#Distributed Energy Storage System Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

If you dial 1-866-584-6757, you can leave an audio post for your followers.

Text

Advance Energy Storage Market Research Report Includes Dynamics Demands, Products, Types and Application 2017 – 2032

Overview of the Market:

providing efficient and reliable storage solutions for electricity generated from renewable and conventional sources. These storage systems enable the balancing of supply and demand, integration of intermittent renewable energy, grid stabilization, and optimization of energy usage. The global advanced energy storage systems market is expected to grow at a CAGR of 9% from 2023 to 2032.

Promising Growth and Demand: The advanced energy storage market has experienced significant growth in recent years, driven by several factors. Increasing renewable energy deployment, declining costs of storage technologies, and supportive government policies promoting clean energy and grid modernization have spurred the demand for advanced energy storage solutions. Additionally, the need for energy resilience, demand management, and peak shaving in industries, commercial buildings, and residential applications has further contributed to market growth.

Platform Type: The advanced energy storage market encompasses various platform types for energy storage:

Battery Energy Storage Systems (BESS): Battery-based energy storage systems are one of the most widely used platforms. They employ rechargeable batteries, such as lithium-ion, lead-acid, or flow batteries, to store and discharge electricity as needed.

Pumped Hydro Storage: Pumped hydro storage utilizes the gravitational potential energy of water by pumping it to a higher elevation during times of excess electricity and releasing it through turbines to generate electricity during peak demand periods.

Thermal Energy Storage: Thermal energy storage systems store and release thermal energy using materials such as molten salts or phase change materials. This technology is often utilized for heating, cooling, and industrial processes.

Flywheel Energy Storage: Flywheel systems store rotational energy in a spinning flywheel, which can be converted back into electricity when needed. They provide high-speed, short-duration energy storage.

Technology: Advanced energy storage systems employ various technologies to store and deliver electricity efficiently:

Lithium-ion Batteries: Lithium-ion batteries are the most common technology used in battery energy storage systems. They offer high energy density, long cycle life, and rapid response times.

Flow Batteries: Flow batteries use electrolyte solutions stored in external tanks to store and release energy. They offer scalability and long cycle life, making them suitable for large-scale applications.

Compressed Air Energy Storage (CAES): CAES systems compress air and store it in underground caverns or tanks. The stored air is then expanded through turbines to generate electricity during peak demand.

Thermal Storage Technologies: Thermal energy storage systems utilize materials with high specific heat capacity or phase change materials to store thermal energy for later use in heating or cooling applications.

End User Industry: The advanced energy storage market serves various end user industries, including:

Utilities and Grid Operators: Utilities and grid operators utilize advanced energy storage systems to optimize grid stability, manage peak demand, integrate renewable energy, and enhance grid resilience.

Commercial and Industrial Sectors: Commercial and industrial facilities deploy energy storage solutions to manage electricity costs, reduce peak demand charges, provide backup power, and optimize on-site renewable energy generation.

Residential Sector: Residential applications of advanced energy storage include residential solar systems with battery storage for self-consumption, backup power during outages, and demand management.

Scope:

The advanced energy storage market has a global scope, with increasing deployment in various regions. The market encompasses equipment manufacturers, system integrators, energy storage developers, and utilities. Market statistics, growth projections, and demand may vary across regions due to factors such as energy policies, market maturity, and renewable energy penetration.

The market's scope extends to various aspects, including technology advancements, cost reduction, grid integration, and energy management solutions. With the increasing need for clean energy, grid stability, and energy efficiency, the demand for advanced energy storage solutions is expected to grow, presenting opportunities for industry players.

In conclusion, the advanced energy storage market is experiencing promising growth globally. The adoption of advanced energy storage systems is driven by factors such as renewable energy integration, grid modernization, and the need for energy management and resilience. The market serves utilities, commercial, industrial, and residential sectors, utilizing technologies such as batteries, pumped hydro, thermal storage, and flywheels. As the world transitions towards a more sustainable energy future, the demand for advanced energy storage solutions is expected to increase, providing significant opportunities for industry participants in the global energy sector.

We recommend referring our Stringent datalytics firm, industry publications, and websites that specialize in providing market reports. These sources often offer comprehensive analysis, market trends, growth forecasts, competitive landscape, and other valuable insights into this market.

By visiting our website or contacting us directly, you can explore the availability of specific reports related to this market. These reports often require a purchase or subscription, but we provide comprehensive and in-depth information that can be valuable for businesses, investors, and individuals interested in this market.

“Remember to look for recent reports to ensure you have the most current and relevant information.”

Click Here, To Get Free Sample Report: https://stringentdatalytics.com/sample-request/solar-panel-recycling-management-market/11372/

Market Segmentations:

Global Solar Panel Recycling Management Market: By Company • First Solar • Envaris • REMA PV Systems • Darfon Electronics • Rinovasol • Chaoqiang Silicon Material • Suzhou Shangyunda Electronics • PV Recycling • Silcontel • Cellnex Energy • IG Solar Private Global Solar Panel Recycling Management Market: By Type • Monocrystalline cells • Polycrystalline cells Global Solar Panel Recycling Management Market: By Application • Industrial • Commercial • Utility • Others Global Solar Panel Recycling Management Market: Regional Analysis The regional analysis of the global Solar Panel Recycling Management market provides insights into the market's performance across different regions of the world. The analysis is based on recent and future trends and includes market forecast for the prediction period. The countries covered in the regional analysis of the Solar Panel Recycling Management market report are as follows: North America: The North America region includes the U.S., Canada, and Mexico. The U.S. is the largest market for Solar Panel Recycling Management in this region, followed by Canada and Mexico. The market growth in this region is primarily driven by the presence of key market players and the increasing demand for the product. Europe: The Europe region includes Germany, France, U.K., Russia, Italy, Spain, Turkey, Netherlands, Switzerland, Belgium, and Rest of Europe. Germany is the largest market for Solar Panel Recycling Management in this region, followed by the U.K. and France. The market growth in this region is driven by the increasing demand for the product in the automotive and aerospace sectors. Asia-Pacific: The Asia-Pacific region includes Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, China, Japan, India, South Korea, and Rest of Asia-Pacific. China is the largest market for Solar Panel Recycling Management in this region, followed by Japan and India. The market growth in this region is driven by the increasing adoption of the product in various end-use industries, such as automotive, aerospace, and construction. Middle East and Africa: The Middle East and Africa region includes Saudi Arabia, U.A.E, South Africa, Egypt, Israel, and Rest of Middle East and Africa. The market growth in this region is driven by the increasing demand for the product in the aerospace and defense sectors. South America: The South America region includes Argentina, Brazil, and Rest of South America. Brazil is the largest market for Solar Panel Recycling Management in this region, followed by Argentina. The market growth in this region is primarily driven by the increasing demand for the product in the automotive sector.

Visit Report Page for More Details: https://stringentdatalytics.com/reports/solar-panel-recycling-management-market/11372/

Reasons to Purchase Solar Panel Recycling Management Market Report:

Informed Decision-Making: A comprehensive market research report provides valuable insights and analysis of the district heating market, including market size, growth trends, competitive landscape, and key drivers and challenges. This information allows businesses to make informed decisions regarding investments, expansion strategies, and product development.

Market Understanding: Research reports offer a deep understanding of the district heating market, including its current state and future prospects. They provide an overview of market dynamics, such as industry trends, regulatory frameworks, and technological advancements, helping businesses identify opportunities and potential risks.

Competitive Analysis: Market research reports often include a competitive analysis, profiling key players in the district heating market. This analysis helps businesses understand their competitors' strategies, market share, and product offerings. It enables companies to benchmark themselves against industry leaders and identify areas for improvement or differentiation.

Market Entry and Expansion: For companies planning to enter the district heating market or expand their existing operations, a market research report provides crucial information about market saturation, customer preferences, and regional dynamics. It helps businesses identify viable market segments, target demographics, and potential growth areas.

Investment Opportunities: Market research reports highlight investment opportunities in the district heating market, such as emerging technologies, untapped regions, or niche markets. This information can assist investors in making informed decisions about capital allocation and portfolio diversification.

Risk Mitigation: By analyzing market trends, customer preferences, and regulatory frameworks, market research reports help businesses identify and mitigate potential risks and challenges. This proactive approach can minimize uncertainties and optimize decision-making processes.

Cost Savings: Investing in a market research report can potentially save businesses time and resources. Rather than conducting extensive primary research or relying on fragmented information sources, a comprehensive report consolidates relevant data, analysis, and insights in one place, making it a cost-effective solution.

Industry Benchmarking: Market research reports provide benchmarks and performance indicators that allow businesses to compare their performance with industry standards. This evaluation helps companies identify areas where they excel or lag behind, facilitating strategic improvements and enhancing their competitive position.

Long-Term Planning: A global market research report offers a forward-looking perspective on the district heating market, including growth projections, emerging trends, and future opportunities. This insight aids businesses in long-term planning, resource allocation, and adapting their strategies to changing market dynamics.

Credibility and Authority: Market research reports are typically prepared by industry experts, analysts, and research firms with in-depth knowledge of the subject matter. Purchasing a reputable report ensures access to reliable and credible information, enhancing decision-making processes and providing confidence to stakeholders.

In general, market research studies offer companies and organisations useful data that can aid in making decisions and maintaining competitiveness in their industry. They can offer a strong basis for decision-making, strategy formulation, and company planning.

About US:

Stringent Datalytics offers both custom and syndicated market research reports. Custom market research reports are tailored to a specific client's needs and requirements. These reports provide unique insights into a particular industry or market segment and can help businesses make informed decisions about their strategies and operations.

Syndicated market research reports, on the other hand, are pre-existing reports that are available for purchase by multiple clients. These reports are often produced on a regular basis, such as annually or quarterly, and cover a broad range of industries and market segments. Syndicated reports provide clients with insights into industry trends, market sizes, and competitive landscapes. By offering both custom and syndicated reports, Stringent Datalytics can provide clients with a range of market research solutions that can be customized to their specific needs

Contact US:

Stringent Datalytics

Contact No - +1 346 666 6655

Email Id - [email protected]

Web - https://stringentdatalytics.com/

#Advance Energy Storage Market#Renewable Energy#Battery Technology#Grid Integration#Energy Storage Systems#Lithium-ion Batteries#Energy Management#Sustainable Power#Energy Transition#Smart Grid#Electric Vehicles#Power Electronics#Distributed Energy Resources#Energy Efficiency#Carbon Emissions#Grid Stability#Solar Energy#Wind Energy#Energy Policy#Energy Storage Capacity#Energy Infrastructure#Energy Market Trends#Energy Storage Solutions#Microgrids#Demand Response#Energy Storage Technologies#Energy Storage Applications#Energy Storage Investment#Energy Storage Economics#Energy Storage Challenges

0 notes

Text

The battery system includes six battery containers, three inverter/transformer containers, and one distribution point container, providing a total electricity capacity of up to 20 MWh. This would be enough to power one electric car for 115,000 km, one household washing machine for 19,000 wash cycles or nearly 3,000 households for one day, Utilitas Wind said.

"Alternative sources of electricity generation such as wind and solar are weather-dependent. If there is strong wind during a particular period, this is likely to be the case throughout the region. This results in a surplus of electricity generated. The opposite is true when there is no wind, when there is a shortfall, but the system we have in place gives us a great advantage - the ability to store 'excess' electricity to make up for when there is a shortfall," said Urbanovičs(..)

P.S. History has been made in Latvia! The Russians' attempt to blackmail the energy market of the Baltic states has suffered a major defeat in Latvia. The first battery of industrial scale will be connected to the energy system...

Utilitas Wind is part of the Estonian energy company OÜ Utilitas. OÜ Utilitas Group develops and manages wind farms in all three Baltic countries and has invested €70 million in the development of the Targale wind farm. Utilitas Wind has an installed capacity of 78.8 MW in Latvia from autumn 2022, generating 171 000 MWh of electricity in 2023, enough to cover the electricity consumption of 56 000 households. In early 2024, Latvenergo AS acquired the Telšiai wind farm project in Lithuania, with a capacity of 124MW, built by Utilitas Wind Ltd(..)

#Latvia#energy independence#energy safety#battery#wind power#renewable energy#russian defeat#Ventspils#Baltic States#Estonia#Utilitas Wind#trump's defeat

8 notes

·

View notes

Text

Lithium Mining Market Report 2025 – Growth, Trends & Demand

Introduction

The global lithium mining market is undergoing rapid expansion, propelled by the surging demand for lithium-ion batteries in electric vehicles (EVs), renewable energy storage systems, and consumer electronics. Market projections estimate the industry will reach USD 18.6 billion by 2032, with a CAGR of 14.3% from 2024 to 2032. This growth is driven by the accelerating adoption of clean energy solutions, government policies supporting EV production, and advancements in battery technologies.

As lithium demand intensifies, the industry faces challenges such as limited high-grade lithium reserves, environmental concerns, and geopolitical risks. However, sustainable lithium extraction (SLE) technologies, including direct lithium extraction (DLE) and eco-friendly mining processes, present significant opportunities for innovation, ensuring long-term market stability.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40617-global-lithium-mining-market

Lithium Mining Market Dynamics

Key Drivers

Expanding EV Market – The electric vehicle industry remains the largest consumer of lithium, with global automakers scaling up production to meet carbon neutrality goals.

Renewable Energy Storage – Grid-scale battery storage projects are growing, increasing lithium demand for stabilizing intermittent renewable energy sources.

Government Policies & Investments – Countries worldwide are implementing policies that favor lithium mining and EV battery production.

Technological Advancements – Innovations in lithium extraction and battery recycling are optimizing resource utilization and sustainability.

Get up to 30% Discount: https://www.statsandresearch.com/check-discount/40617-global-lithium-mining-market

Lithium Mining Market Challenges

Geopolitical Risks – Trade tensions and regional instabilities impact lithium supply chains.

Environmental Concerns – Water-intensive mining practices in regions with scarce water resources raise sustainability issues.

Price Volatility – Fluctuating lithium prices due to supply-demand imbalances affect market stability.

Lithium Mining Market Opportunities

Development of Sustainable Lithium Extraction (SLE) – Reducing water usage and carbon footprint in lithium mining.

Battery Recycling Technologies – Circular economy initiatives focusing on recovering lithium from used batteries.

Geographical Diversification – New lithium mining projects in Africa, Canada, and South America reducing reliance on dominant suppliers.

Lithium Mining Market Segmentation Analysis

By Source

Brine Deposits – The largest contributor to the lithium supply, particularly in South America’s "Lithium Triangle" (Argentina, Bolivia, Chile).

Hard Rock (Spodumene) Deposits – Dominant in Australia and Canada, expected to grow at a CAGR of 15.7% due to increasing demand for high-purity lithium.

Clay Deposits – Emerging as a future source with advancing extraction technologies improving commercial viability.

By Extraction Method

Conventional Mining – Primarily used for spodumene extraction, dominant in Australia.

Evaporation Process – Common for South American brine deposits but under scrutiny for high water usage.

Direct Lithium Extraction (DLE) – Expected to grow at CAGR 18.3%, reducing environmental impact and enhancing extraction efficiency.

By Application

Batteries – The dominant application, driven by EVs and renewable energy storage.

Glass & Ceramics – Lithium enhances durability and thermal resistance in industrial applications.

Lubricants & Greases – Used in aerospace and industrial machinery for high-performance lubrication.

By End-Use Industry

Automotive (EVs) – Largest end-user, accounting for 60.5% of global lithium demand.

Energy Storage – Fastest-growing segment, projected to grow at a CAGR of 17.4%.

Consumer Electronics – Lithium-ion batteries power smartphones, laptops, and other devices.

By Distribution Channel

Direct Sales – Lithium producers secure long-term agreements with battery manufacturers.

Distributors & Traders – Facilitating supply to multiple industrial sectors.

Online Sales & E-commerce – Emerging as a niche channel with CAGR 12.6% growth.

Regional Outlook

Asia-Pacific – Dominates with a 45.4% market share, led by China’s battery manufacturing and lithium refining capacity.

South America – Rich in brine deposits, playing a crucial role in the lithium supply chain.

North America – Growing mining projects in the U.S. and Canada aimed at reducing reliance on imports.

Europe – Accelerating EV adoption and battery gigafactories drive lithium demand.

Middle East & Africa – Emerging as a new lithium mining region, with significant potential in Zimbabwe and Namibia.

Competitive Landscape

The global lithium mining market is highly competitive, with key players focusing on capacity expansion, technological innovation, and strategic partnerships.

Lithium Mining Market Leading Companies

Albemarle Corporation

Sociedad Química y Minera de Chile (SQM)

Pilbara Minerals

Ganfeng Lithium

Tianqi Lithium

Rio Tinto

Lithium Americas Corp.

Recent Developments

Albemarle Corporation – Announced expansion plans in Chile and Australia to boost lithium hydroxide production.

Pilbara Minerals & Ganfeng Lithium – Joint venture for a new lithium conversion facility in China.

Rio Tinto – Investing $2.4 billion in Argentina’s Rincon lithium project, utilizing DLE technology.

Future Trends & Innovations

Sustainable Lithium Extraction (SLE)

The industry is shifting towards eco-friendly extraction processes to minimize water and chemical usage. Direct Lithium Extraction (DLE) is emerging as a game-changing method.

Battery Recycling & Circular Economy

With lithium supply constraints, battery recycling is becoming crucial. Companies are investing in advanced recovery technologies to reclaim lithium from used batteries and industrial waste.

Regional Expansion & Diversification

New mining projects across Africa and North America aim to diversify global lithium supply, reducing dependency on a few key players.

Conclusion

The global lithium mining market is poised for substantial growth, driven by rising demand for EVs, renewable energy storage, and consumer electronics. While challenges such as price volatility, environmental concerns, and supply chain disruptions persist, advancements in sustainable extraction technologies, battery recycling, and regional diversification offer lucrative growth opportunities.

Companies investing in direct lithium extraction (DLE), strategic partnerships, and sustainable mining practices will lead the next wave of industry transformation. With government policies favoring clean energy and the expansion of battery manufacturing capacities, the lithium mining sector is set to thrive in the coming decade.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40617-global-lithium-mining-market

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

#lithium mining#lithium market#lithium mining market#lithium mining trends#lithium mining forecast#lithium mining 2025#global lithium mining#lithium industry growth#lithium demand#lithium mining report#lithium market analysis#battery minerals#electric vehicle demand#lithium supply chain#lithium production trends#lithium mining investment#mining market insights#lithium mining growth#sustainable lithium mining

1 note

·

View note

Text

Iraq Oil and Gas Construction Companies: Key Players in Energy Development

As one of the world’s largest oil-producing countries, Iraq relies heavily on its oil and gas industry to drive economic growth. Iraq oil and gas construction companies are essential in building the infrastructure needed for exploration, extraction, and distribution of oil and gas. These companies play a vital role in constructing pipelines, refineries, storage facilities, and processing plants, which are crucial for Iraq’s energy sector. The expertise and efficiency of Iraq oil and gas construction companies directly influence the country’s ability to maintain its role as a global energy provider.

The Importance of Iraq’s Oil and Gas Sector

The oil and gas sector contributes around 90% of Iraq’s national revenue, making it a cornerstone of the economy. With abundant reserves and a strategic location, Iraq has positioned itself as a major player in the global energy market. However, the sector faces challenges, including the need to update outdated infrastructure and improve efficiency in extraction and refining processes. This is where Iraq oil and gas construction companies step in, offering the expertise and technology to modernize and expand infrastructure. Through their work, these companies not only contribute to economic growth but also help secure Iraq’s future as a competitive energy producer.

Key Services Offered by Iraq Oil and Gas Construction Companies

Iraq’s oil and gas construction companies provide a variety of services to meet the complex demands of the industry. These services include:

Pipeline Construction and Maintenance One of the most critical components of the oil and gas infrastructure is pipelines. They enable the safe and efficient transport of crude oil and natural gas across long distances. Iraq oil and gas construction companies specialize in designing, building, and maintaining pipelines that meet both national and international safety standards. Regular maintenance of these pipelines is crucial for preventing leaks and ensuring smooth operation, making these companies indispensable to the sector.

Refinery Construction and Expansion Refineries are vital for processing crude oil into usable products, such as gasoline, diesel, and petrochemicals. Iraq oil and gas construction companies are skilled in constructing new refineries and expanding existing ones to meet the increasing demand. These projects require advanced engineering and the latest technology to maximize efficiency and reduce environmental impact.

Storage Facilities Efficient storage solutions are essential for managing the supply of oil and gas, especially as global demand fluctuates. Iraq’s construction companies build and maintain large-scale storage facilities, which help manage the country’s energy reserves and stabilize the supply chain. Properly constructed storage facilities also ensure the safe handling of hazardous materials, reducing the risk of accidents.

Processing Plants and Equipment Installation Processing plants convert raw oil and gas into products ready for distribution. Iraq oil and gas construction companies work on both the construction and maintenance of these plants, installing specialized equipment designed to maximize output and minimize waste. This involves incorporating technology that meets international standards for efficiency and environmental protection, supporting Iraq’s long-term goals for sustainable energy production.

Technology and Innovation in Iraq’s Oil and Gas Construction Sector

To stay competitive and meet the demands of an evolving energy market, Iraq oil and gas construction companies are increasingly incorporating advanced technology into their projects. Key technologies used include:

Digital Monitoring and Automation: Digital sensors and automated systems help monitor pipeline pressure, detect leaks, and manage refinery operations more efficiently.

Drones and Robotics: Drones are now commonly used for aerial surveys and inspections, especially in challenging terrain. Robotics aid in tasks such as welding and equipment installation, enhancing precision and safety.

Environmental Technologies: New technologies designed to reduce emissions and manage waste are also being integrated. For instance, gas flaring reduction technology is becoming more common, helping to minimize environmental impact.

The Role of Local Expertise and International Partnerships

While Iraq oil and gas construction companies possess significant expertise, international partnerships are often crucial for large-scale projects. Collaborating with global firms allows Iraqi companies to leverage foreign technology, knowledge, and financing, enhancing their ability to complete complex projects successfully. These partnerships also facilitate knowledge transfer, training local engineers and workers in the latest techniques and technologies. This local expertise, combined with international standards, strengthens Iraq’s position in the global oil and gas market and builds a more sustainable workforce.

Challenges Faced by Iraq Oil and Gas Construction Companies

Despite their importance, Iraq oil and gas construction companies face several challenges. These include:

Security Concerns: Iraq has areas where security remains a concern, which can disrupt project timelines and create additional costs for safety measures.

Regulatory Hurdles: The regulatory environment can be complex, particularly for international partnerships. Compliance with both local and international regulations requires careful planning and adaptability.

Environmental Impact: With a growing emphasis on sustainability, Iraq oil and gas construction companies are increasingly pressured to reduce their environmental footprint, requiring additional investment in green technology and eco-friendly practices.

Conclusion

Iraq oil and gas construction companies are key drivers of the nation’s energy industry, enabling the development, maintenance, and expansion of crucial infrastructure. Their services in pipeline construction, refinery expansion, storage, and processing plants are foundational to Iraq’s energy production and economic stability. By embracing technological advancements and fostering international partnerships, these companies continue to support Iraq’s ambitions in the global energy sector. Despite challenges, the expertise and innovation of Iraq oil and gas construction companies remain essential for ensuring Iraq’s future as a competitive energy powerhouse.

2 notes

·

View notes

Text

At the Argus conference in Istanbul, someone asked me if I had ever thought about hedging the fertiliser business through agricultural commodities trading. I tried to recall which major agricultural trading houses had ever ventured into the fertiliser market.

It’s intriguing that giants like Dreyfus, ADM, Toepfer, or Bunge haven’t found the same success in fertiliser trading despite their dominance in agricultural commodities. One might think their deep market knowledge and extensive networks in grain trading would position them for success in fertilisers, but the reality is more complex.

Fertilisers are closely tied to energy markets, especially natural gas, and mined resources like potash and phosphates. While these companies handle agricultural commodities, where pricing is more transparent, fertilisers operate in opaque markets driven by local factors, regulations, and geopolitical issues. This makes fertiliser hedging through agricultural commodities less effective.

Logistics further complicate things. Fertilisers are bulky, need to be transported across vast distances, and must arrive within specific planting windows. The precision needed in fertiliser distribution is far more challenging than that of grains, where storage and delivery are more flexible.

Moreover, the fertiliser market is dominated by a few large players, making it difficult for newcomers like ADM or Dreyfus to gain ground. Unlike grain trading, fertilisers involve dealing with strong regional players, less transparent pricing systems, and complex regulations.

Then there’s the issue of risk management. Hedging fertiliser positions with agricultural commodities seems logical, but the two markets aren’t perfectly correlated. Fertiliser prices depend on energy costs and mining outputs, which make hedging across commodities complicated and often unreliable.

Despite their vast resources and networks, these companies faced challenges they weren’t fully equipped to overcome in fertilisers. Their experience highlights the complexity of the fertiliser market, where success requires mastering logistics, risk management, and navigating a unique set of market dynamics.

And yes, I do remember Ameropa.

#agicommodities #fertilisers #adm #ameropa #bunge #toepfer #hedging #dreyfus #logistics #marketvolatility #trading

#agriculture#fertilizer#fertilization#urea#corn#usa#wheat#india#vessel#nola#imstory#adm#bunge#ameropa#hedge#agribusiness#logistics

2 notes

·

View notes

Text

Why Blockchain Matters ?

1/ Blockchains will replace networks with markets.

2/ Humans are the networked species. The first species to network across genetic boundaries and thus seize the world.

3/ Networks allow us to cooperate when we would otherwise go it alone. And networks allocate the fruits of our cooperation.

4/ Overlapping networks create and organize our society. Physical, digital, and mental roads connecting us all.

5/ Money is a network. Religion is a network. A corporation is a network. Roads are a network. Electricity is a network...

6/ Networks must be organized according to rules. They require Rulers to enforce these rules. Against cheaters.

7/ Networks have "network effects." Adding a new participant increases the value of the network for all existing participants.

8/ Network effects thus create a winner-take-all dynamic. The leading network tends towards becoming the only network.

9/ And the Rulers of these networks become the most powerful people in society.

10/ Some are run by kings and priests who choose what is money and law, sacred and profane. Rule is closed to outsiders and based on power.

11/ Many are run by corporations. The social network. The search network. The phone or cable network. Closed but initially meritocratic.

12/ Some are run by elites. The university network. The medical network. The banking network. Somewhat open and somewhat meritocratic.

13/ A few are run by the mob. Democracy. The Internet. The commons. Open, but not meritocratic. And very inefficient.

14/ Dictatorships are more efficient in war than democracies. The Internet and physical commons are overloaded with abuse and spam.

15/ The 20th century created a new kind of network - market networks. Open AND meritocratic.

16/ Merit in markets is determined by a commitment of resources. The resource is money, a form of frozen and trade-able time.

17/ The market networks are titans. The credit markets. The stock markets. The commodities markets. The money markets. They break nations.

18/ Market networks work where there is a commitment of money. Otherwise they are just mob networks. The applications are limited.

19/ Until now.

20/ Blockchains are a new invention that allows meritorious participants in an open network to govern without a ruler and without money.

21/They are merit-based, tamper-proof, open, voting systems.

22/ The meritorious are those who work to advance the network.

23/ As society gives you money for giving society what it wants, blockchains give you coins for giving the network what it wants.

24/ It's important to note that blockchains pay in their own coin, not the common (dollar) money of financial markets.

25/ Blockchains pay in coin, but the coin just tracks the work done. And different blockchains demand different work.

26/ Bitcoin pays for securing the ledger. Etherium pays for (executing and verifying) computation.

27/ Blockchains combine the openness of democracy and the Internet with the merit of markets.

28/ To a blockchain, merit can mean security, computation, prediction, attention, bandwidth, power, storage, distribution, content...

29/ Blockchains port the market model into places where it couldn't go before.

30/ Blockchains' open and merit based markets can replace networks previously run by kings, corporations, aristocracies, and mobs.

31/ It's nonsensical to have a blockchain without a coin just like it's nonsensical to have a market without money.

32/ It's nonsensical to have a blockchain controlled by a sovereign, a corporation, an elite, or a mob.

33/ Blockchains give us new ways to govern networks. For banking. For voting. For search. For social media. For phone and energy grids.

34/ Networks governed without kings, priests, elites, corporations and mobs. Networks governed by anyone with merit to the network.

35/ Blockchain-based market networks will replace existing networks. Slowly, then suddenly. In one thing, then in many things.

36/ Ultimately, the nation-state is just a network (of networks).

FIN/ Thank you, Satoshi Nakomoto. And to all the shoulders that Satoshi stands upon.

via: https://medium.com/the-naked-founder/naval-ravikants-36-tweets-on-cryptocurrencies-f9b2b64106c1

2 notes

·

View notes

Text

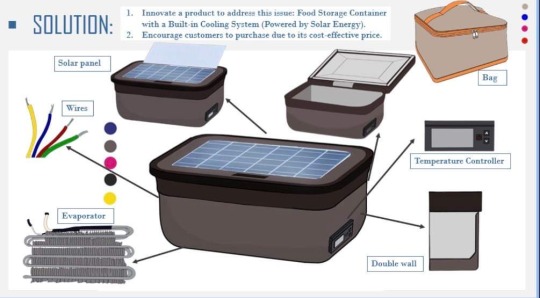

Food Storage Container with a Built-in Cooling System (Powered by Solar Energy).

In the fast-evolving landscape of food storage solutions, our latest product aims to redefine the way we preserve perishable items. The Food Storage Container with a Built-in Cooling System, meticulously designed and powered by solar energy, marks a groundbreaking stride towards sustainable and efficient food storage. Let's delve into the intricate details of this innovative product through the lens of the Business Model Canva.

1. Customer Segments:

Our Food Storage Container caters to a diverse range of customer segments, from households seeking sustainable storage solutions to outdoor enthusiasts in need of portable and efficient food preservation during activities such as camping or picnics, with a focus on boarding students or tenants of Central Mindanao University (CMU) who wish to preserve their food to reduce expenses, campers and ecologically minded clients who emphasized sustainability

2. Value Proposition:

Centrally rooted in our product is a steadfast commitment to offering users an unparalleled solution for extending the shelf life of perishable items. Our built-in cooling system, powered by solar energy, not only guarantees freshness but also aligns seamlessly with the escalating demand for eco-friendly and energy-efficient alternatives. With a focus on preserving, maintaining quality, and extending the consumption window of food items, our product serves as a reliable means to prevent and reduce spoilage of perishable goods. Moreover, its versatility shines through, as its utilization remains viable at any time and from any location, providing convenience and efficiency to users across diverse settings.

3. Channels:

Employing a versatile multi-channel strategy, our product seamlessly reaches customers through various avenues, encompassing online platforms and carefully chosen retail outlets. This strategic approach ensures accessibility and convenience for a diverse customer base. Our sales force, adept in marketing and advertising, spearheads our presence in both online and select retail spaces. In the online domain, we leverage web sales via our online storefront and e-commerce platform. Additionally, our presence is augmented through partner stores, strategically positioned in popular online shopping apps and dedicated appliances stores. This multi-pronged distribution strategy aligns with our commitment to reaching customers through channels that suit their preferences and lifestyles.

4. Customer Relationships:

We foster strong customer relationships by providing comprehensive support through user manuals, personalized online assistance or online guides, offering appliance maintenance, and responding promptly to customer inquiries while servicing e-commerce, ensuring satisfaction and responsive customer service. Regular updates on maintenance and new features further engage our customers.

5. Revenue Streams:

Direct selling of solar food containers to students at set prices, offering discounts, promotions, and refurbishment services for product longevity. The Food Storage Container presents a one-time purchase model with additional revenue streams through accessories like replacement cooling modules and eco-friendly cleaning solutions. This model ensures a steady income while offering customers the flexibility to enhance their product over time.

6. Key Resources:

At the core of our operations are key resources that drive our success: cutting-edge manufacturing facilities, sustainable material sourcing, and a team of dedicated engineers committed to ongoing improvements in cooling technology. These resources are instrumental in upholding the standards of our products, ensuring both quality and innovation. Our resource portfolio encompasses a variety of elements, ranging from raw materials and skilled experts to branding, copyrights, and patents. Additionally, we leverage valuable assets such as customer databases, personal funds, and the integration of renewable light energy. This comprehensive array of resources positions us at the forefront of our industry, facilitating continuous advancement and reinforcing our commitment to excellence.

7. Key Activities:

Our core activities, including product development, rigorous quality control, and continuous exploration of eco-friendly materials and energy-efficient technologies, underscore our commitment to innovation. These efforts position us at the forefront of the industry, where regular updates and improvements exemplify our dedication to staying ahead. In terms of production, we focus on specific design variations, offering a range of colors and sizes, and ensure efficient delivery with multiple payment options like COD, COP, and Gcash. Our problem-solving initiatives are comprehensive, providing customers with a detailed appliances manual that covers aspects like product features, installation processes, diverse use cases, potential risks, and solutions to commonly faced challenges. These structured activities collectively embody our dedication to delivering a cutting-edge product while ensuring customer satisfaction through informative and solution-oriented support materials.

8. Key Partnerships:

Strategic collaborations lie at the core of our business, establishing robust partnerships with solar technology providers, environmental organizations, and retailers. These alliances not only fortify the backbone of our operations but also contribute significantly to the sustainability and extended market reach of our innovative product. Key partners encompass online platforms such as TikTok, Shopee, and Facebook, alongside crucial connections with electricians. While our key suppliers primarily consist of wholesalers, the specifics are yet to be finalized. Essential resources, both physical, including raw materials, and human, in terms of expertise, are acquired through these strategic partnerships. Key activities performed by our partners involve production, focusing on manufacturing processes, and establishing partnerships to seamlessly integrate our product into online shopping platforms. These collaborative efforts collectively propel our business towards success, emphasizing both environmental responsibility and efficient market presence.

9. Cost Structure:

Our primary expenditures encompass critical areas such as research and development, manufacturing processes, marketing campaigns, and the steadfast commitment to maintaining sustainable practices. These investments are indispensable, forming the financial backbone to ensure the creation of a high-quality, eco-friendly product that aligns with our core values. The cost structure comprises fixed and variable elements. Fixed costs range from PHP 5,500 to PHP 6,500, providing the foundation for our operations. Variable costs, on the other hand, involve allocating funds to essential components like raw materials, including an evaporator (PHP 1,000 to PHP 2,000), a small solar panel (around PHP 2,000), stainless steel for the container (PHP 1,000), and plastic containers (ranging from PHP 50 to PHP 200 per unit). Additionally, variable costs encompass man labor, with electrician services in the range of PHP 300 to PHP 800 per day. These detailed cost allocations are pivotal in sustaining our commitment to delivering an innovative and eco-conscious product to our valued customers.

In conclusion, the Food Storage Container with a Built-in Cooling System is not merely a product; it's a testament to our commitment to sustainability, innovation, and customer satisfaction. Through the lens of the Business Model Canva, we envision a future where our revolutionary food storage solution becomes a household staple, reshaping the way we think about freshness and sustainability.

2 notes

·

View notes

Text

ERW Pipes in Oil and Gas Industry: Key Roles and Market Trends

A stable and efficient infrastructure is crucial for the transportation of hydrocarbons in the oil and gas industry. Electric Resistance Welded (ERW) pipes are a critical component that assumes a central role in this system. The pipes in question are renowned for their multifunctionality, resilience, and economical nature, rendering them a widely favoured option for diverse applications within the oil and gas industry. The strength of seamless connectivity - Choose ERW Pipes offered by Tube Trading Co. – an excellent ERW Pipe Supplier in Gujarat for your critical applications.

This blog examines the significant functions of ERW pipes within the industry and investigates the most recent market trends pertaining to these important components.

What are ERW Pipes?

ERW pipes are a variant of steel pipes that are manufactured through the application of a high-frequency electrical current along the edges of the steel strip or coil. The flow of electrical current produces thermal energy, resulting in the fusion of the adjacent edges and the creation of a connection without any visible seams. ERW pipes are extensively utilised in the oil and gas sector owing to their exceptional mechanical characteristics, rendering them appropriate for many applications in both onshore and offshore environments.

Key Roles of ERW Pipes in the Oil and Gas Industry:

Exploration and Production:

ERW pipes are widely employed in drilling activities within the upstream portion of the oil and gas industry. The primary function of these pipes is to act as protective casings for the wellbore, thereby preserving its structural integrity and mitigating the risk of collapse during the drilling process. ERW pipes are utilised in well-completion operations to enhance the effective extraction of hydrocarbons.

Transportation:

Transportation plays a crucial role in the hydrocarbon industry as it facilitates the movement of extracted hydrocarbons from wells to processing units or refineries. ERW pipes, known for their exceptional strength and weldability, serve as the fundamental component of pipelines utilised for the extensive transit of oil and gas. They facilitate the uninterrupted transportation of hydrocarbons from the point of extraction to the ultimate consumers.

Distribution and Storage:

Electric resistance welded (ERW) pipes are of significant importance in the midstream sector, since they are utilised for the purpose of distributing and storing refined fuels, including petrol, diesel and natural gas. The utilisation of these pipes is crucial to the establishment of distribution networks and terminals, facilitating the effective transportation of energy products to end-users.

Offshore Applications:

ERW pipes are commonly utilised in offshore drilling and production due to their notable resilience in challenging marine environments. These components find application in the construction of platforms, risers, and subsea pipelines, offering enhanced stability and dependability in demanding offshore environments.

Experience efficiency in every weld. Order precision-engineered ERW Pipes offered by Tube Trading Co. – a renowned ERW Pipe Provider in Gujarat!

Market Trends of ERW Pipes in the Oil and Gas Industry:

Increasing Demand:

The increasing global demand for electric resistance welded (ERW) pipes within the oil and gas sector is driven by the ongoing growth of exploration and production operations, with a particular emphasis on emerging economies. The consistent expansion in energy consumption and the imperative for novel infrastructure are significant factors that contribute to the heightened adoption of Electric Resistance Welded (ERW) pipes.

Technological Advancements:

Technological advancements in the field of ERW pipes are being pursued by manufacturers through ongoing investments in research and development, with the aim of improving their inherent qualities. The utilisation of advanced welding methodologies and enhanced steel compositions has resulted in the development of pipes exhibiting elevated levels of strength, corrosion resistance, and durability. Consequently, these pipes have emerged as highly suitable for deployment in demanding oil and gas applications.

Environmental Considerations:

The increasing focus of the industry on sustainability and environmental preservation has led to a transition towards more environmentally friendly practices. ERW pipes, due to their environmentally friendly nature and recyclability, are very compatible with these objectives, hence establishing themselves as a favoured option for enterprises that prioritise environmental consciousness.

Focus on Pipeline Safety:

The issue of pipeline safety has garnered significant attention due to worries surrounding leaks and ruptures, resulting in the implementation of more stringent regulations and standards. The superior weld quality and consistency of ERW pipes result in a decreased likelihood of failures, hence enhancing the safety of pipelines.

Market Consolidation:

The ERW pipe market is currently through a process of consolidation, wherein prominent industry participants are actively engaging in mergers and acquisitions to enhance their range of products and increase their market reach. The objective of this trend is to address the increasing demand and sustain a competitive advantage within the sector.

Final Thoughts:

ERW pipes are of significant importance within the oil and gas sector, as they fulfil crucial functions throughout a range of activities spanning from exploration to distribution. The indispensability of these components in the industry's infrastructure can be attributed to their versatility, durability, and cost-effectiveness.

The anticipated increase in the utilisation of ERW pipes is attributed to the escalating demand for energy and the heightened significance of environmental considerations. The continuous endeavours of manufacturers to innovate and enhance these pipes will inevitably result in the development of more effective and environmentally friendly solutions, thereby strengthening their significance as a crucial element within the ever-evolving realm of oil and gas transportation and distribution. Seamless solutions for your piping needs – Partner with Tube Trading Co. – the most reliable ERW Pipe Supplier in Gujarat today!

#ERW Pipe Supplier in Gujarat#ERW Pipe Provider in Gujarat#Business#Manufacturer#Steel industry#Steel company#Oil and gas industry#Oil companies#Agriculture industry

6 notes

·

View notes

Text

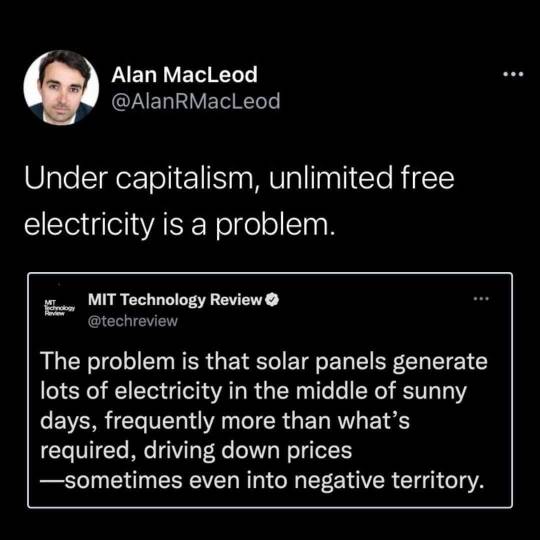

flooding a free market with cheap supplies will drive down price, like how gravity pulls down a ball, it's not "a problem with capitalism" it's a reality to work with. If a market is saturated with supply, clean energy is wing-clipped by petrofascism in not being able to store our clean energy and sell it later when electricity prices go up and supplies are scarce.

We need to be able to store energy in something other than the form of unburnt fuel, the petrofascist has this monopoly on energy storage and protects it at gunpoint, using words like "capitalism" are like complaining about gravity though, and distract from how the petrofascists have taken over and are handcuffing us to a sinking ship.

We skipped right past land-back and reparations and went straight to "death to capitalists like the people who run the local bookstore and coffee shop" meanwhile, communism means an erasure of indigenous religions, local book store and coffee shop owners hitting the guillotine, and petrofascists likely bribing the people in charge and maintaining the status quo. This is why I have to speak out when people get confused and bark up the "capitalism" tree because it represents a fundamental departure of how we can defeat petrofascism and fossil fuel.

To be honest I see a ton of students protesting at colleges, when headquarters and executive residences for oil and gas as well as weapons contractors are like, right there. Our universities are just trying to invest their endowment while upsetting the least number of people; students today need to ask to proverbially speak to the manager, going to raise hell at the Chevron HQ, at the oil and gas tar sands manufacturing sites, and whoever makes the phosphorous bombs and similar, I know there are protests happening there we don't hear about as much, but I'm a firm believer that it's the easy choice to protest where you go to school or work, it's the hard choice to figure out where Warren Buffet, the single largest investor in oil and gas, likes to eat his morning McDonald's and then go blockade the drive through line urging him to divest from killing us

This may sound like a ridiculous concern, yet every time there is a world war, a major country in the world goes communist, it's plausible that this will occur in our lifetimes that say, India goes communist at the end of a potential large war. To me this will be a step in the sideways direction unless that communist revolt is focused on dismantling and replacing petrofascism with a viable system of storing and distributing clean energy. Truly if your revolt is only about shifting around paper then it's nothing more than a banking transaction, a true revolt needs to re-program how energy flows in a society, with clean energy.

#solarpunk#anti#communist manifesto#?#political economic ramblings of tumblr#oracular thoughts#lmao#i'm already critiquing the 2031 communist revolution of India for not going hard enough on clean energy

73K notes

·

View notes

Text

FBG Pressure Sensor Market: Strategic Forecast for Manufacturers and Stakeholders 2025-2032

MARKET INSIGHTS

The global FBG Pressure Sensor Market size was valued at US$ 184.7 million in 2024 and is projected to reach US$ 297.3 million by 2032, at a CAGR of 7.0% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to witness the fastest growth at 6.8% CAGR through 2032.

Fiber Bragg Grating (FBG) pressure sensors are advanced photonic devices that measure pressure variations by detecting wavelength shifts in reflected light. These sensors consist of optical fibers with periodic refractive index modifications that create wavelength-specific reflection patterns. Key product variants include static pressure sensors (dominating 68% market share in 2024) and dynamic pressure sensors, with applications spanning oil storage monitoring, engine testing, and structural health assessment in harsh environments.

The market growth is driven by increasing adoption in oil & gas infrastructure monitoring, where FBG sensors outperform traditional alternatives in explosion-prone zones. Recent technological advancements include multi-point sensing arrays from Luna Innovations and high-temperature resistant designs from FBGS. However, the higher initial costs compared to electrical sensors remain a market restraint, particularly in price-sensitive emerging economies. Leading players like HBM (Spectris plc) and Technica are addressing this through hybrid sensor solutions combining FBG and conventional technologies.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Structural Health Monitoring Fuels FBG Pressure Sensor Adoption

The increasing emphasis on structural health monitoring across industries such as civil engineering, aerospace, and energy is significantly driving the FBG pressure sensor market. These sensors offer unparalleled advantages in harsh environments where traditional electronic sensors fail, including immunity to electromagnetic interference, corrosion resistance, and multiplexing capabilities. In the energy sector alone, deployment of FBG pressure sensors in oil & gas pipelines has grown by approximately 18% annually due to their ability to operate in explosive environments while providing real-time pressure data. The global infrastructure development boom, particularly in emerging economies, further amplifies this trend as governments implement stricter safety regulations for critical structures.

Advancements in Optical Sensing Technology Accelerate Market Expansion

Technological innovations in fiber Bragg grating (FBG) manufacturing are removing previous limitations in pressure sensing applications. Recent developments have yielded sensors with improved temperature compensation and higher pressure sensitivity, with some models now achieving measurement accuracy within ±0.1% FS. The automotive industry represents a particularly promising growth area, where FBG pressure sensors are increasingly deployed in engine monitoring systems. Manufacturers now offer compact, ruggedized sensor packages capable of withstanding extreme vibration and temperature ranges from -40°C to 300°C - a critical requirement for modern combustion engine testing and development.

Growing Industrial Automation Spurs Sensor Integration in Smart Manufacturing

Industry 4.0 implementation across manufacturing facilities worldwide is creating substantial opportunities for FBG pressure sensor adoption. These sensors play a pivotal role in predictive maintenance systems, where their ability to provide continuous pressure monitoring helps prevent equipment failures and optimize production processes. The chemicals processing sector has reported up to 30% reductions in unplanned downtime through deployment of FBG-based monitoring systems. Furthermore, the sensors' compatibility with distributed sensing networks makes them ideal for comprehensive facility monitoring, with single fiber lines often replacing dozens of traditional pressure transducers.

MARKET RESTRAINTS

High Implementation Costs Limit Widespread Industrial Adoption

Despite their advantages, FBG pressure sensors face significant market penetration challenges due to their premium pricing compared to conventional electronic sensors. A complete FBG measurement system including interrogators and specialized fiber optic cables can cost 3-5 times more than equivalent electronic solutions. This cost premium stems from complex manufacturing processes requiring precise laser systems for grating fabrication and the need for specialized installation expertise. Many small and medium-sized enterprises find these costs prohibitive, particularly for applications where the superior capabilities of FBG technology aren't absolutely necessary.

Technical Complexities in System Integration Pose Implementation Barriers

The implementation of FBG pressure sensor systems presents unique technical challenges that can deter potential adopters. Unlike conventional sensors with standardized electrical outputs, FBG systems require specialized optical interrogators and frequently need custom calibration for specific applications. The interrogation equipment alone represents a significant capital investment, with high-end units costing upwards of $20,000. Additionally, the technology requires expertise in both optical physics and instrumentation engineering - a combination of skills that remains scarce in many industrial settings. These integration complexities have slowed adoption in sectors where simpler sensor technologies can adequately meet measurement requirements.

Other Challenges

Limited Standardization The absence of universal standards for FBG sensor specifications and performance metrics creates uncertainty for potential users. This lack of standardization complicates procurement decisions and makes direct comparison between competing products challenging.

Supply Chain Vulnerabilities Reliance on specialized optical fibers and components sourced from limited suppliers creates potential supply chain risks. Disruptions in these niche supply channels could significantly impact product availability and delivery timelines.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Create New Growth Frontiers

The rapid expansion of renewable energy infrastructure worldwide presents significant opportunities for FBG pressure sensor manufacturers. In wind energy applications, these sensors are proving invaluable for blade pressure monitoring, with installed base growing at approximately 25% annually in this sector alone. The technology's immunity to lightning strikes - a critical advantage over electronic sensors in wind turbines - makes it particularly well-suited for these applications. Similarly, in hydrogen energy systems, FBG sensors' ability to operate safely in potentially explosive environments positions them as the preferred solution for pressure monitoring throughout the hydrogen value chain.

Miniaturization Trends Open Doors for Medical and Aerospace Applications

Recent advances in micro-optics and packaging technologies are enabling development of miniaturized FBG pressure sensors suitable for medical and aerospace applications. In the medical field, prototypes of catheter-based FBG pressure sensors have demonstrated sub-millimeter diameters while maintaining clinical-grade accuracy. The aerospace sector shows equally promising potential, with FBG sensors being evaluated for integration into composite aircraft structures and fuel systems. These emerging applications could drive significant market expansion, particularly as sensor manufacturers continue refining their fabrication techniques to meet stringent size and weight requirements.

Other Opportunities

Smart City Infrastructure Growing investments in smart city development worldwide create opportunities for FBG pressure sensors in water distribution monitoring, building structural monitoring, and traffic management systems.

Underwater Applications The sensors' corrosion resistance and ability to operate in high-pressure environments make them ideal for submarine pipeline monitoring, offshore platforms, and deep-sea exploration equipment.

MARKET CHALLENGES

Technical Limitations in Harsh Environments Constrain Market Growth

While FBG pressure sensors excel in many challenging environments, they face limitations in extremely high-temperature applications exceeding 300°C, where specialized coatings and packaging become necessary. These environmental constraints limit adoption in sectors like metallurgy and certain chemical production processes. Furthermore, maintaining sensor performance under conditions involving intense radiation or extreme mechanical shock remains technically challenging. Though recent material science advancements have improved performance limits, these technical barriers continue to restrict market expansion in some industrial segments where environmental conditions exceed current technological capabilities.

Competition from Alternative Sensing Technologies Intensifies

The FBG pressure sensor market faces growing competition from emerging sensing technologies that offer comparable benefits at lower costs. Silicon photonics-based sensors, for example, are achieving measurement performance approaching that of FBG solutions while leveraging more standardized manufacturing processes. Similarly, advances in wireless sensor networks and MEMS technology are providing viable alternatives for many industrial pressure monitoring applications. This competitive pressure forces FBG sensor manufacturers to continuously innovate while justifying their technology's premium pricing through superior performance in niche applications where alternatives fall short.

Other Challenges

Data Interpretation Complexity The specialized nature of FBG sensor data requires trained personnel for proper interpretation, creating workforce training challenges for organizations adopting the technology.

Long-Term Reliability Concerns While FBG sensors demonstrate excellent long-term stability in laboratory conditions, real-world performance data over extended periods (10+ years) remains limited for many application environments.

FBG PRESSURE SENSOR MARKET TRENDS

Increasing Adoption in Oil & Gas and Aerospace Applications to Drive Market Growth

The FBG (Fiber Bragg Grating) pressure sensor market is experiencing significant growth due to increasing utilization in critical industries such as oil & gas and aerospace. Unlike traditional sensors, FBG-based solutions offer superior performance in extreme temperatures, harsh environments, and electromagnetic interference-prone zones. The oil & gas sector, which accounts for nearly 28% of the global industrial sensor demand, particularly benefits from these sensors for pipeline monitoring and refinery pressure measurements. Their ability to withstand high-pressure conditions while delivering real-time data makes them indispensable in safety-critical operations. Furthermore, the aerospace industry leverages FBG sensors for structural health monitoring, fuel systems, and engine performance analysis due to their lightweight and corrosion-resistant properties.

Other Trends

Integration with Structural Health Monitoring Systems

The rising adoption of smart infrastructure and IoT-driven structural health monitoring systems presents a substantial opportunity for FBG pressure sensors. Governments worldwide are investing heavily in smart city projects, with structural integrity monitoring being a key focus area. FBG sensors are increasingly embedded in bridges, dams, and buildings to detect pressure anomalies or material stress in real time. Major infrastructure projects in Asia-Pacific and North America have reported a 17% year-over-year increase in the deployment of FBG-based monitoring solutions. The non-intrusive, highly sensitive nature of these sensors allows for proactive maintenance, reducing long-term operational risks and costs.

Technological Advancements Enhancing Sensor Capabilities

Recent innovations in FBG sensor technology are expanding their application scope across various sectors. Manufacturers are focusing on developing multi-parameter FBG sensors capable of measuring pressure, temperature, and strain simultaneously with micron-level precision. The emergence of miniaturized sensors with wireless data transmission capabilities has further fueled adoption in medical devices and automotive testing environments. Additionally, improvements in signal demodulation techniques have enhanced measurement accuracy by over 30%, making these sensors viable alternatives to conventional piezoresistive and capacitive pressure sensors in precision-demanding applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership in FBG Pressure Sensor Segment

The global FBG Pressure Sensor market demonstrates a dynamic competitive environment, characterized by both established multinational corporations and agile specialized manufacturers. HBM (Spectris plc) and Luna Innovations currently hold prominent positions, leveraging their technological expertise in fiber optic sensing and strong distribution networks across North America and Europe. Together, these top five players accounted for approximately 45% of the 2024 market revenue.

While AtGrating Technologies leads in static pressure sensor applications with its patented grating designs, Femto Sensing International has carved a niche in high-precision dynamic pressure monitoring for aerospace and defense sectors. Recent joint ventures between FBGS and Asian manufacturers highlight the growing importance of regional partnerships to access emerging markets.

Two distinct strategies are emerging among market participants: larger firms like Spectris focus on acquiring complementary technologies, while specialist players such as Optromix invest heavily in customized solutions for industrial IoT applications. This bifurcation is reshaping price competitiveness across different application segments.

Notably, Chinese manufacturers including Aunion Tech Co., Ltd. are gaining traction through government-backed R&D initiatives, particularly in oil storage monitoring systems. Their competitive pricing structures have compelled Western players to relocate portions of their manufacturing operations to maintain cost efficiency.

List of Key FBG Pressure Sensor Manufacturers Profiled

HBM (Spectris plc) (Germany)

Luna Innovations (U.S.)

AtGrating Technologies (China)

Optromix (U.S.)

FBGS (Belgium)

Technica (U.S.)

T&S Communication Co, Ltd (China)

Femto Sensing International (Singapore)

FiberStrike (Cleveland Electric Laboratories) (U.S.)

Aunion Tech Co., Ltd (China)

Segment Analysis:

By Type

Static Pressure Sensors Lead Market Due to Rising Demand in Industrial Monitoring Applications

The market is segmented based on type into:

Static Pressure Sensor

Subtypes: Absolute pressure, Gauge pressure, Differential pressure

Dynamic Pressure Sensor

Subtypes: Piezoelectric, Capacitive, MEMS-based

By Application

Oil Storage Tank Monitoring Emerges as Key Application Segment for FBG Pressure Sensors

The market is segmented based on application into:

Oil Storage Tank Monitoring

Engine Pressure Monitoring

Structural Health Monitoring

Aerospace and Defense

Others

By End User

Oil & Gas Industry Dominates End User Segment Due to Critical Pressure Monitoring Needs

The market is segmented based on end user into:

Oil & Gas Industry

Automotive

Aerospace and Defense

Energy and Power

Others

Regional Analysis: FBG Pressure Sensor Market

North America The FBG pressure sensor market in North America is characterized by strong technological adoption and significant investments in industrial automation and energy infrastructure. The U.S. dominates the region, accounting for over 65% of regional demand, driven by applications in oil & gas, aerospace, and civil engineering. Strict safety regulations and the push for smart infrastructure monitoring systems further bolster demand. Key players like Luna Innovations and HBM (Spectris plc) leverage strong R&D capabilities to maintain competitiveness. However, high production costs and supply chain complexities pose challenges for mid-sized manufacturers.

Europe Europe exhibits steady growth in FBG pressure sensor adoption, particularly in Germany and the U.K., where industrial IoT integration and renewable energy projects are prioritized. The region benefits from stringent EU directives on structural health monitoring, fueling demand in wind turbines and pipeline systems. The presence of established manufacturers such as FBGS and Technica supports localized innovation, though market fragmentation and competition from alternate sensing technologies (e.g., piezoelectric sensors) limit price flexibility. Collaborations between research institutes and industry players are common, driving advancements in high-temperature and corrosion-resistant sensor designs.

Asia-Pacific As the fastest-growing market, Asia-Pacific is propelled by China's expansive infrastructure projects and Japan’s precision manufacturing sector—”static pressure sensors” claim the largest share due to their use in hydraulic systems and aerospace testing. India’s refinery expansions and Southeast Asia’s oil storage investments present new opportunities. While cost sensitivity initially favored traditional strain gauges, FBG sensors are gaining traction for their long-term reliability in harsh environments. Local players like Aunion Tech Co., Ltd. compete aggressively on price, though technology gaps persist compared to Western offerings.

South America Market penetration in South America remains nascent but promising, with Brazil leading in oilfield applications. Economic instability and limited local manufacturing hinder scalability, but offshore exploration projects (e.g., Brazil’s pre-salt basins) drive niche demand. Most FBG sensors are imported, creating dependency on North American and European suppliers. Governments’ sporadic investments in sensor-based monitoring for dams and pipelines signal gradual growth, though political unpredictability delays large-scale deployments.

Middle East & Africa The region focuses on oil storage tanks and pipeline monitoring, leveraging FBG sensors’ explosion-proof properties. Saudi Arabia and the UAE lead adoption, supported by national oil companies’ modernization initiatives. Africa’s market is constrained by budgetary limitations, but mining sectors in South Africa and infrastructure projects in North Africa show potential. Competition from cheaper alternatives (e.g., capacitive sensors) slows FBG uptake, though partnerships with global firms like Optromix aim to address technical and cost barriers over time.

Report Scope

This market research report provides a comprehensive analysis of the global and regional FBG Pressure Sensor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global FBG Pressure Sensor market was valued at USD 220 million in 2024 and is projected to reach USD 380 million by 2032, growing at a CAGR of 7.1% during the forecast period.

Segmentation Analysis: Detailed breakdown by product type (Static Pressure Sensor, Dynamic Pressure Sensor), application (Oil Storage Tank, Engine, Others), and end-user industry to identify high-growth segments and investment opportunities. Static Pressure Sensors accounted for 62% market share in 2024.

Regional Outlook: Insights into market performance across North America (28% market share), Europe (23%), Asia-Pacific (37%), Latin America, and the Middle East & Africa, including country-level analysis where relevant. China is expected to grow at 8.5% CAGR.

Competitive Landscape: Profiles of leading market participants including AtGrating Technologies, HBM(Spectris plc), Luna Innovations, and FBGS, covering their product offerings (15+ product lines), R&D focus, manufacturing capacity, and recent M&A activities. Top 5 players held 45% market share in 2024.

Technology Trends & Innovation: Assessment of emerging technologies including AI integration, IoT connectivity, and advanced fabrication techniques with 120+ patents filed in 2023-2024 period.

Market Drivers & Restraints: Evaluation of factors driving market growth (12% YOY increase in oil & gas applications) along with challenges (supply chain disruptions affecting 18% of manufacturers in 2024).

Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators (70+ active companies), and investors regarding the evolving ecosystem and strategic opportunities in aerospace and energy sectors.

Primary and secondary research methods are employed, including interviews with 50+ industry experts, data from verified manufacturing reports, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global FBG Pressure Sensor Market?

-> FBG Pressure Sensor Market size was valued at US$ 184.7 million in 2024 and is projected to reach US$ 297.3 million by 2032, at a CAGR of 7.0% during the forecast period 2025-2032

Which key companies operate in Global FBG Pressure Sensor Market?

-> Key players include AtGrating Technologies, HBM(Spectris plc), Technica, Optromix, Luna Innovations, FBGS, T&S Communication Co, Ltd, Femto Sensing International, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand from oil & gas sector (35% of applications), aerospace industry modernization, and infrastructure monitoring requirements.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (37%), while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, multi-parameter sensing capabilities, and integration with wireless monitoring systems.