Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by industryoverview2025 and here's what we found interesting.

Average Info

Notes Per Post

0

Likes Per Post

0

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

3 days

Number of Posts By Type

Text

17

Last Seen Tumblr Blogs

Fun Fact

Tumblr.com is the 103rd most visited website in the world.

Text

Regulatory Affairs Outsourcing Market for Clinical Trial Applications

The global regulatory affairs outsourcing market is entering a period of robust expansion, fueled by the growing intricacy of international compliance requirements, cost pressures on pharmaceutical and biotech companies, and the rising number of clinical trials across diverse therapeutic areas. According to a recent report by Transparency Market Research, the market was valued at US$ 7.4 Bn in 2024 and is projected to expand at a CAGR of 10.6% to reach over US$ 22.3 Bn by 2035.

Rising Regulatory Complexity Spurs Outsourcing Demand

One of the primary drivers behind the market’s growth is the escalating complexity of the regulatory landscape. Drug developers are facing stringent and frequently evolving guidelines imposed by agencies such as the FDA (U.S.), EMA (Europe), PMDA (Japan), and increasingly rigorous regulators in emerging economies. Navigating this landscape requires specialized knowledge and localized expertise—capabilities that regulatory outsourcing firms are well-positioned to offer.

Moreover, the globalization of clinical trials has increased the demand for strategic regulatory guidance across multiple jurisdictions. Pharmaceutical and biotech companies are increasingly relying on outsourcing partners to handle submissions, ensure local compliance, and facilitate faster product approvals, thus accelerating time to market.

Consult our report for a thorough exploration of essential insights -

Expanding Service Portfolio

Regulatory affairs outsourcing now extends far beyond document preparation. The market has matured to include a broad spectrum of services:

Regulatory consulting & legal representation

Product registration & clinical trial applications

Regulatory writing and publishing

Submission management and lifecycle maintenance

These services are crucial at all stages of drug development—ranging from preclinical and clinical phases to post-market authorization activities. Companies outsource these tasks to enhance flexibility, reduce operational burden, and focus internal resources on innovation and core competencies.

Small and Mid-sized Enterprises (SMEs) Drive Outsourcing Uptake

While large pharmaceutical companies continue to dominate the outsourcing landscape, the most rapid growth is occurring among small and mid-sized enterprises (SMEs). These organizations often lack the in-house regulatory infrastructure to handle complex and region-specific submissions. Outsourcing allows them to stay agile while meeting regulatory expectations and timelines efficiently.

Therapeutic Area Expansion

The demand for regulatory services is particularly high in therapeutic areas such as oncology, neurology, cardiology, immunology, and dermatology. These fields are characterized by rapid innovation and a high volume of new drug applications, thereby increasing the need for expert support in regulatory affairs and compliance documentation.

Regional Outlook: Asia-Pacific Takes the Lead

The Asia-Pacific region has emerged as the largest and fastest-growing regulatory affairs outsourcing market, accounting for over 40% of global revenue in 2023, according to Grand View Research. Countries such as India, China, Singapore, and South Korea have established themselves as key hubs due to:

Lower operational costs

Large patient populations for clinical trials

Growing regulatory harmonization with ICH and FDA standards

Presence of experienced and qualified regulatory professionals

North America and Europe remain strong markets, particularly for high-value consulting and specialized regulatory submissions. However, cost-sensitive projects and volume-driven outsourcing continue to flow toward the Asia-Pacific region.

Competitive Landscape

The regulatory affairs outsourcing industry is moderately fragmented, with key players including:

PAREXEL International Corporation

IQVIA Holdings Inc.

ICON plc

Covance Inc.

Freyr Solutions

Medpace Holdings, Inc.

Charles River Laboratories

PharmaLex GmbH

These companies compete on capabilities in therapeutic specialization, global presence, regulatory intelligence, and integrated service delivery. Strategic partnerships, acquisitions, and regional expansion are key tactics used to gain market share.

Industry Trends & Outlook

Key trends shaping the future of the market include:

Digital transformation in regulatory operations (e.g., use of AI for document creation and submission tracking)

Integration of regulatory affairs with clinical and pharmacovigilance functions

Increased demand for strategic consulting services in early drug development

Rising complexity of combination products, biologics, and cell & gene therapies driving specialized outsourcing

With regulatory scrutiny expected to intensify in the wake of new therapies and global supply chain disruptions, the role of outsourced regulatory partners will become even more critical.

Conclusion

The global regulatory affairs outsourcing market is on a strong upward trajectory, driven by the pressing need for expert guidance in navigating increasingly stringent global regulations. As biopharma companies prioritize speed, efficiency, and compliance, outsourcing will remain a vital strategic lever. With a CAGR of 10.6% through 2035 and growing demand from both SMEs and multinationals, the sector is set to play a pivotal role in the future of pharmaceutical innovation and access.

Want to know more? Get in touch now. -https://www.transparencymarketresearch.com/contact-us.html

0 notes

Text

The laboratory analytical equipment market is at the heart of scientific innovation and critical decision-making across various industries. From pharmaceutical drug development and food safety to environmental monitoring and forensic investigations, these instruments enable accurate measurement, detection, and characterization of materials at the molecular level. As global industries embrace precision-driven operations, the reliance on sophisticated analytical tools is intensifying. The market is projected to grow steadily from 2025 to 2035, fueled by increased investments in R&D, evolving healthcare diagnostics, and a push toward automation and digital transformation in laboratories.

Market Overview

The laboratory analytical equipment market encompasses a broad array of instruments used to analyze chemical, biological, and physical properties of substances. These include chromatographs, spectrometers, microscopes, titrators, and thermal analyzers, among others. The market is witnessing robust growth, underpinned by expanding applications in clinical diagnostics, pharmaceuticals, biotechnology, environmental science, materials testing, and food quality control. Moreover, advancements in miniaturization, real-time analysis, and integrated software systems are transforming how labs conduct testing and generate data.

As laboratories modernize and automation becomes more accessible, there is a significant shift toward instruments that offer high throughput, improved accuracy, and reduced human error. This transformation is especially evident in the pharmaceutical and biotech sectors, where fast and precise results are essential to meet stringent regulatory requirements and competitive timelines.

Key Market Drivers

1. Rising Demand from the Healthcare and Pharmaceutical Sectors

The global focus on health and wellness, particularly in the aftermath of COVID-19, has intensified investments in clinical research and diagnostics. Laboratory analytical equipment plays a crucial role in drug development, biomarker analysis, genetic screening, and disease diagnostics. The rise of personalized medicine, which requires highly accurate molecular-level analysis, has further boosted demand for next-generation instruments.

2. Technological Advancements

Modern analytical instruments are being integrated with AI, machine learning, and cloud-based data management to facilitate smarter laboratories. These technologies enhance data interpretation, speed up workflows, and enable predictive analytics. Instruments such as automated mass spectrometers, high-resolution microscopes, and real-time PCR systems are examples of how technology is reshaping laboratory operations.

3. Regulatory and Quality Assurance Requirements

Industries such as pharmaceuticals, food and beverage, and chemicals are bound by strict quality assurance and compliance standards. Regulatory frameworks including GMP (Good Manufacturing Practices), ISO certifications, and FDA requirements demand precise and reproducible testing protocols. This has led to increased procurement of high-performance analytical tools to ensure product safety and regulatory compliance.

4. Growing Focus on Environmental Monitoring

With increasing global awareness around environmental pollution and climate change, demand for analytical tools in water, air, and soil testing has surged. Instruments like atomic absorption spectrometers and gas chromatographs are essential for detecting contaminants and ensuring adherence to environmental standards. Government agencies, academic institutions, and private organizations are expanding their monitoring efforts, contributing to market growth.

Market Segmentation

By Product Type:

Chromatography Systems: Widely used in pharmaceuticals and food testing for separating and identifying components of complex mixtures.

Spectroscopy Instruments: Include UV-Vis, NMR, and Mass Spectrometry; vital for quantitative and structural analysis.

Microscopes: Optical, electron, and atomic force microscopes enable visualization of micro and nano-scale structures.

Titrators and Electrochemical Analyzers: Used in chemical and petrochemical labs for quality control.

Thermal Analyzers: Employed in material science to study properties like melting point and heat capacity.

Others: Includes particle size analyzers, rheometers, and pH meters.

Among these, chromatography and spectroscopy dominate the market due to their extensive use in analytical laboratories and their ability to deliver comprehensive chemical profiles.

By End-user:

Pharmaceutical & Biotechnology Companies: The largest end-user segment, driven by the need for consistent product testing, formulation research, and regulatory validation.

Academic & Research Institutions: These entities drive innovation through basic and applied research across disciplines.

Environmental Testing Laboratories: Utilize analytical instruments for pollution monitoring, resource management, and sustainability studies.

Food & Beverage Industry: Instruments are employed to verify ingredient authenticity, detect adulteration, and comply with food safety regulations.

Chemical & Petrochemical Industry: Analytical tools are essential for monitoring process chemistry, ensuring product specifications, and improving production efficiency.

Clinical Diagnostics Laboratories: Use instruments for routine tests, infectious disease detection, and personalized diagnostics.

By Region:

North America: Leading the market due to strong R&D infrastructure, high healthcare expenditure, and early adoption of automation.

Europe: Driven by stringent quality regulations and a strong academic research base.

Asia Pacific: Fastest-growing region, supported by expanding pharmaceutical manufacturing, increased government investments in R&D, and growing academic initiatives in countries like China, India, and South Korea.

Latin America and MEA: Emerging regions showing growth due to improvements in healthcare access and environmental monitoring initiatives.

Emerging Trends

1. Automation and Smart Labs

Laboratories are increasingly embracing automation to improve efficiency and data accuracy. Robotic sample handlers, smart sensors, and automated titration systems are being integrated with software platforms to streamline workflows and reduce human error. Fully integrated labs capable of remote operation are becoming a reality.

2. Portable and Miniaturized Instruments

There is a growing demand for handheld or portable analytical devices in industries such as agriculture, environmental testing, and food safety. These instruments offer real-time results at the point of use, significantly speeding up decision-making processes.

3. Cloud Connectivity and Remote Monitoring

Instruments with cloud-based data storage and real-time monitoring features are revolutionizing laboratory data management. Scientists can now access, share, and analyze data remotely, improving collaboration and workflow continuity.

4. Green Laboratory Practices

Sustainability is gaining importance in laboratory operations. Equipment that reduces chemical usage, energy consumption, and waste generation is increasingly preferred. Manufacturers are also focusing on developing eco-friendly instruments and consumables.

Competitive Landscape

The market is moderately consolidated, with leading players focused on continuous innovation, global expansion, and strategic partnerships. Major players include:

Thermo Fisher Scientific Inc.

Agilent Technologies Inc.

Shimadzu Corporation

PerkinElmer Inc.

Waters Corporation

Bruker Corporation

Danaher Corporation (including Beckman Coulter and Sciex)

Metrohm AG

Horiba Ltd.

Hitachi High-Tech Corporation

These companies offer comprehensive product portfolios and frequently invest in R&D to improve instrument sensitivity, portability, and automation. Strategic acquisitions and collaborations are also common as companies seek to enter new markets or expand their technological capabilities.

Market Forecast and Outlook (2025–2035)

The global laboratory analytical equipment market is poised for strong, sustained growth over the next decade. As more industries integrate data-driven and evidence-based decision-making processes, the need for robust analytical infrastructure will only intensify. While developed markets will continue to invest in high-end instruments and digital integration, emerging economies will witness increased adoption due to improved funding and awareness.

By 2035, the market is expected to benefit from:

Widespread adoption of AI and big data tools in labs

Growing importance of regulatory compliance

Rapid technological innovation in sample preparation and real-time analysis

Expansion of testing applications in non-traditional fields such as nutraceuticals, cosmetics, and agriculture

Conclusion

The laboratory analytical equipment market is undergoing a profound evolution shaped by technological advancements, changing regulatory landscapes, and shifting scientific priorities. As laboratories worldwide seek faster, smarter, and greener solutions, the demand for next-generation analytical tools will continue to accelerate. The period between 2025 and 2035 will be pivotal in defining the market's future—marked by greater automation, decentralized testing, and cross-sector innovation.

0 notes

Text

0 notes

Text

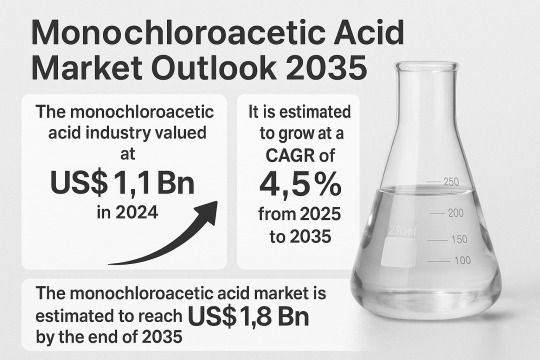

How to Tap Into the Booming Monochloroacetic Acid Market and Stay Ahead of Global Trends

The global Monochloroacetic Acid (MCA) market is experiencing a steady upswing, reflecting the growing demand across diverse sectors such as agrochemicals, pharmaceuticals, and specialty chemicals. With a projected value of US$ 1.8 billion by 2035, rising from US$ 1.1 billion in 2024, the market is poised to expand at a compound annual growth rate (CAGR) of 4.5% over the forecast period from 2025 to 2035. As the demand for crop protection products, pharmaceutical intermediates, and eco-friendly additives rises, MCA's role as a crucial chemical intermediate positions it as a key component in several industrial value chains.

This article explores how businesses and investors can capitalize on the growth of the MCA market, navigate evolving global trends, and gain a competitive edge in this dynamic sector.

Understanding the Strategic Importance of MCA

Monochloroacetic acid is a chlorinated derivative of acetic acid and serves as a foundational intermediate in the synthesis of various chemical products. The most prominent applications include:

Glyphosate production, a widely used herbicide in global agriculture

Carboxymethyl cellulose (CMC), used in food, pharmaceuticals, and cosmetics

Thioglycolic acid, used in the cosmetics industry

Glycine and other fine chemicals

Surfactants and specialty intermediates in personal care and industrial chemicals

Its versatility and functionality in forming value-added derivatives make MCA indispensable to modern manufacturing ecosystems.

Key Growth Drivers in the MCA Market

1. Boom in Agrochemicals

MCA is a crucial intermediate in the production of glyphosate, one of the most widely used herbicides globally. As food security becomes a pressing global concern due to population growth and limited arable land, the agriculture sector is under immense pressure to boost crop yields efficiently. Glyphosate plays a vital role in controlling invasive weeds, and the rising demand for herbicide-resistant crops is directly stimulating the need for MCA.

Moreover, the increasing awareness about crop protection and farm productivity, especially in developing regions, further amplifies MCA’s growth potential in the agrochemical segment.

2. Expansion of the Pharmaceutical Sector

The pharmaceutical industry continues to expand, driven by an aging global population, growing prevalence of chronic diseases, and increased healthcare spending. MCA acts as a key intermediate in the synthesis of antibiotics, anti-inflammatory drugs, and other pharmaceutical compounds. With biotechnology and personalized medicine becoming more mainstream, demand for complex chemical intermediates like MCA is expected to escalate, presenting new avenues for investment and innovation.

3. Surging Demand for Carboxymethyl Cellulose (CMC)

CMC, derived from MCA, is witnessing heightened demand due to its biodegradable nature, low toxicity, and multifunctionality. It is used as a thickener, stabilizer, and binder in a variety of industries such as food & beverages, personal care, textiles, and paper manufacturing. The rise in consumption of processed and convenience foods, as well as the global shift toward eco-friendly cosmetic formulations, is further boosting the demand for CMC — and by extension, MCA.

Global Market Dynamics and Regional Opportunities

Asia Pacific: Leading the Charge

The Asia Pacific region dominates the global MCA market, accounting for 57.3% of total market share. This dominance is attributed to rapid industrialization, favorable manufacturing infrastructure, and high consumption from agriculture and pharmaceuticals — especially in China and India. Both countries serve as major production hubs for agrochemicals and generic pharmaceuticals, creating consistent demand for MCA.

Europe and North America: Innovation and Regulation

Europe holds a 23.9% share of the global market, driven by stringent environmental regulations promoting eco-friendly agricultural inputs. North America follows, with a strong focus on technological advancements and innovation in sustainable production. These regions are likely to influence green manufacturing processes and lead the shift towards ISCC-certified MCA, which enhances market credibility and investor interest.

Emerging Markets: Latent Growth Potential

Regions such as Latin America, Middle East, and Africa, though currently holding smaller market shares, are expected to experience rapid industrial growth and infrastructure development, unlocking new consumption frontiers for MCA in the coming decade.

Trends Reshaping the MCA Landscape

1. Sustainable Production and Green Chemistry

Environmental considerations and regulatory pressures are steering the MCA industry toward cleaner and sustainable production processes. Companies like Nouryon, with its ISCC Plus-certified green MCA, are leading by example. Sustainability is no longer optional; it is an essential strategy for market entry and expansion.

2. Capacity Expansions to Meet Surging Demand

Players like Archit Organosys Limited are ramping up production capacities. Its 2022 expansion project increased MCA output by 6,000 tons per year, demonstrating the growing confidence in market scalability. Strategic investments in manufacturing facilities, especially in Asia, will be crucial to meet rising global demand.

3. Innovation in Application Development

R&D is unveiling novel applications for MCA, especially in biodegradable surfactants, specialty polymers, and cosmetics. These innovations not only expand the scope of MCA usage but also align with consumer demand for natural and safe products — creating premium market opportunities.

Key Players and Competitive Landscape

The MCA market is highly consolidated, with key players holding strong positions due to their integrated production capabilities, global distribution, and continuous innovation.

Notable companies include:

CABB Group GmbH

Niacet Corporation

Denak Co., Ltd.

Shandong Minji Chemical Co., Ltd.

Jubilant Life Sciences Ltd.

Nouryon

PCC SE

Meghmani Organics Limited

IOL Chemicals & Pharmaceuticals Ltd.

These players are actively investing in capacity expansion, product diversification, and green certification to remain competitive and aligned with evolving market expectations.

Strategic Recommendations: Tapping into the MCA Market

To successfully enter and thrive in the MCA market, businesses should consider the following strategic steps:

1. Localize Production in High-Demand Regions

Setting up or partnering with manufacturers in Asia Pacific, particularly in China and India, allows companies to optimize cost structures and align with high local demand for agrochemical and pharmaceutical intermediates.

2. Invest in Sustainable Manufacturing

Pursue ISCC Plus or equivalent certifications for green production. Investors and end-users are increasingly prioritizing environmentally responsible supply chains, and such initiatives provide a competitive differentiator.

3. Diversify Product Offerings Across Applications

Expand MCA usage beyond traditional sectors into personal care, bio-based polymers, and food additives. This not only spreads risk but also captures value from emerging niche markets.

4. Leverage R&D for Differentiation

Invest in application-specific innovation to develop proprietary derivatives of MCA or custom solutions for target industries. Strategic R&D partnerships with academic and industry institutions can accelerate this process.

5. Monitor Regulatory Trends

Stay ahead of regulatory developments in the EU, U.S., and APAC to ensure compliance and avoid disruptions. Proactively adapting to environmental standards enhances brand reputation and ensures long-term sustainability.

Positioning for the Future

The Monochloroacetic Acid market is at a promising juncture, driven by rising demand in agriculture, healthcare, and specialty chemicals. With evolving consumer preferences, environmental regulations, and global economic dynamics, the MCA industry offers a fertile ground for growth — but only for those who act strategically.

By localizing production, investing in green technologies, innovating across applications, and aligning with regional trends, businesses can not only tap into this booming market but also lead the next wave of industrial transformation.

🌍 The Monochloroacetic Acid (MCA) Market Is on the Rise – Are You Ready to Capitalize? 📈

🔍 Key Growth Drivers:

Surge in glyphosate and herbicide production for global food security

Expanding pharmaceutical applications in antibiotics and anti-inflammatories

Rising use of carboxymethyl cellulose (CMC) across food, pharma, and cosmetics

📊 Asia Pacific dominates with over 57% market share, led by strong demand from China and India, while Europe and North America contribute through sustainability-focused innovations and advanced pharma applications.

🏭 From regulatory shifts to ISCC+ certified green MCA, companies like CABB Group GmbH, Nouryon, and Archit Organosys Ltd. are leading the transformation with strategic expansions and eco-friendly production.

💡 Want to explore how your business can tap into this evolving opportunity? Check out our latest insights on market segmentation, global trends, key players, and future outlook — and learn what it takes to stay ahead.

The global MCA market is projected to grow from US$ 1.1 Bn in 2024 to US$ 1.8 Bn by 2035, expanding at a steady CAGR of 4.5%. With rising demand across agrochemicals, pharmaceuticals, and personal care industries, there's never been a better time to position your business in this high-value chemical segment.

#ChemicalIndustry #Agrochemicals #Pharmaceuticals #MCA #BusinessGrowth #Sustainability #MarketTrends #Innovation #LinkedInInsights #SpecialtyChemicals #CMC #Glyphosate #GreenChemistry

0 notes

Text

Otoscopes Market Analysis: Key Drivers and Opportunities

The otoscopes market is witnessing a steady rise, fueled by technological advancements and increasing demand for accurate ear health diagnostics worldwide. Valued at approximately US$ 184.2 million in 2024, the market is projected to grow at a compound annual growth rate (CAGR) of 3.9%, reaching over US$ 278.5 million by 2035. This growth is propelled by innovations in digital otoscopy, rising prevalence of ear disorders, and expanding healthcare infrastructure globally.

Understanding Otoscopes and Their Importance

Otoscopes are essential diagnostic tools used by healthcare professionals to examine the ear canal and tympanic membrane. Their primary role is to detect ear infections, hearing impairments, and other ear-related health issues. Early and accurate diagnosis via otoscopy can prevent complications such as chronic infections and irreversible hearing loss. The simplicity of the otoscopy process combined with its critical role in ear health management underpins the growing importance of otoscopes in both clinical and domestic settings.

Market Drivers: Digital Transformation and Rising Ear Disorders

A major catalyst for market growth is the rising adoption of digital otoscopes, which are technologically superior to traditional analog models. Digital otoscopes provide high-definition images and video recordings of the ear canal, enabling more precise diagnosis of subtle conditions such as infections, blockages, and structural abnormalities. These devices also support telemedicine by allowing remote sharing of diagnostic images, which is particularly beneficial for patients in underserved or rural areas.

In parallel, the increasing global prevalence of ear disorders fuels the demand for otoscopes. According to the World Health Organization (WHO), over 430 million people require rehabilitation for disabling hearing loss, including 34 million children. By 2050, this figure is expected to rise to 2.5 billion people, with over 700 million requiring medical intervention. Contributing factors include rising noise pollution, unsafe listening habits, and increasing noise-induced hearing loss, particularly among younger populations. This alarming trend is heightening public awareness of ear health and emphasizing the need for regular ear screenings, thereby driving otoscope demand.

Modality Analysis: Wired Digital Otoscopes Lead the Market

The market is segmented into two key modalities: wired digital and wireless otoscopes. Currently, wired digital otoscopes dominate the market due to their robust functionality, reliable connectivity, and superior imaging capabilities. These devices are favored in professional healthcare settings where precision is paramount.

Government initiatives worldwide also support the adoption of wired digital otoscopes. For example, China’s New Cooperative Medical Scheme subsidizes healthcare costs for rural populations, enabling better access to advanced diagnostic tools. Similarly, Australia’s Statewide Infant Screening-Hearing (SWISH) program aims to identify hearing impairments in newborns, driving demand for high-quality otoscopic devices.

Design and End-User Segmentation

Otoscopes come in two main designs: wall-mounted and handheld. Handheld otoscopes are gaining popularity due to their portability and ease of use, especially in home care and remote healthcare settings. Wall-mounted models are typically installed in hospitals and clinics for routine examinations.

Regarding end users, the market serves hospitals, clinics, ENT (ear, nose, and throat) centers, and research institutes. Hospitals and ENT centers constitute the largest end-user segment, reflecting the growing need for accurate diagnostics in specialized medical environments.

Regional Outlook: North America Leads the Charge

North America remains the frontrunner in the global otoscopes market. The region boasts advanced healthcare infrastructure, high accessibility to cutting-edge medical technology, and a proactive approach by healthcare professionals in adopting innovative devices. The United States, in particular, accounts for a significant share due to widespread awareness of ear health and the prevalence of hearing disorders.

Europe, Asia Pacific, Latin America, and the Middle East & Africa also show promising growth prospects. Asia Pacific is emerging as a key market due to improving healthcare infrastructure and increasing government focus on early diagnosis in countries like China and India.

Competitive Landscape and Key Players

The otoscopes market is highly competitive with established players such as 3M, Welch Allyn, American Diagnostic Corporation, HEINE Optotechnik, Midmark Corporation, Olympus Corporation, and others driving innovation and market penetration. These companies frequently collaborate with hospitals and healthcare providers to expand their footprint and introduce advanced products.

A noteworthy development in 2025 was the announcement by JEDMed Otologic Technologies of the world’s first AI-enabled digital otoscope. This device leverages artificial intelligence to analyze ear images for enhanced diagnostic accuracy, reducing human error and expediting treatment decisions. Such technological breakthroughs highlight the future direction of the market, combining AI and telemedicine to revolutionize ear health diagnostics.

The global otoscopes market is on a solid growth trajectory supported by technological innovations, rising ear health awareness, and increasing incidence of hearing disorders. With digital and AI-enabled otoscopes becoming the new norm, the market is set to transform how ear diagnostics are conducted, enhancing patient outcomes and expanding access to quality care worldwide. Healthcare providers, governments, and manufacturers must continue to collaborate in fostering advancements and accessibility to meet the growing global demand through 2035 and beyond.

Visit our report to discover essential insights and analysis -

0 notes

Text

Digital Pathology Market Set to Surge to US$ 4.2 Bn by 2035: Key Insights and Projections

The global digital pathology market is witnessing a paradigm shift, transforming how pathologists diagnose and collaborate across distances. This transition from conventional microscopy to digital platforms is not only enhancing diagnostic accuracy and workflow efficiency but is also paving the way for AI integration in modern pathology. Valued at US$ 1.1 Bn in 2024, the market is projected to surge to over US$ 4.2 Bn by 2035, expanding at a CAGR of 12.4% from 2025 to 2035.

Introduction: The Digital Evolution in Pathology

Digital pathology, the practice of digitizing glass slides using whole-slide imaging and storing them for analysis and collaboration, is a crucial advancement in modern healthcare. Traditional pathology involved microscopic analysis of tissue samples, a time-intensive and geographically restricted process. With digital tools, pathologists can now view, annotate, and share high-resolution images from virtually any location, leading to quicker, more consistent diagnoses.

This transformation is being driven by several interconnected trends: increasing prevalence of chronic diseases, the rising demand for precision diagnostics, and technological advancements in AI and machine learning. Additionally, the global focus on personalized medicine and remote healthcare delivery models is further propelling adoption. As healthcare systems worldwide strive to improve diagnostic outcomes while optimizing operational efficiency, digital pathology emerges as a key enabler of next-generation pathology workflows.

Market Drivers: Fueling the Growth of Digital Pathology

Enhancing Lab Efficiency through Digital Adoption

One of the most significant drivers of the digital pathology market is the technology's potential to improve laboratory efficiency. By digitizing tissue slides, laboratories can reduce reliance on physical storage, streamline workflows, and cut down turnaround times. Digital pathology enables easier archiving, faster retrieval, and automated analysis—enhancing both accuracy and productivity.

During the COVID-19 pandemic, the urgent need for remote diagnostics accelerated the adoption of digital and telepathology solutions. Laboratories that implemented digital workflows experienced fewer disruptions, ensuring continuity of care. These benefits have made digital pathology not just a convenience but a strategic necessity for modern healthcare systems.

Accelerating Drug Discovery and Research Applications

In research and drug development, digital pathology offers high-throughput analysis and deep insights into tissue morphology. Researchers can examine multiple samples in parallel, annotate complex data, and integrate molecular diagnostics seamlessly. AI-powered image analysis further boosts accuracy and scalability.

The technology also supports longitudinal studies by enabling consistent data archiving and retrieval, vital for tracking disease progression and evaluating therapeutic responses. As pharmaceutical companies intensify their search for novel targets and biomarkers, digital pathology stands at the forefront of research innovation.

Product Insights: Devices Dominate Digital Pathology Offerings

Among the various product categories, devices—including whole-slide imaging systems, scanners, and visualization equipment—account for the largest market share. These devices play a central role in converting physical samples into digital images with ultra-high resolution.

The demand for devices is being driven by the increasing need for precision diagnostics, especially in oncology and chronic disease management. Modern scanners now offer automated slide loading, faster processing speeds, and integration with cloud platforms. These improvements reduce time-to-diagnosis and enhance collaboration among specialists, particularly in multidisciplinary teams. As imaging technologies become more affordable and scalable, their adoption is expected to grow across both developed and emerging healthcare systems.

Application Analysis: A Multi-disciplinary Utility

Digital pathology has broad applicability across clinical, academic, and research domains. It is increasingly used in:

Drug Discovery & Development: Supporting target identification, biomarker validation, and toxicity studies.

Academic Research: Enabling scalable image analysis and remote collaboration in histological studies.

Disease Diagnosis: Particularly in oncology, where precise cellular imaging is critical to patient care.

Other Applications: Including forensic pathology, veterinary diagnostics, and regulatory toxicology.

With AI tools enhancing image analysis, digital pathology is poised to redefine disease detection and monitoring by providing highly granular tissue-level insights.

End-user Analysis: Who's Using Digital Pathology?

The major end-users of digital pathology solutions include:

Hospitals: Leveraging digitized workflows for faster diagnosis and better clinical outcomes.

Biotech & Pharma Companies: Employing image analytics in preclinical and clinical research.

Diagnostic Laboratories: Seeking to scale operations and enable remote consultations.

Academic & Research Institutes: Utilizing digital platforms for education and advanced research.

Hospitals and large diagnostic chains are expected to maintain dominance due to the volume of cases processed, but adoption is rising across all segments, particularly with the expansion of telepathology in rural and underserved areas.

Regional Outlook: North America Leads the Way

North America commands the largest share of the global digital pathology market, thanks to a mature healthcare ecosystem and early technological adoption. The U.S., in particular, benefits from favorable regulations, substantial investments in health IT, and a strong network of hospitals and research institutions.

Furthermore, collaborations between tech giants and healthcare providers are fostering the development of AI-driven pathology tools. The region is also witnessing rapid growth in digital health startups, creating a fertile ground for innovation and scalability.

Europe follows closely, with countries like Germany and the UK leading in digital imaging integration. Asia Pacific is emerging as a high-growth region, with investments in healthcare infrastructure and digitization in countries such as China, India, and Japan.

Competitive Landscape: Key Players and Innovations

The digital pathology market is competitive and innovation-driven, with key players continuously enhancing their offerings through partnerships, acquisitions, and product development. Leading companies include:

Leica Biosystems

Koninklijke Philips N.V.

F. Hoffmann-La Roche Ltd.

EVIDENT

Morphle Labs, Inc.

Hamamatsu Photonics

Fujifilm Holdings

PathAI

OptraSCAN

Sectra AB

Siemens Healthcare

3DHISTECH Ltd.

Recent developments include:

Charles River Laboratories and Deciphex (Feb 2025): A collaboration to integrate AI-powered digital pathology in toxicologic pathology.

Sectra and Region Västra Götaland (Feb 2025): Expansion of a 20-year partnership for integrated digital pathology and radiology systems aimed at enhancing cancer diagnostics.

These strategic initiatives underscore the importance of integrated solutions that combine imaging, AI, and cloud capabilities for scalable diagnostics.

Conclusion: A Digital Future for Pathology

The digital pathology market is on a fast trajectory, underpinned by technological innovations, a growing need for diagnostic accuracy, and a systemic push toward healthcare digitization. As AI becomes more integral and cloud infrastructures mature, digital pathology will become the norm in modern laboratories and healthcare institutions.

From academic research and drug development to routine diagnostics and personalized medicine, digital pathology holds the promise of improving patient outcomes while optimizing operational efficiency. Stakeholders across the healthcare value chain must invest in scalable, secure, and interoperable solutions to fully harness the potential of this transformative technology.

Discover key insights by visiting our in-depth report -

0 notes

Text

Digital Biomanufacturing Market Analysis by Technology and Application, 2025-2035

The global digital biomanufacturing market was valued at��US$ 21.1 Bn in 2024. The market is projected to expand at a CAGR of 9.2% from 2025 to 2035, reaching a value of US$ 55.6 Bn by the end of 2035. Rise in demand for biologics, cell and gene therapies, and vaccines is prompting the adoption of advanced manufacturing technologies. Integration of artificial intelligence (AI), machine learning (ML), Internet of Things (IoT), and robotics is redefining traditional biomanufacturing workflows.

Analysts’ Viewpoint Rapid advancements in digitalization across the pharmaceutical manufacturing ecosystem, combined with an increase in the production of complex biologics, are shaping the future of the digital biomanufacturing market. Implementation of manufacturing execution systems (MES), process analytical technologies (PAT), and digital twins is enabling real-time process control, improved quality assurance, and increased production efficiency. The convergence of automation, cloud technologies, and predictive analytics is expected to fuel the adoption of digital biomanufacturing platforms globally.

Digital Biomanufacturing Market Overview

Digital biomanufacturing refers to the integration of digital technologies to automate, monitor, and optimize biopharmaceutical production. The approach offers significant advantages such as enhanced process scalability, reduced costs, increased efficiency, and consistent product quality. Key technologies—such as MES, PAT, data analytics software, and digital twins—form a digital ecosystem that enables smart decision-making, flexible manufacturing models, and rapid adaptation to market demand, particularly in the realm of personalized medicine.

Key Market Drivers

Rising Demand for Biologics Growing prevalence of chronic conditions, autoimmune diseases, and various forms of cancer has fueled the demand for monoclonal antibodies, gene therapies, and vaccines. The complexity and precision required in biologics production necessitate digital solutions for process optimization and scale-up.

Advancements in Digital Manufacturing Technologies Integration of AI and machine learning for real-time insights, IoT-enabled sensors for predictive maintenance, and robotic automation to minimize human error are driving operational efficiency. Digital twins enable simulation and validation of processes before implementation, reducing risk and improving time-to-market.

Regulatory Support for Digitization Regulatory agencies such as the U.S. FDA are increasingly endorsing the adoption of digital technologies in compliance with quality standards, thereby facilitating smoother approval pathways and fostering trust in digital biomanufacturing systems.

Market Segmentation

By Technology

Manufacturing Execution System (MES)

Process Analytical Technology (PAT)

Data Analytics Software

Digital Twins

By Deployment Type

Cloud-based

On-premises

By Biologic Type

Vaccines

Antibodies

Cell and Gene Therapies

Others

By Application

Biomanufacturing Process Automation

Remote Equipment Monitoring

Digital Bioreactor Scaling

Others

By End-user

Biopharmaceutical Companies

Contract Manufacturing Organizations (CMOs)

Others

Regional Market Insights

North America held the dominant share of the global digital biomanufacturing market in 2024. This is attributed to the strong presence of leading biopharma companies, government support for digital transformation, and substantial investments in R&D. The U.S. Food and Drug Administration’s (FDA) push for modernization and digital compliance is accelerating the integration of PAT, MES, and digital twins in manufacturing processes. Meanwhile, Asia Pacific is emerging as a lucrative market due to expanding biologics production in China, India, and Japan.

Competitive Landscape

Prominent players in the digital biomanufacturing market are focused on strategic collaborations, innovation, and portfolio expansion. Key companies include:

Cytiva (Danaher Corporation)

Eppendorf SE

Sartorius AG

Merck KGaA

Aspen Technology Inc.

Thermo Fisher Scientific Inc.

ABB

Siemens

Dassault Systèmes

Bruker

Hamilton Company

Genedata AG

Körber AG

Invert, Inc.

AmpleLogic

Kymanox Corporation

Key Developments

In April 2025, Sartorius Stedim Biotech partnered with Tulip Interfaces to develop Biobrain Operate, a next-gen suite of digital applications for biopharma manufacturing.

In January 2025, Cytiva announced a strategic collaboration with Cellular Origins to combine the Sefia platform and Constellation robotic platform, aiming to digitally transform cell and gene therapy manufacturing.

Gain a deeper perspective by visiting our detailed report -

0 notes

Text

Wearable Healthcare Devices Market Trends 2025–2035: AI Integration and Chronic Disease Management Drive Growth

The global wearable healthcare devices market was valued at US$ 70.4 Bn in 2024 and is projected to expand at a CAGR of 16.9% from 2025 to 2035, reaching more than US$ 379.4 Bn by the end of 2035, according to the latest market report by Transparency Market Research.

Increasing launches of next-generation wearable health devices, rising public awareness regarding preventive care, and integration of artificial intelligence (AI) with real-time health monitoring are key factors expected to drive market growth in the near future. Consumer preference for home-based healthcare, expansion of telehealth services, and the rapid adoption of digital health tools are further contributing to market expansion.

Rise in Preventive Health Consciousness and Remote Monitoring Technologies Fuel Market Outlook

According to analysts at TMR, wearable healthcare devices are transitioning from basic fitness trackers to multifunctional health monitoring tools capable of managing chronic diseases such as diabetes, hypertension, and cardiovascular conditions. The integration of these devices with telemedicine platforms is enabling continuous, real-time health tracking, which supports early intervention and personalized care.

Recent product launches, such as the VIV Ring by VIV Health—marketed as the world’s first smart ring with generative sleep aid sound technology—reflect the rising trend of AI-powered wearable technologies that combine comfort with health analytics.

Surge in Diagnostic & Monitoring Devices and Consumer-grade Wearables to Strengthen Market Expansion

Based on device type, diagnostic and monitoring devices account for the largest share of the wearable healthcare devices market. This segment includes wearable blood pressure monitors, ECG monitors, glucose monitors, and multi-parameter health bands. Their integration with telehealth systems and remote diagnostics solutions makes them highly relevant in modern digital healthcare.

By grade, the consumer-grade wearable devices segment dominates the global market. Products such as Apple Watch, Fitbit, and Samsung health wearables are widely adopted due to their affordability, ease of use, and integration with smartphone applications. These devices empower individuals to take control of their health while promoting data-driven wellness practices.

North America to Maintain Dominance in Wearable Healthcare Devices Market

In terms of region, North America held the largest share of the global wearable healthcare devices market in 2024. The region’s leadership can be attributed to its robust healthcare infrastructure, high prevalence of chronic diseases, growing geriatric population, and significant investments in digital health technologies. Government initiatives promoting preventive healthcare and the presence of major medical device manufacturers further bolster regional growth.

Key Developments in Wearable Healthcare Devices Market

In January 2024, Nanowear received FDA 510(k) clearance for its AI-enabled wearable and software platform, SimpleSense™. This non-invasive, cuffless blood pressure monitor delivers continuous cardiopulmonary diagnostics and enhances hypertension management.

In June 2024, Abbott secured FDA clearance for its new Lingo and Libre Rio CGM systems. While Lingo supports health optimization for general consumers, Libre Rio caters to adults with Type 2 diabetes not using insulin.

Competitive Landscape of Wearable Healthcare Devices Market

Prominent players operating in the global wearable healthcare devices market include:

Medtronic plc

Omron Corporation

GE HealthCare

Abbott

Koninklijke Philips N.V.

Biobeat

VitalityWatch

SOMNOmedics AG

LiveMetric S.A.

Xplore Health Technologies Pvt. Ltd.

These companies are focusing on expanding their product portfolios, incorporating AI and cloud-based analytics, and forming strategic collaborations with healthcare providers to strengthen their presence in the global market.

Wearable Healthcare Devices Market Segmentation

By Device Type

Diagnostic & Monitoring Devices

Fitness Bands

Smartwatches

Smartclothing

Others

Therapeutic Devices

Wearable Defibrillators

Drug Delivery Devices

Pain Management Devices

Hearing Aids

Others

By Product Type

Remote Patient Monitoring & Home Healthcare

Sports & Fitness

By Grade

Consumer Grade

Clinical Grade

By Distribution Channel

Pharmacies

Online Channels

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Key Countries Covered

U.S., Canada, Germany, U.K., France, Italy, Spain, China, India, Japan, Australia & New Zealand, Brazil, Mexico, GCC Countries, South Africa

Visit our report to discover essential insights and analysis -

0 notes

Text

Drug-Eluting Stents Market Regulatory Landscape and FDA Approvals

The drug-eluting stents (DES) market is witnessing a dynamic transformation as cardiovascular diseases (CVDs) continue to rank among the leading causes of mortality worldwide. According to recent industry insights, the global drug-eluting stents market was valued at US$ 7.7 Bn in 2024 and is projected to reach US$ 14.2 Bn by 2035, expanding at a compound annual growth rate (CAGR) of 5.7% during the forecast period. This robust growth is driven by technological advancements in stent design and drug formulation, an aging global population, and an increasing preference for minimally invasive procedures. DES, which release antiproliferative medications to prevent arterial re-narrowing post angioplasty, are rapidly becoming the gold standard in treating coronary and peripheral artery diseases. As innovation in materials, drug delivery mechanisms, and biocompatibility continues to evolve, the DES market is poised to redefine cardiovascular care over the next decade.

Market Drivers: Technological Innovation and Epidemiological Trends

Technological advancement stands as one of the most significant growth catalysts in the DES market. The evolution from bare-metal stents to sophisticated drug-eluting systems has revolutionized interventional cardiology. Modern DES use advanced polymer coatings—both biodegradable and non-biodegradable—that control the release of drugs such as sirolimus, paclitaxel, zotarolimus, and everolimus. These drugs inhibit the proliferation of smooth muscle cells, significantly reducing the risk of restenosis. Furthermore, next-generation DES incorporate bioresorbable scaffolds and thin-strut designs, offering better patient compatibility and reducing the need for long-term dual antiplatelet therapy.

Alongside technological progress, demographic and epidemiological trends play a critical role. The rising incidence of CVDs—fueled by sedentary lifestyles, unhealthy diets, smoking, and increasing rates of diabetes and hypertension—has intensified the demand for effective treatment modalities. The World Health Organization estimates that CVDs account for nearly 17.9 million deaths each year, highlighting the urgent need for innovative cardiovascular interventions. The aging global population further compounds this trend, with elderly individuals more susceptible to coronary complications. As the burden of CVD continues to mount, drug-eluting stents offer a timely and efficacious solution, combining minimally invasive delivery with long-term clinical benefits.

Segment Analysis: Materials, Drugs, Applications, and End Users

Material-Based Insights: The DES market is segmented by material into metal and polymer stents. Among these, polymer-based stents—particularly those utilizing biodegradable polymers—lead the market owing to their improved biocompatibility and reduced long-term risks. Polymers serve as drug carriers, allowing for controlled, localized drug release that mitigates restenosis and inflammation. Biodegradable polymers gradually dissolve after drug release, minimizing adverse reactions and eliminating the need for permanent implants. This has opened new avenues in designing stents for complex arterial anatomies and patient-specific interventions. Metal stents, while traditionally dominant, are increasingly being enhanced with polymer coatings to optimize performance.

Drug-Based Insights: On the basis of drug type, the market includes sirolimus, paclitaxel, zotarolimus, everolimus, and others. Everolimus and zotarolimus are particularly preferred due to their high efficacy and favorable safety profiles. These drugs exhibit potent antiproliferative properties that suppress neointimal hyperplasia, a key cause of restenosis. Sirolimus remains a foundational drug in DES technology, often used in combination with biodegradable polymers. As research continues into novel drug formulations and release mechanisms, drug elution is expected to become more precise and patient-customized.

Application-Based Insights: In terms of application, coronary artery disease (CAD) accounts for the largest share of the DES market. As a leading cause of death globally, CAD necessitates prompt and effective treatment. DES are widely used in percutaneous coronary interventions (PCI) to prevent artery re-blockage post-angioplasty. Peripheral artery disease (PAD), though smaller in share, represents a growing segment due to increased diagnosis rates and expansion of DES applications beyond coronary use. The development of stents tailored for peripheral arteries, which often face different biomechanical stresses, is further enhancing market opportunities.

End-user Insights: Hospitals dominate the end-user segment, driven by their capacity to handle high volumes of PCI procedures and access to advanced cardiovascular equipment. Ambulatory surgical centers (ASCs) are gaining traction, however, as minimally invasive procedures become more common and reimbursement frameworks evolve. ASCs offer cost-effective alternatives for lower-risk patients and have the potential to broaden DES accessibility in both urban and rural settings.

Regional Outlook: North America Leads, Asia Pacific Rising

North America continues to hold the largest market share in the global drug-eluting stents industry, thanks to its robust healthcare infrastructure, high prevalence of CVDs, and substantial investment in medical technology innovation. The region's regulatory environment—led by the U.S. Food and Drug Administration (FDA)—also promotes the introduction of next-generation DES, enhancing market penetration. Furthermore, favorable reimbursement policies, widespread insurance coverage, and strong presence of key industry players such as Abbott, Boston Scientific, and Medtronic, contribute to the region’s dominance.

Europe follows closely, supported by increasing awareness of cardiovascular health and government initiatives promoting early detection and treatment. Countries like Germany, France, and the UK are major contributors, aided by advanced healthcare systems and growing elderly populations.

Asia Pacific represents the fastest-growing regional market. Rapid urbanization, changing lifestyles, and improved access to healthcare services are accelerating the adoption of DES in countries like China, India, and Japan. The region also benefits from rising healthcare expenditure and government programs targeting non-communicable diseases. Local manufacturers are becoming increasingly competitive, offering cost-effective solutions that challenge global incumbents. With increasing clinical trials and regulatory alignment, Asia Pacific is expected to emerge as a key hub for DES innovation and distribution.

Competitive Landscape and Key Developments

The global drug-eluting stents market is moderately consolidated, with leading players engaging in strategic partnerships, product launches, and mergers to strengthen their market positions. Key players include Abbott Laboratories, Medtronic plc, Boston Scientific Corporation, B. Braun Melsungen AG, Cook Medical Inc., Lepu Medical, Elixir Medical Corp., and Biosensors International Group, Ltd.

In June 2024, Elixir Medical received Breakthrough Device Designation from the U.S. FDA for its DynamX Sirolimus-Eluting Coronary Bioadaptor System, a novel platform designed to improve vessel function and reduce the need for re-intervention. In May 2024, Abbott launched the XIENCE Sierra Everolimus-eluting stent in India, expanding its footprint in emerging markets and introducing cutting-edge stent technology with enhanced deliverability and safety.

These developments underscore a shift toward personalized and adaptive stenting solutions. Investments in biodegradable materials, AI-guided procedures, and remote monitoring technologies are setting the stage for the next era of cardiovascular treatment.

The drug-eluting stents market is set to experience sustained and significant growth through 2035. Technological innovation, coupled with a growing burden of cardiovascular diseases, will continue to fuel demand for DES across both developed and emerging economies. Biocompatible materials, precision drug delivery, and minimally invasive techniques are transforming cardiovascular care—making treatments safer, more effective, and more accessible.

As healthcare systems worldwide seek cost-effective interventions with long-term benefits, DES stand at the forefront of cardiovascular innovation. Stakeholders—including manufacturers, healthcare providers, and policymakers—must work collaboratively to overcome existing challenges such as high treatment costs and long-term risks like thrombosis. Continued investment in R&D, regulatory harmonization, and patient-centric design will be crucial to unlocking the full potential of DES and ensuring better heart health outcomes for the global population.

Uncover valuable insights by exploring our comprehensive report -

0 notes

Text

Laryngeal Implants Market Emerging Trends: What to Expect by 2035

The global laryngeal implants market is witnessing a gradual yet significant transformation driven by advancements in biomaterials, growing demand for minimally invasive procedures, and increasing awareness about vocal health. As the need for functional voice restoration rises—especially among aging populations and vocal professionals—the market is evolving to deliver more effective, patient-centric solutions. According to recent projections, the global laryngeal implants market was valued at US$ 136.1 Mn in 2024 and is expected to reach US$ 221.9 Mn by 2035, expanding at a CAGR of 4.5% from 2025 to 2035.

Surge in Voice Disorders and Aging Populations: A Foundational Growth Driver

One of the most critical factors fueling the growth of the laryngeal implants market is the increasing prevalence of voice disorders, particularly among the elderly. As people age, physiological changes in the vocal folds—including muscle atrophy, reduced elasticity, and nerve degeneration—can lead to conditions such as presbyphonia or vocal cord paralysis. These disorders significantly impact communication abilities and overall quality of life, creating a clear medical need for laryngeal augmentation surgeries.

Medical professionals are increasingly emphasizing restorative care that addresses both airway and phonatory functions. This trend is evident in countries like Japan, where over 28% of the population is aged 65 and older, leading to the establishment of advanced voice clinics to treat vocal impairments. Similarly, Western Europe is seeing a rise in medialization laryngoplasty procedures in older patients, propelled by improved reimbursement policies and better referral systems. As the geriatric demographic continues to expand globally, implant manufacturers are innovating age-specific products to meet the unique anatomical and functional needs of this group, thus ensuring sustained market demand.

Technological Advancements Revolutionizing Implant Design and Surgical Techniques

The laryngeal implants market is undergoing a technological revolution, thanks to continuous innovation in materials science, imaging, and minimally invasive surgical tools. The development of biocompatible materials such as silicone, Gore-Tex (ePTFE), and calcium hydroxylapatite (CaHA) has enabled safer and more effective implants. Furthermore, emerging technologies such as shape-memory alloys, customizable polymer blends, and 3D printing are allowing for more precise implant design tailored to each patient’s vocal anatomy.

Minimally invasive surgical techniques have also gained traction, especially with the advent of endoscopic approaches and real-time voice monitoring tools. For example, some U.S.-based centers have started employing intraoperative adjustable titanium implants, allowing surgeons to fine-tune tension and position in real time during procedures. In South Korea, AI-based voice analysis tools are being used pre-operatively to determine the optimal implant strategy. These innovations are reducing surgical revision rates and enhancing patient outcomes, helping to mainstream laryngeal implant procedures across various healthcare settings.

Injectable Implants Leading the Market by Type

By type, injectable implants have emerged as the dominant segment and are expected to maintain their lead through 2035. These implants are minimally invasive, cost-effective, and can be administered in outpatient settings, making them an attractive option for both patients and practitioners. Materials such as hyaluronic acid, calcium hydroxylapatite, and collagen derivatives are commonly used in these formulations.

Injectable implants are especially effective for patients suffering from unilateral vocal fold paralysis or temporary glottic insufficiency. ENT clinics in the U.S. and Germany, for instance, increasingly use hyaluronic acid-based injectables for transient medialization in cases of reversible nerve damage. In Japan, calcium-based injectables have proven particularly beneficial for elderly patients who are not suitable candidates for invasive surgery. With the added benefits of dosage flexibility, repeatability, and reduced recovery times, injectable implants are likely to remain the go-to solution for many laryngeal disorders.

Regional Insights: North America Leading the Global Market

North America currently holds the lion’s share of the global laryngeal implants market and is projected to retain this position throughout the forecast period. The region’s dominance stems from a combination of factors: a well-established healthcare infrastructure, early adoption of cutting-edge medical technologies, and a growing elderly population vulnerable to voice disorders. Prominent academic centers like Mayo Clinic and Johns Hopkins Medicine are not only leading in procedural volume but also contributing to product innovation through ongoing clinical trials and pilot programs.

Furthermore, public and private health insurance systems, including Medicare, play a crucial role in expanding access to voice restoration surgeries. The presence of several specialized ENT surgeons and medical device manufacturers also contributes to the region’s leadership. In particular, the U.S. is witnessing increased demand from professionals in vocally intensive fields—such as teachers, broadcasters, and singers—who are proactively seeking elective procedures to maintain vocal clarity and stamina.

Strategic Collaborations and Product Innovations Fueling Market Expansion

The competitive landscape of the laryngeal implants market is marked by dynamic partnerships, product launches, and cross-disciplinary collaborations. Notable players such as Merz Pharmaceuticals, LLC, Medtronic, Soluvos Medical, E. Benson Hood Laboratories, Inc., and APrevent are continuously refining their product portfolios through innovation and research.

In January 2024, a landmark collaboration between AIIMS and IIT Delhi resulted in the development of a cost-effective prosthesis for throat cancer patients. Designed for placement through the tracheoesophageal puncture (TEP) procedure, this device offers an affordable solution for those who have lost their ability to speak. Similarly, research institutions in the Netherlands and South Korea are partnering with implant developers to enhance material strength and tissue compatibility, further reinforcing consumer confidence in the long-term reliability of these devices.

Outlook: A Market Poised for Steady Growth and Clinical Integration

As the global burden of vocal disorders continues to rise, particularly among aging populations and professional voice users, the laryngeal implants market is poised for steady growth. The convergence of biomaterial science, personalized medicine, and digital health technologies is setting the stage for more precise, efficient, and accessible treatment options. Meanwhile, the decentralization of specialist ENT care to secondary cities and emerging economies is democratizing access to voice restoration procedures, further expanding the addressable market.

Looking ahead, stakeholder collaboration will be key in driving innovation, regulatory approvals, and clinical adoption. With a strong foundation built on scientific advancement and rising patient awareness, the laryngeal implants market is set to play a pivotal role in transforming the landscape of voice restoration surgery.

Uncover valuable insights by exploring our comprehensive report -

0 notes

Text

Stair Lifts Market Dynamics: Key Trends and Investment Opportunities

The global stair lifts market is on a steady upward trajectory, driven by the convergence of an aging global population, increasing mobility-related health challenges, and rapid technological advancements. As of 2024, the market was valued at US$ 1.1 billion. According to recent industry analysis, it is poised to expand at a CAGR of 4.7% from 2025 to 2035, reaching a valuation of over US$ 1.8 billion by the end of the forecast period.

Market Overview: Supporting Independence through Innovation

Stair lifts, also referred to as chair lifts or stair gliders, are mechanical devices designed to aid individuals—especially the elderly or physically challenged—in ascending and descending staircases safely. These devices consist of a motorized seat mounted on a rail system that follows the contour of the stairs. Available for both straight and curved staircases, stair lifts are typically used in residential homes, healthcare facilities, and public buildings to promote accessibility and autonomy.

The stair lift market is witnessing increasing adoption due to the growing awareness of disability inclusion, rising healthcare standards, and a collective emphasis on independent living. Products in this category are increasingly customizable, featuring remote controls, foldable seats, battery backups, and even integration with smart home technologies. These advancements not only enhance functionality but also make stair lifts a practical and aesthetic solution for modern homes.

Market Drivers: Aging Population and Technological Progress

Aging Demographics Fueling Market Expansion

A principal driver of the stair lifts market is the steady growth of the aging population. According to the World Health Organization (WHO), the proportion of the global population aged 65 and above is expected to rise from 10% in 2022 to 16% by 2050. This demographic shift underscores a pressing need for accessibility solutions. Musculoskeletal conditions such as osteoarthritis and osteoporosis—common among seniors—further increase the demand for assistive mobility devices like stair lifts.

Moreover, WHO estimates that 1.3 billion people globally live with significant disabilities, with a substantial number facing daily mobility challenges. These factors collectively bolster the market for stair lifts, particularly among households looking for cost-effective alternatives to professional caregiving or residential mobility aids.

Technological Advancements Transforming Product Offerings

The stair lift industry is undergoing a digital transformation. Key innovations include IoT-enabled diagnostics, AI-powered predictive maintenance, and enhanced battery performance for uninterrupted operation. New product variants are also integrating wheelchair accessibility and space-saving features, making them suitable for a broader range of architectural layouts.

Additionally, governments and veteran care organizations, especially in countries like the U.S., are providing financial assistance for stair lift installations. For instance, the VA Aid and Attendance Benefits support elderly veterans in making their homes more accessible. As a result, the adoption of stair lifts is not only growing in residential segments but also expanding to healthcare and public infrastructure projects.

Key Market Segments: Understanding Diverse Consumer Needs

Device Type: Straight vs. Curved Lifts

Among device types, straight stair lifts continue to dominate due to their cost-effectiveness and easy installation. However, curved stair lifts, which are tailored to more complex stair layouts, are gaining popularity as they offer enhanced versatility and safety features. Refurbished and rental stair lifts are also emerging as viable options for temporary or budget-conscious users.

User Orientation: Seated Segment Leads

The seated stair lift segment holds the lion’s share of the market, particularly in residential settings. It is preferred due to its affordability, comfort, and compatibility with common mobility impairments. As reported by the WHO, 1.71 billion individuals suffer from musculoskeletal disorders, making seated lifts an essential home mobility solution.

Installation: Indoor vs. Outdoor

While indoor stair lifts constitute the majority of installations, outdoor variants are gaining attention for their ability to provide access to porches, decks, and garden areas. Outdoor stair lifts are built to withstand varying weather conditions, featuring waterproof components and rust-resistant materials.

End-user: Residential Sector Dominates

The residential segment is the primary revenue contributor in the stair lifts market. Older adults increasingly prefer aging-in-place solutions that allow them to stay in their own homes rather than moving into assisted living facilities. The ability to install stair lifts on most staircases enhances their practicality. Additionally, non-residential applications in healthcare facilities and leisure & entertainment venues are seeing increased demand as inclusivity becomes a norm.

Regional Insights: North America at the Forefront

North America remains the leading regional market, driven by advanced healthcare infrastructure, high consumer awareness, and supportive government initiatives. The United States and Canada account for significant shares, bolstered by an aging population and increasing diagnoses of chronic conditions like arthritis.

According to the Centers for Disease Control and Prevention (CDC), more than 78 million U.S. adults are expected to be diagnosed with arthritis by 2040. With mobility limitations rising in tandem, stair lifts present a compelling solution for home and institutional settings alike.

Furthermore, events such as the COVID-19 pandemic have accelerated the need for in-home mobility solutions. During periods of lockdown and hospital overload, many elderly individuals were advised to remain at home, further fueling demand for stair lifts as a safe, at-home mobility option.

Competitive Landscape: Key Players and Strategic Developments

The stair lifts market features a mix of established manufacturers and emerging players focusing on innovation and accessibility. Key market participants include:

Acorn Stairlifts

Bruno Independent Living Aids

Stannah Stairlifts Ltd.

Handicare Group AB

Otolift Stairlifts Ltd

Prism U.K. Medical Limited

Platinum Stair Lifts Ltd.

Savaria Corp

Thyssenkrupp AG

These companies are investing heavily in R&D to develop products that offer enhanced safety, efficiency, and design flexibility. Partnerships with healthcare facilities, government programs, and NGOs are also expanding their market reach.

A notable development includes Mobility Stairlifts’ 2022 launch of a stairlift removal service in the UK, simplifying the process of uninstalling existing devices and promoting product recycling or resale. This trend is reflective of a growing secondary market for refurbished stair lifts, appealing to environmentally conscious and budget-savvy consumers.

Conclusion: A Market Poised for Inclusive Growth

The stair lifts market is positioned for robust growth over the next decade. A combination of demographic shifts, technological progress, and policy support is paving the way for wider adoption across residential and institutional settings. As awareness increases and costs become more manageable through financing and rental options, stair lifts will continue to be instrumental in enhancing the quality of life for millions around the world.

Access our report for a deep dive into the critical insights –

0 notes

Text

Medical Radioisotopes Market Pipeline: Next-Gen Radiopharmaceuticals

The medical radioisotopes market is undergoing a significant transformation, propelled by the increasing adoption of nuclear medicine in modern diagnostics and therapeutics. As healthcare systems evolve toward precision-based, non-invasive interventions, the role of medical radioisotopes becomes increasingly critical. From advanced imaging procedures to targeted therapies for cancer and cardiovascular diseases, radioisotopes are becoming essential components of the healthcare delivery ecosystem. According to Transparency Market Research, the global medical radioisotopes market was valued at US$ 5.9 billion in 2024 and is expected to reach US$ 14.1 billion by 2035, expanding at a CAGR of 8.1% during the forecast period. This blog delves into the underlying factors shaping this growth trajectory, along with the latest trends and future outlook.

Market Introduction

Medical radioisotopes refer to radioactive substances used in various diagnostic and therapeutic medical applications. These isotopes emit radiation that can be captured through specialized imaging equipment, enabling physicians to visualize and assess internal organs and tissues without the need for surgical intervention. One of the most widely used isotopes, technetium-99m, is prized for its ideal physical properties such as a short half-life and optimal gamma radiation energy, making it suitable for numerous imaging procedures. On the therapeutic side, isotopes like iodine-131 play a pivotal role in treating thyroid-related conditions and certain forms of cancer.

The versatility of radioisotopes has expanded their use across medical disciplines including cardiology, oncology, neurology, nephrology, and endocrinology. These isotopes support early detection, disease staging, and treatment monitoring, improving patient care outcomes while minimizing invasive procedures. The market has witnessed a rapid expansion in recent years, thanks to ongoing advancements in radiopharmaceutical technology, growing disease burdens globally, and increased healthcare infrastructure investments.

Market Drivers

Growing Awareness of Nuclear Medicine

One of the primary factors fueling the growth of the medical radioisotopes market is the rising awareness and adoption of nuclear medicine in clinical settings. Educational initiatives, physician training programs, and public awareness campaigns are gradually shifting perceptions around nuclear medicine, emphasizing its safety and efficacy. The emergence of advanced imaging techniques such as positron emission tomography (PET) and single-photon emission computed tomography (SPECT) has further highlighted the role of medical radioisotopes in delivering highly detailed, real-time visualizations of internal body processes.

The increasing prevalence of chronic diseases such as cancer and cardiovascular disorders is also necessitating the use of more precise diagnostic tools. Unlike conventional imaging, PET and SPECT offer functional insights at a cellular level, aiding in accurate diagnosis and effective treatment planning. As more patients and physicians recognize the benefits of early detection and individualized care, the demand for nuclear medicine and associated radioisotopes is expected to grow substantially.

Rising Demand for Personalized Medicine

Personalized medicine, which tailors medical treatment to the individual characteristics of each patient, is reshaping modern healthcare. Medical radioisotopes are central to this shift, particularly in targeted radionuclide therapy (TRT) where radioactive particles are directed specifically at diseased tissues such as tumors, sparing healthy cells from unnecessary radiation. This approach not only enhances therapeutic efficacy but also significantly reduces side effects.