applications. With over 2 million 5G base stations expected to be deployed worldwide by 2026, the demand for specialized ceramic bonding tools is projected to increase substantially. This trend is particularly prominent in Asia, where countries are aggressively expanding their 5G networks to support growing digital economies.

Automotive Electronics Revolution Drives Innovation in Bonding Technology

The automotive industry’s rapid electrification is transforming the ceramic bonding tool market. Modern vehicles incorporate hundreds of semiconductor devices for applications ranging from engine control to advanced driver assistance systems (ADAS). Ceramic bonding tools are critical for assembling these automotive-grade components that must withstand harsh operating conditions. With the automotive electronics market expected to surpass $600 billion by 2030, bonding tool manufacturers are developing specialized solutions for automotive applications. These include tools with enhanced durability to handle thicker bonding wires and advanced materials for high-temperature applications in electric vehicle power modules.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes Limit Market Penetration

While ceramic bonding tools offer superior performance characteristics, their high manufacturing costs present a significant market barrier. The production of precision ceramic tools requires specialized equipment and skilled technicians, resulting in costs that are substantially higher than conventional metal bonding tools. Small and medium-sized packaging houses often find these costs prohibitive, particularly in price-sensitive markets. Additionally, the complex manufacturing process leads to longer lead times, making it challenging for manufacturers to respond quickly to fluctuating demand. These factors collectively restrict the adoption of ceramic bonding tools, especially in cost-conscious market segments.

Technical Challenges in Miniaturization Pose Development Constraints

As semiconductor packaging continues to shrink, ceramic bonding tool manufacturers face increasing technical challenges in tool miniaturization. Developing capillary tips that can reliably handle sub-30μm bond wire diameters requires advanced materials science expertise and precision manufacturing capabilities. The brittleness of ceramic materials makes them particularly challenging to work with at these microscopic scales. Furthermore, maintaining dimensional stability and surface finish at reduced sizes affects tool longevity and performance. These technical hurdles slow down product development cycles and increase R&D costs, making it difficult for smaller players to compete in the high-end segment of the market.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Production Consistency

The ceramic bonding tool market faces ongoing challenges from global supply chain disruptions affecting critical raw materials. High-purity alumina and zirconia, essential for tool manufacturing, have experienced price volatility and availability issues in recent years. These supply chain constraints are compounded by the concentration of advanced ceramic production in limited geographical regions. Manufacturers must navigate these challenges while maintaining stringent quality standards, as even minor material inconsistencies can significantly impact tool performance. The situation has prompted industry participants to reevaluate their supply chain strategies, with many exploring alternative materials and local sourcing options to mitigate risks.

Technological Shift Towards Direct Chip Attach Creates Adaptation Pressures

The emergence of advanced packaging technologies like flip-chip and wafer-level packaging presents both opportunities and challenges for ceramic bonding tool manufacturers. As these alternative interconnection methods gain market share, traditional wire bonding applications may see reduced growth in certain segments. This technological shift requires tool manufacturers to adapt their product portfolios and develop new capabilities. Companies that successfully integrate expertise in both wire bonding and emerging interconnection technologies will be better positioned to maintain market leadership. However, the transition requires substantial investment and carries significant technological risk, particularly for smaller players with limited R&D budgets.

MARKET OPPORTUNITIES

Rise of Advanced Packaging Technologies Opens New Application Areas

The growing adoption of 2.5D and 3D integrated circuit packaging creates significant opportunities for specialized ceramic bonding tools. These advanced packaging approaches require precise bonding solutions for interposer connections and through-silicon vias (TSVs). Ceramic tools with enhanced thermal properties and dimensional stability are particularly well-suited for these demanding applications. As the advanced packaging market is projected to grow at over 10% annually, tool manufacturers have the opportunity to develop innovative solutions tailored to these emerging requirements. Leading companies are already investing in R&D to create bonding tools optimized for heterogeneous integration and chiplet-based architectures.

Expansion in Emerging Markets Presents Growth Potential

The establishment of new semiconductor manufacturing facilities in emerging economies represents a significant growth opportunity for ceramic bonding tool suppliers. Countries in Southeast Asia and South America are aggressively developing their domestic semiconductor industries, creating demand for high-quality bonding tools. These regions offer attractive growth prospects as they work to reduce reliance on imported electronic components. With governments providing incentives for local semiconductor production, ceramic bonding tool manufacturers have the opportunity to establish long-term relationships with emerging market customers. Successful market entry strategies will require adapting products to local requirements while maintaining the high performance standards expected in global semiconductor manufacturing.

CERAMIC BONDING TOOL MARKET TRENDS

Growing Demand for Miniaturized Electronics Drives Market Expansion

The increasing need for compact and high-performance electronic components is fueling the demand for advanced ceramic bonding tools. As semiconductor manufacturers push the boundaries of miniaturization, ceramic bonding tools—particularly capillaries and wedge bonding tools—are becoming critical for precise wire bonding in IC packaging. The global market, valued at approximately $250 million in 2024, is expected to grow at a CAGR of 5.7% through 2032, driven largely by the semiconductor industry’s transition to smaller node technologies. Notably, advancements in LED packaging and 5G infrastructure are further accelerating this trend, as ceramic tools offer superior thermal and mechanical stability compared to traditional materials.

Other Trends

Shift Toward High-Performance Materials

Manufacturers are increasingly adopting alumina and zirconia-based ceramic bonding tools due to their exceptional wear resistance and longevity. These materials, which account for nearly 65% of the market share, significantly reduce downtime in high-volume production environments. While metallic bonding tools dominated the market in the past, ceramics now offer a competitive edge by minimizing contamination risks in sensitive applications like medical device manufacturing and aerospace electronics. The Asia-Pacific region, led by China and Japan, has emerged as a key adopter of these solutions, contributing over 40% of global revenue.

Automation and Industry 4.0 Integration Reshape Production

The integration of automation in semiconductor fabrication is transforming ceramic bonding tool applications. Smart manufacturing systems now utilize AI-driven alignment technologies to enhance precision in wire bonding processes, reducing error rates by up to 30%. Companies like Kulicke & Soffa and Adamant Namiki are pioneering IoT-enabled bonding tools that provide real-time performance data, enabling predictive maintenance. This shift aligns with broader Industry 4.0 trends, where operational efficiency and reduced waste are prioritized. Furthermore, collaborative robots (cobots) are being deployed alongside ceramic tools to handle ultra-fine pitch bonding tasks that demand sub-micron accuracy, a critical requirement for next-gen MEMS and sensor packaging.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Competition

The global ceramic bonding tool market features a moderately fragmented competitive landscape, with established players competing alongside regional manufacturers. Kulicke & Soffa emerged as a dominant force in 2024, commanding significant market share through its technologically advanced capillary bonding tools and strong foothold in semiconductor packaging applications across Asia and North America.

SPT Technologies and Adamant Namiki Precision Jewel have solidified their positions as key innovators, particularly in high-precision wedge bonding solutions for LED and microelectronics applications. These companies benefit from decades of metallurgical expertise and patented ceramic formulations that enhance tool durability.

Recent industry movements indicate intensified competition in the high-growth Asia-Pacific region. Kosma and Delywin have aggressively expanded production capacities in China to capitalize on the booming local semiconductor industry, which now accounts for over 35% of global ceramic bonding tool demand.

Mid-sized players like Suntech Advanced Ceramics are differentiating through specialized solutions for emerging applications in power electronics and 5G component packaging. Meanwhile, Japanese manufacturer TOTO leverages its ceramic engineering heritage to maintain premium positioning in high-temperature bonding applications.

List of Key Ceramic Bonding Tool Manufacturers

Kulicke & Soffa (Singapore)

SPT Technologies (Japan)

PECO (U.S.)

Adamant Namiki Precision Jewel (Japan)

Kosma (China)

TOTO (Japan)

CCTC (China)

Suntech Advanced Ceramics (China)

Mijiaoguang Technology (China)

Delywin (China)

Segment Analysis:

By Type

Capillaries Segment Dominates the Market Due to High Precision in Semiconductor Bonding Applications

The market is segmented based on type into:

Capillaries

Subtypes: Fine pitch, Medium pitch, and Large pitch capillaries

Wedge Bonding Tools

By Application

IC Packaging Segment Leads Due to Rising Demand for Advanced Semiconductor Packaging Solutions

The market is segmented based on application into:

IC Packaging

LED Packaging

Diode

Triode

Other (including MEMS and sensors)

By Material Composition

Alumina-Based Tools Maintain Market Share Due to Superior Thermal and Mechanical Properties

The market is segmented based on material composition into:

Alumina (Al2O3)

Zirconia (ZrO2)

Silicon Carbide (SiC)

Composite Ceramics

By Bonding Technology

Thermosonic Bonding Segment Grows with Increasing Demand for High-Reliability Interconnections

The market is segmented based on bonding technology into:

Thermosonic Bonding

Ultrasonic Bonding

Thermocompression Bonding

Regional Analysis: Ceramic Bonding Tool Market

North America The North American ceramic bonding tool market is characterized by strong demand from the semiconductor and electronics manufacturing sectors, particularly in the U.S. where advanced packaging technologies are driving innovation. The region benefits from significant R&D investments in microelectronics, with major players like Kulicke & Soffa and PECO maintaining strong market positions. Growth is further propelled by the CHIPS Act, which allocates $52 billion for domestic semiconductor production. However, high production costs and stringent regulatory standards pose challenges for manufacturers. The capillaries segment dominates due to its critical role in precision bonding applications, while wedge bonding tools find increasing use in specialized LED packaging.

Europe Europe’s market demonstrates steady growth, supported by a mature electronics industry and emphasis on high-quality manufacturing standards. Germany leads regional demand, benefiting from its robust automotive electronics sector and presence of equipment manufacturers like Kosma. The EU’s focus on sustainable electronics production is gradually shifting preferences toward durable ceramic bonding solutions with extended lifecycle. While the market faces pressure from Asian competitors on pricing, European manufacturers maintain competitiveness through precision engineering and customized tooling solutions. Recent developments include collaborative research initiatives between academic institutions and industry players to develop next-generation bonding materials.

Asia-Pacific As the fastest-growing regional market, Asia-Pacific accounts for over 60% of global ceramic bonding toolkit consumption, driven by China’s massive electronics manufacturing base. The region’s competitive advantage stems from vertically integrated supply chains and cost-effective production capabilities. Chinese manufacturers like CCTC and Suntech Advanced Ceramics are gaining market share through aggressive pricing strategies, though Japanese firms maintain leadership in premium tool segments. While traditional wire bonding applications dominate, the rapid expansion of advanced packaging in South Korea and Taiwan is creating new opportunities. The market faces challenges from cyclical semiconductor demand and increasing labor costs in coastal manufacturing clusters.

South America The South American market remains nascent but shows gradual growth potential, primarily serving local electronics assembly operations in Brazil and Argentina. Limited domestic semiconductor production constrains market expansion, with most bonding tools imported from North America and Asia. Economic instability and currency fluctuations have slowed capital investments in advanced manufacturing equipment. However, growing consumer electronics demand is spurring interest imported bonding solutions for local packaging facilities. The market’s development trajectory heavily depends on broader regional economic recovery and government incentives for high-tech manufacturing.

Middle East & Africa This emerging market shows selective growth in countries with developing electronics sectors such as Turkey, Israel, and South Africa. While regional demand constitutes a small fraction of the global market, increasing foreign direct investment in semiconductor test and assembly facilities presents opportunities. The UAE’s focus on technology diversification under initiatives like Operation 300bn could stimulate future demand. Current limitations include underdeveloped supply chains and reliance on imported tools, though regional players are beginning to establish basic packaging capabilities. Long-term growth will depend on successful technology transfer partnerships and development of local technical expertise.

The global ceramic bonding tool market reflects significant regional disparities in adoption drivers and growth patterns

Technology leadership remains concentrated in North America and East Asia, while other regions gradually build capabilities

Market expansion increasingly ties to government-supported semiconductor initiatives worldwide

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Ceramic Bonding Tool markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Ceramic Bonding Tool market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Capillaries, Wedge Bonding Tools) and application (IC Packaging, LED Packaging, Diode, Triode, Others) to identify high-growth segments.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

Competitive Landscape: Profiles of leading market participants including Kosma, SPT, PECO, Kulicke & Soffa, and Adamant Namiki Precision Jewel, covering their product offerings, market share, and recent developments.

Technology Trends & Innovation: Assessment of emerging manufacturing techniques, material advancements, and precision engineering developments in ceramic bonding tools.

Market Drivers & Restraints: Evaluation of factors driving market growth including semiconductor industry expansion, along with challenges such as material costs and technical constraints.

Stakeholder Analysis: Insights for semiconductor manufacturers, tool suppliers, investors, and policymakers regarding market opportunities and strategic positioning.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/chip-solid-tantalum-capacitor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-electrical-resistance-probes.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/high-temperature-tantalum-capacitor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-link-choke-market-innovations.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/multirotor-brushless-motors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/planar-sputtering-target-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ferrite-core-choke-market-opportunities.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/float-zone-silicon-crystal-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/carbon-composition-resistors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/resistor-network-array-market-analysis.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/melf-resistors-market-key-drivers-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-foil-resistors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-oxidation-resistors-market-size.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ferrite-toroid-coils-market-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/vacuum-fluorescent-displays-market.html

0 notes

Text

Optical Materials Market

Optical Materials Market size is forecast to reach US$4.6 billion by 2026 after growing at a CAGR of 4.7% during 2021–2026.

🔗 𝐆𝐞𝐭 𝐑𝐎𝐈-𝐟𝐨𝐜𝐮𝐬𝐞𝐝 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐟𝐨𝐫 𝟐𝟎𝟐𝟓-𝟐𝟎𝟑𝟏 → 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐍𝐨𝐰

Optical Materials Market is driven by the increasing demand for advanced materials used in lenses, optical fibers, coatings, and components across industries like telecommunications, electronics, healthcare, and automotive. These materials are essential for enhancing visual clarity, light manipulation, and high-performance optical systems.

Key segments include lenses, prisms, mirrors, and filters, with innovations in nanomaterials and coatings expanding their capabilities. As demand for technologies like augmented reality, fiber-optic communications, and high-resolution imaging grows, the market is poised for significant expansion.

🔸 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐜𝐚𝐥 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬: Continuous innovation in optics, including the development of high-performance lenses, coatings, and fiber optics, is a major driver. The rise of technologies like augmented reality (AR), virtual reality (VR), and quantum computing boosts demand for specialized optical materials.

🔸 𝐆𝐫𝐨𝐰𝐭𝐡 𝐢𝐧 𝐓𝐞𝐥𝐞𝐜𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬: The increasing demand for high-speed internet and 5G infrastructure is pushing the need for advanced optical fibers and components, driving market expansion.

🔸 𝐑𝐢𝐬𝐢𝐧𝐠 𝐃𝐞𝐦𝐚𝐧𝐝 𝐢𝐧 𝐇𝐞𝐚𝐥𝐭𝐡𝐜𝐚𝐫𝐞: Optical materials are crucial for diagnostic imaging, lasers, and medical devices, especially with the growing use of technologies like endoscopy, optical coherence tomography (OCT), and lasers in surgery.

🔸 𝐀𝐮𝐭𝐨𝐦𝐨𝐭𝐢𝐯𝐞 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐈𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧: The growing adoption of optical materials in advanced driver-assistance systems (ADAS), laser sensors, and LiDAR for autonomous vehicles is contributing to the market’s growth.

🔸 𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐄𝐥𝐞𝐜𝐭𝐫𝐨𝐧𝐢𝐜𝐬: The proliferation of high-definition displays, optical sensors, and camera technologies in smartphones, wearables, and other gadgets is creating strong demand for optical materials.

𝐋𝐢𝐦𝐢𝐭𝐞𝐝-𝐓𝐢𝐦𝐞 𝐎𝐟𝐟𝐞𝐫: 𝐆𝐞𝐭 $𝟏𝟎𝟎𝟎 𝐎𝐟𝐟 𝐘𝐨𝐮𝐫 𝐅𝐢𝐫𝐬𝐭 𝐏𝐮𝐫𝐜𝐡𝐚𝐬𝐞

𝐓𝐨𝐩 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬:

Optical Express | Dehlawi Optical Industries | Sumitomo Electric Optical Interconnect | ABB OPTICAL GROUP | SCHNEIDER Optical Machines | PDS Optical | PPG | MILDEX OPTICAL INC. | Hitachi High-Tech Optical Communication | Ciena | FLIR Systems | Corning Incorporated | ZEISS Group

#OpticalMaterials #AdvancedOptics #OpticalTechnology #FiberOptics #Telecommunications #ARVR #SmartMaterials #OpticalInnovation #MedicalImaging #PrecisionOptics #5GTechnology #FutureOfOptics #AutonomousVehicles #OpticalCoatings #SustainableTech

0 notes

Text

0 notes

Text

Advanced Driver Assistance Systems (ADAS) Market Size | Analysis, Trends 2024 - 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Advanced Driver Assistance Systems (ADAS) Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2031.” The study provides a detailed analysis of the industry, including the global Advanced Driver Assistance Systems (ADAS) Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Advanced Driver Assistance Systems (ADAS) Market?

The advanced driver assistance system (ADAS) market was US$ 28.1 Billion in 2022. Furthermore, the advanced driver assistance system (ADAS) market to register a CAGR of 17.1% which is expected to result in a market forecast value for 2031 of US$ 116.3 Billion.

What are Advanced Driver Assistance Systems (ADAS)?

Advanced Driver Assistance Systems (ADAS) are electronic systems embedded in vehicles to improve safety and convenience by aiding drivers in various tasks. Using technologies like sensors, cameras, radar, and lidar, ADAS offer real-time data for features such as adaptive cruise control, lane departure warnings, automatic emergency braking, and parking assistance. These systems aim to minimize human error, prevent accidents, and enhance the overall driving experience by providing alerts, automation, and control support. As a crucial element in the evolution of autonomous vehicles, ADAS significantly advance road safety and driving efficiency.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2068

What are the growth prospects and trends in the Advanced Driver Assistance Systems (ADAS) industry?

The advanced driver assistance systems (ADAS) market growth is driven by various factors and trends. The advanced driver assistance systems (ADAS) market is rapidly expanding due to the increasing demand for enhanced vehicle safety and automation. This market includes various technologies such as adaptive cruise control, lane departure warnings, automatic emergency braking, and parking assistance, all designed to improve driving safety and convenience. Key growth drivers are heightened consumer awareness of safety features, stringent government road safety regulations, and advancements in sensor and camera technologies. The movement towards autonomous vehicles also boosts the ADAS market, as these systems are vital for self-driving technology. Consequently, the ADAS market is crucial in the automotive industry’s progress towards safer and more efficient driving experiences. Hence, all these factors contribute to advanced driver assistance systems (ADAS) market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Type:

Parking Assist System

Adaptive Front-lighting

Night Vision System

Blind Spot Detection

Advanced Automatic Emergency Braking System

Collision Warning

Driver Drowsiness Alert

Traffic Sign Recognition

Lane Departure Warning

Adaptive Cruise Control

By Technology:

Radar

Lidar

Camera

By Vehicle Type:

Passenger Cars

Commercial Vehicles

By Applications:

Transportation and Logistics

Agriculture

Construction

Mining

Public Transportation

Security

By Region

North America

United States

Canada

Europe

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

Benelux

Nordic

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East & Africa

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Renesas Electronics Corporation

NXP Semiconductors

Panasonic Holdings Corporation

Valeo SA

Denso Corporation

Robert Bosch GmbH

Continental AG

Texas Instruments Incorporated

Magna International Inc.

AUTOLIV INC.

Infineon Technologies AG

View Full Report: https://www.reportsandinsights.com/report/Advanced Driver Assistance Systems (ADAS)-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Advanced Driver Assistance Systems (ADAS) Market share#Advanced Driver Assistance Systems (ADAS) Market size#Advanced Driver Assistance Systems (ADAS) Market trends

0 notes

Text

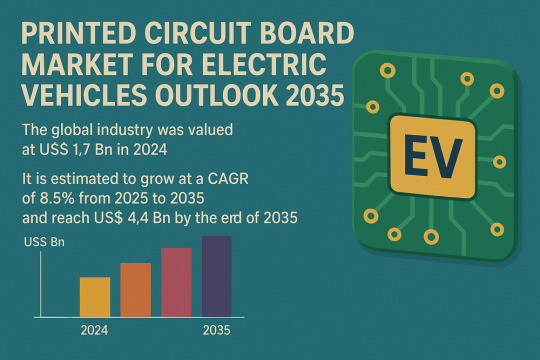

Smart Mobility Drives Smart PCBs: Market to Hit $4.4Bn by 2035

The global Printed Circuit Board (PCB) Market for Electric Vehicles (EVs) is set to witness significant expansion over the next decade, according to the latest market analysis. Valued at US$ 1.7 billion in 2024, the market is projected to grow at a CAGR of 8.5% from 2025 to 2035, reaching a valuation of US$ 4.4 billion by the end of the forecast period.

Market Overview: Printed Circuit Boards (PCBs) are the electronic backbone of electric vehicles, enabling power distribution, connectivity, and control across critical systems such as battery management, motor control, infotainment, and advanced safety features. With EV adoption accelerating globally, PCBs have become essential to the performance, reliability, and innovation of next-generation vehicles.

Market Drivers & Trends

One of the primary drivers of this market is the growing investment and strategic partnerships in the EV supply chain. Leading automakers and electronics companies are heavily investing in R&D and manufacturing capacity to meet the increasing demand for high-performance PCBs.

Moreover, the rise of autonomous and connected vehicles has made sophisticated electronics an indispensable part of modern transportation. The proliferation of features like ADAS (Advanced Driver-Assistance Systems), V2X communication, and in-vehicle infotainment is pushing the demand for compact, multi-layer, high-speed, and thermally efficient PCBs.

In 2023, EV sales in the U.S. surged by 60%, while the European Commission invested over US$ 6 billion in EV infrastructure further stimulating demand for advanced PCB solutions.

Latest Market Trends

The industry is witnessing a rapid shift toward flexible and high-density interconnect (HDI) PCBs, which are crucial for compact and space-saving vehicle designs. Flexible PCBs, in particular, are gaining traction in battery management systems and advanced sensor modules due to their lightweight and adaptable nature.

Additionally, regulatory advancements such as the FCC's allocation of the 5.9 GHz band for vehicle safety and autonomous functions have opened doors for new PCB capabilities. Real-time, high-speed data transmission requires advanced PCB materials and multi-layer configurations.

Key Players and Industry Leaders

Some of the most prominent players shaping the global printed circuit board market for electric vehicles include:

ABL CIRCUITS

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft I

Chin Poon Industrial Co., Ltd.

Compeq Manufacturing Co., Ltd.

HannStar Board Corporation

Kinwong Electronic Co. Ltd

LG Innotek

MEIKO ELECTRONICS Co., Ltd.

Nan Ya Printed Circuit Board Corporation

RayMing PCB

Rush PCB Ltd.

SCHWEIZER ELECTRONIC AG

Shenzhen Capel Technology Co., Ltd.

Shenzhen Fastprint Circuit Tech Co., Ltd.

TTM Technologies

Unimicron Technology Corporation

Victory Giant Technology Co., Ltd.

WUS Printed Circuit Co., Ltd.

Young Poong Group

Zhen Ding Tech. Group

Among Others

These companies are prioritizing innovation, expanding global manufacturing footprints, and forging strategic alliances to maintain competitiveness and cater to evolving industry needs.

Download now to explore primary insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86464

Recent Developments

October 2024 – Mektech Manufacturing announced a 920 million baht investment in Thailand to expand production capacity for flexible PCBs and FPCBA used in electric vehicles.

July 2024 – Omron Electronic Components Europe launched a high-power PCB relay for Level 2 EV charging stations. The innovation features double-break contact designs, enabling reduced heat dissipation and enhanced energy efficiency.

Market Opportunities

The market is poised for significant opportunities, particularly in:

OEM collaborations to co-develop application-specific PCBs for power electronics and smart mobility.

Flexible PCB technology, which is expected to revolutionize EV design with lightweight, customizable circuit boards.

Geographical expansion into regions like South Asia and Latin America, where EV adoption is accelerating, and supply chains are emerging.

Additionally, the ongoing reshoring of PCB manufacturing in regions such as North America and Europe presents untapped potential for local players.

Future Outlook

According to analysts, the convergence of EV electrification, autonomy, and connectivity will demand ever more sophisticated PCB solutions. Next-generation EVs will require PCBs capable of managing 50 Gbps data speeds, robust thermal management, and high signal integrity. Flexible, multilayer, and ceramic PCBs are expected to gain ground rapidly.

As regulations around emissions and vehicle safety become more stringent, automakers will rely heavily on advanced PCB solutions to remain compliant and competitive. From battery optimization to smart in-vehicle systems, the demand for high-performance PCBs is set to skyrocket.

Market Segmentation

The global PCB market for EVs is segmented across several parameters:

By Type: Multilayer (dominant with 73.98% market share in 2024), Double-sided, Single-sided

By Substrate Type: HDI/Micro-via/Build-up, Flexible, Rigid-flex, Rigid 1-2 Sided

By Material: FR4, Metal-Based, Ceramic, PTFE, Power Combi-boards

By Application: ADAS, Battery Management, Powertrain, Lighting & Display, Charging, Connectivity, etc.

By Vehicle Type: Passenger Cars, Buses, Two-Wheelers, Trucks, Off-Highway Vehicles

By End Users: OEMs, Tier 1 & 2 Suppliers, Aftermarket

Regional Insights

East Asia is the undisputed leader in the global market, accounting for 68.3% of the total share in 2024. The region’s dominance stems from:

A well-established electronics manufacturing ecosystem

Government support for EV expansion and green technology

Cost-effective production and high R&D capabilities

Japan, South Korea, and China house the majority of leading PCB suppliers and EV component manufacturers. Their early investment in automation and material innovation is positioning East Asia as the global hub for EV electronics.

Other key regions include:

North America, driven by government initiatives like the CHIPS Act

Europe, focused on sustainable manufacturing and reducing supply chain reliance on Asia

South Asia, emerging as a low-cost, high-volume manufacturing zone

Why Buy This Report?

This in-depth industry report offers:

Detailed market sizing and forecast (2020–2035)

Comprehensive segmentation across product, material, vehicle type, and region

Competitive landscape with profiles of 20+ leading companies

Insights into trends, innovations, and regional dynamics

Strategic recommendations for stakeholders, investors, and policymakers

Whether you're an investor, OEM, component supplier, or policy planner, this report serves as a strategic guide to understanding growth dynamics and identifying emerging opportunities in the PCB market for electric vehicles.

Explore Latest Research Reports by Transparency Market Research: Active Optical Cable Market: https://www.transparencymarketresearch.com/active-optical-cables.html

3D Cameras Market: https://www.transparencymarketresearch.com/3d-cameras-market.html

Optoelectronics Market: https://www.transparencymarketresearch.com/optoelectronics-market.html

Machine Safety Market: https://www.transparencymarketresearch.com/machine-safety-market.html

DC-DC Converter OBC Market: https://www.transparencymarketresearch.com/dc-dc-converter-obc-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Tyre Pressure Monitoring System Market Booming as EV Adoption and Connected Vehicles Demand Rise Steadily

The Tyre Pressure Monitoring System (TPMS) market has been gaining significant traction globally, fueled by increasing safety concerns, stringent government regulations, and rising awareness among consumers. TPMS is a crucial automotive safety feature designed to monitor the air pressure inside tyres and alert the driver if it falls below a safe level. By providing real-time tyre pressure data, TPMS helps reduce the risk of accidents, improves fuel efficiency, and extends tyre life.

Market Drivers

One of the primary drivers of the TPMS market is the rising demand for vehicle safety systems. As road safety becomes a greater concern, automotive manufacturers are integrating advanced technologies to minimize accidents. TPMS plays a pivotal role in preventing issues such as tyre blowouts and uneven tyre wear, which are common causes of accidents and breakdowns.

Moreover, government mandates and regulations in major economies have significantly accelerated the adoption of TPMS. For instance, in the United States, the TREAD Act mandates TPMS in all vehicles sold after 2007. Similarly, the European Union has made TPMS mandatory in all new passenger cars since 2014. Countries in Asia-Pacific, such as China and India, are also progressively adopting similar safety standards, further boosting market growth.

Technological Advancements

Technological innovation is another key factor propelling the TPMS market. The development of intelligent TPMS (iTPMS) and direct TPMS has enhanced the accuracy, reliability, and real-time responsiveness of tyre pressure monitoring. While indirect TPMS relies on wheel speed sensors, direct TPMS uses pressure sensors mounted on each tyre, providing more precise and timely information.

Integration with advanced driver-assistance systems (ADAS) and Internet of Things (IoT) platforms has also opened new avenues for growth. Smart TPMS can now relay data to smartphones, onboard diagnostics, and even cloud-based fleet management systems. These developments are particularly beneficial for commercial vehicle operators who manage large fleets and require constant tyre maintenance data.

Market Segmentation

The TPMS market can be segmented based on type, vehicle type, sales channel, and region. Based on type, the market is divided into direct and indirect TPMS. The direct TPMS segment dominates due to its accuracy and widespread use in high-end and mid-range vehicles.

By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and electric vehicles (EVs). Passenger vehicles represent the largest share, driven by growing consumer demand for safety and comfort. However, the EV segment is expected to grow rapidly, as manufacturers increasingly integrate TPMS to improve efficiency and range.

The sales channel segment includes OEMs and the aftermarket. Original equipment manufacturers (OEMs) hold the major market share, supported by regulations and consumer expectations for built-in safety features. Meanwhile, the aftermarket is also witnessing growth due to the rising adoption of TPMS kits in older vehicle models.

Regional Insights

North America and Europe are the leading markets for TPMS, attributed to strict safety regulations and high consumer awareness. The United States, Germany, France, and the UK are the major contributors. However, the Asia-Pacific region is projected to register the fastest growth, driven by the expansion of the automotive industry in China, India, South Korea, and Japan.

Latin America and the Middle East & Africa are emerging markets, showing promising growth potential due to rising vehicle ownership and gradual regulatory developments.

Challenges and Opportunities

Despite robust growth, the TPMS market faces several challenges, including high installation and replacement costs, especially for direct TPMS. Lack of awareness in developing regions and compatibility issues with older vehicles also pose hurdles.

However, these challenges are being offset by emerging opportunities. The growing popularity of connected cars, autonomous driving, and electric mobility is creating a demand for smart, efficient, and integrated TPMS solutions. Manufacturers investing in R&D and strategic collaborations are well-positioned to capitalize on these trends.

Future Outlook

The future of the TPMS market looks promising with continuous advancements in sensor technology, digital integration, and regulatory support. As the automotive industry transitions towards smarter, safer, and more sustainable mobility solutions, TPMS will remain a critical component in enhancing driver safety and vehicle performance.

0 notes

Text

Radar Market Drivers Fueling Technological Advancements and Expanding Application Across Global Sectors

The radar market is undergoing significant transformation, driven by technological innovations, growing applications, and heightened security concerns. Radar systems, which are vital for detecting objects and determining their range, speed, and direction, are increasingly being adopted across defense, automotive, aviation, weather monitoring, and maritime industries. As global industries evolve, a combination of economic, technological, and geopolitical factors is propelling the demand for radar systems. This article explores the major drivers behind the radar market’s growth and how they are influencing future developments.

Rising Defense and Security Expenditure

One of the most significant drivers of the radar market is the increasing investment in defense and security infrastructure by nations worldwide. Countries are focusing on enhancing border security, surveillance systems, and combat readiness, especially in the face of evolving geopolitical tensions and modern warfare threats. Radar technology plays a crucial role in missile detection, early warning systems, airspace monitoring, and naval navigation. Governments are allocating substantial budgets for upgrading radar capabilities, which in turn fuels market demand for advanced systems.

Expansion of Automotive Radar Applications

The rapid evolution of the automotive industry—especially the shift toward electric vehicles and autonomous driving—is pushing radar technology into the mainstream. Automotive radars are essential components of Advanced Driver Assistance Systems (ADAS), including adaptive cruise control, collision avoidance, lane-keeping assistance, and blind-spot detection. As consumer preference grows for safer and smarter vehicles, original equipment manufacturers (OEMs) are integrating radar systems to meet stringent safety regulations and enhance the driving experience. This trend is expected to be a long-term driver of the radar market.

Technological Advancements and Miniaturization

Innovations in radar technology have made systems more compact, energy-efficient, and cost-effective. The miniaturization of components using technologies like Gallium Nitride (GaN) and CMOS is enabling the development of radars that can be integrated into smaller platforms, including drones, smartphones, and compact vehicles. Enhanced digital signal processing, artificial intelligence (AI) integration, and improved resolution are expanding radar functionality in both commercial and military sectors. As performance continues to improve, radar systems are finding new use cases, broadening their market potential.

Increasing Use in Weather Monitoring and Disaster Management

Climate change and the increasing frequency of extreme weather events have underscored the importance of accurate weather forecasting and disaster preparedness. Radars are widely used for real-time tracking of storms, rainfall, and atmospheric disturbances. Governments and meteorological agencies are investing in Doppler radar systems and phased-array radar technologies to enhance forecasting capabilities and mitigate disaster impacts. This growing reliance on radar for environmental monitoring contributes significantly to market growth.

Growth in Air Traffic and Airport Modernization

The aviation sector remains a major consumer of radar systems. With air travel recovering post-pandemic and global passenger traffic on the rise, there is a renewed focus on airspace management, collision avoidance, and runway safety. Airport modernization projects, particularly in emerging economies, are boosting the deployment of advanced air traffic control radars and surveillance systems. These developments not only improve operational efficiency but also elevate safety standards, creating additional demand for radar solutions.

Maritime Safety and Port Management

Another key driver is the increasing need for maritime surveillance and navigation. As global trade and shipping traffic expand, ports and vessels are relying heavily on radar systems for collision prevention, docking, route planning, and environmental monitoring. Radar plays a pivotal role in ensuring safe navigation under challenging conditions such as fog, darkness, or congested routes. Governments and private port authorities are upgrading their radar infrastructure to enhance maritime security and efficiency.

Government Regulations and Initiatives

Regulatory support and strategic initiatives are also playing an influential role in shaping the radar market. Governments are mandating the use of radar-based safety technologies in vehicles and aerospace systems. Initiatives supporting smart infrastructure, such as intelligent transportation systems (ITS), encourage the integration of radar technology into city planning and management. These policy measures act as a catalyst for innovation and adoption, particularly in countries with active digital transformation agendas.

Demand from Emerging Economies

Rapid industrialization and urbanization in emerging economies are opening up new markets for radar system deployment. Countries in Asia-Pacific, the Middle East, and Latin America are investing in defense modernization, infrastructure development, and public safety systems. These regions are adopting radar solutions in varied applications—from smart traffic management and border surveillance to disaster preparedness—thus expanding the global footprint of radar technologies.

In conclusion, the radar market is being shaped by a dynamic mix of drivers spanning technology, security, transportation, and climate resilience. From autonomous vehicles and smart cities to border defense and weather prediction, radar systems are at the heart of several transformative changes. As innovations continue to improve radar capabilities and reduce costs, adoption is expected to deepen across both traditional and emerging sectors, ensuring sustained market growth in the years ahead.

0 notes