Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by finprocounsulting and here's what we found interesting.

Average Info

Notes Per Post

0

Likes Per Post

0

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

3 days

Number of Posts By Type

Text

17

Last Seen Tumblr Blogs

Fun Fact

Post activity is at the highest at 4:00 pm EDT; notes peak at 10:00 pm EDT.

Text

At Finpro Consulting, our DIP IFRS programs are led by experts who make global standards easy to understand and apply. Because great learning starts with great mentorship.Contact Us Now:-084214 38047

#GuruPurnima2025#DIPIFRS#IFRSTraining#LearnFromExperts#GlobalAccounting#FinanceProfessionals#OfflineLearning#OnlineLearning#RecordedSessions#AccountingCareer#MentorshipMatters#GuruPurnimaSpecial#FinanceLearning#TrainWithTheBest

0 notes

Text

Get the latest and most comprehensive Diploma in IFRS (ACCA DipIFR) study material to prepare confidently for your upcoming exams. Our study kit includes updated notes, practice questions, revision summaries, and past exam papers with solutions—perfect for self-study or revision. ✅ Covers entire ACCA DipIFR syllabus ✅ Updated as per latest IFRS standards ✅ Instant digital access or courier delivery ✅ Ideal for June & December exam sessions Boost your exam success rate with expert-curated IFRS content. 📞 Contact us today to get your material!:- +91 8421438047

#diploma in ifrs#accounting#dipifrs#dipifr course#ifrs#ifrs online classes#finpro consulting#finproconsulting#diplomainifrs#acca

0 notes

Text

Advance your career with FinPro’s IFRS Certification tailored for Chartered Accountants. Gain global recognition, enhance your finance skills, and open international career opportunities—right from India. Enroll now to upskill for success! Contact US Now:- +91 8421438047

#FinPro#IFRSCertification#GlobalRecognition#CharteredAccountant#FinanceProfessionals#UpskillIndia#CareerInFinance#CAIndia#GlobalAccountant#AccountingStandards#FinanceCareerGrowth#StudyIFRS

0 notes

Text

IFRS 13: Fair Value Measurement – Part 2

In our previous blog– IFRS 13: Fair Value Measurement- Part 1, we discussed on the definition of fair value and key aspects of which management requires to consider while determining fair value under IFRS 13. Fair value is an exit price, thus while measuring fair value one should consider the price of such asset or a liability on the basis of its units (standalone or within group like CGU) and its characteristics, price in a principal market or most advantageous market, price in hypothetical transaction between market participants & the price to take exit from that asset or a liability or group. We have discussed these concepts with the help of suitable examples.

In this blog, we will further discuss the few more concepts required for fair value measurement viz. factors to consider for a non-financial asset, valuation techniques and hierarchy of information to be used while determining FV. We know that fair value is not an entity specific measure but is market participants’ perception. All these concepts ensure that an exit price is based on market participants’ assumptions and entity-specific factors are not considered while measuring fair value.

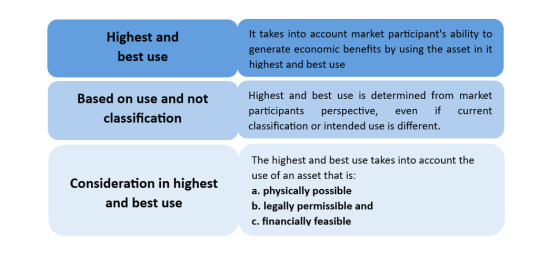

Considerations for non-financial asset (PPE, investment property etc.)

Generally, financial assets do not have alternative use because they have specific contractual terms and can have a different use only if the contractual terms of the instruments are changed. However, non- financial assets viz. PPE, investment property etc. do not have specific contractual use and can be used for multiple purposes.

Fair value is a market-based measurement, it is measured using the assumptions that market participants would use when pricing the asset. For e.g., an entity’s intention to hold an intangible asset or to use it defensively to protect its exiting intangible asset or otherwise is not relevant when measuring the fair value of that asset. Thus, fair valuation in the case of such non-financial assets often requires looking for the highest and best use by its market participants and that will be the reference point to evaluate fair value of such non-financial assets.

Fair value shall always be based on the market participant’s perspective and never be entity specific. The concept of highest and best use makes the non-financial asset separate from any specific entity who would like to use such asset in their own specific purposes which may or may not be its best use.

If market or other factors do not suggest different use by market participants that maximises assets value, then fair value should be based on the asset’s current use.

Example 1

An entity XYZ bought some land which is intended to be used for business purposes. However, the entity now wants to sell this piece of land at its fair value. One has to evaluate all possible uses of this land before determining its fair value. The land could be used to make a commercial place, which could be more in value as compared to when it is used for business purposes. The commercial place value would be considered its highest and best use if the same is allowed in its near locations and condition.

Example 2 – Potential use as Highest and Best Use

ABC Ltd owns a property, which comprises land with an old warehouse on it. It has been determined that the land could be redeveloped into a leisure park. The land’s market value would be higher if redeveloped than the market value under its current use. ABC Ltd is unclear about whether the investment property’s fair value should be based on the market value of the property (land and warehouse) under its current use, or the land’s potential market value if the leisure park redevelopment occurred.

The property’s fair value should be based on the land’s market value for its potential use. The ‘highest and best use’ is the most appropriate model for fair value. Under this approach, the property’s existing-use value is not the only basis considered. Fair value is the highest value, determined from market evidence, by considering any other use that is physically possible, legally permissible and financially feasible.

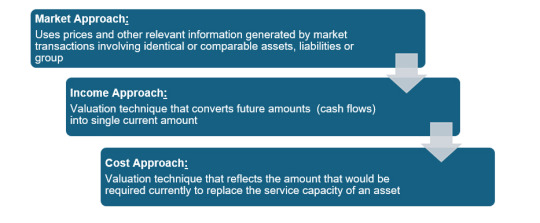

Valuation techniques – approaches for arriving at the price

An entity shall use valuation techniques that are:

appropriate in the circumstances and

for which sufficient data are available to measure fair value,

maximising the use of relevant observable inputs and minimising the use of unobservable inputs

Three main approaches for measuring fair value are:

NOTES –

It is worth noting that in case of availability of quoted prices which are being used in an active market, there is no need to consider any other valuation approach further.

The standard requires and allows using one or combination of more than one approach to measure any fair value.

Selecting an appropriate approach is matter of judgment and based on the available inputs related to the asset / liability.

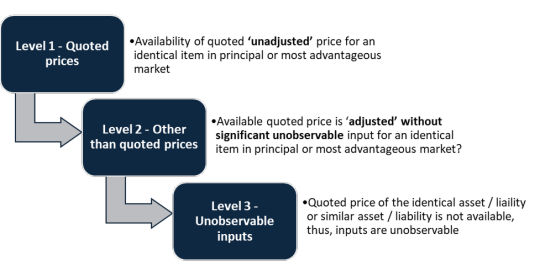

Fair value hierarchy

Valuation techniques used to measure fair value shall maximize the use of relevant observable inputs and minimize the use of unobservable inputs.

Observable Inputs: Inputs that are developed using market data, such as publicly available information about actual events or transactions, and that reflect the assumptions that market participants would use when pricing the asset or liability.

Unobservable Inputs: Inputs for which market data are not available and that are developed using the best information available about the assumptions that market participants would use when pricing the asset or liability.

Example 3

If a market participant would take into account the effect of a restriction on the sale of an asset when estimating the price for the asset, an entity would adjust the quoted price to reflect the effect of that restriction. If that quoted price is a Level 2 input and the adjustment is an unobservable input that is significant to the entire measurement, the measurement would be categorised within Level 3 of the fair value hierarchy.

Example 4

An entity is holding investment which is quoted in BSE, India and NYSE, USA. However, significant activities are being done at BSE only. The fair value of the investment would be referenced to the quoted price at BSE India, which is Level 1 fair value – direct quoted price with no adjustments.

Example 5

Receive-fixed, pay-variable interest rate swap based on a yield curve denominated in a foreign currency. It requires rate for 11 years can be established using extrapolation or some other techniques which is based on 10 years’ available rates of swap. The fair value of 11 years so derived would-be Level 2 fair value.

Example 6 – Cash-generating unit

A Level 3 input would be a financial forecast (e.g. of cash flows or profit or loss) developed using the entity’s own data, if there is no reasonably available information that indicates usage of different assumptions by market participants.

We hope this blog helps you to understand the important concepts to arrive at the price which is considered to be a market-based measure i.e. FV by considering the highest and best use for non-financial assets, applying appropriate approach for valuation and using fair value hierarchy.

Thank you for reading! For more simplified insights on IFRS, fair value measurement, and other accounting standards, follow our blog and stay updated.

Other IFRS-related blogs:

#ifrs#accounting#dipifr course#dipifrs#finpro consulting#diploma in ifrs#ifrs online classes#diplomainifrs#acca#finproconsulting

0 notes

Text

IFRS 13: Fair Value Measurement – Part 2

In our previous blog– IFRS 13: Fair Value Measurement- Part 1, we discussed on the definition of fair value and key aspects of which management requires to consider while determining fair value under IFRS 13. Fair value is an exit price, thus while measuring fair value one should consider the price of such asset or a liability on the basis of its units (standalone or within group like CGU) and…

View On WordPress

#dipifr training#Diploma in IFRS#ifrs certification courses#ifrs certification pune#ifrs course in pune#ifrs training#IFRS Training in India#indian accounting#Indian Accounting Standard#online ifrs course

0 notes

Text

The time for action is NOW. You have postponed enough; it's time to hit play on your success story. Whether it's a new certification, skill upgrade, or career leap, FinPro Consulting is here to make it happen. Register today and start building the future you deserve! Contact Us now;- 84214 38047

#RegisterNow#TakeAction#CareerGoals#SuccessMindset#FinProConsulting#FutureReady#InvestInYourself#NoMoreExcuses#UnlockYourPotential

0 notes

Text

ACCA DipIFR Online Certification by Industry Experts

Elevate your finance career by becoming an IFRS specialist. Join our comprehensive ACCA DipIFR online course, designed and taught by practicing Chartered Accountants and industry experts with years of real-world IFRS implementation experience. Our structured program is focused on one thing: helping you pass the DipIFR exam on your first attempt.

Why Choose Us? ✅ Live Interactive Classes: Learn directly from experts, not just from pre-recorded videos. ✅ Exam-Focused Approach: We cover the entire syllabus with a focus on exam questions and case studies. ✅ Practical Knowledge: Go beyond theory with real-world examples from seasoned professionals. ✅ Comprehensive Mock Exams: Get exam-ready with tests that simulate the actual DipIFR paper. ✅ Dedicated Doubt-Clearing Sessions: Get all your questions answered. ✅ Flexible Weekend/Weekday Batches

Perfect for: CAs, ACCAs, Finance Managers, Auditors, and Accounting Professionals.

Enroll in our upcoming batch and take the next step in your global finance career. ➡️ Request a FREE Demo Class & Course Brochure! Contact Us now:- +91 8421438047

#diploma in ifrs#accounting#dipifr course#dipifrs#ifrs online classes#finpro consulting#ifrs#finproconsulting#diplomainifrs#acca

0 notes

Text

Let IFRS certification be your ultimate passport to international work opportunities! Equip yourself with the globally recognized standard in financial reporting and open doors worldwide. Contact us Now;-84214 38047

#IFRS#InternationalOpportunities#GlobalFinance#CareerBoost#FinProConsulting#FinanceEducation#WorkAbroad#CFO#Accountant#FutureProofYourCareer

0 notes

Text

In our previous blog, we discussed ACCA DipIFR exam utility interface & answer writing tips which will help students to get comfortable with CBE interface and to be familiar with the examination pattern and face it with confidence.

0 notes

Text

In our previous blog, we discussed ACCA DipIFR exam utility interface & answer writing tips which will help students to get comfortable with CBE interface and to be familiar with the examination pattern and face it with confidence.

#diploma in ifrs#accounting#dipifrs#dipifr course#ifrs#finpro consulting#diplomainifrs#finproconsulting#ifrs online classes#acca

0 notes

Text

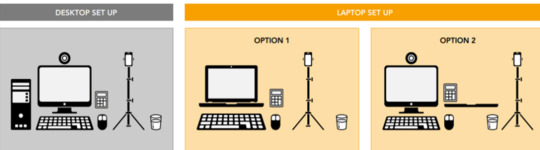

ACCA DipIFR Remote Exam: Requirement, Set-up & Tips

In our previous blog, we discussed ACCA DipIFR exam utility interface & answer writing tips which will help students to get comfortable with CBE interface and to be familiar with the examination pattern and face it with confidence.

This blog is especially for the students who chose Remote examination session i.e., who would appear from home or office instead of centre-based examination. This blog will guide you about technical requirements of the allowed devices and necessary care to be taken before and during the remote examination session.

System Requirements:

Operating System

• Windows 11 and 10 (64-bit) – (excluding ‘S Mode’) • macOS 13 and above – (excluding beta versions)

Note: • Mac OS, starting with Mojave, now requires permission from the user to allow any hardware access to an application, which includes OnVUE (proctorapp). Candidates should be prompted to allow this application • Windows Operating Systems must pass Genuine Windows Validation.

Unsupported operating systems

• Windows 8/8.1, Windows 7, Windows XP, and Windows Vista • Linux/Unix and Chrome based Operating Systems

Firewall

• Corporate firewalls should be avoided as they often cause this delivery method to fail. • VPNs and proxies should not be used. • We recommend testing on a personal computer. Work computers generally have more restrictions that may prevent successful delivery.

RAM Required

Recommended Minimum RAM of 4 GB or more

Display

Minimum Resolution: 1024 x 768 in 16-bit col Recommended Resolution: 1920 x 1080 or higher in 32-bit color • If using an external monitor, you must close your laptop and use an external keyboard, mouse, and webcam. • Multiple monitors are forbidden. • Touch screens are strictly forbidden.

Webcam

• The webcam may be internal or external. It must be forward-facing and at eye level to ensure your head and shoulders are visible within the webcam. • The webcam must remain in front of you and cannot be placed at an angle. • Webcam filters are not allowed (for example, Apple’s ‘Reactions’). • Webcam must have a minimum resolution of 640x480 @ 10 fps.

Note: • Mobile phones are strictly prohibited as a webcam for exam delivery. • Mac OS users may need to allow OnVUE within their System Preferences: Security & Privacy: Privacy settings for camera & microphone.

Speakers and microphone

Speakers: • Speakers must be built-in or wired. • Bluetooth speakers or the use of headphones* as speakers are not allowed. Headphones: • Headphones and headsets are not allowed unless explicitly approved by your test sponsor. • If allowed, headphones must be wired – Bluetooth are not allowed.

Browser settings

Internet Cookies must be enabled.

Device

All tablets are strictly prohibited, unless they have a physical keyboard and meet the operating system requirements mentioned earlier.

Power

Make sure you are connected to a power source before starting your exam to avoid draining your battery during the exam.

Internet Browser

The newest versions of Microsoft Edge, Safari, Chrome, and Firefox, for web registrations or downloading the secure browser.

Internet Connection

• For better performance, a reliable and stable connection speed of 12 Mbps download and 3 Mbps upload required. • We recommend testing on a wired network as opposed to a wireless network. • If testing from home, ask others within the household to avoid internet use during your exam session.

We strongly recommend using equipment that meets or exceeds the Recommended Specifications. The minimum requirements will change periodically based on the needs of exam sponsors.

Mobile phone: You may have the option to use your mobile phone to complete the check-in process. The mobile must meet the following requirements:

• Android (11+, Chrome) or IOS (15+, Safari) operating systems • A functioning camera with a stable internet connection

A mobile phone is used only for completing admission steps and must not be used during the exam. After completing the check-in steps, please place the mobile phone where it is not accessible to you during the exam. As a reminder, phones are a prohibited item and should not be within your reach or visible to you while sitting in front of your computer.

Pre-exam requirements

Passing the Mandatory system test

• You MUST pass mandatory system test prior to your check-in for exam. • When taking the test, use same device and the same location you we’ll use on exam day. • Make sure your last test run is a pass, so that you are eligible for all post-exam options. • Go to Exam Planner & hit the Run System Test button.

Practice using the scratch pad

Remember, you cannot use scratch paper for remote exam session. So, it’s important to get used to using the scratch pad on the Practice Platform before your live exam.

Exam set-up

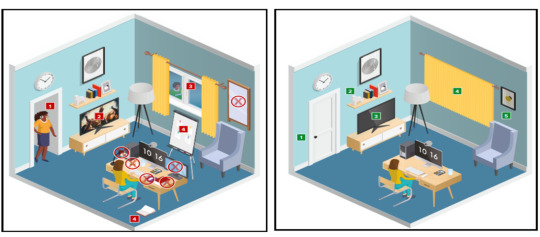

Your room setup

You will be under exam conditions and monitored by an invigilator throughout. Make sure below conditions are being followed: • A private and quite room with solid walls and doors. • No other person can be visible or heard for full duration of exam. • Use curtains or blinds to cover windows if anyone can be seen through them. • Switch all other unnecessary electrical equipment off. • Refer below images to have an idea about ideal exam environment.

Prohibited Permitted

Your desk setup

Your desk must be setup in a way that meets the rules and regulations of the exam: • No scrap paper• Only one monitor • A glass/bottle of water with label removed permitted • No headphones / earbuds / earphones • No watches

The check-in process

• Check in to your exam by going the exam planner and click launch exam button. • You can launch your exam 30 minutes prior your scheduled time. • If you are more than 15 minutes late you will miss your exam attempt and be marked as Absent.

Using your mobile phone:

• You may use your mobile phone during the check-in process – On-screen instruction will guide you.• You’ll be asked to take and upload photos of your exam environment, yourself and your ID. • Once completed this process place your mobile phone on silent and out of arm’s reach. • Do not use your mobile phone for any other purpose during exam (exception if invigilator calls you) • Taking photos of your screen or making calls during the exam is strictly prohibited.

Under exam conditions:

In addition to the desk/room requirements you should be aware that the following is also prohibited:

• Talking aloud during your exam. • People being audible outside your room. • Leaving the exam early – DO NOT end your exam early, you must stay supervised for the full-time duration.

Contacting the invigilator

• To start a chat with your invigilator, select the chat button. • Your invigilator will be with you as soon as they are available. • Unlikely they can assist you, but you should inform your invigilator if you are experiencing any technical difficulties. • You must inform your invigilator if you wish to use your permitted bathroom break.

Bathroom breaks

You can take one bathroom break during your exam of up to 5 minutes: • Notify your invigilator when you are leaving and returning from bathroom break. • You do not have to wait for the invigilator to give you their permission before taking your bathroom break. • The exam timing will continue to run – if you exceed 5 minutes your exam may be terminated.

Post-exam options: In the event of technical issue disrupting your exam, you may wish to use post-exam options which can be accessed on exam planner or under Contact Us on ACCA’s website.

Minimise the risk of the technical issue by: • Performing your equipment and connectivity test. • Accessing troubleshooting resources.

Using post exam options

To use rebook or withdrawal option you must have: • attempted to check-in your exam • experienced a technical issue impacting your ability to complete exam.

Additional withdrawal eligibility criteria

• The mandatory system test must be taken ahead of each exam session. • Student must have passed the mandatory system test in their last attempt prior to checking in for your exam.

Make sure that your device / other equipment’s are compatible as per the provided requirements and you are availed with the environment requisite for the exam purpose. Everyone should make sure to follow fair practices during exam to avoid any disqualification or disciplinary action.

We hope, this blog about ACCA DipIFR Remote Exam Requirement, Set-up & Tips shall assist in making the necessary arrangements.

Further, please watch video related to the remote examination on the below link: https://youtube.com/playlist?list=PLRYOefFr48S0apGK6f0kw0sX7fC6uSzsx&feature=shared

Best wishes from Team FinPro!

#finproconsulting#diploma in ifrs#accounting#dipifrs#ifrs#ifrs online classes#finpro consulting#dipifr course#diplomainifrs#acca

0 notes

Text

ACCA DipIFR Remote Exam: Requirement, Set-up & Tips

In our previous blog, we discussed ACCA DipIFR exam utility interface & answer writing tips which will help students to get comfortable with CBE interface and to be familiar with the examination pattern and face it with confidence. This blog is especially for the students who chose Remote examination session i.e., who would appear from home or office instead of centre-based examination. This…

View On WordPress

#dipifr training#Diploma in IFRS#ifrs certification courses#ifrs course in pune#ifrs training#IFRS Training in India#indian accounting#Indian Accounting Standard#online ifrs course

0 notes

Text

Nothing makes us prouder than seeing our students thrive and achieve their goals. This amazing feedback fuels our passion to keep delivering top-notch education. Ready to write your own success story? Contact Us Now:-84214 38047

#StudentSuccess#Testimonial#HappyLearners#FinProConsulting#CareerGoals#EducationExcellence#FutureLeaders#SuccessStories

0 notes

Text

Our IFRS training equips you to adapt and thrive. Register Now! Contct Us Now:-+91 8421438047

0 notes

Text

Examinations are set for June 5th & 6th, 2025

Here's what you need to know:

Format: 3 hours 15 minutes, 100 marks total (50% to pass). No MCQs!

Questions: Four compulsory 25-mark questions. Expect consolidation in Q1, with detailed scenario-based IFRS case studies for Q2-4 (numerical answers need explanations!).

Action: Don't forget to download your exam docket via your ACCA login!

Ready to ace it? FinPro's got you covered!

#ACCA#DipIFR#IFRSEmExams#FinProConsulting#FinanceProfessionals#ExamPrep#Accounting#IFRS#June2025#StudyTips#ComputerBasedExam#FinancialReporting#CareerGoals#Auckland

0 notes

Text

The ACCA Diploma in International Financial Reporting (Dip-IFRS) is a globally recognized qualification, where the syllabus is rich and practical, however, many students find the mode of examination (Computer Based Examination – CBE) and time pressure to be challenging hurdles. Further, per the examiners’ report over past many years, it is an observation of examination team that frequently students lack in understanding the question or what is expected in the answer. Also, students do not explain their numeric answers adequately.

#accounting#dipifr course#dipifrs#ifrs online classes#ifrs#finpro consulting#diplomainifrs#diploma in ifrs#careergrowth#finproconsulting

0 notes

Text

ACCA Dip-IFRS Exam Structure & Time Management Tips

The ACCA Diploma in International Financial Reporting (Dip-IFRS) is a globally recognized qualification, where the syllabus is rich and practical, however, many students find the mode of examination (Computer Based Examination – CBE) and time pressure to be challenging hurdles. Further, per the examiners’ report over past many years, it is an observation of examination team that frequently students lack in understanding the question or what is expected in the answer. Also, students do not explain their numeric answers adequately.

To overcome the above hurdles or challenges, first important step is to understand the exam structure or structure of the question paper. Second step is to understand how the examination utility looks on a computer machine and how to navigate through the various exhibits in question scenario and how to answer without losing time in navigation. The third most important and last step is to practice on such platform in order to reduce time required to solve the question paper. In this blog, we’ll focus on the first step to overcome the hurdles i.e. understanding structure of the exam.

Let us break down and analyse the exam paper pattern and try to understand what ACCA on a broad level expects from the students of Diploma IFRS examination. This will help students to plan their revision based on the expectations of examiner and more importantly to plan 3 hours of examination. Student has 3 hours and 15 minutes at his disposal. Student can use it as per his own convenience for reading questions and writing answers. However, our suggestion is to keep total 15 minutes for reading and planning the question paper and another 10 minutes as a buffer. Thus, out of 195 minutes, remaining 170 minutes can be utilised to solve the question paper. Thus, 1.7 minutes per mark can be used as a very broad level guideline for the time management. However, considering the level of difficulty of a particular question, this time may be revised.

Exam consists of 100 marks with 4 questions, each attracting 25 marks. All questions are compulsory, and no alternative is available for any question.

Question One

This question will involve the preparation of a consolidated financial statement, as examinable within the syllabus. This question will often include issues that will need to be addressed prior to performing the consolidation procedures for e.g. procedures mentioned in IFRS 3 – Business Combinations viz. calculation of purchase consideration, NCI, goodwill etc. Generally, these issues will relate to the financial statements of the parent entities prior to their consolidation. A key purpose of this question is to assess technical consolidation skills. However, the question may also require candidates to adjust for transactions that have been incorrectly or incompletely accounted for in the financial statements of group entities (usually the parent entity). In order to make these adjustments candidates will need to apply the provisions of relevant IFRS Standards. In Question one, the focus will primarily on application rather than explanation. No explanations are expected in the question number

Question Two

This question will often be related to a scenario in which questions arise regarding the appropriate accounting treatment and/or disclosure of a range of issues. In this question candidates may be asked to comment on management’s chosen accounting treatment and determine a more appropriate one, based on circumstances described in the question. This question will also contain an ethical and professional component related to the accounting treatment that is being examined.

Question Three

This question will usually deal with one or two IFRS Standards in some detail. Such a question would require candidates to describe key features of the IFRS Standard and apply it to two or more situations that the question describes. In contrast with Question 1, there will be a limited number of marks available for technical preparation of financial statements extracts and the majority of marks are available for identifying and quantifying the appropriate adjustments. However, it is expected that students can explain how these adjustments will affect line items in the financial statements.

Question Four

This question will often present candidates with a scenario or a range of scenarios for which the correct financial reporting treatment is complex or uncertain. Often the question will place the candidate in a ‘real-life’ role, for example chief accountant reporting to the chief executive officer or senior accountant supervising an assistant. The question frequently requires candidates to address a series of questions that have been posed by the other party in the scenario. The question will often ask candidates to present a reply or report that deals with the appropriate financial reporting of the issues raised in the scenario. The primary skill in this question is identifying and describing the issues, rather than the detailed computation of numbers. Questions 2, 3 and 4

will be more about identification and explanation of financial reporting issues rather than of financial statements preparation. Practicing these questions from the past exam questions is very good exam preparation as generally candidates find the narrative style questions more challenging than the numerical style of question one. These past papers continue to be relevant, but students should bear in mind that sometimes additional query or explanation of an additional IFRS Standard can be demanded.We hope knowing the ACCA Dip-IFRS exam structure will help you approach the exam with a clear plan. Understanding the types of questions, marks distribution, and how the paper is set will make it easier for you to focus on your study and manage your time during the exam.

Best wishes from Team FinPro!

Thank you for reading our blog, stay tuned for such insightful tips.

Thank you for reading our blog. Stay tuned for more such insightful tips. If you have any questions or need assistance, feel free to contact us.

#finproconsulting#diploma in ifrs#accounting#dipifr course#dipifrs#finpro consulting#ifrs#ifrs online classes#diplomainifrs#careergrowth

0 notes