#Eligibility and verification

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a 66 index score for customer satisfaction in the US.

Text

Payment Posting

To provide the #financial picture of medical practice by depicting the #insurancepayments in EOBs, including #patient #payments and #insurance checks from #ERAS.

Denials

To account for the count of #claims denial along with analyzing the causes behind such occurrences to undertake the necessary steps at the earliest.

Accounts Receivable

To follow-up the denied or rejected claims so as to reopen them with full evidence to receive 100% #reimbursements from the insurers.

Charge Posting

To make sure there will be no rejections after sending a claim to insurance to follow every guideline according to the Speciality. Correct use of modifiers updated ICD and billed amount , with accurate CPT.

Rejections

Some times numerous rejected claims get stuck in the clearing house, so we make sure to assign a professional who can fix all of them and send them to insurance.

Patient Collection

To have a dedicated professional who can do daily and regular followups on patient's due balance to collect their balances on your behalf.

Eligibility And Verification

To make time for your patients and the front office, we provide dedicated FTE to who can check eligibility and benefits before patients arrive for their appointment and also get authorization in advance for the procedures that need authorization.

#medical billing services#health care#it solutions for increasing revenue#medical billing outsource#medical billing company#Charge posting#Payment posting#Patient Calling#Health Care Outsource#Best medical Billing company#medical billing#US healthcare RCM#FTE#Full Time Equivalent AR#Account receivable#Eligibility and verification#Authorization#Prior Auth#Medical Billing Outsource#Doctor Billing#USA medical Billing#Revenue Cycle Management#HealthCare Outsource

0 notes

Text

How to Compare the Processing Time of Different Lenders?

When applying for a personal loan, one of the most crucial factors to consider is the processing time. Different lenders have varying approval and disbursal timelines, which can significantly impact borrowers who need funds urgently. While some lenders offer instant personal loans, others take a few days to process applications due to extensive documentation and verification procedures.

Understanding how to compare the processing time of different lenders can help you make an informed decision and choose the right lender based on your urgency and financial situation.

1. Why Is Loan Processing Time Important?

The processing time of a personal loan refers to the total duration from the moment you apply for the loan until the funds are disbursed into your account. The quicker the process, the faster you can meet urgent financial needs.

✅ Key Reasons to Consider Loan Processing Time:

Emergency Expenses – If you need funds for a medical emergency or urgent home repairs, a lender with instant approval is ideal.

Loan Approval Predictability – Faster lenders provide quicker decisions, preventing unnecessary delays.

Convenience – Choosing a lender with minimal paperwork and digital verification saves time and effort.

Better Financial Planning – Knowing the expected loan disbursal time helps you plan your expenses more efficiently.

📌 Tip: Always check the lender’s estimated processing time before applying for a personal loan, especially if you need urgent funds.

2. Factors That Influence Personal Loan Processing Time

Several factors affect how quickly a lender can approve and disburse your personal loan. Understanding these can help you compare lenders effectively.

✅ Type of Lender

Banks: Traditional banks usually have longer processing times (3-7 days) due to extensive verification.

NBFCs (Non-Banking Financial Companies): These lenders often have faster processing (24-48 hours), with minimal paperwork.

Fintech Lenders: Online lending platforms offer instant personal loans (a few minutes to hours) with digital verification.

✅ Application Mode

Online applications are processed faster than in-person applications.

Mobile banking and fintech apps provide quicker approval and disbursal compared to offline methods.

✅ Credit Score & Loan Eligibility

A higher credit score (700+) speeds up approval.

Lenders may take longer to verify documents for applicants with a low credit score.

✅ Existing Relationship with the Lender

If you have an existing account or prior loan with the lender, your loan may be processed faster.

Pre-approved loans are often disbursed within minutes.

✅ Loan Amount & Type

Higher loan amounts require additional verification, increasing processing time.

Small-ticket loans are often approved quickly.

✅ KYC & Income Verification

If a lender requires extensive income proof and KYC documentation, the processing time may increase.

Lenders using Aadhaar-based eKYC and digital verification process loans faster.

📌 Tip: Opt for lenders that provide pre-approved offers, as these have minimal documentation and faster disbursal.

3. How to Compare the Processing Time of Different Lenders?

When comparing different lenders, consider these key aspects to determine the fastest loan processing option:

✅ Check the Loan Processing Stages

Different lenders have unique processing steps. A standard personal loan process includes: 1️⃣ Application Submission – Online or offline loan application. 2️⃣ Document Verification – KYC, income proof, and employment verification. 3️⃣ Approval & Offer Finalization – Loan approval and finalizing loan terms. 4️⃣ Loan Agreement Signing – Digital or physical loan agreement. 5️⃣ Loan Disbursal – Funds transferred to the borrower’s bank account.

Compare how long each lender takes at these stages to estimate the total processing time.

✅ Research Online Reviews & Customer Feedback

Look for customer reviews on Google, Trustpilot, or financial forums.

Check if customers have faced delays in loan disbursal.

Prefer lenders with positive feedback on fast approvals.

✅ Compare Instant Loan Providers

Fintech lenders and NBFCs typically offer instant personal loans with approval in minutes.

Traditional banks may take 3-7 days, depending on internal verification.

✅ Check for Pre-Approved Loan Offers

Some lenders offer pre-approved loans to existing customers.

These loans have minimal documentation and quick disbursal (within 24 hours).

✅ Analyze Loan Terms & Hidden Processing Delays

Some lenders claim instant approvals but have hidden processing delays.

Always read loan terms for possible hidden charges or conditions.

📌 Tip: Choose a lender based on both speed of processing and transparency of terms.

4. List of Fastest Personal Loan Lenders in India (2024)

While lender policies change frequently, here are some of the fastest personal loan providers in India:

✅ Instant Loan Lenders (Disbursal within Minutes to 24 Hours):

Bajaj Finserv

HDFC Bank Insta Loan

ICICI Bank Pre-Approved Loans

PaySense & KreditBee (Fintech lenders)

Navi & MoneyTap (Instant loan apps)

✅ Fast Personal Loan Lenders (Disbursal in 24-48 Hours):

Axis Bank & Kotak Mahindra Bank

Tata Capital

IDFC First Bank

Fullerton India

✅ Traditional Banks (Processing Time: 3-7 Days):

State Bank of India (SBI)

Punjab National Bank (PNB)

Bank of Baroda (BOB)

📌 Tip: Always check the latest loan processing time on the lender’s official website before applying.

5. Tips to Speed Up Your Loan Processing Time

If you want faster loan approval, follow these best practices:

✅ Choose Online Lenders – Digital lenders process applications faster than traditional banks. ✅ Keep Documents Ready – Ensure KYC documents and income proof are available. ✅ Improve Your Credit Score – A high credit score speeds up approval. ✅ Opt for Pre-Approved Offers – If your bank offers a pre-approved loan, it’s the quickest option. ✅ Apply During Working Hours – Applications processed on weekends may experience delays.

📌 Tip: Avoid applying for multiple loans simultaneously, as multiple hard inquiries can slow down the approval process.

Final Thoughts: How to Choose the Fastest Lender for Your Personal Loan?

Choosing the right lender based on processing time ensures you get funds when you need them. Consider factors like approval speed, documentation requirements, and digital processing capabilities before finalizing your choice.

🚀 Choose Instant Loan Lenders If: ✔ You need quick approval and disbursal. ✔ You have a high credit score and stable income. ✔ You prefer minimal paperwork and digital verification.

💰 Choose Traditional Banks If: ✔ You prefer a well-established financial institution. ✔ You are willing to wait longer for approval. ✔ You need a higher loan amount with flexible repayment options.

Comparing processing times among lenders can help you secure a personal loan quickly while ensuring the best interest rates and repayment terms.

For expert guidance on choosing the right personal loan, visit www.fincrif.com today!

#personal loan online#nbfc personal loan#bank#personal loans#fincrif#loan services#finance#personal loan#loan apps#personal laon#Personal loan#Loan processing time#Fast personal loan approval#Instant personal loan#Online personal loan application#Personal loan disbursal time#Quick loan approval#Personal loan eligibility#Compare personal loan lenders#Loan processing speed#Personal loan documentation#Digital loan application#Pre-approved personal loan#Personal loan verification process#Loan approval criteria#Loan disbursal process#Personal loan interest rate comparison#Best personal loan lenders#NBFC personal loan approval#Bank vs NBFC loan processing time

1 note

·

View note

Text

Streamlining Patient Eligibility Verification Process

In today’s healthcare environment, patient eligibility verification is more critical than ever. As the financial pressures on healthcare providers in the USA continue to rise, ensuring that patients are covered and services are reimbursable before they’re rendered is a vital administrative task.

Hospitals, private practices, and specialty clinics must optimize their verification processes to maintain operational efficiency and avoid costly claim denials.

This article takes a deep dive into the significance of this process, its impact on your revenue cycle, and how providers can integrate technology and best practices to streamline operations and enhance patient satisfaction.

Why Patient Eligibility Verification Matters

One of the primary reasons providers lose money is due to services rendered to ineligible patients. Whether because of expired coverage, incorrect plan types, or unmet deductibles, these issues lead to denied claims that strain practice cash flow and waste valuable staff time on rework.

Key stats to consider:

Over 25% of claim denials are due to eligibility issues.

Manual verification processes can cost practices thousands annually in labor and reprocessing efforts.

On average, denied claims can take 30-45 days longer to reimburse.

Proper eligibility verification ensures the right services are provided under the right plan terms, improving both provider reimbursement and patient transparency. In short, it sets the foundation for a clean claim.

The Patient Experience and Revenue Cycle

Verification does more than help the bottom line—it also reduces patient frustration. When patients know in advance what is covered and what they may owe, they are less likely to dispute bills or delay payments.

Transparent verification helps providers:

Set accurate expectations for out-of-pocket costs.

Reduce surprise billing.

Speed up check-in and reduce wait times.

Enhance trust and satisfaction.

As the patient experience becomes more central to value-based care models, ensuring administrative clarity is a competitive differentiator.

Key Components of a Verification Process

A strong verification process includes several critical checkpoints:

1. Insurance Coverage Validation

Ensure that the patient’s coverage is active on the date of service. This includes:

Policy number validation

Effective and expiration dates

Insurance carrier details

2. Benefits and Plan Coverage

Understand what services are covered under the patient’s plan. This step includes:

Deductibles and co-pays

Coverage limits

Preauthorization requirements

3. Patient Demographics

Check that patient information matches the insurer’s records exactly, including:

Full name

Date of birth

Address and contact information

4. Provider Network Status

Is your facility or provider in-network with the patient’s insurer? Being out-of-network can shift financial responsibility to the patient.

5. Prior Authorizations

Some services require approval before treatment. Failing to secure authorization leads to automatic denials, regardless of coverage status.

Challenges in the Current System

Even though the verification process is vital, many providers still rely on outdated or manual systems. Fax machines, phone calls, and inconsistent portals create bottlenecks and leave room for human error.

Common challenges include:

Inconsistent payer requirements

Manual errors in data entry

Difficulty obtaining real-time responses from payers

Staff shortages or lack of training

With these obstacles, it’s no surprise that small to mid-sized practices struggle to keep up without external help or automation.

Leveraging Technology for Better Outcomes

To address inefficiencies, many practices are turning to technology solutions that integrate with Electronic Health Records (EHRs) and Practice Management Systems (PMS). These platforms offer real-time eligibility checks, integrate patient benefits data, and trigger alerts for missing authorizations.

Benefits of automated systems include:

Faster eligibility checks (real-time or batch)

Reduced human errors

More accurate patient estimates

Streamlined workflow for front desk staff

Investing in an automated platform may seem costly upfront, but the long-term gains in speed and denied claims reduction provide excellent ROI.

Outsourcing as a Strategic Advantage

For many healthcare providers, outsourcing patient eligibility verification to a dedicated partner is a smart move. Outsourcing providers are experienced in dealing with multiple payer systems, keeping up with policy changes, and performing verifications quickly and accurately.

Advantages of outsourcing include:

24/7 verification support

Scalability for high-volume periods

Reduced burden on in-house staff

Expertise in complex insurance policies and regulations

One such trusted partner is Mava Care Medical Billing company, known for supporting healthcare organizations in the USA with accurate, efficient verification and billing services.

Best Practices for Healthcare Providers

If you’re managing eligibility checks in-house, it’s essential to implement best practices that ensure accuracy and efficiency.

1. Verify Early and Often

Ideally, verifications should be done during appointment scheduling and again 24–48 hours before the visit.

2. Standardize Workflows

Use standardized checklists and scripts for front desk or billing staff to follow. This improves consistency and reduces missed steps.

3. Train and Educate Staff

Front desk teams should be well-trained in how to use systems, contact payers, and recognize red flags in insurance data.

4. Track and Measure KPIs

Monitor denial rates due to eligibility, time to complete verifications, and patient satisfaction metrics to refine your process.

Compliance and HIPAA Considerations

Eligibility verification involves handling sensitive patient information. It’s critical to ensure compliance with HIPAA regulations, particularly when sharing data across platforms or with third-party services.

Healthcare providers should:

Use encrypted platforms for digital communication.

Limit access to sensitive data to authorized personnel only.

Regularly audit and update their privacy policies.

Outsourcing companies must also sign Business Associate Agreements (BAAs) and demonstrate full compliance.

The Future of Eligibility Verification

As healthcare continues to evolve, patient eligibility verification will become even more automated and data-driven. Artificial Intelligence and machine learning are being applied to identify verification risks, flag problem areas in advance, and even estimate likelihood of denial based on historical patterns.

Blockchain technology is also being explored for secure, patient-centric insurance data sharing, which could someday eliminate the need for third-party verifications altogether.

Conclusion:

For healthcare providers in the USA, patient eligibility verification is not just a box to check—it’s a vital part of delivering excellent care and maintaining financial stability. With rising costs, changing payer rules, and increasing patient expectations, a robust verification strategy can be a game-changer.

Whether you choose to invest in advanced automation tools or partner with a trusted third-party like Mava Care Medical Billing company, improving your eligibility verification process is an investment that pays off across the board.

#mavacare#medical billing company#medical billing services#medical billing in usa#patient eligibility verification

0 notes

Text

Why Eligibility Verification Is the First Step to Prevent Medical Billing Errors

In today’s complex healthcare landscape, medical billing errors are a costly and time-consuming problem for both providers and patients. From claim denials to delayed reimbursements, inaccurate billing can significantly disrupt the revenue cycle and hurt patient satisfaction. One of the most effective ways to minimize these issues is by performing accurate patient eligibility and benefits verification and doing it early.

Eligibility verification isn't just another administrative task; it's the foundation of successful healthcare revenue cycle management. It ensures that providers are paid on time, patients understand their financial responsibilities, and claims aren’t denied for preventable reasons.

What Is Eligibility Verification?

Eligibility verification is the process of confirming a patient’s health insurance coverage, benefits, and financial responsibility before services are provided. This includes checking:

Whether the insurance policy is active

What benefits are covered

Deductibles and co-pays

Pre-authorization requirements

In-network vs. out-of-network status

This verification process is usually done through payer portals, clearinghouses, or automated software integrations with the EHR.

Why It Must Come First

1. It Prevents Claim Denials and Rejections

According to industry data, insurance eligibility issues are one of the top five reasons for claim denials. If a patient’s coverage has expired, if their plan doesn’t cover a procedure, or if the provider is out-of-network, the claim will likely be denied—costing your staff time in rework and appeals.

Verifying eligibility before the appointment ensures that any coverage gaps or issues can be addressed ahead of time, avoiding unnecessary denials and write-offs.

2. It Improves Cash Flow and Accelerates Reimbursements

A clean claim starts with accurate patient data. When eligibility is confirmed in advance and benefits are clearly understood, the likelihood of submitting a clean claim increases significantly. Fewer denials mean faster reimbursements, reduced days in A/R, and a healthier revenue cycle.

Additionally, when patients understand their coverage and out-of-pocket responsibility ahead of time, they are more likely to pay their share at the time of service—boosting front-end collections.

3. It Reduces Patient Confusion and Billing Disputes

Patients are increasingly frustrated by surprise medical bills. One common reason? They weren’t aware of what their insurance would or wouldn’t cover.

When eligibility and benefits are verified before the visit, providers can clearly communicate:

Co-pay and deductible amounts

Services that require pre-authorization

Any out-of-pocket estimates

This transparency builds trust and reduces the likelihood of patients disputing bills or failing to pay.

4. It Frees Up Staff Time by Preventing Rework

Correcting a denied claim can take hours of staff time—time that could be spent on more productive tasks. If eligibility isn’t confirmed in advance, your medical billing team may have to:

Re-contact the patient

Re-submit claims

Appeal denials

Adjust accounts

By verifying coverage upfront, you eliminate the need for much of this back-and-forth and improve operational efficiency.

5. It Helps Determine Pre-Authorization Requirements

Many insurance plans require prior authorization services for high-cost or specialty services. If eligibility and benefits aren’t checked early, your team might miss this crucial requirement, resulting in denied claims—even if the procedure is medically necessary.

Eligibility checks often reveal which services need prior auth, allowing your staff to initiate that process ahead of time and prevent billing disruptions.

How to Implement a Reliable Eligibility Verification Workflow

To prevent billing errors, eligibility verification must be systematic, consistent, and integrated into your front-office workflow. Here’s how to build a strong process:

Verify insurance eligibility at least 48–72 hours before the appointment.

Use real-time eligibility tools or clearinghouse platforms to automate the process.

Train front-desk staff on how to check coverage details and ask the right questions.

Flag discrepancies and resolve them before the patient arrives.

Document verification details in the EHR or practice management system.

Communicate benefit information and financial responsibility to patients prior to the visit.

The Role of Technology in Error-Free Eligibility Verification

Manually calling payers or logging into multiple portals is time-consuming and error-prone. That's why many practices are turning to eligibility verification software that integrates directly with their practice management or EHR system.

These tools can:

Pull real-time eligibility data from payers

Identify pre-auth requirements

Alert staff to coverage limitations

Provide patient responsibility estimates

Automating eligibility verification reduces human error, speeds up workflows, and ensures your practice is always working with accurate, up-to-date information.

Final Thoughts

Eligibility verification is not optional—it’s essential. It’s the front line of defense against billing errors, claim denials, and patient dissatisfaction. By verifying coverage before the point of care, practices can protect their revenue, improve patient communication, and streamline their operations.

In an era where payers are becoming stricter and patients are more cost-conscious, getting eligibility right from the start is not just a best practice—it’s a business imperative.

#priorauthorization#medicalbillingservices#medicalbilling#prior authorization services#healthcarercmservices#patient eligibility & benefits verification

0 notes

Text

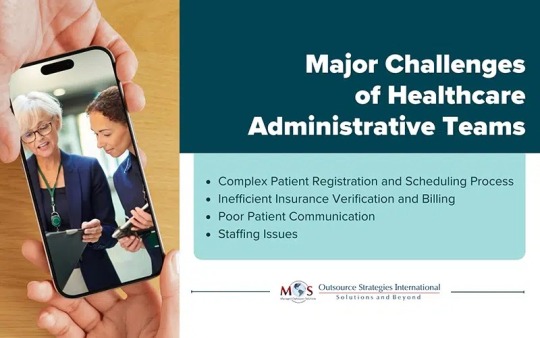

Key Challenges Faced by Healthcare Administrative Offices

Is your front desk team slammed by phone calls, scheduling errors, and dissatisfied patients?

Learn how you can tackle common administrative challenges in medical practices, ranging from communication breakdowns to insurance headaches. Discover how technology, training, and outsourcing can streamline operations and improve patient experience.

0 notes

Text

Boost Your Revenue Cycle: The Power of Outsourcing Eligibility Verification

Simplify your front-end processes and minimize billing errors by outsourcing insurance eligibility verification. Accurate verification improves cash flow, reduces administrative burden, and helps healthcare practices maintain strong financial health.

#insurance eligibility verification#medical billing services#rcm companies in usa#dme billing services#medical billing company

0 notes

Text

🩺📋 Tired of Insurance Headaches in Healthcare? We’ve Got You. 📋🩺

Ever had a claim denied because of eligibility issues? Or watched your front desk team drown in insurance verification chaos?

At RevMax Healthcare, we take the stress out of insurance eligibility and verification—so you can focus on patients, not paperwork. 💼✨

💡 Here's why our service matters: ✔️ Faster patient onboarding ✔️ Fewer claim denials ✔️ Real-time verification ✔️ 100% HIPAA compliant ✔️ Increased revenue & trust

Whether you're a clinic, hospital, or private practice, accurate insurance checks can make all the difference in how smoothly your operations run.

🔗 Learn more: revmaxhealthcare.com →

Because in healthcare, every detail matters. 🧾✅

#medical billing specialist#healthcare#medical billing services#insurance#medical billing and coding#medical billing company#health insurance#medical billing outsourcing#medical coding#insurance eligibility verification#usa#united states of america#united states

0 notes

Text

How to Be Listed on Google News Search: A Comprehensive Guide

Table of Contents Introduction Understanding Google News Search Eligibility Criteria for Google News Inclusion How to Apply for Google News Indexing Optimizing Your Website for Google News The Role of AI in Google News Inclusion Featured Snippets and AEO Optimization Geo-Targeting for Google News Best Practices for Content Creation Case Studies: Success Stories Customer Reviews and…

#AI in google news#google news algorithm#google news content guidelines#google news E-E-A-T#google news eligibility#google news featured snippets#google news for businesses#google news geo targeting#google news inclusion criteria#google news indexing#google news local seo#google news optimization#google news publisher verification#google news ranking factors#google news schema markup#google news search visibility#google news seo#google news SEO best practices#google news structured data#google news submission#google news traffic growth#google news vs google discover#google publisher center#how to be listed on google news#how to rank in google news

0 notes

Text

Steps to Get a Personal Loan Without Income Proof

A personal loan can be a great financial tool to manage unexpected expenses, but lenders usually require proof of income before approving your application. However, if you don’t have formal income documentation, there are still ways to secure a personal loan. In this guide, we will discuss the steps you can take to improve your chances of getting a personal loan without income proof.

1. Maintain a Good Credit Score

Your credit score plays a crucial role in determining your loan eligibility. A high credit score (typically above 700) indicates financial responsibility and increases your chances of securing a personal loan even without income proof. Paying credit card bills and existing loan EMIs on time will help maintain a good credit score.

2. Apply with a Co-Applicant or Guarantor

If you do not have income proof, applying with a co-applicant or guarantor can strengthen your loan application. The co-applicant should have a stable income and a good credit score to increase approval chances.

3. Offer Collateral for a Secured Loan

A secured personal loan requires you to pledge assets like gold, fixed deposits, or property. Lenders are more willing to approve loans against security as it reduces their risk.

4. Show Alternative Sources of Income

Even without traditional salary slips, you can present alternative income sources such as:

Freelancing earnings

Rental income

Investment returns

Business profits

Providing bank statements or other financial documents proving consistent earnings can help build your case.

5. Choose NBFCs or Digital Lenders

Banks have strict income proof requirements, but Non-Banking Financial Companies (NBFCs) and digital lenders offer more flexible eligibility criteria. Some of the best personal loan providers in India include:

IDFC First Bank Personal Loan

Bajaj Finserv Personal Loan

Tata Capital Personal Loan

Axis Finance Personal Loan

Axis Bank Personal Loan

InCred Personal Loan

6. Maintain a Strong Relationship with Your Bank

If you have an existing relationship with a bank, such as a savings account or a past loan, your chances of securing a personal loan without income proof increase. Banks prioritize loyal customers with a good transaction history.

7. Opt for a Lower Loan Amount

Applying for a smaller loan amount increases the chances of approval as the risk for the lender is lower. Once you successfully repay a small loan, you can apply for a higher amount in the future.

8. Improve Debt-to-Income Ratio

A lower debt-to-income ratio (DTI) increases your chances of loan approval. Reduce existing debts before applying for a personal loan to improve your financial profile.

9. Provide a Detailed Business Plan (for Self-Employed Individuals)

If you are self-employed, showing a well-structured business plan and projected earnings can help convince lenders of your repayment capability.

10. Apply Through the Right Channels

Applying through online lending platforms or directly visiting the bank’s branch can make a difference. Some lenders have specific policies for individuals without income proof.

Conclusion

While getting a personal loan without income proof can be challenging, it is possible with the right approach. Maintaining a strong credit score, offering collateral, choosing the right lender, and showing alternative income sources can significantly improve your chances of approval. Compare loan options on Fincrif to find the best deals.

#Personal loan#Loan without income proof#Instant personal loan#No income verification loan#Loan approval process#Personal loan for unemployed#Loan without salary slip#Personal loan eligibility#Secured personal loan#Unsecured personal loan#Credit score for loan#Loan with alternative income#Bank statement loan#Low documentation loan#Self-employed personal loan#Loan with guarantor#Best NBFC personal loan#Digital lender loans#Collateral-based loan#Easy approval loans#High credit score loan#Personal loan options#Loan for freelancers#Personal loan EMI#Best personal loan banks#Loan for business owners#Minimum loan requirements#Personal loan documents#Personal loan without payslip#How to get a loan without proof of income

0 notes

Text

Understanding UTI ICD 10 Codes and Their Importance in Billing

Urinary Tract Infections (UTIs) are one of the most common health issues that healthcare providers encounter daily. Accurate diagnosis and coding of UTIs are crucial for effective treatment and proper reimbursement from insurance providers.

One of the critical tools in ensuring that a UTI diagnosis is coded correctly is the UTI ICD 10 code. The ICD 10 system, which stands for the International Classification of Diseases, 10th Edition, is used worldwide to standardize the coding of diseases and medical conditions.

For healthcare providers, understanding the correct use of UTI ICD 10 codes is essential for both diagnosis and billing purposes. In this blog, we will delve into what UTI ICD 10 codes are, their significance, and how they impact patient care, insurance claims, and reimbursement.

Additionally, we will explore how partnering with a trusted billing company like Mava Care Medical Billing Company can ensure that UTI diagnoses are accurately coded, leading to better reimbursement and fewer claim rejections.

What is UTI ICD 10 Code?

The UTI ICD 10 code refers to a specific code used to classify urinary tract infections in the ICD 10 coding system. The ICD 10 codes are used to identify medical diagnoses in a standardized manner. These codes are crucial for documentation, billing, and reimbursement purposes, as they enable healthcare providers to communicate diagnoses and treatment procedures to insurance companies and other stakeholders.

There are several UTI-related ICD 10 codes, each representing different types of urinary tract infections. The most common codes include:

N39.0 - Urinary tract infection, site not specified: This code is used when the infection location is not clearly defined.

N30.0 - Acute cystitis: A code used for bladder infections, often associated with UTI.

N10 - Acute pyelonephritis: This refers to a kidney infection, a more severe form of UTI.

N12 - Tubulo-interstitial nephritis: Used for infections involving the kidney tubules.

Each of these codes helps healthcare providers communicate the exact nature of the UTI, which is essential for proper treatment and accurate billing. The correct application of these codes ensures that the patient’s medical history is well-documented and that healthcare providers can be reimbursed appropriately for their services.

The Importance of Correct UTI ICD 10 Coding:

Accurate coding is a fundamental part of the healthcare process for several reasons:

Proper Diagnosis and Treatment: When a healthcare provider correctly uses the UTI ICD 10 code, it ensures that the diagnosis is clear and specific. This can lead to more effective treatment plans for the patient, as the healthcare team can identify the exact type of infection and how best to address it.

Insurance Reimbursement:

Insurance companies use ICD 10 codes to determine the amount of reimbursement a healthcare provider will receive for a specific diagnosis or treatment. Incorrect coding can lead to claim denials or delays, meaning that healthcare providers may not get paid for their services.

By using the correct UTI ICD 10 code, healthcare providers can ensure they receive appropriate payment for their services.

Data Reporting and Research:

The ICD 10 coding system is used to track diseases and conditions on a global scale. This data is crucial for public health reporting, medical research, and resource allocation. Accurate UTI ICD 10 coding helps ensure that this information is reliable and useful for policymakers and researchers.

Compliance:

Healthcare providers must comply with numerous regulations and standards in the healthcare industry. Proper use of ICD 10 codes, including UTI-related codes, helps ensure compliance with the Health Insurance Portability and Accountability Act (HIPAA) and other regulatory requirements.

Reducing the Risk of Audit:

Incorrect coding can increase the risk of audits, which can be time-consuming and costly for healthcare providers. Accurate UTI ICD 10 coding reduces this risk and ensures that healthcare providers remain compliant with payer requirements.

Common UTI ICD 10 Coding Errors:

Despite its importance, many healthcare providers struggle with UTI ICD 10 coding due to its complexity. Common coding errors include:

Choosing the Wrong Code:

Sometimes, healthcare providers may select a code that is too broad or does not accurately reflect the type of UTI. For example, using a code for a simple bladder infection when a patient actually has a kidney infection can lead to issues with reimbursement or patient care.

Missing Documentation:

Incomplete or unclear documentation can result in incorrect coding. For instance, if a healthcare provider fails to document the site of the infection, they may be forced to use the generic UTI code, leading to less accurate billing.

Overuse of Non-Specific Codes:

While there are codes for "unspecified" UTI types, overuse of these codes can be problematic. Payers may require more detailed information before processing claims, so relying on non-specific codes can lead to claim denials.

Not Updating Codes:

ICD 10 codes are updated periodically. Failing to use the most recent codes or updates for UTI classifications can result in coding errors and missed reimbursement opportunities.

Want the full scoop? Click here to discover more: ,Understanding UTI ICD 10 Coding for Accurate Claims

How to Improve UTI ICD 10 Coding Accuracy:

To improve the accuracy of UTI ICD 10 coding, healthcare providers should consider the following best practices:

Train Medical Coders Regularly:

Ensure that all medical coders are thoroughly trained on the correct use of UTI ICD 10 codes. Regular training sessions can help coders stay up-to-date with the latest coding guidelines and prevent errors.

Ensure Comprehensive Documentation:

Accurate coding starts with comprehensive documentation. Healthcare providers should make sure that patient records include all the relevant details about the UTI, including the site of infection, severity, and any underlying conditions.

Use Specific Codes:

Whenever possible, healthcare providers should use specific codes for UTI diagnosis. Avoid using vague or unspecified codes unless absolutely necessary. The more specific the code, the more accurate the billing and reimbursement process will be.

Implement Automated Coding Systems:

Automated coding systems can help reduce human error and improve the efficiency of the coding process. These systems can automatically select the appropriate code based on the information entered by healthcare providers, reducing the risk of mistakes.

Outsource to Expert Billing Companies:

Many healthcare providers choose to outsource their billing and coding tasks to specialized companies. These companies have teams of experienced coders who are familiar with the nuances of ICD 10 codes, including those for UTIs.

By outsourcing to professionals like Mava Care Medical Billing Company, healthcare providers can ensure that their UTI ICD 10 coding is accurate and compliant.

Why Partner with Mava Care Medical Billing Company?

Mava Care Medical Billing Company is a trusted name in the healthcare billing industry. They specialize in medical coding services and offer expert solutions for healthcare providers across the USA. Here’s how Mava Care Medical Billing Company can help with UTI ICD 10 coding:

Expert Coders:

The team at Mava Care Medical Billing Company includes certified medical coders who are well-versed in ICD 10 codes, including those for UTIs. Their expertise ensures that codes are selected correctly, reducing the risk of errors.

Timely and Accurate Billing:

By outsourcing your UTI ICD 10 coding to Mava Care Medical Billing Company, you can ensure that your claims are submitted on time and are free from errors. This leads to faster reimbursement and fewer claim denials.

Comprehensive Coding Solutions:

Mava Care Medical Billing Company offers a wide range of billing and coding services, from initial coding to follow-up on claims. Their team ensures that your practice’s coding needs are handled efficiently, allowing you to focus on patient care.

Compliance Assurance:

Healthcare regulations and payer requirements are constantly changing. Mava Care Medical Billing Company stays up-to-date with these changes, ensuring that your coding practices remain compliant and accurate.

Cost-Effective Solutions:

Outsourcing your UTI ICD 10 coding to Mava Care Medical Billing Company can help reduce overhead costs associated with hiring and training in-house coders. Their services provide a cost-effective way to ensure accurate coding and timely reimbursement.

Conclusion:

Accurate UTI ICD 10 coding is crucial for effective diagnosis, treatment, and reimbursement in healthcare. By using the correct codes, healthcare providers can ensure that their practices remain compliant, avoid claim denials, and receive timely payments.

However, the complexity of the ICD 10 coding system can lead to errors, which can be costly for healthcare providers.

By partnering with a trusted billing company like Mava Care Medical Billing Company, healthcare providers can ensure that their UTI ICD 10 coding is accurate and efficient, ultimately improving their revenue cycle management.

With their team of experienced coders and advanced technology, Mava Care Medical Billing Company can help you streamline your billing processes and enhance patient care.

If you’re looking to improve the accuracy of your UTI ICD 10 coding and optimize your billing practices, consider working with Mava Care Medical Billing Company.

Their expertise and commitment to accuracy can help ensure your practice thrives in today’s complex healthcare environment.

#mavacare#medical billing company#medical billing services#healthcare#medical billing in usa#patient eligibility verification

0 notes

Text

Finnastra’s patient eligibility verification service ensures that insurance coverage is confirmed before appointments, streamlining your operations. This process not only prevents claim denials but also supports efficient billing cycles, allowing your team to focus on essential patient care. Our real-time verification methods simplify your workflow, enhance claim acceptance rates, and save valuable time by avoiding delays. Choose Finnastra’s eligibility solutions for smooth, reliable, and stress-free verification to keep revenue on track and your operations worry-free.

0 notes

Text

Key Benefits of a Clearinghouse Service

Learn about the crucial role of clearinghouse services in medical billing. This post explains how clearinghouses act as intermediaries, ensuring accurate claim submission, eligibility verification, and faster reimbursement for healthcare providers. See how reliable clearinghouse services can help streamline the billing process.

0 notes

Text

0 notes

Text

0 notes

Text

Simplify insurance verification with Adit — boost efficiency and enhance patient satisfaction in your dental practice!

0 notes

Text

Can Gig Workers Get a Personal Loan?

The gig economy has transformed the way people work, offering flexibility and independence. Gig workers, including freelancers, delivery agents, ride-hailing drivers, consultants, and digital creators, often face difficulties in securing personal loans due to the absence of a fixed salary. However, with the rise of alternative income verification methods and digital lending platforms, many banks and NBFCs now offer personal loans for gig workers.

In this article, we will explore how gig workers can qualify for a personal loan, the best loan options available, and the documents required for approval.

1. Can Gig Workers Qualify for a Personal Loan?

Yes! Even though gig workers may not have a fixed monthly salary, they can still qualify for personal loans by providing alternative income proof, such as bank statements, invoices, tax returns, or digital payment records. Many lenders assess an applicant’s financial stability by looking at their average income over several months rather than requiring a traditional salary slip.

2. Best Personal Loan Options for Gig Workers

2.1. Unsecured Personal Loans from Banks and NBFCs

Several banks and NBFCs now offer personal loans for self-employed individuals, including gig workers. These loans are based on average monthly earnings, credit score, and banking transactions.

Loan Amount: ₹50,000 – ₹25 lakh

Interest Rate: 11-24% per annum

Repayment Tenure: 12 to 60 months

Eligibility: Minimum annual income of ₹2-3 lakh, based on bank statements

🔗 Best Lenders for Gig Workers:

IDFC First Bank Personal Loan

Bajaj Finserv Personal Loan

Axis Finance Personal Loan

2.2. Digital Lending Platforms and FinTech Loans

Several FinTech lenders provide instant personal loans for gig workers by evaluating their digital transactions, UPI payments, and online earnings instead of traditional salary slips.

Loan Amount: ₹10,000 – ₹5 lakh

Interest Rate: 15-30% per annum

Approval Time: Within 24 hours

Repayment Tenure: 3 to 36 months

🔗 Top Digital Loan Apps for Gig Workers:

PaySense

MoneyTap

KreditBee

CASHe

These platforms offer instant loan approvals and allow repayment via EMIs, making them ideal for freelancers and gig workers who need quick access to funds.

2.3. Secured Loans Against Fixed Deposits, Gold, or Investments

For gig workers who struggle to get an unsecured loan, opting for a secured personal loan can increase approval chances. These loans are backed by collateral such as gold, a fixed deposit, or mutual funds.

Loan Amount: Up to 90% of the collateral value

Interest Rate: 7-12% per annum (lower than unsecured loans)

Repayment Tenure: Up to 7 years

Eligibility: No fixed income required; depends on asset value

🔗 Best Secured Loan Providers:

Tata Capital Personal Loan

Axis Bank Personal Loan

3. How Gig Workers Can Improve Loan Approval Chances

3.1. Maintain a High Credit Score

A credit score of 700+ significantly improves loan approval chances. Gig workers should: ✔ Pay credit card bills on time ✔ Avoid excessive loan applications ✔ Maintain a low credit utilization ratio

3.2. Show Consistent Income Proof

Lenders evaluate an applicant’s earning stability based on: ✔ Bank statements (last 6-12 months) ✔ Invoices from clients or payment platforms ✔ Income tax returns (ITR) for the last 2 years

3.3. Apply for a Loan with a Co-Applicant

Gig workers can increase their approval chances by applying with a salaried spouse, sibling, or parent as a co-applicant. This adds financial security for the lender.

3.4. Choose a Secured Loan

If a gig worker struggles with approval, opting for a loan against gold, fixed deposits, or mutual funds ensures faster approval and lower interest rates.

4. Eligibility Criteria for Gig Workers Applying for a Personal Loan

While each lender has different requirements, the general eligibility criteria for gig workers include:

Age: 21 to 60 years

Minimum Income: ₹2-3 lakh per annum

Credit Score: 650+ for unsecured loans

Work Experience: At least 1 year of self-employment or freelance work

Banking Transactions: Consistent earnings through bank transfers, UPI, or digital wallets

Lenders may also check past repayment history and existing liabilities before approving the loan.

5. Documents Required for Gig Workers to Get a Personal Loan

Since gig workers do not have salary slips, they must provide alternative documents to prove income stability and financial credibility.

5.1. Identity & Address Proof

Aadhaar Card

PAN Card

Passport or Voter ID

Utility Bill (for address verification)

5.2. Income Proof

Bank statements (last 6-12 months) showing consistent income

Payment receipts from clients, gig platforms, or apps

Income Tax Returns (ITR) for last 2 years

Profit and Loss Statement (if applicable)

5.3. Additional Documents (if required by the lender)

GST registration certificate (for self-employed individuals)

Digital earnings report from PayPal, Razorpay, or UPI transactions

Collateral documents (for secured loans)

6. How to Apply for a Personal Loan as a Gig Worker?

Applying for a personal loan as a gig worker is simple and can be done online or offline. Follow these steps:

Step 1: Compare Loan Offers

Check interest rates, loan amounts, and repayment terms from multiple lenders to find the best deal.

Step 2: Check Eligibility

Ensure you meet the income, credit score, and banking history requirements.

Step 3: Gather Required Documents

Keep identity proof, bank statements, and income proof ready for submission.

Step 4: Submit Loan Application

Apply online through the lender’s website or visit the nearest bank branch to submit a physical application.

Step 5: Loan Disbursement

Once the application is approved, the loan amount is credited to your bank account within a few days.

Best Loan Options for Gig Workers

Even though gig workers face challenges in securing traditional personal loans, many banks and NBFCs now provide flexible loan options based on digital earnings, alternative income proof, and secured collateral.

By maintaining a high credit score, showing stable income, and applying with a co-applicant, gig workers can successfully secure a personal loan to meet their financial needs.

🔗 Apply for a Personal Loan Today:

Explore Personal Loans

With the rise of digital lending solutions, getting a personal loan as a gig worker has become easier than ever!

#finance#nbfc personal loan#personal loans#loan services#personal loan online#bank#fincrif#loan apps#personal laon#personal loan#Personal loan for gig workers#Freelancer personal loan#Loan options for self-employed individuals#Personal loan for independent contractors#How gig workers can get a personal loan#Best loans for gig economy workers#Unsecured loans for freelancers#Loan eligibility for gig workers#Self-employed loan approval#Instant loans for gig workers#Personal loan without salary slip#Gig worker financial assistance#Alternative income proof for personal loans#How to qualify for a loan as a freelancer#Digital lending for self-employed#Low-interest loans for independent workers#Best banks for freelancer loans#Personal loan approval for non-salaried individuals#Gig worker income verification for loans#Loan against digital earnings

0 notes