marketsreport-blog

Semiconductor and Electronics Market Research Reports & Consulti

266 posts

Don't wanna be here? Send us removal request.

Last Seen Blogs

madurohunt

Unbetitelt

genealogical-analysis

a-priori

lgbtlunaverse

I don't have to woobify the author does it for me

myanonymuniverse

Nordmädchen

standfordslostlawstudent

Azazel's Special Child

Text

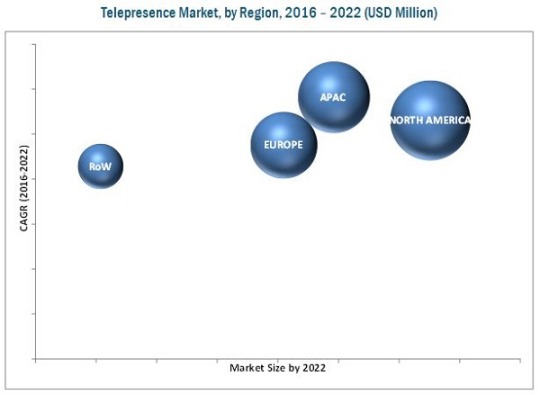

Telepresence Market Is Forecast To Reach $ 2.63 Billion By 2022

According to the new report "Telepresence (Videoconferencing) Market by Component (Hardware, Software and Service), System Type (immersive Telepresence, Personal Telepresence, Holographic Telepresence, and Robotic Telepresence), Industry, and Geography - Global Forecast to 2022", the global telepresence market is expected to reach USD 2.63 Billion by 2022 at a CAGR of 19.6% between 2016 and 2022. Factors such as technological superiority, reduced costs of travel for small and large enterprises, minimized operational cost, and growing demand for robotic telepresence are the key drivers for telepresence market.

Browse 68 market data Tables and 53 Figures spread through 152 Pages and in-depth TOC on "Telepresence (Videoconferencing) Market - Global Forecast to 2022"

https://www.marketsandmarkets.com/Market-Reports/telepresence-videoconferencing-market-193932914.html

Early buyers will receive 10% customization on reports.

Software component held the largest market share in 2015 and is expected to exhibit high growth during the forecast period

Software is major component in a telepresence system. A telepresence system works on various software such as cloud computing and CAD among others. The updating of software provides easy access to IP networks and flexibility to collaborate with devices such as desktops, tablets, and smartphones. These periodic upgrades contribute toward the growth of the telepresence market for software.

Telepresence helps reduce travel costs in the enterprise sector

Many small to large business sectors use telepresence systems for virtual meetings with their distantly located customers, employees, or partners. It facilitates efficient communication with people across the globe, without having to travel physically. This significantly reduces the travel expenses; this is one of the major driving factors for the growth of the telepresence market, globally.

North America held the largest share of the telepresence market

The major tech companies such as Cisco Systems Inc. (U.S.), Polycom Inc. (U.S.), ZTE Corp. (U.S.), Avaya Inc. (U.S.) and Vidyo Inc. (U.S.) among others has been developing telepresence systems for various verticals; this is one factor responsible for the dynamic growth of the telepresence market in North America. The U.S. held the largest market share in North America, in 2015. Additionally, their application in the medical sector has fueled market growth.

The market in APAC is expected to grow at the highest CAGR during the forecast period. The increasing number of businesses in APAC has increased the demand for videoconferencing technologies. The use of advanced videoconferencing such as telepresence help users experience close-to-real presence of a person in some other part of the world. Japan, China, and India hold a large share of this market in APAC.

Some of the players operating in APAC are Cisco Systems, Inc. (U.S.), Polycom Inc. (U.S.), Avaya Inc. (U.S.), ZTE Corp. (U.S.), Huawei Technologies Co., Inc. (China), VGo Communications, Inc. (U.S.), Vidyo Inc. (U.S.), Teliris Inc. (U.K.) and Array Telepresence (U.S.) among others.

Don’t miss out on business opportunities in Telepresence Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

Digital Temperature and Humidity Sensor Market Reach A Value Of $1,084.38 Million Forecast Till 2020

According to a new market research report “Digital Temperature and Humidity Sensor Market for Automotive Application by Technology (CMOS, MEMS, TFPT), Packaging Type (SMT, Pin Type), Application (Powertrain, Body Electronics, Alternative Fuel Vehicle), & Geography Forecast to 2020”, the market size of digital temperature & humidity sensors for automotive applications was worth $1,084.38 Million in 2013 and is expected to reach $2,129.68 Million, at a CAGR of 11.05% between 2014 and 2020.

Browse 72 market data tables and 63 figures spread through 141 pages and in-depth TOC on “Digital Temperature and Humidity Sensor Market for Automotive Application - Forecast to 2020"

https://www.marketsandmarkets.com/Market-Reports/automotive-temperature-humidity-sensor-market-187951783.html

Early buyers will receive 10% customization on reports.

In the automotive industry, temperature & humidity sensors are used for various applications. These include powertrain, body electronics, and alternative fuel vehicles (AFV). Digital sensors offer many advantages over conventional sensors such as high performance and accuracy coupled with low cost, easy implementation, no requirement for complex calibration, and low power consumption among others.

This report covers automotive temperature & humidity sensors on the basis of different technologies and packaging types. It also segments the smart sensors market on the basis of various applications like powertrain, body electronics, alternative fuel vehicle (AFV); and geographically into the Americas, Europe, Asia-Pacific, and Rest of the World.

The automotive temperature & humidity sensor market statistics have been included pertaining to various aspects such as technology, packaging type, applications, and geography. The major types of technologies covered in the report are CMOS, MEMS, and TFPT.

Apart from the market statistics, the report also includes qualitative analysis such as value chain with detailed process flow diagrams; market dynamics such as drivers, restraints, and opportunities; winning imperatives; and industry trends for the overall smart sensor market.

Don't miss out on business opportunities in Digital Temperature and Humidity Sensor Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

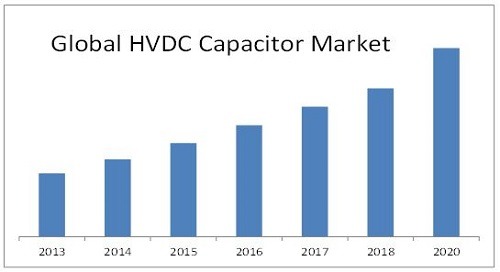

HVDC Capacitor Market Scope, Application and Development Forecast 2020

The Global HVDC capacitor Market is estimated to grow at a CAGR of 16.02% to reach $3,890.00 million by 2020. HVDC capacitors aim at optimizing safety, reliability, and cost-effectiveness. HVDC capacitors assure safety and reliability by identifying flaws and defects in products without disrupting operations or delaying processes.

Key applications of high voltage capacitors included in the report are commercial, industrial, energy and power sector, and defense sectors. Among all the applications, the energy and power sector is expected to be the largest contributor to the overall HVDC capacitor market, which held ~50% share. While smaller application sectors, such as defense and others (medical, electronics, and so on), which accounted for about 17% of high voltage capacitors market in 2013, are also expected to generate more demand over the coming years.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=175421495

The report discusses two of the HVDC capacitor technologies - Line Commutated Converter and Voltage Source Converter. It also covers the market for geographic regions comprising North America, Europe, Asia-Pacific, and the Rest of the World (RoW). In 2013, Europe was the largest geography in terms of market size for the HVDC capacitor market. APAC, Europe, and RoW are also considered as promising markets, along with China, Japan, India, Germany, and the Middle East, which provide impetus to the growth. It is expected that the high investments made by governments in the development of existing power infrastructure and other supportive government regulations to promote the use of renewable energy sources will help in the adoption of HVDC in the Americas.

The types of HVDC capacitor technologies covered in the report are Line Commutated Converter, Voltage Source Converter, and others. The applications of HVDC capacitors discussed in the report are commercial, industrial, energy and power, defense, and other sectors. The report also covers the market for the following types of HVDC capacitors - plastic film capacitors, aluminum electrolytic capacitors, ceramic capacitors, tantalum wet capacitors, reconstituted mica capacitors, and glass capacitors. The HVDC capacitor market for the geographic regions including Americas, Europe, and Asia-Pacific, and the Rest of the World (RoW) have also been included in the report.

The major drivers for the HVDC capacitor market are supportive government regulations, need for improved stability, and low transmission losses in the existing power infrastructure and demand driven by smaller, niche end-user segments. There are also some restraining factors for the market, such as high infrastructure cost and lack of standardization. A huge growth is expected for the HVDC capacitor industry, primarily due to the increasing popularity of renewable energy sources for power generation and huge demand generated for high voltage applications by smaller, niche end-user segments such as defense electronics, semiconductor manufacturing, medical electronics, and so on.

The report discusses the future of the global market with road-map, upcoming technologies, markets, and applications with respect to HVDC capacitors. The HVDC capacitor market is rapidly growing in the renewable energy sector, which represents potential end-users for this market. Key players in this industry include ABB Ltd. (Switzerland), Epcos AG (Germany), Siemens (Germany), Alstom SA (France), and others.

Don’t miss out on business opportunities in HVDC Capacitor Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

Voice over LTE Market Information Procurement and Data Analysis by 2018-2022

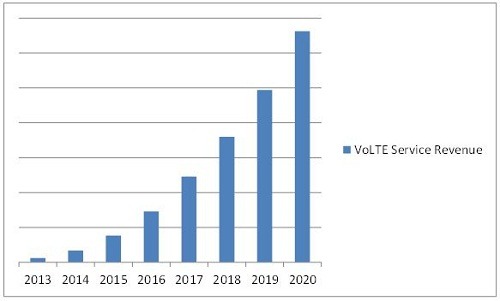

The Voice over LTE (VoLTE) Market for LTE is in the Americas and that for voice over Long-Term Evolution is in the Asia-Pacific region, which is expected to grow at a CAGR of 54.20% from 2014 to 2020. Based on the technology, the voice over LTE market can be divided into Circuit Switched Fallback (CSFB), Voice over IP multimedia subsystem (VoIMS), and Dual radio or Simultaneous Voice and LTE (SV LTE). The CSFB market accounted for the major share in 2013, but the VoIMS is expected to grow faster as compared to CSFB and SV LTE in the next 6 years.

Voice over LTE (VoLTE) empowers mobile network operators to offer rich voice, video, and messaging services as a core offering. Voice over LTE enables the operators to use data network to transmit voice services in small sized packets. It helps to increase spectrum efficiency and reduce operational and maintenance costs as only one network is used. Voice over LTE also enables operators to offer new set of standards based services referred to as Rich Communication Services or RCS which include video calling, real time language translation, video voice mail, and instant messaging. These advanced features will help mobile network operators to compete against OTT providers.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=142676771

The report provides the profiles of all the major companies in the LTE and voice over Long-Term Evolution market. The report also provides the competitive landscape of the key players, which indicates the growth strategy of the Voice over LTE Market in the industry. The report also covers the entire value chain for the market, right from the infrastructure provider to the subscriber. Along with the value chain, this report also provides an in-depth view on the technology, end-user devices; geographic analysis of the Long-Term Evolution market and technology; and geographic analysis of the voice over Long-Term Evolution market. The market for VoLTE is estimated to reach up to $6,624.04 million by 2020, at a CAGR of 64.40% from 2014 to 2020.

The report also provides the market dynamics such as drivers, restraints, opportunities and challenges for the voice over LTE market. Apart from the market segmentation, the report also includes the critical market data and qualitative information with regard to voice over Long-Term Evolution; along with the qualitative analysis, such as the Porter’s five force analysis, value chain analysis, and the market crackdown analysis.

Voice over LTE Market is perceived as a long term strategic solution for LTE, which makes use of IMS call control as defined by 3GPP TS 23.228 for LTE voice services delivery. IMS offers legacy voice services such as call originating or terminating, calling line identification, and supplementary services; as well as value added, advanced multimedia services such as video sharing. Voice over LTE is becoming a popular technology as it provides win-win situation for both the entities; that is, the mobile network operators and the subscribers. LTE offers twice the spectral efficiency of 3G/HSPA and more than six times efficiency as that of the GSM technology; this allows allocating more bandwidth for more data services. Reuse of existing 2G and 3G spectrum reduces the need for new spectrum. Optimization of network and simplification of service delivery help to reduce costs.

Key players in the LTE and voice over LTE market include Huawei Technologies Co. Ltd.(China), Nokia Solutions and Networks (Finland), Ericsson (Sweden), Alcatel-Lucent (France),LG Uplus (South Korea), SK Telecom (South Korea), Metro PCS (U.S.), AT&T Inc. (U.S.), KT Corp. (South Korea), and Verizon Wireless (U.S.),among others. The detailed explanation of the different market segments is given below:

Don’t miss out on business opportunities in Voice over LTE Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

Security Screening Market Growth, Demand, Opportunities and Forecast 2020

The global Security Screening Market is expected to reach $9.10 Billion by 2020; at an expected compound annual growth rate (CAGR) of 9.46% from 2014 to 2020. Security screening market is considered as one of the most important sectors as it involves the individual’s security at places such as airports, railways, stadiums, public places, border checkpoints, government applications, and private sectors, among others. Security screening helps to avoid financial, economic, and human loss. There has been an increase in unethical and unlawful practices in the world and this can be controlled with the help of the security screening products such as full body X-ray scanners, explosive trace detectors, electromagnetic metal detectors, and the biometric technology.

Biometrics technology is known in all the fields and is used more at airports and private sectors, such as for passports and in office premises. The important aspect of this technology is that it can be used with different measures such as face scanner, voice scanner, iris scanner, retina scanner, and fingerprint scanner. E-passports use biometrics technology; the initial E-passport was issued in Malaysia in March 1998. Since 2004, there has been a steady flow of countries joining the ranks of E-passport issuers. As of 2014, there are more than 100 countries using E-passports. This basically ensures the security and safety measures at airports and reduces use of fake passports. Recently, India announced that it will be issuing E-passports from 2015. Thus, the use of biometrics is increasing with the increasing need of security screening.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=264685413

Security screening market is growing well at airports, public places, and private sectors as compared to the other major application areas. The increasing number of airports is increasing the need for security screening.

In terms of the number of airports , the U.S. stands first, accounting for ~32% of the total airports in the world; followed by Brazil, Mexico, and Canada with ~10%, ~4%, and ~4% respectively. The security screening is done more at airports as compared to the other application areas of this market; thus, there is a huge scope for this market to grow in the aviation segment. There is a growing need for security screening in the public and private segments. Ensuring people’s safety at public places such as malls, hotels, casinos, hospitals, and banks is of utmost importance, so as to avoid terrorism and unlawful activities.

The security screening market is expected to witness more demand in the APAC region followed by North America as compared to the Europe and the Rest of the world, in the coming years. APAC is expected to grow ata CAGR of 10.14%, followed by North America, with a CAGR of 10.03% from 2014 to 2020. The total requirement of security screening is more in APAC as compared to other regions due to reasons such as the increasing number of terrorism and unlawful activities, greater number of public places and private sectors, among others.

Security screening market by geography is divided on the basis of the different geographical regions; namely North America, Europe, APAC, and Row. APAC is growing at a fast CAGR; itis expected to account for 10.14% share of the overall market from 2014 to 2020). Currently, North America occupies the major share of the market for screening in terms of market size, that is, ~38% of the total market. The main reason for the higher growth of these regions as compared to the Europe and the Rest of the World can be the rise in the amount of terrorism and unethical practices in these regions.

Brazil is expected to grow well due to the fact that the country is involved in major public events such as FIFA 2014 and the upcoming event – Rio 2016 Olympics; which involve huge amount of security screening of people and their belongings. In terms of the number of airports, Brazil stands second after North America, accounting for ~10% of the total airports in the world. Thus, the country can explore more in future in terms of the security screening market.

Market players involved in the development of the security screening are American Science and Engineering, Inc. (U.S.), Analogic Corporation (U.S.), Argus Global Pty Ltd (Australia), Aware Incorporation (U.S.), Digital Barriers plc. (U.K.), Implant Sciences Corporation (U.S.), Magal Security Systems Ltd (Israel), OSI Systems, Incorporation (U.S.), Safran SA (France), and Smiths Group plc. (U.K.).

Don’t miss out on business opportunities in Security Screening Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

Data Converter Market Growth, Share, Opportunities and Forecast by 2023

According to the new market research report "Data Converter Market by Type (Analog-to-Digital Converter and Digital-to-Analog Converter), Sampling Rate (High-Speed Data Converter and General-Purpose Data Converter), Application, and Region - Global Forecast to 2023", the data converter market is expected to grow from USD 3.52 Billion in 2017 to USD 5.08 Billion by 2023, at a CAGR of 6.3%. The factors that are driving the growth of this market are the rising demand for test and measurement solutions by end users and growing demand for high-resolution images in scientific and medical applications.

“Data converter market for ADCs expected to grow at the highest rate during the forecast period”

The market for analog-to-digital converters (ADCs) is expected to grow at the highest CAGR between 2017 and 2023. The growing adoption of industrial data acquisition (DAQ) systems and medical devices such as cardiac monitors, hemodynamic monitors, respiratory monitors, multi-parameters monitors, digital thermometers, endoscopes, and ophthalmoscopes are likely to drive the market for ADCs.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=26991458

“The data converter market for the communications application to grow at a high rate between 2017 and 2023”

Among various applications, the communications application accounted for the highest CAGR of the overall data converter market between 2017 and 2023. The evolution of wireless communication networks, such as 3G, 4G, and long-term evolution (LTE), has resulted in the growth of base stations, optical communication devices, and other communications-based infrastructural products. With all this development in the communications application, the demand for data converters would also rise.

“The Asia Pacific expected to lead the data converter market between 2017 and 2023”

The Asia Pacific is expected to hold the largest size of the data converter market during the forecast period. This growth is mainly attributed to the increasing demand for communications systems and consumer equipment in China, Japan, and India. Furthermore, the growing adoption of industrial automation in the APAC would enable the requirement of data converters integrated into sensor-based systems.

The major players operating in the data converter market are Analog Devices (US), Texas Instruments (US), Maxim Integrated (US), Cirrus Logic (US), Microchip Technology (US), Intersil (Renesas) (US), DATEL (US), Asahi Kasei Microdevices (US), Avia Semiconductor (Xiamen) (China), IQ-Analog (US).

About MarketsandMarkets

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth emerging opportunities/threats which will impact 70% to 80% of worldwide companies' revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Contact:

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

Email: [email protected]

0 notes

Text

Thermal Management Market Development of Underground Mining Equipment Market 2022

According to the new market research report "Thermal Management Market by Material Type (Adhesive, Non-Adhesive), Devices (Conduction, Convection, Advanced, Hybrid), Service (Installation & Calibration, Optimization & Post Sales), End-Use Application - Global Forecast to 2022", the thermal management market is expected to be worth USD 14.24 Billion by 2022, growing at a CAGR of 7.91% between 2017 and 2022. The factors driving the growth of this market include rising demand for thermal management in consumer electronics, growing application arena, and radical miniaturization of electronic devices.

Convection cooling devices was the largest segment in terms of market size in 2016

Convection cooling devices are widely used in electronic circuits and printed circuit boards (PCBs). This has resulted in the growth of thermal management device market. Thus, these devices help lower the peak temperature of the systems with natural and forced convection cooling technologies. Devices such as loop heat pipes, heat pumps, heat sinks, and heat spreaders are used in providing effective cooling solutions in processors and computers, among others. Thus, the demand to maintain high efficiency of the electronic devices is expected to fuel the growth of the thermal management market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=15504922

Thermal management market for thermal tapes expected to grow at highest CAGR during the forecast period

Thermally adhesive tapes are used to mechanically and thermally bond electronic components to heat sinks. These tapes consist of a pressure-sensitive adhesive (PSA) film that is filled with thermally conductive materials such as metals, metal oxides, polyimide film, fiberglass mat, aluminium foil, and silica or ceramic particles. These particles allow thermal conduction through the tape. Thermal tapes are widely used for thermal management of the light emitting diodes (LEDs) in the automotive industry as they provide high mechanical strength, and good shock and vibration performance. The increasing use of tapes in consumer electronics and automotive applications is driving the overall market for adhesive materials.

The market in North America expected to grow at the highest CAGR during forecast period

North America is expected to hold the largest share of thermal management market by 2022, and it holds a tremendous potential for the market in the coming future due to its large investment in healthcare applications, increasing use of electric and hybrid vehicles, and growing data centers across the region. The market in North America consists of some of the leading markets such as the US, Canada, and Mexico.

Major players in this market include Honeywell International Inc. (US), Aavid Thermalloy LLC (US), Vertiv Co (US), European Thermodynamics Ltd (UK), Master Bond Inc.(US), Laird PLC (UK), Henkel AG & Company, KGaA (Germany), Delta Electronics, Inc. (Taiwan), Advanced Cooling Technologies, Inc. (US), Dau Thermal Solutions Inc. (US), Amerasia International (AI) Technology Inc.(US), Heatex Ab (Sweden), Lord Corporation (US), and Parker Chomerics (US).

About MarketsandMarkets

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth emerging opportunities/threats which will impact 70% to 80% of worldwide companies' revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Contact:

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

Email: [email protected]

0 notes

Text

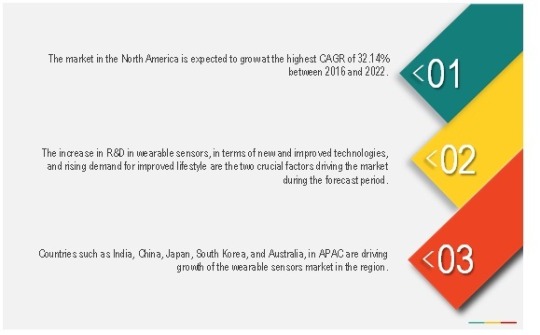

Wearable Sensors Market Expected To Reach USD 1,654.0 Million by 2023

According to the new market research report "Wearable Sensors Market by Type (Accelerometers, Magnetometers, Gyroscopes, Image Sensors, Inertial Sensors, Temperature & Humidity Sensors, Pressure & Force Sensors, Touch Sensors and Motion Sensors), Application (Wristwear, Eyewear, Bodywear), Vertical, and Geography - Global Forecast to 2022", The wearable sensors market is expected to grow from USD 189.4 Million in 2015 to USD 1,654.0 Million by 2022, at a CAGR of 30.14% between 2016 and 2022. The major factors driving the growth of the wearable sensors market include the increasing advancement toward smaller, smarter, and cheaper sensors, miniaturization trend in sensors, and mounting benefits of wearable devices in the healthcare sector.

“Accelerometers expected to hold a major share of the wearable sensors market during the forecast period”

Accelerometers are among the major sensors used in the wearable sensors market. Some of the prominent applications of wearable technology for this sensor are in wearable devices such as wristwear, bodywear, and eyewear. The demand for wristwear in sectors such as medical, healthcare, and consumer electronics is more compared with other end-user industries. Accelerometer sensors are widely used to detect velocity, position, shock, and vibration. They are widely used in smart watches and smart bands for tracking and navigation purposes.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158101489

“Market for bodywear application expected to grow at the highest rate between 2016 and 2022”

The wearable sensors market for the bodywear application is expected to witness the highest growth rate between 2016 and 2022. These are widely used in consumer electronics, industrial, and medical sectors for various applications. The bodywear application consists of textiles embedded with sensors, which is an emerging trend in the market. Bodywear offering works on fibertronics technology which integrates electronics and computational functionality into textile fabrics. They have attracted the emerging trend of techno-fashion clothing that brings sensors close to our skin for measuring various health and fitness parameters.

“Wearable sensors market in North America expected to grow at the highest rate during the forecast period”

Wearable sensors have a growing demand in North Americaowing to the increasing focus of the region toward industrial, consumer electronics, and healthcare sectors. In this study, the North Americanmarket has been segmented into Canada, Mexico, and the U.S. The APAC region is among the major markets for various sectors such as consumer electronics and industrial. Moreover, Europe is one of the potential markets for healthcare and industrial sectors as countries such as the U.K, Germany, and France are actively trying to strengthen their position in these markets.

The major companies involved in the development of wearable sensors include NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland), TE Connectivity Ltd. (U.S.), Broadcom Limited (U.S.), Knowles Electronics, LLC. (U.S.), Analog Devices, Inc. (U.S.), Infineon Technologies AG (Germany), Asahi Kasei Corporation (Japan), Sensirion AG (Switzerland), InvenSense, Inc. (U.S.), Robert Bosch GmbH (Germany), Texas Instruments Incorporated (U.S.), Panasonic Corporation (Japan), mCube, Inc. (U.S.), ams AG (Austria), and ARM Holdings Plc. (U.K), among others.

About MarketsandMarkets

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth emerging opportunities/threats which will impact 70% to 80% of worldwide companies' revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Contact:

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

Email: [email protected]

0 notes

Text

Current Sensor Market Size Worth $3.6 Billion By 2024

The Current Sensor Market is expected to grow from USD 2.4 billion by 2019 to USD 3.6 billion by 2024 at a CAGR of 8.34%. The increasing use of battery-powered applications and renewable energy forms, and growing market for Hall effect current sensors are among the key driving factors for this market. Moreover, the growth of automotive electronic control systems and new vehicle technologies, and large-scale commercialization of IoT and IIoT are among the other factors fueling the market growth.

Key Market Players

Key players in the current sensor market include Asahi Kasei Microdevices (Japan), Melexis (Belgium), Allegro Microsystems (US), Siliocn Labs (US), LEM International (Switzerland), Sensitec (Germany), Koshin Electrin (Japan). Asahi Kasei Microdevices (Japan) is a leader in the current sensing industry. The company has shown consistent growth in the market by demonstrating capability to serve new markets, and its product launches and promotional activities have boosted its revenue growth.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=26656433

Recent Developments

In February 2019, ACEINNA released a family of AMR-based isolated magnetic current sensors with high accuracy, wide bandwidth (1.5MHz, 3dB), low phase delay, and fast response time for a wide range of power and electrical applications. The current sensors have isolation of 4.8kV and are UL/IEC/EN60950-1 and UL1577 certified. These safety, reliability, and performance-related features are offered in an integrated “All-In-One,” simple-to-use, single-chip solution at effective costs.

In October 2018, AKM launched CZ-370x (x: 0 to 6), an ultrahigh-accuracy coreless current sensor supporting 60 Arms with more than 8 mm of creepage/clearance distance. These sensors have applications in AC motors, DC motors, UPS, general inverters, and power conditioners.

In February 2019, AKM acquired Senseair AB (Sweden), a manufacturer of gas sensor modules. This acquisition is expected to enable the company to expand its business activities in the market for air, gas, and alcohol sensors.

Critical Questions Answered by Report:

Where will all these developments take the industry in the mid to long term?

What are the leading industries of current sensors?

How are the advancements in various industries influencing the current sensor market?

Which current sensor type is expected to penetrate significantly in the overall market in the coming years?

Which countries are expected to witness significant growth in the current sensor market?

Don’t miss out on business opportunities in Current Senor Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

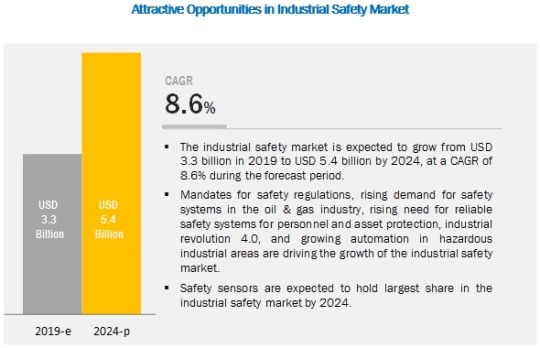

Industrial Safety Market Is Expected to Reach USD 5.4 Billion by 2024

The Industrial Safety Market is expected to grow from USD 3.3 billion in 2019 to USD 5.4 billion by 2024, at a CAGR of 8.6% during the forecast period. The market’s growth is propelled by the mandates for safety regulations, rising demand for safety systems in the oil & gas industry, rising need for reliable safety systems for personnel and asset protection, industrial revolution 4.0, and growing automation in hazardous industrial areas.

Key Market Players

As of 2018, Emerson (US), Honeywell (US), Rockwell (US), ABB (Switzerland), Schneider (France), Yokogawa (Japan), General Electric (US), Hima Paul (US), Omron (Japan), Siemens (Germany), Proserv Ingenious Simplicity (UK), Johnson Controls (Tyco) (Ireland), Balluff (US), Euchner (Germany), and Fortress Interlocks (UK) were the major players in the industrial safety market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=19720540

Schneider Electric has a strong presence in discrete and process automation industries. The company has grown through mergers of various business divisions; as a result, it typically offers more than one brand and product in most markets and sectors. Its strong position in various markets gives it a competitive advantage. The company has identified certain countries in Latin America, Asia, the Middle East, Eastern Europe, and Africa as “new economies” (experiencing accelerated growth due to urbanization, industrialization, digitalization, and development) that it intends to penetrate with long-term investments.

Recent Developments

In July 2018, Schneider Electric launched a series of industrial safety products in Australia, including the Telemecanique XCSR contactless RFiD safety sensor and Harmony range of pushbuttons. Both products present unique safety features to enable industrial operations to uphold the highest safety standards.

In March 2018, Schneider Electric opened its East Asia & Japan headquarters in Singapore, bringing together multiple operations across the island to one location to better serve regional customers and industry partners.

Critical Questions:

Which industrial safety equipment is expected to witness the highest demand in the future?

What is the most-widely adopted industrial safety product?

How is industrial safety implemented across industries?

What are the key trends in the industrial safety market?

Most suppliers adopt agreements, partnerships, and collaborations as key growth strategies (as seen from their recent developments); where will these take the market in the mid to long term?

Don’t miss out on business opportunities in Industrial Safety Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

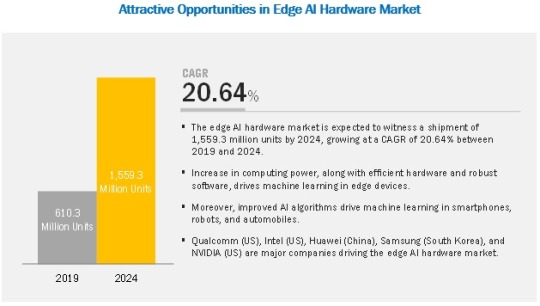

Edge AI Hardware Market Is Forecast To Reach $1559.3 Billion By 2024

The report "Edge AI Hardware Market by Device (Smartphones, Cameras, Robots, Automobile, Smart Speakers, Wearables, and Smart Mirror), Processor (CPU, GPU, ASIC and Others), Power Consumption, Process, End User Industry, and Region - Global Forecast to 2024", The edge AI hardware market is expected to register a shipment of 610 million units in 2019 and is likely to reach 1559.3 million units by 2024, at a CAGR of 20.64% during the forecast period. Major drivers for the market’s growth are growing demand for low latency and real-time processing on edge devices and emergence of AI coprocessors for edge computing. Further, underlying opportunities for the edge AI hardware market include growing demand for edge computing in IoT and dedicated AI processors for on-device image analytics. Major restraints for the market are limited on-device training and limited number of AI experts. Power consumption and size constraint pose major challenges to the edge AI hardware market.

In Term of Device Type, the Market for Cameras is Expected to Grow at the Highest CAGR During the Forecast Period in the Edge AI Hardware Market

Cameras have been an integral part of various smart devices with Wi-Fi support, smart functions, superior speed, and enhanced performance for years. However, cameras as standalone smart devices with vision processing units (VPU) that help deliver power-efficient solutions for vision and artificial intelligence are now entering the market. Such devices are designed to run deep neural networks at high speed and low power without compromising on accuracy, which enables devices to see, understand, and respond to their environment in real time.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158498281

The VPU market is constantly witnessing advancements. For instance, the previous-generation Myriad 2 VPU developed by Movidius offered deep neural network support at relatively low power. The new Myriad X VPU (introduced by Intel (US) in August 2017), however, can achieve roughly 10X better performance; with multiple neural networks running simultaneously, to offer extended autonomous capabilities across wide range of applications such as drones, robotics, VR, and smart cameras. Due to developments like these, the market is witnessing an influx of cameras powered by AI chips that allow these devices to judge moment’s best suited to capture stills or videos.

Smartphones is Expected to Hold the Largest Market for Edge AI Hardware

Dedicated AI chip or AI processors were one of the major developments in the smartphone technology last year. Increasing demand for real-time speech and voice recognition and analysis, as well as technical advancements in smartphone image recognition is driving the market for AI processors in smartphones. A majority of AI processors have an additional inbuilt Neural Processing Unit (NPU) that can handle significant amounts of parallel processing, uses low power, and is capable of cognitive tasks. Till date, most AI-related processing like prediction, detection, pattern matching, and classification tasks on mobile apps and assistants take place primarily in the cloud. However, with AI processors built in a phone, these AI tasks could be carried out right on the device, even without any connectivity; this would not only improve performance of the device, but also reduce strain on the battery. The AI features in smartphones at present are mainly focused on imaging and photography, power efficiency and security

In APAC, China is the Largest Contributor for Edge AI Hardware Market in Terms of Market Share

Currently, China is undertaking many projects, especially in the infrastructure sector, such as rail, airport, stadiums, and highway systems that are expected to require high-definition surveillance systems, which can capture clear images even in darkness. China is home to video surveillance players such as Dahua (China) and Hikvision (China) that dominate the video surveillance hardware market. Both Hikvision and Dahua have already launched deep learning surveillance cameras in the market. China has already started deploying cloud AI based surveillance cameras to monitor its citizens. This development will lead to adoption of edge AI in surveillance cameras. China is among the highest spenders on the manufacturing sector in APAC. The manufacturing sector in China is growing rapidly, resulting in the introduction of new robotics and big data technologies. In addition, China, being a global manufacturing hub, holds immense potential for the automotive industry. These factors are expected to fuel the growth of the edge AI hardware market in China as AI is increasingly being used in the country’s automotive and transportation sectors.

Intel Corporation (US), NVIDIA Corporation (US), Samsung Electronics Co., Ltd. (South Korea), Huawei Technologies Co., Ltd. (China), Google Inc. (US), MediaTek Inc. (Taiwan), Xilinx Inc. (US), Imagination Technologies Limited (UK), and Microsoft Corporation (US) are a few major players in the edge AI hardware market.

Don’t miss out on business opportunities in Edge AI Hardware Market . Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

Flexible AC Transmission System Market To Increase From USD 1.26 Billion by 2020

According to a new market research report "Flexible AC Transmission Systems (FACTS) Market by Compensation Type (Shunt, Series & Combined), Component, Application, Verticals (Electric Utilities, Renewables, Railways, Industrial, And Oil & Gas), and by Geography - Global Forecast to 2020", The global flexible AC transmission systems (FACTS) market is valued at USD 988.5 million in 2015 and is expected to reach USD 1.26 Billion by 2020, at a CAGR of 5.10% between 2015 and 2020.

The flexible AC transmission systems (FACTS) market is expected to exhibit moderate growth in the next five years. There is a growing adoption of flexible AC transmission systems (FACTS) in applications such as electric utilities, renewables, railways, industrial, and oil & gas.

This report provides a detailed analysis of the overall flexible AC transmission systems (FACTS) market and segments the same on the basis of compensation type, components, application, verticals, and geography. The market segmented on the basis of compensation type includes shunt, series, and combined shunt, and series compensation. The shunt compensation is expected to hold the major market share among all compensation type, while series compensation is expected to grow at the highest CAGR of 7.56% during the forecast period between 2015 and 2020.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1228

The objective of the research study was to analyze the market trends for each of the industries, growth rates of the various industry (electric utilities, renewables, railways, industrial, and oil & gas), and the demand for different compensation type of flexible AC transmission systems (FACTS) market.

The size of the flexible AC transmission systems (FACTS) market is given on the basis of the four geographical regions, namely, Americas, Europe, Asia-Pacific, and the Rest of the World (RoW). The region of Americas is estimated to hold the major share; however, it is expected to grow at the second-highest CAGR of 5.1% in the overall flexible AC transmission systems (FACTS) market during the forecast period.

Apart from the market segmentation, the report also covers the Porter’s analysis, the market’s value chain with a detailed process flow diagram, and the market dynamics such as drivers, restraints, and opportunities in the overall flexible AC transmission systems (FACTS) market.

This report profiles the major companies involved in the flexible AC transmission systems (FACTS) market, such as ABB Ltd. (Switzerland), Siemens AG (Germany), Mitsubishi Electric Corp. (Japan), General Electric (U.S.), Eaton Corp PLC (Ireland), Alstom (France), American Electric Power (U.S.), Hyosung (South Korea), NR Electric Co. Ltd. (China) and, Adani Power (India) among others.

Don’t miss out on business opportunities in Flexible AC Transmission System Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes

Text

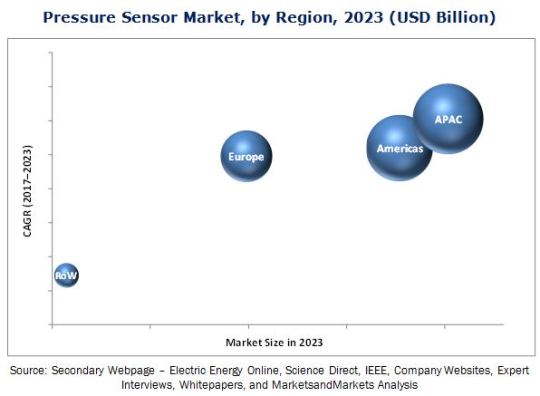

Pressure Switch Market worth 2.09 billion USD by 2023

The Pressure Sensor Market is expected to grow from USD 8.30 Billion in 2017 to USD 11.30 Billion by 2023, at a CAGR of 5.27% between 2017 and 2023. The growth of this market is fueled by advancements in MEMS technology and its rapid adoption in connected devices, growing demand from automotive and medical device industries, increasing adoption of pressure sensors in consumer goods and wearables, and stringent government regulations. Developments in the pressure sensor market ecosystem through organic and inorganic growth strategies, such as product developments, merger and acquisition, partnerships, collaborations, and agreements, further drive the growth of this market.

Among the different product types, the market for differential pressures sensors is expected to grow at the highest CAGR between 2017 and 2023. Differential pressure sensors provide the difference between two pressure sources through two ports, allowing users to provide required pressure inputs to the device for measuring the readings. This flexibility offered by the device helps drive the growth of the differential pressure sensor market at the highest CAGR during the forecast period.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=871

The pressure sensor market for the optical technology is expected to grow at a high CAGR between 2017 and 2023 driven by the growing adoption of optical technology over other technologies. In places that are remote or experience very high temperature, optical pressure sensors are used for various applications. In applications where other technologies can fail due to electromagnetic interference, optical pressure sensors can work very well due to their immunity to interference. These sensors also work well in the presence of chemicals or explosive materials.

Among various applications, automotive held the largest share of the overall pressure sensor market in 2016 owing to the increased use of pressure sensors in oil pressure monitoring, fuel pressure monitoring, nitrous pressure monitoring, transmission pressure monitoring, and tire pressure monitoring.

Asia Pacific (APAC) is expected to hold the largest share of the pressure sensor market during the forecast period. The pressure sensor market in countries such as China, India, Japan, and South Korea is expected to grow at the highest CAGR due to the increasing deployment of automated storage and retrieval systems (ASRS) and rising awareness about the advantages of automated systems.

The key restraining factor for the growth of the pressure sensor market is the intense pricing pressure. The consumers of pressure sensors are key players in applications such as utilities, oil & gas, consumer electronics, automotive, oil & gas, aviation, marine, medical, industrial, and others. The major demand for pressure sensors is from the automotive and medical applications. While both these industries are growing rapidly, they face a stiff price competition in the market. Therefore, the players in these applications demand low-cost pressure sensors to bring down the price of the final product.

Key market players such as Honeywell (US), ABB (Switzerland), NXP Semiconductors (Netherland), Infineon Technologies (Germany), Emerson Electric (US), General Electric (US), Siemens (Germany), STMicroelectronics (Switzerland), Robert Bosch (Germany), TE Connectivity (Switzerland), Schneider Electric (France), Denso (Japan), Continental (Germany), Endress+Hauser (Switzerland), SSI Technologies (US), and Delphi (UK) focus on strategies such as product launches and developments, agreements, mergers and acquisitions, partnerships, and collaborations to enhance their product offerings and expand their business.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

0 notes

Text

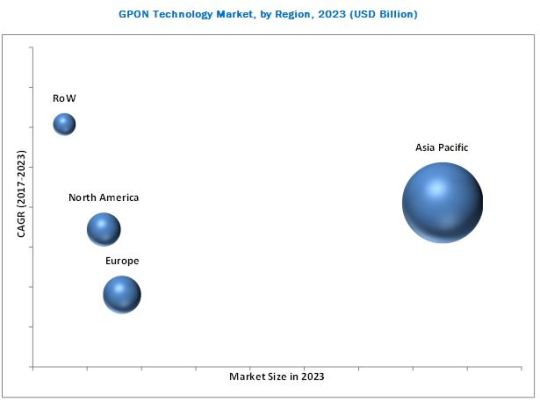

GPON Technology Market to Witness a CAGR of 7.45% During 2016-2023

The overall GPON technology Market was valued at USD 6.71 Billion in 2016 and is expected to reach USD 11.07 Billion by 2023, at a CAGR of 7.45% between 2017 and 2023.The growth of this market is driven by the increasing penetration of FTTH services in Asia Pacific, growing demand for high-speed broadband services, advancements in GPON technology, and high demand for GPON for triple-play services.

In this report, the GPON technology market is segmented on the basis of component, technology, application, vertical, and geography. Optical network terminal led the market in 2016 primarily owing to the high demand for GPON for triple-play services, growing demand for high-speed broadband services, advancements in GPON technology, and increasing penetration of FTTH services in APAC. The NG-PON2 technology is expected to be commercialized by 2018 and is expected to grow at the highest CAGR till 2023, replacing the 2.5G PON technology. The FTTH application held the largest size of the GPON technology market in 2016, while the market for the backhaul application is likely to grow at the highest CAGR during the forecast period primarily because of the growth of the XGS-PON and NG-PON2 technologies, which will witness higher adoption in the mobile backhaul application compared to 2.5G PON and XG-PON.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=86493601

The residential vertical is expected to hold the largest size of the GPON technology market during the forecast period. The GPON technology is primarily used for the FTTH market as optical fiber technology gained popularity owing to its ability to provide Internet connection directly to the home. AT&T, Verizon, and other leading operators in the US are investing in installing GPON architecture that will be installed in residencies either through the FTTH or FTTP route. GPON technology for the residential purpose is primarily used for the applications such as high-speed data, IPTV, voice, and CATV services

Asia Pacific held the largest share of the GPON technology market in 2016. The high government spending for expanding optical network distribution in the region and the increasing adoption of FTTx applications are some of the factors driving the growth of GPON technology market in the region. Additionally, the deployment of 4G and 5G mobile network applications is further expected to boost the demand for the GPON technology market in APAC

The GPON technology ecosystem includes the research and development (R&D) phase, followed by manufacturing, installation, marketing and sales, and post-sales services. Huawei (China), Nokia (Finland), ZTE (China), FiberHome (China), Calix (US), ADTRAN (US), DASAN Zhone (US), Cisco (US), NEC (Japan), Allied Telesis (Japan), Iskratel (Slovenia), Unizyx (Taiwan), and Alphion (US) are involved in the manufacturing and assembly of the GPON technology market.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Key Target Audience

Original device manufacturers (ODMs)

Component suppliers

Research organizations and consulting companies

Application providers

Subcomponent manufacturers

Maintenance and service providers

Technology providers

Associations, organizations, forums, and alliances related to the GPON technology

0 notes

Text

Solid State Drives Market To Reach A Value Of $60.22 Billion Forecast Till 2023

The overall Solid State Drive Market (SSD Market) is expected to increase from USD 26.47 Billion in 2017 to USD 60.22 Billion by 2023, at a CAGR of 14.68% between 2017 and 2023. Some of the key factors driving this market are increasing penetration of high-end cloud computing, growing adoption of SSDs in data centers, and advantages of SSDs over HDDs.

The market for SATA interface–based solid state drive accounted for the largest market in 2016. The large market of SATA interface solid state drive is mainly attributed to low-cost interface design. SATA interface also offers lower cable size and cost, faster data transfer through higher signaling rates, and more efficient transfer through an I/O queuing protocol, lower cable size and cost, faster data transfer through higher signaling rates, and more efficient transfer through an I/O queuing protocol.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=75076578

The market for half height, half length (HHHL); or; even bigger form factor; full height, half length (FHHL) is expected to grow at the highest rate during the forecast period. These form factors offer high performance as PCIe bus (with direct contact) offers a very low latency. The solid state drive market for TLC Planar held the largest market in 2016. With the shift in the usage of technology from SLC to MLC and from MLC to TLC, the price per GB of SSDs becomes cheaper. Therefore, TLC offers the cheapest solutions among all other technologies, along with high storage density. This leads to the increasing adoption of TLC SSDs in consumer applications such as notebooks, tablets, and others.

The solid state drive market in automotive is expected to grow at the highest rate during the forecast period. The increasing demand for automotive infotainment systems and next-generation connected cars is expected to boost the growth of the solid state drive market, as connected car applications require high-performance graphics, communications, and data storage, and SSDs meet all of these requirements. SSD is a flash storage solution that enables reliable, high-performance storage in a wide range of in-vehicle applications such as 3D mapping and advanced augmented reality in navigation systems, entertainment systems, intuitive driver-assist technology, and data event recorders.

Samsung (South Korea) is one of the leading companies in the solid state drive market, followed by Western Digital (US), Intel (US), Toshiba (US), and Micron (US) with a large contribution to the parent market share and high financial power, providing a broad product portfolio in the solid state drive market with a strong technical expertise. Samsung (South Korea), for instance, offers an innovative technology V-NAND that improves the latency in its SSD products. Also, the Charge Trap Flash (CTF) technology prevents data corruption caused by cell-to-cell interference and also leads to improved speed, power efficiency, and endurance. Western Digital (US) offers a wide range of products in the solid state drive market comprising internal SSD storage and portable SSD storage.

Target Audience:

Companies in the SSD market

Companies involved in the ecosystem of memory and storage businesses

Government and financial institutions, as well as investment communities

Analysts and strategic business planners

End users that want to know more about solid state drives and the latest technological developments in this industry

Research and consulting firms

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

0 notes

Text

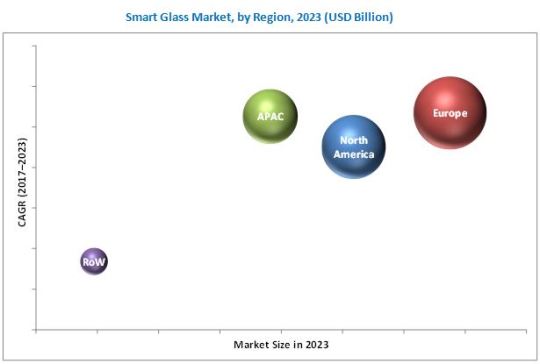

Smart Glass Market Expected To Reach $ 8.35 Billion, Globally by 2023

The Global Smart Glass Market is expected to reach USD 8.35 Billion by 2023 from USD 3.32 Billion by 2017, at a CAGR of 16.61% between 2017 and 2023. Some of the key factors driving the growth of this market are the growing demand for smart glass in automobile applications, strong government support through mandates and legislations for energy-efficient construction, and optimal energy saving through smart glass applications.

Governments and the policymakers across the world have started framing policies, legislations, and laws to increase the energy-efficiency of buildings. For example, the energy-efficiency directive from the European Union (EU) defines the measures to increase the efforts from member states to use energy more efficiently at all stages of the energy chain from the transformation and distribution of energy to its consumption. The directive includes the legal mandates to establish energy-efficiency obligations schemes or policy measures in all the member states. This will further drive the adoption of smart glass-enabled energy-efficient products in residential and commercial building construction, and in the transport sector, despite the higher cost of these glasses than the normal (flat) glass.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=907

The smart glass market based on technology has been segmented into suspended particle display (SPD), electrochromic, liquid crystal (LC), micro-blinds, photochromic, and thermochromic technologies. The smart glass market for SPD is expected to grow at the highest CAGR between 2017 and 2023. SPD glass offers many benefits due to its unmatched working capacity to change its light emission property to the desired level. This type of glass can adjust its light emission property from transparent to dark within 1–3 seconds and can be used to effectively control the glare from sun rays. SPD-enabled smart glass also restricts UV light up to 99%, providing a healthy ambiance with a sufficient amount of natural light.

The key players in the market include SAGE Electrochromics, Research Frontiers, View, Inc., Asahi Glass Co., Gentex, Hitachi Chemical, Glass Apps, Pleotint, Polytronix, RavenWindow, Scienstry, Smartglass International, and SPD Control Systems. The key players in this market are increasingly undertaking partnerships and collaborations, and product developments and launches to develop and introduce new technologies and products in the market.

The following are the major objectives of the study.

To define, describe, and forecast the smart glass market, in terms of value, segmented on the basis of technology, application, and geography

To forecast the smart glass market, in terms of volume, segmented on the basis of technology

To analyze the market structure by identifying various subsegments of the smart glass market

To forecast the market size, in terms of value, with regard to 4 main regions—Asia Pacific (APAC), Europe, North America, and Rest of the World (RoW)—along with their respective countries

To provide detailed information regarding the major factors influencing the growth of the market (drivers, restraints, opportunities, and challenges)

To strategically analyze micromarkets with respect to individual growth trends, prospects, and contribution to the total market

To identify the major market trends and factors driving or restricting the growth of the smart glass market and its various sub-markets

To provide a detailed overview of the smart glass value chain

To analyze opportunities in the market for stakeholders by identifying the high-growth segments of the smart glass ecosystem

To profile the key players in the smart glass market and comprehensively analyze their market shares and core competencies in each segment

To analyze competitive developments in the smart glass market, such as alliances, joint ventures, and mergers and acquisitions

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

0 notes

Text

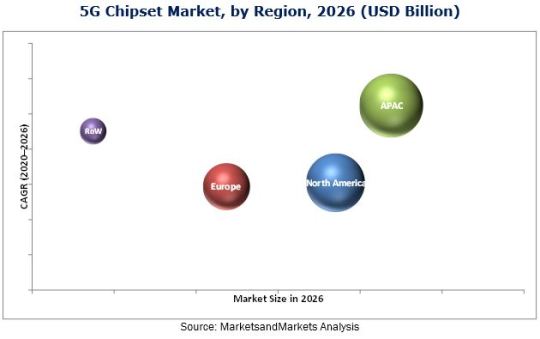

5G Chipset Market Trends, Scope and Driver Analysis by 2018-2026

The 5G Chipset Market is expected to grow at a CAGR of 49.2% between 2020 and 2026, from USD 2.03 Billion in 2020 to USD 22.41 Billion by 2026. Growing demand for high-speed internet and broad network coverage with reduced latency and power consumption is supplementing the growth of the 5G chipset market.5G is the next-generation wireless network technology that promises to deliver more data to more devices with lower latency and higher consistency than previous-generation technologies. 5G chipsets are poised to become an integral part of the much-anticipated 5G-enabled products, such as smartphones, tablets, laptops, C-V2X devices, and routers.

The 5G chipset market is gaining momentum as a result of organic as well as inorganic growth strategies followed by players operating in this market. Product launch is the most prominent growth strategy adopted by players in this market. Product developments and launches are mainly focused on the development of low-cost, less-power-intensive, latest 3GPP’s non-stand-alone standard-compliant chipsets with small form factor. Moreover, companies adopted collaborations and strategic partnerships as key growth strategies in the 5G chipset market. The key players following these strategies are Qualcomm (US), Intel (US), Nokia (Finland), Samsung Electronics (South Korea), Integrated Device Technology (US), Infineon Technologies (Germany), Qorvo (US), and Xilinx (US), among others.

To know about the assumptions considered for the study, Download the PDF Brochure

Qualcomm (US) is an important player in the 5G chipset market. It has strong expertise in 3G, 4G, and Wi-Fi, which has helped the company develop chipsets for 5G. Qualcomm has been a leader in the mobile processor market and is likely to dominate the 5G market as well in the future. Qualcomm has also collaborated with industry leaders to drive and implement 3GPP 5G New Radio (NR) standardizations along with field trials. In the past 2 years, Qualcomm has significantly demonstrated its strong inorganic growth strategy. In February 2018, Qualcomm announced that its Qualcomm Snapdragon X50 5G modem has been selected for use in live, over-the-air mobile 5G NR trials with multiple global wireless network operators in both the sub-6 GHz and millimeter wave (mmWave) spectrum bands. AT&T, British Telecom, China Telecom, China Mobile, China Unicom, Deutsche Telekom, KDDI, KT Corporation, LG Uplus, NTT DOCOMO, Orange, Singtel, SK Telecom, Sprint, Telstra, TIM, Verizon, and Vodafone Group will conduct the trials, which will be based on the 3GPP Release 15 5G NR standard.

Intel (S) is among the key players involved in the development of 5G chipsets. The company offers 5G chipset modems and embedded chipset-based small cells to support the initial network trial. The company has dominated the market for microprocessors for several years and now intends to develop itself in the cellular chip market. The latest release of XMM 8000 series of modems, along with partnership with network operators and cellular device OEMs, is expected to improve its position in the 5G chipset market in the coming years.

Don’t miss out on business opportunities in 5G Chipset Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

0 notes