#Wireless Connectivity Technology Growth Rate

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

130K people were victims of a chain letter scam that affected Tumblr in May 2011.

Text

Wireless Connectivity Technology to Witness Significant Growth by Forecast

Wireless Connectivity Technology Market Information

The Wireless Connectivity Technology Market Report provides essential insights for business strategists, offering a comprehensive overview of industry trends and growth projections. It includes detailed historical and future data on costs, revenues, supply, and demand, where applicable. The report features an in-depth analysis of the value chain and distributor networks.

Employing various analytical techniques such as SWOT analysis, Porter’s Five Forces analysis, and feasibility studies, the report offers a thorough understanding of competitive dynamics, the risk of substitutes and new entrants, and identifies strengths, challenges, and business opportunities. This detailed assessment covers current patterns, driving factors, limitations, emerging developments, and high-growth areas, aiding stakeholders in making informed strategic decisions based on both current and future market trends. Additionally, the report includes an examination of the Automatic Rising Arm Barriers sector and its key opportunities.

According to Straits Research, the global Wireless Connectivity Technology market size was valued at USD XX Billion in 2023. It is projected to reach from USD XX Billion in 2024 to USD XX Billion by 2032, growing at a CAGR of 13.3% during the forecast period (2024–2032).

Get Free Request Sample Report @ https://straitsresearch.com/report/wireless-connectivity-technology-market/request-sample

TOP Key Industry Players of the Wireless Connectivity Technology Market

Qualcomm Incorporated

Intel Corporation

NXP Semiconductors NV.

Texas Instruments Inc.

STMicroelectronics NV.

Broadcom

Panasonic Corporation

Infineon Technologies AG

Renesas Electronics

MediaTek Inc.

Global Wireless Connectivity Technology Market: Segmentation

As a result of the Wireless Connectivity Technology market segmentation, the market is divided into sub-segments based on product type, application, as well as regional and country-level forecasts.

By Technology

Wi-Fi

Bluetooth

Zigbee

NFC

Cellular

Others

By Application

Consumer Electronics

Automotive

Healthcare

Aerospace and Defense

IT & Telecom

Others

Browse Full Report and TOC @ https://straitsresearch.com/report/wireless-connectivity-technology-market/request-sample

Reasons for Buying This Report:

Provides an analysis of the evolving competitive landscape of the Automatic Rising Arm Barriers market.

Offers analytical insights and strategic planning guidance to support informed business decisions.

Highlights key market dynamics, including drivers, restraints, emerging trends, developments, and opportunities.

Includes market estimates by region and profiles of various industry stakeholders.

Aids in understanding critical market segments.

Delivers extensive data on trends that could impact market growth.

Research Methodology:

Utilizes a robust methodology involving data triangulation with top-down and bottom-up approaches.

Validates market estimates through primary research with key stakeholders.

Estimates market size and forecasts for different segments at global, regional, and country levels using reliable published sources and stakeholder interviews.

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Address: 825 3rd Avenue, New York, NY, USA, 10022

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

#b2b#digitalmarketing#technology#trending#Wireless Connectivity Technology#Wireless Connectivity Technology Industry#Wireless Connectivity Technology Share#Wireless Connectivity Technology Size#Wireless Connectivity Technology Trends#Wireless Connectivity Technology Regional Analysis#Wireless Connectivity Technology Growth Rate

0 notes

Text

Medical Devices Market Size, Share, Growth & Research Report 2034

Medical Devices Market Size

According to Expert Market Research, the global medical devices market was valued at USD 562.60 billion in 2024. Driven by the increasing prevalence of chronic diseases, aging populations, and rapid technological innovation, the market is anticipated to expand at a compound annual growth rate (CAGR) of 6.20% during the forecast period from 2025 to 2034, reaching an estimated USD 1026.70 billion by 2034.

The demand for advanced diagnostic tools, minimally invasive surgical devices, wearable health technologies, and home-based monitoring systems is rising rapidly. Additionally, the integration of artificial intelligence, 3D printing, and IoT in healthcare is revolutionizing medical device design and functionality, enhancing patient outcomes and operational efficiency across healthcare systems worldwide.

Introduction to Medical Devices

Medical devices encompass a wide range of instruments, machines, implants, and tools used in the diagnosis, monitoring, treatment, and prevention of diseases and health conditions. These include diagnostic imaging systems, surgical instruments, orthopedic implants, cardiovascular devices, dental equipment, and wearable health trackers. With the increasing burden of non-communicable diseases such as diabetes, cardiovascular ailments, cancer, and respiratory disorders, the demand for innovative and reliable medical devices has grown significantly. In addition, healthcare digitization and patient-centric care models are further fueling the adoption of smart and connected devices across global healthcare systems.

Key Market Drivers

Rising Burden of Chronic Diseases

The surge in lifestyle-related illnesses such as diabetes, hypertension, and cardiovascular diseases is creating a consistent demand for diagnostic, therapeutic, and monitoring devices. According to WHO, non-communicable diseases account for nearly 74% of all global deaths, highlighting the urgent need for early detection and effective management tools.

Aging Global Population

The increasing geriatric population, particularly in developed and emerging economies, is a major factor contributing to the demand for medical devices. Elderly individuals are more susceptible to chronic diseases, requiring continuous care, diagnostics, and rehabilitation tools that enhance their quality of life and prolong independence.

Technological Advancements in Healthcare

The integration of cutting-edge technologies such as artificial intelligence, robotics, 3D printing, augmented reality, and smart sensors into medical devices has led to greater precision, automation, and minimally invasive procedures. These technologies are not only improving patient outcomes but also reducing hospital stays and lowering healthcare costs.

Growing Demand for Home Healthcare and Wearables

The preference for home-based care and remote patient monitoring is accelerating the adoption of portable, wearable, and wireless medical devices. Patients can now track vital signs, manage chronic diseases, and receive timely alerts without frequent hospital visits, making healthcare more accessible and personalized.

Government Initiatives and Healthcare Investments

Public and private sector investments in healthcare infrastructure, R&D, and regulatory reforms are fostering innovation and ensuring faster product approvals. National health programs, insurance coverage expansion, and the adoption of value-based care models are also encouraging the integration of advanced medical technologies into public healthcare systems.

Get a Free Sample Report and Table of Contents: Click Here

Market Segmentation

Market Breakup by Type of Device

Respiratory Devices

Nebulizers

Humidifiers

Oxygen Concentrators

Positive Airway Pressure Devices

Ventilators

Gas Analyzers

Others

Cardiology Devices

Diagnostic & Monitoring Devices

Electrocardiogram (ECG)

Remote Cardiac Monitoring Devices

Others

Therapeutic & Surgical Devices

Stents

Catheters

Grafts

Heart Valves

Others

Orthopedic Devices

Replacement Devices

Bone Fixation Devices

Orthobiologics

Braces

Others

Diagnostic Imaging Devices

X-Ray Machines

MRI Scanners

CT Scanners

Ultrasound Systems

Nuclear Imaging Devices

Others

Endoscopy Devices

Rigid Endoscopy Devices

Flexible Endoscopy Devices

Capsule Endoscopy Devices

Disposable Endoscopy Devices

Robot Assisted Endoscopy Devices

Endoscopy Visualization Component

Operative Devices

Others

Ophthalmology Devices

Optical Coherence Tomography Scanners

Fundus Cameras

Perimeters/Visual Field Analyzers

Autorefractors and Keratometers

Slit Lamps

Wavefront Aberrometers

Optical Biometry Systems

Corneal Topography Systems

Specular Microscopes

Retinoscopes

Others

Others

Market Breakup by Application

Cardiology

Oncology

Neurology

Orthopedics

Respiratory

Diabetes Care

Ophthalmology

Others

Market Breakup by End User

Hospitals

Specialty Clinics

Homecare Settings

Ambulatory Surgical Centers

Others

Market Breakup by Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Regional Insights

North America

North America dominates the global medical devices market, with the United States holding the largest share. The region benefits from advanced healthcare infrastructure, strong R&D capabilities, and a high adoption rate of innovative technologies. Increasing healthcare expenditure and favorable reimbursement policies also support market growth in the region.

Europe

Europe holds a significant position in the global market, driven by well-established public healthcare systems, aging populations, and high demand for orthopedic and cardiovascular devices. Countries like Germany, France, and the UK are actively investing in medical innovation, AI in healthcare, and digital health technologies.

Asia-Pacific

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. Factors such as rising healthcare awareness, expanding medical tourism, growing chronic disease prevalence, and favorable government policies are contributing to the rapid adoption of advanced medical technologies in countries like China, India, Japan, and South Korea.

Latin America

The Latin American medical devices market is gradually expanding, supported by improvements in healthcare access, infrastructure development, and increased government and private investments. Brazil and Mexico are among the leading countries in this region, particularly in diagnostics and surgical equipment.

Middle East and Africa

The market in the Middle East and Africa is gaining momentum due to increasing healthcare expenditure, urbanization, and the rising burden of non-communicable diseases. The UAE, Saudi Arabia, and South Africa are making significant strides in upgrading their medical infrastructure and adopting modern healthcare solutions.

Market Challenges

Despite the positive outlook, the medical devices market faces challenges such as stringent regulatory requirements, high R&D costs, product recalls, and cybersecurity risks associated with connected medical devices. Additionally, disparities in healthcare infrastructure, limited access to advanced technologies in developing regions, and lack of skilled professionals may hamper market growth.

Key Players

Medtronic plc

Johnson & Johnson Services, Inc.

Fresenius Medical Care AG & Co.

Abbott

GE HealthCare

Koninklijke Philips N.V.

Siemens Healthcare GmbH

Stryker

Cardinal Health

Baxter International, Inc.

BD

Terumo Corporation

Smiths & Nephew plc

Dentsply Sirona

F. Hoffman-La Roche Ltd.

Future Trends in the Medical Devices Market

AI-Driven and Smart Medical Devices

Artificial intelligence is transforming healthcare diagnostics, imaging, and decision-making. AI-enabled devices can interpret medical scans, predict patient deterioration, and support early diagnosis, significantly enhancing clinical accuracy and efficiency.

Remote Monitoring and Telemedicine Integration

As remote care becomes more mainstream, the development of telehealth-integrated devices is accelerating. These devices support continuous health tracking, remote consultations, and early interventions, particularly in rural and underserved areas.

3D Printing for Customized Devices

3D printing is enabling the creation of patient-specific implants, prosthetics, and surgical tools. This technology offers customization, rapid prototyping, and cost-effectiveness, especially in orthopedic and dental applications.

Wearable and Implantable Devices

Wearables like fitness bands, ECG monitors, and smart patches are gaining traction among both patients and clinicians. Implantable devices such as defibrillators, pacemakers, and glucose monitors are also evolving with wireless and data-sharing capabilities.

Focus on Minimally Invasive and Robotic Procedures

The trend toward minimally invasive surgeries is fueling demand for devices that reduce patient trauma, recovery time, and hospital stays. Robotic-assisted surgery systems are becoming increasingly popular in urology, gynecology, orthopedics, and oncology.

The global medical devices market is set for significant expansion over the next decade, driven by technological advancements, rising healthcare needs, and a growing emphasis on patient-centric care. The convergence of AI, IoT, and personalized medicine is transforming how healthcare is delivered and managed. While regulatory challenges and cost constraints remain, innovation and strategic collaborations will continue to shape the future of the medical device industry.

Frequently Asked Questions (FAQs)

What is the projected size of the medical devices market by 2034? The global medical devices market is projected to reach USD 1026.70 billion by 2034, growing at a CAGR of 6.20% from USD 562.60 billion in 2024.

Which factors are driving the growth of the medical devices market? Key growth drivers include rising chronic diseases, aging populations, technological advancements, increasing demand for home healthcare, and supportive government initiatives.

What are the latest trends in the medical devices industry? Emerging trends include AI-powered diagnostics, wearable health monitors, remote patient monitoring, 3D printing, and robotic surgical systems.

Which regions are leading the medical devices market? North America is the largest market, followed by Europe and the rapidly growing Asia-Pacific region, particularly China, India, and Japan.

Who are the key players in the global medical devices market? Major companies include Medtronic, Abbott, Siemens Healthineers, GE Healthcare, Philips, Johnson & Johnson, BD, Boston Scientific, and Stryker, among others.

Media Contact:

Company Name: Claight Corporation Email: [email protected] Toll Free Number: +1-415-325-5166 | +44-702-402-5790 Address: 30 North Gould Street, Sheridan, WY 82801, USA Website: https://www.expertmarketresearch.com

#MedicalDevicesMarket#HealthcareDevices#MedicalDeviceGrowth#MedicalDeviceIndustry#GlobalMedicalDevices#MedicalDeviceTrends#MedicalTechnologyMarket

0 notes

Text

5G Radio Frequency Front End Module Market: Emerging Applications and End-User Demand 2025-2032

MARKET INSIGHTS

The global 5G Radio Frequency Front End Module Market size was valued at US$ 4,830 million in 2024 and is projected to reach US$ 9,740 million by 2032, at a CAGR of 10.2% during the forecast period 2025-2032. This growth is fueled by rapid 5G network deployments worldwide, with China leading the charge by accounting for over 60% of global 5G base stations as of 2022.

5G Radio Frequency Front End Modules (RFFEM) are critical components in wireless communication systems that manage signal transmission and reception. These modules integrate multiple technologies including RF filters, power amplifiers, switches, and low-noise amplifiers to ensure efficient high-frequency signal processing required for 5G's enhanced mobile broadband and low-latency applications.

The market expansion is driven by three key factors: accelerating 5G infrastructure investments (global mobile operators are projected to invest USD 1.1 trillion in 5G between 2020-2025), increasing smartphone penetration with 5G capabilities (GSMA forecasts 5G will account for 51% of mobile connections by 2030), and growing demand for IoT applications. Major players like Skyworks Solutions and Qorvo are innovating with integrated module solutions to address the complex frequency bands in 5G NR deployments.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of 5G Infrastructure Deployment Accelerating Market Growth

The global push for 5G network expansion is driving unprecedented demand for RF front end modules. With telecom operators investing heavily in infrastructure upgrades, the market is witnessing exponential growth. Countries worldwide are racing to achieve nationwide 5G coverage, with China already deploying over 2.3 million 5G base stations - representing more than 60% of the global total. This infrastructure boom creates a ripple effect across the semiconductor supply chain, particularly benefiting RF front end module manufacturers. The technology's ability to handle higher frequencies and increased data throughput makes it indispensable for modern 5G networks. Recent product launches incorporating advanced packaging technologies and improved power efficiency demonstrate how manufacturers are rising to meet this demand.

Smartphone Proliferation and 5G Device Penetration Fueling Market Expansion

The smartphone industry's rapid transition to 5G-compatible devices serves as a powerful market catalyst. With global mobile users exceeding 5.4 billion, device manufacturers are under constant pressure to integrate advanced RF front end solutions that support multiple frequency bands and power modes. The average 5G smartphone now contains 30-40% more RF components than its 4G predecessor, directly translating to higher module demand. Market data reveals that 5G smartphone shipments grew by over 25% in 2023 compared to the previous year, indicating strong consumer adoption. This trend is particularly pronounced in Asia-Pacific markets where 5G adoption rates outpace other regions, creating localized demand surges for high-performance RF components.

MARKET RESTRAINTS

Complex Integration Challenges Impeding Widespread Adoption

While 5G's technological promise is undeniable, integrating RF front end modules into modern devices presents significant engineering hurdles. The need to support an expanding array of frequency bands while maintaining signal integrity and power efficiency creates complex design challenges. Module manufacturers must balance performance requirements against physical space constraints, particularly in compact mobile devices. This complexity often results in extended development cycles and higher production costs. Recent industry reports indicate that nearly 40% of 5G device failures can be traced back to RF front end integration issues, highlighting the technical barriers that continue to restrain market growth. As spectrum allocations become more fragmented globally, these integration challenges are expected to persist.

Supply Chain Vulnerabilities Creating Market Volatility

The RF front end module market remains susceptible to ongoing global supply chain disruptions. Concentrated production of specialized semiconductor components in specific geographical regions creates potential bottlenecks. Recent geopolitical tensions and trade restrictions have further exacerbated these vulnerabilities, leading to fluctuating component prices and extended lead times. The industry's reliance on advanced compound semiconductor materials like gallium arsenide and silicon germanium adds another layer of supply chain complexity, as these materials require specialized manufacturing processes. Such constraints have caused intermittent shortages, prompting some manufacturers to maintain elevated inventory levels despite the associated cost burdens.

MARKET OPPORTUNITIES

Emerging mmWave Applications Opening New Revenue Streams

The gradual rollout of millimeter wave (mmWave) 5G networks presents significant growth opportunities for advanced RF front end module developers. While current deployments primarily utilize sub-6GHz spectrum, the transition to higher frequency bands necessitates specialized components capable of handling extreme bandwidth requirements. Early movers in mmWave-optimized module development are positioning themselves to capture premium market segments. Industry projections suggest that mmWave-compatible RF front end modules will command price premiums of 35-50% over conventional solutions, representing a high-value market niche. The automotive sector's growing interest in 5G-enabled vehicle-to-everything (V2X) communication systems further amplifies this opportunity, creating parallel demand across multiple industries.

Integration of AI and Machine Learning Creating Competitive Differentiation

Forward-thinking manufacturers are leveraging artificial intelligence to create next-generation intelligent RF front end solutions. Machine learning algorithms are being employed to optimize power consumption, dynamically adjust signal parameters, and predict component failures before they occur. Several industry leaders have already announced products featuring embedded AI capabilities, with early adopters reporting performance improvements of 15-20% in real-world conditions. This technological evolution is particularly valuable for power-sensitive applications like IoT devices and wearables, where energy efficiency directly impacts product viability. As these intelligent systems mature, they're expected to redefine performance benchmarks across the entire RF front end module market.

MARKET CHALLENGES

Technical Complexity and Power Consumption Issues

The increasing technical complexity of 5G RF front end modules presents ongoing development challenges. Supporting the growing number of frequency bands while maintaining power efficiency requires innovative architectural approaches. Current modules must handle more than 20 different bands, with each addition introducing new interference and thermal management concerns. Power consumption remains a critical pain point, particularly for battery-operated devices, where RF components can account for up to 40% of total energy usage. Recent field tests show that thermal issues cause approximately 15% of premature module failures, underscoring the need for improved thermal design methodologies. These technical hurdles require substantial R&D investments, creating barriers to entry for smaller market players.

Rapid Technology Obsolescence Pressuring Profit Margins

The breakneck pace of 5G standard evolution creates significant challenges for RF front end module manufacturers. Frequent specification updates and new feature requirements often render existing product designs obsolete within 12-18 months. This rapid technology turnover forces companies to maintain aggressive development cycles while managing product lifecycle risks. The resulting pressure on profit margins is particularly acute for manufacturers serving price-sensitive consumer electronics markets. Industry analysis indicates that average selling prices for mainstream RF front end modules have declined by approximately 8% annually since 2021, despite increasing technical complexity. This trend is forcing market participants to seek alternative revenue streams through value-added services and customized solutions.

5G RADIO FREQUENCY FRONT END MODULE MARKET TRENDS

Expansion of 5G Infrastructure Driving RF Front-End Module Demand

The global rollout of 5G networks is accelerating the demand for Radio Frequency (RF) Front-End Modules (FEMs), which are critical components in 5G-enabled devices. As telecom operators worldwide invest heavily in infrastructure deployment, the market for RF FEMs is projected to grow at a CAGR of over 10% through 2032, reaching multimillion-dollar valuations. China currently leads in 5G infrastructure, accounting for more than 60% of global 5G base stations—highlighting the immense demand for high-performance RF components. Furthermore, innovations in 5G mmWave and sub-6GHz technologies necessitate advanced FEMs with superior power efficiency and signal integrity.

Other Trends

Miniaturization and Integration of RF Components

The push toward smaller, more efficient devices has led to significant advancements in RF front-end module designs. System-on-Chip (SoC) and heterogeneous integration techniques are enabling manufacturers to combine multiple components—such as filters, switches, and power amplifiers—into compact modules. This trend is particularly crucial for smartphones and IoT devices, where space constraints demand high integration densities. Recent developments in RF SOI (Silicon-on-Insulator) and GaN (Gallium Nitride) technologies are further enhancing performance while reducing power consumption, making them increasingly preferred in both consumer and military applications.

Increasing Demand Across Military and Civil Applications

The adoption of 5G FEMs is expanding rapidly across both military and civil sectors. In defense applications, 5G-enabled communication systems rely on ruggedized RF FEMs to support secure, high-bandwidth transmissions for unmanned systems and battlefield networks. Meanwhile, in civilian applications, the proliferation of 5G smartphones, smart cities, and industrial IoT is fueling demand. Commercial shipments of 5G smartphones surpassed 700 million units in 2023, reinforcing the need for high-quality RF front-end solutions. Additionally, advancements in AI-driven RF optimization are helping manufacturers tailor modules for specific use cases, further driving market diversification.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Collaborations Drive Market Competition

The global 5G Radio Frequency Front End Module (RFFEM) market is characterized by intense competition among semiconductor giants, with Skyworks Solutions and Broadcom emerging as dominant players. These companies collectively held over 35% market share in 2024, owing to their comprehensive product portfolios spanning RF filters, power amplifiers, and switches. Their technological leadership in millimeter-wave and sub-6GHz solutions positions them strongly as 5G deployment accelerates worldwide.

Murata Manufacturing and Qorvo have demonstrated remarkable growth, particularly in the Asia-Pacific region where 5G infrastructure investments are surging. Murata's advanced filtering technologies and Qorvo's integrated front-end modules have become critical components for smartphone OEMs and base station manufacturers. Both companies are investing heavily in BAW (Bulk Acoustic Wave) filter development to address the complex frequency requirements of 5G networks.

The competitive landscape is further intensified by strategic maneuvers from Qualcomm and Taiwan Semiconductor Manufacturing Company (TSMC). Qualcomm's system-level expertise in 5G modem-RF integration gives it a unique advantage in smartphone applications, while TSMC's cutting-edge wafer fabrication processes enable superior performance in high-frequency modules. Recent industry reports indicate these companies are allocating 18-22% of their R&D budgets specifically toward 5G RF innovations.

Meanwhile, NXP Semiconductors and Analog Devices are strengthening their positions through targeted acquisitions and partnerships. NXP's 2023 collaboration with a major Chinese telecom equipment provider and Analog Devices' acquisition of a specialist RF assets underscore the industry's consolidation trend. These moves enable faster time-to-market for next-generation solutions while addressing the growing demand for energy-efficient RF components.

List of Key 5G RFFEM Companies Profiled

Skyworks Solutions, Inc. (U.S.)

Broadcom Inc. (U.S.)

Murata Manufacturing Co., Ltd. (Japan)

Qorvo, Inc. (U.S.)

Qualcomm Technologies, Inc. (U.S.)

Taiwan Semiconductor Manufacturing Company (Taiwan)

NXP Semiconductors N.V. (Netherlands)

Analog Devices, Inc. (U.S.)

Texas Instruments Incorporated (U.S.)

STMicroelectronics N.V. (Switzerland)

Infineon Technologies AG (Germany)

MACOM Technology Solutions (U.S.)

Segment Analysis:

By Type

RF Filter Segment Leads Due to Its Critical Role in 5G Signal Processing

The market is segmented based on type into:

RF Filter

Subtypes: SAW, BAW, and others

RF Switch

Power Amplifier

Subtypes: GaN-based, Si-based, and others

Duplexer

Low-Noise Amplifier

Others

By Application

Civil Applications Dominate Owing to Widespread 5G Infrastructure Deployment

The market is segmented based on application into:

Military

Civil

Subtypes: Smartphones, IoT devices, and others

By Frequency Band

Sub-6 GHz Segment Holds Major Share Due to Broader Network Coverage

The market is segmented based on frequency band into:

Sub-6 GHz

mmWave

By Component Integration

Integrated Modules Gain Traction for Space-Constrained Devices

The market is segmented based on component integration into:

Discrete Components

Integrated Modules

Regional Analysis: 5G Radio Frequency Front End Module Market

North America North America represents a highly advanced market for 5G RF front-end modules, driven by substantial investments in next-generation infrastructure and the presence of leading semiconductor manufacturers. The U.S. accounts for over 65% of regional demand, fueled by early 5G deployment initiatives like the FCC’s $20.4 billion Rural Digital Opportunity Fund. Carrier aggregation technologies and mmWave spectrum utilization are pushing innovation in power amplifiers and antenna tuners. However, geopolitical tensions affecting semiconductor supply chains and complex spectrum allocation policies create moderate adoption barriers. Key players like Skyworks Solutions and Qorvo dominate component supply with specialized solutions for high-frequency bands.

Europe European adoption focuses on sub-6GHz deployments with strong emphasis on energy-efficient designs to align with the EU Green Deal initiative. Germany and the UK lead installations, collectively hosting 38% of regional 5G base stations. The presence of NXP Semiconductors and STMicroelectronics supports localized production of RF filters and switches. Strict radio equipment directives (RED) mandate rigorous certification processes, slowing time-to-market but ensuring quality standardization. Recent collaborations between telecom operators and automotive manufacturers are creating new application avenues for integrated RF modules in connected vehicles and smart city infrastructure.

Asia-Pacific China's dominance in 5G infrastructure is reshaping global RF front-end module dynamics, with domestic suppliers like Murata Manufacturing capturing 28% of the regional market share. The country's 2.3 million active 5G base stations generate unparalleled demand for power amplifiers and duplexers. India emerges as the fastest-growing market (projected 42% CAGR through 2030), driven by ₹14,000 crore (∼$1.7 billion) government allocations for indigenous 5G development. Southeast Asia shows divergent trends - while Singapore adopts cutting-edge mmWave solutions, Indonesia and Vietnam prioritize cost-effective sub-6GHz modules for broader population coverage.

South America Brazil constitutes 60% of regional demand, with major carriers deploying 5G NSA networks across 26 state capitals. However, economic instability limits investment in advanced RF components, causing reliance on mid-tier Chinese imports. Argentina and Chile show promising pilot projects in industrial IoT applications, requiring ruggedized front-end solutions. The lack of local semiconductor fabrication facilities creates complete import dependency, with average lead times exceeding 12 weeks during peak demand cycles. Recent trade agreements with Asian manufacturers aim to stabilize supply but face bureaucratic hurdles in customs clearance.

Middle East & Africa Gulf Cooperation Council nations drive premium segment growth through extensive smart city projects - Dubai's 5G network already covers 95% of urban areas using advanced massive MIMO configurations. In contrast, Sub-Saharan Africa experiences slower uptake due to 4G/LTE prioritization, with South Africa being the notable exception having allocated 5G spectrum to three major operators. The region faces unique challenges including extreme temperature operation requirements and limited technical expertise for mmWave deployment. Emerging partnerships between infrastructure providers and module manufacturers aim to address these constraints through customized thermal management solutions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional 5G Radio Frequency Front End Module markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global 5G RF Front End Module market was valued at USD 5.2 billion in 2024 and is projected to reach USD 12.8 billion by 2032, growing at a CAGR of 11.7% during the forecast period.

Segmentation Analysis: Detailed breakdown by product type (RF Filters, RF Switches, Power Amplifiers, etc.), technology (sub-6GHz, mmWave), application (military, civil), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific (China dominates with over 60% global 5G base stations), Latin America, and Middle East & Africa.

Competitive Landscape: Profiles of 16 leading market participants including Skyworks Solutions, Qorvo, Broadcom, and Murata Manufacturing, covering their product portfolios, R&D investments, and strategic partnerships.

Technology Trends: Assessment of emerging innovations including AI-integrated RF modules, advanced packaging techniques, and energy-efficient designs for 5G networks.

Market Drivers & Restraints: Evaluation of growth drivers (5G infrastructure expansion, IoT proliferation) and challenges (semiconductor shortages, design complexity).

Stakeholder Analysis: Strategic insights for component suppliers, telecom operators, device manufacturers, and investors navigating the 5G ecosystem.

The research methodology combines primary interviews with industry leaders and analysis of verified market data from regulatory filings, trade associations, and financial reports to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 5G RF Front End Module Market?

-> 5G Radio Frequency Front End Module Market size was valued at US$ 4,830 million in 2024 and is projected to reach US$ 9,740 million by 2032, at a CAGR of 10.2% during the forecast period 2025-2032.

Which companies lead the 5G RF Front End Module Market?

-> Top players include Skyworks Solutions, Qorvo, Broadcom, Murata Manufacturing, and Qualcomm, collectively holding 68% market share.

What drives market growth?

-> Key drivers are 5G network deployments (2.31M+ base stations in China alone), smartphone upgrades, and IoT expansion.

Which region dominates 5G RF module adoption?

-> Asia-Pacific leads with 72% market share, driven by China's 561 million 5G users and massive infrastructure investments.

What are emerging technology trends?

-> Emerging trends include integrated mmWave modules, GaN-based power amplifiers, and AI-optimized RF designs for 5G-Advanced networks.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/automotive-magnetic-sensor-ics-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ellipsometry-market-supply-chain.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/online-moisture-sensor-market-end-user.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/computer-screen-market-forecasting.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/high-power-gate-drive-interface.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/strobe-overdrive-digital-controller.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/picmg-half-size-single-board-computer.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/automotive-isolated-amplifier-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/satellite-messenger-market-regional.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/sic-epi-wafer-market-innovations.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/heavy-duty-resistor-market-key-players.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/robotic-collision-sensor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/gas-purity-analyzer-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/x-ray-high-voltage-power-supply-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/reflection-probe-market-industry-trends.html

0 notes

Text

Global Base Transceiver Station (BTS) Market Watch 2025: Fastest Growing Segments

Global Base Transceiver Station (BTS) Market was valued at USD X.X Billion in 2024 and is projected to reach USD X.X Billion by 2032, growing at a CAGR of X.X% from 2026 to 2032. What are the potential factors contributing to the growth of the global Base Transceiver Station (BTS) market? The global BTS market is witnessing notable expansion due to increasing mobile data traffic and widespread smartphone adoption. Rapid urbanization and expanding population densities have driven the need for enhanced cellular coverage, directly boosting BTS installations. Additionally, government initiatives supporting digital infrastructure and smart city development fuel market demand. The rollout of advanced technologies such as 4G, 5G, and IoT connectivity continues to increase the need for reliable and scalable wireless communication systems, where BTS plays a key role. Rural connectivity programs and emerging economies upgrading their telecom infrastructure further promote BTS market growth. Moreover, the surge in demand for high-speed internet, video streaming, and online services creates a robust need for network capacity expansion. Technological advancements in compact, energy-efficient, and cost-effective BTS hardware are also encouraging their rapid deployment across various regions. These developments collectively push the market forward by ensuring both reach and reliability in communication networks. Get | Download Sample Copy with TOC, Graphs & List of Figures @ https://www.verifiedmarketresearch.com/download-sample/?rid=437880&utm_source=PR-News&utm_medium=205 The competitive landscape of a market explains strategies incorporated by key players of the Global Base Transceiver Station (BTS) Market. Key developments and shifts in management in recent years by players have been explained through company profiling. This helps readers to understand the trends that will accelerate the growth of the Global Base Transceiver Station (BTS) Market. It also includes investment strategies, marketing strategies, and product development plans adopted by major players of the Global Base Transceiver Station (BTS) Market. The market forecast will help readers make better investments. The report covers extensive analysis of the key market players in the market, along with their business overview, expansion plans, and strategies. The key players studied in the report include: Key Player 1 Key Player 2 Key Player 3 Key Player 4 Key Player 5 Key Player 6 Key Player 7 Key Player 8 Key Player 9 Key Player 10 Global Base Transceiver Station (BTS) Market Segmentation Global Base Transceiver Station •BTS Market Size By Technology By Component By End-User• By Geography • North America• Europe• Asia Pacific• Latin America• Middle East and Africa The comprehensive segmental analysis offered in the report digs deep into important types and application segments of the Global Base Transceiver Station (BTS) Market. It shows how leading segments are attracting growth in the Global Base Transceiver Station (BTS) Market. Moreover, it includes accurate estimations of the market share, CAGR, and market size of all segments studied in the report. Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount/?rid=437880&utm_source=PR-News&utm_medium=205 The regional segmentation study is one of the best offerings of the report that explains why some regions are taking the lead in the Global Base Transceiver Station (BTS) Market while others are making a low contribution to the global market growth. Each regional market is comprehensively researched in the report with accurate predictions about its future growth potential, market share, market size, and market growth rate. Geographic Segment Covered in the Report: • North America (USA and Canada) • Europe (UK, Germany, France and the rest of Europe) • Asia Pacific (China, Japan, India, and the rest of the Asia Pacific region) • Latin America (Brazil, Mexico, and the rest of Latin America) • Middle East and Africa (GCC and rest of the Middle East and Africa)

Key questions answered in the report: • What is the growth potential of the Global Base Transceiver Station (BTS) Market? • Which product segment will take the lion's share? • Which regional market will emerge as a pioneer in the years to come? • Which application segment will experience strong growth? • What growth opportunities might arise in the Welding industry in the years to come? • What are the most significant challenges that the Global Base Transceiver Station (BTS) Market could face in the future? • Who are the leading companies on the Global Base Transceiver Station (BTS) Market? • What are the main trends that are positively impacting the growth of the market? • What growth strategies are the players considering to stay in the Global Base Transceiver Station (BTS) Market? For More Information or Query or Customization Before Buying, Visit @ https://www.verifiedmarketresearch.com/product/base-transceiver-station-bts-market/ Detailed TOC of Global Global Base Transceiver Station (BTS) Market Research Report, 2023-2030 1. Introduction of the Global Base Transceiver Station (BTS) Market Overview of the Market Scope of Report Assumptions 2. Executive Summary 3. Research Methodology of Verified Market Research Data Mining Validation Primary Interviews List of Data Sources 4. Global Base Transceiver Station (BTS) Market Outlook Overview Market Dynamics Drivers Restraints Opportunities Porters Five Force Model Value Chain Analysis 5. Global Base Transceiver Station (BTS) Market, By Product 6. Global Base Transceiver Station (BTS) Market, By Application 7. Global Base Transceiver Station (BTS) Market, By Geography North America Europe Asia Pacific Rest of the World 8. Global Base Transceiver Station (BTS) Market Competitive Landscape Overview Company Market Ranking Key Development Strategies 9. Company Profiles 10. Appendix About Us: Verified Market Research® Verified Market Research® is a leading Global Research and Consulting firm that has been providing advanced analytical research solutions, custom consulting and in-depth data analysis for 10+ years to individuals and companies alike that are looking for accurate, reliable and up to date research data and technical consulting. We offer insights into strategic and growth analyses, Data necessary to achieve corporate goals and help make critical revenue decisions. Our research studies help our clients make superior data-driven decisions, understand market forecast, capitalize on future opportunities and optimize efficiency by working as their partner to deliver accurate and valuable information. The industries we cover span over a large spectrum including Technology, Chemicals, Manufacturing, Energy, Food and Beverages, Automotive, Robotics, Packaging, Construction, Mining & Gas. Etc. We, at Verified Market Research, assist in understanding holistic market indicating factors and most current and future market trends. Our analysts, with their high expertise in data gathering and governance, utilize industry techniques to collate and examine data at all stages. They are trained to combine modern data collection techniques, superior research methodology, subject expertise and years of collective experience to produce informative and accurate research. Having serviced over 5000+ clients, we have provided reliable market research services to more than 100 Global Fortune 500 companies such as Amazon, Dell, IBM, Shell, Exxon Mobil, General Electric, Siemens, Microsoft, Sony and Hitachi. We have co-consulted with some of the world’s leading consulting firms like McKinsey & Company, Boston Consulting Group, Bain and Company for custom research and consulting projects for businesses worldwide. Contact us: Mr. Edwyne Fernandes Verified Market Research® US: +1 (650)-781-4080UK: +44 (753)-715-0008APAC: +61 (488)-85-9400US Toll-Free: +1 (800)-782-1768 Email: [email protected] Website:- https://www.verifiedmarketresearch.com/ Top Trending Reports https://www.verifiedmarketresearch.com/ko/product/germany-video-surveillance-market/

https://www.verifiedmarketresearch.com/ko/product/south-africa-oral-antidiabetic-drug-market/ https://www.verifiedmarketresearch.com/ko/product/hong-kong-capital-market/ https://www.verifiedmarketresearch.com/ko/product/hong-kong-credit-cards-market/ https://www.verifiedmarketresearch.com/ko/product/spain-light-commercial-vehicles-market/

0 notes

Text

Electric Vehicle Battery Connector Market

Powering the Future: Electric Vehicle Battery Connector Market Surges with High-Performance Demand Electric Vehicle Battery Connector Market

As the world accelerates toward a clean energy future, electric vehicles (EVs) have taken center stage—and behind their smooth operation lies an often-overlooked component: the battery connector. The Electric Vehicle Battery Connector Market was valued at US$ 599.24 million in 2024, and is forecast to grow at a remarkable CAGR of 19.50% from 2025 to 2032. This exponential growth is being fueled by rising EV adoption, technological innovations in fast charging, and the race for superior energy efficiency.

What Is an EV Battery Connector?

An Electric Vehicle Battery Connector is a vital component that enables the secure and efficient transmission of electrical energy between the EV battery pack and its related systems—including onboard chargers, motors, and external charging stations. These connectors are responsible for:

Enabling fast charging and discharging cycles

Ensuring thermal stability and electrical safety

Withstanding vibrations, moisture, and extreme temperatures

Supporting high-voltage and high-current applications across different EV platforms

From everyday commuter EVs to commercial electric trucks, battery connectors are essential in managing the dynamic power demands of modern e-mobility.

What’s Driving Market Growth?

1. Surging Electric Vehicle Adoption

Governments worldwide are pushing aggressive zero-emission vehicle policies, offering subsidies, tax incentives, and infrastructure investments. Automakers are rolling out dozens of EV models across all price segments. As a result, the need for reliable battery connectors—capable of handling larger energy flows and fast charging—has increased sharply.

2. Innovation in Charging Technology

The emergence of ultra-fast DC charging, bidirectional charging (V2G), and wireless charging has heightened the technical demands placed on battery connectors. Next-generation EV connectors must support high-voltage systems (400V to 800V and beyond), requiring innovation in contact materials, insulation, and connector geometry.

3. Advances in Battery Architecture

As EV batteries shift toward modular and pack-level designs such as cell-to-pack (CTP) and cell-to-chassis (CTC), the need for flexible, high-durability connectors has risen. These architectures depend on precise interconnectivity to reduce weight and enhance thermal management, creating opportunities for specialized connector manufacturers.

4. Focus on Safety and Standardization

Battery connectors must meet strict safety regulations related to short-circuit prevention, EMI shielding, and IP-rated sealing. Global standards for EV connectors, such as CCS (Combined Charging System) and CHAdeMO, require manufacturers to align designs with industry interoperability protocols—promoting uniformity and mass-market scalability.

Key Market Trends

Miniaturization and Lightweighting: OEMs are demanding compact, low-profile connectors that save space and reduce vehicle weight without sacrificing current-carrying capability.

Increased Use of Composite Materials: Materials like high-performance thermoplastics and silver-plated copper alloys are being used for better conductivity, heat resistance, and durability.

Smart Connectors: Equipped with sensors to monitor temperature, voltage, and current in real-time, enhancing battery management system (BMS) performance.

Modular Design: Enables compatibility across multiple EV models and simplifies assembly, repair, or upgrades.

Competitive Landscape

The Electric Vehicle Battery Connector Market is witnessing intense innovation and strategic partnerships as global players race to secure their positions in the EV supply chain. The competition is centered around product reliability, customization, and compliance with evolving industry standards.

Leading Market Players:

TE Connectivity Ltd.: A global leader offering high-voltage connectors designed for EVs, with a focus on thermal management and compact design.

Tesla: Not just a leading EV manufacturer, Tesla develops proprietary battery connector solutions for its advanced powertrains and Supercharger network.

Aptiv PLC: Supplies a range of high-voltage connectors and wiring harnesses for EVs, with emphasis on modularity and safety.

Siemens AG: Through its eMobility division, Siemens develops power distribution and connector systems supporting electric vehicle infrastructure.

HUBER+SUHNER: Known for high-voltage and high-power connectors tailored for EV charging stations and battery packs.

Amphenol: Offers a broad portfolio of rugged, sealed connectors suitable for electric drivetrains and energy storage systems.

Bosch: Supplies complete electric powertrain solutions, including standardized connector platforms for hybrid and fully electric vehicles.

These companies are actively involved in co-developing technologies with OEMs, forming supply agreements, and expanding production capacities to meet surging global demand.

Regional Outlook

Asia-Pacific: The dominant region in EV manufacturing, especially China, is home to top battery and connector manufacturers. Strong government EV mandates and fast infrastructure rollout make this a high-growth market.

Europe: Driven by stringent emission norms, incentives, and a shift toward zero-emission zones in major cities. Germany and Nordic countries are front-runners in EV adoption and connector innovation.

North America: The U.S. EV market, led by Tesla and supported by the Biden administration’s infrastructure investments, is witnessing rising demand for next-gen connectors and charging solutions.

Latin America & Middle East: Emerging EV markets are slowly integrating advanced battery connectors as part of their urban mobility and sustainability goals.

As the EV ecosystem becomes more complex and demanding, the humble battery connector is proving to be a linchpin in ensuring safety, efficiency, and performance. Whether it's extending range, reducing charging time, or future-proofing against evolving battery tech, the Electric Vehicle Battery Connector Market is poised to play a pivotal role in shaping tomorrow’s electrified transport networks.

Browse more Report:

Electrolysis Merchant Hydrogen Generation Market

Electroluminescent Displays Market

Driver Drowsiness Monitoring System Market

Deep Packet Inspection & Processing Market

Commercial Vehicle Remote Diagnostics Market

0 notes

Text

Point of Sales (PoS) Printers Market Sees Growth Fueled by Retail Digitization and Automation Trends

In today's world, point‑of‑sale (PoS) and receipt printing remain foundational to retail, hospitality, healthcare, and various service industries. Though it may seem like a mature segment, the point of sales (PoS) printers market is undergoing transformation, driven by rapid shifts in technology, buying behavior, and regulatory trends. Let us unpack the current scenario, major players, market drivers, key challenges, and where the future is headed.

Market Size & Growth

From 2019 to 2023, the global PoS printer market posted a robust compound annual growth rate (CAGR) of approximately 12.3%, increasing in value from USD 7.7 billion in 2019 to about USD 12.65 billion in 2023. Looking ahead, projections indicate continued momentum: Credence Research estimates an expansion from USD 14.3 billion in 2024 to USD 39.5 billion by 2032 (CAGR ~13.5 %), while DataHorizzon anticipates growth from USD 3.53 billion in 2024 to USD 6.06 billion by 2033 at a CAGR of 6.2 %. Despite differences in market definitions and scopes, consensus remains strong: significant growth is forecast across the next decade.

Key Drivers Fueling Expansion

Retail, Hospitality & Healthcare Growth The explosion of organized retail, quick-service eateries, pharmacies, and clinics drives demand for fast, accurate printing. Retailers in North America report over 70% deployment of thermal PoS printers, while approximately 35% of foodservice businesses have adopted mobile printing units. Meanwhile, thermal printing dominates with a 70 %+ market share across applications .

Rise of Mobile & Wireless Printing A shift toward mobile PoS (mPoS) printers especially Bluetooth- and Wi‑Fi-enabled devices is visible across restaurants, pop-ups, and remote retail setups. The emergence of compact, battery-powered printers enables on-the-spot billing and improved customer engagement.

Cloud Integration & IoT Connectivity Cloud-based printing and printer management enabling centralized firmware updates, real-time analytics, and remote configuration have become integral. Over 30% of printer installations support cloud integration; approximately 45% now include Bluetooth connectivity.

Sustainability & Regulatory Pressures Eco-conscious firms are opting for energy-efficient printers built from recycled plastics, along with innovations in recyclable thermal papers. Government regulations such as EU circular economy initiatives are pushing the industry in a greener direction .

Digital Payments & E‑Receipts Rising adoption of contactless and digital transactions demands printers compatible with QR codes, NFC, and durable barcode technologies. Many devices are now tailored for digital and e‑receipt generation.

Market Segmentation & Regional Highlights

SegmentHighlights, By TechnologyThermal printers dominate (>70% global share) with fast, maintenance-free operation. Impact and inkjet units persist primarily in niche sectors. |By Form FactorDesktop printers are widely used in fixed POS systems, while mobile and wireless models grow rapidly in foodservice and event environments. By End‑User IndustryRetail (~45%) leads in adoption, followed by hospitality, healthcare, and ticketing. The healthcare segment is also seeing increased uptake.

Regional Insights:

Asia-Pacific is the fastest-growing region, fueled by urbanization, economic rise in China and India, and government pushes for digital payments. Asia accounts for ~20–25% of the market, with projected CAGRs of 7–8 %.

North America, the most mature market, holds about 30–38 % share, led by strong uptake of advanced desktop and mobile printers.

Europe accounts for ~28 % share, with growth driven by retail and hospitality, sustainability mandates, and fiscal regulations .

Latin America and MEA are smaller but growing markets (~6–10 % combined share), with high adoption among pharmacies, retail chains, and new hospitality ventures.

Competitive Landscape

The market remains competitive and fragmented:

Tier‑1 players: Epson, Star Micronics, Zebra, Bixolon, Citizen lead global market share (roughly 55–60%), thanks to strong R&D and product diversification.

Tier‑2 vendors: Brother, Dymo, TSC offer specialized, industry-specific printers.

Tier‑3 and regional niche players cater to small businesses with cost-effective solutions, often undercutting on price but offering local service and customization .

Market activity is intensifying with frequent tech-led launches (e.g., Epson's eco‑printers, HP’s cloud‑ready models) and partnerships with software providers. Industry consolidation is also underway, as bigger companies absorb innovative startups to enhance portfolios.

Challenges & Restraints

High setup and upkeep costs: Initial investments, consumables (paper), and repairs pose challenges particularly for SMEs.

Digital shift to paperless receipts: As digital alternatives gain traction, demand for printed receipts may decline in developed economies.

Compatibility and system integration: Legacy systems and disparate platforms may restrict adoption of modern printers.

Security concerns: Printers in transactional environments must maintain high standards of data protection to meet regulatory requirements.

Future Outlook & Opportunities

IoT and AI integration: Cloud connectivity, remote firmware updates, predictive maintenance, and analytics-powered printers will shape next-gen PoS ecosystems.

Next‑gen compact and multifunction printers: Devices that combine printing, scanning, and payment acceptance reduce counter clutter and enhance scalability.

Customized receipts as marketing tools: QR codes, brand messaging, coupons printed directly on receipts offer monetization and loyalty-building opportunities.

Growth in emerging markets: Untapped retail and hospitality sectors in Africa, Southeast Asia, and Latin America present significant expansion potential.

Health‑sector innovation: Increasing adoption of PoS printers for patient IDs, labels, prescriptions, and secure transactional printouts.

Conclusion

The PoS printer market is far from static. Bolstered by strong demand in key verticals, rapid technological innovation, and rising adoption in emerging economies, it’s set for sustained, double-digit expansion. Thermal printers maintain dominance, but on-the-go mobile and IoT-enabled devices are emerging as vital tools. Manufacturers addressing cost, eco‑friendliness, AI, and system integration will flourish in the next wave. For businesses, aligning investments with mobility, cloud connectivity, and sustainability will define competitive advantage in tomorrow’s retail and service landscapes.

0 notes

Text

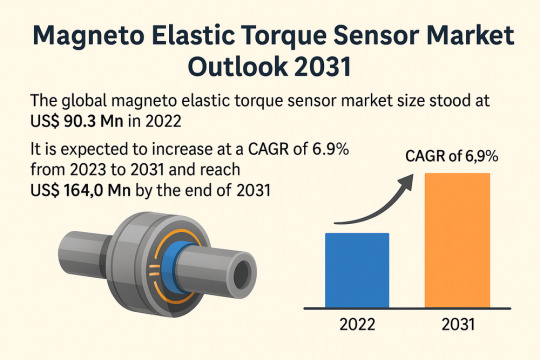

Global Magneto Elastic Torque Sensor Market Set for 6.9% CAGR Surge Through 2031

The global Magneto Elastic Torque Sensor Market is poised for substantial expansion, projected to grow from USD 90.3 Mn in 2022 to USD 164.0 Mn by the end of 2031, advancing at a compound annual growth rate (CAGR) of 6.9% during the forecast period from 2023 to 2031. Increasing demand for accurate torque measurement in electric mobility, robotics, and smart industrial applications is expected to drive this growth trajectory.

Market Overview: Magneto elastic torque sensors are critical in measuring the torque or twisting force on rotating components like shafts, motors, and gearboxes. Their non-contact operation, high accuracy, and compact design make them ideal for applications across automotive, aerospace, industrial automation, healthcare, and research sectors.

These sensors work on the principle of measuring strain-induced changes in magnetic permeability. Their versatility, long-term reliability, and digital compatibility have rendered them indispensable in environments requiring precise motion control and performance optimization.

Market Drivers & Trends

The rapid shift toward electric and hybrid vehicles and the expansion of automated industrial systems are among the primary factors accelerating magneto elastic torque sensor market growth. Torque sensors play a crucial role in managing and improving the performance of EV drivetrains, offering precise torque feedback for real-time adjustments and efficiency gains.

Moreover, stringent emission regulations are driving the adoption of torque sensors in combustion and hybrid engines to improve fuel efficiency and reduce CO₂ output. The trend toward smart factories, powered by Industry 4.0 technologies, has further amplified demand for compact and wireless torque sensors that support predictive maintenance and remote diagnostics.

Latest Market Trends

Recent trends shaping the market include:

Miniaturization of sensors to fit confined spaces, particularly in aerospace and automotive applications.

Wireless and non-contact torque sensors gaining traction for their ease of integration and lower maintenance needs.

Integration with IoT platforms, enabling real-time data acquisition and torque analysis for smart manufacturing systems.

Growing use of torque sensors in wind energy systems and medical devices for enhanced operational safety and efficiency.

Key Players and Industry Leaders

The global magneto elastic torque sensor market is consolidated, with a few prominent players commanding a significant share. These companies are continuously investing in R&D, product innovation, and strategic collaborations to expand their global footprint. Key players include:

ABB Ltd.

Applied Measurements Ltd.

Crane Electronics Ltd.

Honeywell Sensing and Control

HITEC Sensor Developments, Inc.

Kistler Instrumente Ltd.

MagCanica

Methode Electronics

Texas Instruments, Inc.

Recent Developments

Several noteworthy developments have taken place in the industry:

April 2021: Datum Electronics Ltd. partnered with Nautils Labs to provide predictive decision support and vessel digitalization for the maritime industry.

November 2020: HBM launched the T40CB torque transducer, optimized for confined automotive testing environments, featuring digital and analog interfaces.

May 2020: Kistler Holding collaborated with Vehico for advanced vehicle testing systems.

April 2020: Infineon Technologies AG completed the acquisition of Cypress Semiconductor Corporation to strengthen its capabilities in connectivity and embedded systems.

These strategic moves highlight a growing focus on digital transformation, expanded sensor functionalities, and diversified application scopes.

Examine key highlights and takeaways from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=24872

Market Opportunities

Opportunities abound in this market, especially in sectors embracing digitalization and green technologies:

E-mobility boom: The global push for electric vehicles opens new avenues for torque sensor integration in EV drivetrains and battery monitoring systems.

Industrial automation: With Industry 4.0 adoption on the rise, torque sensors are critical in machine learning environments for real-time diagnostics.

Healthcare sector: Miniaturized sensors are increasingly being deployed in prosthetics, surgical robotics, and precision instruments.

Renewable energy: Torque measurement is vital in optimizing wind turbines and hydroelectric systems for efficient energy conversion.

The emergence of smart torque sensing solutions integrated with AI and machine learning is expected to unlock new potential in process optimization and equipment lifecycle management.

Future Outlook

The magneto elastic torque sensor market is on a stable growth trajectory, bolstered by macroeconomic trends in clean energy, smart manufacturing, and digital healthcare. As industries demand higher levels of precision, real-time monitoring, and system intelligence, the role of advanced torque sensing will become even more critical.

Future innovation is likely to focus on:

Multi-sensor integration for simultaneous measurement of torque, temperature, and pressure.

AI-powered predictive analytics for preventive maintenance.

Cloud-based torque monitoring systems for remote asset management.

By 2031, the market is expected to be characterized by smarter, more compact, and interoperable torque sensing solutions with applications across emerging and established economies.

Market Segmentation

The magneto elastic torque sensor market is segmented as follows:

By Application:

Automotive: Dominant application, particularly in EVs and hybrid powertrains.

Aerospace & Defense: For load monitoring and structural testing.

Research and Development: Academic and industrial torque testing.

Industrial: Robotics, automation, machine tools.

Others: Healthcare devices, renewable energy systems.

By Region:

Asia Pacific: Leading the market with significant contributions from China, Japan, South Korea, and India. The region benefits from a strong automotive base and growing EV adoption.

North America: High technology integration in manufacturing and defense sectors.

Europe: Home to key automotive and industrial automation players.

Rest of World: Emerging opportunities in South America and the Middle East driven by industrial digitization.

Regional Insights

Asia Pacific dominated the global market in 2022 and is projected to maintain its lead throughout the forecast period. The region’s growth is propelled by:

High production and export volume of electric and hybrid vehicles.

Strong governmental support for industrial automation and emission control.

Advancements in manufacturing technologies in countries such as China, Japan, and India.

Other regions such as North America and Europe are also witnessing steady growth due to their robust R&D infrastructure, early adoption of IoT technologies, and stringent safety standards in automotive and industrial systems.

Why Buy This Report?

This report provides:

A comprehensive overview of market dynamics including drivers, restraints, and opportunities.

In-depth segmentation by application and region, with detailed analysis.

Competitive landscape featuring major players, their strategies, and recent developments.

Historical and forecasted market size from 2017 to 2031.

Insights into current and emerging trends shaping the industry.

Strategic recommendations for stakeholders, investors, and new entrants.

Customizable data formats (PDF & Excel) for quick access and business planning.

0 notes

Text

United States of America Continuous Glucose Monitoring Market Forecast and Industry Analysis

The United States of America Continuous Glucose Monitoring Market is poised for significant transformation, driven by evolving technology and increased adoption across diabetic care management. The industry size commands growing attention due to its pivotal role in improving patient outcomes and operational efficiencies in healthcare. Market Size and Overview

The United States of America Continuous Glucose Monitoring Market is estimated to be valued at USD 652.2 Mn in 2025 and is expected to reach USD 1177.0 Mn by 2032, growing at a compound annual growth rate (CAGR) of 8.8% from 2025 to 2032.

This market growth is propelled by advancements in sensor technology, rising prevalence of diabetes, and increasing awareness regarding real-time glucose monitoring. Continuous innovations and penetration in outpatient care settings contribute significantly to the expanding industry size. The market report further highlights the expanding market scope fueled by integration of AI and wireless connectivity in CGM systems. Use Case Scenarios

- Diabetes Management in Clinical Settings: Large healthcare providers across the U.S. implemented real-time glucose monitoring solutions in 2024, improving glycemic control and reducing hospital readmission rates by over 15% within a year. - Remote Patient Monitoring Programs: Leading insurers actively integrated CGM devices into their telehealth offerings, enabling continuous remote monitoring for outpatients, which reduced emergency visits and enhanced patient compliance. - Fitness and Wellness Applications: Wearable CGM technology found growing adoption among health-conscious consumers and elite athletes seeking precise metabolic data, signifying unique market opportunities beyond traditional diabetes care. Policy and Regulatory Impact

- The FDA’s approval of next-generation CGM systems with enhanced interoperability standards in early 2025 significantly accelerated market growth strategies and adoption rates. - CMS updated reimbursement policies in 2024 to expand coverage of CGM devices under medical benefits, easing market constraints and driving business growth for CGM market players. - The implementation of updated HIPAA-compliant data security frameworks for patient-generated health data fostered market confidence in deploying connected CGM systems through 2025, influencing market dynamics positively. Key Players

Prominent market companies dominating the United States of America Continuous Glucose Monitoring market include: - Abbott - Dexcom, Inc. - Medtronic - Senseonics, Inc. - F. Hoffmann-La Roche Ltd.

‣ Get More Insights On: United States of America Continuous Glucose Monitoring Market

‣ Get this Report in Japanese Language: アメリカ合衆国の持続血糖測定市場

‣ Get this Report in Korean Language: 미국연속포도당모니터링시장

0 notes

Text

Bluetooth Mouse Market Growth and Industry Trends 2025-2032

The Bluetooth mouse industry continues to evolve rapidly, driven by increasing consumer demand for wireless peripherals supporting enhanced mobility and convenience. Rising adoption of laptops, desktops, and smart devices has spurred strong market growth, supported by ongoing innovation in connectivity, battery life, and ergonomic design. The global Bluetooth mouse market size is estimated to be valued at USD 2.03 billion in 2025 and is expected to reach USD 3.37 billion by 2032, exhibiting a compound annual growth rate (CAGR) of 7.5% from 2025 to 2032. Bluetooth Mouse Market Size demonstrates strong market growth driven by increasing adoption of wireless peripherals in both commercial and consumer segments. The market report highlights growing market revenue, expanding market segments like gaming and office use, and evolving market dynamics such as integration with multi-device ecosystems. Emerging market drivers include rising work-from-home trends and upgrades in Bluetooth technology, while market restraints relate to competitive pricing pressures and alternative input devices. Get more insights on, Bluetooth Mouse Market

#Coherent Market Insights#Bluetooth Mouse#Bluetooth Mouse Market#Bluetooth Mouse Market Insights#Bluetooth Low Energy

1 note

·

View note

Text

Sleep Apnea Diagnostic Systems Market Outlook: USD 4.48 Billion by 2025

The sleep apnea diagnostic systems market is estimated to reach USD 4.483 billion in 2025. It is estimated that revenue will increase at a CAGR of 3.3% between 2025 and 2035. The market is anticipated to reach USD 6.224 billion by 2035.

The sleep apnea diagnostic systems market plays a vital role in the healthcare industry, addressing the growing need for effective diagnosis of sleep apnea—a disorder characterized by interrupted breathing during sleep. Sleep apnea can lead to serious health complications, including cardiovascular diseases, daytime fatigue, and cognitive impairments if left undiagnosed. Sleep apnea diagnostic systems enable clinicians to monitor breathing patterns, oxygen levels, and other physiological parameters to detect this condition accurately. These systems range from traditional polysomnography devices used in sleep labs to portable home-based monitoring solutions.

The increasing prevalence of sleep disorders globally has put the spotlight on the importance of reliable diagnostic tools. Healthcare providers and patients alike are demanding more convenient, accessible, and accurate systems that can provide timely diagnosis without the need for extended hospital stays. The sleep apnea diagnostic systems market is evolving rapidly to meet these demands, driven by technological advancements and a growing awareness of sleep health.

Get Sample Report: - https://www.futuremarketinsights.com/reports/sample/rep-gb-777

Market Trends

Several trends are shaping the sleep apnea diagnostic systems market today. One noticeable trend is the shift towards home-based sleep apnea diagnostic systems. Traditional polysomnography, though comprehensive, requires patients to spend nights in specialized sleep centers, which can be inconvenient and expensive. In contrast, home sleep apnea testing devices offer greater comfort, convenience, and affordability, leading to their growing adoption.

Technology integration is another significant trend, with many systems now featuring wireless connectivity, cloud-based data management, and smartphone compatibility. These advancements allow for real-time monitoring, remote data access by healthcare professionals, and improved patient engagement through mobile apps. Artificial intelligence and machine learning are also beginning to influence the market by enhancing data analysis accuracy and providing predictive insights.

There is also a clear movement towards miniaturization and wearable technology within this market. Lightweight, discreet devices that patients can use without disrupting their sleep are becoming increasingly popular. These innovations are expected to expand the reach of sleep apnea diagnostics to a broader patient population, including those with mild symptoms who might otherwise remain undiagnosed.

Driving Forces Behind Market Growth

Several key factors drive the growth of the sleep apnea diagnostic systems market. Foremost is the rising prevalence of sleep apnea worldwide, which is partly attributed to lifestyle changes, increasing obesity rates, and aging populations. As more individuals experience symptoms such as excessive daytime sleepiness and loud snoring, demand for diagnostic services grows accordingly.

Increased awareness about the health risks associated with untreated sleep apnea also fuels market expansion. Educational campaigns by health organizations and improved physician training have led to higher diagnosis rates. People are becoming more proactive about their sleep health, seeking timely diagnosis and treatment.

Technological innovation continues to propel the market forward. The development of advanced sensors, improved algorithms for data interpretation, and integration with telemedicine platforms have made diagnostic systems more efficient and user-friendly. Additionally, the rising adoption of personalized medicine and digital health solutions encourages the use of sophisticated sleep apnea diagnostic tools tailored to individual patient needs.

Government initiatives aimed at improving sleep disorder diagnosis and management provide further impetus. Reimbursement policies for home sleep apnea testing and increased funding for sleep research contribute positively to market dynamics. Healthcare providers are investing in better infrastructure and training to accommodate the growing need for sleep diagnostics.

Challenges and Opportunities

Despite the promising growth prospects, the sleep apnea diagnostic systems market faces several challenges. One major hurdle is the variability in diagnostic accuracy between different systems, especially home-based devices compared to in-lab polysomnography. Ensuring consistent and reliable results remains critical to maintaining clinical confidence and patient trust.

Another challenge is the lack of awareness or delayed diagnosis in certain populations, particularly in developing regions where access to healthcare resources and diagnostic tools may be limited. Stigma associated with sleep disorders and misconceptions about the symptoms can further delay diagnosis and treatment.

Data privacy and security concerns also pose challenges, especially with the increasing use of cloud-based and connected diagnostic devices. Protecting sensitive patient information while enabling seamless data sharing is a delicate balance that manufacturers and healthcare providers must address.

However, these challenges open the door for significant opportunities. Enhancing device accuracy and developing user-friendly, affordable diagnostic systems can increase adoption across diverse patient groups. Expanding into emerging markets where awareness and healthcare infrastructure are improving presents untapped potential.