#Home Automation System Market Home Automation System Market Forecast Home Automation System Market Growth Home Automation System Market Tren

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

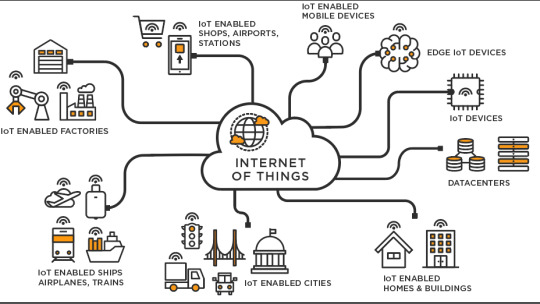

Internet of Things Technology Market

Internet of Things Technology Market is analyzed to grow at a CAGR of 11.9% during the forecast 2021–2026 to reach $1,021 billion by 2026.

🔗 𝐆𝐞𝐭 𝐑𝐎𝐈-𝐟𝐨𝐜𝐮𝐬𝐞𝐝 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐟𝐨𝐫 𝟐𝟎𝟐𝟓-𝟐𝟎𝟑𝟏 → 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐍𝐨𝐰

Internet of Things (IoT) technology market is experiencing rapid growth, driven by rising demand for connected devices, smart automation, and real-time data analytics across industries. Valued at over USD 600 billion in 2024, the market is projected to surpass USD 1.5 trillion by 2030, fueled by advancements in 5G, AI, and cloud computing. IoT is transforming sectors like manufacturing, healthcare, transportation, and smart homes by enabling predictive maintenance, efficient resource use, and enhanced user experiences. As enterprises pursue digital transformation, the IoT ecosystem continues to expand, integrating edge computing and cybersecurity solutions to support secure, scalable connectivity worldwide.

🔌 𝟏. 𝐑𝐢𝐬𝐢𝐧𝐠 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐨𝐟 𝐒𝐦𝐚𝐫𝐭 𝐃𝐞𝐯𝐢𝐜𝐞𝐬

Increasing use of smartphones, wearables, smart appliances, and industrial sensors is expanding IoT deployment across consumer and enterprise sectors.

☁️ 𝟐. 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬 𝐢𝐧 𝐂𝐥𝐨𝐮𝐝 𝐂𝐨𝐦𝐩𝐮𝐭𝐢𝐧𝐠 & 𝐄𝐝𝐠𝐞 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐲

Cloud platforms enable scalable data storage and analytics, while edge computing allows real-time processing close to devices — crucial for latency-sensitive applications.

📶 𝟑. 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐨𝐟 𝟓𝐆 𝐍𝐞𝐭𝐰𝐨𝐫𝐤𝐬

Faster and more reliable connectivity from 5G is enhancing IoT performance in real-time applications like autonomous vehicles and remote healthcare.

🏭 𝟒. 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐢𝐚𝐥 𝐀𝐮𝐭𝐨𝐦𝐚𝐭𝐢𝐨𝐧 & 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝟒.𝟎

Manufacturers are leveraging IoT for predictive maintenance, supply chain optimization, and energy efficiency as part of digital transformation efforts.

🧠 𝟓. 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐰𝐢𝐭𝐡 𝐀𝐈 & 𝐌𝐚𝐜𝐡𝐢𝐧𝐞 𝐋𝐞𝐚𝐫𝐧𝐢𝐧𝐠

AI/ML allows IoT systems to process and act on large volumes of data, enabling smarter decision-making and automation.

𝐓𝐨𝐩 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬:

LG Electronics | Qualcomm | Whirlpool Corporation | Lenovo | ASML | Advanced Energy | AMD | Infineon Technologies Canada Inc. | TE Connectivity | NVIDIA | STMicroelectronics | Texas Instruments | ZTE Corporation | Micron Technology

#DigitalTransformation #Industry40 #SmartManufacturing #IoTInBusiness #TechTrends #IoTInnovation #FutureOfTech #SmartCities #SmartHomes #IndustrialIoT

0 notes

Text

AIoT Market Growth, Drivers & Opportunities 2034

The Internet of Things (IoT) and Artificial Intelligence (AI) are combined in AIoT (Artificial Intelligence of Things), which creates intelligent, networked systems that can gather data, analyse it, and make decisions on their own. AIoT improves IoT devices' functionality, efficiency, and flexibility by incorporating AI features including computer vision, machine learning, and natural language processing. In addition to communicating and exchanging information, this technology allows smart devices to anticipate results, learn from data trends, and streamline procedures without the need for human intervention. In order to enhance automation, security, and user experience, AIoT is extensively used in smart homes, healthcare, manufacturing, transportation, and other sectors.

According to SPER market research, ‘Global AIoT Market Size- By Component, By Deployment, By End User - Regional Outlook, Competitive Strategies and Segment Forecast to 2034’ state that the Global AIoT Market is predicted to reach 2737.44 billion by 2034 with a CAGR of 31.91%.

Drivers:

Because smart automation and predictive maintenance are increasing operational efficiency in the manufacturing sector, the worldwide AIoT market is expanding significantly. By fusing real-time analytics and sophisticated data processing, AIoT platform devices provide great efficiency and facilitate quicker, better-informed decision-making. For improved performance and productivity, this capability is being used more and more in a variety of industries, such as healthcare, transportation, and energy. Furthermore, governments' and businesses' increasing expenditures in IoT infrastructure and AI technologies are spurring innovation and integration of AIoT solutions, which are crucial for digital transformation and gaining a competitive edge in the global market.

Request a Free Sample Report: https://www.sperresearch.com/report-store/aiot-market.aspx?sample=1

Restraints:

The shortage of skilled professionals in both AI and IoT technologies is one of the main challenges facing the worldwide AIoT sector. Businesses capacity to successfully deploy and administer AIoT technologies is hampered by this skilled shortage. Significant difficulties are also presented by the intricacies of the industry value chain, including system integration, data security, and interoperability among various devices. Some organisations find it challenging to fully realise the potential benefits of AIoT due to these problems, which raise deployment costs and cause implementation delays.

Because of its robust technological infrastructure, which includes cutting-edge IT systems and high-performance computers, North America held a sizable market share. The expansion of sophisticated AIoT solutions is facilitated by significant investments in R&D as well as collaborations with academic institutions. Government initiatives supporting telemedicine and digital health solutions are supporting the rapid use of AIoT technology in the healthcare industry. Some of the key market players are Google LLC, IBM Corporation, Microsoft, Oracle, PTC, Salesforce, Inc, SAS Institute, Inc, and others.

For More Information, refer to below link: –

AIoT Market future

Related Reports:

B2C E-commerce Market Share, Growth, Scope, Challenges and Future Business Opportunities Till 2034

Software-Defined Data Center Market Size, Growth Factors, Trends, Analysis, Demand, and Future Prospects

Follow Us –

LinkedIn | Instagram | Facebook | Twitter

Contact Us:

Sara Lopes, Business Consultant — USA

SPER Market Research

+1–347–460–2899

0 notes

Text

Edge AI Meets Smart Sensors: Real-Time Data Processing Takes the Lead

The global smart sensors market is experiencing unprecedented growth, fueled by rapid digital transformation across industries, rising adoption of IoT-enabled devices, and the integration of artificial intelligence in sensor technologies. As industries shift toward automation, real-time monitoring, and data-driven operations, smart sensors have become the backbone of modern electronic ecosystems.

Unlock exclusive insights with our detailed sample report :

According to recent industry insights, the smart sensors market was valued at USD 45.63 billion in 2023 and is projected to reach USD 145.23 billion by 2031, growing at a CAGR of 15.6% during the forecast period. Key industries including automotive, healthcare, consumer electronics, aerospace, and manufacturing are witnessing a surge in demand for intelligent sensors capable of capturing and processing environmental data with minimal latency.

Market Drivers and Growth Opportunities

1. Proliferation of IoT Devices and Smart Infrastructure The explosion of IoT applications in smart homes, smart cities, and industrial IoT (IIoT) has driven the need for sensors that are not only accurate but also intelligent. These sensors support seamless data transmission and decision-making capabilities in connected ecosystems.

2. Automation and Industry 4.0 Transformation Industries are investing heavily in predictive maintenance, process automation, and robotics. Smart sensors such as temperature, pressure, proximity, and image sensors are at the core of these applications, enabling real-time monitoring and adaptive control in automated systems.

3. Rising Demand in Healthcare Smart sensors are revolutionizing healthcare through wearable technology, patient monitoring devices, and remote diagnostics. With the growing geriatric population and demand for personalized healthcare, sensor integration in medical devices is a key market driver.

4. Growing Popularity of Smart Consumer Electronics From smartphones and smartwatches to AR/VR devices and home appliances, the integration of multi-functional smart sensors is enhancing user experience and device interactivity, contributing to soaring market demand.

5. Environmental Monitoring and Sustainability Climate change and environmental regulations are encouraging governments and industries to adopt smart sensors for air quality, water purity, and pollution monitoring. These solutions are essential for meeting global sustainability goals.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

https://www.datamintelligence.com/customize/smart-sensors-market

Market Segmentation Overview

By Sensor Type: Includes pressure sensors, temperature sensors, image sensors, touch sensors, motion sensors, and gas sensors. Image and motion sensors are gaining traction in automotive and consumer electronics sectors.

By Technology: MEMS (Microelectromechanical Systems), CMOS (Complementary Metal-Oxide-Semiconductor), and optical sensing technologies dominate due to their efficiency, miniaturization, and compatibility with IoT platforms.

By End-Use Industry: Automotive, healthcare, industrial automation, consumer electronics, and aerospace & defense are key application areas. Among them, industrial and healthcare sectors are the fastest growing.

U.S. and Japan Market Insights

United States The U.S. remains a dominant force in smart sensor adoption, driven by strong demand across aerospace, automotive, defense, and healthcare industries. In early 2025, the U.S. Department of Energy announced a $1.2 billion fund for smart grid modernization, which includes significant investment in smart sensors for energy distribution and consumption tracking. Additionally, major tech firms such as Apple, Texas Instruments, and Honeywell are innovating sensor fusion technologies to enable smarter and more efficient devices.

Japan Japan, a global leader in robotics and automation, is rapidly advancing smart sensor deployment in its manufacturing and automotive sectors. With its focus on Smart Factories under “Society 5.0,” Japan is integrating AI-powered sensors into robotics, EVs, and public infrastructure. In March 2025, a leading Japanese electronics manufacturer launched a new line of miniaturized smart sensors for next-generation autonomous vehicles and wearable healthcare devices, underscoring Japan’s strong R&D capabilities.

Latest Trends and Innovations

AI-Embedded Smart Sensors: Integration of edge AI allows sensors to process data locally, improving response times and reducing the load on central systems. This is particularly useful in autonomous vehicles, predictive maintenance, and smart healthcare.

Sensor Fusion for Enhanced Accuracy: Combining multiple sensor inputs (e.g., gyroscope + accelerometer + magnetometer) provides more precise data. This trend is rising in consumer electronics and wearable fitness devices.

Advances in MEMS Technology: MEMS-based sensors are evolving rapidly, enabling lower power consumption and smaller form factors. These are ideal for implantable medical devices and compact electronics.

Energy Harvesting Sensors: To support sustainability, sensors that draw energy from ambient sources like light, heat, or motion are becoming more prominent, especially in remote monitoring and IoT applications.

Cybersecurity in Sensor Networks: As smart sensors become part of critical infrastructure, the importance of secure data transmission and sensor-level encryption is gaining attention, especially in military, healthcare, and smart grid applications.

Buy the exclusive full report here:

Competitive Landscape

The market is moderately consolidated with global players focusing on R&D, strategic collaborations, and geographic expansion to maintain competitiveness. Key players include:

Honeywell International Inc.

STMicroelectronics

Infineon Technologies AG

Robert Bosch GmbH

Texas Instruments Incorporated

TE Connectivity Ltd.

NXP Semiconductors

Analog Devices, Inc.

Siemens AG

Omron Corporation

These companies are pushing the boundaries in multi-sensor integration, AI-powered detection systems, and low-power sensor networks.

Future Outlook and Market Opportunities

1. Smart City Initiatives: Governments across the globe, particularly in the U.S. and Asia, are investing in smart infrastructure. Smart sensors will play a central role in traffic management, lighting, surveillance, and environmental monitoring.

2. Growth in Electric Vehicles (EVs): EVs require a wide array of sensors for battery management, motor control, and safety systems. As EV adoption surges globally, the demand for automotive-grade smart sensors will follow suit.

3. Space and Aerospace Applications: High-reliability smart sensors are being developed for satellites and space missions to monitor pressure, radiation, and temperature in extreme environments.

4. Expanding Use in Agriculture (AgriTech): Smart sensors are increasingly used in precision farming, monitoring soil moisture, crop health, and weather patterns to optimize resource use and productivity.

Stay informed with the latest industry insights-start your subscription now:

Conclusion

The global smart sensors market stands at the intersection of innovation, automation, and connectivity. With widespread applications across industries and increasing integration of AI and IoT, smart sensors are redefining how machines interact with their environments. The market’s rapid expansion—led by the U.S. and Japan—signals a transformative shift toward a more responsive, efficient, and intelligent future. As sensor technologies continue to evolve, businesses and governments alike must harness their full potential to stay ahead in the digital age.

About us:

At DataM Intelligence, we specialize in delivering end-to-end market research and consulting solutions designed to unlock your business potential. By harnessing proprietary insights, market trends, and breakthrough developments, we craft intelligent strategies that drive results.

With a repository of 6,300+ detailed reports across 40+ sectors, we’ve helped over 200 global businesses across 50+ nations achieve growth. From syndicated analysis to tailored research, our dynamic approach addresses the critical intelligence your business needs to thrive.

Contact US:

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: [email protected]

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

#Smart sensors market#Smart sensors market size#Smart sensors market growth#Smart sensors market share#Smart sensors market analysis

0 notes

Text

CPE Chip Market Analysis: CAGR of 12.1% Predicted Between 2025–2032

MARKET INSIGHTS

The global CPE Chip Market size was valued at US$ 1.58 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 12.1% during the forecast period 2025-2032. This growth trajectory aligns with the broader semiconductor industry expansion, which was valued at USD 579 billion in 2022 and is expected to reach USD 790 billion by 2029 at a 6% CAGR.

CPE (Customer Premises Equipment) chips are specialized semiconductor components that enable network connectivity in devices such as routers, modems, and gateways. These chips power critical functions including signal processing, data transmission, and protocol conversion for both 4G and 5G networks. The market comprises two primary segments – 4G chips maintaining legacy infrastructure support and 5G chips driving next-generation connectivity with higher bandwidth and lower latency.

Market expansion is being propelled by three key factors: the global rollout of 5G infrastructure, increasing demand for high-speed broadband solutions, and the proliferation of IoT devices requiring robust connectivity. However, supply chain constraints in the semiconductor industry and geopolitical factors affecting chip production present ongoing challenges. Major players like Qualcomm and MediaTek are investing heavily in R&D to develop advanced CPE chipsets, while emerging players such as UNISOC and ASR are gaining traction in cost-sensitive markets. The Asia-Pacific region dominates production and consumption, accounting for over 45% of global CPE chip demand in 2024.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Accelerates Demand for Advanced CPE Chips

The global transition to 5G networks continues to drive exponential growth in the CPE chip market. As telecom operators roll out next-generation infrastructure, the demand for high-performance customer premise equipment has surged by over 40% in the past two years. Modern 5G CPE devices require specialized chipsets capable of supporting multi-gigabit speeds, ultra-low latency, and massive device connectivity. Leading chip manufacturers are responding with integrated solutions that combine baseband processing, RF front-end modules, and AI acceleration. For instance, Qualcomm’s latest 5G CPE platforms deliver 10Gbps throughput while reducing power consumption by 30% compared to previous generations.

IoT Adoption Creates New Growth Avenues for CPE Chip Vendors

The proliferation of Internet of Things (IoT) applications across smart cities, industrial automation, and connected homes is generating significant opportunities for CPE chip manufacturers. With over 15 billion IoT devices projected to connect to networks by 2025, telecom operators require CPE solutions that can efficiently manage diverse traffic patterns and quality-of-service requirements. This has led to the development of specialized chipsets featuring advanced traffic management, edge computing capabilities, and enhanced security protocols. Recent product launches demonstrate this trend, with companies like MediaTek introducing chips optimized for IoT gateways that support simultaneous connections to hundreds of endpoints while maintaining reliable performance.

Remote Work Infrastructure Investments Fuel Market Expansion

The permanent shift toward hybrid work models continues to stimulate demand for enterprise-grade CPE solutions. Businesses worldwide are upgrading their network infrastructure to support distributed workforces, driving a 25% year-over-year increase in CPE deployments. This trend has particularly benefited manufacturers of chips designed for business routers and SD-WAN appliances, which require robust performance for VPNs, unified communications, and cloud applications. Leading semiconductor firms have responded with system-on-chip solutions integrating Wi-Fi 6/6E, multi-core processors, and hardware-accelerated encryption to meet these evolving requirements.

MARKET RESTRAINTS

Supply Chain Disruptions Continue to Challenge Production Stability

Despite strong demand, the CPE chip market faces persistent supply chain constraints that limit growth potential. The semiconductor industry’s reliance on advanced fabrication nodes has created bottlenecks, with lead times for certain components extending beyond 12 months. These challenges are compounded by geopolitical tensions affecting rare earth material supplies and export controls on specialized manufacturing equipment. While the situation has improved from pandemic-era shortages, inventory levels remain below historical averages, forcing many CPE manufacturers to implement allocation strategies and redesign products with available components.

Rising Component Costs Squeeze Profit Margins

Escalating production expenses present another significant restraint for CPE chip suppliers. The transition to more advanced process nodes has increased wafer costs by approximately 20-30% across the industry. Additionally, testing and packaging expenses have risen due to higher energy prices and labor costs. These factors have compressed gross margins, particularly for mid-range CPE chips where pricing pressure is most intense. Manufacturers are responding by optimizing chip architectures, consolidating IP blocks, and investing in yield improvement initiatives, but these measures require significant R&D expenditures that may take years to yield returns.

Regulatory Complexity Slows Time-to-Market

The CPE chip industry faces growing regulatory scrutiny that delays product launches and increases compliance costs. New spectrum regulations, cybersecurity requirements, and equipment certification processes have extended development cycles by 3-6 months on average. In particular, the automotive and industrial sectors now demand comprehensive safety certifications that require extensive testing and documentation. These regulatory hurdles disproportionately affect smaller chip vendors who lack dedicated compliance teams, potentially limiting innovation and competition in certain market segments.

MARKET CHALLENGES

Technology Complexity Increases Design and Validation Costs

Modern CPE chips incorporate increasingly sophisticated architectures that pose significant engineering challenges. Designs now routinely integrate multiple processor cores, AI accelerators, and specialized radio interfaces, requiring advanced simulation tools and verification methodologies. The associated R&D costs have grown exponentially, with some 5G chip development projects now exceeding $100 million in budget. This creates a high barrier to entry for potential competitors and forces established players to carefully prioritize their product roadmaps. Furthermore, the complexity makes post-silicon validation more difficult, potentially leading to costly respins if critical issues emerge late in the development cycle.

Talent Shortage Constrains Innovation Capacity

The semiconductor industry’s rapid expansion has created intense competition for skilled engineers, particularly in critical areas like RF design, digital signal processing, and physical implementation. CPE chip manufacturers report vacancy rates exceeding 30% for certain technical positions, with hiring cycles stretching to 9-12 months for specialized roles. This talent crunch limits companies’ ability to execute aggressive product roadmaps and forces difficult tradeoffs between projects. While firms are investing in training programs and academic partnerships, the pipeline for experienced chip designers remains insufficient to meet current demand.

Standardization Gaps Create Integration Headaches

The evolving nature of 5G and edge computing technologies has led to fragmented standards across different markets and regions. CPE chip vendors must support multiple protocol variants, frequency bands, and security frameworks, complicating both hardware and software development. This fragmentation increases testing overhead and makes it difficult to achieve economies of scale across product lines. While industry groups continue working toward greater harmonization, interim solutions often require additional engineering resources to implement customized features for specific customers or geographies.

CPE CHIP MARKET TRENDS

5G Network Expansion Accelerates Demand for Advanced CPE Chips

The rapid global deployment of 5G networks is significantly driving the CPE (Customer Premises Equipment) chip market, with the segment projected to grow at over 30% CAGR through 2032. Telecom operators worldwide invested nearly $280 billion in 5G infrastructure in 2023 alone, creating substantial demand for compatible CPE devices. Chip manufacturers are responding with innovative solutions featuring multi-band support and improved power efficiency, with next-generation modem-RF combos now achieving throughputs exceeding 7Gbps. While 4G CPE chips still dominate current installations, representing about 65% of 2024 shipments, 5G solutions are rapidly gaining share due to superior performance in high-density urban environments.

Other Trends

Smart Home Integration

The proliferation of IoT devices in residential settings, expected to reach 29 billion connected units globally by 2027, is creating new requirements for CPE chips that can handle simultaneous broadband and IoT traffic management. Modern gateway solutions now incorporate AI-powered traffic prioritization and mesh networking capabilities to maintain quality of service across dozens of connected devices. Semiconductor vendors have responded with system-on-chip (SoC) designs integrating Wi-Fi 6/6E, Bluetooth, and Zigbee radios alongside traditional cellular modems. North America leads this adoption curve, with over 75% of new home internet subscriptions in 2023 opting for smart gateway solutions compared to just 32% in 2020.

Edge Computing and Network Virtualization Impact Chip Designs

Emerging virtualization technologies are reshaping CPE architectures, creating demand for chips with enhanced processing capabilities beyond traditional modem functions. Virtual CPE (vCPE) solutions now account for 18% of business installations, requiring chipsets that can efficiently run containerized network functions (CNFs) while maintaining low power envelopes. The enterprise segment has proven particularly receptive, with large-scale adoption in multi-tenant office buildings and smart city applications. Meanwhile, silicon designed for edge computing applications is increasingly incorporating hardware acceleration blocks for AI inference, allowing real-time processing of video analytics and other bandwidth-intensive applications at the network periphery. This evolution has prompted traditional chip vendors to expand their portfolios through strategic acquisitions in the FPGA and specialty processor spaces.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Partnerships Fuel Growth in the CPE Chip Market

The global CPE (Customer Premises Equipment) chip market remains highly competitive, characterized by technological innovation and aggressive expansion strategies. Qualcomm dominates the market with its extensive portfolio of 4G and 5G chipsets, capturing approximately 35% revenue share in 2024. The company’s leadership stems from its strong foothold in North America and strategic partnerships with telecom operators.

MediaTek and Intel follow closely, collectively accounting for 28% market share, owing to their cost-effective solutions for emerging markets and industrial applications. These players continue investing heavily in R&D, particularly for energy-efficient 5G chips catering to IoT deployments and smart city infrastructure.

Chinese manufacturers like Hisilicon and UNISOC are rapidly gaining traction through government-supported initiatives and localized supply chains. Their aggressive pricing strategies and custom solutions for Asian markets have enabled 18% year-over-year growth in 2024, challenging established western players.

Meanwhile, specialized firms such as Eigencomm and Sequans are carving niche positions through innovative chip architectures optimized for low-power wide-area networks (LPWAN) and private 5G deployments. Their collaborations with network equipment providers have become crucial differentiators in this evolving landscape.

List of Key CPE Chip Manufacturers Profiled

Qualcomm Technologies, Inc. (U.S.)

UNISOC (Shanghai) Technologies Co., Ltd. (China)

ASR Microelectronics Co., Ltd. (China)

HiSilicon (Huawei Technologies Co., Ltd.) (China)

XINYI Semiconductor (China)

MediaTek Inc. (Taiwan)

Intel Corporation (U.S.)

Eigencomm (China)

Sequans Communications S.A. (France)

Segment Analysis:

By Type

5G Chip Segment Dominates the Market Due to its High-Speed Connectivity and Low Latency

The CPE Chip market is segmented based on type into:

4G Chip

5G Chip

By Application

5G CPE Segment Leads Due to Escalated Demand for High-Performance Wireless Broadband

The market is segmented based on application into:

4G CPE

5G CPE

By End User

Telecom Operators Segment Dominates with Growing Infrastructure Investments

The market is segmented based on end user into:

Telecom Operators

Enterprises

Residential Users

Regional Analysis: CPE Chip Market

North America The mature telecommunications infrastructure and rapid 5G deployments in the U.S. and Canada are fueling demand for high-performance 5G CPE chips, particularly from vendors like Qualcomm and Intel. With major carriers investing over $275 billion in network upgrades, chip manufacturers are prioritizing low-latency, power-efficient designs. However, stringent regulatory scrutiny on semiconductor imports creates supply chain challenges. The region also leads in IoT adoption, driving demand for hybrid 4G/5G chips in smart city solutions and enterprise applications. Local chip designers benefit from strong R&D ecosystems but face growing competition from Asian suppliers.

Europe EU initiatives like the 2030 Digital Compass (targeting gigabit connectivity for all households) are accelerating CPE chip demand, though adoption varies across nations. Germany and the U.K. lead in 5G CPE deployments using chips from MediaTek and Sequans, while Eastern Europe still relies heavily on cost-effective 4G solutions. Strict data privacy laws and emphasis on open RAN architectures are reshaping chip design requirements. The region faces headwinds from component shortages but maintains steady growth through government-industry partnerships in semiconductor sovereignty programs.

Asia-Pacific Accounting for over 60% of global CPE chip consumption, the region is driven by China’s massive “5G+” infrastructure push and India’s expanding broadband networks. Local giants HiSilicon and UNISOC dominate low-to-mid range segments, while South Korean/Japanese firms focus on premium chips. Southeast Asian markets show explosive growth (20%+ CAGR) due to rural connectivity projects. However, geopolitical tensions and import restrictions create supply volatility. Price sensitivity remains high, favoring integrated 4G/5G combo chips over standalone 5G solutions in emerging economies.

South America Limited 5G spectrum availability keeps the market reliant on 4G LTE chips, though Brazil and Chile are early adopters of 5G CPEs using ASR and MediaTek solutions. Economic instability and currency fluctuations hinder large-scale infrastructure investments, causing operators to prioritize cost-effective Chinese chip suppliers. The lack of local semiconductor manufacturing creates import dependency, but recent trade agreements aim to improve component accessibility. Enterprise demand for industrial IoT routers presents niche opportunities for mid-tier chip vendors.

Middle East & Africa Gulf nations (UAE, Saudi Arabia) drive premium 5G CPE adoption through smart city projects, leveraging Qualcomm and Eigencomm chips. Sub-Saharan Africa depends on affordable 4G solutions from Chinese vendors, with mobile network operators deploying low-power chips for extended coverage. While underdeveloped fiber backhaul limits 5G potential, satellite-CPE hybrid chips are gaining traction in remote areas. Political instability in some markets disrupts supply chains, though rising digitalization funds (like Saudi’s $6.4bn ICT strategy) indicate long-term growth potential.

Report Scope

This market research report provides a comprehensive analysis of the global and regional CPE Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global CPE Chip market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (4G Chip, 5G Chip), application (4G CPE, 5G CPE), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates the market due to rapid 5G adoption.

Competitive Landscape: Profiles of leading market participants including Qualcomm, UNISOC, ASR, Hisilicon, and MediaTek, including their product offerings, R&D focus, and recent developments.

Technology Trends & Innovation: Assessment of emerging technologies in semiconductor design, fabrication techniques, and evolving industry standards for CPE devices.

Market Drivers & Restraints: Evaluation of factors driving market growth such as 5G rollout and IoT expansion, along with challenges including supply chain constraints and regulatory issues.

Stakeholder Analysis: Insights for chip manufacturers, network equipment providers, telecom operators, investors, and policymakers regarding the evolving ecosystem.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/fieldbus-distributors-market-size-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/consumer-electronics-printed-circuit.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-alloy-current-sensing-resistor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/modular-hall-effect-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/integrated-optic-chip-for-gyroscope.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/industrial-pulsed-fiber-laser-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/unipolar-transistor-market-strategic.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/zener-barrier-market-industry-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/led-shunt-surge-protection-device.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/type-tested-assembly-tta-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/traffic-automatic-identification.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/one-time-fuse-market-how-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/pbga-substrate-market-size-share-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nfc-tag-chip-market-growth-potential-of.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silver-nanosheets-market-objectives-and.html

0 notes

Text

Cardiac Monitoring Devices Market Forecast to Reach $48.6B by 2032

The Cardiac Monitoring Devices Market is undergoing robust expansion. In 2021, it was valued at approximately USD 7.7 billion and is projected to grow at a steady compound annual growth rate (CAGR) of around 5.9% through 2031. Other forecasts suggest the market may grow from USD 29.1 billion in 2023 to USD 48.6 billion by 2032. This growth is being driven by the rising global burden of cardiovascular diseases, aging demographics, and technological advancements in wearable and implantable cardiac monitoring solutions.

To Get Free Sample Report :https://www.datamintelligence.com/download-sample/cardiac-monitoring-devices-market

Key Market Drivers

1. Rising Cardiovascular Disease Prevalence Cardiovascular diseases (CVDs) remain the leading cause of death worldwide. In many developed nations, including the United States and Japan, heart disease continues to account for a substantial share of healthcare costs and mortality rates. The demand for continuous, non-invasive monitoring technologies that can detect heart abnormalities early is rising dramatically.

2. Home-Based and Remote Monitoring Demand The shift from hospital-based care to home-based healthcare is driving demand for wearable ECG monitors, implantable loop recorders, and mobile telemetry systems. Remote cardiac monitoring reduces hospital readmissions and enables long-term management of chronic cardiac conditions in the comfort of a patient’s home.

3. Integration of Artificial Intelligence and Connectivity Artificial intelligence (AI), edge computing, and machine learning technologies are revolutionizing how cardiac data is collected and interpreted. Advanced algorithms can now analyze real-time ECG data, predict arrhythmias, and alert both patients and clinicians through mobile apps and cloud-based platforms. Smart wearables and patch-based monitors are becoming integral to daily heart monitoring.

4. Aging Population and Chronic Disease Management Globally, the number of people aged 65 and older is increasing significantly. This group is more likely to experience conditions like arrhythmia, heart failure, and hypertension. Cardiac monitoring devices are essential for proactive heart health management in older adults, supporting early diagnosis and improved clinical outcomes.

U.S. and Japan at the Forefront of Innovation

United States The U.S. dominates the global cardiac monitoring devices market in terms of market share, with strong support from healthcare infrastructure, reimbursement policies, and innovation ecosystems. Leading medical technology companies have developed FDA-cleared wearable ECG monitors and implantable recorders, allowing for real-time heart data transmission and automated analysis.

Smartphone-integrated cardiac monitors and remote telemetry systems are seeing broad adoption across U.S. healthcare networks. The growing use of wearables in both clinical and consumer health is fueling continued product development, especially as hospitals adopt AI-powered decision-support tools.

Japan Japan, with one of the world’s oldest populations, has emerged as a leader in cardiac monitoring innovation. The country is witnessing rapid growth in demand for mobile telemetry and patch-based cardiac monitors. Japan’s healthcare system has embraced digital health tools, particularly for its aging citizens, enabling proactive care and reducing strain on hospitals.

Several Japanese technology companies are developing advanced algorithms for real-time arrhythmia detection and patient risk stratification. The integration of wearable tech into traditional cardiology is helping Japan bridge the gap between innovation and healthcare delivery.

Product and Technology Trends

1. Wearable Devices Wearable cardiac monitoring devices, such as wristbands, smartwatches, and adhesive patches, are increasingly used for detecting heart rhythm irregularities like atrial fibrillation. These devices offer non-invasive, continuous monitoring and are widely adopted in outpatient settings.

2. Implantable Loop Recorders Implantable cardiac monitors allow for long-term tracking of irregular heartbeats and unexplained fainting. These devices are valuable for patients at risk of stroke or suffering from infrequent arrhythmias.

3. ECG Monitoring Systems Resting ECG machines, stress ECGs, and Holter monitors remain standard tools in hospitals and diagnostic labs. However, they are being complemented by mobile and portable versions that can transmit data remotely.

4. AI-Enhanced Diagnostics AI-powered diagnostic platforms are now capable of analyzing millions of cardiac signals in seconds. These technologies improve the detection of arrhythmias and can reduce the workload on cardiologists by offering real-time alerts and clinical insights.

Get the Demo Full Report: https://www.datamintelligence.com/enquiry/cardiac-monitoring-devices-market

Growth Opportunities

1. Expansion of AI and Predictive Analytics The use of predictive algorithms to detect cardiac events before they occur offers significant potential. Advanced ECG platforms can now identify subtle abnormalities that were previously difficult to detect.

2. Miniaturization and Edge Computing The miniaturization of sensors and the development of low-power edge computing allow cardiac devices to deliver instant, offline diagnostics especially important in home settings or remote regions.

3. Chronic Disease Management Programs Integrating cardiac monitoring into broader chronic care platforms offers long-term engagement for patients with hypertension, diabetes, or previous cardiac incidents. These systems reduce emergency visits and improve quality of life.

4. Emerging Markets and Telehealth Integration As global healthcare moves toward digital integration, emerging markets in Asia-Pacific and Latin America are adopting mobile cardiac monitors. Japan’s innovation in combining wearables with teleconsultation services could serve as a blueprint for others.

Challenges to Overcome

High Device Costs While prices are declining, many advanced wearable and implantable cardiac monitors remain expensive. Cost remains a barrier in low- and middle-income countries.

Regulatory Approvals Gaining approval for AI-based or implantable devices across multiple markets can be time-consuming due to varying regulatory frameworks.

Data Privacy and Cybersecurity Real-time data transmission raises concerns around privacy. Ensuring compliance with healthcare data regulations is critical for mass adoption.

Lack of Standardization The cardiac monitoring ecosystem includes many devices from different vendors, leading to interoperability issues and integration challenges within hospital systems.

Conclusion

The cardiac monitoring devices market is entering a new era one shaped by intelligent diagnostics, wearable convenience, and the growing need for remote cardiac care. With rising cardiovascular disease cases, technological innovation, and strong momentum in the U.S. and Japan, the industry is well-positioned for sustained global growth.

Manufacturers that invest in AI integration, miniaturization, cloud-based platforms, and consumer-friendly design will be at the forefront of transforming how heart health is managed in the years ahead. As patients demand more autonomy and clinicians seek better data, the cardiac monitoring market will continue to thrive as a pillar of modern digital healthcare.

#Cardiac Monitoring Devices Market#Cardiac Monitoring Devices Market share#Cardiac Monitoring Devices Market size

0 notes

Text

Smart Smoke Detectors Market Trends: Growth Potential and Challenges

United States of America – June 19, 2025 – The Insight Partners is proud to release its thorough research, "Smart Smoke Detectors Market: An In-depth Analysis," which reveals the way smarter technologies are transforming fire safety norms around the world.

Overview of Smart Smoke Detectors Market Spurred by smart home take-up and increasingly stringent safety codes, the smart smoke detectors market is transforming with IoT, AI, and cloud integration. Consumers and commercial organizations both are gravitating toward automated and networked safety systems.

Key Findings and Insights

Market Size and Growth • Historical Data: Trends in adoption reflect strong growth, especially in urbanized and technology-embracing areas. • Major drivers: Growing cases of home and industrial fires, smart home expansion, and growing insurance incentives.

Market Segmentation • By Type (Photoelectric, Ionization, Dual Sensor) • By Connectivity (Wi-Fi, Zigbee, Bluetooth, Z-Wave) • By End Use (Residential, Commercial, Industrial) • By Region (North America, Europe, Asia-Pacific, Middle East & Africa, South America)

Identifying Emerging Trends • Technology Advancements: Integration with home assistants, remote monitoring, battery health notifications. • Shifting Consumer Preferences: Demand for multi-functional devices with CO detection and smartphone app support. • Regulatory Shifts: Regulations mandating networked and smart alarms for residential spaces.

Opportunities for Growth Market expansion into emerging regions, association with home automation vendors, and retrofitting plans in public buildings point the way towards growth opportunities.

Conclusion The Smart Smoke Detectors Market report allows stakeholders to tap into the transformative potential of networked technologies in safety, giving vital insight into opportunities and strategic mandates.

About The Insight Partners The Insight Partners is a leading provider of syndicated research, customized research, and consulting services. Our reports combine quantitative forecasting and trend analysis to offer forward-looking insights for decision-makers. With a client-first approach, we deliver actionable intelligence and strategic guidance across various industries

Visit our website- https://www.theinsightpartners.com/ to learn more and access our comprehensive market reports.

Get Sample Report- https://www.theinsightpartners.com/sample/TIPRE00017175

0 notes

Text

Real Estate Trends in Gurgaon: 2025 Forecast

Gurgaon has always been a hotspot for real estate investments, and as we step into 2025, the market is buzzing with exciting opportunities. Whether you're looking to buy a luxury apartment, invest in a commercial space, or secure an SCO plot, Gurgaon continues to offer high growth potential.

In this article, we’ll break down the top real estate trends in Gurgaon for 2025—what’s hot, what’s changing, and where the best investment opportunities lie. Plus, if you need expert advice on residential, commercial, or SCO plots in Gurgaon, Laveek Estates is here to guide you every step of the way.

Why Gurgaon Remains a Real Estate Powerhouse in 2025?

Before diving into trends, let’s understand why Gurgaon is still a top choice for investors:

✅ Infrastructure Boom – Projects like Dwarka Expressway, Metro expansion, and new flyovers are improving connectivity. ✅ Corporate Hub – Companies like Google, Microsoft, and startups are expanding offices here. ✅ Luxury Living Demand – High-net-worth individuals (HNIs) are driving demand for premium apartments and villas. ✅ Commercial Growth – Retail spaces, co-working hubs, and SCO plots are seeing record-high demand.

If you’re planning to invest, now is the time to explore Gurgaon’s best properties before prices climb higher.

Top 5 Real Estate Trends in Gurgaon for 2025

1. Rise of Affordable & Mid-Segment Housing

While luxury projects dominate headlines, affordable and mid-range housing is gaining traction. With more professionals migrating to Gurgaon, builders are focusing on:

Compact 2-3 BHK apartments in sectors like Sohna, New Gurgaon, and Dwarka Expressway.

Flexible payment plans to attract first-time buyers.

Ready-to-move-in options to avoid construction delays.

If you’re looking for a budget-friendly home in Gurgaon, Laveek Estates can help you find the best deals.

2. SCO Plots – The Next Big Commercial Investment

Shop-Cum-Office (SCO) plots are becoming a favorite among entrepreneurs and investors. Why?

Lower risk compared to high-rise commercial spaces.

Flexibility to run a business or rent it out.

High appreciation in areas like Golf Course Extension, Sohna Road, and SPR.

Want to explore SCO plots in Gurgaon? Check out our exclusive listings today!

3. Co-Living & Co-Working Spaces on the Rise

With startups and freelancers growing, shared spaces are in demand. Trends include:

Co-living hubs near corporate offices (Cyber City, Udyog Vihar).

Co-working spaces with premium amenities.

Hybrid workspaces for small businesses.

4. Green & Sustainable Housing

Homebuyers are now prioritizing eco-friendly features like:

Solar-powered homes.

Rainwater harvesting systems.

Vertical gardens & energy-efficient designs.

Builders are adapting quickly, making sustainability a key selling point in 2025.

5. Luxury Real Estate Continues to Thrive

Gurgaon’s luxury market isn’t slowing down. High-end buyers are looking for:

Penthouses & villas in DLF Phase 5, Golf Course Road.

Smart homes with AI-based security & automation.

Gated communities with private clubs, spas, and concierge services.

If luxury living is your goal, Laveek Estates offers the finest properties in premium locations.

Best Areas to Invest in Gurgaon (2025)

1. Dwarka Expressway

Why? Direct connectivity to Delhi & IGI Airport.

What’s Hot? Affordable housing, SCO plots, malls.

2. Golf Course Extension Road

Why? Premium residential & commercial projects.

What’s Hot? Luxury apartments, corporate hubs.

3. Sohna Road

Why? Rapid infrastructure development.

What’s Hot? Mid-range housing, retail spaces.

4. New Gurgaon (Sectors 76-80)

Why? Budget-friendly options with good amenities.

What’s Hot? Ready-to-move-in flats.

5. Cyber City & Udyog Vihar

Why? Best for commercial & office spaces.

What’s Hot? Co-working hubs, startup offices.

Need help choosing the best location for investment? Laveek Estates provides expert insights!

Should You Invest in Gurgaon Real Estate in 2025?

Yes! Here’s why: ✔ Prices are rising but still reasonable in emerging sectors. ✔ Rental yields are strong (5-8% for residential, 8-12% for commercial). ✔ Infrastructure upgrades will boost property values. ✔ High demand ensures liquidity.

However, always:

Research builders & legal clearances.

Compare locations based on your budget.

Consult a trusted real estate advisor like Laveek Estates.

#RealEstateGurgaon#GurgaonProperty#InvestInGurgaon#SCOPlots#CommercialRealEstate#ResidentialProperty#LaveekEstates#GurgaonTrends2025#PropertyInvestment#DwarkaExpressway

0 notes

Text

Hair Restoration Market: A Global Overview of Trends and Forecasts

The Hair Restoration Market has evolved into one of the most dynamic segments in the broader cosmetic and dermatological industry. Rising concerns about hair loss, influenced by genetics, stress, pollution, and hormonal imbalances, have led to increased demand for both surgical and non-surgical hair restoration procedures globally. This market is not only growing but also diversifying, with new technologies and treatment modalities reshaping how patients approach hair loss.

Current Market Landscape

As of recent years, the Hair Restoration Market is valued at several billion USD and is projected to grow at a steady compound annual growth rate (CAGR) through 2030. North America, followed by Europe and Asia-Pacific, dominates the market due to higher disposable incomes, increased awareness of aesthetic procedures, and the presence of advanced healthcare infrastructure.

Key players in the market include names like Bosley, Hair Club, Bernstein Medical, and several regional clinics that offer highly specialized services. Emerging markets such as India, China, Brazil, and the Middle East are witnessing rapid growth due to rising medical tourism and a growing middle-class population seeking affordable treatment.

Major Trends Driving the Market

Technological Innovations: Techniques such as Follicular Unit Extraction (FUE) and Direct Hair Implantation (DHI) are gaining traction due to their minimally invasive nature and faster recovery times. Automation and robotics are also being introduced to improve precision and efficiency.

Rising Male Grooming Awareness: There is a noticeable shift in cultural attitudes around male grooming and aesthetics. Hair restoration is increasingly seen as a valid form of self-care, particularly among men aged 25–45.

Increased Adoption of Non-Surgical Solutions: Non-invasive treatments such as Platelet-Rich Plasma (PRP), low-level laser therapy (LLLT), and stem cell-based procedures are capturing attention due to their low risk and affordable price points.

Growth of At-Home Products: Consumers are also investing in advanced at-home kits, including FDA-approved laser caps, topical minoxidil solutions, and natural serums that promise hair regrowth.

Celebrity and Influencer Endorsements: Social media influencers and public figures openly endorsing hair restoration procedures have helped reduce stigma and normalized such treatments, expanding the consumer base.

Key Forecasts and Opportunities

By 2030, the Hair Restoration Market is expected to surpass its current valuation significantly, with increased adoption across emerging economies. Technological integration, especially in robotic hair transplant systems, will contribute to better outcomes and higher patient satisfaction.

Stem cell therapy and regenerative medicine hold immense promise as future growth areas. These treatments aim to activate dormant hair follicles and promote natural regrowth without surgical intervention. Their progress through clinical trials will be closely watched in the coming years.

Another area of opportunity is the integration of Artificial Intelligence (AI) and machine learning in personalized treatment planning. AI can help analyze scalp conditions, predict outcomes, and recommend tailored solutions, thereby increasing treatment effectiveness.

Regional Insights

North America: The U.S. leads the region with the highest number of surgical and non-surgical procedures. A highly competitive market, patients in this region demand cutting-edge solutions with minimal downtime.

Europe: Germany, the UK, and France are key markets with growing interest in aesthetic medicine. Medical tourism from neighboring countries also boosts demand.

Asia-Pacific: Countries like India, South Korea, and Japan are gaining global attention due to high-quality, cost-effective hair transplant procedures. Cultural acceptance and a booming beauty industry also support this growth.

Middle East & Africa: Increasing investment in medical infrastructure and a shift in beauty standards are driving demand in Gulf countries.

Challenges to Address

Despite optimistic projections, challenges remain. High procedure costs, limited insurance coverage, and lack of standardized protocols across clinics are significant barriers. Moreover, accessibility in rural or tier-2 cities is still minimal, despite rising interest.

Patient education remains crucial. Many still harbor unrealistic expectations or fear side effects, highlighting the need for better consultation and transparency from providers.

Conclusion

The Hair Restoration Market is positioned for robust growth, fueled by technological progress, shifting societal norms, and increasing consumer interest in aesthetics and wellness. With expanding treatment options and more clinics entering the space, the competition will intensify. Providers must focus on innovation, affordability, and customer-centric care to stay relevant in this ever-evolving market.

0 notes

Text

Gas Sensors Market Industry, Trends, Share by 2025-2033 | Reports and Insights

The Reports and Insights, a leading market research company, has recently releases report titled “Gas Sensors Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033.” The study provides a detailed analysis of the industry, including the global Gas Sensors Market Research share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Gas Sensors Market?

The global gas sensors market was valued at US$ 3.1 Billion in 2024 and is expected to register a CAGR of 8.9% over the forecast period and reach US$ 6.7 Billion in 2033.

What are Gas Sensors?

Gas sensors are instruments used to detect and measure the levels of specific gases in the environment. They function by detecting changes in electrical, optical, or chemical properties triggered by the presence of target gases like carbon monoxide, methane, or oxygen. These sensors are essential in various applications, including industrial safety, environmental monitoring, automotive systems, and consumer electronics. By delivering real-time information on gas concentrations, gas sensors are critical for maintaining safety, meeting regulatory standards, and improving operational efficiency across different fields.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2392

What are the growth prospects and trends in the Gas Sensors industry?

The gas sensors market growth is driven by various factors and trends. The gas sensors market is growing significantly due to rising needs for safety and environmental monitoring across various sectors. This growth is driven by increased industrial activity, stricter environmental regulations, and advancements in sensor technology. Key applications include industrial safety, air quality monitoring, automotive systems, and smart homes, where gas sensors play a crucial role in providing real-time data. Major market players are focusing on developing advanced sensors with improved sensitivity and accuracy. Despite challenges such as high costs and the necessity for ongoing technological updates, the market is expanding due to continuous innovation and the broader adoption of gas sensors across multiple industries. Hence, all these factors contribute to gas sensors market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Product

Oxygen (O2)/Lambda Sensors

Carbon Dioxide (CO2) Sensors

Carbon Monoxide (CO) Sensors

Nitrogen Oxide (NOx) Sensors

Methyl Mercaptan Sensor

Others (Hydrogen, Ammonia, and Hydrogen Sulfide)

By Type

Wireless

Wired

By Technology

Electrochemical

Semiconductor

Solid State/MOS

Photo-ionization Detector (PID)

Catalytic

Infrared (IR)

Others

By End-Use

Medical

Building Automation & Domestic Appliances

Environmental

Petrochemical

Automotive

Industrial

Agriculture

Others

North America

United States

Canada

Europe

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

Benelux

Nordic

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East & Africa

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

ABB Ltd.

AlphaSense Inc.

City Technology Ltd.

Dynament

FLIR Systems, Inc.

Figaro Engineering Inc.

GfG Gas Detection UK Ltd.

Membrapor

Nemoto & Co. Ltd.

Robert Bosch LLC

Siemens

Among Others

View Full Report: https://www.reportsandinsights.com/report/Gas Sensors-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

Rising Demand for Safer Spaces: A Strategic Analysis of the Global Smoke Detector Market (2022–2030)

Smoke Detector Market Overview

The global smoke detector market has witnessed consistent growth over the past decade, driven by increasing awareness of fire safety, stringent building safety regulations, and technological advancements. The rise in urban infrastructure, smart home adoption, and industrial safety mandates are key factors propelling market expansion.

The global smoke detector market was valued at USD 1.1 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 7.30% from 2022 to 2030, reaching approximately USD 1.9 billion by the end of the forecast period.

Market Dynamics

Drivers

Increasing Fire Safety Regulations: Governments and regulatory bodies worldwide are implementing stricter fire codes in commercial and residential buildings.

Smart Home Integration: Integration of IoT in fire safety systems has spurred the demand for smart smoke detectors.

Growing Awareness: Public awareness campaigns about fire hazards and preventive systems are boosting adoption in emerging economies.

Restraints

High Installation Costs: Advanced and interconnected systems can be costly, especially for small businesses or older infrastructure retrofits.

False Alarms & Maintenance Issues: Traditional detectors can trigger false alarms, leading to user dissatisfaction and additional maintenance needs.

Opportunities

AI-Powered Detection Systems: Use of AI and machine learning in detection mechanisms can enhance accuracy and response time.

Expansion in Emerging Markets: Untapped markets in Asia, Africa, and Latin America present lucrative opportunities due to rising construction activity.

Regional Analysis

North America

Dominates the market due to early adoption of smart technologies and stringent building codes, especially in the U.S. and Canada.

Europe

Holds a significant share, with strong fire safety legislation across the UK, Germany, France, and Nordic countries.

Asia-Pacific

Expected to witness the fastest growth rate. Urbanization, smart city projects, and expanding real estate in China, India, and Southeast Asia drive demand.

Latin America and Middle East & Africa

Gradual growth driven by infrastructure development and increasing awareness of fire safety regulations.

Segmental Analysis

By Product Type

Ionization Smoke Detectors

Photoelectric Smoke Detectors

Dual Sensor Smoke Detectors

Photoelectric detectors dominate due to better performance in detecting smoldering fires.

By Power Source

Battery-Powered

Hardwired with Battery Backup

Hardwired Only

Battery-powered detectors lead due to ease of installation and flexibility.

By End User

Residential

Commercial

Industrial

The residential segment holds the largest share, driven by consumer safety awareness and home insurance incentives.

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/13143

List of Key Players

Honeywell International Inc.

Johnson Controls

Siemens AG

Schneider Electric

Hochiki Corporation

Robert Bosch GmbH

BRK Brands Inc. (Newell Brands)

Nest Labs (Google LLC)

Halma plc

United Technologies Corporation

Key Trends

Shift towards smart, connected detectors with mobile alerts and remote control.

Integration with home automation systems and voice assistants like Alexa and Google Assistant.

Rising investment in AI-enhanced fire detection solutions.

Emergence of eco-friendly and low-power detection technologies.

Conclusion

The smoke detector market is poised for robust growth, fueled by regulatory backing, technological innovation, and increasing demand for residential and industrial safety. As smart city initiatives and building modernization accelerate, so will the opportunities in this critical life-saving sector.

For Further Information:

Market Introduction

Market Dynamics

Segment Analysis

Some of the Key Market Players

0 notes

Text

Solar Panel Cleaning Market

Solar Panel Cleaning Market size is valued at $690 Million in 2022 and is expected to reach a value of $1.8 billion by 2030 at a CAGR of 13% during the forecast period 2023–2030.

🔗 𝐆𝐞𝐭 𝐑𝐎𝐈-𝐟𝐨𝐜𝐮𝐬𝐞𝐝 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐟𝐨𝐫 𝟐𝟎𝟐𝟓-𝟐𝟎𝟑𝟏 → 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐍𝐨𝐰

Solar panel cleaning is essential to maintain the efficiency and longevity of solar energy systems. Over time, dust, dirt, bird droppings, and pollution accumulate on panels, blocking sunlight and reducing power output. Regular cleaning ensures panels absorb maximum sunlight, improving energy production and saving money on electricity bills. Professional cleaning uses gentle, eco-friendly methods to avoid damaging the panels while removing grime effectively. Clean panels not only boost performance but also extend the system’s lifespan.

1️⃣𝐒𝐮𝐫𝐠𝐞 𝐢𝐧 𝐒𝐨𝐥𝐚𝐫 𝐈𝐧𝐬𝐭𝐚𝐥𝐥𝐚𝐭𝐢𝐨𝐧𝐬: The global shift towards renewable energy has led to an increase in solar panel installations. To maintain optimal performance and energy output, regular cleaning is essential, thereby boosting demand for cleaning services.

2️⃣𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐜𝐚𝐥 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬: Innovations such as automated cleaning systems, robotic cleaners, and AI-driven solutions have enhanced cleaning efficiency and reduced labor costs. These technologies also promote water conservation and minimize environmental impact.

3️⃣𝐆𝐨𝐯𝐞𝐫𝐧𝐦𝐞𝐧𝐭 𝐈𝐧𝐜𝐞𝐧𝐭𝐢𝐯𝐞𝐬 𝐚𝐧𝐝 𝐏𝐨𝐥𝐢𝐜𝐢𝐞𝐬: Subsidies and tax incentives for solar installations have lowered initial costs, leading to increased adoption. Additionally, some policies mandate regular maintenance, including cleaning, to ensure the effectiveness of solar panels.

4️⃣𝐄𝐧𝐯𝐢𝐫𝐨𝐧𝐦𝐞𝐧𝐭𝐚𝐥 𝐀𝐰𝐚𝐫𝐞𝐧𝐞𝐬𝐬: As consumers become more environmentally conscious, there’s a growing preference for sustainable cleaning methods, such as waterless or eco-friendly solutions, which further drives market growth.

5️⃣𝐑𝐢𝐬𝐢𝐧𝐠 𝐄𝐥𝐞𝐜𝐭𝐫𝐢𝐜𝐢𝐭𝐲 𝐃𝐞𝐦𝐚𝐧𝐝: The increasing need for electricity, especially in regions with high solar adoption, necessitates the efficient operation of solar panels, leading to a higher demand for cleaning services to maintain energy production.

𝐓𝐨𝐩 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬:

Kept Companies | CSG Glass | HB McClure Company | Perfect Solar Home | Schimmer Metal Standard | BOL WORKS Ltd. | Solar panel & solar cells manufacturer — Solar N Plus | Solar Panel Manufacturer — UK | First Solar | Solar Leading | Zhejiang Shengtai Energy Solar Panel Manufacturer | Solar Brasil | ADT Solar

#SolarPanelCleaning #CleanEnergy #SolarPower #EcoFriendlyCleaning #RenewableEnergy #SolarEfficiency #GreenEnergy #SolarMaintenance #CleanSolarPanels #SustainableEnergy

0 notes

Text

The Ultimate List of Villas Near Jigani Anekal Road: Find Your Dream Residence

Introduction

The real estate scene near Jigani Anekal Road is booming, especially for those looking for luxury lake-facing villas near jigani As demand grows, more homebuyers seek homes that offer scenic views and peaceful surroundings. Choosing the right villa can boost your lifestyle, serve as a smart investment, and connect you to a vibrant community. This guide reveals the top villa projects, key features to look for, tips on buying, and expert insights to help you find your perfect home.

Why Choose Villas Near Jigani Anekal Road? An Overview

Strategic Location Benefits

Located close to major IT parks and industrial corridors, Jigani Anekal Road is a prime spot for homebuyers. Its proximity to tech hubs makes commuting easy, which saves time and reduces stress. Good roads and transportation options mean you can reach Bengaluru city or other important areas quickly.

Lifestyle Advantages

Imagine waking up to stunning lake views every morning. The area offers a calm, green environment away from city noise. Many villa communities here include amenities like parks, clubhouses, and swimming pools, creating a resort-style living experience.

Market Growth Insights

In recent years, property prices near Jigani Anekal Road have steadily increased. The area’s development plans promise future growth, making villas here a promising investment. As infrastructure improves, property values are likely to climb, offering good returns.

Top Villa Developments by The BeautifulLake Near Jigani Anekal Road

Popular Villa Projects Overview

Several villa projects have gained popularity along this stretch. Notable names include By The BeautifulLake Villas,. These developments typically range from square feet, offering versatile layouts suitable for families or singles.

Highlights of Each Project:

BeautifulLake Villas: Focus on spacious living, with options for 3 to 4 BHK villas. Known for its eco-friendly design.

Developer Reputation and Track Record

Many developers here have built trusted communities with quality construction and timely delivery. Always check company history and reviews before finalizing. Reputable builders reduce risks and ensure your investment is secure.

Villa Features and Designs

These villas showcase modern architecture with large windows, open layouts, and customizable interiors. Some offer eco-friendly features such as solar power and rainwater harvesting, emphasizing sustainability and low utility bills.

Pricing and Investment Potential

Villa prices typically start at around ₹1.5 crore and can go up to ₹4 crore, depending on size and location within the project. With consistent appreciation and rental demand, these villas can provide attractive rental yields of 3-5%. Market data forecasts steady appreciation over the next 5-10 years.

Key Features and Amenities of By The BeautifulLake Villas

Luxurious Interiors and Finishes

Expect high-quality materials, spacious living rooms, and modern fixtures. Many villas include smart home features such as automated lighting, security systems, and climate controls.

Community and Lifestyle Amenities

Community living is enhanced with amenities like:

Clubhouses for social gatherings

Swimming pools and fitness centers

Beautiful landscaped gardens

Play areas for kids

Walking tracks and outdoor seating spaces

Security and Safety Measures

Gated entrances, CCTV surveillance, and trained security staff create a safe environment. Fire safety systems and disaster preparedness plans are standard, giving residents peace of mind.

Factors to Consider Before Buying a Villa Near Jigani Anekal Road

Location and Accessibility

Look for proximity to top schools, hospitals, and shopping centers. Ease of access via major roads or public transportation makes daily life smoother.

Legal and Documentation Checks

Ensure the land title is clear, and all necessary approvals are obtained from authorities. Avoid projects with pending legal issues or incomplete documentation.

Investment and Resale Value

Study market trends to assess future growth potential. Choose well-located developments with good reputation to maximize your return on investment.

Expert Recommendations and Market Insights

Real estate experts recommend focusing on projects with strong developer histories, good infrastructure, and community features. Upcoming infrastructure projects like new roads and metro expansions will enhance connectivity and property value.

According to consultants, the area's growth is expected to accelerate in the next few years, making now the right time to invest. Always seek advice from trusted real estate agents who understand local trends and can guide you through the buying process.

How to Choose Your Dream Villa Near Jigani Anekal Road

Buying Process Step-by-Step

Research: Explore listings online and visit model homes.

List priorities: Determine your preferred size, budget, and amenities.

Visit developments: Inspect sample villas for quality and layout.

Check legal papers: Verify land titles, approvals, and developer credentials.

Negotiate: Discuss prices, payment plans, and discounts.

Secure financing: Obtain home loans or mortgage approvals.

Finalize: Complete paperwork and sign contracts.

Key Questions for Developers

What are the project completion timelines?

Are there any hidden charges or fees?

What warranty coverage is provided?

Can I customize interior layouts?

Visiting Homes Tips

Check the construction quality, ventilation, lighting, and noise levels. Ask about maintenance plans and community rules before deciding.

Conclusion

Living near Jigani Anekal Road offers a perfect mix of scenic beauty and strategic convenience. Villas by The BeautifulLake stand out with their premium features, eco-friendly designs, and community amenities. Take your time to research options, ask the right questions, and choose a development that matches your lifestyle and investment goals. Contact trusted agents today to make your dream of owning a lake-facing villa a reality. The perfect home might just be a visit away.

0 notes

Text

One-Time Fuse Market: How Industry Players Are Driving Growth in 2025–2032

MARKET INSIGHTS

The global One-Time Fuse Market size was valued at US$ 345 million in 2024 and is projected to reach US$ 556 million by 2032, at a CAGR of 7.0% during the forecast period 2025-2032. While the U.S. accounts for 25% of the global market, China’s rapid industrialization is expected to drive significant growth with a projected CAGR of 5.8% through 2032.

One-Time Fuses are critical circuit protection devices designed to interrupt excessive current flow by melting when overloaded. These non-resettable fuses come in various types including quick disconnect and slow-breaking variants, each serving distinct applications in industries ranging from household appliances to industrial equipment. The quick disconnect segment alone is projected to grow at 5.1% CAGR, reaching USD 420 million by 2032.

Market expansion is primarily driven by increasing electrification across sectors and stricter safety regulations globally. Key players like Littelfuse and Eaton are innovating with compact, high-performance fuses to meet evolving industry demands. However, supply chain disruptions and raw material price volatility remain challenges. The competitive landscape remains concentrated, with the top five manufacturers holding about 40% market share in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Electrical Safety Solutions to Propel Market Expansion

The global one-time fuse market is experiencing significant growth driven by the increasing emphasis on electrical safety across industries. With rising incidents of electrical faults causing equipment damage and fire hazards, the demand for reliable circuit protection devices has surged. Industrial facilities, in particular, are adopting one-time fuses as cost-effective solutions to protect sensitive equipment from power surges. The market has witnessed notable growth in sectors such as manufacturing, energy, and construction, where electrical safety regulations are becoming more stringent. Recent data indicates that electrical faults account for over 25% of industrial equipment failures annually, creating substantial demand for protective devices like one-time fuses.

Expansion of Smart Home Technologies Creating New Demand Channels

The proliferation of smart home systems and IoT-enabled appliances is generating substantial growth opportunities for the one-time fuse market. As households increasingly adopt connected devices, the need for reliable circuit protection in residential settings has grown exponentially. Manufacturers are developing specialized fuses with faster response times to meet the unique requirements of smart home ecosystems. This trend is particularly pronounced in developed markets, where smart home penetration rates now exceed 35% in major urban centers. The integration of renewable energy systems in residential properties further amplifies this demand, as these installations require robust protection against voltage fluctuations and surges.

Industrial Automation Boom Driving Premium Product Demand

The ongoing automation revolution across manufacturing sectors is creating a strong pull for high-performance one-time fuses. Modern automated equipment with sensitive electronic components requires precise and reliable protection against electrical anomalies. This has led to increased adoption of quick-disconnect fuses in industrial control panels and robotics applications. The automotive industry’s shift toward electric vehicles has further accelerated this trend, with EV charging infrastructure requiring specialized fuse solutions. Recent industry reports suggest that the industrial automation sector now accounts for over 40% of premium one-time fuse sales globally, a figure projected to grow as automation adoption continues.

MARKET RESTRAINTS

Price Volatility of Raw Materials Creates Margin Pressures

The one-time fuse market faces significant challenges from fluctuating raw material costs, particularly for copper and silver used in fuse element manufacturing. Recent supply chain disruptions have led to price increases exceeding 30% for key materials, forcing manufacturers to either absorb costs or pass them to customers. This pricing pressure is particularly acute in cost-sensitive segments like residential applications, where consumers demonstrate high price elasticity. The situation is compounded by trade policies affecting metal imports, creating regional disparities in material availability.

Competition from Resettable Circuit Protection Devices