#Optical Imaging Market Analysis

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr.com rank in the US is 25.

Text

Future Growth of Optical Imaging Systems Market: Insights on Size, Share, and Revenue Projections

Optical Imaging Systems Market: Growth, Trends, and Forecasts 2035

The Optical Imaging Systems Market is witnessing significant growth due to the increasing demand for advanced imaging technologies across various industries. Optical imaging systems play a crucial role in enhancing the quality and accuracy of imaging in sectors like healthcare, automotive, entertainment, defense, and manufacturing. These systems offer high-resolution imaging, non-invasive monitoring, and the ability to capture real-time data, making them highly valued in modern technological applications.

Request Sample Copy: https://wemarketresearch.com/reports/request-free-sample-pdf/optical-imaging-systems-market/1632

Overview of the Optical Imaging Systems Market

Optical imaging systems are used to capture and analyze light to create images of objects or structures. These systems rely on optical technologies such as lasers, lenses, and sensors to visualize and interpret data. They find widespread use in medical diagnostics, scientific research, industrial applications, and even in consumer electronics. The Optical Imaging Systems Market Size has been expanding rapidly in recent years due to advancements in technology and the growing need for high-quality imaging solutions.

Factors Driving the Optical Imaging Systems Market Growth

Several factors are contributing to the growth of the Optical Imaging Systems Market. Among them, the increasing demand for non-invasive medical imaging systems is one of the most significant. Optical imaging techniques like optical coherence tomography (OCT) and confocal microscopy are revolutionizing diagnostics by enabling doctors to detect diseases at their early stages without the need for surgery. Moreover, the growing adoption of optical imaging in the automotive industry for driver assistance systems and the increasing use in the entertainment sector for high-definition displays are also driving the market.

Market Trends and Innovations

The Optical Imaging Systems Market Trends indicate a shift toward miniaturization and portability of optical imaging devices. As the demand for handheld and compact imaging devices rises, manufacturers are developing portable systems that provide high-quality imaging in a more convenient form factor. This trend is expected to continue as optical imaging systems become more integrated with mobile devices and wearable technology.

Another noteworthy trend is the increasing emphasis on the integration of optical imaging systems with complementary technologies like ultrasound, magnetic resonance imaging (MRI), and X-ray to provide hybrid imaging solutions. These multi-modal systems offer enhanced diagnostic capabilities by combining the strengths of different imaging techniques, thereby improving the overall accuracy and reliability of results. The convergence of optical imaging and other advanced technologies is expected to expand the Optical Imaging Systems Market Value significantly.

Regional Insights: Optical Imaging Systems Market Forecast

Geographically, the Optical Imaging Systems Market Forecast suggests that North America will continue to dominate the market due to the presence of well-established healthcare infrastructure, high investment in R&D, and the growing adoption of advanced imaging systems. The United States, in particular, has been a leader in the integration of optical imaging technologies across sectors, including medical diagnostics, defense, and industrial applications.

Europe follows closely behind, with a significant contribution to the Optical Imaging Systems Market Size. The region's strong healthcare sector, along with advancements in research and development in imaging technologies, is fueling market growth. The presence of major players in the optical imaging industry, such as Carl Zeiss AG and Leica Microsystems, further supports the market's expansion in Europe.

Asia-Pacific is expected to exhibit the highest growth rate over the next decade, driven by rapid technological advancements, increasing healthcare investments, and a growing demand for optical imaging systems in industrial applications. Countries like China, Japan, and India are emerging as key markets for optical imaging systems, owing to their expanding healthcare infrastructure and the increasing adoption of high-tech imaging solutions.

Optical Imaging Systems Market Potential in Healthcare

In the healthcare industry, the Optical Imaging Systems Market Potential is enormous. These systems provide numerous advantages, such as enhanced visualization, non-invasive tissue analysis, and the ability to monitor treatment progress in real-time. Technologies like Optical Coherence Tomography (OCT), which is commonly used in ophthalmology, and fluorescence imaging, used for cancer detection, are gaining traction in medical diagnostics. As a result, the demand for advanced optical imaging systems in healthcare is poised for steady growth.

The rise of personalized medicine and the focus on early detection of diseases such as cancer and cardiovascular conditions are also fueling the growth of optical imaging technologies in the medical field. The integration of AI and machine learning is further enhancing the market's potential by enabling automated data analysis and faster decision-making.

Challenges in the Optical Imaging Systems Market

Despite the numerous growth opportunities, the Optical Imaging Systems Market faces several challenges. One of the primary hurdles is the high cost of advanced optical imaging systems, which limits their accessibility in developing regions. Additionally, the complexity of integrating these systems with existing medical equipment or industrial machines can be an obstacle to adoption. Manufacturers must also address issues related to system calibration, image quality, and data storage to enhance the overall user experience.

Related Report:

Encorafenib Market

Avelumab Market

Elotuzumab Market

Carfilzomib Market

Conclusion: A Promising Future for Optical Imaging Systems

In conclusion

The Optical Imaging Systems Market Growth is driven by continuous technological innovations, rising demand for non-invasive imaging techniques, and the expanding application of optical imaging in various industries. With growing investments in research and development, the market is poised to see substantial growth in the coming years. As technologies evolve and new applications emerge, the Optical Imaging Systems Market Analysis suggests that the market will continue to thrive, offering immense opportunities for companies, healthcare providers, and researchers alike.

#Optical Imaging Market#Optical Imaging Market Size#Optical Imaging Market Share#Optical Imaging Market Price#Optical Imaging Market Growth#Optical Imaging Market Trends#Optical Imaging Market Potential#Optical Imaging Market Forecast#Optical Imaging Market Analysis

0 notes

Text

Field Programmable Gate Array (FPGA) Market - Forecast(2024 - 2030)

The FPGA market was valued at USD 4.79 Billion in 2017 and is anticipated to grow at a CAGR of 8.5% during 2017 and 2023. The growing demand for advanced driver-assistance systems (ADAS), the growth of IoT and reduction in time-to-market are the key driving factors for the FPGA market. Owing to benefits such as increasing the performance, early time to market, replacing glue logic, reducing number of PCB spins, and reducing number of parts of PCB, field programmable gate arrays (FPGA’s) are being used in many CPU’s. Industrial networking, industrial motor control, industrial control applications, machine vision, video surveillance make use of different families of FPGA’s.

North America is the leading market for field programmable gate arrays with U.S. leading the charge followed by Europe. North America region is forecast to have highest growth in the next few years due to growing adoption of field programmable gate arrays.

What is Field Programmable Gate Arrays?

Field Programmable Gate Arrays (FPGAs) are semiconductor devices. The lookup table (LUT) is the basic block in every FPGA. Different FPGAs use variable sized LUTs. A lookup table is logically equivalent to a RAM with the inputs being the address select lines and can have multiple outputs in order to get two Boolean functions of the same inputs thus doubling the number of configuration bits. FPGAs can be reprogrammed to desired application or functionality requirements after manufacturing. This differentiates FPGAs from Application Specific Integrated Circuits (ASICs) although they help in ASIC designing itself, which are custom manufactured for specific design tasks.

In a single integrated circuit (IC) chip of FPGA, millions of logic gates can be incorporated. Hence, a single FPGA can replace thousands of discrete components. FPGAs are an ideal fit for many different markets due to their programmability. Ever-changing technology combined with introduction of new product portfolio is the major drivers for this industry.

Request Sample

What are the major applications for Field Programmable Gate Arrays?

FPGA applications are found in Industrial, Medical, Scientific Instruments, security systems, Video & Image Processing, Wired Communications, Wireless Communications, Aerospace and Defense, Medical Electronics, Audio, Automotive, Broadcast, Consumer Electronics, Distributed Monetary Systems, Data and Computer Centers and many more verticals.

Particularly in the fields of computer hardware emulation, integrating multiple SPLDs, voice recognition, cryptography, filtering and communication encoding, digital signal processing, bioinformatics, device controllers, software-defined radio, random logic, ASIC prototyping, medical imaging, or any other electronic processing FGPAs are implied because of their capability of being programmable according to requirement. FPGAs have gained popularity over the past decade because they are useful for a wide range of applications.

FPGAs are implied for those applications in particular where the production volume is small. For low-volume applications, the leading companies pay hardware costs per unit. The new performance dynamics and cost have extended the range of viable applications these days.

Market Research and Market Trends of Field Programmable Gate Array (FPGA) Ecosystem

FPGA As Cloud Server: IoT devices usually have limited processing power, memory size and bandwidth. The developers offer interfaces through compilers, tools, and frameworks. This creates effectiveness for the customer base and creates strong cloud products with increased efficiency which also included new machine learning techniques, Artificial Intelligence and big data analysis all in one platform. Web Service Companies are working to offer FPGAs in Elastic Compute Cloud (EC2) cloud environment.

Inquiry Before Buying

Artificial Intelligence: As an order of higher magnitude performance per Watt than commercial FPGAs and (Graphical Processing Unit) GPUs in SOC search giant offers TPUs (Google’s Tensor Processing Units). AI demands for higher performance, less time, larger computation with more power proficient for deep neural networks. Deep neural network power-up the high-end devices. Google revealed that the accelerators (FGPAs) were used for the Alpha GO systems which is a computer developed by Google DeepMind that plays the board game Go. CEA also offers an ultra-low power programmable accelerator called P-Neuro.

Photonic Networks for Hardware Accelerators: Hardware Accelerators normally need high bandwidth, low latency, and energy efficiency. The high performance computing system has critical performance which is shifted from the microprocessors to the communications infrastructure. Optical interconnects are able to address the bandwidth scalability challenges of future computing systems, by exploiting the parallel nature and capacity of wavelength division multiplexing (WDM). The multi-casted network uniquely exploits the parallelism of WDM to serve as an initial validation for architecture. Two FPGA boarded systems emulate the CPU and hardware accelerator nodes. Here FPGA transceivers implement and follow a phase-encoder header network protocol. The output of each port is individually controlled using a bitwise XNOR of port’s control signal. Optical packets are send through the network and execute switch and multicasting of two receive nodes with most reduced error

Low Power and High Data Rate FPGA: “Microsemi” FPGAs provides a non-volatile FPGA having 12.7 GB/s transceiver and lower poor consumption less than 90mW at 10 GB/s. It manufactured using a 28nm silicon-oxide-nitride-oxide-silicon nonvolatile process on standard CMOS technology. By this they address cyber security threats and deep submicron single event upsets in configuration memory on SRAM-based FPGA. These transceivers use cynical I/O gearing logic for DDR memory and LVDS. Cryptography research provides differential power analysis protection technology, an integrated physical unclonable function and 56 kilobyte of secure embedded non-volatile memory, the built-in tamper detectors parts and counter measures.

Schedule a Call

Speeds up FPGA-in-the-loop verification: HDL Verifier is used to speed up FPGA-in-the-loop (FIL) verification. Faster communication between the FPGA board and higher clock frequency is stimulated by the FIL capabilities. This would increase the complexity of signal processing, control system algorithms and vision processing. For validation of the design in the system context simulate hardware implementation on an FPGA board. HDL Verifier automates the setup and connection of MATLAB and Simulink test environments to designs running on FPGA development boards. The R2016b has been released that allows engineers to specify a custom frequency for their FPGA system clock with clock rates up to five times faster than previously possible with FIL. This improves faster run-time. From MATLAB and Simulink is an easy way to validate hardware design within the algorithm development environment

Xilinx Unveils Revolutionary Adaptable Computing Product Category: Xilinx, Inc. which is leader in FGPAs, has recently announced a new product category which is named as Adaptive Compute Acceleration Platform (ACAP) and has the capabilities far beyond of an FPGA. An ACAP is a highly integrated multi-core heterogeneous compute platform that can be changed at the hardware level to adapt to the needs of a wide range of applications and workloads. ACAP has the capability of dynamic adaption during operation which enables it to deliver higher performance per-watt levels that is unmatched by CPUs or GPUs.

Lattice Releases Next-Generation FPGA Software for Development of Broad Market Low Power Embedded Applications: Lattice Semiconductor, launched its FPGA software recently. Lattice Radiant targeted for the development of broad market low power embedded applications. Device’s application expands significantly across various market segments including mobile, consumer, industrial, and automotive due to is rich set of features and ease-of-use, Lattice Radiant software’s support for iCE40 Ultra plus FPGAs. ICE40 Ultra Plus devices are the world’s smallest FPGAs with enhanced memory and DSPs to enable always on, distributed processing. The Lattice Radiant software is available for free download.

Who are the Major Players in market?

The companies referred in the market research report include Intel Inc, Microsemi, Lattice Semiconductor, Xilinx, Atmel, Quick Logic Corp., Red Pitaya, Mercury Computer, Nallatech Inc., Achronix Semiconductor Corporation, Acromag Inc., Actel Corp., Altera Corp.

Buy Now

What is our report scope?

The report incorporates in-depth assessment of the competitive landscape, product market sizing, product benchmarking, market trends, product developments, financial analysis, strategic analysis and so on to gauge the impact forces and potential opportunities of the market. Apart from this the report also includes a study of major developments in the market such as product launches, agreements, acquisitions, collaborations, mergers and so on to comprehend the prevailing market dynamics at present and its impact during the forecast period 2017-2023.

All our reports are customizable to your company needs to a certain extent, we do provide 20 free consulting hours along with purchase of each report, and this will allow you to request any additional data to customize the report to your needs.

Key Takeaways from this Report

Evaluate market potential through analyzing growth rates (CAGR %), Volume (Units) and Value ($M) data given at country level – for product types, end use applications and by different industry verticals.

Understand the different dynamics influencing the market – key driving factors, challenges and hidden opportunities.

Get in-depth insights on your competitor performance – market shares, strategies, financial benchmarking, product benchmarking, SWOT and more.

Analyze the sales and distribution channels across key geographies to improve top-line revenues.

Understand the industry supply chain with a deep-dive on the value augmentation at each step, in order to optimize value and bring efficiencies in your processes.

Get a quick outlook on the market entropy – M&A’s, deals, partnerships, product launches of all key players for the past 4 years.

Evaluate the supply-demand gaps, import-export statistics and regulatory landscape for more than top 20 countries globally for the market.

#field programmable gate array market#field programmable gate array market report#field programmable gate array market research#field programmable gate array market size#field programmable gate array market shape#field programmable gate array market forecast#field programmable gate array market analysis#Image processing#Wave form generation#Partial reconfiguration#Wired Communications#Optical Transport Network

0 notes

Text

Electro Optical Systems Market Size, Share, Growth, Demand, Trends and Forecast 2034

The global electro optical systems market is projected to expand from USD 12.8 billion in 2024 to USD 19.5 billion by 2034, registering a CAGR of 4.3% over the forecast period. This growth is driven by increasing demand across defense, aerospace, telecommunications, medical devices, and industrial sectors.

Request a Sample of this Report: https://www.factmr.com/connectus/sample?flag=S&rep_id=7834

Market Analysis

The global electro optical systems market is undergoing rapid expansion, driven by growing demand for advanced surveillance, targeting, and detection technologies across both defense and commercial sectors. As modern military operations evolve toward more precision-driven and real-time data-dependent strategies, the integration of electro optical systems has become critical. These systems, combining optical and electronic technologies, are pivotal in providing improved situational awareness and target identification capabilities.

Market growth is strongly influenced by heightened defense budgets, particularly in the U.S. and U.K., where governments are actively investing in battlefield modernization programs. In the U.S., the Department of Defense continues to prioritize sensor fusion and autonomous capability upgrades, spurring procurement of state-of-the-art electro optical payloads for unmanned aerial vehicles (UAVs), armored vehicles, and naval platforms. Similarly, the United Kingdom is advancing its Future Soldier and Integrated Review defense initiatives, which emphasize surveillance and electronic warfare—areas where electro optical technologies are essential.

Technological innovation is also a powerful market driver. The development of multispectral and hyperspectral imaging, AI-enhanced targeting systems, and improved infrared sensors has pushed the boundaries of what electro optical systems can achieve. These technologies are being increasingly adopted not only in military contexts but also in border control, law enforcement, environmental monitoring, and disaster response operations.

Segment Analysis

By Component:

Sensors: Crucial for detecting and converting physical phenomena into signals, sensors are integral to electro optical systems.

Displays: Used for visual representation of data, displays are essential in various applications, including military and medical devices.

Optical Devices: Components like lenses and mirrors are fundamental in directing and focusing light within systems.

Processors: Responsible for analyzing and interpreting data, processors are vital for system functionality.

Transceivers: These components enable communication by transmitting and receiving signals.

By Application:

Defense and Military: The largest application segment, driven by the need for advanced surveillance and targeting systems.

Aerospace: Electro optical systems are used in navigation and communication systems in aircraft and spacecraft.

Telecommunications: These systems facilitate high-speed data transmission and are integral to network infrastructure.

Medical Devices: Used in imaging and diagnostic equipment, enhancing patient care and treatment outcomes.

Industrial: Applications include quality control, automation, and safety systems in manufacturing processes.

Country-wise Insights

The U.S. market is expected to grow at a CAGR of 2.9% through 2034, from a 2024 valuation of USD 2.2 billion. This growth is attributed to increased defense spending and advancements in surveillance technologies/

In the UK, market growth is supported by investments in defense modernization and the integration of electro optical systems in various sectors, including healthcare and telecommunications.

Germany's focus on industrial automation and smart manufacturing drives the adoption of electro optical systems, enhancing efficiency and productivity.

Key Players

Prominent companies in the electro optical systems market include:

BAE Systems plc

Canon Inc.

Elbit Systems Ltd.

General Dynamics Corporation

Hensoldt AG

Honeywell International Inc.

L3Harris Technologies, Inc.

Leonardo S.p.A.

Lockheed Martin Corporation

MKS Instruments, Inc.

Nikon Corporation

Northrop Grumman Corporation

Opgal Optronic Industries Ltd.

QinetiQ Group plc

Raytheon Technologies Corporation

Rockwell Collins (a subsidiary of Collins Aerospace)

Teledyne Technologies Incorporated

Thales Group

Zygo Corporation

Strategic Outlook and Industry Trends

The electro optical systems market is poised for significant advancements:

Integration of AI and Machine Learning: Enhancing system capabilities for real-time data analysis and decision-making.

Miniaturization: Developing compact systems suitable for a wider range of applications, including portable medical devices and unmanned vehicles.

Energy Efficiency: Focus on developing systems with lower power consumption to meet sustainability goals.

Quantum Imaging and Augmented Reality: Emerging technologies are expected to revolutionize applications in defense, healthcare, and consumer electronics.

Manufacturers that prioritize innovation, adaptability, and compliance with evolving regulations are well-positioned to capitalize on these trends.

Browse Full Report: https://www.factmr.com/report/electro-optical-systems-market

Segmentation of Electro Optical Systems Market

By Component:

Sensors

Displays

Optical Devices

Processors

Transceivers

By Application:

Defense and Military

Aerospace

Telecommunications

Medical Devices

Industrial

By Technology:

Imaging

Non-Imaging

By End User:

Government

Commercial

Others

By Region:

North America

Latin America

Europe

East Asia

South Asia & Pacific

Middle East & Africa

𝐂𝐨𝐧𝐭𝐚𝐜𝐭: US Sales Office 11140 Rockville Pike Suite 400 Rockville, MD 20852 United States Tel: +1 (628) 251-1583, Email: [email protected]

0 notes

Text

The Role of Optical Materials in AI, Quantum, and 6G Technologies

For decades, silicon has been the pillar of optical Materials technologies, utilized in lasers, modulators, and photodetectors across industries ranging from telecommunications to healthcare. However, recent advancements are bringing non-silicon materials into the spotlight. Chalcogenides, organic polymers, and photonic crystals are emerging as transformative alternatives to silicon in optical devices, enabling breakthroughs in areas like infrared communication, flexible photonics, and quantum computing. This article delves into these unconventional materials, exploring their applications and highlighting why they are key to the future of photonics.

Understanding Optical Materials and Their Historical Dominance of Silicon

Optical materials are substances used to manipulate light for applications in fields like telecommunications, medical devices, and electronics. Silicon, due to its excellent optical and electrical properties, has long been the dominant material in this domain. Silicon photonics have powered the information age by enabling high-speed data transmission and low-cost manufacturing.

𝐌𝐚𝐤𝐞 𝐈𝐧𝐟𝐨𝐫𝐦𝐞𝐝 𝐃𝐞𝐜𝐢𝐬𝐢𝐨𝐧𝐬 – 𝐀𝐜𝐜𝐞𝐬𝐬 𝐘𝐨𝐮𝐫 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐈𝐧𝐬𝐭𝐚𝐧𝐭𝐥𝐲! https://www.futuremarketinsights.com/reports/sample/rep-gb-1863

Yet, despite its success, silicon has its limitations. In areas requiring light manipulation at wavelengths outside of the visible spectrum—such as mid-infrared light—silicon falls short. As technology advances and demands become more specific, alternative materials have begun to surface, offering unique advantages that silicon simply cannot match.

The Rise of Non-Silicon Optical Materials

Materials such as chalcogenide glasses, organic polymers, and photonic crystals are rapidly gaining attention for their specialized properties that silicon cannot provide. Unlike silicon, these materials offer greater flexibility, enhanced efficiency, and the ability to operate in non-traditional spectral regions. Each of these materials is addressing a different challenge in photonics, from high-speed communication and sensing to flexible electronic devices.

For instance, chalcogenide glasses excel in infrared optics, where silicon struggles to transmit light efficiently. Organic polymers are reshaping consumer electronics with their lightweight and flexible nature, while photonic crystals promise to revolutionize the way light is manipulated on a nanoscale.

Chalcogenide Glasses: The Mid-Infrared Revolution

Chalcogenide glasses are a family of materials that are particularly well-suited for mid-infrared applications, which include telecommunications, environmental sensing, and medical diagnostics. These glasses are composed primarily of chalcogen elements like sulfur, selenium, and tellurium. Unlike silicon, chalcogenide glasses have a broad transmission window that spans from the visible to the mid-infrared spectrum, making them ideal for a range of high-performance applications.

One of the most significant advantages of chalcogenide glasses is their ability to transmit light with minimal loss over long distances, especially in the infrared region. This makes them invaluable for fiber-optic communication systems, where data needs to travel over great distances without degradation. Beyond telecommunications, chalcogenides are used in medical imaging, where they enable deep tissue analysis and infrared spectroscopy, providing insights into biological systems that are difficult to obtain with traditional optical materials.

𝐔𝐧𝐥𝐨𝐜𝐤 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬 – 𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐭𝐡𝐞 𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐍𝐨𝐰: Optical Materials Market - Trends & Forecast 2025 to 2035

Organic Polymers and Their Role in Flexible Photonics

Organic polymers are an exciting class of materials that are gaining prominence in photonics due to their flexibility, tunable properties, and ease of integration into lightweight, flexible devices. While typically associated with consumer electronics, these materials are making their way into advanced optical systems.

One of the most notable applications of organic polymers is in Organic Light-Emitting Diodes (OLEDs), which are widely used in modern display technologies. OLEDs, integrated with organic polymers, provide energy-efficient lighting with superior color rendering, and their flexibility allows for the creation of foldable or curved displays—an area that has become increasingly important in the smartphone and television industries.

Moreover, organic polymers are being used in photonic circuits and flexible optical fibers. These fibers, made from organic polymers, offer an alternative to traditional glass fibers, as they can be molded and integrated into a variety of devices, such as wearable health monitoring systems. These systems use the flexibility of organic polymers to create sensors capable of detecting physiological parameters like blood oxygen levels or body temperature, with applications ranging from fitness trackers to medical diagnostic devices.

Photonic Crystals: The Future of Optical Communication

Photonic crystals represent a unique category of optical materials that can control light with unprecedented precision. These materials consist of a periodic structure that affects the movement of photons, allowing them to guide and filter light in highly specific ways. One of the most promising applications of photonic crystals is in photonic crystal fibers (PCFs), which are already making a significant impact in optical communication.

PCFs differ from traditional optical fibers in that their structure allows for highly efficient light transmission with minimal loss. This feature makes them ideal for applications that require high-speed communication over long distances. The tunable nature of photonic crystals also allows them to function at a variety of wavelengths, making them ideal for quantum communication, which depends on the ability to manipulate and transmit photons securely.

The future of photonic crystals in optical materials lies in their ability to support quantum technologies, such as quantum key distribution for secure communication. As quantum computing and cryptography evolve, the demand for efficient, lossless communication channels will increase, and photonic crystals are positioned to meet this demand.

General & Advanced Materials Industry Analysis: https://www.futuremarketinsights.com/industry-analysis/general-and-advanced-materials

Why the Shift Matters: Challenges and Opportunities

The rise of non-silicon optical materials is not without its challenges. The high cost and complex manufacturing processes of materials like chalcogenides and photonic crystals are significant barriers to widespread adoption. Furthermore, while these materials offer advantages in specialized applications, their scalability and stability in large-scale, real-world applications are still under study.

Despite these challenges, the potential of these materials cannot be overstated. As industries such as telecommunications, medical diagnostics, and quantum computing continue to grow, the need for more efficient, customizable, and high-performance optical materials will drive the market forward. Non-silicon materials, with their unique capabilities, offer the opportunity to solve problems that silicon-based technologies cannot address.

For example, chalcogenides are already pushing the boundaries of infrared communication, offering lower energy consumption and higher data transfer speeds than traditional materials. Organic polymers are revolutionizing consumer electronics, enabling the development of flexible, lightweight devices that could pave the way for new forms of wearable technology. Meanwhile, photonic crystals are opening up possibilities for secure, high-speed quantum communication, which is set to be the next frontier in global cybersecurity.

The Future of the Optical Materials Market

The evolution of the optical materials market is being driven by the increasing demand for materials that offer more than what traditional silicon can provide. Chalcogenides, organic polymers, and photonic crystals are at the forefront of this shift, offering unique properties that will redefine the way light is used in a variety of industries. As research into these materials progresses and manufacturing processes become more cost-effective, we can expect them to play a pivotal role in the next generation of photonic devices.

According to Future Market Insights, the market is projected to grow from USD 11,164.8 million in 2025 to USD 18,872.6 million by 2035, at a CAGR of 5.4% during the forecast period.

Key Segmentations - Optical Materials Market

By Product Type:

Glass

Quartz

Polymers

Metals

Others

By End-use Industry:

Consumer Electronics

Energy

Construction

Automotive

Healthcare

Aerospace & Defense

Others

By Region:

North America

Latin America

Europe

South Asia Pacific

East Asia

Middle East & Africa (MEA)

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analystsworldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries. Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

Contact Us:

Future Market Insights Inc. Christiana Corporate, 200 Continental Drive, Suite 401, Newark, Delaware - 19713, USA T: +1-347-918-3531 For Sales Enquiries: [email protected] Website: https://www.futuremarketinsights.com LinkedIn| Twitter| Blogs | YouTube

0 notes

Text

Authentication and Brand Protection Market Size, Share, Analysis, Forecast, and Growth Trends to 2032: Sustainability and Security Go Hand-in-Hand

The Authentication And Brand Protection Market was valued at USD 3.1 billion in 2023 and is expected to reach USD 6.9 billion by 2032, growing at a CAGR of 9.23% from 2024-2032.

Authentication and Brand Protection Market is becoming increasingly vital as global brands face mounting threats from counterfeiting, product diversion, and online fraud. With the rise of e-commerce and globalized supply chains, companies across sectors—particularly in pharmaceuticals, luxury goods, electronics, and food & beverage—are investing in advanced protection technologies to safeguard brand integrity and consumer trust.

Authentication and Brand Protection Market Booms in the US Amid Rising Counterfeiting Threat

the U.S. Authentication And Brand Protection Market was valued at USD 0.7 billion in 2023 and is expected to reach USD 1.6 billion by 2032, growing at a CAGR of 8.97% from 2024-2032

Authentication and Brand Protection Market is seeing a surge in innovation as digital solutions like blockchain, QR-based tracking, and serialization gain traction. These tools not only enhance product traceability but also empower consumers to verify authenticity in real-time, giving brands a critical edge in competitive markets.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6660

Market Keyplayers:

Avery Dennison Corporation – SecureRFID Labels

SICPA Holding SA – SICPATRACE

De La Rue plc – IZON Holograms

Authentix Inc. – Fuel Integrity Program

Zebra Technologies Corporation – Zebra ZXP Series Printers

3M Company – 3M Secure Labeling Solutions

Centro Grafico dg S.p.A. – Diffractive Optical Variable Image Devices (DOVIDs)

OpSec Security Group – OpSec Insight Platform

Aegate (now part of Arvato Systems) – Medicine Verification System

Catalent, Inc. – Serialized Packaging Solutions

TraceLink Inc. – Digital Supply Network

AlpVision SA – FingerPrint Authentication

Systech International – UniSecure

Infineon Technologies AG – OPTIGA Authenticate

Scantrust SA – Secure QR Codes

Market Analysis

The market is driven by escalating counterfeit activities, estimated to cause billions in global losses annually. As consumer awareness grows and governments tighten regulations, brands are under pressure to implement reliable, scalable authentication systems. North America leads due to its early adoption of anti-counterfeit technologies and robust IP enforcement, while Europe shows strong momentum with its regulatory focus on product transparency and traceability.

Market Trends

Increased use of smart packaging and tamper-evident technologies

Blockchain adoption for transparent and immutable supply chains

Cloud-based authentication platforms for scalable deployment

Consumer-facing mobile verification tools

Integration of AI and machine learning for fraud detection

Rising demand for multi-layered authentication in high-risk industries

Government mandates on serialization in pharmaceuticals and food sectors

Market Scope

The Authentication and Brand Protection Market extends across diverse verticals, driven by digital transformation and consumer safety demands. Solutions are evolving from traditional holograms to intelligent systems capable of offering real-time insights and global traceability.

End-to-end supply chain visibility

Real-time authentication via mobile apps

Digital watermarks and encrypted labeling

Integrated compliance tracking

AI-powered threat intelligence platforms

Industry-specific authentication solutions (e.g., pharma, luxury, electronics)

Brand engagement through secure packaging

Forecast Outlook

The market is poised for rapid expansion, fueled by rising global trade, complex distribution channels, and increasing reliance on online retail. The future of brand protection will center around intelligent, interoperable, and proactive systems. Strategic partnerships between tech providers and brand owners will define the next wave of innovation, with regional growth powered by strong enforcement and digital readiness in both the US and Europe.

Access Complete Report: https://www.snsinsider.com/reports/authentication-and-brand-protection-market-6660

Conclusion

In a world where consumer trust can be won or lost in a click, the Authentication and Brand Protection Market is not just a defensive strategy—it’s a growth enabler. As brands seek to secure value and stand out in saturated markets, investing in robust, smart authentication solutions is becoming a strategic imperative.

Related Reports:

U.S.A businesses are rapidly adopting Zero Trust Security to safeguard critical data

U.S.A businesses are rapidly shifting towards passwordless authentication solutions

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Authentication and Brand Protection Market#Authentication and Brand Protection Market Scope#Authentication and Brand Protection Market Growth

0 notes

Text

Thermal Binocular Market Size, Insights and Trends to 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Thermal Binocular Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Thermal Binocular Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Thermal Binocular Market?

The global thermal binocular market size reached US$ 126.5 million in 2023. Looking forward, Reports and Insights expects the market to reach US$ 170.9 million in 2032, exhibiting a growth rate (CAGR) of 3.4% during 2024-2032.

What are Thermal Binocular?

Thermal binoculars are advanced optical devices that use thermal imaging technology to detect and visualize heat emitted by objects, rather than relying on visible light. By utilizing infrared sensors, these binoculars convert thermal radiation into a visible image, allowing users to see in total darkness or through obstructions such as fog, smoke, or haze. They are widely used in military, law enforcement, search and rescue operations, and wildlife observation, offering improved visibility and situational awareness in difficult conditions.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1904

What are the growth prospects and trends in the Thermal Binocular industry?

The thermal binoculars market growth is driven by various factors and trends. The thermal binoculars market is expanding due to rising demand for sophisticated imaging technology in sectors such as military, law enforcement, search and rescue, and outdoor activities. This growth is fueled by advancements in thermal imaging technology, increased security concerns, and the need for better visibility in difficult conditions. The market offers a range of products suited for various applications, from tactical and professional to recreational uses. North America and Europe lead the market due to their robust defense and security industries, while the Asia-Pacific region is also seeing notable growth, driven by increased investments in security and defense technologies. Hence, all these factors contribute to thermal binoculars market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Technology:

Uncooled

Cooled

By Type:

Handheld

Helmet-Mounted

Weapon-Mounted

By Application:

Defense and Military

Law Enforcement and Security

Search and Rescue

Hunting and Wildlife Observation

Outdoor Activities and Sports

By Range:

Short Range

Medium Range

Long Range

By Resolution:

Low Resolution

Medium Resolution

High Resolution

By End-User:

Government and Defense Agencies

Law Enforcement Agencies

Commercial Sector

Individuals

By Sales Channel:

Online Retail

Offline Retail

By Price Range:

Low Cost

Mid-Range

Premium

By Distribution Channel:

Direct Sales

Distributors/Resellers

Segmentation By Region:

North America:

United States

Canada

Europe:

Germany

The U.K.

France

Spain

Italy

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

India

Japan

South Korea

Australia

New Zealand

ASEAN

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

Middle East & Africa:

Saudi Arabia

United Arab Emirates

South Africa

Egypt

Israel

Rest of MEA.

Who are the key players operating in the industry?

The report covers the major market players including:

FLIR Systems, Inc.

L3Harris Technologies, Inc.

BAE Systems plc

Thales Group

Leonardo S.p.A.

Raytheon Technologies Corporation

Axis Communications AB

Hikvision Digital Technology Co., Ltd.

Harris Corporation

Bosch Security Systems, Inc.

Armasight Inc. (FLIR)

ATN Corporation

Zeiss Group

View Full Report: https://www.reportsandinsights.com/report/Thermal Binocular-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

🔍 A Close Look at Lenses — Trade Snapshot

Lenses play a pivotal role in industries like medical imaging, photography, and optical equipment. Their demand has driven a sharp rise in global trade — especially among tech-savvy nations.

🌏 Top Exporting Countries: 🇨🇳 China 🇯🇵 Japan 🇩🇪 Germany

📦 Leading Importers: 🇺🇸 USA 🇫🇷 France 🇮🇳 India

🔬 Major Sectors: Medical optics, cameras, high-tech instruments

📊 Market Movement: Exports to North America are rising, and Asia remains the hub of optical manufacturing.

📖 For a detailed look at lens exports, imports, and country-wise analysis: 👉 Read Full Blog

0 notes

Text

In Vivo Preclinical Brain Imaging Devices Market Size, Share, Demand, Future Growth, Challenges and Competitive Analysis

Global In Vivo Preclinical Brain Imaging Devices Market - Size, Share, Demand, Industry Trends and Opportunities

Global In Vivo Preclinical Brain Imaging Devices Market, By Imaging Modality Type (MRI, PET/SPECT, CT, Optical Miniscopes, 2 Photon Confocal, US, NIR Fluorescence, OCT, Bioluminescence, and Others), Application (Drug Discovery, Disease Characterization, and Toxicology), Therapeutic Area (Alzheimer’s Disease, Parkinson's Disease, Oncology, and Other Therapeutic Areas), Biological Variable (BOLD, Oxygenation, Blood Flow, Microvessels, Neuronal Activity, and Soft Tissue), Temporal Format of Use (Under an Hour, Many Hours, and Longitudinal), End User (Pharma-Inhouse, CRO, Academia, and Others) - Industry Trends.

Access Full 350 Pages PDF Report @

**Segments**

- By Product Type: The market can be segmented into MRI Systems, CT Systems, PET Systems, SPECT Systems, and Other Imaging Systems. MRI systems are expected to dominate the market due to their ability to provide detailed anatomical images of the brain.

- By Modality: The market can be segmented into Standalone Devices and Multimodal Devices. Standalone devices are expected to witness significant growth as they offer specific imaging capabilities focused solely on brain imaging.

- By End-User: The market can be segmented into Hospitals, Diagnostic Centers, Research Institutes, and Others. Hospitals are anticipated to be the largest end-user segment due to the high prevalence of neurological disorders requiring brain imaging services.

- By Geography: The market can be segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. North America is expected to lead the market owing to technological advancements and high healthcare spending in the region.

**Market Players**

- Aspect Imaging - Bruker - MR Solutions - Trifoil Imaging - Mediso Ltd. - MILabs B.V. - Agilent Technologies, Inc. - SCANCO Medical - Hitachi, Ltd. - NeuroLogica Corp. - Thermo Fisher Scientific - Siemens Healthcare GmbH - PerkinElmer Inc. - GE Healthcare - Canon Inc.

These market players are focusing on strategic collaborations, product launches, and acquisitions to gain a competitive edge in the market. The increasing investment in research and development activities by these players is expected to drive market growth in the coming years.

https://www.databridgemarketresearch.com/reports/global-in-vivo-preclinical-brain-imaging-devices-marketThe global in-vivo preclinical brain imaging devices market is experiencing significant growth driven by various factors such as technological advancements in imaging modalities, increasing prevalence of neurological disorders, and the rising demand for early and accurate diagnosis. MRI systems are expected to dominate the market due to their ability to provide detailed anatomical images of the brain, allowing for precise analysis and diagnosis of neurological conditions. The market segmentation by modality into standalone and multimodal devices further highlights the trend towards standalone devices witnessing significant growth, as they offer focused brain imaging capabilities catering to specific research and diagnostic requirements.

In terms of end-users, hospitals are anticipated to be the largest segment due to the high prevalence of neurological disorders that necessitate advanced brain imaging services for accurate diagnosis and treatment planning. Moreover, the segmentation by geography indicates that North America is poised to lead the market, primarily attributed to the region's robust healthcare infrastructure, technological advancements, and high healthcare spending. These factors create a conducive environment for the adoption of in-vivo preclinical brain imaging devices in the region.

The market players in the global in-vivo preclinical brain imaging devices market are actively engaged in strategic initiatives to gain a competitive edge. These include collaborations, product launches, and acquisitions aimed at expanding their product portfolios, enhancing technological capabilities, and strengthening their market presence. The focus on research and development activities by these key players is expected to drive innovation, leading to the introduction of advanced imaging solutions that address the evolving needs of researchers and healthcare professionals.

Furthermore, advancements in imaging technologies such as PET systems, SPECT systems, and other imaging systems are expected to offer new opportunities for market growth, enabling enhanced visualization and analysis of brain structures and functions. With a growing emphasis on precision medicine and personalized healthcare, the demand for in-vivo preclinical brain imaging devices is anticipated to rise, driven by the need for early detection and monitoring of neurological conditions.

In conclusion, the global in-vivo preclinical brain imaging devices market is poised for substantial growth, fueled by advancements in imaging technologies, increasing disease burden, and strategic efforts by market players to innovate and expand their market presence. The evolving landscape of brain imaging technologies presents exciting prospects for improved diagnosis, treatment planning, and research in the field of neuroscience.The global in-vivo preclinical brain imaging devices market is witnessing significant growth driven by various factors contributing to the expansion of the industry. One of the key drivers is the continuous technological advancements in imaging modalities, enabling healthcare professionals and researchers to acquire high-quality, detailed images of the brain for accurate diagnosis and treatment planning. MRI systems, known for their ability to provide precise anatomical images of the brain, are expected to dominate the market due to their effectiveness in analyzing neurological conditions. These advanced imaging systems play a crucial role in enhancing the understanding of brain structures and functions, thereby supporting research efforts and clinical decision-making processes.

Moreover, the increasing prevalence of neurological disorders globally is creating a growing demand for in-vivo preclinical brain imaging devices. Early and accurate diagnosis of conditions such as Alzheimer's disease, Parkinson's disease, and stroke is crucial for effective disease management and patient outcomes. As a result, healthcare facilities, especially hospitals, are adopting these advanced imaging technologies to cater to the rising need for brain imaging services. The availability of these devices in diagnostic centers and research institutes is also contributing to market growth by facilitating scientific research and academic endeavors related to brain health and disorders.

The market segmentation based on geography reveals that North America is expected to lead the global in-vivo preclinical brain imaging devices market. This is primarily due to the region's advanced healthcare infrastructure, significant technological innovations, and substantial investments in healthcare. The presence of key market players in North America further contributes to the region's dominance in the market, fostering collaborations and strategic partnerships to drive market expansion and product development initiatives. Europe, Asia-Pacific, South America, and the Middle East & Africa regions also present growth opportunities for the market, fueled by increasing awareness about neurological conditions and the adoption of advanced imaging solutions.

In terms of market players, the industry is characterized by intense competition and dynamic innovation. Companies such as Siemens Healthcare, GE Healthcare, Hitachi, and Canon are actively involved in strategic initiatives to enhance their market presence and gain a competitive edge. Collaborations, product launches, and acquisitions are common strategies employed by these players to expand their product portfolios, introduce new technologies, and meet the evolving needs of customers. The focus on research and development activities is paramount, as it enables companies to stay ahead of the curve in terms of technological advancements and product differentiation.

Looking ahead, the global in-vivo preclinical brain imaging devices market is poised for continued growth, driven by ongoing advancements in imaging technologies, increasing healthcare needs, and a strong emphasis on precision medicine. The industry is expected to witness further innovation, leading to the development of cutting-edge imaging solutions that will revolutionize the way brain disorders are diagnosed, monitored, and treated. As the demand for early detection and personalized healthcare services rises, the market players will continue to play a pivotal role in shaping the future of brain imaging technology and its applications in healthcare and research domains.**Segments**

- Global In Vivo Preclinical Brain Imaging Devices Market, By Imaging Modality Type (MRI, PET/SPECT, CT, Optical Miniscopes, 2 Photon Confocal, US, NIR Fluorescence, OCT, Bioluminescence, and Others), Application (Drug Discovery, Disease Characterization, and Toxicology), Therapeutic Area (Alzheimer’s Disease, Parkinson's Disease, Oncology, and Other Therapeutic Areas), Biological Variable (BOLD, Oxygenation, Blood Flow, Microvessels, Neuronal Activity, and Soft Tissue), Temporal Format of Use (Under an Hour, Many Hours, and Longitudinal), End User (Pharma-Inhouse, CRO, Academia, and Others) - Industry Trends and Forecast to 2030.

The global in-vivo preclinical brain imaging devices market is a dynamic landscape driven by various segments that cater to specific imaging needs, applications, therapeutic areas, biological variables, temporal formats of use, and end-user preferences. The market segmentation based on imaging modality type highlights a diverse range of technologies such as MRI, PET/SPECT, CT, Optical Miniscopes, 2 Photon Confocal, US, NIR Fluorescence, OCT, Bioluminescence, and others, each offering unique capabilities for brain imaging in preclinical settings. These modalities serve different purposes in drug discovery, disease characterization, and toxicology studies, contributing to the comprehensive understanding of neurological conditions and their impact on brain function.

Within the therapeutic area segment, the market addresses key neurological disorders such as Alzheimer’s Disease, Parkinson's Disease, Oncology, and Other Therapeutic Areas, reflecting the broad applications of in-vivo preclinical brain imaging devices in research and drug development for various brain-related conditions. The consideration of biological variables such as BOLD, Oxygenation, Blood Flow, Microvessels, Neuronal Activity, and Soft Tissue further enhances the precision and depth of brain imaging data, enabling researchers to investigate different aspects of brain function and pathology.

Moreover, the temporal format of use segmentation categorizes the use of imaging devices based on time intervals, including Under an Hour, Many Hours, and Longitudinal, which align with the specific research requirements and study protocols in preclinical settings. This segmentation provides flexibility and adaptability in imaging sessions, allowing for tailored approaches to data collection and analysis based on the study objectives and experimental design.

The end-user segmentation highlights the diverse stakeholders in the market, including Pharma-Inhouse, Contract Research Organizations (CROs), Academia, and others, who rely on in-vivo preclinical brain imaging devices for research, drug development, and academic pursuits. Each end user brings unique perspectives and demands to the market, influencing the development and adoption of brain imaging technologies in preclinical research settings.

In conclusion, the segmentation of the global in-vivo preclinical brain imaging devices market into various categories such as imaging modality type, application, therapeutic area, biological variable, temporal format of use, and end user underscores the multifaceted nature of the industry. The integration of advanced imaging technologies with diverse applications and user preferences positions the market for continued growth and innovation, driving the development of tailored imaging solutions for preclinical brain research and drug discovery. As technology evolves and research needs expand, the market is poised to witness transformative changes that will shape the future of in-vivo preclinical brain imaging and its implications for neuroscience and healthcare.

TABLE OF CONTENTS

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Research Methodology

Part 04: In Vivo Preclinical Brain Imaging Devices Market Landscape

Part 05: Pipeline Analysis

Part 06: Market Sizing

Part 07: Five Forces Analysis

Part 08: Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers and Challenges

Part 13: Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

How the Report Aids Your Business Discretion?

This section of this Market report highlights some of the most relevant factors and growth enablers that collectively ensure a high-end growth spurt

The report unravels details on pronounced share assessments across both country-wise as well as region-based segments

A leading synopsis of market share analysis of dynamic players inclusive of high-end industry veterans

New player entry analysis and their scope of new business models

The report includes strategic recommendations for new business veterans as well as established players seeking novel growth avenues

A detailed consultation services based on historical as well as current timelines to ensure feasible forecast predictions

A thorough evaluation and detailed study of various segments as well as sub-segments across regional and country-specific developments

Details on market estimations, market size, dimensions

A review of market competitors, their high-end product and service portfolios, dynamic trends, as well as technological advances that portray high end growth in this Market

The Report Can Answer the Following Questions:

Who are the global key players of In Vivo Preclinical Brain Imaging Devices industry? How are their operating situation (capacity, production, price, cost, gross and revenue)?

What are the types and applications of In Vivo Preclinical Brain Imaging Devices? What is the market share of each type and application?

What are the upstream raw materials and manufacturing equipment of In Vivo Preclinical Brain Imaging Devices? What is the manufacturing process of In Vivo Preclinical Brain Imaging Devices?

Economic impact on In Vivo Preclinical Brain Imaging Devices industry and development trend of In Vivo Preclinical Brain Imaging Devices industry.

What are the key factors driving the global In Vivo Preclinical Brain Imaging Devices industry?

What are the key market trends impacting the growth of the In Vivo Preclinical Brain Imaging Devices market?

What are the In Vivo Preclinical Brain Imaging Devices market challenges to market growth?

What are the In Vivo Preclinical Brain Imaging Devices market opportunities and threats faced by the vendors in the global In Vivo Preclinical Brain Imaging Devices market?

Browse Trending Reports:

Lunch Bags Market Tattoo Removal Devices Market Time-Sensitive Networking Market Paper Pallets Market Wafer Solar Cell Market Traction Motor Market Oxygenated Solvents Market Portable E Tanks Market Aquafeed Premix Market Clinical Analytics Solution Market Bariatric Patient Care Handling Equipment Market Residential Portable Air Purifier Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]

0 notes

Text

Strategic Analysis of the Preclinical Imaging Industry: Market Size, Share, and Growth Projections

The global preclinical imaging market was valued at USD 4.56 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 4.36% from 2025 to 2030. This growth is primarily driven by rising investments and funding in research and development (R&D), as well as ongoing technological advancements that are enabling the creation of sophisticated hybrid imaging systems. These innovations are playing a crucial role in enhancing the accuracy, speed, and efficiency of preclinical studies across pharmaceutical, biotechnology, and academic research institutions.

Preclinical research is revolutionizing the landscape of modern healthcare by enabling more precise and early-stage insights into disease mechanisms and treatment responses. Preclinical imaging technologies are especially valuable due to their ability to minimize biological variability, gather large volumes of detailed biological data, and reduce the number of animals used in experiments, in alignment with the 3R principles—Replacement, Reduction, and Refinement. This ethical and scientific approach is gaining widespread adoption, particularly as global research institutions focus on more humane and effective methodologies.

The expanding number of clinical research organizations (CROs) and pharmaceutical companies worldwide is also contributing significantly to the market's growth. These entities are increasingly investing in in-vivo imaging systems for drug development and toxicology studies, which require real-time visualization of biological processes at the molecular and cellular levels. As a result, the demand for advanced imaging platforms, including micro-PET, micro-MRI, micro-CT, and optical imaging systems, continues to rise.

The integration of artificial intelligence (AI) into preclinical imaging represents a transformative trend within the industry. AI-driven analytics tools are capable of managing and interpreting vast amounts of complex imaging data, enabling researchers to extract critical insights, enhance diagnostic accuracy, and expedite decision-making in preclinical trials. A notable development in this space occurred in May 2023, when Koninklijke Philips N.V. launched the Philips CT 3500. This high-throughput CT system is designed to meet the rigorous demands of mass screening programs and routine radiology workflows. Equipped with advanced image reconstruction technologies and workflow optimization features, the CT 3500 delivers high-quality, rapid imaging, empowering clinicians and researchers to enhance operational efficiency and diagnostic confidence even in high-volume settings.

Despite these advancements, the market faces challenges stemming from regulatory constraints on animal testing, driven by the increasing influence of animal welfare organizations. These restrictions are prompting a shift toward alternative research methodologies, including in-vitro testing, micro-dosing strategies, computer-simulated models, virtual drug testing, and the creation of comprehensive digital databases for experimental validation. While these alternatives are gaining traction, imaging modalities that offer non-invasive capabilities, such as magnetic resonance imaging (MRI) and computed tomography (CT), continue to see strong adoption. These systems allow for detailed, repeated assessments of biological systems without causing harm, making them ideal for longitudinal studies and further reinforcing their importance in the future of preclinical research.

Get a preview of the latest developments in the Preclinical Imaging Market? Download your FREE sample PDF copy today and explore key data and trends

Detailed Segmentation:

Product Insights

The optical imaging segment held the largest revenue share of 13.6% in 2024 owing to their wide usage in small animal imaging and new drug discovery projects. The growing adoption of optical preclinical imaging can be attributed to several factors.

Application Insights

In terms of application, the research & development segment captured the largest revenue share in 2024. The National Institutes of Health (NIH) conducts clinical research trials for numerous diseases and conditions, including Alzheimer’s disease, neurological disorders, allergies, cancer, and infectious diseases.

End-use Insights

The pharma and biotech companies segment captured the largest revenue share of 39.9% in 2024. The demand for pre-clinical imaging in biotech companies has been steadily increasing in recent years and is expected to continue growing in the coming years. T

Regional Insights

North America preclinical imaging market held the largest revenue share of 30.1% in 2024. This can be attributed to thewell-developed research infrastructure, the availability of skilled professionals, a large number of preclinical projects, and higher adoption rates of technically advanced devices in the region.

Key Preclinical Imaging Companies:

The following are the leading companies in the preclinical imaging market. These companies collectively hold the largest market share and dictate industry trends.

Bruker Corporation,

Siemens A.G.

General Electric(GE)

TriFoil Imaging

PerkinElmer, Inc.

FUJIFILM SonoSite

Mediso Ltd.

Agilent Technologies

MILabs B.V.

MR Solutions

Molecubes

Recent Developments

In April 2024, Spectral Instruments Imaging announced the launch of Aura 4.5, the newest iteration of its in vivo imaging software.

In April 2023, Southern Scientific unveiled its role as the new distributor in the UK for Spectral Instruments Imaging, a leading manufacturer of preclinical in vivo imaging systems.

In April 2023, Scintica, a distributor specializing in advanced preclinical research instrumentation, has announced a new collaboration with Bioemtech, a company focused on desktop SPECT, PET, and Optical scanners used in preclinical research. This partnership aims to broaden the accessibility of Bioemtech’s preclinical instruments to research scientists worldwide.

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Microscopy Market Trends and Innovations Driving Growth Across Healthcare and Scientific Research Fields

The microscopy market has experienced significant growth over recent years, driven by advancements in technology and expanding applications across various industries. Microscopy, the technique of using microscopes to view objects that are not visible to the naked eye, is a critical tool in scientific research, healthcare, materials science, and many other fields. As technological innovations continue to evolve, the microscopy market is poised to expand even further, presenting new opportunities and challenges.

One of the primary factors fueling the growth of the microscopy market is the increasing demand for high-resolution imaging techniques in biomedical research. Researchers rely on advanced microscopy tools to observe cells, tissues, and microorganisms in greater detail, enabling breakthroughs in understanding diseases and developing new treatments. For instance, fluorescence microscopy and confocal microscopy have revolutionized biological research by providing three-dimensional images and precise localization of molecules within cells.

Healthcare is another major driver of the microscopy market. Pathologists and medical researchers use microscopes for diagnostic purposes, including cancer detection and infectious disease identification. With the rising prevalence of chronic diseases and the demand for personalized medicine, there is a growing need for more sophisticated and accurate microscopy techniques. Digital pathology, which combines microscopy with digital imaging and artificial intelligence (AI), is gaining traction as it allows remote diagnostics and automated image analysis, improving efficiency and accuracy.

The materials science sector also heavily relies on microscopy for analyzing the structural properties of metals, polymers, ceramics, and composites. Electron microscopy, including scanning electron microscopy (SEM) and transmission electron microscopy (TEM), is extensively used to study material composition and surface morphology at the nanoscale. This has significant implications for industries such as aerospace, automotive, electronics, and nanotechnology, where understanding material properties is crucial for innovation and quality control.

Technological advancements continue to be a cornerstone of growth in the microscopy market. The development of super-resolution microscopy techniques, such as stimulated emission depletion (STED) microscopy and structured illumination microscopy (SIM), has pushed the boundaries of optical resolution beyond the traditional limits set by light wavelength. These innovations allow scientists to observe molecular interactions and cellular structures with unprecedented clarity.

Another emerging trend is the integration of microscopy with digital technologies, such as AI, machine learning, and big data analytics. These integrations facilitate automated image processing, pattern recognition, and predictive analysis, significantly enhancing the speed and accuracy of microscopy-based research and diagnostics. Portable and smartphone-based microscopes are also becoming popular, especially in remote or resource-limited settings, expanding access to microscopy tools worldwide.

Geographically, the microscopy market is witnessing robust growth in North America and Europe due to well-established research infrastructure, high healthcare expenditure, and strong government funding. Asia-Pacific is emerging as a key region with rapid industrialization, increasing investments in research and development, and growing demand from pharmaceutical and biotechnology companies. The expanding middle class and improving healthcare infrastructure in countries like China and India contribute to market growth in this region.

Despite the promising prospects, the microscopy market faces challenges. The high cost of advanced microscopy equipment and the need for skilled operators can limit adoption, especially in smaller laboratories or in developing countries. Additionally, maintaining and calibrating sophisticated microscopes requires specialized knowledge and resources. Data management and storage are becoming critical issues as microscopy generates large volumes of high-resolution images that require efficient handling and analysis.

Companies in the microscopy market are focusing on product innovation, strategic collaborations, and expanding their global footprint to stay competitive. Major players are investing in research to develop more user-friendly, compact, and affordable microscopy solutions. Furthermore, collaborations between academia, healthcare institutions, and industry are accelerating the translation of microscopy technologies into practical applications.

In conclusion, the microscopy market is on a robust growth trajectory fueled by technological advancements, expanding applications in healthcare and materials science, and increasing global demand for high-resolution imaging. While challenges such as cost and technical complexity exist, ongoing innovations and the integration of digital technologies are likely to overcome these barriers. As microscopy continues to evolve, it will remain an indispensable tool driving scientific discovery and innovation across multiple disciplines.

#MicroscopyMarket#MicroscopyTechnology#BiomedicalResearch#HealthcareInnovation#MaterialScience#ScientificResearch

0 notes

Text

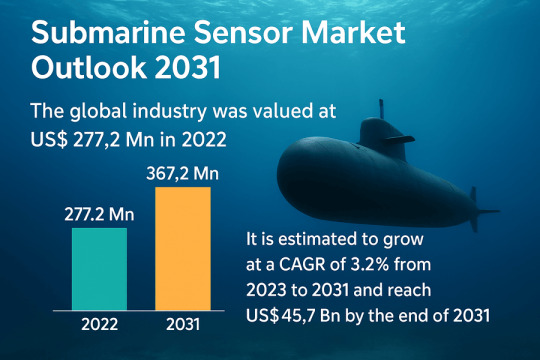

Global Submarine Sensor Market Outlook 2031: Growth Amid Rising Maritime Security Needs

The “Submarine Sensor Market” report offers a comprehensive analysis of the global submarine sensor industry, valued at US$ 277.2 Mn in 2022 and projected to reach US$ 367.2 Mn by the end of 2031, at a steady compound annual growth rate (CAGR) of 3.2% over the forecast period (2023–2031). This press release highlights key findings, recent developments, and strategic insights into market drivers, emerging trends, competitive landscape, and future opportunities.

Market Overview: Submarines are sophisticated naval platforms relying on an array of sensors for communication, navigation, surveillance, and environmental monitoring. The global submarine sensor market encompasses submersible technologies underwater pressure sensors, temperature sensors, motion sensors, and acoustic arrays that gather critical data to ensure operational safety, tactical advantage, and mission success. In 2022, the industry’s valuation stood at US$ 277.2 Mn. With navies worldwide modernizing their fleets amid evolving maritime threats, the market is forecast to grow to US$ 367.2 Mn by 2031, registering a CAGR of 3.2%.

Market Drivers & Trends

High Versatility of Acoustic Sensing Technology

Acoustic sensors dominate underwater communication and navigation due to minimal sound attenuation in saltwater compared to electromagnetic waves. Technologies such as Long Baseline (LBL), Short Baseline (SBL), and Ultra-Short Baseline (USBL) systems enable centimeter-level positioning accuracy, crucial in high-stakes naval operations.

Rise in Demand for Advanced Warfare Capabilities

Geopolitical tensions and naval conflicts, exemplified by the Russia–Ukraine confrontation, are driving defense budgets and accelerating the adoption of AI-assisted smart sensors. These systems lower operator workload, enhance target detection accuracy, and provide real-time threat classification for both offensive and defensive missions.

Integration of Artificial Intelligence & Machine Learning

AI and ML algorithms are transforming sonar and sensor array processing. Automated threat recognition, reduced false-alarm rates, and predictive maintenance analytics are redefining operational readiness.

Latest Market Trends

Miniaturization & Energy Efficiency: Manufacturers are developing smaller, low-power sensors suitable for unmanned underwater vehicles (UUVs) and autonomous systems.

Multi-Modal Sensor Fusion: Combining acoustic, electromagnetic, and fiber optic sensing improves data reliability in complex underwater environments.

Cyber-Resilient Architectures: With growing cyber threats, sensor networks are adopting hardened encryption protocols and anti-tampering mechanisms to safeguard communications.

Key Players and Industry Leaders

The competitive landscape is led by established defense and electronics giants investing significantly in R&D, strategic partnerships, and portfolio expansion:

ATLAS ELEKTRONIK

Lockheed Martin

Northrop Grumman

DRS Technologies

Ducommun

Safran Electronics & Defense

Raytheon

Thales Group