#Telecom Generator market shape

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. is using 66 technologies for its website.

Text

Telecom Generator Market - Forecast(2024 - 2030)

Telecom Generator Market size is estimated to reach $3.1 billion by 2030, growing at a CAGR of 10.2% during the forecast period 2024–2030. The increasing demand for reliable and uninterrupted power supply for telecom equipment, such as antennas, switches, routers, servers and other network components are propelling the Telecom Generator Market growth.

Additionally, growing adoption of renewable energy sources is creating substantial growth opportunities for the Telecom Generator Market. These factors positively influence the Telecom Generator industry outlook during the forecast period.

COVID-19 / Ukraine Crisis — Impact Analysis:

● The COVID-19 pandemic significantly impacted the telecom generator market. A decline in economic activity led to reduced demand for telecom services, consequently decreasing the demand for telecom generators. Telecom generators are commonly utilized as backup power in telecom infrastructure, so this decline was exacerbated by the pandemic’s disruption of supply chains, which made it challenging for telecom operators to acquire generators. However, the telecom generator market is expected to recover in the long term, as the telecom industry is critical and there is a need for uninterrupted communication services. As the global economy rebounds, there will likely be an increased demand for telecom services, and consequently, a rise in demand for telecom generators as backup power sources.

● The conflict between Russia and Ukraine significantly impacted the telecom generator market, the telecom operators faced a surge in demand for generators, relying on them as backup power sources for telecom towers and infrastructure that had been damaged or disrupted. This increased demand resulted in price increases and shortages in the telecom generator market. Additionally, the Ukraine crisis had a broader impact on the global economy. The crisis caused economic uncertainty worldwide, making it more difficult for telecom operators to secure financing for their projects. As a result, the growth of the telecom generator market slowed down.

Key Takeaways:

● Fastest Growth Asia-Pacific Region

Geographically, in the global Telecom Generator Market share, Asia Pacific is analyzed to grow with the highest CAGR of 11.5% during the forecast period 2024–2030. The demand for mobile data and internet services in the Asia-Pacific region is experiencing a notable upswing, highlighting the need for dependable power supply to sustain telecom towers and base stations. With rapid urbanization, urban areas are witnessing a surge in demand for telecom services, underscoring the crucial role of telecom generators in ensuring uninterrupted power. The substantial investments by regional governments in infrastructure development present new opportunities for the telecom generator market. Moreover, telecom operators are increasingly acknowledging the significance of backup power, contributing to the growing demand for telecom generators.

● Gas to Register the Fastest Growth

In the Telecom Generator Market analysis, the Gas segment is estimated to grow with the highest CAGR during the forecast period. Telecom operators are increasingly focused on eco-friendly power solutions due to heightened environmental awareness. Gas generators are gaining favor over diesel generators for their superior environmental performance and cost-effectiveness. With the wide availability of natural gas as a reliable fuel source, it has become a preferred choice for telecom generators. Additionally, several governments are promoting gas generators as part of emission reduction regulations.

● Standby Load is Leading the Market

According to the Telecom Generator Market forecast, the Standby Load held the largest market share in 2022 owing to the growing the demand for uninterrupted power supply in the telecommunications industry, particularly in the standby load segment. Standby generators play a crucial role in providing backup power during power outages, ensuring the continuity of telecommunications services. The rising usage of mobile devices and data-intensive applications further amplifies the need for standby generators in the telecom sector.

● The Surging Demand for Reliable Telecom Power Supply for Telecom Equipment

Telecom operators and service providers recognize the importance of uninterrupted communication services and actively invest in reliable power solutions like telecom generators. The growing reliance on mobile devices, data-intensive applications and high-speed internet further contributes to the need for uninterrupted power supply. Technological advancements in telecom generators, improving efficiency and reducing emissions, fuel their adoption in the industry is escalating demand for reliable power significantly propels market growth as the telecommunications industry expands and technology advances.

● The Escalating Trend of Renewable Energy Sources Adoption

The market growth of telecom generators is fueled by the rising adoption of renewable energy sources like solar and wind power. Several factors contribute to this trend, including the increasing cost competitiveness of renewable energy, which appeals to telecom operators seeking to reduce operating expenses. Technological advancements such as battery storage and smart grids enhance the reliability of renewable energy, ensuring uninterrupted power supply. Furthermore, the environmentally friendly nature of renewables aligns with the sustainability objectives of telecom operators. As a result, the market for telecom generators utilizing renewable energy sources is anticipated to witness substantial growth in the future.

● High Costs of Generators Hamper the Market Growth

Increasing prices of raw materials like diesel and natural gas used to fuel generators and contribute to their un-affordability for many telecom operators, especially in developing countries. Consequently, operators are compelled to resort to less reliable backup power alternatives such as batteries or solar panels, compromising the network’s reliability and performance. Moreover, the substantial expenditure on generators reduces telecom operators’ profitability and hampers their capacity to invest in infrastructure upgrades or expansion. This cost barrier limits the adoption of vital backup power solutions, impeding market growth in the telecom industry.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Telecom Generator Market. The top 10 companies in this industry are listed below:

Caterpillar Inc. (Cat 3512C Generator Set, Cat 3512C Generator Set)

Kohler Co. (Kohler KDE75S-BT-EU, Kohler KDE75S-BT-US

Cummins Inc. (Cummins QSK60-ME, Cummins QSK95-ME)

Generac Holdings Inc. (Generac PWR-Pro 75S2E, Generac PWR-Pro 100S2E)

Briggs & Stratton Corporation(Briggs & Stratton 20000E Series, Briggs & Stratton 30000E Series)

Yanmar Co., Ltd. (Yanmar G125S-BT, Yanmar G250S-BT)

Doosan Corporation.(Doosan DL250SE-BT, Doosan DL350SE-BT)

Siemens Energy AG (SGen-100A/1000Agenerator series, SGen-2000P generator series)

Wärtsilä Corporation (16V46DF generator, 20V46DF generator)

Mitsubishi Heavy Industries, Ltd. (MU-G Series, MGS Series)

#Telecom Generator#Telecom Generator market#Telecom Generator forecast#Telecom Generator market analysis#Telecom Generator market shape#Telecom Generator market analysis#industry outlook

0 notes

Text

Photonic Integrated Circuit Market 2033: Key Players, Segments, and Forecasts

Market Overview

The Global Photonic Integrated Circuit Market Size is Expected to Grow from USD 11.85 Billion in 2023 to USD 94.05 Billion by 2033, at a CAGR of 23.02% during the forecast period 2023-2033.

Photonic Integrated Circuit (PIC) Market is witnessing transformative momentum, fueled by the global push towards faster, energy-efficient, and miniaturized optical components. As data demands soar and photonics become essential in telecom, AI, quantum computing, and biosensing, PICs are emerging as the nerve center of next-generation optical solutions. These chips integrate multiple photonic functions into a single chip, drastically improving performance and cost-efficiency.

Market Growth and Key Drivers

The market is set to grow at an exceptional pace, driven by:

Data Center Expansion: Surging internet traffic and cloud services are fueling PIC-based optical transceivers.

5G & Beyond: Demand for faster, low-latency communication is driving adoption in telecom infrastructure.

Quantum & AI Computing: PICs are critical to the advancement of light-based quantum circuits and high-speed AI processors.

Medical Diagnostics: Miniaturized photonic sensors are revolutionizing biomedical imaging and lab-on-chip diagnostics.

Defense & Aerospace: PICs provide enhanced signal processing and secure communication capabilities.

Get More Information: Click Here

Market Challenges

Despite strong potential, the PIC market faces several hurdles:

Fabrication Complexity: Advanced PICs demand high-precision manufacturing and integration techniques.

Standardization Issues: Lack of global standards slows down mass deployment and interoperability.

High Initial Investment: R&D and setup costs can be prohibitive, especially for SMEs and startups.

Thermal Management: Maintaining performance while managing heat in densely packed circuits remains a challenge.

Market Segmentation

By Component: Lasers, Modulators, Detectors, Multiplexers/Demultiplexers, Others

By Integration Type: Monolithic Integration, Hybrid Integration

By Material: Indium Phosphide (InP), Silicon-on-Insulator (SOI), Others

By Application: Optical Communication, Sensing, Biomedical, Quantum Computing, RF Signal Processing

By End User: Telecom, Healthcare, Data Centers, Aerospace & Defense, Academia

Regional Analysis

North America: Leading in R&D, startups, and federal defense contracts.

Europe: Home to silicon photonics innovation and academic-industrial collaboration.

Asia-Pacific: Witnessing rapid adoption due to telecom expansion and smart manufacturing in China, South Korea, and Japan.

Middle East & Africa: Emerging opportunities in smart city and surveillance tech.

Latin America: Gradual growth driven by increasing telecom and IoT penetration.

Competitive Landscape

Key players shaping the market include:

Intel Corporation

Cisco Systems

Infinera Corporation

NeoPhotonics

IBM

II-VI Incorporated

Hewlett Packard Enterprise

Broadcom Inc.

GlobalFoundries

PhotonDelta (Europe-based accelerator)

Positioning and Strategies

Leading companies are focusing on:

Vertical Integration: Owning every stage from design to packaging for cost control and performance.

Strategic Partnerships: Collaborations with telecom operators, hyperscalers, and research institutes.

Application-Specific Customization: Tailoring PICs for specific end-user applications (e.g., medical devices or LiDAR systems).

Global Fab Alliances: Leveraging cross-continental manufacturing capabilities for scale and speed.

Buy This Report Now: Click Here

Recent Developments

Intel unveiled a next-gen 200G PIC-based optical transceiver targeting AI data centers.

Infinera's XR optics platform is redefining network scaling with dynamic bandwidth allocation.

European Photonics Alliance launched an initiative to accelerate PIC adoption in SMEs.

Startups like Ayar Labs and Lightmatter raised significant VC funding to develop photonics-based computing solutions.

Trends and Innovation

Co-Packaged Optics (CPO): Integrating optics with switching ASICs for power and latency optimization.

Silicon Photonics: Scalable, CMOS-compatible manufacturing opening the doors to mass production.

Quantum Photonic Chips: Rapid R&D in quantum-safe communications and computing.

Edge Photonics: Enabling localized, high-speed data processing for Industry 4.0 and IoT applications.

AI-Powered Design: ML models used for photonic circuit simulation and optimization.

Related URLS:

https://www.sphericalinsights.com/our-insights/antimicrobial-medical-textiles-market https://www.sphericalinsights.com/our-insights/self-contained-breathing-apparatus-market https://www.sphericalinsights.com/our-insights/ozone-generator-market-size https://www.sphericalinsights.com/our-insights/agro-textile-market

Opportunities

Telecom & Cloud Providers: Demand for next-gen, low-latency networks creates significant opportunities.

Healthcare Startups: PICs enable affordable, portable diagnostics, expanding precision medicine.

Defense & Security: High-performance signal processing and surveillance enhancements.

Automotive LiDAR: Integration of PICs into autonomous vehicle sensor suites.

Future Outlook

The Photonic Integrated Circuit Market is moving from research-focused innovation to mainstream commercial adoption. By 2030, PICs are expected to power a wide array of industries—fundamentally redefining computing, communication, and sensing systems. Standardization, improved design tools, and silicon photonics will be pivotal in unlocking scalable mass adoption.

Conclusion

As digital transformation becomes more photon-powered, Photonic Integrated Circuits stand at the frontier of high-speed, high-efficiency technology. For decision-makers, investors, startups, and policymakers, now is the moment to align strategies, fund innovation, and build the ecosystem that will define the photonic era.

About the Spherical Insights

Spherical Insights is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

Contact Us:

Company Name: Spherical Insights

Email: [email protected]

Phone: +1 303 800 4326 (US)

Follow Us: LinkedIn | Facebook | Twitter

1 note

·

View note

Text

Tata Group’s Business Empire—Every Company You Need to Know

The Tata Group is not just a conglomerate—it’s a legacy. Founded in 1868 by Jamsetji Tata, it has grown to become one of India’s most respected and influential business empires. With operations in over 100 countries and companies across diverse sectors, the Tata Group touches nearly every aspect of modern life—from the salt on your table to the software running your business.

In this article, we’ll explore the key sectors the group operates in, highlight major companies under its umbrella, and provide a complete overview of the Tata Group Companies List that defines India’s global corporate footprint.

A Legacy That Shaped Indian Industry

Before we dive into specific companies, it’s important to understand what sets Tata apart. The group is known not only for its scale and global presence but also for its strong emphasis on ethics, philanthropy, and nation-building. The Tata Trusts, which control a majority of the holding company, reinvest much of the group's profits into social development, healthcare, and education.

Core Sectors of Tata Group

The Tata Group operates across more than a dozen industries. Here are some of its major sectors and leading companies:

1. Information Technology

Tata Consultancy Services (TCS): A global IT services giant and the crown jewel of the group. TCS is among the top 3 IT service providers in the world.

2. Automobiles

Tata Motors: India’s leading automobile manufacturer with vehicles ranging from passenger cars to military trucks.

Jaguar Land Rover (JLR): Acquired by Tata in 2008, this luxury brand expanded Tata’s global presence.

3. Steel & Engineering

Tata Steel: One of the top steel producers in the world with operations in India, Europe, and Southeast Asia.

Tata Power and Tata Projects: Leaders in energy and infrastructure solutions.

4. Consumer Products

Tata Consumer Products: Includes household names like Tata Salt, Tata Tea, and Tetley.

Trent: Operates popular retail chains like Westside and Zudio.

5. Telecom & Digital

Tata Communications: A global digital ecosystem enabler.

Tata Play (formerly Tata Sky): A key player in India's DTH entertainment space.

6. Financial Services

Tata Capital and Tata AIG: Provide a wide range of financial products, insurance, and investment solutions.

The Tata Group Companies: A Quick Overview

With more than 30 major companies under its umbrella, the Tata Companies are vast and diverse. Some other notable names include:

Tata Chemicals – A key player in the global chemicals market

Tata Elxsi – Specializes in design and technology for automotive and media

Taj Hotels (IHCL) – A luxury hotel chain with properties worldwide

Titan Company – A leading brand in watches, eyewear, and jewelry

Voltas – A major air conditioning and engineering solutions company

Each of these companies operates independently under the umbrella of Tata Sons, the principal investment holding company of the group.

Why Tata Group Stands Out

While the size of the Tata Group Companies is impressive, what truly sets the group apart is its commitment to sustainability, ethics, and nation-building. With a deep focus on social impact, the group reinvests a large portion of its profits back into the community. This makes Tata not just a business empire, but a force for good.

Conclusion

The Tata Group’s influence spans industries, continents, and generations. From technology and automobiles to hospitality and retail, the Tata Group Companies List reflects a business built on vision, values, and versatility. As India continues to rise on the global stage, the Tata Group remains a beacon of responsible and innovative enterprise.

0 notes

Text

Understanding Dividend Yield in the Context of Income-Producing Equities

Highlights:

Dividend Yield represents a ratio comparing annual dividend distribution to share price.

Commonly used in sectors with consistent cash flow, such as utilities and telecom.

Influenced by share price changes and corporate payout adjustments.

The Dividend Yield is a financial metric often associated with companies in the equity income sector, which includes utilities, telecommunications, and consumer staples. These sectors typically feature firms with stable earnings and a history of distributing regular cash payments. The Dividend Yield represents the ratio of a company’s annual dividend to its current share price. It serves as a reference point to understand how much income is being distributed relative to market valuation.

Calculating the Dividend Yield

The calculation of Dividend Yield involves dividing the total expected annual dividend per share by the current market price per share. This figure is generally expressed as a percentage. Since both dividend amounts and share prices may change over time, the resulting percentage can vary, even if one component remains stable. This variation reflects the dynamic relationship between company payouts and market valuation.

Sector Influence on Dividend Metrics

Utilities, telecommunications, and real estate firms often report relatively higher Dividend Yield values due to their consistent income streams. These companies typically operate in mature markets with regulated pricing structures or long-term service contracts. Their ability to generate predictable cash flows supports regular distributions, which, when compared with share price levels, influence the overall Dividend Yield metric.

Share Price Movement and Yield Variation

Fluctuations in share price directly affect the Dividend Yield even if the dividend payout remains unchanged. When share prices decline, the yield tends to rise, and when share prices increase, the yield generally decreases. This inverse relationship results in yield changes that are not always aligned with corporate performance. Market-wide movements, economic conditions, and sector trends may lead to shifts in share prices, thereby impacting the Dividend Yield ratio.

Dividend Policy and Company Behavior

The level of Dividend Yield is also shaped by a company's approach to distributing profits. Some firms follow a policy of consistent or gradually increasing payouts, while others may adjust based on cash reserves, profit margins, or capital expenditure plans. These internal policies influence how the dividend component of the Dividend Yield is set, contributing to overall yield variations across different periods.

Macroeconomic Factors and Yield Trends

Broader economic elements such as interest rates, inflation, and fiscal policy can influence the behavior of Dividend Yield across the equity market. For example, during periods of low interest rates, the relative attractiveness of dividend-paying equities may change, impacting how yields are perceived. Similarly, inflationary pressures may lead companies to adjust dividend levels to align with cost structures, affecting the yield percentage.

Industry Comparisons and Market Interpretation

The Dividend Yield varies across industries depending on capital requirements, growth strategies, and market structure. Capital-intensive sectors may retain a larger portion of earnings for reinvestment, leading to lower yields, while income-focused sectors typically maintain steady payout levels. Comparing yields across similar industries can offer insight into how companies allocate profits under varying operating models, although differences in financial strategy may also contribute to these disparities.

Yield Stability and Historical Trends

Long-term tracking of Dividend Yield across sectors or specific companies can highlight patterns in income distribution. Some firms are known for uninterrupted dividend payments over extended periods, leading to a perception of consistency. However, changes in regulation, operating costs, or strategic direction may affect future payouts, thereby influencing the reported yield without advance notice.

0 notes

Text

EML Laser Chip market

EML Laser Chip Market Set for Robust Growth Amid Rising Demand for High-Speed Communication

The EML Laser Chip market is witnessing a surge in demand, driven by the global expansion of high-speed optical communication systems. Valued at USD 182 Million in 2024, the market is forecasted to reach USD 352 Million by 2030, growing at a CAGR of 10.3% from 2025 to 2030. As next-generation technologies like 5G, AI, and cloud computing take center stage, the EML laser chip has become a vital component in ensuring faster and more efficient data transmission.

What’s Driving the EML Laser Chip Market?

The exponential rise in global internet usage, streaming services, and smart devices is putting immense pressure on communication networks. To handle this demand, telecom operators and data centers are rapidly turning to EML laser chips for their ability to transmit high-speed data over long distances with low signal degradation. These capabilities are accelerating the EML Laser Chip market growth across multiple regions.

Key EML Laser Chip market drivers include increased fiber-optic network deployments, rising adoption of 5G infrastructure, and the need for low-latency communication systems. As a result, the Global EML Laser Chip market is drawing strong interest from both established manufacturers and new entrants aiming to tap into this lucrative opportunity.

Key Trends Shaping the Market

The EML Laser Chip industry is evolving quickly, with innovations focusing on compact chip design, energy efficiency, and improved reliability. These trends are opening new EML Laser Chip market opportunities, particularly in automotive LiDAR, industrial automation, and advanced healthcare equipment.

Additionally, the shift toward integrated photonics and silicon photonics is influencing the EML Laser Chip market trends, making production more cost-effective and scalable. Companies investing in R&D are leading the charge in reshaping the future of optical communication technologies.

Market Restraints and Challenges

While the growth outlook is promising, the EML Laser Chip market is not without challenges. High initial manufacturing costs and the technical complexity of chip integration pose significant EML Laser Chip market restraints, especially for small and mid-sized players. However, ongoing efforts in innovation and standardization are expected to ease these issues over time.

Future Outlook: A Market on the Rise

According to the latest EML Laser Chip market analysis, the sector is on a strong upward trajectory. With expanding use cases and growing adoption across industries, the EML Laser Chip market volume is set to increase significantly over the next five years. The ongoing EML Laser Chip market study continues to uncover promising growth avenues and potential shifts in the competitive landscape.

For stakeholders, understanding the current EML Laser Chip market insights, including EML Laser Chip market statistics, trends, and forecast data, will be critical in capitalizing on future opportunities. As the digital world continues to evolve, the EML Laser Chip market share will increasingly favor those at the forefront of innovation and agility.

0 notes

Text

5G Infrastructure Market Size, Share, Trends, Forecast & Growth Analysis 2034

5G Infrastructure Market is on a meteoric rise, projected to grow from $10.9 billion in 2024 to a staggering $131.4 billion by 2034, registering a remarkable CAGR of 28.3%. This sector is the backbone of next-generation wireless communication, enabling ultra-fast internet, real-time connectivity, and the seamless integration of billions of smart devices. From enhanced mobile broadband and IoT to autonomous vehicles and smart city ecosystems, 5G infrastructure is revolutionizing how the world connects, communicates, and operates. This market includes key technologies like Radio Access Networks (RAN), core networks, and advanced transport networks — each playing a critical role in delivering low latency, high throughput, and massive device capacity.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS21346

Market Dynamics

The explosive demand for high-speed internet and real-time data transmission is at the core of this market’s dynamic growth. The rise in smart devices, increasing consumption of video content, and digital transformation initiatives across industries are amplifying the need for robust 5G infrastructure. Among various segments, Radio Access Networks (RAN) continue to dominate with a 45% market share, driven by the expansion of small cell deployments and the need for better spectrum efficiency. Meanwhile, the core network segment — constituting 30% — is flourishing due to virtualization and network slicing. A rising trend in edge computing is shaping the market further, especially for applications that require ultra-low latency such as AR/VR, telemedicine, and industrial automation.

Key Players Analysis

Market leadership is held by major global telecom equipment providers such as Nokia Networks, Ericsson, ZTE Corporation, and Samsung Networks. These firms are pioneering innovations in both hardware and software, ensuring scalable and cost-effective deployment. Emerging players like Mavenir Systems and Altiostar Networks are making their mark by offering cloud-native, open-RAN solutions tailored to meet modern network demands. Meanwhile, collaborative initiatives, such as Nokia’s partnerships with hyperscalers like Microsoft, are redefining how telecom infrastructure is delivered and managed. The competitive landscape is dynamic, with heavy investments in R&D and strategic alliances focused on expanding reach and enhancing service capabilities.

Regional Analysis

Asia-Pacific is taking the lead in global 5G deployments, with China, South Korea, and Japan spearheading aggressive rollouts. These countries are heavily investing in telecom infrastructure as part of broader smart city and digital economy initiatives. North America is not far behind, with the United States at the forefront, driven by both public and private investments. The region benefits from early spectrum auctions, strong regulatory support, and the rapid adoption of 5G-enabled services. Europe is progressing steadily, led by Germany, the UK, and France, supported by EU-level strategies for digital innovation. The Middle East and Africa are emerging players, with the UAE and Saudi Arabia making significant progress in deploying 5G for industrial and smart governance purposes. Latin America, while still evolving, shows great promise, particularly in Brazil and Mexico, where telecom companies are beginning to adopt 5G as part of broader modernization goals.

Recent News & Developments

Recent developments highlight the growing integration of edge computing, IoT, and AI into 5G networks. Partnerships between telecom and tech companies are becoming common to enable next-gen solutions. Notably, collaborations like Ericsson with Intel, and Nokia with AWS, are aiming to create cloud-native 5G environments. Governments are fast-tracking spectrum auctions and building regulatory frameworks to support safe and efficient 5G rollouts. Moreover, initiatives like Open RAN are gaining momentum, promoting vendor diversity and reducing costs. Hardware advancements, especially in base stations, antennas, and transceivers, are making networks more flexible and scalable. These innovations are pushing the boundaries of what 5G can deliver — from smart healthcare to autonomous transportation.

Browse Full Report : https://www.globalinsightservices.com/reports/5g-infrastructure-market/

Scope of the Report

This report covers in-depth analysis of the 5G Infrastructure Market across various segments, including RAN, core networks, transport networks, and services. It evaluates deployment modes such as standalone and non-standalone networks, and provides a breakdown by key equipment and end users. From telecom giants and enterprises to government applications, the scope is wide-ranging. The analysis also identifies growth patterns, strategic alliances, and technology roadmaps that are shaping the industry’s future. With the continued evolution of mobile and cloud technologies, 5G is not just a faster network — it’s a transformative platform for innovation and economic growth across every region and sector.#5ginfrastructure #smartconnectivity #edgecomputing #digitaltransformation #iotenabled #nextgenwireless #telecominnovation #smartcitiesnetwork #autonomousfuture #cloudnative5g

Discover Additional Market Insights from Global Insight Services:

Semiconductor Waste Management Market : https://linkewire.com/2025/07/08/semiconductor-waste-management-market/

Embedded Hypervisor Market : https://linkewire.com/2025/07/08/embedded-hypervisor-market/

Corrosion Under Insulation Monitoring Market : https://linkewire.com/2025/07/08/corrosion-under-insulation-monitoring-market-2/

GPS Tracking Device Market : https://linkewire.com/2025/07/08/gps-tracking-device-market-3/

Optical Transceiver Market : https://linkewire.com/2025/07/08/optical-transceiver-market-2/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

The Future Is Now: Generative AI Market Set to Reach 133.9 billion by 2032

Meticulous Research®—a leading global market research company, published a research report titled ‘Generative AI Market—Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication from Meticulous Research®, the generative AI market is expected to reach $133.9 billion by 2032, at a CAGR of 32.6% from 2025 to 2032.

The generative AI market is primarily driven by the rising demand for content creation and creative applications, advancements in AI and deep learning technologies, increasing adoption in the IT and telecom sectors, and a growing emphasis on customer satisfaction. However, concerns related to data privacy and security may restrain market growth.

Furthermore, the rising adoption of generative AI to enhance productivity, the increasing utilization of large language models, the growing demand for automated business processes, and the expanding use of generative AI in the media and entertainment sector are anticipated to create significant growth opportunities for market players. On the other hand, the misconception and limited understanding of generative AI solutions present a challenge that affects the growth of the generative AI market.

A New Era for Industry:

With a market size expected to reach nearly a trillion dollars, generative AI is poised to fundamentally reshape how industries operate. In healthcare, for example, AI-generated insights are making diagnostics faster and more accurate, while in finance, automated content creation and risk assessment are streamlining compliance and boosting efficiency. Manufacturing is seeing smarter supply chains and predictive maintenance, and in retail, personalized recommendations are transforming the customer experience.

But the impact goes beyond automation. Generative AI is enabling companies to innovate at a pace never seen before. Product development cycles are shrinking as AI helps simulate and test new ideas virtually. Media and entertainment companies are using AI to create content tailored to individual tastes, while entirely new business models—like AI-driven design services and content generation platforms—are emerging. The ripple effects will be felt across the global economy, with businesses that adapt quickly reaping the greatest rewards.

What’s Fuelling the Boom?

Several factors are behind the rapid rise of generative AI. First, there’s an ever-increasing demand for innovation and efficiency. Companies are under pressure to do more with less, and AI tools are helping them automate repetitive tasks, generate content, and make smarter decisions. The technology itself has also become more accessible, thanks to advances in large language models and user-friendly platforms.

Another major driver is the clear competitive advantage that early adopters are gaining. Businesses that harness AI for personalized marketing, predictive analytics, or smarter automation are pulling ahead of their peers. The versatility of generative AI means it can be applied to everything from HR and R&D to customer service and product design, making it a valuable asset in almost any sector.

The Role of Market Leaders:

The future of generative AI is being shaped by a handful of major players. Companies like NVIDIA, IBM, OpenAI, Microsoft, Google, and AWS are setting the pace, not just by developing advanced models and infrastructure, but by making these tools available to a wide audience. NVIDIA’s powerful GPUs have become the backbone of AI computing, while OpenAI and Google are constantly pushing the boundaries with new models and APIs.

These leaders are also making it easier for businesses of all sizes to adopt AI, offering flexible pricing, cloud-based solutions, and partnerships that lower the barriers to entry. By democratizing access to advanced AI technology, they’re fostering a vibrant ecosystem of innovation and ensuring that the benefits of generative AI reach far beyond the tech sector.

How Businesses Can Get Ahead:

For companies looking to capitalize on the explosive growth of generative AI, now is the time to act. The first step is to identify areas where AI can have the biggest impact—whether it’s automating customer support, accelerating product development, or delivering personalized experiences. Encouraging a culture of experimentation is also key; teams that are empowered to test new tools and workflows often uncover valuable insights and efficiencies.

Collaboration is another smart move. By partnering with established AI vendors, businesses can tap into world-class expertise and technology, accelerating their own adoption and reducing risk. It’s also important to stay informed about evolving regulations and ethical standards, ensuring that AI is deployed responsibly and builds trust with customers and stakeholders.

Key Players

The key players operating in the generative AI market are NVIDIA Corporation (U.S.), IBM Corporation (U.S.), Amazon Web Services, Inc. (U.S.), Capgemini SE (France), Google LLC. (U.S), Kyndryl Holdings, Inc. (U.S.), Intel Corporation (U.S.), Synthesia (U.K.), Writesonic (U.S.), Salesforce, Inc. (U.S.), D-ID (Israel), and Adobe Inc. (U.S.).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6008

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Generative Adversarial Networks#Generative AI#Image Synthesis#Text Generation#Deep Learning#Generative AI Market

0 notes

Text

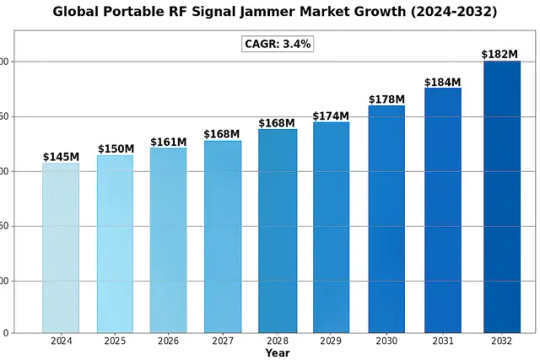

Portable RF Signal Jammer Market : Global outlook, Emerging Trends-Technologies, and Forecast to 2032

The global Portable RF Signal Jammer Market was valued at 145 million in 2024 and is projected to reach US$ 182 million by 2032, at a CAGR of 3.4% during the forecast period.

Portable RF Signal Jammers are devices designed to block wireless communication signals by emitting radio frequency interference. These compact systems disrupt signals across various frequencies used by cellular networks, Wi-Fi, GPS, and other wireless technologies. The technology works by overwhelming target frequencies with noise or transmitting signals that prevent legitimate communication.

The market growth is driven by increasing security concerns in sensitive locations like government facilities, military zones, and correctional institutions, where unauthorized communication poses risks. However, strict regulations in many countries limit civilian use because RF jamming interferes with licensed spectrum operations. While military-grade jammers dominate the market with advanced capabilities, general-purpose models are finding niche applications in corporate and educational settings for maintaining focused environments. Technological advancements are focusing on selective jamming capabilities to comply with evolving regulations while meeting security needs.

Get Full Report with trend analysis, growth forecasts, and Future strategies : https://semiconductorinsight.com/report/portable-rf-signal-jammer-market/

Segment Analysis:

By Type

Military Grade Segment Dominates Due to High Security and Government Adoption

The market is segmented based on type into:

General Purpose

Military Grade

By Application

Government and Law Enforcement Agencies Lead Due to Anti-Terrorism and Security Requirements

The market is segmented based on application into:

Educational Institution

Government and Law Enforcement Agencies

Military and Defense

Other

By End User

Defense Sector Represents the Largest Consumer Base

The market is segmented based on end user into:

Commercial

Defense

Government

By Frequency Range

Multi-Band Jammers Gain Traction Due to Their Versatility

The market is segmented based on frequency range into:

Single Band

Multi-Band

Regional Analysis: Portable RF Signal Jammer Market

North America The North American market holds a significant share in the global Portable RF Signal Jammer industry due to stringent regulatory frameworks and high adoption rates among government and defense sectors. The U.S. leads the region, where agencies like the Department of Defense and law enforcement utilize military-grade jammers for critical operations. Canada follows closely, with increasing investments in cybersecurity and frequency management. However, strict FCC regulations limit commercial usage, ensuring jammers remain largely within authorized applications. Market growth is also driven by rising concerns over data breaches and corporate espionage, pushing demand for signal-blocking solutions in high-security environments like boardrooms and government facilities. Technological advancements, such as adaptive jamming and AI-driven frequency hopping, are further enhancing product capabilities.

Europe Europe’s market is shaped by robust telecom regulations and privacy laws, restricting the legal use of jammers to authorized entities. Countries like Germany, France, and the UK dominate demand, primarily for defense, counter-terrorism, and prison security applications. The EU’s strict spectrum allocation policies ensure limited but critical deployment in controlled environments. Despite regulatory hurdles, interest is growing in sectors like education (preventing cheating in exams) and corporate security (protecting confidential discussions). Challenges include public skepticism and ethical debates around communication suppression, though advancements in precision jamming—targeting only unauthorized frequencies—are opening new opportunities. Compliance with CE and RED directives remains a key focus for manufacturers.

Asia-Pacific The Asia-Pacific region is witnessing the fastest growth, fueled by China’s expansive military modernization and India’s counter-insurgency operations. China leads production and adoption, leveraging state-backed R&D for advanced jamming systems. India’s market is expanding due to border security needs and anti-terror initiatives. Japan and South Korea focus on defense and corporate applications, while Southeast Asia shows rising demand for prison and government use. The region’s lower regulatory barriers (outside Japan and Australia) encourage commercialization, though concerns over misuse persist. Cost-effective general-purpose jammers are popular, but military-grade devices drive revenue. Urbanization and digital infrastructure growth are indirectly boosting demand by increasing RF interference risks.

South America South America’s market remains niche, with Brazil and Argentina as primary adopters for law enforcement and military purposes. Economic instability limits large-scale investments, but drug cartel operations and jailbreak prevention initiatives sustain demand in Brazil. Chile and Colombia show sporadic interest in counter-drone jamming for public safety. Regulatory frameworks are underdeveloped, leading to a gray market for consumer-grade devices, though penalties for unauthorized use are escalating. Manufacturers face challenges in balancing affordability with compliance, as budget constraints push buyers toward non-certified products. Long-term potential lies in modernization of defense and prison systems, contingent on economic recovery.

Middle East & Africa This region is characterized by high defense expenditures, particularly in Gulf nations like Saudi Arabia and the UAE, where portable jammers are deployed for military and VIP protection. Israel stands out for its technologically advanced jamming systems, driven by geopolitical tensions. Africa’s market is fragmented, with South Africa and Egypt leading in tactical applications for anti-poaching and border security. Challenges include uneven regulation and limited awareness outside defense sectors. The lack of standardized policies hampers market growth, but rising terrorism threats and infrastructure projects (e.g., smart cities) are expected to drive adoption. Partnerships with global manufacturers are critical to overcoming technical and financial barriers.

MARKET OPPORTUNITIES

Emerging AI-Powered Adaptive Jamming Technologies Creating New Growth Prospects

The integration of artificial intelligence in RF jamming systems presents transformative opportunities, enabling real-time threat analysis and dynamic response capabilities. Next-generation systems incorporating machine learning algorithms can autonomously identify and neutralize threats while avoiding interference with authorized communications. This technological evolution is particularly significant for border security applications, where adaptive systems demonstrated 92% effectiveness in recent field tests compared to 68% for conventional solutions.

Expanding Counter-Drone Applications Across Multiple Sectors

The proliferation of commercial drones has created a substantial market for specialized jamming solutions, with airport security accounting for 35% of current deployments. Recent technological advancements have reduced drone neutralization times from 30 seconds to under 5 seconds in operational scenarios. Energy infrastructure protection represents another high-growth sector, with oil refineries and power plants increasingly investing in portable anti-drone systems as part of comprehensive security strategies.

PORTABLE RF SIGNAL JAMMER MARKET TRENDS

Growing Demand for Security and Privacy Solutions Drives Market Expansion

The global Portable RF Signal Jammer market, valued at $145 million in 2024, is witnessing substantial growth due to increasing concerns over unauthorized communication interception and espionage. Projections indicate the market will reach $182 million by 2032, growing at a CAGR of 3.4% during the forecast period. This surge is primarily driven by rising demand from government agencies, military sectors, and corporate entities for securing sensitive facilities against cyber threats and data breaches. Additionally, the proliferation of wireless technology has amplified the need for effective countermeasures to prevent signal-based attacks.

Other Trends

Technological Advancements in Jamming Capabilities

The market is witnessing significant investments in next-generation signal jamming technologies, including AI-driven frequency hopping mitigation and adaptive jamming systems. Innovations such as multi-band jammers, capable of disrupting signals across Wi-Fi, Bluetooth, drones, and cellular networks, enhance operational efficiency. Furthermore, advancements in miniaturization and portability have expanded the application scope, catering to sectors like law enforcement and event security, where discreet and lightweight jammers are crucial.

Regulatory and Ethical Constraints Shape Market Dynamics

While demand grows, the market faces challenges due to strict government regulations on spectrum usage. Countries like the U.S. and EU nations enforce stringent policies to prevent misuse of jammers in civilian spaces. Ethical concerns regarding potential disruptions to emergency communications also prompt tighter controls. However, manufacturers are innovating compliance-focused solutions, such as selective jamming protocols, which target specific frequencies while leaving emergency bands unaffected. This balance between security needs and regulatory compliance remains a pivotal factor in market evolution.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Players Expand Portfolio to Meet Rising Security Demands

The portable RF signal jammer market exhibits a fragmented competitive landscape, with key players actively investing in technological advancements to gain market share. SESP Group, a prominent industry leader, has strengthened its position through strategic partnerships with defense and law enforcement agencies, particularly in North America and Europe. The company specializes in high-power military-grade jammers, capturing approximately 15% of the global market revenue in 2024.

Rantelon and HSS Development have emerged as significant competitors, focusing on compact, multi-frequency jammers for government applications. These companies account for a combined 22% market share, driven by increasing demand from correctional facilities and secure government installations. Their product development strategies emphasize adaptive jamming technologies that comply with evolving radio spectrum regulations.

Meanwhile, Asian manufacturers like Shenzhen Tangreat Technology are gaining traction in cost-sensitive markets through competitive pricing strategies. The company has expanded its distribution network across Southeast Asia, capturing nearly 18% of regional sales volume. This growth reflects the rising adoption of general-purpose jammers in commercial sectors such as educational institutions and corporate environments.

The market dynamic is further influenced by niche players such as Digital RF and LDAF, which specialize in customized solutions for specialized applications. These companies focus on R&D investments to develop intelligent jamming systems with AI-powered frequency detection capabilities. Their technological edge positions them favorably in high-growth segments, particularly for counter-drone applications in military and security sectors.

List of Key Portable RF Signal Jammer Companies Profiled

SESP Group (China)

Rantelon (UK)

HSS Development (USA)

Phantom Technologies (Israel)

Shenzhen Tangreat Technology (China)

Enterprise Control Systems (USA)

Digital RF (Germany)

LDAF (France)

Mctech Technology (South Korea)

RF-Technologies (USA)

Learn more about Competitive Analysis, and Forecast of Global Portable RF Signal Jammer Market : https://semiconductorinsight.com/download-sample-report/?product_id=103582

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Portable RF Signal Jammer Market?

-> Portable RF Signal Jammer Market was valued at 145 million in 2024 and is projected to reach US$ 182 million by 2032, at a CAGR of 3.4% during the forecast period.

Which key companies operate in Global Portable RF Signal Jammer Market?

-> Key players include SESP Group, Rantelon, HSS Development, Phantom Technologies, Shenzhen Tangreat Technology, Enterprise Control Systems, Digital RF, and RF-Technologies.

What are the key growth drivers?

-> Key growth drivers include increasing security threats, military modernization programs, and demand for secure communication zones in government facilities.

Which region dominates the market?

-> North America holds the largest market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include multi-band jamming capabilities, portable battery-operated designs, and integration with IoT security systems.

Browse Related Research Reports :

https://semiconductorinsight.com/report/global-sata-hard-disk-drives-market/

https://semiconductorinsight.com/report/global-ignition-safety-device-isd-market/

https://semiconductorinsight.com/report/global-fiber-optic-probe-market/

https://semiconductorinsight.com/report/global-thermopile-sensors-market/

https://semiconductorinsight.com/report/motion-capture-sensors-market/

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 +91 8087992013 [email protected]

0 notes

Text

Tata Group Companies List: From Steel to Software

The Tata Group is one of India’s oldest and most trusted conglomerates, with a legacy spanning over 150 years. From pioneering industries to setting global benchmarks, Tata companies have played a significant role in shaping India’s economic growth. Their businesses range from traditional heavy industries like steel to modern technology and digital services.

A Legacy of Diverse Businesses

The Tata Group Companies List is a testament to the group’s diversity and reach. Starting with Tata Steel, India’s first integrated steel plant, the group has grown into multiple sectors including automotive, IT, telecom, hospitality, and consumer goods.

Tata Motors is a household name in the automobile industry, producing cars, buses, and trucks sold across the world. Tata Consultancy Services (TCS) is a global leader in IT services, consistently ranking among the top technology companies worldwide.

Expanding Global Footprint

Tata companies are not just limited to India. The group owns iconic international brands like Jaguar Land Rover and Tetley Tea, expanding its presence to over 100 countries. This global reach has helped the Tata Group become a respected name synonymous with trust and quality.

It’s interesting to note that while the Tata Group leads India’s corporate landscape, it shares the stage with other big names like mukesh ambani Firms, which are also shaping various industries from energy to telecom.

Innovation and Sustainability

One of the key reasons behind the Tata Group’s enduring success is its focus on innovation and sustainability. Companies like Tata Power are investing in renewable energy, while Tata Chemicals works on sustainable materials and solutions. TCS continues to push boundaries in digital transformation and AI solutions, serving clients across industries.

In addition to technological advancement, the Tata Group places immense emphasis on corporate social responsibility. Through the Tata Trusts, the group funds and supports education, healthcare, rural development, and community welfare across India.

Key Companies in the Tata Group

To give you a quick glimpse, here are some major names from the Tata Group Companies List:

Tata Steel: One of the world’s top steel producers.

Tata Motors: Leading auto manufacturer with global brands.

Tata Consultancy Services (TCS): Among the largest IT services firms worldwide.

Tata Power: A key player in conventional and renewable energy.

Tata Chemicals: Focuses on chemicals, crop protection, and innovation.

Titan Company: Famous for watches, jewelry, and eyewear.

Tata Communications: Provides telecom and digital infrastructure services.

Indian Hotels Company Limited (Taj Hotels): One of Asia’s largest hospitality groups.

Looking Ahead

The Tata Group’s journey from steel to software is a reflection of India’s growth story itself — evolving from an industrial economy to a digital powerhouse. As new industries emerge and technology reshapes markets, Tata companies continue to adapt, innovate, and lead with values that have earned them respect across generations.

Whether you look at legacy sectors or modern digital solutions, the Tata Group Companies List proves that the conglomerate’s commitment to nation-building and global excellence remains stronger than ever.

0 notes

Text

Europe Generative AI Market: Revolutionizing Content Creation with AI

The Europe generative AI market was valued at USD 2.42 billion in 2023 and is projected to surge to USD 19.63 billion by 2030, demonstrating a robust compound annual growth rate (CAGR) of 35.8% from 2024 to 2030. This significant expansion is primarily driven by the increasing availability of vast datasets across various sectors like finance, healthcare, and entertainment, which are crucial for training sophisticated generative AI models. Furthermore, continuous advancements in deep learning techniques, particularly neural networks such as Variational Autoencoders (VAEs) and Generative Adversarial Networks (GANs), are instrumental in enabling the creation of highly realistic and high-quality content.

Key Market Insights:

Germany's Dominance: In 2023, Germany led the market with a 23.0% share, propelled by accelerated adoption across traditional sectors like manufacturing, retail, telecoms, and healthcare, alongside ongoing development in artificial intelligence (AI) computing power.

Software Segment Leads: The software segment held the largest revenue share of 64.6% in 2023 and is anticipated to maintain its dominance throughout the forecast period.

Transformers Technology Prevails: The transformers segment commanded the largest revenue share in 2023, largely due to the increasing use of transformer applications such as text-to-image AI, which converts textual input into visual output.

Natural Language Processing (NLP) Drives Application Growth: The Natural Language Processing (NLP) segment dominated the market in 2023 and is projected to exhibit a significant CAGR over the forecast period, reflecting the widespread utility of generative AI in language-based applications.

Multimodal Generative Models Fastest Growing: Multimodal generative models are expected to experience the fastest growth during the forecast period, driven by the escalating demand for AI models capable of processing and generating content across diverse modalities including text, images, and audio.

Media & Entertainment Leads End-Use: The media & entertainment segment secured the largest revenue share in 2023 and is projected to grow at a significant CAGR. This growth is fueled by the increasing application of generative AI to enhance advertising and campaign journalism within these sectors.

Order a free sample PDF of the Europe Generative AI Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2023 Market Size: USD 2.42 Billion

2030 Projected Market Size: USD 19.63 Billion

CAGR (2024-2030): 35.8%

Key Companies & Market Share Insights

Some key players actively shaping the European generative AI market include Aleph Alpha, Mistral AI, and Helsing.

Aleph Alpha, a German AI application and research company founded in 2019 and headquartered in Heidelberg, focuses on developing and operationalizing large-scale AI models for language, strategy, and image data. Their mission is to empower enterprises and governments with sovereign, human-centric AI technology. Aleph Alpha offers a platform designed to ensure operations align with regulatory requirements and mitigate risks, incorporating trustworthiness features that provide explainability and control over AI-driven processes and decisions. They are known for their Luminous LLM, which offers multimodal and multilingual capabilities.

Mistral AI, a French AI company founded in 2023 and based in Paris, specializes in developing large open-weight language models. Their models, such as the Mixtral 8x7B (with 46.7 billion parameters), have demonstrated strong performance across multiple languages. Mistral AI is committed to developing open-weight models that rival proprietary solutions, serving both the open-source community and enterprise clients.

Helsing, a German defense technology company founded in 2021 and headquartered in Munich, focuses on developing AI software and integrated platforms to enhance military capabilities for democratic governments. While primarily operating in the defense sector, their expertise in real-time information processing and AI-driven decision-making contributes to the broader European AI landscape. Helsing emphasizes ethical considerations in its operations and aims to achieve global technology leadership in processing unstructured sensor data into actionable intelligence for defense applications.

Key Players

Pixis

Everseen

DeepL

Creative Fabrica

PolyAI

Humanloop

Conjecture

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The European generative AI market is experiencing significant expansion, driven by increasing data availability and advancements in deep learning. Germany leads regional adoption, with software and transformer technologies dominating. Natural Language Processing and multimodal models are key growth areas, while media and entertainment are major end-users. Key players like Aleph Alpha, Mistral AI, and Helsing are fostering innovation and expanding capabilities to meet this growing demand.

0 notes

Text

5G Base Station Market to Witness Massive Growth as Demand for High-Speed Connectivity Surges

Market Overview

The 5G base station market is poised for significant expansion, fueled by the global shift toward next-generation connectivity. With telecom providers investing heavily in infrastructure upgrades, the industry is experiencing rapid deployment of both standalone and non-standalone 5G architectures. As urbanization, IoT adoption, and mobile data traffic continue to increase, 5G base stations market is emerging as critical assets in meeting bandwidth and latency demands.

The 5G Base Station Market size is projected to grow from USD 37.44 billion in 2025 to USD 132.06 billion by 2030, reflecting an impressive compound annual growth rate (CAGR) of 28.67% during the forecast period.

Key Trends

Expansion of mmWave Deployments Millimeter wave (mmWave) technology is being increasingly adopted due to its ability to provide ultra-fast data rates. While it has shorter range, its role in urban small-cell networks is proving crucial to meet high-density demand.

Rise in Network Densification Initiatives To ensure consistent 5G performance, operators are deploying dense clusters of small base stations. This densification trend is pivotal in improving coverage, especially in indoor and metropolitan areas.

Increased Investment in Smart City Infrastructure Governments and city planners are investing in smart city projects, where 5G base stations are essential to power applications like autonomous vehicles, surveillance systems, and traffic management.

Edge Computing Integration The integration of edge computing with 5G base stations enables faster data processing closer to the user. This development is particularly important for mission-critical applications in healthcare and manufacturing.

Open RAN (O-RAN) Adoption The shift toward Open Radio Access Networks is reshaping the 5G base station industry by allowing network operators to mix and match components from different vendors, reducing costs and enhancing flexibility.

Challenges

Despite the optimistic outlook, the 5G base station market faces several challenges. High deployment and operational costs, particularly in rural or low-revenue regions, continue to hinder adoption. Additionally, regulatory hurdles, spectrum availability, and concerns over cybersecurity are barriers that stakeholders must navigate to ensure seamless rollouts.

For a detailed overview and more insights on the 5G Base Station Market, you can refer to the full market research report by Mordor Intelligence: https://www.mordorintelligence.com/industry-reports/5g-base-station-market?utm_source=tumblr

Conclusion

The 5G base station market is on an upward trajectory, with vast opportunities unfolding across telecom, enterprise, and public sectors. As the global digital economy evolves, the 5G base station market size will continue to expand, shaping the future of connectivity. Strategic investments, innovation in deployment models, and regulatory support will be key to unlocking the full potential of this transformative industry.

Other Related Reports:

Esports Industry

Power Electronics Market

Language Services market

Crystal Oscillator Market

#5g base station market#5g base station market size#5g base station industry#5g base station market trends#5g base station market share#5g base station market report

0 notes

Text

Antenna in Package (AiP) Market Transformation Fueled by Millimeter-Wave and High-Frequency Applications

The Antenna in Package (AiP) Market is undergoing a transformative phase, driven by the rapid evolution of wireless communication, miniaturization of devices, and the widespread adoption of 5G technologies. AiP is an advanced packaging technology that integrates antenna elements directly within the package of a radio frequency (RF) front-end module. This eliminates the need for a separate antenna, significantly reducing the device footprint while improving performance. With the growing demand for compact, efficient, and high-speed wireless solutions across industries such as consumer electronics, automotive, and telecommunications, AiP is becoming a crucial enabler of next-generation applications.

Technological Advancements Driving the Market

One of the primary factors accelerating the AiP market growth is the increasing deployment of 5G infrastructure globally. AiP solutions are vital to mmWave (millimeter-wave) 5G technology, where higher frequencies are utilized to deliver ultra-fast data speeds. These frequencies require dense antenna arrays that can only be realized with compact and efficient integration techniques, which is precisely where AiP excels.

Additionally, the development of AI-driven smart devices and the Internet of Things (IoT) ecosystem has further pushed the boundaries for smaller, faster, and more energy-efficient antennas. AiP technology supports high-frequency operation and multi-band performance, making it ideal for multifunctional devices used in smart homes, autonomous vehicles, wearables, and industrial automation.

Expanding Applications Across Key Industries

The adoption of AiP is prominent in consumer electronics, particularly in smartphones, tablets, and laptops. Leading manufacturers are incorporating AiP modules to achieve sleeker designs while enhancing signal integrity. The automotive industry is also experiencing a significant impact from AiP integration, especially in advanced driver-assistance systems (ADAS) and vehicle-to-everything (V2X) communication, where reliable and compact antenna solutions are critical.

In the defense and aerospace sector, AiP is enabling robust and secure communication systems that meet stringent size, weight, and performance (SWaP) requirements. Furthermore, in the healthcare sector, AiP is facilitating the development of compact medical imaging and diagnostic devices with enhanced wireless connectivity, especially for remote monitoring and telemedicine applications.

Market Dynamics and Regional Insights

The global AiP market is expected to grow at a substantial CAGR over the next several years. North America currently leads in terms of revenue share, primarily due to early 5G rollouts, strong presence of leading tech companies, and significant investments in R&D. However, the Asia-Pacific region is projected to witness the fastest growth, driven by massive consumer electronics production, rising demand for advanced connectivity solutions, and increased government focus on smart city initiatives and digital transformation.

China, Japan, and South Korea are at the forefront of AiP adoption in Asia-Pacific, with Chinese manufacturers aggressively expanding 5G networks and launching AiP-enabled devices. Europe is also emerging as a strong player in the AiP space, supported by technological innovation and regulatory support for clean and connected mobility.

Key Players and Strategic Initiatives

Prominent players in the AiP market include Qualcomm, Murata Manufacturing, Amkor Technology, MediaTek, and Samsung Electronics. These companies are continuously investing in research and innovation to develop next-generation AiP modules that meet the demands of evolving wireless communication standards.

Strategic collaborations, partnerships, and mergers are shaping the competitive landscape. For instance, partnerships between semiconductor companies and telecom giants are accelerating the integration of AiP into 5G infrastructure. Moreover, increased venture capital funding in AiP startups is spurring innovation and commercialization of advanced packaging solutions.

Future Outlook

The future of the AiP market looks highly promising. With the rise of 6G research, augmented reality (AR), virtual reality (VR), and ubiquitous IoT connectivity, the demand for miniaturized, high-performance antennas will surge even further. AiP technology, with its ability to combine efficiency, compactness, and reliability, is poised to become the standard for next-generation wireless devices.

However, challenges such as high manufacturing costs, thermal management issues, and integration complexities remain. Overcoming these barriers will require collaborative efforts between technology providers, material scientists, and manufacturers.

In conclusion, the Antenna in Package (AiP) Market is at the heart of a wireless revolution, powering innovations across various industries. As technological trends evolve, AiP is set to redefine the standards of antenna performance, paving the way for a smarter, more connected future.

0 notes

Text

Power Supply Unit (PSU) Market: Innovation Trends and Technological Advancements 2025–2032

Global Power Supply Unit (PSU) Market Research Report 2025(Status and Outlook)

Power Supply Unit (PSU) Market size was valued at US$ 12.47 billion in 2024 and is projected to reach US$ 21.38 billion by 2032, at a CAGR of 6.3% during the forecast period 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=95800

MARKET INSIGHTS

The global Power Supply Unit (PSU) Market size was valued at US$ 12.47 billion in 2024 and is projected to reach US$ 21.38 billion by 2032, at a CAGR of 6.3% during the forecast period 2025-2032. This growth is driven by increasing demand for energy-efficient computing solutions and expansion of data centers worldwide.

A Power Supply Unit (PSU) is a critical hardware component that converts alternating current (AC) to direct current (DC) while regulating voltage for computer systems. Modern PSUs feature modular designs, 80 PLUS certification for energy efficiency, and advanced thermal management systems. The market offers two primary variants: AC power supplies (for general computing applications) and DC power supplies (specialized for industrial equipment and telecom infrastructure).

Key growth drivers include the rapid expansion of cloud computing infrastructure and increasing adoption of high-performance computing solutions. However, the market faces challenges from alternative power solutions and supply chain disruptions affecting semiconductor availability. Recent technological advancements focus on improving energy efficiency – with leading manufacturers like Corsair and Seasonic introducing PSUs achieving 94% conversion efficiency under Titanium certification standards. The competitive landscape features established players including Thermaltake, FSP Group, and Cooler Master, who collectively hold over 45% of the global market share through continuous product innovation and strategic partnerships with OEMs.

List of Key Power Supply Unit Manufacturers Profiled

Seasonic (Taiwan)

Corsair (U.S.)

Cooler Master (Taiwan)

Thermaltake (Taiwan)

FSP Group (Taiwan)

SilverStone Technology (Taiwan)

Antec (U.S.)

XFX (Hong Kong)

New Japan Radio (Japan)

Gigabyte (Taiwan)

Segment Analysis:

By Type

AC Power Supply Segment Leads the Market Owing to Widespread Adoption in Industrial Applications

The market is segmented based on type into:

AC Power Supply

DC Power Supply

By Application

PC Computers Segment Dominates Due to Increasing Demand for Gaming and High-Performance PCs

The market is segmented based on application into:

PC Computers

Mobile Devices

Industrial Equipment

Telecommunications

Others

By Power Rating

300W-500W Segment Holds Major Share for Mid-Range Computing Needs

The market is segmented based on power rating into:

Below 300W

300W-500W

500W-800W

Above 800W

By Form Factor

ATX Segment Dominates Compatibility With Standard Desktop Configurations

The market is segmented based on form factor into:

ATX

SFX

TFX

Flex ATX

Others

Regional Analysis: Global Power Supply Unit (PSU) Market

North America The North American PSU market is characterized by high technological adoption and stringent energy efficiency standards. The region’s mature PC gaming industry and data center expansion are key growth drivers, with the U.S. accounting for over 60% of regional demand. 80 PLUS certification requirements have pushed manufacturers toward modular, high-efficiency (90%+) units. However, market saturation in desktop PC segments has led vendors to focus on premium gaming PSUs and server-grade solutions. The Canadian market shows steady growth, fueled by increasing investments in hyperscale data centers.

Europe Europe’s PSU market is shaped by the EU Ecodesign Directive and energy labeling regulations, driving innovation in low-power consumption units. Germany and France lead in industrial and commercial applications, while the UK gaming sector sustains demand for high-wattage modular PSUs. The region has seen a 12% CAGR in server PSU demand, with increased cloud computing investments. A significant trend is the shift toward fanless and silent PSUs in residential and office environments. Eastern Europe presents emerging opportunities as PC component manufacturing expands to countries like Poland and Hungary.

Asia-Pacific As the largest and fastest-growing PSU market, Asia-Pacific benefits from concentrated electronics manufacturing in China, Taiwan, and South Korea. China’s DIY PC culture and esports boom have created a $2.1 billion PSU segment, while India shows the highest growth potential (18% YoY) due to increasing PC penetration. Japan maintains demand for high-reliability industrial PSUs, and Southeast Asian countries prioritize cost-effective solutions. The region faces challenges with counterfeit products but leads in OEM production, supplying 75% of global PSU units. Recent developments include GaN (Gallium Nitride) technology adoption among premium brands.

South America Market growth in South America is constrained by economic instability but shows pockets of opportunity in Brazil and Chile. The Brazilian gaming market, valued at $1.3 billion, drives demand for entry-level to mid-range PSUs. Argentina’s import restrictions have encouraged local assembly operations, though component quality remains inconsistent. A key trend is the growing second-hand PSU market, accounting for nearly 30% of transactions. Internet cafe expansions in Colombia and Peru provide steady commercial demand, while voltage stability issues necessitate robust surge protection features in consumer units.

Middle East & Africa This emerging market is bifurcated between high-end demand in GCC countries and price-sensitive segments across Africa. The UAE and Saudi Arabia show strong preference for branded 80 PLUS Gold/Platinum units, aligned with data center expansions. In contrast, African markets prioritize durability under unstable power conditions, making hybrid ATX units popular. South Africa leads in regional distribution, while North African countries see growing OEM partnerships. Challenges include counterfeit imports and low consumer awareness about efficiency ratings, though infrastructure development projects promise long-term growth.

MARKET DYNAMICS

The PSU industry continues facing significant supply chain challenges, particularly for critical components like capacitors and power ICs. Lead times for certain semiconductor components have extended to 50+ weeks, forcing manufacturers to redesign products or accept lower margins. The situation is particularly acute for high-wattage PSUs requiring premium components, with some vendors reporting 20-30% production shortfalls.

While developed markets embrace high-efficiency PSUs, price sensitivity in emerging economies continues restraining premium segment growth. In price-conscious markets, consumers often prioritize upfront cost over long-term energy savings, creating challenges for manufacturers attempting to recoup R&D investments. The situation is particularly evident in the Asian retail sector, where 80 Plus Bronze units still dominate despite wider availability of more efficient models.

The lack of universal standards for certain PSU form factors and connectors creates compatibility issues that slow market growth. While ATX has become dominant in desktop computing, specialized applications continue using proprietary formats. This fragmentation increases development costs and limits economies of scale, particularly in industrial and embedded applications where customization is frequently required.

The rapid deployment of edge computing infrastructure presents significant opportunities for PSU manufacturers specializing in ruggedized, reliable power solutions. As computing moves closer to data sources, demand grows for PSUs capable of operating in harsh environments with minimal maintenance. This market segment is particularly attractive, with projected CAGR of 18% through 2030. Leading manufacturers are already introducing new product lines featuring extended temperature ranges and enhanced protection against power fluctuations.

The incorporation of IoT connectivity and predictive maintenance capabilities into PSU designs represents a growing revenue stream. Smart PSUs capable of monitoring load conditions, predicting failures, and optimizing power delivery are gaining traction in data center and industrial applications. These advanced units typically command 50-75% premium over conventional models while delivering significant operational savings through improved reliability and energy management.