Statistics

We looked inside some of the posts by vtechviral and here's what we found interesting.

Average Info

Notes Per Post

0

Likes Per Post

0

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

11 days

Number of Posts By Type

Text

17

Last Seen Tumblr Blogs

Fun Fact

In February 2021, Tumblr had 518.6 million blog accounts.

Text

Introduction to AI's Evolution: A Historical Overview of AI Development

Early Beginnings: The Conceptual Foundations of AI The conceptual foundations of artificial intelligence (AI) trace back to philosophical inquiries into the nature of thought and intelligence. Philosophers such as Aristotle pondered the mechanistic aspects of reasoning, laying an early groundwork for the idea of machine intelligence. These initial musings set the stage for more concrete…

0 notes

Text

The Basics of Bond Investing Long-Term

Introduction Investing in bonds can be a smart long-term strategy for individuals looking to diversify their investment portfolios and generate steady income. Bonds are debt securities issued by governments, municipalities, and corporations to raise capital. In this blog post, we will explore the basics of bond investing for the long term, including the benefits, risks, and key considerations. The Benefits of Bond Investing Bond investing offers several advantages for long-term investors: - Steady Income: Bonds pay regular interest payments, known as coupon payments, which provide investors with a steady income stream. - Capital Preservation: Bonds are generally considered less volatile than stocks, making them a more conservative investment option for preserving capital. - Diversification: Including bonds in an investment portfolio can help diversify risk and reduce overall portfolio volatility. - Predictable Returns: Bonds have fixed maturity dates, allowing investors to plan for future cash flows and estimate returns. Risks and Considerations While bond investing offers many benefits, it is important to be aware of the risks involved: - Interest Rate Risk: Bond prices are inversely related to interest rates. When interest rates rise, bond prices fall, and vice versa. Long-term bond investors should be prepared for potential fluctuations in bond prices. - Credit Risk: Bonds issued by entities with lower credit ratings carry a higher risk of default. Investors should carefully assess the creditworthiness of the bond issuer before investing. - Inflation Risk: Inflation erodes the purchasing power of future bond income. Long-term investors should consider the potential impact of inflation on their bond investments. - Liquidity Risk: Some bonds may have limited liquidity, making it difficult to sell them at a desired price. Investors should be aware of the liquidity of the bonds they choose to invest in. Types of Bonds There are various types of bonds available for long-term investors: - Government Bonds: Issued by national governments, these bonds are generally considered low-risk and offer stable returns. - Municipal Bonds: Issued by local governments or municipalities, these bonds are often tax-exempt and can be attractive for investors in higher tax brackets. - Corporate Bonds: Issued by corporations, these bonds offer higher yields but carry higher credit risk compared to government or municipal bonds. - Treasury Inflation-Protected Securities (TIPS): These bonds are designed to protect investors against inflation by adjusting the principal value based on changes in the Consumer Price Index. Long-Term Bond Investing Strategies Here are some strategies to consider when investing in bonds for the long term: - Ladder Strategy: This strategy involves diversifying investments across bonds with different maturity dates. By spreading investments, investors can mitigate the risk of interest rate fluctuations. - Buy and Hold: Investors can choose to buy individual bonds and hold them until maturity, ensuring a predictable stream of income. - Bond Funds: Investing in bond mutual funds or exchange-traded funds (ETFs) allows investors to gain exposure to a diversified portfolio of bonds managed by professionals. Conclusion Bond investing can be a valuable long-term investment strategy for those seeking steady income and capital preservation. By understanding the benefits, risks, and different types of bonds available, investors can make informed decisions and create a well-rounded investment portfolio. Remember to consult with a financial advisor to determine the best bond investment strategy based on your individual financial goals and risk tolerance. Read the full article

0 notes

Text

Lifestyle Inflation: Avoiding the Trap as Your Income Grows

As your income grows, it's only natural to want to enjoy the fruits of your labor. You may be tempted to upgrade your lifestyle, buy a bigger house, or splurge on luxury items. This phenomenon is known as lifestyle inflation, and while it may seem harmless at first, it can quickly become a trap that hinders your financial well-being in the long run. What is Lifestyle Inflation? Lifestyle inflation refers to the tendency of individuals to increase their spending as their income rises. It's a common occurrence that can happen to anyone, regardless of their income level. When people earn more money, they often feel the need to spend more, which can lead to a cycle of continuously increasing expenses. For example, let's say you get a promotion and a significant raise at work. Suddenly, you find yourself with more disposable income. You might decide to buy a new car, move into a bigger house, or dine at fancy restaurants more frequently. While these choices may bring temporary happiness, they can also create a financial burden that becomes difficult to sustain. The Dangers of Lifestyle Inflation While it's natural to want to enjoy the benefits of your hard work, lifestyle inflation can have several negative consequences: 1. Increased Debt: When you start spending more money, you may find yourself relying on credit cards or loans to maintain your lifestyle. This can lead to a cycle of debt that becomes increasingly difficult to break free from. 2. Limited Savings: As your expenses increase, it becomes harder to save money for emergencies, retirement, or other long-term financial goals. This lack of savings can leave you vulnerable to unexpected expenses or financial hardships in the future. 3. Reduced Financial Freedom: Lifestyle inflation can create a situation where you are dependent on your income to maintain your lifestyle. This can limit your ability to explore new opportunities, take risks, or make career changes that may lead to greater fulfillment or higher income potential. Avoiding the Lifestyle Inflation Trap While it's important to enjoy the benefits of your hard work, it's equally crucial to avoid falling into the lifestyle inflation trap. Here are some strategies to help you maintain financial stability: 1. Set Financial Goals: Define your financial goals and prioritize them. Whether it's saving for retirement, paying off debt, or starting a business, having clear goals will help you stay focused and avoid unnecessary expenses. 2. Create a Budget: Develop a budget that aligns with your financial goals. Track your income and expenses to ensure that you're living within your means and saving for the future. 3. Delay Gratification: Avoid impulsive purchases and practice delayed gratification. Give yourself time to evaluate whether a purchase is necessary or if it aligns with your long-term financial goals. 4. Avoid Comparisons: Avoid comparing your lifestyle to others. Just because someone else can afford a certain lifestyle doesn't mean you need to as well. Focus on your own financial well-being and what brings you true happiness. 5. Invest Wisely: Instead of spending all your extra income, consider investing it wisely. Explore opportunities such as stocks, real estate, or retirement accounts that can help grow your wealth over time. 6. Practice Gratitude: Take time to appreciate what you already have. Cultivating a sense of gratitude can help you find contentment in the present moment and reduce the desire for unnecessary material possessions. Conclusion Lifestyle inflation can be a tempting trap, but with careful planning and self-awareness, it's possible to avoid its negative consequences. By setting clear financial goals, creating a budget, and practicing delayed gratification, you can maintain financial stability and enjoy a fulfilling life without falling into the lifestyle inflation trap. Read the full article

0 notes

Text

Creating a Will: A Step-by-Step Guide

Creating a will is an essential step in ensuring that your assets are distributed according to your wishes after your passing. While the thought of planning for the end of life can be daunting, having a will in place can provide peace of mind and help avoid potential conflicts among your loved ones. This step-by-step guide will walk you through the process of creating a will. Step 1: Determine Your Assets and Debts The first step in creating a will is to take stock of your assets and debts. This includes your bank accounts, investments, real estate, vehicles, personal belongings, and any outstanding loans or debts. Having a clear understanding of your financial situation will help you make informed decisions about how you want your assets to be distributed. Step 2: Choose an Executor An executor is the person responsible for carrying out the instructions in your will. It is important to choose someone you trust and who is willing to take on this responsibility. Your executor should be organized, detail-oriented, and capable of handling the legal and financial aspects of settling your estate. Step 3: Decide on Beneficiaries Next, you need to determine who will inherit your assets. This may include family members, friends, or charitable organizations. Be sure to consider any special circumstances or needs of your beneficiaries, such as minor children or individuals with disabilities. Step 4: Outline Your Wishes Now it's time to outline your wishes in your will. This includes specifying how you want your assets to be distributed among your beneficiaries. You may also want to include any specific instructions for the care of minor children, the disposal of personal belongings, or the establishment of trusts. Step 5: Consult with an Attorney While it is possible to create a will on your own, it is highly recommended to consult with an attorney who specializes in estate planning. They can provide valuable guidance and ensure that your will is legally valid and properly executed. An attorney can also help you navigate complex issues such as tax implications and the distribution of assets in multiple jurisdictions. Step 6: Sign and Store Your Will Once your will is complete, it must be signed in the presence of witnesses. The requirements for valid witnesses may vary depending on your jurisdiction, so be sure to follow the legal guidelines. After signing, store your will in a safe and easily accessible place, such as a fireproof safe or with your attorney. Step 7: Review and Update Regularly Creating a will is not a one-time event. It is important to regularly review and update your will to reflect any changes in your circumstances or wishes. Major life events such as marriage, divorce, the birth of a child, or the acquisition of significant assets should prompt a review of your will to ensure it remains accurate and up to date. Conclusion Creating a will is a crucial part of estate planning. By following this step-by-step guide, you can ensure that your assets are distributed according to your wishes and minimize the potential for disputes among your loved ones. Remember to consult with an attorney to ensure that your will is legally valid and properly executed. Regularly reviewing and updating your will is essential to keep it current and reflective of your changing circumstances. Read the full article

0 notes

Text

Financial Literacy for College Students

As a college student, managing your finances can be a daunting task. It's important to develop financial literacy skills early on to ensure a secure financial future. This blog post will provide you with essential tips and advice on how to become financially literate while studying in college. 1. Create a Budget One of the first steps toward financial literacy is creating a budget. Start by listing your sources of income, such as part-time jobs or scholarships, and then outline your monthly expenses. This will help you understand where your money is going and how much you can save. Stick to your budget and make adjustments as needed. 2. Track Your Expenses Keep track of your expenses by recording them in a spreadsheet or using a budgeting app. This will give you a clear picture of your spending habits and help you identify areas where you can cut back. By being aware of your expenses, you can make informed decisions about your finances. 3. Save for Emergencies Unexpected expenses can arise at any time, so it's important to have an emergency fund. Set aside a portion of your income each month and build up a savings cushion. This will provide you with peace of mind and protect you from financial stress in case of emergencies. 4. Understand Student Loans If you have student loans, it's crucial to understand the terms and conditions. Familiarize yourself with the interest rates, repayment plans, and any deferment or forgiveness options available. Make a plan to pay off your loans efficiently and avoid unnecessary debt. 5. Avoid Credit Card Debt Credit cards can be useful tools, but they can also lead to debt if not used responsibly. Avoid accumulating credit card debt by only charging what you can afford to pay off each month. Pay your credit card bills on time to maintain a good credit score. 6. Seek Financial Education Take advantage of the financial education resources available to you. Many colleges offer workshops or courses on personal finance. Additionally, there are numerous online resources, books, and podcasts that can help you improve your financial literacy. Educate yourself and stay informed about financial topics. 7. Plan for the Future While it may seem far off, it's never too early to start planning for your future. Consider your long-term financial goals, such as buying a house or starting a business. Start saving and investing early to take advantage of compound interest and secure your financial future. 8. Seek Professional Advice If you're unsure about your financial decisions, don't hesitate to seek professional advice. Financial advisors can provide guidance tailored to your specific situation and help you make informed choices. They can assist you with budgeting, investing, and planning for major life events. 9. Be Mindful of Student Discounts As a college student, take advantage of the various student discounts available to you. Many retailers, restaurants, and entertainment venues offer discounted rates for students. Be mindful of these opportunities and save money whenever possible. 10. Practice Self-Control Lastly, practice self-control when it comes to your spending. Avoid impulsive purchases and think carefully before making big financial decisions. By developing self-discipline, you'll be able to make wise financial choices and build a solid foundation for your future. By following these tips and developing financial literacy skills, you'll be well-equipped to navigate the financial challenges of college life and beyond. Remember, it's never too early to start building a strong financial foundation. Read the full article

0 notes

Text

Balancing Risk and Reward in Investing

Investing is a crucial aspect of financial planning and wealth creation. Whether you're a seasoned investor or just starting out, finding the right balance between risk and reward is essential. In this blog post, we will explore the importance of balancing risk and reward in investing and provide some tips to help you navigate this delicate balance. The Relationship between Risk and Reward When it comes to investing, risk and reward go hand in hand. Generally, the higher the potential reward, the higher the risk involved. This means that while some investments may offer the possibility of significant returns, they also come with a higher chance of loss. On the other hand, safer investments may offer more stability but with lower returns. Understanding the relationship between risk and reward is crucial for making informed investment decisions. It's important to assess your risk tolerance and financial goals before diving into any investment opportunity. A high-risk investment might be suitable for someone with a higher risk tolerance and a longer investment horizon, while a low-risk investment might be more appropriate for someone with a lower risk tolerance and a shorter time frame. Diversification: Spreading Out the Risk One effective strategy for balancing risk and reward is diversification. Diversifying your investment portfolio means spreading out your investments across different asset classes, sectors, and geographic regions. By doing so, you reduce the impact of any single investment on your overall portfolio. Diversification helps to mitigate risk by ensuring that if one investment performs poorly, others may offset the losses. For example, if you have investments in stocks, bonds, and real estate, a decline in the stock market may be offset by gains in the bond market or real estate sector. This approach can help smooth out the ups and downs of the market and potentially enhance your overall returns. Research and Due Diligence Another crucial aspect of balancing risk and reward in investing is conducting thorough research and due diligence. It's important to understand the fundamentals of any investment opportunity before committing your hard-earned money. Research can involve analyzing financial statements, understanding market trends, and evaluating the track record of the investment manager or company. By doing your homework, you can gain valuable insights into the potential risks and rewards associated with a particular investment. Additionally, seeking professional advice from financial advisors or investment experts can provide you with an objective perspective and help you make more informed decisions. Setting Realistic Expectations When it comes to investing, it's essential to set realistic expectations. While we all dream of high returns and quick profits, it's important to remember that investing involves risks and uncertainties. Avoid falling into the trap of chasing after hot investment trends or trying to time the market. Instead, focus on long-term goals and develop a disciplined investment approach. By setting realistic expectations and staying committed to your investment strategy, you can better manage the risks and rewards associated with investing. Regular Monitoring and Review Lastly, balancing risk and reward requires regular monitoring and review of your investment portfolio. Markets are dynamic, and economic conditions can change quickly. It's important to stay informed and make adjustments to your portfolio as needed. Regularly reviewing your investments allows you to assess their performance, identify any potential risks, and make necessary adjustments. This proactive approach can help you maintain the desired balance between risk and reward and ensure that your investment strategy remains aligned with your financial goals. Conclusion Investing involves finding the right balance between risk and reward. By understanding the relationship between the two, diversifying your portfolio, conducting thorough research, setting realistic expectations, and regularly monitoring your investments, you can navigate the world of investing with greater confidence. Remember, investing is a long-term journey, and it's important to stay focused on your financial goals while managing the risks along the way. With a balanced approach, you can maximize your chances of achieving your investment objectives and securing your financial future. Read the full article

0 notes

Text

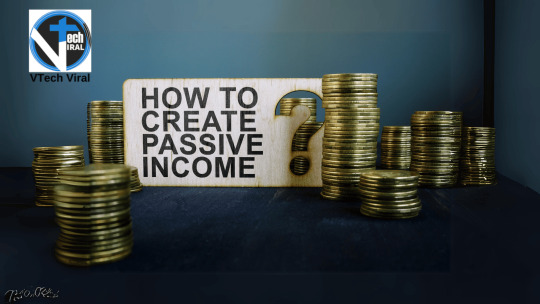

Passive Income Streams: How to Get Started

Introduction Passive income is a term that has gained popularity in recent years, and for good reason. It offers the potential to earn money while you sleep, giving you the freedom to pursue your passions and live life on your own terms. In this blog post, we will explore the concept of passive income streams and discuss how you can get started on your journey to financial freedom. What is Passive Income? Passive income is income that is earned with little to no effort on your part. Unlike active income, where you trade your time and skills for money, passive income allows you to earn money on a recurring basis without the need for constant work or supervision. It is a way to make your money work for you. Types of Passive Income Streams There are several different types of passive income streams that you can explore. Here are a few popular options: 1. Rental Properties Investing in rental properties can be a lucrative way to generate passive income. By purchasing properties and renting them out to tenants, you can earn a steady stream of rental income each month. While there may be some initial work involved in finding and managing tenants, rental properties have the potential to provide a consistent source of passive income. 2. Dividend Stocks Investing in dividend stocks is another way to generate passive income. Dividend stocks are shares of companies that distribute a portion of their profits to shareholders on a regular basis. By investing in dividend stocks, you can earn passive income through regular dividend payments. 3. Peer-to-Peer Lending Peer-to-peer lending platforms allow you to lend money to individuals or businesses in exchange for interest payments. By diversifying your lending portfolio and carefully selecting borrowers, you can earn passive income through the interest payments you receive. 4. Affiliate Marketing Affiliate marketing is a popular method for earning passive income online. By promoting products or services on your website or social media platforms and earning a commission on each sale or lead generated, you can create a passive income stream. With the right strategies and audience targeting, affiliate marketing can be a highly profitable venture. 5. Digital Products If you have a skill or expertise in a particular area, you can create and sell digital products such as e-books, online courses, or software. Once you have created the product, it can be sold repeatedly without requiring additional work on your part, allowing you to earn passive income. Getting Started with Passive Income Now that you have an understanding of the different types of passive income streams, here are some steps to help you get started: 1. Set Financial Goals Define your financial goals and determine how much passive income you would like to earn. Having a clear goal in mind will help you stay motivated and focused on your journey to financial freedom. 2. Research and Choose the Right Passive Income Stream Take the time to research and evaluate different passive income streams. Consider your interests, skills, and resources to determine which option is the best fit for you. Remember to consider the level of effort required, potential returns, and any associated risks. 3. Create a Plan Develop a plan for how you will generate passive income. This may include setting up a real estate investment strategy, building an affiliate marketing website, or creating and marketing your digital products. Outline the necessary steps and create a timeline to keep yourself accountable. 4. Take Action Once you have a plan in place, it's time to take action. Start implementing your strategies and be prepared to learn and adapt along the way. Building passive income takes time and effort, but the rewards can be well worth it. 5. Monitor and Optimize Regularly monitor your passive income streams and make adjustments as needed. Keep track of your earnings, expenses, and any changes in the market or industry. By staying proactive and optimizing your strategies, you can maximize your passive income potential. Conclusion Creating passive income streams is a powerful way to achieve financial independence and live life on your own terms. By exploring different options, setting clear goals, and taking consistent action, you can start building passive income streams that will provide you with financial security and freedom in the long run. Remember, it's never too late to get started on your journey to passive income. Read the full article

0 notes

Text

The Basics of Bond Investing Long-Term

Introduction Investing in bonds can be a smart long-term strategy for individuals looking to diversify their investment portfolios and generate steady income. Bonds are debt securities issued by governments, municipalities, and corporations to raise capital. In this blog post, we will explore the basics of bond investing for the long term, including the benefits, risks, and key considerations. The Benefits of Bond Investing Bond investing offers several advantages for long-term investors: - Steady Income: Bonds pay regular interest payments, known as coupon payments, which provide investors with a steady income stream. - Capital Preservation: Bonds are generally considered less volatile than stocks, making them a more conservative investment option for preserving capital. - Diversification: Including bonds in an investment portfolio can help diversify risk and reduce overall portfolio volatility. - Predictable Returns: Bonds have fixed maturity dates, allowing investors to plan for future cash flows and estimate returns. Risks and Considerations While bond investing offers many benefits, it is important to be aware of the risks involved: - Interest Rate Risk: Bond prices are inversely related to interest rates. When interest rates rise, bond prices fall, and vice versa. Long-term bond investors should be prepared for potential fluctuations in bond prices. - Credit Risk: Bonds issued by entities with lower credit ratings carry a higher risk of default. Investors should carefully assess the creditworthiness of the bond issuer before investing. - Inflation Risk: Inflation erodes the purchasing power of future bond income. Long-term investors should consider the potential impact of inflation on their bond investments. - Liquidity Risk: Some bonds may have limited liquidity, making it difficult to sell them at a desired price. Investors should be aware of the liquidity of the bonds they choose to invest in. Types of Bonds There are various types of bonds available for long-term investors: - Government Bonds: Issued by national governments, these bonds are generally considered low-risk and offer stable returns. - Municipal Bonds: Issued by local governments or municipalities, these bonds are often tax-exempt and can be attractive for investors in higher tax brackets. - Corporate Bonds: Issued by corporations, these bonds offer higher yields but carry higher credit risk compared to government or municipal bonds. - Treasury Inflation-Protected Securities (TIPS): These bonds are designed to protect investors against inflation by adjusting the principal value based on changes in the Consumer Price Index. Long-Term Bond Investing Strategies Here are some strategies to consider when investing in bonds for the long term: - Ladder Strategy: This strategy involves diversifying investments across bonds with different maturity dates. By spreading investments, investors can mitigate the risk of interest rate fluctuations. - Buy and Hold: Investors can choose to buy individual bonds and hold them until maturity, ensuring a predictable stream of income. - Bond Funds: Investing in bond mutual funds or exchange-traded funds (ETFs) allows investors to gain exposure to a diversified portfolio of bonds managed by professionals. Conclusion Bond investing can be a valuable long-term investment strategy for those seeking steady income and capital preservation. By understanding the benefits, risks, and different types of bonds available, investors can make informed decisions and create a well-rounded investment portfolio. Remember to consult with a financial advisor to determine the best bond investment strategy based on your individual financial goals and risk tolerance. Read the full article

0 notes

Text

Lifestyle Inflation: Avoiding the Trap as Your Income Grows

As your income grows, it's only natural to want to enjoy the fruits of your labor. You may be tempted to upgrade your lifestyle, buy a bigger house, or splurge on luxury items. This phenomenon is known as lifestyle inflation, and while it may seem harmless at first, it can quickly become a trap that hinders your financial well-being in the long run. What is Lifestyle Inflation? Lifestyle inflation refers to the tendency of individuals to increase their spending as their income rises. It's a common occurrence that can happen to anyone, regardless of their income level. When people earn more money, they often feel the need to spend more, which can lead to a cycle of continuously increasing expenses. For example, let's say you get a promotion and a significant raise at work. Suddenly, you find yourself with more disposable income. You might decide to buy a new car, move into a bigger house, or dine at fancy restaurants more frequently. While these choices may bring temporary happiness, they can also create a financial burden that becomes difficult to sustain. The Dangers of Lifestyle Inflation While it's natural to want to enjoy the benefits of your hard work, lifestyle inflation can have several negative consequences: 1. Increased Debt: When you start spending more money, you may find yourself relying on credit cards or loans to maintain your lifestyle. This can lead to a cycle of debt that becomes increasingly difficult to break free from. 2. Limited Savings: As your expenses increase, it becomes harder to save money for emergencies, retirement, or other long-term financial goals. This lack of savings can leave you vulnerable to unexpected expenses or financial hardships in the future. 3. Reduced Financial Freedom: Lifestyle inflation can create a situation where you are dependent on your income to maintain your lifestyle. This can limit your ability to explore new opportunities, take risks, or make career changes that may lead to greater fulfillment or higher income potential. Avoiding the Lifestyle Inflation Trap While it's important to enjoy the benefits of your hard work, it's equally crucial to avoid falling into the lifestyle inflation trap. Here are some strategies to help you maintain financial stability: 1. Set Financial Goals: Define your financial goals and prioritize them. Whether it's saving for retirement, paying off debt, or starting a business, having clear goals will help you stay focused and avoid unnecessary expenses. 2. Create a Budget: Develop a budget that aligns with your financial goals. Track your income and expenses to ensure that you're living within your means and saving for the future. 3. Delay Gratification: Avoid impulsive purchases and practice delayed gratification. Give yourself time to evaluate whether a purchase is necessary or if it aligns with your long-term financial goals. 4. Avoid Comparisons: Avoid comparing your lifestyle to others. Just because someone else can afford a certain lifestyle doesn't mean you need to as well. Focus on your own financial well-being and what brings you true happiness. 5. Invest Wisely: Instead of spending all your extra income, consider investing it wisely. Explore opportunities such as stocks, real estate, or retirement accounts that can help grow your wealth over time. 6. Practice Gratitude: Take time to appreciate what you already have. Cultivating a sense of gratitude can help you find contentment in the present moment and reduce the desire for unnecessary material possessions. Conclusion Lifestyle inflation can be a tempting trap, but with careful planning and self-awareness, it's possible to avoid its negative consequences. By setting clear financial goals, creating a budget, and practicing delayed gratification, you can maintain financial stability and enjoy a fulfilling life without falling into the lifestyle inflation trap. Read the full article

0 notes

Text

Creating a Will: A Step-by-Step Guide

Creating a will is an essential step in ensuring that your assets are distributed according to your wishes after your passing. While the thought of planning for the end of life can be daunting, having a will in place can provide peace of mind and help avoid potential conflicts among your loved ones. This step-by-step guide will walk you through the process of creating a will. Step 1: Determine Your Assets and Debts The first step in creating a will is to take stock of your assets and debts. This includes your bank accounts, investments, real estate, vehicles, personal belongings, and any outstanding loans or debts. Having a clear understanding of your financial situation will help you make informed decisions about how you want your assets to be distributed. Step 2: Choose an Executor An executor is the person responsible for carrying out the instructions in your will. It is important to choose someone you trust and who is willing to take on this responsibility. Your executor should be organized, detail-oriented, and capable of handling the legal and financial aspects of settling your estate. Step 3: Decide on Beneficiaries Next, you need to determine who will inherit your assets. This may include family members, friends, or charitable organizations. Be sure to consider any special circumstances or needs of your beneficiaries, such as minor children or individuals with disabilities. Step 4: Outline Your Wishes Now it's time to outline your wishes in your will. This includes specifying how you want your assets to be distributed among your beneficiaries. You may also want to include any specific instructions for the care of minor children, the disposal of personal belongings, or the establishment of trusts. Step 5: Consult with an Attorney While it is possible to create a will on your own, it is highly recommended to consult with an attorney who specializes in estate planning. They can provide valuable guidance and ensure that your will is legally valid and properly executed. An attorney can also help you navigate complex issues such as tax implications and the distribution of assets in multiple jurisdictions. Step 6: Sign and Store Your Will Once your will is complete, it must be signed in the presence of witnesses. The requirements for valid witnesses may vary depending on your jurisdiction, so be sure to follow the legal guidelines. After signing, store your will in a safe and easily accessible place, such as a fireproof safe or with your attorney. Step 7: Review and Update Regularly Creating a will is not a one-time event. It is important to regularly review and update your will to reflect any changes in your circumstances or wishes. Major life events such as marriage, divorce, the birth of a child, or the acquisition of significant assets should prompt a review of your will to ensure it remains accurate and up to date. Conclusion Creating a will is a crucial part of estate planning. By following this step-by-step guide, you can ensure that your assets are distributed according to your wishes and minimize the potential for disputes among your loved ones. Remember to consult with an attorney to ensure that your will is legally valid and properly executed. Regularly reviewing and updating your will is essential to keep it current and reflective of your changing circumstances. Read the full article

0 notes

Text

Financial Literacy for College Students

As a college student, managing your finances can be a daunting task. It's important to develop financial literacy skills early on to ensure a secure financial future. This blog post will provide you with essential tips and advice on how to become financially literate while studying in college. 1. Create a Budget One of the first steps toward financial literacy is creating a budget. Start by listing your sources of income, such as part-time jobs or scholarships, and then outline your monthly expenses. This will help you understand where your money is going and how much you can save. Stick to your budget and make adjustments as needed. 2. Track Your Expenses Keep track of your expenses by recording them in a spreadsheet or using a budgeting app. This will give you a clear picture of your spending habits and help you identify areas where you can cut back. By being aware of your expenses, you can make informed decisions about your finances. 3. Save for Emergencies Unexpected expenses can arise at any time, so it's important to have an emergency fund. Set aside a portion of your income each month and build up a savings cushion. This will provide you with peace of mind and protect you from financial stress in case of emergencies. 4. Understand Student Loans If you have student loans, it's crucial to understand the terms and conditions. Familiarize yourself with the interest rates, repayment plans, and any deferment or forgiveness options available. Make a plan to pay off your loans efficiently and avoid unnecessary debt. 5. Avoid Credit Card Debt Credit cards can be useful tools, but they can also lead to debt if not used responsibly. Avoid accumulating credit card debt by only charging what you can afford to pay off each month. Pay your credit card bills on time to maintain a good credit score. 6. Seek Financial Education Take advantage of the financial education resources available to you. Many colleges offer workshops or courses on personal finance. Additionally, there are numerous online resources, books, and podcasts that can help you improve your financial literacy. Educate yourself and stay informed about financial topics. 7. Plan for the Future While it may seem far off, it's never too early to start planning for your future. Consider your long-term financial goals, such as buying a house or starting a business. Start saving and investing early to take advantage of compound interest and secure your financial future. 8. Seek Professional Advice If you're unsure about your financial decisions, don't hesitate to seek professional advice. Financial advisors can provide guidance tailored to your specific situation and help you make informed choices. They can assist you with budgeting, investing, and planning for major life events. 9. Be Mindful of Student Discounts As a college student, take advantage of the various student discounts available to you. Many retailers, restaurants, and entertainment venues offer discounted rates for students. Be mindful of these opportunities and save money whenever possible. 10. Practice Self-Control Lastly, practice self-control when it comes to your spending. Avoid impulsive purchases and think carefully before making big financial decisions. By developing self-discipline, you'll be able to make wise financial choices and build a solid foundation for your future. By following these tips and developing financial literacy skills, you'll be well-equipped to navigate the financial challenges of college life and beyond. Remember, it's never too early to start building a strong financial foundation. Read the full article

0 notes

Text

Balancing Risk and Reward in Investing

Investing is a crucial aspect of financial planning and wealth creation. Whether you're a seasoned investor or just starting out, finding the right balance between risk and reward is essential. In this blog post, we will explore the importance of balancing risk and reward in investing and provide some tips to help you navigate this delicate balance. The Relationship between Risk and Reward When it comes to investing, risk and reward go hand in hand. Generally, the higher the potential reward, the higher the risk involved. This means that while some investments may offer the possibility of significant returns, they also come with a higher chance of loss. On the other hand, safer investments may offer more stability but with lower returns. Understanding the relationship between risk and reward is crucial for making informed investment decisions. It's important to assess your risk tolerance and financial goals before diving into any investment opportunity. A high-risk investment might be suitable for someone with a higher risk tolerance and a longer investment horizon, while a low-risk investment might be more appropriate for someone with a lower risk tolerance and a shorter time frame. Diversification: Spreading Out the Risk One effective strategy for balancing risk and reward is diversification. Diversifying your investment portfolio means spreading out your investments across different asset classes, sectors, and geographic regions. By doing so, you reduce the impact of any single investment on your overall portfolio. Diversification helps to mitigate risk by ensuring that if one investment performs poorly, others may offset the losses. For example, if you have investments in stocks, bonds, and real estate, a decline in the stock market may be offset by gains in the bond market or real estate sector. This approach can help smooth out the ups and downs of the market and potentially enhance your overall returns. Research and Due Diligence Another crucial aspect of balancing risk and reward in investing is conducting thorough research and due diligence. It's important to understand the fundamentals of any investment opportunity before committing your hard-earned money. Research can involve analyzing financial statements, understanding market trends, and evaluating the track record of the investment manager or company. By doing your homework, you can gain valuable insights into the potential risks and rewards associated with a particular investment. Additionally, seeking professional advice from financial advisors or investment experts can provide you with an objective perspective and help you make more informed decisions. Setting Realistic Expectations When it comes to investing, it's essential to set realistic expectations. While we all dream of high returns and quick profits, it's important to remember that investing involves risks and uncertainties. Avoid falling into the trap of chasing after hot investment trends or trying to time the market. Instead, focus on long-term goals and develop a disciplined investment approach. By setting realistic expectations and staying committed to your investment strategy, you can better manage the risks and rewards associated with investing. Regular Monitoring and Review Lastly, balancing risk and reward requires regular monitoring and review of your investment portfolio. Markets are dynamic, and economic conditions can change quickly. It's important to stay informed and make adjustments to your portfolio as needed. Regularly reviewing your investments allows you to assess their performance, identify any potential risks, and make necessary adjustments. This proactive approach can help you maintain the desired balance between risk and reward and ensure that your investment strategy remains aligned with your financial goals. Conclusion Investing involves finding the right balance between risk and reward. By understanding the relationship between the two, diversifying your portfolio, conducting thorough research, setting realistic expectations, and regularly monitoring your investments, you can navigate the world of investing with greater confidence. Remember, investing is a long-term journey, and it's important to stay focused on your financial goals while managing the risks along the way. With a balanced approach, you can maximize your chances of achieving your investment objectives and securing your financial future. Read the full article

0 notes

Text

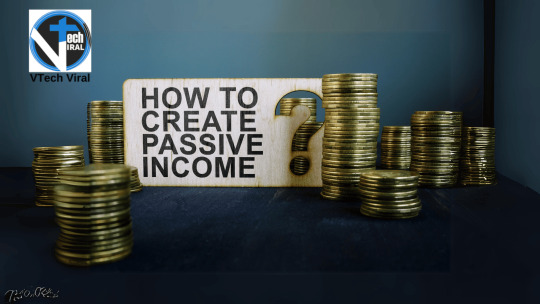

Passive Income Streams: How to Get Started

Introduction Passive income is a term that has gained popularity in recent years, and for good reason. It offers the potential to earn money while you sleep, giving you the freedom to pursue your passions and live life on your own terms. In this blog post, we will explore the concept of passive income streams and discuss how you can get started on your journey to financial freedom. What is Passive Income? Passive income is income that is earned with little to no effort on your part. Unlike active income, where you trade your time and skills for money, passive income allows you to earn money on a recurring basis without the need for constant work or supervision. It is a way to make your money work for you. Types of Passive Income Streams There are several different types of passive income streams that you can explore. Here are a few popular options: 1. Rental Properties Investing in rental properties can be a lucrative way to generate passive income. By purchasing properties and renting them out to tenants, you can earn a steady stream of rental income each month. While there may be some initial work involved in finding and managing tenants, rental properties have the potential to provide a consistent source of passive income. 2. Dividend Stocks Investing in dividend stocks is another way to generate passive income. Dividend stocks are shares of companies that distribute a portion of their profits to shareholders on a regular basis. By investing in dividend stocks, you can earn passive income through regular dividend payments. 3. Peer-to-Peer Lending Peer-to-peer lending platforms allow you to lend money to individuals or businesses in exchange for interest payments. By diversifying your lending portfolio and carefully selecting borrowers, you can earn passive income through the interest payments you receive. 4. Affiliate Marketing Affiliate marketing is a popular method for earning passive income online. By promoting products or services on your website or social media platforms and earning a commission on each sale or lead generated, you can create a passive income stream. With the right strategies and audience targeting, affiliate marketing can be a highly profitable venture. 5. Digital Products If you have a skill or expertise in a particular area, you can create and sell digital products such as e-books, online courses, or software. Once you have created the product, it can be sold repeatedly without requiring additional work on your part, allowing you to earn passive income. Getting Started with Passive Income Now that you have an understanding of the different types of passive income streams, here are some steps to help you get started: 1. Set Financial Goals Define your financial goals and determine how much passive income you would like to earn. Having a clear goal in mind will help you stay motivated and focused on your journey to financial freedom. 2. Research and Choose the Right Passive Income Stream Take the time to research and evaluate different passive income streams. Consider your interests, skills, and resources to determine which option is the best fit for you. Remember to consider the level of effort required, potential returns, and any associated risks. 3. Create a Plan Develop a plan for how you will generate passive income. This may include setting up a real estate investment strategy, building an affiliate marketing website, or creating and marketing your digital products. Outline the necessary steps and create a timeline to keep yourself accountable. 4. Take Action Once you have a plan in place, it's time to take action. Start implementing your strategies and be prepared to learn and adapt along the way. Building passive income takes time and effort, but the rewards can be well worth it. 5. Monitor and Optimize Regularly monitor your passive income streams and make adjustments as needed. Keep track of your earnings, expenses, and any changes in the market or industry. By staying proactive and optimizing your strategies, you can maximize your passive income potential. Conclusion Creating passive income streams is a powerful way to achieve financial independence and live life on your own terms. By exploring different options, setting clear goals, and taking consistent action, you can start building passive income streams that will provide you with financial security and freedom in the long run. Remember, it's never too late to get started on your journey to passive income. Read the full article

0 notes

Text

The Basics of Bond Investing Long-Term

Introduction Investing in bonds can be a smart long-term strategy for individuals looking to diversify their investment portfolios and generate steady income. Bonds are debt securities issued by governments, municipalities, and corporations to raise capital. In this blog post, we will explore the basics of bond investing for the long term, including the benefits, risks, and key considerations. The Benefits of Bond Investing Bond investing offers several advantages for long-term investors: - Steady Income: Bonds pay regular interest payments, known as coupon payments, which provide investors with a steady income stream. - Capital Preservation: Bonds are generally considered less volatile than stocks, making them a more conservative investment option for preserving capital. - Diversification: Including bonds in an investment portfolio can help diversify risk and reduce overall portfolio volatility. - Predictable Returns: Bonds have fixed maturity dates, allowing investors to plan for future cash flows and estimate returns. Risks and Considerations While bond investing offers many benefits, it is important to be aware of the risks involved: - Interest Rate Risk: Bond prices are inversely related to interest rates. When interest rates rise, bond prices fall, and vice versa. Long-term bond investors should be prepared for potential fluctuations in bond prices. - Credit Risk: Bonds issued by entities with lower credit ratings carry a higher risk of default. Investors should carefully assess the creditworthiness of the bond issuer before investing. - Inflation Risk: Inflation erodes the purchasing power of future bond income. Long-term investors should consider the potential impact of inflation on their bond investments. - Liquidity Risk: Some bonds may have limited liquidity, making it difficult to sell them at a desired price. Investors should be aware of the liquidity of the bonds they choose to invest in. Types of Bonds There are various types of bonds available for long-term investors: - Government Bonds: Issued by national governments, these bonds are generally considered low-risk and offer stable returns. - Municipal Bonds: Issued by local governments or municipalities, these bonds are often tax-exempt and can be attractive for investors in higher tax brackets. - Corporate Bonds: Issued by corporations, these bonds offer higher yields but carry higher credit risk compared to government or municipal bonds. - Treasury Inflation-Protected Securities (TIPS): These bonds are designed to protect investors against inflation by adjusting the principal value based on changes in the Consumer Price Index. Long-Term Bond Investing Strategies Here are some strategies to consider when investing in bonds for the long term: - Ladder Strategy: This strategy involves diversifying investments across bonds with different maturity dates. By spreading investments, investors can mitigate the risk of interest rate fluctuations. - Buy and Hold: Investors can choose to buy individual bonds and hold them until maturity, ensuring a predictable stream of income. - Bond Funds: Investing in bond mutual funds or exchange-traded funds (ETFs) allows investors to gain exposure to a diversified portfolio of bonds managed by professionals. Conclusion Bond investing can be a valuable long-term investment strategy for those seeking steady income and capital preservation. By understanding the benefits, risks, and different types of bonds available, investors can make informed decisions and create a well-rounded investment portfolio. Remember to consult with a financial advisor to determine the best bond investment strategy based on your individual financial goals and risk tolerance. Read the full article

0 notes

Text

Debt Consolidation: Is It Right for You?

Introduction Debt can be a heavy burden to carry, causing stress and financial strain. If you find yourself juggling multiple debts and struggling to keep up with payments, debt consolidation might be a solution worth considering. In this article, we will explore what debt consolidation is, how it works, and whether it is the right option for you. What is Debt Consolidation? Debt consolidation is the process of combining multiple debts into a single loan or payment plan. Instead of making multiple payments to different creditors, you consolidate your debts into one monthly payment. This can simplify your financial situation and potentially lower your overall interest rate. How Does Debt Consolidation Work? There are several ways to consolidate your debts: 1. Debt Consolidation Loans A debt consolidation loan involves taking out a new loan to pay off your existing debts. This loan typically has a lower interest rate than your current debts, which can save you money in the long run. With a debt consolidation loan, you make a single monthly payment to the lender. 2. Balance Transfer Credit Cards If you have credit card debts, you can transfer the balances to a single credit card with a lower interest rate. This allows you to consolidate your debts onto one card and potentially save on interest charges. However, be cautious of any balance transfer fees and make sure you can pay off the balance before the promotional interest rate expires. 3. Home Equity Loans or Lines of Credit If you own a home, you may be able to use the equity you have built up to secure a loan or line of credit. This can be an effective way to consolidate your debts and take advantage of lower interest rates. However, it's important to remember that your home is used as collateral, and failure to make payments could result in the loss of your property. Is Debt Consolidation Right for You? While debt consolidation can be a useful tool for managing your debts, it may not be the right solution for everyone. Here are some factors to consider: 1. Your Financial Situation Debt consolidation is most beneficial for individuals with a steady income and the ability to make regular payments. It can provide relief by simplifying your finances and reducing the overall interest you pay. However, if you are struggling to make ends meet or have a history of missed payments, debt consolidation may not be the best option. 2. Interest Rates One of the primary advantages of debt consolidation is the potential for lower interest rates. Before pursuing consolidation, compare the interest rates of your current debts with the rates offered by consolidation options. If the rates are similar or higher, consolidation may not provide significant financial benefits. 3. Financial Discipline Debt consolidation can be a powerful tool for debt management, but it requires discipline. It is essential to avoid accumulating new debts while paying off the consolidated loan. Without proper financial discipline, you may find yourself in a worse situation than before. 4. Long-Term Financial Goals Consider your long-term financial goals before deciding on debt consolidation. If your goal is to become debt-free and improve your credit score, consolidation can be a step in the right direction. However, if you plan to make significant financial changes, such as starting a business or buying a home, it's important to assess how consolidation fits into your overall strategy. Conclusion Debt consolidation can be an effective tool for managing multiple debts and simplifying your financial situation. It can potentially lower your interest rates and provide a clear path towards becoming debt-free. However, it's important to carefully evaluate your financial situation and consider the long-term implications before deciding if debt consolidation is right for you. Consulting with a financial advisor can also provide valuable guidance in determining the best course of action. Read the full article

0 notes

Text

Protect Yourself: Avoiding Common Financial Scams and Frauds

Financial scams and frauds are unfortunately prevalent in today's world, targeting individuals and businesses alike. It is essential to be aware of these scams and take necessary precautions to protect yourself and your hard-earned money. Here are some tips to help you avoid falling victim to common financial scams and frauds. 1. Be Skeptical of Unsolicited Communications Whether it's a phone call, email, or text message, be cautious when dealing with unsolicited communications. Scammers often pose as legitimate organizations, such as banks or government agencies, to gain your trust. Never provide personal or financial information to anyone you don't know or trust. 2. Verify the Source Before sharing any sensitive information or making a financial transaction, verify the source. Double-check the email address or phone number, and independently search for the organization's official contact information. Legitimate businesses will never ask for your personal information through email or over the phone. 3. Protect Your Personal Information Keep your personal information, such as social security number, bank account details, and credit card information, secure. Be cautious when sharing personal information online, and only provide it on secure websites with a trusted connection. 4. Stay Informed Stay updated on the latest scams and frauds by regularly checking reputable sources, such as government websites and consumer protection agencies. Being well-informed will help you recognize red flags and avoid falling victim to new scamming techniques. 5. Use Strong Passwords Protect your online accounts by using strong and unique passwords. Avoid using easily guessable passwords or reusing the same password across multiple accounts. Consider using a password manager to securely store and generate complex passwords. 6. Be Wary of Investment Opportunities Exercise caution when approached with investment opportunities that promise high returns with little risk. Research and seek advice from trusted financial professionals before making any investment decisions. Remember, if it sounds too good to be true, it probably is. By following these tips and staying vigilant, you can significantly reduce the risk of falling victim to financial scams and frauds. Remember, it's always better to be cautious and verify before sharing any personal or financial information. Read the full article

0 notes

Text

Lifestyle Inflation: Avoiding the Trap as Your Income Grows

As your income grows, it's only natural to want to enjoy the fruits of your labor. You may be tempted to upgrade your lifestyle, buy a bigger house, or splurge on luxury items. This phenomenon is known as lifestyle inflation, and while it may seem harmless at first, it can quickly become a trap that hinders your financial well-being in the long run. What is Lifestyle Inflation? Lifestyle inflation refers to the tendency of individuals to increase their spending as their income rises. It's a common occurrence that can happen to anyone, regardless of their income level. When people earn more money, they often feel the need to spend more, which can lead to a cycle of continuously increasing expenses. For example, let's say you get a promotion and a significant raise at work. Suddenly, you find yourself with more disposable income. You might decide to buy a new car, move into a bigger house, or dine at fancy restaurants more frequently. While these choices may bring temporary happiness, they can also create a financial burden that becomes difficult to sustain. The Dangers of Lifestyle Inflation While it's natural to want to enjoy the benefits of your hard work, lifestyle inflation can have several negative consequences: 1. Increased Debt: When you start spending more money, you may find yourself relying on credit cards or loans to maintain your lifestyle. This can lead to a cycle of debt that becomes increasingly difficult to break free from. 2. Limited Savings: As your expenses increase, it becomes harder to save money for emergencies, retirement, or other long-term financial goals. This lack of savings can leave you vulnerable to unexpected expenses or financial hardships in the future. 3. Reduced Financial Freedom: Lifestyle inflation can create a situation where you are dependent on your income to maintain your lifestyle. This can limit your ability to explore new opportunities, take risks, or make career changes that may lead to greater fulfillment or higher income potential. Avoiding the Lifestyle Inflation Trap While it's important to enjoy the benefits of your hard work, it's equally crucial to avoid falling into the lifestyle inflation trap. Here are some strategies to help you maintain financial stability: 1. Set Financial Goals: Define your financial goals and prioritize them. Whether it's saving for retirement, paying off debt, or starting a business, having clear goals will help you stay focused and avoid unnecessary expenses. 2. Create a Budget: Develop a budget that aligns with your financial goals. Track your income and expenses to ensure that you're living within your means and saving for the future. 3. Delay Gratification: Avoid impulsive purchases and practice delayed gratification. Give yourself time to evaluate whether a purchase is necessary or if it aligns with your long-term financial goals. 4. Avoid Comparisons: Avoid comparing your lifestyle to others. Just because someone else can afford a certain lifestyle doesn't mean you need to as well. Focus on your own financial well-being and what brings you true happiness. 5. Invest Wisely: Instead of spending all your extra income, consider investing it wisely. Explore opportunities such as stocks, real estate, or retirement accounts that can help grow your wealth over time. 6. Practice Gratitude: Take time to appreciate what you already have. Cultivating a sense of gratitude can help you find contentment in the present moment and reduce the desire for unnecessary material possessions. Conclusion Lifestyle inflation can be a tempting trap, but with careful planning and self-awareness, it's possible to avoid its negative consequences. By setting clear financial goals, creating a budget, and practicing delayed gratification, you can maintain financial stability and enjoy a fulfilling life without falling into the lifestyle inflation trap. Read the full article

0 notes