#edge computing solutions for telecom

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been banned in Indonesia for providing people with access to pornographic content.

Text

Available Cloud Computing Services at Fusion Dynamics

We Fuel The Digital Transformation Of Next-Gen Enterprises!

Fusion Dynamics provides future-ready IT and computing infrastructure that delivers high performance while being cost-efficient and sustainable. We envision, plan and build next-gen data and computing centers in close collaboration with our customers, addressing their business’s specific needs. Our turnkey solutions deliver best-in-class performance for all advanced computing applications such as HPC, Edge/Telco, Cloud Computing, and AI.

With over two decades of expertise in IT infrastructure implementation and an agile approach that matches the lightning-fast pace of new-age technology, we deliver future-proof solutions tailored to the niche requirements of various industries.

Our Services

We decode and optimise the end-to-end design and deployment of new-age data centers with our industry-vetted services.

System Design

When designing a cutting-edge data center from scratch, we follow a systematic and comprehensive approach. First, our front-end team connects with you to draw a set of requirements based on your intended application, workload, and physical space. Following that, our engineering team defines the architecture of your system and deep dives into component selection to meet all your computing, storage, and networking requirements. With our highly configurable solutions, we help you formulate a system design with the best CPU-GPU configurations to match the desired performance, power consumption, and footprint of your data center.

Why Choose Us

We bring a potent combination of over two decades of experience in IT solutions and a dynamic approach to continuously evolve with the latest data storage, computing, and networking technology. Our team constitutes domain experts who liaise with you throughout the end-to-end journey of setting up and operating an advanced data center.

With a profound understanding of modern digital requirements, backed by decades of industry experience, we work closely with your organisation to design the most efficient systems to catalyse innovation. From sourcing cutting-edge components from leading global technology providers to seamlessly integrating them for rapid deployment, we deliver state-of-the-art computing infrastructures to drive your growth!

What We Offer The Fusion Dynamics Advantage!

At Fusion Dynamics, we believe that our responsibility goes beyond providing a computing solution to help you build a high-performance, efficient, and sustainable digital-first business. Our offerings are carefully configured to not only fulfil your current organisational requirements but to future-proof your technology infrastructure as well, with an emphasis on the following parameters –

Performance density

Rather than focusing solely on absolute processing power and storage, we strive to achieve the best performance-to-space ratio for your application. Our next-generation processors outrival the competition on processing as well as storage metrics.

Flexibility

Our solutions are configurable at practically every design layer, even down to the choice of processor architecture – ARM or x86. Our subject matter experts are here to assist you in designing the most streamlined and efficient configuration for your specific needs.

Scalability

We prioritise your current needs with an eye on your future targets. Deploying a scalable solution ensures operational efficiency as well as smooth and cost-effective infrastructure upgrades as you scale up.

Sustainability

Our focus on future-proofing your data center infrastructure includes the responsibility to manage its environmental impact. Our power- and space-efficient compute elements offer the highest core density and performance/watt ratios. Furthermore, our direct liquid cooling solutions help you minimise your energy expenditure. Therefore, our solutions allow rapid expansion of businesses without compromising on environmental footprint, helping you meet your sustainability goals.

Stability

Your compute and data infrastructure must operate at optimal performance levels irrespective of fluctuations in data payloads. We design systems that can withstand extreme fluctuations in workloads to guarantee operational stability for your data center.

Leverage our prowess in every aspect of computing technology to build a modern data center. Choose us as your technology partner to ride the next wave of digital evolution!

#Keywords#services on cloud computing#edge network services#available cloud computing services#cloud computing based services#cooling solutions#hpc cluster management software#cloud backups for business#platform as a service vendors#edge computing services#server cooling system#ai services providers#data centers cooling systems#integration platform as a service#https://www.tumblr.com/#cloud native application development#server cloud backups#edge computing solutions for telecom#the best cloud computing services#advanced cooling systems for cloud computing#c#data center cabling solutions#cloud backups for small business#future applications of cloud computing

0 notes

Text

Transform Your Network with Managed Network Edge and SD-WAN

In today’s fast-paced digital environment, efficient network management is crucial. SolveForce, in partnership with Spectrum Enterprise, brings you the Managed Network Edge with SD-WAN solution. This robust offering simplifies the expansion, management, and security of networks across multiple locations using a single platform. Simplify Your Network Management Managed Network Edge is a modular…

#Cisco Meraki#Cloud Computing#Digital Transformation#Managed Network Edge#Network Management#Network Security#SD-WAN#SolveForce#Spectrum Enterprise#Telecom Solutions

0 notes

Text

Top Global Solution IT Service Providers in New Delhi

New Delhi, the bustling capital of India, has emerged as a major hub for the IT industry. With a growing demand for digital transformation, businesses are increasingly relying on IT service providers to streamline their operations, enhance security, and develop innovative solutions. Here’s a look at some of the Top global IT service providers in New Delhi that are leading the way in technology solutions and support.

Tata Consultancy Services (TCS)

TCS is one of the largest IT service providers in India and has a strong presence in New Delhi. The company specializes in IT consulting, cloud solutions, artificial intelligence, and cybersecurity. With decades of experience and a global presence, TCS provides cutting-edge solutions for enterprises across industries.

HCL Technologies

Headquartered in Noida, close to New Delhi, HCL Technologies is a global IT services company known for its expertise in software development, IT infrastructure management, and digital transformation solutions. The company has a strong clientele across banking, healthcare, and manufacturing sectors.

Wipro Limited

Wipro is another IT giant with a significant footprint in New Delhi. It offers services in cloud computing, data analytics, business process outsourcing (BPO), and cybersecurity. Wipro's commitment to innovation and sustainability has made it a preferred IT partner for enterprises worldwide.

Infosys

Infosys is a leader in IT services and consulting, providing businesses with digital transformation solutions, AI-driven insights, and enterprise cloud services. The company has a strong presence in the capital and supports industries such as finance, retail, and healthcare.

Tech Mahindra

Tech Mahindra, part of the Mahindra Group, is a well-established IT service provider in New Delhi. The company focuses on telecom, IT consulting, and digital transformation services. It also offers specialized solutions in AI, blockchain, and IoT for businesses looking to innovate.

NIIT Technologies (Coforge)

Now known as Coforge, NIIT Technologies is a renowned IT service provider in New Delhi, specializing in digital services, cloud computing, and application development. The company serves industries like travel, banking, and insurance with customized IT solutions.

Cognizant

Cognizant has a strong presence in New Delhi, providing IT solutions in digital engineering, AI, and data analytics. The company caters to industries such as healthcare, retail, and finance, helping businesses achieve digital growth.

IBM India

IBM India is a trusted name in IT services, offering cloud solutions, AI, cybersecurity, and blockchain technology. With an established base in New Delhi, IBM supports enterprises in enhancing their IT infrastructure and business processes.

Dell Technologies

Dell provides IT consulting, hardware solutions, cloud computing, and enterprise-grade cybersecurity services. Businesses in New Delhi rely on Dell for data storage, virtualization, and IT infrastructure solutions.

OrangeMantra

A fast-growing IT solutions provider based in Gurugram, near New Delhi, OrangeMantra offers web development, mobile app development, AI-based solutions, and e-commerce platforms. The company caters to startups and established enterprises looking for customized IT services.

2 notes

·

View notes

Text

A Comprehensive Guide to the Top Industries Attracting FDI in India

India has emerged as one of the most attractive destinations for Foreign Direct Investment (FDI) in recent years, thanks to its robust economic growth, favorable demographics, and ongoing policy reforms. FDI plays a crucial role in stimulating economic development by bringing in capital, technology, and expertise. In this comprehensive guide, we will delve into the top industries that are attracting FDI in India.

1. Information Technology (IT) and Software Services:

India's IT industry has been a pioneer in attracting FDI, fueling the country's economic growth and creating millions of jobs. With a large pool of skilled IT professionals, cost-effective services, and a conducive business environment, India continues to be a global hub for software development, IT outsourcing, and business process outsourcing (BPO).

India's Information Technology (IT) and software services industry have been pivotal in attracting Foreign Direct Investment (FDI) due to several key factors:

1. Skilled Workforce:

India boasts a vast pool of highly skilled IT professionals, including software engineers, developers, and project managers. The country's education system emphasizes STEM (Science, Technology, Engineering, and Mathematics) fields, producing a large number of graduates with expertise in computer science and information technology. This skilled workforce is instrumental in delivering high-quality software development, IT outsourcing, and business process outsourcing (BPO) services to clients worldwide.

2. Cost-Effectiveness:

The cost of labor in India is significantly lower compared to developed countries, making it an attractive destination for outsourcing IT projects and services. Foreign companies can leverage India's cost-effective labor market to reduce their operational expenses while maintaining high standards of quality and efficiency. This cost advantage has been a major driver for multinational corporations to set up offshore development centers and service delivery hubs in India.

3. Conducive Business Environment:

India offers a conducive business environment for IT companies, characterized by liberalized policies, supportive government initiatives, and a well-established legal framework. The government has implemented various reforms to promote ease of doing business, simplify regulatory procedures, and encourage foreign investment in the IT sector. Additionally, initiatives such as Digital India and Make in India have further propelled the growth of the IT industry by fostering innovation, entrepreneurship, and technology adoption.

4. Global Reputation:

Over the years, India has built a strong reputation as a leading destination for IT and software services globally. Indian IT companies have demonstrated expertise in delivering cutting-edge solutions, leveraging emerging technologies, and meeting the diverse needs of clients across industries. This reputation has attracted multinational corporations to partner with Indian firms, outsource IT projects, and establish long-term collaborations for software development, maintenance, and support services.

5. Innovation and R&D:

India's IT industry is not just about cost arbitrage; it is also a hub for innovation, research, and development. Many global technology firms have set up innovation centers, research labs, and technology incubators in India to tap into the country's talent pool and drive innovation. These centers focus on developing next-generation technologies, conducting R&D activities, and creating intellectual property in areas such as artificial intelligence, machine learning, blockchain, and cloud computing.

2. Telecommunications:

India's telecommunications sector has witnessed significant FDI inflows, driven by the rapid expansion of mobile and internet services. With a massive consumer base and increasing smartphone penetration, telecom companies are investing heavily in network infrastructure, spectrum auctions, and digital technologies to capitalize on the growing demand for data services.

India's telecommunications sector has emerged as a prominent recipient of Foreign Direct Investment (FDI) due to several key factors:

1. Expanding Market Potential:

India has one of the largest telecommunications markets in the world, with over a billion mobile subscribers and rapidly increasing internet penetration. The country's vast population, growing middle class, and rising disposable incomes have fueled the demand for voice, data, and digital services across urban and rural areas. This immense market potential offers lucrative opportunities for telecom companies to invest in network infrastructure, spectrum allocation, and innovative services to cater to the diverse needs of consumers.

2. Mobile Revolution:

India has witnessed a mobile revolution in recent years, driven by affordable smartphones, competitive tariffs, and widespread adoption of mobile internet services. The proliferation of mobile devices has transformed communication, commerce, and entertainment, creating new business models and revenue streams for telecom operators. Foreign investors recognize India's mobile-first market dynamics and are keen to capitalize on the growing demand for voice calls, messaging apps, mobile data, and value-added services.

3. Digital Connectivity:

The government's Digital India initiative aims to bridge the digital divide and promote inclusive growth by ensuring broadband connectivity to all citizens. This ambitious program has spurred investments in fiber-optic networks, 4G/5G infrastructure, and rural broadband initiatives to enhance digital connectivity and enable access to digital services in remote areas. Foreign telecom companies view India's digital transformation as an opportunity to deploy advanced technologies, improve network coverage, and deliver high-speed internet services to underserved communities.

4. Spectrum Auctions:

Spectrum is a critical asset for telecom operators to expand their network capacity, improve service quality, and offer new services to customers. India's spectrum auctions provide an opportunity for telecom companies to acquire additional spectrum bands and strengthen their market position. Foreign investors participate in these auctions to acquire spectrum licenses and invest in network upgrades, spectrum refarming, and technology modernization to enhance their competitiveness in the market.

5. Convergence of Services:

The convergence of telecommunications with other sectors such as media, entertainment, and technology is driving investment opportunities in integrated services and content delivery platforms. Foreign telecom operators are exploring partnerships, mergers, and acquisitions with content providers, OTT (Over-the-Top) platforms, and digital media companies to offer bundled services, streaming content, and personalized experiences to subscribers.

6. Policy Reforms:

The Indian government has introduced several policy reforms to liberalize the telecom sector, attract foreign investment, and promote healthy competition. Initiatives such as National Digital Communications Policy (NDCP), ease of doing business reforms, and regulatory clarity have created a favorable investment climate for telecom companies. Foreign investors are encouraged by the government's commitment to reforming regulations, promoting innovation, and fostering a vibrant telecom ecosystem in India.

3. Automobiles and Automotive Components:

The Indian automotive industry has attracted substantial FDI from global automakers and component manufacturers seeking to establish manufacturing facilities, R&D centers, and distribution networks. India's competitive manufacturing costs, skilled workforce, and improving infrastructure have positioned it as a key player in the global automotive market.

4. Pharmaceuticals and Healthcare:

The pharmaceutical sector in India has been a magnet for FDI due to its strong regulatory framework, large market potential, and cost advantages in drug manufacturing. Foreign pharmaceutical companies are investing in research collaborations, production facilities, and distribution networks to tap into India's growing healthcare needs and leverage its expertise in generic drugs.

5. Renewable Energy:

India's ambitious renewable energy targets and supportive government policies have attracted significant FDI inflows into the sector. Foreign investors are investing in solar, wind, hydro, and biomass projects, driven by India's vast renewable energy potential, favorable regulatory environment, and growing demand for clean energy solutions.

6. Retail and E-Commerce:

India's retail and e-commerce sector has witnessed a surge in FDI with the liberalization of FDI policies and the rapid growth of online shopping. Global retail giants are partnering with Indian companies or establishing their own operations to tap into the country's burgeoning consumer market and rising middle-class population.

7. Real Estate and Construction:

The Indian real estate sector continues to attract FDI, driven by urbanization, infrastructure development, and demand for commercial and residential properties. Foreign investors are participating in joint ventures, development projects, and real estate investment trusts (REITs) to capitalize on India's growing urban centers and infrastructure needs.

8. Financial Services:

India's financial services industry is experiencing a steady influx of FDI, driven by liberalization measures, digital transformation, and increasing investor interest. Foreign banks, insurance companies, and fintech startups are expanding their presence in India to cater to the growing demand for banking, insurance, and digital payment services.

9. Food Processing:

The food processing sector in India has attracted FDI due to its vast agricultural resources, changing consumer preferences, and government incentives. Foreign companies are investing in food processing plants, cold chains, and distribution networks to meet the rising demand for processed and packaged food products in India.

10. Infrastructure:

India's infrastructure sector offers immense opportunities for FDI across various segments such as transportation, energy, and urban development. Foreign investors are participating in public-private partnerships (PPPs), infrastructure projects, and investment funds to address India's infrastructure gaps and support its economic growth.

In conclusion, India offers a diverse range of investment opportunities across various industries, making it an attractive destination for FDI. With a growing economy, favorable demographics, and ongoing policy reforms, India continues to attract foreign investors seeking high returns and long-term growth prospects. However, investors need to navigate regulatory challenges, market dynamics, and cultural nuances to succeed in India's competitive business landscape.

This post was originally published on: Foxnangel

#fdi in india#fdi investment in india#foreign invest in india#foreign direct investment#it industry#foreign companies#renewable energy#green energy#foxnangel#invest in india

2 notes

·

View notes

Text

Empowering Digital Innovation: Microlent Systems' Comprehensive Web Development Services

Microlent Systems

In an era dominated by digital transformation, businesses are relentlessly pursuing innovation to stay ahead in their respective markets. Amid this digital race, Microlent Systems emerges as a beacon of technological advancement and a pioneer in web development services. With a robust portfolio that spans web application development, TV application development, wearable technology solutions, enterprise solution development, AI/ML-based solutions, and IoT/hardware integrated solutions, Microlent stands at the forefront of enabling businesses to unlock their full potential in the digital landscape.

Web Application Development: A Cornerstone for Digital Success At the heart of Microlent's services lies its web application development expertise. In understanding the critical role that web applications play in today's business ecosystems, Microlent delivers bespoke solutions that are not just about coding and deployment but about creating a digital experience that resonates with end-users. From e-commerce sites that handle millions of transactions to SaaS platforms that automate business processes, Microlent's approach is to build scalable, secure, and dynamic web applications that drive user engagement and business growth.

Revolutionizing Television with TV Application Development The television industry is undergoing a transformation, with digital platforms and OTT services changing the way content is consumed. Microlent's TV application development service is tailored to meet this new wave of demand. By focusing on user experience, Microlent helps content providers, telecoms, and OTT platforms deliver applications that are intuitive, engaging, and accessible across devices, ensuring content reaches viewers worldwide in the most effective manner possible.

Pioneering in Wearable Technology with Android and Apple Watch Application Development As wearable technologies become an integral part of our daily lives, Microlent is at the helm of developing innovative applications for Android and Apple Watch devices. These applications are not just about extending smartphone functionalities to one's wrist but are designed with a focus on health, fitness, productivity, and lifestyle, ensuring users have a seamless and enriched wearable experience.

Enterprise Solution Development: Catalyzing Business Transformation Microlent recognizes the challenges businesses face in adapting to rapidly changing market conditions. Its enterprise solution development services are focused on building robust, cutting-edge solutions that enable businesses to streamline operations, enhance efficiency, and maintain competitive advantage. Whether it's through CRM systems, ERP solutions, or custom software tailored to specific business needs, Microlent's solutions are a catalyst for digital transformation.

Leading the Way in AI/ML-Based Solutions In the realm of artificial intelligence and machine learning, Microlent is a trailblazer, providing cutting-edge solutions that drive innovation across industries. From predictive analytics and natural language processing to computer vision and intelligent automation, Microlent leverages the latest in AI and ML technologies to help businesses unlock new opportunities, enhance decision-making, and create value in ways never before possible.

Bridging the Physical and Digital with IoT/Hardware Integrated Solutions Microlent's expertise extends into the burgeoning field of IoT and hardware-integrated solutions, where the physical and digital worlds converge. By enabling smart interactions between devices, systems, and services, Microlent's solutions facilitate enhanced data collection, real-time monitoring, and automated control, driving efficiency, sustainability, and innovation across sectors.

Conclusion In the constantly evolving digital landscape, Microlent Systems stands out as a partner of choice for businesses looking to harness the power of technology for growth, innovation, and digital transformation. With a commitment to excellence, a passion for innovation, and a comprehensive suite of web development services, Microlent is dedicated to empowering businesses to achieve their digital aspirations.

#india#software development#mobile app development#mobile app development company in india#web design india#softwaredevelopment#web development

2 notes

·

View notes

Text

Unlocking Opportunities in the Digital Era

In the ever-evolving landscape of the telecommunications industry, pursuing a Post Graduate Diploma in Management (PGDM) with a specialization in Telecom Management can be a strategic career move. India, home to some of the top business schools like Poddar Business School in Rajasthan, offers excellent opportunities for students to gain expertise in this field. Let's delve into the significance of Telecom Management in a PGDM course and how it can shape the future of aspiring professionals.

Navigating the Digital Transformation: The telecom industry is at the forefront of the digital revolution, driving connectivity and technological advancements. A specialized PGDM in Telecom Management equips students with the knowledge and skills to navigate this transformation. They gain insights into emerging technologies like 5G, the Internet of Things (IoT), cloud computing, and artificial intelligence (AI), enabling them to contribute effectively to the industry.

Understanding Industry Dynamics: Telecom Management programs provide a comprehensive understanding of the telecom industry's structure, competitive landscape, and regulatory environment. Students learn about market trends, consumer behavior, and the impact of globalization on the industry. This knowledge enables them to make informed decisions and develop strategies that address the challenges and opportunities in this dynamic sector.

Developing Managerial Competencies: PGDM courses with a specialization in Telecom Management develop a range of managerial competencies specific to the telecom industry. Students acquire skills in strategic planning, project management, operations, marketing, and finance, tailored to the unique requirements of the sector. These skills empower them to lead telecom organizations and drive growth in an increasingly competitive market.

Leveraging Data Analytics: In the digital era, data is a valuable asset for telecom companies. PGDM programs in Telecom Management emphasize data analytics skills, enabling students to extract meaningful insights from large datasets. They learn to analyze customer behavior, identify market trends, and optimize business operations. Proficiency in data analytics equips graduates with a competitive edge in decision-making and positions them for leadership roles.

Fostering Innovation and Entrepreneurship: Telecom Management programs encourage students to think innovatively and explore entrepreneurship opportunities in the industry. They learn about emerging business models, disruptive technologies, and startup ecosystems. This fosters an entrepreneurial mindset and equips graduates to identify untapped market niches, develop innovative solutions, and launch their ventures.

Networking and Industry Exposure: Top business schools in India, such as Poddar Business School, facilitate industry interactions, guest lectures, and internships in collaboration with leading telecom companies. This provides students with networking opportunities and firsthand exposure to real-world challenges and practices. Such engagements enable students to develop professional connections and gain practical insights that enhance their employability.

In conclusion, pursuing a PGDM with a specialization in Telecom Management from a top business school in India, like Poddar Business School in Rajasthan, offers immense potential for aspiring professionals. The program equips students with the necessary knowledge and skills to thrive in the dynamic telecom industry. From understanding industry dynamics and leveraging data analytics to fostering innovation and entrepreneurship, Telecom Management in a PGDM course unlocks opportunities in the digital era and positions graduates for successful careers in this evolving sector.

0 notes

Text

CPE Chip Market Analysis: CAGR of 12.1% Predicted Between 2025–2032

MARKET INSIGHTS

The global CPE Chip Market size was valued at US$ 1.58 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 12.1% during the forecast period 2025-2032. This growth trajectory aligns with the broader semiconductor industry expansion, which was valued at USD 579 billion in 2022 and is expected to reach USD 790 billion by 2029 at a 6% CAGR.

CPE (Customer Premises Equipment) chips are specialized semiconductor components that enable network connectivity in devices such as routers, modems, and gateways. These chips power critical functions including signal processing, data transmission, and protocol conversion for both 4G and 5G networks. The market comprises two primary segments – 4G chips maintaining legacy infrastructure support and 5G chips driving next-generation connectivity with higher bandwidth and lower latency.

Market expansion is being propelled by three key factors: the global rollout of 5G infrastructure, increasing demand for high-speed broadband solutions, and the proliferation of IoT devices requiring robust connectivity. However, supply chain constraints in the semiconductor industry and geopolitical factors affecting chip production present ongoing challenges. Major players like Qualcomm and MediaTek are investing heavily in R&D to develop advanced CPE chipsets, while emerging players such as UNISOC and ASR are gaining traction in cost-sensitive markets. The Asia-Pacific region dominates production and consumption, accounting for over 45% of global CPE chip demand in 2024.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Accelerates Demand for Advanced CPE Chips

The global transition to 5G networks continues to drive exponential growth in the CPE chip market. As telecom operators roll out next-generation infrastructure, the demand for high-performance customer premise equipment has surged by over 40% in the past two years. Modern 5G CPE devices require specialized chipsets capable of supporting multi-gigabit speeds, ultra-low latency, and massive device connectivity. Leading chip manufacturers are responding with integrated solutions that combine baseband processing, RF front-end modules, and AI acceleration. For instance, Qualcomm’s latest 5G CPE platforms deliver 10Gbps throughput while reducing power consumption by 30% compared to previous generations.

IoT Adoption Creates New Growth Avenues for CPE Chip Vendors

The proliferation of Internet of Things (IoT) applications across smart cities, industrial automation, and connected homes is generating significant opportunities for CPE chip manufacturers. With over 15 billion IoT devices projected to connect to networks by 2025, telecom operators require CPE solutions that can efficiently manage diverse traffic patterns and quality-of-service requirements. This has led to the development of specialized chipsets featuring advanced traffic management, edge computing capabilities, and enhanced security protocols. Recent product launches demonstrate this trend, with companies like MediaTek introducing chips optimized for IoT gateways that support simultaneous connections to hundreds of endpoints while maintaining reliable performance.

Remote Work Infrastructure Investments Fuel Market Expansion

The permanent shift toward hybrid work models continues to stimulate demand for enterprise-grade CPE solutions. Businesses worldwide are upgrading their network infrastructure to support distributed workforces, driving a 25% year-over-year increase in CPE deployments. This trend has particularly benefited manufacturers of chips designed for business routers and SD-WAN appliances, which require robust performance for VPNs, unified communications, and cloud applications. Leading semiconductor firms have responded with system-on-chip solutions integrating Wi-Fi 6/6E, multi-core processors, and hardware-accelerated encryption to meet these evolving requirements.

MARKET RESTRAINTS

Supply Chain Disruptions Continue to Challenge Production Stability

Despite strong demand, the CPE chip market faces persistent supply chain constraints that limit growth potential. The semiconductor industry’s reliance on advanced fabrication nodes has created bottlenecks, with lead times for certain components extending beyond 12 months. These challenges are compounded by geopolitical tensions affecting rare earth material supplies and export controls on specialized manufacturing equipment. While the situation has improved from pandemic-era shortages, inventory levels remain below historical averages, forcing many CPE manufacturers to implement allocation strategies and redesign products with available components.

Rising Component Costs Squeeze Profit Margins

Escalating production expenses present another significant restraint for CPE chip suppliers. The transition to more advanced process nodes has increased wafer costs by approximately 20-30% across the industry. Additionally, testing and packaging expenses have risen due to higher energy prices and labor costs. These factors have compressed gross margins, particularly for mid-range CPE chips where pricing pressure is most intense. Manufacturers are responding by optimizing chip architectures, consolidating IP blocks, and investing in yield improvement initiatives, but these measures require significant R&D expenditures that may take years to yield returns.

Regulatory Complexity Slows Time-to-Market

The CPE chip industry faces growing regulatory scrutiny that delays product launches and increases compliance costs. New spectrum regulations, cybersecurity requirements, and equipment certification processes have extended development cycles by 3-6 months on average. In particular, the automotive and industrial sectors now demand comprehensive safety certifications that require extensive testing and documentation. These regulatory hurdles disproportionately affect smaller chip vendors who lack dedicated compliance teams, potentially limiting innovation and competition in certain market segments.

MARKET CHALLENGES

Technology Complexity Increases Design and Validation Costs

Modern CPE chips incorporate increasingly sophisticated architectures that pose significant engineering challenges. Designs now routinely integrate multiple processor cores, AI accelerators, and specialized radio interfaces, requiring advanced simulation tools and verification methodologies. The associated R&D costs have grown exponentially, with some 5G chip development projects now exceeding $100 million in budget. This creates a high barrier to entry for potential competitors and forces established players to carefully prioritize their product roadmaps. Furthermore, the complexity makes post-silicon validation more difficult, potentially leading to costly respins if critical issues emerge late in the development cycle.

Talent Shortage Constrains Innovation Capacity

The semiconductor industry’s rapid expansion has created intense competition for skilled engineers, particularly in critical areas like RF design, digital signal processing, and physical implementation. CPE chip manufacturers report vacancy rates exceeding 30% for certain technical positions, with hiring cycles stretching to 9-12 months for specialized roles. This talent crunch limits companies’ ability to execute aggressive product roadmaps and forces difficult tradeoffs between projects. While firms are investing in training programs and academic partnerships, the pipeline for experienced chip designers remains insufficient to meet current demand.

Standardization Gaps Create Integration Headaches

The evolving nature of 5G and edge computing technologies has led to fragmented standards across different markets and regions. CPE chip vendors must support multiple protocol variants, frequency bands, and security frameworks, complicating both hardware and software development. This fragmentation increases testing overhead and makes it difficult to achieve economies of scale across product lines. While industry groups continue working toward greater harmonization, interim solutions often require additional engineering resources to implement customized features for specific customers or geographies.

CPE CHIP MARKET TRENDS

5G Network Expansion Accelerates Demand for Advanced CPE Chips

The rapid global deployment of 5G networks is significantly driving the CPE (Customer Premises Equipment) chip market, with the segment projected to grow at over 30% CAGR through 2032. Telecom operators worldwide invested nearly $280 billion in 5G infrastructure in 2023 alone, creating substantial demand for compatible CPE devices. Chip manufacturers are responding with innovative solutions featuring multi-band support and improved power efficiency, with next-generation modem-RF combos now achieving throughputs exceeding 7Gbps. While 4G CPE chips still dominate current installations, representing about 65% of 2024 shipments, 5G solutions are rapidly gaining share due to superior performance in high-density urban environments.

Other Trends

Smart Home Integration

The proliferation of IoT devices in residential settings, expected to reach 29 billion connected units globally by 2027, is creating new requirements for CPE chips that can handle simultaneous broadband and IoT traffic management. Modern gateway solutions now incorporate AI-powered traffic prioritization and mesh networking capabilities to maintain quality of service across dozens of connected devices. Semiconductor vendors have responded with system-on-chip (SoC) designs integrating Wi-Fi 6/6E, Bluetooth, and Zigbee radios alongside traditional cellular modems. North America leads this adoption curve, with over 75% of new home internet subscriptions in 2023 opting for smart gateway solutions compared to just 32% in 2020.

Edge Computing and Network Virtualization Impact Chip Designs

Emerging virtualization technologies are reshaping CPE architectures, creating demand for chips with enhanced processing capabilities beyond traditional modem functions. Virtual CPE (vCPE) solutions now account for 18% of business installations, requiring chipsets that can efficiently run containerized network functions (CNFs) while maintaining low power envelopes. The enterprise segment has proven particularly receptive, with large-scale adoption in multi-tenant office buildings and smart city applications. Meanwhile, silicon designed for edge computing applications is increasingly incorporating hardware acceleration blocks for AI inference, allowing real-time processing of video analytics and other bandwidth-intensive applications at the network periphery. This evolution has prompted traditional chip vendors to expand their portfolios through strategic acquisitions in the FPGA and specialty processor spaces.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Partnerships Fuel Growth in the CPE Chip Market

The global CPE (Customer Premises Equipment) chip market remains highly competitive, characterized by technological innovation and aggressive expansion strategies. Qualcomm dominates the market with its extensive portfolio of 4G and 5G chipsets, capturing approximately 35% revenue share in 2024. The company’s leadership stems from its strong foothold in North America and strategic partnerships with telecom operators.

MediaTek and Intel follow closely, collectively accounting for 28% market share, owing to their cost-effective solutions for emerging markets and industrial applications. These players continue investing heavily in R&D, particularly for energy-efficient 5G chips catering to IoT deployments and smart city infrastructure.

Chinese manufacturers like Hisilicon and UNISOC are rapidly gaining traction through government-supported initiatives and localized supply chains. Their aggressive pricing strategies and custom solutions for Asian markets have enabled 18% year-over-year growth in 2024, challenging established western players.

Meanwhile, specialized firms such as Eigencomm and Sequans are carving niche positions through innovative chip architectures optimized for low-power wide-area networks (LPWAN) and private 5G deployments. Their collaborations with network equipment providers have become crucial differentiators in this evolving landscape.

List of Key CPE Chip Manufacturers Profiled

Qualcomm Technologies, Inc. (U.S.)

UNISOC (Shanghai) Technologies Co., Ltd. (China)

ASR Microelectronics Co., Ltd. (China)

HiSilicon (Huawei Technologies Co., Ltd.) (China)

XINYI Semiconductor (China)

MediaTek Inc. (Taiwan)

Intel Corporation (U.S.)

Eigencomm (China)

Sequans Communications S.A. (France)

Segment Analysis:

By Type

5G Chip Segment Dominates the Market Due to its High-Speed Connectivity and Low Latency

The CPE Chip market is segmented based on type into:

4G Chip

5G Chip

By Application

5G CPE Segment Leads Due to Escalated Demand for High-Performance Wireless Broadband

The market is segmented based on application into:

4G CPE

5G CPE

By End User

Telecom Operators Segment Dominates with Growing Infrastructure Investments

The market is segmented based on end user into:

Telecom Operators

Enterprises

Residential Users

Regional Analysis: CPE Chip Market

North America The mature telecommunications infrastructure and rapid 5G deployments in the U.S. and Canada are fueling demand for high-performance 5G CPE chips, particularly from vendors like Qualcomm and Intel. With major carriers investing over $275 billion in network upgrades, chip manufacturers are prioritizing low-latency, power-efficient designs. However, stringent regulatory scrutiny on semiconductor imports creates supply chain challenges. The region also leads in IoT adoption, driving demand for hybrid 4G/5G chips in smart city solutions and enterprise applications. Local chip designers benefit from strong R&D ecosystems but face growing competition from Asian suppliers.

Europe EU initiatives like the 2030 Digital Compass (targeting gigabit connectivity for all households) are accelerating CPE chip demand, though adoption varies across nations. Germany and the U.K. lead in 5G CPE deployments using chips from MediaTek and Sequans, while Eastern Europe still relies heavily on cost-effective 4G solutions. Strict data privacy laws and emphasis on open RAN architectures are reshaping chip design requirements. The region faces headwinds from component shortages but maintains steady growth through government-industry partnerships in semiconductor sovereignty programs.

Asia-Pacific Accounting for over 60% of global CPE chip consumption, the region is driven by China’s massive “5G+” infrastructure push and India’s expanding broadband networks. Local giants HiSilicon and UNISOC dominate low-to-mid range segments, while South Korean/Japanese firms focus on premium chips. Southeast Asian markets show explosive growth (20%+ CAGR) due to rural connectivity projects. However, geopolitical tensions and import restrictions create supply volatility. Price sensitivity remains high, favoring integrated 4G/5G combo chips over standalone 5G solutions in emerging economies.

South America Limited 5G spectrum availability keeps the market reliant on 4G LTE chips, though Brazil and Chile are early adopters of 5G CPEs using ASR and MediaTek solutions. Economic instability and currency fluctuations hinder large-scale infrastructure investments, causing operators to prioritize cost-effective Chinese chip suppliers. The lack of local semiconductor manufacturing creates import dependency, but recent trade agreements aim to improve component accessibility. Enterprise demand for industrial IoT routers presents niche opportunities for mid-tier chip vendors.

Middle East & Africa Gulf nations (UAE, Saudi Arabia) drive premium 5G CPE adoption through smart city projects, leveraging Qualcomm and Eigencomm chips. Sub-Saharan Africa depends on affordable 4G solutions from Chinese vendors, with mobile network operators deploying low-power chips for extended coverage. While underdeveloped fiber backhaul limits 5G potential, satellite-CPE hybrid chips are gaining traction in remote areas. Political instability in some markets disrupts supply chains, though rising digitalization funds (like Saudi’s $6.4bn ICT strategy) indicate long-term growth potential.

Report Scope

This market research report provides a comprehensive analysis of the global and regional CPE Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global CPE Chip market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (4G Chip, 5G Chip), application (4G CPE, 5G CPE), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates the market due to rapid 5G adoption.

Competitive Landscape: Profiles of leading market participants including Qualcomm, UNISOC, ASR, Hisilicon, and MediaTek, including their product offerings, R&D focus, and recent developments.

Technology Trends & Innovation: Assessment of emerging technologies in semiconductor design, fabrication techniques, and evolving industry standards for CPE devices.

Market Drivers & Restraints: Evaluation of factors driving market growth such as 5G rollout and IoT expansion, along with challenges including supply chain constraints and regulatory issues.

Stakeholder Analysis: Insights for chip manufacturers, network equipment providers, telecom operators, investors, and policymakers regarding the evolving ecosystem.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/fieldbus-distributors-market-size-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/consumer-electronics-printed-circuit.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-alloy-current-sensing-resistor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/modular-hall-effect-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/integrated-optic-chip-for-gyroscope.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/industrial-pulsed-fiber-laser-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/unipolar-transistor-market-strategic.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/zener-barrier-market-industry-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/led-shunt-surge-protection-device.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/type-tested-assembly-tta-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/traffic-automatic-identification.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/one-time-fuse-market-how-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/pbga-substrate-market-size-share-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nfc-tag-chip-market-growth-potential-of.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silver-nanosheets-market-objectives-and.html

0 notes

Text

ez-Q Engine 2.0: QuantumCTek’s 1000-Qubit Control System

QuantumCTek, a well-known Chinese quantum computing startup, has developed and delivered its groundbreaking ez-Q Engine 2.0 superconducting quantum measurement and control system, advancing the global quantum computing environment. On Monday, June 17, this cutting-edge technology was unveiled that can manage over 1,000 qubits. It advances large-scale quantum computing. Its capabilities and architecture focus on superconducting qubits, a major quantum computing hardware platform.

While meeting globally sophisticated technical standards, the ez-Q Engine 2.0 will cost less than half as much as comparable foreign technology. This impressive combination of cost-effectiveness and high performance should accelerate quantum computing technology commercialisation and make it more accessible for research and development. QuantumCTek supplied this system to the University of Science and Technology of China and China Telecom Quantum Group, two major research institutions.

Quantum Computer Nerve Centre

For quantum computing, the ez-Q Engine 2.0 is the “nerve centre”. Its main task is sophisticated signal production control for quantum devices to make quantum computers work. The fundamental component of RF signal processing is needed to manipulate and read superconducting qubit states. This new system has tenfold better integration than its predecessor, increasing design efficiency and capacity, according to the Anhui Quantum Computing Engineering Research Centre.

Tang Shibiao, head of the Anhui Quantum Computing Engineering Research Centre, stressed the innovation's commercial value. He previously stated, “The cost of controlling a single superconducting qubit with a control system was very high”. Historically, excessive cost has hindered quantum system scalability. But the ez-Q Engine 2.0 solves this problem with a highly advanced and cost-effective solution that is “less than half the price of similar products developed by foreign competitors.”

China's Self-Sufficiency Drive

China's pursuit of quantum computer technology is linked to this discovery. China has been carefully investing in quantum computing to ensure its computer dominance. The ez-Q Engine 2.0 uses domestically made essential components, which boosts China's technical ecosystem and reduces its dependence on foreign suppliers. This measure is part of a bigger national push to dominate quantum technology, ensuring that the essential infrastructure is constructed nationally.

Performance and Verification

QuantumCTek's revolutionary control technology has been extensively tested in quantum computing environments. The ez-Q Engine 2.0's validation on China's 504-qubit superconducting quantum computer demonstrated its endurance and capacity to handle complex large-scale systems. This validation shows it can manage several qubits practically.

It also powered the 105-qubit Zuchongzhi 3.0 CPU. Chinese researchers say that the Zuchongzhi 3.0 can accomplish very complex tasks quadrillions of times quicker than typical supercomputers, demonstrating QuantumCTek's control systems' computing prowess. Validations show that the ez-Q Engine 2.0 is feasible and meets high performance standards.

Increasing Quantum Infrastructure

QuantumCTek has great plans for its cutting-edge control technology. Several universities will receive control services for over 5,000 qubits from the company. This effort represents a strategic push towards larger and more complicated quantum systems to handle more difficult issues. Quantum computing infrastructure in China also grew. This breakthrough would increase China's quantum race standing by providing high-capacity quantum computing resources.

QuantumCTek has a busy innovation pipeline. Wang Zhehui, leader of QuantumCTek's research team and deputy director of the Anhui Quantum Computing Engineering Research Centre, said the company is already developing a next-generation system. This system is expected to handle 10,000 qubits and offer advanced error-correction. Scalable and practical quantum computers require error correction because qubits are brittle and error-prone.

Global Quantum Race Heats Up

The release of the ez-Q Engine 2.0 shows worldwide quantum computing competition growing. The US, China, and many European nations are racing to create useful applications for this new technology. Financial modelling, medical research, and cryptography may change with quantum computing. Quantum computing uses quantum mechanics to calculate complex data exponentially faster. This solves intractable material science, AI, finance, and cryptography issues.

China is a formidable competitor in the global quantum race thanks to QuantumCTek's ez-Q Engine 2.0's high qubit management capacity, cost reduction, and smart domestic component design. The technique is an example of the "Quantum Leap" countries are pursuing to achieve broadly available, large-scale quantum computing.

The official Quantum News portal, Quantum Zeitgeist, routinely highlights quantum computing as one of the most inventive technologies of our day, having the potential to transform many businesses and the planet itself. This QuantumCTek innovation is another breakthrough in the Quantum Zeitgeist and a crucial “nugget of quantum goodness” for the industry.

#QuantumCTek#ezQEngine20#quantumcomputing#qubits#superconductingquantum#Zuchongzhi30#News#Technews#Technology#Technologynews#Technologytrends#Govindhtech

0 notes

Text

All Ordinaries Index: Telstra Group Ltd (ASX:TLS) Expands Telco Infrastructure Across Regions

Highlights:

Telstra Group Ltd continues to lead the telecommunications sector through domestic and international infrastructure expansion.

The company strengthens digital connectivity via network enhancements and strategic technology deployments.

ASX:TLS is part of the All Ordinaries Index, reflecting a diverse mix of listed Australian entities.

Telecommunications Sector Overview with All Ordinaries Index Relevance Telstra Group Ltd (ASX:TLS) operates in the telecommunications sector and plays a key role in digital infrastructure and network services across Australia and select international regions. As part of the All Ordinaries Index, the company is recognised among a broad spectrum of entities listed on the Australian Securities Exchange. The All Ordinaries Index captures the performance of leading companies across multiple sectors, providing a representative view of market movement and corporate participation in the Australian economy.

Telstra’s inclusion in this index affirms its prominence in technology-driven services, network operations, and communications-based innovation. With an extensive footprint in mobile, broadband, and enterprise network solutions, Telstra supports both individual and business-grade connectivity. Its services extend from metropolitan regions to remote communities through satellite, fibre, and wireless networks.

Core Network Capabilities and Infrastructure Assets Telstra operates one of the largest mobile networks in the Southern Hemisphere, complemented by extensive fibre optic lines and subsea cable systems. These infrastructure components form the backbone of its core network services, connecting domestic endpoints and international data hubs. The company has built a long-standing reputation for reliability in signal coverage, bandwidth scalability, and low-latency performance.

Network enhancements remain a regular feature of Telstra’s operations, including upgrades to base stations, switching centres, and transmission equipment. The company also continues to develop software-defined networking (SDN) capabilities and edge computing infrastructure. These capabilities support advanced enterprise solutions, media distribution, and content streaming applications.

Enterprise and Government Solutions Beyond consumer telecommunications, Telstra Group Ltd serves business and government clients with end-to-end network management services. Solutions include managed networks, cloud access systems, mobile workforce integration, and global data routing. The company’s enterprise segment aligns closely with public sector needs, supporting secure and scalable connectivity for mission-critical platforms.

Telstra’s services cover sectors such as education, healthcare, emergency response, and defence communications. These deployments require specialised configurations to ensure continuity and data integrity. The company also offers satellite communication services to regional operations, further extending its technological reach to remote infrastructure hubs.

International Ventures and Strategic Growth Telstra’s growth strategy includes expanding its international cable systems and joint ventures with global telecom operators. Through Telstra International, the company maintains a presence in multiple Asia-Pacific nations, enabling cross-border data services and business process platforms. Submarine cable partnerships with international providers enhance bandwidth availability and connect Australia to major economic centres in Asia and North America.

Recent focus has included the extension of data centre agreements and partnerships with hyperscale cloud providers. These collaborations are designed to deliver cloud-ready connectivity and high-speed transfer capacity for modern application environments. Telstra’s role in next-generation networking is further strengthened by participation in mobile innovation platforms and international standards organisations.

Technology Roadmap and Sector Evolution The company’s roadmap aligns with broader telecommunications sector evolution trends. These include shifts toward 5G deployment, network virtualisation, and convergence between mobile and fixed-line services. Telstra has completed nationwide 5G rollout milestones and continues to add 5G coverage through spectrum allocation upgrades and smart antenna installations.

Research and development within Telstra focus on artificial intelligence applications in network diagnostics, predictive maintenance, and customer service optimisation. Additional developments include investments in network security frameworks and end-user authentication technologies. These upgrades support seamless connectivity while maintaining operational control over distributed digital systems.

0 notes

Text

📶 IoT Telecom-Services Market Size, Share & Growth Analysis 2034: The Smart Network Boom

IoT Telecom Services Market is witnessing remarkable growth, with projections estimating a leap from $22.3 billion in 2024 to $97.8 billion by 2034, at an impressive CAGR of 15.9%. This market is central to enabling communication between billions of interconnected devices that form the backbone of smart homes, connected cars, industrial automation, and smart cities. By providing essential connectivity services, network management, data analysis, and security solutions, IoT telecom services are transforming how industries operate, facilitating innovation and enhanced efficiency in the digital era.

As IoT ecosystems continue to scale, telecom providers are evolving from traditional connectivity suppliers to strategic enablers of integrated, intelligent solutions. This shift is being driven by the demand for real-time monitoring, data-driven decision-making, and scalable communication infrastructure, which are vital to the functioning of complex IoT networks.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS24639

Market Dynamics

The rapid adoption of 5G technology is revolutionizing the IoT telecom services landscape. Enhanced bandwidth and ultra-low latency are paving the way for applications like autonomous vehicles, remote healthcare, and industrial IoT. The growing focus on edge computing is another pivotal trend, enabling faster data processing and reducing strain on centralized servers.

However, with growth come challenges. Concerns about data privacy, interoperability, and network vulnerabilities are significant hurdles. Additionally, integration with legacy infrastructure and a shortage of skilled professionals are impeding seamless deployment in certain regions. Despite these barriers, flexible pricing models like pay-as-you-go and cloud-based deployment options are making services more accessible to enterprises of all sizes.

Key Players Analysis

The competitive landscape of the IoT Telecom Services Market is composed of a blend of established telecom giants and innovative startups. Leading companies like Tata Communications, Thales Group, KORE Wireless, Telit, Sierra Wireless, and u-blox are at the forefront, offering robust connectivity and device management solutions.

Emerging players such as Nexiot, Soracom, and Particle are disrupting the market with agile platforms focused on edge processing, lightweight protocols, and affordable deployment. Companies that prioritize cybersecurity, seamless device integration, and customer-centric solutions are expected to gain a competitive edge in this evolving space.

Regional Analysis

Asia-Pacific currently leads the IoT Telecom Services Market, driven by robust technological adoption in countries like China, Japan, and South Korea. Government-led initiatives, such as smart cities and Industry 4.0 programs, have significantly fueled the demand for IoT-based services.

North America, particularly the U.S. and Canada, follows closely behind due to mature digital infrastructure and high investment in emerging technologies. Europe is seeing rapid growth in markets such as Germany, the U.K., and France, which are focusing on sustainability and smart mobility.

Regions like Latin America, the Middle East, and Africa are emerging as potential hotspots, bolstered by growing urbanization and government incentives for digital transformation. Countries like Brazil, UAE, and Saudi Arabia are ramping up efforts to implement smart city and e-governance initiatives.

Recent News & Developments

Recent developments in the IoT telecom services space include the global rollout of 5G, which has dramatically improved service delivery capabilities. Companies are also increasingly adopting AI-powered analytics to enhance device performance and customer engagement.

Additionally, regulatory bodies are moving toward standardizing communication protocols and data privacy policies. This regulatory momentum is expected to ensure smoother interoperability and better security compliance across devices and platforms.

Cybersecurity continues to be a focal point, with telecom providers investing in advanced encryption and authentication mechanisms. Subscription-based models and customizable service tiers are being introduced to cater to businesses with varied IoT needs, making services more scalable and flexible.

Browse Full Report : https://www.globalinsightservices.com/reports/iot-telecom-services-market/

Scope of the Report

This report covers an in-depth analysis of the IoT Telecom Services Market from 2018 to 2034, including historical trends, current dynamics, and future projections. It delves into market segmentation by type, product, services, technology, application, and region, offering a comprehensive view of each segment’s performance and potential.

The study evaluates key market drivers, emerging trends, restraints, and opportunities, supported by detailed competitive profiling of both established and emerging players. It also includes regulatory overviews, SWOT analysis, and value-chain assessments to help stakeholders formulate informed business strategies.

As digital transformation accelerates across industries, the IoT Telecom Services Market stands at the forefront of enabling smarter, more connected ecosystems. Businesses that align with market trends and invest in resilient, secure, and scalable IoT solutions will be best positioned to lead in this evolving digital landscape.

Discover Additional Market Insights from Global Insight Services:

Printed Circuit Board Market : https://www.globalinsightservices.com/reports/printed-circuit-board-market/

Asset Integrity Management Market :https://www.globalinsightservices.com/reports/asset-integrity-management-market/

Medical Sensors Market ; https://www.globalinsightservices.com/reports/medical-sensors-market/

Smart Factory Market : https://www.globalinsightservices.com/reports/smart-factory-market/

Wearable Sensors Market : https://www.globalinsightservices.com/reports/wearable-sensors-market/

#iottelecom #smartconnectivity #5gnetworks #edgecomputing #smartcities #iotplatforms #networkmanagement #digitaltransformation #industrialiot #connectedfuture

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

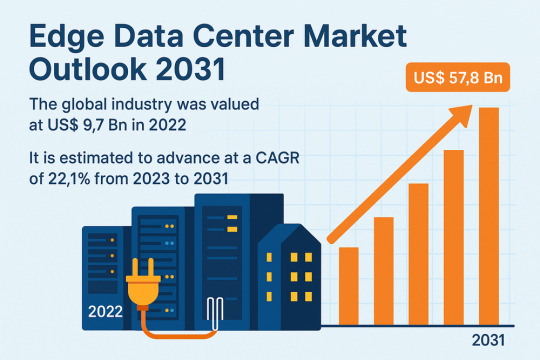

Edge Computing Demand Accelerates Market Growth at 22.1% CAGR

The global Edge Data Center Market was valued at USD 9.7 Bn in 2022 and is projected to reach USD 57.8 Bn by the end of 2031, expanding at an impressive CAGR of 22.1% from 2023 to 2031. This rapid growth is fueled by the increasing demand for real-time data processing, the rise of streaming services, growth in IoT and AI-driven technologies, and the adoption of autonomous vehicles.

Market Overview: Edge data centers are smaller, decentralized data facilities located close to the end-users and connected devices. These centers reduce latency, improve bandwidth efficiency, and enable faster data processing by bringing computation and storage closer to the data source.

Edge computing is being adopted across a variety of sectors, including healthcare, manufacturing, automotive, and telecom, as organizations seek to leverage real-time analytics and improve user experience. With 5G networks and AI-based solutions gaining traction globally, the need for edge infrastructure is growing significantly.

Market Drivers & Trends

One of the primary market drivers is the surge in demand for video streaming services. Platforms such as Netflix, YouTube, and Disney+ are increasingly dependent on edge data centers to deliver content with minimal latency and buffering. For instance, Netflix uses edge infrastructure to reduce content delivery costs and ensure a seamless user experience.

Additionally, the rapid adoption of IoT devices and AI technologies has heightened the need for low-latency data processing. Applications like autonomous vehicles, smart cities, industrial automation, and digital healthcare depend on instantaneous data collection and response, which edge data centers facilitate.

The expansion of 5G networks further accelerates edge data center deployment. As bandwidth and connection speeds increase, so does the demand for faster and more reliable data delivery.

Latest Market Trends

Increased deployment in rural and semi-urban areas: Edge data centers are being built in remote areas to bridge the digital divide. For example, RailTel Corp. is constructing 102 edge data centers across rural and semi-urban India to support digital services with minimal latency.

Integration of edge with AI and ML: Enterprises are leveraging edge computing to run machine learning models directly at the source of data. This results in faster decision-making and enhances operational efficiency.

Sustainable data centers: Growing environmental concerns are pushing companies to build eco-friendly edge data centers powered by renewable energy and equipped with energy-efficient cooling systems.

Key Players and Industry Leaders

Some of the leading players in the global edge data center market include:

365 Data Centers

Eaton Corporation plc

EdgeConneX Inc.

Vertiv Group Corp.

Reichle & De-Massari (R&M)

Dätwyler IT Infra GmbH

L&T Smart World

Siemon

Rittal GmbH & Co. KG

H5 Data Centers

NEXTDC LTD.

These companies are investing heavily in R&D and strategic collaborations to expand their edge capabilities, enhance service offerings, and cater to new markets.

Recent Developments

November 2022: 365 Data Centers acquired Sungard Availability Services’ U.S. colocation and network operations, expanding its footprint in high-growth edge markets.

April 2022: EdgeConneX acquired Indonesia’s GTN to develop a 90MW data center in Jakarta, highlighting the growing edge data center demand in Southeast Asia.

January 2022: RailTel Corp. announced its plan to build 102 edge data centers across India to promote digital transformation in underdeveloped regions.

Market Opportunities

The proliferation of autonomous vehicles opens new frontiers for edge data centers. An autonomous car can generate up to 5 TB of data per hour, necessitating real-time processing capabilities only edge facilities can offer. According to MIT (2022), over 30 million autonomous vehicles are already on the roads globally, a number that will increase exponentially.

Similarly, the growth of eSports and gaming platforms, which require ultra-low latency, will boost the demand for local data processing units. Industrial automation and smart manufacturing further contribute to the rising demand for edge data infrastructure.

Preview essential insights and takeaways from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=79151

Future Outlook

With businesses and governments increasing their focus on digital transformation, the edge data center market is expected to witness widespread adoption across industries. The combination of 5G, AI, IoT, and cloud computing is expected to shape the future of decentralized data management.

Companies are likely to prioritize edge data centers to ensure compliance with data localization regulations, optimize service delivery, and maintain high-security standards.

By 2031, the edge data center industry will play a crucial role in reshaping the global data processing ecosystem, especially as the number of connected devices continues to rise.

Market Segmentation

By Component:

Solutions

Services

Designing & Consulting

Implementation & Integration

Support & Maintenance

By Enterprise Size:

SMEs

Large Enterprises

By Industry:

BFSI

IT & Telecom

Healthcare

Manufacturing

Automotive

Others

By Region:

North America

Europe

Asia Pacific

Middle East & Africa

South America

Regional Insights

North America currently dominates the global edge data center market, led by the U.S., which boasts high internet penetration, advanced telecom infrastructure, and robust digital consumption.

Asia Pacific is projected to register the fastest CAGR through 2031, driven by increasing 5G deployment, digital business expansion, and the presence of major tech hubs in countries like China, India, and Japan.

Europe follows closely with significant investments in edge technologies to support the growing demand for smart cities and Industry 4.0 initiatives.

Why Buy This Report?

Gain insights into a market poised to grow at a CAGR of 22.1%

Understand emerging trends, technological advancements, and opportunities

Analyze competitive landscape with detailed company profiles

Evaluate the impact of regional growth trends on market performance

Identify potential investment areas and target customer segments

This comprehensive analysis helps stakeholders make informed strategic decisions based on in-depth market intelligence.

Frequently Asked Questions (FAQs)

1. What is the current size of the global edge data center market? The market was valued at US$ 9.7 Bn in 2022.

2. What is the projected market size by 2031? The edge data center market is expected to reach US$ 57.8 Bn by 2031.

3. What is the CAGR for the forecast period 2023–2031? The market is anticipated to grow at a CAGR of 22.1%.

4. Which region leads the global edge data center market? North America dominates the market due to its mature technology landscape and early adoption of edge computing.

5. What are the key factors driving market growth? Rising demand for low-latency data processing, streaming services, 5G expansion, IoT device proliferation, and AI-based applications.

6. Who are the key players in the market? Major players include 365 Data Centers, EdgeConneX, Eaton, Vertiv, H5 Data Centers, and NEXTDC LTD.

Explore Latest Research Reports by Transparency Market Research: 3D Modeling, 3D Visualization, and 3D Data Capture Market: https://www.transparencymarketresearch.com/3d-modeling-3d-visualization-and-3d-data-capture-market.html

IT Asset Disposition (ITAD) Market: https://www.transparencymarketresearch.com/it-asset-disposition-market.html

Identity-as-a-Service (IDaaS) Market: https://www.transparencymarketresearch.com/identity-as-a-service-market.html

Point-of-Sale [POS] Terminal Market: https://www.transparencymarketresearch.com/point-of-sale-terminals-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Cloud Networking Market Innovation Surges as Businesses Prioritize Scalable Secure Cloud Network Solutions

The cloud networking market is undergoing a significant transformation, driven by the increasing demand for scalable, agile, and cost-efficient networking solutions. Cloud networking refers to the use of cloud-based services and infrastructure to manage and deliver network functions such as connectivity, security, and performance management. As enterprises continue to embrace digital transformation, cloud networking has become a foundational component in achieving operational efficiency, innovation, and competitiveness.

Market Overview

The global cloud networking market has seen rapid growth in recent years. This expansion is primarily fueled by the proliferation of cloud-based applications, the shift towards hybrid and multi-cloud environments, and the rising need for improved network agility and automation. Organizations are moving away from traditional on-premises networking models and investing in cloud-native networking solutions that offer on-demand scalability and centralized control.

Key industry players such as Cisco, Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and IBM are continuously innovating and expanding their cloud networking portfolios. These companies are integrating artificial intelligence (AI), machine learning (ML), and automation capabilities into their networking services, which has enhanced network visibility, threat detection, and overall performance.

Market Drivers

Several critical factors are propelling the growth of the cloud networking market:

Increased Adoption of Cloud Services: As more businesses migrate their workloads to the cloud, the demand for secure and reliable cloud networking infrastructure continues to rise.

Remote Work and BYOD Trends: The global shift to remote and hybrid work environments has underscored the need for scalable cloud networking that supports seamless access to resources from any location or device.

Edge Computing and IoT Integration: The rise of edge computing and Internet of Things (IoT) devices has led to the need for decentralized networking models, further increasing the demand for cloud-based network management tools.

Security and Compliance Requirements: Modern cloud networking solutions offer enhanced security features, including network segmentation, zero-trust models, and compliance monitoring, making them ideal for organizations in regulated industries.

AI and Automation Integration: The integration of AI and automation into cloud networking platforms is enabling predictive analytics, self-healing networks, and automated troubleshooting, which reduce operational costs and enhance user experiences.

Market Segmentation

The cloud networking market can be segmented based on:

Deployment Type: Public cloud, private cloud, and hybrid cloud.

Component: Solutions (e.g., SD-WAN, cloud routers, cloud firewalls) and services (e.g., consulting, integration).