#U.S. Robotics Integration for the Manufacturing Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

130K people were victims of a chain letter scam that affected Tumblr in May 2011.

Text

The U.S. robotics integration for the manufacturing market is estimated to reach $7.48 billion by 2029 from $3.94 billion in 2023, growing at a CAGR of 11.69% during the forecast period 2024-2029.

#U.S. Robotics Integration for the Manufacturing Market#U.S. Robotics Integration for the Manufacturing Report#U.S. Robotics Integration for the Manufacturing Industry#Robotics and Automation#BISResearch

0 notes

Text

Comprehensive Study: U.S. Robotics Integration in Manufacturing Sector

According to the BIS Research, the U.S. Robotics Integration for the Manufacturing Market is projected to reach $7.48 Billion by 2029 from $3.94 Billion in 2023, growing at a CAGR of 11.69 % during the forecast period 2023-2029.

#U.S. Robotics Integration for the Manufacturing Market#U.S. Robotics Integration for the Manufacturing Market Report#U.S. Robotics Integration for the Manufacturing Market Research#U.S. Robotics Integration for the Manufacturing Market Forecast#Robotics#Automation#BIS Research

1 note

·

View note

Text

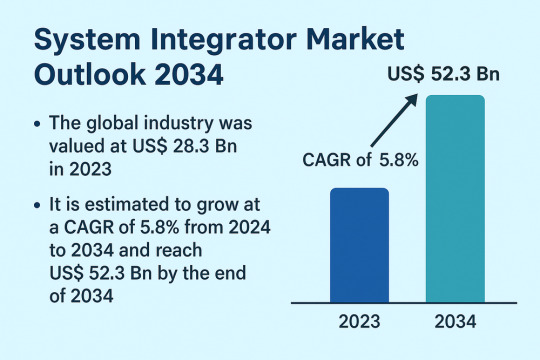

Automation and Integration Needs Power Robust Growth in System Integrator Market

The global System Integrator Market is poised for significant growth, projected to rise from US$ 28.3 Bn in 2023 to US$ 52.3 Bn by 2034, growing at a CAGR of 5.8% from 2024 to 2034. This growth is driven by the widespread adoption of industrial robots, technological advancements, and a pressing need among businesses to optimize operational efficiencies through connected systems.

System integrators play a pivotal role in designing, implementing, and maintaining integrated solutions that bring together hardware, software, and consulting services. These services support organizations in unifying internal and external systems, such as SCADA, HMI, MES, PLC, and IIoT, to enable seamless data flow and system interoperability.

Market Drivers & Trends: One of the primary market drivers is the rise in adoption of industrial robots. As industries accelerate automation, robotic system integrators have become vital in delivering customized, scalable, and high-performing solutions tailored to complex manufacturing needs.

Another major catalyst is the surge in technological advancements. Integrators are deploying cloud-based tools and platforms that provide real-time data insights, improve developer productivity, and support hybrid architectures. The increasing use of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) in integration solutions is fostering innovation and growth.

Latest Market Trends

Several emerging trends are shaping the system integrator landscape:

Cloud modernization platforms such as IBM’s Z and Cloud Modernization Center are enabling businesses to accelerate the transition to hybrid cloud environments.

Modular automation platforms are gaining popularity, allowing companies to rapidly deploy and scale integration solutions across multiple industry verticals.

Edge computing and cybersecurity solutions are increasingly being integrated to support secure, real-time decision-making on the production floor.

Digital hubs and scalable workflow engines are being adopted by integrators to support multi-specialty applications with high adaptability.

Key Players and Industry Leaders

The system integrator market is characterized by a strong mix of global leaders and regional specialists. Key players include:

ATS Corporation

Avanceon

Avid Solutions

Brock Solutions

JR Automation

MAVERICK Technologies, LLC

Burrow Global, LLC

BW Design Group

John Wood Group PLC

TESCO CONTROLS

These companies are actively investing in next-generation technologies, enhancing their product portfolios, and pursuing strategic acquisitions to strengthen market presence. For instance, in July 2023, ATS Corporation acquired Yazzoom BV, a Belgian AI and ML solutions provider, expanding their capabilities in smart manufacturing.

Recent Developments

Olympus Corporation launched the EASYSUITE ES-IP system in July 2023 in the U.S., offering advanced visualization and integration solutions for procedure rooms.

IBM introduced key updates in 2021 and 2022 to streamline mission-critical application modernization using cloud services and hybrid IT strategies.

Asia-Pacific companies have led the charge in deploying advanced integrated systems, reflecting the rapid industrial digitization in countries such as China, Japan, and South Korea.

Market Opportunities

Opportunities abound in both mature and emerging markets:

Smart factories and Industry 4.0 transformation offer immense potential for integrators to offer comprehensive solutions tailored to real-time analytics, predictive maintenance, and remote monitoring.

Government-led infrastructure modernization projects, particularly in Asia and the Middle East, are increasing demand for integrated control systems and plant asset management solutions.

The energy transition movement, including renewables and electrification of industrial processes, requires new types of integration across decentralized assets.

Future Outlook

As industries pursue digital transformation, the role of system integrators will evolve from traditional project implementers to long-term strategic partners. The future will see increasing demand for intelligent automation, cross-domain expertise, and real-time adaptive solutions. Vendors who can provide holistic, secure, and scalable services will dominate the landscape.

With continued advancements in AI, IoT, and robotics, the system integrator market will continue to thrive, transforming operations across diverse sectors, from automotive and food & beverages to oil & gas and pharmaceuticals.

Review critical insights and findings from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=82550

Market Segmentation

The market is segmented based on offering, technology, and end-use industry.

By Offering:

Hardware

Software

Service (Consulting, Design, Installation)

By Technology:

Human-Machine Interface (HMI)

Supervisory Control and Data Acquisition (SCADA)

Manufacturing Execution System (MES)

Functional Safety System

Machine Vision

Industrial Robotics

Industrial PC

Industrial Internet of Things (IIoT)

Machine Condition Monitoring

Plant Asset Management

Distributed Control System (DCS)

Programmable Logic Controller (PLC)

By End-use Industry:

Oil & Gas

Chemical & Petrochemical

Food & Beverages

Automotive

Energy & Power

Pharmaceutical

Pulp & Paper

Aerospace

Electronics

Metals & Mining

Others

Regional Insights

Asia Pacific leads the global system integrator market, holding the largest market share in 2023. This leadership is attributed to:

Rapid industrialization and digital transformation in China, Japan, and India.

Strong investments in smart manufacturing and Industry 4.0 initiatives.

Government support for infrastructure modernization, especially through Smart City programs and cybersecure IT frameworks.

North America and Europe also show strong demand, driven by the presence of established manufacturing facilities and a robust focus on sustainable operations and green automation.

Why Buy This Report?

Comprehensive Market Analysis: Deep insights into market size, share, and growth across all major segments and geographies.

Detailed Competitive Landscape: Profiles of leading companies with analysis of their strategy, product offerings, and key financials.

Actionable Intelligence: Understand technological trends, regulatory developments, and investment opportunities.

Forecast-Based Strategy: Develop long-term strategic plans using data-driven forecasts up to 2034.

Frequently Asked Questions (FAQs)

1. What is the projected value of the system integrator market by 2034? The global system integrator market is projected to reach US$ 52.3 Bn by 2034.

2. What is the current CAGR for the forecast period 2024–2034? The market is anticipated to grow at a CAGR of 5.8% during the forecast period.

3. Which region holds the largest market share? Asia Pacific dominated the global market in 2023 and is expected to continue leading due to rapid industrialization and technology adoption.

4. What are the key growth drivers? Key drivers include the rise in adoption of industrial robots and continuous advancements in integration technologies like IIoT, AI, and cloud platforms.

5. Who are the major players in the system integrator market? Prominent players include ATS Corporation, JR Automation, Brock Solutions, MAVERICK Technologies, and Control Associates, Inc.

6. Which industries are adopting system integrator services the most? High adoption is seen in industries such as automotive, oil & gas, food & beverages, pharmaceuticals, and electronics.

Explore Latest Research Reports by Transparency Market Research:

Multi-Mode Chipset Market: https://www.transparencymarketresearch.com/multi-mode-chipset-market.html

Accelerometer Market: https://www.transparencymarketresearch.com/accelerometer-market.html

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Advanced Marine Power Supply Market: https://www.transparencymarketresearch.com/advanced-marine-power-supply-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Magnetic Sensor Market Forecast to Reach USD 8–9 Billion by 2032

Magnetic Sensors Market to Exceed USD 8 Billion by 2033, Driven by EV, Automation, and Smart Tech Demand

The Magnetic Sensors Market, valued at approximately USD 4.5 billion in 2024, is expected to grow steadily and reach USD 8–9 billion by 2033. This expansion reflects a compound annual growth rate (CAGR) of 6–8%, fueled by the rapid proliferation of electric vehicles, advancements in industrial automation, rising demand in consumer electronics, and growing Internet of Things (IoT) applications.

To Get Free Sample Report : https://www.datamintelligence.com/download-sample/magnetic-sensors-market

Key Market Drivers

1. Automotive Industry Electrification As the shift toward electric and hybrid vehicles continues, magnetic sensors play a central role in applications like anti-lock braking systems (ABS), steering angle detection, throttle position sensing, and battery management. The integration of advanced driver assistance systems (ADAS) is also driving demand for highly accurate Hall-effect and magnetoresistive sensors.

2. Rise in Consumer Electronics and Wearables Miniaturized magnetic sensors are now standard in mobile phones, tablets, and wearable devices for functions like electronic compassing, gesture control, and spatial navigation. The trend toward compact, multifunctional smart devices is accelerating demand across OEMs and component suppliers.

3. Industry 4.0 and Smart Manufacturing Magnetic sensors support real-time monitoring in industrial automation environments. They provide position, proximity, and rotational speed feedback in CNC machinery, robotic arms, elevators, and conveyor systems ensuring accurate performance in dynamic manufacturing conditions.

4. Growth in Renewable and Clean Energy Applications Magnetic sensors are used in wind turbine pitch systems, solar panel tracking, and electric grid condition monitoring. As global investment in renewable energy infrastructure rises, these sensors are increasingly vital to system control and energy efficiency.

Technology Segmentation & Market Trends

Hall-Effect Sensors Dominate Hall-effect sensors accounted for more than 50% of global revenue in 2023. They are valued for their reliability, compact design, and broad applicability in automotive and consumer electronics.

Magnetoresistive Sensors Gaining Ground Giant magnetoresistive (GMR) and tunneling magnetoresistive (TMR) sensors are being adopted for high-precision, low-power applications in robotics, medical devices, and automation control systems.

MEMS-Based Magnetic Sensors and 3D Integration Microelectromechanical systems (MEMS) magnetic sensors are enabling ultra-compact, low-cost 3D field sensing in smartphones and wearables. Their rise is central to the IoT movement and portable device innovation.

Regional Market Insights

Asia-Pacific Leads Global Demand Asia-Pacific dominates with over 45% market share, led by China, Japan, and South Korea. The region’s strong consumer electronics production base and leadership in electric vehicle manufacturing have solidified its position. Japan, in particular, has advanced high-end magnetic sensor design and exports globally.

United States Market Outlook The U.S. magnetic sensors market is driven by continued growth in ADAS development, aerospace and defense technologies, and industrial digitalization. Strong R&D investments and manufacturing automation have boosted adoption in both the public and private sectors.

European Innovation and Regulation Europe’s automotive innovation and renewable energy initiatives fuel magnetic sensor use. Germany, in particular, drives demand through automotive mechatronics, factory robotics, and wind energy monitoring systems.

Emerging Growth Opportunities

Automated Guided Vehicles (AGVs) and Drones Magnetic sensors are essential for orientation and obstacle navigation. Growth in smart logistics, drone surveillance, and delivery services is enhancing their role in autonomous guidance.

Healthcare & Medical Imaging In MRI systems and wearable diagnostic devices, magnetic sensors are crucial for position tracking and motion compensation. Sensor miniaturization is expanding opportunities in health monitoring devices.

High-Precision Robotics Sensors enabling feedback-controlled movement in robotics and cobots (collaborative robots) are opening high-value industrial and defense applications.

Smart Infrastructure and Building Automation In smart buildings, magnetic sensors are used for security (door/window detection), elevator systems, and HVAC control offering energy-saving advantages and enhanced monitoring.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/magnetic-sensors-market

Challenges in the Market

Price Pressure and Commoditization: Low-cost alternatives in saturated markets can hinder profit margins and innovation incentives.

Magnetic Interference Issues: High electromagnetic noise environments can disrupt performance unless proper shielding and design optimization are applied.

Raw Material Supply Risks: The availability of rare earth materials impacts sensor magnet production, making the industry vulnerable to geopolitical shifts.

Stringent Automotive and Industrial Certification: Reliability and safety standards for automotive-grade sensors require long testing cycles, increasing time to market for new products.

Conclusion

The global magnetic sensors market is evolving rapidly, supported by strong demand from automotive systems, consumer electronics, industrial automation, and renewable energy technologies. With a projected valuation surpassing USD 8–9 billion by 2033, the sector offers promising opportunities for sensor manufacturers, OEMs, and system integrators.

As technology continues to evolve, innovations in magnetoresistive and MEMS-based sensor designs will unlock new capabilities, while advanced signal processing and integration techniques will further elevate sensor precision and versatility. Key players investing in scalable manufacturing, regional expansion, and application-specific R&D will lead the next era of magnetic sensing solutions.

0 notes

Text

Edge AI Meets Smart Sensors: Real-Time Data Processing Takes the Lead

The global smart sensors market is experiencing unprecedented growth, fueled by rapid digital transformation across industries, rising adoption of IoT-enabled devices, and the integration of artificial intelligence in sensor technologies. As industries shift toward automation, real-time monitoring, and data-driven operations, smart sensors have become the backbone of modern electronic ecosystems.

Unlock exclusive insights with our detailed sample report :

According to recent industry insights, the smart sensors market was valued at USD 45.63 billion in 2023 and is projected to reach USD 145.23 billion by 2031, growing at a CAGR of 15.6% during the forecast period. Key industries including automotive, healthcare, consumer electronics, aerospace, and manufacturing are witnessing a surge in demand for intelligent sensors capable of capturing and processing environmental data with minimal latency.

Market Drivers and Growth Opportunities

1. Proliferation of IoT Devices and Smart Infrastructure The explosion of IoT applications in smart homes, smart cities, and industrial IoT (IIoT) has driven the need for sensors that are not only accurate but also intelligent. These sensors support seamless data transmission and decision-making capabilities in connected ecosystems.

2. Automation and Industry 4.0 Transformation Industries are investing heavily in predictive maintenance, process automation, and robotics. Smart sensors such as temperature, pressure, proximity, and image sensors are at the core of these applications, enabling real-time monitoring and adaptive control in automated systems.

3. Rising Demand in Healthcare Smart sensors are revolutionizing healthcare through wearable technology, patient monitoring devices, and remote diagnostics. With the growing geriatric population and demand for personalized healthcare, sensor integration in medical devices is a key market driver.

4. Growing Popularity of Smart Consumer Electronics From smartphones and smartwatches to AR/VR devices and home appliances, the integration of multi-functional smart sensors is enhancing user experience and device interactivity, contributing to soaring market demand.

5. Environmental Monitoring and Sustainability Climate change and environmental regulations are encouraging governments and industries to adopt smart sensors for air quality, water purity, and pollution monitoring. These solutions are essential for meeting global sustainability goals.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

https://www.datamintelligence.com/customize/smart-sensors-market

Market Segmentation Overview

By Sensor Type: Includes pressure sensors, temperature sensors, image sensors, touch sensors, motion sensors, and gas sensors. Image and motion sensors are gaining traction in automotive and consumer electronics sectors.

By Technology: MEMS (Microelectromechanical Systems), CMOS (Complementary Metal-Oxide-Semiconductor), and optical sensing technologies dominate due to their efficiency, miniaturization, and compatibility with IoT platforms.

By End-Use Industry: Automotive, healthcare, industrial automation, consumer electronics, and aerospace & defense are key application areas. Among them, industrial and healthcare sectors are the fastest growing.

U.S. and Japan Market Insights

United States The U.S. remains a dominant force in smart sensor adoption, driven by strong demand across aerospace, automotive, defense, and healthcare industries. In early 2025, the U.S. Department of Energy announced a $1.2 billion fund for smart grid modernization, which includes significant investment in smart sensors for energy distribution and consumption tracking. Additionally, major tech firms such as Apple, Texas Instruments, and Honeywell are innovating sensor fusion technologies to enable smarter and more efficient devices.

Japan Japan, a global leader in robotics and automation, is rapidly advancing smart sensor deployment in its manufacturing and automotive sectors. With its focus on Smart Factories under “Society 5.0,” Japan is integrating AI-powered sensors into robotics, EVs, and public infrastructure. In March 2025, a leading Japanese electronics manufacturer launched a new line of miniaturized smart sensors for next-generation autonomous vehicles and wearable healthcare devices, underscoring Japan’s strong R&D capabilities.

Latest Trends and Innovations

AI-Embedded Smart Sensors: Integration of edge AI allows sensors to process data locally, improving response times and reducing the load on central systems. This is particularly useful in autonomous vehicles, predictive maintenance, and smart healthcare.

Sensor Fusion for Enhanced Accuracy: Combining multiple sensor inputs (e.g., gyroscope + accelerometer + magnetometer) provides more precise data. This trend is rising in consumer electronics and wearable fitness devices.

Advances in MEMS Technology: MEMS-based sensors are evolving rapidly, enabling lower power consumption and smaller form factors. These are ideal for implantable medical devices and compact electronics.

Energy Harvesting Sensors: To support sustainability, sensors that draw energy from ambient sources like light, heat, or motion are becoming more prominent, especially in remote monitoring and IoT applications.

Cybersecurity in Sensor Networks: As smart sensors become part of critical infrastructure, the importance of secure data transmission and sensor-level encryption is gaining attention, especially in military, healthcare, and smart grid applications.

Buy the exclusive full report here:

Competitive Landscape

The market is moderately consolidated with global players focusing on R&D, strategic collaborations, and geographic expansion to maintain competitiveness. Key players include:

Honeywell International Inc.

STMicroelectronics

Infineon Technologies AG

Robert Bosch GmbH

Texas Instruments Incorporated

TE Connectivity Ltd.

NXP Semiconductors

Analog Devices, Inc.

Siemens AG

Omron Corporation

These companies are pushing the boundaries in multi-sensor integration, AI-powered detection systems, and low-power sensor networks.

Future Outlook and Market Opportunities

1. Smart City Initiatives: Governments across the globe, particularly in the U.S. and Asia, are investing in smart infrastructure. Smart sensors will play a central role in traffic management, lighting, surveillance, and environmental monitoring.

2. Growth in Electric Vehicles (EVs): EVs require a wide array of sensors for battery management, motor control, and safety systems. As EV adoption surges globally, the demand for automotive-grade smart sensors will follow suit.

3. Space and Aerospace Applications: High-reliability smart sensors are being developed for satellites and space missions to monitor pressure, radiation, and temperature in extreme environments.

4. Expanding Use in Agriculture (AgriTech): Smart sensors are increasingly used in precision farming, monitoring soil moisture, crop health, and weather patterns to optimize resource use and productivity.

Stay informed with the latest industry insights-start your subscription now:

Conclusion

The global smart sensors market stands at the intersection of innovation, automation, and connectivity. With widespread applications across industries and increasing integration of AI and IoT, smart sensors are redefining how machines interact with their environments. The market’s rapid expansion—led by the U.S. and Japan—signals a transformative shift toward a more responsive, efficient, and intelligent future. As sensor technologies continue to evolve, businesses and governments alike must harness their full potential to stay ahead in the digital age.

About us:

At DataM Intelligence, we specialize in delivering end-to-end market research and consulting solutions designed to unlock your business potential. By harnessing proprietary insights, market trends, and breakthrough developments, we craft intelligent strategies that drive results.

With a repository of 6,300+ detailed reports across 40+ sectors, we’ve helped over 200 global businesses across 50+ nations achieve growth. From syndicated analysis to tailored research, our dynamic approach addresses the critical intelligence your business needs to thrive.

Contact US:

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: [email protected]

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

#Smart sensors market#Smart sensors market size#Smart sensors market growth#Smart sensors market share#Smart sensors market analysis

0 notes

Text

Electric Motor Market Dynamics: Growth Trends & Forecast CAGR

The latest research publication titled “Electric Motor Industry Trend, Share, Size, Growth, Opportunities & Forecast 2025-2032” by Fortune Business Insights delivers an in-depth market analysis, offering actionable insights into global and regional trends. The report serves as a reliable resource for stakeholders, highlighting competitive dynamics, innovation trends, and market outlook. Electric Motor Market Size, Share, Growth, Trends, Industry Analysis & Forecast 2025-2032

The global electric motor market size was valued at USD 145.15 billion in 2024 and is projected to be worth USD 155.40 billion in 2025 and reach USD 258.17 billion by 2032, exhibiting a CAGR of 7.52% during the forecast period. Asia Pacific dominated the global market with a share of 40.75% in 2024. The Electric Motor market in the U.S. is projected to grow significantly, reaching an estimated value of USD 51.30 billion by 2032, driven by the growing adoption of automation & robotics in manufacturing and other industries.

Electric Motor Market Overview:

The Electric Motor Market has experienced rapid expansion in recent years, fueled by increasing demand, technological innovations, and the diversification of application areas. This report provides a detailed breakdown of market performance, outlining key growth drivers, challenges, and emerging opportunities.

Electric Motor Market Size & CAGR Growth

Industry Dynamics & Ecosystem Trends

Technological Developments & Product Innovations

Regulatory & Economic Impact Factors

Request a Sample Copy Here: Sample Report

Competitive Landscape:

The report profiles leading players in the global Electric Motor market, offering insights into strategic developments, R&D investments, product portfolios, and financial metrics. Key companies included:

Electric Motor Market Key Players

Key Players:

ABB Ltd.

Siemens AG

Nidec Corporation

WEG S.A.

Regal Beloit Corporation

Toshiba Corporation

Rockwell Automation, Inc.

Johnson Electric Holdings Limited

Ametek, Inc.

Franklin Electric Co., Inc.

(Additional profiles of top-tier players with SWOT analysis, global presence, and growth strategies)

Market Segmentation:

By Type:

AC Motors

Induction Motors

Synchronous Motors

DC Motors

Brushed DC Motors

Brushless DC Motors

By Voltage Rating:

Low Voltage

Medium Voltage

High Voltage

By Power Output:

Fractional Horsepower (FHP)

Integral Horsepower (IHP)

By Application:

Industrial

Commercial

Residential

Transportation (EVs, Railways, Marine)

HVAC Systems

By End-User Industry:

Automotive

Aerospace & Defense

Energy & Utilities

Healthcare

Consumer Electronics

Others

By Geography:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Key Opportunities and Growth Drivers:

Rising demand in [industry/sector]

Technological breakthroughs in [related field]

Expansion into untapped regional markets

Strategic mergers, acquisitions & product launches

This report examines both historical trends and forward-looking data to uncover high-potential growth segments and investment opportunities.

Future Outlook:

Electric Motor Market forecast by value and volume (2025–2032)

Competitive strategy benchmarking

Product lifecycle assessment and innovation timeline

Price trend analysis and supply chain insight

Get Discount on This Report: Buy Now

Why This Report Matters:

Access verified data and forecasts

Understand emerging consumer trends

Benchmark your position among competitors

Optimize market entry and expansion strategies

FAQs Answered in the Report:

Who are the top players in the Electric Motor Market?

What is the projected market size by 2025?

Which regions are expected to lead in terms of revenue?

What trends will shape the Electric Motor market in the next 5 years?

How intense is the competitive rivalry in this sector?

About Us: Fortune Business InsightsTM offers expert corporate analysis and accurate data, helping organizations of all sizes make timely decisions. We tailor innovative solutions for our clients, helping them address challenges specific to their businesses. Our goal is to empower our clients with holistic market intelligence, giving a granular overview of the market they are operating in.

Contact Us: Fortune Business InsightsTM Pvt. Ltd. Email: [email protected]

0 notes

Text

medical devices manufacturing

Imagine a world where diagnosis, monitoring, and treatment of diseases were impossible without machines. That’s the world we would live in without medical devices manufacturing. This field is the backbone of modern healthcare, producing everything from surgical tools to smart implants.

With rising global demand, the industry has transformed significantly. One company making waves in this space is Foxxtechnologies, known for its cutting-edge manufacturing solutions tailored for the medical sector.

What is Medical Devices Manufacturing?

Simply put, it’s the process of designing, engineering, producing, and distributing devices that assist in medical treatment or diagnosis. These range from basic thermometers to complex robotic surgical systems.

Importance of the Medical Devices Industry

This industry ensures hospitals and clinics have the tools they need to save lives. It’s not just about machines — it’s about healthcare innovation, patient safety, and efficiency.

Understanding the Manufacturing Process

Research and Development (R&D)

Every great product starts with an idea. In medical devices manufacturing, R&D is where the magic begins.

Ideation and Concept Testing

Teams brainstorm, sketch, and simulate product ideas. Then, they test concepts through small trials and user feedback to determine viability.

Prototyping and Product Design

Before going to mass production, a prototype is created. This helps identify design flaws and gather early clinical feedback.

Role of CAD and 3D Modelling

Design engineers use advanced software to build detailed 3D models, helping predict performance and optimize the structure.

Materials Used in Medical Device Production

The choice of material can make or break a device.

Biocompatible Materials

Manufacturers use plastics, metals, and ceramics that are non-toxic and accepted by the human body. Titanium and medical-grade silicone are common choices.

Regulatory Standards and Certifications

You can’t just create a device and sell it — there are rules.

FDA, ISO, and CE Certifications

Medical devices must meet strict quality and safety regulations. These include FDA approvals in the U.S., CE marks in Europe, and ISO 13485 certification globally.

Key Technologies in Medical Devices Manufacturing

Automation and Robotics

Modern factories use robotics to improve precision, reduce errors, and accelerate production.

3D Printing in Medical Devices

3D printing is transforming the industry by allowing customized implants, faster prototyping, and reduced waste.

AI and IoT Integration

Smart medical devices connected through IoT can transmit real-time health data to doctors. AI helps in predictive maintenance and quality control.

Foxxtechnologies – Leading the Innovation

Overview of Foxxtechnologies

Foxxtechnologies is not your average manufacturer. They specialize in innovative, scalable, and high-quality medical device production services. With a solid reputation, they cater to both startups and large healthcare brands.

Unique Manufacturing Capabilities

Customization and Rapid Prototyping

Need a device tailored to your needs? Foxxtechnologies provides rapid prototyping, saving both time and cost in development.

Cleanroom Production Facilities

Sterility is crucial. Their ISO-class cleanrooms ensure that every product meets stringent hygiene standards.

Compliance and Quality Assurance

Foxxtechnologies doesn’t just build — they ensure every product is tested, validated, and certified according to international standards.

Trends Shaping the Future of Medical Device Manufacturing

Sustainability and Eco-Friendly Practices

As the world shifts towards greener practices, manufacturers like Foxxtechnologies are adopting recyclable materials and low-waste processes.

Smart Devices and Wearables

From fitness trackers to glucose monitors, wearable technology is booming and changing how we manage health.

Global Market Growth and Expansion

The global market for medical devices is expected to surpass $800 billion by 2030. Companies must scale fast — and smart.

Challenges in Medical Device Manufacturing

Navigating Regulations

Each country has its own rules. Global manufacturing means tackling multiple regulatory frameworks.

Ensuring Sterility and Biocompatibility

The challenge is to ensure every device is safe and performs flawlessly inside the human body.

High Costs of R&D and Manufacturing

Innovation isn’t cheap. It demands huge investments in technology, skilled labor, and compliance.

Why Choose Foxxtechnologies for Medical Device Manufacturing?

Industry Expertise and Experience

With years of hands-on experience, Foxxtechnologies knows what works and what doesn't in this highly sensitive sector.

Client-Centric Solutions

From idea to delivery, the team works closely with clients, offering end-to-end support.

Scalable and Efficient Processes

Whether it’s a batch of 100 or 10,000 units, Foxxtechnologies scales seamlessly without compromising quality.

Conclusion

Medical devices manufacturing is not just a process — it’s a commitment to healthcare, innovation, and patient safety. As technology evolves, companies like Foxxtechnologies are leading the charge by integrating cutting-edge tech, adhering to global standards, and providing client-focused solutions.

Whether you're a startup with a prototype idea or an established healthcare brand looking to expand production, Foxxtechnologies is your go-to partner in the realm of medical device manufacturing.

Email Us : [email protected]

0 notes

Text

Modular Hall Effect Sensors Market: Future Growth of the Semiconductor Sector, 2025–2032

MARKET INSIGHTS

The global Modular Hall Effect Sensors Market size was valued at US$ 834 million in 2024 and is projected to reach US$ 1.34 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to witness the highest growth rate at 7.8% CAGR through 2032.

Modular Hall Effect sensors are compact, overmolded devices that detect magnetic fields with IP67-rated protection. These sensors separate the magnetic target from enclosed electronics, enabling space-efficient installations in demanding environments. They offer both analog and digital output options, making them versatile for position sensing, speed detection, and current measurement applications across industries.

The market growth is driven by increasing automation in manufacturing and rising electric vehicle production, where these sensors enable precise motor control. Furthermore, advancements in Industry 4.0 technologies and growing adoption in consumer electronics for touchless interfaces are expanding application horizons. Key players like Allegro MicroSystems and Texas Instruments are introducing energy-efficient variants with integrated signal conditioning, addressing the need for smarter IoT-enabled solutions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption in Automotive Applications Fuels Market Expansion

The automotive industry’s increasing reliance on modular Hall effect sensors is a primary driver for market growth. These sensors are critical for position sensing in throttle control, gear shift detection, and braking systems in modern vehicles. With the automotive sector accounting for over 35% of global Hall effect sensor demand, the transition toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) creates substantial opportunities. The integration of these sensors in brushless DC motors for EV powertrains, where they offer high reliability in harsh environments, is particularly noteworthy. Recent technological advancements have enhanced their ability to operate in temperature ranges from -40°C to 150°C, making them indispensable for automotive applications.

Industrial Automation Boom Accelerates Demand

Industrial automation represents another significant growth avenue, with modular Hall effect sensors finding extensive use in motor controls, robotics, and conveyor systems. The global industrial automation market is projected to grow at nearly 9% CAGR through 2030, creating parallel demand for precision sensing solutions. These sensors enable non-contact position detection in harsh industrial environments where traditional mechanical switches fail. Their modular design with IP67-rated housings provides robust protection against dust and moisture, a critical requirement in manufacturing facilities. Furthermore, Industry 4.0 initiatives are driving the adoption of smart sensors with digital outputs that can interface directly with IoT systems, creating new integration possibilities.

➤ An analysis of production data shows that industrial applications now account for approximately 28% of modular Hall effect sensor deployments, with particularly strong uptake in packaging machinery and CNC equipment.

The trend toward miniaturization in consumer electronics also presents significant growth potential. As devices become smaller, modular Hall effect sensors offer compact solutions for lid position detection in laptops and foldable smartphones, with some models now measuring less than 2mm x 2mm.

MARKET CHALLENGES

Intense Price Competition from Alternative Technologies

While modular Hall effect sensors offer distinct advantages, they face mounting competition from alternative sensing technologies like magnetoresistive (MR) and giant magnetoresistive (GMR) sensors. These alternatives often provide higher sensitivity and better signal-to-noise ratios in certain applications, putting pressure on Hall sensor manufacturers to differentiate their offerings. In price-sensitive markets such as consumer electronics, this competition frequently leads to margin erosion, with some sensor prices declining by approximately 15% over the past three years. Maintaining profitability while meeting the demand for cost reductions remains an ongoing challenge for major players.

Other Challenges

Supply Chain Vulnerabilities The semiconductor shortage impacts have revealed vulnerabilities in the sensor supply chain, particularly for specialized packaging materials. Lead times for certain sensor components have extended to 26 weeks in some cases, disrupting production schedules.

Technical Limitations Achieving sub-micron position resolution remains technically challenging for standard Hall effect designs, limiting their adoption in ultra-high precision applications compared to optical encoders.

MARKET RESTRAINTS

Design Complexity in High-Temperature Applications

While modular Hall effect sensors perform well in standard industrial environments, their application in extreme conditions presents design challenges. Operation above 150°C requires specialized materials and packaging techniques that can increase unit costs by 30-40%. This temperature limitation restricts their use in certain aerospace and oil/gas applications where environments routinely exceed these thresholds. The thermal drift characteristics of Hall elements also necessitate sophisticated compensation circuits, adding to system complexity and BOM costs.

Additionally, the need for precise magnetic field calibration in production creates yield challenges, with typical manufacturing tolerances requiring adjustments to ±1% or better for critical applications. These factors collectively restrain broader market adoption in some specialized segments.

MARKET OPPORTUNITIES

Emerging Medical Applications Present Significant Growth Potential

The medical device sector represents a high-growth opportunity, with modular Hall effect sensors finding new applications in surgical robotics, drug delivery systems, and implantable devices. The medical sensors market is projected to exceed $20 billion by 2027, creating substantial demand for reliable position sensing solutions. Recent innovations include contactless sensing for MRI-compatible equipment and miniature sensors for insulin pump mechanisms. The sterilization compatibility of properly packaged modular sensors makes them particularly attractive for single-use medical devices.

Furthermore, the development of ultra-low power Hall sensors consuming less than 10μA enables new battery-powered wearable applications with multi-year operational life, opening additional market segments. Strategic partnerships between sensor manufacturers and medical OEMs are accelerating the development of application-specific solutions.

MODULAR HALL EFFECT SENSORS MARKET TRENDS

Shift Towards Compact, High-Performance Sensing Solutions Drives Market Growth

The global Modular Hall Effect Sensors market, valued at $XX million in 2024, is experiencing robust expansion due to increasing demand for compact and reliable sensing solutions in industrial and automotive applications. These sensors, known for their IP67-rated durability and separation of magnetic targets from enclosed electronics, offer significant advantages in space-constrained installations. The automotive sector alone accounts for over 30% of total sensor demand, driven by the need for precise position detection in electric power steering and transmission systems. As industries continue miniaturizing components while requiring higher precision, modular Hall effect sensors are becoming the technology of choice for engineers worldwide.

Other Trends

Industrial Automation Revolution

The fourth industrial revolution is accelerating adoption across manufacturing sectors, with modular Hall effect sensors playing a critical role in Industry 4.0 implementations. These contactless sensors enable precise speed measurement in conveyor systems with an accuracy margin of ±1%, while their modular design allows easy integration into existing automated workflows. The global industrial automation market’s projected CAGR of 9.3% through 2032 directly correlates with increasing sensor deployments in robotic assembly lines and smart factory environments.

Advancements in Material Science and Chip Design

Recent breakthroughs in semiconductor materials and 3D packaging technologies are enabling sensor manufacturers to develop products with 30% higher sensitivity compared to previous generations. Leading manufacturers are now incorporating graphene-based elements and advanced ferromagnetic alloys that maintain stability across extreme temperature ranges from -40°C to 150°C. These innovations are particularly crucial for aerospace applications where sensors must perform reliably in both stratospheric cold and engine compartment heat. Digital output variants now dominate new product launches, representing 58% of 2024 modular Hall sensor introductions due to their compatibility with modern IoT ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global modular Hall Effect sensors market exhibits a moderately consolidated competition structure, where established electronic component manufacturers compete with specialized sensor providers. Sensata Technologies leads the segment with an estimated 18% revenue share in 2024, leveraging its diversified industrial sensor portfolio and strong OEM relationships in the automotive sector.

Texas Instruments and Allegro MicroSystems collectively hold approximately 25% market share, driven by their advanced semiconductor expertise and vertically integrated production capabilities. These companies continue to dominate due to their ability to offer customized solutions for high-growth applications such as electric vehicles and Industry 4.0 automation systems.

While traditional players maintain strong positions, emerging competitors like Melexis are disrupting the market through innovative packaging technologies and miniaturized sensor designs. The Belgium-based company recently launched its third-generation Hall Effect ICs, specifically optimized for space-constrained medical devices and wearables.

The supplier ecosystem is witnessing increased M&A activity as manufacturers seek to consolidate expertise. Littelfuse’s 2023 acquisition of C&K Components exemplifies this trend, enhancing their position in ruggedized industrial sensors. Similarly, Rohm Semiconductor expanded its European footprint through strategic partnerships with automotive Tier 1 suppliers.

List of Key Modular Hall Effect Sensor Companies Profiled

Sensata Technologies (U.S.)

Texas Instruments (U.S.)

Rohm Semiconductor (Japan)

Littelfuse (U.S.)

ZF Switches & Sensors (Germany)

Marposs (Italy)

Allegro MicroSystems (U.S.)

Lake Shore Cryotronics (U.S.)

Regal Components (Sweden)

Silicon Labs (U.S.)

Melexis (Belgium)

Segment Analysis:

By Type

Hall Switch Segment Leads the Market with Extensive Use in Position Sensing and Switching Applications

The market is segmented based on type into:

Hall Switch

Subtypes: Unipolar, Bipolar, and Omnipolar

Linear Hall Sensor

Subtypes: Analog Output and Digital Output

Others

By Application

Automotive Segment Dominates Due to Increasing Adoption in Position Detection and Current Sensing Applications

The market is segmented based on application into:

Consumer Electronics

Automotive

Aerospace

Medical

Industrial

By Functionality

Position Sensing Segment Holds Major Share with Growing Demand Across Industries

The market is segmented based on functionality into:

Position Sensing

Current Sensing

Speed Detection

Others

By Output

Analog Output Segment Maintains Strong Position in Various Measurement Applications

The market is segmented based on output into:

Analog Output

Digital Output

Subtypes: Pulse Width Modulation (PWM), I2C, and SPI

Others

Regional Analysis: Modular Hall Effect Sensors Market

North America The North American market remains a key revenue generator for modular Hall effect sensors, driven by strong automotive and industrial automation demand. The U.S. accounts for over 60% of the regional market value, benefiting from heavy investments in electric vehicle manufacturing and smart factory initiatives. Recent technological advancements by market leaders like Allegro MicroSystems and Texas Instruments have strengthened product offerings in high-temperature and high-precision applications. However, pricing pressures from Asian manufacturers pose a challenge to domestic producers. The Canadian market shows steady growth, particularly in aerospace and medical equipment segments where reliability is paramount.

Europe Europe’s market is characterized by stringent quality standards and innovation-driven demand, particularly in automotive and industrial sectors. Germany leads adoption with its robust manufacturing base, while Nordic countries demonstrate increasing usage in renewable energy systems. The Hall Switch segment dominates due to its prevalence in automotive position sensing applications. European OEMs emphasize miniaturization and energy efficiency, creating opportunities for modular sensors with integrated signal processing. However, the transition to electric vehicles has temporarily disrupted traditional supply chains, causing suppliers to realign production capacities toward EV-specific sensor solutions.

Asia-Pacific Asia-Pacific represents the fastest-growing regional market, projected to capture over 45% of global demand by 2032. China’s dominance stems from massive electronics production and government-backed Industry 4.0 initiatives fueling industrial automation. Japanese manufacturers lead in high-precision applications like robotics, while South Korea sees strong demand from consumer electronics giants. The region witnesses intense price competition, with local players like ROHM Semiconductor gaining market share through cost-effective solutions. India emerges as a promising market with expanding automotive manufacturing and infrastructure modernization programs, though quality consistency remains a concern among buyers.

South America Market growth in South America remains moderate, constrained by economic instability and limited local manufacturing capabilities. Brazil accounts for nearly half the regional demand, primarily serving automotive and appliance industries. Cost sensitivity drives preference for basic Hall Switch models over advanced linear sensors. While foreign investments in Argentina’s industrial sector show potential, currency volatility discourages long-term commitments from major sensor suppliers. The aftermarket for sensor replacements presents steady opportunities, particularly in aging industrial equipment maintenance across the continent.

Middle East & Africa This region demonstrates uneven growth patterns, with Gulf Cooperation Council countries leading adoption in oil/gas and building automation applications. Israel’s thriving medical technology sector drives specialist demand for high-reliability sensors. South Africa serves as an industrial hub for sub-Saharan Africa, though infrastructure limitations hinder widespread sensor integration. The market sees increasing Chinese imports due to competitive pricing, while European suppliers maintain dominance in high-value industrial projects. Government initiatives to diversify economies toward manufacturing create long-term growth potential, albeit from a comparatively small base.

Report Scope

This market research report provides a comprehensive analysis of the global Modular Hall Effect Sensors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Hall Switch, Linear Hall Sensor), application (Consumer Electronics, Automotive, Aerospace, Medical, Industrial), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America (USD million market size in U.S.), Europe, Asia-Pacific (China projected at USD million), Latin America, and Middle East & Africa.

Competitive Landscape: Profiles of leading market participants including Sensata Technologies, Texas Instruments, Allegro MicroSystems, and others holding approximately % market share in 2024.

Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with IoT systems, and evolving industry standards for magnetic sensing applications.

Market Drivers & Restraints: Evaluation of factors including automotive electrification, industrial automation demand, along with supply chain constraints and material cost challenges.

Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/global-video-sync-separator-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silicon-rings-and-silicon-electrodes_17.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-bonding-tool-market-investments.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/coaxial-panels-market-challenges.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/oled-and-led-automotive-light-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/gas-cell-market-demand-for-ai-chips-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digital-demodulator-ic-market-packaging.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nano-micro-connector-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/single-mode-laser-diode-market-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silicon-rings-and-silicon-electrodes.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/battery-management-system-chip-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/scanning-slit-beam-profiler-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/atomic-oscillator-market-electronics.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/plastic-encapsulated-thermistor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-bonding-tool-market-policy.html

0 notes

Text

🔬 Advanced Optics Market Size, Share & Growth Analysis 2034: Shaping the Future of Vision Tech

Advanced Optics Market is set for a significant growth trajectory, projected to surge from $4.5 billion in 2024 to $9.8 billion by 2034, at a steady CAGR of 8.1%. This market comprises high-performance optical components and technologies that drive critical innovations in industries like telecommunications, aerospace, healthcare, and defense. Products such as precision lenses, optical fibers, waveplates, and adaptive optics are now vital in imaging, sensing, and communication applications. With industries rapidly digitalizing and adopting technologies like 5G, AI, and AR, advanced optics is at the forefront of enabling ultra-precise performance, pushing market demand upward.

Market Dynamics

Several forces are propelling the growth of this industry. Firstly, the integration of artificial intelligence with optics is enabling smarter imaging and analysis solutions across healthcare and industrial automation. Secondly, the growing demand for miniaturized and portable devices in consumer electronics and wearables is pushing the boundaries of design in optical components.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS21465

Additionally, green manufacturing practices and a push toward eco-friendly materials have gained prominence, aligning the industry with global sustainability goals. On the other hand, challenges such as the high costs of advanced optics, stringent regulatory requirements, and geopolitical supply chain disruptions — especially concerning rare earth materials — pose hurdles for market players.

Key Players Analysis

The market is dominated by stalwarts like Carl Zeiss AG, Corning Incorporated, and Nikon Corporation, all known for their advanced research in material science and photonics. Companies such as Jenoptik, Lumentum, and Edmund Optics continue to push the boundaries in high-precision components, while emerging innovators like Photonica Innovations, Spectra Nova, and Aether Light Technologies are introducing disruptive technologies. Strategic collaborations, especially those focusing on quantum photonics and AI-driven optics, are accelerating product innovation and market reach. These players are investing heavily in nanotechnology and automated manufacturing, significantly enhancing performance and scalability.

Regional Analysis

North America leads the global advanced optics market, driven by robust R&D activity, especially in the U.S., across defense, healthcare, and telecommunications sectors. The region benefits from a rich tech ecosystem and strong institutional support.

Europe is a close contender, with Germany and the UK at the helm, leveraging strengths in automotive, aerospace, and photonic innovations. The presence of leading universities and photonics research hubs enhances the region’s capabilities.

Asia-Pacific is rapidly catching up, with countries like China, Japan, South Korea, and Taiwan leading manufacturing and electronic component integration. Rising investments in smart city infrastructure and 5G networks make the region a hotbed for advanced optical applications.

In Latin America, Brazil and Mexico are spearheading growth through increased adoption in healthcare and industrial sectors. Meanwhile, the Middle East and Africa — particularly the UAE and Saudi Arabia — are making strides through smart surveillance and infrastructure projects.

Recent News & Developments

Recent trends showcase a strong pivot towards AI-integrated optical systems, enhancing performance in sectors such as autonomous vehicles, telemedicine, and industrial robotics. Pricing in this market is diverse — ranging from $100 basic components to over $10,000 for complex laser systems — reflecting the vast scope and customization in demand.

Notably, companies are embracing sustainable practices, such as using recyclable optical materials and reducing energy consumption in production. Moreover, regulatory landscapes continue to evolve, with stricter requirements for precision and safety, influencing product design and market entry strategies. Collaborations between tech giants and optics specialists are on the rise, aiming to build next-gen solutions that address both performance and environmental concerns.

Browse Full Report :https://www.globalinsightservices.com/reports/advanced-optics-market/

Scope of the Report

This report delivers a comprehensive analysis of the Advanced Optics Market, covering diverse market segments including product types, applications, technologies, and regional dynamics. It includes qualitative and quantitative data, covering past trends (2018–2023) and forecasts through 2034. Market segmentation spans everything from lenses and optical coatings to adaptive and diffractive optics, and covers end users from medical to industrial sectors.

The research also provides detailed assessments of competitive strategies, regulatory landscapes, and regional opportunities, offering actionable insights for investors, manufacturers, and policymakers. It identifies key development areas such as custom optics, optical design services, and smart imaging systems, providing a clear roadmap for stakeholders to navigate future growth in this fast-evolving industry.

#advancedoptics #photonics #telecomtechnology #medicalimaging #opticalinnovation #aerospaceoptics #defensetechnology #aiopticsintegration #sustainabletech #5ginfrastructure

Discover Additional Market Insights from Global Insight Services:

Data Center Interconnect Market : https://www.globalinsightservices.com/reports/data-center-interconnect-market/

Advanced Optics Market : https://www.globalinsightservices.com/reports/advanced-optics-market/

Class D Audio Amplifier Market : https://www.globalinsightservices.com/reports/class-d-audio-amplifier-market/

Service Robotics Market : https://www.globalinsightservices.com/reports/service-robotics-market/

Radio Frequency Identification Market : https://www.globalinsightservices.com/reports/radio-frequency-identification-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

Digital Transformation Market – Will Cloud and AI Redefine Competitive Advantage by 2032

Digital Transformation Market was valued at USD 895.7 Billion in 2023 and is expected to reach USD 6877.6 Billion by 2032 and grow at a CAGR of 25.44% from 2024-2032.

Digital Transformation Market is reshaping global industries as organizations accelerate the adoption of advanced technologies to remain competitive. Cloud computing, AI, IoT, automation, and big data are no longer optional—they're foundational. Companies across sectors are rethinking operations, improving customer experience, and building agile infrastructure to drive long-term success.

U.S.: Enterprises are rapidly embracing digital-first models to lead in agility, scalability, and efficiency

Digital Transformation Market continues to thrive as enterprises prioritize innovation and resilience. With increased investment in digital tools, especially post-pandemic, the market has evolved into a strategic priority. Businesses are now focusing on seamless integration, data-driven decision-making, and enhancing productivity through smarter digital ecosystems.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/2834

Market Keyplayers:

Microsoft - Microsoft Azure

IBM - IBM Watson

Salesforce - Salesforce Customer 360

Oracle - Oracle Cloud Infrastructure

SAP - SAP S/4HANA

Google - Google Cloud Platform

Amazon Web Services (AWS) - AWS Lambda

Cisco - Cisco Meraki

Accenture - myConcerto

Deloitte - Deloitte Digital

Infosys - Infosys Digital Services

Capgemini - Capgemini Cloud Services

Wipro - Wipro HOLMES

HCL Technologies - HCL Digital Transformation Services

Adobe - Adobe Experience Cloud

TCS (Tata Consultancy Services) - TCS BaNCS

ServiceNow - ServiceNow ITSM

Atos - Atos Digital Transformation Solutions

Zebra Technologies - Zebra's SmartVision

Pega - Pega Customer Decision Hub

Market Analysis

The digital transformation journey is being shaped by rising customer expectations, the demand for real-time insights, and the need to modernize legacy systems. In both the U.S. and Europe, industries including finance, healthcare, manufacturing, and retail are leveraging digital tools to streamline operations, ensure compliance, and unlock new growth avenues. Strategic partnerships between tech providers and enterprises are further fueling adoption.

Market Trends

Surge in cloud-native application development

Increased investment in AI-powered analytics

Adoption of remote and hybrid work tech stacks

Growth of edge computing for faster data processing

Rise in cybersecurity platforms integrated with digital infrastructure

Expansion of RPA (Robotic Process Automation) to automate workflows

Use of digital twins in manufacturing and infrastructure

Market Scope

The Digital Transformation Market is expanding at an unprecedented pace, touching nearly every industry and process. Organizations are not only adopting technology but embedding it into their core strategies.

End-to-end digital integration across business units

Scalable SaaS platforms supporting cross-functional teams

Industry-specific transformation frameworks

Real-time customer experience management tools

AI and machine learning models enhancing personalization

Smart infrastructure for cities and enterprises

Forecast Outlook

The market outlook for digital transformation is one of aggressive innovation and cross-industry convergence. With continuous advancement in AI, automation, and cloud computing, enterprises will increasingly leverage digital technologies to boost agility and customer-centricity. U.S. and European firms are expected to lead in deployment, setting benchmarks for global digital maturity. Competitive advantage will hinge on speed of adoption, data utilization, and transformation strategy execution.

Access Complete Report: https://www.snsinsider.com/reports/digital-transformation-market-2834

Conclusion

Digital transformation is no longer about future-proofing—it's about leading the present. In a market where agility defines market share, businesses that integrate digital into their DNA will dominate. As the U.S. sets benchmarks in enterprise-scale deployment and Europe emphasizes secure, compliant digital growth, the stage is set for an era of smarter, faster, and more connected organizations.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Related Reports:

U.S.A embraces cutting-edge innovations to revolutionize the Digital Farming Market

U.S.A sees rising investment in the Distribution Automation Market to boost energy efficiency and reliability

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

0 notes

Text

U.S. Robotics Integration for the Manufacturing Market Research Forecast (2024-2029) | BIS Research

The integration of robotics into manufacturing processes has been revolutionizing the industrial landscape, driving efficiency, productivity, and competitiveness. In the United States, the robotics integration for the manufacturing market is poised for significant growth.

With the release of the comprehensive "U.S. Robotics Integration for the Manufacturing Market" report by BIS Research, industry stakeholders are poised to gain invaluable insights into this transformative phenomenon.

The report delves deep into the intricacies of U.S. robotics integration for the manufacturing industry, offering a meticulous analysis of market trends, growth drivers, challenges, and opportunities. By leveraging data-driven research methodologies, the organization provides a holistic view of the current landscape and future projections for robotics integration in manufacturing.

According to BIS Research, the U.S. Robotics Integration for the Manufacturing Market is estimated to reach $7.48 Billion in 2029 from $3.94 Billion in 2023, at a CAGR of 11.69% during the forecast period 2024-2029.

Overview of the U.S. Robotics Integration for the Manufacturing Market

The U.S. Robotics Integration for the Manufacturing Industry is experiencing a transformative phase, as automation becomes a critical driver of industrial progress. The market encompasses the adoption and integration of robotics systems, including industrial robots, collaborative robots (cobots), and autonomous mobile robots (AMRs), into manufacturing facilities across various industries. These robots are designed to perform repetitive, complex, and hazardous tasks, enhancing efficiency, quality, and workplace safety.

Empower your strategic planning with data-driven insights. Download our Free U.S. Robotics Integration for the Manufacturing Market Research Report to gain a competitive edge.

Key Market Insights on Robotics Integration

Increasing Demand for Automation: The U.S. manufacturing industry is witnessing a growing demand for automation to address challenges such as labor shortages, rising labor costs, and the need for improved productivity. Robotics integration offers manufacturers the ability to streamline operations, increase production throughput, reduce errors, and enhance overall efficiency.

Advancements in Robotics Technology: Industrial robots are becoming more advanced, with features such as improved sensing capabilities, more precise motion control, and increased payload capacities. Cobots, designed to work safely alongside human workers, offer flexibility and versatility in manufacturing environments. AMRs are gaining prominence in logistics and warehousing, enabling autonomous material transportation and fulfillment operations.

Cost Reduction and Return on Investment (ROI): While the initial investment in robotics integration can be significant, the long-term benefits and return on investment are compelling for manufacturers. By automating processes, manufacturers can reduce labor costs, improve product quality, minimize waste, and optimize resource utilization.

Collaboration between Humans and Robots: The concept of human-robot collaboration (HRC) is gaining traction in the U.S. manufacturing industry. Cobots, equipped with safety features such as force sensors and vision systems, can work alongside human workers without the need for physical barriers.

U.S. Robotics Market Segmentation by Application

Aviation

SpaceTech and Aerospace

Automotive

Consumer Electronics

Robotics and Automation

Semiconductor

Renewable Energy and Power

FoodTech

Warehousing

HealthTech and MedTech

Research Forecast and Future Opportunities

According to the research forecast by BIS Research, the U.S. robotics integration for the manufacturing industry is expected to witness substantial growth in the coming years (2024-2029). Factors such as the increasing demand for automation, advancements in robotics technology, and the pursuit of operational excellence are driving market expansion. The research also highlights the potential growth opportunities in sectors such as automotive, electronics, pharmaceuticals, food and beverage, and logistics.

Conclusion

In conclusion, as the manufacturing landscape continues to evolve, the U.S. Robotics Integration for the Manufacturing Industry is poised for significant growth, driven by the need for automation, technological advancements, and the pursuit of operational excellence. As manufacturers embrace robotics integration, they can achieve higher productivity, improved product quality, and enhanced workplace safety. The collaborative nature of human-robot interaction is reshaping the manufacturing landscape, enabling efficient and harmonious collaboration between humans and robots.

#U.S. Robotics Integration for the Manufacturing Market#U.S. Robotics Integration for the Manufacturing Report#U.S. Robotics Integration for the Manufacturing Industry#U.S. Robotics Integration for the Manufacturing Market Size#U.S. Robotics Integration for the Manufacturing Market Forecast#U.S. Robotics Integration for the Manufacturing Market CAGR#U.S. Robotics Integration for the Manufacturing Industry Analysis#U.S. Robotics Integration for the Manufacturing Market Research#BIS Research#Robotics and Automation

0 notes

Text

Industrial Efficiency Gains Spark Growth in Torque Limiter Market

The global Torque Limiter Market was valued at US$ 324.9 Mn in 2023 and is projected to grow at a CAGR of 5.8% from 2024 to 2034, reaching US$ 597.4 Mn by the end of the forecast period. Increasing demand for machine safety, process efficiency, and the integration of advanced technologies is fueling this robust expansion.

Market Overview: Torque limiters, essential components in mechanical systems, play a critical role in protecting machinery from damage due to overload conditions. They disengage the drive system when preset torque levels are exceeded, ensuring operational safety and minimizing downtime.

The ongoing transition to smart manufacturing, fueled by Industry 4.0, is significantly contributing to the adoption of torque limiters. Industries such as automotive, aerospace, and renewable energy are the largest consumers of these components due to their need for precision, reliability, and safety.

Market Drivers & Trends

Automation in Production Processes: The proliferation of automation, especially in developing economies, is a major growth driver. Smart factories demand precise safety mechanisms, prompting widespread integration of torque limiters.

Electric Vehicle Growth: Torque limiters are essential in protecting sensitive EV components from torque surges. The EV boom, especially in Asia and Europe, is translating to increased product demand.

Wind Energy Integration: As wind turbines face varying loads, torque limiters prevent mechanical failure, ensuring operational reliability. This is particularly significant as global wind capacity surpassed 900 GW in 2023.

Latest Market Trends

Smart Torque Limiters: IoT-enabled limiters with real-time monitoring capabilities are becoming mainstream. These systems offer predictive maintenance and better control, aligning with smart factory goals.

Customization and Miniaturization: With the rise of compact machinery and robotics, manufacturers are offering smaller and application-specific torque limiters.

Sustainability and Energy Efficiency: Modern torque limiters are being designed with a focus on energy savings, lighter materials, and recyclability to meet environmental standards.

Key Players and Industry Leaders

The market is moderately fragmented with the presence of prominent players including:

Chr. Mayr GmbH + Co. KG

R+W Antriebselemente GmbH

KTR Systems GmbH

Nexen Group, Inc.

Tsubakimoto Chain Co.

Altra Industrial Motion Corp.

RINGSPANN GmbH

Howdon Power Transmission Ltd.

These companies are investing heavily in R&D, digital capabilities, and strategic partnerships to enhance their offerings and global presence.

Explore the highlights and essential data from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=32813

Recent Developments

Regal Rexnord Corporation (June 2023) launched the next-gen Autogard F400 Series torque limiter with enhanced performance and drop-in compatibility.

ENEMAC (May 2023) introduced the ECP torque limiter featuring an integrated ball bearing for superior concentricity and overload protection in indirect drives.

U.S. Tsubaki (2020) unveiled a torque limiter sprocket assembly combining torque control and drive in a single unit, offering ease of installation and reliability.

Market Opportunities

Emerging Economies: Expanding industrial bases in India, Southeast Asia, and Latin America present substantial growth avenues, especially with increasing government investments in automation.

Retrofit Solutions: As legacy equipment needs upgrades to comply with safety norms, torque limiter retrofits offer a lucrative opportunity.

Predictive Maintenance Services: There’s rising demand for service models that combine hardware with analytics-driven maintenance, particularly in high-risk environments.

Future Outlook

According to industry analysts, the torque limiter market is on a steady trajectory, driven by the convergence of smart manufacturing, safety standards, and sustainable industrial practices. The integration of torque limiters into predictive maintenance ecosystems and their indispensable role in electrification will sustain long-term market momentum.

While higher upfront costs of advanced models may pose a challenge in cost-sensitive regions, the return on investment in terms of reduced downtime and equipment longevity makes a compelling case for adoption.

Market Segmentation

By Type:

Friction Type

Ball & Roller Type (Dominated market with 65.6% share in 2023)

Others

By Torque Range:

< 150 Nm

151–500 Nm

501–3000 Nm (Held 35.9% market share in 2023)

3000 Nm

By End-user Industry:

Automotive

Aerospace

Energy & Power

Fabricated Metal Manufacturing

Food & Beverage

Packaging & Labelling

Plastic & Rubber

Others

Regional Insights