#Reactive Power Compensation Device Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was the first site to host the blog for President Barack Obama in 2011.

Text

Powering Stability: Leading Static VAR Generator Manufacturers in India

In today’s fast-evolving industrial and commercial landscape, power quality has become more critical than ever. With increasing automation, sensitive electronics, and fluctuating load patterns, voltage stability and reactive power compensation are major concerns. That’s where Static VAR Generators (SVGs) come into play — and India has rapidly emerged as a hub for reliable SVG manufacturing.

What is a Static VAR Generator?

A Static VAR Generator is an advanced power quality device used to provide dynamic reactive power compensation. Unlike traditional capacitor banks or reactors, SVGs use power electronic converters to inject or absorb reactive power in real time, improving power factor, reducing voltage fluctuations, and minimizing harmonic distortion.

Why India for SVGs?

India's power and infrastructure sector is undergoing a major transformation, pushing the demand for smart, efficient, and scalable energy solutions. As a result, several Indian manufacturers have stepped up to develop world-class SVGs tailored to local as well as international standards.

Top Static VAR Generator Manufacturers in India

Here are some key players contributing to India's rise in the SVG market:

1. Statcon Energiaa

With over three decades of power electronics expertise, Statcon Energiaa offers robust SVG solutions for industries, commercial complexes, and renewable energy applications. Their products are known for high reliability and quick response times.

2. KEC International (RPG Group)

KEC International is a major infrastructure EPC player that also offers cutting-edge reactive power compensation products, including Static VAR Generators designed for high-voltage applications.

3. Powerone Micro Systems

Based in Bengaluru, Powerone is known for innovative power quality solutions, including Active Harmonic Filters and SVGs. Their products cater to sectors like IT, hospitals, and manufacturing.

4. Servokon Systems

Servokon, a well-known name in electrical transformers and voltage stabilizers, also manufactures SVGs with a strong focus on energy savings and consistent voltage regulation.

5. Hitachi Energy (India)

Formerly ABB Power Grids, Hitachi Energy offers high-performance SVGs for industrial grids, railways, and renewable projects. Their solutions are globally benchmarked yet adapted for Indian needs.

Key Features of Indian SVGs

Real-Time Compensation – Immediate response to load changes.

Compact Design – Saves space in industrial settings.

Low Maintenance – Fewer moving parts and automated control.

Energy Efficiency – Reduces power bills by correcting poor power factor.

Smart Monitoring – Enabled with IoT and SCADA compatibility.

Applications Across Industries

Steel and metal industries

Data centers

Commercial buildings

Renewable energy (solar/wind farms)

Automotive manufacturing

Textiles and pharmaceuticals

Final Thoughts

India is not just a consumer of high-end power quality equipment — it is now a creator. With a growing list of reliable and innovative manufacturers, Static VAR Generators made in India are empowering industries with cleaner, stable, and more efficient energy systems. If you're planning to invest in power quality solutions, considering an Indian SVG manufacturer could be a smart and sustainable choice.

0 notes

Text

Power Quality Equipment Market: Emerging Trends Shaping Future Demand

The power quality equipment market has witnessed notable growth in recent years, driven by the increasing demand for reliable electricity supply and the rapid expansion of industrial and commercial infrastructure. Power quality refers to the stability and purity of electric power, which is essential for the smooth operation of sensitive electronic devices and critical systems. Power quality equipment plays a crucial role in mitigating voltage fluctuations, harmonics, transients, and other electrical disturbances that can cause equipment malfunction or failure.

As global power systems become more complex with the integration of renewable energy and the proliferation of smart devices, ensuring high-quality power delivery becomes more challenging and essential. In this context, emerging trends in the power quality equipment market are not only transforming the industry landscape but are also opening new avenues for innovation and growth.

Surge in Renewable Energy Integration

One of the most significant trends impacting the power quality equipment market is the growing integration of renewable energy sources such as solar and wind. These sources, while environmentally friendly, are inherently intermittent and variable, often introducing power fluctuations and instability into the grid. To address these challenges, there is an increasing demand for power quality solutions such as voltage regulators, harmonic filters, and energy storage systems that can smooth out supply irregularities and ensure stable power delivery.

Additionally, the decentralization of power generation through distributed energy resources (DERs) calls for advanced monitoring and control technologies to maintain grid stability, further boosting the market for intelligent power quality devices.

Growing Industrial Automation and Digitization

The rise of Industry 4.0 and smart manufacturing has significantly increased the reliance on automated machinery, robotics, and data-driven processes. These systems are highly sensitive to power disturbances and require uninterrupted, clean power to function efficiently. As a result, industries are investing heavily in uninterruptible power supplies (UPS), surge protection devices, and power conditioning equipment.

Moreover, the digitization of industrial operations has led to the deployment of advanced sensors and monitoring tools that provide real-time data on power quality. These insights enable predictive maintenance, reduce downtime, and optimize energy consumption—benefits that are driving wider adoption across manufacturing and processing sectors.

Advancements in Smart Grid Technologies

Smart grids are playing a pivotal role in reshaping the power quality equipment landscape. These grids use digital communication technology to detect and react to local changes in usage, thereby enhancing the reliability and efficiency of electricity distribution. With smart grids, utilities can better manage load fluctuations, detect faults instantly, and deploy corrective measures automatically.

Power quality monitoring devices integrated within smart grid infrastructure can track parameters such as voltage sags, swells, and harmonic distortions, allowing utilities and consumers to take corrective actions proactively. The growing investments in smart grid development are, therefore, expected to fuel the demand for next-generation power quality solutions.

Rising Awareness of Energy Efficiency

Energy efficiency is becoming a central theme in both commercial and residential sectors, spurred by regulatory policies and growing environmental consciousness. Power quality equipment contributes significantly to energy efficiency by reducing losses associated with poor power conditions. For example, reactive power compensation devices can improve power factor, reduce energy consumption, and lower electricity bills.

Businesses and utilities are increasingly recognizing the long-term financial and environmental benefits of investing in power quality systems. This awareness is encouraging the adoption of energy-efficient devices that not only ensure power reliability but also contribute to sustainability goals.

Technological Innovations and Product Development

The power quality equipment market is witnessing rapid innovation with the development of compact, intelligent, and IoT-enabled devices. These new-generation products offer improved performance, easier integration, and enhanced diagnostic capabilities. IoT connectivity allows for remote monitoring, automated reporting, and real-time alerts, significantly improving maintenance efficiency and system uptime.

Manufacturers are also focusing on developing modular solutions that can be customized based on the unique requirements of different industries and grid conditions. These innovations are not only improving user experience but also expanding the market reach of power quality equipment.

Conclusion

The power quality equipment market is undergoing a transformative phase fueled by trends such as renewable energy integration, industrial automation, smart grid adoption, and increasing energy efficiency demands. As global energy systems evolve, the importance of maintaining high power quality becomes ever more critical. Companies operating in this space must embrace innovation, invest in advanced technologies, and stay aligned with market trends to capitalize on the emerging opportunities. The future of the power quality equipment market looks promising, marked by technological evolution and a growing emphasis on sustainable energy practices.

0 notes

Text

Emerging Trends Shaping the Global Power Capacitors Market Through 2030 and Beyond

Power capacitors are often the unsung heroes in the realm of electrical infrastructure. These components, essential for improving power factor, voltage regulation, and overall energy efficiency, play a vital role across various sectors industrial, commercial, and even residential. With the growing demand for efficient power systems and renewable energy integration, the power capacitors market is gaining significant momentum. In this blog, we’ll delve into the market’s dynamics, current trends, and the challenges it faces.

What Are Power Capacitors?

Power capacitors are devices that store and discharge electrical energy. Their primary function is to regulate the power factor in electrical systems essentially improving the efficiency of power transmission. They help reduce losses in the system, stabilize voltage, and enhance the capacity of the power supply. These devices are commonly used in substations, power plants, manufacturing facilities, and increasingly in renewable energy applications like solar and wind installations.

Market Overview and Growth Drivers

The global power capacitors market has been witnessing steady growth, and this trend is expected to continue. Several factors are contributing to this expansion:

Rising Demand for Energy Efficiency: With the global push toward reducing carbon emissions and optimizing energy use, power capacitors are in demand to improve the efficiency of existing power infrastructure.

Modernization of Power Grids: Aging power grids, especially in developed countries, are being upgraded to smart grids. Power capacitors play a key role in these systems, helping with voltage control and reactive power compensation.

Growth of Renewable Energy: As more solar and wind power sources are added to grids, the need for voltage stability increases. Power capacitors provide necessary support to manage these intermittent energy sources.

Industrial Growth in Emerging Economies: Countries like India, China, and Brazil are investing heavily in manufacturing and infrastructure. These sectors require stable and efficient electrical systems, driving up the need for power capacitors.

Segmentation and Market Landscape

The power capacitors market can be segmented by type, voltage rating, application, and geography.

By Type: The market includes ceramic capacitors, aluminum electrolytic capacitors, and plastic film capacitors, among others. Plastic film capacitors are particularly popular due to their reliability and high-performance characteristics.

By Voltage: Low voltage capacitors are dominant due to their widespread use in consumer and industrial applications, but medium and high voltage capacitors are gaining traction in utility and grid applications.

By Application: Power capacitors are used in utilities, industrial power systems, and commercial buildings. The utility segment remains the largest, largely due to investments in transmission and distribution.

By Region: Asia-Pacific leads the global market, thanks to rapid industrialization and energy infrastructure projects, especially in China and India. North America and Europe also show significant market activity due to grid modernization efforts.

Challenges in the Market

Despite the positive outlook, the power capacitors market is not without its hurdles:

Raw Material Volatility: Many capacitor components rely on materials like aluminum, polypropylene, and certain rare metals. Price fluctuations and supply chain disruptions can significantly impact production costs.

Complex Regulatory Environments: Different regions have varied standards and compliance requirements for electrical components. Navigating these can be costly and time-consuming for manufacturers.

Competition from Alternative Technologies: Power electronics and newer grid management solutions sometimes compete directly with traditional capacitor-based systems, potentially limiting market share in certain applications.

Future Outlook

The future of the power capacitors market looks promising. With governments around the world committing to green energy and infrastructure development, demand for efficient power management systems is likely to rise. Innovations in capacitor design such as the development of more compact, durable, and temperature-resistant models will further push the market forward.

Conclusion

In conclusion, power capacitors may not always grab headlines, but their impact on modern electrical systems is undeniable. As industries and governments alike pursue greater energy efficiency and cleaner power, these components will continue to play a pivotal role. For investors, manufacturers, and engineers, keeping an eye on this evolving market could offer both insights and opportunities in the years ahead.

0 notes

Text

TIBCON Capacitor Manufacturers: Powering Efficiency Across Industries

Capacitors are fundamental components in electrical and electronic circuits, vital for energy storage, power regulation, and ensuring smooth operation of various devices. Among the leading names in capacitor production is TIBCON, a trusted brand known for manufacturing high-quality capacitors for a wide array of applications. TIBCON capacitor manufacturers have established a strong presence in both domestic and international markets, providing reliable solutions for industries ranging from consumer electronics to heavy machinery.

A Legacy of Quality: The TIBCON Advantage

TIBCON, part of Tibrewala Electronics Ltd., has been a prominent player in the capacitor manufacturing industry for over three decades. With a focus on innovation, precision, and reliability, TIBCON capacitor manufacturers have built a reputation for delivering high-performance capacitors that meet the stringent demands of modern electronics and electrical systems.

What sets TIBCON apart is its commitment to quality and adherence to global standards. The company’s capacitors are engineered to provide long-lasting performance, withstanding extreme temperatures, voltage fluctuations, and mechanical stresses. These characteristics make TIBCON capacitors an ideal choice for critical applications where durability and consistency are paramount.

Types of Capacitors Manufactured by TIBCON

TIBCON offers a wide range of capacitors, each designed for specific industrial and consumer applications. Some of the key capacitor types produced by TIBCON capacitor manufacturers include:

Motor Run Capacitors: TIBCON’s motor run capacitors are widely used in air conditioners, refrigerators, pumps, and compressors. These capacitors help motors start smoothly and run efficiently, providing energy savings and improved performance in appliances and industrial equipment.

Lighting Capacitors: TIBCON manufactures capacitors for fluorescent and LED lighting systems. These capacitors ensure stable and flicker-free lighting while enhancing the longevity of the lighting equipment.

Fan Capacitors: TIBCON fan capacitors are known for their reliability in ceiling fans, exhaust fans, and table fans, ensuring consistent speed and smooth operation.

Power Factor Correction (PFC) Capacitors: Power factor correction is crucial for reducing energy wastage in industrial and commercial operations. TIBCON’s PFC capacitors help improve energy efficiency by compensating for reactive power in electrical systems.

AC Capacitors: Used in air conditioners and cooling systems, TIBCON’s AC capacitors are designed to withstand high-voltage environments, ensuring optimal cooling performance even under heavy loads.

TIBCON’s Commitment to Innovation and Sustainability

One of the defining features of TIBCON capacitor manufacturers is their relentless focus on innovation. The company continually invests in research and development to improve capacitor performance and adapt to emerging technologies and applications. This commitment to innovation has allowed TIBCON to develop capacitors that are more compact, energy-efficient, and reliable than ever before.

In addition to technological advancements, TIBCON is also dedicated to sustainability. By designing capacitors that improve energy efficiency and reduce power consumption, TIBCON is contributing to greener and more sustainable industrial practices. Many of their products, such as PFC capacitors, help industries minimize energy wastage, which is essential for reducing environmental impact.

Why Choose TIBCON Capacitors?

Businesses across various sectors prefer TIBCON capacitor manufacturers for several reasons:

Global Standards Compliance: TIBCON capacitors adhere to international standards like IEC and ISI, ensuring they meet the highest quality and safety requirements for both domestic and international markets.

Durability and Reliability: Designed to perform under demanding conditions, TIBCON capacitors offer long service life and consistent performance, making them suitable for heavy-duty industrial applications.

Custom Solutions: TIBCON capacitor manufacturers provide customized solutions tailored to the specific needs of clients across industries, offering flexibility in design and specifications.

Strong After-Sales Support: TIBCON is renowned for its excellent customer service and technical support, assisting businesses with capacitor selection, installation, and maintenance.

Wide Application Range: From household appliances and lighting systems to industrial machinery and power factor correction, TIBCON capacitors are versatile and can be found in a wide range of applications.

Applications of TIBCON Capacitors in Key Industries

HVAC and Appliances: TIBCON motor run and AC capacitors are commonly used in HVAC systems, refrigerators, washing machines, and other household appliances. They ensure energy-efficient operation and reliable performance.

Industrial Machinery: In industrial settings, TIBCON’s PFC capacitors play a crucial role in optimizing power usage and improving the efficiency of large machinery and electrical systems.

Lighting Solutions: TIBCON lighting capacitors are ideal for both residential and commercial lighting systems, ensuring stable performance and prolonging the life of lighting equipment.

Renewable Energy Systems: As the renewable energy sector grows, TIBCON capacitors are finding increasing use in solar and wind energy systems, where they help manage power distribution and improve system reliability.

Conclusion

With a focus on innovation, quality, and customer satisfaction, TIBCON capacitor manufacturers have earned their place as industry leaders. Their capacitors are trusted by businesses across the globe to deliver reliable performance, energy efficiency, and durability. As industries continue to evolve and demand more efficient electronic components, TIBCON remains at the forefront of capacitor manufacturing, powering progress across various sectors.

Whether for industrial, commercial, or residential applications, TIBCON capacitors provide the performance and reliability that businesses need to stay competitive in today’s fast-paced technological landscape.

0 notes

Text

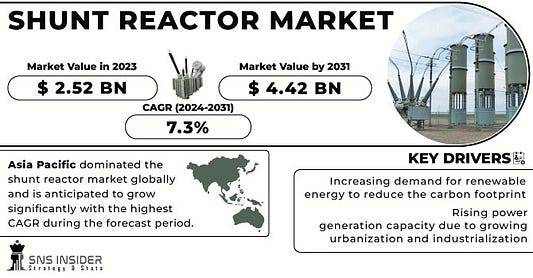

Shunt Reactor Market Set for Significant Growth Through 2031 Driven by Rising Demand for Voltage Control in Electrical Grids

The Shunt Reactor Market size was valued at US$ 2.52 billion in 2023 and is expected to grow to US$ 4.42 billion by 2030 and grow at a CAGR of 7.3% over the forecast period of 2024–2031.

Shunt reactors are critical devices used in electrical networks to manage and compensate for reactive power. By absorbing excess reactive power, they help maintain voltage levels within acceptable ranges, thereby enhancing the reliability and performance of power systems. The integration of renewable energy sources, such as wind and solar, often leads to voltage fluctuations that can jeopardize grid stability. Shunt reactors mitigate these fluctuations, making them indispensable in modern power systems.

The increasing global demand for electricity, coupled with the need for sustainable energy solutions, is driving investments in shunt reactor installations. As countries aim to meet their climate goals and improve energy efficiency, the importance of effective reactive power management continues to grow.

Request Sample Report@ https://www.snsinsider.com/sample-request/2730

Key Market Drivers

Increasing Demand for Reactive Power Compensation: The need for reactive power compensation in high-voltage transmission systems is a significant driver of the shunt reactor market. Utilities are increasingly investing in shunt reactors to ensure voltage stability and compliance with regulatory standards.

Integration of Renewable Energy Sources: The expansion of renewable energy technologies often leads to voltage fluctuations. Shunt reactors play a crucial role in managing these fluctuations, thereby facilitating the integration of variable generation sources into the grid.

Grid Modernization Initiatives: Governments and utilities worldwide are investing in the modernization of electrical grids to enhance their reliability and efficiency. This trend is propelling the demand for shunt reactors as part of broader grid improvement projects.

Rising Electricity Consumption: The growing global population and increasing industrialization are driving up electricity consumption. This surge in demand necessitates the enhancement of power infrastructure, including the implementation of shunt reactors.

Supportive Government Policies: Various governments are implementing policies and regulations to promote grid stability and efficiency, further encouraging investments in shunt reactor technology.

Market Segmentation

The Shunt Reactor Market can be segmented by type, installation, application, and region.

By Type

Air-Core Shunt Reactors: These reactors are used primarily in high-voltage applications due to their low losses and high efficiency. They are commonly installed in substations and transmission networks.

Oil-Filled Shunt Reactors: These reactors utilize oil for cooling and insulation and are typically employed in power systems where higher insulation levels are necessary.

Dry-Type Shunt Reactors: Utilizing air as a cooling medium, dry-type reactors are suitable for lower voltage applications and are preferred for indoor installations due to their compact design.

By Installation

Indoor Shunt Reactors: Installed within substations or facilities, these reactors are designed for environments with limited space and require additional protection.

Outdoor Shunt Reactors: Designed for installation in open areas, outdoor reactors are built to withstand environmental conditions, making them suitable for high-voltage transmission applications.

Buy a Complete Report of Hydrogen Fuel Cells Market 2024–2032@ https://www.snsinsider.com/checkout/2730

By Application

Transmission Systems: Shunt reactors are predominantly used in high-voltage transmission systems to maintain voltage levels and improve overall system stability.

Distribution Systems: In distribution networks, shunt reactors help manage reactive power, ensuring efficient delivery of electricity to end consumers.

Renewable Energy Integration: Shunt reactors are increasingly used in conjunction with renewable energy projects to mitigate voltage fluctuations caused by variable generation.

Regional Analysis

North America: The North American shunt reactor market is set to grow significantly due to ongoing investments in grid modernization and the integration of renewable energy sources. The U.S. and Canada are leading efforts to adopt advanced power management technologies.

Europe: Europe remains a key player in the shunt reactor market, with countries like Germany, France, and the UK investing in grid stability measures to support their renewable energy initiatives.

Asia-Pacific: The Asia-Pacific region is expected to witness rapid growth in the shunt reactor market, particularly in countries like China, India, and Japan, which are investing heavily in power infrastructure.

Middle East & Africa: The Middle East and Africa are exploring the potential of shunt reactors to enhance electricity infrastructure, focusing on improving grid stability and reliability.

Latin America: Countries like Brazil and Chile are beginning to invest in shunt reactors, recognizing the importance of these devices in supporting their expanding energy needs.

Current Market Trends

Technological Innovations: Manufacturers are focusing on developing advanced shunt reactors that minimize losses and enhance efficiency, responding to the demands of modern power systems.

Smart Grid Implementation: The integration of smart grid technologies is increasing the demand for shunt reactors as utilities seek to optimize power management and enhance grid resilience.

Decentralized Energy Systems: The trend towards decentralized energy systems, including distributed generation and microgrids, is creating new opportunities for shunt reactors to manage reactive power locally.

Sustainability Focus: As sustainability becomes a priority for industries and utilities, the demand for efficient and reliable shunt reactors is growing to support renewable energy integration and reduce environmental impact.

About Us:

SNS Insider is a global leader in market research and consulting, shaping the future of the industry. Our mission is to empower clients with the insights they need to thrive in dynamic environments. Utilizing advanced methodologies such as surveys, video interviews, and focus groups, we provide up-to-date, accurate market intelligence and consumer insights, ensuring you make confident, informed decisions. Contact Us: Akash Anand — Head of Business Development & Strategy [email protected] Phone: +1–415–230–0044 (US) | +91–7798602273 (IND)

1 note

·

View note

Text

Synchronous Condenser Market: Size, Share, Trends, Key Players Analysis, and Forecast till 2031

Synchronous condensers are synchronous mains-connected machines without prime movers and they are an essential part of an electric power system used mainly for reactive power support, system stability and voltage control. Electric power systems around the world are under growing demand in terms of size and reliable operation; consequently, the global synchronous condenser market is projected to show tremendous growth.

Market Overview

The market size of synchronous condenser is projected to reach US$ 939.03 million by 2031 from US$ 680 million in 2023, while it is expected to register a CAGR of 4.1% in 2023-2031.

The synchronous condenser market is driven by various factors, including:

Grid Stability: Synchronous condensers keep the grid stable because they can act as a source of reactive power, working the same way that real generators do, helping to compensate for voltage fluctuations, leading to better overall reliability.

Renewable Energy Integration: Abundant intermittent energy sources such as solar and wind power plants, which are increasingly becoming higher penetration in the grid, cause fluctuations in power output. Synchro condensers are able to counteract these fluctuations and deliver grid regulation.

Power Quality Improvement: These devices improve power quality by suppressing harmonics and stabilising voltage, thereby improving the efficiency of sensitive equipment.

Peak Load Management: Synchronous condensers can be used to absorb peak loads by providing reactive power support in high-demand periods, thereby mitigating the need for additional generation capacity.

Market Trends and Growth Drivers

Smart Grid Technology: Development of smart grids is driving demand for smart synchronous condensers which feature advanced control systems and communication ability.

Energy efficiency: Energy efficiency considerations are driving the use of synchronous condensers with high-efficiency ratings.

Geographic diversification of urbanisation and industrialisation: The growing rate of urbanisation and industrialisation in the developing economy is resulting in an increased appetite for power supplies stabilised and secured, which in turn propels the demand in the synchronous condenser market growth.

Regulations from Government: There are regulations which have been created by government firms that are also promoting the demand for synchronous condensers by enhancing grid reliability and supporting the connection of renewable energy.

Market Segmentation

By Cooling Type

Air-Cooled

Hydrogen-Cooled

Water-Cooled

By Reactive Power Rating

Up to 100 MVAr

100–200 MVAr

Above 200 MVAr

By Starting Method

Pony Motor

Static Frequency Converter

Others

By Application

Metal and Mining

Electrical Utilities and Grid Operators

Marine

Oil and Gas

Others

Regional Overview

North America

Europe

Asia-Pacific

South and Central America

Middle East and Africa

Competitive Landscape

The competitive scenario of the global synchronous condenser market features a large number of players, including :

ABB Ltd.

BRUSH Group

Eaton Corporation PLC

Fuji Electric Co., Ltd.

General Electric

Hyundai Idela Electric Co.

Mitsubishi Electric Corporation

Siemens AG

Voith GmBH

WEG Electric corp

Future Outlook

Driven by the growing complexity of the grids, penetration of renewable energy sources, as well as the necessity power, the synchronous condenser market is predicted to witness expansion in the upcoming years. The development of new and more efficient and compact synchronous condensers shall also positively impact the market growth.

Conclusion

Without synchronous condensers, electrical power systems might become unstable or unreliable, leading to outages and other issues. In general, as the demand for clean, efficient, and reliable electrical power increases over time, the market for synchronous condensers is likewise projected to expand substantially. When looking at macro level analysis of data on the synchronous condenser market, there are several major results. First, there are various trends, drivers, and challenges shown that can have a notable impact on market growth. By considering them, leaders can make sound decisions when it comes to the future of the industry.

Frequently Asked Questions

What are the growth drivers of the synchronous condenser market?

Ans - SmartGrid Technology, Energy Efficiency and Urbanization and Industrialization is driving factor of Synchronous condenser Market.

What are the Segments on which the synchronous condenser market research is based on?

Ans - The Cooling Type, Reactive Power Rating, Starting Method and Application are the segments based on which the synchronous condenser market research is presently being carried out.

Which are the major companies in the synchronous condenser market?

Ans- The major key players in the synchronous condensor are ABB Ltd., BRUSH Group, Eaton Corporation PLC, Fuji Electric Co., Ltd., General Electric, Hyundai Idela Electric Co., Mitsubishi Electric Corporation, Siemens AG, Voith GmBH, WEG Electric corp.

How big is the Synchronous Condenser Market?

Ans: The Synchronous Condenser market size will be growing to US$ 939.03 million during the forecast period 2023 to 2031.

What is the Growth Rate of the Synchronous Condenser Market?

Ans: The Synchronous Condenser market is anticipated to grow with a CAGR of 4.1 % during the forecast period (2023-2031).

Reach out to Us: The Insight Partners

0 notes

Text

Flexible AC Transmission System Market in Asia Pacific is expected to expand at a rapid CAGR | Allied Market Research

Allied Market Research, titled, “Flexible AC Transmission System Market," The flexible ac transmission system market was valued at $1.2 billion in 2022, and is estimated to reach $2.3 billion by 2032, growing at a CAGR of 7% from 2023 to 2032.

Flexible Alternating Current Transmission System (FACTS) refers to a collection of power electronic devices and systems used in electrical power transmission networks. The purpose of FACTS is to enhance the control and flexibility of AC (alternating current) power flow. These devices are strategically placed in the power grid to regulate voltage, stabilize power flow, and increase the transmission capacity of lines. By actively manipulating key parameters, such as voltage, impedance, and phase angle, FACTS devices optimize power transmission, mitigate issues like voltage fluctuations and line congestion, and improve overall system stability and efficiency.

Flexible alternating current transmission system (FACTS) devices such as Static Var Compensators (SVC) and Static Synchronous Compensators (STATCOM), are used to regulate voltage levels and maintain voltage stability in power systems. They provide reactive power compensation and help mitigate voltage fluctuations caused by varying load conditions or disturbances in the grid. Flexible Alternating Current Transmission System (FACTS) devices such as Unified Power Flow Controllers (UPFC), Thyristor-Controlled Series Capacitors (TCSC), and Static Synchronous Series Compensators (SSSC), enable control of active and reactive power flow in transmission lines. They can adjust line impedance, improve power transfer capability, and optimize power flow distribution within the grid.

The flexible AC transmission systems (FACTS) market is segmented on the basis of compensation type, controller, industry vertical and region. On the basis of compensation type, the flexible AC transmission system market outlook is divided into series compensation, shunt compensation, and combined series-shunt compensation. In 2022, the series compensation segment dominated the market, in terms of revenue, and combined series-shunt compensation segment is projected to acquire the highest CAGR from 2023 to 2032. On the basis of controller, the flexible AC transmission system market forecast is segregated into synchronous compensator (STATCOM), static VAR compensator (SVC), unified power flow controller (UPFC), thyristor controlled series compensator (TCSC), and others. The others segment acquired the largest share in 2022 and synchronous compensator (STATCOM) is expected to grow at a significant CAGR from 2023 to 2032. On the basis of industry vertical, the flexible AC transmission system market growth is bifurcated into oil and gas, electric utility, railways, and others. The others segment acquired the largest share in 2022 and electric utility segment is expected to grow at a significant CAGR from 2023 to 2032.

Region-wise, the flexible AC transmission systems (FACTS) market trends are analyzed across North America (the U.S., Canada, and Mexico), Europe (UK, Germany, France, Italy, and Rest of Europe), Asia-Pacific (China, India, Japan, Australia , and Rest of Asia-Pacific), and LAMEA (Latin America, Middle East, and Africa). Asia-Pacific remain significant participants in the flexible AC transmission systems (FACTS) market for installing flexible AC transmission line using various flexible AC transmission system devices during the forecast period.

KEY FINDINGS OF THE STUDY

The Flexible AC Transmission System Industry has been witnessing steady growth over the years, driven by increasing demand for grid optimization, renewable energy integration, and power quality improvement. The Flexible AC Transmission System Market Size is expected to continue expanding in the coming years.

Grid modernization initiatives, aimed at upgrading aging infrastructure and improving grid flexibility and reliability, have been a major driver for the deployment of FACTS devices. Governments and utilities are investing in the modernization of transmission systems, creating a huge opportunity for Flexible AC Transmission System Market share.

The adoption of FACTS technologies varies across regions. Developed economies, such as North America and Europe, have been early adopters of FACTS devices due to their well-established power infrastructure and grid modernization efforts. However, emerging economies in Asia-Pacific, such as China and India, are expected to exhibit significant market growth due to their increasing electricity demand and infrastructure development plans. Therefore, such Flexible AC Transmission System Market Trends are observed around the developing nations.

Market players are increasingly forming strategic collaborations and partnerships to enhance their technological capabilities, expand their market reach, and offer integrated solutions. These collaborations aim to leverage the expertise of different stakeholders in the value chain and accelerate market growth.

The key players profiled in the report include ABB Ltd, Adani Power Ltd, ALSTOM SA, CG Power and Industrial Solutions Limited, Eaton Corporation, General Electric, Hyosung Corporation, Mitsubishi Electric Corporation, NR Electric Co. Ltd, and Siemens AG. Market players have adopted various strategies such as collaboration, investment, and contracts to expand their foothold in the Flexible AC Transmission System Market analysis.

0 notes

Text

𝐏𝐨𝐰𝐞𝐫 𝐄𝐥𝐞𝐜𝐭𝐫𝐨𝐧𝐢𝐜𝐬 𝐌𝐚𝐫𝐤𝐞𝐭 𝐆𝐫𝐨𝐰𝐭𝐡 𝐀𝐧𝐚𝐥𝐲𝐬𝐢𝐬 𝐛𝐲 𝐒𝐢𝐳𝐞, 𝐒𝐡𝐚𝐫𝐞 & 𝐅𝐨𝐫𝐞𝐜𝐚𝐬𝐭 𝐭𝐨 2030 | 𝐆𝐐 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡

The Power Electronics market is set to witness remarkable growth, as indicated by recent market analysis conducted by GQ Research. In 2023, the global Power Electronics market showcased a significant presence, boasting a valuation of US$ 27.89 Billion. This underscores the substantial demand for Power Electronics technology and its widespread adoption across various industries.

Get Sample of this Report at: https://gqresearch.com/request-sample/global-power-electronics-market/

Projected Growth: Projections suggest that the Power Electronics market will continue its upward trajectory, with a projected value of US$ 41.80 Billion by 2030. This growth is expected to be driven by technological advancements, increasing consumer demand, and expanding application areas.

Compound Annual Growth Rate (CAGR): The forecast period anticipates a Compound Annual Growth Rate (CAGR) of 4.25%, reflecting a steady and robust growth rate for the Power Electronics market over the coming years.

Technology Adoption: The adoption of power electronics technologies spans diverse sectors, including automotive, renewable energy, consumer electronics, industrial automation, and telecommunications. Innovations such as silicon carbide (SiC) and gallium nitride (GaN) semiconductors, advanced control algorithms, and digital power management systems enable enhanced efficiency, higher power density, and improved reliability in power electronic devices. Moreover, the proliferation of electric vehicles, smart grids, and renewable energy systems drives the demand for innovative power electronics solutions, accelerating technology adoption across industries.

Application Diversity: Power electronics find applications in an array of systems and devices, ranging from motor drives, inverters, and converters to uninterruptible power supplies (UPS), electric vehicle powertrains, and renewable energy converters. Their versatility allows for precise control of voltage, current, and frequency, facilitating energy conversion and management in diverse environments. Additionally, power electronics play a crucial role in grid stabilization, power factor correction, and reactive power compensation, contributing to the efficiency and reliability of electrical infrastructure.

Consumer Preferences: Consumers value power electronics solutions that offer energy efficiency, reliability, and compatibility with emerging technologies. In the consumer electronics sector, demand for energy-efficient power adapters, chargers, and inverters drives the preference for compact, lightweight, and high-performance devices. Moreover, as sustainability gains prominence, consumers seek products with minimal environmental impact, prompting manufacturers to prioritize energy-efficient designs, recyclable materials, and eco-friendly manufacturing processes.

Technological Advancements: Technological advancements in power electronics encompass improvements in semiconductor materials, packaging techniques, and system integration methods. The development of wide-bandgap semiconductors, such as SiC and GaN, enables higher operating temperatures, reduced switching losses, and increased power density in electronic devices. Furthermore, advancements in digital control algorithms, predictive maintenance techniques, and fault-tolerant designs enhance system performance, reliability, and safety across diverse applications.

Market Competition: The power electronics market is characterized by intense competition among established players, semiconductor manufacturers, and emerging startups. Key market players invest in research and development to drive innovation, expand product portfolios, and gain a competitive edge in rapidly evolving markets. Strategic collaborations, partnerships, and acquisitions enable technology integration, market penetration, and differentiation, fueling market growth and diversification.

Environmental Considerations: Environmental considerations are integral to the design, manufacturing, and operation of power electronics systems. Efforts to improve energy efficiency, reduce power losses, and minimize environmental impact drive the adoption of eco-friendly materials, energy-efficient designs, and recyclable components. Additionally, initiatives to promote circular economy principles, such as product refurbishment, remanufacturing, and end-of-life recycling, contribute to resource conservation and sustainability in the power electronics industry.

Regional Dynamics: Different regions may exhibit varying growth rates and adoption patterns influenced by factors such as consumer preferences, technological infrastructure and regulatory frameworks.

Key players in the industry include:

ABB Group

Renesas Electronics Corporation

Rockwell Automation Inc.

Microsemi Corporation

Texas Instruments Inc.

Infineon Technologies AG

STMicroelectronics NV

Fuji Electric Co.Ltd.

Qualcomm Inc.

Mitsubishi Electric Corp.

The research report provides a comprehensive analysis of the Power Electronics market, offering insights into current trends, market dynamics and future prospects. It explores key factors driving growth, challenges faced by the industry, and potential opportunities for market players.

For more information and to access a complimentary sample report, visit Link to Sample Report: https://gqresearch.com/request-sample/global-power-electronics-market/

About GQ Research:

GQ Research is a company that is creating cutting edge, futuristic and informative reports in many different areas. Some of the most common areas where we generate reports are industry reports, country reports, company reports and everything in between.

Contact:

Jessica Joyal

+1 (614) 602 2897 | +919284395731

0 notes

Text

Static VAR Compensator Market Trends, Outlook, and Size Analysis 2023-2030

In the world of electrical power systems, maintaining stability and reliability is paramount. Enter Static VAR Compensators (SVCs), the unsung heroes of the electricity grid. These advanced devices play a crucial role in regulating voltage, improving power factor, and enhancing system performance. Join us as we delve into the dynamic realm of the Static VAR Compensator Market, where innovation meets energy efficiency, and grid stability takes center stage.

Unveiling the Power of Control: Understanding the Static VAR Compensator Market

The Static VAR Compensator (SVC) Market is a key segment of the power electronics industry, dedicated to enhancing the stability and efficiency of electrical grids. SVCs are sophisticated devices that dynamically adjust reactive power to regulate voltage levels, mitigate voltage fluctuations, and improve the power factor of transmission and distribution systems. With the increasing integration of renewable energy sources and the evolving demands of modern power systems, the demand for SVCs is on the rise, driving innovation and investment in the market.

Request Sample Report: https://www.snsinsider.com/sample-request/3195

Exploring Precision Engineering: Segmentation Analysis

To better understand the Static VAR Compensator Market, let's break down its key segments:

Type of SVC: SVCs come in various configurations, including Thyristor-Controlled SVCs (TCSC), Thyristor-Switched Capacitor (TSC), and Thyristor-Controlled Reactor (TCR), each with specific applications and performance characteristics.

Voltage Rating: SVCs are classified based on their voltage capacity, ranging from low-voltage distribution systems to high-voltage transmission networks, catering to diverse grid requirements.

Application: SVCs find applications in transmission grids, distribution networks, industrial facilities, renewable energy plants, and other critical infrastructure, where voltage stability and power quality are paramount.

End-User Sector: Utilities, grid operators, industrial facilities, renewable energy developers, and infrastructure projects are among the key users driving the adoption of SVC technology.

Harnessing Grid Intelligence: Impact on Power Systems

The Static VAR Compensator Market is not just about reactive power control; it's about enhancing grid stability, reliability, and efficiency. By dynamically adjusting reactive power output, SVCs help maintain voltage levels within acceptable limits, improve power factor, and mitigate voltage flicker and oscillations. Moreover, by providing fast and precise response to grid disturbances, SVCs enhance the resilience of power systems, reduce transmission losses, and optimize the utilization of existing infrastructure, leading to cost savings and improved performance.

Global Perspectives: Regional Outlook

The adoption of Static VAR Compensators varies across different regions, influenced by factors such as grid infrastructure, regulatory environment, and energy policies. Developed economies in North America, Europe, and Asia-Pacific lead the market, driven by investments in grid modernization, renewable energy integration, and transmission upgrades. Emerging economies in Latin America, Africa, and the Middle East present opportunities for market growth, as governments prioritize infrastructure development and energy transition initiatives.

Driving Innovation and Collaboration: Competitive Analysis

Leading companies in the Static VAR Compensator Market, such as ABB Ltd., Siemens AG, and GE Renewable Energy, are driving innovation and shaping the future of grid stability solutions. Through research and development initiatives, strategic partnerships, and investments in smart grid technologies, these companies are pushing the boundaries of SVC technology and unlocking new opportunities for grid optimization and resilience. Moreover, startups and technology providers are entering the market, exploring niche applications and disruptive solutions, driving competition and innovation.

Conclusion: Powering a Resilient Future

In conclusion, the Static VAR Compensator Market represents a critical enabler of grid stability and reliability in an era of increasing energy complexity and renewable integration. By harnessing the power of reactive power control and grid intelligence, SVCs play a pivotal role in ensuring the smooth operation of power systems, enhancing energy efficiency, and supporting the transition to a sustainable energy future. As utilities, grid operators, and energy stakeholders embrace the importance of grid stability, let us leverage the potential of Static VAR Compensators to build a resilient, reliable, and sustainable energy infrastructure for generations to come.

Access Full Report Details: https://www.snsinsider.com/reports/static-var-compensator-market-3195

0 notes

Text

GaN Semiconductor Device Market Booming Worldwide with Latest Trend and Future Scope by 2028

The global GaN semiconductor device market size is estimated to be worth USD 21.1 billion in 2023 and is projected to reach USD 28.3 billion by 2028, at a CAGR of 6.1% during the forecast period.

Increasing adoption of GaN semiconductor devices in consumer and business enterprises, surging deploymnet of GaN semiconductor devices in energy & power industry, and growing integration of GaN semiconductor devices in automotive industry are some of the major factors driving the market growth globally.

Discrete semiconductor segment to register largest market share in the GaN semiconductor device market during forecast period

Discrete GaN semiconductor components include GaN transistors and GaN diodes that are individually packaged and marketed. These components are used in diverse applications such as power supply units, inverters, and radio frequency (RF) amplifiers. GaN transistors and diodes effectively manage substantial voltage and current levels, leading to powerful designs. Additionally, they enable more compact and lightweight circuits suitable for applications where constraints on size and weight are paramount.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=698

Power & Energy to register highest CAGR in the GaN semiconductor device market during forecast period The energy & power segment is expected to grow at the highest CAGR during the forecast period. This growth can be attributed to the rising integration of GaN semiconductor devices into electronic systems to work in elevated temperatures, pressures, and voltages. Moreover, The GaN semiconductor technology foresees extensive adoption in energy and power solutions, encompassing realms such as energy storage systems, solar DC to AC inverters, AC solar panels, and volt-ampere reactive (VAR) compensators in the future.

Asia Pacific held for the largest GaN semiconductor device market share in 2022 Asia Pacific is accounted for the largest share of the GaN semiconductor device market in 2022. The presence of established several semiconductor manufacturing companies such as Toshiba (Japan), Nichia Corporation (Japan), and Mitsubishi Electric (Japan), increasing integration in consumer & business enterprise verticals, government-led initiatives for innovation and industrial development are the major factors driving the market growth in Asia Pacific.

GaN Semiconductor Device Market Key Players The major players in the GaN semiconductor device companies include Qorvo, Inc. (US), Wolfspeed, Inc. (US), Sumitomo Electric Industries, Ltd. (Japan), MACOM Technology Solutions Holdings, Inc. (US) and Infineon Technologies AG (Germany). These companies have used both organic and inorganic growth strategies such as product launches, agreements, collaborations, acquisitions, partnerships and expansions to strengthen their position in the market.

0 notes

Text

0 notes

Text

May 24, 2022 (Market Insight Reports) -- Reactive Power Compensation Device Market (US, Europe, Asia-Pacific) 2022 Global Industry Market research report gives key assessment on the market status of the Reactive Power Compensation Device producers with Market Size, improvement, share, floats similarly as industry cost structure. Reactive Power Compensation Device Market Report will incorporate the examination of the impact of COVID-19 on this industry.

0 notes

Text

"After John James Audubon (American Woodsman)" 2021.

Vintage posters, Franklinia alatamaha seeds, cotton, antique frame, plywood, plexi, glue, hardware, vintage lumber, iron oxide stain, light-reactive sound device, 1950s sound recordings of Vermivora bachmanii, vintage darning egg, vintage needle and spools, Sturnus vulgaris skull, wool socks knitted by Bobby Wilcox, original wallpaper digitally designed using copyright free historic images, printed by SpoonFlower Inc, self-published zine.

I was invited by Goucher College Curator and Director of Exhibitions Alex Ebstein to create this installation for the "Rediscovering Goucher's Lost Museum" exhibition in fall 2021. Documentation photos generously made by Vivian Marie Doering @vivianmariephoto on Instagram.

Artist Statement:

“On the whole, the task of turning Audubon’s original images into marketable engravings proved to be an extremely labor-intensive process that relied, almost immediately, on the work of dozens of artisans, often working directly under Audubon’s ever-critical eye. But the work process went well beyond the engraver’s shop. Unseen and unheralded others likewise made a critical contribution to the project: the papermakers who produced the huge, high-quality sheets Audubon required; the copper smelters who turned raw ore into clean ingots; the miners who extracted the ore from the earth in the first place; and so forth, back through all the prior steps of production. In that sense, The Birds of America was not just an extensive work of art, not just an example of the sole genius of the lone, struggling artist. It was, rather, an ambitious business venture that relied on a complex labor process and an extensive supply chain, an enterprise in which the artist became not just the designer of the work, but the administrative manager of dozens of people, many of whom could be called artists in their own right, and a marketer to prospective customers, many of whom he had to track down wherever he could find them, on both sides of a very wide ocean.”

--Gregory Nobles, John James Audubon: The Nature of the American Woodsman, 2017. p103

Beyond the ‘supply chain’ of compensated workers existed a backdrop of the truly Unseen and Unheralded – the enslaved Black people whose supportive labor was violently coerced; and the work of Maria Martin, an ‘artist in [her] own right’ whose labor was given, and taken, freely due to her faith and her standing as an unmarried, white woman in the Antebellum South. Utilizing the exquisite Martin-Audubon collaborative painting, "Bachman's Warbler", as a jumping-off point, this installation is a visual exploration of the cultural and structural scaffolding that made such erasure possible during that era, as well as two examples of natural history showcased by the painting that have been lost and found - the now extinct Bachman's Warbler (Vermivora bachmanii) for which this painting and a few short sound recordings are our best documentation of the species' existence, and Franklin Tree (Franklinia alatamaha) a species native to the southeastern US that narrowly avoided utter extinction thanks to the collectors John and William Bartram, and that now exists in scattered cultivation across the country.

This project is not meant as a wholesale ‘cancel’ of John James Audubon or early American naturalists – whose work, at times disturbingly tainted by prevailing beliefs and customs, nevertheless paved the way for the scientific fields of biology and ecology today. This installation is, rather, an acknowledgment of the conflicted entanglements between history, nature, people, race, gender, ideology, belief, imagery, and power.

Collections are essentially a grandiose form of appropriation, recontextualizing objects for myriad purposes. This installation plays with two traditions: collections and appropriation, by appropriating and recontextualizing Audubon’s work, as well as other historical illustrations from various collections, and using metaphor and allegory as tools to tell the story. It would not have been made possible without the help, labor, and/or support of many unseen and unheralded, including the anonymous archivists at the Internet Archive, New York Public Library Digital Collections, and Cornell’s Macaulay Library, collectors on Ebay, Etsy, Facebook Marketplace, and Bazaar in Hamden, the production team at Spoonflower, and most especially Alex Ebstein, Bobby Wilcox, Seth Adelsberger, Denise Wilcox, Patti Murphy, Wyatt Hersey, Jenny Rieke and Oona McKay.

4 notes

·

View notes

Text

PLATINUM

The most precious metal is platinum.

Platinum is a type of precious metal, not to mention the most valuable metal in the world, which is just a few trillion dollars.

Metals that are difficult to extract from ore and that are commercially very expensive are called rare metals.

Chemically rare metals are less reactive than other basic substances. They are usually soft and elastic and have a light glow. Historically rare metals were used as currency. But now, they are used as industrial and investment products. Such as gold, silver, platinum, and palladium each have an IS and 4216 currency code.

The most well-known rare metals are gold and silver. These are used in making art, jewelry, and coins. Platinum group metals are also considered rare metals. Such as ruthenium, rhodium, palladium, osmium, iridium, and platinum. Of these, platinum is used commercially as a commodity. There is a demand for rare metals in practical aspects and investment and as a holder of assets. Historically, the market price of rare metals is much higher than that of ordinary industrial metals.

Advantages: Thermocouple series platinum and rhodium thermocouple with maximum precision, best durability, temperature range, long life, high-temperature, high limit advantage. Suitable for use in oxidizing and emergency atmospheres, but also for short-term use in the case of vacuums, but not in reduced atmospheres or the atmosphere of metals or irregular vapors. A significant advantage of the Type B thermocouple is that compensation is not required because the thermoelectric power is less than 3μV between 0 and 50 C.

Disadvantages: Lack of platinum and radium thermoelectric energy thermocouple, low thermal power rate, high-temperature mechanical energy read sensitive, highly sensitive to pollution, expensive precious metal materials, and thus one-time investment.

Platinum and rhodium thermocouple work Platinum and rhodium thermocouples are made up of two different components of conductors at both ends of the loop. While the two junction temperatures are different, it will generate heat in the loop. Suppose there is a temperature difference between the thermocouple and the working end at the reference end. In that case, the display device will indicate the potential corresponding temperature value of the thermoelectric generated by the thermocouple.

Platinum and Rhodium Thermocouple Selection: Normal Measurement Temperature 1000 ~ 1300 ℃ Single Platinum and Rhodium Thermocouple (Platinum and Rhodium 10-Platinum), 1200 ~ 1600 ℃ General Measurement Double Platinum and Rhodium Measurement Temperature and Rhodium 6), used to ensure the service life of the temperature range platinum and rhodium the diameter of type B thermocouple filament for the precious metal thermocouple is 0.5 mm, the deviation is -0.015 mm. The nominal chemical composition of the positive electrode (BP) is platinum, and rhodium alloy, which is 30% rhodium, 70% platinum, negative (BN) is platinum and radium alloy, 6% radium, hence commonly known as double platinum and rhodium The maximum temperature of the thermocouple is 1600 ℃, the maximum temperature is 1800. thermocouple.

4 notes

·

View notes

Text

Reactive Power Compensation Device Global Market 2019-2025 Growth, Trends and Demands Research Report

Reactive Power Compensation Device Global Market 2019-2025 Growth, Trends and Demands Research Report

The portion of power that, averaged over a complete cycle of the AC waveform, results in net transfer of energy in one direction is known as active power.

With the gradual maturity and improvement of SVC and SVG technology, the product costs have been dropping, the application field will continue to expand, and the active power market share will also increase, while the market share of shunt…

View On WordPress

#Reactive Power Compensation Device#Reactive Power Compensation Device CAGR#Reactive Power Compensation Device industry#Reactive Power Compensation Device market#Reactive Power Compensation Device report#Reactive Power Compensation Device research#Reactive Power Compensation Device sales#Reactive Power Compensation Device trends

0 notes