#Data Center Colocation Market Applications

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

1,644 Tumblr posts in 1 second.

Text

What are Key Factors Predicted to Cause Boom of Data Center Colocation Market in North America Between 2020 and 2030?

The global data center colocation market generated a revenue of $42.1 billion in 2019 and is predicted to progress at a CAGR of 14.8% from 2020 to 2030. The main factors responsible for this surge are the creation of huge volumes of data, huge expenses associated with the maintenance of private data centers, various financial benefits provided by data colocation services, and rapid incorporation of cloud on-ramp in business operations.

The data colocation services allow the companies to rent the bandwidth and space of data centers for storing their information technology (IT) data, servers, and hardware. In many companies, the volume of data being created is very inconsistent. Furthermore, there has been a huge rise in the volume of data created in organizations because of the adoption of advanced technologies such as artificial intelligence (AI) and internet of things (IoT) and growing digitization. Thus, because of these factors, the requirement of effective data analysis and storage is rising rapidly.

Apart from the aforementioned factors, the high construction and maintenance costs of private data centers is another factor driving the growth of the data center colocation market across the world. In several countries, the construction cost of a private data storage building can be as high as $200 per square foot, with an additional $10,000 required for setting up a mile of fiber cabling. These exorbitant construction costs make the development of private data storage centers unaffordable for a most of the companies, especially the small and medium enterprises (SMEs).

Due to the above-mentioned reason, the data colocation services are rapidly becoming popular all over the world. On the basis of type, the data center colocation market is divided into wholesale colocation and retail colocation categories. Between the two, the retail colocation category is currently exhibiting higher growth in the market. This is credited to the fact that the retail colocation solutions allow the service providing organizations to serve many customers at once with carrier and cloud connectivity, on-site staff, and managed services.

In the coming years, the data center colocation market will register the highest growth in North America, according to the estimates of P&S Intelligence, a market research company. This is primarily attributed to the presence of a large number of colocation service providing companies and data centers in the North American nations. Furthermore, many leading technology companies in the world such as Facebook Inc., Amazon.com Inc., and Google LLC have their headquarters in the North American nations and are further expanding their businesses throughout the region.

Hence, it can be said without any hesitation that the market will demonstrate substantial growth in the forthcoming years, mainly because of the increasing generation of huge volumes of data and the subsequent surge in the need for data storage and analysis, growing popularity of cloud on-ramp, and the soaring costs of developing and maintaining private data centers all over the world.

Source: P&S Intelligence

#Data Center Colocation Market Share#Data Center Colocation Market Size#Data Center Colocation Market Growth#Data Center Colocation Market Applications#Data Center Colocation Market Trends

1 note

·

View note

Text

Data Center Market Forecast & Growth Trends

The global data center market was valued at USD 347.60 billion in 2024 and is expected to reach USD 652.01 billion by 2030, expanding at a robust compound annual growth rate (CAGR) of 11.2% from 2025 to 2030. This growth is primarily driven by the exponential surge in data generation across various sectors, fueled by widespread digital transformation initiatives and the increasing adoption of advanced technologies such as cloud computing, artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT).

As organizations generate and process vast volumes of data, the demand for scalable, secure, and energy-efficient data center infrastructure has intensified. Enterprises are seeking agile and resilient IT architectures to support evolving business needs and digital services. This has led to the rapid expansion of data center capacity worldwide, with a particular focus on hyperscale and colocation facilities.

Hyperscale data center operators—including major players such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud—are continuously scaling their infrastructure to meet global demands for cloud storage, computing power, and data processing. These tech giants are making substantial investments in constructing new data centers and upgrading existing ones to ensure seamless service delivery, latency reduction, and improved data security.

Simultaneously, the colocation segment is gaining momentum as businesses pursue cost-effective solutions to manage IT infrastructure. Colocation centers offer shared facilities equipped with high-speed connectivity, advanced cooling systems, and robust physical and cyber security. These benefits allow companies—especially small and medium enterprises—to scale their operations flexibly without the high capital expenditure required to build and maintain in-house data centers.

Another major trend accelerating market growth is the rise of edge computing. As the number of IoT devices and real-time applications grows, there is an increasing need for decentralized computing infrastructure. Edge data centers, located closer to end-users and data sources, provide reduced latency and faster response times—critical for applications in sectors such as autonomous vehicles, remote healthcare, industrial automation, and smart cities.

Key Market Trends & Insights

In 2024, North America dominated the global data center market with a share of over 40.0%, propelled by the widespread adoption of cloud services, AI-powered applications, and big data analytics across industries.

The United States data center market is anticipated to grow at a CAGR of 10.7% between 2025 and 2030, driven by continued digital innovation, enterprise cloud adoption, and the expansion of e-commerce and fintech platforms.

On the basis of components, the hardware segment accounted for the largest market share of more than 67.0% in 2024. The surge in online content consumption, social networking, digital transactions, and IoT connectivity has significantly boosted demand for high-capacity, high-performance hardware.

Within the hardware category, the server segment emerged as the market leader, contributing over 34.0% to revenue in 2024. Modern servers are being equipped with enhanced processing power, memory, and storage efficiency, all of which are crucial to supporting next-generation computing needs.

Among software solutions, the virtualization segment held a dominant share of nearly 18.0% in 2024. Virtualization allows data centers to maximize hardware utilization by enabling multiple virtual machines (VMs) to operate on a single physical server, reducing costs and increasing operational flexibility.

Order a free sample PDF of the Data Center Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 347.60 Billion

2030 Projected Market Size: USD 652.01 Billion

CAGR (2025-2030): 11.2%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Key players operating in the data center industry are Amazon Web Services (AWS), Inc. Microsoft, Google Cloud, Alibaba Cloud, and Equinix, Inc. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

In February 2025, Alibaba Cloud, the digital technology arm of Alibaba Group, opened its second data center in Thailand to meet the growing demand for cloud computing services, particularly for generative AI applications. The new facility enhances local capacity and aligns with the Thai government's efforts to promote digital innovation and sustainable technology. Offering a range of services including elastic computing, storage, databases, security, networking, data analytics, and AI solutions, the data center aims to address industry-specific challenges.

In December 2024, Amazon Web Services (AWS) introduced redesigned data center infrastructure to accommodate the growing demands of artificial intelligence (AI) and sustainability. The updates features advancements in liquid cooling, power distribution, and rack design, enabling a sixfold increase in rack power density over the next two years. AWS stated that these enhancements aims to deliver a 12% boost in compute power per site, improve energy efficiency, and enhance system availability.

In May 2024, Equinix, Inc. launched its first two data centers in Malaysia, with the International Business Exchange (IBX) facilities now operational in Johor and Kuala Lumpur. The facilities are intended to cater to Equinix Inc.'s customers in Malaysia while enhancing regional connectivity.

Key Players

Alibaba Cloud

Amazon Web Services, Inc.

AT&T Intellectual Property

Lumen Technologies (CenturyLink)

China Telecom Americas, Inc.

CoreSite

CyrusOne

Digital Realty

Equinix, Inc.

Google Cloud

IBM Corporation

Microsoft

NTT Communications Corporation

Oracle

Tencent Cloud

Browse Horizon Databook on Global Data Center Market Size & Outlook

Conclusion

The global data center market is undergoing rapid expansion, driven by the growing digital economy, technological advancements, and the ever-increasing demand for data storage, computing power, and connectivity. Hyperscale and colocation facilities are at the forefront of this transformation, offering scalable and secure infrastructure that supports cloud computing, AI workloads, and real-time applications. Edge computing is further reshaping the landscape by bringing processing capabilities closer to data sources, enabling faster and more efficient services across various industries.

As the market continues to evolve, investment in energy-efficient hardware, software virtualization, and regional data center development will be critical to meeting future demands. Companies that adopt flexible, sustainable, and innovation-driven data infrastructure strategies will be best positioned to capitalize on the tremendous growth opportunities in the data center space over the coming years.

0 notes

Text

Data Center Market Report Highlights: Tendencies in Bfsi, Healthcare, And It Sectors

In these days’s rapid-evolving virtual international, the want for strong and scalable data infrastructure has become more vital than ever. The data center market report presents valuable insights into how distinctive industries are leveraging data facilities to meet increasing data processing needs. Many of the maximum dynamic sectors featured in the data center market report are BFSI (Banking, economic offerings, and insurance), Healthcare, and data era (IT). Each of these sectors has shown outstanding developments, boom styles, and demanding situations that are shaping the global data center landscape.

BFSI Area: Rising Demand For At Ease And Scalable Data Infrastructure

The data center market report reveals that the BFSI sector continues to be one of the top contributors to data center demand. As banks and financial institutions increasingly pass to digital platforms, the volume of data generated and stored has exploded. With services like mobile banking, online transactions, digital wallets, and AI-driven consumer experiences, there’s a strong emphasis on data safety, regulatory compliance, and disaster recuperation.

Consistent with the data center market report, many BFSI companies are turning to colocation data centers, hybrid cloud models, and area computing to ensure quicker data get right of entry to and more desirable provider reliability. The developing adoption of blockchain era and actual-time analytics in finance has also pushed the demand for excessive-performance computing environments, as highlighted in the data center market report.

Healthcare Sector: Digitization And Real-Time Data Access Drive Growth

Healthcare is undergoing a big digital transformation. As per the data center market report, the world has visible unheard-of boom in data extent because of digital fitness data (ehrs), telemedicine, wearable health devices, and AI diagnostics. This large data era requires relaxed, compliant, and scalable data storage and processing structures.

The data center market report emphasizes the need for HIPAA-compliant infrastructure and the integration of AI and ML algorithms for predictive analytics in healthcare. Part data centers also are gaining recognition to make certain real-time get right of entry to to important affected person data, specially in emergency care. Furthermore, the pandemic multiplied the shift in the direction of cloud-based totally fitness platforms, a trend that maintains to develop as in keeping with the modern-day data center market report.

IT Area: Fueling Worldwide Data Center Innovation

The IT industry remains at the forefront of data center innovation. The data center market report identifies the IT region as both a driving force and a consumer of advanced data center answers. With the upward thrust of big data, synthetic intelligence, iot, and cloud-local applications, IT organizations are continuously demanding extra effective, energy-green, and coffee-latency data environments.

In line with the data center market report, hyperscale data facilities are being evolved to cater to the growing needs of tech giants and cloud service vendors. There may be also an improved recognition on inexperienced data facilities, with IT corporations adopting renewable energy and sustainable cooling technology. Additionally, the data center market report notes that hybrid and multi-cloud techniques have become the norm in IT operations, providing flexibility and fee performance.

Cross-Industry Traits and Technology

The data center market report sheds mild on several overarching trends which might be impacting all 3 sectors:

Area Computing: All 3 sectors—BFSI, Healthcare, and IT—are integrating part computing to lessen latency and improve the consumer experience.

AI & Automation: From fraud detection in finance to diagnostics in healthcare and IT infrastructure management, AI is revolutionizing operations, a fashion properly reported in the data center market report.

Cybersecurity: With data breaches becoming extra sophisticated, the data center market report underscores the urgency of imposing sturdy protection protocols throughout all industries.

Sustainability: there may be a developing shift closer to f6ba901c5019ebe39975adc2eb223bef data facilities, as agencies goal to reduce carbon footprints even as scaling their digital infrastructure.

Conclusion: Quarter-Precise Needs, Unified Increase

The data center market report highlights how the BFSI, Healthcare, and IT sectors, even as distinct in their center capabilities, percentage a unified dependence on superior data center technology to gasoline their virtual transformation trips. Whether it's the want for actual-time data in healthcare, compliance in finance, or scalability in IT, the data center market report makes it clean that tailored data center answers are essential for area-precise desires.

As these industries keep to evolve and adopt rising technology, the insights from the data center market report will continue to be important for stakeholders, investors, and selection-makers searching for to live ahead of the curve in a competitive digital economic system.

1 note

·

View note

Text

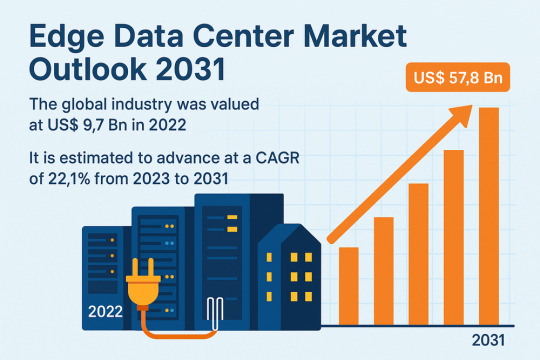

Edge Computing Demand Accelerates Market Growth at 22.1% CAGR

The global Edge Data Center Market was valued at USD 9.7 Bn in 2022 and is projected to reach USD 57.8 Bn by the end of 2031, expanding at an impressive CAGR of 22.1% from 2023 to 2031. This rapid growth is fueled by the increasing demand for real-time data processing, the rise of streaming services, growth in IoT and AI-driven technologies, and the adoption of autonomous vehicles.

Market Overview: Edge data centers are smaller, decentralized data facilities located close to the end-users and connected devices. These centers reduce latency, improve bandwidth efficiency, and enable faster data processing by bringing computation and storage closer to the data source.

Edge computing is being adopted across a variety of sectors, including healthcare, manufacturing, automotive, and telecom, as organizations seek to leverage real-time analytics and improve user experience. With 5G networks and AI-based solutions gaining traction globally, the need for edge infrastructure is growing significantly.

Market Drivers & Trends

One of the primary market drivers is the surge in demand for video streaming services. Platforms such as Netflix, YouTube, and Disney+ are increasingly dependent on edge data centers to deliver content with minimal latency and buffering. For instance, Netflix uses edge infrastructure to reduce content delivery costs and ensure a seamless user experience.

Additionally, the rapid adoption of IoT devices and AI technologies has heightened the need for low-latency data processing. Applications like autonomous vehicles, smart cities, industrial automation, and digital healthcare depend on instantaneous data collection and response, which edge data centers facilitate.

The expansion of 5G networks further accelerates edge data center deployment. As bandwidth and connection speeds increase, so does the demand for faster and more reliable data delivery.

Latest Market Trends

Increased deployment in rural and semi-urban areas: Edge data centers are being built in remote areas to bridge the digital divide. For example, RailTel Corp. is constructing 102 edge data centers across rural and semi-urban India to support digital services with minimal latency.

Integration of edge with AI and ML: Enterprises are leveraging edge computing to run machine learning models directly at the source of data. This results in faster decision-making and enhances operational efficiency.

Sustainable data centers: Growing environmental concerns are pushing companies to build eco-friendly edge data centers powered by renewable energy and equipped with energy-efficient cooling systems.

Key Players and Industry Leaders

Some of the leading players in the global edge data center market include:

365 Data Centers

Eaton Corporation plc

EdgeConneX Inc.

Vertiv Group Corp.

Reichle & De-Massari (R&M)

Dätwyler IT Infra GmbH

L&T Smart World

Siemon

Rittal GmbH & Co. KG

H5 Data Centers

NEXTDC LTD.

These companies are investing heavily in R&D and strategic collaborations to expand their edge capabilities, enhance service offerings, and cater to new markets.

Recent Developments

November 2022: 365 Data Centers acquired Sungard Availability Services’ U.S. colocation and network operations, expanding its footprint in high-growth edge markets.

April 2022: EdgeConneX acquired Indonesia’s GTN to develop a 90MW data center in Jakarta, highlighting the growing edge data center demand in Southeast Asia.

January 2022: RailTel Corp. announced its plan to build 102 edge data centers across India to promote digital transformation in underdeveloped regions.

Market Opportunities

The proliferation of autonomous vehicles opens new frontiers for edge data centers. An autonomous car can generate up to 5 TB of data per hour, necessitating real-time processing capabilities only edge facilities can offer. According to MIT (2022), over 30 million autonomous vehicles are already on the roads globally, a number that will increase exponentially.

Similarly, the growth of eSports and gaming platforms, which require ultra-low latency, will boost the demand for local data processing units. Industrial automation and smart manufacturing further contribute to the rising demand for edge data infrastructure.

Preview essential insights and takeaways from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=79151

Future Outlook

With businesses and governments increasing their focus on digital transformation, the edge data center market is expected to witness widespread adoption across industries. The combination of 5G, AI, IoT, and cloud computing is expected to shape the future of decentralized data management.

Companies are likely to prioritize edge data centers to ensure compliance with data localization regulations, optimize service delivery, and maintain high-security standards.

By 2031, the edge data center industry will play a crucial role in reshaping the global data processing ecosystem, especially as the number of connected devices continues to rise.

Market Segmentation

By Component:

Solutions

Services

Designing & Consulting

Implementation & Integration

Support & Maintenance

By Enterprise Size:

SMEs

Large Enterprises

By Industry:

BFSI

IT & Telecom

Healthcare

Manufacturing

Automotive

Others

By Region:

North America

Europe

Asia Pacific

Middle East & Africa

South America

Regional Insights

North America currently dominates the global edge data center market, led by the U.S., which boasts high internet penetration, advanced telecom infrastructure, and robust digital consumption.

Asia Pacific is projected to register the fastest CAGR through 2031, driven by increasing 5G deployment, digital business expansion, and the presence of major tech hubs in countries like China, India, and Japan.

Europe follows closely with significant investments in edge technologies to support the growing demand for smart cities and Industry 4.0 initiatives.

Why Buy This Report?

Gain insights into a market poised to grow at a CAGR of 22.1%

Understand emerging trends, technological advancements, and opportunities

Analyze competitive landscape with detailed company profiles

Evaluate the impact of regional growth trends on market performance

Identify potential investment areas and target customer segments

This comprehensive analysis helps stakeholders make informed strategic decisions based on in-depth market intelligence.

Frequently Asked Questions (FAQs)

1. What is the current size of the global edge data center market? The market was valued at US$ 9.7 Bn in 2022.

2. What is the projected market size by 2031? The edge data center market is expected to reach US$ 57.8 Bn by 2031.

3. What is the CAGR for the forecast period 2023–2031? The market is anticipated to grow at a CAGR of 22.1%.

4. Which region leads the global edge data center market? North America dominates the market due to its mature technology landscape and early adoption of edge computing.

5. What are the key factors driving market growth? Rising demand for low-latency data processing, streaming services, 5G expansion, IoT device proliferation, and AI-based applications.

6. Who are the key players in the market? Major players include 365 Data Centers, EdgeConneX, Eaton, Vertiv, H5 Data Centers, and NEXTDC LTD.

Explore Latest Research Reports by Transparency Market Research: 3D Modeling, 3D Visualization, and 3D Data Capture Market: https://www.transparencymarketresearch.com/3d-modeling-3d-visualization-and-3d-data-capture-market.html

IT Asset Disposition (ITAD) Market: https://www.transparencymarketresearch.com/it-asset-disposition-market.html

Identity-as-a-Service (IDaaS) Market: https://www.transparencymarketresearch.com/identity-as-a-service-market.html

Point-of-Sale [POS] Terminal Market: https://www.transparencymarketresearch.com/point-of-sale-terminals-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Hybrid Cooling in Data Centers: Innovations & Market Forecast

Hybrid cooling market for data centersis gaining significant traction, propelled by the necessity to manage escalating computing demands while enhancing energy efficiency. By 2024, more and more colocation and hyperscale data centers will have implemented hybrid cooling systems, which combine liquid and air cooling techniques. In addition to satisfying the requirements of increased rack density, these systems use less water and adhere to more stringent environmental standards.

It is anticipated that developments in sensors, materials, and intelligent control systems would significantly improve the scalability and efficiency of hybrid cooling by 2034. High-performance and environmentally responsible data center operations are being made possible by hybrid cooling thanks to features like real-time thermal balancing and predictive maintenance.

Market Segmentation

By Application

1. Centralized Data Centers

Enterprise Data Centers: Individually owned and operated by organizations to support internal IT workloads, often requiring balanced and cost-effective cooling.

Hyperscale Data Centers: Operated by major cloud providers (e.g., Google, AWS), these massive server farms demand ultra-efficient hybrid cooling systems to manage extremely high power densities.

Colocation Data Centers: Multi-tenant facilities that lease out space, power, and cooling; they favor flexible hybrid cooling solutions to support varied client needs and equipment types.

2. Edge Data Centers

Smaller, decentralized facilities located closer to end users or data sources.

Require compact, modular, and efficient hybrid cooling systems capable of operating in constrained or remote environments to support latency-sensitive applications.

By Product

1. Liquid-to-Air Cooling Systems

Rear Door Heat Exchangers / Liquid-Assisted Air Cooling: Uses a liquid-cooled panel at the rear of the rack or integrates liquid circuits into air pathways to remove heat more efficiently than air cooling alone.

Closed Loop Liquid Cooling with Air Augmentation: Circulates liquid coolant within a closed system while supplementing with directed airflow to handle hotspots in high-density deployments.

2. Air-to-Liquid Cooling Systems

Direct-to-Chip / Cold Plate Cooling: Applies liquid coolant directly to heat-generating components (e.g., CPUs, GPUs) with residual air cooling used to manage ambient rack temperature.

Others (Chilled Beam, Immersion + Air Extraction): Encompasses innovative hybrid methods like chilled beams for overhead cooling or partial component immersion combined with air extraction to manage thermal loads.

Market Trend

The incorporation of AI-powered controls into hybrid cooling systems is a significant new trend. These clever technologies dynamically adjust cooling performance by using machine learning and real-time data. They can detect thermal inefficiencies, modify cooling ratios, and predict changes in workload, all of which greatly increase Power Usage Effectiveness (PUE). Data centers are becoming more intelligent, flexible, and energy-efficient as a result of the combination of AI and hybrid cooling.

Market Drivers

The worldwide drive for energy efficiency and sustainability is the main driver of the implementation of hybrid cooling. Data centers are being forced to lower their carbon emissions, electricity use, and water consumption due to regulatory pressure and corporate ESG requirements. By mixing air and liquid cooling methods, hybrid cooling provides a workable option that enhances thermal management without compromising performance, balancing environmental responsibility with operational objectives.

Market Restrain

High Initial Costs: The initial outlay required for hybrid cooling systems may be too costly for smaller facilities.

Complex Setup: Deployment calls for complex parts such as liquid pipes, heat exchangers, and cold plates.

Retrofitting Challenges: It might be technically challenging to integrate hybrid systems into older infrastructures.

Extended Payback Period: Adoption may be hampered by the delayed ROI, despite the fact that long-term savings are substantial.

Skilled Labor Requirement: The necessity for specialized knowledge of both liquid and air systems makes operations more complex.

Key Market Players

Schneider Electric SE

Vertiv Holdings Co.

STULZ GmbH

Rittal GmbH & Co. KG

Mitsubishi Electric Corporation

Trane Technologies

Airedale International Air Conditioning Ltd

Take Action: Gain Valuable Insights into the Rising Investments and Market Growth of Hybrid Cooling Market For Data Centers!

Learn more about Energy and Power Vertical. Click Here!

Conclusion

Data center hybrid cooling is becoming a vital component of contemporary IT infrastructure as compute demands rise and environmental laws become more stringent. Hybrid systems handle high-density workloads and provide improved energy efficiency and sustainability by fusing liquid and air-based techniques. Hybrid cooling is a critical element of next-generation data centers because of the potential for retrofitting, AI integration, and future scalability, even in the face of obstacles like expensive initial investment and complex infrastructure. With environmental effects coming under more and more scrutiny, hybrid cooling is set to become a key component of high-performance, sustainable digital infrastructure on a global scale.

0 notes

Text

3D Printing Market to Witness Exponential Growth, Driven by Industrial and Healthcare Innovation

Market Overview

The global 3D printing market is undergoing a significant transformation, powered by technological advancements, cost-efficient production capabilities, and expanding industrial applications. Originally focused on prototyping, the technology has matured into a core component of modern manufacturing, especially in complex industries such as aerospace, automotive, and medical devices. As organizations prioritize faster production cycles and greater design flexibility, the demand for 3D printing solutions continues to grow.

Fueled by investments in R&D and the increasing adoption of additive manufacturing processes, the 3D printing industry growth is set to outpace traditional manufacturing methods. According to recent 3D printing market research, both developed and developing regions are witnessing a surge in adoption due to its scalability and customization benefits.

Key Trends

Expansion of 3D Printing Services Market The growth in on-demand manufacturing has boosted the 3D printing services market. Service providers offer access to advanced printing technologies without requiring capital-intensive investments, enabling small and medium enterprises to benefit from additive manufacturing.

Rising Adoption in Aerospace and Automotive Aerospace and automotive industries are major contributors to the 3D printing market growth. Lightweight components, rapid prototyping, and cost reduction in low-volume production have made 3D printing a preferred option in these sectors.

Healthcare Sector Embraces Customization Customized medical implants, prosthetics, and dental products are driving 3D printing market trends in healthcare. The ability to produce patient-specific models with precision is revolutionizing medical treatment planning and delivery.

Material Innovations Continued innovation in printing materials, including metals, biopolymers, and ceramics, is expanding the 3D printing industry market size. These new materials are enabling diverse applications across high-performance industries.

Government and Institutional Support Supportive policies, public-private collaborations, and dedicated funding for research are playing a pivotal role in accelerating the 3D printing industry growth globally, particularly in Asia-Pacific and Europe.

Challenges

Despite its rapid growth, the 3D printing market faces several challenges. High initial costs for industrial-grade printers, limited standardization, and intellectual property concerns continue to hinder broader adoption. Additionally, skill shortages and the need for advanced training remain barriers in leveraging the full potential of additive manufacturing technologies.

Conclusion

The 3D printing market is on a dynamic growth trajectory, driven by its transformative impact on production, innovation, and efficiency across multiple sectors. As the 3D printing market size expands, stakeholders must navigate evolving trends and challenges to capture the full potential of this disruptive technology. With sustained investment and innovation, the 3D printing industry is poised to redefine the future of manufacturing. Other Related Reports:

Self Storage Market

Data Center Colocation Market

Artificial Intelligence Market

Smart Homes Market

#3d printing market#3d printing market size#3d printing market share#3d printing market trends#3d printing market analysis#3d printing industry#3d printing industry trends

0 notes

Text

Data Center Robotics Market Size, Share, Analysis, Forecast, and Growth Trends to 2032 – Edge Computing Drives Robotic Adoption

Data Center Robotics Market was valued at USD 11.06 billion in 2023 and is expected to reach USD 67.05 billion by 2032, growing at a CAGR of 17.31% from 2024-2032.

Data Center Robotics Market is rapidly transforming the global IT infrastructure landscape, offering next-generation solutions for automation, maintenance, and efficiency. As the volume of data explodes and demand for uninterrupted uptime intensifies, robotics is emerging as a key enabler in data center operations across the USA and Europe. These smart systems are reducing human error, improving scalability, and lowering operational costs.

Robots Power the Future: U.S. Data Center Robotics Market Set for Explosive Growth

Data Center Robotics Market is becoming increasingly vital as companies prioritize energy efficiency, security, and remote management. Robotic systems—ranging from autonomous monitoring units to AI-powered repair bots—are being integrated into hyperscale and enterprise data centers to optimize workflows and support 24/7 operations without interruption.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6673

Market Keyplayers:

365 Data Centers (Colocation Services, Cloud Storage Solutions)

ABB (IRB Series Robots, RobotStudio)

Amazon Web Services (AWS RoboMaker, AWS Outposts)

BMC Software, Inc. (BMC Helix, TrueSight Automation for Data Centers)

China Telecom (IDC Services, Cloud Managed Network Services)

Cisco Systems, Inc. (Cisco UCS, Cisco Intersight)

ConnectWise LLC (ConnectWise Automate, ConnectWise RMM)

Digital Realty (PlatformDIGITAL, ServiceFabric)

Equinix (Equinix Fabric, Equinix Metal)

Hewlett Packard Enterprise Development LP (HPE GreenLake, HPE OneView)

Huawei Technologies Co., Ltd. (FusionModule Data Center, iManager NetEco)

Microsoft Corporation (Azure Robotics, Azure Stack Hub)

NTT Communications (Nexcenter Data Centers, Smart Data Platform)

Rockwell Automation Inc. (FactoryTalk, Arena Simulation)

Siemens AG (SIMATIC Robot Library, TIA Portal)

Verizon (Verizon Colocation, Verizon Intelligent Edge)

Google (Google Cloud Robotics, Google Distributed Cloud)

Market Analysis

The market is driven by the growing complexity and size of data centers, which demand high-speed, high-precision maintenance solutions. Robotics helps minimize downtime, streamline server diagnostics, and perform physical tasks like cabling, hardware replacement, and climate control. In the USA, innovation is fueled by tech giants investing in automation, while in Europe, sustainability goals are a major driver, pushing for energy-efficient robotic operations within green data centers.

Market Trends

Adoption of AI-integrated robots for predictive maintenance

Rise in mobile robotic units for real-time monitoring and inspection

Deployment of robotic arms for automated hardware handling

Integration with DCIM (Data Center Infrastructure Management) platforms

Increasing demand for remote and touchless operations post-pandemic

Use of thermal imaging and sensors for climate optimization

Expansion of robotics-as-a-service (RaaS) models

Market Scope

As demand for digital services surges, data center operators are turning to robotics to maintain resilience, reduce latency, and improve operational control. The scope of the market spans mission-critical applications across sectors such as cloud computing, banking, e-commerce, and telecom.

Robotics supporting 24/7 server maintenance

Enhanced operational efficiency and reduced human risk

Climate and power monitoring through automated systems

Scalable solutions for hyperscale and colocation centers

Faster issue detection and resolution

Compliance with stringent data and facility security standards

Smart integration with AI, IoT, and edge computing systems

Forecast Outlook

The Data Center Robotics Market is poised for impressive growth, fueled by increasing data demands, global cloud expansion, and the need for operational precision. As edge computing becomes mainstream and data centers multiply in urban and remote locations alike, robotics will serve as the backbone for managing physical infrastructure intelligently. With both the USA and Europe emphasizing technological leadership and sustainability, the market is set to evolve rapidly, unlocking innovation in automated facility management.

Conclusion

In a world powered by data, robotics is reshaping the way data centers operate—bringing intelligence, automation, and resilience to the core of digital infrastructure. From smart bots navigating massive server farms to automated systems minimizing downtime, the Data Center Robotics Market is defining the future of IT operations.

Data Center Robotics Market is rapidly transforming the global IT infrastructure landscape, offering next-generation solutions for automation, maintenance, and efficiency. As the volume of data explodes and demand for uninterrupted uptime intensifies, robotics is emerging as a key enabler in data center operations across the USA and Europe. These smart systems are reducing human error, improving scalability, and lowering operational costs.

Data Center Robotics Market is becoming increasingly vital as companies prioritize energy efficiency, security, and remote management. Robotic systems—ranging from autonomous monitoring units to AI-powered repair bots—are being integrated into hyperscale and enterprise data centers to optimize workflows and support 24/7 operations without interruption.

Market Analysis

The market is driven by the growing complexity and size of data centers, which demand high-speed, high-precision maintenance solutions. Robotics helps minimize downtime, streamline server diagnostics, and perform physical tasks like cabling, hardware replacement, and climate control. In the USA, innovation is fueled by tech giants investing in automation, while in Europe, sustainability goals are a major driver, pushing for energy-efficient robotic operations within green data centers.

Market Trends

Adoption of AI-integrated robots for predictive maintenance

Rise in mobile robotic units for real-time monitoring and inspection

Deployment of robotic arms for automated hardware handling

Integration with DCIM (Data Center Infrastructure Management) platforms

Increasing demand for remote and touchless operations post-pandemic

Use of thermal imaging and sensors for climate optimization

Expansion of robotics-as-a-service (RaaS) models

Market Scope

As demand for digital services surges, data center operators are turning to robotics to maintain resilience, reduce latency, and improve operational control. The scope of the market spans mission-critical applications across sectors such as cloud computing, banking, e-commerce, and telecom.

Robotics supporting 24/7 server maintenance

Enhanced operational efficiency and reduced human risk

Climate and power monitoring through automated systems

Scalable solutions for hyperscale and colocation centers

Faster issue detection and resolution

Compliance with stringent data and facility security standards

Smart integration with AI, IoT, and edge computing systems

Forecast Outlook

The Data Center Robotics Market is poised for impressive growth, fueled by increasing data demands, global cloud expansion, and the need for operational precision. As edge computing becomes mainstream and data centers multiply in urban and remote locations alike, robotics will serve as the backbone for managing physical infrastructure intelligently. With both the USA and Europe emphasizing technological leadership and sustainability, the market is set to evolve rapidly, unlocking innovation in automated facility management.

Conclusion

In a world powered by data, robotics is reshaping the way data centers operate—bringing intelligence, automation, and resilience to the core of digital infrastructure. From smart bots navigating massive server farms to automated systems minimizing downtime, the Data Center Robotics Market is defining the future of IT operations.

Data Center Robotics Market is rapidly transforming the global IT infrastructure landscape, offering next-generation solutions for automation, maintenance, and efficiency. As the volume of data explodes and demand for uninterrupted uptime intensifies, robotics is emerging as a key enabler in data center operations across the USA and Europe. These smart systems are reducing human error, improving scalability, and lowering operational costs.

Data Center Robotics Market is becoming increasingly vital as companies prioritize energy efficiency, security, and remote management. Robotic systems—ranging from autonomous monitoring units to AI-powered repair bots—are being integrated into hyperscale and enterprise data centers to optimize workflows and support 24/7 operations without interruption.

Market Analysis

The market is driven by the growing complexity and size of data centers, which demand high-speed, high-precision maintenance solutions. Robotics helps minimize downtime, streamline server diagnostics, and perform physical tasks like cabling, hardware replacement, and climate control. In the USA, innovation is fueled by tech giants investing in automation, while in Europe, sustainability goals are a major driver, pushing for energy-efficient robotic operations within green data centers.

Market Trends

Adoption of AI-integrated robots for predictive maintenance

Rise in mobile robotic units for real-time monitoring and inspection

Deployment of robotic arms for automated hardware handling

Integration with DCIM (Data Center Infrastructure Management) platforms

Increasing demand for remote and touchless operations post-pandemic

Use of thermal imaging and sensors for climate optimization

Expansion of robotics-as-a-service (RaaS) models

Market Scope

As demand for digital services surges, data center operators are turning to robotics to maintain resilience, reduce latency, and improve operational control. The scope of the market spans mission-critical applications across sectors such as cloud computing, banking, e-commerce, and telecom.

Robotics supporting 24/7 server maintenance

Enhanced operational efficiency and reduced human risk

Climate and power monitoring through automated systems

Scalable solutions for hyperscale and colocation centers

Faster issue detection and resolution

Compliance with stringent data and facility security standards

Smart integration with AI, IoT, and edge computing systems

Forecast Outlook

The Data Center Robotics Market is poised for impressive growth, fueled by increasing data demands, global cloud expansion, and the need for operational precision. As edge computing becomes mainstream and data centers multiply in urban and remote locations alike, robotics will serve as the backbone for managing physical infrastructure intelligently. With both the USA and Europe emphasizing technological leadership and sustainability, the market is set to evolve rapidly, unlocking innovation in automated facility management.

Access Complete Report: https://www.snsinsider.com/reports/data-center-robotics-market-6673

Conclusion

In a world powered by data, robotics is reshaping the way data centers operate—bringing intelligence, automation, and resilience to the core of digital infrastructure. From smart bots navigating massive server farms to automated systems minimizing downtime, the Data Center Robotics Market is defining the future of IT operations.

Related Reports:

USA leads innovations in Micro Mobile Data Center solutions for agile IT infrastructure

U.S.A reshapes the future of connectivity through dynamic Data Center Networking advancements

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Data Center Robotics Market#Data Center Robotics Market Scope#Data Center Robotics Market Share#Data Center Robotics Market Gowth

0 notes

Text

Dedicated Server Hosting Netherlands

Why Buy a Netherlands Dedicated Server for Business Growth and High-Speed Hosting?

The Amsterdam Internet Exchange (AMS-IX) processes an incredible 8.3TB of data each second, with peaks hitting 11.3TB per second. This makes dedicated server hosting Netherlands a smart choice for companies that need strong hosting solutions. The country stands third in Europe for data center facilities, with almost 300 data centers operating in 2024. Only Germany and the UK have more facilities.

Netherlands dedicated server services let you handle up to 30 times your website's normal daily traffic. This capacity works perfectly to manage promotional events and unexpected traffic spikes. The country's advanced fiber optic network provides smooth connectivity, and its strict GDPR compliance will give you solid data protection. Amsterdam's data centers boast a 99.97% uptime guarantee. The Netherlands ranks seventh worldwide for reliable power supply, creating an infrastructure that excels in both performance and reliability.

This piece will help you learn about how Netherlands dedicated servers can stimulate your business growth. We'll get into the infrastructure capabilities and explore budget-friendly aspects of this hosting solution.

Netherlands Server Infrastructure Analysis 2024

"The Netherlands is an excellent place for hosting dedicated servers due to the high-quality streaming and adaptable solutions that are available there."

The Netherlands' data center market reached USD 1.20 Billion in 2023. We invested heavily in reliable infrastructure to achieve this growth. AMS-IX Network Architecture runs on a distributed exchange system that connects multiple independent colocation facilities in Amsterdam. The network uses MPLS/VPLS infrastructure and supports connections through 10GE, 100GE, and 400GE interfaces. Traffic peaked at an impressive 11.92 Tb/s in January 2024.

A reliable power grid forms the life-blood of dedicated server hosting in the Netherlands. The grid operator TenneT maintains 99.99% availability, making it one of the world's most dependable power systems. The network's exceptional reliability comes from its 265,000 km of underground cables. These cables make up 97% of the infrastructure and protect it from bad weather.

New fiber-optic connections grew by 250,000 in Q1 2024. The network now serves 7.38 million households, with 2.92 million subscribers using fiber-optic plans. Some areas still lack fiber coverage, including parts of Groningen, Noord-Holland, Zuid-Holland, Zeeland, and Limburg.

AMS-IX Technical Specifications

Core Infrastructure

Juniper MX10008

Connection Options

10/100/400GE

Total Capacity

49 Tb/s

Peak Traffic Record

11.92 Tb/s

Server Configuration Options for Business Growth

The right server configuration is crucial to business growth in the Netherlands' hosting environment.

Enterprise-Grade Hardware Specifications

Today's dedicated servers in the Netherlands come with multi-core processors that offer 4 to 64 cores. Businesses can pick between Intel Xeon or AMD EPYC processors. AMD's latest EPYC "Turin" processors support up to 192 cores. RAM options start at 16GB and go up to 1536GB. These specifications work perfectly for high-demand applications and virtual machine setups.

Storage options include SATA drives, SSDs, and NVMe drives. SSDs run 5-10 times faster than standard drives, which makes them perfect for data-heavy operations. Servers usually have 4 to 12 drive slots. This setup allows businesses to add more storage when needed.

Scalable Resource Allocation Systems

The Netherlands' dedicated server hosting infrastructure supports both vertical and horizontal scaling. Businesses can upgrade RAM and storage with minimal downtime through vertical scaling. This approach works best for applications that have predictable resource needs.

Horizontal scaling with extra servers works better for changing workloads. This setup allows:

Resource distribution across multiple servers

Automated provisioning based on needs

Pay-per-use resource allocation

This scalable structure supports automated backend services and gives control over reboots, OS reloads, and IP management. Private network options help create secure hybrid cloud setups that ensure continuous resource allocation across different infrastructure parts.

Performance Benchmarks and Metrics

"The current implementation of the AMS-IX peering platform uses an MPLS/VPLS infrastructure. This setup allows for a resilient and highly scalable infrastructure inherent to MPLS, while at the same time the interface towards the members and customers is still the common shared Layer 2 Ethernet platform." — AMS-IX, Amsterdam Internet Exchange

Speed and reliability tests show that Netherlands-based servers have major advantages over others.

Latency Comparison: EU vs Global Locations

Network tests show impressive low latency results within European connections. Servers in Amsterdam can reach UK locations in just 11ms, which helps European users the most. Our largest longitudinal study shows that cross-Atlantic connections take 90-100ms. This makes Dutch server hosting a smart choice for European markets.

Connection Route

Average Latency

Netherlands-UK

11ms

Netherlands-US

90-100ms

Local (AMS-IX)

<10ms

Bandwidth Throughput Analysis

Dutch infrastructure delivers outstanding bandwidth performance through the AMS-IX network. Recent tests confirm that servers reach 40 Gbit backbone connectivity, which ensures stable throughput for demanding applications. Dutch networks keep speeds consistent thanks to direct backbone connections.

Load Testing Results

Load testing services showcase these servers' reliable capabilities:

Support for up to 100,000 concurrent users

Up-to-the-minute data analysis from multiple global points

Clear insights into server response under peak loads

Dutch dedicated server options excel at handling sudden traffic spikes. Stress tests prove that servers stay stable even under very heavy loads. Businesses get detailed metrics about their setup's performance and practical suggestions to optimize it.

Cost-Benefit Analysis for Business Investment

Financial analysis shows dedicated server hosting in Netherlands costs USD 80.00 monthly. This is higher than shared hosting at USD 10.00.

Total Cost of Ownership Calculator

The TCO covers several essential components. Direct costs include hardware procurement while indirect expenses relate to maintenance and operations. A detailed TCO analysis should consider:

Hardware maintenance and repairs

Power consumption (USD 731.94 annually per server)

Technical support and staffing

Software licensing fees

Physical space requirements

These factors help businesses save 79% on their IT budget when they choose Netherlands dedicated servers instead of on-premises infrastructure over five years.

ROI Projections: 3-Year Analysis

We calculated the three-year ROI by comparing operational costs with the original investment. Standard configurations (2 vCPUs, 8GB RAM, 512GB storage) cost USD 313.90 monthly to operate. This is significantly lower than on-premises solutions at USD 1476.31.

Cost Component

Year 1

Year 2

Year 3

Initial Investment

USD 28042.00

-

-

Annual Benefits

USD 184750.00

USD 184750.00

USD 184750.00

Total Value

USD 156708.00

USD 341458.00

USD 526208.00

buy Netherlands dedicated server shows a 155% ROI over three years. The benefits grow through lower maintenance costs and no hardware refresh cycles. Annual subscriptions provide extra savings by reducing monthly costs from USD 130.00 to about USD 80.00.

Conclusion

Netherlands dedicated servers are a compelling choice for businesses that want to build a strong digital presence in Europe. The state-of-the-art infrastructure uses AMS-IX's remarkable 11.92 Tb/s peak capacity. These servers provide exceptional performance for demanding applications.

Enterprise-grade hardware specifications and flexible expandable solutions let businesses adapt their resources when they just need to grow. The performance advantages become clear in European markets. Businesses can expect low latency rates of 11ms to UK locations and reliable bandwidth throughput with 40 Gbit backbone connectivity.

The numbers show most important long-term benefits with a 155% ROI over three years and 79% savings compared to on-premises solutions. Netherlands' reliable power infrastructure keeps 99.99% grid availability. These factors make dedicated servers an affordable choice for businesses that prioritize performance and value.

Netherlands dedicated servers support up to 100,000 concurrent users while prices start at just USD 80.00 monthly. Businesses don't have to choose between quality and value anymore. This combination of capabilities and affordable pricing makes Netherlands dedicated hosting an ideal solution for businesses looking for reliable, high-performance hosting services.

FAQs

Q1. What are the main advantages of using a dedicated server in the Netherlands?

Dedicated servers in the Netherlands offer improved performance, enhanced security, and increased reliability. They provide exclusive access to server resources, allowing for optimal performance during traffic spikes and the ability to handle up to 100,000 concurrent users.

Q2. How does the Netherlands' server infrastructure compare to other European countries?

The Netherlands boasts exceptional internet infrastructure, with the AMS-IX network handling up to 11.92 Tb/s of traffic. The country ranks third in Europe for data center facilities and offers low latency connections, making it an ideal choice for businesses targeting European markets.

Q3. What server configuration options are available for business growth?

Businesses can choose from a range of enterprise-grade hardware specifications, including multi-core processors (4 to 64 cores), RAM configurations up to 1536GB, and various storage solutions like SSDs and NVMe drives. Scalable resource allocation systems support both vertical and horizontal scaling approaches.

Q4. How cost-effective are dedicated servers in the Netherlands?

While dedicated servers start at a higher price point than shared hosting, they offer significant long-term benefits. Businesses can expect a 155% ROI over three years and 79% savings compared to on-premises solutions. Monthly costs can be as low as $80 with annual subscriptions.

Q5. What performance metrics can businesses expect from Netherlands dedicated servers?

Netherlands servers demonstrate remarkably low latency within European connections, achieving round-trip times of 11ms to UK locations. They offer 40 Gbit backbone connectivity, ensuring stable throughput for high-demand applications. Load testing shows support for up to 100,000 concurrent users with maintained stability under heavy loads.

0 notes

Text

Global Hyperscale Data Center Market Insights: Forecast, Size, Share & Growth Report 2032

The Hyperscale Data Center Market Size was valued at USD 124.30 Billion in 2023 and is expected to reach USD 957.23 Billion by 2032 and grow at a CAGR of 25.48% over the forecast period 2024-2032.

hyperscale data center—massive facilities designed to efficiently support robust, scalable, and high-density computing workloads. These centers are vital for powering everything from content streaming and cloud services to enterprise applications and advanced analytics, leading to an unprecedented investment boom across the global tech landscape.

Hyperscale Data Center Market growth is being driven by rapid digital transformation across industries, expansion of global internet usage, and the increasing demand for low-latency computing environments. Enterprises are shifting from traditional on-premise systems to cloud-based solutions, encouraging major players like Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and others to expand their hyperscale infrastructure. The market is not only witnessing exponential growth in capacity but also in strategic collaborations, energy-efficient technologies, and geographic diversification.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/5453

Market Keyplayers:

Amazon Web Services (AWS) (Compute, Storage)

Microsoft Azure (Virtual Machines, Storage)

Google Cloud (BigQuery, Cloud Storage)

IBM (Cloud Servers, Network Services)

Facebook (Networking Equipment, Storage Solutions)

Alibaba Cloud (Elastic Compute Service, Storage)

Oracle (Autonomous Database, Compute Infrastructure)

Tencent Cloud (Server Hosting, Database Services)

Baidu (Cloud Storage, Compute Resources)

Cisco (Data Center Switching, Security Solutions)

HPE (Rack Servers, Storage Solutions)

Dell Technologies (PowerEdge Servers, Data Storage)

Huawei (Network Hardware, Storage Solutions)

Equinix (Interconnection, Colocation Services)

Digital Realty (Data Center Hosting, Interconnection)

Iron Mountain (Data Center Solutions, Colocation Services)

Rackspace Technology (Cloud Hosting, Migration Services)

Fujitsu (Data Center Solutions, Network Services)

Lenovo (Data Center Servers, Storage Solutions)

Hitachi (Compute Solutions, Storage Systems)

Trends Shaping the Market

Several key trends are actively defining the evolution of the hyperscale data center market:

Cloud-First Strategies Across Enterprises: As businesses accelerate cloud adoption, the demand for scalable and flexible infrastructure continues to rise. Hyperscale data centers provide the necessary agility and resilience to meet these evolving needs.

Sustainable and Green Data Centers: With rising concerns over energy consumption, there’s a growing push toward carbon-neutral and energy-efficient data centers. Operators are integrating renewable energy sources, liquid cooling, and AI-powered power management to reduce environmental impact.

Edge Integration and Hybrid Models: While hyperscale facilities are central hubs, integration with edge data centers is enabling faster data processing for latency-sensitive applications like autonomous vehicles, smart cities, and AR/VR services.

AI and Automation: Hyperscale operators are implementing AI-driven systems for workload management, predictive maintenance, and operational optimization. This is improving uptime and lowering operational costs while enhancing scalability.

Geographic Expansion and Colocation Demand: Providers are investing in emerging markets such as Southeast Asia, Eastern Europe, and Latin America to tap into underserved regions and meet global digital demand. Colocation services are also seeing a boost as enterprises seek flexibility without owning infrastructure.

Enquiry of This Report: https://www.snsinsider.com/enquiry/5453

Market Segmentation:

BY COMPONENT

• Solutions

Cooling

Power

Networking Equipment

DCIM

LV/MV Distribution

• Services

Installation and Deployment

Maintenance and Support

Consulting

BY END-USE

• Cloud Providers

• Colocation Providers

• Enterprises

BY INDUSTRIES

• BFSI

• IT and Telecom

• Government and Defense

• Entertainment and Media

• Others

BY DATA CENTER TYPE

• Hyperscale Self Build

• Hyperscale Colocation

BY ENTERPRISE SIZE

• Large Enterprises

• SMEs

BY INFRASTRUCTURE

• Electrical Infrastructure

• Mechanical Infrastructure

• Cooling System

• Cooling Technique

• General Construction

Market Analysis

The hyperscale data center market has witnessed extraordinary growth over the past decade and is expected to continue its upward trajectory. According to industry estimates, the market is projected to grow at a double-digit CAGR through 2032. This expansion is underpinned by increasing data traffic, driven by video streaming, online gaming, AI workloads, and enterprise cloud migration.

North America currently leads the market, with the United States hosting the largest number of hyperscale facilities, driven by major cloud providers and favorable infrastructure. Europe follows closely, emphasizing data sovereignty and green data centers. Asia-Pacific is emerging as the fastest-growing region due to digital adoption, government-led data localization mandates, and the rise of regional cloud players.

The market is highly competitive, with key players focusing on strategic investments, partnerships, and acquisitions. Significant capital is being poured into land acquisition, modular designs, and renewable energy sourcing to build the next generation of scalable, efficient, and future-proof hyperscale campuses.

Future Prospects

The hyperscale data center market is expected to evolve significantly in the next decade, shaped by technology shifts, regulatory frameworks, and environmental priorities. Emerging technologies like quantum computing, 6G networks, and AI-as-a-service will place new demands on data infrastructure, requiring greater processing power, lower latency, and more efficient energy usage.

As governments worldwide tighten data protection and energy efficiency regulations, operators will need to align with stricter compliance standards. This will likely accelerate the adoption of modular and prefabricated data centers, enabling rapid deployment and better resource optimization.

The future also points toward closer integration between hyperscale and edge environments, allowing organizations to benefit from centralized power while meeting local data processing requirements. Additionally, ongoing investments in submarine cables, satellite internet, and private networks will enhance global connectivity and redefine data center deployment strategies.

Access Complete Report: https://www.snsinsider.com/reports/hyperscale-data-center-market-5453

Conclusion

The hyperscale data center market is poised for robust and sustained growth through 2032, acting as the digital foundation for a data-driven world. With increasing cloud reliance, surging data volumes, and rapid tech innovation, these mega-facilities are becoming indispensable to global IT infrastructure. As organizations seek to modernize, scale, and future-proof their operations, hyperscale data centers will remain at the core of the digital revolution—pushing the boundaries of performance, efficiency, and global connectivity.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Global Hyperscale Data Center Market#Global Hyperscale Data Center Market Scope#Global Hyperscale Data Center Market Growth

0 notes

Text

Data Center Liquid Cooling Market Regional and Global Industry Insights to 2033

Introduction

The exponential growth of data centers globally, driven by the surge in cloud computing, artificial intelligence (AI), big data, and high-performance computing (HPC), has brought thermal management to the forefront of infrastructure design. Traditional air-based cooling systems are increasingly proving inadequate in terms of efficiency and scalability. This has led to the rapid adoption of liquid cooling solutions, which offer higher thermal performance and energy efficiency. The data center liquid cooling market is poised for significant growth through 2032, fueled by the increasing density of IT equipment and a global push for sustainable and energy-efficient data centers.

Market Overview

The global data center liquid cooling market is expected to witness a compound annual growth rate (CAGR) of over 20% from 2023 to 2032. Valued at approximately USD 2.5 billion in 2022, the market is forecasted to surpass USD 12 billion by 2032, according to industry estimates. North America leads the market, followed closely by Europe and Asia-Pacific.

Key drivers include:

Growing need for high-performance computing in AI and ML workloads.

Increase in data center construction across hyperscale, edge, and colocation segments.

Environmental regulations promoting energy efficiency and sustainability.

Download a Free Sample Report:-https://tinyurl.com/34z8dxuk

Market Segmentation

By Type of Cooling

Direct-to-Chip (D2C) Cooling In D2C systems, liquid coolant flows through pipes in direct contact with the chip or processor. These systems are highly effective in cooling high-density servers and are gaining traction in HPC and AI applications.

Immersion Cooling This method involves submerging entire servers in dielectric coolant fluid. Immersion cooling offers superior thermal management and reduced operational noise. It's increasingly used in crypto mining and AI/ML workloads.

Rear Door Heat Exchangers These solutions replace traditional server cabinet doors with heat exchangers that transfer heat from air to liquid. This hybrid approach is popular among data centers looking to enhance existing air cooling systems.

By Component

Coolants (Dielectric fluids, water, glycol, refrigerants)

Pumps

Heat Exchangers

Plumbing systems

Cooling Distribution Units (CDUs)

By Data Center Type

Hyperscale Data Centers

Enterprise Data Centers

Colocation Data Centers

Edge Data Centers

By Application

High-Performance Computing

Artificial Intelligence & Machine Learning

Cryptocurrency Mining

Cloud Service Providers

Banking, Financial Services, and Insurance (BFSI)

Key Market Trends

1. Rising Power Densities

Modern servers used for AI and HPC workloads often exceed power densities of 30 kW per rack, making traditional air cooling impractical. Liquid cooling efficiently handles heat loads upwards of 100 kW per rack, prompting widespread adoption.

2. Sustainability and ESG Goals

With energy consumption by data centers accounting for nearly 1% of global electricity use, companies are under pressure to reduce their carbon footprint. Liquid cooling systems reduce Power Usage Effectiveness (PUE), water usage, and total energy costs, aligning with environmental goals.

3. Edge Computing Growth

The rise of 5G and IoT technologies necessitates edge data centers, which are often space-constrained and located in harsh environments. Liquid cooling is ideal in such scenarios due to its silent operation and compact form factor.

4. Innovation in Coolant Technologies

Companies are investing in advanced non-conductive and biodegradable dielectric fluids. These innovations enhance performance while reducing environmental impact and regulatory compliance costs.

5. Strategic Partnerships and Investments

Major tech players like Google, Microsoft, and Amazon are investing heavily in liquid cooling R&D. Partnerships between data center operators and liquid cooling vendors are accelerating product development and commercialization.

Competitive Landscape

Key Players

Vertiv Group Corp.

Schneider Electric SE

LiquidStack

Submer

Iceotope Technologies

GRC (Green Revolution Cooling)

Asetek

Midas Green Technologies

These companies are focused on product innovation, strategic acquisitions, and expanding into emerging markets to gain a competitive edge.

Recent Developments

In 2023, Microsoft expanded its partnership with LiquidStack to deploy immersion cooling in Azure data centers.

Google announced plans to test immersion cooling in its data centers to improve energy efficiency.

Intel unveiled its open IP immersion cooling design to promote standardized adoption across the industry.

Regional Insights

North America

Dominates the market due to high demand from hyperscale cloud providers and advanced R&D capabilities. The U.S. government's energy regulations also promote adoption of energy-efficient systems.

Europe

Adoption is fueled by strict carbon emission regulations and sustainability initiatives. Countries like Germany, the UK, and the Netherlands are leading the charge.

Asia-Pacific

The fastest-growing region, driven by increasing digitization, rapid cloud adoption, and government-led smart city initiatives. China and India are key markets due to massive data center expansions.

Challenges and Restraints

High Initial Investment: Liquid cooling systems have higher upfront costs compared to traditional air cooling, which can deter smaller operators.

Maintenance Complexity: Requires specialized maintenance and training.

Market Fragmentation: Lack of standardization in liquid cooling solutions can slow down interoperability and integration.

Future Outlook (2024–2032)

The next decade will see mainstream adoption of liquid cooling, especially among hyperscale data centers and AI-focused operations. Regulatory support, combined with a clear ROI on energy savings, will drive adoption across all regions.

Key predictions:

Over 30% of new data centers will incorporate liquid cooling technologies by 2030.

Hybrid cooling systems combining air and liquid methods will bridge the transition period.

Liquid cooling-as-a-service (LCaaS) will emerge, especially for edge deployments and SMEs.

Conclusion

The data center liquid cooling market is at a pivotal point in its growth trajectory. As workloads become more compute-intensive and sustainability becomes non-negotiable, liquid cooling is emerging not just as an alternative—but as a necessity. Stakeholders across the ecosystem, from operators to manufacturers and service providers, are recognizing the benefits in cost, performance, and environmental impact. The next decade will witness liquid cooling go from niche to norm, fundamentally transforming how data centers are designed and operated.

Read Full Report:-https://www.uniprismmarketresearch.com/verticals/chemicals-materials/data-center-liquid-cooling.html

0 notes

Text

Edge, Hyperscale, and Sustainability: The Next Wave of Data Center Builds

The global data center construction market was valued at approximately USD 240.97 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 11.8% from 2025 to 2030. This anticipated growth is largely attributed to the rising demand for robust digital infrastructure across various industry sectors. Several key factors are contributing to this trend, including the accelerated expansion of cloud computing, the proliferation of big data, and the increasing adoption of artificial intelligence (AI) and Internet of Things (IoT) technologies.

As enterprises continue to generate and manage vast volumes of data, there is a growing reliance on cloud service providers (CSPs) and colocation data centers. These facilities are essential for supporting large-scale storage, computing, and data processing needs. Consequently, the market is witnessing a surge in the construction of new, high-capacity data centers. At the same time, the rise of edge computing is driving the development of smaller, decentralized data centers that reduce latency and enable real-time data processing—particularly critical in applications such as autonomous vehicles, smart cities, and industrial IoT.

Investment by hyperscale data center operators such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud is playing a pivotal role in shaping the market. These tech giants are expanding their global infrastructure footprint to meet the soaring demand for cloud-based services. For instance, in March 2025, Thailand’s investment board approved USD 2.7 billion in investments for data center and cloud projects. Notable initiatives include data centers developed by Beijing Haoyang Cloud & Data Technology from China, Empyrion Digital from Singapore, and Thailand’s GSA Data Center 02.

The market is also being propelled by technological advancements such as the rollout of 5G networks and broader implementation of AI-powered applications, which require high-performance computing environments. Additionally, governments across the globe are actively promoting digital infrastructure development by offering financial incentives, subsidies, and regulatory support, which further accelerates market growth.

A significant trend shaping the industry is the shift toward sustainable and energy-efficient construction. Data center operators are increasingly prioritizing the development of green data centers that utilize renewable energy, advanced cooling systems, and environmentally-conscious architectural designs. These facilities aim to reduce power consumption and minimize carbon emissions, aligning with global sustainability goals. The modular data center construction approach is also gaining popularity due to its faster deployment, flexibility, and scalability.

In response to growing concerns around data security and business continuity, there is a heightened demand for high-redundancy data centers, such as those classified under Tier III and Tier IV standards. These facilities are engineered to provide uninterrupted service, ensuring seamless operations even during failures or disasters.

Curious about the Data Center Construction Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Detailed Segmentation:

Infrastructure Insights The IT infrastructure segment dominated the market in 2024, accounting for over 81% of the total market share. This segment includes critical components such as networking equipment, servers, and storage systems—all of which form the backbone of data center operations. The rising demand for computing power and scalable storage solutions continues to reinforce this segment's dominance.