#Wood Plastic Composite Market Share

Text

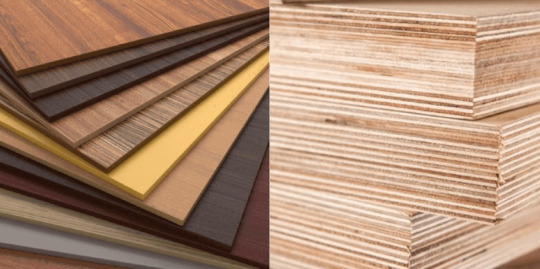

Wood Plastic Composite Market Comprehensive Analysis And Future Estimations 2032

Global Wood Plastic Composite Market Report from Market Research Forecast highlights deep analysis on market characteristics, sizing, estimates and growth by segmentation, regional breakdowns & country along with competitive landscape, player’s market shares, and strategies that are key in the market. The exploration provides a 360° view and insights, highlighting major outcomes of the industry. These insights help the business decision-makers to formulate better business plans and make informed decisions to improved profitability. In addition, the study helps venture or private players in understanding the companies in more detail to make better informed decisions.

Major Players in This Report Include:

Seven Trust (China), Meghmani Group (India), Biologic (Belgium), Trex Company, Inc. (U.S.), UFP Industries, Inc. (U.S.), Fiberon LLC (U.S.), Axion International, Inc. (U.S.), Josef Ehrler GmbH & Co KG (Germany), Croda International Plc (UK), CertainTeed (U.S.) and Others

Free Sample Report + All Related Graphs & Charts @: https://marketresearchforecast.com/report/wood-plastic-composite-market-1618/sample-report

The Wood Plastic Composite Marketsize was valued at USD 4.77 USD Billion in 2023 and is projected to reach USD 6.76 USD Billion by 2032, exhibiting a CAGR of 5.1 % during the forecast period.

Market Drivers:

Increasing Airplane Fleet Worldwide To Propel The Demand For Aerospace Materials

Restrains:

Fluctuating Raw Material Prices Shall Hinder Market Growth

Enquire for customization in Report @: https://marketresearchforecast.com/report/wood-plastic-composite-market-1618/enquiry-before-buy

In this research study, the prime factors that are impelling the growth of the Global Wood Plastic Composite market report have been studied thoroughly in a bid to estimate the overall value and the size of this market by the end of the forecast period. The impact of the driving forces, limitations, challenges, and opportunities has been examined extensively. The key trends that manage the interest of the customers have also been interpreted accurately for the benefit of the readers.

The Wood Plastic Composite market study is being classified Material: Polyethylene, Polypropylene, Polyvinyl Chloride and Others","Application: Decking, Automotive, Sliding & fencing, Technical Application, Furniture, Consumer Goods and Others

The report concludes with in-depth details on the business operations and financial structure of leading vendors in the Global Wood Plastic Composite market report, Overview of Key trends in the past and present are in reports that are reported to be beneficial for companies looking for venture businesses in this market. Information about the various marketing channels and well-known distributors in this market was also provided here. This study serves as a rich guide for established players and new players in this market.

Get Reasonable Discount on This Premium Report @ https://marketresearchforecast.com/report/wood-plastic-composite-market-1618/request-discount

Extracts from Table of Contents

Wood Plastic Composite Market Research Report

Chapter 1 Wood Plastic Composite Market Overview

Chapter 2 Global Economic Impact on Industry

Chapter 3 Global Market Competition by Manufacturers

Chapter 4 Global Revenue (Value, Volume*) by Region

Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions

Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type

Chapter 7 Global Market Analysis by Application

………………….continued

This report also analyses the regulatory framework of the Global Markets Wood Plastic Composite Market Report to inform stakeholders about the various norms, regulations, this can have an impact. It also collects in-depth information from the detailed primary and secondary research techniques analysed using the most efficient analysis tools. Based on the statistics gained from this systematic study, market research provides estimates for market participants and readers.

Contact US :

Craig Francis (PR & Marketing Manager)

Market Research Forecast

Unit No. 429, Parsonage Road Edison, NJ

New Jersey USA – 08837

Phone: (+1 201 565 3262, +44 161 818 8166)

[email protected]

#Global Wood Plastic Composite Market#Wood Plastic Composite Market Demand#Wood Plastic Composite Market Trends#Wood Plastic Composite Market Analysis#Wood Plastic Composite Market Growth#Wood Plastic Composite Market Share#Wood Plastic Composite Market Forecast#Wood Plastic Composite Market Challenges

0 notes

Text

Wood Plastic Composite Market To Grow Fastest in the APAC Region

The total size of the wood plastic composite market was about USD 7,489.7 million in 2023, and it will power at a rate of 10% by the end of this decade, to touch USD 14,412.9 million by 2030.

Wood plastic composites are smooth and firm pellets created from a mix of ultra-fine wood elements and renewable, biodegradable, or recycled plastic. They are put to use in outdoor decking materials,…

View On WordPress

#Wood-Plastic Composite Market#Wood-Plastic Composite Market Demand#Wood-Plastic Composite Market Growth#Wood-Plastic Composite Market Share#Wood-Plastic Composite Market Size

0 notes

Text

Exploring the Lucrative Wood Plastic Composite Market: A Comprehensive Analysis

Wood Plastic Composite (WPC) is a type of composite material that combines wood fibers or particles with thermoplastics to create a versatile and durable product. WPC offers a combination of the natural aesthetics of wood with the added benefits of plastic, such as moisture resistance, durability, and low maintenance requirements. This unique combination has led to its widespread use in various industries, including construction, automotive, furniture, and packaging.

The global Wood Plastic Composite market has experienced significant growth in recent years and is expected to continue expanding at a substantial rate. Several factors have contributed to the market's growth, including the increasing demand for sustainable and eco-friendly building materials, the rising preference for low-maintenance products, and the growing construction activities in emerging economies.

Key Factors Driving the Wood Plastic Composite Market:

Sustainable Construction Practices: WPCs are considered environmentally friendly materials as they utilize recycled materials and reduce the demand for virgin plastics and wood. The rising awareness and adoption of sustainable construction practices have driven the demand for WPC in the building and construction industry.

Low Maintenance Requirements: Compared to traditional wood products, WPC requires minimal maintenance, such as sealing, staining, or painting. This feature has made it a popular choice among consumers, especially in applications such as decking, fencing, and outdoor furniture.

Durability and Longevity: WPC offers enhanced durability, resistance to rot, decay, and insect damage, making it a suitable alternative to natural wood. The long lifespan of WPC products reduces replacement costs and contributes to its growing demand.

Versatility of Applications: Wood Plastic Composite can be molded into various shapes, sizes, and profiles, providing designers and architects with versatility in their applications. It is used in a wide range of products, including decking, railing, cladding, fencing, furniture, automotive interiors, and packaging materials.

Rising Construction Activities: The growing construction industry, particularly in developing economies, has fueled the demand for Wood Plastic Composite products. Rapid urbanization, infrastructure development, and increased disposable incomes have resulted in higher demand for cost-effective and sustainable construction materials.

Government Regulations and Policies: Government initiatives promoting sustainable construction practices and environmental regulations encouraging the use of recycled materials have positively impacted the Wood Plastic Composite market. Supportive policies and incentives offered by governments across various regions have further boosted the market growth.

Regional Analysis:

The Wood Plastic Composite market is geographically segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

North America: The North American market has witnessed significant growth due to the rising demand for eco-friendly and sustainable building materials. The stringent regulations regarding the use of hazardous chemicals in construction materials have also driven the adoption of Wood Plastic Composite products in this region.

Europe: Europe is a mature market for WPC, with increased focus on sustainable construction practices and regulations promoting the use of recycled materials. The demand for WPC in decking and outdoor applications is particularly high in countries like Germany, the UK, and France.

Asia Pacific: Asia Pacific is the fastest-growing region for the Wood Plastic Composite market. Rapid urbanization, infrastructure development, and increasing disposable incomes in countries like China and India have fueled the demand for WPC products. The region is also a significant producer of wood-based materials, providing ample availability of raw materials for WPC production.

Latin America: The Latin American market has shown considerable growth potential due to the increasing construction activities and the demand for low-maintenance and durable materials. Brazil and Mexico are the key markets driving the growth in this region.

Middle East and Africa: The Middle East and Africa region is witnessing growth in the Wood Plastic Composite market due to the rising construction industry and the need for sustainable materials. The market is driven by countries like Saudi Arabia, UAE, and South Africa.

Key Players:

The Wood Plastic Composite market is highly competitive, with several prominent players operating globally. Some of the key players in the market include:

Trex Company, Inc.

Advanced Environmental Recycling Technologies, Inc.

Fiberon LLC

UPM-Kymmene Corporation

TimberTech (Azek Building Products)

CertainTeed (Saint-Gobain)

Beologic N.V.

Polyplank AB

Tamko Building Products, Inc.

Green Plank AB

These companies are actively engaged in research and development activities, strategic collaborations, mergers and acquisitions, and product innovations to strengthen their market position and expand their product portfolios.

Conclusion:

The Wood Plastic Composite market has witnessed substantial growth in recent years, driven by the increasing demand for sustainable and low-maintenance construction materials. The market is expected to continue expanding due to factors such as rising construction activities, the need for eco-friendly products, and supportive government regulations. With ongoing technological advancements and product innovations, the Wood Plastic Composite industry is poised for further development and offers significant opportunities for manufacturers, suppliers, and investors worldwide.

0 notes

Text

The global biocomposites market size was USD 24.4 billion in 2021 and is expected to reach USD 51.2 billion by 2026, projecting a CAGR of 16.0% between 2021 and 2026. Biocomposites are increasingly used in the transportation end-use industry as they decrease weight and increase fuel efficiency. Automotive manufacturers are increasingly using biocomposites in various automobile models. The regulatory legislation imposed by the EU and other countries, such as the US, India, and Japan; are expected to increase the use of biocomposites, primarily in the automotive end-use industry. The EU legislation sets mandatory emission reduction targets for new cars to improve fuel economy and reduce the CO2 emissions.

The US has also imposed stricter Corporate Average Fuel Economy (CAFE) and tailpipe emission standards for the automobile sector. The proposed mandate raised CAFÉ standards to 39 mpg for passenger cars by 2016 and 54.5 mpg by 2025. China and Japan have also announced vehicle fuel economy regulations. Brazil, India, Mexico, and South Africa are expected to initiate similar measures in the near future. The above-mentioned factors and increased incorporation of biocomposites are expected to increase their demand mainly in the automobile sector.

The automotive industry focuses on stringent regulations, such as the Corporate Average Fuel Efficiency (CAFE) standards and the European Emission Standards (EES) by the US and European governments, respectively, for vehicle manufacturers. According to the United States Environmental Protection Agency (EPA), the transportation industry in the US is one of the largest contributors to greenhouse gas emissions. The US government has, thus, made it a critical concern for automakers to follow the average miles per gallon standard for their vehicles. A similar situation is prevalent in other regions across the globe. In order to reduce carbon dioxide (CO2) emissions, automakers focus significantly on producing lightweight vehicles to comply with government regulations and enhance fuel efficiency.

#Biocomposites Market#bio composite#bio composites#biocomposite products#biocomposite plastic#biocomposites reinforced with natural fibers#bio composite material#biofibres and biocomposites#Biocomposites Industry#COVID 19 impact on Biocomposites Market#Asia Pacific Biocomposites Market#wood fiber composites#Global Biocomposites Market#Biocomposites Market share#Biocomposites Market Size#Biocomposites Market Demand#Biocomposites Market Growth#Biocomposites Market Opportunity#Sales of Biocomposites#Demand of Biocomposites#Europe Biocomposites Market#North America Biocomposites Market

0 notes

Text

Formwork Panels Market Analysis, Size, Share, Growth, Trends, and Forecasts by 2031

Formwork panels are a critical component in the construction of concrete structures and buildings. The global formwork panels market provides the molds and frames used to shape poured concrete for walls, columns, beams, slabs, and foundations. As infrastructure development accelerates worldwide, the demand for high-quality formwork panels continues to grow.

𝐆𝐞𝐭 𝐚 𝐅𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭:https://www.metastatinsight.com/request-sample/2581

Top Companies

Doka Group

PERI GmbH

ULMA Construction

Alsina Formwork Solutions

MEVA Schalungs-Systeme GmbH

RMD Kwikform

Hünnebeck GmbH

PASCHAL-Werk G. Maier GmbH

NOE-Schaltechnik Georg Meyer-Keller GmbH + Co. KG

Ischebeck Titan GmbH

Construx b.v.b.a

Faresin Formwork

Sateco SAS

RINGER GmbH

EFCO Corp.

Formwork panels create a temporary mold into which wet concrete is poured and contained as it hardens. Panels are typically made of wood, steel, aluminum, or fiberglass. They interlock in a grid-like configuration using ties and braces to build the overall concrete form. Panels must withstand concrete pressure while maintaining dimensional accuracy for the cured structure.

Access Full Report @https://www.metastatinsight.com/report/formwork-panels-market

Increasingly, constructors are adopting system formwork over traditional site-built wooden forms. System formwork relies on prefabricated modular panels that are erected on-site. These systems boost productivity and enable faster, safer construction of complex structures. As urbanization and massive projects like high-rises, bridges, dams, and stadiums increase globally, system formwork adoption fuels formwork panel market growth.

Asia Pacific currently dominates the global formwork panels market, with many major suppliers based in China. Developing nations across the Asia Pacific region are undergoing rapid development of commercial and residential buildings as populations urbanize. North America and Europe are mature markets for formwork panels used in non-residential construction. The Middle East, Africa, and Latin America present high growth potential as infrastructure investments modernize urban centers.

Trends impacting the global formwork panels market include labor shortages, demand for faster project timelines, and a need for more complex geometries. In response, manufacturers are developing innovative new lightweight panels along with ancillary products like release agents and automated installation systems. Building information modeling aids in formwork design and construction engineering. Plastic and composite formwork promises improved sustainability over traditional materials.

As the formwork panels market evolves worldwide, suppliers aim to provide value-added services and optimized concrete forming solutions. Increasing quality, cost-competitiveness, and on-time delivery gives companies an edge in this essential construction materials sector. With the global demand for landmark buildings and advanced infrastructure projected to accelerate, the market for high-performance formwork panels will continue expanding apace.

Global Formwork Panels market is estimated to reach $9,268.5 Million by 2031; growing at a CAGR of 5.2% from 2024 to 2031.

Contact Us:

+1 214 613 5758

#FormworkPanelsMarket#marketsize#marketgrowth#marketforecast#marketanalysis#marketdemand#marketreport#marketresearch

0 notes

Text

Heat Exchangers Market 2024: Industry Analysis and Opportunity Assessment, Forecast to 2030

Heat Exchangers Industry Overview

The global heat exchangers market size was estimated at USD 18.19 billion in 2023 and is expected to expand at a compounded annual growth rate (CAGR) of 5.4% from 2024 to 2030.

Rising focus on efficient thermal management in various industries, including oil & gas, power generation, chemical & petrochemical, food & beverage, and HVAC & refrigeration, is expected to drive the demand for heat exchangers over the forecast period. Rising demand from chemical industry coupled with increasing technological advancements and a growing focus on improving efficiency standards is expected to drive heat exchangers market growth. Most processes in petrochemical facilities involve high pressure and temperature, thus, necessitating the optimization of heat transfer and enhancement of energy savings, which, in turn, is likely to boost the demand for energy-efficient heat exchangers.

Gather more insights about the market drivers, restrains and growth of the Heat Exchangers Market

U.S. dominated the North America heat exchanger market in 2023, owing to high electricity demand, industrialization, and investments in renewable power generation. Rising investments by oil & gas companies in exploration & production activities in the U.S. are expected to boost the demand for these products in oil & gas industry.

Significant power markets such as China, U.S., India, Russia, and Japan are restructuring their operating models to adopt the structure of renewable energy and efficient utilization of energy by installing heat exchangers and shifting from traditional energy use. This is expected to drive the demand for heat exchangers.

Technological advancements such as tube inserts in heat exchangers are expected to complement the market growth. Furthermore, ongoing technological improvements to improve energy efficiency, total life cycle cost, durability, and compactness of heat exchangers are expected to drive industry growth.

Manufacturers of these products face a long list of difficult supply chain challenges, including increasing demand variability, intense global competition, more environmental compliance regulations, increasing human- and nature-based risks, and inventory proliferation. COVID-19 pandemic has created new challenges, which are compelling manufacturers to innovate their supply chains at a faster speed.

Heat Exchangers Market Segmentation

Grand View Research has segmented the global heat exchangers market report based on product, end-use, material and region:

Product Outlook (Revenue, USD Billion, 2018 - 2030)

Plate & Frame Heat Exchanger

Brazed Plate & Frame Heat Exchanger

Gasketed Plate & Frame Heat Exchanger

Welded Plate & Frame Heat Exchanger

Others

Shell & Tube Heat Exchanger

Air-Cooled Heat Exchanger

Others

End-use Outlook (Revenue, USD Billion, 2018 - 2030)

Chemical & Petrochemical

Oil & Gas

HVAC & Refrigeration

Power GenerationFood & Beverage

Pulp & Paper

Others

Material Outlook (Revenue, USD Billion, 2018 - 2030)

Metals

Alloys

Others

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

France

Italy

Spain

UK

Asia Pacific

China

Japan

India

South Korea

Australia

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

South Africa

Browse through Grand View Research's Advanced Interior Materials Industry Research Reports.

The global wood plastic composites market size was estimated at USD 7.15 billion in 2023 and is expected to grow at a CAGR of 11.6% from 2024 to 2030.

The global industrial fasteners market size was estimated at USD 95.57 billion in 2023 and is expected to grow at a CAGR of 4.7% from 2024 to 2030.

Key Companies & Market Share Insights

Global heat exchangers industry is characterized by presence of multinational as well as regional players that are engaged in designing, manufacturing, and distributing these products. Product manufacturers strive to obtain a competitive edge over their competitors by increasing application scope of their products.

Strategies adopted by manufacturers include new product development, diversification, mergers & acquisitions, and geographical expansion. These strategies aid the companies in expanding their market penetration and catering to changing technological demand across various end-use industries.

Key Heat Exchangers Companies:

Alfa Laval

Danfoss

Kelvion Holding GmbH

Güntner Group GmbH

Xylem Inc

API Heat Transfer

Mersen

Hisaka Works, Ltd.

Chart Industries, Inc

Johnson Controls International

HRS Heat Exchangers

SPX FLOW, Inc.

Funke Wärmeaustauscher Apparantebau GmbH

Koch Heat Transfer Company

Southern Heat Exchanger Corporation

Recent Developments:

For instance, in April 2023, Kelvion launched dedicated air cooler series for natural refrigerants. The CDF & CDH ranges are dual discharge air coolers highlighting a similar proficient tube system.

In May 2023, Alfa Laval is enhancing its brazed plate heat exchanger capacity to bolster the global energy transition. The establishment of new facilities in Italy, China, Sweden, and the U.S. signifies significant progress in their initiative to advance manufacturing intelligence and efficiency throughout the entire supply chain.

In January 2021, Alfa Laval, opened a new facility for the production of brazed heat exchangers in San Bonifacio, Italy. The new facility will have more capacity to fulfill the increasing customer demand.

Order a free sample PDF of the Heat Exchanger Market Intelligence Study, published by Grand View Research.

0 notes

Text

Reactive Hot Melt Adhesives Market projected to reach $2.6 billion by 2028

The report "Reactive Hot Melt Adhesives Market by Resin Type (Polyurethane, Polyolefin), Substrate (Plastic, Wood), Application (Automotive & Transportation, Doors & Windows, Furniture & Upholstery, Lamination, Textile), & Region - Global Forecast to 2028", is growing at a high rate due to the increased demand from various applications. The global reactive hot melt adhesives market size was USD 1.6 billion in 2022 and is projected to reach USD 2.6 billion by 2028, at a CAGR of 7.5% between 2023 and 2028. In the market for reactive hot melt adhesives, Asia Pacific is in the lead. Manufacturing and industrialization have surged as a result of the Asia Pacific region's several nations experiencing swift economic growth. This has consequently increased demand across a range of industries for sophisticated adhesive solutions like reactive hot melt adhesives.

Download pdf-https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=222009468

Reactive hot melt adhesives' increased performance, adaptability, and application efficiency are all a result of technological developments in the industry. Improvements in curing technology help to make curing procedures quicker and more effective. One example of this is the creation of adhesives that cure more quickly, allowing for speedier manufacturing cycles across a range of sectors. These days, certain reactive hot melt adhesives come with dual-cure systems that combine UV (ultraviolet) and hot melt curing technologies. This enables improved control over the curing process and offers versatility in bonding various materials.

Polyurethane segment is expected to hold largest share of the reactive hot melt adhesives market during the forecasted period.

Polyurethane reactive (PUR) hot melt systems typically serve as one-component adhesives, rapidly bonding to various substrates. Once applied, PUR initiates cross-linking, achieving 50%-80% of its ultimate bond strength within 3-6 hours, with a complete reactive cure expected within 24-36 hours post-application, influenced by air and substrate moisture conditions. These bonds are very strong and have exceptional heat resistance, cold resistance, and moisture-, cold, and moisture resistance.

Plastic substrate segment hold the largest segment in overall reactive hot melt adhesives market during forecast period.

Reactive hot melt adhesives are used widely on plastic substrates. The unique characteristics of reactive hot melt adhesives make them well-suited for bonding plastic substrates. They provide strong, durable, and efficient adhesion in industries such as automotive and electronics where plastics are widely used. When exposed to heat, reactive hot melt adhesives undergo a reactive process, often involving crosslinking. This results in a bond with enhanced strength and durability, which is crucial for applications with a robust connection, such as in the assembly of plastic components in automotive or electronics.

Automotive & Transportation is the fastest-growing application of the global reactive hot melt adhesives market during forecasted period.

In the automotive sector, reactive hot melt adhesives find broad application in bonding diverse components, such as plastic and metal parts. They play a crucial role in enhancing structural integrity, reducing noise, and streamlining assembly processes. These adhesives are extensively employed to create lightweight designs, enhance performance, and construct structures using a variety of materials like carbon fiber composites, glass fiber-reinforced composites, aluminum, and other multi-material combinations.

Sample Request- https://www.marketsandmarkets.com/requestsampleNew.asp?id=222009468

Asia Pacific region likely to account the largest share of the global reactive hot melt adhesives market during forecasted period.

Asia Pacific is one of the largest reactive hot melt adhesives markets, in terms of both value and volume, and is projected to grow significantly during the forecast period. The thriving construction industry, propelled by urbanization and infrastructure development, significantly contributes to the demand for these adhesives. Their applications extend to bonding materials in construction, furniture, and related sectors. Notably, the automotive industry, a key consumer of reactive hot melt adhesives, has witnessed remarkable growth in the Asia Pacific region. The increased utilization of these adhesives for purposes like lightweighting and structural bonding in the automotive manufacturing process has further fueled their demand.

The key companies profiled in this report are Henkel AG & Co. KGaA (Germany), The Dow Chemical Company (US), H.B. Fuller Company (US), Jowat SE (Germany), and 3M (US).

0 notes

Text

Heat Exchangers Market Analysis, Opportunities And Forecast Report 2024-2030

The global heat exchangers market size was estimated at USD 18.19 billion in 2023 and is expected to expand at a compounded annual growth rate (CAGR) of 5.4% from 2024 to 2030.

Rising focus on efficient thermal management in various industries, including oil & gas, power generation, chemical & petrochemical, food & beverage, and HVAC & refrigeration, is expected to drive the demand for heat exchangers over the forecast period. Rising demand from chemical industry coupled with increasing technological advancements and a growing focus on improving efficiency standards is expected to drive heat exchangers market growth. Most processes in petrochemical facilities involve high pressure and temperature, thus, necessitating the optimization of heat transfer and enhancement of energy savings, which, in turn, is likely to boost the demand for energy-efficient heat exchangers.

Gather more insights about the market drivers, restrains and growth of the Heat Exchangers Market

U.S. dominated the North America heat exchanger market in 2023, owing to high electricity demand, industrialization, and investments in renewable power generation. Rising investments by oil & gas companies in exploration & production activities in the U.S. are expected to boost the demand for these products in oil & gas industry.

Significant power markets such as China, U.S., India, Russia, and Japan are restructuring their operating models to adopt the structure of renewable energy and efficient utilization of energy by installing heat exchangers and shifting from traditional energy use. This is expected to drive the demand for heat exchangers.

Technological advancements such as tube inserts in heat exchangers are expected to complement the market growth. Furthermore, ongoing technological improvements to improve energy efficiency, total life cycle cost, durability, and compactness of heat exchangers are expected to drive industry growth.

Manufacturers of these products face a long list of difficult supply chain challenges, including increasing demand variability, intense global competition, more environmental compliance regulations, increasing human- and nature-based risks, and inventory proliferation. COVID-19 pandemic has created new challenges, which are compelling manufacturers to innovate their supply chains at a faster speed.

Heat Exchangers Market Segmentation

Grand View Research has segmented the global heat exchangers market report based on product, end-use, material and region:

Product Outlook (Revenue, USD Billion, 2018 - 2030)

• Plate & Frame Heat Exchanger

• Brazed Plate & Frame Heat Exchanger

• Gasketed Plate & Frame Heat Exchanger

• Welded Plate & Frame Heat Exchanger

• Others

• Shell & Tube Heat Exchanger

• Air-Cooled Heat Exchanger

• Others

End-use Outlook (Revenue, USD Billion, 2018 - 2030)

• Chemical & Petrochemical

• Oil & Gas

• HVAC & Refrigeration

• Power GenerationFood & Beverage

• Pulp & Paper

• Others

Material Outlook (Revenue, USD Billion, 2018 - 2030)

• Metals

• Alloys

• Others

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o France

o Italy

o Spain

o UK

• Asia Pacific

o China

o Japan

o India

o South Korea

o Australia

• Central & South America

o Brazil

o Argentina

• Middle East & Africa

o Saudi Arabia

o UAE

o South Africa

Browse through Grand View Research's Advanced Interior Materials Industry Research Reports.

• The global wood plastic composites market size was estimated at USD 7.15 billion in 2023 and is expected to grow at a CAGR of 11.6% from 2024 to 2030.

• The global industrial fasteners market size was estimated at USD 95.57 billion in 2023 and is expected to grow at a CAGR of 4.7% from 2024 to 2030.

Key Companies & Market Share Insights

Global heat exchangers industry is characterized by presence of multinational as well as regional players that are engaged in designing, manufacturing, and distributing these products. Product manufacturers strive to obtain a competitive edge over their competitors by increasing application scope of their products.

Strategies adopted by manufacturers include new product development, diversification, mergers & acquisitions, and geographical expansion. These strategies aid the companies in expanding their market penetration and catering to changing technological demand across various end-use industries.

Key Heat Exchangers Companies:

• Alfa Laval

• Danfoss

• Kelvion Holding GmbH

• Güntner Group GmbH

• Xylem Inc

• API Heat Transfer

• Mersen

• Hisaka Works, Ltd.

• Chart Industries, Inc

• Johnson Controls International

• HRS Heat Exchangers

• SPX FLOW, Inc.

• Funke Wärmeaustauscher Apparantebau GmbH

• Koch Heat Transfer Company

• Southern Heat Exchanger Corporation

Recent Developments:

• For instance, in April 2023, Kelvion launched dedicated air cooler series for natural refrigerants. The CDF & CDH ranges are dual discharge air coolers highlighting a similar proficient tube system.

• In May 2023, Alfa Laval is enhancing its brazed plate heat exchanger capacity to bolster the global energy transition. The establishment of new facilities in Italy, China, Sweden, and the U.S. signifies significant progress in their initiative to advance manufacturing intelligence and efficiency throughout the entire supply chain.

• In January 2021, Alfa Laval, opened a new facility for the production of brazed heat exchangers in San Bonifacio, Italy. The new facility will have more capacity to fulfill the increasing customer demand.

Order a free sample PDF of the Heat Exchanger Market Intelligence Study, published by Grand View Research.

#Heat Exchanger Market#Heat Exchanger Industry#Heat Exchanger Market size#Heat Exchanger Market share#Heat Exchanger Market analysis

0 notes

Text

Pigment Dispersants Market: Current Analysis and Forecast (2022-2028)

According to a new report published by UnivDatos Markets Insights, the Pigment Dispersants Market was valued at more than USD 38 billion in 2020 and is expected to grow at a CAGR of around 4% from 2022-2028. The analysis has been segmented into Pigment Type (Organic Pigment and Inorganic Pigment); Dispersion Type (Water-based and Solvent-based); Application (Decorative Paints & Coatings, Automotive Paints & Coatings, Industrial Paints & Coatings, Plastic, and Others); and Region/Country.

The pigment dispersants market report has been aggregated by collecting informative data on various dynamics such as market drivers, restraints, and opportunities. This innovative report makes use of several analyses to get a closer outlook on the pigment dispersants market. The pigment dispersants market report offers a detailed analysis of the latest industry developments and trending factors in the market that are influencing market growth. Furthermore, this statistical market research repository examines and estimates the pigment dispersants market at the global and regional levels.

Market Overview

Pigment dispersants are two-component structures, with the anchoring group providing strong adsorption onto the pigment surface. Polymeric chains, which are attached to the anchor group, provide stabilization. Pigment dispersants are used by manufacturers to color a wide range of materials, including paint, coatings, and plastics. Thermoset composites, inks, plastics, textiles, and decorative and industrial applications are some major factors in their uses.

The growing demand for paints and coatings in automotive, construction, and other industries in developing nations positively influences the growth of the market. For instance, according to the National Bureau of Statistics, construction output contributed 25.9% of China's GDP in 2020, up from 6.2% in 2019. This rapid growth in construction activity contributed to the growth of the pigment dispersant market.

Some of the major players operating in the market include BASF SE, King Industries Inc., Dow, Ethox Chemicals LLC., Solvay S.A., The Lubrizol Corporation, Elementis plc, Kao Corporation, Palsgaard, and American Element.

COVID-19 Impact

The recent covid-19 pandemic has disrupted the world and has brought a state of shock to the global economy. The global pandemic has impacted almost every industry. Also, the companies suffered a huge downfall in revenue due to a halt in production activities and regulations forbidding social gatherings. Furthermore, disruption in raw material supply, liquidity shortage, and labor shortage. These factors affected the market growth during the pandemic.

The global pigment dispersants market report is studied thoroughly with several aspects that would help stakeholders in making their decisions more curated.

On the basis of dispersion type, the market is categorized into water-based and solvent-based. Among these, the solvent-based category to hold a significant share of the market in 2020. This is mainly due to the wide range of applications, beneficial properties, and high consumption of these pigments. Moreover, these pigments are highly used in labels and packaging inks, in coatings for wood & metal, and in cosmetic nail lacquers which will boost their market growth during the forecast period.

Based on application, the pigment dispersants market has been classified into decorative paints & coatings, automotive paints & coatings, industrial paints & coatings, plastic, and others. The decorative paints & coatings category is to witness considerable growth during the forecast period. This is mainly due to their demand in the residential, commercial building construction, and automotive sectors.

Pigment Dispersants Market Geographical Segmentation Includes:

North America (United States, Canada, and Rest of North America)

Europe (Germany, United Kingdom, Spain, Italy, France, and the Rest of Europe)

Asia-Pacific (China, Japan, India, and the Rest of Asia-Pacific)

Rest of the World

This is mainly due to the rapidly growing middle-class population, which fuels the textile and plastic demand. The pigments and dyes market will majorly be concentrated in the Asia Pacific region, mainly due to lenient environmental laws, cheap labor costs, easy availability of low-cost raw materials, and higher market demands. Furthermore, the development of new products and the availability of market players in developing countries are also contributing to the growth of the market in the region. For instance, in 2021, AkzoNobel N.V. and Mercedes-Benz expand their partnership agreement for another 4 years. This means the company will continue to provide vehicle refinish products including automotive and specialty coatings and services in China and a preferred partner in Indonesia.

Request Free Sample Pages with Graphs and Figures Here https://univdatos.com/get-a-free-sample-form-php/?product_id=32458

The major players targeting the market include

Competitive Landscape

The degree of competition among prominent global companies has been elaborated by analyzing several leading key players operating worldwide. The specialist team of research analysts sheds light on various traits such as global market competition, market share, most recent industry advancements, innovative product launches, partnerships, mergers, or acquisitions by leading companies in the Pigment Dispersants Market. The major players have been analyzed by using research methodologies for getting insight views on global competition.

Key questions resolved through this analytical market research report include:

• What are the latest trends, new patterns, and technological advancements in the pigment dispersants market?

• Which factors are influencing the pigment dispersants market over the forecast period?

• What are the global challenges, threats, and risks in the pigment dispersants market?

• Which factors are propelling and restraining the pigment dispersants market?

• What are the demanding global regions of the pigment dispersants market?

• What will be the global market size in the upcoming years?

• What are the crucial market acquisition strategies and policies applied by global companies?

We understand the requirement of different businesses, regions, and countries, we offer customized reports as per your requirements of business nature and geography. Please let us know If you have any custom needs.

About UnivDatos Market Insights

UnivDatos Market Insights (UMI) is a passionate market research firm and a subsidiary of Universal Data Solutions. We believe in delivering insights through Market Intelligence Reports, Customized Business Research, and Primary Research. Our research studies are spread across topics across the world, we cover markets in over 100 countries using smart research techniques and agile methodologies. We offer in-depth studies, detailed analysis, and customized reports that help shape winning business strategies for our clients.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

0 notes

Text

0 notes

Text

The global Urea Market size is expected to be worth around USD 99.3 billion by 2033, from USD 72.5 billion in 2023, growing at a CAGR of 3.2% during the forecast period from 2023 to 2033.

The urea market encompasses the production, distribution, and use of urea, a nitrogen-rich compound widely used as a fertilizer in agriculture due to its high nitrogen content, which is essential for plant growth. Urea is also used in various industrial applications, including the production of resins, adhesives, and pharmaceuticals. The market is driven by the increasing demand for food production, which necessitates efficient fertilizers, and the expanding industrial applications of urea. Additionally, advancements in urea production technologies and the development of more sustainable agricultural practices influence market dynamics. The Asia-Pacific region is the largest consumer of urea, primarily due to its extensive agricultural activities.

Market Key Players:

Yara International ASA

SABIC

Qatar Fertiliser Company

OCI NV

CF Industries Holdings, Inc.

EuroChem Group AG

Nutrien AG

Koch Fertilizer, LLC

Coromandel International Limited

Acron Group

Chambal Fertilisers and Chemicals Ltd

Uralchem Group

Others

Click here for request a sample : https://market.us/report/urea-market/request-sample/

By Purity:

In 2023, urea with above 95% purity dominated the market, capturing over a 42.2% share. This high-purity urea is preferred in agriculture for its efficiency and effectiveness in enhancing crop growth and yield, while also minimizing impurities that can harm crops and soil. Urea with 90-95% purity is widely used in industrial applications, such as resins and adhesives, due to its balance of cost and performance. Urea below 90% purity is used in specific industrial processes and lower-grade fertilizers where high purity is not crucial.

By Grade:

In 2023, fertilizer-grade urea held the largest market share at 48.6%, driven by its crucial role in agriculture for promoting plant growth and increasing crop yields. This grade dissolves easily, making it efficient for farming applications. Technical-grade urea, important for industrial uses, is utilized in manufacturing plastics, adhesives, and chemicals, where high purity and specific chemical properties are required. Feed-grade urea is used as a non-protein nitrogen supplement in animal feed, aiding in the cost-effective nourishment of livestock.

By Application:

In 2023, agriculture dominated the urea market, accounting for 68.2% of the share, underscoring its role as a vital nitrogen fertilizer for enhancing crop productivity. Urea's high nitrogen content and cost-effectiveness make it a preferred choice for farmers. The chemical synthesis segment, though smaller, is essential for producing plastics, resins, and adhesives, particularly urea-formaldehyde used in composite wood products. Urea is also used in animal feed to increase the protein content for ruminants, supporting livestock nutrition economically.

By End-Use:

In 2023, the fertilizer segment captured 65.5% of the urea market, emphasizing its importance in agriculture for improving crop yields and soil health. Urea is popular for its cost-effectiveness and ease of application. The urea-formaldehyde resin segment, while smaller, is critical in producing composite wood products, adhesives, and coatings, driven by demand in construction and furniture industries for its strength and water resistance.

Key Market Segments:

By Purity

Below 90%

90-95%

Above 95%

By Grade

Technical Grade

Fertilizer Grade

Feed Grade Urea

By Application

Agriculture

Chemical Synthesis

Animal Feed

Others

By End-Use

Fertilizer

Urea Formaldehyde Resin

Others

Drivers:

The urea market is driven by the rising global agricultural demand, fueled by the need to increase crop yields to feed a growing population projected to reach nearly 10 billion by 2050. Urea, as a high-nitrogen fertilizer, enhances crop growth and health, making it essential for meeting food production needs. Its high nitrogen content supports protein synthesis in plants, leading to better yields. Urea’s ease of application and cost-effectiveness further boost its widespread use, particularly in intensive farming practices aimed at maximizing arable land use. This demand is especially significant in developing countries where agriculture is crucial for the economy and food security.

Restraints:

The urea market faces restraints due to environmental concerns and regulatory restrictions related to nitrogen runoff and emissions. Unabsorbed nitrogen from urea can lead to water contamination and air pollution, prompting stricter regulations on fertilizer use. Governments and environmental organizations are imposing limits on nitrogen application rates, and promoting best management practices to minimize nitrogen losses. The push for organic farming, which excludes synthetic fertilizers like urea, and the development of alternative sustainable fertilizers, also challenge the market. Increasing public awareness and advocacy for environmental protection further pressure policymakers to enforce stricter controls on urea use.

Opportunity:

The development and expansion of enhanced-efficiency fertilizers (EEFs) present significant opportunities in the urea market. EEFs are designed to reduce nitrogen losses and improve nutrient uptake efficiency through technologies like urease and nitrification inhibitors. These advanced products address environmental concerns while boosting crop productivity. As regulatory pressures and sustainability goals grow, the demand for EEFs increases. Technological advancements in fertilizer production allow for more stable and effective formulations, expanding their applications. Companies investing in EEFs can capture substantial market share by offering solutions that meet both agricultural and environmental needs.

Trends:

The urea market is influenced by the growing adoption of precision agriculture, which optimizes fertilizer application using technologies like GPS, sensors, drones, and data analytics. Precision agriculture enhances urea efficiency by ensuring precise application, reducing waste, and maximizing crop productivity. Tools like variable rate technology adjust urea application based on real-time field data, improving effectiveness and minimizing environmental impact. Sensor technology and data analytics monitor soil health and plant needs, enabling targeted urea usage. As smart farming technologies become more widespread and affordable, the demand for judicious urea use aligned with sustainable practices is expected to rise.

0 notes

Text

5 Essential Tips for Picking the Perfect Perfume Bottle Material

Choosing the right material for your perfume bottle is more than a matter of aesthetics; it’s a crucial decision that impacts the longevity, safety, and appeal of your fragrance. With a variety of options available, each offering distinct benefits and drawbacks, making an informed choice can be challenging. In this blog, we’ll explore the pros and cons of various materials used for perfume bottles, helping you navigate your options with confidence.

1. Glass: The Classic Choice

Pros:

· Elegance and Clarity: Glass offers a timeless appeal with its transparency, allowing consumers to appreciate the color and texture of the perfume.

· Chemical Stability: It is non-reactive, ensuring that the perfume's composition remains unaltered over time.

· Reusability: Glass bottles can be cleaned and reused, contributing to eco-friendly practices.

Cons:

· Fragility: Despite its many virtues, glass is prone to breaking if not handled carefully.

· Weight: Glass bottles tend to be heavier, which can increase shipping costs and make the perfume less convenient to carry.

Ideal For: High-end fragrances where visual appeal and chemical stability are paramount.

2. Plastic: The Practical Alternative

Pros:

· Lightweight: Plastic bottles are significantly lighter than glass, making them ideal for travel and everyday use.

· Durability: Less prone to breakage, which reduces the risk of loss or damage.

· Cost-Effective: Generally more affordable to produce and purchase compared to glass.

Cons:

· Chemical Interaction: Some plastics may react with the perfume’s ingredients, potentially altering its scent.

· Aesthetic Limitations: Often perceived as less luxurious than glass, which can impact the overall brand perception.

Ideal For: Budget-friendly or travel-size perfumes where cost and convenience are priorities.

3. Metal: The Modern Marvel

Pros:

· Durability: Metal bottles are robust and resistant to breakage, offering superior protection for the perfume.

· Innovative Designs: Metals allow for unique and intricate designs, adding a contemporary touch to the packaging.

· Light-Shielding: Metals provide excellent protection against light, which can degrade the perfume’s quality.

Cons:

· Weight: Similar to glass, metal bottles can be heavy, affecting portability.

· Cost: High-quality metal packaging can be expensive to manufacture.

Ideal For: Premium perfumes where durability and a modern aesthetic are desired.

4. Ceramic: The Artisanal Option

Pros:

· Unique Aesthetics: Ceramic bottles offer a distinct, handcrafted appearance that can appeal to niche markets.

· Heat Resistance: Ceramics do not easily heat up, helping to maintain the perfume’s integrity.

Cons:

· Fragility: Like glass, ceramics can be brittle and prone to chipping or breaking.

· Weight: Typically heavier than plastic and sometimes comparable to glass, which can affect usability.

Ideal For: Limited edition or artisanal perfumes where exclusivity and artistry are emphasized.

5. Wood: The Eco-Friendly Choice

Pros:

· Sustainability: Wood is a renewable resource, making it an environmentally friendly option.

· Distinct Appearance: Offers a rustic, natural look that can differentiate the product in a crowded market.

Cons:

· Porosity: Wood can absorb the fragrance, potentially altering its scent and leading to wastage.

· Maintenance: Wooden bottles may require special care to maintain their appearance and functionality.

Ideal For: Eco-conscious brands and consumers looking for a natural and sustainable packaging solution.

Conclusion

Glass provides elegance and stability but can be fragile. Plastic offers practicality and affordability at the potential cost of chemical stability. Metal combines durability with modern aesthetics, albeit at a higher price point. Ceramic appeals with its artisanal charm but shares glass’s fragility. Wood stands out for its eco-friendliness and unique appearance but requires careful handling.

For expert guidance on selecting the best material for your perfume bottle, feel free to reach out to us at:

contact us at :

WhatsApp: +86 180 2861 9410

We’re here to help and look forward to connecting with you!

0 notes

Text

Global Synthetic Resin Adhesive Market Size,Growth Rate,Industry Opportunities 2024-2030

On 2024-7-5 Global Info Research released【Global Synthetic Resin Adhesive Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030】. This report includes an overview of the development of the Synthetic Resin Adhesive industry chain, the market status of Consumer Electronics (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), Household Appliances (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), and key enterprises in developed and developing market, and analysed the cutting-edge technology, patent, hot applications and market trends of Synthetic Resin Adhesive.

Synthetic resin adhesive, also commonly referred to as simply resin adhesive, is a type of adhesive (glue) that is formulated from synthetic polymers. These adhesives are engineered to provide strong and durable bonds between various materials such as wood, plastics, metals, and composites. The term "synthetic resin" refers to a wide range of polymer compounds that are manufactured artificially rather than being naturally occurring. These resins are typically derived from petrochemicals or other organic compounds and are synthesized through chemical reactions. Synthetic resin adhesives come in various forms, including liquid, paste, or solid, and they can be applied through different methods such as spreading, spraying, or dipping. They are widely used in industries such as woodworking, construction, automotive, aerospace, and electronics for bonding components, assemblies, and structures.

According to our (Global Info Research) latest study, the global Synthetic Resin Adhesive market size was valued at US$ 5946 million in 2023 and is forecast to a readjusted size of USD 7948 million by 2030 with a CAGR of 4.2% during review period.

Global key players of Synthetic Resin Adhesive include Henkel, 3M, DuPont, H.B. Fuller, Shanghai Kangda New Materials, etc. The top five players hold a share about 34%. Asia-Pacific is the largest market, and has a share about 45%, followed by Europe and North America with share 25% and 21%, separately. In terms of product type, Thermoplastic Resin Adhesive is the largest segment, occupied for a share of 65%. In terms of application, Building & Construction has a share about 31 percent.

This report is a detailed and comprehensive analysis for global Synthetic Resin Adhesive market. Both quantitative and qualitative analyses are presented by manufacturers, by region & country, by Type and by Application. As the market is constantly changing, this report explores the competition, supply and demand trends, as well as key factors that contribute to its changing demands across many markets. Company profiles and product examples of selected competitors, along with market share estimates of some of the selected leaders for the year 2024, are provided.

Market segment by Type: Thermoplastic Resin Adhesive、Thermosetting Resin Adhesive

Market segment by Application:Building & Construction、Automotive & Transportation、Electrical & Electronics、Others

Major players covered: Henkel、3M、DuPont、H.B. Fuller、Shanghai Kangda New Materials、Sika、Hexion、Lord Corporation、Bostik、Huntsman、Ashland、Mapei、ITW Performance Polymers、MasterBond、Adhesives Technology Corp、Jowat Adhesives、Permabond

Market segment by region, regional analysis covers: North America (United States, Canada and Mexico), Europe (Germany, France, United Kingdom, Russia, Italy, and Rest of Europe), Asia-Pacific (China, Japan, Korea, India, Southeast Asia, and Australia),South America (Brazil, Argentina, Colombia, and Rest of South America),Middle East & Africa (Saudi Arabia, UAE, Egypt, South Africa, and Rest of Middle East & Africa).

The content of the study subjects, includes a total of 15 chapters:

Chapter 1, to describe Synthetic Resin Adhesive product scope, market overview, market estimation caveats and base year.

Chapter 2, to profile the top manufacturers of Synthetic Resin Adhesive, with price, sales, revenue and global market share of Synthetic Resin Adhesive from 2019 to 2024.

Chapter 3, the Synthetic Resin Adhesive competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast.

Chapter 4, the Synthetic Resin Adhesive breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030.

Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030.

Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Synthetic Resin Adhesive market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030.

Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis.

Chapter 13, the key raw materials and key suppliers, and industry chain of Synthetic Resin Adhesive.

Chapter 14 and 15, to describe Synthetic Resin Adhesive sales channel, distributors, customers, research findings and conclusion.

Data Sources:

Via authorized organizations:customs statistics, industrial associations, relevant international societies, and academic publications etc.

Via trusted Internet sources.Such as industry news, publications on this industry, annual reports of public companies, Bloomberg Business, Wind Info, Hoovers, Factiva (Dow Jones & Company), Trading Economics, News Network, Statista, Federal Reserve Economic Data, BIS Statistics, ICIS, Companies House Documentsm, investor presentations, SEC filings of companies, etc.

Via interviews. Our interviewees includes manufacturers, related companies, industry experts, distributors, business (sales) staff, directors, CEO, marketing executives, executives from related industries/organizations, customers and raw material suppliers to obtain the latest information on the primary market;

Via data exchange. We have been consulting in this industry for 16 years and have collaborations with the players in this field. Thus, we get access to (part of) their unpublished data, by exchanging with them the data we have.

From our partners.We have information agencies as partners and they are located worldwide, thus we get (or purchase) the latest data from them.

Via our long-term tracking and gathering of data from this industry.We have a database that contains history data regarding the market.

Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provides market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

#wood plastic composite#wood plastic composites market#WPC market#WPC decking market#WPC compounds demand

0 notes

Text

The global biocomposites market size was USD 24.4 billion in 2021 and is expected to reach USD 51.2 billion by 2026, projecting a CAGR of 16.0% between 2021 and 2026. Biocomposites are increasingly used in the transportation end-use industry as they decrease weight and increase fuel efficiency. Automotive manufacturers are increasingly using biocomposites in various automobile models. The regulatory legislation imposed by the EU and other countries, such as the US, India, and Japan; that are expected to increase the use of biocomposites, primarily in the automotive end-use industry. The EU legislation sets mandatory emission reduction targets for new cars to improve the fuel economy and reduce the CO2 emissions.

The US has also imposed stricter Corporate Average Fuel Economy (CAFE) and tailpipe emission standards for the automobile sector. The proposed mandate raised CAFÉ standards to 39 mpg for passenger cars by 2016 and 54.5 mpg by 2025. China and Japan have also announced vehicle fuel economy regulations. Brazil, India, Mexico, and South Africa are expected to initiate similar measures in the near future. The above-mentioned factors and increased incorporation of biocomposites are expected to increase their demand mainly in the automobile sector.

The automotive industry focuses on stringent regulations, such as the Corporate Average Fuel Efficiency (CAFE) standards and the European Emission Standards (EES) by the US and European governments, respectively, for vehicle manufacturers. According to the United States Environmental Protection Agency (EPA), the transportation industry in the US is one of the largest contributors to greenhouse gas emissions. The US government has, thus, made it a critical concern for automakers to follow the average miles per gallon standard for their vehicles. A similar situation is prevalent in other regions across the globe. In order to reduce carbon dioxide (CO2) emissions, automakers focus significantly on producing lightweight vehicles to comply with government regulations and enhance fuel efficiency.

#Biocomposites Market#bio composite#bio composites#biocomposite products#biocomposite plastic#biocomposites reinforced with natural fibers#bio composite material#biofibres and biocomposites#Biocomposites Industry#COVID 19 impact on Biocomposites Market#Asia Pacific Biocomposites Market#wood fiber composites#Global Biocomposites Market#Biocomposites Market share#Biocomposites Market Size#Biocomposites Market Demand#Biocomposites Market Growth#Biocomposites Market Opportunity#Sales of Biocomposites#Demand of Biocomposites#Europe Biocomposites Market#North America Biocomposites Market

0 notes

Text

Exploring Emerging Applications: Bioplastic Packaging Market Evolution

Bioplastic Packaging Market growth is driven by increasing demand for eco-friendly products

The Bioplastic Packaging Market offers sustainable packaging solutions that are biodegradable and compostable. Bioplastics are plastic polymers produced from renewable biomass sources such as vegetable fats and oils, corn starch, or microbiota and are comparable to conventional plastic in terms of performance and functionality. They can be used to manufacture items like grocery bags, food containers, bottles, clothing, diapers, packaging film, and much more in an environmentally-friendly way. Biodegradation enables the packaged products to completely break down without harming the environment at the end of their useful lifespan.

The Global Bioplastic Packaging Market is estimated to be valued at US$ 10.60 Bn in 2024 and is expected to exhibit a CAGR of 29% over the forecast period 2023 to 2030.

Growing awareness among consumers about the harmful effects of conventional plastics and the need for sustainability are driving the demand for greener alternatives in the packaging industry. Major food brands and retailers have been actively replacing fossil-fuel-based materials with bioplastics to meet sustainability goals and comply with regulations restricting single-use plastics.

Key Takeaways

Key players operating in the Bioplastic Packaging Market are BASF SE, Koninklijke DSM N.V., NatureWorks, LLC, Metabolix, Inc., and The Dow Chemical Company. These companies have been extensively investing in research and development to enhance bioplastic performance and reduce costs to drive wider adoption.

Growing consumer demand for environmentally-friendly alternatives to conventional plastics combined with government support through favorable policies is fueling the bioplastics market growth. Various international organizations have also been promoting biodegradability standards, which is encouraging new product development.

Asia Pacific region is anticipated to witness the fastest Bioplastic Packaging Market expansion during the forecast period. Countries like China, India, and Indonesia have been heavily pushing the use of renewable materials to tackle the massive plastic waste generation problem across cities. Manufacturers are increasingly setting up production plants in Asia in response to the strong market potential.

Market key trends

Sustainable fiber-based biopolymers are gaining popularity as a recyclable packaging material. They include products like paper, paperboard, and greaseproof paper made using wood pulp or non-food crops. Research is ongoing to develop agricultural residues and wood wastes into high-performance composites with barrier properties rivaling plastic. Improved fiber technology offers an eco-friendly solution with a lower carbon footprint compared to traditional plastics.

Porter's Analysis

Threat of new entrants: Thebioplastic packaging market has moderate threat due to high capital requirement and the presence of dominant players globally. However, opportunities in emerging markets to facilitate growth.

Bargaining power of buyers: Buyers have moderate power due to availability of substitutes and difficulty in differentiating products. Product quality and pricing determine their preference.

Bargaining power of suppliers: Suppliers have low to moderate power due to availability of alternatives and reliance on agricultural raw materials. Long-term relationships help balance their interests.

Threat of new substitutes: Threat is moderate as substitute materials replicate functionality but fall short on sustainability. Shift to renewable options gains momentum to curb use of finite resources.

Competitive rivalry: Intense competition exists among existing players to gain market share and expand globally. Innovation and portfolio expansion remain key strategies.

Geographical Regions

North America dominated the bioplastic packaging market, accounting for over 35% share in 2024 due to stringent regulations and supportive emission reduction policies. Government initiatives to foster adoption and investments by leading companies stimulate growth.

Asia Pacific projected to grow at the fastest pace during the forecast period due to rising industrial activities, population, and demand for packaged food in countries including China, India, Indonesia, and Japan. Rapid infrastructural development and industrialization offer opportunities for stakeholders.

0 notes

Last Seen Blogs

lxvechauncey

The Bass Blog

madamehydex

Madame Hyde

frutilinhas

ー ★!

sporadicbeauty

Grace

frozen-hearts-and-white-ski-blog

My Food Blog