#Medical Robotics Market Overview

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The KCSC sent more than 20K requests to delete posts related to prostitution and porn to Tumblr from January to June 2017.

Text

The Medical Robotics Market in 2023 is US$ 13.53 billion, and is expected to reach US$ 44.07 billion by 2031 at a CAGR of 15.91%.

0 notes

Text

#intellectualmarketinsights#Global Medical Robotics Market Overview#Size#Share#Top Companies#Growth Will Expand at a CAGR of 22.19% by 2028

0 notes

Text

How Israeli Tech is Shaping the Future of Additive Manufacturing Worldwide

Overview of Israel’s Strategic Position in Additive Manufacturing

Israel has rapidly emerged as a global force in additive manufacturing (AM), fortified by a powerful high-tech ecosystem, robust government support, and a legacy of innovation in defense, aerospace, and medical technologies. With the Israel additive manufacturing market valued at USD 221.4 billion in 2024 and forecasted to exceed USD 280.3 billion by 2032, the nation is positioned to lead transformative advances in 3D printing technologies. The Israel additive manufacturing market compound annual growth rate (CAGR) of approximately 7% reflects both escalating domestic demand and global interest in Israeli AM innovation.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40589-israel-additive-manufacturing-market-research

Driving Forces of Growth in Israel's Additive Manufacturing Market

Innovation Across Key Industrial Verticals

Israel additive manufacturing market sector is evolving as a backbone for modernization in:

Aerospace and Defense: Lightweight components, complex geometries, and high-performance materials enable operational efficiency and reduced lead times.

Healthcare: Customized prosthetics, implants, bioprinting, and surgical models offer patient-centric care and improved clinical outcomes.

Automotive and Industrial Manufacturing: Rapid prototyping, tooling, and small-batch production optimize supply chains and cut production timelines.

These sectors benefit from the convergence of additive technologies with AI, machine learning, and advanced robotics, all core competencies of Israel's high-tech sector.

Rising Demand for Customization and Sustainability

The shift toward sustainable manufacturing and personalized solutions is fueling AM adoption. Israeli startups and research institutions are developing biocompatible, recyclable, and multi-material printing solutions that meet stringent regulatory and industry-specific standards.

Get up to 30%-40% Discount: https://www.statsandresearch.com/check-discount/40589-israel-additive-manufacturing-market-research

Technological Landscape of the Israeli Additive Manufacturing Ecosystem

Polymer-Based Additive Manufacturing

Valued at USD 306.31 million in 2024, this segment dominates due to its cost-effectiveness, versatility, and compatibility with lightweight, complex part production. With an expected CAGR of 17.3%, applications in consumer goods, automotive interiors, and medical devices continue to surge.

Metal-Based Additive Manufacturing

Growing at a robust 20.1% CAGR, metal AM is the cornerstone of defense and aerospace advancements. In 2024, it accounted for USD 180.86 million, projected to exceed USD 775.48 million by 2032. Israel’s focus on titanium, aluminum alloys, and nickel-based superalloys supports structural applications with high thermal and mechanical stability.

Hybrid Additive Manufacturing

By blending subtractive and additive processes, hybrid AM enhances surface finish and dimensional accuracy, critical in precision tooling, aerospace, and dental prosthetics. This segment is rapidly gaining traction due to its versatility and integration into smart manufacturing systems.

Segmental Breakdown of the Israel Additive Manufacturing Market

By Component

Hardware: Represents the largest share, valued at USD 1,137.28 million in 2024, supporting high-throughput production and industrial-scale fabrication.

Software: Fueled by AI-powered design, generative modeling, and process simulation, this segment is experiencing 19.9% CAGR, revolutionizing digital twin applications and real-time process monitoring.

Services: The on-demand printing ecosystem is expanding, empowering SMEs to access advanced AM capabilities with minimal capital expenditure.

By Deployment Model

In-House Manufacturing: With a Israel additive manufacturing market valuation of USD 317.09 million in 2024, large enterprises prefer internal AM operations for confidentiality and operational control.

Service-Based Models: Growing at 19.4% CAGR, third-party service bureaus are crucial in democratizing access to advanced AM technologies for startups and research institutions.

By Functionality

Prototyping: Dominates with USD 340.60 million in 2024, essential for R&D, iterative design, and proof-of-concept validation.

Production: The rising shift to end-use part manufacturing is catalyzing growth in this segment, valued at USD 197.73 million in 2024.

Tooling: Customized, high-durability tooling supports faster transitions from design to production across various industrial sectors.

By Printer Size

Small/Compact Printers: Most accessible and dominant segment, valued at USD 253.09 million in 2024, ideal for labs, healthcare, and educational institutions.

Medium and Large Printers: Increasingly adopted in industrial manufacturing, these enable batch production and larger component fabrication.

End-Use Industries Driving Adoption

Aerospace & Defense

USD 159.32 million in 2024, this sector prioritizes weight reduction, material performance, and supply chain agility. With Israel’s defense sector being R&D intensive, 3D printing significantly enhances manufacturing autonomy and mission-readiness.

Healthcare & Medical

USD 131.40 million in 2024, growing due to demand for patient-specific devices, bioprinted tissues, and anatomical models. With innovations in regenerative medicine, Israel is at the forefront of personalized healthcare.

Industrial & Automotive

Israel’s industrial ecosystem leverages AM for lightweighting, thermal management, and low-volume production, especially in EV components and robotics enclosures.

Strategic Movements and Competitive Intelligence

Leading Israel Additive Manufacturing Market Participants

Stratasys: A global pioneer, deeply rooted in Israel, with continuous development in multi-material, high-resolution systems.

XJet: Revolutionizing ceramic and metal printing with NanoParticle Jetting™ technology.

Nano Dimension: Innovator in multi-layer electronics and PCB printing, driving miniaturization and functional integration.

Recent Developments

XJet (June 2024): Launched new ceramic printers with applications in automotive and aerospace, enhancing resolution and mechanical strength.

Nano Dimension (Sept 2024): Acquired startups to advance multi-material electronics printing, expanding their capabilities in embedded sensor systems.

Challenges and Strategic Opportunities

Major Israel Additive Manufacturing Market Challenges

Capital Intensity: High upfront costs limit adoption, especially among SMEs.

Talent Gap: Scarcity of AM-trained professionals hampers rapid scaling.

Scaling Complexity: Transitioning from prototype to full production requires new QA methodologies and workflow optimization.

Strategic Israel Additive Manufacturing Market Opportunities

Workforce Development: Partnerships with universities and technical institutes to offer AM-centric curricula.

Material Innovation Hubs: Support from government and private sectors to develop high-strength composites, bioresorbable materials, and nanostructured alloys.

Sustainability Mandates: Incentives for closed-loop manufacturing systems, energy-efficient printers, and recyclable materials.

Future Outlook: Israel’s Role in Global Additive Manufacturing Leadership

Israel is poised to lead the next frontier of digital manufacturing, where data-driven fabrication, machine learning-enhanced design, and autonomous production lines define industry 4.0. With unmatched cross-sector collaboration between startups, research centers, and government agencies, the nation’s AM sector is evolving from rapid prototyping to full-fledged production infrastructure.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40589-israel-additive-manufacturing-market-research

Conclusion

Israel additive manufacturing market is entering a golden era, driven by its technological prowess, strategic policy initiatives, and vibrant innovation culture. As the global demand for agile, sustainable, and customized manufacturing solutions intensifies, Israel is uniquely equipped to lead the charge. Enterprises, investors, and policy makers must align to fully harness this momentum and establish Israel as a global additive manufacturing powerhouse.

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

#Israel#Additive Manufacturing#3D Printing#Israeli Tech#Advanced Manufacturing#Industrial 3D Printing#Aerospace#Medical Devices#Defense Technology#Innovation#Startups#Tel Aviv#Prototyping#Manufacturing Industry#AM Materials#Digital Manufacturing#Smart Manufacturing#High-Tech Industry#Metal 3D Printing#Polymer Printing#R&D#Technology Trends#Engineering#Robotics#Supply Chain#Product Development

1 note

·

View note

Text

Personal Service Robotics Market Share Revolutionizing Daily Life Through Intelligent Assistance

The Personal Service Robotics Market Share is rapidly transforming the way individuals interact with technology in their daily lives. From robotic vacuum cleaners and lawn mowers to personal assistants and eldercare robots, these intelligent systems are enhancing convenience, safety, and quality of life across diverse households and institutions.

According to Market Share Research Future, the global personal service robotics market is projected to reach USD 94.3 billion by 2030, growing at an impressive CAGR of 38.6% during the forecast period. This exceptional growth is driven by technological advancements in artificial intelligence (AI), machine learning, sensors, and edge computing, coupled with increasing demand for domestic automation and aging population care.

Market Share Overview

Personal service robots are semi-autonomous or fully autonomous machines designed to assist individuals with non-commercial tasks. These robots are typically used in residential, healthcare, entertainment, and educational settings to perform chores, provide companionship, aid the elderly, or assist people with disabilities.

The rapid integration of intelligent voice assistants, improved computer vision, and wireless connectivity has significantly advanced the capabilities of these robots. With consumers becoming more comfortable with AI-powered devices and smart homes, the personal robotics segment is poised for accelerated adoption in the coming years.

Enhanced Market Share Segmentation

By Product Type:

Domestic Robots

Vacuuming and Cleaning Robots

Lawn Mowing Robots

Window Cleaning Robots

Entertainment and Leisure Robots

Elderly and Handicap Assistance Robots

Security and Surveillance Robots

Educational Robots

Companion Robots

By Component:

Hardware

Sensors

Actuators

Controllers

Power Supply

Software

AI Algorithms

Navigation and Control Software

Voice Recognition and Natural Language Processing (NLP)

By Connectivity:

Wi-Fi

Bluetooth

Zigbee

Cloud-Based Systems

By End-User:

Residential

Healthcare

Educational Institutions

Assisted Living Facilities

By Region:

North America – Leading due to high disposable income and tech awareness

Europe – Growing demand for eldercare robotics

Asia-Pacific – Fastest-growing region, driven by smart home trends and aging demographics in Japan, South Korea, and China

Rest of the World – Emerging opportunities in the Middle East and Latin America

Trends Driving Market Share Growth

AI and Machine Learning Integration: Robots are becoming increasingly intelligent, capable of learning user behavior and improving task performance over time.

Rise of Companion Robots: Emotional AI is enabling robots to detect mood and respond empathetically, especially for mental health and eldercare applications.

Voice Assistant Integration: Integration with Alexa, Google Assistant, and Siri enhances functionality, enabling seamless interaction with smart homes.

Affordable and Modular Designs: Open-source platforms and modular hardware are reducing entry costs and encouraging customization for individual needs.

Sustainability and Energy Efficiency: Many robots now offer energy-saving modes and recyclable components, aligning with global sustainability goals.

Segment Insights

Domestic Service Robots

Domestic robots, particularly robotic vacuum cleaners and lawn mowers, dominate the market. Their popularity is due to time-saving convenience, affordability, and improved suction/navigation capabilities. With smart mapping and AI-based dirt detection, these products continue to gain mass-market appeal.

Elderly Assistance Robots

As populations age globally, particularly in Japan and Europe, robots for mobility support, medication reminders, fall detection, and companionship are seeing strong adoption. These robots are designed to promote independent living and reduce caregiver burden.

Educational Robots

Educational institutions are adopting interactive robots for STEM learning. These robots help children understand coding, AI, and mechanical design through hands-on activities.

End-User Insights

Residential Consumers

This is the largest end-user segment. Smart homes equipped with IoT devices are becoming fertile grounds for robotic assistants. Convenience, cleanliness, and connectivity are top priorities for consumers.

Healthcare Sector

Hospitals and assisted living facilities use robots for patient monitoring, rehabilitation assistance, and delivering medication or food. Robots reduce repetitive tasks for medical staff, improving efficiency and safety.

Elderly Care Facilities

These institutions leverage robots for mobility support, cognitive stimulation, and constant monitoring. With increasing senior populations, demand for robotic caregivers will continue to rise.

Educational Institutions

Schools and after-school programs integrate robots into their curriculum to encourage early adoption of technology and problem-solving skills among students.

Key Players

Leading companies are investing heavily in AI, user-centric design, and market-specific innovations to expand their offerings:

iRobot Corporation

SoftBank Robotics

Intuitive Surgical, Inc.

Blue Frog Robotics

Sony Corporation

Samsung Electronics

LG Electronics

Honda Motor Co., Ltd.

Ubtech Robotics

Xiaomi Corporation

These companies are continuously improving product features like obstacle avoidance, interactive learning, and multilingual voice support to cater to diverse user bases.

Future Outlook

The future of the personal service robotics market lies in intelligent, emotionally aware, and fully autonomous robots that adapt to dynamic environments. Innovations in tactile sensors, cloud robotics, edge AI, and 5G connectivity will further enhance real-time performance and expand use cases.

With increasing societal acceptance and affordability, personal robots will evolve from luxury gadgets to indispensable household companions, supporting wellness, learning, and productivity.

Trending Report Highlights

Explore insights from rapidly growing tech and automation markets:

Ultrasonic Testing Market Share

USB Cable Market Share

Utility Marker Market Share

UV Light Stabilizer Market Share

Vehicle Occupancy Detection System Market Share

Ethernet Storage Fabric Market Share

Reference Thermometer Market Share

Retail Display Market Share

RF Isolator Market Share

RF Transistor Market Share

RFID Sensor Market Share

Sound Level Meter Market Share

0 notes

Text

Compressed Load Cell Market: Forecast and Competitive Overview 2025–2032

Global Compressed Load Cell Market size was valued at US$ 284.6 million in 2024 and is projected to reach US$ 438.9 million by 2032, at a CAGR of 6.4% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China’s market is expected to grow at a faster CAGR of 6.8% through 2032.

Compressed load cells are precision force measurement devices designed to operate under compressive loads. These robust sensors convert mechanical force into electrical signals through strain gauge technology, enabling accurate weight and force measurement across industrial applications. Key product variants include analogue and digital compressed load cells, with analogue types currently dominating 62% of market share.

Market growth is being driven by increasing automation in manufacturing, stricter quality control requirements, and the expansion of material testing applications. The industrial sector remains the primary end-user, accounting for 45% of 2024 revenues, particularly in heavy equipment monitoring and process weighing systems. Recent developments include TE Connectivity’s 2023 launch of its Model 3130 high-capacity load cell series, featuring improved overload protection and temperature compensation for harsh environments.

Get Full Report : https://semiconductorinsight.com/report/compressed-load-cell-market/

MARKET DYNAMICS

MARKET DRIVERS

Industrial Automation Boom Accelerates Demand for Compressed Load Cells

The global surge in industrial automation adoption is creating substantial demand for precision measurement devices like compressed load cells. Manufacturing facilities across automotive, aerospace, and heavy industries are increasingly integrating automated systems that require accurate force measurement capabilities. Recent data indicates that over 80% of industrial facilities now use some form of automation, with compressed load cells becoming critical components in robotic assembly lines, quality control stations, and material testing applications. The transition to Industry 4.0 standards has particularly boosted adoption, as these sensors enable real-time monitoring and data collection essential for smart manufacturing processes. Several leading manufacturers have reported 20-25% annual growth in orders from automation integrators, reflecting this strong market trend.

Medical Equipment Advancements Drive Specialized Load Cell Requirements

The healthcare sector’s rapid technological evolution is creating new opportunities for compressed load cell applications. Modern medical devices, from surgical robots to advanced patient monitoring systems, increasingly incorporate miniature load cells for precise force measurement. The medical equipment market’s projected 7% annual growth directly correlates with rising demand for sensor components. Compressed load cells are particularly valuable in applications requiring high accuracy within compact form factors, such as prosthetic limb pressure sensors and minimally invasive surgical tools. Recent product launches in the rehabilitation equipment segment have specifically highlighted integrated load cell technology as a key differentiator, with manufacturers emphasizing durability and measurement consistency.

Transportation Safety Regulations Spur Market Growth

Stricter global transportation safety standards are accelerating compressed load cell adoption across vehicle and infrastructure applications. Regulatory mandates now frequently require weight monitoring systems in commercial vehicles, aircraft landing gear, and railway components – all areas where compressed load cells provide ideal solutions. The commercial vehicle sector alone accounts for approximately 35% of transportation-related load cell deployments. Emerging applications in electric vehicle battery pack monitoring and autonomous vehicle systems further expand market potential. Recent policy developments in multiple regions have specifically referenced load measurement accuracy requirements, driving OEMs to upgrade their sensor technologies.

MARKET RESTRAINTS

High Precision Requirements Limit Adoption in Cost-Sensitive Segments

While compressed load cells offer superior performance, their technical complexity and precision manufacturing requirements result in higher costs that deter price-sensitive markets. Entry-level industrial applications often prioritize affordability over measurement accuracy, opting for simpler sensor solutions. The price differential can exceed 200-300% between basic force sensors and high-end compressed load cells, creating a significant adoption barrier. Price pressures are particularly acute in developing markets, where budget constraints limit technology upgrades despite growing awareness of load cell advantages. This challenge is compounded by the need for compatible instrumentation and regular calibration, which adds to total cost of ownership.

Other Restraints

Supply Chain Vulnerabilities The compressed load cell market remains susceptible to disruptions in rare material supply chains, particularly for specialized strain gauge components. Recent geopolitical tensions and trade restrictions have created lead time uncertainties for certain critical materials, forcing manufacturers to maintain larger inventories and impacting production flexibility.

Technical Integration Challenges Implementing compressed load cells in existing systems often requires substantial engineering modifications, deterring retrofits. Compatibility issues with legacy equipment and the need for specialized installation expertise present additional hurdles, particularly for small and medium enterprises lacking in-house technical resources.

MARKET CHALLENGES

Technical Expertise Shortage Constrains Market Expansion

The compressed load cell industry faces a critical shortage of skilled professionals capable of designing, installing, and maintaining these precision measurement systems. As sensor technology becomes more sophisticated, the gap between available workforce capabilities and technical requirements continues to widen. Industry surveys indicate that over 60% of manufacturers struggle to find qualified personnel for quality control and field service roles. This talent shortage not only limits production capacity but also delays implementation timelines for end-users, potentially slowing overall market growth. The challenge is particularly acute in emerging markets where specialized technical education programs remain underdeveloped.

Emerging Competitive Technologies Alternative force measurement technologies, including optical and capacitive sensors, are gaining traction in certain applications traditionally served by compressed load cells. While these alternatives currently lack the robustness and measurement range of load cells, their improving performance in specific niches creates competitive pressure. Some industry analysts predict these technologies could capture up to 15-20% of current load cell applications within the next decade, particularly in miniaturized and high-cycle applications where they offer potential advantages.

MARKET OPPORTUNITIES

Renewable Energy Sector Presents Untapped Potential

The rapid expansion of renewable energy infrastructure creates significant opportunities for compressed load cell applications. Wind turbine manufacturers increasingly incorporate load monitoring systems into blade and tower designs, while solar tracking systems benefit from precise force measurement in positioning mechanisms. The global wind energy market alone is projected to require over 500,000 specialized load cells annually by 2030. These applications often demand ruggedized designs capable of withstanding harsh environmental conditions, presenting both technical challenges and premium pricing opportunities for manufacturers that can deliver suitable solutions.

Smart City Initiatives Drive Infrastructure Monitoring Demand

Urban infrastructure modernization programs worldwide are creating new markets for structural health monitoring systems that utilize compressed load cells. Bridge safety monitoring, smart building technologies, and advanced public transportation systems all require precise force measurement capabilities. Pilot programs in major cities have demonstrated 30-40% improvements in maintenance efficiency through load cell-enabled predictive maintenance systems. As municipalities increasingly adopt IoT-enabled infrastructure management solutions, the demand for reliable, networked load measurement devices continues to grow. This trend is particularly pronounced in Asia-Pacific regions, where new urban development projects frequently incorporate smart technologies from initial construction phases.

Material Science Breakthroughs Enable Novel Applications

Advances in composite materials and nanotechnology are expanding the performance boundaries of compressed load cells, creating opportunities in previously inaccessible markets. New strain gauge materials with enhanced sensitivity and temperature stability enable applications in extreme environments, from deep-sea exploration to aerospace testing. Similarly, developments in wireless power and data transmission allow for completely self-contained load cell designs suitable for rotating machinery and mobile equipment. Manufacturers investing in these advanced material technologies gain competitive advantages in high-value market segments while establishing intellectual property barriers against lower-cost competitors.

COMPRESSED LOAD CELL MARKET TRENDS

Industrial Automation and Smart Factories Driving Demand for Compressed Load Cells

The global compressed load cell market is experiencing significant growth due to increasing adoption in industrial automation and smart manufacturing facilities. With Industry 4.0 implementations accelerating worldwide, manufacturers are incorporating precision weighing systems in production lines for quality control and process optimization. Compressed load cells play a critical role in these applications, offering high accuracy measurements in confined spaces. The market valuation reached $490 million in 2024, with projections indicating a robust 6.8% CAGR through 2032. Growth is particularly strong in pharmaceutical manufacturing and food processing industries where regulatory compliance mandates precise weight measurements at various production stages.

Other Trends

Healthcare Sector Adoption

Medical applications are emerging as a key growth segment for compressed load cells, driven by advancements in patient monitoring systems and surgical equipment. Hospitals are increasingly using these sensors in rehabilitation devices, patient lift systems, and medical beds to monitor weight distribution and prevent pressure injuries. The trend toward telehealth and remote patient monitoring has further increased demand for compact, high-precision load cells that can integrate with IoT-enabled medical devices. This healthcare segment is projected to grow at 8.2% annually through 2030.

Technological Advancements in Sensor Design

Manufacturers are focusing on developing next-generation compressed load cells with improved durability and measurement capabilities. Recent innovations include wireless load cells with battery-powered operation, smart load cells with integrated Bluetooth connectivity, and ultra-compact designs for space-constrained applications. The introduction of corrosion-resistant materials like titanium and specialized alloys has expanded usage in harsh industrial environments. Additionally, advancements in signal processing technology have enhanced measurement accuracy to ±0.02% of full scale, making these sensors viable for critical applications in aerospace and defense sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Market Competition in Compressed Load Cell Segment

The global compressed load cell market features a semi-consolidated competitive landscape with AMETEK, FUTEK Advanced Sensor Technology, and Honeywell emerging as dominant players. These companies collectively held approximately 35-40% market share in 2024, according to industry analysis. Their leadership stems from comprehensive product portfolios covering both analogue and digital compressed load cells, coupled with strong distribution networks across North America and Europe.

METTLER TOLEDO and Vishay Precision Group have strengthened their positions through strategic acquisitions and expanded manufacturing capabilities. The companies reported year-over-year revenue growth of 8-12% in their industrial measurement segments during 2023-2024, with compressed load cells contributing significantly to this performance.

While established players dominate the premium segment, mid-sized companies like TE Connectivity and Interface, Inc. are gaining traction in emerging markets through competitive pricing and localized support. These firms have successfully penetrated the Asian market, particularly in China and India, where industrial automation demand continues to rise.

Regional players such as LAUMAS Elettronica (Italy) and Celmi (Spain) maintain strong positions in European specialty applications, particularly in food processing and pharmaceutical industries where precision measurement requirements are stringent.

List of Key Compressed Load Cell Manufacturers

AMETEK (U.S.)

FUTEK Advanced Sensor Technology, Inc. (U.S.)

Honeywell (U.S.)

METTLER TOLEDO (Switzerland)

Vishay Precision Group (U.S.)

TE Connectivity (Switzerland)

Interface, Inc. (U.S.)

HBM (Germany)

LAUMAS Elettronica (Italy)

Celmi (Spain)

Siemens (Germany)

WIKA (Germany)

GEFRAN (Italy)

Sherborne Sensors (U.K.)

Dini Argeo (Italy)

Segment Analysis:

By Type

Analogue Compressed Load Cell Segment Dominates Due to Widespread Industrial Adoption

The market is segmented based on type into:

Analogue Compressed Load Cell

Subtypes: High-capacity, Medium-capacity, Low-capacity

Digital Compressed Load Cell

By Application

Industrial Segment Leads Owing to High Utilization in Manufacturing and Process Industries

The market is segmented based on application into:

Industrial

Medical

Transportation

Others

By Capacity

Medium-capacity Segment Maintains Strong Position for General Industrial Applications

The market is segmented based on capacity into:

High-capacity (Above 100 tons)

Medium-capacity (10-100 tons)

Low-capacity (Below 10 tons)

By Technology

Strain Gauge Technology Remains Predominant Due to Reliability and Accuracy

The market is segmented based on technology into:

Strain gauge

Hydraulic

Piezoelectric

Others

Regional Analysis: Compressed Load Cell Market

North America North America is a mature yet highly competitive market for compressed load cells, driven by stringent industrial safety standards (OSHA, ANSI) and widespread automation adoption. The U.S. dominates with a projected 2024 valuation of $XX million, fueled by demand from aerospace (Boeing, Lockheed Martin) and advanced manufacturing sectors. Canada’s oil & gas industry is adopting explosion-proof load cells for hazardous environments, while Mexico’s automotive OEMs are integrating these sensors into production line robotics. The region faces pricing pressures due to commoditization of analog load cells, pushing manufacturers toward IoT-enabled digital solutions with real-time data analytics capabilities.

Europe European demand is shaped by the ATEX Directive’s explosion protection requirements and the push for Industry 4.0 compliance. Germany leads in precision manufacturing applications (65% of regional industrial demand), particularly in automotive test benches and pharmaceutical packaging lines. Scandinavian countries are early adopters of wireless load cells for offshore renewables maintenance. However, CE certification complexities and high labor costs constrain SME adoption. The market sees consolidation among mid-tier players – HBM and Flintec merged in 2022 to strengthen their position in custom load cell solutions.

Asia-Pacific APAC is the fastest-growing market (CAGR 7.2% 2024-2032), with China accounting for 40% regional share due to booming construction machinery production (+18% YoY). Japan’s emphasis on miniaturization drives demand for micro load cells in robotics, while India’s Make in India initiative boosts local sensor manufacturing. Southeast Asian food processing plants increasingly use stainless steel load cells for hygienic weighing. Price sensitivity remains acute, with domestic players like Zhenghua undercutting Western brands by 30-50%. Digital twin adoption in smart factories is creating new opportunities for networked load monitoring systems.

South America Market growth is uneven, with Brazil’s mining sector (Vale, Petrobras) driving bulk weighing demand and Argentina’s economic crisis suppressing industrial investment. Chile’s copper industry uses heavy-capacity load cells (>500t) for haul truck payload monitoring. Infrastructure gaps in product certification labs force reliance on imported, pre-certified load cells. Local assembly is emerging – Bráulio & Cia now produces IP68-rated compression load cells under license from European partners. Political instability continues to deter major FDI in regional sensor manufacturing facilities.

Middle East & Africa The GCC’s oilfield services sector is the primary adopter, using intrinsically safe load cells for drilling equipment monitoring. UAE’s logistics hubs deploy compression load cells in automated cargo handling systems. Africa’s growth is piecemeal – South African mining and Nigerian food processing account for 72% of Sub-Saharan demand. Import dependence remains high (85% of supply) due to limited local technical expertise in strain gauge manufacturing. Recent trade agreements are enabling Turkish and Indian manufacturers to gain market share with competitively priced offerings compliant with ISO 17025 standards.

Get a detailed Sample of the Market Research Report : https://semiconductorinsight.com/download-sample-report/?product_id=97913

Report Scope

This market research report provides a comprehensive analysis of the global and regional Compressed Load Cell markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Compressed Load Cell market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Analogue/Digital), application (Industrial, Medical, Transportation, Others), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

Competitive Landscape: Profiles of 40+ leading manufacturers including ACRN, ADOS, AMETEK, FUTEK, HBM, Honeywell, METTLER TOLEDO, and TE Connectivity, with their market shares and strategic developments.

Technology Trends: Assessment of emerging innovations in load cell design, materials, IoT integration, and smart sensor technologies.

Market Drivers & Restraints: Evaluation of industrial automation growth, accuracy requirements, versus cost pressures and supply chain challenges.

Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors in the measurement technology ecosystem.

The research employs primary interviews with industry experts and validated secondary data from financial reports, trade associations, and patent analysis to ensure accuracy.

Customisation of the Report

In case of any queries or customisation requirements, please connect with our sales team, who will ensure that your requirements are met.

Related Reports :

Contact us:

+91 8087992013

0 notes

Text

Canada Artificial Organs and Bionic Implants Market Guide 2025: From Procurement to Deployment

Canada Artificial Organs and Bionic Implants Market was valued at USD X.X Billion in 2024 and is projected to reach USD X.X Billion by 2032, growing at a CAGR of X.X% from 2026 to 2032. What are the key factors driving the growth of the artificial organs and bionic implants market in Canada? The growth of the artificial organs and bionic implants market in Canada is primarily driven by several factors. Firstly, the increasing prevalence of chronic diseases such as cardiovascular disorders, diabetes, and kidney failure has heightened the demand for alternative treatment options. For instance, in 2022, an estimated 750,000 Canadians were living with heart failure, with 100,000 new diagnoses each year. Secondly, the aging population contributes significantly to the rise in organ failures, necessitating advanced medical solutions. Additionally, the scarcity of organ donors exacerbates the need for artificial organs and bionic implants. Government initiatives, including investments in research and development, further support the market's expansion. Technological advancements in biocompatible materials, robotics, and artificial intelligence have enhanced the functionality and accessibility of these devices, making them more effective and patient-friendly. Moreover, increased awareness and acceptance among healthcare professionals and patients have facilitated the adoption of these technologies. Lastly, the integration of artificial intelligence and machine learning into medical devices has improved real-time monitoring and personalized treatment, thereby boosting market growth. Get | Download Sample Copy with TOC, Graphs & List of Figures @ https://www.verifiedmarketresearch.com/download-sample/?rid=468227&utm_source=PR-News&utm_medium=205 The report covers extensive analysis of the key market players in the market, along with their business overview, expansion plans, and strategies. The key players studied in the report include: Synaptive Medical MyndTec Inc. MacDonald Dettwiler and Associates (MDA) Bionik Laboratories Invivo Myomo Ottobock Ossur ReWalk Robotics and Touch Bionics. Canada Artificial Organs and Bionic Implants Market Segmentation By Type of Machinery By Application By Stone Type By Geography • North America• Europe• Asia Pacific• Latin America• Middle East and Africa The comprehensive segmental analysis offered in the report digs deep into important types and application segments of the Canada Artificial Organs and Bionic Implants Market. It shows how leading segments are attracting growth in the Canada Artificial Organs and Bionic Implants Market. Moreover, it includes accurate estimations of the market share, CAGR, and market size of all segments studied in the report. Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount/?rid=468227&utm_source=PR-News&utm_medium=205 The regional segmentation study is one of the best offerings of the report that explains why some regions are taking the lead in the Canada Artificial Organs and Bionic Implants Market while others are making a low contribution to the global market growth. Each regional market is comprehensively researched in the report with accurate predictions about its future growth potential, market share, market size, and market growth rate. Geographic Segment Covered in the Report: • North America (USA and Canada) • Europe (UK, Germany, France and the rest of Europe) • Asia Pacific (China, Japan, India, and the rest of the Asia Pacific region) • Latin America (Brazil, Mexico, and the rest of Latin America) • Middle East and Africa (GCC and rest of the Middle East and Africa) Key questions answered in the report: • What is the growth potential of the Canada Artificial Organs and Bionic Implants Market? • Which product segment will take the lion's share? • Which regional market will emerge as a pioneer in the years to come? • Which application segment will experience strong growth? • What growth opportunities

might arise in the Welding industry in the years to come? • What are the most significant challenges that the Canada Artificial Organs and Bionic Implants Market could face in the future? • Who are the leading companies on the Canada Artificial Organs and Bionic Implants Market? • What are the main trends that are positively impacting the growth of the market? • What growth strategies are the players considering to stay in the Canada Artificial Organs and Bionic Implants Market? For More Information or Query or Customization Before Buying, Visit @ https://www.verifiedmarketresearch.com/product/canada-artificial-organs-and-bionic-implants-market/ Detailed TOC of Global Canada Artificial Organs and Bionic Implants Market Research Report, 2023-2030 1. Introduction of the Canada Artificial Organs and Bionic Implants Market Overview of the Market Scope of Report Assumptions 2. Executive Summary 3. Research Methodology of Verified Market Research Data Mining Validation Primary Interviews List of Data Sources 4. Canada Artificial Organs and Bionic Implants Market Outlook Overview Market Dynamics Drivers Restraints Opportunities Porters Five Force Model Value Chain Analysis 5. Canada Artificial Organs and Bionic Implants Market, By Product 6. Canada Artificial Organs and Bionic Implants Market, By Application 7. Canada Artificial Organs and Bionic Implants Market, By Geography North America Europe Asia Pacific Rest of the World 8. Canada Artificial Organs and Bionic Implants Market Competitive Landscape Overview Company Market Ranking Key Development Strategies 9. Company Profiles 10. Appendix About Us: Verified Market Research® Verified Market Research® is a leading Global Research and Consulting firm that has been providing advanced analytical research solutions, custom consulting and in-depth data analysis for 10+ years to individuals and companies alike that are looking for accurate, reliable and up to date research data and technical consulting. We offer insights into strategic and growth analyses, Data necessary to achieve corporate goals and help make critical revenue decisions. Our research studies help our clients make superior data-driven decisions, understand market forecast, capitalize on future opportunities and optimize efficiency by working as their partner to deliver accurate and valuable information. The industries we cover span over a large spectrum including Technology, Chemicals, Manufacturing, Energy, Food and Beverages, Automotive, Robotics, Packaging, Construction, Mining & Gas. Etc. We, at Verified Market Research, assist in understanding holistic market indicating factors and most current and future market trends. Our analysts, with their high expertise in data gathering and governance, utilize industry techniques to collate and examine data at all stages. They are trained to combine modern data collection techniques, superior research methodology, subject expertise and years of collective experience to produce informative and accurate research. Having serviced over 5000+ clients, we have provided reliable market research services to more than 100 Global Fortune 500 companies such as Amazon, Dell, IBM, Shell, Exxon Mobil, General Electric, Siemens, Microsoft, Sony and Hitachi. We have co-consulted with some of the world’s leading consulting firms like McKinsey & Company, Boston Consulting Group, Bain and Company for custom research and consulting projects for businesses worldwide. Contact us: Mr. Edwyne Fernandes Verified Market Research® US: +1 (650)-781-4080UK: +44 (753)-715-0008APAC: +61 (488)-85-9400US Toll-Free: +1 (800)-782-1768 Email: [email protected] Website:- https://www.verifiedmarketresearch.com/ Top Trending Reports https://www.verifiedmarketresearch.com/ko/product/head-up-display-market/ https://www.verifiedmarketresearch.com/ko/product/industrial-wax-market/ https://www.verifiedmarketresearch.com/ko/product/personal-care-ingredients-market/ https://www.verifiedmarketresearch.com/ko/product/prescriptive-analytics-market/

https://www.verifiedmarketresearch.com/ko/product/robot-software-market/

0 notes

Text

Internet of Things (IoT) Operating Systems Market : Size, Trends, and Growth Analysis 2032

As connected devices increasingly define how the world functions, the digital backbone supporting this transformation lies in the operating systems specifically tailored for the Internet of Things (IoT). These lightweight, real-time platforms enable billions of sensors, actuators, and devices to communicate, compute, and collaborate seamlessly. The rapidly advancing Internet of Things (IoT) Operating Systems Market has emerged as a critical foundation for powering smart environments in homes, cities, industries, and beyond.

IoT Operating Systems (OS) are specialized software platforms designed to manage hardware and software resources in devices with constrained processing power, memory, and energy capacity. Unlike conventional OS used in smartphones or computers, IoT OS are optimized to run on microcontrollers and embedded systems that form the core of IoT networks. Their ability to deliver real-time processing, low-latency communication, and secure data handling makes them indispensable in connected ecosystems.

Market Overview

The Internet of Things (IoT) Operating Systems Market was valued at USD 789 million in 2024, and is projected to grow at a CAGR of 40.5% from 2025 to 2032. This exponential growth is driven by the widespread adoption of IoT in smart homes, wearables, industrial automation, automotive systems, healthcare, and agriculture. The need for energy efficiency, seamless interoperability, and enhanced security in billions of devices has fueled the demand for robust IoT operating systems.

The market encompasses a variety of operating system architectures—from open-source microkernels to proprietary platforms—each tailored for specific performance benchmarks and industry use cases.

Key Market Drivers

1. Explosion in IoT Device Deployment

With over 30 billion IoT devices expected to be in use by 2030, the volume and diversity of endpoints—ranging from thermostats to autonomous vehicles—necessitate lightweight, scalable OS platforms. Each device requires an operating system capable of handling communication protocols, data transmission, and local processing, often with limited power and memory. This massive proliferation drives the demand for IoT OS that can operate under constrained conditions.

2. Need for Real-Time Processing and Edge Computing

IoT environments often demand real-time decision-making, particularly in industrial and medical contexts. For example, predictive maintenance in smart factories or remote patient monitoring in healthcare relies on millisecond-level responsiveness. IoT operating systems like FreeRTOS, Zephyr, and RIOT are engineered for real-time operations and efficient multi-threading, allowing edge devices to process data locally without relying solely on cloud-based systems.

3. Rise of Smart Cities and Industrial IoT (IIoT)

The push toward smart urban infrastructure—featuring intelligent traffic systems, waste management, and public safety—is accelerating the deployment of edge-based sensors and actuators. Similarly, IIoT applications such as robotics, asset tracking, and condition monitoring in factories require dependable OS platforms that can operate autonomously and securely at scale. IoT OS enables such distributed intelligence, supporting large-scale deployments with minimal latency.

4. Security and Device Management

Security is a fundamental concern in the IoT ecosystem. Compromised devices can become entry points for cyberattacks, data breaches, and system failures. IoT operating systems must incorporate advanced features such as secure boot, encrypted communication, and over-the-air (OTA) updates. As the threat landscape evolves, vendors are integrating robust security protocols within the core of their OS offerings.

Device management is equally crucial—especially in enterprise and industrial scenarios where thousands of devices may require remote configuration, monitoring, and firmware updates. Modern IoT OS platforms facilitate centralized control through APIs and cloud integration, simplifying large-scale management.

Application Landscape

Consumer IoT: Smart home devices such as lighting, thermostats, voice assistants, and appliances require ultra-low-power OS platforms to manage data exchange and device functionality. These devices also integrate with mobile and cloud apps, relying on OS to ensure secure and smooth operation.

Healthcare: IoT OS are used in wearables, patient monitors, and smart diagnostic tools that capture and process vital signs, enabling real-time medical interventions. The operating system must support secure data transmission and comply with regulatory standards like HIPAA.

Automotive and Transportation: Modern vehicles utilize IoT OS in advanced driver-assistance systems (ADAS), infotainment units, and vehicle-to-everything (V2X) communications. These OS platforms ensure fast processing and secure connectivity under real-world driving conditions.

Industrial IoT (IIoT): Applications include predictive maintenance, energy optimization, supply chain management, and safety monitoring. Real-time data processing and interoperability are vital, demanding highly reliable OS frameworks.

Agriculture: IoT OS power smart irrigation, soil monitoring, and autonomous drones used in precision farming. Devices must be rugged, energy-efficient, and capable of long-range communication—features that the right OS makes possible.

Regional Insights

North America dominates the market due to early adoption of IoT technologies, strong presence of key tech giants, and investments in smart city projects. The U.S. leads with widespread deployment in industrial automation, healthcare, and consumer electronics.

Europe follows with a focus on sustainable smart infrastructure, Industry 4.0 initiatives, and regulatory support for secure IoT deployments. Countries like Germany, France, and the UK are spearheading developments in automotive IoT and renewable energy systems.

Asia-Pacific is the fastest-growing region, fueled by massive consumer electronics production in China, India, and South Korea. Rapid urbanization, supportive government policies, and booming industrial sectors are accelerating adoption across the region.

Latin America and MEA are emerging markets where smart agriculture, utility monitoring, and transport management systems are creating demand for efficient IoT platforms.

Key Players and Competitive Landscape

Prominent players in the IoT Operating Systems Market are focusing on platform development, ecosystem expansion, and open-source collaboration to capture market share. Key industry contributors include:

Microsoft Corporation – Offers Azure RTOS, a real-time operating system designed for low-power IoT devices with integrated cloud connectivity via Microsoft Azure.

Google LLC – Provides Android Things, optimized for embedded devices and compatible with Google’s AI and machine learning capabilities.

IBM Corporation – Promotes cloud integration and device management through IBM Watson IoT and supports several open-source IoT operating systems.

Amazon Web Services (AWS) – Provides FreeRTOS, one of the most widely adopted real-time operating systems, optimized for microcontrollers and tightly integrated with AWS cloud services.

Intel Corporation – Contributes to the development of open-source OS like Zephyr and supports edge computing infrastructure for smart manufacturing and robotics.

Huawei Technologies Co. Ltd. – Offers LiteOS, a lightweight operating system for smart devices, widely used in Asia and integrated with Huawei’s IoT platforms.

These companies are investing heavily in improving interoperability, edge AI support, security protocols, and developer tools to enhance their operating systems and secure competitive advantages.

Market Trends

Open-Source OS Platforms: Growing developer communities are contributing to OS like Zephyr, RIOT, and Mbed, making them more feature-rich and accessible.

Edge AI Integration: IoT OS are being enhanced to support machine learning models that run on-device, enabling smarter, autonomous decision-making.

OTA Updates and Remote Management: Advanced OS are offering seamless firmware upgrades and centralized fleet control, essential for large-scale IoT implementations.

Cross-Platform Compatibility: Demand for interoperability between various OS, hardware platforms, and cloud ecosystems is shaping the evolution of IoT software stacks.

Browse more Report:

Automotive MLCCs Market

Automotive Start-Stop Battery Market

Automotive Slack Adjuster Market

Automotive Rear Cross Traffic Alert Market

Automotive Industry Consulting Services Market

0 notes

Text

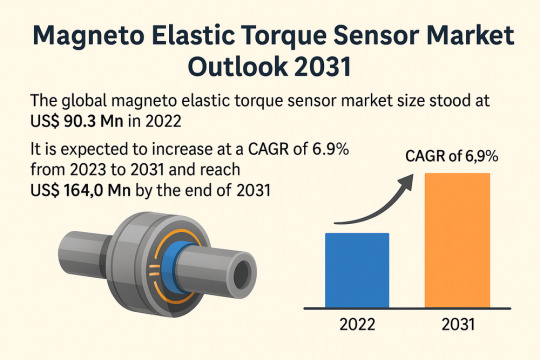

Global Magneto Elastic Torque Sensor Market Set for 6.9% CAGR Surge Through 2031

The global Magneto Elastic Torque Sensor Market is poised for substantial expansion, projected to grow from USD 90.3 Mn in 2022 to USD 164.0 Mn by the end of 2031, advancing at a compound annual growth rate (CAGR) of 6.9% during the forecast period from 2023 to 2031. Increasing demand for accurate torque measurement in electric mobility, robotics, and smart industrial applications is expected to drive this growth trajectory.

Market Overview: Magneto elastic torque sensors are critical in measuring the torque or twisting force on rotating components like shafts, motors, and gearboxes. Their non-contact operation, high accuracy, and compact design make them ideal for applications across automotive, aerospace, industrial automation, healthcare, and research sectors.

These sensors work on the principle of measuring strain-induced changes in magnetic permeability. Their versatility, long-term reliability, and digital compatibility have rendered them indispensable in environments requiring precise motion control and performance optimization.

Market Drivers & Trends

The rapid shift toward electric and hybrid vehicles and the expansion of automated industrial systems are among the primary factors accelerating magneto elastic torque sensor market growth. Torque sensors play a crucial role in managing and improving the performance of EV drivetrains, offering precise torque feedback for real-time adjustments and efficiency gains.

Moreover, stringent emission regulations are driving the adoption of torque sensors in combustion and hybrid engines to improve fuel efficiency and reduce CO₂ output. The trend toward smart factories, powered by Industry 4.0 technologies, has further amplified demand for compact and wireless torque sensors that support predictive maintenance and remote diagnostics.

Latest Market Trends

Recent trends shaping the market include:

Miniaturization of sensors to fit confined spaces, particularly in aerospace and automotive applications.

Wireless and non-contact torque sensors gaining traction for their ease of integration and lower maintenance needs.

Integration with IoT platforms, enabling real-time data acquisition and torque analysis for smart manufacturing systems.

Growing use of torque sensors in wind energy systems and medical devices for enhanced operational safety and efficiency.

Key Players and Industry Leaders

The global magneto elastic torque sensor market is consolidated, with a few prominent players commanding a significant share. These companies are continuously investing in R&D, product innovation, and strategic collaborations to expand their global footprint. Key players include:

ABB Ltd.

Applied Measurements Ltd.

Crane Electronics Ltd.

Honeywell Sensing and Control

HITEC Sensor Developments, Inc.

Kistler Instrumente Ltd.

MagCanica

Methode Electronics

Texas Instruments, Inc.

Recent Developments

Several noteworthy developments have taken place in the industry:

April 2021: Datum Electronics Ltd. partnered with Nautils Labs to provide predictive decision support and vessel digitalization for the maritime industry.

November 2020: HBM launched the T40CB torque transducer, optimized for confined automotive testing environments, featuring digital and analog interfaces.

May 2020: Kistler Holding collaborated with Vehico for advanced vehicle testing systems.

April 2020: Infineon Technologies AG completed the acquisition of Cypress Semiconductor Corporation to strengthen its capabilities in connectivity and embedded systems.

These strategic moves highlight a growing focus on digital transformation, expanded sensor functionalities, and diversified application scopes.

Examine key highlights and takeaways from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=24872

Market Opportunities

Opportunities abound in this market, especially in sectors embracing digitalization and green technologies:

E-mobility boom: The global push for electric vehicles opens new avenues for torque sensor integration in EV drivetrains and battery monitoring systems.

Industrial automation: With Industry 4.0 adoption on the rise, torque sensors are critical in machine learning environments for real-time diagnostics.

Healthcare sector: Miniaturized sensors are increasingly being deployed in prosthetics, surgical robotics, and precision instruments.

Renewable energy: Torque measurement is vital in optimizing wind turbines and hydroelectric systems for efficient energy conversion.

The emergence of smart torque sensing solutions integrated with AI and machine learning is expected to unlock new potential in process optimization and equipment lifecycle management.

Future Outlook

The magneto elastic torque sensor market is on a stable growth trajectory, bolstered by macroeconomic trends in clean energy, smart manufacturing, and digital healthcare. As industries demand higher levels of precision, real-time monitoring, and system intelligence, the role of advanced torque sensing will become even more critical.

Future innovation is likely to focus on:

Multi-sensor integration for simultaneous measurement of torque, temperature, and pressure.

AI-powered predictive analytics for preventive maintenance.

Cloud-based torque monitoring systems for remote asset management.

By 2031, the market is expected to be characterized by smarter, more compact, and interoperable torque sensing solutions with applications across emerging and established economies.

Market Segmentation

The magneto elastic torque sensor market is segmented as follows:

By Application:

Automotive: Dominant application, particularly in EVs and hybrid powertrains.

Aerospace & Defense: For load monitoring and structural testing.

Research and Development: Academic and industrial torque testing.

Industrial: Robotics, automation, machine tools.

Others: Healthcare devices, renewable energy systems.

By Region:

Asia Pacific: Leading the market with significant contributions from China, Japan, South Korea, and India. The region benefits from a strong automotive base and growing EV adoption.

North America: High technology integration in manufacturing and defense sectors.

Europe: Home to key automotive and industrial automation players.

Rest of World: Emerging opportunities in South America and the Middle East driven by industrial digitization.

Regional Insights

Asia Pacific dominated the global market in 2022 and is projected to maintain its lead throughout the forecast period. The region’s growth is propelled by:

High production and export volume of electric and hybrid vehicles.

Strong governmental support for industrial automation and emission control.

Advancements in manufacturing technologies in countries such as China, Japan, and India.

Other regions such as North America and Europe are also witnessing steady growth due to their robust R&D infrastructure, early adoption of IoT technologies, and stringent safety standards in automotive and industrial systems.

Why Buy This Report?

This report provides:

A comprehensive overview of market dynamics including drivers, restraints, and opportunities.

In-depth segmentation by application and region, with detailed analysis.

Competitive landscape featuring major players, their strategies, and recent developments.

Historical and forecasted market size from 2017 to 2031.

Insights into current and emerging trends shaping the industry.

Strategic recommendations for stakeholders, investors, and new entrants.

Customizable data formats (PDF & Excel) for quick access and business planning.

0 notes

Text

Powered Surgical Instrument Market to Gain From Technological Advancements in Battery-Operated Devices

Market Overview

The powered surgical instrument market is witnessing significant growth driven by rising surgical procedures across the globe and the increasing adoption of advanced medical technologies. These precision-engineered tools—ranging from electric and pneumatic devices to battery-powered instruments—are revolutionizing surgical practices by improving speed, accuracy, and patient outcomes. The market encompasses a wide array of products including drill systems, saw systems, staplers, reamers, and shavers, catering to various surgical needs. The increasing prevalence of chronic diseases and traumatic injuries is further fueling the demand for these instruments, especially in orthopedic, neurosurgical, ENT, and cardiothoracic procedures.

As healthcare providers emphasize shorter recovery periods and less invasive techniques, powered surgical tools integrated with robotics and minimally invasive technology are becoming central to modern surgical interventions. With robust investments in healthcare infrastructure and rising demand for advanced procedures, the powered surgical instrument market is expected to see continuous expansion through 2034.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS26973

Market Dynamics

Several factors are shaping the dynamics of the powered surgical instrument market. One of the primary drivers is the growing volume of surgeries due to an aging population and rising incidences of lifestyle-related ailments. Orthopedic, dental, and plastic surgeries are on the rise, creating a consistent demand for instruments that offer precision and efficiency.

Technological advancements are a game-changer, with innovations in robotics, advanced energy solutions, and minimally invasive systems leading the charge. Healthcare providers are increasingly opting for devices that are not only effective but also cost-efficient in terms of maintenance, repair, and calibration. Battery-powered instruments, for instance, are gaining preference in ambulatory surgical centers and specialty clinics for their ease of use and mobility.

However, market growth is tempered by challenges such as the high cost of advanced equipment, especially for smaller clinics and hospitals in developing regions. Additionally, strict regulatory approvals and the need for consistent training of medical personnel pose hurdles. Nevertheless, the market continues to thrive on opportunities such as increasing government healthcare spending and the growing trend of outpatient surgeries.

Key Players Analysis

The powered surgical instrument market is moderately consolidated with several global and regional players vying for market share. Major companies like Medtronic plc, Stryker Corporation, Johnson & Johnson (DePuy Synthes), Zimmer Biomet Holdings Inc., and B. Braun Melsungen AG are leading the charge by consistently launching innovative product lines and expanding their geographical presence.

These players are focusing on strategic mergers, acquisitions, and partnerships to strengthen their portfolios. Investments in R&D for developing ergonomic, high-speed, and efficient devices are also prevalent. Some companies offer comprehensive service packages including repair, calibration, and training, adding value and ensuring customer loyalty in the long run.

Regional Analysis

Geographically, North America holds the largest share of the powered surgical instrument market due to well-established healthcare systems, a high number of surgical procedures, and rapid adoption of advanced technologies. The United States, in particular, leads in robotic-assisted surgeries and orthopedic procedures.

Europe follows closely, driven by strong healthcare frameworks in countries like Germany, the U.K., and France. Government initiatives and favorable reimbursement policies are further boosting market demand in the region.

The Asia-Pacific region is emerging as the fastest-growing market. Countries such as China, India, and Japan are investing heavily in healthcare infrastructure and are increasingly adopting advanced surgical tools. Rising medical tourism, coupled with a growing middle-class population seeking quality surgical care, is expected to propel regional growth.

Latin America and the Middle East & Africa regions are gradually catching up, with increased healthcare access and a focus on modernizing surgical practices.

Recent News & Developments

Recent developments in the market highlight a surge in strategic partnerships and technology rollouts. Leading manufacturers are integrating AI and robotics into their powered surgical systems, improving surgeon control and reducing procedural time. Medtronic’s recent launch of AI-assisted surgical drill systems and Stryker’s expansion of its Mako robotic platform showcase the industry's direction toward automation and minimally invasive solutions.

Service enhancements such as remote calibration and mobile repair units are also making headlines, ensuring downtime is minimized and device performance is optimized.

Browse Full Report @ https://www.globalinsightservices.com/reports/powered-surgical-instrument-market/

Scope of the Report

This report offers a comprehensive analysis of the powered surgical instrument market, covering various segments by type, product, technology, application, functionality, and end user. It provides insight into the market's current state and future projections through 2034, supported by key trends, challenges, and growth drivers.

With the growing focus on healthcare modernization and patient-centric care, the powered surgical instrument market is set to evolve rapidly. Hospitals, ambulatory surgical centers, and specialty clinics will continue to invest in these devices, prioritizing both reusable and single-use options based on procedural needs.

In summary, the powered surgical instrument market is on a promising trajectory, fueled by technological innovation, expanding healthcare access, and the global emphasis on precision-driven, minimally invasive surgical care.

Discover Additional Market Insights from Global Insight Services:

Wearable Breast Pumps Market: https://www.globalinsightservices.com/press-releases/wearable-breast-pumps-market/

Eyewear Market: https://www.globalinsightservices.com/reports/eyewear-market/

Abdominal Pads Market: https://www.globalinsightservices.com/reports/abdominal-pads-market/

Advanced 3D Bioprinting Ink Market: https://www.globalinsightservices.com/reports/advanced-3d-bioprinting-ink-market/

Advanced Neuroscience Implants Market: https://www.globalinsightservices.com/reports/advanced-neuroscience-implants-market/

0 notes

Text

Neodymium-Iron-Boron Permanent Magnet Market Size, Share & Global Insights (2021–2031)

The global Neodymium-Iron-Boron (NdFeB) permanent magnet market is poised for substantial expansion, projected to grow from US$ 15,204.23 million in 2024 to US$ 29,129.11 million by 2031, registering a CAGR of 10.3% during the forecast period (2025–2031).

🌐 Executive Summary & Global Market Outlook

The NdFeB magnet market is experiencing accelerated growth driven by the demand for high-performance, compact, and energy-efficient solutions across multiple industries. These powerful magnets are critical in the functionality of electric vehicles (EVs), wind turbines, consumer electronics, and medical devices, where strong magnetic performance and space efficiency are essential.

Key growth enablers include:

Global shift toward renewable energy sources

Rising electrification in automotive and industrial applications

Continuous miniaturization and automation in electronics

As sustainability, recycling of rare earth elements, and resilient supply chains gain prominence, industry leaders are investing in advanced R&D, greener manufacturing, and localized sourcing strategies.

While Asia-Pacific remains a dominant hub for production, emerging players in North America and Europe are leveraging high-quality magnet innovation, environmental stewardship, and regional supply chains to capture market share.

📥 [Download Sample Report]

📊 Market Segmentation Overview

By Type:

Sintered NdFeB Magnets (Market leader in 2024)

Bonded NdFeB Magnets

By End-User:

Automotive (Largest share)

Consumer Electronics

Power Generation (Wind Turbines)

Industrial Automation & Robotics

Medical Devices

Others

By Geography:

Asia-Pacific (Dominant region)

North America

Europe

Middle East & Africa

South & Central America

⚡ Market Drivers & Emerging Opportunities

Electrification of Mobility: The rapid global adoption of electric vehicles is a primary driver of NdFeB magnet demand. These magnets enable compact, energy-efficient EV motors that meet strict performance and sustainability standards.

Growth in Smart Manufacturing & Green Energy: Industrial automation and renewable energy systems—particularly wind turbines—are creating robust demand for high-grade sintered NdFeB magnets capable of enduring extreme conditions and offering strong magnetic power.

🔍 Type-Based Insight

Sintered NdFeB magnets dominate the market owing to their high coercivity, thermal stability, and energy product. Produced through powder metallurgy, they are ideal for heavy-duty applications in EVs, aerospace, wind energy, and medical equipment.

🏭 Key Market Participants

Hitachi Metals, Ltd.

Shin-Etsu Chemical Co., Ltd.

TDK Corporation

Ningbo Yunsheng Co., Ltd.

Beijing Zhong Ke San Huan High-Tech Co., Ltd.

Vacuumschmelze GmbH & Co. KG

Neo Performance Materials Inc.

🧩 About Us

Business Market Insights delivers actionable research across key industries including chemicals, automotive, healthcare, electronics, and aerospace. Our data-driven insights empower global organizations to make strategic, evidence-based decisions.

#NeodymiumMagnets#NdFeB#PermanentMagnets#EVMarket#WindTurbines#MagnetIndustry#MagnetTechnology#RareEarthMagnets#Electrification#GreenEnergy#ConsumerElectronics#SinteredMagnets#CleanTech#AdvancedMaterials#RenewableEnergy#EVComponents#SmartManufacturing#MagneticMaterials#IndustrialAutomation#SustainableTech

0 notes

Text

Robot Sensor Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forec

Global robot sensor market size was valued at USD 867 million in 2024. The market is projected to grow from USD 934 million in 2025 to USD 1,344 million by 2032, exhibiting a CAGR of 7.5% during the forecast period.

Robot sensors are critical components that enable robots to perceive and interact with their environment by estimating conditions and transmitting signals to controllers. These sensors mimic human sensory functions, providing essential data on position, force, vision, touch, and other environmental factors. The market primarily focuses on industrial robot applications, with key sensor types including movement sensors, vision sensors, touch sensors, and voice sensors.

Expansion into New Applications

The sensor market is diversifying beyond traditional industrial applications. Medical robotics now incorporates sterilizable force sensors for surgical procedures, while agricultural robots utilize hyperspectral imaging sensors for crop analysis. In logistics, autonomous mobile robots rely on LiDAR and ultrasonic sensors for navigation in dynamic environments, with deployment growing at 35% CAGR. This application growth aligns with the projected market expansion from $867 million in 2024 to $1,344 million by 2032. Emerging sectors like underwater robotics and space exploration are further pushing the boundaries of sensor technology through extreme-environment adaptations.

List of Key Robot Sensor Companies Profiled

Cognex Corporation (U.S.)

Balluff GmbH (Germany)

Baumer Group (Switzerland)

IFM Electronic GmbH (Germany)

Keyence Corporation (Japan)

Rockwell Automation (U.S.)

Daihen Corporation (Japan)

Infineon Technologies (Germany)

ATI Industrial Automation (U.S.)

Sick AG (Germany)

Honeywell International Inc. (U.S.)

Datalogic (Italy)

Texas Instruments (U.S.)

TDK Corporation (Japan)

Sensopart (Germany)

Segment Analysis:

By Robot Type

The market is segmented based on Robot Type into:

Industrial Robots

Service Robots

Collaborative Robots

Mobile Robots

Others

By Sensor Type

Vision Sensors Segment Dominates the Market Due to Increased Automation in Industrial Applications

The market is segmented based on type into:

Movement Sensors

Vision Sensors

Subtypes: 2D Vision, 3D Vision, and others

Touch Sensors

Voice Sensors

Position/Navigation Sensors

Others

By Application

Electronics Manufacturing Segment Leads Due to High Precision Requirements in Assembly Lines

The market is segmented based on application into:

Automotive

Machinery

Aerospace

Electronics Manufacturing

Others

By Technology

LiDAR Technology Gains Traction Due to Advancements in Autonomous Navigation

The market is segmented based on technology into:

MEMS-Based Sensors

Optical Sensors

Capacitive/Inductive Sensors

Ultrasonic and Infrared Sensors

CMOS Image Sensors

Others

By End-User

Industrial Sector Maintains Dominance Through Widespread Adoption in Manufacturing Processes

The market is segmented based on end-user into:

Industrial

Manufacturing

Healthcare

Logistics

Consumer Electronics

Other

Key Coverage Areas:

· ✅ Market Overview

o Global and regional market size (historical & forecast)

o Growth trends and value/volume projections

· ✅ Segmentation Analysis

o By product type or category

o By application or usage area

o By end-user industry

o By distribution channel (if applicable)

· ✅ Regional Insights

o North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

o Country-level data for key markets

· ✅ Competitive Landscape

o Company profiles and market share analysis

o Key strategies: M&A, partnerships, expansions

o Product portfolio and pricing strategies

· ✅ Technology & Innovation

o Emerging technologies and R&D trends

o Automation, digitalization, sustainability initiatives

o Impact of AI, IoT, or other disruptors (where applicable)

· ✅ Market Dynamics

o Key drivers supporting market growth

o Restraints and potential risk factors

o Supply chain trends and challenges

· ✅ Opportunities & Recommendations

o High-growth segments

o Investment hotspots

o Strategic suggestions for stakeholders

· ✅ Stakeholder Insights

o Target audience includes manufacturers, suppliers, distributors, investors, regulators, and policymakers

FREQUENTLY ASKED QUESTIONS:

▶ What is the current market size of Global Robot Sensor Market?

The Global Robot Sensor market was valued at USD 867 million in 2024 and is projected to reach USD 1344 million by 2032.

▶ Which key companies operate in Global Robot Sensor Market?

Key players include Cognex, Baluff Ag, Baumer Group, Ifm Electronic Gmbh, Keyence, Rockwell Automation, Daihen Corporation, and Infineon Technologies, among others.

▶ What are the key growth drivers?

Key growth drivers include industrial automation demand, advancements in sensor technology, expansion of robotics applications, and government initiatives supporting Industry 4.0 adoption.

▶ Which region dominates the market?

Asia-Pacific leads the market with 40% share, followed by Europe and North America. China remains the largest consumer of robot sensors globally.

▶ What are the emerging trends?