#Robotic Process Automation in Aerospace Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

1,644 Tumblr posts in 1 second.

Text

Global Robotic process automation in Aerospace market was valued at 6.5 billion is expected to grow at a skyrocket CAGR of ~24% during the forecast period (2023-2030).

0 notes

Text

#Robotic Process Automation In Aerospace In Aerospace Market#Robotic Process Automation In Aerospace In Aerospace Market Trends#Robotic Process Automation In Aerospace In Aerospace Market Growth#Robotic Process Automation In Aerospace In Aerospace Market Industry#Robotic Process Automation In Aerospace In Aerospace Market Research#Robotic Process Automation In Aerospace In Aerospace Market Report

0 notes

Text

Top 10 Pneumatic Actuator Brands In 2025

The pneumatic actuator market continues to thrive in 2025, driven by advancements in automation and industrial efficiency. Based on comprehensive evaluations by CN10/CNPP research departments, which integrate big data analytics, AI-driven insights, and market performance metrics, here are the leading brands shaping the industry.

1. SMC (SMC Corporation)

Performance & Reliability: As a global leader since 1959, SMC delivers over 10,000 pneumatic components, including high-precision cylinders, valves, and F.R.L. units. Its products are renowned for durability, energy efficiency, and adaptability to extreme industrial conditions. Industry Applications: Widely used in automotive manufacturing, semiconductor production, and robotics, SMC’s actuators ensure seamless automation across 80+ countries. Its China-based facilities, established in 1994, serve as a primary global production hub.

2. FESTO (Festo AG & Co. KG)

Performance & Reliability: With nearly a century of expertise, Festo combines innovative engineering with IoT-enabled solutions. Its actuators emphasize precision control, low maintenance, and compatibility with smart factory ecosystems. Industry Applications: Festo dominates sectors like pharmaceuticals, food processing, and renewable energy, offering customized automation systems that enhance productivity and sustainability.

Other Notable Brands In The 2025 Rankings

While SMC and Festo lead the list, the following brands also excel in specific niches:

Brand A: Specializes in compact actuators for medical devices.

Brand B: Focuses on heavy-duty applications in construction machinery.

Brand C: Pioneers eco-friendly designs with reduced carbon footprints.

Key Trends Driving Market Growth

Smart Automation: Integration of AI and real-time monitoring in actuator systems.

Sustainability: Energy-efficient designs aligned with global decarbonization goals.

Customization: Tailored solutions for niche industries like aerospace and biotechnology.

This ranking underscores the critical role of innovation and adaptability in maintaining competitive advantage. Brands that prioritize R&D and cross-industry collaboration are poised to lead the next decade of pneumatic automation.

If you want to learn more about low-priced products, please visit the following website: www.xm-valveactuator.com

2 notes

·

View notes

Text

China Recruitment Results 2025: Trends, Insights, and Analysis

As the arena's second-biggest economy, China is still a primary player within the international exertions marketplace. The today's recruitment effects from 2025 display key trends and insights across industries, demographics, and regions. Companies, activity seekers, and policymakers alike can gain from know-how these shifts, as they replicate China's evolving economic landscape, expertise priorities, and marketplace demands.

Recruitment Process In China

1. Strong Recovery in Recruitment Activity

In 2025, China’s recruitment market noticed a incredible rebound, following years of pandemic-associated disruptions and financial uncertainty. According to statistics from a couple of human resources and exertions market tracking agencies, general job openings in China increased through about 12% 12 months-on-12 months. This growth turned into frequently driven via sectors which include generation, renewable power, superior production, and modern-day offerings, which includes finance and healthcare.

The surge in recruitment pastime is basically attributed to China’s push closer to monetary modernization and innovation, aligning with the government’s "14th Five-Year Plan" and its vision for incredible development. Furthermore, easing COVID-19 restrictions inside the past two years has revitalized domestic demand, especially in urban centers like Shanghai, Shenzhen, and Beijing, wherein expertise demand stays high.

2. Sector-by using-Sector Breakdown

Technology Sector

China’s tech enterprise stays one in every of the most important recruiters in 2025, with hiring increasing with the aid of 15% in comparison to 2024. Companies running in regions such as synthetic intelligence (AI), semiconductor production, cloud computing, and 5G/6G network infrastructure are main the demand. In precise, the AI and automation sectors skilled document-breaking recruitment, as agencies throughout numerous industries put into effect virtual transformation techniques.

Manufacturing and New Energy

Advanced manufacturing—together with robotics, aerospace, and electric vehicles (EVs)—recorded an eleven% uptick in hiring. With China striving to grow to be a global leader in EV production and inexperienced technology, recruitment in battery generation, renewable energy engineering, and environmental technology has also elevated. The expansion of sun and wind electricity initiatives in inland provinces which include Inner Mongolia and Xinjiang has opened new activity opportunities out of doors main metropolitan hubs.

Financial and Business Services

Financial offerings confirmed a moderate but consistent 7% increase in hiring, in particular in fintech, funding banking, and risk management roles. The fast adoption of virtual finance systems and the growth of inexperienced finance initiatives contributed to this upward fashion. Similarly, prison and compliance departments saw a surge in call for, as stricter regulatory requirements and international exchange dynamics precipitated corporations to strengthen their internal controls.

Healthcare and Life Sciences

China’s growing old populace and the authorities's focus on enhancing healthcare infrastructure have boosted hiring within the medical and pharmaceutical sectors. Hospitals, biotech firms, and healthtech startups elevated recruitment via nine% yr-on-12 months. Special emphasis become placed on roles associated with scientific research, clinical trials, and public fitness management, reflecting China's ambitions to beautify its healthcare resilience.

Three. Regional Disparities in Recruitment

While Tier 1 towns like Beijing, Shanghai, Guangzhou, and Shenzhen hold to dominate in phrases of activity vacancies, there was a major uptick in hiring in Tier 2 and Tier 3 towns, which includes Chengdu, Hangzhou, Xi’an, and Suzhou. The government’s urbanization strategy and nearby improvement rules are riding this shift. Inland provinces and less-advanced regions are actually attracting extra investment, main to activity advent in industries along with logistics, e-trade, and smart production.

This geographic diversification is also related to the upward thrust of far off work, as agencies come to be more bendy in hiring talent from diverse locations. As a end result, skilled specialists are now not limited to standard financial hubs and are finding competitive possibilities in rising cities.

4. Recruitment Challenges: Skills Gaps and Talent Shortages

Despite the overall high quality recruitment results, several sectors pronounced continual demanding situations, specially regarding skills shortages in high-tech and specialised fields. For instance, the semiconductor enterprise keeps to stand a essential gap in skilled engineers and researchers, while the inexperienced electricity area is struggling to find sufficient skilled task managers and technical experts.

Soft abilties consisting of leadership, go-cultural communique, and trouble-fixing also continue to be in excessive demand, mainly as Chinese organizations make bigger their global operations. Talent shortage has led to accelerated competition among employers, riding up salaries for niche roles and prompting groups to make investments extra heavily in inner schooling and improvement packages.

Five. Demographic Shifts: Youth Employment and Aging Workforce

Youth employment remains a complicated problem in China. While job opportunities for younger graduates have grown along financial recuperation, excessive competition and high expectancies hold to pose demanding situations. The countrywide young people unemployment charge stood at about 14% in early 2025, slightly decrease than in 2024 but nonetheless a subject for policymakers.

In reaction, the authorities has expanded employment subsidies, vocational education initiatives, and entrepreneurship programs focused on young human beings. Additionally, more college students are choosing internships, apprenticeships, and industry-connected educational pathways to decorate employability earlier than commencement.

Meanwhile, the getting old group of workers provides its very own set of challenges. Industries including manufacturing, logistics, and healthcare are increasingly more searching out ways to preserve older employees through re-skilling applications and flexible work preparations.

6. Trends in Hiring Practices

Recruitment practices in China are evolving, with organizations leveraging AI-pushed recruitment equipment, virtual exams, and facts analytics to streamline hiring processes. Many organizations now prioritize candidate experience, the use of era to lessen time-to-lease and improve engagement at some point of the recruitment cycle.

Campus recruitment remains a key approach for principal agencies, mainly in sectors which includes generation, finance, and engineering. However, there may be a developing desire for hiring candidates with realistic revel in, main to greater collaboration between universities and companies to offer industry-relevant guides and internships.

Diversity and inclusion are also gaining traction. Companies are increasingly dedicated to gender balance and hiring talent from numerous backgrounds, which include ethnic minorities and worldwide candidates, specially within the tech and R&D sectors.

7. Outlook for 2025 and Beyond

Looking in advance, China’s recruitment panorama is predicted to remain dynamic. The persisted improvement of emerging sectors consisting of quantum computing, biotechnology, smart towns, and the metaverse will create new employment opportunities, specially for skills with interdisciplinary ability sets.

Policy shifts, which includes similarly liberalization of the hard work market and supportive measures for small and medium corporations (SMEs), may also stimulate job advent. Additionally, the emphasis on sustainable improvement and digital innovation is in all likelihood to reshape hiring priorities, with an growing awareness on inexperienced jobs and virtual literacy.

However, geopolitical uncertainties, change tensions, and worldwide monetary fluctuations will remain key elements influencing China’s hard work marketplace within the close to destiny. Businesses and activity seekers alike will need to stay agile, adapting to changing financial situations and technological advancements.

#Recruitment Process In China#12th pass students apply#college pass students apply china government recruitment result

2 notes

·

View notes

Text

Industrial Efficiency Gains Spark Growth in Torque Limiter Market

The global Torque Limiter Market was valued at US$ 324.9 Mn in 2023 and is projected to grow at a CAGR of 5.8% from 2024 to 2034, reaching US$ 597.4 Mn by the end of the forecast period. Increasing demand for machine safety, process efficiency, and the integration of advanced technologies is fueling this robust expansion.

Market Overview: Torque limiters, essential components in mechanical systems, play a critical role in protecting machinery from damage due to overload conditions. They disengage the drive system when preset torque levels are exceeded, ensuring operational safety and minimizing downtime.

The ongoing transition to smart manufacturing, fueled by Industry 4.0, is significantly contributing to the adoption of torque limiters. Industries such as automotive, aerospace, and renewable energy are the largest consumers of these components due to their need for precision, reliability, and safety.

Market Drivers & Trends

Automation in Production Processes: The proliferation of automation, especially in developing economies, is a major growth driver. Smart factories demand precise safety mechanisms, prompting widespread integration of torque limiters.

Electric Vehicle Growth: Torque limiters are essential in protecting sensitive EV components from torque surges. The EV boom, especially in Asia and Europe, is translating to increased product demand.

Wind Energy Integration: As wind turbines face varying loads, torque limiters prevent mechanical failure, ensuring operational reliability. This is particularly significant as global wind capacity surpassed 900 GW in 2023.

Latest Market Trends

Smart Torque Limiters: IoT-enabled limiters with real-time monitoring capabilities are becoming mainstream. These systems offer predictive maintenance and better control, aligning with smart factory goals.

Customization and Miniaturization: With the rise of compact machinery and robotics, manufacturers are offering smaller and application-specific torque limiters.

Sustainability and Energy Efficiency: Modern torque limiters are being designed with a focus on energy savings, lighter materials, and recyclability to meet environmental standards.

Key Players and Industry Leaders

The market is moderately fragmented with the presence of prominent players including:

Chr. Mayr GmbH + Co. KG

R+W Antriebselemente GmbH

KTR Systems GmbH

Nexen Group, Inc.

Tsubakimoto Chain Co.

Altra Industrial Motion Corp.

RINGSPANN GmbH

Howdon Power Transmission Ltd.

These companies are investing heavily in R&D, digital capabilities, and strategic partnerships to enhance their offerings and global presence.

Explore the highlights and essential data from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=32813

Recent Developments

Regal Rexnord Corporation (June 2023) launched the next-gen Autogard F400 Series torque limiter with enhanced performance and drop-in compatibility.

ENEMAC (May 2023) introduced the ECP torque limiter featuring an integrated ball bearing for superior concentricity and overload protection in indirect drives.

U.S. Tsubaki (2020) unveiled a torque limiter sprocket assembly combining torque control and drive in a single unit, offering ease of installation and reliability.

Market Opportunities

Emerging Economies: Expanding industrial bases in India, Southeast Asia, and Latin America present substantial growth avenues, especially with increasing government investments in automation.

Retrofit Solutions: As legacy equipment needs upgrades to comply with safety norms, torque limiter retrofits offer a lucrative opportunity.

Predictive Maintenance Services: There’s rising demand for service models that combine hardware with analytics-driven maintenance, particularly in high-risk environments.

Future Outlook

According to industry analysts, the torque limiter market is on a steady trajectory, driven by the convergence of smart manufacturing, safety standards, and sustainable industrial practices. The integration of torque limiters into predictive maintenance ecosystems and their indispensable role in electrification will sustain long-term market momentum.

While higher upfront costs of advanced models may pose a challenge in cost-sensitive regions, the return on investment in terms of reduced downtime and equipment longevity makes a compelling case for adoption.

Market Segmentation

By Type:

Friction Type

Ball & Roller Type (Dominated market with 65.6% share in 2023)

Others

By Torque Range:

< 150 Nm

151–500 Nm

501–3000 Nm (Held 35.9% market share in 2023)

3000 Nm

By End-user Industry:

Automotive

Aerospace

Energy & Power

Fabricated Metal Manufacturing

Food & Beverage

Packaging & Labelling

Plastic & Rubber

Others

Regional Insights

Europe leads the global torque limiter market, accounting for 32.6% of global revenue in 2023. Germany, France, and the U.K. are key contributors due to their strong automotive and manufacturing sectors. Europe’s focus on Industry 4.0, energy efficiency, and safety regulations underpins its market leadership.

North America follows closely with 29.3% share, driven by its robust industrial base and emphasis on advanced automation. The U.S. and Canada are adopting IoT-enabled torque limiters in line with smart factory initiatives.

Asia Pacific is witnessing rapid growth due to massive industrialization and the EV boom in China, India, and Japan. The region is also the fastest-growing market in terms of volume consumption.

Why Buy This Report?

Gain in-depth understanding of the torque limiter market dynamics, including macroeconomic trends and sector-specific drivers.

Access historical data (2020–2023) and forecasts (2024–2034) for strategic planning.

Evaluate key opportunities by segment, region, and application.

Review competitive benchmarking and company profiles of major and emerging players.

Identify investment and partnership opportunities in emerging regions and technologies.

Frequently Asked Questions (FAQs)

Q1: What is the projected size of the torque limiter market by 2034? A1: The market is expected to reach US$ 597.4 Mn by 2034, growing at a CAGR of 5.8%.

Q2: Which industry is the largest consumer of torque limiters? A2: The automotive industry is the largest, driven by rising EV adoption and drivetrain protection needs.

Q3: What is the fastest-growing torque range segment? A3: The 501–3000 Nm range is the fastest-growing due to demand in heavy machinery and manufacturing.

Q4: Which region dominates the global torque limiter market? A4: Europe, with 32.6% market share in 2023, leads due to its industrial modernization and safety regulations.

Q5: What are the latest innovations in the torque limiter market? A5: Innovations include IoT-enabled smart torque limiters, predictive maintenance integration, and lightweight materials.

Q6: Who are the key market players? A6: Major players include Chr. Mayr GmbH + Co. KG, KTR Systems GmbH, Tsubakimoto Chain Co., and Nexen Group, Inc.

Explore Latest Research Reports by Transparency Market Research:

GMC based Motion Controller Market: https://www.transparencymarketresearch.com/gmc-based-motion-controller-market.html

Metal Oxide Varistors Market: https://www.transparencymarketresearch.com/metal-oxide-varistors-market-2018-2026.html

GaN on Diamond Semiconductor Substrates Market: https://www.transparencymarketresearch.com/gan-diamond-semiconductor-substrates-market.html

Humidity Meter Market: https://www.transparencymarketresearch.com/humidity-meter-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Ceramic Coating Market Growth Fueled by Asia-Pacific Industrialization and Automotive Sector Development

The ceramic coating market has emerged as a rapidly growing segment within the advanced materials industry, driven by rising demand for high-performance coatings across various end-use sectors. Ceramic coatings, typically composed of alumina, silicon carbide, titania, and other ceramic compounds, are applied to surfaces to provide enhanced thermal resistance, corrosion protection, chemical resistance, and superior mechanical durability. These coatings are commonly applied using techniques such as thermal spraying, physical vapor deposition (PVD), and chemical vapor deposition (CVD).

One of the primary drivers of the ceramic coating market is the automotive sector. Ceramic coatings are extensively used in vehicles to enhance surface durability, improve heat resistance in engine parts, and provide long-lasting protection for exteriors. With increasing consumer demand for luxury vehicles and the global shift toward electric vehicles (EVs), the use of advanced coatings is anticipated to grow steadily. EVs, in particular, benefit from ceramic coatings for thermal management in battery systems and to ensure longer service life of components.

The aerospace industry also contributes significantly to market growth. Ceramic coatings are used to protect engine components and airframes from extreme temperatures and corrosive environments. In high-altitude and high-speed flight conditions, the materials used in aerospace applications must endure considerable stress. Ceramic coatings offer the necessary protection and performance benefits, making them indispensable in modern aircraft manufacturing and maintenance.

Industrial applications also represent a considerable market share. Power plants, refineries, and chemical processing facilities rely on ceramic coatings to protect critical equipment from wear and corrosion. These coatings enable machinery to operate efficiently even under harsh environmental conditions, reducing downtime and maintenance costs. As industries increasingly focus on operational efficiency and equipment longevity, the demand for durable and resistant coatings is expected to rise.

Another promising area is the healthcare sector, where ceramic coatings are used for medical implants, instruments, and devices. These coatings offer biocompatibility, sterilization resistance, and enhanced surface hardness. With the expansion of medical infrastructure and increasing demand for surgical precision, the role of ceramic coatings in ensuring safety and reliability is becoming more pronounced.

In terms of regional growth, North America holds a significant market share due to its well-established aerospace and automotive industries. The United States, in particular, invests heavily in R&D for defense and space exploration, which fuels the demand for high-performance ceramic coatings. Europe follows closely, with Germany, the UK, and France contributing through advancements in automotive engineering and healthcare technology.

Meanwhile, Asia-Pacific is anticipated to witness the fastest growth over the coming years. Countries like China, India, Japan, and South Korea are investing in automotive manufacturing, infrastructure development, and energy production. Rapid industrialization, combined with favorable government policies and increasing foreign investments, creates a lucrative landscape for ceramic coating manufacturers.

The market is also evolving technologically, with companies focusing on developing eco-friendly and cost-effective coatings. The integration of nanotechnology is enabling the production of ceramic coatings with improved surface adhesion, enhanced properties, and thinner layers. Furthermore, automation and robotics in application processes have improved precision and consistency, contributing to higher adoption across industries.

However, despite its growth potential, the ceramic coating market faces certain challenges. The high cost of raw materials and application processes can hinder widespread adoption, especially among small and medium-sized enterprises. Additionally, the complexity of application techniques often requires skilled professionals, adding to operational costs. Addressing these barriers will be crucial for expanding market penetration and maintaining growth momentum.

The competitive landscape includes major players such as A&A Coatings, Praxair Surface Technologies, Saint-Gobain, Bodycote, and APS Materials, among others. These companies focus on strategic partnerships, mergers and acquisitions, and continuous innovation to strengthen their market positions. Customized solutions and the development of advanced products tailored to specific industrial needs are likely to be the core strategies going forward.

In conclusion, the ceramic coating market is poised for significant growth, driven by technological advancements and increased demand across automotive, aerospace, industrial, and medical sectors. As end-use industries continue to prioritize durability, performance, and sustainability, ceramic coatings will play an increasingly vital role in modern manufacturing and product design.

0 notes

Text

Edge AI Meets Smart Sensors: Real-Time Data Processing Takes the Lead

The global smart sensors market is experiencing unprecedented growth, fueled by rapid digital transformation across industries, rising adoption of IoT-enabled devices, and the integration of artificial intelligence in sensor technologies. As industries shift toward automation, real-time monitoring, and data-driven operations, smart sensors have become the backbone of modern electronic ecosystems.

Unlock exclusive insights with our detailed sample report :

According to recent industry insights, the smart sensors market was valued at USD 45.63 billion in 2023 and is projected to reach USD 145.23 billion by 2031, growing at a CAGR of 15.6% during the forecast period. Key industries including automotive, healthcare, consumer electronics, aerospace, and manufacturing are witnessing a surge in demand for intelligent sensors capable of capturing and processing environmental data with minimal latency.

Market Drivers and Growth Opportunities

1. Proliferation of IoT Devices and Smart Infrastructure The explosion of IoT applications in smart homes, smart cities, and industrial IoT (IIoT) has driven the need for sensors that are not only accurate but also intelligent. These sensors support seamless data transmission and decision-making capabilities in connected ecosystems.

2. Automation and Industry 4.0 Transformation Industries are investing heavily in predictive maintenance, process automation, and robotics. Smart sensors such as temperature, pressure, proximity, and image sensors are at the core of these applications, enabling real-time monitoring and adaptive control in automated systems.

3. Rising Demand in Healthcare Smart sensors are revolutionizing healthcare through wearable technology, patient monitoring devices, and remote diagnostics. With the growing geriatric population and demand for personalized healthcare, sensor integration in medical devices is a key market driver.

4. Growing Popularity of Smart Consumer Electronics From smartphones and smartwatches to AR/VR devices and home appliances, the integration of multi-functional smart sensors is enhancing user experience and device interactivity, contributing to soaring market demand.

5. Environmental Monitoring and Sustainability Climate change and environmental regulations are encouraging governments and industries to adopt smart sensors for air quality, water purity, and pollution monitoring. These solutions are essential for meeting global sustainability goals.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

https://www.datamintelligence.com/customize/smart-sensors-market

Market Segmentation Overview

By Sensor Type: Includes pressure sensors, temperature sensors, image sensors, touch sensors, motion sensors, and gas sensors. Image and motion sensors are gaining traction in automotive and consumer electronics sectors.

By Technology: MEMS (Microelectromechanical Systems), CMOS (Complementary Metal-Oxide-Semiconductor), and optical sensing technologies dominate due to their efficiency, miniaturization, and compatibility with IoT platforms.

By End-Use Industry: Automotive, healthcare, industrial automation, consumer electronics, and aerospace & defense are key application areas. Among them, industrial and healthcare sectors are the fastest growing.

U.S. and Japan Market Insights

United States The U.S. remains a dominant force in smart sensor adoption, driven by strong demand across aerospace, automotive, defense, and healthcare industries. In early 2025, the U.S. Department of Energy announced a $1.2 billion fund for smart grid modernization, which includes significant investment in smart sensors for energy distribution and consumption tracking. Additionally, major tech firms such as Apple, Texas Instruments, and Honeywell are innovating sensor fusion technologies to enable smarter and more efficient devices.

Japan Japan, a global leader in robotics and automation, is rapidly advancing smart sensor deployment in its manufacturing and automotive sectors. With its focus on Smart Factories under “Society 5.0,” Japan is integrating AI-powered sensors into robotics, EVs, and public infrastructure. In March 2025, a leading Japanese electronics manufacturer launched a new line of miniaturized smart sensors for next-generation autonomous vehicles and wearable healthcare devices, underscoring Japan’s strong R&D capabilities.

Latest Trends and Innovations

AI-Embedded Smart Sensors: Integration of edge AI allows sensors to process data locally, improving response times and reducing the load on central systems. This is particularly useful in autonomous vehicles, predictive maintenance, and smart healthcare.

Sensor Fusion for Enhanced Accuracy: Combining multiple sensor inputs (e.g., gyroscope + accelerometer + magnetometer) provides more precise data. This trend is rising in consumer electronics and wearable fitness devices.

Advances in MEMS Technology: MEMS-based sensors are evolving rapidly, enabling lower power consumption and smaller form factors. These are ideal for implantable medical devices and compact electronics.

Energy Harvesting Sensors: To support sustainability, sensors that draw energy from ambient sources like light, heat, or motion are becoming more prominent, especially in remote monitoring and IoT applications.

Cybersecurity in Sensor Networks: As smart sensors become part of critical infrastructure, the importance of secure data transmission and sensor-level encryption is gaining attention, especially in military, healthcare, and smart grid applications.

Buy the exclusive full report here:

Competitive Landscape

The market is moderately consolidated with global players focusing on R&D, strategic collaborations, and geographic expansion to maintain competitiveness. Key players include:

Honeywell International Inc.

STMicroelectronics

Infineon Technologies AG

Robert Bosch GmbH

Texas Instruments Incorporated

TE Connectivity Ltd.

NXP Semiconductors

Analog Devices, Inc.

Siemens AG

Omron Corporation

These companies are pushing the boundaries in multi-sensor integration, AI-powered detection systems, and low-power sensor networks.

Future Outlook and Market Opportunities

1. Smart City Initiatives: Governments across the globe, particularly in the U.S. and Asia, are investing in smart infrastructure. Smart sensors will play a central role in traffic management, lighting, surveillance, and environmental monitoring.

2. Growth in Electric Vehicles (EVs): EVs require a wide array of sensors for battery management, motor control, and safety systems. As EV adoption surges globally, the demand for automotive-grade smart sensors will follow suit.

3. Space and Aerospace Applications: High-reliability smart sensors are being developed for satellites and space missions to monitor pressure, radiation, and temperature in extreme environments.

4. Expanding Use in Agriculture (AgriTech): Smart sensors are increasingly used in precision farming, monitoring soil moisture, crop health, and weather patterns to optimize resource use and productivity.

Stay informed with the latest industry insights-start your subscription now:

Conclusion

The global smart sensors market stands at the intersection of innovation, automation, and connectivity. With widespread applications across industries and increasing integration of AI and IoT, smart sensors are redefining how machines interact with their environments. The market’s rapid expansion—led by the U.S. and Japan—signals a transformative shift toward a more responsive, efficient, and intelligent future. As sensor technologies continue to evolve, businesses and governments alike must harness their full potential to stay ahead in the digital age.

About us:

At DataM Intelligence, we specialize in delivering end-to-end market research and consulting solutions designed to unlock your business potential. By harnessing proprietary insights, market trends, and breakthrough developments, we craft intelligent strategies that drive results.

With a repository of 6,300+ detailed reports across 40+ sectors, we’ve helped over 200 global businesses across 50+ nations achieve growth. From syndicated analysis to tailored research, our dynamic approach addresses the critical intelligence your business needs to thrive.

Contact US:

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: [email protected]

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

#Smart sensors market#Smart sensors market size#Smart sensors market growth#Smart sensors market share#Smart sensors market analysis

0 notes

Text

Temperature Sensor Market Size, Share, and Global Outlook

Devices called temperature sensors are employed in a variety of settings and applications to measure and track temperature. They detect changes in temperature and convert this data into readable signals for analysis or control. These sensors come in different types, including thermocouples, resistance temperature detectors (RTDs), thermistors, and infrared sensors, each suited for specific uses. Temperature sensors are widely used in industries such as manufacturing, automotive, healthcare, and consumer electronics to ensure optimal performance, safety, and efficiency. They play a critical role in processes that require precise thermal regulation, such as climate control systems, medical equipment, and industrial automation, ensuring accurate and reliable temperature monitoring.

According to SPER Market Research, states that Global Temperature Sensor Market is estimated to reach 13.09 USD billion by 2034 with a CAGR of 6.25%.

Drivers:

The need for precise, real-time temperature readings in a variety of sectors, including consumer electronics, manufacturing, automotive, and healthcare, is propelling the global market. Temperature sensors are essential for enhancing operating procedures and controlling energy efficiency. The market's expansion can be ascribed to the growing necessity for industrial automation, improvements in sensor technology, and the growing significance of preserving ideal temperature levels for a range of applications. For instance, Honeywell International has witnessed a significant increase in the use of its cutting-edge temperature sensors because of their potential to improve energy management and facilitate industrial Internet of things (IoT) applications. The need for accurate temperature monitoring is further fueled by the expanding trend of smart homes and connected gadgets.

Request a Free Sample Report: https://www.sperresearch.com/report-store/temperature-sensor-market.aspx?sample=1

Restraints:

The high initial cost of sophisticated sensors is one of the major market barriers, especially in sectors where price sensitivity is an issue. Despite the excellent precision and dependability of these sensors, their price may discourage smaller businesses or those in price-sensitive areas from implementing them. Costs may go up when including cutting edge features like wireless and Internet of Things connectivity. The expensive cost of modern temperature sensors, especially in small-scale operations, may hinder their adoption in some applications, such as pharmaceutical manufacture and food processing. These sectors might opt for less expensive, lower-quality, and less precise temperature sensors in an effort to reduce costs, which could significantly compromise the accuracy and reliability of temperature control. This compromise may lead to suboptimal performance in sensitive applications, potential safety risks, and a higher likelihood of system malfunctions or product defects due to improper thermal regulation.

United States of America held the biggest revenue share in the Global Temperature sensors Market. This dominance is attributed to high adoption rates in various industries like healthcare, aerospace, automotive, and food and beverage. Some of the key market players are STMicroelectronics. NXP Semiconductors, Omega Engineering Inc., Yokogawa Electric Corporation, Murata Manufacturing Co. Ltd., IFM Electronic GmbH and Dwyer Instruments

For More Information, refer to below link: –

Temperature Sensor Market Growth

Related Reports:

Global Retail Automation Market Growth

Global SCARA Robots Market Growth

Follow Us –

LinkedIn | Instagram | Facebook | Twitter

Contact Us:

Sara Lopes, Business Consultant — USA

SPER Market Research

+1–347–460–2899

#Temperature Sensor Market#Temperature Sensor Market Growth#Temperature Sensor Market Share#Temperature Sensor Market Size#Temperature Sensor Market Revenue#Temperature Sensor Market Demand#Temperature Sensor Market Analysis#Temperature Sensor Market Segmentation#Temperature Sensor Market Future Outlook#Temperature Sensor Market Scope#Temperature Sensor Market Challenges#Temperature Sensor Market Competition#Temperature Sensor Market forecast

0 notes

Text

The Rise of Deeptech Startups in India: How Deeptech Funding is Shaping the Future of Innovation

India’s Deeptech Ecosystem: Startups, Investments, and Strategic Growth The Indian deeptech ecosystem has emerged as a powerhouse of innovation, driven by advancements in artificial intelligence, semiconductor design, space technology, and robotics. Over the past three months, the sector has witnessed significant funding inflows, strategic government interventions, and breakthroughs in research commercialization. Startups are leveraging cutting-edge technologies to address both domestic and global challenges, supported by a gro wing network of venture capital firms and policy frameworks. This report examines the current state of deeptech in India, analyzing key sectors, investment trends, and the interplay between public and private stakeholders shaping the future of this dynamic landscape. Know More

Key Sectors Driving Deeptech Innovation

Artificial Intelligence and Multi-Agent Systems AI startups are moving beyond conventional SaaS solutions to build core, infrastructure-level innovations. Alchemyst AI, for instance, is creating multi-agent systems that can embed into enterprise processes. Its AI system, Maya, is designed to act as a digital co-worker in sales development teams, automating complex tasks while enabling more coordinated workflows. Another rising player, Deceptive AI, is pushing the envelope on AGI with advanced capabilities in image synthesis and semantic segmentation, targeting use cases in fashion, media, and design. India’s AI sector is steadily evolving from end-user applications toward fundamental research and systems development with practical, cross-sector deployment potential.

Semiconductor and Hardware Innovation Hardware innovation in India is gaining ground. Mindgrove Technologies reached a key milestone by taping out a 28nm Secure-IoT chip earlier this year. Built using the open-source Shakti core from IIT Madras, this chip has applications in automotive electronics and consumer devices, offering a homegrown alternative to imported components. Government programs such as the Design Linked Incentive (DLI) are playing a critical role by supporting fabless startups and covering R&D costs. Meanwhile, Agnikul Cosmos has demonstrated engineering ingenuity by launching the first rocket powered by a single-piece 3D-printed engine—an achievement that speaks volumes about India’s growing stature in aerospace and additive manufacturing. Read More

Quantum Computing and Robotics Startups in quantum computing are beginning to explore solutions in optimization and cryptographic security, though most applications are still in the lab phase. Robotics, on the other hand, is seeing more immediate commercialization. Sedeman Mechatronics, a venture incubated at IIT Bombay, recently filed for an IPO to raise between ₹800–1,000 crore, aiming to scale its industrial automation systems. Its work in precision manufacturing is especially aligned with national goals like “Make in India” and the growing interest in dual-use technologies that can support both civilian and defense sectors. Explore

Government Initiatives and Policy Support

₹10,000 Crore Fund of Funds for Deeptech A major push came in April 2025 when Commerce Minister Piyush Goyal announced a ₹10,000 crore Fund of Funds to channel long-term capital into early-stage deeptech ventures. Administered by Small Industries Development Bank of India (SIDBI), the scheme focuses on startups working in AI, quantum computing, robotics, and biotech. The initial allocation of ₹2,000 crore is aimed at supporting ventures navigating the difficult transition from lab research to market readiness. This scheme adds to existing initiatives like the Indian Semiconductor Mission (ISM), which backs fabless innovation through grants and collaborative infrastructure.

Academic-Industry Collaboration Institutions such as IIT Madras and IIT Bombay continue to play an outsized role in pushing new ideas from research labs into commercial ecosystems. The Shakti processor project, which powered Mindgrove’s chip, is a prime example of academic innovation meeting market demand. The National Deep Tech Startup Policy (NDTSP) is also expected to ease IP licensing processes and promote closer ties between universities and startups. Over half of India’s deeptech ventures originate from academic environments, making these institutional linkages essential for sustained progress.

Investment Trends and Venture Capital Activity

Surge in Early-Stage Funding Deeptech investments reached $324 million across 35 deals in the first four months of 2025, doubling from $156 million in the same period in 2024. Notable deals include:

Netradyne raised $90 million for its AI-driven fleet management platform.

SpotDraft secured $54 million to expand its AI-based contract management solutions.

Tonbo Imaging garnered $21 million for advanced thermal imaging systems used in defense and automotive sectors.

Generalist funds like Peak XV Partners (formerly Sequoia India) and Blume Ventures are increasingly backing deeptech, diversifying from their traditional SaaS focus. Sector-specific funds like Seafund continue to lead early-stage rounds, with a portfolio emphasizing AI, IoT, and healthcare technologies.

Public Market Momentum The IPO pipeline reflects growing maturity, with MTAR Technologies and Tata Technologies emerging as top gainers in the deeptech sector, posting returns of 2.3% and 1.4%, respectively. Conversely, Olectra Greentech saw a 6.6% decline, highlighting volatility in clean-tech segments amid subsidy revisions.

Seafund’s Role in Shaping the Future of Deeptech Startups in India Seafund, a Bengaluru-based venture capital firm, is at the forefront of supporting India’s deeptech revolution. With a Rs 250 crore Fund II, Seafund plans to invest in 18-20 deeptech startups by FY27, focusing on areas like AI SaaS, mobility, sustainability, semiconductors, and clean energy.

Investment Strategy Seafund’s approach includes:

Early-Stage Focus: Investing from pre-seed to pre-Series A rounds, enabling startups to develop and refine their technologies.

Strategic Support: Providing mentorship, market access, and growth strategies to help startups scale effectively.

Sustainability Commitment: Allocating 20% of its corpus to clean energy and mobility startups, reflecting a commitment to sustainable innovation.

Portfolio Highlights Seafund has already invested in several deeptech startups:

RedWings: Specializes in drone logistics, aiming to revolutionize delivery systems.

Docker Vision: Utilizes AI-driven computer imaging to enhance port operations by accelerating the mobility of shipping containers and assessing their conditions in real-time.

Swapp Design: Develops modular battery swapping solutions using autonomous robots, facilitating efficient energy management for electric vehicles.

Simactricals: Focuses on wireless EV charging technologies, aiming to simplify and expedite the charging process for electric vehicles.

CalligoTech: Develops POSIT-based accelerator hardware for high-precision, low-power HPC solutions seamlessly integrated into enterprise systems.

TakeMe2Space: Builds affordable, radiation-shielded LEO satellites with onboard compute capabilities to power next-gen space-based AI applications.

These investments reflect Seafund’s commitment to fostering innovation in critical areas of deeptech, positioning India as a leader in technological advancements. Read More

Future Outlook and Strategic Recommendations

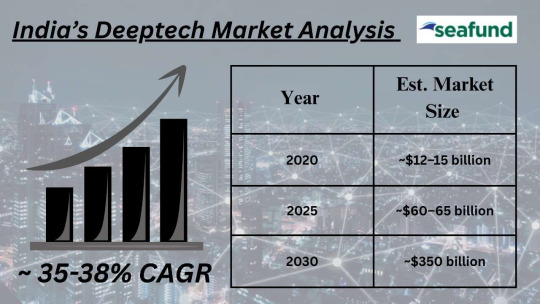

Projected Growth and Global Leadership Inc42 forecasts a 40% CAGR for India’s deeptech sector through 2027, driven by advancements in AI, quantum computing, and space tech. By 2030, the ecosystem is expected to contribute $350 billion to GDP, with startups transitioning from “lab-to-market” at unprecedented scale. Key drivers include:

Increased participation from generalist funds at Series A and beyond.

Expansion of design-linked incentives for semiconductor startups.

Growth in cross-border partnerships, particularly with Japan and the EU in robotics and IoT.

Policy Interventions for Sustained Growth

Accelerate Fund Disbursements: Simplify approval processes for the Fund of Funds to ensure timely access to capital.

Strengthen IP Frameworks: Introduce fast-track patent approvals and tax breaks for IP-driven startups.

Enhance Corporate Engagement: Mandate PSUs (Public Sector Undertakings) to allocate 5% of procurement budgets to deeptech solutions.

India’s deeptech ecosystem stands at an inflection point, buoyed by technological breakthroughs, strategic funding, and policy tailwinds. While challenges like funding gaps and adoption barriers persist, the convergence of academic excellence, entrepreneurial vigor, and global demand positions the country as a future leader in frontier technologies. The next decade will hinge on translating innovation into economic impact, ensuring that deeptech becomes a cornerstone of India’s $10 trillion GDP ambition.

FAQs:

What makes deeptech startups different from regular tech startups? Deeptech startups in India focus on building solutions grounded in advanced scientific research or engineering innovation. Unlike typical tech startups that often rely on existing platforms or business model tweaks, deeptech ventures tackle fundamental problems using technologies like AI, robotics, quantum computing, or space tech—usually requiring longer development timelines and more R&D funding.

Why is deeptech funding on the rise in India now? The sharp rise in deeptech funding—up 78% in 2024—is driven by global demand for advanced technologies, India’s skilled engineering talent pool, and supportive policies. There’s growing investor confidence that Indian startups can build globally competitive solutions in AI, semiconductors, and clean energy, pushing capital into this high-impact sector.

Which deeptech sectors are currently showing the most potential in India? Key areas seeing strong traction include artificial intelligence, which attracted 87% of all deeptech funding in 2024, as well as space tech, quantum computing, robotics, and semiconductors. These fields not only offer commercial potential but also strategic importance for India’s technological self-reliance and global positioning.

What challenges are holding back the growth of deeptech startups in India? The biggest hurdles include a shortage of deeptech talent, long development cycles, and regulatory complexity. Deeptech ventures also face difficulties in accessing early-stage capital due to the technical risk and slower path to profitability, making targeted government and ecosystem support crucial.

Have insights or bold ideas? Drop your thoughts, and let’s shape the next wave of innovation together!

Lets Connect!!

#Keywords#venture capital company#investment in startups#funding for startups#private equity venture capital#capital venture investors#stages of venture capital financing#venture capital investment#venture capital investors#venture capital firm#venture capital firms in india#leading venture capital firms#india alternatives investment advisors#best venture capital firms in india#early stage venture capital firms#venture capital investors in india#early stage investors#seed investors in bangalore#invest in startups bangalore#business investors in kerala#funders in bangalore#startup investment fund#seed investors in delhi#private equity firms investing in aviation#venture investment partners#venture management services#defense venture capital firms#popular venture capital firms#funding for startups in india#early stage funding for startups

0 notes

Text

CNC Turning Services India

Introduction to CNC Turning Services

What is CNC Turning?

CNC turning is one of the most precise and efficient manufacturing techniques available today. At its core, CNC (Computer Numerical Control) turning is a subtractive machining process where a cutting tool removes material from a rotating workpiece. This technique is commonly used to create cylindrical parts and is controlled by pre-programmed computer software. Unlike manual machining, CNC turning enables extreme precision and repeatability, making it ideal for high-volume production and intricate designs.

Imagine trying to carve a perfect cylinder out of metal using just your hands—tough, right? That’s where CNC turning comes in. It's like using a super-smart robot arm that follows digital instructions down to the last micron. Whether it’s producing bolts, screws, engine components, or delicate aerospace parts, CNC turning ensures every item meets exact specifications.

This method supports a wide range of materials, from simple aluminum to more complex alloys, enabling industries to innovate and manufacture with unparalleled consistency and quality.

Importance of CNC Turning in Modern Manufacturing

In today’s fast-paced industrial world, precision isn’t just a luxury—it’s a necessity. From automotive engines to medical implants, even the smallest component must function flawlessly. That’s where CNC turning Services India. It guarantees precision, consistency, and scalability that manual processes simply can’t match.

Why is this important? Think about your car’s engine. Every tiny part needs to be perfectly made or you risk the whole machine breaking down. CNC turning allows manufacturers to produce complex geometries at lightning speed without compromising accuracy.

Moreover, the integration of digital technology into machining has opened up a world of possibilities. Engineers can now simulate processes, reduce errors, and streamline production lines—all thanks to the power of CNC turning.

This technique also supports lean manufacturing principles. With minimal waste, quick turnaround times, and automation, it helps businesses stay competitive while adhering to sustainability goals. Whether it's prototyping or full-scale production, CNC turning is at the heart of modern manufacturing.

Overview of CNC Turning Industry in India

Growth and Expansion of CNC Services in India

India has rapidly emerged as a global hub for CNC machining, and CNC turning is a big part of that success story. Over the past decade, the Indian CNC turning industry has grown significantly, fueled by rising demand from domestic sectors and global markets. Factors like Make in India initiatives, growing foreign investments, and advancements in infrastructure have all contributed to this boom.

Walk through any industrial corridor in India, and you'll find modern CNC shops humming with activity. These are not just job shops—they’re highly organized, tech-savvy businesses catering to industries ranging from automotive to aerospace. According to market analysts, India's CNC machining market is expected to grow by over 7% CAGR between 2024 and 2029.

Part of this growth comes from India's ability to offer a cost-effective yet high-quality solution to global clients. Thanks to the country's rich engineering talent pool and relatively lower operational costs, Indian CNC turning services are in high demand across Europe, North America, and Asia-Pacific.

The shift towards automation and digitization is also accelerating the expansion. Indian manufacturers are investing in high-end CNC machines, robotic arms, and CAD/CAM integration to stay ahead in the global race.

Key Sectors Utilizing CNC Turning in India

CNC turning services are deeply integrated into multiple key sectors across India:

Automotive: India is one of the largest automotive manufacturing hubs in the world. CNC turning is used extensively to produce engine parts, gear components, brake systems, and custom hardware.

Aerospace: From satellite components to aircraft engine parts, CNC turning ensures the extreme precision required in this high-stakes sector.

Medical Devices: CNC turning plays a vital role in crafting surgical tools, orthopedic implants, and dental equipment with unmatched accuracy.

Defense and Military: High-grade components used in weaponry, communication systems, and armored vehicles are all products of CNC turning.

Electronics and Telecommunications: This includes connectors, heatsinks, and enclosures that require tight tolerances and exact dimensions.

India’s diversified industrial base, combined with its technical capabilities, makes it a go-to destination for precision CNC turned components.

Advantages of Choosing CNC Turning Services in India

Cost-Effectiveness and Affordability

One of the biggest reasons companies outsource CNC turning to India is cost-effectiveness. Let’s face it—precision manufacturing in Western countries often comes with a hefty price tag. But India offers a sweet spot: high-quality output at a fraction of the cost.

How’s that possible? Lower labor costs, competitive material sourcing, and optimized operations make Indian CNC service providers some of the most affordable in the world. And we're not talking cheap in quality—just in price. The best shops follow international standards like ISO, TS, or AS certifications, so you’re getting premium-grade components without draining your budget.

Another benefit? Many Indian companies offer flexible pricing models. Whether it’s prototyping, small batch production, or full-scale manufacturing, you can find a service package that fits your needs and budget.

Outsourcing to India also saves on infrastructure costs. You don’t need to invest in machinery, manpower, or maintenance. Just send your design files, and get the parts delivered to your door—fast, affordable, and efficient.

Skilled Workforce and Technical Expertise

India’s engineering education system churns out thousands of skilled professionals every year, and many of them specialize in CNC Turning Services India . From machine programmers to CAD/CAM designers, you’ll find a deep talent pool that knows how to get things done.

More importantly, Indian CNC shops don’t just follow instructions—they understand the "why" behind every cut. This means fewer errors, better optimization, and even design suggestions that can save you money and time.

Many technicians and operators are trained to work on state-of-the-art equipment. Whether it's 3-axis or 5-axis CNC lathes, Swiss-type turning, or robotic automation, the Indian CNC ecosystem is both skilled and future-ready.

And let’s not forget about language. English is widely spoken in the engineering and manufacturing sectors, making communication seamless and effective.

#CNC Turning Services India#CNC Machining Services India#CNC Milling Service India#Cold Forging Services India

0 notes

Text

Raj Industries in India Growth with Quality Manufacturing and Innovation

Raj Industries in india has established itself as a leader in India's manufacturing sector, driven by a commitment to quality, innovation, and efficiency. Specializing in precision-engineered products across various industries, the company has embraced advanced technology and sustainable practices to enhance production standards. With a strong focus on customer satisfaction, Raj Industries ensures durable, high-performance solutions tailored to evolving market needs. Its growth is fueled by continuous research, development, and adaptation to global standards, making it a preferred choice for businesses seeking reliability. By integrating smart manufacturing techniques, Raj Industries is shaping India's industrial landscape and reinforcing its position as a trusted manufacturer.

A Legacy of Excellence in Indian Manufacturing

Raj Industries in India has built a strong reputation for delivering high-quality manufacturing solutions across various industries. From precision-engineered components to large-scale industrial products, the company emphasizes durability, efficiency, and performance. Its journey has been marked by continuous improvement, embracing new technologies to stay ahead in an ever-evolving market. Through its commitment to excellence, Raj Industries has become a trusted name for businesses seeking reliable manufacturing partners. By prioritizing customer satisfaction, maintaining strict quality control, and investing in innovation, the company continues to expand its footprint, reinforcing India’s industrial growth and global competitiveness.

Innovation-Driven Manufacturing Processes

Technological advancements play a key role in Raj Industries’ success, enabling superior manufacturing precision and efficiency. The company has integrated automation, artificial intelligence, and smart manufacturing techniques to enhance product quality and production speed. From CNC machining to robotic assembly, Raj Industries is at the forefront of adopting cutting-edge processes that minimize errors and optimize resources. Research and development drive its innovation, ensuring that the latest materials, designs, and engineering solutions are implemented. This commitment to modern manufacturing standards strengthens India's industrial capabilities and allows Raj Industries to remain competitive in both domestic and international markets.

Commitment to Sustainable and Eco-Friendly Production

Sustainability is a core value at Raj Industries, as the company actively adopts environmentally friendly manufacturing practices. Energy-efficient processes, waste reduction strategies, and the use of recyclable materials ensure minimal environmental impact. Green manufacturing techniques, such as water-saving solutions and low-emission production, align with global sustainability goals. Raj Industries' dedication to sustainability not only benefits the environment but also meets the growing demand for responsible manufacturing from businesses and consumers. By integrating eco-conscious production methods, the company sets a benchmark for sustainable industrial growth in India, contributing to a greener future.

Expanding Industrial Footprint Across Sectors

Raj Industries serves a wide range of industries, including automotive, construction, aerospace, electronics, and healthcare. Its diverse portfolio of products and services ensures that businesses across various sectors receive tailored manufacturing solutions. The company’s versatility in handling complex manufacturing requirements has strengthened its position as a preferred supplier for major corporations. With increasing demand for precision-engineered components, Raj Industries continues to diversify its product offerings, adapting to new industry trends. This expansion highlights its capability to support India’s growing industrial needs while maintaining its reputation for quality and innovation.

Global Reach and Export Capabilities

Raj Industries has successfully expanded beyond India's borders, supplying high-quality products to international markets. Its adherence to global quality standards and competitive pricing has positioned it as a trusted exporter of industrial components. The company maintains strong trade partnerships, leveraging advanced logistics and supply chain management to ensure seamless international distribution. As India's manufacturing sector gains prominence on the global stage, Raj Industries plays a vital role in strengthening the country’s presence in international trade. By meeting diverse market demands, it reinforces India’s reputation as a hub for world-class manufacturing solutions.

Customer-Centric Approach to Business Growth

Raj Industries places customer satisfaction at the heart of its operations, ensuring seamless communication, product customization, and efficient service delivery. The company understands the unique needs of its clients and tailors solutions accordingly, maintaining long-term relationships with partners across industries. Its commitment to quality assurance, prompt responsiveness, and after-sales support sets it apart in the competitive manufacturing sector. As businesses seek reliable and adaptable suppliers, Raj Industries continues to build trust and loyalty, driving its sustained growth and reinforcing its position as a leader in India's industrial landscape.

Future Prospects and Industry Leadership

The future of Raj Industries is promising, with continuous investment in research, technology, and workforce development. As automation and artificial intelligence reshape manufacturing, the company remains dedicated to staying at the forefront of innovation. Its focus on precision, sustainability, and customer-driven solutions will ensure long-term success. With India's manufacturing sector expanding rapidly, Raj Industries is well-positioned to lead the industry through quality-driven growth. By embracing technological advancements and industry demands,it aims to play a key role in shaping India's industrial future,setting new benchmarks for excellence in manufacturing.

Conclusion

Raj Industries has positioned itself as a leader in India's manufacturing sector by prioritizing quality, innovation, and sustainability. With advanced technology, precision engineering, and customer-centric solutions, the company has strengthened its foothold in diverse industries, from automotive to aerospace. Its commitment to eco-friendly practices and global standards has enhanced its reputation worldwide. As the demand for high-performance industrial components rises, Raj Industries continues to evolve, adapting to technological advancements and market needs. By fostering innovation and maintaining excellence in production, the company is not only shaping India's industrial growth but also establishing itself as a trusted global manufacturer.

0 notes

Text

Automatic Dicing Saw Market Growth Analysis 2025

The global Automatic Dicing Saw market was valued at US$ 567.4 million in 2024 and is projected to reach US$ 785.3 million by 2032, registering a CAGR of 4.6% from 2025 to 2032. This growth trajectory is attributed to the rapid expansion of the semiconductor industry, rising demand for consumer electronics, and technological advancements in wafer processing equipment. The increasing adoption of 5G technology, Internet of Things (IoT), and automotive electronics further contribute to the market's upward momentum. Historically, the market has demonstrated resilience, recovering strongly from disruptions like the COVID-19 pandemic and geopolitical trade tensions. The Asia-Pacific region, particularly China, Japan, and South Korea, continues to dominate the market, owing to its robust semiconductor fabrication ecosystem.

Automatic dicing saws are high-precision cutting tools widely used in semiconductor manufacturing and other high-tech industries. They perform the critical task of cutting silicon wafers, ceramics, and other materials into discrete, functional units. Controlled by advanced software systems, these machines ensure ultra-clean cuts, minimal kerf loss, and high throughput. Depending on the application, automatic dicing saws can handle a variety of materials and dimensions, making them indispensable in fabricating microelectronic components like integrated circuits (ICs), micro-electromechanical systems (MEMS), and optoelectronic devices. The integration of vision systems and robotic automation has further enhanced the efficiency, accuracy, and adaptability of modern dicing saws.

get free sample of this report at https://www.intelmarketresearch.com/manufacturing-and-construction/823/global-automatic-dicing-saw-2025-2032

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Booming Semiconductor Industry: The proliferation of smartphones, AI chips, and autonomous vehicle systems is accelerating demand for advanced semiconductor components, thereby driving the need for precise dicing solutions.

Rise in MEMS and IoT Devices: Devices like smart sensors and wearable tech rely on ultra-small components that require highly accurate dicing processes.

Automation and Smart Manufacturing: Industry 4.0 is pushing manufacturers toward automated, software-driven tools for increased efficiency and lower labor costs.

Restraints

High Initial Investment: The cost of fully automatic dicing systems and associated setup can be prohibitively high for small and mid-sized enterprises.

Technical Complexity: The operation and maintenance of these machines require skilled personnel, which can be a barrier in less developed regions.

Opportunities

Emerging Markets: Expanding semiconductor operations in countries like India, Vietnam, and Brazil offer significant growth potential.

Advancements in Vision Technology: Integration of AI and machine learning in vision systems can improve defect detection and operational precision.

Challenges

Supply Chain Disruptions: Trade tensions and raw material shortages can delay manufacturing and increase costs.

Regulatory and Compliance Issues: Adhering to international standards and environmental regulations can pose operational hurdles.

Regional Analysis

Asia-Pacific

The Asia-Pacific region dominates the Automatic Dicing Saw market, led by powerhouses like China, Japan, South Korea, and Taiwan. These countries are home to major semiconductor foundries and OEMs. Japan, for example, hosts leading companies like DISCO Corporation and Tokyo Seimitsu, while China benefits from substantial government-backed semiconductor initiatives.

North America

The U.S. continues to play a critical role due to its innovation-led tech sector and presence of companies like Plasma Therm. The demand for advanced packaging solutions in AI and aerospace sectors propels the market.

Europe

Germany and the UK are pivotal due to their strong industrial base and automotive electronics sector. Companies like Besi from the Netherlands contribute significantly to regional growth.

Rest of the World

Countries in Latin America and the Middle East are gradually increasing their footprint in microelectronics, offering new avenues for market expansion.

Competitor Analysis (in brief)

The Automatic Dicing Saw market features a mix of established players and emerging innovators. DISCO Corporation and Tokyo Seimitsu lead the market with comprehensive product portfolios and global distribution networks. Companies like ADT Corporation, Synova SA, and Kulicke & Soffa bring niche technologies and specialized offerings. Han’s Laser and CETC cater predominantly to the growing Chinese market, while Loadpoint Ltd. and Besi focus on European customers. Strategic partnerships, R&D investments, and product differentiation are key strategies employed to stay competitive.

Global Automatic Dicing Saw Market: Market Segmentation Analysis

This report provides a deep insight into the global Automatic Dicing Saw market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Automatic Dicing Saw Market. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Automatic Dicing Saw market in any manner.

Market Segmentation (by Type)

Fully Automatic Dicing Saws

Semi-Automatic Dicing Saws

Market Segmentation (by Cagetgory)

Single Spindel

Twin Spindel

Market Segmentation (by Dicing Blade)

Nickel-Bond Dicing Blades

Resin-Bond Dicing Blades

Metal Sintered Dicing Blades

Market Segmentation (by Application)

Silicon Wafer Dicing

Semiconductor Dicing

Glass Sheet Dicing

Ceramic Dicing

Others

Market Segmentation (by End Use Industry)

Electronics & Semiconductor

Military & Aerospace

Telecommunications

Passive Component Manufacturing

Medical Electronics

Others

Key Company

DISCO Corporation (Japan)

Tokyo Seimitsu Co., Ltd. (ACCRETECH) (Japan)

Loadpoint Ltd. (UK)

ASMPT (Singapore/Germany)

Kulicke & Soffa (K&S) (Singapore/USA)

ADT Corporation (Taiwan)

Besi (Netherlands)

Synova SA (Switzerland)

Han’s Laser (China)

CETC (China Electronics Technology Group) (China)

Plasma Therm (USA)

TOKYO WELD Co., Ltd. (Japan)

Geographic Segmentation

North America (United States, Canada, Mexico)

Europe (Germany, UK, France, Italy, Russia)

Asia-Pacific (China, Japan, South Korea, India, Southeast Asia)

South America (Brazil, Argentina, Colombia)

Middle East & Africa (Saudi Arabia, UAE, Egypt, South Africa)

FAQ

��� What is the current market size of the Automatic Dicing Saw market?

The global market was valued at US$ 567.4 million in 2024 and is projected to grow to US$ 785.3 million by 2032.

▶ Which are the key companies operating in the Automatic Dicing Saw market?

Key players include DISCO Corporation, Tokyo Seimitsu, ADT Corporation, Synova SA, and Kulicke & Soffa, among others.

▶ What are the key growth drivers in the Automatic Dicing Saw market?

Major drivers include the growth of the semiconductor industry, increased demand for MEMS and IoT devices, and rising automation in manufacturing.

▶ Which regions dominate the Automatic Dicing Saw market?

Asia-Pacific leads the market, followed by North America and Europe.

▶ What are the emerging trends in the Automatic Dicing Saw market?

Trends include integration of AI-powered vision systems, automation, and expansion into emerging semiconductor hubs like India and Vietnam.

get free sample of this report at https://www.intelmarketresearch.com/manufacturing-and-construction/823/global-automatic-dicing-saw-2025-2032

0 notes

Text

Optical Encoder Market to Expand Rapidly Thanks to Precision Motion Control Demand

The optical encoder market encompasses devices that convert mechanical motion into electrical signals, enabling precise control in robotics, industrial automation, medical equipment, and aerospace systems. Optical encoders offer high resolution, reliability, and minimal signal noise, making them vital components in motion feedback loops. As industries pursue Industry 4.0 and smart manufacturing, there is a growing need for accurate position sensing and speed measurement to optimize processes, ensure safety, and reduce downtime. Continuous advancements in miniaturization and integration have expanded applications in consumer electronics, automotive steering systems, and renewable energy installations.

Get More Insights on Optical Encoder Market https://www.patreon.com/posts/optical-encoder-131064922

#OpticalEncoderMarket#HighResolutionEncoders#IndustrialAutomation#MotionControlSystems#CoherentMarketInsights

0 notes

Text

AI and IoT Fuel Smart Active Isolation Systems

The Vibration Isolators Market was valued at approximately $2.6 billion in 2022 and is forecast to reach $4.1 billion by 2030, growing at a CAGR of 6.3%. This growth is supported by increasing demand from industrial, aerospace, and semiconductor applications. North America holds about 28% of the market share, followed closely by Asia-Pacific, the fastest-growing region.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/vibration-isolators-market

Key Market Drivers

1. Elastomeric Isolators Lead Adoption With a 40% share of the market in 2023, elastomeric isolators are widely used in automotive, HVAC, and heavy machinery. Their cost-effectiveness, vibration attenuation, and durability make them the dominant type across multiple industries.

2. Pneumatic and Compact Isolators Expand Use Cases Pneumatic isolators, particularly air-spring-based systems, are preferred in precision engineering sectors such as semiconductors, optics, and medical equipment. Compact pneumatic systems are gaining favor due to adjustable performance and low maintenance.

3. Active and Smart Isolation Technologies on the Rise Active vibration control systems, incorporating sensors and real-time feedback loops, are driving advanced use cases in the semiconductor, biotech, and defense sectors. Integration of AI and IoT technologies is enhancing responsiveness and remote monitoring capabilities.

4. Aerospace & Defense Fuel High CAGR The aerospace sector is expected to grow at a CAGR of 7.8% through 2030 due to stringent vibration control requirements in aircraft, drones, and satellite systems. Vibration isolators are essential to ensure structural safety and performance reliability.

5. Semiconductor Industry Drives Demand The semiconductor sector alone accounts for over 40% of isolation demand. Cleanroom environments, lithography, and fabrication processes require ultra-low vibration, making high-precision isolators indispensable in chip manufacturing.

6. Sustainability and Innovation Drive Market Evolution The trend toward sustainable products is leading to the adoption of recyclable elastomers, natural rubber, and 3D-printed isolators. Companies are innovating to produce compact, lighter, and more environmentally responsible isolation systems.

Application Insights

Construction and Architecture: Base isolators are increasingly used in earthquake-prone zones. Seismic base isolation and vibration dampers are widely applied in smart city infrastructure and high-rise buildings.

Industrial Machinery: Vibration isolators are crucial for extending equipment life and ensuring production consistency in CNC machines, compressors, and conveyor systems.

Medical Devices: MRI, CT, and surgical robots benefit from ultra-low vibration environments made possible by smart isolators.

Consumer Electronics: Compact vibration pads are being embedded in wearable and handheld devices for protection and enhanced user experience.

Regional Analysis

North America leads the market with a 28% share, driven by aerospace R&D, smart manufacturing, and industrial automation investments. The U.S. is a key contributor due to its advanced defense and semiconductor industries.

Asia-Pacific is the fastest-growing region with a projected CAGR of 8.5%, led by China, Japan, and South Korea. Rapid industrialization, growing electronics manufacturing, and seismic construction practices are propelling demand.

Europe holds about 22% of the global share, with major contributions from Germany, France, and the UK. The region benefits from well-established automotive and aviation sectors.