#Mobile Remittance Service Market Growth

Text

Mobile Remittance Service Market: Forthcoming Trends and Share Analysis by 2030

Global Mobile Remittance Service Market size is expected to grow from USD 22211.01 Million in 2023 to USD 85191.62 Million by 2032, at a CAGR of 16.11% during the forecast period (2024–2032)

You can use a mobile phone to send and receive money electronically with a mobile remittance service. It's an easy and accessible alternative to going in person to a bank or money transfer agency to transfer money. Bill payments and peer-to-peer transactions are made easier with the usage of mobile remittance services, which are available both domestically and internationally. They provide consumers with freedom in managing their finances by meeting the increasing demand for cross-border remittances and facilitating transactions between conventional bank accounts and mobile wallets. The market for conventional bank accounts is also present.

Financial inclusion, cost effectiveness, speed, and convenience are all provided by mobile remittance services. They enable customers to start transactions whenever and wherever they choose by doing away with the necessity for actual trips to banks or remittance centers. They are perfect for urgent financial situations because they offer transfers that happen almost instantly. Financial inclusion for individuals without simple access to traditional banking is further enhanced by the fact that digital transactions frequently have lower fees than traditional methods.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://introspectivemarketresearch.com/request/4013

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Leading players involved in the Mobile Remittance Service Market include:

Mobetize Corp. (U.S.)

MoneyGram (U.S.)

Remitly (U.S.)

Regalii (U.S.)

Flywire (U.S.)

PayPal. (U.S.)

Ria Financial Services (U.S)

Western Union Holdings, Inc. (U.S)

Currency Cloud (UK)

Azimo (UK)

WorldRemit (UK)

TransferWise (UK)

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

If You Have Any Query Mobile Remittance Service Market Report, Visit:

https://introspectivemarketresearch.com/inquiry/4013

Segmentation of Mobile Remittance Service Market:

By Type

Banks

Money Transfer Operators

By Application

Migrant Labor Workforce

Low-income Households

Small Businesses

An in-depth study of the Mobile Remittance Service industry for the years 2024–2032 is provided in the latest research. North America, Europe, Asia-Pacific, South America, the Middle East, and Africa are only some of the regions included in the report's segmented and regional analyses. The research also includes key insights including market trends and potential opportunities based on these major insights. All these quantitative data, such as market size and revenue forecasts, and qualitative data, such as customers' values, needs, and buying inclinations, are integral parts of any thorough market analysis.

Market Segment by Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

Key Benefits of Mobile Remittance Service Market Research:

Research Report covers the Industry drivers, restraints, opportunities and challenges

Competitive landscape & strategies of leading key players

Potential & niche segments and regional analysis exhibiting promising growth covered in the study

Recent industry trends and market developments

Research provides historical, current, and projected market size & share, in terms of value

Market intelligence to enable effective decision making

Growth opportunities and trend analysis

Covid-19 Impact analysis and analysis to Mobile Remittance Service market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=4013

About us:

Introspective Market Research (introspectivemarketresearch.com) is a visionary research consulting firm dedicated to assist our clients grow and have a successful impact on the market. Our team at IMR is ready to assist our clients flourish their business by offering strategies to gain success and monopoly in their respective fields. We are a global market research company, specialized in using big data and advanced analytics to show the bigger picture of the market trends. We help our clients to think differently and build better tomorrow for all of us. We are a technology-driven research company, we analyze extremely large sets of data to discover deeper insights and provide conclusive consulting. We not only provide intelligence solutions, but we help our clients in how they can achieve their goals.

Contact us:

Introspective Market Research

3001 S King Drive,

Chicago, Illinois

60616 USA

Ph no: +1 773 382 1049

Email: [email protected]

#Mobile Remittance Service#Mobile Remittance Service Market#Mobile Remittance Service Market Size#Mobile Remittance Service Market Share#Mobile Remittance Service Market Growth#Mobile Remittance Service Market Trend#Mobile Remittance Service Market segment#Mobile Remittance Service Market Opportunity#Mobile Remittance Service Market Analysis 2023

0 notes

Text

In a bold initiative aimed at enhancing the financial landscape of Pakistan, Visa has set its sights on exponentially increasing the acceptance of digital payments within the country. This strategic plan, articulated by Visa's general manager for Pakistan, North Africa, and Levant, Leila Serhan, seeks a tenfold expansion over the next three years through a partnership with 1Link, the largest payment service provider in Pakistan. This collaborative effort is not just about technology; it aims to empower businesses, streamlining transactions, and improving financial inclusivity for a large segment of the population.

Pakistan is at a critical juncture, grappling with a significant challenge in its banking landscape. Despite a population of approximately 240 million, only 60% of the 137 million adults have access to banking services. This presents both a challenge and an opportunity for Visa and its partners. With the introduction of innovative solutions such as turning smartphones into payment devices and the integration of widely accepted payment methods like QR codes and contactless card tapping, the potential for transforming the payments ecosystem in Pakistan is immense.

To achieve these ambitious goals, Visa plans to invest heavily in developing digital payment infrastructure. This investment not only focuses on making digital transactions more affordable and user-friendly but also addresses the needs of smaller merchants who often struggle with high transaction fees and complex setups. By lowering barriers to entry for digital payments, Visa aims to encourage widespread adoption among businesses of all sizes.

The partnership with 1Link is particularly critical in enhancing the remittance process, which plays a vital role in Pakistan’s economy. With remittances contributing significantly to the nation’s GDP, improving the mechanisms for these transactions can have far-reaching effects. The collaboration involves allowing 1Link's PayPak cards to be utilized on Visa’s online platforms, offering customers more choices and simplified processes. This strategic move is noteworthy as it signifies a cooperative approach between two competitors working towards a common goal of financial inclusion.

Moreover, this initiative aligns with Pakistan’s ongoing economic reforms, particularly following the $7 billion bailout from the International Monetary Fund (IMF). In an environment where digital payments are becoming increasingly central to economic recovery and growth, Visa's commitment to supporting these reforms showcases the company’s foresight in recognizing the importance of digital payments in modern economies.

Visa’s strategy is underpinned by a deep understanding of the current market dynamics in Pakistan. The company is not merely pushing technology for technology's sake; instead, it is tailoring its offerings to meet the specific needs of the Pakistani consumer and business owner. For instance, the ability to facilitate various payment methods through established networks and technological innovations is critical in a country where many people remain unbanked.

The integration of digital payment solutions can also help ensure that businesses operate more efficiently. With mobile payment options becoming more popular, particularly in urban areas, businesses that adopt these technologies stand to benefit significantly. Not only do they gain access to a broader customer base, but they also enhance their operational efficiencies through automated processes that reduce cash handling and the associated risks.

As Visa moves forward with this initiative, it hopes to foster a more secure payment environment. Enhanced security features that accompany digital transactions can help build trust among users, encouraging them to switch from cash to digital solutions. The cooperation with 1Link adds an extra layer of reliability to this goal, as both entities are focused on ensuring that transactions remain secure and compliant with international standards.

Digital transformation is not just about improving processes; it's about creating a more inclusive financial system that can benefit everyone, especially those who have previously been left out. Visa's significant investment in infrastructure, combined with innovative solutions, has the potential to reshape the financial landscape in Pakistan in ways that benefit consumers and businesses alike.

In conclusion, Visa's partnership with 1Link marks a pivotal moment for digital payments in Pakistan. As the country stands on the brink of a technological revolution in finance, it is essential to support this transition effectively. The ambitious plan to expand digital payment acceptance is not just about Visa; it’s about empowering millions of Pakistanis and positioning the economy for sustainable growth in the years to come.

#News#UzbekistanPakistanITCollaborationTelecommunicationsDigitalInnovation#digitalpayments#financialinclusion#fintech#Visa

0 notes

Text

Open Banking Market is Predicted to Grow At More Than 22% CAGR till 2032

Open Banking Market size is estimated to be valued at USD 130.2 Bn till 2032. The rising integration with digital currency platforms to enable seamless transactions between fiat currencies and cryptocurrencies will influence the industry growth. The implementation of robust security measures, such as encryption, multi-factor authentication, and real-time monitoring, has grown critical for protecting sensitive financial data in open banking. Of late, leading financial institutions and fintech firms are exploring subscription-based models for open banking services to offer premium features and value-added services through tiered pricing plans.

Request for Sample Copy report @ https://www.gminsights.com/request-sample/detail/6210

Open banking market share from the digital currencies financial services segment is expected to exponentially expand between 2024 and 2032. By directly linking digital wallets to their banking systems, open banking streamlines the acceptance of digital currency payments by merchants. This integration lowers the hurdles for businesses eager to embrace cryptocurrencies. Furthermore, it enables connections with global financial institutions, simplifying cross-border transactions and allowing users to effortlessly send and receive payments in various currencies worldwide.

The on-premise deployment model segment is expected to account for considerable share of the open banking industry by 2032. Financial institutions using on-premise open banking solutions can fully control sensitive customer data. As concerns about data breaches and cyberattacks grow, numerous banks are opting to manage data in-house instead of depending on third-party cloud services. On-premise deployments further allow banks to customize their open banking infrastructure as per their specific needs. This flexibility is particularly important for large financial institutions with complex IT environments that require bespoke solutions.

Request for customization this report @ https://www.gminsights.com/roc/6210

Asia Pacific open banking industry size is anticipated to reach a significant share by 2032. This is propelled by the surge in cross-border open banking services, particularly in areas, such as remittances and international payments. Countries like India, Indonesia, and Vietnam are witnessing a swift expansion of open banking. With a vast unbanked populace and a strong mobile presence, these nations present lucrative prospects for open banking solutions. The proliferation of digital payments in China and India will also influence regional market growth.

Partial chapters of report table of contents (TOC):

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Base estimates & calculations

1.3.1 Base year calculation

1.3.2 Key trends for market estimation

1.4 Forecast model

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 API platforms and gateway providers

3.2.2 Security solutions providers

3.2.3 RegTech providers

3.2.4 End user

3.3 Profit margin analysis

3.4 Technology & innovation landscape

3.5 Patent analysis

3.6 Key news & initiatives

3.7 Regulatory landscape

3.8 Impact forces

3.8.1 Growth drivers

3.8.1.1 Increase in adoption of digital banking for convenience and accessibility

3.8.1.2 Technological advancements in big data analytics, artificial intelligence (AI), and APIs

3.8.1.3 Government initiatives and regulatory support to enhance financial transparency

3.8.1.4 Consumer demand for personalized services

3.8.2 Industry pitfalls & challenges

3.8.2.1 Security and privacy concerns

3.8.2.2 Lack of consumer trust and adoption

3.9 Growth potential analysis

3.10 Porter’s analysis

3.11 PESTEL analysis

About Global Market Insights:

Global Market Insights, Inc., headquartered in Delaware, U.S., is a global market research and consulting service provider; offering syndicated and custom research reports along with growth consulting services. Our business intelligence and industry research reports offer clients with penetrative insights and actionable market data specially designed and presented to aid strategic decision making. These exhaustive reports are designed via a proprietary research methodology and are available for key industries such as chemicals, advanced materials, technology, renewable energy and biotechnology.

Contact us:

Aashit Tiwari

Corporate Sales, USA

Global Market Insights Inc.

Toll Free: +1-888-689-0688

USA: +1-302-846-7766

Europe: +44-742-759-8484

APAC: +65-3129-7718

Email: [email protected]

0 notes

Text

The Future of Financial Services: Embracing Digital Transformation

In an era characterized by rapid technological advancements, the financial services industry stands at the forefront of a significant transformation. The fusion of cutting-edge technology with traditional financial practices is reshaping the landscape, offering unprecedented opportunities for innovation, efficiency, and customer engagement. This digital transformation is not merely a trend but a fundamental shift that will define the future of financial services.

The Rise of Fintech

Financial technology, or fintech, has emerged as a game-changer in the industry. Startups and established firms alike are leveraging technology to create innovative solutions that cater to the evolving needs of consumers. Mobile banking apps, peer-to-peer payment platforms, robo-advisors, and blockchain technology are just a few examples of how fintech is revolutionizing the way we manage money.

The convenience and accessibility of these services have led to widespread adoption, particularly among younger, tech-savvy consumers. Mobile banking, for instance, allows users to perform transactions, monitor their accounts, and even apply for loans from the comfort of their homes. This shift towards digital solutions is driving financial institutions to rethink their strategies and invest heavily in technology.

Artificial Intelligence and Automation

Artificial Intelligence (AI) and automation are playing pivotal roles in enhancing operational efficiency and customer experience in financial services. AI-powered chatbots and virtual assistants are now common in customer service, providing instant responses and personalized assistance. These tools not only improve customer satisfaction but also free up human resources for more complex tasks.

In addition to customer service, AI is being used for risk management, fraud detection, and investment analysis. Machine learning algorithms can analyze vast amounts of data to identify patterns and trends, enabling more accurate predictions and informed decision-making. This data-driven approach is crucial in today’s fast-paced financial markets, where timely and accurate information can make all the difference.

Blockchain and Cryptocurrency

Blockchain technology and cryptocurrencies are other key components of the digital transformation in financial services. Blockchain offers a decentralized and secure way of recording transactions, reducing the need for intermediaries and increasing transparency. This technology has the potential to revolutionize various aspects of the financial industry, from payments and remittances to trade finance and regulatory compliance.

Cryptocurrencies, while still relatively new, are gaining traction as alternative investment assets. Bitcoin, Ethereum, and other digital currencies are being embraced by both individual investors and institutional players. The growing acceptance of cryptocurrencies highlights the need for financial institutions to adapt and develop new services that cater to this emerging market.

Regulatory Challenges and Opportunities

As financial services copywriter undergo digital transformation, regulatory frameworks must evolve to address new risks and challenges. Cybersecurity, data privacy, and compliance are critical issues that require robust regulatory oversight. Financial institutions must work closely with regulators to ensure that innovation does not compromise the stability and integrity of the financial system.

At the same time, regulatory changes present opportunities for growth and innovation. Regulatory sandboxes, for example, allow fintech companies to test new products and services in a controlled environment, fostering experimentation and collaboration. By striking a balance between innovation and regulation, the financial services industry can continue to thrive in the digital age.

The Path Forward

The digital transformation of copywriting for financial services is an ongoing journey that requires continuous adaptation and investment. Financial institutions must embrace a culture of innovation, prioritize customer-centric solutions, and stay ahead of technological advancements. Collaboration between traditional banks, fintech startups, and regulatory bodies will be crucial in shaping a resilient and dynamic financial ecosystem.

In conclusion, the future of financial services lies in the successful integration of technology with traditional practices. By embracing digital transformation, financial institutions can enhance efficiency, improve customer experience, and drive sustainable growth. The journey ahead is challenging, but the rewards are immense for those who dare to innovate and lead the way.

0 notes

Text

Impact of Crypto Token Development on the Global Financial System

The emergence of cryptocurrencies has created seismic shifts in the landscape of the global financial system. The proliferation of crypto tokens has also led to new investment vehicles and financial products. Institutional investors are increasingly seeking exposure to cryptocurrencies, driving the development of exchange-traded funds (ETFs), futures, and options based on digital assets, We will explore the impact of crypto token development on financial systems, institutions, and the broader economy.

What is crypto token development?

Crypto token development refers to creating digital assets (tokens) that operate on a blockchain technology platform. These tokens can represent various forms of value or utility and serve multiple purposes within the ecosystem wherein the blockchain developers build on it.

Utility Tokens: Provide users access to a product or service within a specific platform. For example, tokens are used for payment within a decentralized application (dApp) or to access certain features.

Security Tokens: represent ownership of an underlying asset, such as shares in a company or real estate. They are subject to securities regulations and provide legal rights to investors.

Stablecoins: These are pegged to traditional currencies (like the US dollar) or other assets to minimize volatility and provide a stable store of value. They facilitate transactions and serve as a medium of exchange.

Non-Fungible Tokens (NFTs): These tokens represent unique items or assets, often used to verify ownership of digital art, collectibles, or real-world assets wherein BSEtec has developed Mint trades – An NFT marketplace script.

Governance Tokens: These give holders the right to participate in the decision-making process of a decentralized platform, allowing them to propose and vote on changes to the protocol.

What are the impacts of Crypto token development?

1. Decentralization and Financial Inclusion

One of the most significant impacts of crypto token development is the push towards decentralization. Intermediaries, high fees, and geographic limitations often plague traditional financial systems. Cryptocurrencies operate on blockchain technology, allowing peer-to-peer transactions without centralized authority. This decentralization can empower individuals in underbanked regions, granting them access to financial services through mobile devices.

Crypto tokens can provide microloans, facilitate remittances, and enable people to save and invest, fostering financial inclusion on a global scale. As more individuals participate in the financial system, the potential for economic growth increases, particularly in developing economies.

2. Innovation in Payment Systems

The development of crypto tokens has given rise to various payment solutions that challenge traditional payment systems. Cryptocurrencies offer faster, cheaper, and borderless transactions than conventional banking. As businesses and consumers adopt crypto for everyday transactions, we are witnessing an evolution in payment infrastructure that can reduce reliance on traditional banks and payment processors. we implement cryptocurrency rather than fiat currencies for various businesses and enterprises in global commerce.

3. Tokenization of Assets

Tokenization is another revolutionary impact of crypto token development. BSEtec strives to create digital representations of real-world assets, such as real estate, art, and commodities, tokenization can democratize access to investment opportunities. Investors can buy fractions of assets, lowering the barriers to entry and increasing liquidity in traditionally illiquid markets.

This new model for asset ownership also enhances transparency and security through blockchain technology, allowing for real-time verification of ownership and transaction history

4. Regulatory Challenges and Responses

The rise of decentralized finance (DeFi) platforms further complicates regulatory efforts, as they operate without central authorities. As regulators adapt to these new realities, there is a potential for innovative frameworks that both foster innovation and protect users. Clear regulations could enhance trust in cryptocurrencies, attract institutional investments, and legitimize the industry.

5. Implications for Central Banks and Monetary Policy

The development of cryptocurrencies and stablecoins is prompting central banks to rethink their approaches to monetary policy. CBDCs, a government-backed digital currency, are being explored by various nations to modernize financial systems and retain control over economic policy in the face of decentralized digital currencies.

CBDCs could enhance transaction efficiency, lower costs, and provide governments with better tools for managing economic stability. However, they also raise questions about privacy, surveillance, and the potential for increased centralization in an era that champions decentralization.

Additionally, the rise of decentralized finance (DeFi) is creating decentralized alternatives to traditional financial products, from lending and borrowing to insurance solutions. This innovation is reshaping how people interact with money and investments, moving toward a more democratized financial system.

Thus, As we navigate this evolving landscape, a collaboration between technologists, regulators, and financial institutions will be crucial in harnessing the power of crypto tokens to create a more equitable and efficient financial system for all.

As we continue to observe these trends, it is essential for stakeholders – be they policymakers, investors, or consumers – to stay informed and adaptable, ensuring responsible and positive integration of crypto technologies into our financial lives with consideration of blockchain development companies in India like BSEtec.

0 notes

Text

Achieve Your Dreams: Trusted Job Placement Agency for Estonia from Pakistan

Introduction:

In an era of global connectivity and career mobility, Manpower Recruitment Agency emerges as a trailblazer, particularly for those seeking employment opportunities in Estonia. Renowned as Pakistan’s foremost ISO-certified recruitment agency, Falisha Manpower excels in bridging the gap between Pakistani talent and international job markets. With License # 4035/RWP and official endorsement from the Ministry of Overseas Pakistanis & Human Resource Development, the agency stands as a beacon of trust and reliability.

Bridging Pakistan and Estonia:

Falisha Manpower Recruitment Agency specializes in creating pathways for Pakistani professionals to thrive in Estonia. The agency’s deep understanding of both markets and extensive network enable it to cater to a wide range of industries, including IT, engineering, healthcare, hospitality, and more. By matching the skills and aspirations of Pakistani job seekers with the needs of Estonian employers, Falisha Manpower ensures mutually beneficial outcomes.

ISO Certification: A Commitment to Excellence:

The ISO certification held by Falisha Manpower is a testament to its unwavering commitment to quality and excellence. This certification signifies that the agency operates with a robust quality management system, ensuring consistency, efficiency, and professionalism in all its recruitment processes. For job seekers and employers alike, the ISO certification provides confidence in the agency’s dedication to delivering superior services.

Official Endorsement and Credibility:

The endorsement by the Ministry of Overseas Pakistanis & Human Resource Development further solidifies Falisha Manpower’s credibility. This official recognition underscores the agency’s adherence to governmental regulations and ethical standards. For job seekers, this endorsement provides assurance of the legitimacy and reliability of the opportunities presented by Falisha Manpower.

Comprehensive Support for Job Seekers:

Falisha Manpower offers a comprehensive suite of services designed to support job seekers at every step of their journey. From initial career counseling and consultation to resume building, interview preparation, and visa assistance, the agency provides holistic support. This all-encompassing approach helps candidates navigate the complexities of the international job market with confidence and ease.

Empowering Pakistani Professionals:

Best Recruitment Agency In Pakistan For Estonia, Falisha Manpower plays a crucial role in empowering Pakistani professionals to build successful international careers. The agency’s efforts not only contribute to the personal and professional growth of individuals but also enhance the economic development of Pakistan. Remittances from overseas workers are a vital component of Pakistan’s economy, and Falisha Manpower’s services help maximize this potential.

A Vision for the Future:

Falisha Manpower Recruitment Agency is dedicated to expanding its reach and setting new benchmarks in the recruitment industry. The agency aims to leverage technological advancements and innovative practices to further enhance its services. By staying ahead of industry trends and continuously improving its processes, Falisha Manpower strives to maintain its position as Pakistan’s leading recruitment agency for jobs in Estonia and beyond.

Conclusion:

Falisha Manpower Recruitment Agency exemplifies excellence in connecting Pakistani talent with global opportunities, particularly in Estonia. With its ISO certification, official endorsement, and comprehensive range of services, the agency stands as a beacon of trust and reliability in the recruitment landscape. For Pakistani professionals aspiring to build successful careers abroad, Falisha Manpower is the go-to partner, providing the expertise, support, and opportunities needed to achieve their dreams.

Estonia awaits, and with Falisha Manpower Recruitment Agency, Pakistani professionals are well-equipped to seize the opportunities and build a brighter future on the global stage. Achieve your dreams with the trusted job placement services of Falisha Manpower.

0 notes

Text

The Impact of Cryptocurrency on Global Remittances

Remittances -- or money sent home by individuals working and living abroad -- are a lifeline for millions around the world. They account for roughly a quarter of GDP in countries like El Salvador and bring financial inclusion to underserved communities. But remittance fees and processing times are often unnecessarily high and cumbersome. The emergence of cryptocurrency as an alternative to traditional money transfers is radically changing this landscape.

Cryptocurrency uses blockchain technology to streamline money transfers. This decentralized and digital system provides transparency by providing an immutable record of every transaction, and eliminates the need for tech ogle intermediaries. It also offers a much lower cost for cross-border payments and reduces exchange rate volatility. The remittance industry is one of the most significant applications for cryptocurrency and has already seen remarkable growth.

However, a number of barriers remain for widespread adoption of cryptocurrency for remittances. First, there are regulatory hurdles. Different countries have varying regulations on cryptocurrencies, with some imposing strict restrictions and bans. Additionally, price volatility is a major concern for people who rely on remittances to meet their daily needs. Stablecoins, which are backed by fiat assets, can mitigate this issue.

Additionally, many people who send remittances have limited access to banking services. According to a World Bank report, nearly 1.4 billion adults worldwide are still bereft of this basic service. This is a large percentage of the population, including those who live in rural areas and are female.

Luckily, new entrants to the technology fact cryptocurrency market are tackling these obstacles by providing low-cost and efficient cryptocurrency remittance solutions. They are focusing on the most underserved markets and using innovative technology to reduce costs and increase accessibility for these populations. One example is Leaf Global Fintech, which enables people to transfer money home using only their mobile phone. Its services are available in Kenya, Rwanda, and Uganda, and the company partners with all of the major mobile money providers, enabling users to cash out their funds into any phone number, even on networks that don’t normally support remittances.

The remittance market is an important area for cryptocurrency because it demonstrates the potential for blockchain to dramatically improve efficiency, reduce costs, and broaden access. This paper identifies opportunities for further research into the transformative impact of cryptocurrency on remittances, which is an urgent need in the face of rising financial inclusion challenges. As cryptocurrency technology continues to evolve, it has the potential to revolutionize remittance services by offering improved efficiency, reduced costs, and broadened access for millions of people around the world. More importantly, it has the potential to transform people’s lives by connecting them across borders and bringing financial freedom and inclusion to underserved populations. For this to happen, there is an urgent need for broader adoption and regulatory support.

1 note

·

View note

Text

Market research and financial services in the Philippines

Market research/FS

Market research and financial services in the Philippines are advancing rapidly, supported by a population of over 100 million people and increasing internet connectivity. The financial sector is embracing digital transformation, with a growing adoption of mobile banking, digital wallets, and online payment solutions. Key players include major banks such as BDO, Metrobank, and BPI, alongside a burgeoning fintech ecosystem offering diverse services like remittances and mobile money. Market research in the Philippines focuses on understanding consumer preferences, behaviors, and regulatory dynamics, crucial for companies navigating this dynamic and competitive market. Overall, the Philippines offers substantial opportunities for growth and innovation in financial services.

0 notes

Text

Navigating the Future of Cross-Border Payments: The Fintech Revolution

In an era where globalization defines business dynamics, the importance of seamless, efficient, and secure cross-border payments cannot be overstated. Fintech companies are at the forefront of this revolution, transforming the landscape of international transactions. Here’s how they’re reshaping the future of cross-border payments:

Speed and Efficiency: Traditional banking systems often lead to delays, with transactions taking days to process. Fintech companies, leveraging cutting-edge technologies like blockchain and artificial intelligence, are drastically reducing transaction times. Real-time payments are no longer a distant dream but a reality for businesses and individuals alike.

Cost Reduction: One of the significant pain points in cross-border transactions has been the high cost, driven by bank fees and unfavorable exchange rates. Fintech solutions offer a more competitive edge, significantly lowering transaction fees and providing more transparent exchange rates. This cost efficiency is crucial for businesses operating on thin margins and for remittances, where every penny counts.

Enhanced Security: Security is paramount in financial transactions. Fintech companies are employing advanced encryption methods and robust authentication processes to ensure that cross-border payments are secure from fraud and cyber threats. Blockchain technology, with its immutable ledger, offers an additional layer of security, making transactions tamper-proof.

Regulatory Compliance: Navigating the regulatory landscape of cross-border payments can be complex. Fintech companies are innovating with compliance solutions that simplify adherence to international regulations. Through automated compliance checks and KYC (Know Your Customer) processes, they ensure that transactions meet all legal requirements, reducing the risk of penalties and facilitating smoother operations.

Inclusivity and Accessibility: Fintech solutions are bridging the gap for underserved markets, providing financial services to those without access to traditional banking. By leveraging mobile technology, they are bringing cross-border payment capabilities to remote and rural areas, promoting financial inclusion and driving economic growth.

The future of cross-border payments lies in the hands of fintech innovators. As they continue to break down barriers, they are not just making transactions faster and cheaper but are also fostering a more connected and inclusive global economy. For businesses and individuals engaged in international transactions, the message is clear:embrace fintech solutions to stay ahead in a rapidly evolving financial landscape.

0 notes

Text

Revolutionizing The Digital Payments In Pakistan

Revolutionizing The Digital Payments In Pakistan

In the heart of Pakistan's bustling cities and vibrant markets, a digital revolution is underway, transforming the way transactions are conducted, businesses operate, and individuals manage their finances. As the world embraces the convenience and efficiency of digital payments, Pakistan stands at the forefront of this technological evolution, poised to harness the transformative power of digital finance to drive economic growth, financial inclusion, and innovation.

Embracing Digital Transformation:

1. Mobile Wallets and Apps:

The proliferation of smartphones and the rise of mobile internet connectivity have paved the way for the widespread adoption of mobile wallets and payment apps. From urban centers to rural villages, individuals can now securely send and receive money, pay bills, and make purchases with the tap of a finger, revolutionizing everyday transactions.

2. Fintech Innovation:

The burgeoning fintech ecosystem in Pakistan is driving innovation in digital payments, with startups and established players alike introducing innovative solutions to address the diverse needs of consumers and businesses. From peer-to-peer lending platforms to digital remittance services, fintech companies are democratizing access to financial services and empowering individuals to take control of their financial futures.

3. Government Initiatives:

The Pakistani government's commitment to fostering a digital economy has catalyzed the adoption of digital payments across the country. Initiatives such as the National Payment Systems Strategy and the Digital Pakistan Vision aim to create an enabling environment for digital innovation, promoting financial literacy, and enhancing the resilience and efficiency of the country's financial infrastructure.

4. Consumer Adoption:

Driven by convenience, security, and accessibility, consumers in Pakistan are increasingly embracing digital payments as their preferred mode of transaction. Whether it's ordering groceries online, paying utility bills, or transferring money to loved ones, digital payments offer unparalleled convenience and peace of mind in an increasingly digital world.

Navigating the Future:

As Pakistan charts a course towards a digital future, the revolution in digital payments holds the promise of driving inclusive economic growth, empowering marginalized communities, and fostering a culture of innovation and entrepreneurship. However, challenges such as cybersecurity, regulatory compliance, and digital literacy must be addressed to ensure the equitable and sustainable development of Pakistan's digital economy.

For a deeper exploration of the transformative impact of digital payments in Pakistan and insights into the future of financial innovation, visit FutureTech Words. Join us on the journey to revolutionize the way Pakistan pays!

0 notes

Text

Revolutionizing Remittances: Cryptocurrency's Role in Faster, Cheaper Cross-Border Transactions

In the era of globalization, the significance of quick and cost-effective cross-border transactions has never been more pronounced. The traditional banking system, often bogged down by its own red tape and geographical constraints, has been a necessary but cumbersome mechanism for these transactions. This is especially true for remittances, where workers send money across borders back to their families. However, with the advent of cryptocurrencies, there is a potential revolution underway in how these remittances are conducted.

Understanding the Remittance Market

Remittances represent a significant financial flow among countries, particularly from developed to developing regions. For many families in these regions, remittances are a lifeline that supports their day-to-day living. Traditional methods of sending remittances typically involve banks or specialized remittance services. These methods, while reliable, come with a set of challenges including high transaction fees, variable exchange rates, and slower processing times which can stretch to a few days. Visit https://cryptograb.io/

Cryptocurrency: A New Hope

Cryptocurrency offers an innovative alternative to traditional banking systems for remittances. By leveraging blockchain technology, cryptocurrency provides a decentralized platform that is not owned by any single entity. This technology supports the transfer of digital currencies across a network of computers globally, without the need for intermediaries. The result is a system where cross-border payments can be faster and cheaper compared to conventional methods.

Speed of Transactions

One of the most significant advantages of using cryptocurrencies for remittances is the speed of transactions. Transfers can be completed in a matter of minutes, regardless of the location of the sender and receiver. This is a considerable improvement over traditional methods, where transfers can take several days.

Lower Transaction Costs

Cryptocurrencies reduce the cost of transactions significantly. Traditional cross-border transactions involve various fees, including transfer fees, exchange rate margins, and sometimes hidden charges. Cryptocurrencies minimize these costs because the transactions do not require intermediaries like banks or remittance companies. The direct transfer between sender and receiver via the blockchain eliminates many of the overhead costs associated with traditional methods.

Accessibility

Cryptocurrencies can be particularly beneficial in regions with underdeveloped financial infrastructure. For populations that are unbanked or underbanked, cryptocurrencies offer an accessible way to receive money directly and securely, needing nothing more than a mobile device and an internet connection. This can empower individuals by giving them direct control over their finances without the necessity of a bank account.

Challenges and Considerations

Despite the advantages, the adoption of cryptocurrencies in remittance services does face challenges. The primary concern is the volatility of cryptocurrencies. The value of digital currencies can fluctuate wildly within very short periods, which can add a layer of risk to both senders and recipients. Moreover, there is also the issue of regulatory challenges. Cryptocurrencies operate in a relatively grey area of the law in many countries, and regulatory clarity is still evolving.

Regulatory Environment

For cryptocurrencies to become a mainstream tool for remittances, supportive regulatory frameworks will need to be established. These regulations will need to address concerns related to security, money laundering, and protection against fraud while also providing enough room for innovation and growth in the use of digital currencies.

Security Concerns

While blockchain itself is secure, cryptocurrency exchanges and wallets are vulnerable to hacks. Ensuring the security of these platforms is crucial for building trust among users. Education around securing digital wallets and awareness about phishing and other forms of cyber threats are necessary to protect users' assets.

The Future Outlook

The potential of cryptocurrencies to revolutionize the remittance industry is immense. As technology matures and more people become digitally literate, the adoption of cryptocurrencies could see a significant rise. This will depend heavily on improvements in technology, regulatory support, and the stability of digital currencies.

In conclusion, while cryptocurrencies present a promising solution to the challenges of traditional remittance methods, their success will hinge on overcoming the issues of volatility, regulatory uncertainties, and security risks. If these challenges can be addressed, cryptocurrencies could very well redefine the landscape of cross-border transactions, making them faster, cheaper, and more accessible to a global population.

0 notes

Text

Exploring the Top Fintech Companies in Morocco

Morocco, a country known for its rich cultural heritage and strategic geographical location, has been making significant strides in the fintech sector. The fintech industry in Morocco is flourishing, driven by a blend of innovative startups and established financial institutions. These companies are leveraging technology to enhance financial services, promote financial inclusion, and drive economic growth. In this blog, we'll explore some of the top fintech companies in Morocco that are leading the way in this dynamic sector.

1. CIH Bank

CIH Bank is a leading financial institution in Morocco that has embraced digital transformation to provide a wide range of fintech solutions. The bank offers innovative mobile banking services, digital wallets, and online payment solutions. CIH Bank’s commitment to digital innovation has made it a key player in Morocco's fintech landscape.

2. Inwi Money

Inwi Money is a pioneering fintech company in Morocco, offering a mobile payment service that allows users to make transactions directly from their mobile phones. Launched by the telecommunications company Inwi, Inwi Money provides services such as money transfers, bill payments, and online purchases. This service is particularly beneficial in promoting financial inclusion, especially in rural areas.

3. Payit

Payit is a Moroccan fintech startup that focuses on providing secure and convenient payment solutions. The company offers a digital wallet that enables users to make payments, transfer money, and manage their finances through a mobile app. Payit’s user-friendly interface and robust security features have made it a popular choice among Moroccan consumers.

4. Hps Worldwide

Hps Worldwide is a global payment solutions provider headquartered in Morocco. The company specializes in designing and developing innovative payment systems for financial institutions, processors, and national switches. Hps Worldwide’s solutions are used in over 90 countries, making it a significant player in the global fintech market.

5. YallaXash

YallaXash is a fintech startup that provides remittance services to the Moroccan diaspora. The platform allows users to send money to Morocco quickly and securely. YallaXash’s competitive exchange rates and low transaction fees have made it a preferred choice for Moroccans living abroad who want to support their families back home.

6. Wafacash

Wafacash, a subsidiary of Attijariwafa Bank, is a leading fintech company specializing in money transfer and payment solutions. The company offers a range of services including domestic and international money transfers, bill payments, and mobile banking. Wafacash’s extensive network and reliable services have earned it a strong reputation in Morocco and beyond.

7. M2T (Maroc Traitement de Transactions)

M2T is a Moroccan fintech company that provides electronic payment processing solutions. The company offers a wide range of services including payment gateways, e-commerce solutions, and mobile payment systems. M2T’s innovative approach to electronic payments has made it a key player in the Moroccan fintech ecosystem.

8. WeCasablanca

WeCasablanca is a fintech startup that focuses on providing smart city solutions, including digital payments and financial services. The company aims to enhance the urban experience for residents and visitors through innovative fintech solutions. WeCasablanca’s initiatives are part of a broader effort to position Casablanca as a leading smart city in Africa.

Conclusion

Morocco's fintech sector is rapidly evolving, driven by a mix of innovative startups and established financial institutions. These companies are leveraging technology to provide a wide range of financial services, promote financial inclusion, and drive economic growth. As the fintech landscape in Morocco continues to develop, it will be exciting to see how these companies and others contribute to the country's digital transformation and economic progress.

Whether you are an investor looking for new opportunities, a consumer seeking convenient financial services, or simply someone interested in the fintech industry, Morocco's vibrant fintech ecosystem offers a lot to explore and appreciate.

0 notes

Text

MARKET GROWTH PROSPECTS OF BANKING SECTOR IN INDIA, 2023- 24 – DART CONSULTING FORECASTS HIGHER GROWTH IN THE NEXT FIVE YEARS

India’s banking sector is sufficiently capitalized and well-regulated. The financial and economic conditions are comparatively better even by comparing with well developed economies. Indian banks are generally resilient and have withstood the global downturn well as can be noted by reviewing previous years records.

The Indian banking industry has recently witnessed the rollout of innovative banking models like payments and small finance banks. In recent years, the Banks are increasingly focusing widening banking reach, through various schemes like the Pradhan Mantri Jan Dhan Yojana and Post payment banks. The rise of Indian NBFCs and fintech have significantly enhanced India’s financial inclusion and helped fuel the credit cycle in the country.

Here is a quick overview of key players in the industry.

HDFC Bank Ltd

HDFC Bank Ltd (HDFC) offers personal and corporate banking, private and investment banking, and other related financial solutions to individuals, MSMEs, government, and agriculture sectors, financial institutions and trusts, and non-resident Indians. It provides a range of deposit services and card products; loans for homes, cars, commercial vehicles, and other personal and business needs; insurance for life, health, and non-life risks; and investment solutions such as mutual funds, bonds, equities, and derivatives. HDFC also provides services such as cash management, corporate finance advisory, customized banking solutions, project and structured finance, trade financing, foreign exchange, internet banking, and payment and settlement services, among others. The bank operates in India through a network of branches, ATMs, phone banking, net banking, and mobile banking. It has overseas branches in Bahrain, Hong Kong, and the UAE, and representative offices in the UAE and Kenya. HDFC is headquartered in Mumbai, Maharashtra, India.

ICICI Bank Ltd

ICICI Bank Ltd (ICICI Bank) provides personal and corporate banking, investment banking, private banking, venture capital, life and non-life insurance solutions, securities broking, and asset management services to corporate and retail clients, high-net-worth individuals, and SMEs. It offers a wide range of products such as deposits accounts including savings and current accounts, and resident foreign currency accounts; investment products; and consumer and commercial cards. ICICI Bank offers to lend for home purchase, commercial business requirements, automobiles, personal needs, and agricultural needs. The bank offers services such as foreign exchange, remittance, import and export financing, advisory, trade services, personal finance management, cash management, and wealth management. It has an operational presence in Europe, Middle East, and Africa (EMEA), the Americas, and Asia. ICICI Bank is headquartered in Mumbai, Maharashtra, India.

State Bank of India

State Bank of India (SBI) is a universal bank. It provides a range of retail banking, corporate banking, and treasury services. The bank serves individuals, corporates, and institutional clients. Its major offerings include deposits services, personal and business banking cards, and loans and financing. The bank provides services such as mobile banking, internet banking, ATM services, foreign inward remittance, safe deposit locker, money transfer, mobile wallet, trade finance, merchant banking, project export finance, treasury, offshore banking, and cash management services. It operates in Asia, the Middle East, Europe, Africa, and North and South America. SBI is headquartered in Mumbai, Maharashtra, India.

Punjab National Bank

Punjab National Bank (PNB) offers retail and commercial banking, agricultural and international banking, and other financial services. Its retail and commercial banking portfolio offers credit and debit cards, corporate and retail loans, deposit services, cash management, and trade finance. Its international banking portfolio includes foreign currency accounts, money transfers, letters of guarantee, and world travel cards, and solutions to non-resident Indians. PNB also offers merchant banking, mutual funds, depository services, insurance, and e-services. The bank operates in India and has overseas operations in the UK, Bhutan, Myanmar, Bangladesh, Nepal, and the UAE. PNB is headquartered in New Delhi, India.

Bank of Baroda

Bank of Baroda (BOB) offers retail, agriculture, private and commercial banking, and other related financial solutions. It includes loans, deposit services, and payment cards. The bank offers loans for homes, vehicles, education, agriculture, personal and corporate requirements, mortgage, securities, and rent receivables, among others. It provides current and savings accounts; fixed and recurring deposits; debit, credit, and prepaid cards. The bank also provides insurance coverage for life, health, and general purposes. It offers services such as treasury, financing, mutual funds, cash management, international banking, digital banking, internet banking, start-Up banking, and wealth management. The bank has operations in Asia-Pacific, Europe, North America, and the Middle East and Africa. BOB is headquartered in Baroda, Gujarat, India.

Industry Performance

The health of the banking system in India has shown steady improvement, according to the Reserve Bank of India’s latest report on trends in the sector. From capital adequacy ratio to profitability metrics to bad loans, both public and private sector banks have shown visible improvement. And as credit growth has also witnessed an acceleration in 2021-22, banks have seen an expansion in their balance sheet at a pace that is a multi-year high. As of November 4, 2022, bank credit stood at Rs. 129.26 lakh crore (US$ 1,585.09 billion). As of November 4, 2022, credit to non-food industries stood at Rs. 128.87 lakh crore (US$ 1.58 trillion).

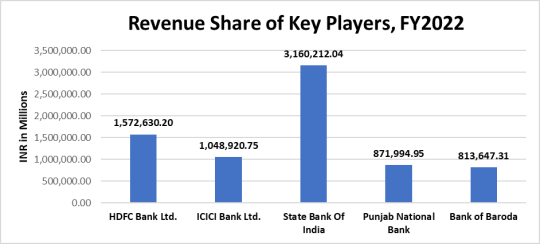

Given the increasing intensity, spread, and duration of the pandemic, economic recovery the performances of key companies in the industry was positive. The reported margin of the industry by analyzing the key players was around 13.7% by taking into consideration the last 3 years’ data. Details are as follows.

Companies Net Margin EBITDA/Sales

HDFC Bank Ltd. 23.5% 31.2%

ICICI Bank Ltd. 22.3% 30.4%

State Bank of India 10.0% 25.7%

Punjab National Bank 4.0% 10.0%

Bank of Baroda 8.9% 13.9%

Industry Margins 13.7% 22.2%

Industry Trends

The macroeconomic picture for 2023 portends mixed fortunes for consumer payment players. Higher rates should boost banks’ net interest margins for card portfolios, but persistent inflation, depletion of savings, and a potential economic slowdown could weigh on consumers’ appetite for spending. Digital identity is expected to evolve as a counterbalancing force to mitigate fraud risks in the long run. Transaction banking businesses are standing firm despite recent market uncertainties. For many banks, these divisions have been a steady source of revenues and profits.

Over the long term, banks will need to pursue new sources of value beyond product, industry, or business model boundaries. The new economic order that will likely emerge over the next few years will require bank leaders to forge ahead with conviction and remain true to their purpose as guardians and facilitators of capital flows. With these factors in mind, the industry is still showing huge growth potential, some of the growth divers that is propelling the industry are:

Rising rural income pushing up demand for banking

Rapid urbanisation, decreasing household size & easier availability of home loans has been driving demand for housing.

Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit.

The industry is attracting major investments as follows.

On June 2022, the number of bank accounts—opened under the government’s flagship financial inclusion drive ‘Pradhan Mantri Jan Dhan Yojana (PMJDY)’—reached 45.60 crore and deposits in the Jan Dhan bank accounts totaled Rs. 1.68 trillion (US$ 21.56 billion).

Some of the major initiatives taken by the government to promote the industry in India are as follows:

As per the Union Budget 2022-23:

National Asset reconstruction company (NARCL) will take over, 15 non-performing loans (NPLs) worth Rs. 50,000 crores (US$ 6.70 billion) from the banks.

National payments corporation India (NPCI) has plans to launch UPI lite this will provide offline UPI services for digital payments. Payments of up to Rs. 200 (US$ 2.67) can be made using this.

In the Union budget of 2022-23 India has announced plans for a central bank digital currency (CBDC) which will be possibly know as Digital Rupee.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed compounded annual growth rate (CAGR) of 9.9% at the end of 2022. Details are as below.

Companies CAGR

HDFC Bank Ltd. 14.02%

ICICI Bank Ltd. 7.3%

State Bank of India 8.4%

Punjab National Bank 9.2%

Bank of Baroda 10.7%

Industry CAGR 9.9%

Working through partnerships both with NBFCs and FinTech is high on the agenda of the Indian banking sector, and this is an area of focus of the FICCI National Committee on Banking. Banks will have to play a very constructive role as India aspires to be the leading economy in future. The strengthened banking sector has the potential to contribute directly and indirectly to GDP, increase job creation and enhance median income. Technology interventions to strengthen the quality and quantity of credit flow to the priority sector will be an important aspect. The need for sustainable finance / green financing is also gaining importance.

With these attributes boosting the sector, the Indian banking industry is likely to grow 5% more than the reported growth rate and is expected to exhibit CAGR of 10.4% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html

0 notes

Text

Moldova Awaits: Reliable Job Placement Services from Pakistan

Introduction:

In a world where global mobility and international careers are increasingly the norm, Manpower Recruitment Agency stands out as a beacon of excellence, particularly for those seeking job opportunities in Moldova. As Pakistan’s foremost ISO-certified recruitment agency, Falisha Manpower has a well-established reputation for connecting talented professionals with promising job opportunities across Europe and the Gulf countries. With License # 4035/RWP and an official endorsement from the Ministry of Overseas Pakistanis & Human Resource Development, Falisha Manpower Recruitment Consultant solidifies its position as a trusted and reliable recruitment agency in Pakistan.

Bridging Pakistan and Moldova:

Falisha Manpower Recruitment Agency excels in creating bridges between job seekers in Pakistan and employers in Moldova. The agency’s extensive network and in-depth understanding of both markets enable it to cater to a wide range of industries, including healthcare, IT, engineering, hospitality, and more. By ensuring a perfect match between the skills of Pakistani professionals and the needs of Moldovan employers, Falisha Manpower contributes significantly to the success of both parties.

ISO Certification: A Mark of Quality:

The ISO certification is a testament to Falisha Manpower’s commitment to maintaining the highest standards of quality in its recruitment processes. This certification guarantees that the agency operates with a robust quality management system, ensuring consistency, efficiency, and professionalism in all its services. For job seekers and employers alike, the ISO certification provides assurance of the agency’s dedication to excellence and continuous improvement.

Official Endorsement and Credibility:

Falisha Manpower’s endorsement by the Ministry of Overseas Pakistanis & Human Resource Development underscores its credibility and compliance with governmental regulations. This official recognition not only enhances the agency’s reputation but also offers job seekers confidence in the legitimacy and reliability of the opportunities presented. The agency’s adherence to legal and ethical standards ensures a transparent and fair recruitment process for all stakeholders.

Comprehensive Services for Job Seekers:

Falisha Manpower Recruitment Agency offers a comprehensive suite of services designed to support job seekers at every step of their journey. From initial career counseling and consultation to resume building, interview preparation, and visa assistance, the agency provides holistic support. This all-encompassing approach helps candidates navigate the complexities of the international job market with confidence and ease.

Empowering Pakistani Professionals:

Best Recruitment Agency In Pakistan For Moldova, Falisha Manpower plays a pivotal role in empowering Pakistani professionals to build successful international careers. The agency’s efforts not only contribute to the personal and professional growth of individuals but also boost the economic development of Pakistan. Remittances from overseas workers are a vital component of Pakistan’s economy, and Falisha Manpower’s services help maximize this potential.

A Vision for the Future:

Falisha Manpower Recruitment Agency is committed to expanding its reach and setting new benchmarks in the recruitment industry. The agency aims to leverage technological advancements and innovative practices to enhance its services further. By staying ahead of industry trends and continuously improving its processes, Falisha Manpower strives to maintain its position as Pakistan’s leading recruitment agency for jobs in Moldova and beyond.

Conclusion:

Falisha Manpower Recruitment Agency exemplifies excellence in connecting Pakistani talent with global opportunities, particularly in Moldova. With its ISO certification, official endorsement, and comprehensive range of services, the agency stands as a beacon of trust and reliability in the recruitment landscape. For Pakistani professionals aspiring to build successful careers abroad, Falisha Manpower is the go-to partner, providing the expertise, support, and opportunities needed to achieve their dreams.

Moldova awaits, and with Falisha Manpower Recruitment Agency, Pakistani professionals are well-equipped to seize the opportunities and build a brighter future on the global stage.

0 notes

Text

EbixCash IPO Date, Price, Review, Company Profile, Financials, Risk, Allotment Details 2023

New Post has been published on https://wealthview.co.in/ebixcash-ipo/

EbixCash IPO Date, Price, Review, Company Profile, Financials, Risk, Allotment Details 2023

EbixCash IPO: EbixCash is a leading Indian fintech company offering a variety of digital products and services across B2C and B2B sectors. They specialize in areas like forex, travel technology, insurance, and BPO. The Indian fintech industry is booming, driven by rapid digital adoption and the government’s push for a cashless economy.

EbixCash IPO Details:

IPO Date: While approved by SEBI, the IPO dates (open, close, and listing) are still undetermined.

Offer size: Up to Rs. 6,000 crore through a fresh issue of equity shares.

Price band: Yet to be announced.

Recent News Updates:

Anticipation and Buzz: Despite the delayed launch, the IPO is highly anticipated due to EbixCash’s strong financials, market leadership in forex and travel tech, and the overall growth potential of the fintech sector.

Ebix Inc. Bankruptcy: Concerns arose in October 2023 when EbixCash’s US parent company filed for bankruptcy. However, EbixCash emphasizes its financial independence and claims the bankruptcy won’t affect its operations.

Continued Monitoring: The market awaits details on the issue date and price band, closely watching how the bankruptcy news and other factors influence investor sentiment.

EbixCash IPO Offer Details:

Securities Offered:

The EbixCash IPO will solely offer equity shares, granting ownership stakes in the company. No bonds or other instruments will be included in this offering.

Investor Category Reservation:

Here’s how the offer size will be distributed among different investor categories:

Retail Individual Investors (RII): 35%

Qualified Institutional Buyers (QIB): 50%

Non-Institutional Investors (NII): 15%

Minimum Lot Size and Investment Amount:

Minimum Lot Size: 100 equity shares

Minimum Investment Amount: The minimum investment will depend on the final IPO price, which is yet to be announced. Based on the offer size of Rs. 6,000 crore and assuming a price band of Rs. 50-60 per share (as speculated by some analysts), the minimum investment could be roughly around Rs. 5,000-6,000.

EbixCash Company Profile:

Founded in 2002, initially known as ItzCash, before rebranding to EbixCash in 2016.

Offers a diverse range of fintech solutions across B2C and B2B sectors, including:

Forex: Leading player in India, handling remittance, currency exchange, and international money transfers.

Travel: Provides technology solutions to travel agents, tour operators, and airlines.

Insurance: Distributes a variety of insurance products and offers tech support to insurers.

BPO: Operates call centers and provides back-office services to various industries.

Extensive physical network exceeding 650,000 outlets, including 50,000 bank branches, giving it the edge over many purely digital competitors.

Strong online presence with mobile apps and an omni-channel platform supporting its services.

Market Position and Share:

Holds a leading position in the Indian forex market, handling a significant portion of remittance transactions.

Commands a dominant position in travel technology, serving many major travel companies.

Growing presence in the insurance and BPO sectors, aiming to further gain market share.

Key Brands and Partnerships:

EbixCash: Primary brand for all services offered.

Yatra Money: Popular travel money card issued by EbixCash.

Partnerships: Collaborates with major banks, airlines, insurance companies, and travel agencies.

Milestones and Achievements:

Clocked $100 million in EBITDA for FY2022-23, demonstrating consistent profitability.

Won several prestigious awards, including “Best Fintech Company” and “Best Forex Service Provider.”

Successfully transitioned from ItzCash to EbixCash, establishing a stronger brand identity.

Competitive Advantages and USP:

Vast Physical Network: Unique blend of extensive physical presence and robust online platform creates a strong distribution advantage.

Diversified Product Portfolio: Caters to various needs, minimizing reliance on any single market segment.

Focus on Technology: Continuous innovation in mobile apps and digital solutions keeps EbixCash ahead of the curve.

Strong Partnerships: Collaborations with leading players add value and enhance reach.

EbixCash Financials:

Revenue Growth: EbixCash has registered consistent double-digit revenue growth exceeding 20% in the past three fiscal years. This strong growth trajectory reflects rising demand for its B2C and B2B offerings.

Profitability: The company has maintained profitability since its inception, achieving Rs. 400 crore in net profit for FY 2022-23 and exceeding $100 million in EBITDA.

Debt Levels: EbixCash’s debt-to-equity ratio currently stands at approximately 0.5, considered moderate and manageable within the industry. This suggests a healthy balance between debt financing and equity capital.

EbixCash IPO Objectives:

EbixCash’s decision to launch an IPO aims to achieve several objectives that align with its future growth strategy:

1. Raise Capital for Expansion: The primary objective is to raise up to Rs. 6,000 crore through the fresh issue of equity shares. This capital will be crucial for:

Funding organic growth initiatives: Expanding its existing product lines, entering new markets, and strengthening its technology infrastructure.

Acquisitions and strategic investments: Identifying and acquiring complementary businesses or technologies to accelerate growth and diversify its offerings.

Meeting working capital requirements: Ensuring adequate financial resources to support ongoing operations and future expansion plans.

2. Enhance Brand Visibility and Reputation: Going public will elevate EbixCash’s profile in the Indian market and attract wider investor attention. This can:

Boost brand awareness and credibility: Attract new customers and partners, potentially leading to increased market share.

Improve access to talent and resources: Attract top talent and secure better loan terms or partnerships due to enhanced public image.

3. Create a Liquidity Event for Investors: Existing shareholders, including Ebix Inc., will have the opportunity to exit their investments and unlock liquidity through the IPO. This can:

Provide financial returns to early investors: Reward their contribution to the company’s growth.

Free up capital for Ebix Inc. to focus on its core business: The US parent company can utilize its proceeds from the IPO for its own turnaround efforts.

EbixCash IPO Lead Managers:

EbixCash has appointed a consortium of five reputable investment banks to guide its IPO journey:

Motilal Oswal Investment Advisors: A leading domestic investment bank with extensive experience in managing large IPOs across various sectors. They’ve successfully handled over 150 IPOs, including prominent names like Delhivery, Adani Wilmar, and Nykaa.

Equirus Capital: Known for their expertise in technology and financial services IPOs. They’ve managed successful offerings for companies like Paytm, Zomato, and Policybazaar.

ICICI Securities: One of India’s largest investment banks with a strong track record in IPOs, having managed over 200 public offerings, including Bajaj Energy, Indigo Paints, and Star Health and Allied Insurance.

SBI Capital Markets: The investment banking arm of the State Bank of India, bringing a vast network and experience in managing large government and private sector IPOs.

Yes Securities: A well-respected investment bank with a growing presence in the IPO market, having managed successful offerings like Nuvoco Vistas Corporation and Sona Comstar.

The collective expertise of these lead managers ensures:

Effective marketing and pricing: Reaching the right investors and determining a suitable IPO price.

Regulatory compliance: Ensuring adherence to SEBI guidelines and other legal requirements.

Smooth execution: Facilitating a seamless IPO process from launch to listing.

Registrar: Keeping Track of the Details

Link Intime India Private Limited has been appointed as the registrar for the EbixCash IPO. Their role is crucial in:

Managing the application process: Receiving and processing IPO applications from investors.

Maintaining the record of applications: Ensuring accuracy and transparency in the allocation process.

Transferring shares to investors’ demat accounts: Facilitating smooth share distribution post-IPO.

EbixCash IPO Risks:

While EbixCash’s IPO holds promise, it’s important to consider potential risks and concerns before making an investment decision:

Industry Headwinds: The fintech sector is competitive and faces regulatory uncertainties. Increased competition or changes in regulations could affect EbixCash’s market share and profitability.

Company-Specific Challenges:

Ebix Inc. Bankruptcy: The ongoing bankruptcy of the US parent company raises concerns about potential financial implications for EbixCash, although the company maintains its operational independence.

Dependence on Forex: A significant portion of EbixCash’s revenue comes from the forex market, which can be volatile due to currency fluctuations.

Limited Profitability: While the company has been profitable, its net profit margin remains relatively low compared to some competitors, raising concerns about its long-term profitability.

Financial Health Analysis:

Debt Levels: EbixCash’s current debt-to-equity ratio of 0.5 is moderate, but future debt accumulation could impact its financial flexibility.

Reliance on Key Partnerships: Certain partnerships drive a significant portion of the company’s revenue, making it vulnerable to disruptions in these relationships.

Limited Track Record as a Public Company: As a yet-to-be listed entity, there’s limited historical data for investors to assess its performance as a publicly traded company.

Red Flags for Investors:

The delayed IPO launch: This could indicate potential challenges or uncertainties.

The impact of Ebix Inc. bankruptcy: Investors need to carefully assess the potential financial and reputational risks associated with this development.

The company’s dependence on specific segments: Over-reliance on forex or a limited product portfolio could expose the company to higher risks.

Read EBIXCASH Limited official DRHP

Also Read: How to Apply for an IPO?

0 notes

Text

Unveiling Financial Convenience: Navigating the Dynamics of the Kuwait Cards and Payments Market

Transformative Trends: A Deep Dive into Kuwait's Financial Landscape

Kuwait's Cards and Payments Market is at the forefront of financial innovation, reflecting the nation's commitment to modernize its economic infrastructure. Kuwait Cards and Payments Market This comprehensive exploration delves into the nuanced dynamics of the Kuwait Cards and Payments sector, unraveling market trends, digital transformations, and the factors shaping the future of financial transactions in the country.

Market Overview: Kuwait's Financial Ecosystem

Payment Infrastructure: A Digital Frontier

Kuwait's Cards and Payments Market operates within a robust digital infrastructure. From traditional payment cards to cutting-edge mobile payment solutions, understanding the diverse range of payment methods offers insights into the nation's quest for financial inclusivity and efficiency.

Financial Institutions: Collaborative Progress

The market is characterized by collaborative efforts among financial institutions, from banks to fintech innovators. Tracking the partnerships and initiatives of key players provides a comprehensive view of the collaborative progress shaping Kuwait's financial landscape.

Digital Transformations: Shaping the Payment Experience

Contactless Payments: The Rise of Tap-and-Go

Contactless payments have become a hallmark of Kuwait's digital transformation. The widespread adoption of contactless cards and mobile payment options showcases a shift towards a more convenient and secure payment experience for consumers.

E-wallets and Mobile Banking: Empowering Consumers

The surge in e-wallets and mobile banking apps empowers Kuwaiti consumers with convenient and accessible financial tools. Examining the functionalities and user experiences of these digital platforms unveils the transformative impact on everyday financial transactions.

Market Trends: Navigating the Evolving Landscape

Cross-Border Transactions: Global Connectivity