#Synthetic Data Generation Market size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

130K people were victims of a chain letter scam that affected Tumblr in May 2011.

Text

Synthetic Data Generation Market Production Value, Gross Margin Analysis

Global synthetic data generation market will grow from $0.3 billion in 2023 to $2.1 billion by 2028, with a growth rate of 45.7% per year during this period.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=176419553&utm_source=tumblr.com&utm_medium=referral+&utm_campaign=chatbotmarket

Uses of Synthetic Data:

The synthetic data generation market is used in various areas, such as AI/ML training, data anonymization, test data management, data sharing, and analytics. Major industries using synthetic data include Banking, Financial Services, and Insurance (BFSI), Healthcare, Retail, Automotive, Government, IT, Energy, Manufacturing, and more.

Why Synthetic Data is Important:

Stricter data privacy rules and security concerns make it harder to use real-world data. Synthetic data provides a safe alternative by allowing organizations to generate data without risking sensitive information. This helps businesses make data-driven decisions while complying with privacy regulations.

BFSI Sector to Lead the Market:

The BFSI (Banking, Financial Services, and Insurance) sector is expected to be the largest user of synthetic data. This sector needs synthetic data to meet privacy rules and improve risk management, fraud detection, and customer analytics. Synthetic data allows BFSI organizations to create realistic datasets without compromising sensitive information, helping them comply with regulations.

Image and Video Data Segment to Dominate:

Synthetic data for image and video involves creating artificial visual content that mimics real-world scenarios. This is crucial for training AI models in areas like computer vision, object detection, and video analysis. Synthetic image and video data are used in developing algorithms for autonomous vehicles, surveillance, medical imaging, and virtual reality. This segment is expected to have the highest market share during the forecast period.

Asia Pacific Region to Experience Fastest Growth:

The synthetic data generation market in Asia Pacific is growing rapidly due to digital transformation, stricter data privacy regulations, and the increasing use of AI and ML technologies. The region’s focus on digitalization and the need for data-driven solutions will drive continued growth and new opportunities in this market.

Key Players in the Market:

Major companies in the synthetic data generation market include Microsoft, Google, IBM, AWS, NVIDIA, OpenAI, Informatica, Broadcom, Sogeti, Mphasis, Databricks, MOSTLY AI, Tonic, MDClone, TCS, Hazy, Synthesia, Synthesized, Facteus, Anyverse, Neurolabs, Rendered.ai, Gretel, OneView, GenRocket, YData, CVEDIA, Syntheticus, AnyLogic, Bifrost AI, and Anonos. These companies are based in various countries, including the US, UK, India, Israel, Austria, Spain, Scotland, and Switzerland.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America's best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

To find out more, visit www.MarketsandMarkets™.com or follow us on Twitter, LinkedIn and Facebook.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: [email protected] Visit Our Website: https://www.marketsandmarkets.com/

#Synthetic Data Generation Market#Synthetic Data Generation Market size#Synthetic Data Generation Market share#Synthetic Data Generation Market trends#Synthetic Data Generation Market demand#Synthetic Data Generation Market overview#Synthetic Data Generation Market New Research Report#Synthetic Data Generation#Synthetic Data Generation Industry

0 notes

Text

Sodium Methoxide Market Size, Share, Development by 2033

According to Fact.MR's latest study, the global sodium methoxide market reached US$ 217.3 million in 2023. Over the period from 2023 to 2033, demand for sodium methoxide catalysts worldwide is expected to grow at a compound annual growth rate (CAGR) of 2.4%, reaching US$ 276 million by 2033.

The global market is anticipated to expand significantly, driven by increasing investments in various sectors such as pharmaceuticals and agrochemicals. Key industry players are also expected to boost their research and development efforts to enhance production capacities and innovate manufacturing processes, thereby creating lucrative opportunities.

Get Free Sample Copy of This Report: https://www.factmr.com/connectus/sample?flag=S&rep_id=2800

The expanding applications of sodium methoxide across industries such as agriculture, pharmaceuticals, and agrochemicals are expected to create significant opportunities for suppliers. Additionally, its role as a catalyst in synthetic detergents, grease, and edible oil processing is poised to further bolster market growth globally.

Key Takeaways from Market Study

In 2022, global demand for sodium methoxide reached US$ 212.2 million.

By 2023, the global sodium methoxide market is estimated to be valued at US$ 217.3 million, with projections indicating it will reach US$ 276 million by the end of 2033.

From 2023 to 2033, worldwide sales of sodium methoxide are expected to grow at a CAGR of 2.4%.

By the conclusion of 2033, Asia Pacific is anticipated to hold a 38.1% share of the global market.

Demand for sodium methoxide in pharmaceutical applications is forecasted to increase at a 2.5% CAGR through 2033.

“Growing use of sodium methoxide as a versatile reagent in several chemical synthesis processes along with its application in the production of fragrances, agrochemicals, etc., is projected to contribute to generating opportunities for players,” says a Fact.MR analyst.

Significant Increase in Biodiesel Production

The expansion of the sodium methoxide market is propelled by the rising production of biodiesel, where sodium methoxide serves as a catalyst. The growing demand for biodiesel is driven by its environmentally friendly and renewable characteristics, contrasting with conventional fossil fuels. Methoxide catalysts are essential in the transesterification process, converting animal fats or vegetable oils into biodiesel. Consequently, the increasing global demand for biodiesel as a clean energy alternative is expected to drive the need for sodium methoxide across various regions.

Leading Market Players

Key manufacturers of sodium methoxide are

Dezhou Longteng Chemical Co. Ltd.

BASF SE

E. I. du Pont de Nemours and Company

Evonik Industries

Anhui Jinbang Medicine Chemical Co. Ltd.

Inner Mongolia Lantai Industries Co., Ltd.

Zibo Xusheng Chemical Co. Ltd.

Read More: https://www.factmr.com/report/2800/sodium-methioxide-market

More Valuable Insights on Offer

Fact.MR, in its new offering, presents an unbiased analysis of the sodium methoxide market, presenting historical demand data for 2018 to 2022 and forecast statistics for 2023 to 2033.

The study divulges essential insights into the market based on type (solid, liquid/solution) and end-use industry (pharmaceuticals, agrochemicals, plastic & polymers, personal care, analytical reagents, biodiesel), across major regions of the world (North America, Europe, Asia Pacific, Latin America, and MEA).

𝐂𝐨𝐧𝐭𝐚𝐜𝐭:

US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, +353-1-4434-232 Email: [email protected]

1 note

·

View note

Text

Global Siliconized Film Market Analysis Report (2025–2031)

"

The Global Siliconized Film Market is projected to grow steadily from 2025 through 2031. This report offers critical insights into market dynamics, regional trends, competitive strategies, and upcoming opportunities. It's designed to guide companies, investors, and industry stakeholders in making smart, strategic decisions based on data and trend analysis.

Report Highlights:

Breakthroughs in Siliconized Film product innovation

The role of synthetic sourcing in transforming production models

Emphasis on cost-reduction techniques and new product applications

Market Developments:

Advancing R&D and new product pipelines in the Siliconized Film sector

Transition toward synthetic material use across production lines

Success stories from top players adopting cost-effective manufacturing

Featured Companies:

Loparex

Polyplex

Siliconature

Avery Dennison

UPM Raflatac

Mondi

Laufenberg GmbH

Infiana

Nan Ya Plastics

Rayven

Toray

Mitsubishi Polyester Film

YIHUA TORAY

NIPPA

Fujiko

TOYOBO

Mitsui Chemicals Tohcello

SJA Film Technologies

HYNT

3M

Saint-Gobain Performance Plastics

Molymer

Garware Polyester

Ganpathy Industries

HSDTC

Xinfeng

Xing Yuan Release Film

Zhongxing New Material Technology

Road Ming Phenix Optical

Hengyu Film

Get detailed profiles of major industry players, including their growth strategies, product updates, and competitive positioning. This section helps you stay informed on key market leaders and their direction.

Download the Full Report Today https://marketsglob.com/report/siliconized-film-market-2/1710/

Coverage by Segment:

Product Types Covered:

PET Substrate Siliconized Film

PE Substrate Siliconized Film

PP Substrate Siliconized Film

Others

Applications Covered:

Labels

Tapes

Medical Products

Industrial

Others

Sales Channels Covered:

Direct Channel

Distribution Channel

Regional Breakdown:

North America (United States, Canada, Mexico)

Europe (Germany, United Kingdom, France, Italy, Russia, Spain, Benelux, Poland, Austria, Portugal, Rest of Europe)

Asia-Pacific (China, Japan, Korea, India, Southeast Asia, Australia, Taiwan, Rest of Asia Pacific)

South America (Brazil, Argentina, Colombia, Chile, Peru, Venezuela, Rest of South America)

Middle East & Africa (UAE, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of Middle East & Africa)

Key Insights:

Forecasts for market size, CAGR, and share through 2031

Analysis of growth potential in emerging and developed regions

Demand trends for generic vs. premium product offerings

Pricing models, company revenues, and financial outlook

Licensing deals, co-development initiatives, and strategic partnerships

This Global Siliconized Film Market report is a complete guide to understanding where the industry stands and how it's expected to evolve. Whether you're launching a new product or expanding into new regions, this report will support your planning with actionable insights.

" Encoder Chips Market Encoder IC Market Encoder Market Encorafenib Market Encrypted Phone Market End Brush Market End Mill Adapters Market End Milling Machine Market End Suction Fire Pump Market End Suction Pumps Market End Tenoner Machine Market End-fixing Tape Market Ending Machine Market Endless Pool Market Endo Bag Market

0 notes

Text

Revolutionize Your Business with Generative AI Services by Advans Appz

In the growing age of intelligent automation, those leveraging innovative technologies and innovative approaches are likely to prosper—significantly outpacing competitors that do not. Advans Appz is helping those small businesses become successful by using its powerful, affordable, and scalable generative AI services. Our goal is to make next-gen artificial intelligence accessible to businesses of all sizes—especially the ones looking to move to automation and utilization without lots of money and time!

Generative AI is among the highest value transformational technologies within the current landscape of digital business. Generative AI is the technology that creates while generative models learn from existing data. Advans Appz is providing services within generative AI while generating value to your teams. From generating better content and marketing items to creating synthetic data and automating graphics, these services used to take teams of employees and hours to create the same deliverables. With Advans Appz, you are empowering your teams and will directly integrate generative AI into your work processes.

We have also created our solutions specifically for small businesses. Our point of leverage is to focus on easy-to-use AI that plugs seamlessly into existing generative AI processes and existing businesses. With our products you can access many means of producing AI generated product descriptions, AI generated email campaigns, AI generated social media content, AI generated responses to customers, and develop quality output in record time and at less cost. We also will support creation of visual generated content like logos, mockups, ads, videos, and other graphics—leveraging advanced generative models.

The Advans Appz method is extremely consultative. Our first step is to analyze your specific needs, pains, and goals. After meeting with you our artificial intelligence professionals will have identified potential areas where generative AI can have a high impact (content creation, lead generation, customer support, operations, etc.), and from there we will build and implement solutions that give you real, measurable, return on investment.

All our generative AI services come with training and post-deployment support. We work with your staff to understand how to use AI tools, manage outputs, and iterate with feedback. As your needs increase our solutions are built on scalable infrastructure and we continue to evolve your AI experience.

Our scope of work includes many industries (retail, marketing, real estate, ecommerce, health, education, etc.). Regardless of industry, our AI solutions help to do more with less, allow more time on productive activities and improve engagement with customers. Our clients typically see massive reductions in operational costs and time wasted of repetitive or redundant tasks and creative processes and outputs will scale exponentially.

Security and ethics are also a focus of Advans Appz. We follow best practices for responsible AI use so that you can be sure your data is safe and your models are transparent. We avoid, to the best of our ability, bias, abide by all data privacy laws, and follow any and all industry regulations relevant in our field.

For an innovative business looking to harness the power of AI, Advans Appz is the right fit for you. The generative AI services we offer are not only cost-effective and reliable, but transformative. With our help, your business can rethink how it creates, communicates and grows.

Start your journey with Advans Appz today. Experience how generative AI transforms your work by finding new use cases, accelerating innovation, and rethinking the way your company works. Contact us now to begin the next revolution and find out how smarter, more automated practices can help your business.

0 notes

Text

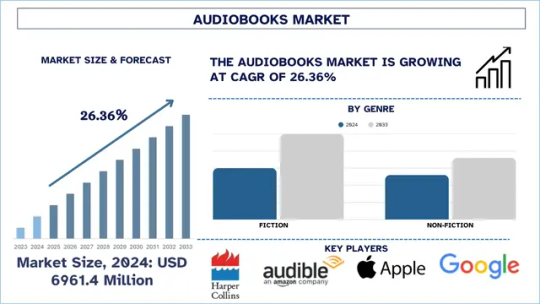

Audiobooks Market Growth, Size, Trends, Share and Forecast to 2033

The audiobook industry has experienced rapid growth over the past decade, transforming from a niche format into a mainstream medium for consuming literature and informational content. Large parts of this growth have been driven by the adoption of sophisticated technologies that are revolutionizing production, distribution, and consumer interaction. From AI-narrated audiobooks to engaging experiences with spatial audio, technology is revolutionizing the future of audiobooks. According to the UnivDatos analysis, the growing popularity of mobile devices, the rising popularity of audiobooks among various age groups, and the integration of advanced technologies drive the audiobooks market. As per their “Audiobooks Market” report, the global market was valued at USD 6,961.4 million in 2024, growing at a CAGR of about 26.36% during the forecast period from 2025 - 2033 to reach USD million by 2033.

AI and Synthetic Voice Narration

One of the biggest technologies on the audiobook platform is the emergence of AI-driven voice narration. Google, Amazon, and startups such as ElevenLabs are creating advanced text-to-speech (TTS) engines that can generate extremely natural, emotionally nuanced audio.

· Cost Efficiency: AI narration significantly cuts the cost of production and time, which makes audiobooks feasible for individual writers and small-scale publishers.

· Multilingual Support: AI enables instant translation and narration of books in other languages, opening up the worldwide audiobook market.

Access sample report (including graphs, charts, and figures): https://univdatos.com/reports/audiobooks-market?popup=report-enquiry

Personalized Recommendations and Adaptive Listening: Tailoring the Experience to the Individual

The integration of data analytics and machine learning algorithms is allowing for a more personalized and adaptable listening experience. Audiobook platforms are now capable of analyzing listening habits, preferences, and even emotional responses to tailor recommendations to individual users. This makes listeners constantly exposed to content that meets their interests, ensuring maximum engagement and discovery. In addition, adaptive listening capabilities are surfacing that dynamically adjust the speed of play, style of narration, and even background music based on the listener's environment and activity. For instance, the audiobook can pause automatically when the listener begins a conversation or change the volume according to the ambient noise level. This degree of personalization generates a smooth and natural listening experience, and the audiobook thus becomes an even more convenient and enjoyable mode of entertainment.

Blockchain and Digital Rights Management (DRM)

New technologies such as blockchain are starting to make a difference to content ownership, royalty tracking, and piracy prevention in the audiobook space.

Transparent Royalty Payments: Smart contracts can automate and ensure fair royalty distribution among authors, narrators, and publishers.

Anti-Piracy Protection: Blockchain can create a verifiable ledger of ownership and distribution, making unauthorized duplication more difficult.

Decentralized Publishing: Independent authors can distribute their work directly to listeners, bypassing traditional gatekeepers.

Although still in its early stages in this sector, blockchain holds promise for improving accountability and equity in the audiobook value chain.

Immersive Experiences Through Spatial Audio

Beyond the narrator's voice, the sound design within an audiobook is crucial to creating an immersive and engaging experience. New audio technologies, especially spatial sound and binaural recording, are adding a new depth and realism to the listening experience. By mimicking the manner in which sound interacts with the human ear and environment, these technologies build a three-dimensional soundscape that immerses listeners into the story itself. Picture hearing the sound of leaves rustling behind you as the main character moves through a forest, or the hum of a crowd around you during a busy marketplace scene. This kind of sonic detail really raises the level of listener involvement and makes for a more engaging and memorable audiobook experience.

For instance, in 2022, Music streaming platform Spotify purchased Findaway, a platform that allows users to create, distribute, and monetize their own audiobooks, for 117 million euros (approx $119 million), leading to a significant growth in the audiobooks market.

Related Reports:

Text-to-Speech Market

Voice Recorder App Market

Kiosk and Subscription-Based Collectibles Market

Comic Book Market

Home Audio Equipment Market

Interactive Audiobooks and Gamification: Transforming Passive Listening into Active Engagement

The future of audiobooks may very well be one of interactivity and gamification. New technology is allowing us to create audiobooks that are more than simply passive listening, where the listener is truly involved in the story. That could mean making choices that drive the story forward, solving puzzles embedded in the sound, or even having a conversation with virtual characters. Imagine an audiobook where you decide the protagonist's actions, leading to different plot outcomes and multiple endings. Such an interactive experience elevates the listening experience beyond a simple passive exercise into an immersive and participatory journey that appeals to a new audience that wants active engagement.

The Future of Audiobooks is Immersive, Interactive, and Personalized

The coming together of revolutionary technologies is shaping the world of audiobooks, turning over new leaves in content creation, delivery, and consumption. From AI narration and immersive audio to recommendations and interactive storytelling, these technologies are revolutionizing the audiobook experience. And so, with technology going further ahead, we can be sure to have yet more creative and immersive listening choices that bridge the gap between conventional book-telling and interactive media. The future of audiobooks is more about being surrounded by a universe of sound than being merely in control of the narratives you experience, actively engaged as a partner to the storylines you're fascinated by, as well as constructing a bespoke bond with the literature you're keen on.

Contact Us:

UnivDatos

Email - [email protected]

Website - www.univdatos.com

#Audiobooks Market#Audiobooks Market Report#Audiobooks Market Segments#Audiobooks Market Growth#Audiobooks Market Size

0 notes

Text

Hemostats Market Demand by Type and Application

Hemostatic Agents Market: Growth, Innovation, and Future Prospects

The hemostatic agents market is experiencing unprecedented growth, driven by technological breakthroughs and an aging global population. As healthcare systems worldwide face increasing surgical volumes and demographic challenges, the demand for advanced bleeding control solutions continues to accelerate.

Market Size and Growth Projections

The hemostatic agents market presents a compelling growth story with varying projections from industry analysts. According to Meticulous Research, the market is projected to reach USD 5.32 billion by 2032, growing at a CAGR of 6.9% during the forecast period. However, alternative industry analyses suggest even more robust growth, with some reports valuing the market at approximately USD 8.9 billion in 2024 and projecting it to reach USD 12.3 billion by 2033. The most optimistic forecasts indicate growth from USD 8.03 billion in 2024 to USD 15.77 billion by 2032, representing a CAGR of 8.8%.

Technological Revolution in Hemostasis

The industry is witnessing a paradigm shift toward bioengineered and synthetic hemostatic agents. Companies like Medcura have developed innovative solutions using patented biopolymer technologies, with their LifeGel™ Absorbable Hemostatic Gel receiving recognition as a 2024/2025 Best Technology in Spine Award. These bioengineered agents offer enhanced biocompatibility, controlled degradation rates, and improved efficacy compared to traditional mechanical methods.

The integration of biomimetic principles has led to materials that closely replicate natural clotting mechanisms. Advanced hemostatic agents, including fibrin sealants and collagen-based sponges, are bioengineered to mimic the body's natural clotting processes, proving valuable in complex surgeries where conventional methods may fall short.

Artificial intelligence and real-time monitoring systems represent the next frontier in hemostatic technology. These systems enable surgeons to make data-driven decisions during procedures, optimizing the selection and application of hemostatic agents based on individual patient characteristics and surgical conditions.

Regulatory Landscape Evolution

The regulatory environment has evolved significantly, with the FDA implementing more nuanced approaches to device classification and approval. The agency has considered loosening premarket expectations for certain absorbable collagen-based hemostatic agents marketed by companies like Integra LifeSciences and Johnson & Johnson's Ethicon.

A notable development is the FDA's proposal to reclassify certain absorbable hemostatic devices from Class III to Class II, potentially streamlining the approval process while maintaining appropriate safety standards. This regulatory evolution encourages greater investment in research and development while balancing innovation with patient safety.

Market Leadership and Competition

The hemostatic agents market is consolidated, with the top 5-6 players accounting for 40-50% of market share in 2024. Key industry leaders include Baxter International Inc., Pfizer Inc., B. Braun Melsungen AG, C. R. Bard Inc., Integra LifeSciences, Medtronic plc, CSL Behring, and Ethicon Inc. (Johnson & Johnson subsidiary).

These major players possess substantial advantages including extensive R&D budgets, established healthcare provider relationships, and comprehensive distribution networks. Their acquisition strategies significantly impact market dynamics, with industry leaders rapidly expanding portfolios by acquiring innovative startups and specialized companies.

Market Segmentation and Applications

Based on application analysis, the surgery segment is expected to account for the largest market share in 2025, driven by recurrent use of hemostatic agents in orthopedic, general, gynecological, and cardiovascular surgeries. The increasing number of accidents and traumatic injuries requiring surgical treatment further supports this segment's growth.

The hospitals and clinics segment dominates the end-user market, attributed to rising patient visits for surgical procedures, increasing surgery volumes, and favorable reimbursement policies. The willingness of hospitals to invest in advanced hemostats reflects the growing recognition of their clinical and economic benefits.

Key Growth Drivers

Multiple factors are propelling market expansion. The increasing prevalence of chronic diseases such as cancer, cardiovascular, orthopedic, and neurological conditions leads to higher surgical procedure volumes. Road traffic crashes, among the leading causes of death globally, represent another significant driver, with approximately 20,653 people killed in road accidents in the EU, representing a 3.7% increase compared to 2021.

The rise in minimally invasive surgical procedures creates substantial demand for sophisticated hemostatic solutions. According to the American Society of Plastic Surgeons, 682,932 non-invasive fat reduction surgeries and 408,970 non-invasive skin tightening surgeries were conducted in the U.S. in 2022, highlighting the growing preference for these procedures.

Emerging Trends and Innovation

Two major trends are shaping the market: biopolymer-based hemostats and dual-action hemostatic technology. Biopolymer-based hemostats are gaining popularity due to their biodegradable, biocompatible, and bioactive properties. These materials come in various forms including particles, powder, sponges, sheets, foams, films, and hydrogels.

Dual-action hemostatic technology represents a significant advancement, effectively controlling bleeding through comprehensive approaches. This technology achieves hemostasis in deep and complex wounds while providing sealing capabilities that offer suture support in vascular surgery.

Market Challenges and Future Outlook

Despite positive growth projections, the market faces challenges including allergic reactions from hemostatic materials and high manufacturing costs that limit adoption in cost-sensitive markets. However, opportunities exist in the increasing use of advanced hemostats, advancements in dental hemostatic agents, and growing demand for preloaded applicators and ready-to-use products.

The future of the hemostatic agents market promises continued innovation, expanding applications, and sustained growth driven by the fundamental need for effective bleeding control in medical procedures. Success will require stakeholders to navigate complex regulatory landscapes, understand diverse regional preferences, and leverage technological capabilities effectively while balancing innovation with safety and cost-effectiveness.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5833

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Hemostats#SurgicalDevices#MinimallyInvasiveSurgery#HealthcareMarket#WoundCare#MedicalDevices#GlobalHemostatsMarket#MarketForecast#SurgicalInnovation#HemostasisSolutions

0 notes

Text

Hemostats Market Demand by Type and Application

Hemostatic Agents Market: Growth, Innovation, and Future Prospects

The hemostatic agents market is experiencing unprecedented growth, driven by technological breakthroughs and an aging global population. As healthcare systems worldwide face increasing surgical volumes and demographic challenges, the demand for advanced bleeding control solutions continues to accelerate.

Market Size and Growth Projections

The hemostatic agents market presents a compelling growth story with varying projections from industry analysts. According to Meticulous Research, the market is projected to reach USD 5.32 billion by 2032, growing at a CAGR of 6.9% during the forecast period. However, alternative industry analyses suggest even more robust growth, with some reports valuing the market at approximately USD 8.9 billion in 2024 and projecting it to reach USD 12.3 billion by 2033. The most optimistic forecasts indicate growth from USD 8.03 billion in 2024 to USD 15.77 billion by 2032, representing a CAGR of 8.8%.

Technological Revolution in Hemostasis

The industry is witnessing a paradigm shift toward bioengineered and synthetic hemostatic agents. Companies like Medcura have developed innovative solutions using patented biopolymer technologies, with their LifeGel™ Absorbable Hemostatic Gel receiving recognition as a 2024/2025 Best Technology in Spine Award. These bioengineered agents offer enhanced biocompatibility, controlled degradation rates, and improved efficacy compared to traditional mechanical methods.

The integration of biomimetic principles has led to materials that closely replicate natural clotting mechanisms. Advanced hemostatic agents, including fibrin sealants and collagen-based sponges, are bioengineered to mimic the body's natural clotting processes, proving valuable in complex surgeries where conventional methods may fall short.

Artificial intelligence and real-time monitoring systems represent the next frontier in hemostatic technology. These systems enable surgeons to make data-driven decisions during procedures, optimizing the selection and application of hemostatic agents based on individual patient characteristics and surgical conditions.

Regulatory Landscape Evolution

The regulatory environment has evolved significantly, with the FDA implementing more nuanced approaches to device classification and approval. The agency has considered loosening premarket expectations for certain absorbable collagen-based hemostatic agents marketed by companies like Integra LifeSciences and Johnson & Johnson's Ethicon.

A notable development is the FDA's proposal to reclassify certain absorbable hemostatic devices from Class III to Class II, potentially streamlining the approval process while maintaining appropriate safety standards. This regulatory evolution encourages greater investment in research and development while balancing innovation with patient safety.

Market Leadership and Competition

The hemostatic agents market is consolidated, with the top 5-6 players accounting for 40-50% of market share in 2024. Key industry leaders include Baxter International Inc., Pfizer Inc., B. Braun Melsungen AG, C. R. Bard Inc., Integra LifeSciences, Medtronic plc, CSL Behring, and Ethicon Inc. (Johnson & Johnson subsidiary).

These major players possess substantial advantages including extensive R&D budgets, established healthcare provider relationships, and comprehensive distribution networks. Their acquisition strategies significantly impact market dynamics, with industry leaders rapidly expanding portfolios by acquiring innovative startups and specialized companies.

Market Segmentation and Applications

Based on application analysis, the surgery segment is expected to account for the largest market share in 2025, driven by recurrent use of hemostatic agents in orthopedic, general, gynecological, and cardiovascular surgeries. The increasing number of accidents and traumatic injuries requiring surgical treatment further supports this segment's growth.

The hospitals and clinics segment dominates the end-user market, attributed to rising patient visits for surgical procedures, increasing surgery volumes, and favorable reimbursement policies. The willingness of hospitals to invest in advanced hemostats reflects the growing recognition of their clinical and economic benefits.

Key Growth Drivers

Multiple factors are propelling market expansion. The increasing prevalence of chronic diseases such as cancer, cardiovascular, orthopedic, and neurological conditions leads to higher surgical procedure volumes. Road traffic crashes, among the leading causes of death globally, represent another significant driver, with approximately 20,653 people killed in road accidents in the EU, representing a 3.7% increase compared to 2021.

The rise in minimally invasive surgical procedures creates substantial demand for sophisticated hemostatic solutions. According to the American Society of Plastic Surgeons, 682,932 non-invasive fat reduction surgeries and 408,970 non-invasive skin tightening surgeries were conducted in the U.S. in 2022, highlighting the growing preference for these procedures.

Emerging Trends and Innovation

Two major trends are shaping the market: biopolymer-based hemostats and dual-action hemostatic technology. Biopolymer-based hemostats are gaining popularity due to their biodegradable, biocompatible, and bioactive properties. These materials come in various forms including particles, powder, sponges, sheets, foams, films, and hydrogels.

Dual-action hemostatic technology represents a significant advancement, effectively controlling bleeding through comprehensive approaches. This technology achieves hemostasis in deep and complex wounds while providing sealing capabilities that offer suture support in vascular surgery.

Market Challenges and Future Outlook

Despite positive growth projections, the market faces challenges including allergic reactions from hemostatic materials and high manufacturing costs that limit adoption in cost-sensitive markets. However, opportunities exist in the increasing use of advanced hemostats, advancements in dental hemostatic agents, and growing demand for preloaded applicators and ready-to-use products.

The future of the hemostatic agents market promises continued innovation, expanding applications, and sustained growth driven by the fundamental need for effective bleeding control in medical procedures. Success will require stakeholders to navigate complex regulatory landscapes, understand diverse regional preferences, and leverage technological capabilities effectively while balancing innovation with safety and cost-effectiveness.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5833

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

Sustainable Aviation Fuel Market Size, Share, Key Growth Drivers, Trends, Challenges and Competitive Landscape

"Executive Summary Sustainable Aviation Fuel Market :

CAGR Value : Data Bridge Market Research analyses that the sustainable aviation fuel market is expected to reach the value of EURO 11,675.53 million by 2029, at a CAGR of 47.9% during the forecast period.

The top notch Sustainable Aviation Fuel Market report additionally encompasses predictions utilizing a practical arrangement of uncertainties and techniques. With this market report study, key opportunities in the market and influencing factors are provided which is useful to take the business to the highest level. By including detailed statistics and market research insights this business report is generated, which results in high growth and thriving sustainability in the market for the businesses. An expert team analyses and forecasts market data using well established market statistical and coherent models to make Sustainable Aviation Fuel Market report outstanding.

The scope of Sustainable Aviation Fuel Market report extends from market scenarios to comparative pricing between major players, cost and profit of the specified market regions. When globalization is rising day by day, many businesses call for global market research for actionable market insights and to support decision making. The identity of respondents is also kept undisclosed and no promotional approach is made to them while analysing the data. Market drivers and market restraints mentioned in wide ranging Sustainable Aviation Fuel Market report help businesses gain an idea about the production strategy. The industry analysis report speaks about the manufacturing process, type and applications.

Discover the latest trends, growth opportunities, and strategic insights in our comprehensive Sustainable Aviation Fuel Market report. Download Full Report: https://www.databridgemarketresearch.com/reports/global-sustainable-aviation-fuel-market

Sustainable Aviation Fuel Market Overview

**Segments:**

- **Fuel Type:** The global sustainable aviation fuel market is segmented by fuel type into biofuel, hydrogen fuel, synthetic fuel, and others. Biofuels are expected to witness significant growth owing to their renewable nature and lower carbon emissions compared to traditional aviation fuels. The increasing focus on reducing carbon footprint in the aviation industry is driving the demand for biofuels as an alternative, sustainable solution.

- **Blending Capacity:** Based on blending capacity, the market is segmented into low blend, full blend, and others. Full blend sustainable aviation fuels are expected to gain traction as they offer a higher proportion of renewable fuel content, thereby maximizing environmental benefits. The stringent regulations promoting the use of full blend sustainable aviation fuels are propelling market growth in this segment.

- **Application:** In terms of application, the market is segmented into commercial aviation, military aviation, and general aviation. The commercial aviation segment dominates the market due to the high volume of fuel consumption by commercial airlines. The increasing initiatives by airlines to reduce carbon emissions and achieve sustainability targets are driving the adoption of sustainable aviation fuels in the commercial aviation sector.

**Market Players:**

- **Neste:** Neste is a key player in the global sustainable aviation fuel market, offering renewable aviation fuel solutions to reduce greenhouse gas emissions. The company's sustainable aviation fuels are derived from renewable feedstocks, contributing to a more environmentally friendly aviation industry.

- **Gevo:** Gevo is another prominent player in the market, specializing in the production of sustainable aviation fuels using renewable resources such as corn and sugarcane. The company's focus on developing low-carbon alternatives to traditional jet fuels is driving its growth in the sustainable aviation fuel market.

- **TotalEnergies:** TotalEnergies is actively involved in the sustainable aviation fuel market, providing advanced biofuels for aviation applications. The company's commitment to sustainability and innovation has positioned it as a leading supplier of sustainable aviation fuels in the global market.

- **SkyNRG:** SkyNRG is a key player in the market, offering sustainable aviation fuels sourced from various feedstocks such as cooking oil and waste materials. The company's partnerships with airlines and aviation stakeholders have strengthened its position in the sustainable aviation fuel market.

The global sustainable aviation fuel market is witnessing significant growth opportunities driven by the increasing focus on reducing carbon emissions in the aviation sector. Market players are investing in research and development to enhance the production and quality of sustainable aviation fuels, thereby contributing to a greener future for the aviation industry.

The global sustainable aviation fuel market is poised for remarkable growth due to the escalating demand for eco-friendly aviation solutions. One emerging trend is the increasing focus on innovative fuel types beyond biofuel, hydrogen fuel, and synthetic fuel. For instance, sustainable aviation fuels derived from algae or waste materials present new opportunities for reducing carbon emissions and enhancing sustainability in the aviation sector. These alternative fuel sources have the potential to revolutionize the industry by offering unique benefits such as reduced waste disposal and lower production costs. Market players exploring these novel fuel types could gain a competitive edge and drive further market expansion.

Moreover, a key factor influencing the market dynamics is the evolving regulatory landscape governing sustainable aviation fuel blending capacity. Regulatory authorities worldwide are implementing stringent policies to limit carbon emissions from aviation activities, thereby encouraging the adoption of higher blend sustainable aviation fuels. Market players focusing on developing full blend solutions are likely to experience a surge in demand as airlines and aircraft operators seek to comply with environmental regulations and achieve sustainability targets. By investing in advanced blending technologies and production processes, companies can position themselves as preferred suppliers of high-quality sustainable aviation fuels, thereby fostering market growth and differentiation.

Furthermore, the application segment of the sustainable aviation fuel market is witnessing notable developments driven by the increasing uptake of eco-friendly fuels across different aviation sectors. While commercial aviation remains a dominant consumer of sustainable aviation fuels, there is a growing interest in expanding the use of these fuels in military and general aviation applications. Military organizations are recognizing the strategic importance of reducing carbon footprint and enhancing operational efficiency through sustainable fuel adoption. General aviation operators, on the other hand, are exploring new opportunities to integrate sustainable aviation fuels into their operations, thereby contributing to a more environmentally conscious industry landscape.

In conclusion, the global sustainable aviation fuel market presents a wealth of opportunities for market players to innovate, collaborate, and drive sustainable growth. By exploring new fuel types, embracing stringent blending capacity regulations, and expanding into diverse application segments, companies can position themselves as key contributors to a greener aviation industry. With ongoing investments in research and development, partnerships with industry stakeholders, and a commitment to sustainability, the market is primed for continued expansion and transformation towards a more sustainable future.The global sustainable aviation fuel market is undergoing significant transformation driven by the increasing emphasis on reducing carbon emissions and achieving sustainability goals in the aviation industry. One of the key trends shaping the market is the exploration of innovative fuel types beyond traditional options such as biofuel, hydrogen fuel, and synthetic fuel. Companies are now venturing into alternative sources like algae-based fuels or waste-derived fuels, offering unique advantages such as enhanced sustainability, reduced waste disposal, and potentially lower production costs. This trend indicates a shift towards more diverse and environmentally friendly fuel solutions, which could revolutionize the aviation sector and create new market opportunities for players in the sustainable aviation fuel industry.

Moreover, the regulatory landscape governing sustainable aviation fuel blending capacity is evolving rapidly, with stringent policies being implemented globally to curb carbon emissions from aviation activities. The focus on higher blend sustainable aviation fuels is increasing, driven by the need for airlines and aircraft operators to comply with environmental regulations and meet sustainability targets. Companies investing in advanced blending technologies and production processes to offer full blend solutions are likely to witness a surge in demand as the industry moves towards more sustainable practices. This regulatory push towards higher blend fuels is expected to drive market growth and differentiation among players, positioning those with superior blending capabilities as preferred suppliers of high-quality sustainable aviation fuels.

Additionally, the application segment of the sustainable aviation fuel market is experiencing notable developments as eco-friendly fuels gain traction across various aviation sectors. While commercial aviation remains a major consumer of sustainable aviation fuels, there is a growing interest in expanding their use in military and general aviation applications. Military organizations are recognizing the strategic importance of reducing carbon footprint and enhancing operational efficiency through sustainable fuel adoption, driving demand in this segment. Similarly, general aviation operators are increasingly looking to integrate sustainable aviation fuels into their operations to align with environmental consciousness trends in the industry. This diversification of applications signifies a broader adoption of sustainable aviation fuels across the aviation sector, presenting opportunities for market players to expand their presence and contribute to a more sustainable industry landscape.

In conclusion, the global sustainable aviation fuel market is poised for significant growth and innovation as companies explore new fuel sources, comply with evolving blending capacity regulations, and expand into diverse application segments. By investing in research and development, forming strategic partnerships, and demonstrating a strong commitment to sustainability, market players can position themselves for success in a market that is moving towards a greener and more environmentally conscious future. The transformative trends and developments in the sustainable aviation fuel market present various avenues for companies to differentiate themselves, drive growth, and contribute to the overall sustainability goals of the aviation industry.

The Sustainable Aviation Fuel Market is highly fragmented, featuring intense competition among both global and regional players striving for market share. To explore how global trends are shaping the future of the top 10 companies in the keyword market.

Learn More Now: https://www.databridgemarketresearch.com/reports/global-sustainable-aviation-fuel-market/companies

DBMR Nucleus: Powering Insights, Strategy & Growth

DBMR Nucleus is a dynamic, AI-powered business intelligence platform designed to revolutionize the way organizations access and interpret market data. Developed by Data Bridge Market Research, Nucleus integrates cutting-edge analytics with intuitive dashboards to deliver real-time insights across industries. From tracking market trends and competitive landscapes to uncovering growth opportunities, the platform enables strategic decision-making backed by data-driven evidence. Whether you're a startup or an enterprise, DBMR Nucleus equips you with the tools to stay ahead of the curve and fuel long-term success.

Key Influence of this Market:

Comprehensive assessment of all opportunities and risk in this Sustainable Aviation Fuel Market

This Market recent innovations and major events

Detailed study of business strategies for growth of the this Market-leading players

Conclusive study about the growth plot of the Sustainable Aviation Fuel Market for forthcoming years

In-depth understanding of this Sustainable Aviation Fuel Market particular drivers, constraints and major micro markets

Favourable impression inside vital technological and market latest trends striking this Market

To provide historical and forecast revenue of the market segments and sub-segments with respect to four main geographies and their countries- North America, Europe, Asia, and Rest of the World (ROW)

To provide country level analysis of the market with respect to the current market size and future prospective

Browse More Reports:

Middle East and Africa Digital Farming Software Market Global Specialty Lancets Market Asia-Pacific Medical Imaging (3D and 4D) Software Market Global Flat Panel Detector (FPD)-Based X-Ray for Cone Beam Computed Tomography (CBCT) Market Global Soy Protein Market Asia-Pacific Botanical Extract Market Europe Laminated Busbar Market Global Moisture Analyser Market Asia-Pacific Indium Market Global Feather Meal Market Global Protein Hydrolysates Market Global X Linked Hypophosphatemia (XLH) Treatment Market Global Musculoskeletal Disorders Drugs Market Global Spinal Stenosis Treatment Market Asia-Pacific Flotation Reagents Market France Artificial Turf Market Global Cardiovascular Genetic Testing Market Global Brass Solenoid Valves Market North America Medical Imaging (3D and 4D) Software Market Global Flexible Insulation Market Global Drug Eluting Stents (DES) Market Middle East and Africa Ostomy Devices Market Global Specialty Yeast Market Global Automotive Blind Spot Detection System Market Global Textile Fabric Market Global Chemical Market Global 3D Printed Jewelry Market Global Jamestown Canyon Virus Treatment Market Europe Botanical Extract Market Global Cloud Applications Market Global Plant Based Protein Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us: Data Bridge Market Research US: +1 614 591 3140 UK: +44 845 154 9652 APAC : +653 1251 975 Email:- [email protected]

"

0 notes

Text

Lanolin Industry Insights: Market Size, Share & Growth Analysis

United States of America – The Insight Partners is delighted to release its newest in-depth report entitled "LANOLIN Market: An In-depth Analysis of the Global Scenario and Future Forecast Period". The report offers a complete overview of the global market, examining current trends, key developments, and future growth prospects during the forecast period.

Overview

The LANOLIN industry is being radically changed by a mix of technology advancement, changing consumer preferences, and increased regulatory controls. is a natural wax produced by wool-producing animals that finds extensive application in cosmetics, pharmaceuticals, and industries. The growing demand for bio-based products and skin-friendly products is fueling the increasing use of across several sectors.

Key Findings and Insights

Market Size and Growth

Historical Data & Forecasts: Lanolin Market to grow at a CAGR of 6% during the forecast period.

Major Drivers of Growth:

Growing demand from personal care and cosmetics owing to natural emollient capabilities.

Growing application in pharmaceutical formulations for topical applications.

Increasing uses in industrial lubricants and coatings.

Transition towards eco-friendly and biodegradable offerings.

Get Sample Report: https://www.theinsightpartners.com/sample/TIPRE00008699

Market Segmentation

By Product Type

Alcohol

Oil

Wax

Cholesterol and Others

By End Use

Personal Care and Cosmetics

Pharmaceuticals

Industrial Products and Others

Identifying Emerging Trends

Technological Developments

Ultra-purification for use in pharmaceutical-grade applications.

Application in nanotechnology-based drug delivery systems.

Refinements in extraction and refining techniques to improve yield while minimizing environmental footprint.

Consumer Lifestyle Changes

Transition from harsh chemical-based personal care products to organic and cruelty-free.

Greater consciousness about skin health, along with natural ingredients, particularly in baby care and dermatology products.

Consumers seeking multi-functional skincare that delivers hydration, healing, and protection, where takes the central stage.

Regulatory Developments

Stricter EU REACH guidelines on labeling of ingredients and traceability.

Increased focus on animal welfare compliance and sustainable sourcing certifications.

FDA announcements on GRAS (Generally Recognized As Safe) status in pharmaceutical use.

Opportunities for Growth

Emerging Markets Expansion: Increased middle-class incomes and awareness in Asia-Pacific and Latin America provide lucrative market opportunity.

R&D Expenditure: Potential to innovate in -based formulations blended with other bio-actives.

Strategic Partnerships: Collaborations between manufacturers and personal care industry majors for tailor-made solutions.

Sustainability Strategies: Branding as a sustainable replacement for synthetic emollients following ESG principles.

Conclusion

The LANOLIN Market: Global Industry Trends, Share, Size, Growth, Opportunity, and Forecast Period report provides a valuable source of information for companies seeking to enter or grow in the industry. Providing in-depth analysis of market trends, dynamics, and competition tactics, the report empowers stakeholders with necessary decision-making tools and long-term success.

About The Insight Partners

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

0 notes

Text

Synthetic Data Generation Market Trend, Segmentation and Growth Factors

According to a research report "Synthetic Data Generation Market by Offering (Solution/Platform and Services), Data Type (Tabular, Text, Image, and Video), Application (AI/ML Training & Development, Test Data Management), Vertical and Region - Global Forecast to 2028" published by MarketsandMarkets, the global synthetic data generation messaging market size to grow from USD 0.3 billion in 2023 to USD 2.1 billion by 2028, at a Compound Annual Growth Rate (CAGR) of 45.7% during the forecast period.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=176419553 The global synthetic data generation market has various applications such as data democratization, AI/ML training and development, data anonymization, test data management, enterprise data sharing, data analytics and visualization, data monetization, and others. The major end-users of the Synthetic Data Generation market include BFSI, Healthcare & Life sciences, Retail & E-commerce, Automotive & Transportation, Government & Defense, IT and ITeS, Energy and Utilities, Manufacturing, and Other Verticals.

Stricter regulations, and limitations on the use of real-world data due to increasing concerns about data privacy and security have created a demand for synthetic data as a viable alternative. Synthetic data generation enables organizations to generate and utilize data without compromising sensitive information, addressing real-world data privacy and security challenges. Businesses are increasingly relying on data-driven decision-making to gain a competitive edge.

Among vertical, the BFSI segment is expected to dominate the market during the forecast period

Based on vertical, the BFSI segment of the synthetic data generation market is projected to hold a larger market size during the forecast period. The adoption of synthetic data generation drives the BFSI (Banking, Financial Services, and Insurance) vertical due to increasing concerns about data privacy and compliance regulations. Synthetic data provides a solution for generating realistic datasets without compromising sensitive information, allowing organizations in the BFSI sector to meet regulatory requirements. It enables improved risk management, fraud detection, model development, and customer analytics, facilitating more accurate predictions.

By data type, image and video segment to record the highest market share during the forecast period

Image and video data represent visual information in the form of images and videos. Synthetic data generation for image and video data involves creating artificial visual content that simulates real-world scenarios. This process is driven by the need for training computer vision models, object detection, image recognition, and video analysis. Synthetic image and video data enable organizations to generate diverse datasets that cover a wide range of scenarios, lighting conditions, and object variations. It supports the development and validation of algorithms for autonomous vehicles, surveillance systems, medical imaging, and virtual reality applications.

Asia Pacific to record the highest growth during the forecast period.

The synthetic data generation market in the Asia Pacific region is experiencing significant growth driven by rapid digital transformation, increasing data privacy regulations, growing adoption of AI and ML technologies, rising cybersecurity concerns, and a thriving startup ecosystem. Organizations in the region are leveraging synthetic data generation to address data-driven challenges, comply with regulations, enhance AI and ML model performance, strengthen cybersecurity measures, and drive innovation. With the region's focus on digitalization and the emerging need for data-driven solutions, Asia Pacific's synthetic data generation market is poised for continued expansion and opportunities.

Get More Info - https://www.marketsandmarkets.com/Market-Reports/synthetic-data-generation-market-176419553.html

Market Players

Major vendors in the synthetic data generation market include Microsoft (US), Google (US), IBM (US), AWS (US), NVIDIA (US), OpenAI (US), Informatica (US), Broadcom (US), Sogeti (France), Mphasis (India), Databricks (US), MOSTLY AI (Austria), Tonic (US), MDClone (Israel) TCS (India), Hazy (UK), Synthesia (UK), Synthesized (UK), Facteus (US), Anyverse (Spain), Neurolabs (Scotland), Rendered.ai (US), Gretel (US), OneView (Israel), GenRocket (US), YData (US), CVEDIA (UK), Syntheticus (Switzerland), AnyLogic (US), Bifrost AI (US), Anonos (US).

#Synthetic Data Generation Market#Synthetic Data Generation Market size#Synthetic Data Generation Market share#Synthetic Data Generation Market trends#Synthetic Data Generation Market demand#Synthetic Data Generation Market Overview#Synthetic Data Generation Market Trends#Synthetic Data Generation Market Demand

0 notes

Text

Acrylic Emulsion Market Size, Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Acrylic Emulsion Market was valued at USD 12.3 billion in 2024 and is expected to experience steady growth at a CAGR of 7.7% between 2025 and 2034. Acrylic emulsions, also known as FKM, are synthetic elastomers prized for their remarkable resistance to heat, chemicals, and a range of fluids. These characteristics make acrylic emulsions indispensable in industries that require durable sealing solutions, such as automotive, aerospace, oil and gas, and chemical processing. As industries continue to innovate and demand materials with superior performance, the acrylic emulsion market is well-positioned for significant expansion. The growing need for eco-friendly and high-performance materials further strengthens the demand for acrylic emulsions, especially in the construction, automotive, and industrial sectors.

Get sample copy of this research report @ https://www.gminsights.com/request-sample/detail/7673

The polymer and copolymer emulsion segment generated USD 6.4 billion in 2024. This segment is particularly notable for its additional polymers and copolymers, which enhance specific properties suited for various industrial applications. These emulsions are widely used in adhesives, sealants, and specialized coatings, offering both versatility and efficiency in meeting diverse market demands. As industries adopt increasingly advanced manufacturing techniques, the demand for these emulsions is expected to rise steadily, ensuring their continued prominence in the marketplace.

In 2024, the paints and coatings segment dominated the market with a significant 54.9% share and is forecast to grow substantially by 2034. Acrylic emulsions are especially favored for premium paints and coatings due to their superior adhesion, weathering resistance, and durability. These essential properties contribute to the production of long-lasting, aesthetically pleasing finishes, driving demand across various industries, including automotive, architecture, and consumer goods. The need for high-quality finishes that stand up to environmental challenges ensures that this segment will continue to see substantial growth in the coming years.

Browse complete summary of this research report @ https://www.gminsights.com/industry-analysis/acrylic-emulsion-market

China acrylic emulsion market reached USD 3.3 billion in 2024 and is projected to grow at an impressive rate between 2025 and 2034. The rapid expansion of the construction industry in China and India significantly drives this demand, as acrylic emulsions are extensively used in paints, coatings, and construction material additives. Urbanization, along with the growth of large-scale infrastructure projects, is playing a key role in increasing the market's size. Furthermore, the thriving automotive sector in countries like Japan and South Korea continues to contribute to the consistent demand for acrylic emulsions. As these regions remain at the forefront of industrial growth, the demand for acrylic emulsions is expected to keep rising, contributing to the global market's expansion.

About Global Market Insights

Global Market Insights Inc., headquartered in Delaware, U.S., is a global market research and consulting service provider, offering syndicated and custom research reports along with growth consulting services. Our business intelligence and industry research reports offer clients with penetrative insights and actionable market data specially designed and presented to aid strategic decision making. These exhaustive reports are designed via a proprietary research methodology and are available for key industries such as chemicals, advanced materials, technology, renewable energy, and biotechnology.

Contact Us:

Aashit Tiwari

Corporate Sales, USA

Global Market Insights Inc.

Toll Free: +1-888-689-0688

USA: +1-302-846-7766

Europe: +44-742-759-8484

APAC: +65-3129-7718

Email: [email protected]

0 notes

Text

Global Binocular Hand-held Slit Lamp Market Forecast (2025–2031): Growth, Trends & Strategic Insights

"

The global Binocular Hand-held Slit Lamp market is expected to experience consistent growth between 2025 and 2031. This in-depth report offers expert insights into emerging trends, leading companies, regional performance, and future growth opportunities. Its a valuable resource for businesses, investors, and stakeholders seeking data-driven decisions.

Access the Full Report Now https://marketsglob.com/report/binocular-hand-held-slit-lamp-market/1655/

What’s Inside:

Latest advancements in Binocular Hand-held Slit Lamp product development

Impact of synthetic sourcing on production workflows

Innovations in cost-efficient manufacturing and new use cases

Leading Companies Profiled:

Haag-Streit

Shin Nippon (Rexxam Co.Ltd)

Kowa

Keeler (Halma plc)

Reichert (AMETEK)

66 Vision Tech

Kang Hua

Suzhou KangJie Medical

Kingfish Optical Instrument

Bolan Optical Electric

Strong focus on R&D and next-generation Binocular Hand-held Slit Lamp products

Shift toward synthetic sourcing techniques

Real-world examples from top players using cost-effective strategies

The report showcases top-performing companies in the Binocular Hand-held Slit Lamp industry, examining their strategic initiatives, innovations, and future roadmaps. This helps you understand the competitive landscape and plan ahead effectively.

Product Types Covered:

Indirect Sales

Direct Sales

Applications Covered:

Hospital

Community Health Service Organizations

Others

Sales Channels Covered:

Direct Channel

Distribution Channel

Regional Analysis:

North America (United States, Canada, Mexico)

Europe (Germany, United Kingdom, France, Italy, Russia, Spain, Benelux, Poland, Austria, Portugal, Rest of Europe)

Asia-Pacific (China, Japan, Korea, India, Southeast Asia, Australia, Taiwan, Rest of Asia Pacific)

South America (Brazil, Argentina, Colombia, Chile, Peru, Venezuela, Rest of South America)

Middle East & Africa (UAE, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of Middle East & Africa)

Key Takeaways:

Market size, share, and CAGR forecast to 2031

Strategic insights into emerging opportunities

Demand outlook for standard vs. premium products

Company profiles, pricing trends, and revenue projections

Insights into licensing, co-development, and strategic partnerships

This detailed report offers a full picture of where the Binocular Hand-held Slit Lamp market stands today and where its headed. Whether you are a manufacturer, investor, or strategist, this report can help you identify key opportunities and make informed business decisions.

" External Turning Tools Market External Urinary Catheters Market Extra Coarse Salt Market Extra High Voltage Devices Market Extra Thick Board Market Extra Thick Steel Plate Market Extra Virgin Avocado Oil Market Extra Virgin Camellia Oil Market Extra Virgin Sesame Oil Market Extracorporeal CO2 Removal Market Extracorporeal Lithotripsy Market Extracted Canola Oil Market Extraction Arms Market

0 notes

Text

Aptamer Based Quartz Crystal Microbalance Biosensor Market: Dynamics, Challenges, and Drivers 2025–2032

Aptamer Based Quartz Crystal Microbalance Biosensor Market: Dynamics, Challenges, and Drivers 2025–2032

MARKET INSIGHTS

The global Aptamer Based Quartz Crystal Microbalance Biosensor Market size was valued at US$ 45.8 million in 2024 and is projected to reach US$ 87.9 million by 2032, at a CAGR of 8.5% during the forecast period 2025-2032. The U.S. market accounted for approximately 35% of global revenue in 2024, while China is expected to witness the fastest growth with a projected CAGR of 9.2% through 2032.

Aptamer-based QCM biosensors are high-precision analytical devices that utilize synthetic oligonucleotides (aptamers) as biorecognition elements on quartz crystal surfaces. These sensors detect mass changes at the nanogram level when target molecules bind to immobilized aptamers, enabling real-time, label-free analysis of biomolecular interactions. Key applications include drug discovery, environmental monitoring, and clinical diagnostics.

The market is driven by increasing demand for rapid, sensitive biosensing technologies in pharmaceutical R&D and diagnostics. However, challenges such as aptamer stability and sensor regeneration persist. Major players like Biolin Scientific and INFICON are investing in next-generation QCM platforms, with the metal biosensors segment projected to reach USD 85 million by 2032. Recent advancements include multiplexed QCM arrays for high-throughput screening, which are gaining traction in academic and industrial laboratories.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption in Pharmaceutical and Biotechnology Research to Propel Market Expansion

The pharmaceutical and biotechnology sectors are increasingly leveraging aptamer-based quartz crystal microbalance (QCM) biosensors due to their high sensitivity and real-time monitoring capabilities. These biosensors enable label-free detection of molecular interactions, making them ideal for drug discovery applications. The global pharmaceutical R&D expenditure has consistently grown, crossing the mark of $200 billion annually, creating substantial demand for advanced analytical tools like QCM biosensors. Moreover, the ability to precisely measure binding kinetics and affinity between drug candidates and targets significantly reduces development timelines, which is crucial in today's competitive landscape.

Rising Prevalence of Chronic Diseases to Accelerate Diagnostic Applications

The increasing global burden of chronic diseases has created an urgent need for rapid, accurate diagnostic solutions. Aptamer-based QCM biosensors are gaining traction in point-of-care diagnostics due to their specificity in detecting disease biomarkers. With cardiovascular diseases and cancer accounting for over 50% of global mortality, healthcare providers are actively seeking innovative diagnostic technologies. These biosensors offer advantages over traditional ELISA tests, including faster turnaround times and the ability to detect low-abundance biomarkers without complex sample preparation. This positions them as transformative tools in early disease detection and monitoring.

The integration of artificial intelligence with QCM biosensor data analysis is further enhancing their diagnostic potential. Machine learning algorithms can now process complex frequency shift patterns to identify disease signatures with greater accuracy. Recent technological advancements have enabled multiplexed detection, allowing simultaneous analysis of multiple biomarkers, which is revolutionizing personalized medicine approaches.

MARKET RESTRAINTS

High Capital Investment and Operational Complexity to Limit Market Penetration

While aptamer-based QCM biosensors offer significant advantages, their adoption is hindered by substantial infrastructure requirements. The initial setup costs for these systems can exceed $50,000, making them prohibitive for smaller research facilities and diagnostic centers. Additionally, the need for specialized cleanroom environments and precise temperature control systems adds to the operational expenses. Many potential users opt for conventional techniques due to these financial barriers, despite the superior performance offered by QCM technology.

The complexity of aptamer selection and immobilization presents another significant challenge. Developing specific aptamers for target molecules through systematic evolution of ligands by exponential enrichment (SELEX) can take several months and requires specialized expertise. Furthermore, maintaining aptamer stability during sensor fabrication and storage remains technically demanding. These factors collectively slow down widespread commercialization and limit market growth potential.

MARKET CHALLENGES

Interference from Non-Specific Binding to Complicate Data Interpretation

Aptamer-based QCM biosensors face significant technical challenges related to non-specific molecular interactions. The quartz crystal surface can accumulate non-target molecules, leading to false-positive signals and reduced measurement accuracy. This interference becomes particularly problematic in complex biological samples like blood or serum, where thousands of potentially interfering substances coexist. Current surface modification techniques can only partially address this issue, requiring careful optimization for each specific application.

Sample Matrix Effects The composition of biological samples varies significantly between individuals and disease states, creating matrix effects that can alter sensor performance. Factors like pH variations, ionic strength differences, and presence of proteins can all impact the binding kinetics measured by QCM biosensors. Developing universal protocols that account for these variations remains an ongoing challenge for researchers and manufacturers alike.

MARKET OPPORTUNITIES

Expansion into Food Safety and Environmental Monitoring to Open New Revenue Streams

The application of aptamer-based QCM biosensors is expanding beyond healthcare into food safety monitoring and environmental analysis. Increasing regulatory requirements for contaminant detection in food products have created a promising market opportunity. These biosensors can rapidly detect pathogens like Salmonella and E. coli, as well as chemical contaminants such as pesticides and mycotoxins, with detection limits meeting stringent food safety standards. The global food safety testing market, valued at over $20 billion, represents a significant growth avenue for QCM biosensor manufacturers.

Environmental monitoring applications are similarly promising, particularly for real-time detection of water pollutants. Governments worldwide are implementing stricter regulations on industrial effluent monitoring, driving demand for advanced sensing technologies. The ability of QCM biosensors to operate continuously in field conditions makes them ideal for such applications, provided durability challenges can be adequately addressed.

The development of portable, battery-operated QCM systems is particularly exciting for field applications. Recent advancements in microfluidics integration have enabled sample processing directly on the sensor chip, eliminating the need for complex laboratory equipment. This innovation is creating opportunities in resource-limited settings where traditional analytical instruments are impractical.

APTAMER BASED QUARTZ CRYSTAL MICROBALANCE BIOSENSOR MARKET TRENDS

Growing Demand for Label-Free Biosensing Technologies Drives Market Expansion

The global aptamer-based quartz crystal microbalance (QCM) biosensor market is experiencing robust growth, driven by increasing adoption of label-free detection technologies in life sciences research and diagnostics. Valued at millions in 2024, the market is projected to reach significant millions by 2032 at a compound annual growth rate in the mid-single digits. This upward trajectory stems from QCM biosensors' ability to provide real-time, quantitative analysis of molecular interactions without requiring fluorescent or radioactive labels, reducing both costs and experimental complexity.

Other Trends

Increasing Applications in Drug Discovery and Development

Pharmaceutical companies are increasingly incorporating aptamer-based QCM biosensors into their drug discovery pipelines, particularly for kinetic analysis of drug-target interactions and high-throughput screening. The technology's sensitivity to mass changes at the nanogram level enables precise monitoring of binding events between potential drug candidates and their targets. Recent advancements have expanded detection capabilities to smaller molecules, making QCM biosensors applicable to approximately 80% of modern drug discovery programs targeting protein interactions.

Technological Advancements in Aptamer Selection and Immobilization