#adhesive films market forecast

Text

Industrial Films Global Market 2024 - By Demand, Share, Size, Trends, Forecast To 2033

The industrial films market size is expected to see strong growth in the next few years. It will grow to $57.05 billion in 2028 at a compound annual growth rate (CAGR) of 6.0%. The growth in the forecast period can be attributed to continued industrialization, sustainable packaging, construction sector growth, agricultural applications expansion, rapid advancements in electronics. Major trends in the forecast period include functional coatings, optical films, heat-shrink films, uv-resistant films, multilayered films.

To access more details regarding this report, visit the link:

https://www.thebusinessresearchcompany.com/report/industrial-films-global-market-report

Segmentation & Regional Insights

The industrial films market covered in this report is segmented –

1) By Type: Linear Low Density Polyethylene (LLDPE) , Low-Density Polyethylene (LDPE) , High-Density Polyethylene (HDPE) , Polyethylene Terephthalate (PET) , Polypropylene (PP) , Polyvinyl Chloride (PVC) , Polyamide, Other Types

2) By Application: Coated Non-Woven Products, Dry Film Adhesives, Electronic and Battery, Barrier and Breathable, Puncture Resistant Coatings and Films

3) By End-Use Industry: Agriculture, Industrial Packaging, Construction, Medical, Transportation, Other End-Use Industries

Asia-Pacific was the largest region in the industrial films market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the industrial films market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Intrigued to explore the contents? Secure your hands-on sample copy of the report:

https://www.thebusinessresearchcompany.com/sample.aspx?id=8272&type=smp

Major Driver Impacting Market Growth

Increasing construction activities and projects in developing countries are expected to propel the growth of the industrial film market going forward. Construction activities refer to a business that is engaged in the design, development, and construction of buildings using construction materials. Industrial films are used to create unique lighting and appearance effects in the construction of buildings and commercial offices. For instance, October 2023, Upmetrics, a US-based AI-powered business plan software solutions company published an article according to which the construction industry of the USA is worth $1.8 trillion, while the global construction industry is valued at $8.9 trillion in 2023 and the global residential construction market is expected to grow to $8.3 trillion by 2032, with a 4.8% annual growth rate. Therefore, increasing construction activities and projects is driving the industrial films market.

Key Industry Players

Major companies operating in the industrial films market report are Mitsui Chemicals Inc., Toyobo Co. Ltd., Eastman Chemical Company, Compagnie de Saint-Gobain SA, DuPont de Nemours Inc., Berry Global Inc., SKC Co. Ltd., Toray Industries Inc., Mitsubishi Chemical Holdings Corporation, Solvay SA, FUJIFILM Holdings Corporation, Sigma Plastics Group, Muraplast d.o.o., Unitika Ltd., Jindal Films Europe Virton Sprl, Transcendia Inc., Mondi plc, Hi-Fi Industrial Film Ltd., Bogucki Folie Sp zoo, Inteplast Group Corporation, 3M Company, Avery Dennison Corporation, Bemis Company Inc., Covestro AG, Filmquest Group Inc., Uflex Ltd., Hyplast NV, Kuraray Co. Ltd., Novamont SpA, Plastipak Holdings Inc., Polifilm Group, Raven Industries Inc., Renolit Group, RKW Group, Saudi Basic Industries Corporation, Saint-Gobain SA, Sealed Air Corporation, SRF Limited, Technipaq Inc., Tredegar Corporation

The industrial films market report table of contents includes:

1. Executive Summary

2. Industrial Films Market Characteristics

3. Industrial Films Market Trends And Strategies

4. Industrial Films Market - Macro Economic Scenario

5. Global Industrial Films Market Size and Growth

....................

31. Global Industrial Films Market Competitive Benchmarking

32. Global Industrial Films Market Competitive Dashboard

33. Key Mergers And Acquisitions In The Industrial Films Market

34. Industrial Films Market Future Outlook and Potential Analysis

35. Appendix

Explore the trending research reports from TBRC:

https://goodprnews.com/electric-control-panel-global-market-size/

https://goodprnews.com/enterprise-performance-management-global-market-size/

https://goodprnews.com/fillings-and-toppings-global-market-size/

https://topprnews.com/electric-control-panel-global-market-share/

https://topprnews.com/enterprise-performance-management-global-market-share/

https://topprnews.com/fillings-and-toppings-global-market-share/

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

India Carbon Black Market Size, Growth Report 2031

Indian Carbon Black Market size was valued at USD 1.75 billion in FY2023 which is expected to reach USD 3.33 billion in FY2031 with a CAGR of 8.36% for the forecast period between FY2024 and FY2031. Recent years have seen a significant increase in the carbon black market in India due to factors like growing industrialization, improved infrastructure, and rising consumer demand for carbon black. Because it is widely used in tire manufacturing to improve performance and durability, the automotive industry is a significant consumer of carbon black. Given that India is one of the biggest markets for automobiles in the world, demand for carbon black is anticipated to rise further.

Further, the demand for carbon black is also influenced by the construction industry, which is fuelled by urbanization and government infrastructure projects. It is used to increase the strength, UV resistance, and other desirable properties of materials like asphalt, concrete, coatings, and adhesives. The demand for carbon black is also further driven by the packaging sector, as it is used in plastic packaging due to its durability and aesthetic appeal.

Additionally, manufacturers have the chance to reach markets outside of their home countries owing to the export potential of Indian carbon black products. Indian carbon black producers are working hard to meet global quality standards and take advantage of the expanding carbon black market in surrounding nations and regions.

Download Free Sample Report@ https://www.marketsandata.com/industry-reports/india-carbon-black-market/sample-request

A boom in Packaging Sector

The demand for packaging materials has increased due to the rapid expansion of e-commerce to guarantee the safe and secure delivery of goods to consumers. Plastic packaging products like bags, containers, and films are typically made using carbon black. These packaging materials can now be used for a variety of products and are guaranteed to remain intact during storage and transportation as carbon black is known for its strength, durability, and UV resistance.

One of India's fastest-growing industries is packaging, which currently has an annual growth rate of 25%. Carbon black is widely used in the packaging sector to achieve the desired colors and aesthetics in product packaging. It is a popular option in the industry because of its capacity to deliver a deep black color and consistent dispersion. The demand for packaged goods and carbon black in the packaging industry both rise along with the expansion of e-commerce.

Growing Automotive Sector

The high rate of urbanization, the average disposable income, and aggressive government initiatives to support domestic manufacturing and the use of electric vehicles in India are all factors driving the growth of the automotive industry. All these factors help to increase the production of vehicles, and as more cars are being produced.

According to the data published by MARKLINES, Indian passenger vehicle sales increased by 12.9% in April 2023. The increase in sales continues throughout India's first quarter of 2023, supporting the country's expanding automotive market demand. The market for Carbon black in India is heavily influenced by the automotive industry. Tire manufacturing involves the extensive use of carbon black, which improves the rubber's performance and strength. The demand for carbon black to produce tires has significantly increased with the expansion of the automotive industry in India.

Strong Growth in Textile Sector

Carbon black is used in the textile industry to create fibres, fabrics, and textiles for a variety of uses. Carbon black is used as a colorant or pigment in textiles. To produce dark-coloured textiles or achieve black shades in textile products, carbon black offers a deep and intense black coloration. During the manufacturing process, carbon black is frequently added to synthetic fibres like polyester, nylon, and acrylic. These fibres’ color fastness, UV resistance, and durability are all enhanced by the addition of carbon black. It aids in minimizing fading or discoloration brought on by sunlight exposure or other environmental elements.

According to a press release by The Textile Magazine, Cotton dominates the Indian textile market with a share of 60% compared to 40% globally. However, the situation is rapidly shifting. Manufacturers and brands are turning toward alternative fibre options, primarily polyester. There are currently 30 businesses with annual revenues exceeding USD 200 million, and many of them are expanding by double digits. The shift from Cotton to fibre along with the increasing textile sector will likely drive up the Carbon Black market in India.

Huge Construction Hikes

The demand for carbon black in India is driven by projects for infrastructure development and rapid urbanization. Carbon black is needed in the building industry for uses such as flooring, adhesives, sealants, and roofing materials in residential, commercial, and industrial construction. Carbon black is widely used in the infrastructure and construction industries. It is used to make asphalt, which is widely used in the construction of roads. Increased carbon black strength, resilience, and UV resistance are advantageous for asphalt.

Additionally, the Indian central government committed nearly USD 10 trillion in direct infrastructure investment as part of the Budget 2023. The Outlay of Pradhan Mantri Awas Yojana-Urban (PMAY-U) has increased by 66%, also, the Urban Infrastructure Development fund is increasing its focus on Tier-2 and Tier-3 cities to build bigger and better infrastructure. All such construction developments abet the rise in Carbon Black market in India.

The carbon black market in India is strongly tied to the country's automotive industry, which heavily relies on carbon black as a reinforcing filler in tire manufacturing and other rubber products. As India's automotive sector continues to grow, so does the demand for carbon black. Additionally, industrial applications such as plastics, coatings, and printing inks contribute to the demand for carbon black in the country.

Factors influencing the dynamics of the Indian carbon black market include the pace of industrialization, regulatory policies on emissions and pollution control, global market trends, availability and cost of raw materials, and the competitive landscape with both domestic and international players.

Carbon black is extensively used as a reinforcing filler in tires and other rubber products, as well as in various other applications such as plastics, inks, and coatings. In India, the demand for carbon black is largely driven by the automotive industry due to the significant presence of automobile manufacturing units.

The market dynamics for carbon black in India are influenced by factors such as:

Automotive Industry: The growth of the automotive sector directly impacts the demand for carbon black, particularly in tire manufacturing. As India's automotive industry continues to expand, so does the demand for carbon black.

Industrialization: Carbon black is also used in various industrial applications such as plastics, coatings, and printing inks. The pace of industrialization in India plays a crucial role in determining the demand for carbon black.

Regulatory Environment: Environmental regulations regarding emissions and pollution control can impact the production and usage of carbon black. Compliance with environmental standards can influence the manufacturing processes and costs associated with carbon black production.

Global Market Trends: Global trends in the carbon black market, such as supply-demand dynamics, pricing trends, and technological advancements, also have an impact on the Indian market.

Raw Material Availability: The availability and cost of raw materials, such as feedstock like coal tar and petroleum derivatives, influence the production cost of carbon black in India.

Competitive Landscape: The presence of key players in the carbon black market, both domestic and international, affects market dynamics, including pricing, product innovation, and distribution channels.

Impact of COVID-19

The global supply chains were disrupted by the pandemic, which also affected the availability of the chemicals and raw materials needed to produce carbon black in the Indian market. Transportation restrictions, logistics issues, and a temporary shutdown of manufacturing facilities impacted the ability of carbon black producers to produce their products. The pandemic's associated travel restrictions, lockdown measures, and economic unpredictability reduced India's overall demand for carbon black. Reduced activity in sectors namely automotive, building, and manufacturing led to a decline in the demand for products containing carbon black in the Indian market. For Instance, Maruti Suzuki reported a 47.4% decline in sales during March 2020.

The Indian carbon black market has shown resiliency and has begun to recover despite the initial difficulties as economic activity gradually picked up. A gradual increase in demand for carbon black has been observed across several industries, including the automotive and construction sectors, because of the relaxation of lockdown regulations and the implementation of government stimulus packages.

Indian Carbon Black Market: Report Scope

Indian Carbon Black Market Assessment, Opportunities and Forecast, FY2017-FY2031”, is a comprehensive report by Markets and Data, providing in-depth analysis and qualitative and quantitative assessment of the current state of the carbon black market in India, industry dynamics and challenges. The report includes market size, segmental shares, growth trends, COVID-19 and Russia-Ukraine war impact, opportunities and forecast between FY2024 and FY2031. Additionally, the report profiles the leading players in the industry mentioning their respective market share, business model, competitive intelligence, etc.

Contact

Mr. Vivek Gupta

5741 Cleveland street,

Suite 120,

VA beach, VA,

USA 23462

Tel: +1 (757) 343-3258

Email: [email protected]

Website: https://www.marketsandata.com/

#Indian Carbon Black Market Size#Indian Carbon Black Market Share#Indian Carbon Black Market Industry#Indian Carbon Black Market Analysis#Indian Carbon Black Market Price#Indian Carbon Black Market Trends#Indian Carbon Black Market Growth#Indian Carbon Black Market Forecast#Indian Carbon Black Market Report#Indian Carbon Black Market Outlook#Indian Carbon Black Market Opportunity

0 notes

Text

Copper Foil Market - From Supply Chain Resilience to Technological Advancements

The global copper foil market size is anticipated to reach USD 22.00 billion by 2030 and is anticipated to expand at a CAGR of 11.9% during the forecast period, according to a new report by Grand View Research, Inc. Increasing adoption of renewable energy sources and electric vehicles (EVs), as a part of decarbonization efforts, is projected to fuel the growth of global market for copper foil. Copper foil functions as the electrical conductor of printed circuit board (PCB). Rising demand for PCBs, due to the aforementioned application of copper foil in them, is likely to play a crucial role in influencing demand for copper foil. PCBs are essential building blocks in electronics manufacturing. As electronic devices become more complex and intelligent, there is an ever-growing demand for PCBs. As a result, rising demand for smart devices is likely to propel growth of the industry.

Copper Foil Market Report Highlights

Based on product, rolled foil held a maximum revenue share of over 55.0% in 2023 and is expected to grow at a significant CAGR over the forecast period due to its high consumption in batteries, solar panels, and IoT-enabled services, among others

Based on application, batteries segment is expected to grow at a lucrative pace over the forecast period owing to the growing EV industry

In solar & alternative energy, tin-plated copper foils in combination with acrylic-based pressure-sensitive adhesive tapes, are used in thin-film solar applications. These are solderable, and their usage provides stable electrical performance and is also easy to work with during the solar panel production process

Asia Pacific dominated the market owing to several countries in region focusing on reducing their carbon emissions by shifting their attention toward the adoption of renewable energy. For instance, according to the International Trade Administration, Taiwan plans to cater to 20% of its energy requirements from renewable sources by 2025. It is expected to harness 20 GW of solar energy by 2025

In January 2024, Hungary-based Volta Energy Solutions announced its geographic expansion into North American market by building a new battery copper foils plant in Quebec, Canada to cater to a fast-growing EV segment. It is a developer of world's first electrodeposited copper foils for batteries

For More Details or Sample Copy please visit link @: Copper Foil Market Report

Use of copper results in reduced carbon emissions and cuts down amount of energy required to generate electricity. There is six times more copper in renewable energy systems than in traditional systems. Hence, growing adoption and transition towards green energy in infrastructure development, such as electric vehicles (EVs) and electricity generation is anticipated to benefit market growth. According to the IEA, the global sales of EVs reached 10.3 million units in 2022 compared to 6.7 million units in 2021 and 3.2 million units in 2020. Global sales are expected to have touched 14.1 million units in 2023; however, actual statistics are yet to be published.

Copper is a commodity that has historically witnessed high price volatility during the historic period of 2018-2022. Fluctuations in prices of copper cathode are expected to have a bearing on the profitability of the producer. Further, hikes in energy prices, supply constraints, and high demand from end-use industries are expected to put pricing pressure on the global market and affect smelter profitability and revenue performances of foil producers over the forecast period. Hence, price volatility of copper is expected to be a significant restraint to the revenue performance of the market.

The market is very competitive, with a strong presence of several large-sized players, such as Nippon Denkai, Ltd., SKC, and Lotte Energy Materials Corporation. Due to growth of end-use applications, players have been investing in increasing their capacities through greenfield projects. For instance, in August 2023, Lotte Energy Materials Corporation announced that it would build a new foil plant in Spain and would be operational in 2025.

#CopperFoilMarket#Electronics#ConductiveMaterials#Manufacturing#Technology#RenewableEnergy#ElectricVehicles#Semiconductors#SupplyChain#Sustainability

0 notes

Text

Roll to Roll Vacuum Coating System, Global Market Size Forecast, Top 13 Players Market Share

Roll to Roll Vacuum Coating System Market Summary

Roll-to-roll vacuum coating systems are designed to deposit films or coatings onto substrates such as plastics or metal foils in a continuous roll-to-roll process. The system typically consists of several key components, including:

Unwind system: This allows a roll of substrate material to be continuously fed into the coating process. Cleaning and Pretreatment Unit: This unit prepares the substrate surface by removing all contaminants and applying a pretreatment process to enhance coating adhesion. Coating chamber: This is the main part of the system where the actual vacuum coating process takes place. It houses one or more coating sources, such as electron beam evaporation, sputtering, or thermal evaporation, which evaporate or ionize the coating material and deposit it onto the moving substrate. Vacuum system: maintains the required vacuum conditions in the coating chamber. It includes a vacuum pump, pressure control system and gas inlet/outlet mechanism. Cooling System: Since the coating process generates heat, a cooling system is required to regulate the temperature and prevent any damage to the substrate or coating material. Winding system: After the coated substrate passes through the coating chamber, it is wound onto a reel to achieve continuous production.

Roll-to-roll vacuum coating systems have the advantages of high production throughput, uniform coating deposition, and the ability to coat large areas of flexible materials. They are widely used in applications such as thin-film solar cells, flexible electronics, barrier coatings for packaging materials, and anti-reflective coatings for displays.

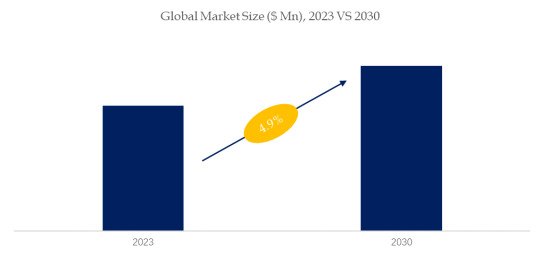

According to the new market research report "Global Roll to Roll Vacuum Coating System Market Report 2024-2030", published by QYResearch, the global Roll to Roll Vacuum Coating System market size is expected to reach USD 1444 million by 2030, at a CAGR of 4.9% during the forecast period.

Figure. Global Roll to Roll Vacuum Coating System Market Size (US$ Million), 2023-2030

Above data is based on report from QYResearch: Global Roll to Roll Vacuum Coating System Market Report 2024-2030 (published in 2023). If you need the latest data, plaese contact QYResearch.

Market Drivers:

The demand for high-quality thin film coatings in electronic products, solar cells, flexible displays and other fields continues to grow, driving the development of the roll-to-roll vacuum coating market. Roll-to-roll vacuum coating systems have important applications in sustainable energy industries such as solar cells. With the continuous development of the renewable energy market, this will further promote the demand for roll-to-roll vacuum coating systems.

Restraint:

Achieving high-quality, consistent and efficient thin film coatings requires solving many technical challenges such as coating uniformity, material loss and processing speed. Solving these problems may require further R&D and innovation, and manufacturers will need to invest significant R&D costs to develop high-quality equipment to meet market demand.

Opportunity:

Roll-to-roll vacuum coating systems are widely used in fields such as electronic products, solar cells, and flexible displays. With the emergence of emerging applications, such as flexible electronic technology and new smart devices, this will provide more development opportunities for the industry.

Figure. Global Roll to Roll Vacuum Coating System Top 13 Players

Above data is based on report from QYResearch: Global Roll to Roll Vacuum Coating System Market Report 2024-2030 (published in 2024). If you need the latest data, plaese contact QYResearch.

This report profiles key players of Roll to Roll Vacuum Coating System such as Applied Materials, Bühler, ULVAC, Hitachi, Intellivation, Mustang Vacuum Systems, FHR Anlagenbau, Angstrom Engineering, NAURA, Guangdong Huicheng, Ziwoo Co, SCREEN Finetech Solutions, Yasui Seiki.

In 2023, the global top three Roll to Roll Vacuum Coating System players account for 60% of market share in terms of revenue.

About The Authors

Tingyue Chen

Email: [email protected]

QYResearch Guangzhou Branch Analyst, as a member of the QYResearch Machinery Manufacturing Department, her main research directions are engineering machinery, electrical machinery, industrial robots and other fields. Some subdivided research topics include industrial heat treatment equipment, farm robots, X-ray fluoroscopy systems, etc. She is also engaged in the development of market segment reports and participates in the writing of customized projects.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

Thermoplastic Elastomers Market: Top 3 Industrial Applications

According to UNEP, energy accounts for approximately 60%of global greenhouse gas emissions, making energy efficiency a top priority across various industries. In this context, thermoplastic elastomers (TPEs) have emerged as a viable solution, reducing energy consumption by nearly 75%. They have gained recognition among product developers and designers as an advanced alternative to thermoset elastomers. Triton’s estimates suggest that the global thermoplastic elastomers market is expected to grow at a CAGR of 6.37% in revenue and 2.61% in volume during 2023-2030.

Another significant factor is the increasing trend of 3D printing. Due to their durable, flexible, chemically resistant, and user-friendly properties, TPEs serve as filaments in additive manufacturing methods like selective laser sintering (SLS) and fused deposition modeling (FDM). For instance, renowned companies such as New Balance, Under Armour, and Nike have adopted thermoplastic polyurethane-based 3D printing for robust and flexible midsoles.

In this blog, we’ll explore the wide-ranging applications of TPEs and their significant presence in the top three industries.

· Automotive:

In terms of industrial vertical, automotive leads with $9325.51 million

These high-performance polymers have gained significant traction in the automotive industry. Polystyrene TPE, for example, is used in multiple auto parts like instrument panels, wheel covers, dashboard elements, pillar trims, door liners, seat belt components, etc. These plastics, unlike metals, are cost-effective and improve vehicle energy efficiency by reducing weight.

Moreover, their lightweight quality boosts vehicle fuel efficiency, with a 10% weight reduction translating to 5-7% lower fuel consumption. This has prompted TPE manufacturers like Covestro AG to introduce new production lines for high-performance thermoplastic polyurethanes to produce paint production films.

Regional Focus: Asia-Pacific set to be the fastest-growing region at 6.46%

Asia-Pacific is the world’s largest automotive producer, with China, India, Japan, and Indonesia leading the way. Nations like India and Indonesia are attracting investments in locomotive and high-speed rail manufacturing, further bolstering the demand for TPE in the region. Additionally, China is actively boosting production, aiming for 7 million annually by 2025, constituting 20% of total new car production. This surge in EV production is set to drive demand for polyurethane and polystyrene in automotive applications, driving the Asia-Pacific thermoplastic elastomers market.

· Electrical & Electronics:

Thermoplastic elastomers are preferred for electrical insulation due to their strength, flexibility, and resistance to corrosive substances like acids. Besides this, TPE composites, including polycarbonate, enhance impact and flame resistance in electronic devices and household appliances. Given these benefits, several companies have entered into partnerships or acquisitions to expand their footing. For example,

- Arkema SA acquired Polytec PT in May 2023 to expand offerings and serve the electronics sector.

- Avient Corporation collaborated with BASF SE to offer colored grades of Ultrason® high-performance polymers to provide users in the electrical & electronics sector with comprehensive technical support.

Widely Employed Material Type:

Thermoplastic polyolefin serves multiple purposes in the sector, finding use in low-voltage wire and extruded hoses. TPOs are preferred over TPVs in wire and cable applications due to their cost-effectiveness, excellent electrical properties, and temperature versatility. As per Triton’s report, polyolefin is expected to register a CAGR of 6.30% during the forecast period 2023-2030 in terms of material type.

· Adhesives & Sealants:

Thermoplastic elastomers have gained popularity in providing strong bonds and flexibility without mixing or high-temperature curing. Since TPE adhesive grades offer durability, electrical insulation, and chemical and water resistance, companies strive to expand footing in the adhesives sector. Arkema SA, for instance, acquired Ashland’s performance adhesive branch in February 2022 to strengthen its adhesives solutions segment.

Regional Analysis: Asia-Pacific dominates the market based on volume

In Asia-Pacific, China dominates paint and coating production, while India is experiencing robust growth due to rapid industrialization and construction activities. Besides this, thermoplastic elastomer manufacturers are expanding in ASEAN countries like Thailand. Hence, the region’s expanding position in adhesive and sealant production fuels the region’s market, spearheaded by China.

Regulations & Shortages Prompt Innovation

Due to increasingly stringent environmental regulations and sustainability goals, elastomer manufacturers are compelled to create more recyclable tire options. This has led to a noticeable shift towards sustainable TPE materials, including bio-based TPEs. Shortages in raw materials further exacerbate the need for recyclable products. Notably, China has witnessed a significant increase in recycled rubber production, capturing more than 80% of the global production landscape.

In summary, the growing demand for eco-friendly solutions, regulatory pressures, and raw material shortages have spurred the adoption of TPEs as an effective means to reduce costs associated with waste tire management. Looking ahead, the industrial commitment to resource efficiency is expected to create lucrative opportunities within the thermoplastic elastomers market.

FAQs:

Q1) How big is the thermoplastic elastomers market in terms of volume?

Based on volume, the thermoplastic elastomers market recorded 7298.81 kilotons in 2022, expected to advance with a CAGR of 2.61% during 2023-2030.

Q2) Which are the 5 key thermoplastic elastomers?

Five key TPEs are polystyrene, polyamide, polyolefin, polyurethane, and elastomeric alloy.

#ThermoplasticElastomersMarket#ThermoplasticElastomers#Thermoplastic#tritonmarketresearch#marketresearchreports

0 notes

Text

Aircraft Interior Films Market Size, Growth Status, Analysis and Forecast 2030

The Insight Partners is excited to announce the release of groundbreaking findings in its latest market research report, "Overview of Aircraft Interior Films Market Share, Size, and Forecast | 2030". The panoramic research, conducted by our team of seasoned experts, provides valuable insights on the Aircraft Interior Films market forecast, key trends, drivers, challenges, and opportunities within the Aircraft Interior Films market.

The report unveils a detailed Aircraft Interior Films market analysis of the current Aircraft Interior Films market size and projects future growth trends based on historical data and market dynamics. At our research firm, we aim to help investors by providing both qualitative and quantitative data through this study. This global Aircraft Interior Films market report, competitive landscape, risks and barriers to entry for market players, sales channels, distributors, and Porter's Five Forces Analysis.

Businesses must have a firm understanding of the market, before making significant investments. It makes financial sense to allocate a modest portion of your company's expenditure to reliable market research. With a team of well-versed experts, we deliver actionable insights and strategic intelligence to help businesses navigate the complexities of the market landscape. Our commitment to excellence and innovation sets us apart as a trusted partner for organizations seeking a competitive edge.

Why Opt for Our Aircraft Interior Films Market Research Report?

Our researchers employ a multi-faceted approach to data collection, utilizing primary and secondary sources to ensure the breadth and depth of information.

Our researchers analyze consumer behavior, market trends, and brand positioning methods. Every piece of data undergoes a rigorous validation process to ensure accuracy and reliability.

We prioritize clarity and conciseness in our reporting, presenting findings in a format that is easily digestible for our clients.

We develop customized analytical models tailored to the specific nuances of the Aircraft Interior Films market, allowing us to uncover hidden patterns and trends.

The report answers the following questions:

What are the primary factors driving the Aircraft Interior Films market growth during the projected period?

What region is likely to witness the most substantial growth?

Which Aircraft Interior Films market trend will take center stage in the coming years?

What are the key challenges hindering the Aircraft Interior Films market expansion?

Emerging Trends: Our report uncovers emerging trends that are poised to reshape the Aircraft Interior Films market equipping businesses with the foresight to stay ahead of the competition.

Competitive Landscape: The Insight Partners explores the competitive landscape, offering insights into key Aircraft Interior Films market players, their strategies, and potential areas for differentiation. The key companies in the Aircraft Interior Films market are 1. 3M, 2. COMAC, 3. Cytec Solvay S.A., 4. DUNMORE Corporation, 5. E. I. du Pont de Nemours and Company, 6. Henkel AG and Co. KGaA, 7. Irkut, 8. ISOVOLTA AG, 9. Schneller LLC, 10. The Boeing Company .

Consumer Insights: Understanding consumer behavior is pivotal. The report includes a comprehensive analysis of consumer trends, preferences, and purchasing patterns.

Market Segmentation- The report breaks down the Aircraft Interior Films market into key segments, providing a detailed examination of each segment's market size, Aircraft Interior Films market growth potential, and strategic considerations.On the Basis of Aircraft Type this market is categorized further into-

Commercial Aircraft

Regional Aircraft

General Aviation

On the Basis of Film Type this market is categorized further into-

Film Adhesives

Decorative Films

Others

On the Basis of Material Type this market is categorized further into-

Epoxy

PVF

Polyimides

Others

On the Basis of Geography this market is categorized further into-

North America

Europe

Asia Pacific

and South and Central America

Key regions Aircraft Interior Films Market Research Report:

North America (U.S., Canada, Mexico)

Europe (U.K., France, Germany, Spain, Italy, Central & Eastern Europe, CIS)

Asia Pacific (China, Japan, South Korea, ASEAN, India, Rest of Asia Pacific)

Latin America (Brazil, Rest of Latin America)

The Middle East and Africa (Turkey, GCC, Rest of the Middle East and Africa)

Rest of the World

About Us:

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

0 notes

Text

Carbon Heating Film Market | Forecast Report | 2024 to 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Carbon Heating Film Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2031.” The study provides a detailed analysis of the industry, including the global Carbon Heating Film Market Size share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Carbon Heating Film Market?

The global carbon heating film market is anticipated to exhibit a compound annual growth rate (CAGR) of 6.4% from 2023 to 2031."

What are Carbon Heating Film?

Carbon heating film is a thin and flexible heating element comprised of carbon fibers embedded within a polymer film substrate, primarily utilized in underfloor heating systems and other scenarios necessitating efficient radiant heat dispersion. Positioned beneath flooring surfaces or within walls, it generates warmth by passing an electric current through the carbon fibers, emitting infrared radiation to uniformly heat the surroundings. Compared to conventional heating methods, carbon heating film offers advantages such as rapid warming, energy efficiency, and unobtrusive installation, minimizing disruption to existing structures. Its adaptability and straightforward installation procedures make it a favored option for residential and commercial heating needs, ensuring comfortable warmth while optimizing energy consumption and preserving design aesthetics.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1928

What are the growth prospects and trends in the Carbon Heating Film industry?

The carbon heating market growth is driven by various factors. The Carbon Heating Film market comprises a variety of flexible heating elements incorporating carbon fibers within a polymer film substrate, primarily utilized in underfloor heating systems and similar contexts. This market is witnessing significant expansion fueled by growing demand for energy-efficient heating alternatives, offering a range of products tailored to residential, commercial, and industrial applications. Leading players in this market deliver advanced solutions characterized by rapid warm-up, energy efficiency, and straightforward installation, meeting the evolving requirements of consumers seeking comfortable and economical heating options. Furthermore, ongoing technological advancements and strict energy efficiency mandates are propelling innovation within the market, ensuring its continued growth and widespread adoption globally. Hence, all these factors contribute to carbon heating market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Product Type:

Self-Adhesive Carbon Heating Film

Carbon Heating Film with Mesh

Others

By Application:

Residential

Commercial

Industrial

By End-Use:

New Construction

Retrofit & Renovation

By Distribution Channel:

Online

Offline

By Region:

North America:

United States

Canada

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Warmup PLC

Nexans S.A.

ThermoSoft International Corporation

Flexel International Ltd.

Klima Group

Rayotec Ltd.

Thermofilm Australia Pty Ltd.

Warmtech Pty Ltd.

Floor Heating Ltd.

View Full Report: https://www.reportsandinsights.com/report/Carbon Heating Film-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

Impact of COVID-19 on the Polyurethane Prepolymer Market: Strategies for Resilience

Polyurethane Prepolymers: An Essential Raw Material for Manufacturing Industries

What are Polyurethane Prepolymers?

Polyurethane prepolymers, also known as isocyanate terminated prepolymers, are polyols that have been reacted with diisocyanates but terminated with residual isocyanate groups. They are highly viscous resins synthesized by reacting a polyol such as polyether polyol or polyester polyol with a diisocyanate like MDI or TDI in a 1:1 or 1:2 stoichiometric ratio resulting in an isocyanate functional prepolymer.

Applications of Polyurethane Prepolymers

Polyurethane prepolymers find wide applications due to their versatile chemical and physical properties. Some key applications include:

Coatings - Prepolymers are used as binders, crosslinkers and intermediates in manufacturing coatings for wood, concrete, leather and various industrial applications. Their excellent adhesion, chemical resistance and flexibility makes them ideal for coatings.

Adhesives and Sealants - The film forming and adhesive properties of prepolymers are leveraged to produce structural and high-performance adhesives as well as sealants for construction and automotive applications.

Elastomers - Prepolymers impart flexibility, elasticity and high strength to elastomers used in hoses, gaskets, rollers and various flexible molded articles. They aid in processability and enhance mechanical properties.

Footwear - The mechanical strength and flexibility imparted by prepolymers in polyurethane enables their use in manufacturing shoe soles, heels and sport shoe midsoles providing comfort and durability.

Types of Polyurethane Prepolymers

Based on the polyol/diisocyanate ratio and reactants used, prepolymers can be categorized as:

- MDI based: Formed from reaction of MDI with polyester polyols or polyether polyols. Offer high strength, hardness and chemical resistance. Widely used.

- TDI based: React TDI with polyols. Provide flexibility and high elongation. Used in elastomers, sealants and adhesives.

- Polyester based: Have good hydrolytic stability and strength. Used in coatings.

Manufacturing Process of Polyurethane Prepolymers

The manufacturing process involves the following key steps:

1. Reaction of Polyol and Diisocyanate: Polyether polyol or polyester polyol is charged into the reactor and heated to the required temperature. Diisocyanate like MDI or TDI is added slowly with agitation.

2. Controlled Polyaddition Reaction: The exothermic polyaddition reaction between hydroxyl groups of polyol and isocyanate groups proceeds. Process parameters like temperature, catalysts are controlled.

3. Termination Reaction: Once the pre-set NCO index is reached, the prepolymer is terminated by residual isocyanate groups and deactivated by adding catalyst kill.

4. Filtration and Packaging: The viscous prepolymer solution is filtered to remove impurities and filled in drums, IBCs or bulk tankers.

Applications determine the suitable type of prepolymer and optimization of process parameters like reaction temperature, reaction time and NCO index yields prepolymers with desired physical and chemical qualities. Strict quality control during manufacturing is vital.

Outlook for Polyurethane Prepolymers Market

The global polyurethane prepolymers market is forecast to grow at over 5% CAGR through 2030 driven by increasing usage in coatings, adhesives, sealants, thermoplastic polyurethanes and various consumer and industrial applications. Rapid growth of key end use industries like footwear, construction, automotive, packaging and furniture will boost demand.

Moreover, continuous product innovation to develop new grades catering to changing industry and regulatory trends along with expansion into emerging markets in Asia Pacific and Middle East regions are factors expected to fuel the prepolymer market in the coming years. However, volatility in raw material prices remain a key challenge. Overall, polyurethane prepolymers market outlook looks positive owing to their excellent performance attributes and versatile usage profile.

#Polyurethane Prepolymer Market Growth#Polyurethane Prepolymer Market Trends#Polyurethane Prepolymer Market

0 notes

Text

Tubes and Cores Market| Market Size, Analysis and Forecast, 2024 – 2028

Originally published on Technavio: Tubes and Cores Market Analysis North America, Europe, APAC, South America, Middle East and Africa - US, Canada, China, Germany, Russia - Size and Forecast 2024-2028

**Tubes and Cores Market Forecast 2024-2028**

**Market Size Projection:**

The tubes and cores market is anticipated to witness substantial growth, with a projected increase of USD 3.96 billion at a Compound Annual Growth Rate (CAGR) of 7.8% from 2023 to 2028.

**Market Overview:**

An in-depth analysis, based on data from 2022, lays the foundation for understanding key drivers, emerging trends, and challenges in the market. This comprehensive assessment assists companies in refining their marketing strategies to gain a competitive edge.

**Key Market Drivers:**

The burgeoning global sporting goods retail sector emerges as a significant driver, propelled by the increasing demand for various sports equipment across the globe. Sports events and clubs further fuel this demand, with sports like cricket, golf, badminton, and tennis witnessing frequent tournaments. Consequently, the need for packaging such sporting goods in tubes and cores is expected to surge, thereby driving market growth.

**Key Market Trends:**

The integration of radio-frequency identification (RFID) tags into tubes and cores is identified as an emerging trend. Manufacturers are leveraging RFID technology to monitor and track the physical condition of tubes and cores throughout the supply chain, enhancing visibility and security. Moreover, RFID-enabled tubes and cores enable real-time status monitoring, positively impacting market growth.

**Major Market Challenge:**

The dynamic nature of the packaging industry poses a significant challenge, with constantly evolving trends such as 3D printing and smart packaging potentially overshadowing traditional tubes and cores. Manufacturers must stay abreast of emerging packaging technologies and adapt their offerings to meet evolving market demands, thereby mitigating the negative impact on market growth.

**Market Segmentation:**

**End-user Analysis:** The paper industry segment is poised for significant growth, driven by the utilization of tubes and cores in packaging and transportation of various paper products. Notably, toilet paper emerges as a major contributor within this segment, with technological advancements further enhancing the industry's efficiency and sustainability.

**Material Analysis:** The market is segmented into paper and plastic, with the paper segment anticipated to dominate. Paper tubes and cores serve as essential supports for packaging adhesive tapes and films, ensuring product integrity and facilitating dispensing across diverse industries.

**Region Analysis:** North America is projected to contribute significantly to global market growth, with factors such as manufacturing reshoring and the expansion of end-user industries driving demand for tubes and cores. Notably, Mexico's emergence as a manufacturing hub and the growth of industries like textiles further bolster market expansion in the region.

**Major Market Companies:**

Key players in the market, including Ace Paper Tube and other prominent entities, are employing strategic initiatives such as partnerships and product launches to enhance their market presence. A detailed competitive landscape analysis aids in understanding market dynamics and the strengths of key players.

**Market Customer Landscape:**

The market research report provides insights into the adoption cycle across various regions, emphasizing essential purchasing factors and price sensitivity. This aids companies in formulating effective growth strategies aligned with evolving consumer preferences.

**Segment Overview:**

The market report offers revenue forecasts at global, regional, and country levels, alongside a comprehensive analysis of market trends and growth opportunities across diverse end-user industries and materials.

**Market Analyst Overview:**

As an integral part of the flexible packaging industry, the tubes and cores market aligns with regulatory directives and focuses on sustainable packaging solutions. Laminated tubes find applications in cosmetics, reflecting the market's responsiveness to economic and environmental factors.

To Learn deeper into this report , View Sample PDF

**Conclusion:**

The tubes and cores market presents lucrative growth opportunities driven by factors such as the expanding global sporting goods retail sector and the integration of RFID technology. However, manufacturers must navigate challenges posed by evolving packaging trends to sustain growth and competitiveness in the market.

For more information please contact.

Technavio Research

Jesse Maida

Media & Marketing Executive

US: +1 844 364 1100

UK: +44 203 893 3200

Email: [email protected]

Website: www.technavio.com/

0 notes

Text

Flip Chip Technology : Worldwide Market Will Generated Large Revenue in Years to Come

According to HTF Market Intelligence, theGlobal Flip Chip Technology market to witness a CAGR of 6.5% during forecast period of 2024-2030. Global Flip Chip Technology Market Breakdown by Application (Automotive, Military/Aerospace, Computing, Life Sciences) by Device (Ball Grid Arrays, Conductive Adhesive, Film Adhesive, Anisotropic, Others) and by Geography (North America, South America, Europe, Asia Pacific, MEA). The Flip Chip Technology market size is estimated to increase by USD Billion at a CAGR of 6.5% from 2024 to 2030. The report includes historic market data from 2019 to 2023E. Currently, market value is pegged at USD 32.39 Billion.

Get Detailed TOC and Overview of Report @

Flip Chip Technology, also known as Controlled Collapse Chip Connection (C4), is an advanced semiconductor packaging technique where the semiconductor die is flipped upside down and mounted directly onto the substrate or another die. This allows for a more direct and efficient connection between the integrated circuit (IC) and the substrate, improving electrical performance and heat dissipation.

Some of the key players profiled in the study are Taiwan Semiconductor Manufacturing Company (Taiwan), Samsung Electronics (South Korea), United Microelectronics Corporation (Taiwan), Global Foundries (United States), Intel Corp. (United States), Flip chip international (United States), Amkor Technology (United States), Qualcomm Inc. (United States), Micron Techology Inc. (United States).

Book Latest Edition of Global Flip Chip Technology Market Study @ https://www.htfmarketintelligence.com/buy-now?format=1&report=2620

About Us:

HTF Market Intelligence is a leading market research company providing end-to-end syndicated and custom market reports, consulting services, and insightful information across the globe. HTF MI integrates History, Trends, and Forecasts to identify the highest value opportunities, cope with the most critical business challenges and transform the businesses. Analysts at HTF MI focuses on comprehending the unique needs of each client to deliver insights that are most suited to his particular requirements.

Contact Us:

Craig Francis (PR & Marketing Manager)

HTF Market Intelligence Consulting Private Limited

Phone: +1 4343220091

[email protected]

0 notes

Text

Global N-Butanol Market Size, Share, Trends, Opportunity, and Forecast

Global N-butanol market is anticipated to increase at an impressive rate through 2031. N-Butanol is an alcohol manufactured by processing petrochemical or fermentation of sugars obtained from corn and is also known as 1 butanol or butyl alcohol. It is a primary alcohol having a colorless liquid of standard volatility and fruit-like odor. Due to its characteristic, n-Butanol is used as a raw material for paint and coating resins, butyl carboxylates such as butyl acrylate, butyl acetate, and glycol ethers.

Growing demand for N-butanol from various end user industries such as paints & coatings, chemical and petrochemical, textile, agriculture, building & construction, pharmaceutical, and personal care for their application is expected to drive the growth of global N-butanol market. Apart from these, growing use of N-butanol as raw materials in different products like fuels, green buildings, and others further increase the demand for N-butanol, thereby driving the market growth. According to reports, butyl alcohol was the world’s 2563rd most traded product worldwide in 2020, which holds 0.003% of world trade. Furthermore, government policies over trade, such as free trade agreements, bilateral agreements, and regional group trade agreements, promote the import and export of raw materials that propel market growth. Thus, it is expected that the global n-Butanol market is going to rise in the projected year.

Growing Demand for Industrial Applications is Going to Propel the Market Growth

N-Butanol is primarily used as an industrial intermediary that is used to make different products like dyes, lacquers, resins, and varnishes. The broad melting and boiling points of N-butanol make it useful for the production of chemicals which are required to cool down entire machinery. Butyl alcohol is used to make rubber cement, safety glass, rayon, photographic film, motion picture, water resistance cloth, artificial leather, and raincoats. Moreover, it has wide application in agriculture for the production of herbicides and other essential agrochemicals. According to the report, the world trade of n-Butanol was amounted to around USD 550 million by value in 2020. In food industries, n-Butanol is used as a dehydrating agent in perfumes and fruit essences and as a flavoring agent in foods and beverages. Hence, owing to its broad application in every end-user industry, it is expected that demand for n-Butanol is going to increase in the projected period.

Market Segmentation

Global N-Butanol market is based on grade and application. Based on grade, the market is divided into industrial grade v/s pharmaceutical grade. Based on application, the market is divided into butyl acetate, butyl acrylate, glycol ethers, direct solvent, plasticizers, and others.

The global market for N-Butanol, a versatile industrial chemical with a wide range of applications, is experiencing significant growth and transformation. This blog post delves into the expansive landscape of the Global N-Butanol Market, exploring its size, the driving factors behind its expansion, key applications, and the promising future trends that shape this dynamic industry.

Market Overview:

The Global N-Butanol Market has emerged as a critical player in the chemical industry, witnessing steady growth driven by its diverse applications. N-Butanol, a four-carbon alcohol, finds utility in various sectors, including chemicals, coatings, pharmaceuticals, and automotive, contributing to its widespread demand.

Driving Factors:

a. Chemical Manufacturing and Solvent Applications:

N-Butanol serves as a crucial intermediate in the production of chemicals, including butyl acrylate, glycol ethers, and butyl acetate. Its properties as a solvent make it valuable in industries such as coatings, adhesives, and sealants, driving demand for N-Butanol globally.

b. Automotive and Paint Industries:

The automotive and paint industries heavily rely on N-Butanol for its use in the formulation of automotive coatings and paints. Its contribution to enhancing the durability, gloss, and performance of coatings has led to consistent demand from these sectors.

c. Pharmaceutical and Agrochemical Applications:

N-Butanol plays a vital role in pharmaceutical manufacturing, serving as a solvent in the production of various medications. Additionally, its application in the formulation of agrochemicals further expands its reach, contributing to the growth of the market.

Market Segmentation:

The Global N-Butanol Market is segmented based on its applications, including:

Chemical Intermediates: Production of butyl acrylate, butyl acetate, and glycol ethers.

Solvents: Widely used in coatings, adhesives, sealants, and inks.

Automotive Coatings: Enhancing the performance and durability of automotive paints.

Pharmaceuticals: Serving as a solvent in the production of medications.

Agrochemicals: Formulation of pesticides and herbicides.

Challenges and Opportunities:

The N-Butanol market faces challenges related to raw material prices, regulatory constraints, and environmental concerns. However, these challenges present opportunities for market players to innovate in sustainable production methods, explore bio-based alternatives, and navigate regulatory landscapes effectively.

Future Trends:

The future of the Global N-Butanol Market is poised for exciting developments, with trends including:

Bio-Based N-Butanol: Growing interest in bio-based alternatives to reduce environmental impact.

Focus on Sustainable Practices: Increasing emphasis on sustainable production methods.

R&D in Advanced Applications: Ongoing research and development for novel applications in emerging industries.

In conclusion, the Global N-Butanol Market stands as a cornerstone in the chemical industry, serving as a crucial component in various applications. As industries continue to evolve, the demand for N-Butanol is expected to grow, fueled by its versatility and contribution to key sectors such as chemicals, coatings, pharmaceuticals, and automotive. With innovation and sustainability at the forefront, the future of the N-Butanol market promises to be dynamic and transformative.

Download Free Sample Report

Market Players

Mitsubishi Chemical Corporation, Dow Chemical Company, BASF SE, OXEA GmbH, Sasol Ltd, KH Neochem Co Ltd, China National Petroleum Corporation (CNPC), INEOS Oxide Ltd, Perstorp Holding AB, and Saudi Kayan Petrochemical Company are the key players operating in the global N-butanol market.

Report Scope:

In this report, global N-butanol market has been segmented into following categories, in addition to the industry trends which have also been detailed below:

Global N-Butanol Market, By Grade:

Industrial Grade

Pharmaceutical Grade

Global N-Butanol Market, By Application:

Butyl Acetate

Butyl Acrylate

Glycol Ethers

Direct Solvent

Plasticizers

Others

Global N-Butanol Market, By region:

North America

United States

Mexico

Canada

Asia-Pacific

China

India

South Korea

Japan

Australia

Europe

France

Germany

United Kingdom

Italy

Spain

South America

Brazil

Argentina

Colombia

Middle East & Africa

Mob : +91 9319642100

Noida One Tower Sec 62 Noida 201301

Sales : [email protected]

Website : https://www.organicmarketresearch.com

0 notes

Text

Vinylidene Chloride Market Analysis: Prices, Index, Trend & Forecast by Procurement Resource

In the Asia Pacific region, sulphur dioxide prices were impacted by inadequate support from feedstock materials, with strong supply due to China's manufacturing resurgence. In the second quarter, while downstream industries improved, excess product availability maintained a bearish price trend.

Request for Real-Time Vinylidene Chloride Prices: https://www.procurementresource.com/resource-center/vinylidene-chloride-price-trends/pricerequest

In Europe, weak feedstock prices and oversupply in domestic markets led to a price decline in the first quarter, with stagnant end-user demand. The second quarter saw a similar trend, with reduced sulphur dioxide production and pessimism among traders due to persistent logistical challenges.

In North America, falling consumption, economic uncertainties, and weak performance in paper, textiles, and pulp sectors, compounded by feedstock issues, contributed to a declining price trend, accentuated by inflation and interest rate concerns in the second quarter.

Definition

Vinylidene chloride is a chemical compound with the molecular formula CH2=CCl2. It is a colorless, flammable gas at room temperature. This compound is highly reactive due to its unsaturated double bond, making it susceptible to polymerization. Vinylidene chloride is primarily used in the production of copolymers, particularly with vinyl chloride. The resulting copolymers have exceptional gas and moisture barrier properties, making them valuable in the packaging industry for food wraps and protective films for electronics. Vinylidene chloride is known for its resistance to chemical permeation and its role in coatings, adhesives, and fire-retardant materials, enhancing product stability and performance.

Key Details About the Vinylidene Chloride Price Trend:

Procurement Resource does an in-depth analysis of the price trend to bring forth the monthly, quarterly, half-yearly, and yearly information on vinylidene chloride price in its latest pricing dashboard. The detailed assessment deeply explores the facts about the product, price change over the weeks, months, and years, key players, industrial uses, and drivers propelling the market and price trends.

Each price record is linked to an easy-to-use graphing device dated back to 2014, which offers a series of functionalities; customization of price currencies and units and downloading of price information as Excel files that can be used offline.

The vinylidene chloride price forecast, including India Vinylidene chloride price, USA Vinylidene chloride price, pricing database, and analysis can prove valuable for procurement managers, directors, and decision-makers to build up their strongly backed-up strategic insights to attain progress and profitability in the business.

Industrial Uses Impacting the Vinylidene Chloride Price Trend:

Vinylidene chloride finds diverse industrial applications due to its unique properties. Its primary use lies in the production of copolymers, especially with vinyl chloride. These copolymers, such as Saran, exhibit exceptional gas and moisture barrier properties, making them invaluable in the packaging industry for food wraps and protective films for electronics.

Vinylidene chloride is also employed in the creation of coatings and adhesives, where its barrier properties and resistance to chemical permeation enhance product performance and stability. In addition, it is utilized in the manufacturing of fire-retardant materials, providing improved resistance to flames and heat. These properties make vinylidene chloride a valuable component in various industrial processes and applications.

Key Players:

Dow

Asahi Kasei

Solvay

Shandong XingLu Chemical

Juhua Group

Jiangsu Huatewei

Nantong Repair-air

About Us:

Procurement Resource offers in-depth research on product pricing and market insights for more than 500 chemicals, commodities, and utilities updated daily, weekly, monthly, and annually. It is a cost-effective, one-stop solution for all your market research requirements, irrespective of which part of the value chain you represent.

We have a team of highly experienced analysts who perform comprehensive research to deliver our clients the newest and most up-to-date market reports, cost models, price analysis, benchmarking, and category insights, which help in streamlining the procurement process for our clientele. Our team tracks the prices and production costs of a wide variety of goods and commodities, hence providing you with the latest and consistent data.

To get real-time facts and insights to help our customers, we work with a varied range of procurement teams across industries. At Procurement Resource, we support our clients with up-to-date and pioneering practices in the industry to understand procurement methods, supply chains, and industry trends so that they can build strategies to achieve maximum growth.

Contact Us:

Company Name: Procurement Resource

Contact Person: Chris Byrd

Email: [email protected]

Toll-Free Number: USA & Canada – Phone no: +1 307 363 1045 | UK – Phone no: +44 7537 132103 | Asia-Pacific (APAC) – Phone no: +91 1203185500

Address: 30 North Gould Street, Sheridan, WY 82801, USA

#VinylideneChlorideMarketAnalysis#VinylideneChlorideMarket#VinylideneChloride#VinylideneChloridePriceTrend#VinylideneChloridePriceForecast

1 note

·

View note

Text

Global film adhesives market is projected to witness a CAGR of 4.1% during the forecast period 2024-2031, growing from USD 1.01 billion in 2023 to USD 1.39 billion in 2031. Film adhesives are essential to many different industries, such as electronics, construction, transportation, and medical applications.

0 notes

Text

0 notes

Text

Exploring Innovations in the Physical Vapor Deposition Market: A Comprehensive Analysis

Physical vapor deposition (PVD) involves depositing thin film coatings onto various substrates through vacuum deposition techniques such as sputtering and evaporation. These PVD coatings have excellent adhesion, uniform thickness, and superior wear and corrosion resistance properties. They are used widely in microelectronics manufacturing to deposit metallic films and barrier coatings on semiconductor devices. The global Physical Vapor Deposition (PVD) Market is estimated to be valued at US$ 18.09 Bn in 2023 and is expected to exhibit a CAGR of 5.5% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Opportunity

The rapid adoption of smartphones, tablets, and other consumer electronic devices provides massive growth opportunities for PVD coatings in the microelectronics industry. A typical smartphone consists of hundreds of layers of PVD coatings to fabricate various semiconductor components as they help improve durability, conductivity and prevent oxidation and corrosion. The miniaturization trend in consumer electronics demands higher precision and deposition thickness uniformity offered by PVD technologies. Factors such as this widespread use of PVD coatings in advanced microdevices will drive the physical vapor deposition market growth over the coming years.

Porter's Analysis

Threat of new entrants: The physical vapor deposition market require high initial capital investment for manufacturing equipment and facilities which act as a barrier for new players.

Bargaining power of buyers: The presence of large number of vendors providing physical vapor deposition services and equipment globally reduce the bargaining power of individual buyers.

Bargaining power of suppliers: The availability of alternative material and equipment suppliers for physical vapor deposition puts less bargaining power on suppliers.

Threat of new substitutes: There are limited technology substitutes for physical vapor deposition process used for thin film coating, thin film materials deposition and materials modification.

Competitive rivalry: The physical vapor deposition market is fragmented with presence of number of global and regional players competing on basis of product innovation, design and manufacturing capabilities.

SWOT Analysis

Strength: Physical vapor deposition process provides uniform thin film coating and materials deposition on substrates of varied shapes and sizes. It offers improved corrosion and wear resistance with minimal material wastage.

Weakness: High initial investment requirements for setting up physical vapor deposition facilities. Stringent government regulations regarding material disposal and effluent treatment.

Opportunity: Growing demand from microelectronics, data storage, optics industries. Increasing R&D towards new PVD applications in photovoltaics, medical devices, and other nanotech industries.

Threats: Volatility in raw material prices can increase overall production cost. Economic slowdowns can impact capital investments of end-use industries.

Key Takeaways

The global physical vapor deposition market is expected to witness high growth driven by increasing demand from electronics and solar industries.

Regional Analysis: Asia Pacific dominates the global physical vapor deposition market with majority of production facilities located in China, Taiwan and South Korea. Regional demand is driven by presence of integrated device manufacturers and outsourced semiconductor and electronics assembly industries.

Key players operating in the physical vapor deposition market are Oerlikon Balzers (Oerlikon Group), IHI Corporation, Silfex Inc., Lam Research Corp, Singulus Technologies AG, Applied Materials, Inc., ULVAC Inc., Veeco Instruments Inc., Buhler AG, Semicore Equipment, Inc., and Platit AG. Oerlikon Balzers is one of the leading vendors providing PVD coating services to mechanical engineering and medical device industries. Lam Research is a prominent player for PVD systems used in semiconductor manufacturing.

#Physical Vapor Deposition Market Share#Physical Vapor Deposition Market Growth#Physical Vapor Deposition Market Demand#Physical Vapor Deposition Market Trend

0 notes

Text

The latest innovations for digitally printed sportswear production

Author: Debbie McKeegan

The latest technologies for sportswear manufacturing continue to drive innovation and disrupt traditional process in this expanding sector. The industry has undergone a transformative journey in 2023, with advancements in printing machinery, software, process and materials playing a pivotal role.

As a sector - The global sports clothing market is estimated to register a CAGR of 4.20% during the forecast period. The global market is likely to capture a valuation of US$ 3,15,035.4 million in 2024 and reach US$ 4,75,689.7 million by 2034 (Future Market Insights).

Sportswear is commonly made from a variety of materials and blends, the most popular includes polyester, nylon, and spandex. These synthetic fibers are lightweight, durable, and moisture-wicking; ideal for activewear. New developments in material science are importantly driving a systemic change by replacing synthetic fibers with high-performance recycled and natural fibers and blends.

This tech review delves into just some of the latest innovations that are reshaping the landscape of sportswear manufacture and customisation, with a keen focus on print technology, fabrics & process.

DTG (Direct to Garment) Printing Technologies

During the year DTG (direct to garment) printing has been concentrated on overcoming the perennial problem of printing onto sportwear’s most popular fibres - polyester and elastane. Where previously print quality and fastness properties were poor, 2023 saw elegant solutions offered to the industry from a variety of players.

At the forefront of innovation Ricoh state that the new “Ri 4000 with the newly developed Enhancer (pretreatment) liquid and Ink realises customers' business growth goals by printing on 100% Polyester material and high-polyester blends with ease. With the built-in enhancer technology, the RICOH Ri 4000 eliminates the inconsistent quality of manual pretreatment to achieve the highest work efficiency”. Their latest technologies offer customised production and deliver industrial garment printing at an affordable price for enterprise users who have demands for sportswear printing on polyester.

DTF (Direct to Film) Technologies

Direct-to-film printing is suitable for heavy-duty sportswear, outerwear, and apparel accessories.

Recently launched for 2023 is the Brother GTX Pro Series DTF Printer who state that “With its advanced technology and user-friendly interface, this printer offers exceptional print quality and fast production speeds. The Brother GTX Pro Series is designed to handle high-volume printing while ensuring accurate colour reproduction and durability. The printer features a large print area, allowing for maximum design possibilities. It also utilizes Brother’s proprietary ink technology, which ensures vibrant colours, excellent washability, and long-lasting prints. The Brother GTX Pro Series DTF Printer is suitable for both small businesses and large-scale production environments.”

From M&R The Quatro Direct to Film (DTF) Transfer Printing System is their newest printing solution, offering high-quality prints with high-quality value. M&R state “The printed apparel decorating industry continues to evolve at a rapid pace, due to several notable trends and technology advancements that are shaping the industry. The M&R Quatro (DTF) Transfer Printing System is a modern and efficient method of applying vibrant, high-quality durable images onto a wide variety of garments and fabric types”.

“The DTF process begins with the creation of a digital design on a computer. Once the design is finalized, it is printed onto a special PET film with a specialized digital inkjet printer using Cyan, Magenta, Yellow, Black and White pigmented aqueous inkjet inks. After printing is complete, and while the ink is still wet, the transfer is prepared by applying a layer of adhesive to the print area. Immediately after the adhesive has been applied, the final construction of film, ink, and adhesive is prepared for the transfer process by running it through a high efficiency infra-red drying system to cure the ink, and to fuse the adhesive to achieve a strong bond between the ink and the fabric, ensuring a durable and long-lasting print.”

Dye Sublimation Technologies

Mimaki dye sublimation printers, together with EarlyVision garment design and visualisation software at Nopinz, are making speed suits for some of the world’s top cycling teams, as well as for competitive amateurs.