Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by marketinsightshare and here's what we found interesting.

Average Info

Notes Per Post

0

Likes Per Post

0

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

1 day

Number of Posts By Type

Text

17

Last Seen Tumblr Blogs

Fun Fact

Users from the US are the majority of Tumblr visitors.

Text

Coronavirus Infection Market - Forecast, 2022-2027

The Coronavirus Infection Market Size is estimated to reach $191.8 billion by 2027 and it is poised to grow at a CAGR of 7.6% over the forecast period of 2022-2027. Corona Virus infection is caused by SARS -CoV-2 Virus from the largest category of coronavirus. It was discovered in December 2019 in Wuhan, China hence it is popularly known as COVID-19. The Covid 19 pandemic challenged the healthcare industry in terms of policy, risk management, supply chain management and healthcare infrastructure. Coronavirus infection shows symptoms like fever, cough, tiredness and difficulty in breathing which happens in chronic bronchiolitis, owing to common symptoms and changing nature of the coronavirus make it difficult to detect at the first stage of the pandemic. To diagnose coronavirus infection nucleic acid amplification tests like polymerase chain reaction (PCR) and antigen test are developed. Severe infection of coronavirus shows severe acute respiratory syndrome (SARS), with respiratory tract infections that cause pneumonia. At the end of May 20, 2022, coronavirus infection cases and deaths are rising in the United States and marked 1 million deaths. Such increasing prevalence of coronavirus infection helps to drive the Coronavirus Infection Market size over the forecast period 2022-2027.

Coronavirus Infection Market Report Coverage

The report: “Coronavirus Infection Market Forecast (2022-2027)", by Industry ARC covers an in-depth analysis of the following segments in the Coronavirus Infection Market. By Diagnosis: Serological test, Chest computed tomography (CT), Magnetic Resonance Imaging (MRI), Antigen Test, Polymerase Chain Reaction Test (PCR) and Others. By Drugs: Remdesivir (Veklury), Ritonavir, Paxlovid, Molnupiravir and Baricitinib.By Therapy: Immune-based Therapy, Anti-inflammatory Therapy and Others. By Healthcare Equipment: PPE kit (Personal Protective Equipment), Diagnostic Tests, Surgical-Mask, Sterilizers, Ventilators and Others.By Specimens: Nasal, Nasopharyngeal, Blood and Others.By Geography: North America (U.S., Canada, Mexico), Europe (Germany, United Kingdom (U.K.), France, Italy, Spain, Russia and the Rest of Europe), Asia Pacific (China, Japan India, South Korea, Australia and New Zealand and Rest of Asia Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America) and Rest of the World (the Middle East and Africa).

Key Takeaways

Geographically, North America held a dominant market share in the year 2021, owing to the increasing prevalence of coronavirus infection and increase in mortality owing to covid cases.

The Coronavirus Infection Market size is predicted to increase owing to the increasing prevalence of covid disease and increasing research and developments to provide new drugs and technologies by key market players to consumers and healthcare. However, the high cost of research and development may limit market growth over the forecast period 2022-2027.

A detailed analysis of strengths, weaknesses, opportunities and threats will be provided in the Coronavirus Infection Market Report.

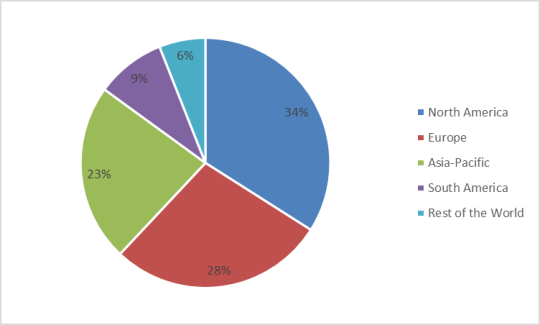

Coronavirus Infection Market: Market Share (%) by Region, 2021

For More Details on This Report - Request for Sample

Coronavirus Infection Market Segmentation Analysis- By Diagnosis

Coronavirus Infection Market based on diagnosis can be further segmented into Serological tests, Chest computed tomography (CT), Magnetic Resonance Imaging (MRI), Antigen tests, Polymerase Chain Reaction Test (PCR) and Others. The Polymerase Chain Reaction Test (PCR) segment held a dominant Coronavirus Infection market share in the year 2021, owing to the high efficiency and accurate result provided by the Rapid PCR test. According to the Indian Council of Medical Association (ICMR), the accuracy rate of PCR testing for Covid-19 is about 98.1%, of the positive nasal sample. Such high accuracy result of Covid-19 detection by PCR analysis develop rapid advancement in healthcare products manufactures company. However, the antigen test is estimated to grow with the fastest CAGR rate of 8.3% over the forecast period. Owing to the easy handling and quick results rapid antigen testing is popular among health care professionals. Rapid antigen testing is cost-cutting technology and helpful to perform in the mass population to quickly detect corona infection and enables to take further measures to limit and treat infections. Recently in May 2022, Nanomix obtained a CE mark for its covid-19 rapid point of care (POC) antigen panel. Also, key market players like Abbott, Access Bio, ACON laboratories and others are working on innovative product launches to diagnose corona infection; and several products have been approved by FDA. Such factors help to grow Coronavirus Infection Market size over the forecast period 2022-2027.

Coronavirus Infection Market Segmentation Analysis- By Drugs

The Coronavirus Infection Market based on drugs can be further segmented into Remdesivir (Veklury), Ritonavir, Paxlovid, Molnupiravir and Baricitinib. The Remdesivir (Veklury) segment held a dominant Coronavirus Infection market share in the year 2021. This is owing to the increasing use of Remdesivir to treat coronavirus infection in adults above age 12. Remdesivir act as a nucleoside analog that inhibits RNA-dependent RNA polymerase (RdRp) of coronavirus including SARS-CoV-2. It is approved by FDA and EUA to treat coronavirus infection, also Remdesivir with a combination of Baricitinib has been granted by FDA and EUA for clinical use. As a result of increasing hospitalization owing to a hike in coronavirus cases demand for Remdesivir is hike respectively. Such increasing use of Remdesivir helps to drive Coronavirus Infections Market. However, Baricitinib is estimated to grow with the fastest CAGR rate of 8.1% over the forecast period 2022-2027. The medicine Baricitinib is used to treat coronavirus infection in hospitalized patients aged 2 to less than 18 years of age with the FDA's approval and an Emergency Use Authorization (EUA). This drug is more helpful in changing the nature of coronavirus infection cases in children and teenagers by limiting pneumonia, bronchiolitis, respiratory tract infection, and Severe Acute Respiratory Syndrome. It is found that the use of Baricitinib and Remdesivir is cost-effective compared to using Remdesivir alone, as per a research article published in Springer. Such factors demand the use of Baricitinib for the treatment of coronavirus infection which helps to grow the coronavirus infection industry over the forecast period 2022-2027.

Coronavirus Infection Market Segmentation Analysis- By Geography

The Coronavirus Infection Market based on Geography can be further segmented into North America, Europe, Asia-Pacific, South America, and the Rest of the World. North America held a dominant Coronavirus Infection market share of 34% in the year 2021. This is owing to increasing cases of coronavirus infection and an increase in mortality by this disease. There are 82,459,419 cases reported of coronavirus infection in the U.S.A with 130,452 cases reported on a single day of May 25 2022, and a total number of deaths are 994,931 occurred to coronavirus infection as data published by World Health Organisation (WHO). Also, the cases of coronavirus infection are hiked by 13% in May 2022, according to Reutres Graphics report. Such increasing cases of coronavirus infections and high rate of mortality help to drive North America Coronavirus Infection Industry. Furthermore, the Asia-Pacific is estimated to grow with the fastest CAGR over the forecast period 2022-2027. This is the result of the recent outbreak of coronavirus in countries like China, on 7th March 2022, China reported 268 new cases of coronavirus infection within 24 hours. In India on 23 May 2022, 94 deaths by coronavirus infections were reported. According to Johns Hopkins University case fatality ratio in India is observed at 1.2%. According to the Health Minister of Maharashtra and Karnataka 4th wave of Covid-19 will hit between June 2022 to July 2022 and last till September 2022 as the increasing rate of coronavirus infection noted in these two states. Up to 26th May 2022, 192,820,355 doses of covid-19 vaccines were completed in India. Owing to such an increase in the number of coronavirus infections, mortality rate and vaccination help to grow the Asia-Pacific Corona Virus Infection Market over the forecast period 2022-2027.

Coronavirus Infection Market Drivers

Changing Nature of Corona Virus and Increasing Number of Deaths is Driving the Market Growth.

Since the emergence of Covid-19 the nature of the virus has been changing its nature as its genome is encoded in RNA like HIV and Influenza, a mutation that occurred in SARS-CoV-2 is the result of errors that occurred during the copy of RNA which leads to the production of different kind of enzymes. For instance, as per Lucy Van Dorp, a computational geneticist at University College London, a Sample of two SARS CoV-2 viruses collected from anywhere in the world shows a difference of 10 RNA letters out of 29903. As of May 2022, CDC listed only one variant of coronavirus as a variant of concern, that is the ‘Omicron’ variant. As per a research article published in WebMD, there are 99.9% cases of coronavirus reported in the United States and daily deaths crossed 2200 deaths in January 2022. Such an increasing number of deaths with new variants of coronavirus helps to drive the Coronavirus Infection industry over the forecast period.

Innovative Products Launched by Key Market Players and funding Provided by Governments and Organizations are Aiding the Market Growth.

Coronavirus infection spread over community-level with record break cases and deaths within a short period of time. There were 37 million Covid-19 cases and 1 million deaths were reported globally between October to December 2020. Nearly half of these cases (48%) and deaths (55%) continue to be reported in the Region of the Americas with the United States of America, Brazil and Argentina accounting for the greatest numbers of new cases and deaths in the region. Numerous academic institutions, governmental research facilities, and pharmaceutical firms have made significant financial investments in R&D to lessen the mortality rate and the effects of diseases including pneumonia, bronchiolitis, respiratory tract infections, and severe Acute Respiratory Syndrome. The International Monetary Fund $1 trillion for an unprecedented number of emergency financing requests for the Covid 19 relief fund. On 18 May 2022, WHO contribute a total fund of 3.35 billion for the vaccine, therapeutics, diagnostics, health systems and response. In February 2022, Cipla Health launched Naselin Anti-Viral Nasal Spray with Povidone-Iodine to protect against coronavirus and respiratory tract infection. Also in the same month, Glenmark Pharma and SaNotize Research launch Nasal Spray for Covid-19 treatment in India. Such a new launch of products and an increase in healthcare funding for diagnosis, treatment and prevention of covid-19 help to drive the market.

Coronavirus Infection Market Challenges

High Treatment Costs and Shortages of Essential Medical Supplies Limit Market Growth.

When a patient needs life support like a ventilator, the expense of hospitalization and medication is generally high. As coronavirus is a highly contagious illness that spreads through contact with infected people and the air, it has expanded quickly throughout the world and put a strain on the healthcare sector. The situation is made worse in nations like India where there are just 0.5 beds per 1,000 inhabitants, which is extremely low compared to other developing nations. The price inflation is also brought on by the increased demand for oxygen tanks and medications like Remdesivir as well as those products' limited supply. According to a January 2022 article in Down to Earth Organization, the average cost of Covid-19 treatment was INR112,179 in government hospitals and INR 297,577 in private hospitals. Prior to the pandemic, the cost for all symptoms combined, such as fever, respiratory infection, chest pain, and breathlessness, was only INR 4,622 in government hospitals and INR 28,932 in private hospitals. Therefore, the market is facing difficulties as a result of the inflation in drug prices. Over the projection period of 2022–2027, the Coronavirus Infection & treatment industry may be hampered by such high mortality and treatment costs.

Coronavirus Infection Industry Outlook

Product launches, mergers and acquisitions, joint ventures and geographical expansions are key strategies adopted by players in the Coronavirus Infection Market. The top 10- Coronavirus Infection Market companies are- 1. Altimune Inc.2. Moderna Inc.3. Gilead Sciences4. Novavax Inc.5. Inovio Pharmaceuticlas6. AbbVie7. Regeneron Pharmaceuticals8. GlaxoSmihKline Plc.9. Co-Diagnostics10. Steris Healthcare

Recent Developments

In March 2022, Moderna entered into a strategic partnership with the Australian Government to establish a state-of-art, domestic mRNA vaccine manufacturing facility in Australia. The new center provides access to a domestically manufactured portfolio of mRNA vaccines against respiratory viruses, including Covid-19, seasonal influenza, respiratory syncytial virus (RSV) and other potential respiratory viruses.

In March 2021, Altimmune Inc. collaborated with Lonza to expand the production of AdCOVID -a single-dose intranasal vaccine for COVID-19. AdCOVID activates systemic immunity (neutralizing antibodies and T cell responses) and mucosal immunity in the respiratory tract which has been proved in preclinical studies.

In March 2021, Gilead Sciences and Merck entered into an agreement to co-develop and co-commercialize long-acting treatment in HIC than combine Gilead’s investigational capsid inhibitor, lenacapavir and Merck’s investigational nucleoside reverse transcriptase translocation inhibitor, islatravir, into a two-drug regimen with the potential to provide new, meaningful treatment options for people living with HIV.

#Coronavirus Infection Market share#Coronavirus Infection Market size#Coronavirus Infection Market forecast

0 notes

Text

Neurodegenerative Disease Market - Forecast(2022 - 2027)

The Neurodegenerative Disease Market size is estimated to reach $49,218 million by 2027. Furthermore, it is poised to grow at a CAGR of 3.9% over the forecast period of 2022-2027. Neurodegenerative diseases are a set of brain disorders that cause the structure and function of neurons in the central nervous system (CNS) and peripheral nervous system (PNS) to deteriorate over time (PNS). Several drugs are currently available to help people lessen physical or mental symptoms and improve their quality of life. Furthermore, researchers are concentrating their efforts on developing molecular diagnostics, particularly biomarkers and imaging spectroscopy, in order to detect and diagnose neurodegenerative illnesses at an early stage and halt their progression. The impact of COVID-19 on the neurodegenerative disease market is projected to be significant, as the pandemic has disrupted clinical trial, research and development, and pipeline product workflows, resulting in relatively modest growth during the pandemic despite a solid late-stage product pipeline. Despite the pandemic the market is forecasted to gradually recover and grow in the years of forecast. The companies with higher funding and revenue are investing more into R&D with development of unique neurodegenerative disease drugs for the various neurodegenerative indications while expanding to new geographic locations through its sales channel expansion. Recently, companies are focusing on making continuous investment across the business to in order to build and maintain the pipeline of new drugs for therapeutics. Companies are also predicted to acquire, grow the foreign market revenue and continue to get timely regulatory approvals. Rising prevalence of Alzheimer disease, increasing public awareness, and a strong product pipeline for neurodegenerative disease treatment are some of the factors driving the drug Industry forward in the projected period of 2022-2027.

Report Coverage

The report: “Neurodegenerative Disease Market Forecast (2022-2027)", by Industry ARC covers an in-depth analysis of the following segments of the Neurodegenerative Disease Market.

By Drug Class- N-Methyl-D-Aspartate (NMDA) Receptor Antagonists, Acetylcholinesterase (AChE) Inhibitors, Dopamine Agonists and Antagonist, Monoamine Oxidase B (MAO-B) Inhibitor, Catechol-O-Methyltransferase (COMT) Inhibitor.

By Indications- Parkinson’s Disease, Huntington Disease, Alzheimer’s Disease, Amyotrophic Lateral Sclerosis, Multiple Sclerosis, Spinal Muscular Atrophy (SMA) and Others.

By Geography- North America (U.S., Canada, Mexico), Europe (Germany, United Kingdom (U.K.), France, Italy, Spain, Russia, and Rest of Europe), Asia Pacific (China, Japan India, South Korea, Australia, and New Zealand, and Rest of Asia Pacific), South America (Brazil, Argentina, and Rest of South America), and Rest of the World (the Middle East, and Africa).

Key Takeaways

Geographically, North America held a dominant market share in the year 2021. The growing geriatric population in the US is increasing the prevalence of neurodegenerative diseases as age is the best known risk factor for such diseases. The geriatric population was estimated to be around 65 million in 2020. This is projected to increase by 18 million between 2020 and 2030 and it is estimated that approximately 1 in every 5 Americans will be 65 or more by 2030..

The surge in neurodegenerative diseases in the US owing to the rising geriatric population is increasing the demand for effective neurodegenerative disease therapies for treating the disease and suppressing symptoms. In addition, it has also resulted in an increase in public R&D expenditure towards drug research, which will further contribute to the market growth. For instance, the Federal Alzheimer's and Dementia Research Funding increased from $2.8 billion in 2019 to $3.2 in 2021.

A detailed analysis of strengths, weaknesses, opportunities, and threats will be provided in the Neurodegenerative Disease Market Report.

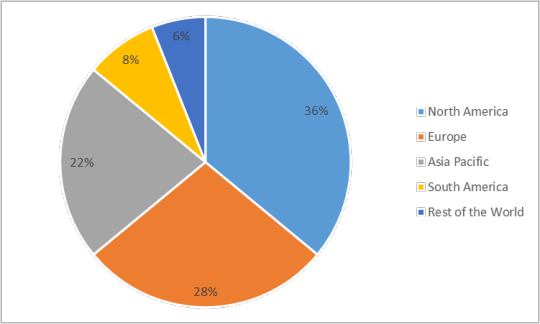

Neurodegenerative Disease Market- Geography (%) for 2021

For More Details on This Report - Request for Sample

Neurodegenerative Disease Market Segmentation Analysis- By Drug Class

The neurodegenerative disease market based on drug class can be further segmented into N-Methyl-D-Aspartate (NMDA) Receptor Antagonists, Acetylcholinesterase (AChE) Inhibitors, Dopamine Agonists and Antagonist, Monoamine Oxidase B (MAO-B) Inhibitor, Catechol-O-Methyltransferase (COMT) Inhibitor. Immunomodulators held a dominant market share in the year 2021. Immunomodulators provides very effective therapy options for a variety of autoimmune and neurodegenerative illnesses. Furthermore, the growing presence of important companies is likely to raise patient and physician awareness of the benefits of immunomodulators. As they strive to obtain a competitive advantage in the market, they are developing novel immunomodulators to treat a variety of chronic conditions.

However, Vesicular Monoamine Transporter 2 (VMAT2) Inhibitors is estimated to be the fastest-growing, with a CAGR of 13.3% over the forecast period of 2022-2027. It is owing to increase in number of patients with bipolar diseases, schizophrenia, and Huntington’s disease and other neuropsychiatric disorders undergoing long-term medical treatments with antipsychotic medication. Furthermore, throughout the projected period, investigational research for the discovery of novel therapies using VMAT2 inhibitors to treat Huntington disease are expected to drive demand.

Neurodegenerative Disease Market Segmentation Analysis- By Indications

The neurodegenerative disease market based on indications can be further segmented into Parkinson’s Disease, Huntington Disease, Alzheimer’s Disease, Amyotrophic Lateral Sclerosis, Multiple Sclerosis, Spinal Muscular Atrophy (SMA) and Others. Multiple Sclerosis held a dominant market share in the year 2021. Recently, more than 4,00,000 people in U.S. are suffering from multiple sclerosis which is rising the adoption of various types of drug class, so the demand for neurodegenerative drugs is expanding. Apart from this, the breakout of the COVID-19 pandemic has had a significant impact on the growth of the multiple sclerosis medications, as it has disrupted the supply chains of numerous important participants in the industry. For example, Biogen announced that sales of one of its important medications, TECFIDERA, which is used to treat multiple sclerosis, fell by 13% in 2020 compared to the previous year such factors are predicted to have a minor impact on market expansion.

However, Huntington Disease is estimated to be the fastest-growing, with a CAGR of 13.2% over the forecast period of 2022-2027. It is owing to various factors such as greater adoption of novel drugs, expanded R&D activity, an increase in the target population, and supportive regulatory measures are all driving the Huntington's Disease incidence. Reportedly, more than 20 drugs are in various phases of clinical trials for the treatment of Huntington's disease.

Neurodegenerative Disease Market Segmentation Analysis- By Geography

The neurodegenerative disease market based on Geography can be further segmented into North America, Europe, Asia-Pacific, South America, and the Rest of the World. North America held a dominant market share of 3.1% in the year 2021 as compared to the other counterparts. It is owing to increasing prevalence of neurodegenerative diseases such as Alzheimer diseases, Huntington disease etc. According to the Centers for Disease Control (CDC), Alzheimer's disease is the 6th leading cause of death among US adults. In 2020, it is estimated that more than 5.8 million Americans aged 65 years or older are suffering from Alzheimer’s disease. This is projected to reach 7.7 million by 2030. Meanwhile, according to the Parkinson’s Foundation Prevalence Project, the prevalence of Parkinson’s in the US is predicted to rise from 930,000 in 2020 to 1.2 million by 2030.

Neurodegenerative Disease Market Drivers

Rising prevalence of Alzheimer disease have readily aided the market growth

Alzheimer's disease is a degenerative neurological disease and the most common form of dementia, characterised by memory loss, loss of thinking skills, and difficulties with problem-solving and language. Alzheimer's disease symptoms appear gradually over many years and eventually grow more severe. According to the World Health Organization (WHO), in 2021 over 50 million individuals suffer from dementia, a frequent form of Alzheimer's disease, with 10 million new cases diagnosed each year. The increased prevalence of these disorders also drives the development of various medications. Besides, the market is growing as people become more aware of the drug therapies for Alzheimer's disease around the world. Furthermore, rising awareness of the different novel treatment alternatives, is also helping to fuel the rise of Alzheimer's Drugs.

Availability of robust pipeline of drugs for neurodegenerative disease treatment is driving the market growth

Availability of robust pipeline of drugs for neurodegenerative disorders is forecasted to drive growth of the global Neurodegenerative Disease Market. Recently, in 2021, GlaxoSmithKline Plc in collaboration with Alector Inc. to develop antibody-based treatments for Parkinson's, Alzheimer's and other similar diseases. This collaboration deals worth up to $2.2 billion which efforts to build a robust pipeline of drugs.

Neurodegenerative Disease Market Challenges

High cost of treatment are some of the factors impeding the market growth

The extremely high cost is anticipated to hamper market growth as it limits the access of quality treatment to the middle and low-income population countries. For instance, in U.S. the average annual medical cost for the treatment of Multiple Sclerosis (MS) can reach more than $70,000. This is highly expensive as the country’s median household income in 2020 was only $67,521.

Neurodegenerative Disease Market Competitive Landscape

Product launches, mergers and acquisitions, joint ventures, and geographical expansions are key strategies adopted by players in the Neurodegenerative Disease Market. The top 10- Neurodegenerative Disease Market companies are-

Biogen Inc.,

F. Hoffman La Roche Ltd.,

Merck KGaA,

Novartis AG,

Sanofi,

Teva Pharmaceuticals Industries Ltd.,

Orion Corporation,

H. Lundbeck A/S.,

Sun Pharmaceutical Industries Ltd.,

UCB S.A.

Recent Developments

In May 2021, Biogen Inc. and Envisagenics announced a new collaboration to advance ribonucleic acid (RNA) splicing research within central nervous system (CNS) diseases. As part of the collaboration, Biogen will leverage Envisagenics’ proprietary artificial intelligence (AI)-driven RNA splicing platform, SpliceCore®, to define and understand the regulation of different RNA isoforms in CNS cell types.

In August 2020, Roche announced that the U.S. Food and Drug Administration (FDA) has approved Evrysdi™ (risdiplam) for the treatment of spinal muscular atrophy (SMA) in adults and children 2 months of age and older. This is predicted to drive the SMA indication segment.

In February 2020, Novartis announced that both the US Food and Drug Administration (FDA) and European Medicines Agency (EMA) have accepted the company’s Supplemental Biologics License Application (sBLA) and Marketing Authorization Application (MAA), respectively, for ofatumumab) for the treatment of relapsing forms of multiple sclerosis (RMS) in adults.

#Neurodegenerative Disease Market share#Neurodegenerative Disease Market size#Neurodegenerative Disease Market forecast

0 notes

Text

Medical Sensors Market Research Report - Forecast(2022 - 2027)

Medical Sensors Market size is estimated to reach $3.3 billion by 2027, growing at a CAGR of 8.3% during the forecast period 2022-2027. Medical sensors are utilized to discover vital signs from patients. Medical sensors are physically fastened to individuals enduring investigation or care and can record a count of key vitals and variables. These involve temperature, blood pressure, weight, pulse rate, and more. Temperature sensors are utilized in numerous industries like motorsport, heating, ventilation, and air conditioning (HVAC), agriculture, industrial, aerospace, and automotive. There are numerous distinct facets of motors and nearly all of them need temperature measurement to guarantee the motor itself does not overheat. Ring terminal temperature sensors are frequently utilized on surface plates owing to their capability to be mounted onto a flat surface and measure temperature efficiently. Pressure sensors are utilized in infusion pumps and sleep apnea medications. A majority of the pressure sensors are combined with embedded systems. Medical Monitor Sensors persist in permitting medical professionals and patients the capability to supervise and record conditions. Sensors are available for blood glucose monitoring. Glucose sensors arrive in either a discrete form (blood glucose meter test strips) or a wearable form (a continuous glucose monitor). The most typical kind of glucose sensor is enzyme-based.

The surging technological progress in low-power electronics, micro-electro-mechanical systems (MEMS), power harvesting, and smart materials together with the establishment of low-key sensing solutions and pressure sensors integrated with embedded systems is set to drive the Medical Sensors Market. The soaring research and development to boost the traditional diagnosis and treatment techniques across the world are set to propel the growth of the Medical Sensors Market during the forecast period 2022-2027. This represents the Medical Sensors Industry Outlook.

Medical Sensors Market Report Coverage

The report: “Medical Sensors Market Forecast (2022-2027)”, by Industry ARC, covers an in-depth analysis of the following segments of the Medical Sensors Market.

By Sensor Type: Pressure Sensor, Temperature Sensor, Flow Sensor, Biosensor, Others. By Application: Surgical, Diagnostic, Therapeutic, Monitoring, Others. By Geography: North America (U.S, Canada, and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia, Rest of South America), and Rest Of The World (Middle East, Africa).

Request Sample

Key Takeaways

Geographically, North America Medical Sensors Market accounted for the highest revenue share in 2021 and it is poised to dominate the market over the period 2022-2027 owing to the existence of a massive count of makers of medical sensors like sensors for blood glucose monitoring in countries like U.S. and Canada in the North American region.

Medical Sensors Market growth is being driven by the soaring technological progress and the accessibility of wearable sensors for everyday application including blood glucose monitoring for supervising patients with obesity, cardiovascular problems, and diabetes. However, binding regulatory processes are one of the major factors hampering the growth of the Medical Sensors Market.

Medical Sensors Market Detailed Analysis on the Strength, Weakness, and Opportunities of the prominent players operating in the market will be provided in the Medical Sensors Market report.

Medical Sensors Market: Market Share (%) by Region, 2021

For more details on this report - Request for Sample

Medical Sensors Market Segment Analysis – By Sensor Type:

The Medical Sensors Market based on sensor type can be further segmented into Pressure Sensor, Temperature Sensor, Flow Sensor, Biosensor, and Others. The Temperature Sensor Segment held the largest market share in 2021. This growth is owing to the soaring application of temperature sensors in medical applications worldwide. Temperature sensors are utilized for monitoring body temperature at the time of RF hyperthermia treatments. The surging application of temperature sensors for NMR/MRI (Nuclear Magnetic resonance/Magnetic Resonance Imaging) systems in research and development is further propelling the growth of the Temperature Sensor segment.

Furthermore, the Pressure Sensor segment is estimated to grow with the fastest CAGR of 9.1% during the forecast period 2022-2027 owing to the proliferating application of differential pressure sensors in oxygen therapy systems for supervision of efficiency of oxygen therapy.

Medical Sensors Market Segment Analysis – By Application:

The Medical Sensors Market based on the application can be further segmented into Surgical, Diagnostic, Therapeutic, Monitoring, and Others. The Monitoring Segment held the largest market share in 2021. This growth is owing to the soaring establishment of distinct kinds of monitoring devices employing different kinds of sensors like pressure sensors for providing different kinds of treatments. The integration of distinct kinds of monitoring devices with smart devices and additional wireless medical sensor instruments for patient care is further propelling the growth of this segment.

Furthermore, the Diagnostic segment is estimated to grow with the fastest CAGR of 9.2% during the forecast period 2022-2027 owing to the promising potential of transistor-based sensors for accelerated diagnosis and treatment for COVID-19 and additional infections in conjunction with the application of other medical sensors like pressure sensors.

Medical Sensors Market Segment Analysis – By Geography:

The Medical Sensors Market based on geography can be further segmented into North America, Europe, Asia-Pacific, South America, and the Rest of the World. North America (Medical Sensors Market) held the largest share with 41% of the overall market in 2021. The growth of this region is owing to the advanced healthcare infrastructure in the region. Temperature sensors and pressure sensors are extensively utilized in medical applications. The soaring attention on the semiconductor industry backing technological progress of sensors is further driving the growth of the Medical Sensors Market in the North American region.

Furthermore, the Asia-Pacific region is estimated to be the region with the fastest CAGR rate over the forecast period 2022-2027. This growth is owing to factors like the soaring population in conjunction with an increasing predominance of incessant ailments like diabetes, respiratory issues, and hypertension in the Asia-Pacific region. The proliferating application of wearable devices from healthcare monitoring in conjunction with the application of medical sensors like temperature sensors and pressure sensors is further fueling the progress of the Medical Sensors Market in the Asia-Pacific region.

Inquiry Before Buying

Medical Sensors Market Drivers

Soaring Applications Of Temperature Sensors Are Projected To Drive The Growth Of Medical Sensors Market:

Temperature sensors are utilized in numerous medical applications. These applications involve supervision of body temperature at the time of RF hyperthermia treatments and measurement of patient surface temperature at the time of MRI, fMRI or additional specially designed electro-surgical processes. These sensors are also typically utilized for NMR/MRI systems in research and development. Moreover, these investigations are well suited for temperature sensing in animal testing processes or at the time of sterilization with RF and UV. Neoptix products are particularly planned for medical application with precision and lasting balance in mind. Their standard T1 temperature investigations are difficult and ruggedized to support accomplishing a secure and favorable project. The proliferating applications of temperature sensors are therefore fueling the growth of the Medical Sensors Market during the forecast period 2022-2027.

Surging Applications Of Pressure Sensors Are Expected To Boost The Demand Of Medical Sensors Market:

Pressure sensors are being utilized in life-saving medical applications. Numerous medical devices presently rely on precise and balanced pressure measurements to perform trustworthily. Patient care is extending beyond the hospital and the GP‘s surgery and appearing in patients’ homes, in the form of home health supervision. Accordingly, establishing pressure sensors has evolved into an integral portion of planning medical applications. A ventilator performs by blending air with pure oxygen to support the respiratory function of a patient. Differential or gauge pressure sensors are usually sited between valves and regulators to guarantee the air and oxygen are blended in the right quantities. In this type of application, small surface-mount sensors are perfect. They will normally be particularized for a pressure range of 2in or 5in H2O and are accessible with either analog or digital (I2C) outputs. In spite of being tiny and low power, these low-pressure sensors can frequently involve an integrated DSP (digital signal processor) for adjusting for non-linearity, offsets or the consequences of temperature. The surging usage of pressure sensors in medical applications is therefore driving the growth of the Medical Sensors Market during the forecast period 2022-2027.

Medical Sensors Market Challenges

Challenges In Manufacturing Superior Medical Sensors Are Hampering The Growth Of The Medical Sensors Market:

Testing sensors at the time of and consequent to production-level manufacturing is not like testing digital integrated circuits. While digital circuits are in sensors and get tested as such, sensors frequently have analog constituents that require calibration and testing. Additionally, sensors are becoming more complex. With multiple sensor types performing in the identical small form factor, the complicated design and testing progress up. The challenge in testing sensors is not regarding normal issues in advanced nodes. With these devices in the analog world, it is about 0.18 micron, moving to possibly 90nm. The larger issue is planning sensors at the system level to acquire adequate precision and good SNR (signal-to-noise ratio) out of a sensor. This issue is thus hampering the growth of the Medical Sensors Market.

Medical Sensors Industry Outlook

Product launches, mergers and acquisitions, joint ventures, and geographical expansions are key strategies adopted by players in this market. Medical Sensors top 10 companies include:

GE Healthcare Inc.

STMicroelectronics

Honeywell Inc.

Omron Corporation

Siemens Corporation

TE Connectivity

Analog Devices

Texas Instruments

Medtronics PLC

First Sensor

Buy Now

Recent Developments

In January 2021, Texas Instruments introduced Wireless Battery Management System for Electric Vehicles. Lithium-ion batteries are the driving force behind the horsepower in electric vehicles, and the novel TI system will keep those lively mustangs regulated without weighing them down. The battery of an electric vehicle is an accumulation of 100 or greater independent cells.

In December 2020, Medtronic plc declared the U.S. commercial introduction of the Carpediem™ Cardio-Renal Pediatric Dialysis Emergency Machine. Succeeding the U.S. Food and Drug Administration's (FDA) marketing endorsement, granted earlier in 2020, the earliest Carpediem™ systems in the U.S were fruitfully installed and are in the application at Cincinnati Children's Hospital Medical Center. The earliest of its type Carpediem™ system is designated for application in acute kidney injury or fluid overloaded patients needing hemodialysis or hemofiltration therapy.

In November 2020, First Sensor introduced a 2-in-1 differential pressure product. First Sensor just brought out its novel LHD ULTRA range, with all sensor types presently accessible as samples – the earliest of which have already been delivered to consumers. The high-precision 2-in-1 differential pressure sensors integrate two sensing elements with distinct pressure series in a single housing.

0 notes

Text

Vision Disorders Market - Forecast, 2022-2027

Vision Disorders Market Size is estimated to reach $47.4 billion by 2027. Furthermore, it is poised to grow at a CAGR of 7.1% over the forecast period of 2022-2027. Vision Disorders are defined as any impairment in the normal sense of vision. Myopia, hyperopia, astigmatism, presbyopia, conjunctivitis, cataract, corneal abrasion, entropion, and glaucoma are only a few of the vision diseases that impact the vast majority of the world's population. The majority of vision impairments are caused by poor nutrition, different diseases, severe eye injury, insertion of foreign objects, and advancing age. Despite tremendous advances in preventing and curing visual impairment in many countries over the last two decades, the World Health Organization (WHO) estimates that over 285 million people worldwide are still visually impaired in 2013. According to the WHO, simple eye examinations such as aberrant blinking frequency, pupil size, and eye color can heal 80 percent of visually impaired patients. Clinical and retinal examinations such as corneal topography, keratometry, pachymetry, fluorescein angiography, Indocyanine Green study (ICG) dye test, and other related studies can confirm the diseases. Ignorance and neglect, on the other hand, might result in serious eye issues or irreversible vision loss. In 2004, the Centers for Disease Control and Prevention (CDC) published research estimating that around 14 million Americans over the age of twelve were affected by various vision impairments, eyeglasses, and contact lenses are generally used in eyesight. Silicone hydrogel contact lenses are a type of advanced soft contact lens that allows more oxygen to pass through to the cornea than traditional soft ("hydrogel") contacts.

Vision disorders Market Report Coverage

The report: “Vision Disorders Market Forecast (2022-2027)", by Industry ARC covers an in-depth analysis of the following segments of the Vision Disorders Market.

By Disease Type- Dry Eye, Eye Allergies, Glaucoma, Cataract, Pterygium, Retinopathy, Eye Infection, Retinal Disorders, Uveitis, and Others.

By Product Type- OTC Drugs, and Prescription Drugs.

By Drug Class- Anti-allergy, Anti-inflammatory, Anti-VEGF (Vascular Endothelial Growth Factor), Anti-glaucoma, Antibacterial, and Others.

By Treatment Type- Drugs, Devices, Others.

By Geography- North America (U.S., Canada, Mexico), Europe (Germany, United Kingdom (U.K.), France, Italy, Spain, Russia, and Rest of Europe), Asia Pacific (China, Japan India, South Korea, Australia, and New Zealand, and Rest of Asia Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), and Rest of the World (the Middle East, and Africa).

Key Takeaways

Geographically, North America held a dominant market share in the year 2021 on account of increasing pharmaceutical industries. Asia-Pacific is expected to offer lucrative growth opportunities to the manufacturers owing to the increasing manufacturing of ophthalmic products in the pharmaceutical industries. The proliferation of ophthalmic products is predicted to augment the market growth during the forecast period of 2022-2027.

The growing number of ophthalmic pharmaceutical companies entering into strategic initiatives coupled with rising awareness regarding gene therapies are estimated to drive the market growth of the Vision Disorders Market. The growing number of patent expiry of blockbuster drugs poses threat to the Vision Disorders Market growth.

A detailed analysis of strengths, weaknesses, opportunities, and threats will be provided in the Vision Disorders Market Report.

Vision Disorders Market: Market Share (%) by region, 2021

For more details on this report - Request for Sample

Vision Disorders Market Segment Analysis – By Disease Type

Vision Disorders Market based on disease type can be further segmented into Dry Eye, Eye Allergies, Glaucoma, Cataract, Pterygium, Retinopathy, Eye Infection, Retinal Disorders, Uveitis, and Others. The Cataract segment held a dominant market share in the year 2021 and is estimated to be the fastest-growing, with a CAGR of 8.1% over the forecast period of 2022-2027. The increasing prevalence of cataracts is consequently increasing the Eye disorders Market. According to WHO, in 2019, In underdeveloped countries, the occurrence of cataracts similarly rises with age, though it begins sooner in life and is more common. Visually significant cataracts, for example, occurred 14 years earlier in an Indian study than in a comparable study in the United States. The age-adjusted prevalence of cataracts in India was three times that of the United States, with 82 percent of Indians aged 75 to 83 years old having visually significant cataracts or aphakia, compared to 46 percent of those aged 75 to 85 years in the United States (senile lens changes associated with a visual acuity of 6/9 or worse, or a history of cataract extraction). Moreover, at the same point, glaucoma prevalence is also increasing. Hence, cataracts and glaucoma are expected to propel the market of eye disorders in the forecast period 2022-2027.

Vision Disorders Market Segment Analysis – By Drug class

Vision Disorders Market based on Drug class can be further segmented into Anti-allergy, Anti-inflammatory, Anti-VEGF (Vascular Endothelial Growth Factor), Anti-glaucoma, Antibacterial, and Others. The Risk Management & Safety Solution segment held a dominant market share in the year 2021 and is estimated to be the fastest-growing, with a CAGR of 8.9% over the forecast period of 2022-2027. Owing to the increasing prevalence of eye diseases especially age-related macular degeneration, and diabetic retinopathy. Anti-VEGF drugs prevent aberrant blood vessels from leaking, developing, and bleeding beneath the retina. The protein vascular endothelial growth factor (VEGF) encourages the formation of new blood vessels. It also renders blood vessels more prone to leakage. Anti-VEGF drugs block the formation of new blood vessels. Anti-VEGF medication has been approved for age-related macular degeneration, diabetic retinopathy, retinal vein occlusion, and myopic choroidal neovascularization in the treatment of vascular and exudative diseases of the retina. Lucentis (ranibizumab) and Avastin are the two most extensively utilized medications at the moment (bevacizumab). Both medications are monoclonal antibodies that attach to each of the three types of VEGF, hence expanding the segment growth.

Vision Disorders Market Segmentation Analysis- By Geography

The Vision Disorders Market based on Geography can be further segmented into North America, Europe, Asia-Pacific, South America, and the Rest of the World. North America held a dominant market share of 31% in the year 2021 as compared to the other counterparts on account of increasing pharmaceutical industries. Furthermore, the presence of prominent competitors in this area, such as Pfizer, Inc., and Alcon, is projected to boost the market growth. For example, Alcon got FDA approval for Pataday Once Daily Relief and Pataday Twice Daily Relief for OTC sale in the United States in February 2020. The Pataday brand is used to treat itching and allergies in the eyes.

However, Asia-Pacific is estimated to be the fastest-growing over the forecast period of 2022-2027 on account of rising healthcare expenditure, and demand for better healthcare facilities. Local businesses are launching strategic endeavors to create and market innovative patient treatment solutions. As a result, market growth is likely to accelerate. Bridge Biotherapeutics, Inc., for example, acquired an early-stage drug candidate for the treatment of a back-eye disorder from Konkuk University (KU) in February 2020. The therapeutic candidate is an inhibitor of a yet-to-be-identified target protein.

Vision Disorders Market Drivers

Pharmaceutical businesses in the ophthalmic field are embarking on strategic efforts that are propelling the market forward

Ophthalmic pharmaceutical firms are pursuing strategic efforts such as collaborations, acquisitions, and partnerships to add new clinical-stage prospects to their product pipelines, which is projected to enhance the market. Rising ophthalmic pharmaceutical business owing to increasing prevalence of eye disorders. According to the World Health Organization, over 2.2 billion individuals will have a vision impairment or blindness in 2021, with at least 1 billion of those having a vision impairment that can be avoided. Those with limited or severe vision impairment due to unresolved refractive error (123.7 million), cataract (65.2 million), glaucoma (6.9 million), corneal opacities (4.2 million), diabetic retinopathy (3 million), and trachoma (2 million), as well as those with imminent vision impairment due to unspecified presbyopia (1.2 billion) (826 million). The growing senior population is exacerbating the prevalence of ocular illnesses, with uncorrected refractive errors and cataracts being the leading causes of vision impairment. The majority of people with vision problems are above the age of 50, enhancing the Vision Disorders Industry.

Rising prevalence of lifestyle changing diseases, especially diabetes is driving the Market for Vision Disorders

According to CDC, in 2021, Diabetic retinopathy (DR) is a common diabetic condition. It is the primary cause of blindness in adults in the United States. Progressive damage of the blood vessels of the retina, the light-sensitive tissue at the back of the eye that is required for good vision, characterizes it. Mild nonproliferative retinopathy (microaneurysms), moderate nonproliferative retinopathy (blockage in some retinal vessels), severe nonproliferative retinopathy (more vessels are blocked, depriving the retina of blood supply, resulting in the formation of new blood vessels), and proliferative retinopathy (growth of new blood vessels) are the four stages of DR (most advanced stage). Both eyes are generally affected by diabetic retinopathy.

Disease management, which includes adequate control of blood sugar, blood pressure, and lipid abnormalities, reduce the risk of DR. Early detection and treatment of DR lessen the risk of vision loss; nevertheless, up to 50% of patients do not have their eyes tested or are detected too late for effective therapy. It is the primary cause of blindness among working-age adults in the United States, ages 20 to 74. Retinopathy and vision-threatening retinopathy impact an estimated 4.1 million and 899,000 Americans, respectively, thereby driving the market growth.

Vision Disorders Market Challenges

The increasing number of blockbuster medicine patents expiring is projected to stifle Market growth of Vision Disorders

Pharmaceutical businesses will lose exclusivity when their patents expire, but medication producers will be granted new chances and difficulties as the generic competition enters the market. The introduction of generic glaucoma eye drops to the market has lowered patient expenses and increased adherence in some patients thereby decreasing the prevalence of glaucoma disorder Market. For instance, Prostaglandin analogs are anticipated to cost patients more than $100 per month on average across the country. When the first generic prostaglandin analog was introduced in 2011, it was projected that patients switching to the generic version would save more than $1,300 per year. 5 A 30-day prescription for generic latanoprost costs between $19 and $30, according to recent data on www.GoodRx.com, where we practice in mid-Missouri, whereas the same prescription for Xalatan (latanoprost ophthalmic solution; Pfizer) costs between $139 and $154. Hence, the increasing number of blockbuster medicine patents expiring is projected to stifle Market growth of Vision Disorders.

Vision Disorders Industry Outlook

Product launches, mergers and acquisitions, joint ventures, and geographical expansions are key strategies adopted by players in the Vision Disorders Market. The top 10- Vision Disorders Market companies are-

Croda International Plc

AbbVie Inc

Aerie Pharmaceuticals, Inc.

Novartis AG

AkzoNobel N.V.

F. Hoffmann-La Roche Ltd.

Evonik Industries

PolyOne Corporation

DuPont

Addcomp Holland

Recent developments

In November 2021, Aerie Pharmaceuticals received marketing authorization approval from the European Commission for its Roclanda (netarsudil and latanoprost ophthalmic solution) 0.02%/0.005% for the reduction of elevated IOP in adult patients with primary open-angle.

In October 2021, Abbvie Inc. launched a new drug named VUITYTM (pilocarpine HCl ophthalmic solution). Presbyopia, often known as age-related hazy near vision, is treated with VUITYTM (pilocarpine HCl ophthalmic solution) 1.25 percent in adults. VUITY is the first and only FDA-approved eye drop to treat this prevalent and degenerative eye disease, which affects 128 million Americans, or over half of the adult population in the United States.

In September 2021, Novartis acquired Arctos Medical, bolstering its ophthalmology portfolio with a pre-clinical optogenetics-based AAV gene therapy program and Arctos' proprietary technology. Novartis' dedication to finding solutions for individuals with vision loss, as well as the potential of optogenetics as a foundation for successful therapeutics, is shown in this acquisition.

0 notes

Text

Healthcare/Medical Simulation Market - Forecast, 2022 - 2027

Healthcare/Medical Simulation Market Size is estimated to reach $4.1 billion by 2027. Furthermore, it is poised to grow at a CAGR of 15.4% over the forecast period of 2022-2027. Medical simulation, or more generally, healthcare simulation, is a subset of simulation that is used in medical education and training in a variety of sectors. Simulations can take place in a classroom, in a situational setting, or in a venue dedicated to a simulation exercise. It can include artificial, human, or a combination of artificial and human patients, educational papers with full simulated animations, casualty assessment in homeland security and military circumstances, emergency response, and support virtual health activities with holographic simulation. Some are Disease-specific such as cardiovascular simulators are available. Learners can use Patient simulators to practice a variety of skills, including those that cannot be safely or ethically mimicked with actual patients. task trainers and tabletop models cater to more specific skill development requirements. Software is used like Simio Software for healthcare simulation modeling is powerful object-based simulation software. Furthermore, its primary goal in the past was to educate medical professionals on how to decrease errors in surgery, prescriptions, crisis interventions, and general practice. It is currently also utilized to teach pupils anatomy, physiology, and communication throughout their schooling when combined with debriefing approaches. The growing number of medical students and the lack of human bodies are some of the factors driving the Healthcare/Medical Simulation Market growth during the forecast period 2022-2027.

Healthcare/Medical Simulation Market Report Coverage

The report: “Healthcare/Medical Simulation Market Forecast (2022-2027)", by Industry ARC covers an in-depth analysis of the following segments of the Healthcare/Medical Simulation Market.

By Product and Service- Medical simulation anatomical models, Web-Based Simulation, Medical Simulation Software, Simulation Training Services.

By End-Users- Academic Institutes, Hospitals, Military Organizations, Others.

By Geography- North America (U.S., Canada, Mexico), Europe (Germany, United Kingdom (U.K.), France, Italy, Spain, Russia, and Rest of Europe), Asia Pacific (China, Japan India, South Korea, Australia, and New Zealand, and Rest of Asia Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), and Rest of the World (the Middle East, and Africa).

Key Takeaways

Geographically, North America held a dominant market share in the year 2021 on account of increasing medical students and practical training.

Growing medical students is estimated to drive the market growth of the Healthcare/Medical Simulation Market. Lack of finances for Healthcare/Medical Simulation poses threat to the market growth.

A detailed analysis of strengths, weaknesses, opportunities, and threats will be provided in the Healthcare/Medical Simulation Market Report.

Healthcare/Medical Simulation Market: Market Share (%) by region, 2021

https://lh3.googleusercontent.com/v0MmVm2jK8qra7qNinBZb2yVW4ab-IgHCDD7zAQ324qfGv85YxwqUasGtFbQfBFdCBaHoq4hXVfU61Fj7QYnu0-efmnQTqx6RuUwlBBsCNw9OuRiaGPzbQfraRXkJ-SoImtrCjJnSfGUQoF-qQ

For More Details on This Report - Request for Sample

Healthcare/Medical Simulation Market Segmentation Analysis- By Product and Service

Healthcare/Medical Simulation Market based on the Product and Service can be further segmented into medical simulation anatomical models, Web-Based Simulation, Medical Simulation Software, and Simulation Training Services. Medical simulation anatomical models held a dominant market share in the year 2021 and are estimated to be the fastest-growing, with a CAGR of 16.7% over the forecast period of 2022-2027. According to Medical news 2020, In medical specialties where anatomy manipulation is not part of the procedure, the anatomical model is just as important for practicing placing the patient in the correct position before the procedure begins especially given the underappreciated risk of injuries that can result from incorrect positioning across disciplines. Another consideration is that all surgical operations need tight collaboration among team members, including the interplay of various tools and the proper positioning of team members around the patient. It's easy to see how a facility like this, with little physical space, makes it difficult for trainees to work and coordinate movement. For instance, Arthroscopy is an excellent illustration of how VirtaMed Knee, Shoulder, Hip, and Ankle models may be physically manipulated and positioned during simulation for a variety of procedural demands, such as obtaining the required visibility of the operating perspective, exactly like a surgeon in real life. Hence, medical simulation anatomical models are dominating the market.

Healthcare/Medical Simulation Market Segmentation Analysis- By End User

Healthcare/Medical Simulation Market based on end-user can be further segmented into Academic Institutes, Hospitals, Military Organizations, Others. The academic Institutes segment held a dominant market share in the year 2021 and is estimated to be the fastest-growing, with a CAGR of 17.1% over the forecast period of 2022-2027 owing to the rising number of medical students. According to AAMC, Simulation is an instructional technique that uses standardized patients, manikins, virtual reality, or a mix of these to imitate parts of health care. Patients, learners, medical instructors, and actual care professionals all benefit from simulation. The research on patient safety suggests that simulation can help learners prepare for clinical practice without putting patients in danger. Technical methods, clinical assessment, teamwork, and communication are just a few of the areas where this has been investigated. Since it allows learners to go through a controlled curriculum and undertake a standardized assessment, simulation provides a competency-based learning and assessment alternative to the unpredictable clinical arena. Simulation is supported by pedagogical theory, which holds that competence is gained via repeated practice led by feedback and reflection. Therefore, academic Institutes dominate the market.

Healthcare/Medical Simulation Market Segmentation Analysis- By Geography

The Healthcare/Medical Simulation Market based on Geography can be further segmented into North America, Europe, Asia-Pacific, South America, and the Rest of the World. North America held a dominant market share of 34% in the year 2021 as compared to the other counterparts on account increased number of healthcare professionals and demand for online and virtual training, all of which can be related to the COVID19 pandemic, helping in generating considerable income in the future years.

However, Asia-Pacific is estimated to be the fastest-growing over the forecast period of 2022-2027. Asia-Pacific is estimated to offer lucrative growth opportunities to the manufacturers owing to the increasing number of patients and demand for better healthcare facilities as well as the boost in the investments done by government and private companies in the pharma industry. The proliferation of Rheumatoid arthritis is predicted to augment the market growth during the forecast period of 2022-2027.

Healthcare/Medical Simulation Market Drivers

Limited Access To Patients Is Driving The Market Growth.

Medical simulators have established a valuable place in medical education across the world since they mimic human traits. Owing to limited access to patients and the need to preserve patient safety throughout training, simulation is increasingly being used in professional training programs and conventional learning. Students can use the simulation to hone their clinical and critical thinking abilities in preparation for high-risk situations. When compared to pre-education or simulation alone, pre-education plus simulation substantially improves student knowledge, confidence in performance, ability in nursing practice, and satisfaction with learning techniques. According to the World Health Organization (WHO), patient safety is one of the most important worldwide public health concerns in 2019, with a one-in-300 probability of a patient being harmed while receiving medical treatment. Moreover, as numerous startups seek chances in this industry, the market is projected to become extremely competitive. CAE, for example, achieved ISO 13485:2016 accreditation for its facilities in Montreal (Canada) and Sarasota (USA) in December 2020. (U.S.). Both are facilities for medical devices and quality management systems. Military branches all across the world are changing their training and education models. As a result, in medicine, simulation has a lot of potential for improving multidisciplinary medical teaching. Hence, limited access to patients is a driving factor for the market.

Rising Healthcare Professionals Is Enhancing The Healthcare/Medical Simulation Industry.

Health care professionals are increasing steading as the number of patients is rising simultaneously. For instance, during COVID 19 calls for health care professionals has received from almost all countries. The countries where health care professionals are lacking suffered owing to pandemics. Moreover, for treatment and vaccination pharmacist, nurse, and other health care professionals also plays a major role in patient cure and safety. According to FSMB 2019, Since 2010, the United States has recruited 168,691 physicians to its medical workforce, serving a population of 331 million people. The number of freshly licensed physicians entering the workforce continues to fuel growth. Hence, the rising number of physicians is estimated to propel the market.

Healthcare/Medical Simulation Market Challenges

Short Supply Of Finances Is Restraining The Market Growth.

Owing to the high expense of high-fidelity simulators and virtual environments, the construction of simulated learning environments and simulation programs necessitates large financial inputs. Medical simulation training facilities rely on government and private financing in the majority of situations. Rapid advances in medical technology, decreased reimbursement for clinical services, rising healthcare professional costs, and decreases in federal GME payments have all contributed to a decrease in financing from government and private institutes in recent years. The expense of running a simulation lab is fairly high. A single high-fidelity simulator, including the monitoring system and other required equipment, can cost up to $200,000. To recreate the experience of treating actual patients in a real hospital, synthetic body fluids, replacement skins, bandages, syringes, and other materials are required. Thus, the short supply of Finances is estimated as a restraining factor for the market.

Healthcare/Medical Simulation Industry Outlook

Product launches, mergers and acquisitions, joint ventures, and geographical expansions are key strategies adopted by players in the Healthcare/Medical Simulation Market. The top 10- Healthcare/Medical Simulation Market companies are-

IngMar

Synaptive Medical

HRV Simulation

Symgery

Synbone

Medical-X

Altay Scientific

VirtaMed AG

Gaumard Scientific Co.

CAE Inc.

Recent Developments

In August 2021, IngMar Medical announced the launch of RespiPro, its next-generation respiratory and ventilation training solution. Using their own genuine ventilators and breathing equipment, educators instruct all levels of learners across many disciplines on the complete breadth of respiratory methods using RespiPro. The ASL 5000TM breathing simulator, as well as easy-to-use software, a true-to-life patient monitor, and a respiratory-focused manikin on a small ICU bed, are all included in the package.

In July 2021, SYNBONE AG announced the launch of the Skull Holder System for use in Trauma, neurosurgery education, and orthognathic surgery. Skull Holder System used specifically for CMF Trauma, Orthognathic, and Neuro Surgery Education. With or without vice attachment, this ingenious and multipurpose system holds all SYNBONE® skulls, half skulls, and maxillas. Two adapters, a 3-pin adapter, and a Hemi-skull adapter allow for a 360° step-less rotation of the skulls and a wide range of applications. The system comes with a sturdy, waterproof traveling container with foam inlays. This dependable Skull Holder System ensures a uniform schooling idea while also impressing its quality and effectiveness.

In May 2021, CAE Inc. announced the launch of CAE Vimedix 3.2, a high-fidelity ultrasound simulator with enhanced 3D and 4D scanning capabilities. CAE Vimedix is a high-fidelity ultrasound simulator that combines heart, lung, abdominal, and OB-GYN ultrasound training into a single platform. CAE Vimedix speeds the development of important psychomotor and cognitive abilities for ultrasound probe handling, picture interpretation, diagnoses, and clinical decision-making using its software and manikin-based system, as well as live, remote learning elements.

#Healthcare/Medical Simulation Market share#Healthcare/Medical Simulation Market size#Healthcare/Medical Simulation Market forecast

0 notes

Text

Neurotherapeutic Drugs Market - Forecast, 2022-2027

The Neurotherapeutic Drugs Market size is estimated to reach $112.3 billion by 2027, growing at a CAGR of 5.4% during the forecast period 2022-2027. Neurotherapeutic drugs market research involves reporting on the segments, drivers, challenges and competitive landscape related to the Neurotherapeutic Drugs Market. In the UK, Neurotherapeutics Solutions Ltd, a medical device firm, aims at neurological ailments with an initial focus on products to help inpiduals with Tourette Syndrome improve their condition without surgical or pharmaceutical interferences. In the U.S., some of the biggest key players are Abbott Laboratories, Inc. and Becton, Dickinson and Company. The increasing predominance of neurological conditions among the elderly is set to drive the Neurotherapeutic Drugs Market. The growing awareness of the Neurotherapeutic drugs market in the U.S. is set to propel the growth of the Neurotherapeutic Drugs Industry during the forecast period 2022-2027. This represents the Neurotherapeutic Drugs Industry Outlook.

Neurotherapeutic Drugs Market Report Coverage

The report: “Neurotherapeutic Drugs Market Report - Forecast (2022-2027)” by IndustryARC, covers an in-depth analysis of the following segments in the Neurotherapeutic Drugs Market.

By Type: Peripheral Nervous System (PNS) Disorders, Autonomous Nervous System (ANS) Disorders, Central Nervous System (CNS) Disorders and Others. By Distribution Channel: Hospital Pharmacies, Retail Pharmacies and Online Pharmacies. By Geography: North America (the US, Canada and Mexico), Europe (Germany, France, the UK, Italy, Spain, Russia and the Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and the Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and the Rest of South America) and the Rest Of The World (the Middle East and Africa).

Key Takeaways

Geographically, North America (Neurotherapeutic Drugs market share) accounted for the highest revenue share in 2021 and it is poised to dominate the market over the period 2022-2027 owing to the principal technological progress in the Neurotherapeutic drugs market in the North American region, particularly the US.

Neurotherapeutic Drugs Market research and growth are being driven by the expanding population of the elderly. However, certain side-effects related to surgical procedures and medications are some of the major factors hampering the growth of the Neurotherapeutic Drugs Market.

Neurotherapeutic Drugs Market Detailed Analysis on the Strength, Weaknesses and Opportunities of the prominent players operating in the market would be provided in the Neurotherapeutic Drugs Market report.

Neurotherapeutic Drugs Market: Market Share (%) by Region, 2021

For more details on this report - Request for Sample

Neurotherapeutic Drugs Market Segment Analysis - By Type

The Neurotherapeutic Drugs Market based on type can be further segmented into Peripheral Nervous System (PNS) Disorders, Autonomous Nervous System (ANS) Disorders, Central Nervous System (CNS) Disorders and Others. The Central Nervous System (CNS) Disorders Segment held the largest share of the Neurotherapeutic Drugs market in 2021. This growth is owing to the increasing predominance of central nervous system disorders like seizures and epilepsy. The surging application of CNS agents like antiparkinsonian drugs is further propelling the growth of the Central Nervous System (CNS) Disorders segment.

Furthermore, the Autonomous Nervous System (ANS) Disorders segment is estimated to grow at the fastest CAGR of 6.6% during the forecast period 2022-2027 owing to the increasing predominance of autonomous nervous system disorders which can happen alone or as the outcome of another ailment, like Parkinson's disease, alcoholism and diabetes.

Neurotherapeutic Drugs Market Segment Analysis - By Distribution Channel

The Neurotherapeutic Drugs Market based on distribution channels can be further segmented into Hospital Pharmacies, Retail Pharmacies and Online Pharmacies. The Hospital Pharmacies Segment held the largest share of the Neurotherapeutic Drugs market in 2021. This growth is driven by the surging availability of neurotherapeutic drugs in hospital pharmacies to treat neurological ailments. The increasing inclination of patients to instantaneously purchase neurotherapeutic medications from hospital pharmacies on the prescription of physicians is further propelling the growth of this segment. Furthermore, the Online Pharmacies segment is estimated to grow with the fastest CAGR of 6.9% during the forecast period 2022-2027 due to the soaring application of online pharmacies by patients to readily purchase the Neurotherapeutic Drugs required as prescribed by physicians right at the click of the mouse with home delivery options and discounted rates.

Neurotherapeutic Drugs Market Segment Analysis - By Geography

North America dominated the Neurotherapeutic Drugs market with a 39% share of the overall market in 2021. The growth of this region is owing to the increasing predominance of neurological ailments, boosting the neurotherapeutic drugs market in the U.S. The existence of key players like Abbott Laboratories, Inc. is further propelling the growth of the Neurotherapeutic Drugs Industry, thereby contributing to the growth of the Neurotherapeutic Drugs Industry Outlook, in the North American region. Furthermore, the Asia-Pacific region is estimated to be the region with the fastest CAGR over the forecast period 2022-2027. This growth is driven by the factors like the expanding healthcare facility upgrade in the Asia-Pacific region. The powerful economic growth in countries like India, China, Japan and Malaysia is further fueling the progress of the Neurotherapeutic Drugs Market in the Asia-Pacific region.

Neurotherapeutic Drugs Market Drivers

Surging Investigations Pertaining to NMDA Antagonists as Neurotherapeutic Drugs:

As per World Health Organization (WHO), in 2019, 301 million people were living with an anxiety ailment, involving 58 million children and teenagers. Antagonists of the N-methyl-D-aspartate (NMDA) subtype of glutamate (Glu) receptor have become the target of appreciable attention as potential neurotherapeutic agents in view of growing evidence showing NMDA receptors in acute central nervous system (CNS) injury syndromes like stroke, trauma and status epilepticus. Additionally, NMDA receptor antagonists are of possible interest for the clinical handling of neuropathic pain and averting the establishment of tolerance to opioid analgesics. The surging investigations pertaining to NMDA Antagonists as neurotherapeutic drugs are therefore fueling the growth of Neurotherapeutic Drugs Market Research during the forecast period 2022-2027.

Soaring Therapeutic Innovations in Neuroscience:

As per World Health Organization (WHO), 1 in every 8 people in the world lives with a mental ailment. Stephenson et al. examine whether and how creative trial designs and technologies can propel the progress of treatments for typical neurological ailments like Parkinson’s disease. These technologies include multiarm adaptive platform designs and digital health tools to supervise progression in rare ailments like Duchenne muscular dystrophy and amyotrophic lateral sclerosis (ALS). Novel platforms including data from finished clinical trials, registries, natural history investigations and preclinical data have been examined. The soaring therapeutic innovations in Neuroscience are therefore driving the growth of the Neurotherapeutic Drugs Industry, thereby contributing to the Neurotherapeutic Drugs Industry Outlook during the forecast period 2022-2027.

Neurotherapeutic Drugs Market Challenges

Scientific Challenges in Neurotherapeutic Pharmaceutical Development:

Generally, sales of CNS therapeutics include nearly 15% of total pharmaceutical sales and $30 billion, globally. Around two-thirds of these sales are for psychiatric treatments. The scientific challenges for therapeutics developers are high in neurotherapeutics. While the move is made from symptomatic treatments to mechanistically targeted cures, there is a battle to base development on fields of knowledge that are very quickly altering and far from complete. Also, the comprehension of the interactions between factors is fragmentary at best in such cases. Neurotherapeutics developers encounter unexpectedly great failure rates and enormous attendant expenses that must be covered by the tiny number of therapeutics that triumph. These issues are thus hampering the growth of the Neurotherapeutic Drugs Market.

Neurotherapeutic Drugs Industry Outlook

Novel and innovative device launches and expanding R&D activities are key strategies adopted by players in the Neurotherapeutic Drugs Market. The top 10 companies in the Neurotherapeutic Drugs market are:

Abbott Laboratories, Inc.

Becton, Dickinson and Company

Novartis AG

Johnson & Johnson

Pfizer, Inc.

Sanofi-Aventis

Biogen, Inc

GlaxoSmithKline, Inc.

AstraZeneca plc

Merck & Co.

Recent Developments

In September 2021, Merck and Acceleron Pharma Inc. declared that the firms have entered into a definitive agreement. Under this agreement, Merck would gain Acceleron for $180 per share in cash. The acquisition completes Merck’s cardiovascular pipeline.

In April 2021, Merck declared the successful finishing of the cash tender offer, by way of a subsidiary. This was performed for all of the outstanding shares of common stock of Pandion Therapeutics, Inc. As of the tender offer termination, 27,770,123 shares of the common stock of Pandion were validly tendered.

In January 2021, Merck declared the acquisition of AmpTec. Based in Hamburg, Germany, AmpTec is a superior, mRNA contract development and manufacturing organization (CDMO). The deal consolidates Merck's capacities to establish and produce mRNA for its customers.

#Neurotherapeutic Drugs Market share#Neurotherapeutic Drugs Market size#Neurotherapeutic Drugs Market forecast

0 notes

Text

Rehabilitation Products Market - Forecast, 2022-2027

The Rehabilitation Products Market Size is estimated to reach $20.1 billion by 2027 and is poised to grow at a CAGR of 6.3% during the forecast period of 2022-2027. Rehabilitation is the treatment designed to facilitate the process of recovery from the state of injury or illness. The most important feature of any Rehabilitation Aid is its ability to provide maximum support without causing any further discomfort to the patient who is already in pain and needs medical beds, patient lifts, daily living aids and mobility equipment. The increasing number of disabilities owing to acute illness, disease, injuries, accidents and the increasing geriatric population drive the market growth. According to Global RA Network, there are more than 350 million people suffering from arthritis in 2021 and more than 22% of adults around the world, who are older than 40, have knee osteoarthritis. According to World Health Organization, by 2060, one in six people in the world would be aged 60 or above, and by 2050 two-thirds of the world population would be over the age of 60 years. Such a rising elderly population and increasing disabilities fuel the growth of rehabilitation products market size. Such increasing prevalence of disabilities and the growing demand for various rehabilitation products in the market create lucrative growth opportunities for key market players as well as the rehabilitation products industry. To fulfill market demand, key market players focused on the joint venture and expansion of business. For instance, in January 2022, MicroPort RehabTech, a subsidiary of MicroPort Scientific Corporation, unveiled a series of new products under its integrated solution for musculoskeletal rehabilitation at a launch event held in Beijing. Such rapid enhancement in technology and rising global need for Rehabilitation Products would drive the growth of the Rehabilitation Products Industry during the forecast period 2022-2027.

Rehabilitation Products Market Report Coverage

The report: “Rehabilitation Products Market Forecast (2022-2027)" by Industry ARC, covers an in-depth analysis of the following segments in the Rehabilitation Products Market.