#China Composite Insulators Market

Text

Aluminium Composite Panels Market: Trends, Growth, and Future Prospects

Aluminium Composite Panels (ACPs) are gaining significant traction in the construction and renovation industries due to their versatile applications, aesthetic appeal, and functional benefits. These panels consist of two aluminium sheets bonded to a non-aluminium core, offering a combination of durability, lightweight properties, and resistance to weathering. The market for ACPs is expanding rapidly, driven by increasing urbanization, rising demand for sustainable building materials, and advancements in technology.

Market Overview

The global aluminium composite panels market has experienced substantial growth over the past decade. According to industry reports, the market size was valued at USD X billion in 2023 and is projected to reach USD Y billion by 2030, growing at a CAGR of Z% during the forecast period. This growth can be attributed to several factors, including the increasing construction activities in emerging economies, the rising focus on energy-efficient buildings, and the growing adoption of modern architectural designs.

Key Drivers

1. Urbanization and Infrastructure Development: Rapid urbanization, particularly in developing countries, is a major driver for the ACP market. As cities expand and new urban areas are developed, the demand for modern construction materials that offer both aesthetic and functional benefits is on the rise. ACPs are favored for their ability to provide a sleek, contemporary look while ensuring durability and cost-effectiveness.

2. Sustainable Building Materials: With growing environmental concerns, there is a heightened focus on sustainable building practices. Aluminium composite panels are increasingly preferred due to their recyclable nature and energy efficiency. They contribute to green building certifications and help in reducing the overall carbon footprint of structures.

3. Technological Advancements: Innovations in manufacturing processes and material technologies have significantly enhanced the performance characteristics of ACPs. Improved fire resistance, better insulation properties, and advanced surface coatings are some of the developments that have broadened the application scope of these panels.

For a comprehensive analysis of the market drivers:- https://univdatos.com/report/aluminium-composite-panels-market/

Applications

ACPs are used in a wide range of applications across various sectors:

- Exterior Cladding: One of the most common uses of ACPs is in exterior cladding or facades. They offer a modern and clean appearance, protect the building structure from weather elements, and provide insulation.

- Interior Decoration: ACPs are also popular for interior applications such as false ceilings, partitions, and wall panels. Their lightweight and flexible nature make them easy to install and maintain.

- Signage and Advertising: The durability and aesthetic appeal of ACPs make them suitable for outdoor signage and advertising boards. They can withstand harsh weather conditions and maintain their appearance over time.

- Transportation: In the transportation industry, ACPs are used for vehicle bodies and interiors, providing a lightweight yet strong solution that enhances fuel efficiency and durability.

For a sample report, visit:- https://univdatos.com/get-a-free-sample-form-php/?product_id=37129

Regional Insights

The ACP market is geographically diverse, with significant growth observed in Asia-Pacific, North America, and Europe.

- Asia-Pacific: This region dominates the market due to rapid urbanization, growing construction activities, and increasing investments in infrastructure development. Countries like China, India, and Japan are major contributors to the market growth.

- North America: The demand for ACPs in North America is driven by the need for energy-efficient buildings and the renovation of old structures. The presence of key manufacturers and technological advancements also contribute to market growth.

- Europe: In Europe, stringent regulations regarding building safety and energy efficiency are propelling the adoption of ACPs. The region's focus on sustainable construction practices further boosts market demand.

Future Prospects

The future of the aluminium composite panels market looks promising, with several trends likely to shape its trajectory:

- Green Buildings: The shift towards green building practices and sustainable construction materials will continue to drive the demand for ACPs. Manufacturers are likely to focus on developing more eco-friendly products to meet this demand.

- Innovative Designs: As architectural trends evolve, there will be a growing need for innovative and customizable ACP solutions. This will encourage manufacturers to invest in R&D and expand their product portfolios.

- Smart Cities: The development of smart cities, with their emphasis on advanced infrastructure and sustainable living, will create new opportunities for ACP applications.

In conclusion, the aluminium composite panels market is set for robust growth, driven by urbanization, sustainability trends, and technological advancements. As the construction industry continues to evolve, ACPs will play a crucial role in shaping modern architectural landscapes.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

#Aluminium Composite Panels Market#Aluminium Composite Panels Market Growth#Aluminium Composite Panels Market Share#Aluminium Composite Panels Market Forecast

0 notes

Text

Owens Corning: Global Locations and Facilities

Owens Corning, a leader in building materials and composite solutions, operates a vast network of facilities worldwide. This article provides an extensive overview of Owens Corning's global locations, highlighting key manufacturing sites, regional offices, and research centers that drive the company's innovation and market reach.

North America

United States

Owens Corning's presence in the United States is extensive, with numerous facilities dedicated to manufacturing, research, and corporate operations.

Key Locations:

Toledo, Ohio: Headquarters and central hub for Owens Corning's corporate operations, housing executive management and key administrative functions.

Granville, Ohio: Science and Technology Center, a cornerstone for research and development activities focused on advancing insulation and composite materials.

Kansas City, Missouri: Major manufacturing site for roofing materials, serving both residential and commercial markets.

Fort Smith, Arkansas: Production facility specializing in insulation products, pivotal for energy efficiency solutions.

Canada

Owens Corning maintains a significant footprint in Canada, with facilities supporting the production of insulation and roofing materials.

Key Locations:

Toronto, Ontario: Regional office and distribution center, coordinating operations across Canada.

Candiac, Quebec: Manufacturing plant for insulation products, catering to the Canadian market's demand for energy-efficient building materials.

Europe

France

Owens Corning operates several key facilities in France, central to its European operations.

Key Locations:

Chambery: Manufacturing site for composite materials, supplying advanced solutions for various industrial applications.

Laval: Insulation production facility, crucial for meeting the energy efficiency needs of the European market.

Germany

Germany hosts important Owens Corning facilities that contribute to its European market leadership.

Key Locations:

Apeldoorn: Production plant for insulation materials, supporting the regional demand for sustainable building solutions.

Birkenfeld: Manufacturing site specializing in composite materials, serving automotive and industrial sectors.

Asia-Pacific

China

Owens Corning has established a robust presence in China, with facilities that bolster its market penetration in the Asia-Pacific region.

Key Locations:

Shanghai: Regional headquarters and innovation center, focusing on strategic growth and technological advancements.

Jiangsu: Major manufacturing site for composite materials, supporting the construction and automotive industries.

India

India is a growing market for Owens Corning, with facilities aimed at expanding its footprint in the region.

Key Locations:

Taloja, Maharashtra: Production plant for insulation and roofing materials, addressing the needs of the Indian construction market.

Latin America

Brazil

Owens Corning's operations in Brazil are essential for serving the Latin American market.

Key Locations:

Rio Claro: Manufacturing facility for insulation products, catering to regional demand for energy-efficient building solutions.

São Paulo: Regional office, coordinating operations and strategic initiatives across Latin America.

Middle East and Africa

Saudi Arabia

In the Middle East, Owens Corning focuses on addressing the region's unique building and industrial requirements.

Key Locations:

Dammam: Manufacturing site for composite materials, crucial for infrastructure projects and industrial applications in the region.

South Africa

Owens Corning's presence in Africa is marked by key facilities supporting regional growth.

Key Locations:

Johannesburg: Regional office and distribution center, managing operations and logistics across the African continent.

Research and Innovation Centers

Owens Corning places a strong emphasis on research and innovation, with dedicated centers worldwide.

Granville, Ohio, USA

The Science and Technology Center in Granville is a pivotal site for Owens Corning's research and development efforts. It focuses on advancing materials science and developing innovative solutions for insulation, roofing, and composites.

Shanghai, China

The Innovation Center in Shanghai is instrumental in driving technological advancements and product development tailored to the Asia-Pacific market. It fosters collaboration with local industries and academic institutions.

Conclusion

Owens Corning's extensive network of global locations underscores its commitment to innovation, sustainability, and market leadership. By strategically positioning its facilities worldwide, the company ensures efficient production, distribution, and customer service, meeting the diverse needs of its global clientele.

0 notes

Text

2032, Expanded Polystyrene (EPS) Recycling Market Growth and Research 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Expanded Polystyrene (EPS) Recycling Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Expanded Polystyrene (EPS) Recycling Market Size share, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Expanded Polystyrene (EPS) Recycling Market?

The expanded polystyrene (EPS) recycling market size reached US$ 19.7 Billion in 2023. Looking forward, Reports and Insights expects the market to reach US$ 36.5 Billion by 2032, exhibiting a growth rate (CAGR) of 6.7% during 2024-2032.

What are Expanded Polystyrene (EPS) Recycling?

EPS recycling is the practice of collecting, sorting, and processing EPS foam products to reclaim the material for reuse. EPS, also known as Styrofoam, is a lightweight and rigid plastic material utilized in packaging and insulation. The recycling process involves compressing the foam to reduce its size and then melting it down to create dense blocks or pellets suitable for manufacturing new products. EPS recycling contributes to environmental sustainability by diverting EPS waste from landfills and reducing the demand for new plastic production.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1775

What are the growth prospects and trends in the Expanded Polystyrene (EPS) Recycling industry?

The expanded polystyrene (EPS) recycling market growth is driven by various factors. The market for recycling expanded polystyrene (EPS) is expanding, fueled by growing environmental consciousness and regulatory measures promoting recycling practices. EPS, widely utilized in packaging and construction, significantly contributes to plastic waste. Recycling EPS involves collecting, cleaning, and processing it into reusable material for diverse applications. Market growth is propelled by increasing demand for recycled EPS in the construction and packaging sectors, driven by sustainability objectives and economic advantages. Moreover, technological advancements in EPS recycling and government support for recycling initiatives are further driving market growth. Hence, all these factors contribute to expanded polystyrene (EPS) recycling market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By EPS Waste Type:

Post-consumer EPS waste

Pre-consumer EPS waste

By EPS Recycling Process:

Mechanical recycling

Chemical recycling

Other recycling processes

By End-Use Industry:

Packaging

Construction

Electrical and Electronics

Automotive

Others

By Recycled EPS Product:

Packaging materials

Insulation boards

Molded products

Composite materials

Others

By Source of Collection:

Municipal recycling programs

Industrial and commercial collection

Retail collection

Other

By Recycling Equipment:

Shredders

Granulators

Densifiers

Extruders

Others

By Application:

Packaging

Building and construction

Insulation

Consumer goods

Others

By Distribution Channel:

Direct sales

Distributor sales

E-commerce

By Market Type:

Business to Business (B2B)

Business to Consumer (B2C)

Segmentation By Region:

North America:

United States

Canad

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Dart Container Corporation

NOVA Chemicals Corporation

ACH Foam Technologies, LLC

Ravago Recycling Group

Styro Recycle LLC

Total, Petrochemicals & Refining USA, Inc.

Alpek Polyester

Repsol S.A.

Vanden Recycling

Plasti-Fab Ltd.

NexKemia Petrochemicals Inc.

EPS Industry Alliance

Vita Group

FPC Foam Plastics Corporation

Winco Foam Industries Limited

View Full Report: https://www.reportsandinsights.com/report/Expanded Polystyrene (EPS) Recycling-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

#Expanded Polystyrene (EPS) Recycling Market share#Expanded Polystyrene (EPS) Recycling Market size#Expanded Polystyrene (EPS) Recycling Market trends

0 notes

Text

Glass Fiber Prices Trend, Database, Chart, Index, Forecast

Glass Fiber prices have been subject to significant fluctuations due to various market dynamics, including supply chain disruptions, raw material costs, and shifts in global demand. In recent years, the glass fiber industry has experienced a notable increase in prices, primarily driven by rising costs of raw materials such as silica sand, limestone, and soda ash. These materials are crucial for the production of glass fibers, and any increase in their prices directly impacts the overall cost of glass fiber production. Additionally, energy costs, which are a major component in the manufacturing process, have also seen an upward trend. This rise in energy prices, particularly for natural gas and electricity, has further contributed to the escalation of glass fiber prices.

The initial phase of the pandemic saw a sharp decline in demand as construction projects were halted and manufacturing activities slowed down. However, as economies began to recover, there was a surge in demand for glass fibers, particularly from the construction and automotive sectors. This sudden increase in demand, coupled with ongoing supply chain disruptions, created a supply-demand imbalance, further driving up prices. Moreover, logistical challenges such as port congestion and transportation bottlenecks exacerbated the situation, leading to delays and increased costs in shipping raw materials and finished products.

Get Real Time Prices of Glass Fiber: https://www.chemanalyst.com/Pricing-data/glass-fiber-1558

Technological advancements and innovations in the glass fiber industry have also played a role in shaping price trends. Manufacturers are continuously investing in new technologies to improve production efficiency and reduce costs. However, the initial investment required for these technological upgrades can be substantial, and these costs are often passed on to consumers in the form of higher prices. On the other hand, advancements that lead to more efficient production processes can eventually help in stabilizing or even reducing prices in the long term.

Environmental regulations and sustainability initiatives have increasingly influenced the glass fiber market. Many countries are implementing stricter environmental standards to reduce carbon emissions and promote sustainable practices. Compliance with these regulations often requires additional investments in cleaner production technologies and processes, which can increase production costs. These costs, in turn, are reflected in the final prices of glass fiber products. However, the push towards sustainability also presents opportunities for innovation and the development of new, eco-friendly products that may command a premium price in the market.

Global trade policies and tariffs have also had a significant impact on glass fiber prices. Trade tensions between major economies, such as the United States and China, have led to the imposition of tariffs on various goods, including glass fibers. These tariffs can lead to increased prices for imported glass fibers, thereby affecting the overall market. Additionally, changes in trade policies can create uncertainty in the market, influencing the pricing strategies of manufacturers and suppliers.

The demand for glass fiber is closely tied to the performance of key end-use industries, such as construction, automotive, wind energy, and aerospace. The construction industry, in particular, is a major consumer of glass fiber products, using them in applications such as insulation, reinforcement, and composites. Economic conditions that affect the construction industry, such as housing market trends and infrastructure investments, can have a direct impact on the demand for glass fibers and, consequently, their prices. Similarly, the growth of the automotive and wind energy sectors, driven by the shift towards renewable energy and lightweight, fuel-efficient vehicles, has boosted the demand for glass fiber-reinforced composites, influencing price trends.

Looking ahead, the glass fiber market is expected to continue experiencing price volatility due to a combination of factors. Continued investments in infrastructure projects, particularly in developing regions, are likely to sustain strong demand for glass fiber products. At the same time, ongoing supply chain challenges and fluctuations in raw material and energy costs will continue to pose challenges for manufacturers. The industry's ability to navigate these challenges while embracing technological advancements and sustainability practices will be crucial in determining future price trends.

In conclusion, glass fiber prices are influenced by a complex interplay of factors including raw material costs, energy prices, supply chain dynamics, technological advancements, environmental regulations, and global trade policies. The recent increase in prices reflects a combination of these factors, exacerbated by the impacts of the COVID-19 pandemic and ongoing supply chain disruptions. As the market continues to evolve, manufacturers and consumers alike will need to adapt to changing conditions and seek innovative solutions to manage costs and ensure a sustainable supply of glass fiber products. The future of glass fiber pricing will depend on the industry's ability to balance demand with sustainable production practices while navigating the challenges posed by global economic and regulatory environments.

Get Real Time Prices of Glass Fiber: https://www.chemanalyst.com/Pricing-data/glass-fiber-1558

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

0 notes

Text

Resin Market: Long-Term Value & Growth Seen Ahead

Market Research Forecast added research publication document on Worldwide Resin Market breaking major business segments and highlighting wider level geographies to get deep dive analysis on market data. The study is a perfect balance bridging both qualitative and quantitative information of Worldwide Resin Market. The study provides valuable market size data for historical (Volume** & Value) from 2019 to 2023 which is estimated and forecasted till 2032*. Some are the key & emerging players that are part of coverage and have being profiled are DuPont (U.S.),Arkema (France),BASF SE (Germany),INEOS Holdings Ltd. (U.K.),Hexion (U.S.),Invista (U.S.),LyondellBasell (Netherlands),Mitsubishi Engineering-Plastics Corporation (Japan),Mitsui Chemicals (Japan),Nova Chemicals (Canada),Qenos (Australia),Radici Group (Italy),SABIC (Saudi Arabia),Repsol (Spain),Sumitomo Chemical Co. Ltd. (Japan),Teijin Limited (Japan),Tosoh Corporation (Japan),Toray Group (Japan).

Get free access to Sample Report in PDF Version along with Graphs and Figures @ https://marketresearchforecast.com/report/reports/resin-market-1341/sample-report

The Resin Marketsize was valued at USD 533.55 USD Billion in 2023 and is projected to reach USD 750.76 USD Billion by 2032, exhibiting a CAGR of 5.0 % during the forecast period.resins can be formulated from either organic or synthetic compounds that convert from the liquid state to a solid, homogeneous structure. Resin is a very tough material which can be used even in such harshest conditions as impact of the water and other environmental factors. Annealing makes wire unbreakable when it is restored to its original properties by cooling. This feature enhances its multi-purpose characteristics for use indoors in settings like bathrooms, kitchens, and living rooms. They might be the products of natural materials or be manufactured using other chemicals. Resins are remarkably resistant to all types of chemicals and therefore a perfect choice for application in a large pool of industrial and commercial utilities. The resins are heat-resistant, therefore, they will not melt nor get stuck to the hot wheels of cars when a garage is being entered. Tackifiers samples are unlike any other clear resins, the fact if they are of a good quality and professional makes them ideal for decorative and aesthetic use.

Keep yourself up-to-date with latest market trends and changing dynamics due to COVID Impact and Economic Slowdown globally. Maintain a competitive edge by sizing up with available business opportunity in Resin Market various segments and emerging territory.

Influencing Market Trend

Rising demand for flexible packaging in the food & beverage industry

Increased adoption of lightweight materials in transportation sectors

Growing use of resins in construction for insulation and reinforcement

Challenges:

Volatile Raw Material Costs: Price fluctuations of crude oil and natural gas impact resin production costs.

Competition from Alternative Materials: Growing adoption of metals, ceramics, and composites in various applications.

Environmental Concerns: Conce

Have Any Questions Regarding Global Resin Market Report, Ask Our Experts@ https://marketresearchforecast.com/report/reports/resin-market-1341/enquiry-before-buy Analysis by Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polyvinyl Chloride, Acrylonitrile Butadiene Styrene, Polyamide, Polycarbonate, Polyurethane, Polystyrene, and Others), by End-use Industry (Packaging, Automotive & Transportation, Building & Construction, Consumer Goods/Lifestyle, Electrical & Electronics, Agriculture, and Others), by North America (U.S., Canada), by Europe (Germany, U.K., France, Italy, Spain, Rest of Europe), by Asia Pacific (China, Japan, India, South Korea, Rest of Asia Pacific), by Latin America (Brazil, Argentina, Mexico, Rest of Latin America), by Middle East & Africa (Saudi Arabia, South Africa, Rest of Middle East & Africa) Forecast 2024-2032

Competitive landscape highlighting important parameters that players are gaining along with the Market Development/evolution

• % Market Share, Segment Revenue, Swot Analysis for each profiled company [DuPont (U.S.),Arkema (France),BASF SE (Germany),INEOS Holdings Ltd. (U.K.),Hexion (U.S.),Invista (U.S.),LyondellBasell (Netherlands),Mitsubishi Engineering-Plastics Corporation (Japan),Mitsui Chemicals (Japan),Nova Chemicals (Canada),Qenos (Australia),Radici Group (Italy),SABIC (Saudi Arabia),Repsol (Spain),Sumitomo Chemical Co. Ltd. (Japan),Teijin Limited (Japan),Tosoh Corporation (Japan),Toray Group (Japan)]

• Business overview and Product/Service classification

• Product/Service Matrix [Players by Product/Service comparative analysis]

• Recent Developments (Technology advancement, Product Launch or Expansion plan, Manufacturing and R&D etc)

• Consumption, Capacity & Production by Players

The regional analysis of Global Resin Market is considered for the key regions such as Asia Pacific, North America, Europe, Latin America and Rest of the World. North America is the leading region across the world. Whereas, owing to rising no. of research activities in countries such as China, India, and Japan, Asia Pacific region is also expected to exhibit higher growth rate the forecast period 2023-2028.

Table of Content

Chapter One: Industry Overview

Chapter Two: Major Segmentation (Classification, Application and etc.) Analysis

Chapter Three: Production Market Analysis

Chapter Four: Sales Market Analysis

Chapter Five: Consumption Market Analysis

Chapter Six: Production, Sales and Consumption Market Comparison Analysis

Chapter Seven: Major Manufacturers Production and Sales Market Comparison Analysis

Chapter Eight: Competition Analysis by Players

Chapter Nine: Marketing Channel Analysis

Chapter Ten: New Project Investment Feasibility Analysis

Chapter Eleven: Manufacturing Cost Analysis

Chapter Twelve: Industrial Chain, Sourcing Strategy and Downstream Buyers

Read Executive Summary and Detailed Index of full Research Study @ https://marketresearchforecast.com/reports/reports/resin-market-1341

Highlights of the Report

• The future prospects of the global Resin Market during the forecast period 2023-2028 are given in the report.

• The major developmental strategies integrated by the leading players to sustain a competitive market position in the market are included in the report.

• The emerging technologies that are driving the growth of the market are highlighted in the report.

• The market value of the segments that are leading the market and the sub-segments are mentioned in the report.

• The report studies the leading manufacturers and other players entering the global Resin Market. Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Middle East, Africa, Europe or LATAM, Southeast Asia.

Contact US :

Craig Francis (PR & Marketing Manager)

Market Research Forecast

Unit No. 429, Parsonage Road Edison, NJ

New Jersey USA – 08837

Phone: +1 201 565 3262, +44 161 818 8166

[email protected]

#Global Resin Market#Resin Market Demand#Resin Market Trends#Resin Market Analysis#Resin Market Growth#Resin Market Share#Resin Market Forecast#Resin Market Challenges

0 notes

Text

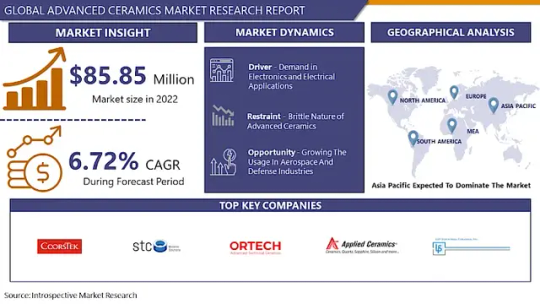

Advanced Ceramics Market: Global Industry Analysis and Forecast 2023 – 2030

Advanced Ceramics Market Size Was Valued at USD 85.85 Billion in 2022, and is Projected to Reach USD 144.44Billion by 2030, Growing at a CAGR of 6.72% From 2023-2030.

The advanced ceramics market encompasses a wide range of high-performance ceramic materials designed for specialized applications across various industries. These ceramics exhibit exceptional mechanical, electrical, thermal, and chemical properties, making them indispensable in demanding environments where traditional materials fall short. Advanced ceramics are used in the production of electronic components such as capacitors, insulators, substrates, and sensors due to their excellent dielectric properties, high thermal conductivity, and resistance to corrosion. Ceramics are employed in automotive engineering for components like catalytic converters, sensors, spark plugs, and brake systems due to their ability to withstand high temperatures, reduce friction, and enhance fuel efficiency.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://introspectivemarketresearch.com/request/15723

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

Leading players involved in the Advanced Ceramics Market include:

CoorsTek, Inc. (US), Superior Technical Ceramics (US), Ortech Advanced Ceramics (US), Applied Ceramics, Inc. (US), LSP Industrial Ceramics, Inc. (US), Momentive Performance Materials Inc. (US), NGK Spark Plug Co., Ltd. (Japan), Ferrotec Corporation (Japan), and Other Major Players.

If You Have Any Query Advanced Ceramics Market Report, Visit:

https://introspectivemarketresearch.com/inquiry/15723

Segmentation of Advanced Ceramics Market:

By Type

Alumina

Titanite

Zirconia

Silicon Carbide

Aluminium Nitride

Silicon Nitride

By Application

Monolithic Ceramics

Ceramic Matrix Composites

Ceramic Coating

By End User Industry

Electrical & Electronics

Transportation

Medical

Defense

Security Chemical

By Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

What to Expect in Our Report?

(1) A complete section of the Advanced Ceramics market report is dedicated for market dynamics, which include influence factors, market drivers, challenges, opportunities, and trends.

(2) Another broad section of the research study is reserved for regional analysis of the Advanced Ceramics market where important regions and countries are assessed for their growth potential, consumption, market share, and other vital factors indicating their market growth.

(3) Players can use the competitive analysis provided in the report to build new strategies or fine-tune their existing ones to rise above market challenges and increase their share of the Advanced Ceramics market.

(4) The report also discusses competitive situation and trends and sheds light on company expansions and merger and acquisition taking place in the Advanced Ceramics market. Moreover, it brings to light the market concentration rate and market shares of top three and five players.

(5) Readers are provided with findings and conclusion of the research study provided in the Advanced Ceramics Market report.

Our study encompasses major growth determinants and drivers, along with extensive segmentation areas. Through in-depth analysis of supply and sales channels, including upstream and downstream fundamentals, we present a complete market ecosystem.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=15723

About Us:

We are technocratic market research and consulting company that provides comprehensive and data-driven market insights. We hold the expertise in demand analysis and estimation of multidomain industries with encyclopedic competitive and landscape analysis. Also, our in-depth macro-economic analysis gives a bird's eye view of a market to our esteemed client. Our team at Pristine Intelligence focuses on result-oriented methodologies which are based on historic and present data to produce authentic foretelling about the industry. Pristine Intelligence's extensive studies help our clients to make righteous decisions that make a positive impact on their business. Our customer-oriented business model firmly follows satisfactory service through which our brand name is recognized in the market.

Contact Us:

Office No 101, Saudamini Commercial Complex,

Right Bhusari Colony,

Kothrud, Pune,

Maharashtra, India - 411038 (+1) 773 382 1049 +91 - 81800 - 96369

Email: [email protected]

#Advanced Ceramics#Advanced Ceramics Market#Advanced Ceramics Market Size#Advanced Ceramics Market Share#Advanced Ceramics Market Growth#Advanced Ceramics Market Trend#Advanced Ceramics Market segment#Advanced Ceramics Market Opportunity#Advanced Ceramics Market Analysis 2023

0 notes

Text

Cryogenic Tanks Market Size and Growth Prospects: A Deep Dive Analysis

Cryogenic Tanks Market will grow at highest pace owing to increasing demand from chemicals and petrochemicals industry

Cryogenic tanks are high-performance containers used for storing gases such as nitrogen, oxygen, argon, hydrogen and natural gas at cryogenic temperatures. Cryogenic tanks find widespread applications in shipping industrial and medical gases over long distances. They play a pivotal role in preserving perishable commodities during transportation. Cryogenic tanks offer excellent thermal insulation to maintain extremely low temperatures inside while preventing the condensation of atmospheric gases. Key advantages include durability, ease of handling and transportation. Rising demand from petrochemical facilities, gas liquefaction plants and research laboratories is fuelling sales of cryogenic tanks.

The Global Cryogenic Tanks Market is estimated to be valued at US$ 6.51 Bn in 2024 and is expected to exhibit a CAGR of 5.0% over the forecast period 2023 to 2030.

Key Takeaways

Key players operating in the Cryogenic Tanks are ArcelorMittal, China Baowu Group, Nippon Steel Corporation, POSCO, Shagang Group, Ansteel Group. Cryogenic tanks find widespread applications in storing and transporting industrial gases in various end-use industries such as energy & power, chemicals, metallurgy, electronics, shipping and biomedical. The global cryogenic tanks market is primarily driven by increasing demand from the chemicals and petrochemicals industry.

Market Trends

One of the key trends in the cryogenic tanks market is the growing demand for mid-sized cryogenic tanks in the energy sector. Mid-sized tanks with capacities ranging from 10,000-40,000 liters are increasingly used for onsite storage of liquefied natural gas and hydrogen at refueling stations. Another major trend is the increasing adoption of cryogenic tanks made from composite materials.

Market Opportunities

One of the major opportunities for cryogenic tank manufacturers is the rising demand from the LNG industry. Rapid infrastructure development and expansion of LNG facilities across Asia Pacific and Middle East are expected to drive sales. Another key opportunity is presented by the hydrogen economy. Widespread commercialization of fuel cell vehicles and setting up of hydrogen refueling network will augment demand for hydrogen storage and transportation cryogenic tanks over the forecast period.

Impact of COVID-19 on Cryogenic Tanks Market

The outbreak of COVID-19 has significantly impacted the cryogenic tanks market. During the lockdown period, demand for cryogenic gases such as oxygen, nitrogen, and argon decreased sharply from industries such as oil & gas, metal manufacturing, healthcare, etc. This led to a decline in the production of cryogenic tanks. Manufacturing facilities were shut down during lockdowns to curb the spread of the virus. Supply chain disruptions affected the availability of raw materials for tank production. Transportation restrictions made it difficult to deliver completed tanks to customers.

Geographical Regions with High Concentration in Cryogenic Tanks Market

Asia Pacific accounts for the largest share of the global cryogenic tanks market in terms of value. This is mainly due to the massive semiconductor, metal manufacturing and healthcare industries in countries such as China, Japan, India and South Korea which create sustained demand for cryogenic gases and associated storage and transportation equipment. North America ranks second powered by oil & gas exploration activities and healthcare sector development in the US and Canada. Europe is another major regional market led by Germany, UK, France and countries increasing investments to bolster industrial gas infrastructure and expand gas transport networks for supporting manufacturing and technology industries.

0 notes

Text

Thermoplastic Elastomers Market: Top 3 Industrial Applications

According to UNEP, energy accounts for approximately 60%of global greenhouse gas emissions, making energy efficiency a top priority across various industries. In this context, thermoplastic elastomers (TPEs) have emerged as a viable solution, reducing energy consumption by nearly 75%. They have gained recognition among product developers and designers as an advanced alternative to thermoset elastomers. Triton’s estimates suggest that the global thermoplastic elastomers market is expected to grow at a CAGR of 6.37% in revenue and 2.61% in volume during 2023-2030.

Another significant factor is the increasing trend of 3D printing. Due to their durable, flexible, chemically resistant, and user-friendly properties, TPEs serve as filaments in additive manufacturing methods like selective laser sintering (SLS) and fused deposition modeling (FDM). For instance, renowned companies such as New Balance, Under Armour, and Nike have adopted thermoplastic polyurethane-based 3D printing for robust and flexible midsoles.

In this blog, we’ll explore the wide-ranging applications of TPEs and their significant presence in the top three industries.

· Automotive:

In terms of industrial vertical, automotive leads with $9325.51 million

These high-performance polymers have gained significant traction in the automotive industry. Polystyrene TPE, for example, is used in multiple auto parts like instrument panels, wheel covers, dashboard elements, pillar trims, door liners, seat belt components, etc. These plastics, unlike metals, are cost-effective and improve vehicle energy efficiency by reducing weight.

Moreover, their lightweight quality boosts vehicle fuel efficiency, with a 10% weight reduction translating to 5-7% lower fuel consumption. This has prompted TPE manufacturers like Covestro AG to introduce new production lines for high-performance thermoplastic polyurethanes to produce paint production films.

Regional Focus: Asia-Pacific set to be the fastest-growing region at 6.46%

Asia-Pacific is the world’s largest automotive producer, with China, India, Japan, and Indonesia leading the way. Nations like India and Indonesia are attracting investments in locomotive and high-speed rail manufacturing, further bolstering the demand for TPE in the region. Additionally, China is actively boosting production, aiming for 7 million annually by 2025, constituting 20% of total new car production. This surge in EV production is set to drive demand for polyurethane and polystyrene in automotive applications, driving the Asia-Pacific thermoplastic elastomers market.

· Electrical & Electronics:

Thermoplastic elastomers are preferred for electrical insulation due to their strength, flexibility, and resistance to corrosive substances like acids. Besides this, TPE composites, including polycarbonate, enhance impact and flame resistance in electronic devices and household appliances. Given these benefits, several companies have entered into partnerships or acquisitions to expand their footing. For example,

- Arkema SA acquired Polytec PT in May 2023 to expand offerings and serve the electronics sector.

- Avient Corporation collaborated with BASF SE to offer colored grades of Ultrason® high-performance polymers to provide users in the electrical & electronics sector with comprehensive technical support.

Widely Employed Material Type:

Thermoplastic polyolefin serves multiple purposes in the sector, finding use in low-voltage wire and extruded hoses. TPOs are preferred over TPVs in wire and cable applications due to their cost-effectiveness, excellent electrical properties, and temperature versatility. As per Triton’s report, polyolefin is expected to register a CAGR of 6.30% during the forecast period 2023-2030 in terms of material type.

· Adhesives & Sealants:

Thermoplastic elastomers have gained popularity in providing strong bonds and flexibility without mixing or high-temperature curing. Since TPE adhesive grades offer durability, electrical insulation, and chemical and water resistance, companies strive to expand footing in the adhesives sector. Arkema SA, for instance, acquired Ashland’s performance adhesive branch in February 2022 to strengthen its adhesives solutions segment.

Regional Analysis: Asia-Pacific dominates the market based on volume

In Asia-Pacific, China dominates paint and coating production, while India is experiencing robust growth due to rapid industrialization and construction activities. Besides this, thermoplastic elastomer manufacturers are expanding in ASEAN countries like Thailand. Hence, the region’s expanding position in adhesive and sealant production fuels the region’s market, spearheaded by China.

Regulations & Shortages Prompt Innovation

Due to increasingly stringent environmental regulations and sustainability goals, elastomer manufacturers are compelled to create more recyclable tire options. This has led to a noticeable shift towards sustainable TPE materials, including bio-based TPEs. Shortages in raw materials further exacerbate the need for recyclable products. Notably, China has witnessed a significant increase in recycled rubber production, capturing more than 80% of the global production landscape.

In summary, the growing demand for eco-friendly solutions, regulatory pressures, and raw material shortages have spurred the adoption of TPEs as an effective means to reduce costs associated with waste tire management. Looking ahead, the industrial commitment to resource efficiency is expected to create lucrative opportunities within the thermoplastic elastomers market.

FAQs:

Q1) How big is the thermoplastic elastomers market in terms of volume?

Based on volume, the thermoplastic elastomers market recorded 7298.81 kilotons in 2022, expected to advance with a CAGR of 2.61% during 2023-2030.

Q2) Which are the 5 key thermoplastic elastomers?

Five key TPEs are polystyrene, polyamide, polyolefin, polyurethane, and elastomeric alloy.

#ThermoplasticElastomersMarket#ThermoplasticElastomers#Thermoplastic#tritonmarketresearch#marketresearchreports

0 notes

Text

Regional Outlook of the Cryogenic Tanks Market: Trends and Forecast

The cryogenic tanks market has been growing significantly over the past decade owing to the increasing demand and consumption of liquefied natural gas globally. Cryogenic tanks are specifically designed storage vessels used for storing liquefied gases at temperatures lower than -150 degree Celsius. The main liquefied gases stored using cryogenic tanks include liquefied natural gas (LNG), oxygen, nitrogen, argon, and liquefied hydrogen. Cryogenic tanks provide an efficient, safe and economical solution for storage and transport of liquefied gases over long distances via ships, railcars or trucks. The burgeoning LNG industry has been the primary growth driver for cryogenic tanks considering its increasing usage in power generation, industrial processes and transportation fuel.

The Global Cryogenic Tanks Market is estimated to be valued at US$ 6.51 Bn in 2024 and is expected to exhibit a CAGR of 5.0% over the forecast period 2023 to 2030.

Key Takeaways

Key players operating in the cryogenic tanks are ArcelorMittal, China Baowu Group, Nippon Steel Corporation, POSCO, Shagang Group, Ansteel Group, Glencore, Sumitomo Metal Mining Company, Linde, INOX India Pvt., Cryofab, FIBA Technologies, Air Products and Chemicals, Inc., M1 Engineering, Chart Industries, Wessington Cryogenics, Isisan, Lapesa, Auguste Cryogenics, and Hoover Ferguson Group, Inc.. Key players are focusing on capacity expansions and investments in research and development to develop improved and more durable cryogenic tank materials.

The growing demand for LNG as a cleaner alternative fuel for power generation and transportation has been driving increased consumption of cryogenic tanks globally. Countries like China and India have emerged as high growth markets for LNG and cryogenic storage infrastructure.

Technological advancements in cryogenic tank materials including 9% nickel steels and composite materials have enhanced durability and reduced maintenance costs of cryogenic storage and transportation systems. Development of vacuum insulated and modular cryogenic tank designs have also optimized storage capacity.

Market Trends

Thinner tank walls: Tank manufacturing companies are developing tank designs with thinner and lighter tank walls through advanced material engineering while maintaining required strength and integrity at cryogenic temperatures.

Modular construction: Modular construction techniques allow cryogenic tanks to be assembled on-site with pre-fabricated sections reducing construction timelines significantly. This helps meet the rapidly growing demand.

Market Opportunities

Reusable cryogenic tanks: There is scope for reusable cryogenic tank designs that can be returned, refilled and redeployed to improve cost efficiencies over the life cycle.

On-site storage: With growing decentralized energy needs, there exists opportunities for scaled-down on-site stationary cryogenic storage for industrial applications.

Impact of COVID-19 on Cryogenic Tanks Market

The outbreak of the COVID-19 pandemic had a significant impact on the growth of the cryogenic tanks market initially. During the lockdown period of 2020-2021, production facilities and manufacturing plants were temporarily shut down due to strict social distancing norms. This led to disruptions in the supply chain and a drop in demand across end-use industries such as oil & gas, metallurgy, power generation and others which use cryogenic tanks. However, with vaccination drives and easing of lockdowns from mid-2021, production and supply chain activities have resumed while following necessary safety protocols. The demand from power generation and healthcare sectors increased significantly driven by the need for medical oxygen which boosting the cryogenic tanks market again. Going forward, the pandemic has highlighted the need for reliable and flexible gas supply infrastructure which is expected to drive investments towards building new liquefaction plants and expanding gas transportation facilities using cryogenic tanks.

Geographical Regions with High Concentration in Cryogenic Tanks Market

Asia Pacific region dominates the global cryogenic tanks market in terms of value owing to high demand from China, India and other developing countries. This is attributed to rapid industrialization, growing demand for LNG and medical oxygen along with government initiatives towards gas-based economy and clean energy. North America is the second largest market for cryogenic tanks driven by increasing production of shale gas and its transportation/storage requirements in the region. Europe also holds significant share in the market supported by ongoing energy transition initiatives towards replacing coal/oil with cleaner natural gas and hydrogen.

Fastest Growing Region for Cryogenic Tanks Market

Asia Pacific region is projected to be the fastest growing market for cryogenic tanks during the forecast period of 2023-2030. This is because majority of planned investments and capacity addition of gas liquefaction, regasification and gas-based power plants are concentrated in emerging economies of China, India and ASEAN countries. Additionally, rising LNG trade activities between Asia and other regions increases the requirements for tanker transportation of gas using cryogenic technology. Government policies supporting gas utilization over other fuels as well as expanding industrialization will further augment the demand for cryogenic tanks from various end-use industries in Asia Pacific.

0 notes

Text

Spherical Alumina Filler, Global Market Size Forecast, Top 15 Players Rank and Market Share

Spherical Alumina Filler Market Summary

Thermal conductive powders currently used for filling composite thermally conductive materials can be divided into multiple categories. According to the chemical composition of the materials, they can be divided into three categories, including metals, carbon powders and inorganic non-metallic powders.

Oxide metal powder has good advantages in the field of preparing high thermal conductivity composite materials due to its good thermal conductivity and insulation properties.

According to the new market research report "Global Spherical Alumina Filler Market Report 2023-2029", published by QYResearch, the global Spherical Alumina Filler market size is projected to reach USD 685 million by 2029, at a CAGR of 9.5% during the forecast period.

Figure. Global Spherical Alumina Filler Market Size (US$ Million), 2018-2029

Based on or includes research from QYResearch: Global Spherical Alumina Filler Market Report 2023-2029.

Market Drivers:

1. National policy support: Policy support is always the core driver of industry development.

2. As the functions of electronic products such as 5G communication equipment and high-end smartphones become increasingly complex and miniaturized, thermal interface materials solve the heat dissipation problem of core components of electronic products, thereby driving the demand for spherical alumina, the continued growth of thermally conductive fillers, and the requirements for media purity and radioactivity are constantly increasing.

3. As the functions of electronic products such as 5G communication equipment and high-end smartphones become increasingly complex and miniaturized, thermal interface materials solve the heat dissipation problem of core components of electronic products, thus driving the demand for spherical alumina. Thermal interface materials continue to grow, with increasing requirements for conductive fillers and media purity and radioactivity.

Restraint:

1. Spherical alumina powder products have high technical barriers, and the biggest technical difficulty lies in the research and development of spheroidization process and production equipment. At present, there is no standard equipment on the market. If new enterprises want to build new production capacity and produce spherical alumina with outstanding quality and stability, they need to overcome related technical bottlenecks.

2. Intensified competition in the industry: The rapid development of the new energy vehicle market in recent years has attracted a large amount of capital to enter the new energy industry, which eventually led to an increase in the number of enterprises in the heat conduction ball aluminum industry. Traditional powder production companies are also diversifying and are gradually adding or expanding spherical alumina production capacity. Companies such as Denka and Anhui Estone Materials have many new production capacity projects and rapid growth in production capacity, which has increased product supply and intensified product price competition.

Opportunity:

Industry development opportunities are mainly reflected in three aspects: policy support, higher thermal conductivity and filling technology, and downstream demand promotion.

Figure. Spherical Alumina Filler, Global Market Size, The Top Five Players Hold 58% of Overall Market

Based on or includes research from QYResearch: Global Spherical Alumina Filler Market Report 2023-2029.

The global key manufacturers of Spherical Alumina Filler include Denka, Admatechs, Bestry Technology, Resonac, Nippon Steel Chemical & Material, Sibelco, China Mineral Processing, Novoray, Daehan Ceramics, Anhui Estone Materials Technology, Triumph Technology, Dongkuk R&S, Lanling Yixin Mining Technology, Suzhou Ginet New Material, Henan Tianma New Material, etc.

In 2022, the global top five Spherical Alumina Filler players account for 58% of market share in terms of revenue. Above figure shows the key players ranked by revenue in Spherical Alumina Filler.

Figure. Spherical Alumina Filler, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Spherical Alumina Filler Market Report 2023-2029.

In terms of product type, 30-80μm is the largest segment, hold a share of 46%.

Figure. Spherical Alumina Filler, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Spherical Alumina Filler Market Report 2023-2029.

In terms of product application, Thermal Interface Materials is the largest application, hold a share of 49%.

When used as thermal interface materials, spherical alumina fillers can be used as heat sink fillers, heat sink (MC board) fillers, thermal paste, phase change sheets, semiconductor sealing resin, silicon-based heat dissipation glue and other compounds. The main suppliers of Thermal Interface Materials include Dow, Panasonic, Parker Hannifin, Shin-Etsu Chemical, Henkel, Fujipoly, DuPont, etc.

At present, the terminal applications driving the demand for spherical alumina are mainly photovoltaic cells, new energy vehicle power batteries, 5G communications/high-end electronic products, and chip packaging. Many companies in the industry have deployed spherical alumina for chip packaging, such as Resonac, Novoray, and Anhui Estone. At the same time, the future development trend of spherical alumina is mainly high purity and low radioactivity.

Figure. Spherical Alumina Filler, Global Market Size, Split by Region (Production)

Based on or includes research from QYResearch: Global Spherical Alumina Filler Market Report 2023-2029.

In terms of production value, Japan is the main producer from 2018 to 2021, with an average share of 50%.

After 2021, with the expansion of production lines of companies such as China's Bestry Technology and Novoray, they will gradually occupy the market share of Japan and South Korea.

By 2023, China's output value share will exceed 45%. In the next few years, China will occupy the main market share.

Figure. Spherical Alumina Filler, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global Spherical Alumina Filler Market Report 2023-2029.

About The Authors

Jiashi Dong

Lead Author

Email: [email protected]

Tel: +86-15278314535

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

Overhead Line Product Market to Witness High Growth

Overhead line products are critical components used in electric power transmission and distribution. These include insulators, bimetallic connectors, surge arresters, fittings and hardware that are installed on utility poles and transmission towers. Utilities rely on overhead line products to safely and efficiently deliver power from bulk generation points to residential and commercial end users. With rapid urbanization and the increasing electrification of developing economies, the demand for electricity continues to grow substantially each year, necessitating investments in expansion and modernization of aging grid networks.

The global overhead line product market is estimated to be valued at US$ 19.78 Bn in 2023 and is expected to exhibit a CAGR of 4.0% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Dynamics

Rising investments in transmission and distribution infrastructure is a major driver propelling the growth of the overhead line product market. According to the International Energy Agency, annual global spending on electricity networks will need to increase to nearly US$ 330 billion by 2030, a 40% rise from 2020 levels, to support the electrification of transport and buildings sectors as well as connectivity and reliability needs. Additionally, replacement of aging assets such as porcelain and polymeric insulators with more durable and efficient composite insulators is boosting demand. However, the deployment of underground power transmission systems in urban areas may limit market expansion to some extent over the forecast period.

SWOT Analysis

Strength: Overhead Line Product Market has strong growth prospects over the forecast period. Standardized and simplified installation process allows for easy maintenance and upgrade of existing infrastructure. Efficient transmission of bulk power over long distances improves reliability of power supply.

Weakness: High initial investment required for setting up transmission lines. Geographical and environmental challenges like obtaining rights of way and addressing public opposition increases project delays and costs. Vulnerable to damage from severe weather events like high winds, ice storms resulting in power outages.

Opportunity: Growing investments in modernizing aging power grids in developed markets. Rapid electrification and expanding transmission networks in developing regions in Asia Pacific and Latin America provide new opportunities. Adoption of advanced materials, digital technologies and solutions helps improve power distribution efficiencies.

Threats: Strict government regulations around land use and environmental protection increases compliance costs. Delay in approval processes can hamper timely execution of projects. Ever evolving power consumption patterns poses new technical challenges. Shift towards decentralized renewable energy sources reduces dependency on conventional transmission grids.

Key Takeaways

The Global Overhead Line Product Market Size is expected to witness high growth over the forecast period supported by ongoing grid infrastructure upgrades worldwide. The global Overhead Line Product Market is estimated to be valued at US$ 19.78 billion in 2023 and is expected to exhibit a CAGR of 4.0% over the forecast period 2023 to 2030.

North America currently dominates the market owing to large investments in modernizing the aging power infrastructure in the United States and Canada. However, the Asia Pacific region is expected grow at the fastest pace with China, India, Japan, South Korea emerging as major markets on account rapid industrialization and infrastructure development. The Asia Pacific region dominates the global Overhead Line Product market with over 35% market share in 2023 led by China, India, Japan and South Korea. The rapid economic growth and rising investments in modernizing national grids in developing countries is expected to drive further infrastructure additions. China alone contributes for over 25% of the regional market demand.

Key players operating in the Overhead Line Product Market include Murata Manufacturing Co. Ltd, Vectron International Inc., Siward Crystal Technology Co. Ltd, Kyocera Corporation, Nihon Dempa Kogyo (NDK) Co. Ltd, Seiko Epson Corp., Daishinku Corp., Hosonic Electronic Co. Ltd, TXC Corporation, Rakon Ltd and SiTime Corporation. These companies hold a significant share of the market and are focused on developing advanced products and solutions through investments in research and development.For More Insights, Read:https://www.newsstatix.com/overhead-line-product-market-trends-growth-and-regional-outlook-2023-2030/

0 notes

Text

Global Transformer Oil Market Size, Market Segmentation and Competitors Analysis 2019 -2030

Global Transformer Oil Market was valued at USD 2,545 million in 2019 which is expected to reach USD 3,530.6 million by 2030 at CAGR 4.8%.

Transformer oil is referred as insulation oil which is steady at high temperatures and a superlative insulator for electricity. This is majorly derivatives of mineral oils, but substitute composition with better chemical and physical properties are growing in demand.

Market Drivers

Increase in focus on rural electrification in emerging countries such as china and India is expected to drive the global transformer oil market. Furthermore, increase in urbanization, drastic industrialization, as well as progressive access to modern electricity grids in rural areas in APAC region which is expected to positively influence the market growth over the forecast period.

Also, increase in consumer requirements and exponential development in distribution networks have also support the market growth during this forecast period. Moreover, rise in demand for electricity across the world has fuel the deployment of new transformers which in turn will propel the market growth.

Market Restraints

A fluctuation in crude oil prices is the major challenging factor which is expected to hinder the global transformer oil market growth. Also, rise in adoption of alternate transformer technologies will limit the global transformer oil market growth.

𝐆𝐞𝐭 𝐭𝐡𝐞 𝐢𝐧𝐬𝐢𝐝𝐞 𝐬𝐜𝐨𝐨𝐩 𝐰𝐢𝐭𝐡 𝐒𝐚𝐦𝐩𝐥𝐞 𝐫𝐞𝐩𝐨𝐫𝐭 : https://qualiketresearch.com/request-sample/Transformer-Oil-Market/request-sample

Market Segmentation

Global Transformer Oil Market is segmented into product type Mineral Based Oil (Naphthenic Base Oil, and Paraffinic Oil), Silicone Based Oil, and Bio-Based Oil. Further, market is segmented into application such as Small-Scale Transformers, Large-Scale Transformers, and Utility Transformer Oil.

Also, Global Transformer Oil Market is fragmented into five regions such as North America, Latin America, Europe, Asia Pacific, and Middle East & Africa.

Market Key Players

BASF SE

Emirates Lube Oil Company

Royal Dutch Shell

Hydrodec Group Plc

Engen Petroleum Ltd

Hyrax Oil Sdn Bhd

Calumet Specialty Products

Cargill Inc

Sinopec Corporation

PetroChina Company Ltd

Valvoline

Ergon Inc

Nynas AB

Dairen Chemical Corporation.

𝐔𝐧𝐥𝐨𝐜𝐤 𝐭𝐡𝐞 𝐜𝐨𝐦𝐩𝐥𝐞𝐭𝐞 𝐫𝐞𝐩𝐨𝐫𝐭 𝐛𝐲 𝐜𝐥𝐢𝐜𝐤𝐢𝐧𝐠 𝐟𝐨𝐫 𝐌𝐨𝐫𝐞 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐡𝐞𝐫𝐞 : : https://qualiketresearch.com/reports-details/Transformer-Oil-Market

About Us:

QualiKet Research is a leading Market Research and Competitive Intelligence partner helping leaders across the world to develop robust strategy and stay ahead for evolution by providing actionable insights about ever changing market scenario, competition and customers.

QualiKet Research is dedicated to enhancing the ability of faster decision making by providing timely and scalable intelligence.

QualiKet Research strive hard to simplify strategic decisions enabling you to make right choice. We use different intelligence tools to come up with evidence that showcases the threats and opportunities which helps our clients outperform their competition. Our experts provide deep insights which is not available publicly that enables you to take bold steps.

Contact Us:

6060 N Central Expy #500 TX 75204, U.S.A

+1 214 660 5449

1201, City Avenue, Shankar Kalat Nagar,

Wakad, Pune 411057, Maharashtra, India

+91 9284752585

Sharjah Media City , Al Messaned, Sharjah, UAE.

+971 56 846 4312

0 notes

Text

APAC Is Dominating the Fiberglass Market

The global fiberglass market is expected to reach an estimated USD 30.1 billion in 2023 and grow by 7.3% during the period between 2024 and 2030, reaching a value of USD 49.1 billion over that period. This is mainly due to the exclusive features of fiberglass, like high tensile strength, high resistance to chemicals, relatively low density, and non-flammable nature. Therefore, it has applications in many industries, like aerospace, construction & infrastructure, automobile, wind energy, septic tanks, boats, and water tanks.

During the projection period, the glass wool category holds the largest share of the fiberglass industry, and the category is also projected to advance at a CAGR of 7.5%. This is mainly because of the growing utilization of glass wool in the construction sector due to its good tensile strength, fire resistance, and insulative properties. It is mainly utilized for roof and ceiling insulation in halls and other huge areas as it blocks the gain or loss of heat. This is also why HVAC ducting systems are a vital application for this material.

In 2023, composites claim the majority share by application, primarily attributed to the numerous advantages of fiberglass composites when compared to conventional materials like wood and steel. These composites offer cost-effectiveness, resistance to corrosion, strong structural capabilities, and minimal maintenance needs. Consequently, the growing adoption of fiberglass composites in industries such as automotive, aerospace, and construction is anticipated to propel market growth throughout the forecast period.

Fiberglass finds extensive application in residential construction, particularly in insulation, owing to its durability and fire-resistant properties. Consequently, as governments strive to provide housing for all, the market is poised to encounter numerous opportunities, especially in densely populated nations such as India and China.

#Fiberglass Market#Fiberglass Market Size#Fiberglass Market Share#Fiberglass Market Growth#Fiberglass Market Demand#Fiberglass Market trends

0 notes

Text

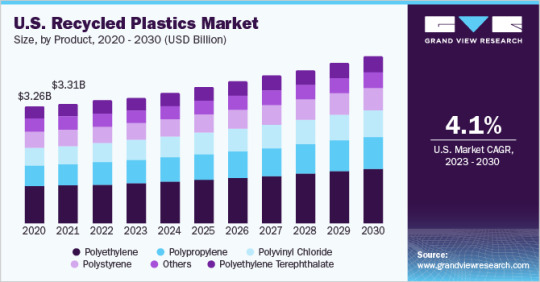

Recycled Plastics Market Is Expected To Grow Swiftly By 2030

The global recycled plastics market size was valued at USD 47.60 billion in 2022 and is expected to exhibit grow at a compound annual growth rate (CAGR) of 4.9% from 2023 to 2030. Increasing environmental concerns, rapid urbanization & industrialization, and the rising need to reduce the carbon footprint in the manufacturing of virgin plastic resin are expected to drive the demand for recycled plastics over the forecast period. The demand for recycled plastics is expected to increase mainly in the packaging application, which includes packaging of processed food & beverages, medical, electronics, and various other products, owing to the growing number of COVID-19 positive cases.

The demand for medical & healthcare products has increased owing to the safety and hygiene required to tackle the pandemic situation. Amid the global COVID-19 pandemic, the demand for electrical & electronic products, such as laptops and mobiles, has increased as companies are following the work-from-home model and educational institutions have shifted from classroom learning to online classes. Thus, the growth in the demand for electrical & electronic products is expected to drive the market over the forecast period. The regional market of Asia Pacific is anticipated to register the fastest growth rate during the forecast period.

This growth can be attributed to various factors, such as the presence of supportive government initiatives like Make in India, Atmanirbhar Bharat (self-dependent India), rising number of manufacturers operating in the electrical & electronics, automotive, and textile industries, and increasing R&D investments by private as well as public organizations for the development of new applications for recycled plastics. In addition, various electronic products and automotive components manufacturing companies have started looking toward India for establishing their manufacturing facilities post-COVID-19 pandemic. This will also provide tremendous growth opportunities to the regional market in the years to come.

Request a free sample copy or view the report summary: Recycled Plastic Market Report

Recycled Plastics Market Report Highlights

The building & construction application segment is expected to witness the fastest CAGR over the forecast period, in terms of revenue

The segment growth is attributed to the rising demand for recycled plastics in composite lumber, roofing tiles, insulation, rocks, and fences

The electrical & electronics application segment accounted for the maximum revenue share in 2021

This is attributed to the high demand for lightweight, durable electronics and electrically well-insulated products for reduced heat loss and improved performance of the electronic components and products

Asia Pacific accounted for the largest revenue share in 2021. The market in China recycled is estimated to witness significant growth to reach a net worth of USD 17.3 billion by 2030

Recycled Plastics Market Segmentation

Grand View Research has segmented the recycled plastics market based on product, application, and region:

Recycled Plastics Product Outlook (Volume, Kilotons; Revenue, USD Million, 2019 - 2030)

Polyethylene

Polyethylene Terephthalate

Polypropylene

Polyvinyl Chloride

Polystyrene

Others

Recycled Plastics Source Outlook (Volume, Kilotons; Revenue, USD Million, 2019 - 2030)

Plastic Bottles

Plastic Films

Polymer Foam

Others

Recycled Plastics Application Outlook (Volume, Kilotons; Revenue, USD Million, 2019 - 2030)

Building & Construction

Packaging

Electrical & Electronics

Textiles

Automotive

Others

Recycled Plastics Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2019 - 2030)

North America

U.S.

Canada

Mexico

Europe

Germany

U.K.

France

Italy

Asia Pacific

China

India

Japan

South East Asia

Malaysia

Indonesia

Thailand

Central & South America

Brazil

Middle East & Africa

Saudi Arabia

List of Key Players of Recycled Plastics Market

REMONDIS SE & Co. KG

Biffa

Stericycle

Republic Services, Inc.

WM Intellectual Property Holdings, L.L.C.

Veolia

Shell International B.V.

Waste Connections

CLEAN HARBORS, INC.

Covetsro AG

0 notes

Text

Phenolic Resin Market: A Multifaceted Gem for Chemical Industry Professionals

The global phenolic resin market is a shining example of resilience and adaptability in the chemical industry. Valued at USD 11.7 billion in 2021, it's projected to reach a cool USD 14.4 billion by 2026, driven by a steady 4.3% CAGR. This growth isn't just happenstance; it's fueled by a potent cocktail of factors that make phenolic resins a true gem for chemical professionals.

Unveiling the Allure of Phenolic Resins:

Phenolic resins aren't your average Joe. They boast a unique blend of properties that make them the envy of the chemical world:

Heat Resistant Hero: Think scorching temperatures. Phenolic resins shrug them off with ease, making them ideal for automotive parts and electrical components that need to withstand the heat.

Molding Master: Need a resin that can be shaped into intricate forms? Phenolic resins are your go-to. They readily conform to your desired design, making them perfect for construction materials and insulation panels.

Strength in Numbers: Don't underestimate the brawn of phenolic resins. They possess impressive mechanical strength, making them the backbone of durable adhesives, wood panels, and foundry binders.

Smoke Signals of Safety: When things get hot, phenolic resins keep their cool. They emit minimal smoke, ensuring safety in applications like aircraft interiors and fire-resistant materials.

Polymer Playmate: Phenolic resins are team players. They blend seamlessly with other polymers, expanding their application possibilities and boosting their versatility.

Riding the Wave of Growth:

The allure of phenolic resins extends beyond their intrinsic properties. They're riding a wave of growth fueled by several megatrends:

Automotive Boom: The quest for fuel-efficient and lightweight vehicles is music to the ears of phenolic resin manufacturers. These resins enable lighter cars through their use in adhesives, reducing weight and emissions.

APAC's Ascendancy: The Asia-Pacific region, with its booming construction and automotive sectors, is becoming a hotbed for phenolic resins. China, India, and Indonesia are leading the charge, creating a vast and dynamic market.

Seizing the Opportunity:

Despite these headwinds, the future of phenolic resins is bright. Here's how chemical professionals can capitalize on this potential:

Innovation Incubator: Develop novel phenolic resin formulations that address specific industry needs and comply with environmental regulations. Think flame-retardant resins for construction or bio-based resins for sustainable solutions.