#Silicon Metal Market Analysis and Forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

US Tumblr user growth rate is estimated to slow down to 4.1%.

Text

Aluminium Alloy Ingot Price Trend 2025: What’s Driving Prices This Year?

The Aluminium Alloy Ingot prices trend in 2025 is gaining attention as industries across automotive, construction, aerospace, and manufacturing look for more durable, lightweight, and cost-effective materials. Unlike pure aluminium ingots, aluminium alloy ingots are blended with elements like silicon, magnesium, copper, or zinc to enhance performance properties. These alloys are used widely in engine parts, body panels, structural frames, and more making their pricing directly tied to broader industrial activity and innovation trends.

👉 👉 👉 Please Submit Your Query for Aluminium Alloy Ingot Price Trend, demand-supply, forecast and market analysis: https://www.price-watch.ai/contact/

As 2025 unfolds, aluminium alloy ingot prices have shown a moderate upward push, especially in regions like China, India, and the European Union. One of the big reasons is the strong rebound in global automotive production, where aluminium alloys play a major role in replacing heavier steel components. Lightweighting is a key trend in both traditional and electric vehicle manufacturing, which continues to support demand for aluminium alloys. The more cars being built, the more alloy ingots are needed, and this naturally adds upward pressure on prices.

Another driver of the price trend is the fluctuation in raw material costs. The base metal aluminium has seen tight supply in some markets due to power shortages, mining delays, and carbon-related policies affecting smelter output. When the cost of aluminium rises, alloy ingot producers pass some of those costs along the chain. On top of that, some alloying materials like magnesium and copper have also seen price increases, making the overall production of aluminium alloy ingots more expensive in 2025.

In the construction and infrastructure sector, alloy ingots are used in doors, railings, pipelines, bridges, and modular frameworks. The continued global investments in smart cities, green buildings, and transport systems are boosting usage. Countries across Asia and the Middle East are ramping up aluminium alloy imports as part of large infrastructure rollouts. This demand-side strength is helping maintain steady price levels for alloy ingots throughout the first half of 2025.

From a manufacturing perspective, recycling is also playing an interesting role in the aluminium alloy ingot market. Since alloys are often created using scrap and recycled aluminium, the availability of quality scrap material significantly affects supply. When scrap becomes scarce or expensive, smelters have to rely more on primary aluminium, which increases costs. In 2025, tighter scrap markets—particularly in China and Southeast Asia—have added some complexity to pricing.

The aluminium alloy ingot market is segmented by alloy type, such as ADC12, LM6, and Al-Si-Mg blends, depending on the application. Automotive-grade alloys continue to dominate in volume, followed by industrial and aerospace grades. The global market size is expected to grow at a healthy pace this year, supported by sustainability targets, industrial automation, and the expansion of lightweight structural components in all kinds of engineered products.

Major suppliers in the aluminium alloy ingot market include Chalco (China), Hindalco (India), Rio Tinto (Australia), Emirates Global Aluminium (UAE), and Novelis (USA). These companies influence global prices not just by how much they produce but also by how they respond to environmental regulations, energy pricing, and trade policies. In 2025, most leading players have been maintaining stable output, though some have begun shifting toward low-carbon or green aluminium initiatives, which may slightly affect production costs going forward.

Looking at the overall forecast for aluminium alloy ingot prices in 2025, a stable to slightly bullish trend is expected through the rest of the year. As long as automotive and infrastructure demand stay strong and energy markets remain unpredictable, prices are unlikely to fall sharply. That said, any major economic slowdown or easing in raw material prices could bring temporary corrections in some regions. Industry watchers suggest staying alert to global aluminium supply, alloying element availability, and regional scrap flows as key indicators of future price movements.

In summary, the aluminium alloy ingot price trend in 2025 reflects a mix of solid demand, raw material cost changes, and sustainable manufacturing goals. For manufacturers, procurement teams, and traders, understanding these market forces is essential for making better buying decisions and planning future supply contracts. The year ahead promises steady activity and evolving opportunities across both developed and emerging markets.

0 notes

Text

Global Ag Power for PV Metallization Silver Paste Market 2025

Ag Power for PV Metallization Silver Paste refers to a high-purity silver paste used in photovoltaic (PV) solar cells for metallization purposes. It plays a crucial role in enhancing electrical conductivity and efficiency in solar panels by forming fine grid lines that collect and transfer generated electricity. This paste is designed to withstand high-temperature processes and maintain superior adhesion to silicon wafers, ensuring long-term performance and durability.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/659/global-ag-power-for-pv-metallization-silver-paste

Market Size

The global Ag Power for PV Metallization Silver Paste market was valued at USD 3,137.43 million in 2023 and is projected to reach USD 3,450.93 million by 2029, registering a Compound Annual Growth Rate (CAGR) of 1.60% during the forecast period. The market's steady growth is attributed to increasing investments in solar energy, advancements in PV technology, and government incentives promoting clean energy adoption.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers:

Growing Solar Energy Adoption: The rapid shift towards renewable energy sources is fueling demand for efficient PV cells, which in turn boosts the requirement for silver paste.

Technological Advancements in PV Cells: Continuous research and development in photovoltaic technology have led to the creation of high-performance silver pastes with improved conductivity and reduced resistance.

Government Incentives for Renewable Energy: Subsidies, tax credits, and favorable policies are accelerating the adoption of solar power, indirectly increasing the demand for metallization silver paste.

Restraints:

High Cost of Silver: The fluctuating price of silver remains a major challenge, as it directly impacts the production cost of silver paste.

Substitution with Alternative Materials: Researchers are exploring cost-effective alternatives, such as copper paste, which may limit the growth potential of silver paste in the long run.

Opportunities:

Emerging Markets in Developing Nations: Countries in Asia-Pacific, Latin America, and Africa are investing heavily in solar energy, creating a new avenue for market growth.

Development of Low-Silver or Silver-Free Alternatives: Innovations in silver paste formulation with reduced silver content can help mitigate cost concerns and boost market penetration.

Challenges:

Environmental Concerns and Recycling Issues: The extraction and disposal of silver paste can have environmental implications, necessitating sustainable production practices.

Supply Chain Disruptions: Fluctuations in raw material availability due to geopolitical tensions or economic downturns can affect production and pricing.

Regional Analysis

Asia-Pacific

Leading the global market, this region benefits from significant solar panel manufacturing industries in China, India, Japan, and South Korea.

North America

The presence of key PV technology companies and government support for renewable energy adoption contribute to market growth.

Europe

Increasing investments in sustainable energy and stringent carbon reduction policies drive demand in countries like Germany, France, and the UK.

Latin America

Countries such as Brazil and Mexico are experiencing growth in solar energy installations, fueling demand for metallization silver paste.

Middle East & Africa

Expanding solar projects in the UAE, Saudi Arabia, and South Africa present significant market opportunities.

Competitor Analysis

Key players in the Ag Power for PV Metallization Silver Paste market include:

DuPont

Heraeus Holding

Samsung SDI

Giga Solar Materials Corporation

Dowa Electronics Materials

Murata Manufacturing

Johnson Matthey

These companies focus on innovation, strategic partnerships, and expanding production capacity to maintain a competitive advantage.

Market Segmentation (by Application)

PERC Solar Cell

BSF Solar Cell

TOPCon Solar Cell

HJT Solar Cell

Others

Market Segmentation (by Type)

Front Side Ag Power

Back Side Ag Power

Global Ag Power for PV Metallization Silver Paste: Market Segmentation Analysis

This report provides a deep insight into the global Ag Power for PV Metallization Silver Paste market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Ag Power for PV Metallization Silver Paste. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Ag Power for PV Metallization Silver Paste market in any manner.

FAQ Section :

1. What is the current market size of the Ag Power for PV Metallization Silver Paste market?

The market was valued at USD 3,137.43 million in 2023 and is projected to reach USD 3,450.93 million by 2029, with a CAGR of 1.60%.

2. Which are the key companies operating in the Ag Power for PV Metallization Silver Paste market?

Major players include DuPont, Heraeus Holding, Samsung SDI, Giga Solar Materials Corporation, Dowa Electronics Materials, Murata Manufacturing, and Johnson Matthey.

3. What are the key growth drivers in the Ag Power for PV Metallization Silver Paste market?

Factors such as rising solar energy adoption, technological advancements in PV cells, and government incentives for renewable energy are driving growth.

4. Which regions dominate the Ag Power for PV Metallization Silver Paste market?

The Asia-Pacific region leads the market, followed by North America and Europe.

5. What are the emerging trends in the Ag Power for PV Metallization Silver Paste market?

Key trends include the development of low-silver alternatives, increasing investments in solar projects, and advancements in metallization technology.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/659/global-ag-power-for-pv-metallization-silver-paste

ttps://www.tumblr.com/intelmarketresearch/786039876505272320/smd-thermistor-market

0 notes

Text

Lithium-Ion Satellite Battery Materials Market - Analysis and Forecast, 2025-2034

What are lithium-ion satellite battery materials?

Specialized components designed to power spacecraft and satellites. These materials include cathodes (e.g., lithium cobalt oxide, nickel manganese cobalt oxide), anodes (typically graphite or silicon-based), and electrolytes (liquid or solid-state). They are engineered to deliver high energy density, long cycle life, and reliability under extreme space conditions such as vacuum, radiation, and temperature fluctuations. These batteries are essential for maintaining satellite operations during eclipse periods and ensuring mission success over extended durations.

The market for lithium-ion satellite battery materials is expected to increase significantly as the space industry develops, particularly in the areas of communication, navigation, and Earth observation. This is due to the growing demand for effective, long-lasting, and lightweight power sources in contemporary satellite technology.

What is the current market size of lithium-ion satellite battery materials?

The Lithium-Ion Satellite Battery Materials Market, valued at $1.62 billion in 2024, is projected to reach $2.57 billion by 2034. It is expected to grow at a CAGR of 4.72% during the forecast period from 2025 to 2034.

Which regions are expected to dominate the lithium-ion satellite battery materials market?

North America (U.S., Canada, Mexico)

Europe (Germany, France, Italy, Spain, U.K., Rest-of-Europe)

Asia-Pacific (China, Japan, South Korea, India, Rest-of-Asia-Pacific)

Asia-Pacific is anticipated to gain traction in terms of production, owing to the continuous growth and the presence of key manufacturers in the region.

Demand Drivers

Rising Demand for Data and Connectivity: The surge in global data consumption and the need for seamless connectivity are driving increased deployment of satellites, boosting demand for reliable lithium-ion battery materials.

Expansion of Satellite Constellations: The growing trend of launching large-scale satellite constellations, especially in low Earth orbit (LEO), requires advanced energy storage solutions to ensure continuous and efficient satellite operation.

Competition Synopsis

The global lithium-ion satellite battery materials market is highly competitive, led by major players such as BASF, Umicore, LG Chem, and Johnson Matthey. To keep their market supremacy, these businesses make use of strong R&D efforts, innovative new materials, and strategic alliances with satellite manufacturers. In the meantime, new companies are concentrating on creating affordable and environmentally friendly alternatives to meet the growing need for high-performance space batteries. Rapid technological breakthroughs, strict regulations, and the accelerating speed of satellite deployments all contribute to intense competition, which encourages constant innovation and cooperation across the industrial value chain.

Who are the key players in the lithium-ion satellite battery materials market?

Umicore

Sumitomo Metal Mining

BASF

LG Chem

EcoPro BM

Toda Kogyo

Nichia Corporation

Download Our Sample Report Now!

Learn more about Aerospace Vertical. Click Here!

Conclusion

The global lithium-ion satellite battery materials market is set for sustained growth, fueled by rising satellite launches, technological innovation, and increasing demand for efficient energy storage in space applications. Leading companies and up-and-coming producers are spending money on cutting-edge, environmentally friendly materials to satisfy performance requirements while tackling issues with cost and durability. The market is poised for growth as a result of ongoing developments in battery technologies and the emergence of Asia-Pacific as a significant production hub. In the rapidly changing satellite industry, overcoming obstacles and seizing new opportunities will require strategic alliances and continuous research and development.

#Lithium-Ion Satellite Battery Materials Market#Lithium-Ion Satellite Battery Materials Industry#Lithium-Ion Satellite Battery Materials Report#aerospace

0 notes

Text

Global GCC Countries PV Metallization Aluminium Paste Market: Forecast Insights Through 2032

Global GCC countries PV metallization aluminium paste market, currently valued at USD 220 million in 2024, is poised for steady growth with a projected CAGR of 6.6% through 2032, according to the latest industry analysis. This expansion comes as solar energy adoption accelerates across Gulf Cooperation Council nations, where government initiatives are transforming the energy landscape.

PV metallization aluminium paste serves as the backbone of solar cell manufacturing, providing the essential conductive layer that enables efficient energy conversion. The material's unique composition of aluminium particles, glass frit, and organic binders has become increasingly sophisticated, with manufacturers now focusing on eco-friendly, lead-free formulations to meet stringent environmental standards while maintaining optimal electrical performance.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/292878/gcc-countries-pv-metallization-aluminium-paste-market

Regional Market Dynamics

Middle Eastern countries, particularly Saudi Arabia and the UAE, dominate regional demand as they implement ambitious renewable energy programs under national visions like Saudi Vision 2030. These projects have triggered unprecedented demand for high-performance metallization pastes compatible with both traditional crystalline silicon and emerging thin-film photovoltaic technologies.

The Asia-Pacific region maintains its position as the global solar manufacturing hub, absorbing over 60% of GCC-produced aluminium pastes. Meanwhile, European manufacturers are increasingly turning to GCC suppliers for RoHS-compliant pastes as the EU tightens environmental regulations on solar component manufacturing.

Key Growth Factors

Solar sector expansion across GCC nations stands as the primary market driver, with regional installed capacity crossing 5.4 GW in recent years. The aluminum paste market benefits directly from this growth, as each new solar park requires substantial quantities of metallization materials. Furthermore, technological advancements in paste formulations have enhanced solar cell efficiencies by 1-1.5%, making projects more viable and accelerating adoption.

Manufacturers have responded to market demands with innovative solutions:

Nanoscale aluminum particle formulations for finer line printing

Optimized glass frit systems improving conductivity

Specialized pastes for harsh desert conditions

Challenges and Restraints

Despite strong growth prospects, the market faces several challenges. Raw material volatility remains a persistent issue, with aluminum prices fluctuating by ±23% in recent years, directly impacting production costs. Additionally, the rapid evolution of solar cell technologies requires constant R&D investment to avoid product obsolescence.

Other notable challenges include:

Intellectual property barriers for regional manufacturers

Supply chain complexities in extreme climates

Competition from alternative metallization technologies

Market Segmentation

The market is segmented by product type into:

Normal aluminium paste

Lead-free aluminium paste

By application, key segments include:

Mono-Si solar cells

Multi-Si solar cells

Thin film solar cells

Competitive Landscape

The market features a mix of global leaders and regional specialists, with companies like Giga Solar Materials Corp., Dupont, and Heraeus Electronics maintaining strong positions through technological innovation and strategic partnerships. Regional players such as Rutech and Toyo Aluminum KK have gained traction by focusing on localized solutions tailored to Middle Eastern conditions.

Key competitive strategies include:

Product portfolio expansion

Strategic collaborations with panel manufacturers

Local production initiatives

Report Scope

This comprehensive analysis covers the global GCC countries PV metallization aluminium paste market landscape from 2024 to 2032, including:

Market size and growth projections

Detailed segmentation analysis

Competitive benchmarking

Technology trends

Regional demand patterns

The research methodology incorporated extensive primary interviews with industry stakeholders and thorough analysis of market developments to provide accurate, actionable insights.

Get Full Report Here: https://www.24chemicalresearch.com/reports/292878/gcc-countries-pv-metallization-aluminium-paste-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

0 notes

Text

Copper Paste for PCB Market 2025

The global Copper Paste for PCB market was valued at US dollars 129.97 million in 2023 and is anticipated to reach US dollars 177.65 million by 2030, witnessing a CAGR of 5.10 percent during the forecast period 2024 to 2030.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/472/copper-paste-pcb-market

Copper paste for PCB or Printed Circuit Board is a conductive paste used to fill voids or gaps in copper traces or to repair damaged copper traces on a PCB. It is typically made from a mixture of copper particles and a binder or carrier material such as silicone or epoxy. The paste is applied to the PCB using a syringe or other dispensing tool and then cured or sintered to create a conductive bond between the copper particles.

The Japan market for Copper Paste for PCB is estimated to increase from US dollars 64.04 million in 2023 to reach US dollars 85.41 million by 2030, at a CAGR of 4.88 percent during the forecast period 2024 through 2030.

The China market for Copper Paste for PCB is estimated to increase from US dollars 27.08 million in 2023 to reach US dollars 41.83 million by 2030, at a CAGR of 6.87 percent during the forecast period 2024 through 2030.

Major global manufacturers of Copper Paste for PCB include Sumitomo Metal Mining Kyoto Elex Tatsuta Chang Sung Corporation NAMICS Mitsuboshi Belting Asahi Solder Heraeus Shoei Chemical Asahi Chemical Yuhon Copprint PrintCB and Ampletec. In 2023, the top three vendors accounted for approximately 49.00 percent of total revenue.

This report provides a comprehensive presentation of the global Copper Paste for PCB market with both quantitative and qualitative analysis. It helps readers develop business and growth strategies, assess the competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Copper Paste for PCB.

Market size estimations and forecasts are provided in terms of output or shipments measured in kilograms and revenue in US dollars millions. The base year is 2023, with historical and forecast data spanning from 2019 to 2030. This report segments the global Copper Paste for PCB market by type, by application, by company, and by region. Regional market sizes and details concerning products by type, by application, and by key players are also provided.

For a more in-depth understanding, the report offers profiles of the competitive landscape, key competitors, and their market ranks. The report also discusses technological trends and new product developments shaping the industry.

This analysis helps Copper Paste for PCB manufacturers, new entrants, and industry chain related companies with information on revenues, production, and average price for the overall market and subsegments across different categories by company, by type, by application, and by region.

Market Segmentation

By Company Sumitomo Metal Mining Kyoto Elex Tatsuta Chang Sung Corporation NAMICS Mitsuboshi Belting Asahi Solder Heraeus Shoei Chemical Asahi Chemical Yuhon Copprint PrintCB Ampletec

Segment by Type Low Temperature Sintered Medium Temperature Sintered High Temperature Sintered

Segment by Application Consumer Electronics Communications Industrial and Medical Automotive Military and Aerospace Others

Production by Region North America Europe China Japan South Korea

Consumption by Region North America United States Canada Asia Pacific China Japan South Korea China Taiwan Southeast Asia India Australia Europe Germany France United Kingdom Italy Spain Rest of Europe Latin America Mexico Brazil Argentina Middle East and Africa Israel GCC Countries Turkey South Africa

The global Copper Paste for PCB market is expected to experience steady growth driven by increasing demand for high-performance electronic devices, rising investments in consumer electronics, and growing automotive and aerospace applications. Technological advances in binder chemistries and particle size control will continue to improve paste performance and reliability. Companies that focus on innovation, quality, and strategic partnerships are likely to strengthen their market position and capture emerging opportunities from 2025 through 2031.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/472/copper-paste-pcb-market

0 notes

Text

HD Grease Market Insights: How Thermal Interface Materials Are Changing the Game

Global Heat Dissipation Grease (HD Grease) Market is experiencing robust expansion, with valuations reaching USD 144 million in 2023. Current projections indicate the market will grow at a compound annual growth rate (CAGR) of 6.8%, potentially reaching USD 260.32 million by 2032. This accelerated trajectory stems from surging demand in electronics manufacturing, electric vehicle production, and next-gen computing infrastructure where thermal management is critical.

Thermal interface materials like HD grease have become indispensable in modern electronics, filling microscopic imperfections between heat-generating components and cooling apparatus. As device miniaturization continues alongside rising power densities, manufacturers are prioritizing advanced formulations with exceptional thermal conductivity (often exceeding 8 W/mK) and extended reliability under thermal cycling.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/288926/global-heat-dissipation-grease-forecast-market-2025-2032-519

Market Overview & Regional Analysis

Asia-Pacific commands over 55% of global HD grease consumption, with China's electronics manufacturing hubs and South Korea's semiconductor industry driving demand. The region benefits from concentrated supply chains and swift adoption of 5G infrastructure, which requires advanced thermal solutions for base stations and edge computing devices. Japanese manufacturers continue leading in high-performance formulations, particularly for automotive electronics.

North America maintains strong growth through its advanced computing sector, where data centers and AI hardware necessitate premium thermal interface materials. Europe's market thrives on stringent electronic reliability standards and growing EV adoption, with Germany's automotive suppliers emerging as key consumers. Emerging markets in Southeast Asia show accelerating demand, fueled by electronics production shifting from traditional manufacturing centers.

Key Market Drivers and Opportunities

The market's expansion hinges on three pivotal factors: the unstoppable march of electronics miniaturization, the automotive industry's rapid electrification, and escalating data center investments. Semiconductor packaging accounts for 38% of HD grease applications, followed by EV power electronics at 22% and consumer electronics at 19%. The burgeoning field of high-performance computing (HPC) presents new frontiers, with GPU clusters and AI accelerators requiring advanced thermal solutions.

Innovation opportunities abound in metal-particle enhanced greases (achieving 12-15 W/mK conductivity) and phase-change materials that combine grease-like application with pad-like stability. The photovoltaic sector also emerges as a growth vector, where solar microinverters demand durable thermal compounds resistant to outdoor weathering. Meanwhile, aerospace applications for satellite electronics create specialized niche markets requiring extreme temperature stability.

Challenges & Restraints

Material scientists face persistent hurdles in balancing thermal performance with practical considerations. High-performance formulations frequently encounter pump-out issues under thermal cycling, while silicone-based variants risk contaminating sensitive optical components. The automotive sector's transition to 800V architectures introduces new challenges - requiring greases that maintain performance across wider temperature swings while resisting electrochemical migration.

Supply chain complexities pose additional concerns, with specialty fillers like boron nitride and aluminum oxide facing periodic shortages. Regulatory landscapes continue evolving, particularly regarding silicone content restrictions in certain electronics applications. Furthermore, the industry struggles with standardization - thermal conductivity claims often vary significantly between testing methodologies.

Market Segmentation by Type

Silicone-Based Thermal Grease

Silicone-Free Thermal Grease

Metal-Particle Enhanced Formulations

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/288926/global-heat-dissipation-grease-forecast-market-2025-2032-519

Market Segmentation by Application

Consumer Electronics (Smartphones, Tablets, Laptops)

Automotive Electronics (EV Batteries, Inverters)

Telecommunications Infrastructure

Data Center Equipment

Industrial Electronics

LED Lighting Systems

Market Segmentation and Key Players

Dow Chemical Company

Henkel AG & Co. KGaA

Shin-Etsu Chemical Co., Ltd.

Parker Hannifin Corporation

3M Company

Laird Technologies

Momentive Performance Materials

Wakefield-Vette

Zalman Tech

Thermal Grizzly

Arctic Silver

Fujipoly

Denka Company Limited

Gelon LIB Group

Dongguan Jiezheng Electronics

Report Scope

This comprehensive analysis examines the global HD grease landscape from 2024 to 2032, providing granular insights into:

Volume and revenue projections across key regions and applications

Detailed technology segmentation by formulation type and performance characteristics

Supply chain dynamics including raw material sourcing and manufacturing trends

Regulatory landscape analysis for major jurisdictions

The report features exhaustive profiles of 25 leading manufacturers, evaluating:

Product portfolios and R&D pipelines

Production capacities and geographic footprints

Key partnerships and client ecosystems

Pricing strategies and distribution networks

Get Full Report Here: https://www.24chemicalresearch.com/reports/288926/global-heat-dissipation-grease-forecast-market-2025-2032-519

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

Other Related Reports:

0 notes

Text

Sealing Coatings Market Industry Competition Analysis, Size and Forecast Till 2025-2033

The Reports and Insights, a leading market research company, has recently releases report titled “Sealing Coatings Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033.” The study provides a detailed analysis of the industry, including the global Sealing Coatings Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Sealing Coatings Market?

The global sealing coatings market was valued at US$ 3.6 Billion in 2024 and is expected to register a CAGR of 5.2% over the forecast period and reach US$ 5.7 Billion in 2033.

What are Sealing Coatings?

Sealing coatings are substances applied to surfaces to form a protective layer that guards against moisture, chemicals, corrosion, and other environmental factors. They are utilized on various surfaces like concrete, metal, and wood to prevent harm and prolong the lifespan of the substrate. Commonly used in construction, automotive, and industrial sectors, these coatings enhance durability and preserve the aesthetic appeal of surfaces.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1788

What are the growth prospects and trends in the Sealing Coatings industry?

The sealing coatings market growth is driven by various factors. The sealing coatings market is experiencing consistent growth due to rising demand for protective coatings across industries like construction, automotive, and manufacturing. These coatings safeguard surfaces against corrosion, moisture, and environmental damage, boosting the longevity of materials. As technology advances and sustainability gains importance, the sealing coatings market is poised for further expansion, offering a variety of solutions to meet the diverse needs of various industries. Hence, all these factors contribute to sealing coatings market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

Resin Type:

Acrylic

Silicone

Polyurethane

Epoxy

Others

Substrate:

Metal

Concrete & Masonry

Wood

Plastic

Others

End-Use Industry:

Building & Construction

Automotive

Industrial

Marine

Aerospace

Electrical & Electronics

Others

Application:

Roofing

Flooring

Walls & Ceilings

Windows & Doors

Tank Linings

Others

Technology:

Water-based

Solvent-based

Radiation-cured

Powder-based

Others

Sales Channel:

Direct Sales

Distributor Sales

Online Sales

Price Range:

Economy

Mid-Range

Premium

Functionality:

Waterproofing

Corrosion Resistance

Thermal Resistance

Chemical Resistance

Others

Curing Type:

Air Cure

Heat Cure

Moisture Cure

Others

Segmentation By Region:

North America:

United States

Canada

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

3M Company

Akzo Nobel N.V.

Axalta Coating Systems

BASF SE

Dow Inc.

Henkel AG & Co. KGaA

Hempel A/S

Jotun Group

Nippon Paint Holdings Co., Ltd.

PPG Industries, Inc.

RPM International Inc.

Sherwin-Williams Company

Sika AG

Tikkurila Oyj

Wacker Chemie AG

View Full Report: https://www.reportsandinsights.com/report/Sealing Coatings-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

Synthetic Lubricants Market Size, Share, Trends, Demand, Growth, Challenges and Competitive Analysis

Global Synthetic Lubricants Market - Size, Share, Demand, Industry Trends and Opportunities

Global Synthetic Lubricants Market, By Product (Silicones, PAO, Esters, PAG, Group 3, Phosphate Ester, Polyolester, Biolubes, Di-Basic Acid Ester, Others), Application (Engine Oil, Hydraulic Fluids, Compressor Oil, Gear Oil, Greases, Refrigeration Oil, Transmission Fluids and Hydraulic Fluids, Turbine Oil, HTF, Metalworking Fluids, Process Oil, Marine Lubricants, General Industrial Oils, Others), End-Use Industry (Construction, Mining, Metal Production, Cement Production, Power Generation, Automotive Manufacturing, Chemical, Marine, Oil and Gas, Food Processing, Textile, Others) - Industry Trends and Forecast to 2023 to 2030.

Access Full 350 Pages PDF Report @

**Segments**

- By Product Type: The synthetic lubricants market is segmented based on product type into PAO (Poly Alpha Olefin), Esters, Group III, PAG (Polyalkylene Glycol), and others. PAO is expected to hold a significant market share due to its excellent thermal and oxidation stability properties, making it suitable for use in high-performance applications. Esters are also gaining traction in the market owing to their superior lubricity and biodegradability compared to traditional mineral oils. Group III synthetic lubricants are gaining popularity as a cost-effective alternative to PAO oils, particularly in automotive and industrial applications.

- By Application: The market can be segmented by application into automotive, industrial, and others. The automotive segment is anticipated to dominate the market, driven by the increasing demand for high-performance lubricants to enhance fuel efficiency and reduce emissions. In the industrial sector, synthetic lubricants are widely used in machinery, turbines, compressors, and hydraulic systems to improve operational efficiency and reduce maintenance costs. Other applications, such as aerospace and marine, are also fueling the growth of the synthetic lubricants market.

- By End-Use Industry: The end-use industry segment includes automotive, aerospace, marine, industrial machinery, and others. Automotive is a key end-use industry for synthetic lubricants, driven by the growing automotive production and the need for advanced lubricants to meet stringent regulations. The aerospace and marine industries also rely on synthetic lubricants for their high-performance characteristics and ability to operate under extreme conditions. In the industrial machinery sector, synthetic lubricants are preferred for their thermal stability and extended service intervals, contributing to market growth.

**Market Players**

- Royal Dutch Shell PLC - Exxon Mobil Corporation - BP p.l.c. - TotalEnergies - Chevron Corporation - FUCHS - Idemitsu Kosan Co.,Ltd. - Pennzoil - Petroliam Nasional Berhad (PETRONAS) - Lukoil -The synthetic lubricants market is highly competitive, with key players constantly focusing on research and development activities to introduce innovative products and gain a competitive edge in the industry. Royal Dutch Shell PLC, Exxon Mobil Corporation, BP p.l.c., TotalEnergies, Chevron Corporation, FUCHS, Idemitsu Kosan Co.,Ltd., Pennzoil, Petroliam Nasional Berhad (PETRONAS), and Lukoil are among the prominent market players driving the growth of the synthetic lubricants market globally.

These market players are strategically investing in expanding their product portfolios, enhancing distribution networks, and establishing strong partnerships to strengthen their market presence. The focus on sustainability and environmental regulations is also shaping the strategies of these players, leading to the development of bio-based synthetic lubricants to meet the growing demand for eco-friendly products.

Market players are also focusing on mergers and acquisitions to expand their geographical reach and customer base. Collaborations with OEMs and industrial manufacturers are helping these companies to provide customized lubricant solutions that cater to specific industry needs. Additionally, investment in digitalization and advanced technologies is enabling market players to offer predictive maintenance solutions and optimize the performance of synthetic lubricants in various applications.

The global shift towards electric vehicles and the growing emphasis on energy efficiency are influencing market players to develop synthetic lubricants specifically designed for electric drivetrains. These specialized lubricants offer enhanced thermal stability, reduce friction, and contribute to the overall efficiency of electric vehicles. Moreover, the increasing demand for synthetic lubricants in emerging markets due to rapid industrialization and infrastructure development presents lucrative opportunities for market players to expand their business footprint.

In conclusion, the synthetic lubricants market is witnessing significant growth due to the rising demand for high-performance lubricants across various industries. Market players are continuously innovating and diversifying their product offerings to meet the evolving needs of customers and address sustainability concerns. With technological advancements and strategic collaborations, these players are expected to maintain their competitive positions and drive the growth of the synthetic lubricants market in**Segments**

- By Product Type: - Silicones - PAO (Poly Alpha Olefin) - Esters - PAG (Polyalkylene Glycol) - Group 3 - Phosphate Ester - Polyolester - Biolubes - Di-Basic Acid Ester - Others

- By Application: - Engine Oil - Hydraulic Fluids - Compressor Oil - Gear Oil - Greases - Refrigeration Oil - Transmission Fluids and Hydraulic Fluids - Turbine Oil - HTF - Metalworking Fluids - Process Oil - Marine Lubricants - General Industrial Oils - Others

- By End-Use Industry: - Construction - Mining - Metal Production - Cement Production - Power Generation - Automotive Manufacturing - Chemical - Marine - Oil and Gas - Food Processing - Textile - Others

Global Synthetic Lubricants Market, By Product, Application, End-Use Industry: Industry Trends and Forecast to 2023 to 2030

The global synthetic lubricants market is poised for steady growth, supported by the increasing demand for high-performance lubricants in various end-use industries. The market segmentation by product type showcases a diverse range of synthetic lubricants catering

Highlights of TOC:

Chapter 1: Market overview

Chapter 2: Global Synthetic Lubricants Market

Chapter 3: Regional analysis of the Global Synthetic Lubricants Market industry

Chapter 4: Synthetic Lubricants Market segmentation based on types and applications

Chapter 5: Revenue analysis based on types and applications

Chapter 6: Market share

Chapter 7: Competitive Landscape

Chapter 8: Drivers, Restraints, Challenges, and Opportunities

Chapter 9: Gross Margin and Price Analysis

Key Questions Answered with this Study

1) What makes Synthetic Lubricants Market feasible for long term investment?

2) Know value chain areas where players can create value?

3) Teritorry that may see steep rise in CAGR & Y-O-Y growth?

4) What geographic region would have better demand for product/services?

5) What opportunity emerging territory would offer to established and new entrants in Synthetic Lubricants Market?

6) Risk side analysis connected with service providers?

7) How influencing factors driving the demand of Synthetic Lubricants in next few years?

8) What is the impact analysis of various factors in the Global Synthetic Lubricants Market growth?

9) What strategies of big players help them acquire share in mature market?

10) How Technology and Customer-Centric Innovation is bringing big Change in Synthetic Lubricants Market?

Browse Trending Reports:

Tablet Kiosk Market Hereditary Testing Market Film Capacitor Market Risk-Based Monitoring Software Market Digital Dentistry Market Starch Blends Biodegradable Plastic Market Automotive Integrated Heating, Ventilation, and Air Conditioning (HVAC) System Market Purpura Treatment Market Candida Infections Drugs Market Latex Pillow Market Antifuse Field Programmable Gate Array Market Virtual Colonoscopy Software Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]

0 notes

Text

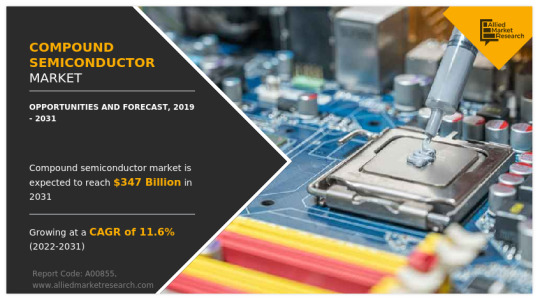

Compound Semiconductor Market Will See Strong Expansion Through 2031

Allied Market Research, titled, “Compound Semiconductor Market Size by Type, Product, Deposition Technology, and Application: Global Opportunity Analysis and Industry Forecast," The compound semiconductor market was valued at $90.7 billion in 2019, and is estimated to reach $347 billion by 2031, growing at a CAGR of 11.6% from 2022 to 2031.

Compound semiconductors are single-crystal semiconductor materials that comprise two or more elements. Some qualities change as two or more elements come together to create a single semiconductor crystal, while other properties are added. Rather than using silicon, which lacks this feature, in light-emitting diodes, compound semiconductor technology is preferred.

Key factors that drive the growth of the compound semiconductor market include an increase in demand for compound semiconductor epitaxial wafer in LED technology, emerging trends toward compound semiconductor wafers in the automotive industry, and the advantage of compound semiconductors over silicon-based technology. Compound semiconductor devices have three times the thermal conductivity and a breakdown electric field strength that is 10 times higher than those made of silicon. This characteristic reduces the complexity and expense of the device, enhancing reliability and enabling it to be used in a variety of high-voltage applications, including solar inverters, power supplies, and wind turbines. The market for compound semiconductor power devices is expanding due to the rising need for power electronics. Electrical power is effectively and efficiently controlled and converted due to power electronics. Compound semiconductor power devices are increasingly being used as a result of the expanding need for power electronics in sectors such as aircraft, medicine, and defense.

The compound semiconductor industry offers growth opportunities to the key players in the market. The technology used in 5G wireless base stations must combine efficiency, performance, and value. GaN solutions play a crucial role in providing these qualities. GaN-on-SiC delivers considerable gains in 5G base station performance and efficiency over Laterally Diffused Metal-Oxide Semiconductors (LDMOS). Greater thermal conductivity, strong robustness & reliability, improved efficiency at higher frequencies, and comparable performance in a lower-size MIMO array are further advantages of GaN-on-SiC. GaN is anticipated to enhance power amplifiers for all network transmission cells (micro, macro, pico, and femto/home routers), which might substantially impact the rollout of next-generation 5G technology.

The compound semiconductor market share is segmented on the basis of type, product, deposition technology, application, and region. By type, the market is categorized into III–V compound semiconductors, II–VI compound semiconductors, sapphire, IV–IV compound semiconductors, and others. The III–V compound semiconductors segment is further divided into gallium nitride (GAN), gallium phosphide (GAP), gallium arsenide (GAAS), indium phosphide (INP), and indium antimonide (INSB). The II–VI compound semiconductors segment is classified into cadmium selenide (CDSE), cadmium telluride (CDTE), and zinc selenide (ZNSE). The IV–IV compound semiconductors segment is bifurcated into silicon carbide (SIC) and silicon germanium (SIGE). The others segment includes aluminum gallium arsenide (ALGAAS), aluminum indium arsenide (ALINAS), aluminum gallium nitride (ALGAN), aluminum gallium phosphide (ALGAP), indium gallium nitride (INGAN), cadmium zinc telluride (CDZNTE), and mercury cadmium telluride (HGCDTE).

On the basis of product, the compound semiconductor market size is categorized into power semiconductors, transistors, integrated circuits (ICs), diodes & rectifiers, and others. The transistors segment is further classified into high electron mobility transistors (HEMTs), metal oxide semiconductor field effect transistors (MOSFETs), and metal-semiconductor field effect transistors (MESFETs). The integrated circuit is bifurcated into monolithic microwave integrated circuits (MMICs) and radio frequency integrated circuits (RFICs). The diode & rectifiers segment is further segmented into PIN diode, Zener diode, Schottky diode, and light emitting diode. By deposition technology, the market is segmented into chemical vapor deposition (CVD), molecular beam epitaxy (MBE), hydride vapor phase epitaxy (HVPE), ammonothermal, liquid phase epitaxy (LPE), atomic layer deposition (ALD), and others.

On the basis of applications, the compound semiconductor market analysis is segregated into IT & telecom, industrial and energy & power, aerospace & defense, automotive, consumer electronics, and healthcare. IT & telecom is further segmented into signal amplifiers & switching systems, satellite communication applications, radar applications, and RF. Aerospace & defense is classified into combat vehicles, ships & vessels, and microwave radiation. Industrial and energy & power are further segmented into wind turbines and wind power systems. Consumer electronics is further segmented into inverters, LED lighting, and switch-mode consumer power supply systems. The automotive segment is further divided into electric vehicles & hybrid electric vehicles, automotive braking systems, rail traction, and automobile motor drives. The healthcare segment is further bifurcated into implantable medical devices and biomedical electronics.

Region-wise, the compound semiconductor market trends are analyzed across North America (the U.S., Canada, and Mexico), Europe (UK, Germany, France, and the rest of Europe), Asia-Pacific (China, Japan, India, Australia, and the rest of the Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa).

KEY FINDINGS OF THE STUDY

The IV-IV compound semiconductor segment dominated the compound semiconductor market growth, in terms of revenue, and is expected to follow the same trend during the forecast period.

The power semiconductor segment was the highest revenue contributor to the market in 2021, and it is anticipated to grow at a significant CAGR during the forecast period.

The chemical vapor deposition and molecular beam epitaxy segments collectively accounted for around 42.7% market share in 2019, with the former constituting around 23.5% share

The IT and telecom segment was the highest revenue contributor to the market in 2021.

Asia-Pacific and North America collectively accounted for around 74.2% share in 2019, with the former constituting around 51.37% share.

The key players profiled in the report include Cree Inc., Infineon Technologies AG, Nichia Corporation, NXP Semiconductor N.V., Qorvo, Renesas Electronics Corporation, Samsung Electronics, STMicroelectronics NV, Taiwan Semiconductor Manufacturing Company Ltd., and Texas Instruments Inc. These players have adopted various strategies such as product launch, acquisition, partnership, and expansion to expand their foothold in the industry.

#semiconductors#Compound Semiconductor#electronics#battery#black sapphire cookie#black sapphire crk#star sapphire#transistor radio

0 notes

Text

Silicone Monomer Market, Global Outlook and Forecast 2025-2032

Silicone Monomer Market, Global Outlook and Forecast 2025-2032

The global Silicone Monomer Market continues to demonstrate robust expansion, with its valuation reaching USD 3.7 billion in 2024. According to the latest industry analysis, the market is projected to grow at a CAGR of 6.2%, reaching approximately USD 5.6 billion by 2032. This growth trajectory is primarily fueled by increasing applications in personal care, construction, and electronics, particularly in developing economies where demand for high-performance materials continues to accelerate.

Silicone monomers serve as the foundational building blocks for silicone polymers, offering exceptional thermal stability, chemical resistance, and flexibility. Their versatility makes them indispensable across industries transitioning toward advanced material solutions. As bio-based and specialty silicones gain prominence, manufacturers are increasingly investing in R&D to meet evolving regulatory and performance requirements.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229992/global-silicone-monomer-forecast-market-2023-2030-238

Market Overview & Regional Analysis

Asia-Pacific commands over 45% of global silicone monomer production, with China emerging as both the largest producer and consumer. The region's dominance stems from its massive manufacturing base for electronics, automotive components, and personal care products. Japan and South Korea contribute significantly through technological innovations in high-purity silicones for semiconductor applications.

North America maintains strong growth through its advanced healthcare and construction sectors, while Europe leads in environmental regulations driving sustainable silicone development. Emerging markets in Latin America and the Middle East show promising adoption rates, though infrastructure limitations currently constrain faster expansion.

Key Market Drivers and Opportunities

The market is propelled by three primary forces: the cosmetics industry's insatiable demand for silicone-based formulations (accounting for 28% of total consumption), the construction sector's need for durable sealants and adhesives (22% share), and the electronics industry's requirement for high-performance thermal management materials (19% share).

Significant opportunities exist in developing medical-grade silicones for implants and prosthetics, along with bio-based monomer alternatives to address environmental concerns. The electric vehicle revolution also presents new avenues for silicone applications in battery components and thermal interface materials.

Challenges & Restraints

The industry faces headwinds from fluctuating silicon metal prices (the key raw material), increasingly stringent environmental regulations on chlorosilane production, and the technical complexity of manufacturing high-purity monomers for electronics applications. Trade tensions and regional supply chain disruptions have further complicated market dynamics in recent years.

Competition from alternative materials in certain applications and the capital-intensive nature of production facility upgrades present additional hurdles for market participants.

Market Segmentation by Type

Methyltrichlorosilane

Trimethylchlorosilane

Methyldichlorosilane

Dimethyldichlorosilane

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229992/global-silicone-monomer-forecast-market-2023-2030-238

Market Segmentation by Application

Cosmetics & Personal Care

Silicone Rubber Production

Construction Materials

Electronics

Healthcare

Others

Market Segmentation and Key Players

Dow Corning

Momentive

Wacker Chemie

Shin-Etsu Chemical

Elkem Silicones

KCC Corporation

Dongyue Group

Hoshine Silicon

Wynca Group

Sanyou Silicon

Zhejiang XinAn Chemical

Tangshan Sanyou

Hubei Xingfa

Luxi Chemical

Jiangsu Hongda

Report Scope

This report provides a comprehensive analysis of the global silicone monomer market from 2024 to 2032, featuring:

Market size estimates and growth projections

Detailed segmentation by product type and application

Regional market analysis and country-level insights

Competitive landscape and market share analysis

Technology trends and innovation landscape

Regulatory framework and impact analysis

The study incorporates extensive primary research with industry stakeholders, supplemented by rigorous analysis of secondary data sources. Our methodology combines bottom-up and top-down approaches to ensure accuracy and reliability of market estimates.

Get Full Report Here: https://www.24chemicalresearch.com/reports/229992/global-silicone-monomer-forecast-market-2023-2030-238

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

0 notes

Text

Spin Rinse Dryer Market set to hit $7.8 billion by 2035

Industry revenue for Spin Rinse Dryer is estimated to rise to $7.8 billion by 2035 from $4.3 billion of 2024. The revenue growth of market players is expected to average at 5.6% annually for the period 2024 to 2035.

Spin Rinse Dryer is critical across several key applications including wafer cleaning, chip manufacturing, metal coating and pharmaceuticals packaging. The report unwinds growth & revenue expansion opportunities at Spin Rinse Dryer’s End User Type, Capacity, Technology and Energy Efficiency including industry revenue forecast.

Industry Leadership and Competitive Landscape

The Spin Rinse Dryer market is characterized by intense competition, with a number of leading players such as Silicon Valley Technology Corporation, MEI Wet Processing Systems and Services, SEMY Engineering, Modutek Corporation, JST Manufacturing, K.C.Tech, ACM Technologies, Silicon Valley Microelectronics, MEI Wet Processing, AXUS Technology, Li-Tek Corporation and OAI Systems.

Detailed Analysis - https://datastringconsulting.com/industry-analysis/spin-rinse-dryer-market-research-report

The Spin Rinse Dryer market is projected to expand substantially, driven by rising demand in semiconductor industry and technological advancements. This growth is expected to be further supported by Industry trends like Pursuit for Efficiency in Industrial Applications.

Moreover, the key opportunities, such as integration and automation in industrial spaces, energy efficient models and compact, portable and multi-purpose spin rinse dryers, are anticipated to create revenue pockets in major demand hubs including U.S., China, Germany, India and Japan.

Regional Shifts and Evolving Supply Chains

North America and Europe are the two most active and leading regions in the market. With challenges like high cost of equipment and stringent energy consumption regulations, Spin Rinse Dryer market’s supply chain from raw material sourcing / component creation & assembly / distribution & logistics to end user s is expected to evolve & expand further; and industry players will make strategic advancement in emerging markets including India, Brazil and Indonesia for revenue diversification and TAM expansion.

About DataString Consulting

DataString Consulting offers a complete range of market research and business intelligence solutions for both B2C and B2B markets all under one roof. We offer bespoke market research projects designed to meet the specific strategic objectives of the business. DataString’s leadership team has more than 30 years of combined experience in Market & business research and strategy advisory across the world. DataString Consulting’s data aggregators and Industry experts monitor high growth segments within more than 15 industries on an ongoing basis.

DataString Consulting is a professional market research company which aims at providing all the market & business research solutions under one roof. Get the right insights for your goals with our unique approach to market research and precisely tailored solutions. We offer services in strategy consulting, comprehensive opportunity assessment across various sectors, and solution-oriented approaches to solve business problems.

0 notes

Text

Silicon Metal Prices in 2025: What’s Happening and Why It Matters

The Silicon Metal price trend in 2025 is something a lot of industries are watching closely. Silicon metal is a refined form of silicon, mostly used in making aluminum alloys, solar panels, electronics, and silicones. It’s not the same as the raw material used in sand or rocks it’s much purer and more valuable for manufacturing. In 2025, prices for silicon metal are moving with a mix of global demand shifts, energy prices, and production levels. After a few years of ups and downs, the market is now showing signs of steady but cautious growth. Buyers, producers, and investors are all trying to read where it’s headed next.

To get a 30-day free trial, you need to submit your query and enter '30-day free trial' when submitting the details below.

👉 👉 👉 Please Submit Your Query for Silicon Metal Price Trend, forecast and market analysis: https://www.price-watch.ai/contact/

How the Market Is Shaping Up in 2025

So far in 2025, the market for silicon metal has been relatively balanced. The price hasn’t seen any wild jumps like during the pandemic years, but it’s still reacting to changes in demand and electricity costs. Since making silicon metal requires a lot of energy, especially electricity, any changes in power prices can affect how much it costs to produce. This is especially true in countries like China, which is the world’s largest producer. The country’s energy policies and production limits play a huge role in shaping global prices. On the demand side, countries increasing their clean energy capacity and electronics manufacturing are pushing the need for high-quality silicon metal.

Global Demand, Market Size, and Industry Growth

In terms of size, the silicon metal market is valued in the billions and is expected to grow steadily. Forecasts show a CAGR of about 5% to 6% over the next few years. One of the main drivers is the rise in renewable energy, especially solar power, where silicon metal is used to make solar-grade polysilicon. Another big area is aluminum alloys. These are widely used in automotive and aerospace sectors because they’re strong and lightweight — and silicon metal helps improve those properties. More electric vehicles, lighter aircraft, and solar panel installations mean more silicon metal is needed globally.

What’s Causing Price Changes in 2025

The main factor influencing prices in 2025 is energy cost. Since smelting silicon metal is energy-intensive, spikes in electricity prices — or even power restrictions — can reduce production and drive prices up. Another reason is environmental regulation. Many countries are now putting limits on carbon emissions and pollution, especially from heavy industries like mining and smelting. This has forced some producers to slow down or upgrade their systems, which has slightly tightened the supply. On the flip side, improved supply chain logistics compared to previous years has helped keep the market from getting too volatile.

Supply Chain, Production, and Market Players

Silicon metal supply is dominated by a few countries. China is by far the largest producer, followed by places like Brazil, Norway, and the U.S. In 2025, many producers are adjusting their operations to be more energy-efficient and environmentally friendly. Companies like Elkem, Ferroglobe, and Hoshine Silicon are among the major global players. These producers are not just selling more volume — they’re also focusing on better quality grades of silicon metal, especially those suitable for electronics and solar applications. On the buyer side, big manufacturers in semiconductors, solar, and automotive are securing long-term contracts to avoid price swings.

What’s Going On in Different Regions

Region-wise, Asia-Pacific remains the largest market — mainly because of China’s role in both supply and demand. India is also growing fast as it builds out solar energy and electronics manufacturing. In Europe, demand is focused more on green energy and automotive, and the EU is trying to localize more production to reduce reliance on imports. In North America, the market is being driven by tech and clean energy goals, but supply depends a lot on imports. Some local production is ramping up to reduce this dependency, but it will take time to become fully self-reliant.

Industry Challenges and Market Risks

Even though demand is growing, the silicon metal industry has some challenges to deal with in 2025. One big one is environmental pressure. Making silicon metal is not easy on the planet — it takes a lot of energy and emits greenhouse gases. Governments are now tightening environmental rules, which could push up production costs or limit output. Another issue is trade policy. Import tariffs, anti-dumping duties, and export restrictions can affect how silicon metal moves around the world. Finally, because the market depends heavily on a few big suppliers, any local disruption can quickly become a global issue.

Future Outlook and Forecast for 2025 and Beyond

Looking at the rest of 2025 and beyond, silicon metal prices are expected to stay stable or rise slightly, depending on how well supply keeps up with growing demand. If energy prices remain under control and environmental regulations don’t cause major production slowdowns, prices will likely remain manageable. But if there are disruptions — like factory closures or power rationing the market could tighten and push prices upward. Long-term, the outlook is positive, especially because silicon metal is crucial for the green energy transition. Solar panels, electric vehicles, and energy-efficient buildings all depend on it, so demand is only expected to grow. To know more visit PriceWatch Today.

0 notes

Text

2025 Global Pharmaceutical Processing Seals Market: Forecast, Growth Drivers, And Challenges

The global Pharmaceutical Processing Seals Market is poised for remarkable expansion, with its size valued at USD 2.55 billion in 2023 and projected to reach USD 6.05 billion by 2032, according to the latest industry analysis. The market is expected to grow at a compound annual growth rate (CAGR) of 10.11% over the forecast period of 2024–2032.

Get Free Sample Report on Pharmaceutical Processing Seals Market

Pharmaceutical processing seals are integral components used in the manufacturing and packaging of drugs and medications. These seals ensure product integrity, contamination-free environments, and compliance with strict industry regulations. As pharmaceutical companies strive for higher efficiency, quality assurance, and sustainability, the demand for high-performance sealing solutions continues to surge globally.

Key Growth Drivers

One of the key factors driving this rapid growth is the increasing investment in pharmaceutical manufacturing facilities. The post-COVID era has seen a significant global shift towards bolstering healthcare infrastructure, increasing vaccine and drug production, and establishing robust supply chains. As a result, the demand for reliable sealing solutions that can withstand complex processing environments has grown substantially.

In addition, the rising incidence of chronic diseases and the growing elderly population worldwide are accelerating the need for pharmaceuticals. This, in turn, increases demand for efficient processing equipment and components, including seals that comply with strict hygienic and safety regulations. Technological advancements in sealing materials—such as high-grade elastomers and PTFE (polytetrafluoroethylene)—are also contributing to market expansion, offering better resistance to extreme temperatures, chemicals, and sterilization processes.

Key Segments

By Material

Metal

Rubber

Silicone

Polymer/Elastomer

Other Materials

By Product

O-rings

Gaskets

Lip Seals

D Seals

Other Products

Challenges and Opportunities

Despite the optimistic growth outlook, the pharmaceutical processing seals market faces several challenges. The fluctuating cost of raw materials and the complexities involved in manufacturing seals that comply with varying global regulations can hamper profitability and slow down production timelines.

Nonetheless, the market offers substantial opportunities for innovation. Companies are increasingly focusing on sustainability and the development of eco-friendly, long-lasting sealing materials. Additionally, the integration of smart manufacturing and automation technologies in pharmaceutical plants is expected to fuel demand for seals that can accommodate high-speed operations with minimal maintenance requirements.

The emergence of personalized medicine and biologics also opens up new avenues for sealing technology, as these drugs often require highly specialized equipment and processing conditions. Seals used in such environments must meet even stricter purity, safety, and performance standards—offering new challenges and growth opportunities for manufacturers.

Key Players and Their Products in the Pharmaceutical Processing Seals Market

Flowserve Corporation – Valves, O-rings, Gaskets, Mechanical Seals

Morgan Advanced Materials PLC – Sealing Rings, Graphite Seals, High-Performance Gaskets

Trelleborg AB – O-rings, Gaskets, Lip Seals, Diaphragms

Garlock – Gaskets, Diaphragms, Compression Packings

Saint-Gobain S.A. – O-rings, Tubing Seals, Polymer Seals

Parker Hannifin Corporation – O-rings, Gaskets, Lip Seals, Metal Seals

IDEX Corporation – O-rings, Peristaltic Pump Seals, Sanitary Seals

James Walker – O-rings, Elastomer Seals, Gaskets

Freudenberg Group – O-rings, Diaphragms, Lip Seals, PTFE Seals

John Crane – Mechanical Seals, O-rings, Gaskets

Outlook for 2024 and Beyond

Looking ahead, the pharmaceutical processing seals market is expected to witness continuous innovation and consolidation. The increasing adoption of Industry 4.0 technologies, combined with growing regulatory focus on product safety and quality, will drive the evolution of advanced sealing solutions.

Make Enquiry about Pharmaceutical Processing Seals Market

The period from 2024 to 2032 represents a transformative phase for the market, with demand being propelled not only by rising pharmaceutical production but also by heightened expectations for operational excellence, safety, and sustainability.

Conclusion

In summary, the pharmaceutical processing seals market is entering an exciting phase of growth and innovation. With a projected market size of USD 6.05 billion by 2032 and a CAGR of 10.11%, the industry presents abundant opportunities for companies willing to adapt to emerging technologies, evolving regulations, and changing customer needs. As pharmaceutical manufacturers gear up for the future, the role of high-quality sealing solutions will remain more critical than ever before.

About US

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President Of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Pharmaceutical Processing Seals Market#Pharmaceutical Processing Seals Market Trend#Pharmaceutical Processing Seals Market Share#Pharmaceutical Processing Seals Market Growth#Pharmaceutical Processing Seals Market.

0 notes

Text

Global Copper Nickel Silicon Rod and Wire Market: Key Developments and Forecast Insights by 2025-2032

Global Copper Nickel Silicon Rod and Wire Market is experiencing steady expansion, driven by growing demand across high-performance electrical and industrial applications. Valued at USD 1.45 billion in 2024, the market is projected to grow at a CAGR of 5.8% through 2032. This growth trajectory reflects increasing adoption in connectors, welding electrodes, and precision engineering components where superior conductivity and corrosion resistance are critical.

Copper Nickel Silicon alloys offer exceptional mechanical strength and thermal stability, making them indispensable in harsh operating environments. Manufacturers are prioritizing these materials as industries transition toward more durable and efficient conductive solutions, particularly in aerospace and automotive electrification initiatives.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/291813/global-copper-nickel-silicon-rod-wire-market-2025-527

Market Overview & Regional Analysis

Asia-Pacific commands over 45% of global production capacity, with Japan and China spearheading technological innovation in alloy formulations. The region's dominance stems from robust electronics manufacturing ecosystems and government support for advanced material research. Meanwhile, North America remains a key innovation hub, where manufacturers focus on high-specification alloys for defense and renewable energy applications.

Europe's market benefits from stringent industrial standards driving premium alloy adoption, particularly in automotive and marine applications. Emerging economies in Latin America and Africa present untapped potential, though limited local production capabilities currently constrain market penetration in these regions.

Key Market Drivers and Opportunities

Three primary forces are reshaping the industry landscape: electrification trends in transportation, miniaturization of electronic components, and rising demand for corrosion-resistant industrial materials. The automotive sector's shift toward electric vehicles has significantly increased demand for high-reliability connectors and busbars made from these alloys.