#techcabal

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Kazakhstan’s Minister of Communications and Informatics has blocked the Tumblr site because it contained 60 sites of terrorism, extremism, and pornography in 2015.

Text

كيفية تفعيل اقتصاد المعرفة والإبداع في إفريقيا وأوروبا؟

ما هذه المجموعة من المختارات تسألني؟ إنّها عددٌ من أعداد نشرة “صيد الشابكة” اِعرف أكثر عن النشرة هنا: ما هي نشرة “صيد الشابكة” ما مصادرها، وما غرضها؛ وما معنى الشابكة أصلًا؟! 🎣🌐هل تعرف ما هي صيد الشابكة وتطالعها بانتظام؟ اِدعم استمرارية النشرة بطرق شتى من هنا: 💲 طرق دعم نشرة صيد الشابكة. 🎣🌐 صيد الشابكة العدد #145 السلام عليكم؛ مرحبًا وبسم الله؛ بخصوص العنوان فهو في قسم من الأقسام أدناه. 🎣🌐 صيد…

#145#Chain-of-Thought (CoT)#ChatGPT#Copilot and Gab AI#Fayetteville State University#Hannatu Musa Musawa#Lennart Meincke#Mario Draghi#MIT Technology Review#Musashino University#Pieter Levels#Risa Aihara#Robert W. McGee#SMARTBRIEF#SSRN#Storythings#TC Daily#TechCabal#Thrillist#University of Pennsylvania; The Wharton School#موقع Thrillist#نشرة Storythings

0 notes

Text

👨🏿🚀TechCabal Daily - Coup in Gabon overthrows Bongo

Happy pre-Friday! ICYMI: Today’s the last day our referral prorgamme will be available. We’re shutting down the programme. We’ll dispense all unclaimed rewards by September 30, so if you’ve qualify for one, we’ll be in touch shortly. Gabon military declares military coup Gabon army officers. Image source: Yenisafak Gabon is borrowing inspiration from Niger. Soldiers in the Central African…

View On WordPress

0 notes

Text

👨🏿🚀TechCabal Daily – Starlink is live (again) in Kenya

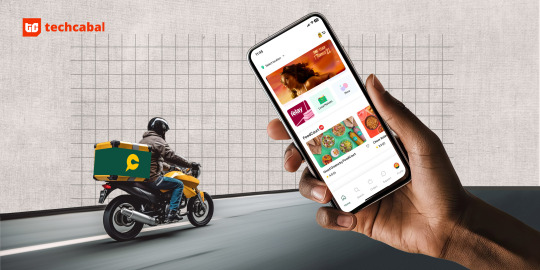

Chowdeck app/Image Source: TechCabal Since 2024, Chowdeck has crossed 1 million users, expanded to more cities across Nigeria, integrated AI services in its customer service operations, and expanded its operations to Ghana. And now? Nigeria-born on-demand YC-backed delivery platform has acquired Mira, the point-of-sale startup founded in 2023. The amount of the deal? Undisclosed. But what’s…

View On WordPress

0 notes

Text

Fidelity Bank Returns to Trillion-Naira Market Cap as Share Price Hits ₦21

Fidelity Bank Plc has reclaimed its place among Nigeria’s elite trillion-naira companies. This comes after a 5.3% rise in its share price, from ₦19.95 to ₦21.00, on May 13, 2025. According to the Nigerian Exchange Limited (NGX), this development brings the number of companies with market capitalisation above ₦1 trillion to 19. Fluctuations and Investor Sentiment As reported by TechCabal, Fidelity…

0 notes

Text

CBN fines Moniepoint and OPay ₦1 Billion each as Nigeria tightens fintech regulation

In a continuation of the Central Bank of Nigeria’s (CBN) increased scrutiny of fintech startups, two of the country’s most prominent unicorns, Moniepoint and OPay, were fined ₦1 billion each in the second quarter of 2024, sources with direct knowledge of the matter told TechCabal. While several other fintech companies were also penalized, the two firms were the hardest hit. The penalties…

0 notes

Text

GTBank Website has been hacked? Recent reports suggested that the temporary outage of Guaranty Trust Bank's (GTBank) website was caused by a cybersecurity breach. However, new information indicates that the issue was more likely due to a delay in renewing the bank's domain name, rather than a hack. The website was offline from Tuesday night until early Thursday morning as the bank's IT teams scrambled to resolve the problem. Four individuals familiar with the situation revealed to TechCabal that the outage was linked to issues with the Domain Name System (DNS) configuration. A Chief Technology Officer (CTO) at one of Nigeria's major fintech companies, speaking anonymously, suggested that GTBank's failure to renew its domain name may have been the root cause of the disruption. GTBank Website Has Been Hacked "There were issues with their domain name registration, and they had to make some changes or move it to a different domain name service," the CTO explained. The delay in renewing the domain name might have opened the door for unknown parties to attempt to purchase the domain, hoping that GTBank would pay a premium to reclaim it. However, experts believe that if GTBank had already patented its website name, it could report the issue to the domain host and retrieve the site after following the necessary procedures—a process that could take time. Domain name renewal lapses are not uncommon. Even tech giants like Google and Microsoft have faced similar issues in the past. In 2015, Google failed to renew "google.com," which was briefly purchased by a former employee. Microsoft also experienced a similar lapse with the hotmail.co.uk domain in 2003. GTBank Website hacked by Hackers? One developer speculated that the delay in GTBank's domain renewal might have been caused by internal issues, such as the custodian of the email tied to the domain leaving the bank without properly handing over responsibilities. Additionally, the bureaucratic process of vendor payment might have further delayed the renewal. GTBank Website Has Been Hacked: What We Know Now As of the time of publication, some GTBank customers were able to access the website, while others continued to experience difficulties. These issues could be related to DNS propagation, which can cause delays in the changes to domain records taking effect across all servers. Another factor could be the security feature known as HTTP Strict Transport Security (HSTS), which forces browsers to connect to the website only over a secure, encrypted connection—a standard practice among banks to protect customer information. GTBank has yet to release an official statement regarding the incident. However, the outage serves as a reminder of the importance of timely domain name renewals and the potential complications that can arise from lapses in this critical area.

0 notes

Text

Exclusive: Flutterwave’s Olugbenga Agboola speaks on FW 3.0, IPO plans, and upgrading Barter

While GB was unclear about a timeline for an IPO for Flutterwave, he said the company’s current goal is digital market expansion.

At the Kauffman Fellows event held in Nairobi this week, TechCabal spoke with Olugbenga Agboola, the CEO of Flutterwave. This publication shared several questions for him, including the state of its products, such as Barter and Send app, and we are posting them here verbatim to fully understand what the company has been up to and what it has planned for the coming days.

You talked about Flutterwave 3.0 a few years ago, which included several business segments. How is Flutterwave structured today, and what are your business segments?

GB: Flutterwave 3.0 was our evolution into a suite of products that would solve actual problems for consumers, Small and Medium Businesses (SMBs) and companies in Africa. We are looking at problems and basically identifying solutions. For example, when we launched the Send app, a remittance product, we made sending money anywhere in the world easier. But that is one problem but we also launched Swap. Swap is already in Nigeria and helps an average Nigerian who wants to swap currencies, from Naira to dollar, to be able to do so directly.

READ MORE: Breaking: Backed by CBN, Flutterwave’s new product Swap wants to solve Nigeria’s FX problems

And that’s our business. We help the average African business, both SMBs and enterprises or global corporations, to scale. 3.0 is when we structured the company into a suite of products where we can aggressively solve problems facing Africans in the African market.

What markets/countries does Flutterwave currently operate in? And what are your key markets?

GB: So, in Kenya, we are a tech platform. We have partners in Kenya that we process payments with, like Uber. We have seen an opportunity in Kenya and are scaling here. Our scaling is in line with regulations and all the required processes. Our primary markets are Nigeria, South Africa, Egypt and Kenya. Our strategic markets are Rwanda, Ghana, Cameroon, Cote d’Ivoire and Senegal.

What is your fastest-growing business segment and country at the moment?

GB: Literally everything is growing very fast. Send app is growing at over 100%, and our portfolio of business is growing massively. So we have been growing massively YoY now.

Barter is Flutterwave’s consumer-facing product focused on remittances, but you’re pushing a separate international payments app with a sleek design and faster payouts. Is Flutterwave going to deprecate Barter?

Well, we used to have a product called Barter. However, currently, it is in an upgrade phase. We want to build a new product to make Barter even more efficient, so we are working on that.

How is Flutterwave Send performing? And what growth metrics can you share?

Send app is growing at over 100 percent. Literally. It has been around, and we launched a new corridor from India to Africa and vice versa.

Flutterwave plans to list on the stock market. Considering the market momentum in recent weeks, what signal will you consider before finalizing your IPO plans? Ballpark on the same?

GB: When it is time, we will let you know for sure. Currently, we focus on customers, revenue, experience, and digital market expansion.

Flutterwave dismissed the allegations of fraud in Kenya, yet overall, statements from the regulator show the company faces a somewhat hostile environment in the country. How much progress has Flutterwave made to strengthen its relationship with the anti-graft agency and the CBK?

GB: The said issues have been addressed, even the ARA (Assets and Recovery Agency) issue, which is good. This is just proof of the proper governance within the company. ARA would not have found us free of every charge if we didn’t have a great infrastructure. We also scaling the team here with Leon Kiptum ( SVP of East Africa) here in Kenya. We are scaling the company and bringing the right people on board, and we are doing everything to scale and grow.

Congrats on receiving the name approval in Kenya from the CBK.

GB: Yes, it is a step towards getting the licence. The first step is getting name approval, and that has been done, which is a very massive step. So very very soon, we should be having a licence.

TC: Bosun Tijani, the Nigerian minister, is a prominent name in the Nigerian/African tech industry. How important is his ministerial selection to Flutterwave and the Nigerian tech industry?

GB: Bosun’s appointment is amazing for Nigeria and the tech ecosystem. He has the experience and has walked the walk. On the government side, building policies is the best thing that can happen in Nigeria, and the country is very lucky to have Bosun. And I am very proud to have someone who has worked with us before.

#olugbengaagboola#payments#paymentsprocesssing#flutterwave#olugbengagboola#flutterwaveceo#coding#fintech#hacking#nigeria

1 note

·

View note

Text

Fintech: The digital key to spotting new markets - Journal Important Online - BLOGGER https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156475&_unique_id=66b199e6a9df3 This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking. In Rwanda, the

recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg BLOGGER - #GLOBAL This article was contributed to TechCabal by Leila Rwagasana. Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic … Read More

0 notes

Text

🧈 الخلاصة: صُنَّاع المحتوى يبنون اقتصادًا جديدًا

ما هذه المجموعة من المختارات تسألني؟ إنّها عددٌ من أعداد نشرة “صيد الشابكة” اِعرف أكثر عن النشرة هنا: ما هي نشرة “صيد الشابكة” ما مصادرها، وما غرضها؛ وما معنى الشابكة أصلًا؟! 🎣🌐 🎣🌐 صيد الشابكة العدد #30 صح فطوركم يا قوم! 🎖️🔎 وفق Ahrefs* -أداة عالمية لتحسين محركات البحث- وعند البحث بعبارة “أسعار كتابة المحتوى” يأتي مقالي حاسبة أسعار كتابة المحتوى النصي [منتج رقمي جديد]** ضمن نتائج البحث العشر…

View On WordPress

#LinkedIn News#LinkedIn News Middle East#Mark Angel#Olufemi Oguntamu#skitmaker#skitmakers#TC Daily#TechCabal#مكتب تنسيق التعريب بالرباط#مجتمع رديف#محمد اليامي#نيجيريا#نشرة 5/3/2 البريدية#نشرة TC Daily#هشام فرج#اقتصاد منشئ المحتوى#اقتصاد المعرفة#اقتصاد صناع المحتوى#المنظمة العربية للتربية والثقافة والعلوم (الألكسو)#الألكسو#التسويق بالفقاعة#دعوة من من أخبار لينكدإن الشرق الأوسط (LinkedIn News Middle East)#رديف

0 notes

Text

Fintech: The digital key to spotting new markets - Journal Important Online https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156474&_unique_id=66b198d02d59c This article was contributed to Tec... BLOGGER - #GLOBAL This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking.

In Rwanda, the recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg #GLOBAL - BLOGGER This article was contributed to TechCabal by Leila Rwagasana. Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic … Read More

0 notes

Text

Starlink reopens sign-ups in Nairobi after 7-month pause

After more than seven months of blocking new users, Starlink is taking fresh sign-ups in Nairobi and other parts of Kenya. Its coverage map now shows availability in key towns, and at least three users told TechCabal they’ve managed to activate their kits this month. “It can be installed anywhere in Kenya right now,” said Isaac Migiro, a customer in Nairobi who purchased a kit in December and…

View On WordPress

0 notes

Text

Fintech: The digital key to spotting new markets - Journal Important Online https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156472&_unique_id=66b198ce518d5 #GLOBAL - BLOGGER BLOGGER This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking.

In Rwanda, the recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg This article was contributed to TechCabal by Leila Rwagasana. Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic … Read More

0 notes

Text

Fintech: The digital key to spotting new markets - Journal Important Online - #GLOBAL https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156471&_unique_id=66b198cd5e8db This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking. In Rwanda, the

recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg BLOGGER - #GLOBAL

0 notes

Text

One week after Nigeria’s Federal Competition and Consumer Protection Commission (FCCPC) fined WhatsApp $220 million for a data privacy violation, the commission's additional demands could lead to WhatsApp suspending operations in the country. At least four people familiar with the matter said Meta was considering "withdrawing certain services" in Nigeria. FCCPC also asked WhatsApp to stop sharing user data with other Facebook companies and third parties without explicit consent. The social media platform must also provide information about data collection and restore user control over data usage. "We want to be really clear that technically, based on the order, it would be impossible to provide WhatsApp in Nigeria or globally," a spokesperson for WhatsApp told TechCabal via email. "This order contains multiple inaccuracies and misrepresents how WhatsApp works. WhatsApp relies on limited data to run our service and keep users safe, and it would be impossible to provide WhatsApp in Nigeria or globally without Meta’s infrastructure. We are urgently appealing the order to avoid any impact on users," the statement added. Meta did not comment on the FCCPC’s claim that WhatsApp did not allow users to opt out of the 2021 policy. However, it insisted that its January 2021 Privacy Policy update does not include sharing user data. "While traditionally mobile carriers and operators store this information, we believe that keeping these records for two billion users would be both a privacy and security risk and we don’t do it," the privacy document reads. If WhatsApp ceases operations in Nigeria, it will have enormous consequences for individuals and small business owners. Many SMEs rely on WhatsApp, Instagram, and Facebook to reach their target customers. Three privacy lawyers questioned the FCCPC’s reference to the National Data Protection Regulation (NDPR) as a basis for the fine. Enacted in 2019 by the National Information Technology Development Agency (NITDA), NDPR is the primary data protection framework in Nigeria. Two lawyers who asked not to be named say the NDPR will not stand up to scrutiny in court and questioned if a government regulation could be authoritative in a matter as significant as privacy. While Meta is undoubtedly subject to regulatory oversight, the proportionality of the $220 million fine levied by the FCCPC is questionable, two government figures who asked not to be named said. "We are too revenue-focused. What is the opportunity cost of $220 million in government coffers?" asked an industry expert. If WhatsApp ceases operating in Nigeria over these demands, the FCCPC and the Nigerian government will have their answer.

0 notes

Text

Flutterwave CEO wins Fintech of the Year at African Banker Awards

Flutterwave, Africa’s most valuable startup, has been named ‘Fintech of the Year’ at the African Banker Awards in recognition of its contributions to the financial technology sector in Africa. The award celebrates Flutterwave and other companies and individuals setting new standards of innovation and contributing to the growth and development of Africa’s banking sector over the past year.

The award is Flutterwave’s third international recognition in 2024 after the fintech giant was included in CNBC’s Disruptor 50 list and Fast Company’s Most Innovative Companies.

Although it remains unclear when Flutterwave will IPO, the awards might lend credence to Flutterwave’s ambitions to go public. The fintech company has been linked to an initial public offering since August 2023, when Olugbenga Agboola, its CEO, disclosed that the fintech would forge ahead with its 2022 IPO plans. The fintech has also recently changed up its executive team after several high-profile exits in recent months.

“We are incredibly honoured to receive this prestigious award,” said Agboola, in a statement seen by TechCabal.

The award ceremony took place last night at the JW Marriott Hotel in Nairobi, Kenya, where over 300 of Africa’s leading figures in banking and finance were attending the African Banker Awards gala.

“This recognition is a testament to the hard work, dedication, and creativity of the entire team at Flutterwave. It also reaffirms our mission to simplify payments for endless possibilities, and we remain committed to building solutions that enable multinationals to expand in and within Africa, and also supporting African companies to compete globally,” an excerpt from the statement read.

Flutterwave also received approval in principle for a payment aggregator licence from the Central Bank of Mozambique today as it looks to expand into the southeastern African region. The licence, if approved, will allow Flutterwave to support businesses expanding into Mozambique and global enterprises expanding into Africa.

Flutterwave’s key business is processing online payments, enabling international businesses like Uber to accept payments from African businesses and customers. The fintech allows these businesses and multinationals to accept various forms of payments, like mobile money, card payments, and bank transfers.

#olugbengaagboola#payments#paymentsprocesssing#flutterwave#olugbengagboola#flutterwaveceo#coding#fintech#hacking#nigeria

1 note

·

View note

Text

Flutterwave lays off 3% of its workforce as it doubles down on enterprise and remittance

African payments giant Flutterwave has laid off about 30 people—around 3% of its workforce—three months after it spoke about repositioning its business to focus on remittance and enterprise, its two biggest revenue drivers. That change of focus led to the shutdown of Barter in March.

Flutterwave confirmed the layoffs to TechCabal but did not share specific details of the affected teams.

“After a thorough analysis of our strategic priorities, including a renewed focus on enterprise customers and remittances, we came to the conclusion that some roles within the organisation are redundant,” Flutterwave told TechCabal in a statement.

Employees were told about the layoffs at a town hall on Monday afternoon, two people with direct knowledge of the matter said. The impacted roles are connected to products the company is no longer pursuing, one person said.

“We will pay an average 3 months of gross salary, depending on the country where the employee is based,” Flutterwave said. “We will also be monetising their unutilised accrued leave days.”

In October, the fintech told TechCabal that enterprise was its biggest revenue driver while retail products had little contribution to revenues.

“Since our founding eight years ago, we have not had to implement a workforce reduction plan, but it became a necessary step in this instance in order to align our current resources with our go-forward strategy and improve our operational efficiency.”

After reshuffling some of its C-suite employees in 2024, Flutterwave revived conversations about a potential public listing that was put on ice in 2022 and 2023.

“Right now our goal is to be IPO-ready, ensuring we have the right corporate governance in place, making sure we are operating well,” CEO Gbenga Agboola told Semafor in April 2024. “We want to be a long-term company in Africa, for Africa – and so the goal is building the right infrastructure to be here for the next ten-plus years

1 note

·

View note