Last Seen Blogs

nicodiangelo-we-stan

I post once a month

obsessionist

Obsessionist

sanne-sims4

Sanne-sims4

witheredbouquet

relinquish your pain unto me

maisblr

Untitled

Text

Before You Invest: 7 Critical Steps for a Solid Financial Foundation

Introduction

Ever wondered how some people seem to make their money grow effortlessly? It's not magic; it's strategy. Before you jump into the world of investments, there are crucial steps to take. Think of them as the sturdy base of a building – without it, the structure won't hold. These steps lay the groundwork for your financial future, ensuring stability and growth. Let's explore these fundamental steps together.

List of 7 Things You Must Do Before You Start Investing

Before diving into the world of investing, it's essential to lay down a clear roadmap of your financial aspirations.

Set Your Investment Goals:

Before you start investing, it's essential to have clear goals in mind. Question yourself what you want to accomplish with your investments. Are you saving for retirement, a house, or your children's education? Knowing your goals will help you determine your investment strategy and the level of risk you're willing to take.

Know Your Risk Level:

Comprehending your risk tolerance is critical for successful investing. It's essential to know how much volatility you can handle in your investments without feeling anxious or making hasty decisions. Assess your comfort level with risk by considering factors like your age, financial situation, and future goals.

Diversified Investment Portfolio Preparation:

Diversification is fundamental to handling risk in your investment portfolio. By spreading your investments across different asset classes, industries, and geographic regions, you can reduce the impact of market fluctuations on your overall portfolio performance. Building a diversified portfolio helps maximize returns while minimizing risk.

Fees and Expenses:

Before investing, it's important to understand the fees and expenses associated with different investment products. These costs can eat into your returns over time, so it's essential to choose investments with reasonable fees. Be sure to consider factors like management fees, trading commissions, and expense ratios when evaluating investment options.

Seek Professional Advice:

Investing can be complex, especially for beginners. Seeking advice from a financial advisor or investment professional can help you navigate the complexities of the market and make informed decisions. A professional can assess your financial situation, risk tolerance, and investment goals to create a personalized investment plan that aligns with your needs.

Getting Rid of Any Debts:

Before you start investing, it's wise to pay off high-interest debt, such as credit card balances or personal loans. High-interest debt can eat into your investment returns and hinder your financial progress. By prioritizing debt repayment, you can free up more money to invest and improve your overall financial health.

Having a Cash Emergency Fund:

Building an emergency fund is crucial before you start investing. An emergency fund provides a financial safety net, allowing you to cover unexpected expenses without resorting to high-interest debt or liquidating your investments. Aim to save enough to cover three to six months' worth of living expenses in a liquid, easily accessible account like a savings or money market account.

Conclusion:

In conclusion, laying the groundwork for your financial future is like building a sturdy bridge – each step is a vital support beam. By taking the time to prepare wisely before investing, you're strengthening your path to financial success. Remember, patience and diligence are your partners in this journey. So, arm yourself with knowledge, set your sights high, and step confidently into the world of investing.

0 notes

Text

youtube

SBI Securities: Stocks, MF, FNO - Apps on Google Play

Invest in stocks, IPOs, Mutual Funds & more with a Demat account. Download SBI Securities: Stocks,MF, FNO.

0 notes

Text

youtube

Mutual Funds SIP with SBI Securities | Invest in MF in India

SBI Securities - Invest systematically in professionally managed Mutual funds with SBI Securities. Get benefits from the power of compounding by investing in Mutual funds online in India.

0 notes

Text

Buy Equity - Online Equity Trading & Investment in India

Looking to invest in shares? SBI Securities offers a seamless online platform for equity investment in India. Begin your journey toward financial growth today!

0 notes

Text

SBI Securities: Stocks,MF, FNO - Apps on Google Play

Invest in stocks, IPOs, Mutual Funds & more with a Demat account. Download SBI Securities: Stocks,MF, FNO.

0 notes

Text

Home Loan for NRI in India | NRI Home Loan Interest Rates

SBI Realty provides NRI home loans at the best interest rates to own your dream home in India. Check interest rates, benefits and documents required.

0 notes

Text

SBI Securities: Stocks,MF, FNO on the App Store

Read reviews, compare customer ratings, see screenshots, and learn more about SBI Securities: Stocks,MF, FNO. Download SBI Securities: Stocks,MF, FNO and enjoy it on your iPhone, iPad, and iPod touch.

0 notes

Text

Mutual Funds SIP with SBI Securities | Invest in MF in India

SBI Securities - Invest systematically in professionally managed Mutual funds with SBI Securities. Get benefits from the power of compounding by investing in MF online in India.

0 notes

Text

Invest online in 54ec Capital gain bonds in India

Capital gain investment - Invest online in Capital Gain Bonds and save long-term capital gain tax. 54 EC CG Bonds issued by IRFC, PFC, REC, NHAI.

0 notes

Text

GST Reduction on Home Loan In 2024

GST reduction can reduce the cost of properties under construction and the cost of renovation of homes, so you can go for a lower amount of loan & pay less EMI.

0 notes

Text

youtube

SBI Securities: Stocks,MF, FNO on the App Store

Read reviews, compare customer ratings, see screenshots, and learn more about SBI Securities: Stocks, MF, FNO. Download SBI Securities: Stocks, MF, FNO and enjoy it on your iPhone, iPad, and iPod touch.

0 notes

Text

youtube

E-Margin Dare to Dream | SBI Securities

Enjoy the videos and music you love, upload original content, and share it all with friends, family, and the world on YouTube.

0 notes

Text

Capital Gains on Stocks, Mutual Funds & House Property

What is Capital Gains Tax?

Simply put, any profit or gains that arises from the sale of a “capital asset” is known “income from capital gains.” Such capital gains are taxable in the year in which the transfer of the capital asset takes place. This is called capital gains tax.

The rate of tax depends on whether it is a long-term capital gain (LTCG) or short-term capital gain (STCG).

But how do we decide whether the gain from the capital asset is long-term or short-term, and how the gains should be treated?

Holding Period for LTCG and Exceptions

The basic definition of long-term capital gains as per the Income Tax Act is any capital asset that has been held, at least, for a period of 36 months. However, there are certain exceptions to this rule.

There are some assets that are not classified as capital assets and hence are free of capital gains tax. This includes business inventory, household & personal effects, agricultural land in rural India, Gold Bonds 1977/1980, National Defence Gold Bonds 1980, Special Bearer Bonds 1991, Gold deposit scheme 1999 and Gold Monetization Scheme 2015. Here, the question of capital gains does not arise.

There is one asset class with a long-term asset classification of 24 months i.e., immovable properties like land, building and house property; effective from FY2017-18. This is only applicable for properties sold after 31-03-2017. Such assets would be classified as long-term asset if held for more than 24 months.

There is a specific set of assets where the definition of long-term capital gains is holding period of 12 months or more. This includes equity and preference shares of listed companies, listed debentures, equity oriented MFs of SEBI registered AMCs and zero-coupon bonds, whether listed or not. In all these cases, any holding above 1 year will be treated as long term capital gains.

The above assets are the exceptions. Apart from these, all the other assets will be subject to long term capital gains tax if held beyond 3 years, but subjected to short term capital gains tax if held below 3 years.

How are equities taxed?

There are multiple levels of taxation of capital gain in equity. When you invest in equities, you earn income from dividends, capital gains and from buyback of shares.

In the past, the dividends were initially exempt, later there was the dividend distribution tax (DDT) and then there were taxes at multiple levels. Now, all tax exemptions on dividend income have been removed effective the Finance Act 2020. Any dividend received by an individual during the year will be taxed as other income at the peak rate applicable; whether 10%, 20% or 30%.

What about capital gains tax on equities? In this case we have to classify capital gains into long-term and short-term capital gains tax.

Any equity share held for less than 12 months is a short-term capital asset and any equity share held more than 12 months is a long-term capital asset. Here are the tax implications.

In the case of short-term capital gains (sold before 12 months), the tax is levied at a concessional rate of 15%. This is much lower than other capital assets.

In the case of long-term capital gains (effective from April 01, 2018), there is a flat 10% tax levied on long term capital gains, above the threshold of Rs. 1,00,000 per year. Flat 10% tax means that there is no benefit of indexation available on long term capital gains on equities, even if you hold these shares for as long as 10 years.

Can losses be set off or carried forward? Short term capital loss on equities can be set off against both short-term gains or long-term capital gains.

Any outstanding losses can be carried forward for a period of 8 assessment years.

In the case of long-term losses on equity (effective from April 01, 2018), it can be set off against other long-term gains and also carried forward for 8 years. However, long term cannot be written off against short term gains.

What about speculative gains and losses (from intraday trading). In such cases, it is treated as speculative income and the peak tax rate is applied. However, the losses on speculation can only be set off against gains from speculation. Speculative losses can only be carried forward for a period of 4 assessment years.

All the above are subject to the condition that securities transaction tax (STT) is paid on these equities.

Finally, let us turn to the question – How is equity buyback taxed?

Effective the Union Budget 2020-21, when a company buys back shares using its free reserves, the tax incidence falls on the company. The company has to pay a tax of 23.296% (20% tax + 12% surcharge + 4% cess) on the difference between the buyback price and the issue price.

The buyback transaction is entirely tax-free in the hands of the shareholder.

How are mutual funds taxed?

For capital gains in mutual funds , the first classification to do is on the type of fund. Here are the 3 types of funds from a tax perspective. This is effective from Union Budget 2023-24.

Equity funds are the mutual funds that have more than 65% exposure to equity as an asset class. The remaining portion, less than 35%, can be in debt.

Non-Equity Hybrid Fund are the funds where the exposure to equity is more than 35% but less than 65%. This classification was made only in Budget 2023-24.

Finally, there are the pure debt funds and hybrid funds where the exposure to equity is less than 35% and are now treated at par with fixed deposits of banks in terms of tax treatment.

Let us now turn to how each of these categories are taxed.

Taxation of equity funds

In the case of equity funds, the treatment is the same as direct equities.

If the equity oriented fund is held for less than 12 months it is short term asset and taxed at flat 15% and does not form part of normal income tax.

If the equity fund is held for a period of more than 12 months, it is long term capital gain and taxed at 10% flat (without indexation). Any long-term capital gain below the threshold of Rs. 1,00,000 each year is exempt from tax.

Investors who prefer regular income in the form of dividends on equity funds can opt for the IDCW option. IDCW is treated as regular income for investors, it’s added to their total income for financial year. IDCW is taxed as per the applicable tax slab of the person. It is also subject to TDS deduction by the fund.

Taxation of non-equity hybrid funds

In the case of non-equity hybrid funds with equity exposure above 35% and below 65%, the tax treatment is as under.

Short term capital gains are defined as capital gains held for less than 36 months and are taxed as normal income as per the applicable tax slab.

Long term capital gains tax held for more than 36 months are taxed at 20% with the additional benefit of cost indexation. This reduces the tax liability to a greater extent.

Taxation of debt funds

In the case of debt funds with 100% in debt or hybrid funds with equity exposure less than 35%, both short-term and the long-term capital gains will be taxed at the applicable tax slab of the individual

Taxation of house property

As we stated earlier, capital gain in house property falls under the category of special assets that are treated as long term capital gains if held for over 24 months. Here is how it is taxed.

Short term capital gains on sale of house property is taxed as other income at the peak applicable rate, if sold before 24 months from date of registration.

Long term capital gains on sale of house property is taxed at a concessional rate of 20%, if held for more than 24 months. In addition, the indexation benefits are also made available.

However, there are some additional benefits available, to make such long-term capital gains from house property exempt from tax.

Under Section 54 of the Income Tax Act, if the sales proceeds of a house or land is reinvested in a new residential house, within a specified period, then capital gain is fully exempt, subject to holding the new asset for at least 3 years.

Under Section 54EC, if the sales proceeds from land or building is reinvested in specified infrastructure bonds of REC or NHAI, such gains will be exempt from long term capital gains tax, subject to holding the new asset for at least 5 years. However, you cannot invest more than a total of Rs. 50 lakhs in these bonds.

In conclusion, capital gains can be tricky and complex, but an in-depth understanding can make your actions tax-smart.

SOURCE URL: https://www.sbisecurities.in/blog/capital-gains-on-stocks-mutual-funds-house-property

0 notes

Text

SBI Home Loan: Apply for Home Loan in India

Apply for SBI home loan online in India at the lowest interest rates and easy EMI option. Make your dream home come to reality with the best housing loan in India.

0 notes

Text

Mutual Funds SIP with SBI Securities | Invest in MF in India

SBI Securities - Invest systematically in professionally managed Mutual funds with SBI Securities. Get benefits from the power of compounding by investing in MF online in India.

0 notes

Text

Invest online in 54ec Capital gain bonds in India

Capital gain investment - Invest online in Capital Gain Bonds and save long-term capital gain tax. 54 EC CG Bonds issued by IRFC, PFC, REC, and NHAI.

0 notes

Text

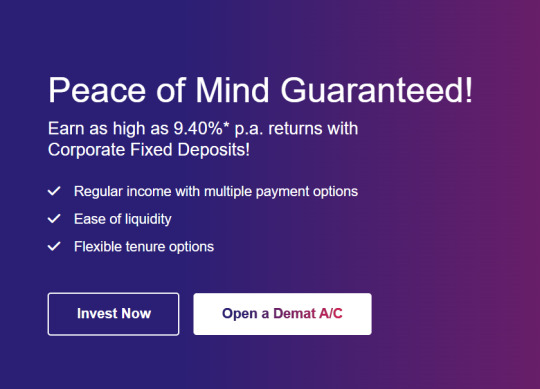

Corporate FD: Company Fixed Deposits in India

SBI Securities - Quickly search and invest in top CFDs and get assured interest rates. Corporate Fixed Deposits are ideal for earning fixed income.

0 notes