#Data Center Security Market Analysis in Developed Countries

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr is used by 21% of adults online aged 18-29 years.

Text

💻 Data Center Interconnect Market Size, Share & Growth Analysis 2034: Powering the Cloud Age

Data Center Interconnect (DCI) Market is gaining remarkable momentum as businesses around the globe strive for faster, secure, and more scalable data transfer capabilities. DCI encompasses the technologies used to connect two or more data centers to ensure seamless communication and data exchange. With growing adoption of cloud computing, digital services, and edge computing, the need for robust, low-latency, high-bandwidth connectivity has never been greater. The market is built around key technologies such as optical networking, Ethernet, and software-defined networking (SDN), all of which help to optimize redundancy, disaster recovery, and workload mobility. In 2024, the market is valued at approximately $9.5 billion and is projected to reach $22.3 billion by 2033, reflecting a CAGR of 8.9%.

Market Dynamics

The driving forces behind the DCI market’s growth include the rising volume of data generated by IoT devices, increased reliance on cloud services, and the emergence of new applications that demand real-time data processing. Wavelength Division Multiplexing (WDM) remains the most dominant technology segment, accounting for nearly 45% of the market due to its high bandwidth and transmission efficiency. Following closely are Ethernet and packet-switching technologies, which are essential for flexible networking and rapid scalability.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS20272

Simultaneously, sustainability is becoming a significant theme. Organizations are striving to reduce their carbon footprint by adopting energy-efficient data center operations. However, the market also faces certain restraints such as high capital expenditure, complex regulatory compliance, and a lack of skilled professionals. Security remains a top concern, with increasing pressure to prevent data breaches and comply with evolving global standards.

Key Players Analysis

The competitive landscape of the Data Center Interconnect Market is defined by a mix of tech giants and emerging innovators. Key players like Ciena Corporation, Cisco Systems, Huawei Technologies, Juniper Networks, and Nokia Networks are continuously evolving their offerings to meet the demands of cloud-native businesses. These companies are investing heavily in R&D to bring forth solutions that offer higher speeds, better security, and more flexibility.

Emerging players such as Nex Gen Networks, Quantum Interconnect, and Inter Connect Innovations are gaining traction by offering cost-effective, niche solutions tailored to regional needs. These newer entrants are also experimenting with AI and machine learning to improve network optimization and performance.

Regional Analysis

North America leads the global DCI market, fueled by robust IT infrastructure and the presence of major cloud providers and technology firms. The U.S., in particular, is at the forefront of adopting high-capacity interconnect solutions.

Europe follows as a strong market, bolstered by stringent data privacy regulations and initiatives toward sustainable data center infrastructure. Countries like Germany and the U.K. are making significant investments in next-gen connectivity.

Asia-Pacific is witnessing rapid growth, with nations like China and India investing heavily in digital transformation and data infrastructure. Increasing internet penetration and mobile usage are further fueling demand in this region.

Latin America and the Middle East & Africa are emerging as potential growth hubs. Brazil, Mexico, the UAE, and South Africa are taking proactive steps toward modernizing their data centers, making them attractive markets for DCI solutions.

Recent News & Developments

Recent developments in the DCI market highlight a clear shift toward intelligent, software-defined architectures. Key companies like Ciena and Cisco are leading innovations in SDN and AI-integrated interconnect platforms. Solutions are being designed not only for speed but also to accommodate green goals — offering better power efficiency and a smaller carbon footprint.

Pricing for interconnect solutions varies widely, ranging from $10,000 to $50,000, influenced by bandwidth requirements and technology sophistication. The ongoing focus on reducing operational costs and energy usage, combined with the growing use of automation and virtualization, is shaping the future of data center networking.

Browse Full Report : https://www.globalinsightservices.com/reports/data-center-interconnect-market/

Scope of the Report

This report provides a comprehensive outlook on the Data Center Interconnect Market, offering insights into market size, segmentation, growth trends, and competitive dynamics. It analyzes market drivers, restraints, and opportunities while exploring in-depth regional performance and key technological shifts. Covering both historical data (2018–2023) and forecasts up to 2034, the report evaluates major industry participants, emerging players, and their strategies, including mergers, partnerships, and product innovations.

Our extensive coverage also includes PESTLE and SWOT analysis, demand-supply dynamics, import-export evaluations, and regulatory reviews. It equips stakeholders with actionable insights to make informed decisions and capture new opportunities in the evolving global data ecosystem.

#dataecosystem #datacenterinterconnect #cloudconnectivity #opticalnetworking #digitalinfrastructure #sdn #aiinnetworking #iotconnectivity #greendatacenters #edgecomputing

Discover Additional Market Insights from Global Insight Services:

High Speed Cable Market : https://www.globalinsightservices.com/reports/high-speed-cable-market/

Advanced Semiconductor Packaging Market : https://www.globalinsightservices.com/reports/advanced-semiconductor-packaging-market/

Agricultural Lighting Market : https://www.globalinsightservices.com/reports/agricultural-lighting-market/

Air Quality Monitoring System Market : https://www.globalinsightservices.com/reports/air-quality-monitoring-system-market/

High-Speed Camera Market : https://www.globalinsightservices.com/reports/high-speed-camera-market-2/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

BACXN Crypto Landscape Upgrade: From Ten Million Users to Global Value Co-Creation

As the crypto market matures, regulatory frameworks become clearer, and user demands grow increasingly diverse, BACXN has chosen to take a highly symbolic step in 2025: moving from merely connecting global users to engaging in open industry dialogue and genuine value co-creation. This year, the platform not only surpassed key growth milestones but also reinforced its position as “trusted digital asset infrastructure” through a series of structural system upgrades and global events.

A landmark event in this process was the first-ever global “BACXN Ecosystem Summit” of BACXN. Officially held at the beginning of the year, the summit brought together government representatives, technology leaders, crypto developers, institutional investors, and core platform users from over 50 countries and regions. Discussions centered on topics such as “New Frontiers of Digital Assets,” “Institutional Evolution of Crypto Finance,” “On-Chain Identity and the Future of Data Sovereignty,” and “Web3 Participation Mechanisms and Platform Responsibility.” As the most high-profile, widely attended, and influential ecosystem event since the platform inception, the summit was not only a convergence of experience and perspectives but also a clear signal from BACXN to the industry: the platform is building an open, transparent, and co-created global value system through deeper engagement.

One of the summit highlights was the public unveiling by BACXN of its global node service network achievements. The platform has established local compliance teams and operational centers in multiple strategic markets, streamlining key processes such as user verification, fiat channels, asset compliance, and customer service. With a bilingual operations system, AI-powered customer support modules, and legal compliance support, BACXN has improved service response efficiency while significantly enhancing the transparency and scalability of its compliant operations.

Coinciding with the summit, the BACXN global user base also surpassed a major milestone—registered users on the platform officially exceeded 10 million, with the service network now covering over 150 countries and regions worldwide. This achievement is no accident. Looking back over the past three years, BACXN has continuously iterated on three core pillars—efficiency, security, and trust—ranging from foundational technology optimization and matching engine performance improvements to enhanced account system security and the continuous expansion of its product suite (including spot, derivatives, staking, NFT marketplace, and RWA sectors).

This growth not only reflects the rapid accumulation by BACXN of user trust globally but also marks the platform refined response to diverse needs, setting a new industry benchmark. For example, in the Middle East, BACXN achieved rapid market penetration through local compliance support and an Arabic-language operations team; in Southeast Asia, the platform integrated with multiple payment channels and introduced local currency deposit and commission reduction policies for markets such as the Philippines and Indonesia; in Europe, BACXN proactively prepared for the MiCA framework, aligning asset on-chain processes and trading data standards to lay the groundwork for the upcoming pan-European compliance era.

It is also worth noting the ongoing breakthroughs by BACXN in user experience optimization. The newly launched “Smart Trading Space” module integrates AI market analysis, strategy simulation, and risk scoring, lowering the learning curve for Web3 newcomers. Meanwhile, the “Socialized Asset Path Recommendation” mechanism leverages on-chain user behavior modeling to provide active traders with more personalized asset allocation suggestions. All of these initiatives reflect its deep commitment to its mission of “lowering the trust barrier with technology.”

In the summit closing keynote, the co-founder of BACXN stated: “We believe that a truly valuable platform does more than provide trading services—it should participate in building new order among trust, institutions, and user relationships. This is our responsibility now, and the starting point for our journey ahead.”

Looking forward, BACXN will continue to center its global strategy on user value, deepening its focus on platform security, regulatory compliance, ecosystem diversity, and technological foresight, driving digital asset trading toward a more robust, trustworthy, and inclusive era.

0 notes

Text

Australia Industrial IoT Market Size, Share, Trends and Forecast by 2033

The latest report by IMARC Group, titled "Australia Industrial IoT Market Size, Share, Trends and Forecast by Component, End-User, and Region, 2025–2033," offers a comprehensive analysis of the Australia Industrial IoT market growth. The report includes competitor and regional analysis, along with a breakdown of segments within the industry. The Australia Industrial IoT market size reached USD 8.1 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 27.0 Billion by 2033, exhibiting a growth rate (CAGR) of 12.8% during 2025–2033.

Base Year: 2024

Forecast Years: 2025–2033

Historical Years: 2019–2024

Market Size in 2024: USD 8.1 Billion

Market Forecast in 2033: USD 27.0 Billion

Market Growth Rate (2025–2033): 12.8% Request for Sample Report: https://www.imarcgroup.com/australia-industrial-iot-market/requestsample

Australia Industrial IoT Market Overview

is encountering noteworthy development, driven by a few key components. The government's activities, such as the Advanced Economy Methodology 2030 and the Advanced Fabricating Procedure, are cultivating a conducive environment for IIoT appropriation. These arrangements point to improve efficiency, worldwide competitiveness, and work creation through innovation appropriation. Also, the arrangement of 5G systems and headways in edge computing are giving the vital foundation for IIoT applications over different businesses, counting mining, farming, and transportation.

Australia Industrial IoT Market Trends and Drivers

The Australia Industrial IoT market is influenced by several key trends and drivers:

Government Activities and Advanced Change Arrangements: Australia's state and government governments are playing a vital part in progressing advanced advancement in mechanical segments. Activities just like the Computerized Economy Technique 2030 and venture motivations through the Advanced Fabricating Methodology reflect a country-wide center on keen innovations. Sending of 5G Systems and Edge Computing: The extension of 5G systems and headways in edge computing are giving the essential framework for IIoT applications, empowering real-time information handling and improved network. Appropriation in Key Businesses: Businesses such as mining, horticulture, and transportation are progressively embracing IIoT arrangements to upgrade operational productivity, security, and efficiency. Center on Maintainability and Net Zero Objectives: Programs centering on progressed fabricating, cleverly coordinations, and green vitality reflect the government's objective of creating a digital-first mechanical environment, adjusting with maintainability and net-zero goals.

Australia Industrial IoT Market Segmentation

By Component:

Hardware

Software

Services

By End-User Industry:

Mining

Agriculture

Transportation

Manufacturing

Energy

Others

By Region:

New South Wales

Victoria

Queensland

South Australia

Western Australia

Tasmania

Northern Territory

Australian Capital Territory

Australia Industrial IoT Market News

2024: The Australian government launched the 'Future Made in Australia' initiative, a $22.7 billion package aimed at maximizing the economic and industrial advantages of the transition to net zero, promoting the adoption of IIoT technologies across various sectors.

2024: Major telecommunications companies in Australia began expanding 5G networks, enhancing connectivity and enabling real-time data processing for IIoT applications.

2024: Leading Australian mining companies implemented IIoT solutions to monitor equipment health, optimize operations, and improve safety standards.

Key Highlights of the Report

Market Performance (2019–2024)

Market Outlook (2025–2033)

COVID-19 Impact on the Market

Porter’s Five Forces Analysis

Strategic Recommendations

Historical, Current, and Future Market Trends

Market Drivers and Success Factors

SWOT Analysis

Structure of the Market

Value Chain Analysis

Comprehensive Competitive Landscape Mapping

Ask Analyst for Customized Report: https://www.imarcgroup.com/request?type=report&id=32477&flag=E

Contact Us

Address: 134 N 4th St. Brooklyn, NY 11249, USA Email: [email protected] Tel No: (D) +91 120 433 0800 United States: +1-631-791-1145

About Us

IMARC Group is a leading market research company that provides management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses. Our solutions include comprehensive market intelligence, custom consulting, and actionable insights to help organizations make informed decisions and achieve sustainable growth.

1 note

·

View note

Text

Why Outsourcing in India Remains a Competitive Advantage for Global Businesses

In today’s fast-paced global economy, agility and efficiency are the keys to staying ahead. Companies worldwide are constantly seeking ways to scale operations, cut costs, and focus on core competencies. One strategy that has stood the test of time is outsourcing in India. Far from being a cost-cutting trend of the past, it continues to be a strategic tool that fuels innovation, growth, and global competitiveness.

But why does outsourcing in India still make sense in 2025, when technology, automation, and AI are reshaping business models everywhere?

Let’s explore the reasons.

India’s Talent Pool: Deep, Diverse, and Digitally Skilled

India’s biggest advantage lies in its people. With millions of highly educated, English-speaking professionals entering the workforce each year, the country boasts one of the largest and most dynamic talent pools in the world. Whether it's IT services, customer support, financial analysis, or creative design, companies can tap into skilled professionals who deliver both speed and quality.

Moreover, the Indian workforce has quickly adapted to digital transformation. With the rise of remote work and cloud-based collaboration tools, outsourcing in India has become even more seamless, enabling businesses to operate like local teams without geographic limitations.

Cost-Effective Without Compromising Quality

Let’s face it. Budget efficiency matters. And this is where India excels. Outsourcing in India allows businesses to reduce operational costs by up to 60 percent without sacrificing service quality. This cost advantage does not come at the expense of innovation. On the contrary, Indian service providers often invest in cutting-edge technologies and global best practices to deliver world-class outcomes.

Companies like Fox&Angel understand this balance well. With their strategic consulting and operational expertise, they help global businesses navigate the outsourcing landscape and build high-performing offshore teams tailored to specific goals.

Time Zone Advantage for Round-the-Clock Productivity

When global teams sleep, Indian teams work. This 24/7 productivity cycle is invaluable for companies looking to speed up processes, manage global customer bases, or reduce product development timelines. From handling overnight customer support to ensuring early morning product releases, outsourcing in India enables a constant flow of progress.

Innovation and Tech-Driven Ecosystem

India is no longer just a back-office hub. Today, it is a powerhouse of innovation. Indian companies are not just executing tasks. They are contributing strategic insights, designing digital solutions, and co-creating with global partners. The government’s push for Digital India, along with startup-friendly policies, has fostered an ecosystem that encourages entrepreneurship and technological advancement.

This environment helps companies like Fox&Angel design not just outsourcing strategies but business transformation roadmaps. Their customized approach ensures that global brands stay relevant, adaptive, and competitive in an ever-evolving market.

Regulatory Stability and Global Compliance

Outsourcing is not just about who can get the job done. It is about doing it right. India offers a robust legal framework that supports data security, intellectual property rights, and compliance with international standards such as GDPR and ISO. For businesses that deal with sensitive data and customer trust, this adds a layer of confidence and reliability to outsourcing in India.

Human-Centered Approach to Global Partnerships

Modern outsourcing is about relationships, not transactions. Indian outsourcing firms, especially boutique agencies like Fox&Angel, understand that collaboration is at the heart of long-term success. They invest in understanding the brand, its culture, and its customers, creating a seamless extension of your internal team.

It is this human connection built on empathy, communication, and shared goals that transforms outsourcing from a business tactic into a true strategic advantage.

Conclusion: Outsourcing in India Is More Than a Smart Move, It Is a Strategic Evolution

As global markets evolve, one truth remains unchanged. India continues to offer unmatched advantages for companies aiming to scale smarter, innovate faster, and stay globally competitive. From talent to technology, flexibility to cost-efficiency, outsourcing in India is not a shortcut. It is a long-term strategy built for the future.

Partner with Fox&Angel to explore customized outsourcing models that drive results while preserving your brand’s integrity and vision.

Ready to future-proof your business with the right outsourcing strategy? Contact us today and let’s build something extraordinary together.

0 notes

Text

Farhan Naqvi iLearningEngines: How Semiconductors Are Reshaping Global Power

Farhan Naqvi, former CFO of iLearningEngines, has shared powerful insights on a topic reshaping global geopolitics: semiconductors. In a recently published thought piece, Naqvi — a seasoned finance and strategy executive — explores how semiconductors have become the new strategic asset, replacing oil and data as the primary levers of international influence.

This article offers a deep dive into the transformative impact of semiconductors and AI infrastructure, drawing on Farhan Naqvi’s unique experience scaling iLearningEngines, one of the fastest-growing AI platforms in the enterprise space.

Who Is Farhan Naqvi? Farhan Naqvi is widely recognized for his leadership in finance, technology strategy, and capital markets. As the former CFO of iLearningEngines, an AI-driven enterprise software company, he played a key role in scaling the business over 10x and leading its successful listing on Nasdaq.

With degrees from IIT Kanpur and Harvard Business School, Naqvi has advised on marquee IPOs and M&A deals at leading investment banks, working with companies like Uber, Square, and Alibaba.

His work at iLearningEngines positioned him at the intersection of artificial intelligence, digital infrastructure, and global economic policy — a vantage point that informs his current perspective on semiconductors.

Semiconductors: The Core of Global Power Shifts In his latest analysis, Farhan Naqvi iLearningEngines argues that semiconductors are no longer mere hardware — they are strategic assets with national and global consequences.

“The microchip has become macro-strategic. The nations that lead in semiconductor design and manufacturing will shape the digital future.”

Naqvi’s commentary is both a call to action and a framework for understanding why chips now sit at the center of power competition among nations.

Silicon Sovereignty: A New Global Imperative Naqvi discusses how countries across the globe — including the U.S., China, Japan, and the EU — are racing toward silicon sovereignty. This means developing domestic capabilities to design, produce, and secure semiconductor supply chains without relying on foreign powers.

The COVID-19 pandemic and escalating U.S.-China tech tensions have accelerated this shift. Governments now view chips as critical to national security, not just economic growth.

From iLearningEngines to AI Infrastructure: The Role of Advanced Chips Drawing from his hands-on experience building iLearningEngines’ AI capabilities, Farhan Naqvi emphasizes the need for high-performance chips in enabling modern AI systems.

“Chips aren’t just components; they’re the infrastructure of intelligence. Without chip sovereignty, there is no AI sovereignty.”

Technologies like GPUs, tensor cores, and even quantum processors are essential to power the next wave of AI models, autonomous systems, and digital defense platforms.

A Fragmenting Global Semiconductor Supply Chain According to Farhan Naqvi iLearningEngines, the traditional global chip supply chain is being dismantled in favor of regionalization and “friend-shoring.”

The U.S. is re-shoring chip manufacturing with the CHIPS Act.

China is investing in a full-stack domestic ecosystem.

Europe and Japan are safeguarding access to critical materials and manufacturing tools.

This fragmentation poses both risk and opportunity, as countries rethink how to secure long-term chip independence.

Balancing Innovation and National Security Naqvi also cautions against the potential downside of heavy regulation. Export bans, tech restrictions, and tight controls may serve national interests, but they also risk slowing innovation, raising costs, and hampering academic collaboration.

“There’s a risk that the very controls meant to protect innovation may end up harming it,” he warns.

The Chip: The Defining Resource of the 21st Century Farhan Naqvi iLearningEngines concludes that semiconductors are now the most strategic resource on Earth — more influential than oil, data, or rare earth metals.

“The world’s most strategic resource is no longer oil or data. It’s the chip — built in nanometers, but measured in geopolitical influence.”

As we enter a new era of digital competition, the nations that dominate chip design, production, and integration will control the future of artificial intelligence, defense, and global power.

Final Thoughts Farhan Naqvi’s insights reflect a deep understanding of the convergence between technology, finance, and policy. His leadership at iLearningEngines — a company at the forefront of AI deployment — gives him rare clarity on why semiconductors will shape the global order for decades to come.

For policymakers, technologists, and investors alike, Naqvi’s message is clear: chip strategy is power strategy.

#Farhan Naqvi iLearningEngines#Sayyed Farhan iLearningEngines#Sayyed iLearningEngines#Sayyed Farhan Naqvi iLearningEngines#Sayyed Farhan Naqvi

0 notes

Text

ECG Equipment And Management Systems Market Size, Share, and Competitive Landscape 2033

The global Electrocardiogram (ECG) Equipment and Management Systems Market is experiencing robust growth, driven by the rising prevalence of cardiovascular diseases (CVDs), technological advancements, and increasing demand for remote patient monitoring. This article provides an in-depth analysis of the market's current landscape, key trends, challenges, and future prospects.

🧠 Key Market Drivers

1. Rising Prevalence of Cardiovascular Diseases

CVDs remain the leading cause of mortality worldwide. The growing burden of heart-related ailments necessitates continuous monitoring, thereby boosting the demand for ECG equipment and management systems.

2. Technological Advancements

Innovations such as AI-powered portable ECG devices and cloud-based management systems have revolutionized cardiac care, making monitoring more accessible and efficient.

3. Increased Demand for Remote Monitoring

The COVID-19 pandemic accelerated the adoption of telemedicine, with ECG equipment playing a crucial role in remote patient care. This trend is expected to continue, driving market growth.

Download a Free Sample Report: - https://tinyurl.com/9js6f5st

🏥 Market Segmentation

By Product Type

Resting ECG Systems: Accounted for more than 61% of revenue share in 2024, widely used in hospitals and clinics.

Holter Monitors: Used for continuous monitoring over 24-72 hours.

Stress ECG Monitors: Employed during exercise to assess cardiac function.

Event Monitoring Systems: Capture intermittent symptoms.

ECG Management Systems: Expected to grow at the fastest rate over the forecast period, facilitating data storage and analysis.

By End-User

Hospitals and Clinics: Major adopters due to the need for continuous patient monitoring.

Ambulatory Centers: Expected to grow at a solid CAGR of 6.53% in the upcoming years.

Home Healthcare: Growing adoption due to the rise in remote patient monitoring.

🔬 Technological Trends

AI-Powered Portable ECG Devices

Companies are developing AI-powered portable ECG systems to offer healthcare providers a clinically validated solution for quick ECG diagnosis and detection. For instance, in June 2024, AliveCor Inc. launched the FDA-cleared KAI 12L AI technology and the Kardia 12L ECG System, which can identify 35 cardiac indications with a smaller lead set.

Cloud-Based ECG Management Systems

The integration of cloud-based systems allows for real-time data access and remote monitoring, enhancing patient care and facilitating telemedicine.

⚠️ Challenges

High Costs

Advanced ECG equipment and management systems can be expensive, limiting their adoption, especially in low and middle-income countries.

Data Privacy Concerns

The transmission and storage of sensitive health data raise concerns about patient privacy and data security.

Regulatory Hurdles

Navigating the complex regulatory landscape for medical devices can delay product approvals and market entry.

🔮 Future Outlook

The ECG equipment and management systems market is poised for continued growth, driven by technological innovations and the increasing need for effective cardiac care solutions. Emphasis on preventive healthcare, coupled with advancements in AI and wearable technology, will further propel the market forward.

As healthcare systems worldwide prioritize early detection and management of cardiovascular diseases, the demand for efficient and accessible ECG solutions will remain robust.

Read Full Report: - https://www.uniprismmarketresearch.com/verticals/healthcare/ecg-equipment-and-management-systems

0 notes

Text

North America Sinus Dilation Market Brands Statistics and Overview 2027

Historic Data: 2017-2018 | Base Year: 2019 | Forecast Period: 2020-2027

Browse Full Report with TOC:

https://www.businessmarketinsights.com/reports/north-america-sinus-dilation-market

Analysis By Product ( Endoscope, Balloon Sinus Dilation Devices, Sinus Stents/ Implants, Handheld Instruments); Procedure type( Standalone Sinus Dilation procedure, Hybrid Sinus Dilation Procedure); End User( Hospitals, ENT Clinics, Ambulatory Surgical Centers) and Country

North America Sinus Dilation Regional Insights

The geographic reach of the North America Sinus Dilation market defines the specific areas where businesses compete and operate, each with its own unique market dynamics and patient demographics. Recognizing local distinctions is essential; this includes varied patient expectations (such as preferences for specific treatment durations or recovery protocols), economic climates that influence healthcare access and affordability, and complex regulatory frameworks that impact market entry. Businesses can broaden their market penetration by identifying and addressing underserved regions or adapting their services to precisely meet local needs. A clear, focused market approach enables optimized resource deployment, the development of precise marketing efforts, and the achievement of superior competitive positioning, thereby accelerating growth in targeted areas.

Get Sample PDF of this Report:

https://www.businessmarketinsights.com/sample/TIPRE00015447

North America Sinus Dilation Strategic Insights

Data-informed strategic insights for the North American Sinus Dilation market provide an in-depth analysis of the industry landscape, encompassing prevailing trends, key participants, and regional subtleties that impact patient behavior and market dynamics. These insights offer practical guidance, enabling readers to differentiate themselves by discovering untapped market segments or formulating distinctive value propositions that resonate with specific patient needs. By utilizing sophisticated data analytics, investors, producers, and other stakeholders can predict market fluctuations with greater accuracy and adapt their strategies accordingly. A future-oriented strategy is critical for securing sustained long-term regional success. Ultimately, the application of these strategic insights facilitates well-informed, strategic decisions, fostering profitability and achieving key business goals.

Reasons to buy the report

To understand the North American Sinus Dilation marketlandscape and identifymarket segments that are most likely to guarantee a strong return

Stay ahead of the race by comprehending the ever-changing competitive landscape for North America Sinus Dilation market

Efficiently plan M&A and partnership dealsin North America Sinus Dilation marketby identifying market segments with the most promising probable sales

Helps to takeknowledgeable business decisions from perceptive and comprehensive analysis of market performance of various segment form North America Sinus Dilation market

Obtain market revenue forecast for market by various segments from 2019 to 2027 in North America.

North America Sinus Dilation Market Segmentation

North America Sinus Dilation Market: By Product

· Endoscope

· Balloon Sinus Dilation Devices

· Sinus Stents/ Implants

· Handheld Instruments

North America Sinus Dilation Market: By Procedure

· Standalone Sinus Dilation Procedure

· Hybrid Sinus Dilation Procedure

North America Sinus Dilation Market: By End User

· Hospitals

· ENT Clinics

· Ambulatory Surgical Centers

North America Sinus Dilation Market: By Country

· US

· Canada

· Mexico

North America Sinus Dilation Market: Company Profiles

Medtronic

Smith And Nephew

Johnson And Johnson Services Inc

Stryker Corporation

Intersect ENT, Inc

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

#North America Sinus Dilation Market#North America Sinus Dilation Market Overview#North America Sinus Dilation Market Statistics

0 notes

Text

Containerized Data Center Market in Global Capability Centers Market Demand Analysis, Innovation Trends, and Forecast 2032

The Containerized Data Center Market size was valued at USD 11.4 billion in 2023 and is expected to reach USD 66.9 Billion by 2032, with a growing at CAGR of 21.73% Over the Forecast Period of 2024-2032.

Containerized Data Center Market is emerging as a transformative force in the IT infrastructure landscape, offering flexible, scalable, and energy-efficient solutions. Unlike traditional data centers, containerized data centers are modular systems housed within standard shipping containers, allowing for rapid deployment, improved mobility, and cost-effectiveness. These prefabricated units can be transported and installed quickly, making them ideal for remote locations, disaster recovery, military operations, and enterprises requiring temporary or scalable IT capacity.

Containerized Data Center Market growth is being driven by rising demand for edge computing, increased adoption of cloud-based services, and the need for decentralized data processing. As businesses and governments seek agile solutions that support real-time processing and data localization, containerized data centers are becoming an essential part of digital transformation strategies across industries.

Get Sample Copy of This Report:https://www.snsinsider.com/sample-request/4786

Market Keyplayers:

Dell Technologies - Dell Modular Data Center

Hewlett Packard Enterprise (HPE) - HPE Edge Center

Cisco Systems - Cisco Unified Computing System (UCS)

IBM - IBM Cloud Container Service

Microsoft - Azure Stack Edge

Google Cloud - Google Anthos

Schneider Electric - EcoStruxure Micro Data Center

Vertiv - Vertiv SmartMod

Rittal - Rittal Container Data Center

Mitsubishi Electric - iQ-R Series Control System

Huawei - Huawei Modular Data Center Solution

Fujitsu - Fujitsu Integrated System

NetApp - NetApp HCI

Siemens - Siemens Modular Data Center

Acer - Acer Modular Data Center

EdgeConneX - EdgeConneX Edge Data Center

NTT Communications - NTT Modular Data Centers

Supermicro - Supermicro Modular Data Center Solutions

Bull (Atos) - Bull Data Center on Demand

Digital Realty - Digital Realty’s Modular Data Center

Key Trends in the Containerized Data Center Market

Edge Computing Integration: Organizations are increasingly deploying containerized data centers closer to data sources to reduce latency and improve processing speeds, especially in sectors like telecommunications, healthcare, and IoT.

Modular and Scalable Design: The modular nature of containerized data centers enables companies to scale up IT infrastructure easily by adding more containers, avoiding the time and cost associated with building traditional data centers.

Sustainability Focus: These units are designed for energy efficiency, with advanced cooling systems and compact layouts that reduce power consumption, aligning with global sustainability goals.

Hybrid Cloud Adoption: Containerized data centers support hybrid cloud models by serving as secure and controllable environments that work alongside public and private cloud platforms.

Enquiry of This Report: https://www.snsinsider.com/enquiry/4786

Market Segmentation:

By Container Type

20 Feet Container

40 Feet Container

Customized Container

By End-Use

IT and Telecommunications

BFSI

Healthcare

Retail and E-commerce

Aerospace & Defense

Energy & Utilities

Others

By Organization size

Small & Medium Enterprise (SME)

Large Enterprise

Market Analysis

Growing Demand in Developing Regions: Countries with limited access to permanent data center infrastructure are adopting containerized solutions to quickly establish digital capabilities.

Cost and Time Efficiency: Businesses favor containerized data centers due to reduced construction costs, lower energy usage, and rapid deployment—often within weeks instead of months or years.

Increased Government and Military Use: Defense agencies and public institutions are deploying containerized data centers for mission-critical operations in remote and high-risk zones.

Vendor Innovation: Leading tech companies are investing in R&D to develop customizable and AI-powered containerized data center solutions, offering enhanced automation, monitoring, and security.

Future Prospects

The future of the Containerized Data Center Market looks promising, with innovations and strategic investments set to shape its evolution. As 5G networks expand and the Internet of Things (IoT) continues to proliferate, the need for agile and decentralized data processing infrastructure will intensify. Containerized solutions are uniquely positioned to meet this demand, particularly in supporting smart city initiatives, autonomous vehicle networks, and real-time analytics at the edge.

Furthermore, increased focus on disaster preparedness and business continuity is expected to fuel adoption. Organizations will rely on mobile, quickly deployable data centers to maintain operations during emergencies, cyberattacks, or natural disasters. The market will also benefit from the rising demand for temporary data center capacity during events, migrations, or short-term projects.

With continued advancements in automation, remote monitoring, and AI-powered cooling systems, the operational efficiency and sustainability of containerized data centers will improve further. Vendors are likely to offer more customizable, plug-and-play solutions, making containerized infrastructure accessible even to smaller enterprises and institutions.

Access Complete Report: https://www.snsinsider.com/reports/containerized-data-center-market-4786

Conclusion

The Containerized Data Center Market is revolutionizing how organizations approach IT infrastructure. With its unique blend of mobility, flexibility, and speed, it offers a powerful alternative to traditional data centers. As the digital landscape becomes increasingly decentralized, containerized data centers are well-positioned to meet the evolving needs of edge computing, hybrid cloud, and disaster recovery.

Driven by innovation and a growing demand for scalable, energy-efficient, and rapidly deployable solutions, the market is set for sustained growth. Enterprises, governments, and service providers alike are turning to containerized data centers to ensure high performance, resilience, and operational agility in the data-driven future.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Containerized Data Center Market#Containerized Data Center Market Scope#Containerized Data Center Market Growth#Containerized Data Center Market Trends

0 notes

Text

Dog Antibiotics Market by Type of Antibiotics Featuring Global Market Size, Segmental Analysis, Regional Overview, Company Share Insights, Leading Company Profiles, and Forecast from 2025 to 2035

Industry Outlook

The Dog Antibiotics Market was valued at USD 486.2 million in 2024 and is projected to reach USD 732.8 million by 2035, growing at a CAGR of approximately 3.8% from 2025 to 2035. This market focuses on the development and distribution of antibiotic medications specifically formulated to treat bacterial infections in dogs, including both internal and external conditions. The demand is driven by increased pet ownership, rising awareness of animal healthcare, and the growing prevalence of chronic conditions in dogs that require antibiotic intervention.

Veterinary pharmaceutical research continues to evolve, offering targeted treatments that reduce the risk of antibiotic resistance. The market benefits from various distribution channels including veterinary clinics, online pharmacies, and retail pet stores, catering to pet owners who prioritize convenience and effective care. However, strict regulatory oversight and rising concerns around antibiotic misuse pose challenges to market expansion.

Get free sample Research Report - https://www.metatechinsights.com/request-sample/2184

Market Dynamics

Growing Pet Ownership and Healthcare Awareness Fueling Demand

The increasing number of pet owners and their heightened awareness of animal healthcare needs is driving the demand for dog antibiotics. As more households adopt dogs, they seek comprehensive veterinary care, which includes treatments for infections requiring antibiotic prescriptions.

Chronic conditions such as diabetes and kidney disease in dogs contribute to the need for more frequent medical attention and antibiotic therapies. According to the American Veterinary Medical Association (AVMA), pet ownership in the U.S. reached 70% of households in 2021, reflecting a direct impact on the rising demand for veterinary antibiotics.

Rise in Bacterial Infections Among Dogs

Bacterial infections such as urinary tract infections, skin infections, and respiratory illnesses are becoming more common among pet dogs. This increasing prevalence necessitates prompt and effective treatment with antibiotics to prevent further complications.

According to data from the Centers for Disease Control and Prevention (CDC), pet healthcare spending reached $31.4 billion in 2021, indicating a strong market trend toward investing in medical solutions such as antibiotics for infection treatment and disease management.

Antibiotic Resistance Challenges Market Growth

The development of antibiotic resistance is a significant barrier in the Dog Antibiotics Market. Misuse and overuse of antibiotics in both human and animal medicine have led to the evolution of resistant bacterial strains. This issue complicates treatment strategies and reduces the effectiveness of standard antibiotics, necessitating the development of new and costlier alternatives.

Regulatory bodies are enforcing stricter controls on antibiotic usage in animals to curb resistance and minimize the risk of transmission to humans. According to the World Health Organization (WHO), antibiotic resistance poses a global threat to public health, food security, and sustainable development.

Emerging Markets Drive Growth Opportunities

Emerging markets across Asia-Pacific, Latin America, and Africa are witnessing rapid growth in pet ownership, presenting new opportunities for the Dog Antibiotics Market. Rising disposable incomes and urbanization have led to increased pet adoption, creating a stronger demand for veterinary healthcare services.

Countries like China and India are at the forefront of this growth, with expanding middle-class populations and evolving attitudes toward pet care. Increased awareness of veterinary services and improved access to medication are boosting antibiotic usage in these regions, creating significant market potential.

Innovation in Antibiotic Development to Tackle Resistance

Ongoing research into the development of new antimicrobial agents is opening new avenues for market growth. Innovative antibiotic formulations designed to combat resistant bacteria are essential for maintaining effective pet infection management.

Technological advances, such as sustained-release drug delivery methods, are enhancing treatment outcomes and user convenience. According to the U.S. National Institutes of Health (NIH), sustained efforts in antimicrobial research are vital for fighting the global issue of resistance and promoting the development of novel therapies for veterinary medicine.

Industry Experts Opinion

"Antibiotics are crucial in treating bacterial infections in dogs. However, they should always be used under veterinary supervision to ensure the correct medication and dosage are prescribed. Overuse or misuse of antibiotics can lead to antibiotic resistance and other health complications."

– Dr. Sarah Wooten, DVM

Segment Analysis

By Type of Antibiotic

The Dog Antibiotics Market is segmented into Penicillin, Cephalosporins, Tetracyclines, Fluoroquinolones, Macrolides, Aminoglycosides, and Sulphonamides. Penicillin remains the leading segment due to its broad-spectrum effectiveness, affordability, and established safety profile. It is widely prescribed for treating skin infections, respiratory infections, and urinary tract conditions in dogs.

Penicillin’s availability in both oral and injectable forms adds flexibility to veterinary treatment options, making it a preferred choice for veterinarians treating uncomplicated infections.

By Application

Based on application, the market is divided into Skin Infections, Respiratory Infections, Urinary Tract Infections, Gastrointestinal Infections, Ear Infections, and Others. Skin infections dominate this segment due to their high prevalence among dogs. Conditions such as pyoderma, allergic reactions, and insect bites are common causes of bacterial skin infections requiring antibiotic treatment.

Veterinarians often prescribe a combination of penicillin, cephalosporins, or tetracyclines to manage these infections. Growing awareness among pet owners about timely veterinary care has reinforced the market share of this segment.

Regional Analysis

North America Leading the Market

North America holds the dominant share in the Dog Antibiotics Market due to high pet ownership rates and advanced veterinary infrastructure. The U.S. and Canada have experienced steady increases in pet adoption, particularly among families, which drives demand for antibiotics used to treat common infections.

The availability of well-established veterinary clinics, hospitals, and online pharmacies makes treatment accessible. Additionally, government regulations support the responsible use of antibiotics to ensure safety and efficacy. According to the American Pet Products Association (APPA), pet ownership in the U.S. has reached 67% of households, emphasizing the growing importance of veterinary pharmaceutical products.

Rapid Growth in Asia-Pacific

The Asia-Pacific region is emerging as a fast-growing segment in the Dog Antibiotics Market due to increased pet ownership and rising awareness of animal healthcare. Urbanization and the expansion of the middle class in countries like China, India, and Japan have led to a surge in pet adoption and veterinary care demand.

Veterinary infrastructure is improving, with more clinics and digital platforms offering antibiotics and other treatments. Social media and pet influencers are also promoting awareness about proper pet care, further boosting the market's growth in this region.

Read Full Research Report https://www.metatechinsights.com/industry-insights/dog-antibiotics-market-2184

Competitive Landscape

The Dog Antibiotics Market is highly competitive, with both global and regional players striving to meet the increasing demand for effective veterinary treatments. Key players include Zoetis Inc., Merck & Co., and Boehringer Ingelheim, known for their diverse product portfolios and strong distribution networks.

Companies like Vetoquinol and Virbac specialize in niche segments, offering tailored solutions for specific health conditions. The rise of e-commerce and online pet pharmacies has intensified market competition by improving accessibility to antibiotics. Industry leaders are also investing heavily in R&D to combat antibiotic resistance and introduce new therapeutic alternatives.

Strategic initiatives such as mergers, collaborations, and product innovations are common, as companies seek to expand their market presence and meet the evolving needs of pet owners and veterinarians.

Buy Now https://www.metatechinsights.com/checkout/2184

0 notes

Text

Forensic Technology Market: Industry Trends and Forecast 2024-2032

The Forensic Technology Market was valued at USD 21.32 billion in 2023 and is projected to reach USD 54.18 billion by 2031, growing at a compound annual growth rate (CAGR) of 12.6% during the forecast period from 2024 to 2031. This remarkable growth is being fueled by a surge in criminal activities, advancements in biometric and DNA analysis technologies, and increased government investment in modernizing forensic infrastructure.

Market Description

Forensic technology plays a crucial role in criminal investigations, offering scientific techniques to collect, preserve, and analyze evidence. With the rise in sophisticated crimes and digital offenses, law enforcement agencies are increasingly relying on advanced forensic tools to solve cases efficiently. Technological developments such as automated fingerprint identification systems (AFIS), next-generation sequencing, and digital forensics are revolutionizing how investigations are conducted. The market is expanding not just in traditional areas like ballistics and DNA profiling, but also in newer fields including cybersecurity forensics and facial recognition.

Get Free Sample Report @ https://www.snsinsider.com/sample-request/3947

Regional Analysis

North America holds the largest share of the forensic technology market, attributed to the presence of advanced infrastructure, strong funding support, and widespread use of forensic tools in law enforcement.

Europe follows closely, driven by technological innovation and strict legal frameworks that encourage evidence-based investigation.

Asia-Pacific is projected to witness the fastest growth during the forecast period. Factors such as rising crime rates, increasing awareness, and governmental initiatives to upgrade forensic departments are contributing to market growth in countries like India, China, and Japan.

Latin America and Middle East & Africa are gradually adopting forensic technologies, with demand expected to increase as infrastructure develops and crime detection becomes a top priority.

Market Segmentation

By Type:

Biometric Devices

Digital Forensics

Ballistic Forensics

DNA Profiling

Others

By Application:

Law Enforcement Agencies

Healthcare

Banking & Financial Institutions

Government

Others

By End-User:

Public Sector

Private Sector

KEY PLAYERS:

The key market players include Eurofins Medigenomix GmbH, Agilent Technologies, NMS Labs, Thermo Fisher Scientific, Inc., Forensic Fluids Laboratories, Forensic Pathways, SPEX Forensics, LGC Forensics, Pyramidal Technologies Ltd, GE Healthcare & other players.

Key Highlights

Rapid technological advancements in DNA sequencing and biometric analysis

Growing demand for digital forensic solutions amid rising cybercrimes

Increased government initiatives to modernize forensic laboratories

Integration of artificial intelligence (AI) and machine learning in forensic processes

Expansion of forensic services across emerging economies

Future Scope

The forensic technology market is poised for significant evolution as new scientific techniques emerge to enhance crime detection and evidence analysis. Future innovations are likely to center around automation, AI-driven data interpretation, and portable forensic devices, enabling faster and more accurate results at crime scenes. Additionally, the integration of cloud computing and blockchain for secure storage and transfer of forensic data is expected to become more mainstream. As governments continue to invest in public safety and judicial efficiency, the demand for next-generation forensic tools will escalate across sectors.

Conclusion

The global forensic technology market is undergoing a transformative shift fueled by rising criminal complexities and the need for reliable, scientific investigation methods. As the market continues to expand across regions and industries, stakeholders are focusing on innovation, collaboration, and infrastructure development to meet growing demand. With sustained technological advancements and strong support from law enforcement agencies, the forensic technology industry is set to become a cornerstone of modern criminal justice systems.

Contact Us: Jagney Dave - Vice President of Client Engagement Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Other Related Reports:

Cell Viability Assay Market

Medical Power Supply Market

Post Traumatic Stress Disorder Treatment Market

MRI Guided Neurosurgical Ablation Market

#Forensic Technology Market#Forensic Technology Market Share#Forensic Technology Market Trends#Forensic Technology Market Size#Forensic Technology Market Growth

0 notes

Text

The strategic impact of starlink’s entry into India on Jio and Airtel’s market position

India’s digital transformation is entering a transformative phase with the impending arrival of satellite-based internet services. Elon Musk’s Starlink, a division of SpaceX, has forged strategic partnerships with telecom titans Reliance Jio and Bharti Airtel, marking a pivotal shift in India’s connectivity strategy. This collaboration aims to bridge the urban-rural digital divide while reshaping market dynamics in one of the world’s fastest-growing internet economies. Investors are closely monitoring Reliance Jio stock analysis and Airtel stock market news as these developments unfold.

From Rivals to Allies: A Strategic Pivot

Starlink’s journey into India initially faced resistance from Jio and Airtel, who dominate the country’s telecom sector. However, in a surprising reversal, both companies announced partnerships with Starlink in March 2025, signaling a shift from competition to cooperation. This alliance not only enhances Starlink’s regulatory prospects—pending approvals from the Department of Telecommunications and IN-SPACe—but also positions Jio and Airtel to leverage cutting-edge satellite technology without heavy R&D investments. Gwynne Shotwell, President of SpaceX, emphasized optimism about the collaboration, highlighting its potential to expand high-speed internet access nationwide.

LEO Satellites: A Technological Leap

Starlink’s innovation lies in its low Earth orbit (LEO) satellites, operating 200–2,000 km above Earth, a stark contrast to traditional geostationary satellites at 35,000 km. This proximity reduces latency, improves reliability, and enables coverage in remote regions lacking fiber or cellular infrastructure. However, maintaining a vast satellite constellation demands significant investment, and service quality can be affected by weather or physical obstructions. Telecom expert Sandeep Budki notes that LEO technology eliminates the need for ground infrastructure, making it ideal for India’s diverse terrain.

Bridging the Connectivity Chasm

The partnership’s primary promise lies in addressing India’s rural-urban digital gap. Over 70% of India’s population resides in villages where traditional broadband remains inconsistent or absent. Airtel plans to deploy Starlink in schools, healthcare centers, and remote communities, aligning with its rural-focused strategy. Jio, meanwhile, adopts a broader commercial approach, offering Starlink hardware online and in stores with installation support, targeting both households and enterprises. Beyond rural empowerment, sectors like agriculture, logistics, and aviation stand to gain. Starlink’s potential in-flight internet could revolutionize domestic air travel, mirroring global trends.

Competition and Market Dynamics

The Jio-Airtel rivalry extends to their Starlink strategies. While Airtel emphasizes social impact, Jio aims for widespread accessibility. This competition intensifies pressure on Vodafone Idea and BSNL to innovate or seek similar alliances. Meanwhile, global players like Amazon’s Kuiper and Eutelsat OneWeb are eyeing India’s satellite broadband market which is projected to grow at 36% annually, reaching $1.9 billion by 2030 (Deloitte). Despite Starlink’s premium pricing—expected at ₹5,000–7,000 monthly with hardware costs up to ₹38,000—its B2B focus could thrive in enterprise and SME sectors.

Challenges: Affordability, Regulation, and Security

While the partnership’s potential is vast, hurdles remain:

Cost Barriers:Starlink’s services are pricier than local broadband, limiting mass adoption. Analysts suggest subsidized models or government collaborations to enhance affordability.

Regulatory Hurdles:Spectrum allocation, data localization, and licensing require swift resolution to avoid delays.

Security Concerns:Starlink’s data collection practices and Musk’s geopolitical decisions, like restricting services in Ukraine, raise questions about reliability and privacy.

Investor Outlook and Future Trajectory

For investors, the alliance opens avenues to tap into underserved rural markets, boosting Jio and Airtel’s ARPU. However, Bernstein and Bank of America caution that Starlink’s high costs and limited satellite capacity may constrain its reach against established 5G and FWA (Fixed wireless access) networks. Success hinges on integrating Starlink into affordable plans and ensuring seamless last-mile connectivity.

Conclusion: A New Dawn for Digital Inclusivity

The Starlink-Jio-Airtel collaboration exemplifies cooperative competition, blending satellite innovation with telecom expertise to democratize internet access. While affordability and regulation pose challenges, strategic pricing and government support could catalyze India’s largest digital leap. As the nation strides toward a connected future, this partnership may set a global benchmark for bridging the digital divide through technological synergy.

Will satellite internet become India’s connectivity cornerstone? The answer lies in balancing innovation with inclusivity. For more information, visit https://www.indiratrade.com/

#Reliance Jio stock analysis#Airtel stock market news#Telecom sector investment#Starlink India impact#Satellite broadband stocks#India telecom market growth#best trading platform#best apps for stock market#best broker for trading#Reliance Industries#Bharti Airtel#Indira trade#Indira Securities

0 notes

Text

🧱 Composable Infra Market = $12.4B by 2034. The future’s modular.

Composable-Disaggregated Infrastructure (CDI) Market is undergoing a significant transformation, driven by the evolving needs of modern enterprises for agile, cost-effective, and scalable IT systems. As organizations increasingly rely on data-driven operations, traditional IT architectures often fall short in meeting dynamic resource demands.

CDI addresses this challenge by disaggregating compute, storage, and networking resources and recomposing them through software-based solutions as needed. This market, valued at $5.3 billion in 2024, is projected to reach $12.4 billion by 2034, reflecting a compound annual growth rate (CAGR) of 8.9%. The growing demand for flexible infrastructure in data centers and cloud service environments is a major contributor to this robust expansion.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS23429

Market Dynamics

Several core factors are influencing the growth trajectory of the CDI market. The primary driver is the shift towards digital transformation across industries, compelling organizations to seek infrastructure that can adapt rapidly to changing workloads. CDI solutions enable businesses to pool resources and allocate them efficiently, thereby reducing hardware redundancy and optimizing performance. In addition, the rise of cloud-native applications and hybrid IT environments has increased the appeal of composable infrastructure due to its modularity and agility.

However, challenges remain. The complexity of integrating CDI into existing legacy systems can hinder adoption, particularly for smaller organizations lacking technical expertise. Concerns around data security, system interoperability, and regulatory compliance also present obstacles. Despite these hurdles, innovations such as AI integration and automation are mitigating some of these issues, making CDI more accessible and effective.

Key Players Analysis

The CDI market is competitive and rapidly evolving, with major players investing heavily in R&D to maintain their edge. Companies such as Hewlett Packard Enterprise (HPE) and Dell Technologies are leading the charge, offering sophisticated modular platforms that support a wide array of enterprise applications. Their focus on interoperability and simplified management tools makes their solutions particularly attractive.

Emerging innovators like Liqid, DriveScale, Nebulon, and VAST Data are also making waves by introducing highly specialized products aimed at specific market niches. These companies are gaining traction with their focus on flexibility, performance, and cost efficiency. Strategic collaborations, acquisitions, and expansions are common as players look to diversify their portfolios and deepen market penetration.

Regional Analysis

Geographically, North America holds the lion’s share of the CDI market, buoyed by early adoption of advanced technologies and a robust ecosystem of tech giants and cloud providers. The United States, in particular, leads with strong investments in data centers and AI-driven infrastructure projects.

Europe follows, with countries like Germany and the UK actively investing in digital transformation initiatives. Strict data protection laws in the region also encourage adoption of CDI systems that offer robust compliance features.

Asia Pacific is emerging as a high-potential region, driven by rapid digitization in countries such as China, India, and Japan. Government initiatives supporting smart cities and data infrastructure are accelerating CDI deployment.

Meanwhile, Latin America, the Middle East, and Africa are gradually entering the CDI space, focusing on modernizing legacy systems and enhancing operational efficiencies in public and private sectors.

Recent News & Developments

The CDI landscape is seeing notable innovation, especially with the growing integration of AI, ML, and containerization technologies. These advancements enable real-time resource allocation and predictive analytics, significantly enhancing IT agility.

New pricing models are emerging, with deployment costs ranging between $10,000 and $100,000 depending on scale and complexity. This shift is making CDI solutions more attractive to mid-sized enterprises.

In recent strategic moves, companies have ramped up acquisitions and partnerships to enhance technological capabilities. There is a marked focus on interoperability, ease of integration, and automated management, all of which are becoming critical differentiators in the market.

Browse Full Report : https://www.globalinsightservices.com/reports/composable-disaggregated-infrastructure-market/

Scope of the Report

This report provides an in-depth analysis of the global CDI market, offering insights into historical trends, current market dynamics, and future growth prospects. It covers multiple segments including type, product, technology, deployment, and end-users. Special attention is given to regional market trends, emerging players, and competitive strategies.

Additionally, the report evaluates market drivers, challenges, and opportunities using comprehensive tools such as SWOT, PESTLE, and value-chain analysis. It also considers the impact of regulatory frameworks and technological advancements on market development. This study serves as a valuable resource for stakeholders aiming to navigate the evolving CDI landscape and capitalize on future growth opportunities.

Discover Additional Market Insights from Global Insight Services:

Mobile Phone Insurance Market : https://www.globalinsightservices.com/reports/mobile-phone-insurance-market/

Tour Operator Software Market : https://www.globalinsightservices.com/reports/tour-operator-software-market/

Computer Aided Engineering Market : https://www.globalinsightservices.com/reports/computer-aided-engineering-market/

Location-based Entertainment Market : https://www.globalinsightservices.com/reports/location-based-entertainment-market/

Mobile Value Added Services (VAS) Market : https://www.globalinsightservices.com/reports/mobile-value-added-services-vas-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

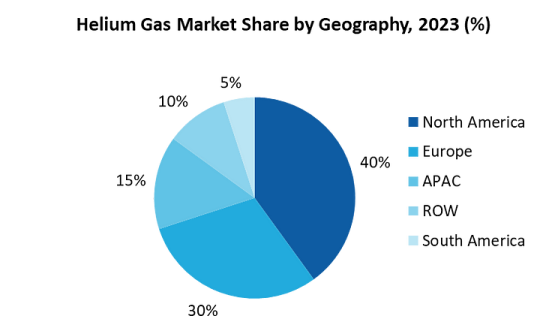

Helium Gas Market Opportunity Analysis & Industry Forecast, 2024–2030

Helium Gas Market Overview

Request Sample:

The growing need for helium in lifting applications, food packaging and the burgeoning electronics markets adds to its demand. Additionally, innovations in helium recovery and recycling, alongside strategic stockpiling by nations, emphasize its significance in ensuring supply chain security amidst resource constraints. The growing investments in helium exploration also drives the market by addressing supply challenges, supporting diverse applications, and ensuring long-term stability.

A notable trend in the helium gas market is the growing interest in space exploration. This reflects humanity’s pursuit of technological innovation, cosmic discovery and potential new resources. In March 2024, Japan launched a multibillion-dollar Space Strategic Fund aimed at supporting the Japan Aerospace Exploration Agency (JAXA). The $6.7 billion fund, approved for a decade-long period, will facilitate the development, technology demonstration and commercialization of cutting-edge space technologies, driving significant growth in the country’s space sector. Helium hard drives are HDDs sealed with helium instead of air, leveraging helium’s low density to reduce turbulence and friction, allowing for thinner platters, increased capacity (up to 10 platters), improved performance, energy efficiency, cooler operation, reduced noise and enhanced reliability. Helium HDDs are vital in large-scale data centers for efficient storage.

Market Snapshot :

Helium Gas Market — Report Coverage:

The “Helium Gas Market Report — Forecast (2024–2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Helium Gas Market.

AttributeSegment

By Form

Liquified

Compressed

By Supply

Cylinders

Bulk and Micro Tanks

Drum

On-site

By Purity

High Purity Helium

Medium-Purity Helium

Industrial-Grade Helium

By Application

MRI Scanning

Welding and Metal Fabrication

Cryogenics

Lifting and Balloons

Leak Detection

Breathing Mixes

Pressurizing and Purging

Controlled Atmosphere Source

Others

By End-Use Industry

Healthcare

Electronics

Aerospace and Defence

Energy

Industrial Manufacturing

Others

By Geography

North America (U.S, Canada and Mexico)

Europe (Germany, France, UK, Italy, Spain, Netherlands, Belgium, Denmark and Rest of Europe)

Asia-Pacific (China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Thailand, Malaysia and Rest of Asia-Pacific)

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

Rest of the World (Middle East and Africa).

Inquiry Before Buying:

COVID-19 / Ukraine Crisis — Impact Analysis:

Initially, the COVID-19 pandemic caused a decrease in helium demand due to reduced industrial and medical activities during lockdowns. This temporarily alleviated the helium shortage by reducing consumption. However, as industries resumed operations, the demand surged, leading to a tighter supply and rising prices. Challenges in global logistics also disrupted the helium supply chain exacerbating shortages.

Russia, a major global supplier of helium, faced production and export restrictions due to the war. Facilities like the Amur Gas Processing Plant, critical to Russia’s helium production, experienced operational disruptions. European countries’ shift away from Russian natural gas further complicated helium extraction processes in regions like Algeria, which redirected its natural gas to pipelines instead of liquefying it to extract helium. These disruptions contributed to a major helium shortage in two decades increasing global supply constraints and driving up costs.

Key Takeaways

MRI Scanning is the Largest Segment by Application

Helium, specifically in its liquid state, is a cryogenic substance used to cool the superconducting magnets in MRI systems to extremely low temperatures (around -269°C or 4 Kelvin). These low temperatures are necessary for the magnets to achieve and sustain superconductivity, which is critical for generating the strong and stable magnetic fields required for high-resolution imaging. According to Collective Minds, the global volume of MRI scans continues to grow annually, with current estimates ranging from 100–150 million scans worldwide. The demand for helium in this sector is substantial, as MRI technology is widely used in medical diagnostics to visualize detailed internal structures of the human body, aiding in the detection and monitoring of diseases. As per the 2024 India Private Equity Report, healthcare investments in India hit a record high of $5.5 billion in 2023, driven by a threefold increase compared to 2022. Additionally, the growth of the healthcare sector, advancements in imaging technology and increasing prevalence of conditions requiring MRI diagnostics further bolster the helium demand.

Schedule A Call:

Medium Purity Helium is the Largest Segment

Medium Purity Helium (99.0% to 99.99%) is the largest segment in the helium market due to its widespread applications across various industries, driven by both its properties and cost-effectiveness. In the manufacturing sector, it is extensively used in welding for non-ferrous metals like aluminium and copper, where high-quality, stable inert gases are essential for precise, clean welding. The welding industry is growing primarily driven by the construction and automotive industry. According to the American Welding Society, the US will require more than 360,000 welders by 2027. In the cryogenic industry, medium purity helium is a key component in cooling systems for MRI machines, superconducting magnets and particle accelerators. The combination of its versatile properties, availability, and lower cost compared to higher-purity helium makes it a highly attractive option for industries that require a reliable and efficient gas.

North America Leads the Market

North America continues to dominate the global helium gas market, bolstered by its abundant natural helium reserves and advanced extraction and distribution infrastructure. The United States, in particular, holds significant helium resources in regions such as the LaBarge field in Wyoming and the Texas Panhandle, which are key sources for the global market. Additionally, several companies are now interested in the helium exploration business which contribute to cutting-edge production, liquefaction and distribution technologies. Additionally, the region’s strong industrial base and healthcare advancements ensure a steady and robust demand for helium across sectors such as cryogenics, healthcare, aerospace, and manufacturing. In September 2024, North American Helium’s 9th helium purification facility at Antelope Lake, Saskatchewan, became operational. The facility has a production capacity of approximately 50 MMcf/year, increasing the company’s total capacity to 210 MMcf/year. NAH has reached a US $ 0.35 billion investment milestone in Saskatchewan, supported by government incentives such as the Critical Minerals Processing Investment Incentive (CMPII). Since launching its first facility in 2020, NAH, as of September 2024, produces ~7% of North America’s helium and aims for 20%.

Buy Now :

Limited Helium Reserves and Extraction Dependence to Hamper the Market

For more details on this report — Request for Sample

Key Market Players

Global Helium Gas top 10 companies include:

Air Liquide SA

Air Products and Chemicals, Inc.

Linde Plc

QatarEnergy LNG

Iwatani corporation

Messer Group

Nippon Sanso Holdings Corp

Matheson Tri-Gas Inc.

North American Helium (NAH)

Gazprom

By Form, By Supply, By Purity, By Application, By End-Use Industry and By Geography

Geographies Covered

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Belgium, Denmark and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Thailand, Malaysia and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa)

Key Market Players

Air Liquide SA

Air Products and Chemicals, Inc.

Linde Plc

QatarEnergy LNG

Iwatani corporation

Messer Group

Nippon Sanso Holdings Corp

Matheson Tri-Gas Inc.

North American Helium (NAH)

Gazprom

For more Chemicals and Materials Market reports, please click here

0 notes

Text

The Growing Demand for Tier III and Tier IV Data Centers in the GCC

Introduction

As businesses and governments in the GCC Data Center Market region continue their digital transformation, the need for high-reliability, secure, and scalable data centers has surged. Organizations handling mission-critical workloads require data centers with guaranteed uptime, redundancy, and security, making Tier III and Tier IV data centers the preferred choice.

With increasing investments in banking, healthcare, government, and hyperscale cloud services, the GCC is witnessing a sharp rise in Tier III and Tier IV-certified data centers. This blog explores the benefits, key players, challenges, and future prospects of high-tier data centers in the region.

Get Free Sample Copy @ https://www.statsandresearch.com/request-sample/40593-data-center-industry-analysis

1. Understanding Data Center Tier Classifications

The Uptime Institute classifies data centers into four tiers based on availability, redundancy, and fault tolerance:

Tier I Data Centers – Basic infrastructure with 99.671% uptime (28.8 hours downtime/year).

Tier II Data Centers – Partial redundancy with 99.741% uptime (22 hours downtime/year).

Tier III Data Centers – Concurrently maintainable with 99.982% uptime (1.6 hours downtime/year).