#Global Controlled Release Drug Delivery Market

Text

Exploring the Pressure Infusion Bags Market: Trends, Growth Drivers, and Innovations

The Pressure Infusion Bags Market is projected to be valued at USD 0.33 billion in 2024 and is anticipated to grow to USD 0.44 billion by 2029, with a compound annual growth rate (CAGR) of 5.49% during the forecast period from 2024 to 2029.

In the evolving landscape of medical devices, the Pressure Infusion Bags market is gaining significant traction. These bags are crucial in facilitating the rapid infusion of fluids and medications, often in emergency and critical care scenarios. Whether it's blood transfusions, IV solutions, or drugs, pressure infusion bags enable fast and controlled administration, enhancing patient outcomes. Let’s explore the key trends, growth drivers, and innovations shaping the market.

Key Trends Driving Market Growth

Rise in Surgical Procedures and Trauma Cases With the increasing number of surgeries and trauma cases globally, demand for pressure infusion bags is surging. These devices are particularly critical in emergency rooms and intensive care units, where rapid fluid administration can be lifesaving. As healthcare infrastructure expands, especially in emerging markets, the need for such devices is set to grow.

Technological Advancements Modern pressure infusion bags are designed with user-friendly features such as pressure gauges, improved durability, and lightweight materials. These enhancements ensure that medical professionals can monitor and adjust the pressure more efficiently, reducing the risk of complications. The integration of smart technologies for precise control and monitoring is also on the rise, aligning with the growing trend of digital healthcare solutions.

Demand from Military and Emergency Services The military and emergency medical services (EMS) sectors are key adopters of pressure infusion bags. In combat zones or disaster-stricken areas, these bags ensure quick and efficient fluid resuscitation, enhancing survival rates. The ruggedness and portability of these devices make them ideal for field operations, driving further market adoption.

Increased Focus on Patient Safety Regulatory bodies and healthcare organizations are placing greater emphasis on patient safety. As a result, manufacturers are innovating to ensure pressure infusion bags are reliable, accurate, and compliant with stringent safety standards. Features like overpressure release valves and ergonomic designs are being incorporated to prevent errors and ensure optimal care delivery.

Market Growth Drivers

Growing Geriatric Population The global aging population is a significant driver of the pressure infusion bags market. Older individuals are more susceptible to chronic illnesses, trauma, and surgical interventions, all of which require rapid fluid administration. As the elderly population grows, so does the need for reliable, efficient medical devices, including pressure infusion bags.

Expanding Healthcare Infrastructure in Emerging Markets Countries in Asia-Pacific, Latin America, and the Middle East are witnessing a surge in healthcare investments. Governments and private players are building hospitals, clinics, and emergency care centers to cater to growing populations. This is creating a favorable environment for the growth of the pressure infusion bags market as hospitals and care centers require advanced medical devices to provide high-quality care.

Rise in Outpatient and Home Healthcare Outpatient procedures and home healthcare are becoming more common due to cost-effectiveness and convenience. Portable and easy-to-use pressure infusion bags are ideal for these settings, enabling healthcare providers to administer fluids and medications outside of traditional hospitals. This trend is expected to significantly boost market demand, particularly in developed countries.

Challenges and Restraints

While the market is on a growth trajectory, it faces challenges such as pricing pressures and regulatory hurdles. Ensuring the safety and efficacy of pressure infusion bags requires compliance with stringent regulatory frameworks, which can slow down product launches and innovation. Additionally, the high cost of advanced infusion systems may limit their adoption in resource-constrained settings.

Future Outlook and Innovations

The future of the pressure infusion bags market looks promising, with continued technological advancements and a rising focus on patient-centric care. Manufacturers are expected to invest in research and development to create more efficient, cost-effective, and environmentally friendly products. Innovations like disposable pressure infusion bags, which reduce the risk of cross-contamination, and smart infusion systems with wireless monitoring capabilities, are likely to dominate the market in the coming years.

Conclusion

As healthcare systems worldwide continue to evolve, the demand for reliable, efficient medical devices like pressure infusion bags is set to increase. With a growing emphasis on patient safety, technological innovation, and the expanding healthcare infrastructure in emerging markets, the pressure infusion bags market is poised for significant growth. Industry stakeholders should focus on balancing innovation with affordability to ensure widespread adoption across diverse healthcare settings.

This blog content outlines the current landscape, opportunities, and future potential for the pressure infusion bags market, providing a comprehensive view of this critical medical device sector.

#Pressure Infusion Bags market trends#Pressure Infusion Bags market size#Pressure Infusion Bags market share#Pressure Infusion Bags market analysis#Pressure Infusion Bags market forecast#Pressure Infusion Bags market demand

0 notes

Text

Global glycolic acid market was valued at USD 307.94 million and is projected to expand at a compound annual growth rate (CAGR) of 9.08% from 2023 to 2032, anticipating a valuation of over USD 676.01 million by 2032.The global glycolic acid market is witnessing significant growth, driven by its increasing applications in various industries such as cosmetics, pharmaceuticals, and industrial cleaning. Glycolic acid, a type of alpha-hydroxy acid (AHA), is known for its excellent exfoliating properties, making it a popular ingredient in skincare products. This compound is also used in the manufacturing of polyglycolic acid, which has applications in medical sutures and biodegradable plastics. The market's expansion is further fueled by the rising consumer demand for personal care products and the growing awareness of the benefits of glycolic acid in skin treatment.

Browse the full report at https://www.credenceresearch.com/report/glycolic-acid-market

Market Size and Forecast

As of 2023, the global glycolic acid market was valued at approximately USD 325 million and is projected to reach USD 450 million by 2028, growing at a compound annual growth rate (CAGR) of 6.7% during the forecast period. The increasing adoption of glycolic acid in the cosmetic industry, particularly in anti-aging and acne treatment products, is a major factor contributing to this growth. Additionally, the pharmaceutical industry's demand for glycolic acid for drug delivery systems and the industrial sector's use for cleaning and descaling applications are expected to drive market expansion.

Key Market Drivers and Trends

1. Rising Demand in Cosmetic Industry: The cosmetic industry's growing focus on anti-aging and skincare solutions is a significant driver for the glycolic acid market. Glycolic acid's ability to improve skin texture, reduce fine lines, and treat hyperpigmentation has led to its widespread use in creams, lotions, and peels. The trend towards natural and organic ingredients in cosmetics also supports the market, as glycolic acid can be derived from natural sources like sugar cane.

2. Increasing Pharmaceutical Applications: Glycolic acid is used in the pharmaceutical industry for drug delivery systems, particularly in controlled-release medications. Its biodegradability and non-toxic nature make it an ideal component for medical applications, including absorbable sutures and implants. The ongoing research and development in drug delivery technologies are expected to enhance the demand for glycolic acid.

3. Growth in Industrial Applications: Glycolic acid's effectiveness as a cleaning and descaling agent has found applications in various industrial sectors, including oil and gas, food and beverage, and water treatment. Its ability to remove rust, scale, and other contaminants without causing damage to surfaces makes it a preferred choice for industrial cleaning solutions.

4. Emerging Markets and Technological Advancements: The market is witnessing growth opportunities in emerging economies, where the demand for personal care and pharmaceutical products is rising. Technological advancements in the production and application of glycolic acid are also contributing to market growth. Innovations in formulation and delivery methods are enhancing the effectiveness and expanding the applications of glycolic acid.

Geographical Analysis

North America and Europe currently dominate the glycolic acid market, owing to the high demand for cosmetic and personal care products in these regions. The presence of major cosmetic brands and advanced healthcare infrastructure further supports market growth. In North America, the United States is the largest market for glycolic acid, driven by the high consumer spending on skincare products and the strong presence of pharmaceutical companies.

Asia-Pacific is expected to witness the highest growth rate during the forecast period. The rising disposable income, increasing awareness of skincare benefits, and the expanding pharmaceutical industry in countries like China, India, and Japan are key factors driving the market in this region. The growing industrial sector and the adoption of advanced cleaning solutions are also contributing to the demand for glycolic acid in Asia-Pacific.

Key Players and Competitive Landscape

The glycolic acid market is moderately fragmented, with several key players contributing to market growth. Major companies operating in the market include:

1. The Chemours Company: A leading player in the glycolic acid market, Chemours offers a wide range of glycolic acid products for various applications, including personal care, industrial, and pharmaceutical sectors.

2. CABB Group: CABB Group is a significant manufacturer of glycolic acid, catering to the needs of multiple industries with its high-quality products and extensive distribution network.

3. China Petroleum & Chemical Corporation (Sinopec): Sinopec is one of the largest producers of glycolic acid in Asia, supplying the chemical for both domestic and international markets.

4. Phibro Animal Health Corporation: Known for its glycolic acid-based products in the pharmaceutical and personal care industries, Phibro Animal Health Corporation is a key player in the market.

5. CrossChem LP: CrossChem specializes in the production of glycolic acid for industrial applications, providing effective cleaning and descaling solutions.

Future Outlook

The glycolic acid market is poised for continued growth, driven by increasing applications in cosmetics, pharmaceuticals, and industrial sectors. The ongoing research and development in drug delivery systems and the rising consumer demand for anti-aging and skincare products are expected to propel market expansion. Additionally, the growing industrial applications and emerging markets present significant opportunities for key players in the glycolic acid market. As technological advancements continue to enhance the production and application of glycolic acid, the market is set to witness robust growth in the coming years.

Key Players:

DuPont

CrossChem Limited

Parchem fine and specialty chemicals

Phibro Animal Health Corporation

Chemsolv, Inc.

Griffin International

Mehul Dye Chem Industries

The Chemours Company

Vytrus Biotech

Zhonglan Industry Co., Ltd.

Water Chemical Co., Ltd.

Hefei TNJ Chemical Industry Co., Ltd.

Sarex Chemicals

Shandong Xinhua Pharmaceutical Company

Chemsafe Sdn. Bhd.

Aurora Fine Chemicals, LLC

Segmentation

By Type

Liquid Form

Powder/Crystal Form

By Application

Personal Care

Household

Industrial

Others

By Region

North America

The U.S.

Canada

Mexico

Europe

Germany

France

The U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/glycolic-acid-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Blepharitis Treatment Market will grow at highest pace owing to rising awareness and availability of novel treatment options

Blepharitis is a common eye condition characterized by irritated, flaky, and itchy eyelids. It involves the base of the eyelashes and/or eyelid margins. Some of the key symptoms include eye redness, burning sensation, watery eyes, and sensitivity to light. Blepharitis can occur due to various factors such as excessive dryness, bacterial or allergen exposure, underlying skin conditions like rosacea or seborrheic dermatitis. The available treatment options aim to reduce inflammation, manage symptoms, and prevent recurrences. This includes warm compresses, eyelid scrubs, artificial tears, antibiotics, steroids, antidepressants, and omega-3 supplements.

The global blepharitis treatment market is estimated to be valued at US$ 2.5 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030.

Key factors driving the market include rising prevalence of blepharitis, growing awareness about the condition and its treatment, and launch of novel treatment therapies.

Key Takeaways

Key players operating in the blepharitis treatment market include Scope Ophthalmic Ltd., NovaBay Pharmaceuticals Inc., Thea Pharmaceuticals Ltd., Perrigo Laboratories, InSite Vision Incorporated, Merck & Co., and Novartis AG.

Rising awareness about blepharitis and its numerous symptoms is boosting the demand for various treatment options across the globe. However, lack of acknowledgement about the condition remains a major challenge.

Development of novel drug formulations and treatment techniques are accelerating the growth of blepharitis treatment market. Players are increasingly focusing on development of combination therapies, controlled-release formulations, and therapies that are less reliant on antibiotic usage.

Market Trends

Increasing adoption of antibiotic-sparing treatments- Growing concerns about antibiotic resistance have prompted players to develop treatments that do not involve antibiotic usage. Players are exploring alternatives such as tear functional lipid emulsion therapies, bacteriophage therapies, etc.

Focus on combination therapies- Combining different treatment modalities such as warm compresses, lid scrubs, and topical therapies is gaining popularity for managing persistent or chronic blepharitis. Players are introducing fixed-dose combination products for enhanced compliance and outcomes.

Market Opportunities

Underpenetrated emerging markets- Markets in Asia Pacific, Latin America, Middle East and Africa currently account for a minimal share and offer lucrative growth opportunities. With improving access and awareness, these regions will likely witness faster uptake of blepharitis treatments.

Novel drug delivery systems- Development of advanced delivery platforms such as controlled-release gels, inserts, and biodegradable implants can help overcome challenges linked to conventional eye drop formulations. This can boost treatment outcomes.

Impact of COVID-19 on Blepharitis Treatment Market Growth

The COVID-19 pandemic has significantly impacted the growth of the blepharitis treatment market. During the initial lockdown phases, doctor consultations and non-essential medical procedures were postponed or delayed, thus restricting market growth. However, as the pandemic unfolded, treatment for chronic diseases including blepharitis continued through teleconsultations and home delivery of medicines.

While the demand for over-the-counter treatments like eyelid scrubs and warm compresses increased during the pandemic, sales of prescription drugs like topical antibiotics and steroids declined owing to deferred in-person consultations. Vaccination drives and introduction of new treatment guidelines focusing on chronic disease management have helped resume regular eye care post pandemic.

With rising awareness about eye hygiene to prevent viral transmission, the blepharitis treatment market is projected to regain lost growth momentum in the forecast period. Market players are also launching new single-use compresses and convenient packaging formats to boost product usage from homes. E-pharmacies and tele-ophthalmology are likely to play an important role for continued blepharitis management in the post-pandemic period.

#Blepharitis Treatment Market Analysis#Blepharitis Treatment Market Growth#Blepharitis Treatment Market Trend

0 notes

Text

Polymer Gel Market Analysis By Industry Growth, Size and Trends Report 2030

Global polymer gel market size was 5042.17 kilotons in 2022, which is expected to grow to 8351.04 kilotons in 2030, with a CAGR of 6.5% during the forecast period between 2023 and 2030.

The prominent variables influencing the growth of the polymer gel market are the bolstering cosmetics and personal care industry, along with the rising adoption of polymer gels in the pharmaceutical industry for application in drug delivery systems. Furthermore, the ongoing product innovations by polymer gel manufacturers to increase the application of chemicals in a diverse range of end-use industries will create a favorable potential for the market in the forecast period.

The increasing demand for baby and adult diaper products, rising innovations in female hygiene products, and the surging adoption of male segment personal care products are the key trends driving the growth of the cosmetics and personal care sector. Likewise, the increasing investment in pharmaceutical development, the surging prevalence of chronic diseases, and rapid advancement in the pharmaceutical manufacturing processes are the prime elements fostering the growth of the pharmaceutical industry. However, the recent closures of the polymer gel manufacturing facilities by global conglomerate is hindering the market growth.

Thus, the booming cosmetics and personal care, and pharmaceutical industry are the vital aspects boosting the demand for polymer gel to ensure the benefit of the three-dimensional accommodative framework. For instance, according to the Cosmetic, Toiletry and Perfumery Association (CTPA), the global cosmetics and personal care industry registered an annual growth rate of 5.4% in 2022.

The increase in research and development in the pharmaceutical industry will augment the polymer gel market growth. For instance, according to the European Federation of Pharmaceutical Industries and Associations (EFPIA), in 2022, the total investment in European Union pharmaceutical research and development was USD 46,860.7 million, an increase of 4.62%.

Sample report- https://www.marketsandata.com/industry-reports/polymer-gel-market/sample-request

Booming Cosmetics and Personal Care Industry are Augmenting Traction for the Market Growth

Polymer gel products such as polyethylene glycol, polyvinyl alcohol, and polymethyl methacrylate are utilized as gelling agents and thickeners in cosmetics ingredients to ensure superior compatibility. The cosmetics and personal care ingredients composed of polymer gel are deployed in products such as creams, lotions, men’s hygiene products, and shampoo. The increasing sales of toiletries products, the development of a new range of cosmetics and personal care products, and the recently launched personal care products manufacturing facilities are the key aspects propelling the cosmetics and personal care industry’s growth.

For instance, according to the Cosmetic, Toiletry and Perfumery Association (CTPA), in 2022, the global toiletry products industry, including diapers, makeup remover, and female hygiene products, was valued at USD 2,527.4 million, representing an annual growth rate of 1.2% as opposed to 2021. Therefore, the prospering cosmetics and personal care are boosting the demand for polymer gel as the chemical is employed as a thickening agent in products such as lip care, conditioners, and male hygiene products, this key factor is augmenting the market growth.

Bolstering Pharmaceutical Industry is Spurring the Market Growth

Polymer gels are employed in the pharmaceutical industry so that in the drug delivery systems, there is surface adherence for a longer period and showcase controlled drug release at the absorption area. The growth of the pharmaceutical sector is attributed to factors such as increasing government spending on the healthcare industry and the recent advancements in drug delivery systems.

For instance, according to the recent statistics published by the European Federation of Pharmaceutical Industries and Associations (EFPIA), in 2021, the global pharmaceutical industry was valued at USD 1,256.8 billion, and in 2022, it was USD 1,287.7 billion, a year-on-year growth rate of 2.5%. Hence, the booming pharmaceutical industry is fueling the demand for polymer gels as the chemical poses excellent rheological properties. Thus, the revenue advancement of the pharmaceutical industry is amplifying the market growth.

Growth of Multiple End-use Industries in Asia-Pacific is Augmenting the Market Growth

Asia-Pacific’s growth is driven by the revenue expansion of the end-use industries, including construction, Cosmetics and Personal Care, and pharmaceutical. Since, these end-use industries are the major end-users of the polymer gel, the expansion of various sectors in Asia-Pacific is supplementing the market growth.

For instance, according to Cosmetics Europe – The Personal Care Association, in 2022, China was the third largest market for Cosmetics and Personal Care industry valued at USD 74.8 billion. Henceforth, the rapid growth of various end-use industries in Asia-Pacific is spurring the demand for polymer gels, which in turn, is fostering market growth.

Future Outlook Scenario

The recent trend for the revenue expansion of personal care and hygiene products will create a lucrative growth outlook for the polymer gel market in the coming years. For instance, according to Invest India, the Indian personal care and hygiene industry will be valued at USD 17.34 billion in 2026.

In line with the revenue expansion of the pharmaceutical market in the upcoming years, the polymer gel industry will register growth as it is deployed in drug delivery systems. For instance, according to the recent data published by IQVIA Inc., the global medicines market will reach USD 1.9 trillion by 2027.

However, the recent phasing out of polymer gel manufacturing facilities will pose a roadblock to market growth in the coming years. For instance, in March 2022, Kuraray Co., Ltd., a Japan-based player in the polymers industry closed the manufacturing facility and sales of KURAGEL, a product range of polyvinyl alcohol (PVA) gel.

Global Polymer Gel Market: Report Scope

“Polymer Gel Market Assessment, Opportunities and Forecast, 2016-2030F”, is a comprehensive report by Markets and Data, providing in-depth analysis and qualitative and quantitative assessment of the current state of global polymer gel market, industry dynamics, and challenges. The report includes market size, segmental shares, growth trends, future outlook scenario, opportunities, and forecast between 2023 and 2030. Additionally, the report profiles the leading players in the industry mentioning their respective market share, business model, competitive intelligence, etc.

Click here for full report- https://www.marketsandata.com/industry-reports/polymer-gel-market

Contact

Mr. Vivek Gupta

5741 Cleveland street,

Suite 120, VA beach, VA, USA 23462

Tel: +1 (757) 343–3258

Email: [email protected]

Website: https://www.marketsandata.com

0 notes

Text

Rivastigmine Patch Manufacturing

In the rapidly evolving pharmaceutical industry, Sparsha Pharma has established itself as a pioneering force, particularly in the realm of transdermal drug delivery systems. Among our many innovative products, the Rivastigmine patch stands out as a testament to our commitment to enhancing patient care and improving therapeutic outcomes.

Commitment to Quality and Innovation

At Sparsha Pharma, quality is the cornerstone of our manufacturing process. Our Rivastigmine patches are designed to provide a reliable and effective treatment for patients suffering from mild to moderate dementia associated with Alzheimer's and Parkinson's diseases. By delivering the drug through the skin, these patches ensure a steady release of medication, maintaining consistent therapeutic levels in the bloodstream and reducing the likelihood of gastrointestinal side effects commonly associated with oral administration.

State-of-the-Art Manufacturing Facilities

Our manufacturing facilities are equipped with the latest technology and adhere to stringent quality control measures to ensure the highest standards of product safety and efficacy. From raw material selection to the final product, each step of the production process is meticulously monitored and tested. This rigorous approach guarantees that our Rivastigmine patches meet and exceed international regulatory requirements.

Research and Development Excellence

Innovation is at the heart of Sparsha Pharma's ethos. Our dedicated research and development team works tirelessly to improve existing formulations and develop new, more effective transdermal delivery systems. The Rivastigmine patch is a result of our continuous efforts to provide patients with a convenient and effective treatment option. By focusing on patient-centric solutions, we aim to enhance the quality of life for those affected by debilitating conditions.

Environmental Responsibility

Sparsha Pharma is also committed to sustainability and environmental responsibility. Our manufacturing processes are designed to minimize waste and reduce our carbon footprint. By implementing eco-friendly practices and using sustainable materials, we strive to contribute positively to the environment while maintaining the highest quality standards for our products.

Customer-Centric Approach

Understanding the needs of our customers is crucial to our success. We work closely with healthcare professionals and patients to gather feedback and continuously improve our products. Our customer service team is always ready to provide support and answer any questions, ensuring a seamless experience from product inquiry to post-purchase support.

Global Reach and Impact

While Sparsha Pharma is proud to be a leading manufacturer in India, our reach extends globally. Our Rivastigmine patches are trusted by healthcare providers and patients worldwide, a testament to our commitment to excellence and innovation. As we continue to expand our presence in international markets, we remain dedicated to improving patient outcomes through high-quality transdermal drug delivery systems.

Conclusion

Sparsha Pharma’s dedication to quality, innovation, and patient care has positioned us as a leader in the pharmaceutical industry. Our Rivastigmine patches exemplify our commitment to providing effective, convenient, and reliable treatment options for patients with Alzheimer's and Parkinson's diseases. As we look to the future, Sparsha Pharma will continue to push the boundaries of transdermal drug delivery, ensuring that our products meet the highest standards of efficacy and safety. Trust Sparsha Pharma for cutting-edge solutions that make a real difference in patients' lives.

0 notes

Text

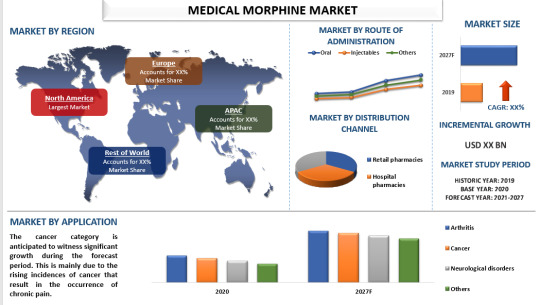

The Medical Morphine Market: Trends, Challenges, and Future Outlook

Morphine, a potent opiate analgesic, is a cornerstone in pain management, especially for severe and chronic pain conditions. Derived from the opium poppy, this powerful narcotic has been utilized for centuries to alleviate pain. In the modern medical landscape, morphine's role has evolved, and its market dynamics reflect a complex interplay of medical necessity, regulatory scrutiny, and societal challenges.

Market Overview

The global medical morphine market is driven by the increasing prevalence of chronic pain conditions, cancer-related pain, and post-surgical pain. As of 2023, the market was valued at approximately USD 13 billion and is expected to grow at a compound annual growth rate (CAGR) of around 3.5% over the next five years. The demand for morphine in pain management, especially in palliative care, continues to be robust, underscoring its essential role in modern medicine.

Key Drivers

1. Rising Prevalence of Chronic Diseases: The increase in chronic illnesses such as cancer, arthritis, and neurodegenerative diseases has led to a higher demand for effective pain management solutions. Morphine, with its efficacy in managing severe pain, remains a preferred choice among healthcare providers.

2. Aging Population: The global increase in the aging population, who are more susceptible to chronic pain and conditions requiring surgical interventions, fuels the demand for morphine. Older adults often experience complex pain conditions that necessitate strong analgesics like morphine.

3. Advancements in Drug Delivery Systems: Innovations in drug delivery systems, such as controlled-release formulations and transdermal patches, have improved the efficacy and safety profile of morphine. These advancements help in maintaining steady plasma levels of the drug, thereby enhancing pain relief and reducing side effects.

4. Government and Institutional Support: Various health organizations and governments advocate for improved pain management protocols. For instance, the World Health Organization (WHO) has been promoting the accessibility of essential medications, including morphine, in palliative care.

For a comprehensive analysis of the market drivers, visit https://univdatos.com/report/medical-morphine-market/

Challenges

Despite its critical role, the medical morphine market faces significant challenges:

1. Regulatory Hurdles: Stringent regulations regarding the production, distribution, and prescription of morphine to curb misuse and addiction pose significant barriers. Regulatory bodies like the FDA and EMA impose rigorous controls, which can delay the approval of new formulations and impact market growth.

2. Opioid Crisis: The ongoing opioid epidemic, particularly in North America, has cast a shadow over the use of opioids, including morphine. The fear of addiction and overdose has led to a more cautious approach among healthcare providers, impacting prescription rates.

3. Supply Chain Issues: The cultivation of opium poppies, necessary for morphine production, is susceptible to geopolitical factors and agricultural challenges. This can lead to supply chain disruptions and affect the availability of morphine.

4. Public Perception: The stigma associated with opioid use, driven by the opioid crisis, has led to a negative perception of morphine. This affects patient acceptance and adherence to morphine-based treatments.

Regional Insights

The medical morphine market exhibits regional variations. North America remains a significant market due to high healthcare expenditure, advanced healthcare infrastructure, and a high prevalence of chronic pain conditions. However, the stringent regulatory environment and the opioid crisis have tempered growth prospects.

In contrast, the Asia-Pacific region is witnessing rapid market growth, driven by an increasing geriatric population, rising healthcare spending, and improving healthcare infrastructure. Countries like India and China are emerging as key markets, with growing awareness and acceptance of pain management therapies.

For a sample report, visit https://univdatos.com/get-a-free-sample-form-php/?product_id=22715

Future Outlook

The future of the medical morphine market lies in balancing the benefits of morphine for pain management with the need to mitigate risks associated with opioid use. Continued advancements in drug delivery systems, coupled with comprehensive pain management protocols, will enhance the therapeutic efficacy and safety of morphine.

Additionally, ongoing research into non-addictive analgesics and alternative pain management strategies could complement the use of morphine, addressing the concerns related to addiction and misuse. Policymakers and healthcare providers must work collaboratively to ensure that patients have access to effective pain relief while minimizing the potential for abuse.

Conclusion

The medical morphine market remains a vital component of the global healthcare landscape, providing essential pain relief for millions of patients. Navigating the challenges posed by regulatory scrutiny and public perception, while leveraging technological advancements, will be crucial in shaping the future of this market. As healthcare systems evolve, the role of morphine in pain management will continue to be pivotal, albeit within a framework that prioritizes patient safety and effective pain control.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411x

Website -www.univdatos.com

#Medical Morphine Market#Medical Morphine Market Size#Medical Morphine Market Growth#Medical Morphine Market Forecast

0 notes

Text

Unlocking Potential: How Technology is Transforming the Global Sphingolipids Market

The global sphingolipid market is on track for remarkable growth, poised to exceed a valuation of USD 564.0 million in 2021 and projected to achieve a Compound Annual Growth Rate (CAGR) of 5.1% by the end of 2032, reaching an estimated value of around USD 991.8 million.

Sphingolipids are essential for the creation and function of cell membranes, and lipid-based drug delivery methods greatly benefit from their special qualities. Sphingolipids present versatile strategies for augmenting drug solubility and stability, as well as enabling targeted administration and controlled release, in an array of therapeutic applications.

Because of its special qualities and potential for therapeutic uses, the broad family of lipids known as sphingolipids is showing up more and more in pharmaceutical formulations. They are essential for cell signaling and structure. Due to the rising need for both natural and synthetic sphingolipids and monomers in the production of numerous medicinal goods, sphingolipid sales are expected to rise.

Gain a Competitive Edge: Request Your Sample:

https://www.futuremarketinsights.com/reports/sample/rep-gb-15713

This factor might significantly improve the adoption and consumption of pharmaceutical sphingolipids. The rising product launches and approvals are expected to contribute to the market growth over the forecast period too.

Key Takeaways from Market Study:

Sphingomyelin is the leading segment as a product and holds approximately 0% market share in 2021, due to its anti-cancer, bacteriostatic, and cholesterol-lowering characteristics.

Synthetic sphingolipids are the leading segment by source, and held about 4% market share in 2021, owing to their potential as therapeutic prospects for treating a range of medical problems.

Conventional lipid-based drug delivery systems (LBDDS) is the leading segment in terms of application holding about 9% of the market share, as compared to traditional tablets or powder-filled capsules, as they can improve bioavailability and reduce dissolving rate-limited absorption because of their pharmacological composition in a solubilized condition.

Semi-solid form of sphingolipids is the leading form as of 2021, withholding about 3% of the global market share, owing to the property of reduced adverse side effects when a high drug load is applied to the area where the medication is actually required.

Pharmaceutical companies are the leading end users of the global market as of 2021, withholding about 5% of the market share, because of increased outsourcing, innovative modalities, and creative patient outreach tactics.

By region, North America is leading in the global sphingolipids market and is expected to continue to do so with a projected CAGR of 4% during the forecasted years.

“Rising initiatives to promote health benefits of sphingolipids products, as well as the increasing ongoing research and development in modifying novel sphingolipids formulations is set to propel the market of sphingolipids across the globe,” says an analyst of Future Market Insights.

Market Competition

Companies are actively working to increase their market share in this industry by forming strategic agreements to diversify their respective service offerings and sphingolipid production capacities.

In January 2022, Pfizer and Acuitas Therapeutics reached an agreement on Lipid Nanoparticle Delivery System for mRNA vaccines and therapeutics.

June 2022: To support customers’ scientific research, CD Bioparticles, enlarged its lipid system portfolio and introduced a number of Sphingolipids products. With the addition of Phosphosphingolipids, Ceramides, Sphingolipid Metabolism, Sphingosines, Glycosphingolipids, Phytosphingosine, and Sphingomyelin, researchers now have more options to choose from and employ in lipid system applications.

Key Companies Profiled

Merck KGaA

CordenPharma International

Lipoid GmbH

LARODAN AB

Croda International Plc.

Biosynth, Santa Cruz Biotechnology, Inc.

Creative Enzymes

CD Bioparticles

Cayman Chemical Company

Biosolve BV

Key Segments Covered In Sphingolipids Industry Research

By Product:

Ceramide

Sphingomyelin

Glucosylceramide (GlcCer)

Lactosylceramide (LacCer)

Ganglioside GM3

Other

By Source:

Synthetic

Semi-synthetic

Natural

By Application:

Conventional Lipid-based Drug Delivery Systems (LBDDS)

Self-Emulsifying Drug Delivery Systems (SEDDS)

Self-Microemulsifying Drug Delivery Systems (SMEDDS)

Liposomes

Solid Lipid Nanoparticles

Nanostructured Lipid Carriers

Others

By Form:

Liquid

Semi-solid

Solid

By End User:

Pharmaceutical Companies

Biopharmaceutical Companies

Academics and Research Institutes

Others

0 notes

Text

Understanding the Growth Dynamics of the Oral Transmucosal Drugs Market

The Oral Transmucosal Drugs Market is projected to be valued at USD 16.57 billion in 2024 and is anticipated to grow to USD 22.97 billion by 2029, with a compound annual growth rate (CAGR) of 6.75% over the forecast period (2024-2029).

The oral transmucosal drugs market has been gaining traction due to its unique drug delivery system that allows medications to be absorbed directly into the bloodstream through the oral mucosa, bypassing the digestive system. This method provides a faster onset of action and is beneficial for patients who struggle with oral intake or those requiring rapid relief. In this blog, we will explore the current trends, key drivers, and challenges shaping the market landscape, based on insights from the market research industry.

1. Market Overview: A Shift Towards Patient-Centric Drug Delivery

The global oral transmucosal drug market is experiencing notable growth due to its convenience and improved patient compliance. This mode of administration is particularly useful in treating conditions like breakthrough cancer pain, migraines, and anxiety, where rapid drug action is critical. The ability to deliver precise dosages through buccal, sublingual, or nasal routes offers a viable alternative to traditional oral or intravenous methods.

Market research points to a growing interest in transmucosal drug delivery systems as pharmaceutical companies look for ways to improve drug efficacy and enhance patient experiences.

2. Key Drivers of Market Growth

a. Advances in Drug Formulations

Continuous advancements in drug formulations are driving the oral transmucosal drugs market forward. Innovations in bioavailability and the stability of drugs administered through the mucosal lining are improving therapeutic outcomes. Pharmaceutical firms are investing in research to create formulations that ensure quicker absorption and minimal side effects.

b. Rising Demand for Pain Management Solutions

Chronic pain management remains one of the top application areas for oral transmucosal drugs. Cancer patients, especially those experiencing breakthrough pain, benefit significantly from this delivery system. Furthermore, the rise in demand for pain management due to the aging population is expected to fuel the market's expansion.

c. Patient Preference for Non-invasive Drug Delivery

Patients are increasingly favoring non-invasive drug delivery methods over traditional injections or tablets. Oral transmucosal administration provides a less invasive approach, making it suitable for individuals with swallowing difficulties, such as pediatric or elderly patients, or those who require rapid symptom control.

3. Challenges and Restraints

a. Regulatory and Approval Complexities

The complexity of obtaining regulatory approvals for transmucosal drugs can be a hurdle for market players. The stringent evaluation of safety, efficacy, and potential risks associated with absorption variability can delay the introduction of new drugs into the market. Pharmaceutical companies need to navigate these regulatory landscapes carefully.

b. Competition from Other Drug Delivery Systems

While oral transmucosal delivery offers distinct advantages, it faces competition from other emerging drug delivery technologies such as transdermal patches, inhalation systems, and implantable devices. Each method comes with its own set of benefits and limitations, leading to a competitive landscape where companies need to differentiate their offerings.

4. Innovations and Opportunities in the Market

a. Breakthroughs in Bioadhesive Technologies

New developments in bioadhesive technologies are enhancing the effectiveness of oral transmucosal drugs. These innovations improve the adhesion of drugs to the mucosal surfaces, ensuring prolonged contact and better absorption rates. The integration of nanoparticles and microencapsulation techniques is also opening new avenues for controlled drug release.

b. Personalized Medicine and Custom Drug Formulations

With the rise of personalized medicine, there is increasing demand for customizable drug formulations in the oral transmucosal segment. Tailoring drug delivery to individual patient needs based on genetic, metabolic, and lifestyle factors offers new possibilities for the industry. This personalized approach aligns with broader trends toward precision medicine, which seeks to optimize treatment outcomes.

5. Future Outlook: Market Expansion and Growth Potential

According to recent market research, the oral transmucosal drugs market is projected to expand significantly over the next decade. This growth will be driven by continued advancements in drug delivery technologies, a rising prevalence of chronic diseases requiring quick therapeutic responses, and increased investments in R&D by pharmaceutical companies. Moreover, the shift towards more patient-centric healthcare solutions will continue to push this market forward.

Final Thoughts

The oral transmucosal drugs market is positioned for substantial growth due to its unique benefits and applications in various therapeutic areas. As pharmaceutical companies focus on enhancing drug delivery methods, investing in innovative formulations, and navigating regulatory challenges, this market will continue to evolve. Understanding the market trends, drivers, and opportunities can help stakeholders in the healthcare sector make informed decisions to capitalize on this burgeoning industry.Call to Action: Interested in exploring more insights on the oral transmucosal drug market? Stay ahead of the curve with comprehensive market research reports that delve deeper into emerging trends and forecast analyses for the next decade.

#Oral Transmucosal Drugs Market trends#Oral Transmucosal Drugs Market size#Oral Transmucosal Drugs Market share#Oral Transmucosal Drugs Market analysis#Oral Transmucosal Drugs Market forecast#Oral Transmucosal Drugs Market demand

0 notes

Text

Gelatin Methacryloyl Market to Reach USD 309.0 million by 2031, Growing at a CAGR of 6.6% from 2023-2031

The global gelatin methacryloyl market is estimated to flourish at a CAGR of 6.6% from 2023 to 2031. According to Transparency Market Research, sales of gelatin methacryloyl are slated to total US$ 309.0 million by the end of the aforementioned period of assessment.

Combining gelatin methacryloyl with other biomaterials like alginate or chitosan has unlocked the potential for creating hybrid hydrogels with enhanced mechanical properties and functionalities. These novel composites find applications in regenerative medicine, drug delivery, and wound healing, showing promising outcomes in various preclinical studies.

Download Sample PDF Copy at: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=85737

Market Segmentation

By Service Type

Synthesis and Purification Services: These services are critical for ensuring high-quality GelMA suitable for sensitive biomedical applications.

Research and Development Services: These services support the innovation of new applications and improvements in GelMA formulations.

By Sourcing Type

Animal-Based GelMA: Derived from animal gelatin, commonly used due to its availability and cost-effectiveness.

Plant-Based GelMA: Emerging as a sustainable and ethically preferred alternative, although currently less common.

By Application

Tissue Engineering: Utilized in developing scaffolds for tissue regeneration.

Drug Delivery Systems: Used to create controlled-release drug delivery mechanisms.

Wound Healing: Applied in developing advanced wound dressings.

3D Bioprinting: Employed in the creation of complex tissue constructs.

By Industry Vertical

Healthcare: Primary market, including hospitals, clinics, and research institutions.

Pharmaceutical: Utilized in drug formulation and delivery systems.

Biotechnology: Used in various biotech research and development activities.

By Region

North America: Leading market due to significant investment in healthcare R&D.

Europe: Strong growth driven by robust biomedical research infrastructure.

Asia-Pacific: Rapid expansion owing to increasing healthcare expenditure and R&D activities.

Latin America: Growing interest and investment in biotechnological advancements.

Middle East & Africa: Emerging market with potential growth due to improving healthcare infrastructure.

Regional Analysis

North America

North America dominates the GelMA market, primarily due to the presence of leading biomedical research institutions and substantial funding for medical research. The United States is the major contributor to the market, with numerous ongoing projects in tissue engineering and regenerative medicine.

Europe

Europe follows closely, with Germany, the UK, and France being the key players. The region's well-established healthcare system and strong emphasis on innovative research contribute to the market growth.

Asia-Pacific

The Asia-Pacific region is witnessing the fastest growth rate, driven by increasing investments in healthcare infrastructure and research. Countries like China, Japan, and India are at the forefront of this expansion.

Latin America and Middle East & Africa

These regions are emerging markets with growing investments in the healthcare sector. Improving medical facilities and increasing research activities are expected to boost market growth in the coming years.

Market Drivers and Challenges

Market Drivers

Increasing Biomedical Research: The surge in research activities in tissue engineering and regenerative medicine fuels the demand for GelMA.

Rising Prevalence of Chronic Diseases: Growing incidence of chronic conditions necessitates advanced therapeutic solutions, driving market growth.

Technological Advancements: Innovations in 3D bioprinting and drug delivery systems enhance the applicability of GelMA.

Market Challenges

High Production Costs: The synthesis and purification of GelMA are cost-intensive, which can limit market growth.

Regulatory Hurdles: Stringent regulatory frameworks governing biomedical materials can pose challenges to market entry and expansion.

Limited Awareness and Expertise: Lack of awareness and technical expertise in emerging regions may hinder market penetration.

Market Trends

Shift Towards Plant-Based GelMA: Increasing preference for sustainable and ethical products is driving research into plant-based GelMA alternatives.

Advancements in 3D Bioprinting: Enhanced capabilities in 3D bioprinting technology are expanding the scope of GelMA applications.

Integration with Smart Technologies: Combining GelMA with smart technologies for responsive drug delivery and tissue engineering applications.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=85737<ype=S

Future Outlook

The Gelatin Methacryloyl market is poised for significant growth over the next decade. Continued advancements in biomedical research and technology, coupled with increasing healthcare investments, will drive the market. Efforts to reduce production costs and streamline regulatory processes will further enhance market expansion. By 2031, the market is expected to reach a valuation of approximately USD 500 million.

Key Market Study Points

Market Dynamics: Understanding drivers, challenges, and trends shaping the market.

Regional Insights: Analyzing market performance and growth opportunities across different regions.

Competitive Landscape: Evaluating key players and their strategies in the market.

Technological Innovations: Assessing the impact of new technologies on market growth.

Competitive Landscape

The Gelatin Methacryloyl market is highly competitive with several key players, including:

X company: Known for extensive R&D and high-quality GelMA products.

Y company: Focuses on cost-effective synthesis and large-scale production.

Z company: Specializes in innovative applications of GelMA in drug delivery and tissue engineering.

Recent Developments

X company's New Facility: Opened a state-of-the-art production facility to enhance GelMA synthesis capabilities.

Y company's Collaboration: Partnered with a leading research institute to explore new applications of GelMA in regenerative medicine.

Z company's Product Launch: Introduced a new line of plant-based GelMA products targeting sustainable and ethical markets.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Shaping Tomorrow's Healthcare: Exploring the Growth Trajectory of 4D Printing

The 4D Printing in Healthcare Market represents a cutting-edge intersection of additive manufacturing technology and healthcare innovation, offering transformative solutions for patient care, personalized medicine, and medical device development. In this analysis, we explore the key drivers, trends, challenges, and opportunities shaping the 4D Printing in Healthcare Market.

𝐆𝐞𝐭 𝐟𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞:

https://www.marketdigits.com/request/sample/3917

One of the primary drivers of the 4D Printing in Healthcare Market is the increasing demand for patient-specific medical devices and implants. Traditional manufacturing techniques often struggle to produce complex, customized medical devices tailored to individual patient anatomy. 4D printing, an advanced form of additive manufacturing, enables the fabrication of dynamic, shape-changing structures with predetermined responses to external stimuli, such as temperature, humidity, or light. This capability allows for the creation of personalized implants, prosthetics, and orthotics that conform to patients' unique anatomical requirements and provide superior fit, comfort, and functionality.

The 4D Printing in Healthcare Market is valued at USD 9.5 million in 2024 and projected to reach USD 47.5 million by 2030, showing a Compound Annual Growth Rate (CAGR) of 22.3% during the forecast period from 2024 to 2032.

Moreover, 4D printing offers significant advantages over traditional manufacturing methods in terms of design flexibility, material selection, and manufacturing efficiency. With 4D printing, designers can create intricate, multi-material structures with precise control over geometry, porosity, and mechanical properties. This versatility enables the development of biocompatible scaffolds, drug delivery systems, and tissue-engineered constructs for regenerative medicine and tissue engineering applications. By integrating bioactive materials and cell-laden hydrogels into 4D-printed constructs, researchers can mimic native tissue architectures and promote tissue regeneration for wound healing, organ repair, and transplantation.

Major vendors in the global 4D printing in healthcare Market are 3D Systems, Organovo Holdings Inc., Stratasys Ltd., Dassault Systèmes, Materialise, EOS GmbH Electro Optical Systems, EnvisionTEC, and Poietis and others

Furthermore, the convergence of 4D printing with advanced imaging technologies, such as computed tomography (CT) and magnetic resonance imaging (MRI), facilitates the creation of patient-specific anatomical models and surgical guides for preoperative planning and intraoperative navigation. Surgeons can use 4D-printed models to visualize complex anatomical structures, simulate surgical procedures, and practice intricate maneuvers before entering the operating room. This enhanced visualization and surgical simulation improve surgical precision, reduce operative time, and minimize complications, ultimately leading to better patient outcomes and healthcare cost savings.

In addition to its applications in medical device manufacturing and surgical planning, 4D printing holds promise for drug delivery and personalized medicine. By incorporating stimuli-responsive polymers and controlled-release mechanisms into 4D-printed drug delivery systems, researchers can achieve targeted, on-demand drug release profiles tailored to individual patient needs. This precision drug delivery approach enables the administration of therapeutics at specific sites of action, optimized dosing regimens, and improved patient compliance. Furthermore, 4D-printed drug-eluting implants and microneedle arrays offer innovative solutions for localized drug delivery, chronic disease management, and regenerative therapies.

However, the 4D Printing in Healthcare Market also faces challenges and barriers to widespread adoption, including material biocompatibility, regulatory approval, and scalability of manufacturing processes. Ensuring the safety, efficacy, and biocompatibility of 4D-printed medical devices and implants requires rigorous testing, validation, and regulatory oversight to meet quality standards and regulatory requirements. Moreover, scaling up 4D printing technologies for mass production while maintaining cost-effectiveness and manufacturing consistency remains a challenge for commercialization and market penetration.

In conclusion, the 4D Printing in Healthcare Market holds immense promise for revolutionizing patient care, personalized medicine, and medical device development. By harnessing the unique capabilities of 4D printing technology, healthcare professionals can create customized solutions that improve treatment outcomes, enhance patient experiences, and advance the practice of precision medicine. While challenges remain, ongoing research, collaboration, and innovation in the field are driving progress and expanding the clinical applications of 4D printing in healthcare.

0 notes

Text

Gastritis Treatment Market to Grow at Highest Pace Owing to Rising Prevalence of Gastric Disorders

The global gastritis treatment market is estimated to be valued at US$ 131.76 billion in 2024 and is expected to exhibit a CAGR of 6.2% over the forecast period 2023 to 2030. Gastritis refers to the inflammation or irritation of the stomach lining. It can occur due to numerous reasons such as infection by Helicobacter pylori bacteria, intake of certain medications like NSAIDs, and heavy alcohol consumption. Gastric disorders like acidity, ulcers, and gastric erosion can develop if gastritis remains untreated for a prolonged period.

The global gastritis treatment market is driven by the rising prevalence of gastric disorders due to changing lifestyle habits and food preferences. According to studies, approximately 60-80% of the global population is infected by H. pylori bacteria, which is a major causative factor for gastritis. Furthermore, the market is also witnessing growth due to the increasing usage of over-the-counter antacids and proton pump inhibitors (PPIs) for instant relief from minor gastric problems.

Key Takeaways

Key players operating in the gastritis treatment market are Pfizer Inc., AstraZeneca plc, Johnson & Johnson, Novartis AG, Takeda Pharmaceutical Company Limited. These players collectively account for a significant share of the global market.

The rising prevalence of gastric disorders like acidity and ulcers is fueling the demand for gastritis treatment drugs. According to estimates, nearly 25% of the adult population suffers from acidity or heartburn issues globally.

Technological advancements are being made in drug delivery systems and formulations for gastritis treatment. Many players are introducing novel drug combinations, controlled-release formulations, and other innovations to enhance drug efficacy.

Market Trends

Increased adoption of combination therapy - Many clinical trials are exploring the efficacy of combining multiple drugs like PPIs with antibiotics for achieving faster and better relief from chronic gastritis caused by H. pylori infections. This trend is expected to continue over the forecast period.

Rise in natural and herbal treatment options - With growing preference for natural remedies, herbal formulations containing ingredients like licorice, slippery elm, and marshmallow are gaining attention for treating minor gastric disorders like acidity.

#Gastritis Treatment Market Demand#Gastritis Treatment Market Analysis#Gastritis Treatment Market Growth

0 notes

Text

Pharmaceuticals Logistics Market to Witness Robust Expansion Throughout the Forecast Period 2024 - 2031

The global pharmaceuticals logistics market continues its upward trajectory, according to a recent report released by SNS Insider. The report reveals that the market size was valued at USD 92.74 billion in 2023 and is expected to double, reaching USD 186.47 billion by 2031. This growth is anticipated to be driven by various factors and trends shaping the pharmaceuticals logistics landscape.

Market Analysis

The pharmaceuticals logistics market is witnessing robust growth due to increasing demand for efficient and secure transportation of pharmaceutical products worldwide. Factors such as the rising prevalence of chronic diseases, expanding pharmaceutical industry, and stringent regulations regarding the transportation of drugs are fueling market growth. Additionally, the COVID-19 pandemic has underscored the importance of reliable logistics systems for the timely delivery of essential medical supplies, further boosting market expansion.

Get Free Sample Report @ https://www.snsinsider.com/sample-request/2749

Emerging Trends and Opportunities

Several emerging trends are reshaping the pharmaceuticals logistics market. The adoption of advanced technologies, including blockchain, IoT, and AI, is enhancing supply chain visibility and traceability, thus reducing the risk of counterfeit drugs and ensuring product integrity. Moreover, the growing popularity of temperature-controlled logistics solutions to maintain the efficacy of temperature-sensitive pharmaceuticals presents lucrative opportunities for market players.

Key Drivers Propelling Growth

Key drivers propelling the growth of the pharmaceuticals logistics market include:

Rising Demand for Biopharmaceuticals: The increasing demand for biopharmaceuticals, coupled with the need for specialized logistics services to handle these complex products, is driving market growth.

Globalization of Pharmaceutical Supply Chains: The globalization of pharmaceutical supply chains is necessitating efficient logistics solutions to ensure seamless distribution of drugs across diverse geographies.

Stringent Regulatory Standards: Stringent regulatory standards pertaining to the transportation and storage of pharmaceuticals are compelling companies to invest in compliant logistics infrastructure.

E-commerce Expansion: The proliferation of e-commerce platforms for pharmaceutical products is creating new avenues for logistics providers to cater to direct-to-consumer distribution channels.

Challenges and Considerations

Despite the promising growth prospects, the pharmaceuticals logistics market faces certain challenges and considerations, including:

Complex Regulatory Environment: Navigating the complex regulatory landscape, especially concerning international shipments, can pose challenges for logistics companies.

Infrastructure Limitations: Inadequate infrastructure in certain regions may hinder the efficient transportation and storage of pharmaceutical products, particularly those requiring specialized handling.

Security Concerns: Ensuring the security and integrity of pharmaceutical shipments against theft, tampering, or counterfeiting remains a critical concern for logistics providers.

Key Takeaways from the Market

In conclusion, the pharmaceuticals logistics market is poised for substantial growth over the forecast period of 2024-2031, driven by increasing demand for pharmaceutical products, advancements in logistics technologies, and evolving regulatory standards. Market players are advised to capitalize on emerging opportunities, such as the adoption of temperature-controlled logistics solutions and the integration of digital platforms for enhanced supply chain visibility. However, addressing challenges related to regulatory compliance, infrastructure limitations, and security concerns will be crucial for sustained market success.

0 notes

Text

Alginates and Derivatives Industry: Comprehensive Study Explore Huge Growth in Future

Alginates and Derivatives Market Overview

The alginates and derivatives market refers to the industry involved in the production, distribution, and sale of alginate compounds and their various derivatives. Alginates are a group of naturally occurring polysaccharides found in brown seaweeds, primarily consisting of mannuronic acid and guluronic acid residues. They are widely used in various industries due to their unique properties, including thickening, gelling, stabilizing, and film-forming capabilities.

Alginates and their derivatives, derived from brown seaweed, exhibit remarkable versatility and have established themselves as indispensable multifunctional ingredients across a variety of industries. Sodium alginate, a key derivative, showcases its adaptability in numerous applications spanning from culinary endeavors to agricultural practices. In the culinary field, alginates function as essential gelling, thickening, and stabilizing agents, enabling the creation of diverse textures and presentations in foods ranging from sauces to desserts.

Beyond the culinary realm, alginates are proving their worth in agriculture, serving as effective soil conditioners that enhance soil structure, moisture retention, and nutrient availability, thereby fostering sustainable farming methods. Moreover, the unique attributes of alginates make them valuable in biotechnological applications, such as cell encapsulation for drug delivery and the development of biocompatible matrices for bioartificial organs. Additionally, alginates contribute significantly to water treatment processes, acting as flocculating agents that aid in the removal of impurities and the clarification of water.

Alginates and Derivatives Market Forecast

The alginates and derivatives market size is estimated at USD 494 million in 2023 and is projected to reach USD 651 million by 2028, at a CAGR of 5.7% from 2023 to 2028.

Factors Driving the Alginates and Derivatives Industry Growth

Alginate, a natural polysaccharide extracted from brown seaweed, offers a remarkable range of functionalities due to its gelling, thickening, biocompatible, and encapsulating properties. These functionalities translate into a vast array of applications across various industries.

Food Industry: Alginate excels as a gelling agent in desserts, dairy products, and meat products. It also acts as a thickening and stabilizing agent in sauces, dressings, and texturizer for various food items, improving texture and mouthfeel. Additionally, alginate films with good water retention properties extend the shelf life of fruits and vegetables.

Make an Inquiry to Address your Specific Business Needs: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=77102420

Pharmaceuticals and Biomedical Applications: Alginate's biocompatibility and low toxicity make it ideal for wound care products, drug delivery systems with controlled release, and tissue engineering.

Other Applications: Alginate derivatives function as emulsifiers in salad dressings, ice cream, and cosmetics. Furthermore, alginate-based materials play a role in environmental applications like wastewater treatment and bioremediation by binding pollutants.

The multifunctionality of alginates and their derivatives results in their widespread adoption across diverse industries, driving the alginate market growth. As industries continue to seek sustainable and natural alternatives, alginate's eco-friendly nature further contributes to its market appeal.

Opportunities for manufacturers in the global alginates and derivatives industry

The global rise in convenience food consumption is driven by factors like busy lifestyles, increased female workforce participation, and longer working hours. This trend creates a significant demand for food additives that enhance the quality, texture, and taste of processed foods like soups, cakes, pastries, bread, gravies, and snacks. Alginates perfectly fit this role.

Functional Benefits of Alginates: Alginates act as thickening, gelling, and binding agents, allowing manufacturers to create appealing textures and mouthfeel in convenience foods. Additionally, alginates can help reduce fat content, catering to the growing consumer preference for low-calorie and low-fat options.

Market Opportunity for Alginate Manufacturers: The demand for customized food additives presents an opportunity for alginate producers. Companies like Ashland Inc. offer specialized alginates for various applications in dairy, confectionery, bakery, and other convenience food sectors.

According to type, sodium alginate is expected to hold the largest alginates and derivatives market share

Culinary Artistry: Sodium alginate's gelling properties revolutionize food presentation through techniques like spherification, while also stabilizing and enhancing textures of sauces and dairy products.

Pharmaceutical Advancements: In the medical field, sodium alginate acts as a disintegrant in drugs, promoting absorption, and facilitates controlled-release drug delivery systems.

Textile Industry: During dyeing and printing, sodium alginate's thickening properties ensure even dye distribution for better color retention in fabrics.

Healthcare Applications: Wound dressings containing sodium alginate manage moisture balance in exuding wounds, accelerating healing.

Biotechnology Frontiers: Sodium alginate plays a crucial role in cell encapsulation, advancing cell culture, tissue engineering, and regenerative medicine. Furthermore, it acts as a flocculating agent in water treatment, aiding in purification.

Creative Realm: Beyond industrial applications, artists and designers utilize sodium alginate's gel-forming properties to create unique molds and casts.

Sodium alginate, derived from seaweed, is a remarkably versatile material with applications that span numerous industries.

The European market will make the most significant contribution to the global alginates and derivatives processing market

The alginates and derivatives market in Europe is experiencing significant growth, driven by industries embracing the diverse applications of this natural compound. The active participation of European countries in global trade enhances the accessibility of alginates, facilitating their flow across borders and supporting various industries with their versatile applications. European nations play pivotal roles in global trade, serving as both importers of raw materials and exporters of finished products. The demand for alginates in Europe influences international trade dynamics, impacting production, pricing, and supply chains on a global scale.

Schedule a call with our Analysts to discuss your business needs: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=77102420

Furthermore, Europe has been leading environmental awareness and sustainability initiatives. Alginate, being a natural and biodegradable material, stands to benefit from the region's growing emphasis on eco-friendly products and practices.

Primary companies highlighted

Alginates and derivatives market key players include FMC Corporation (US), Kimica Corporation (Japan), Cargill, Inc (US), E.I. Dupont De Nemours And Company (US), The Dow Chemical Company (UK), Penford Corporation (US), Ashland Inc. (US), Brenntag AG (Germany), Dastech International, Inc (US), Snap Natural & Alginate Products Pvt. Ltd (India), Bright Moon Group (China), and Döhler Group (Germany). These players in this market are focusing on increasing their presence through expansion

Key Questions Addressed by the alginates and derivatives market report

What is the current size of the global alginates and derivatives market?

What is the economic importance of alginate?

What drives the alginates & derivatives market?

0 notes

Text

Global Sustained Release Excipients Market Insights

The Global Sustained Release Excipients Market size was valued at USD 1.26 billion in 2022 and is projected to grow at a CAGR of 8.4% during the forecast period (2024-2031), reaching USD 2.60 billion by 2031.

Sustained release excipients are vital components in pharmaceutical formulations designed to release drugs gradually over an extended period. This gradual release enhances patient compliance, reduces dosing frequency, and improves therapeutic outcomes. The market for sustained release excipients has witnessed significant growth, driven by factors such as the increasing prevalence of chronic diseases, the demand for innovative drug delivery systems, and the rising adoption of controlled-release formulations by pharmaceutical companies.

Market Snapshot - 2024-2031:

Global Market Size:

2022: USD 1.26 billion

2023: USD 1.37 billion

2031: USD 2.60 billion

Growth Rate: 8.4% CAGR

Global Sustained Release Excipients Market Segmental Analysis:

Product Type:

Polymers: Dominating the market due to versatility and compatibility.

Sugars: Emerging as the fastest-growing segment due to increasing awareness and interest in natural excipients.

Technology:

Targeted Delivery: Leading due to the demand for precision in drug delivery.

Microencapsulation: Fastest-growing segment, offering versatility and controlled release benefits.

For More Information: https://www.skyquestt.com/report/commercial-building-automation-market

Global Sustained Release Excipients Market Regional Insights:

North America: Dominates the market with a well-established pharmaceutical industry and strong regulatory frameworks.

Asia-Pacific: Witnessing rapid growth driven by increasing disposable incomes and expanding pharmaceutical manufacturing capabilities.

Global Sustained Release Excipients Market Dynamics:

Drivers: Growing aging population and emphasis on personalized medicine.

Restraints: Regulatory challenges and navigating complex approval processes.

Global Sustained Release Excipients Market Competitive Landscape:

Fierce competition among companies driving innovation in excipient formulations and delivery systems.

Strategic partnerships and acquisitions to expand market reach.

Top Players:

Allergan PLC

AstraZeneca

GlaxoSmithKline PLC

Pfizer Inc.

Novartis AG

Johnson & Johnson

Teva Pharmaceutical Industries Ltd

and others.

Recent Developments:

Introduction of sustained-release Prolanza ashwagandha by Nutriventia.

Optimism for rimegepant by Biohaven Pharmaceutical Holding Company Ltd and Pfizer Inc.

Key Market Trends:

Increased focus on personalized medicine.

Adoption of advanced technologies such as nanotechnology and biodegradable excipients.

Conclusion: The sustained release excipients market is poised for significant growth driven by the increasing demand for controlled-release drug formulations and emphasis on personalized medicine. Strategic partnerships, technological advancements, and regulatory compliance will shape the market's trajectory, offering ample opportunities for innovation and growth.

About Us-

SkyQuest Technology Group is a Global Market Intelligence, Innovation Management & Commercialization organization that connects innovation to new markets, networks & collaborators for achieving Sustainable Development Goals.

Contact Us-

SkyQuest Technology Consulting Pvt. Ltd.

1 Apache Way,

Westford,

Massachusetts 01886

USA (+1) 617–230–0741

Email- [email protected]

Website: https://www.skyquestt.com

0 notes

Text

Opioids Market Global Industry Analysis and Forecast (2023-2032)

Market Overview –

The opioids market is predicted to grow at a 5.4% CAGR between 2023 and 2032, reaching USD 6.93 billion.

The Opioids Market encompasses pharmaceutical drugs derived from opium or synthesized to mimic its effects, primarily used for pain management. Opioids are potent analgesics commonly prescribed for acute and chronic pain conditions, including postoperative pain, cancer-related pain, and severe injuries. However, the widespread use of opioids has led to concerns about addiction, overdose, and misuse.

The opioids market, while grappling with addiction concerns, sees a promising trend with the growing adoption of naltrexone. This medication offers a novel approach to managing opioid dependence by blocking opioid receptors, reducing cravings and withdrawal symptoms. As awareness rises, naltrexone's role in addiction treatment strengthens, contributing to a multifaceted approach to opioid management.

In recent years, the opioids market has witnessed significant growth globally due to several factors. Firstly, there has been increasing recognition of the need for effective pain management options, particularly in the context of aging populations and rising prevalence of chronic pain conditions. Key players in this market include pharmaceutical companies, healthcare providers, pain management clinics, and regulatory agencies, collaborating to develop and distribute opioids responsibly while mitigating risks of abuse and addiction.

Moreover, advancements in opioid formulations and delivery systems have led to the development of extended-release, abuse-deterrent, and non-opioid combination products. These innovations aim to improve pain control, reduce side effects, and minimize the potential for addiction and misuse.

Segment analysis