#Material Handling Robotics Material Handling Robotics market Material Handling Robotics Industry Global Material Handling Robotics industry

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. is funded by 13 investors.

Text

Iraq Oil and Gas Construction Companies: Key Players in Energy Development

As one of the world’s largest oil-producing countries, Iraq relies heavily on its oil and gas industry to drive economic growth. Iraq oil and gas construction companies are essential in building the infrastructure needed for exploration, extraction, and distribution of oil and gas. These companies play a vital role in constructing pipelines, refineries, storage facilities, and processing plants, which are crucial for Iraq’s energy sector. The expertise and efficiency of Iraq oil and gas construction companies directly influence the country’s ability to maintain its role as a global energy provider.

The Importance of Iraq’s Oil and Gas Sector

The oil and gas sector contributes around 90% of Iraq’s national revenue, making it a cornerstone of the economy. With abundant reserves and a strategic location, Iraq has positioned itself as a major player in the global energy market. However, the sector faces challenges, including the need to update outdated infrastructure and improve efficiency in extraction and refining processes. This is where Iraq oil and gas construction companies step in, offering the expertise and technology to modernize and expand infrastructure. Through their work, these companies not only contribute to economic growth but also help secure Iraq’s future as a competitive energy producer.

Key Services Offered by Iraq Oil and Gas Construction Companies

Iraq’s oil and gas construction companies provide a variety of services to meet the complex demands of the industry. These services include:

Pipeline Construction and Maintenance One of the most critical components of the oil and gas infrastructure is pipelines. They enable the safe and efficient transport of crude oil and natural gas across long distances. Iraq oil and gas construction companies specialize in designing, building, and maintaining pipelines that meet both national and international safety standards. Regular maintenance of these pipelines is crucial for preventing leaks and ensuring smooth operation, making these companies indispensable to the sector.

Refinery Construction and Expansion Refineries are vital for processing crude oil into usable products, such as gasoline, diesel, and petrochemicals. Iraq oil and gas construction companies are skilled in constructing new refineries and expanding existing ones to meet the increasing demand. These projects require advanced engineering and the latest technology to maximize efficiency and reduce environmental impact.

Storage Facilities Efficient storage solutions are essential for managing the supply of oil and gas, especially as global demand fluctuates. Iraq’s construction companies build and maintain large-scale storage facilities, which help manage the country’s energy reserves and stabilize the supply chain. Properly constructed storage facilities also ensure the safe handling of hazardous materials, reducing the risk of accidents.

Processing Plants and Equipment Installation Processing plants convert raw oil and gas into products ready for distribution. Iraq oil and gas construction companies work on both the construction and maintenance of these plants, installing specialized equipment designed to maximize output and minimize waste. This involves incorporating technology that meets international standards for efficiency and environmental protection, supporting Iraq’s long-term goals for sustainable energy production.

Technology and Innovation in Iraq’s Oil and Gas Construction Sector

To stay competitive and meet the demands of an evolving energy market, Iraq oil and gas construction companies are increasingly incorporating advanced technology into their projects. Key technologies used include:

Digital Monitoring and Automation: Digital sensors and automated systems help monitor pipeline pressure, detect leaks, and manage refinery operations more efficiently.

Drones and Robotics: Drones are now commonly used for aerial surveys and inspections, especially in challenging terrain. Robotics aid in tasks such as welding and equipment installation, enhancing precision and safety.

Environmental Technologies: New technologies designed to reduce emissions and manage waste are also being integrated. For instance, gas flaring reduction technology is becoming more common, helping to minimize environmental impact.

The Role of Local Expertise and International Partnerships

While Iraq oil and gas construction companies possess significant expertise, international partnerships are often crucial for large-scale projects. Collaborating with global firms allows Iraqi companies to leverage foreign technology, knowledge, and financing, enhancing their ability to complete complex projects successfully. These partnerships also facilitate knowledge transfer, training local engineers and workers in the latest techniques and technologies. This local expertise, combined with international standards, strengthens Iraq’s position in the global oil and gas market and builds a more sustainable workforce.

Challenges Faced by Iraq Oil and Gas Construction Companies

Despite their importance, Iraq oil and gas construction companies face several challenges. These include:

Security Concerns: Iraq has areas where security remains a concern, which can disrupt project timelines and create additional costs for safety measures.

Regulatory Hurdles: The regulatory environment can be complex, particularly for international partnerships. Compliance with both local and international regulations requires careful planning and adaptability.

Environmental Impact: With a growing emphasis on sustainability, Iraq oil and gas construction companies are increasingly pressured to reduce their environmental footprint, requiring additional investment in green technology and eco-friendly practices.

Conclusion

Iraq oil and gas construction companies are key drivers of the nation’s energy industry, enabling the development, maintenance, and expansion of crucial infrastructure. Their services in pipeline construction, refinery expansion, storage, and processing plants are foundational to Iraq’s energy production and economic stability. By embracing technological advancements and fostering international partnerships, these companies continue to support Iraq’s ambitions in the global energy sector. Despite challenges, the expertise and innovation of Iraq oil and gas construction companies remain essential for ensuring Iraq’s future as a competitive energy powerhouse.

2 notes

·

View notes

Text

Assembly Trays Market Size, Share, Demand, Growth and Global Industry Analysis 2034

Assembly Trays Market is projected to grow from $2.5 billion in 2024 to $4.3 billion by 2034, expanding at a compound annual growth rate (CAGR) of approximately 5.6%. These trays play a vital role in organizing, storing, and transporting components during manufacturing and assembly operations across industries such as electronics, automotive, aerospace, and healthcare. With the rising demand for precision, efficiency, and sustainability in industrial processes, assembly trays have become indispensable in supporting streamlined workflows and protecting sensitive parts.

This market has witnessed strong momentum due to the increased adoption of automation and the rise of lean manufacturing practices. The trays not only enhance operational efficiency but also reduce handling time and minimize errors in production lines. Additionally, companies are increasingly seeking eco-friendly, reusable, and customizable tray solutions that align with sustainability targets while maintaining durability and precision.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS22407

Market Dynamics

The dynamics driving the assembly trays market revolve around technological advancement, evolving material science, and shifting industry needs. A major driver is the growing reliance on automation in sectors like electronics and automotive, where trays enable compatibility with robotic systems and high-speed assembly lines. As industries push for faster turnaround times and greater accuracy, the demand for trays that are ESD-safe, cleanroom compliant, or custom-engineered is growing rapidly.

Plastic continues to dominate the market with a 45% share, valued for its lightweight, moldability, and cost-effectiveness. Metal and composite materials follow, preferred for applications requiring extra strength and temperature resistance. The surge in electric vehicle production, medical device innovation, and semiconductor manufacturing further amplifies tray demand.

However, the market is not without challenges. Volatile raw material prices, especially for polymers and metals, are pressuring margins. Regulatory compliance with safety and environmental standards also adds to operational complexity. Moreover, supply chain disruptions and increasing demand for product customization require manufacturers to remain flexible and innovative to stay competitive.

Key Players Analysis

The competitive landscape of the assembly trays market is shaped by a mix of global giants and emerging specialists. Prominent players such as 3M, Bosch, and Stanley Black & Decker hold significant market shares, benefiting from their strong industrial expertise and continuous investment in product innovation. Bosch’s emphasis on automation integration and 3M’s commitment to sustainable and recyclable tray solutions have set benchmarks for the industry.

Other key companies like UFP Technologies, Nelipak Healthcare Packaging, and Prent Corporation specialize in custom-engineered trays tailored to niche markets such as healthcare and precision electronics. Emerging players like Tray Tech Innovations, Eco Tray Manufacturing, and Smart Tray Solutions are gaining traction by focusing on sustainability, smart tracking capabilities, and adaptive designs for modern manufacturing environments.

Regional Analysis

Asia Pacific leads the global assembly trays market, fueled by industrial expansion in China, India, and Southeast Asia. These countries are experiencing a manufacturing boom in electronics, automotive, and consumer goods, creating massive demand for efficient and reliable tray systems. The region’s economic growth and emphasis on production scalability contribute significantly to the market’s upward trajectory.

North America follows closely, with the United States at the forefront. Its advanced manufacturing infrastructure and adoption of Industry 4.0 practices have driven demand for smart, reusable, and automation-compatible trays. The strong presence of leading tray manufacturers also supports regional growth.

Europe remains a vital player, particularly Germany and France, where precision engineering and sustainable manufacturing practices dominate. European regulations on material recyclability and worker safety drive innovation in environmentally friendly and ergonomic tray solutions.

Latin America and the Middle East & Africa show steady growth potential. Countries like Brazil and Mexico are investing in automotive and electronics production, while the UAE and South Africa are gradually developing their industrial sectors, increasing the need for high-performance assembly trays.

Recent News & Developments

The market has seen several transformative trends in recent years. Automation and digitalization are leading the way, with trays now being integrated with RFID and barcode tracking to improve inventory visibility and streamline assembly operations. Additionally, many manufacturers are shifting towards biodegradable and recyclable materials in response to growing environmental awareness.

Strategic partnerships are also shaping the landscape. For instance, tray manufacturers are collaborating with robotics and automation companies to co-develop solutions optimized for smart factories. This includes innovations in anti-static materials, heat resistance, and form-fitting compartments that support delicate and irregularly shaped components.

Cost efficiency remains a critical factor. With unit prices ranging from $5 to $50 depending on complexity, many companies are investing in thermoforming and injection molding technologies to scale up production without compromising quality.

Browse Full Report : https://www.globalinsightservices.com/reports/assembly-trays-market/

Scope of the Report

This report offers a comprehensive analysis of the global Assembly Trays Market, covering segmentation by type, product, material, application, technology, and functionality. It provides both qualitative and quantitative insights into current market trends, challenges, and future projections. The report assesses the competitive landscape and profiles major players, highlighting strategies like product innovation, mergers, and geographic expansion.

It also examines regulatory trends, regional market dynamics, and technological advancements shaping the industry. The research supports stakeholders in making informed decisions, identifying growth opportunities, and adapting to evolving customer demands. As industries continue to seek leaner, greener, and smarter solutions, the assembly trays market is well-positioned to deliver value across a broad spectrum of applications.

Discover Additional Market Insights from Global Insight Services:

Cold Forming and Cold Heading Market : https://www.globalinsightservices.com/reports/cold-forming-and-cold-heading-market/

Aviation Crew Management System Market : https://www.globalinsightservices.com/reports/aviation-crew-management-system-market/

Electron Beam Machining Market : https://www.globalinsightservices.com/reports/electron-beam-machining-market/

Ballast Tampers Market : https://www.globalinsightservices.com/reports/ballast-tampers-market/

Spring Energized Seals Market :https://www.globalinsightservices.com/reports/spring-energized-seals-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

Top Insights from Exploring the Impact of Robotics on Modern Manufacturing

Manufacturing is undergoing a profound shift, one where automation and intelligent systems are rewriting traditional production models. At the heart of this transformation lies robotics. Exploring the impact of robotics on modern manufacturing reveals not just improvements in output and accuracy but also deep changes in workforce dynamics, operational agility, and global competitiveness. Robotics is no longer just a cost-cutting tool—it is a strategic lever for innovation and sustainability.

The Evolution of Robotics in Manufacturing From the assembly lines of the 20th century to today’s smart factories, robotics has evolved from mechanical repetition to sophisticated autonomy. Early robotic arms performed singular tasks, but today’s robots are agile, adaptable, and connected to cloud-based intelligence. The integration of AI, machine vision, and predictive analytics allows modern robots to learn, optimize, and respond in real time, opening the door to mass customization and operational flexibility.

Robotic Automation and Production Efficiency One of the most significant contributions of robotics is the increase in speed and throughput. Robots handle repetitive tasks with unwavering consistency, allowing human workers to focus on supervision, analysis, and innovation. By minimizing downtime and eliminating errors, robotic automation enhances cycle times and streamlines workflows. This shift is crucial in meeting global demand without compromising quality.

Quality Control and Precision Engineering Consistency is the hallmark of robotic systems. In high-precision sectors such as electronics, automotive, and aerospace, robotics ensures microscopic accuracy and repeatability that human labor alone cannot guarantee. Integrated vision systems and sensors enable real-time monitoring and defect detection. This has not only reduced waste and rework but has elevated the overall reliability of production systems.

Workforce Transformation and Human-Robot Collaboration Contrary to fears of job displacement, robotics is redefining roles rather than replacing them. The focus is shifting toward collaboration, where robots perform strenuous tasks while humans handle decision-making and maintenance. This symbiosis improves workplace safety, reduces fatigue, and opens new opportunities for upskilling. As robotic systems grow more intuitive, the future workplace will rely on human-robot teams working side by side.

Supply Chain Resilience Through Robotic Integration Disruptions over the last few years have emphasized the need for agile, responsive manufacturing systems. Robotics plays a vital role in enabling just-in-time operations and localized production. Automated warehousing, robotic sorting, and predictive logistics powered by AI allow manufacturers to manage inventory better, reduce lead times, and improve responsiveness to market shifts.

Robotics and Sustainable Manufacturing Energy-efficient robotics and resource-optimized automation are supporting the industry’s shift toward sustainability. Robotic systems reduce material waste, optimize energy usage, and ensure precision in raw material handling. Additionally, by enabling closed-loop manufacturing models and recycling processes, robotics supports circular economy principles. Manufacturers are increasingly leveraging robots not just for efficiency but also to meet ESG goals.

Challenges and Considerations in Robotics Adoption While the benefits are clear, implementation requires thoughtful planning. Upfront investment, training needs, cybersecurity concerns, and system interoperability remain common challenges. However, as costs decline and modular, scalable robotics become more accessible, even small and mid-sized manufacturers are finding paths to adoption. A strategic approach ensures that robotics enhances rather than disrupts core operations.

For More Info https://bi-journal.com/exploring-the-impact-of-robotics-on-modern-manufacturing/

Conclusion Exploring the impact of robotics on modern manufacturing shows that automation is more than a technological upgrade—it is a blueprint for resilience, competitiveness, and innovation. Robotics empowers manufacturers to scale sustainably, adapt to changing demands, and create smarter, safer work environments. The integration of robotics represents not the end of the traditional manufacturing workforce, but the beginning of a new era where machines enhance human potential and drive forward the future of industry.

#Smart Manufacturing#Industrial Automation#Robotics In Manufacturing#BI Journal#BI Journal news#Business Insights articles

0 notes

Text

Neuromorphic Chip Market Emerging Trends Shaping Future Intelligent Computing Systems

The global neuromorphic chip market is rapidly evolving, propelled by increasing demand for energy-efficient, brain-inspired hardware capable of handling complex computational tasks. Neuromorphic chips, modeled after the human brain's neural architecture, offer immense advantages in cognitive processing, enabling real-time learning, low power consumption, and adaptive performance. With industries embracing AI-driven solutions, the demand for neuromorphic chips is expected to surge, fostering innovation across sectors such as robotics, automotive, healthcare, and defense.

Emerging Trends in the Neuromorphic Chip Market

1. Rising Integration of Neuromorphic Chips in Edge AI Devices

One of the most notable trends is the increasing deployment of neuromorphic chips in edge computing environments. Traditional cloud-based AI systems face challenges such as latency, bandwidth limitations, and data privacy concerns. Neuromorphic chips, with their low power consumption and real-time processing abilities, are ideal for edge AI applications like smart cameras, drones, autonomous vehicles, and IoT devices. Their capability to perform on-device learning and decision-making is transforming edge AI, enhancing speed, efficiency, and data security.

2. Growing Adoption in Autonomous Vehicles and Robotics

The autonomous vehicle industry and robotics sector are among the early adopters of neuromorphic technology. Self-driving cars and intelligent robots require systems that can process massive amounts of sensory data, adapt to dynamic environments, and make real-time decisions. Neuromorphic chips replicate the brain’s neural networks, making them exceptionally suitable for such applications. Companies are investing heavily in integrating neuromorphic processors to improve perception, navigation, and decision-making capabilities, contributing to safer and more efficient autonomous systems.

3. Expansion of Neuromorphic Computing in Healthcare Devices

Healthcare is emerging as a significant application area for neuromorphic chips. Medical devices equipped with neuromorphic processors are being developed for real-time monitoring, predictive diagnostics, and intelligent prosthetics. These chips enable continuous learning and adaptation, essential for devices assisting patients with neurological disorders, wearable health monitors, or AI-based diagnostic systems. The fusion of neuromorphic technology with healthcare is expected to enhance patient care, improve diagnostic accuracy, and enable more personalized medical interventions.

4. Advancements in Brain-Machine Interfaces (BMI)

The convergence of neuromorphic chips with brain-machine interfaces is accelerating research into advanced neuroprosthetics and human augmentation technologies. Neuromorphic hardware can process neural signals more efficiently and in real time, facilitating better communication between human brains and machines. This trend is particularly promising for assisting individuals with motor disabilities, developing mind-controlled devices, and exploring cognitive enhancement technologies.

5. Increasing Research and Collaboration Initiatives

Global research institutions, tech companies, and governments are investing significantly in neuromorphic computing research. Collaborative projects such as the Human Brain Project and DARPA's SyNAPSE program are driving innovation in neuromorphic chip design, materials, and architectures. This surge in collaborative efforts aims to overcome existing technological barriers, enhance scalability, and develop next-generation neuromorphic processors suited for commercial deployment.

6. Emergence of Neuromorphic Hardware Startups

The neuromorphic chip market is witnessing a wave of startups focused on specialized neuromorphic hardware solutions. These startups are introducing innovative chip designs leveraging novel materials like memristors, spintronics, and phase-change memory to emulate synaptic behaviors. Their agile approach to R&D and niche focus areas are accelerating breakthroughs in chip performance, energy efficiency, and scalability, challenging traditional semiconductor players to innovate faster.

7. Energy-Efficient Computing Driving Market Demand

With growing concerns over the energy consumption of AI data centers and computing infrastructures, energy-efficient neuromorphic chips are gaining traction. These chips offer significant reductions in power usage compared to conventional processors while maintaining high-performance cognitive processing capabilities. As sustainability becomes a critical focus for technology development, neuromorphic chips are poised to play a vital role in achieving greener, low-power AI systems.

Conclusion

The neuromorphic chip market is at the forefront of redefining intelligent computing with its brain-inspired design and unparalleled efficiency. Emerging trends such as edge AI integration, healthcare applications, autonomous systems, and advancements in BMI are fueling market expansion. As research, collaborations, and startup innovations continue to accelerate, neuromorphic chips are expected to become a cornerstone of next-generation AI, fostering breakthroughs across industries and revolutionizing how machines learn and interact with the world.

0 notes

Text

Flexible Automation Needs Drive Strong Demand for Collaborative Robots

The global collaborative robot (cobot) market was valued at USD 1.2 billion in 2023 and is projected to expand at a remarkable CAGR of 26.1% from 2024 to 2034, reaching a market size of USD 15.3 billion by the end of 2034, according to the latest industry research. This exponential growth is primarily driven by the growing demand for workplace automation, enhanced safety standards, and advancements in robotics technology.

Market Overview: Collaborative robots designed to work safely alongside humans are transforming industries by combining precision, productivity, and adaptability. Unlike traditional industrial robots, cobots feature integrated safety mechanisms, including force-limiting sensors and intelligent programming, enabling them to perform tasks in dynamic environments shared with human workers.

These robots are increasingly adopted across industries including automotive, electronics & semiconductors, healthcare, food & beverage, and logistics, owing to their flexibility, efficiency, and cost-effectiveness.

Market Drivers & Trends

1. Surging Demand for Automation

Industries worldwide are facing escalating labor costs and demand for consistent output. Cobots are bridging the gap by enhancing productivity without replacing human labor, enabling businesses to stay competitive in fast-evolving global markets.

2. Focus on Workplace Safety & Ergonomics

Companies are investing heavily in solutions that enhance worker safety and comfort. Cobots, designed with built-in torque and speed control features, address these concerns effectively—significantly reducing workplace injuries and enhancing job satisfaction.

3. Flexibility and Reusability

Cobots can be easily programmed, re-deployed, and adapted for various tasks. This makes them invaluable in dynamic production settings, especially in consumer electronics and automotive manufacturing, where production lines often change.

Latest Market Trends

Integration of AI Capabilities: The latest cobots incorporate artificial intelligence and machine learning, enabling smarter task execution, predictive maintenance, and real-time decision-making.

Human-Robot Collaboration Enhancements: Next-gen cobots are now equipped with advanced vision systems, touch sensitivity, and voice commands, allowing seamless interaction with human co-workers.

Compact and Lightweight Designs: Smaller cobots are gaining traction among SMEs that require affordable automation with minimal footprint.

Key Players and Industry Leaders

The collaborative robot market is moderately consolidated, with leading players holding around 55–60% market share. Major companies include:

ABB Group

FANUC CORPORATION

KUKA AG

Kawasaki Heavy Industries Ltd.

Mitsubishi Electric Corporation

Yaskawa Electric Corporation

OMRON Corporation

Schneider Electric SE

These companies are investing aggressively in R&D, product portfolio expansion, and strategic acquisitions.

Access an overview of significant conclusions from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=15536

Recent Developments

Universal Robots launched the UR20 in April 2023, the company’s most powerful cobot, featuring a 20 kg payload and a 1750 mm reach—ideal for heavy-duty applications.

In March 2023, Fanuc upgraded its CRX series with enhanced AI features, simplifying programming and improving adaptability for diverse manufacturing tasks.

ABB introduced the GoFa cobot, combining high payload capacity with safety-focused operations for assembly and material handling.

Market Opportunities

As cobot technologies evolve, new applications are emerging in healthcare, pharmaceuticals, logistics, and 3PL operations. These sectors are expected to witness substantial adoption due to labor shortages and increasing demand for precision, hygiene, and continuous operations.

The electronics & semiconductors sector, in particular, is anticipated to remain a dominant force, holding a 26.5% market share in 2023 and forecast to grow at a 30.9% CAGR, driven by increasing complexity in microelectronic assemblies.

Future Outlook

Analysts forecast a bright future for the collaborative robot industry, with wider integration across small and medium-sized enterprises, AI-embedded robotics, and scalable solutions becoming the norm. Governments supporting smart manufacturing and Industry 4.0 are further fueling demand.

Companies that adopt cobot solutions early stand to benefit from:

Increased output

Enhanced safety

Greater operational flexibility

Reduced downtime

Stronger return on investment (ROI)

Market Segmentation

By Type:

Power and Force Limiting Cobots

Hand Guiding Cobots

Safety Monitored Stop Cobots

Speed and Separation Cobots

By Component:

Hardware (End Effectors, Robot Arm, Controllers, Sensors)

Software

Services

By Payload:

<5 Kg

5–10 Kg

10–20 Kg

Above 20 Kg

By Application:

Material Handling

Assembly

Inspection & Quality Testing

Painting

Others

By End-use Industry:

Automotive

Electronics & Semiconductors

Healthcare

Food & Beverage

Aerospace & Defense

3PL

Others

Regional Insights

Asia Pacific led the global collaborative robot market in 2023 with a 34.2% share and is expected to grow at 28.9% CAGR. The region houses the world’s top manufacturing economies—China, Japan, South Korea, and India—driven by:

Large-scale manufacturing units

Government incentives for automation

Growing SMEs looking for cost-effective automation solutions

North America and Europe are also growing steadily due to technological maturity and early adoption of automation solutions.

Why Buy This Report?

Comprehensive market sizing and forecasts (2024–2034)

Detailed segmentation by type, payload, component, application, and region

Strategic analysis of key players and market shares

Coverage of recent innovations and technological developments

Insights into growth opportunities and investment areas

Regional performance analysis across North America, Europe, Asia Pacific, and more

In-depth industry dynamics: drivers, restraints, and future prospects

Explore Latest Research Reports by Transparency Market Research:

Surface Acoustic Wave (SAW) Devices Market: https://www.transparencymarketresearch.com/surface-acoustic-wave-sensors.html

Rugged Power Supply Market: https://www.transparencymarketresearch.com/rugged-power-supply-market.html

Ceramified Cable Market: https://www.transparencymarketresearch.com/ceramified-cable-market.html

Gantry (Cartesian) Robot Market: https://www.transparencymarketresearch.com/gantry-robot-market.htmlAbout Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Material Handling Equipment Market Outlook Global Trends, Statistics, Size, Share, Regional Analysis by Key Players (2021-2031)

The Material handling equipment market size is expected to reach US$ 92.63 billion by 2031 from US$ 60.05 billion in 2024. The market is estimated to record a CAGR of 6.51% from 2025 to 2031.

Executive Summary and Global Market Analysis

The global material handling equipment market is experiencing strong growth. This is largely due to rapid industrialization, increased warehouse automation, and the expanding e-commerce sector. The market includes a wide array of equipment used for transporting, storing, controlling, and protecting materials throughout various processes, including manufacturing, distribution, and disposal.

The industry's expansion is primarily driven by a growing need for operational efficiency, the increasing adoption of automation technologies, and a demand for better supply chain transparency. In response, manufacturers are developing innovative solutions that integrate advanced technologies like artificial intelligence (AI), the Internet of Things (IoT), and robotics to optimize warehouse operations and logistics infrastructure. Geographically, the Asia-Pacific region leads the market, thanks to significant infrastructure investments and rapid urbanization in countries like China and India.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/BMIPUB00031690

Material Handling Equipment Market Segmentation Analysis

The material handling equipment market analysis is derived from key segments: technology, material, application, and end user.

By Equipment Type, the market is segmented into:

Cranes and Lifting Equipment

Industrial Trucks

Automated Storage and Retrieval Systems (AS/RS)

Conveying Systems

Racking and Storage Equipment

Automated Guided Vehicles (AGVs)

Bulk Material Handling Equipment

Others

By End-Use Industry, the market is segmented into:

Logistics

Automotive

Construction

Food & Beverages

Pharmaceuticals/Healthcare

Semiconductor & Electronics

By Application Type, the market is segmented into:

Assembly

Transportation

Distribution

Others

Material Handling Equipment Market Drivers and Opportunities

The rapid expansion of e-commerce is a significant driver for the material handling equipment market. As online retail grows, companies like Amazon and Alibaba are investing in automated warehouses to manage high order volumes. This, in turn, increases the demand for equipment such as forklifts, conveyors, and Automated Guided Vehicles (AGVs).

Urbanization and rising consumer expectations for quick deliveries further boost the need for efficient logistics systems. The growth of warehousing in regions like Asia-Pacific and North America directly fuels equipment sales. As e-commerce continues its upward trend, the demand for advanced material handling solutions to streamline operations and reduce delivery times will significantly propel market expansion.

Material Handling Equipment Market Size and Share Analysis

By Equipment Type: Cranes and Lifting Equipment, along with Industrial Trucks, Automated Storage and Retrieval Systems (AS/RS), Conveying Systems, Racking andStorage Equipment, Automated Guided Vehicles (AGVs), and Bulk Material Handling Equipment, are crucial. Cranes and lifting equipment are vital across construction, manufacturing, heavy engineering, automotive, and logistics for efficiently moving heavy materials and payloads. The construction industry, in particular, drives substantial demand due to ongoing urbanization, infrastructure development, and large-scale industrial projects.

By End-User Industry: The global growth of automobile production necessitates efficient material handling systems to manage the flow of materials and finished vehicles within factories and distribution centers. Automotive manufacturing plants are increasingly adopting modernized material handling infrastructure to improve assembly processes, reduce turnaround times, and support lean manufacturing principles, all of which require advanced handling equipment. The automotive industry's adoption of automation, robotics, and IoT-enabled material handling solutions enhances operational efficiency and safety, further boosting the demand for sophisticated equipment.

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

0 notes

Text

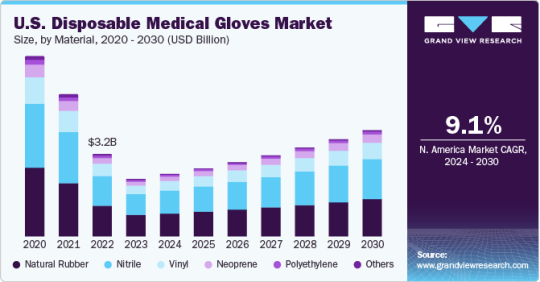

From Clinics to Labs: Applications Expanding in the Disposable Medical Gloves Market

Disposable Medical Gloves Market Growth & Trends

The global disposable medical gloves market is set to reach USD 12.49 billion by 2030, growing at a Compound Annual Growth Rate (CAGR) of 8.9% from 2024 to 2030. This robust growth, as per a new report by Grand View Research, Inc., is primarily fueled by the rising incidence of infectious diseases and viral outbreaks, coupled with increasing healthcare expenditures.

Key Market Drivers and Trends

Several factors are contributing to the expansion of the disposable medical gloves market:

Increasing Prevalence of Infectious Diseases and Viral Outbreaks: The heightened awareness and need for infection control, particularly in the wake of global health crises like the COVID-19 pandemic, are significantly driving demand. The resurgence of COVID-19 is expected to further boost hospital visits and product demand.

Rising Healthcare Expenditure: Growing investments in both public and private healthcare sectors, coupled with an expanding geriatric population and a high influx of migrants, are bolstering the overall healthcare industry, which in turn increases the demand for medical gloves.

Adoption of Novel Healthcare Practices and Advanced Medical Technologies: The continuous evolution of medical care products and technologies, alongside the adoption of modern medical infrastructure, necessitates the use of disposable medical gloves for safety and hygiene.

Technological Advancements and Strategic Investments

The industry is also witnessing significant technological advancements and strategic initiatives by market players:

Automation in Manufacturing: The COVID-19 pandemic accelerated the adoption of automation in glove manufacturing. Robotics are increasingly being used in various processes, including manufacturing, packaging, and counting. For example, Doka Industrial Automation has developed machines to automate the entire glove production and packaging process.

Strategic Investments for Expansion: Companies are making substantial strategic investments to enhance their production capabilities and product portfolios. In March 2021, Hartalega Holdings Berhad acquired 250 acres of land in Kedah for USD 55.4 million to expand its glove manufacturing operations, aiming to increase its annual production capacity significantly over the long term. This expansion, part of a larger RM7 billion investment, is set to solidify Malaysia's position as a global leader in glove manufacturing.

Curious about the Disposable Medical Gloves Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Disposable Medical Gloves Market Report Highlights

The natural rubber material segment contributed to the maximum revenue share in 2023. These materials are flexible and easy to wear & use, which makes them ideal for use in handling water-based or biological materials

The demand for surgical disposable medical gloves is expected to witness significant growth from 2023 to 2030 on account of precise sizing and design that offers high accuracy and tactile sensitivity as required by healthcare workers

The hospital end-use segment accounted for the largest revenue share in 2023 owing to the high prevalence of chronic diseases, which increased the number of hospital visits and re-admissions

The Asia Pacific regional market is expected to register the fastest CAGR over the forecast period owing to the rapidly growing healthcare infrastructure including hospitals and clinics coupled with rising medical tourism

In December 2021, Supermax Corp. Berhad incorporated Maxter Healthcare Inc., a new wholly-owned subsidiary in the U.S. to produce Personal Protective Equipment (PPE) and medical gloves

Disposable Medical Gloves Market Segmentation

Grand View Research has segmented the global disposable medical gloves market based on material, product, application, end-use, region:

Disposable Medical Gloves Material Outlook (Revenue, USD Billion, 2018 - 2030)

Natural Rubber

Nitrile

Vinyl

Neoprene

Polyethylene

Others

Disposable Medical Gloves Product Outlook (Revenue, USD Billion, 2018 - 2030)

Powdered

Powder-free

Disposable Medical Gloves Application Outlook (Revenue, USD Billion, 2018 - 2030)

Examination

Surgical

Disposable Medical Gloves End-use Outlook (Revenue, USD Billion, 2018 - 2030)

Hospitals

Home Healthcare

Outpatient/Primary Care Facilities

Others

Download your FREE sample PDF copy of the Disposable Medical Gloves Market today and explore key data and trends.

0 notes

Text

Top-Quality Automotive OEM Services Grand Rapids MI Experts

When it comes to meeting the high demands of the auto manufacturing industry, precision and reliability are key. For manufacturers in Michigan, finding dependable partners for automotive OEM services Grand Rapids MI is essential to staying competitive and delivering quality products. Companies in this region require custom, scalable, and high-performance solutions that meet rigorous automotive standards while also staying cost-effective.

Grand Rapids, MI has long been a hub for manufacturing excellence, particularly in the automotive sector. With a skilled workforce, advanced technology, and close proximity to major automotive centers, it’s no surprise that automotive OEM suppliers Grand Rapids MI are among the most trusted in the industry. These suppliers provide critical components, assemblies, and fabrication services that fuel the production lines of major auto brands.

Businesses seeking automotive OEM services Grand Rapids MI can expect a wide array of capabilities, from metal fabrication and CNC machining to engineering support and full prototype-to-production runs. What sets Grand Rapids apart is not only the range of services available but also the dedication to customer satisfaction and quality control. The suppliers here are committed to meeting stringent industry requirements, including IATF 16949 certification and continuous improvement practices.

One major advantage of working with automotive OEM suppliers Grand Rapids MI is their flexibility and ability to adapt to complex project specifications. Whether a company needs rapid prototyping or long-term production runs, these suppliers can handle changing needs with efficiency and precision. Many offer vertically integrated solutions, reducing lead times and increasing overall reliability for automotive manufacturers.

The automotive industry continues to evolve with innovations in electric vehicles, lightweight materials, and enhanced safety systems. To keep pace, OEM suppliers must also innovate. In Grand Rapids, OEM partners are investing in automation, robotics, and quality assurance systems that ensure every component meets exact specifications. This commitment to innovation makes the region a key player in the future of automotive manufacturing.

Choosing a local supplier also means better communication, quicker turnaround, and easier coordination for engineering changes or urgent production needs. The relationships developed with trusted partners in Grand Rapids are built on years of collaboration and proven results, making it easier for manufacturers to stay agile and competitive in a global market.

To stay ahead in today’s fast-paced automotive industry, partnering with the right supplier is more important than ever. With the growing demand for advanced vehicle components, manufacturers benefit greatly from dependable automotive OEM services Grand Rapids MI. Collaborating with experienced automotive OEM suppliers Grand Rapids MI ensures precision, consistency, and innovation at every stage of production. Grand Rapids continues to lead as a center of excellence, offering the expertise and cutting-edge capabilities that drive the future of automotive manufacturing.

0 notes

Text

Global Ultrasonic Radar Market : Share, Size, Trends by 2025-2032

MARKET INSIGHTS

The global Ultrasonic Radar Market was valued at US$ 1.7 billion in 2024 and is projected to reach US$ 3.4 billion by 2032, at a CAGR of 9.0% during the forecast period 2025-2032. While the U.S. holds the largest market share at USD 310 million in 2024, China is expected to witness accelerated growth with projected revenues reaching USD 420 million by 2032.

Ultrasonic radar systems utilize high-frequency sound waves to detect objects and measure distances through echolocation technology. These systems consist primarily of transmitters, receivers, and signal processors, finding applications in automotive parking assistance, collision avoidance, and autonomous navigation across various industries. The market is segmented into PA (Parking Assist) and APA (Automatic Parking Assist) ultrasonic radar systems, with APA systems projected to grow at a faster 9.2% CAGR through 2032.

The market expansion is driven by increasing ADAS adoption in vehicles, with over 45% of new cars globally now equipped with ultrasonic sensors. However, technological challenges in harsh weather conditions remain a restraint. Key industry players including Valeo, Bosch, and Denso collectively hold 58% market share, with recent developments focusing on higher frequency (80+ kHz) sensors for improved accuracy in autonomous vehicle applications.

MARKET DYNAMICS MARKET DRIVERS

Growing Demand for Advanced Driver-Assistance Systems (ADAS) to Accelerate Market Expansion

The ultrasonic radar market is experiencing robust growth due to the increasing adoption of ADAS in modern vehicles. With over 60% of new vehicles globally now equipped with some form of ADAS, ultrasonic sensors have become indispensable for parking assistance and collision avoidance systems. These radar systems provide accurate short-range detection, typically between 30 cm to 500 cm, making them ideal for low-speed maneuverability. Automakers are increasingly integrating multiple ultrasonic sensors around vehicle perimeters to enable 360-degree obstacle detection, driving component demand. The expansion of autonomous vehicle testing programs across North America, Europe, and Asia further amplifies this need for reliable proximity sensing solutions.

Expansion of Industrial Automation to Fuel Ultrasonic Radar Adoption

Industrial sectors are rapidly adopting ultrasonic radar technology for material handling, robotic positioning, and conveyor belt monitoring applications. The technology’s immunity to environmental factors like dust, smoke, or lighting conditions makes it particularly valuable in manufacturing environments. Recent advancements in signal processing algorithms have enhanced measurement accuracy to sub-millimeter levels, enabling precise robotic control in automated assembly lines. With the global industrial automation market projected to maintain steady growth, ultrasonic radar solutions are becoming critical components in smart factory implementations across automotive, electronics, and logistics sectors.

MARKET CHALLENGES

Signal Interference Issues to Hamper Market Progress

While ultrasonic radar offers numerous advantages, the technology faces persistent challenges with signal interference in crowded electromagnetic environments. Multiple ultrasonic sensors operating simultaneously can create signal crosstalk, leading to false readings or detection failures. This limitation becomes particularly pronounced in complex industrial settings where numerous automated systems operate in close proximity. Current solutions involving time-division multiplexing or frequency modulation add complexity and cost to system implementations. Additionally, environmental factors such as temperature fluctuations and humidity variations can impact signal propagation characteristics, requiring sophisticated compensation algorithms to maintain accuracy.

Other Challenges

Limited Detection Range The effective operating range of ultrasonic radar typically falls below 5 meters, restricting its applications compared to competing technologies like LiDAR or microwave radar. This range limitation prevents ultrasonic solutions from being used in highway-speed collision avoidance systems where longer detection distances are required.

Acoustic Noise Sensitivity High ambient noise levels in industrial environments can mask ultrasonic signals, reducing system reliability. Although signal processing techniques help mitigate this issue, they increase computational requirements and power consumption.

MARKET RESTRAINTS

Competition from Alternative Sensing Technologies to Limit Market Penetration

Ultrasonic radar systems face increasing competition from emerging sensing technologies, particularly in premium automotive applications. While ultrasonic sensors dominate parking assistance applications, their market share in forward collision warning systems is being eroded by camera-based vision systems and millimeter-wave radar. These alternative technologies offer superior performance in critical parameters such as detection range, angular resolution, and resistance to weather conditions. Automotive OEMs are increasingly adopting sensor fusion approaches that combine multiple technologies, potentially reducing the number of ultrasonic sensors per vehicle. This industry shift toward multi-modal sensing architectures could constrain the growth potential for standalone ultrasonic radar solutions.

MARKET OPPORTUNITIES

Emerging Applications in Mobile Robotics to Drive Future Market Growth

The rapid expansion of service robotics and automated guided vehicles (AGVs) presents significant growth opportunities for ultrasonic radar manufacturers. Autonomous mobile robots require robust proximity sensing for navigation and obstacle avoidance in dynamic environments. Emerging applications in healthcare robots, warehouse logistics automatons, and last-mile delivery drones are fueling demand for compact, low-power ultrasonic sensing solutions. The development of advanced phased-array ultrasonic radar systems capable of beam-forming and 3D object classification opens new possibilities for robotic perception systems. With the global service robot market expected to maintain strong growth, ultrasonic radar technologies are well-positioned to capture a substantial portion of this expanding application space.

Smart City Infrastructure Development to Create New Revenue Streams

Municipalities worldwide are deploying intelligent transportation systems as part of smart city initiatives, creating opportunities for ultrasonic radar applications. Innovative implementations include ultrasonic vehicle detection at intersections, parking space monitoring, and traffic flow analysis. These applications benefit from the technology’s reliability and lower cost compared to alternative sensing methods. The increasing focus on pedestrian safety in urban environments is driving demand for ultrasonic crosswalk monitoring systems that can detect vulnerable road users in all weather conditions. As smart city projects gain momentum globally, ultrasonic radar solutions are emerging as cost-effective components for various infrastructure monitoring applications.

ULTRASONIC RADAR MARKET TRENDS Increasing Automotive Safety Requirements Driving Market Growth

The ultrasonic radar market is witnessing robust growth due to stringent automotive safety regulations and the rising adoption of advanced driver assistance systems (ADAS). With over 60% of new passenger vehicles now equipped with parking assistance systems incorporating ultrasonic sensors, demand for high-performance ultrasonic radar solutions has surged. Emerging innovations such as 4D imaging radar are pushing the boundaries of object detection accuracy, enabling vehicles to detect obstacles with millimeter-level precision. Furthermore, the integration of AI-powered signal processing algorithms has enhanced the capability of ultrasonic radar systems to distinguish between static and dynamic objects in challenging environments.

Other Trends

Expansion in Autonomous Robotics

The proliferation of autonomous mobile robots (AMRs) and drones across industrial and commercial applications is creating new opportunities for ultrasonic radar technology. Unlike traditional optical sensors, ultrasonic systems perform reliably in diverse lighting conditions, making them ideal for warehouse automation and last-mile delivery drones. Recent market data indicates that 35% of commercial drones now incorporate ultrasonic obstacle avoidance systems, demonstrating the technology’s crucial role in collision prevention. As robotics manufacturers seek more cost-effective sensing solutions, ultrasonic sensors are becoming preferred alternatives to expensive LiDAR systems for short-range applications.

Miniaturization and Energy Efficiency Advancements

Technological breakthroughs in semiconductor manufacturing are enabling the development of smaller, more power-efficient ultrasonic radar solutions. The latest generation of MEMS-based ultrasonic sensors consumes 40% less power while offering improved detection ranges compared to conventional piezoelectric counterparts. This evolution is particularly significant for battery-powered IoT devices and wearable applications where size and energy constraints dictate design parameters. Concurrently, advancements in beamforming techniques are allowing single ultrasonic sensor units to replace multi-sensor arrays in certain applications, reducing system complexity and cost without compromising performance.

COMPETITIVE LANDSCAPE Key Industry Players

Automotive Giants and Tech Innovators Drive Ultrasonic Radar Market Competition

The global ultrasonic radar market features a mix of established automotive suppliers and emerging technology specialists, creating a dynamic competitive environment. Valeo and Bosch currently dominate the market, collectively holding approximately 35% revenue share in 2024. Their leadership stems from decades of automotive sensor development and strong OEM relationships across Europe, North America, and Asia.

Meanwhile, Denso Corporation has been gaining significant traction through its advanced parking assist systems, while Murata Manufacturing brings unique miniaturization expertise from the electronics sector. These companies are driving innovation in compact radar designs, particularly for drone and robotics applications where size and weight are critical factors.

The competitive intensity is further heightened by Chinese manufacturers like Audiowell Electronics and Hangsheng Electronics who are rapidly expanding their production capacity. These regional players are fueling price competition while simultaneously improving technological capabilities, particularly in the cost-sensitive Asian markets.

Strategic movements in the sector include Continental AG’s 2023 acquisition of a specialized sensor firm to boost its ultrasonic technology portfolio. Similarly, Whetron Electronics recently announced a joint development program with two major Chinese automakers, indicating how partnerships are becoming crucial for market penetration.

List of Key Ultrasonic Radar Companies Profiled Valeo (France) Bosch (Germany) Nicera (Japan) Murata Manufacturing (Japan) Denso Corporation (Japan) Audiowell Electronics(Guangdong)Co.,Ltd. (China) Continental AG (Germany) Coligen (China) Corp. (China) Hangsheng Electronics (China) Whetron Electronics (Taiwan) Tung Thih Electron (Taiwan) Shunhe (China) Longhorn Auto (China) Segment Analysis: By Type

PA Ultrasonic Radar Segment Leads Due to Cost-Effectiveness and Automotive Integration

The market is segmented based on type into:

PA Ultrasonic Radar Subtypes: Single-beam, Multi-beam, and others APA Ultrasonic Radar By Application

Automotive Segment Dominates Market Share Owing to Rising Demand for Parking Assistance Systems

The market is segmented based on application into:

Automotive Drone Robot Other By Frequency Range

40-100kHz Range Holds Major Share Due to Optimal Balance of Range and Resolution

The market is segmented based on frequency range into:

20-40kHz 40-100kHz Above 100kHz Regional Analysis: Ultrasonic Radar Market

North America The North American ultrasonic radar market is experiencing steady growth, driven by strong demand from the automotive sector, particularly for parking assistance and collision avoidance systems. The United States leads the region, accounting for a significant share of the market revenue, supported by stringent safety regulations and the rapid adoption of advanced driver-assistance systems (ADAS). The Infrastructure Investment and Jobs Act has further spurred demand by allocating funds for smart mobility solutions. Key players like Bosch and Continental are investing in next-generation ultrasonic sensing technologies to meet evolving industry needs. However, high development costs and competition from LiDAR-based systems pose challenges to market expansion.

Europe Europe remains a critical hub for ultrasonic radar innovation, with Germany and France at the forefront. The region benefits from strict automotive safety standards under the European New Car Assessment Programme (Euro NCAP), which mandates collision avoidance and parking assistance features. European automakers are integrating ultrasonic radars with AI-powered systems for autonomous driving, creating new market opportunities. Environmental regulations also encourage manufacturers to enhance energy efficiency in sensor production. While market penetration is high, competition from alternative sensing technologies and economic uncertainties in Eastern Europe pose growth constraints.

Asia-Pacific As the fastest-growing ultrasonic radar market, the Asia-Pacific region is powered by China, Japan, and South Korea’s thriving automotive industries. China dominates both production and consumption, with automakers leveraging ultrasonic sensors for cost-effective ADAS solutions. Emerging applications in robotics and drones further boost demand, particularly in industrial automation. However, pricing pressures from regional low-cost manufacturers challenge profitability for global suppliers. India’s expanding auto sector presents significant opportunities, though infrastructure limitations slow widespread adoption. The shift toward electric vehicles (EVs) is expected to drive ultrasonic radar integration in battery management and charging systems.

South America South America’s ultrasonic radar market is nascent but growing, fueled by Brazil and Argentina’s efforts to modernize automotive safety standards. Local manufacturers prioritize affordability, leading to increased adoption of ultrasonic radar systems as a cost-efficient alternative to LiDAR. Economic volatility and supply chain disruptions, however, limit the scope of technological advancements. The aftermarket segment plays a crucial role due to slower OEM adoption, though government initiatives promoting smart mobility could accelerate market expansion in the coming years.

Middle East & Africa The Middle East & Africa region shows moderate growth potential, with the UAE and Saudi Arabia investing in smart city projects and autonomous vehicle trials. Ultrasonic radar adoption is increasing in fleet management and logistics applications. However, low vehicle electrification rates and limited regulatory frameworks hinder broader market penetration. Africa’s market remains underdeveloped, though urbanization and infrastructure investments in select countries could create future opportunities.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Ultrasonic Radar markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Ultrasonic Radar market was valued at USD million in 2024 and is projected to reach USD million by 2032. Segmentation Analysis: Detailed breakdown by product type (PA Ultrasonic Radar, APA Ultrasonic Radar), application (Automotive, Drone, Robot, Others), and end-user industry to identify high-growth segments and investment opportunities. Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million. Competitive Landscape: Profiles of leading market participants including Valeo, Bosch, Nicera, Murata, Denso, Audiowell Electronics, and others, covering their product offerings, R&D focus, and recent developments. Technology Trends & Innovation: Assessment of emerging technologies in ultrasonic sensing, integration with ADAS systems, and evolving industry standards. Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers. Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/06/global-pecvd-equipment-market-size.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-embedded-sbc-market-trends-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-encoder-chips-market-driving.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-bluetooth-audio-chips-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/semiconductor-ip-blocks-market-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-dc-power-supply-for.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-high-voltage-power-supply-for.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-industrial-sun-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-consumer-grade-contact-image.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-non-residential-occupancy.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-standalone-digital-signage.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/12-inch-silicon-wafers-market-global-12.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-12-inch-semiconductor-silicon.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-extreme-ultraviolet-lithography.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-industrial-touchscreen-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-distributed-fiber-optic-sensor.html

0 notes

Text

Top PET Preform Manufacturers India Leaders in Packaging Innovation

India has emerged as a global powerhouse in PET preform manufacturing, with top manufacturers leading the way in packaging innovation and sustainability. These industry leaders are known for their cutting-edge technology, precision engineering, and commitment to quality, catering to diverse sectors such as beverages, pharmaceuticals, cosmetics, and household products. By offering customized, eco-friendly, and cost-effective solutions, India’s PET preform manufacturers are setting new benchmarks in the global packaging industry. This blog explores the top PET preform manufacturers in India, highlighting their capabilities, production standards, and contributions to transforming the future of packaging with efficiency, reliability, and environmental responsibility at the core.

India’s PET Preform Industry A Rapidly Growing Sector

The pet preform manufacturers india industry in India has seen remarkable growth over the last decade, fueled by rising demand in beverage, pharma, and FMCG sectors. Indian manufacturers have scaled their operations using world-class machinery, automation, and R&D to deliver preforms that meet international standards. This growth is not only driven by domestic needs but also by increasing exports to Asia, Africa, and the Middle East. The Indian government’s support for manufacturing and sustainability further enhances the sector’s competitiveness. With a focus on innovation, Indian PET preform producers are now seen as reliable global partners for premium-quality packaging solutions.

Technology-Driven Manufacturing for Precision and Consistency

Top PET preform manufacturers in India leverage state-of-the-art injection molding machines, robotics, and advanced quality control systems to ensure consistency in weight, clarity, and dimensional accuracy. Automation plays a significant role in reducing human error and enhancing productivity. These technological investments allow for faster turnaround times and flexible production lines capable of handling custom specifications. From high-speed manufacturing units to integrated software monitoring, India’s leading manufacturers are setting a new standard for precision. This technical edge not only ensures product reliability but also improves efficiency across supply chains, benefiting both domestic clients and international buyers.

Customization Capabilities to Serve Diverse Industries

One of the defining strengths of Indian PET preform manufacturers is their ability to offer tailor-made solutions. Whether it’s neck size, weight variation, or specific color and resin requirements, manufacturers provide complete customization to meet client specifications. This versatility caters to a wide range of applications, including water, carbonated beverages, edible oils, cosmetics, and pharmaceuticals. The flexibility to create preforms suitable for unique bottle shapes or specialized storage conditions gives Indian manufacturers a competitive advantage. This adaptability ensures that businesses can maintain brand consistency, improve product protection, and respond swiftly to changing market trends.

Strict Quality Control and Global Certifications

India’s top PET preform manufacturers adhere to rigorous quality control standards and hold international certifications such as ISO 9001, FSSC 22000, and GMP. These manufacturers conduct in-depth testing at every stage of production—from raw material assessment to final product inspection. Parameters such as color uniformity, acetaldehyde content, and dimensional precision are meticulously checked to ensure flawless output. With dedicated in-house laboratories and real-time monitoring systems, Indian producers guarantee high-quality and safe packaging materials. Their commitment to quality has earned them long-standing trust among global brands, especially those in the food and pharmaceutical sectors where compliance is non-negotiable.

Eco-Friendly Practices and Sustainable Production

Sustainability is becoming a core priority for PET preform manufacturers in India. Many top companies are adopting green practices such as energy-efficient machinery, waste recycling systems, and the use of recycled PET materials. Lightweighting initiatives help reduce plastic usage without compromising performance. These sustainable innovations not only lower environmental impact but also reduce production costs for clients. Additionally, manufacturers focus on eco-friendly packaging designs that support recycling and reduce landfill waste. By integrating environmental responsibility into their operations, India’s PET preform leaders are playing a vital role in shaping the future of sustainable packaging worldwide.

Cost-Effectiveness and Competitive Advantage

One of the key reasons global buyers are turning to India for PET preform solutions is cost-effectiveness. Indian manufacturers offer high-quality preforms at competitive prices, thanks to efficient production systems, affordable labor, and access to raw materials. Bulk manufacturing capabilities and strategic supply chain management further drive down operational costs. Despite lower pricing, these companies maintain strict quality standards and fast turnaround times, making them highly attractive for both small-scale and large-scale packaging needs. This value-for-money proposition allows Indian PET preform suppliers to compete successfully in both domestic and international markets without compromising on excellence.

Export Excellence and Global Market Reach

India’s leading PET preform manufacturers have significantly expanded their international footprint, supplying to over 50 countries across the globe. Backed by strong logistics networks, adherence to international regulations, and superior product quality, they serve clients in Europe, the Middle East, Africa, and Southeast Asia. Export-driven growth is also supported by government incentives and trade agreements that encourage Indian companies to explore new markets. By participating in global packaging expos and forging strategic partnerships, these manufacturers continuously boost their brand visibility. Their global presence affirms India’s rising status as a trusted, innovative, and scalable PET preform production hub.

Conclusion

The top PET preform manufacturers in India are redefining the standards of packaging through innovation, quality, and sustainability. With state-of-the-art technology, strict quality control, and a customer-centric approach, these industry leaders cater to a wide range of sectors both locally and globally. Their ability to offer customized, cost-effective, and eco-friendly solutions positions India as a key player in the global packaging market. As demand for reliable and sustainable packaging continues to grow, India’s PET preform manufacturers stand ready to meet future challenges and opportunities, delivering excellence at every stage of the production and supply chain.

0 notes

Text

Automatic Dicing Saw Market Growth Analysis 2025

The global Automatic Dicing Saw market was valued at US$ 567.4 million in 2024 and is projected to reach US$ 785.3 million by 2032, registering a CAGR of 4.6% from 2025 to 2032. This growth trajectory is attributed to the rapid expansion of the semiconductor industry, rising demand for consumer electronics, and technological advancements in wafer processing equipment. The increasing adoption of 5G technology, Internet of Things (IoT), and automotive electronics further contribute to the market's upward momentum. Historically, the market has demonstrated resilience, recovering strongly from disruptions like the COVID-19 pandemic and geopolitical trade tensions. The Asia-Pacific region, particularly China, Japan, and South Korea, continues to dominate the market, owing to its robust semiconductor fabrication ecosystem.

Automatic dicing saws are high-precision cutting tools widely used in semiconductor manufacturing and other high-tech industries. They perform the critical task of cutting silicon wafers, ceramics, and other materials into discrete, functional units. Controlled by advanced software systems, these machines ensure ultra-clean cuts, minimal kerf loss, and high throughput. Depending on the application, automatic dicing saws can handle a variety of materials and dimensions, making them indispensable in fabricating microelectronic components like integrated circuits (ICs), micro-electromechanical systems (MEMS), and optoelectronic devices. The integration of vision systems and robotic automation has further enhanced the efficiency, accuracy, and adaptability of modern dicing saws.

get free sample of this report at https://www.intelmarketresearch.com/manufacturing-and-construction/823/global-automatic-dicing-saw-2025-2032

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Booming Semiconductor Industry: The proliferation of smartphones, AI chips, and autonomous vehicle systems is accelerating demand for advanced semiconductor components, thereby driving the need for precise dicing solutions.

Rise in MEMS and IoT Devices: Devices like smart sensors and wearable tech rely on ultra-small components that require highly accurate dicing processes.

Automation and Smart Manufacturing: Industry 4.0 is pushing manufacturers toward automated, software-driven tools for increased efficiency and lower labor costs.

Restraints

High Initial Investment: The cost of fully automatic dicing systems and associated setup can be prohibitively high for small and mid-sized enterprises.

Technical Complexity: The operation and maintenance of these machines require skilled personnel, which can be a barrier in less developed regions.

Opportunities

Emerging Markets: Expanding semiconductor operations in countries like India, Vietnam, and Brazil offer significant growth potential.

Advancements in Vision Technology: Integration of AI and machine learning in vision systems can improve defect detection and operational precision.

Challenges

Supply Chain Disruptions: Trade tensions and raw material shortages can delay manufacturing and increase costs.

Regulatory and Compliance Issues: Adhering to international standards and environmental regulations can pose operational hurdles.

Regional Analysis

Asia-Pacific

The Asia-Pacific region dominates the Automatic Dicing Saw market, led by powerhouses like China, Japan, South Korea, and Taiwan. These countries are home to major semiconductor foundries and OEMs. Japan, for example, hosts leading companies like DISCO Corporation and Tokyo Seimitsu, while China benefits from substantial government-backed semiconductor initiatives.

North America

The U.S. continues to play a critical role due to its innovation-led tech sector and presence of companies like Plasma Therm. The demand for advanced packaging solutions in AI and aerospace sectors propels the market.

Europe

Germany and the UK are pivotal due to their strong industrial base and automotive electronics sector. Companies like Besi from the Netherlands contribute significantly to regional growth.

Rest of the World

Countries in Latin America and the Middle East are gradually increasing their footprint in microelectronics, offering new avenues for market expansion.

Competitor Analysis (in brief)

The Automatic Dicing Saw market features a mix of established players and emerging innovators. DISCO Corporation and Tokyo Seimitsu lead the market with comprehensive product portfolios and global distribution networks. Companies like ADT Corporation, Synova SA, and Kulicke & Soffa bring niche technologies and specialized offerings. Han’s Laser and CETC cater predominantly to the growing Chinese market, while Loadpoint Ltd. and Besi focus on European customers. Strategic partnerships, R&D investments, and product differentiation are key strategies employed to stay competitive.

Global Automatic Dicing Saw Market: Market Segmentation Analysis

This report provides a deep insight into the global Automatic Dicing Saw market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Automatic Dicing Saw Market. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Automatic Dicing Saw market in any manner.

Market Segmentation (by Type)

Fully Automatic Dicing Saws

Semi-Automatic Dicing Saws

Market Segmentation (by Cagetgory)

Single Spindel

Twin Spindel

Market Segmentation (by Dicing Blade)

Nickel-Bond Dicing Blades

Resin-Bond Dicing Blades

Metal Sintered Dicing Blades