#Budgeting and Financial Planning

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was named as a finalist in Lead411’s New York City Hot 125 in Aug 2010.

Text

Building Resilience: How Financial Stability Affects Mental Health

Written by Delvin In today’s fast-paced and uncertain world, financial stability plays a crucial role in our overall well-being. Beyond its tangible impact on our material possessions, financial stability also significantly influences our mental health and resilience. In this blog post, we will delve into the relationship between financial stability and mental health, exploring how building…

View On WordPress

#Budgeting and Financial Planning#Confidence#dailyprompt#Financial#Financial Literacy#Mental Health#Mental Wellness#Money Management#Multiple Income Streams#Personal Finance#Resilience#Self Care#Self Esteem#Stress Reduction#The Link Between Financial Stability and Mental Health

1 note

·

View note

Text

my girlfriend is so fucking cute. we had a discussion on our finances bc we're moving in together in the next couple of months, and she fucking got horny from me talking about financial responsibility & my budgeting setup

#i have a really strict system from when i was living on a shoestring budget and it's still in place even now that i have a decent income#which means that when we were discussing how much we're both going to be putting into our shared account#i was very easily able to be like ok taxes are this much yearly; electricity and gas are this much per month; etc etc; therefore our total#costs are x; which means if we split that 50/50 and i pay the mortgage we both end up spending less than we do now#which means we can save xyz towards a new kitchen etc etc etc#(and she grew up financially insecure so it's v important to her that we're financially compatible in terms of having a budget)#vi tag#also!! with this plan we can finish paying off her student loans in like the next 5 years!!!!! which made her short circuit#bc for context: her mother never finished paying off her own college loans & dropped out bc she got pregnant so it's so important to my gf#to be able to be rid of that burden at some point#anyway tmi and tldr we're moving in together! and we've talked abt this before abstractly but now with actual numbers

14 notes

·

View notes

Text

to everyone whos struggling now.

#money management#rich girl#wealth#financialmanagement#financetips#budgeting#financial freedom#financial planning#personal finance#rich life#richwomen#expensive#millionaire#money

9 notes

·

View notes

Text

Listen to every episode of our podcast right here.

7 notes

·

View notes

Text

How to Budget Money That Actually Sticks: A Foolproof Guide

Did you know that emergency funds should account for three to six months of expenses?

Learning how to budget money effectively is the foundation for achieving this financial safety net. Yet, many of us struggle to create a monthly budget that actually sticks. One popular approach is the 50/30/20 budget, which allocates 50% of your income for needs, 30% for wants, and 20% for savings and debt repayment.

Consider this: a typical monthly budget might include $4,000 in take-home pay with $2,540 going to fixed expenses and $1,460 to variable expenses. However, the key to successful budgeting isn't just about creating these numbers—it's about making every dollar work for you.

Surprisingly, budgeting to zero (where income minus expenses equals zero) ensures all your money has a purpose. Additionally, making smart choices like choosing generic brands over name brands can save you 8-9% per grocery trip.

In this guide, we'll walk you through a foolproof system for how to budget and save money that actually works. Whether you're struggling with how to budget better or looking to create an effective budget for the first time, we've got you covered with practical steps that will transform your financial habits for good.

Step 1: Know Your Real Income

The foundation of any successful budget begins with a clear understanding of how much money you really have to work with. Many budgets fail because people use the wrong income figure from the start.

Understand net vs gross income

When examining your paycheck, you'll notice two distinctly different numbers. Your gross income is the total amount you earn before any deductions are taken out. This is the larger figure that represents your full salary or hourly wage multiplied by hours worked. Meanwhile, your net income is what actually lands in your bank account after taxes and other deductions.

For example, if you earn $15 per hour and work 20 hours in a week, your gross income would be $300. Nevertheless, your take-home pay will be significantly lower after various withholdings.

These deductions typically include:

Federal income tax (10% to 37% depending on income bracket)

Social Security (6.2%)

Medicare (1.45%)

State and local taxes (varies by location)

Health insurance premiums

Retirement contributions

In fact, someone with a $50,000 gross annual salary might only take home between $38,942 and $34,290 after deductions—a difference of up to $15,710 per year or $1,309 monthly. This substantial gap explains why choosing the correct income figure for your budget is crucial.

Account for irregular or freelance income

For the growing number of freelancers, gig workers, and commission-based employees (over 73 million in the U.S. alone), budgeting presents unique challenges. Unlike salaried employees, your income likely fluctuates month to month.

When planning your budget with irregular income, the safest approach is to use your lowest expected monthly earnings. Look at your income over the past six months and identify your lowest-earning month. This conservative approach ensures you can always cover essential expenses, even during lean periods.

Furthermore, if you're a freelancer, remember to set aside approximately 25-30% of your income for taxes. This includes not only income tax but also self-employment tax, which amounts to 15.3% of your net business profit for Social Security and Medicare. Unlike traditional employees whose employers pay half this tax, self-employed individuals bear the full burden.

Why net income matters for budgeting

Budgeting with gross income is a recipe for disaster. When you plan spending based on your before-tax income, you essentially "double count" money that's already committed elsewhere. Consequently, you might believe you have more available funds than you actually do.

For most people, budgeting based on net income proves most effective. This approach offers several advantages:

First, it's simpler since you don't need to manually track payroll deductions. Second, it's more practical because you're planning with money that actually hits your account.

Additionally, understanding the relationship between your gross and net income helps you make informed decisions about tax withholdings, retirement contributions, and other financial choices that impact your take-home pay.

Essentially, your monthly budget should reflect what you can realistically spend and save, not theoretical amounts that never reach your wallet. This fundamental principle forms the cornerstone of any budgeting method that truly sticks.

Step 2: Track and Categorize Your Spending

After understanding your income, the next critical step in building a budget that sticks is getting a clear picture of where your money actually goes. Tracking your spending gives you power over your finances rather than wondering where your paycheck disappeared to.

Use bank statements or budgeting apps

Initially, you'll need to choose a tracking method that works for your lifestyle. Review your bank and credit card statements from the past three to six months to gain insight into your spending history. This provides a solid baseline of data to work with.

While manual tracking works for some, budgeting apps offer powerful automation that simplifies the process. These apps connect with your financial accounts, track spending, and categorize expenses automatically, giving you a comprehensive view of your money habits. Some popular options include:

Monarch: Offers two budgeting strategies - a simple "flex" view with three buckets or detailed category budgeting

YNAB: Uses zero-based budgeting to help you allocate every dollar

Good budget: Based on the envelope system for those who prefer planning over tracking

Pocket Guard: Shows how much you have left after necessities, bills, and goals

For couples, Honeydue allows both partners to sync accounts and set monthly limits with alerts when approaching them.

Separate fixed and variable expenses

Understanding the difference between fixed and variable expenses is fundamental to effective budget management. Fixed expenses remain largely the same each month and typically include:

Rent or mortgage payments

Car payments

Insurance premiums

Childcare costs

Subscription services

Variable expenses fluctuate based on consumption and personal choices. These include:

Groceries

Dining out

Entertainment

Clothing

Utilities

Fixed expenses are generally easier to budget for since they're predictable, while variable expenses require more attention. A helpful approach is to budget for essential expenses first, whether they're fixed or variable. For essential variable expenses like groceries, review spending over the past six months to estimate an appropriate monthly allocation.

Spot spending patterns and leaks

Regular monitoring of your finances is crucial for identifying trends and making adjustments. Most people find it takes about three months of consistent budgeting to truly understand their spending patterns.

To spot "budget leaks" – small, often overlooked expenses that add up significantly – examine your transactions with a fine-tooth comb. Look beyond broad categories and amounts to understand the context behind each purchase. Common leaks include:

Forgotten subscriptions and memberships (streaming services, apps, gym memberships)

Frequent small purchases (daily coffee stops, impulse buys)

Multiple grocery trips due to poor meal planning

Food delivery services exceeding reasonable budget allocations

Banking fees and service charges

One financial coach discovered a client was spending approximately $200 monthly at Starbucks – amounting to $2,400 annually – without realizing the magnitude until tracking. Similarly, someone might consistently underestimate regular expenses like tolls, creating monthly shortfalls of $100-200.

Setting regular financial check-ins – monthly or quarterly – helps maintain awareness and allows for timely adjustments to your budget. This consistent attention to your spending habits forms the foundation for all the budgeting methods we'll explore in later steps.

Step 3: Set Clear and Realistic Financial Goals

Setting financial goals creates purpose behind your budgeting efforts. Without clear objectives, it's easy to overspend or miss financial opportunities that could improve your future.

Short-term vs long-term goals

Financial goals typically fall into different timeframes, each requiring specific planning approaches:

Short-term goals can be achieved within one year and focus on building financial stability. These include creating a monthly budget, building an emergency fund of 3-6 months of expenses, paying off high-interest credit card debt, or saving for a vacation.

Long-term goals take five years or more to accomplish and typically involve securing your financial independence. Examples include planning for retirement, paying off a mortgage, creating generational wealth, or establishing an estate plan.

Between these lie mid-term goals (1-5 years), such as saving for a home down payment or financing study abroad expenses.

According to research, time is your biggest advantage for long-term financial planning—the earlier you start saving for retirement, the less financial stress you'll face later.

Include savings and debt in your goals

Effective budgeting requires balancing both savings and debt repayment objectives. When setting your financial hierarchy, consider these priorities:

Emergency fund (your first priority before investing)

High-interest debt reduction

Retirement savings

Other financial goals

Debt management deserves special attention in your goals. The average American has approximately $96,371 in debt, including mortgages. Moreover, according to Experian, average consumer debt balances increased in 2023 with credit card, auto loans and mortgages all rising.

For tackling debt, consider strategies like the "snowball method" (paying smallest debts first) or the "avalanche method" (tackling highest-interest debts first).

How goals help you stick to a budget

Creating SMART financial goals—Specific, Measurable, Achievable, Relevant, and Time-bound—significantly increases your likelihood of budgeting success.

Instead of vague intentions like "save more money," a SMART goal might be: "I will save $10,000 for a house down payment within 18 months by setting aside $555 monthly".

Written financial goals particularly boost commitment—a Charles Schwab survey found that 96% of people with written financial plans felt "very confident" about reaching their financial goals.

Additionally, breaking larger goals into smaller, manageable steps makes them less overwhelming and easier to track. For instance, if you need to save $15,000 for an emergency fund, start with smaller targets of $500 or $1,000.

Altogether, clear financial goals provide direction for your budget, help you prioritize spending decisions, and create accountability through regular progress assessments.

Step 4: Choose a Budgeting Method That Works

Now that you've analyzed your income and spending patterns, it's time to select a budgeting strategy that fits your financial style. The right method can transform how you manage money and help create habits that last.

50/30/20 rule

This straightforward approach divides your after-tax income into three categories: 50% for necessities like rent and groceries, 30% for wants such as dining out, and 20% toward savings and debt repayment. For instance, with a monthly income of $3,500, you would allocate $1,750 to needs, $1,050 to wants, and $700 to savings. The simplicity of this framework makes it ideal for beginners or those who prefer a less rigid budgeting style.

Zero-based budgeting

With zero-based budgeting (ZBB), you start from scratch each month, giving every dollar a specific purpose until your income minus expenses equals zero. Unlike traditional budgeting that only examines new expenditures, ZBB requires justification for both new and recurring expenses. This method often reveals unnecessary costs and helps prioritize activities that generate the most value. Although more time-intensive, it provides complete control over where every penny goes.

Envelope system

Originally a cash-based method, the envelope system involves dividing money into different categories (envelopes) for specific expenses. Once an envelope is empty, you stop spending in that category until the next budget period. The physical act of handling cash creates an emotional connection to your money, potentially reducing impulsive purchases. Today, apps like Good budget offer digital alternatives to physical cash envelopes, making this system more convenient while maintaining its benefits.

Pay-yourself-first method

This "reverse budgeting" approach prioritizes savings above all else. You immediately set aside a portion of your income for savings or investments before paying bills or discretionary spending. By automating transfers to retirement accounts or emergency funds, you ensure savings happen consistently rather than waiting to see what's left over. This method works well for those focused on long-term financial goals.

How to pick the right method for you

Choosing the most effective budgeting technique depends on your specific situation. Consider these factors:

Financial personality: Zero-based or envelope methods benefit those needing strict spending controls, whereas 50/30/20 offers more flexibility.

Time commitment: Zero-based budgeting demands more attention than automated systems like pay-yourself-first.

Financial goals: If building savings is your priority, the pay-yourself-first method might be most effective.

The best budget ultimately comes down to the one you'll actually follow.

Step 5: Adjust, Automate, and Review Regularly

Creating a budget is just the beginning—the key to financial success lies in proper implementation and maintenance. Consider these final yet critical steps that turn budgeting from a one-time activity into a sustainable financial habit.

Automate savings and bill payments

Having money automatically transferred to dedicated savings accounts supports virtually any financial goal. Even small monthly contributions add up significantly over time without requiring constant attention. First, prioritize automating bill payments to avoid late fees and penalty APRs that can suddenly increase interest rates.

For effective automation:

Link payment sources to bill payment services

Schedule regular transfers from checking to savings

Direct portions of paychecks directly to savings accounts

Perform brief monthly checks to ensure all deductions appear as expected

Cut back on non-essentials

Examine your recurring monthly expenses with a critical eye. Make a list of all subscriptions and honestly ask yourself: "Do I really need this?" and "Can I live without this?". Recurring payments often go unnoticed yet add up substantially.

Temporarily suspend services like gym memberships when not using them, or consider pausing public transportation accounts during periods when you're not commuting. Additionally, identify emotional spending triggers to prevent impulse purchases that derail your financial goals.

Review your budget monthly

Monthly check-ins help you catch discrepancies early before minor issues become significant problems. These reviews allow you to understand your financial habits without being overly critical of every small overspend. Look specifically for:

Forgotten or unnecessary recurring charges

Areas where you consistently over or under budget

Opportunities to adjust allocations based on changing priorities

Subsequently, conduct deeper quarterly reviews to assess bigger-picture trends and adjust long-term strategy.

Adapt to life changes

Budgets are living documents that need regular revision to stay relevant. Major life transitions—whether positive like a promotion or challenging like income reduction—require budgetary adjustments. When experiencing income increases, consider allocating half toward retirement and half toward general spending. Conversely, during income drops, review essential expenses and identify non-essential areas to reduce.

Conclusion

Budgeting effectively requires commitment and consistent effort, but the financial freedom it provides makes every step worthwhile. Throughout this guide, we've explored how understanding your net income creates a solid foundation for realistic planning. Additionally, tracking your spending reveals patterns that might surprise you and highlights areas where adjustments can make significant differences.

Setting clear financial goals gives purpose to your budget and transforms it from a restrictive exercise into a powerful tool for achieving what matters most to you. Whether you choose the flexibility of the 50/30/20 rule, the precision of zero-based budgeting, the tangibility of the envelope system, or the prioritization of the pay-yourself-first method, the best approach remains the one you'll actually follow.

Remember, your budget should adapt as your life changes. Major events such as promotions, relocations, or family changes will necessitate adjustments to your financial plan. Regular monthly reviews coupled with quarterly check-ins ensure your budget evolves alongside your life circumstances.

Financial success rarely happens by accident. People who achieve their money goals typically follow deliberate strategies and maintain consistent habits. Your budget serves as the roadmap guiding these daily decisions toward long-term prosperity.

Start small if you need to. Even implementing just one concept from this guide can significantly improve your financial situation. Afterward, you can gradually incorporate additional strategies as your confidence grows. The journey toward financial control happens one step at a time, and each positive choice builds momentum toward lasting change.

Above all, be patient with yourself. Budgeting mastery develops through practice, adjustment, and sometimes learning from missteps. The fact that you've s

ought out this information already puts you ahead of many who never take that first crucial step toward financial empowerment.

#self improvement#self care#planner#financial planning#budget#budget planning#home budget#professional development#artists on tumblr#art#home improvement#viral trends#trending#trend#viralpost#writers on tumblr

2 notes

·

View notes

Text

"We take pride in building lifelong relationships with our clients. The Xantias wealth management program ensures that we take the time to understand you, explain how we operate, and what you should expect. You can feel confident that we understand your values, objectives and individual circumstances. We specialise in strategies for legal, accounting, medical and dental professionals, and consulting senior executives."

#xantias financial management#financial advisors melbourne#finance and budgeting for men#financial experts#financial growth#financial planning#finance#investment advice#wealth management#cash flow#melbourne

2 notes

·

View notes

Text

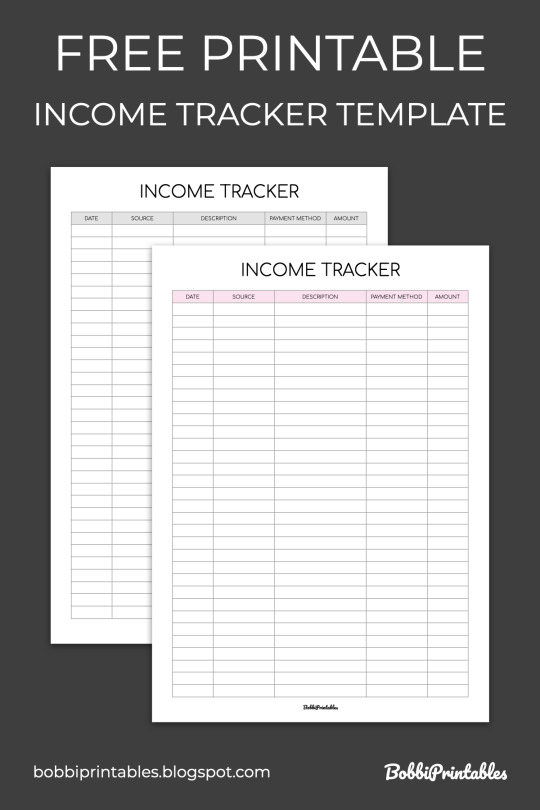

Free Printable Income Tracker Template

Download Here

#free printable#income tracker#budgeting#money management#personal finance#financial planning#printable template#free template

3 notes

·

View notes

Text

So this plumbing job is costing around $500. Have to empty my savings and go into serious overdraft to cover it

Of course I have unexpected plumbing expenses the same week we have to pay rent and Jon has to buy his bus pass. Of course I do

Coincidentally, today a friend offered me a cat-sitting job that would earn me enough to cover this cost! But. It is not until July lol

I may or may not make a fundraising post about this later. I need to think about things

I may be completely broke, but at least I will have a functioning kitchen again very soon

#we originally planned to do this part of the install ourselves#but when Dad came to help with the disconnections before the counter install we discovered more damage#stuff we didn't know how to fix ourselves. so this plumbing expense was unexpected and not in the original budget#oof#thought i could just get dad to do everything originally but. he's getting older. and plumbing was never his forte#he's more of a drywall and carpentry/woodwork specialist#my uncle who was a plumber passed away last summer... we miss you uncle tony#not just because you were good at plumbing and i could pay you in shortbread and tea#but that is a factor#sorry i'm just babbling now#mod post#plumbing#financial stuff#kitchen renovation#kitchen reno#the countertop saga

2 notes

·

View notes

Text

Listen, if I influence anyone to try self-experimentation, such as trying out regular sleep, or trying a multivitamin etc... and documenting it's impacts, I will consider that a win. Please don't hold back on account of seeing me get such mixed results, my body is very -very- very incredibly weird. Like multiple genetic mutations weird.

Other things I found useful for a time or might try again:

-Documenting what you eat at each meal to track potential triggers for symptoms

-Documenting your general mood and sleep quality daily to look for patterns

-Actually keeping a financial record even if you don't think it will change anything

-Tracking things like your blood pressure and heart rate

Like worst case scenario, you were right all along and now you have the recorded data to back it up.

#Now that I have the breathing space away from other people I am apparently impulsively trying one thing at a time to improve my health#and quality of life#only I am me#so I am going about it weirdly methodically and one thing at a time to control for variables as if that's my most basic instinct#first it was sleep#then we delved into budgeting and financial planning#then I fixed my sex-life#now It's multivitamins#At some point I will get to the actual downsizing part of organizing#soon#Getting on top of medical shit was in there too but it's an ongoing lengthy process

8 notes

·

View notes

Photo

Reducing debt is crucial for financial freedom, but the motivations behind it can be surprising. This article explores odd debt reduction reasons, from avoiding financial embarrassment to gaining the ability to invest, donate generously, and even vacation without post-trip debt. It also critiques traditional debt advice, highlighting the importance of balance—cutting expenses, but not at the cost of financial well-being. The key takeaway? No matter your reason, eliminating debt improves financial security and peace of mind. (¬‿¬)

https://www.canajunfinances.com/odd-debt-reduction-reasons/

(via Odd Debt Reduction Reasons)

3 notes

·

View notes

Text

Biblical Wisdom for Managing Money God's Way

Are you tired of feeling stressed about money every month, wondering if God actually cares about your financial struggles?

Money is one of the most talked-about topics in the Bible, with over 2,000 verses addressing finances, wealth, and possessions. This isn't because God is obsessed with money – it's because He knows how money affects our hearts, relationships, and spiritual lives. Jesus said, "Where your treasure is, there your heart will be also" (Matthew 6:21), revealing that our financial choices reflect our spiritual priorities.

The Bible presents a radically different approach to money than our culture promotes. While the world says "get all you can," God says "give all you can." While society preaches "you deserve it," Scripture teaches stewardship and contentment. While culture promotes debt as normal, the Bible warns that "the borrower is slave to the lender" (Proverbs 22:7).

Stewardship is the foundational principle of biblical money management. Everything we have belongs to God – our income, possessions, and even our ability to earn money are gifts from Him. First Chronicles 29:14 declares, "Everything comes from you, and we have given you only what comes from your hand." This perspective transforms how we view our finances from ownership to management.

Tithing, giving the first 10% of our income to God, establishes Him as Lord over our finances. Malachi 3:10 contains God's only recorded invitation to test Him: "Bring the whole tithe into the storehouse, that there may be food in my house. Test me in this," says the Lord Almighty, "and see if I will not throw open the floodgates of heaven and pour out so much blessing that there will not be room enough to store it."

Many Christians struggle with tithing because they feel they can't afford it. But the question isn't whether you can afford to tithe – it's whether you can afford not to. Tithing isn't about God needing your money; it's about you needing to trust God with your money. When you give first, you're declaring that God is your provider, not your paycheck.

Budgeting becomes an act of worship when done with biblical principles. Start with giving (tithe and offerings), then cover necessities (housing, food, transportation), then tackle debt, build savings, and finally enjoy discretionary spending. This order reflects biblical priorities and protects against impulse decisions that derail financial goals.

The Bible strongly discourages debt, especially consumer debt for wants rather than needs. Romans 13:8 instructs, "Let no debt remain outstanding, except the continuing debt to love one another." While some debt (like mortgages) may be necessary, the goal should always be freedom from financial bondage.

Contentment is perhaps the most challenging aspect of biblical money management in our consumer culture. First Timothy 6:6-8 teaches, "Godliness with contentment is great gain. For we brought nothing into the world, and we can take nothing out of it. But if we have food and clothing, we will be content with that." This doesn't mean living in poverty, but finding satisfaction in God's provision rather than constantly wanting more.

Building an emergency fund demonstrates wisdom and faith. Proverbs 21:20 says, "The wise store up choice food and olive oil, but fools gulp theirs down." Having 3-6 months of expenses saved provides peace of mind and prevents debt during unexpected circumstances.

Generosity should increase as God blesses you financially. Second Corinthians 9:7 reminds us that "God loves a cheerful giver." When you give joyfully and generously, you're reflecting God's character and participating in His work on earth.

Remember that God's definition of wealth isn't just monetary. True wealth includes health, relationships, peace, purpose, and eternal perspective. Many financially wealthy people are spiritually poor, while many with modest incomes are rich in faith, joy, and contentment.

#Christian Finances#Biblical Money Management#Christian Budgeting#Tithing#Christian Stewardship#Money And Faith#Christian Debt Freedom#Biblical Wealth#Christian Giving#Financial Stewardship#Christian Devotional#Money Stress#Christian Contentment#Biblical Wisdom#Christian Financial Planning#Faith And Money#Christian Generosity#Financial Freedom#Christian Lifestyle#Gods Provision#Christian Support#Biblical Principles#Money Management#Christian Encouragement#Financial Peace

1 note

·

View note

Text

Life Insurance Premium Calculator: Plan Smart, Secure Smarter

When planning for your family's financial future, choosing the Right Life Insurance Policy is essential, but understanding the premium cost is just as important. That’s where a Life Insurance Premium Calculator becomes a powerful tool. It helps you estimate how much you'll need to pay to get the life cover and benefits you desire.

In this article, we’ll explore what a life insurance premium calculator is, how it works, and why it’s vital when comparing the best life insurance policy options.

What is a Life Insurance Premium Calculator?

A Life Insurance Premium Calculator is an online tool that helps individuals estimate the premium they need to pay for a particular life insurance policy. It uses various parameters such as age, income, policy term, sum assured, and smoking habits to provide an accurate premium estimate.

This tool is especially helpful when comparing life insurance plans or determining affordability before making a financial commitment.

Why Use a Life Insurance Premium Calculator?

Using a premium calculator before buying a policy ensures you:

Avoid Under or Over Coverage

Understand Premium Variations Across Plans

Compare the Cost of Different Policy Terms

Evaluate the Impact of Riders/Add-ons

Make Informed Financial Decisions

How Does the Life Insurance Premium Calculator Work?

The calculator works by taking specific inputs from you and instantly generating a premium estimate based on your selected life insurance plan. Here's how:

Age – Younger individuals usually pay lower premiums.

Gender – Premium rates may vary based on gender; for example, females often have slightly lower premiums due to lower risk statistics.

Policy Term – The length of the coverage period affects the premium. Longer policy terms generally lead to higher premiums.

Sum Assured – This is the coverage amount you want. A higher sum assured means a higher premium.

Type of Policy – Whether it's Term Insurance, Whole Life Insurance, ULIP, Endowment, or Money-Back Plan—each type has different premium structures.

Smoking Habits – Smokers are considered high-risk, and hence pay higher premiums compared to non-smokers.

Riders/Add-ons – Adding extra benefits like Critical Illness Cover, Accidental Death Benefit, or Waiver of Premium increases the premium amount.

Benefits of Using a Life Insurance Premium Calculator

Let’s look at the key benefits of life insurance premium calculators:

✅ Quick Estimates: Get instant quotes without paperwork or waiting.

✅ Customizable Options: Modify variables to find the perfect plan.

✅ Informed Comparison: Compare multiple insurers and types of life insurance policies.

✅ Transparent Costing: No hidden charges or surprises.

✅ Time-Saving: Avoid agent consultations for basic premium insights.

Types of Life Insurance Policies You Can Calculate Premiums For

Before using a premium calculator, it’s important to know the types of life insurance policies commonly available:

1. Term Life Insurance

Pure protection plan offering high coverage at low premiums.

2. Whole Life Insurance

Covers your entire life (usually up to 99 or 100 years), with maturity or death benefit.

3. Endowment Plans

Offer savings along with life cover, ideal for long-term wealth creation.

4. Unit Linked Insurance Plans (ULIPs)

Market-linked plans that offer dual benefits of investment and insurance.

5. Money Back Policies

Provide periodic returns along with life cover.

Each of these policies can have different premium amounts, so the calculator helps you find what suits your budget and goals.

Features of Life Insurance Premium Calculators

User-Friendly Interface – Simple and easy to use; no financial expertise required.

2. Mobile-Friendly – Works smoothly on smartphones, so you can calculate premiums anytime, anywhere.

3. No Personal Details Needed – Most calculators give you premium estimates without asking for your phone number, email, or OTP.

4. Rider Comparison – You can add or remove riders like critical illness or accidental death benefit to see how they impact your premium.

5. Real-Time Calculation – Instantly generates accurate premium quotes so you can make quick and informed decisions.

Importance of Life Insurance in Financial Planning

Understanding the importance of life insurance is key before even calculating the premium. Life insurance:

Acts as income replacement for your family.

Helps cover outstanding debts, especially home loans.

Offers tax-saving benefits under Section 80C and 10(10D).

Helps build wealth or retirement corpus (in savings-based plans).

Offers peace of mind through financial security.

Using a life insurance premium calculator ensures that you can achieve all these benefits while staying within your budget.

How to Use an Online Life Insurance Calculator

Most insurance providers and aggregators offer free online calculators. Here’s a step-by-step guide:

Visit the insurer's official website.

Go to the Life Insurance Plans section.

Click on “Calculate Premium.”

Enter your age, annual income, policy term, and sum assured.

Add any riders like critical illness or accidental death benefit.

Click “Calculate” to view your premium.

Now you can compare plans or tweak values to match your financial goals.

Tips for Choosing the Best Life Insurance Policy

To make the most of your premium calculation and plan selection, keep the following in mind:

Choose a plan based on your life stage (young, married, with kids, nearing retirement).

Opt for a sum assured that is at least 10–15 times your annual income.

Consider whole life insurance if you want long-term family protection.

Look for flexible plans with premium waiver and critical illness riders.

Always check claim settlement ratio and customer service of the insurer.

Final Thoughts

A Life Insurance Premium Calculator is a must-use tool when planning to buy a life insurance policy. It ensures you're not underinsured or overburdened by premium costs. Whether you’re exploring term insurance, whole life insurance, or investment-linked plans, calculating your premium first will give you the clarity and confidence to make the right choice.

With rising uncertainties, understanding the features of life insurance, and utilizing digital tools to find the best life insurance policy has become more important than ever. So don’t delay—use a premium calculator today and take the first step toward protecting your family’s future.

#life insurance#insurance calculator#life insurance premium calculator#term insurance#whole life insurance#insurance tips#financial planning#money matters#insurance policy#insurance advice#insurance quotes#online insurance#personal finance#insurance guide#budget planning#secure future#insurance for family#best life insurance#life goals#protect your future

1 note

·

View note

Text

#wealth#money management#budgeting#financial freedom#financetips#financialmanagement#financial planning#personal finance

2 notes

·

View notes

Text

fuck. someone stop me from buying dungeon meshi complete series in japanese off ebay

#fuck fuck fuck this is dire#okay no i csnt justify it#ok here's my plan. wait til the end of the month#wait til i do my budget snd see how many Financial Crimes i already committed this month

11 notes

·

View notes

Text

VB Abundance - Financial Advisory Services

VB Abundance guides you in building a balanced, resilient portfolio through effective asset allocation. By diversifying across asset classes like equities, bonds, and real estate, we help you reduce risk and enhance potential returns. Our team customizes your allocation strategy based on your goals, risk tolerance, and market trends. Trust VB Abundance to provide a secure, well-rounded approach to growing your wealth for long-term stability and success!

vb abundance - financial advisor - https://lnkd.in/grNDa3K5

If you want more details click here, https://vbabundance.com/ or call us +91 99430 18682.

Address : Ganapathy Complex, No. 104 - 1st Floor, AK Nagar, Saibaba Colony, Coimbatore - 11.

Map Location : https://lnkd.in/gSjkrkXd

asset allocation

#asset allocation#budgeting#finance#goal setting#investing#accounting#sales#ecommerce#financial planning#taxplanning

2 notes

·

View notes

Text

How to Create a Financial Plan for Your Business in 2025

Introduction

A strong financial foundation is the backbone of every successful business. Whether you’re launching a startup or running an established company, knowing how to create a financial plan for your business in 2025 is essential for growth, profitability, and long-term sustainability.

Why Business Financial Planning Is Crucial in 2025

The economic landscape continues to evolve in 2025, influenced by inflation, AI integration, shifting consumer behavior, and a dynamic labor market. That’s why small business financial strategy must be more proactive, data-driven, and flexible than ever before.

✅ Benefits of Financial Planning:

Set clear short- and long-term goals

Improve decision-making with real-time data

Secure funding and build investor confidence

Monitor and control spending

Minimize risks and prepare for emergencies

💡 A well-crafted financial plan is not just a document—it’s a living tool that guides every aspect of your business.

Step 1: Define Your Business Goals

Start by identifying your business goals for 2025. These should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

Examples:

Increase revenue by 20%

Launch a new product line in Q3

Reduce overhead by 15%

Expand into two new markets

🎯 Your goals will shape every part of your financial plan, from budgeting to forecasting.

Step 2: Analyze Your Current Financial Position

Before planning ahead, understand where you stand today. Collect and review key financial statements:

Balance Sheet – Shows assets, liabilities, and equity

Income Statement (Profit & Loss) – Shows revenue and expenses

Cash Flow Statement – Tracks how money moves in and out of your business

💡 Use this data to spot trends, identify problem areas, and evaluate performance over time.

Step 3: Create a Business Budget

Creating a business budget is one of the most important components of business financial planning. A solid budget helps you plan expenses, monitor profits, and prepare for seasonal fluctuations.

How to Create a Business Budget:

Estimate Revenue – Use past data and future projections

List Fixed Costs – Rent, salaries, insurance, subscriptions

List Variable Costs – Inventory, marketing, shipping

Include One-Time Expenses – Equipment purchases, legal fees

Set Aside Savings – Emergency fund or reserve account

💡 Review your budget monthly and adjust based on actual performance.

Step 4: Forecast Revenue and Expenses

A financial forecast helps you anticipate future income and expenses. It’s critical for small business financial strategy, especially when applying for loans or attracting investors.

Forecasting Tips:

Use 3–5 years of historical data (if available)

Factor in market conditions and industry trends

Consider best-case, worst-case, and most likely scenarios

Update quarterly based on actual results

📈 Your forecast should align with your growth strategy and guide spending decisions.

Step 5: Manage Cash Flow Effectively

Even profitable businesses can fail due to poor cash flow. Create a cash flow management plan to ensure you can cover operating expenses year-round.

Cash Flow Management Tips:

Invoice promptly and offer early payment discounts

Avoid unnecessary expenses or delays in collections

Use accounting software to monitor daily cash position

Keep at least 3 months’ worth of operating expenses in reserves

💡 Regularly reviewing cash flow ensures you're prepared for both opportunities and setbacks.

Step 6: Set KPIs and Financial Metrics

Use key performance indicators (KPIs) to track your financial health and measure success.

Important Financial KPIs:

Gross Profit Margin

Net Profit Margin

Operating Expense Ratio

Customer Acquisition Cost (CAC)

Return on Investment (ROI)

Current Ratio (liquidity)

📊 These metrics help you evaluate progress and adjust your business financial strategy as needed.

Step 7: Plan for Taxes and Legal Compliance

Don’t let taxes catch you off guard. Incorporate tax planning into your 2025 financial strategy.

Tax Planning Tips:

Work with a CPA or tax advisor

Track deductible expenses and tax credits

Pay quarterly estimated taxes

Maintain clean, accurate financial records

Understand changes in local, state, and federal tax laws

📝 Staying compliant saves money, avoids penalties, and simplifies tax season.

Step 8: Prepare for Funding and Investment

If you’re planning to raise capital in 2025, a professional financial plan is a must-have for lenders and investors.

Include in Your Funding Plan:

Business overview and executive summary

Detailed use of funds

Financial projections and KPIs

Exit strategy (if applicable)

💡 A credible financial plan boosts your chances of securing business funding or attracting partners.

Tools to Help You Create a Business Financial Plan

QuickBooks – Accounting and budgeting

LivePlan – Business plan and financial forecasting

Xero – Cash flow management and reporting

Excel or Google Sheets – Customizable templates

Wave – Free accounting and invoicing for small businesses

Common Financial Planning Mistakes to Avoid

🚫 Underestimating expenses 🚫 Not revisiting the plan regularly 🚫 Failing to separate business and personal finances 🚫 Skipping cash flow projections 🚫 Ignoring tax planning

✅ Review your financial plan at least quarterly and update as your business evolves.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include credit repair and passive income programs.

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - [email protected]

Final Thoughts: Build a Financial Roadmap to Thrive in 2025

Creating a financial plan isn’t just a good business practice—it’s your roadmap to profitability, growth, and resilience in 2025 and beyond. With economic uncertainty still on the horizon, now is the perfect time to refine your small business financial strategy.

✅ Set clear goals ✅ Build a smart, flexible budget ✅ Forecast and manage your finances with confidence

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include credit repair and passive income programs.

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - [email protected]

🎯 Ready to create your business budget and financial plan for 2025? Start today—and set your business up for long-term success.

Prestige Business Financial Services LLC

"Your One Stop Shop To All Your Personal And Business Funding Needs"

Website- https://prestigebusinessfinancialservices.com

Email - [email protected]

Phone- 1-800-622-0453

#business financial planning#small business financial strategy#create business budget#entrepreneur#personal finance#businessfunding#personal loans

1 note

·

View note