#Biomarker Solutions

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

Genomics Market - Forecast(2024 - 2030)

Global Genomic Market Overview:

A genome is the genetic material of an organism. It includes both the genes and the noncoding DNA, as well as mitochondrial DNA and chloroplast DNA. The study of genomes is called genomics. The genomics market is gaining traction owing to its applications in various fields of study such as intragenomic phenomenon including epistasis, pleiotropy, heterosis, and other interactions between loci and alleles within the genome. In this era of medical and life science innovations shaping itself as an inevitable uptake for sustainability of mankind, the genomic research is poised for exponential growth owing to imperative genetic innovations feeding off it. Abundant potential has driven this arcade to reach a staggering market size of $16 billion - $16.5 billion as of 2018, and the demand is estimated to increment at formidable CAGR of 9.2% to 10.2% during the forecast period of 2019 to 2025.

Request Sample

Global Genomic Market Outlook:

Genomics is extensively employed in healthcare, agriculture, biotechnology, DNA sequencing, and diagnostics. In the healthcare segment, genomics is used for the development of vaccines and drugs. This segment leads the application vertical and is growing with a CAGR of 10.1%-10.7 % through to 2025. Genomics plays a significant part in diagnosis of several genetic disorders. It has an ample scope in personalized medication as it can advocate a medical management constructed on the genetic face of a person with the help of clinical data and AI. It is also applied in synthetic biology and bioengineering. Genomics research in agriculture is hired for plant breeding and genetics to cultivate crop production. The understanding of gene function and the accessibility of genomic maps along with an enhanced understanding of genetic variant will aid the plant breeders to identify the traits and then manipulate those traits to obtain a high yield. All these factors affecting the enormous medical and agricultural sector are all set to stroke the genomics market with abundant demand.

Inquiry Before Buying

Global Genomic Market Growth Drivers:

As per the National Center for Biotechnology Information, U.S, the progression in oncology (study and treatment of tumor) expenses is forecast to rise 7%–10% annually throughout 2020, with universal oncology cost exceeding $150 billion[1]. As per the WHO, cancer is a leading cause of death worldwide, accounting for an estimated 9.6 million deaths in 2018[2]. And the total annual economic cost of cancer at the initial period of this decade was estimated at approximately $1.16 trillion. Thus the application of genomics in exploring cell-free circulating DNA by several R&D sectors as a potential biomarker for cancers is driving the market towards exponential growth. The genomics market with its current potential displays all the necessary traits it can adapt in the coming years to divert a huge chunk of traffic and revenue from the omnipresent cancer diagnostics.

As per the Food and Agriculture Organization of United Nations, between 1960 and 1990 the arable land increased by 1.5 billion ha, and in the recent past decades the elevation recorded is just 155 million ha[3]. With decreasing arable floor and the increasing global population augmenting the demand for food by 70% (by 2050), obtaining a high yield is a major trend in the agricultural sector. Genomics market is all set to capitalize on this unprecedented demand scenario. Genomics supplements the understanding of gene function and the accessibility of genomic maps along with an enhanced understanding of genetic variant, thus aiding the plant breeders to identify the traits and then manipulate those traits to obtain a high yield.

After an acute analysis of the regional insights of the global genomics market, North America is revealed to hold 39% to 40% of the entire global market size as of 2018. Such dominance can be attributed to several aspects such as cumulative investment on research by federal administrations, growing patient awareness, and accessibility of urbane healthcare facilities.

Schedule a Call

Global Genomics Market Players Perspective:

Some of other key players profiled in this IndustryARC business intelligence report are Beckton Dickson, Synthetic Genomics Inc. (SGI) ,Cepheid, Inc., Affymetrix, Inc., Bio-Rad Laboratories, Inc., Agilent Technologies, GE Healthcare, Illumina, Inc., Danaher Corporation,F. Hoffmann-La Roche, QIAGEN, Thermo Fisher Scientific and PacBio (Pacific Biosciences of California). Majority of the companies mentioned are situated in North America augmenting the regional affluence in the global market.

Global Genomics Market Trends:

High overload owing to a wide range of reagents and consumables has propelled companies into approving different policies to endure in the market and stay ahead of the curve.

For instance, in January 2017, BD launched Precise WTA Reagents for precise and guileless quantification of hereditary data form single cell analysis. Moreover, in July 2016, SGI-DNA entered into a distribution agreement with VWR International, an American company involved in the distribution of research laboratory products, with over 1,200,000 items to more than 250,000 customers in North America and Europe.

Genomics Market Research Scope

The base year of the study is 2018, with forecast done up to 2025. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. It also provides information on unit shipments. These provide the key market participants with the necessary business intelligence and help them understand the future of the Genomics Market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats. The key areas of focus include the types of equipment in the Genomics Market, and their specific applications in different phases of industrial operations.

Buy Now

Genomics Market Report: Industry Coverage

Types of Solutions Genomics Market:

By Product Types- Microarray chip, Sequencers.

By Application- Genotyping, SNP analysis.

By End-User- Anthropology, Diagnostics.

The Genomics Market report also analyzes the major geographic regions for the market as well as the major countries for the market in these regions. The regions and countries covered in the study include:

North America: The U.S., Canada, Mexico

South America: Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, Costa Rica

Europe: The U.K., Germany, Italy, France, The Netherlands, Belgium, Spain, Denmark

APAC: China, Japan, Australia, South Korea, India, Taiwan, Malaysia, Hong Kong

Middle East and Africa: Israel, South Africa, Saudi Arabia

#genomics#genomics market#genomics market size#genomics market share#genomics market value#genomics market report#DNA microarrays#Electrophoresis#X-Ray Crystallography#Polymerase Chain Reaction#DNA Sequencers#Chromatography#Bio-informatics Tools#Bio-informatics Database#DNA Sample Sequencing#SNPS Analysis#Molecular Biology#Gene Expression Analysis#Genotyping#Targeted Re-sequencing#Individual Genome Sequencing#Biomarker Solutions

0 notes

Text

Peter Ellman, President and CEO of Certis Oncology Solutions – Interview Series

New Post has been published on https://thedigitalinsider.com/peter-ellman-president-and-ceo-of-certis-oncology-solutions-interview-series/

Peter Ellman, President and CEO of Certis Oncology Solutions – Interview Series

Certis Oncology Solutions, led by Peter Ellman, President and CEO, is a life science technology company dedicated to realizing the promise of precision oncology. The company’s product is Oncology Intelligence® — highly predictive therapeutic response data derived from advanced cancer models. Certis partners with physician-scientists and industry researchers to expand access to precision oncology and address the critical translation gap between preclinical studies and clinical trials.

Can you describe the broader problem in oncology research that the CertisOI Assistant is addressing?

The failure rate of oncology investigational drug candidates is high. It was recently reported that in 2023, 90% of oncology programs ultimately failed. That figure is a remarkable improvement over the historical trend, which hovered around 96% until 2022. Considering the cost of developing drugs, a 90% failure rate is not sustainable. Imagine how patients would benefit if the success rate were even 50%.

CertisOI Assistant immediately addresses two really important issues that contribute to this failure rate:

Improved preclinical model selection: Many compounds show promising results in preclinical studies but fail to demonstrate a sufficient therapeutic effect in humans.Most members of the scientific community point to preclinical models as part of the problem. Choosing preclinical models with the correct gene expression signature (and using orthotopic engraftments for pivotal studies) can improve “translation” into the clinic.

Earlier, better biomarker identification: Relying on biomarkers that do not accurately predict therapeutic response can result in failed clinical trials. CertisOI Assistant is integrated with CertisAI, our patent-pending predictive AI/ML platform, enabling the identification of predictive biomarkers early in the drug development process.

How does the CertisOI Assistant use AI to improve access to oncology data, and what sets it apart from other AI tools in the field?

The CertisOI Assistant provides advanced data analysis and predictive modeling capabilities through an easy-to-use, natural language interface. It stands out in several ways:

Comprehensive Dataset Integration: The assistant integrates a wide range of oncology data, including patient information, tumor characteristics, genetic profiles, and drug response predictions. This holistic approach allows for a more comprehensive analysis than tools focusing on isolated data types.

AI-Based Predictions: The assistant employs AI algorithms to predict drug response and resistance, offering insights into which treatments will likely be effective for specific cancer models. This predictive capability is crucial for personalized medicine and sets it apart from tools that rely solely on historical data.

User-Friendly Interface: By providing an intuitive interface for querying and analyzing complex datasets, the assistant makes it easier for researchers to access and interpret oncology data without requiring advanced technical skills.

Focus on Pre-Clinical Models: The assistant specializes in pre-clinical oncology research, particularly PDX and cell line models, offering unique insights into early-stage drug development and tumor biology.

Interactive Visualizations: The assistant supports interactive visualizations, such as pharmacology and tumor growth studies, enabling researchers to explore data more engaging and informatively.

How does the tool transform complex data into actionable insights, especially for researchers working on drug sensitivity or genomic data?

CertisOI Assistant leverages a structured workflow to transform raw data into meaningful insights. It involves querying a comprehensive oncology dataset, analyzing the data, and presenting the results in a clear and interpretable format. Here’s how it works:

Data Querying: CertisOI Assistant can access a relational database containing detailed information about oncology models, including patient data, tumor characteristics, genomic data, and drug response predictions. It uses SQL-like queries to extract relevant data based on the researcher’s specific needs.

Data Analysis: Once the data is retrieved, CertisOI Assistant can perform various analyses, such as identifying common mutations, correlating gene expression with drug sensitivity, or evaluating pharmacology study results. It can also rank and filter data to highlight the most significant findings.

Visualization: The assistant can present data in tabular formats, generate interactive charts for pharmacology and tumor growth studies, and display histology images. This visualization helps researchers quickly grasp complex data patterns and relationships.

Interpretation and Insights: By providing a clear interpretation of the data, including predictions for drug sensitivity or resistance, CertisOI Assistant helps researchers make informed decisions about potential therapeutic strategies or further experimental directions.

Customization and Flexibility: Researchers can tailor their queries to focus on specific cancer types, genetic markers, or treatment responses, allowing for a highly customized analysis that aligns with their research objectives.

How does the CertisOI Assistant enhance researchers’ ability to select cancer models, design biomarker strategies, or perform in silico validations?

I covered the first two areas – the cancer model section and biomarker strategy design – at the outset of this interview, so I’ll focus on performing in silico validations. CertisOI Assistant provides a virtual environment to test and validate hypotheses related to drug efficacy, target engagement, and biomarker discovery without the need for immediate laboratory experiments. This allows them to rapidly refine their hypotheses and focus experimental efforts on the most promising avenues.

Here are a few examples:

Drug Response Predictions: Use AI-based predictions for drug response and resistance to assess how different models are likely to respond to specific drugs. This can help validate the potential efficacy of a drug in silico before moving to in vitro or in vivo studies.

Genomic and Molecular Profiling: Analyze the genomic data, including mutations, gene expression, and copy number variations, to identify potential targets and validate their relevance to the drug’s mechanism of action. This can help in understanding the molecular basis of drug sensitivity or resistance.

Biomarker Discovery: Correlate molecular characteristics with drug response predictions to identify potential predictive biomarkers. This can guide the selection of patient populations more likely to benefit from a particular therapy.

Combination Therapy Exploration: Explore drug synergy predictions to identify promising drug combinations that may enhance therapeutic outcomes. This can provide insights into potential combination strategies that can be further validated experimentally.

Histological Analysis: Use histology images to validate the morphological effects of drugs on tumor tissues, providing additional evidence for the drug’s mechanism of action and potential efficacy.

Cross-Model Comparisons: Compare different models to understand how various genetic backgrounds influence drug response, helping to validate hypotheses about the role of specific genes or pathways in silico.

Virtual Screening: Perform virtual screening of drugs against a wide range of models to prioritize candidates for further experimental validation.

Can you share examples of how researchers are anticipated to use this tool to improve their workflows or achieve breakthroughs?

The simplest example is preclinical model selection. Every preclinical study begins with the selection of tumor models. CertisOI Assistant takes the manual effort out of this process and brings great precision to selecting the optimal models for any given study.

Another is developing a biomarker strategy. The traditional approach is to hypothesize what biomarker or biomarkers might be linked to the drug’s mechanism of action and then test those hypotheses in preclinical studies, which is usually an iterative process. If preclinical data is promising, researchers must validate predictive biomarkers in human clinical trials—and as discussed, the failure rate is high.

The CertisOI Assistant helps researchers identify and validate more precise, predictive gene expression biomarkers earlier in the development process and with less iteration than the traditional workflow—saving time, and money, and improving chances for commercial success.

What kinds of cancer models or datasets does the tool support, and how does this breadth benefit the research community?

The current version of CertisOI gives researchers access to Certis’ rapidly expanding library of PDX and PDX-derived tumor models and the entire Cancer Cell Line Encyclopedia (CCLE) of models. The platform’s algorithms also draw on data from Genomics of Drug Sensitivity in Cancer (GDSC), International Cancer Genome Consortium (ICGC), CI ALMANAC, O’Neil, and other datasets. This holistic approach to data integration allows for a more comprehensive analysis than tools that focus on isolated data types.

The CertisOI Assistant is designed to be user-friendly. How do you ensure that it is accessible to researchers who may not have extensive technical expertise?

Several features make CertisOI Assistant accessible to researchers at all levels:

Intuitive Interface: The interface is designed to be intuitive and easy to navigate, allowing users to perform complex queries and analyses without needing to understand the underlying technical details.

Guided Workflows: The assistant provides guided workflows for common research tasks, such as querying drug response predictions, analyzing genomic data, and exploring pharmacology studies. This helps users focus on their research questions without getting bogged down in technical complexities.

Natural Language Processing: Users can interact with the assistant using natural language queries, making accessing the information they need easier for those without technical expertise. The assistant interprets the queries and translates them into the appropriate database queries.

Comprehensive Documentation: Detailed documentation and tutorials help users understand how to use the assistant effectively. This includes step-by-step guides, examples, and explanations of key concepts.

Interactive Visualizations: The assistant provides interactive visualizations for data analysis, such as charts and histology images, allowing users to explore and interpret data visually without needing to write code.

Responsive Support: Users can access responsive support to assist with any questions or issues. This ensures they can get help quickly and continue their research without unnecessary delays.

Customizable Queries: While the assistant provides default workflows, it also allows for customization, enabling users to tailor queries to their specific research needs without requiring deep technical knowledge.

Collaboration is a key aspect of research. How does the CertisOI Assistant facilitate teamwork among researchers or institutions?

With CertisOI Assistant, researchers from different teams or institutions can access the same dataset and tools, allowing them to work collaboratively on shared projects or research questions. The platform also makes it easy to download and share data queries, results, and insights among team members so everyone involved in a project can contribute effectively.

What are the biggest challenges in scaling AI adoption in cancer research, and how can they be addressed?

Significant challenges include data security, data integration, and trust in AI‐based outcome predictions. I am not an expert on data security or data integration, but great minds are working to solve those challenges. With respect to trusting AI-generated predictions, we need efficient and credible ways to validate those predictions.

Certis has taken a two-pronged approach to this: in silico validation via internal, cross-validation studies, and in vivo validation—performing studies in clinically relevant mouse models to evaluate the accuracy of our platform’s predictions. Over time, these tools will also be validated clinically in human patients—but of course, that will take a great deal of time and money, as well as the willingness to change the current cancer treatment paradigm. The medical and regulatory community will have to stop relying on how things have always been done and embrace the power of computational analyses to inform decisions.

How do you envision tools like the CertisOI Assistant shaping the future of cancer treatment and precision medicine?

Modern medicine doesn’t yet have a great way to match patients to the ideal treatments. Overall, only 10% of cancer patients experience a clinical benefit from treatments matched to tumor DNA mutations. That not only hurts patients’ health, but it also harms them financially. An estimated $2.5 billion —with a B—is wasted on ineffective therapies. It is a very sad fact that 42% of cancer patients fully deplete their assets by the second year of their diagnosis.

Tools like CertisOI Assistant and CertisAI will help us realize the promise of precision medicine—getting people the optimal treatment for their unique form of cancer the first time, every time…. And to democratize access to more effective, personalized care.

Thank you for the great interview, readers who wish to learn more should visit Certis Oncology Solutions.

#2022#2023#adoption#ai#AI adoption#ai tools#AI/ML#Algorithms#almanac#analyses#Analysis#approach#assets#billion#Biology#biomarkers#Cancer#cancer treatment#cell#CEO#Certis Oncology Solutions#change#charts#clinical#code#Collaboration#Community#comprehensive#course#data

0 notes

Text

In 1972, Drs. Evelyn and John Billings and colleagues published a seminal article demonstrating that 22 women, adequately trained, could detect the approach of ovulation in the fertile window of their menstrual cycle...

Subsequently, Dr. Thomas Hilgers and colleagues introduced a standardized system for women to record these symptoms…This developed further the concept of fertility biomarkers, which provide information about normal ovarian cycle conditions or suggest the presence of pathological conditions…Many other clinicians and researchers have also expanded our knowledge of the medical applications of fertility biomarkers.

These findings established the biological foundations of a tool of fertility awareness tracking that has facilitated the development of restorative reproductive medicine: an approach that can be applied to identify and treat the underlying causes of infertility/subfertility…

However, the emergence of in vitro fertilization (IVF) in 1978, with the first successful birth of a baby girl, introduced a solution that operates independently of the causes of infertility. As a result, the RRM approach, which focuses on uncovering the underlying biological causes of infertility, has lost priority in clinical practice.

Commentary on Infertility and Restorative Reproductive Medicine

26 notes

·

View notes

Text

DNA-like molecule may survive Venus-like cloud conditions

Punishing conditions in the clouds of Venus could be home to a DNA-like molecule capable of forming genes in life very different to that on Earth, according to a new study.

Long thought to be hostile to complex organic chemistry because of the absence of water, the clouds of Earth's sister planet are made of droplets of sulfuric acid, chlorine, iron, and other substances.

But research led by Wrocław University of Science and Technology shows how peptide nucleic acid (PNA)—a structural cousin of DNA—can survive under lab conditions made to mimic conditions that can occur in Venus' perpetual clouds.

The research is published in the journal Science Advances.

The international team drew on expertise from Cardiff University, Massachusetts Institute of Technology, Worcester Polytechnic Institute and industry collaborators Symeres for the study, which assessed PNA's ability to withstand a 98% sulfuric acid solution at room temperature for a period of two weeks.

Their findings add to the evidence that shows that concentrated sulfuric acid can sustain a diverse range of organic chemistry that might be the basis of a form of life different from Earth.

Lead author, Dr. Janusz Jurand Petkowski from Wrocław University of Science and Technology, said, "People think concentrated sulfuric acid destroys all organic molecules and therefore kills all life, but this is not true. While many biochemicals, like sugars, are unstable in such an environment, our research to date shows that other chemicals found in living organisms, such as nitrogenous bases, amino acids, and some dipeptides, don't break down.

"Here, we've started a new chapter on the potential of sulfuric acid as a solvent for life, demonstrating that PNA—a complex molecule, structurally related to DNA, and known to interact specifically with nucleic acids—exhibits remarkable stability in concentrated sulfuric acid at room temperature."

The work builds on findings from mid-2020, where a team of scientists from Imperial College London presented evidence for the presence of phosphine, a toxic gas produced in oxygen-poor environments, on Venus.

In the same year, a group of scientists from Cardiff University shared preliminary results from their research indicating the presence of ammonia on the planet.

Dr. William Bains from Cardiff University's School of Physics and Astronomy was part of both studies.

He added, "Both ammonia and phosphine are biomarkers, which means they can indicate the presence of life. But Venus's clouds are utterly hostile to life as we know it on Earth. So our latest study seeks to explore the potential of concentrated sulfuric acid as a solvent that could support the complex chemistry needed for life in these seemingly uninhabitable clouds.

"To find that PNA with its similarities to DNA can remain in concentrated sulfuric acid for hours is quite astonishing. It's a new piece of a much larger puzzle in our understanding of how life, albeit very different from ours, is made and where in the universe it might exist."

The findings also offer new ways of understanding the chemistry of sulfuric acid, one of the most widely used industrial chemicals, that may have practical use in the future, according to the team.

Dr. Pętkowski added, "Our study shows that PNA is no longer stable in sulfuric acid at temperatures higher than 50°C. So, our future research will focus on creating a genetic polymer—a molecule that can play the role that DNA plays in life on Earth—that is stable in concentrated sulfuric acid over the temperature range of Venus's clouds, between 0°C and 100°C, and not just at room temperature.

"The discoveries so far are therefore only the first step towards finding such a stable polymer."

IMAGE: PNA hexamers and monomers.(A) PNA hexamers composed of six identical, consecutive units of nucleic acid bases: adenine (A6), guanine (G6), cytosine (C6), and thymine (T6). PNA backbone (AEG) residues are colored in red, the acetyl linker residues are in pink, and the nucleic acid bases are in blue. (B) Structures of PNA monomers, mA, mG, mC, and mT. Credit: Science Advances (2025). DOI: 10.1126/sciadv.adr0006

4 notes

·

View notes

Text

Is the Drug Discovery Services Market Ready for a Revolution?

Introduction: A Transformative Era for Drug Discovery Services

The global drug discovery services market is experiencing unprecedented growth, fueled by the rising demand for innovative therapeutics, breakthrough technologies, and evolving research dynamics. The drug discovery sector is projected to escalate from $17.47 billion in 2025 to approximately $29.45 billion by 2032. This robust expansion is propelled by several key factors: the escalating need for personalized medicine, the increasing prevalence of chronic diseases, and the growing investment in biotechnology and pharmaceutical R&D.

Pharmaceutical companies and biotech firms are increasingly outsourcing drug discovery processes to specialized contract research organizations (CROs), aiming to enhance efficiency, mitigate costs, and accelerate time-to-market. The increasing importance of precision medicine is reshaping the landscape, with an emphasis on developing treatments tailored to individual genetic profiles.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40632-global-drug-discovery-services-market

Market Dynamics: Drivers, Challenges, and Opportunities

Key Drug Discovery Services Market Drivers

Technological Advancements: The integration of artificial intelligence (AI), machine learning (ML), high-throughput screening (HTS), and computational modeling is revolutionizing drug discovery processes. These innovations significantly enhance target identification, drug screening, and lead optimization, expediting the discovery of novel therapeutics.

Increased R&D Investments: Pharmaceutical companies and biotech firms are ramping up investments in R&D, particularly in the development of biologics, small molecules, and RNA-based therapeutics. The focus on targeted therapies and gene editing technologies like CRISPR is further propelling this market.

Chronic Disease Prevalence: The rise in chronic diseases such as oncology, cardiovascular diseases, and neurological disorders is driving the demand for innovative drug discovery solutions. With the global aging population and a surge in lifestyle-related diseases, the need for novel and effective treatments has never been greater.

Government Initiatives and Regulatory Support: Regulatory bodies around the world are providing expedited approval pathways for breakthrough therapies, further fueling the demand for innovative drug discovery services. Initiatives like Fast Track and Breakthrough Therapy Designation are accelerating drug development timelines.

Get up to 30% Discount: https://www.statsandresearch.com/check-discount/40632-global-drug-discovery-services-market

Challenges Facing the Drug Discovery Services Market

Despite its rapid growth, the drug discovery services sector is not without its challenges. The high costs associated with drug development, regulatory hurdles, and long clinical trial timelines are significant obstacles. Moreover, the high failure rates of drug candidates in the discovery phase and clinical trials continue to pose risks for investors and stakeholders.

The complexity of intellectual property rights, evolving regulations, and the challenge of maintaining data privacy in global markets also create barriers to entry for new players in the market.

Segmentation Analysis: Breaking Down the Market by Service, Drug Type, and Therapeutic Area

By Service Type

Biology Services: Accounting for 35% of the market share, biology services dominate the landscape, driven by increasing demand for target identification, biomarker research, and assay development. The projected CAGR for biology services is 11.8%, reflecting the increasing reliance on advanced biological research in drug discovery.

Medicinal Chemistry Services: Holding a 30% market share, medicinal chemistry services are expected to grow at a CAGR of 12.5%. This growth is attributed to the rising emphasis on small-molecule drug discovery and AI-driven screening methods that enhance the efficacy of lead compounds.

Toxicology Services: As drug safety is paramount, the toxicology services segment is gaining traction, particularly in the preclinical development phase, ensuring the safety of drug candidates before they proceed to clinical trials.

Preclinical Development: Preclinical services are essential for evaluating a drug’s pharmacokinetics, toxicity, and efficacy in animal models. This segment continues to expand, driven by the increasing complexity of drugs under development.

By Drug Type

Small Molecules: The small molecules segment, accounting for 55% of the market share, is the dominant player due to the long-standing role small molecules play in treating chronic diseases. Small molecules have established manufacturing processes, high market penetration, and cost-effective production. This segment is projected to grow at a CAGR of 10.5%.

Biologics: Biologics, including monoclonal antibodies, gene therapies, and cell therapies, are on the rise, with a projected CAGR of 13.1%. The biologics segment is gaining ground, driven by the increasing focus on immunotherapies, personalized medicine, and next-generation vaccines.

By Therapeutic Area

Oncology: Oncology remains the largest therapeutic area, contributing over 42% of the market share. The rise in cancer cases, coupled with the demand for targeted treatments, is spurring growth in this segment. Immunotherapies and precision oncology are transforming the landscape.

Neurology: With a market share of 15%, the neurology sector is poised for robust growth, with significant breakthroughs in Alzheimer's, Parkinson's, and multiple sclerosis treatments.

Infectious Diseases: The need for novel treatments in the face of rising antimicrobial resistance (AMR) and emerging pathogens is driving the growth of the infectious diseases sector. This area represents approximately 12% of the market, expanding at a CAGR of 10.8%.

By Process Stage

Target Discovery & Validation: Accounting for 30% of the market, this stage benefits from the latest advances in genomics and proteomics, enabling more precise identification of drug targets. The projected CAGR of 11.7% reflects the growing importance of early-stage discovery in streamlining drug development.

Lead Optimization: This segment, responsible for refining drug candidates, is expected to grow at a CAGR of 11.3%, as pharmaceutical companies focus on improving efficacy, safety, and bioavailability before clinical trials.

Preclinical Development: The preclinical development stage represents a significant portion of the market. The growing reliance on 3D cell culture models, organ-on-chip technologies, and animal models is driving innovation in this area.

Regional Insights: Global Dynamics and Emerging Markets

North America

North America is the leading market for drug discovery services, driven by significant R&D investments, the presence of major contract research organizations (CROs), and an advanced healthcare infrastructure. The U.S., in particular, is home to many of the world’s largest pharmaceutical companies and has been a key player in driving the global drug discovery market.

Europe

Europe follows closely as the second-largest market, with strong contributions from both government initiatives and collaborations between academic institutions and pharmaceutical companies. The European market benefits from a robust regulatory environment that encourages innovative research.

Asia Pacific

Asia Pacific is the fastest-growing region, with countries like China, India, Japan, and South Korea emerging as key players in the global drug discovery space. The region benefits from cost-effective research, an expanding middle class, and a growing demand for innovative therapeutics.

Competitive Landscape: Key Players and Strategic Developments

The drug discovery services market is highly competitive, with major players continuously expanding their service offerings to meet the rising demand for specialized drug development solutions.

WuXi AppTec: This leading CRO has significantly enhanced its service portfolio through strategic acquisitions and partnerships, expanding its capabilities in biologics and gene therapies.

Charles River Laboratories: A key player in preclinical research, Charles River provides comprehensive drug discovery services, including toxicology and medicinal chemistry services.

Evotec AG: With its strong presence in high-throughput screening, Evotec is well-positioned to capitalize on the growth of AI-driven drug discovery.

Recent Developments

WuXi Biologics sold its vaccine manufacturing facility in Ireland to Merck & Co. for $500 million in January 2025, shifting its focus towards more strategic areas of drug discovery.

Halozyme Therapeutics proposed a $2 billion acquisition of Evotec in late 2024, aiming to combine drug-delivery technologies with proprietary drug discovery platforms.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40632-global-drug-discovery-services-market

Future Outlook: Shaping the Future of Drug Discovery

The global drug discovery services market is poised for continued growth, driven by the increasing emphasis on precision medicine, AI and machine learning technologies, and innovations in biologics and small molecules. As new research tools, platforms, and collaborations emerge, the market will continue to evolve, offering exciting opportunities for innovation and scientific breakthroughs.

To remain competitive, industry stakeholders must adapt to evolving regulatory environments, embrace next-generation technologies, and focus on developing personalized and targeted therapies that cater to the unique needs of patients worldwide.

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

#Drug Discovery Services#Drug Discovery Market#Pharmaceutical Services#Clinical Trials#Drug Development#Drug Discovery Outsourcing#Global Drug Discovery Market#AI in Drug Discovery#Precision Medicine#Drug Discovery CRO#Biopharma Market Trends#Drug Discovery Market Size#Drug Discovery Industry Report

2 notes

·

View notes

Text

Biomarkers Market Comprehensive Analysis, Forecast to 2032

The global biomarkers market was valued at USD 38.41 billion in 2018 and is expected to soar to USD 190.81 billion by 2032, registering a robust CAGR of 12.1% over the forecast period. In 2018, North America led the biomarkers market, accounting for a dominant market share of 38.53%.

A biomarker, or biological marker, refers to a measurable indicator of the biological state or condition of an organ, tissue, or cell. Biomarkers play a crucial role in medicine, safety assessments, and drug discovery and development. They are classified into various types based on their functions, including diagnostic biomarkers, prognostic biomarkers, predictive biomarkers, and more. Biomarkers significantly contribute to enhancing the drug development process and advancing biomedical research. Additionally, based on biological characteristics, biomarkers are further categorized into genomics, proteomics, and other segments.

The growing use of biomarkers in diagnostic applications is a major driver propelling the expansion of the biomarkers industry. Increasing investments in research and development by biotechnology and pharmaceutical companies, along with the rising global prevalence of cancer, are key biomarkers market trends fueling demand. These factors are collectively accelerating the growth and development of the biomarkers market.

Request a Free Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/biomarkers-market-102173

Biomarkers Market: Market Trend The Biomarkers Market is experiencing a significant surge in interest due to advancements in precision medicine and personalized therapies. Growing adoption of biomarkers in drug discovery and development is reshaping pharmaceutical strategies. Liquid biopsy and genomic biomarkers are gaining traction as they offer non-invasive diagnostic solutions with high accuracy. Furthermore, technological advancements in bioinformatics and high-throughput screening are accelerating the pace of biomarker research, contributing to the dynamic growth of the Biomarkers Market.

Biomarkers Market: Market Growth The Biomarkers Market is poised for robust growth, driven by increasing incidences of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions. The demand for early and accurate diagnosis is pushing healthcare providers to integrate biomarker-based testing into their clinical workflows. Moreover, growing investments in research and development, along with favorable regulatory approvals, are expected to further propel the Biomarkers Market. The increasing focus on companion diagnostics is also playing a crucial role in market expansion.

List Of Key Companies Covered:

F. Hoffmann-La Roche Ltd.

Abbott

Thermo Fisher Scientific

Bio-Rad Laboratories, Inc.

CENTOGENE N.V.

Axon Medchem

Sino Biological Inc.,

R&D System

BioVision Inc.

Myriad RBM

Other players

Biomarkers Market: Market Segmentation The Biomarkers Market is comprehensively segmented based on type, application, disease indication, and end-user. In terms of type, the Biomarkers Market includes safety biomarkers, efficacy biomarkers, validation biomarkers, and predictive biomarkers. Among these, predictive biomarkers hold a dominant share in the Biomarkers Market due to their critical role in forecasting disease risk and response to specific treatments.

When categorized by application, the Biomarkers Market covers diagnostics, drug discovery & development, personalized medicine, and disease risk assessment. Diagnostic applications lead the Biomarkers Market, as healthcare providers increasingly rely on biomarkers for early detection and disease monitoring. The integration of biomarkers in drug development pipelines is also expanding, reinforcing the Biomarkers Market's role in improving clinical trial success rates.

Based on disease indication, the Biomarkers Market segments include cancer, cardiovascular diseases, neurological disorders, and infectious diseases. The cancer segment commands the largest share in the Biomarkers Market, as oncology research heavily depends on biomarkers for identifying genetic mutations and predicting therapy responses. However, the application of biomarkers in cardiovascular and neurological diseases is rapidly growing, further diversifying the scope of the Biomarkers Market.

In terms of end-users, the Biomarkers Market encompasses hospitals & clinics, academic & research institutes, pharmaceutical & biotechnology companies, and diagnostic laboratories. Pharmaceutical and biotechnology companies represent a significant portion of the Biomarkers Market, given their continuous efforts to develop targeted therapies. Diagnostic laboratories are also crucial players in the Biomarkers Market, driven by increasing demand for specialized testing services.

Biomarkers Market: Restraining Factors Despite its promising potential, the Biomarkers Market faces several challenges. High costs associated with biomarker validation and testing limit accessibility, especially in developing regions. Additionally, complexities in biomarker discovery and the need for stringent regulatory compliance can slow down the approval process. Ethical concerns related to genetic testing and data privacy also pose barriers to the broader adoption of biomarker technologies within the Biomarkers Market.

Biomarkers Market: Regional Analysis Geographically, North America dominates the Biomarkers Market, supported by advanced healthcare infrastructure, extensive research funding, and the presence of key industry players. Europe follows closely, benefiting from supportive government initiatives and increasing clinical trials. Meanwhile, the Asia-Pacific region is emerging as a high-potential market for biomarkers, fueled by rising healthcare investments, growing awareness, and an expanding patient base. Countries such as China and India are expected to contribute significantly to the growth of the Biomarkers Market in the coming years, making the region a focal point for future expansion.

Key Industry Developments:

In May 2021, QIAGEN N.V. announced the launch of its FDA-approved tissue companion diagnostic designed to detect the KRAS G12C mutation in non-small cell lung cancer (NSCLC) tumors. This advancement is set to strengthen QIAGEN's precision medicine portfolio, particularly in the field of lung cancer treatment. In April 2021, F. Hoffmann-La Roche Ltd revealed a series of five new applications for their cardiac biomarkers, utilizing the Elecsys technology. These biomarkers have demonstrated effectiveness in enhancing the management of cardiovascular diseases, further expanding Roche’s capabilities in cardiac care.

1 note

·

View note

Text

Undergrad research blast from the past. Here I am in 2020 assembling a micro fluidic flow cell with a gold electrode block. I think I took this video for myself so I knew what to clip to what. This was when I worked with electrochemical sensors, transducing signals via impedance spectroscopy.

A lot of electrochemical techniques rely on measuring voltages or currents, but in this lab we looked at impedance- which is a fancy combination of regular resistance (like the same one from ohms law) and the imaginary portion of the resistance that arises from the alternating current we supply.

I would functionalize different groups on the gold working electrode by exposing the surface to a solution of thiolated biomarker capture groups. Thiols love to form self-assembled mono layers over gold, so anything tagged with thiol ends up sticking. [Aside: Apparently after I left the group they moved away from gold thiol interactions because they weren't strong enough to modify the electrode surface in a stable and predictable way, especially if we were flowing the solution over the surface (which we wanted to do for various automation reasons)]. The capture groups we used were various modified cyclodextrins- little sugar cups with hydrophobic pockets inside and a hydrophilic exterior. Cyclodextrins are the basis of febreeze- a cyclodextrin spray that captures odor molecules in that hydrophobic pocket so they can't interact with receptors in your nose. We focused on capturing hydrophobic things in our little pocket because many different hydrophobic biomarkers are relevant to many different diseases, but a lot of sensors struggle to interact with them in the aqueous environment of bodily fluids.

My work was two fold:

1) setting up an automated system for greater reproducibility and less human labor. I had to figure out how to get my computer, the potentiostat (which controls the alternating current put in, and reads the working electrode response), the microfluidic pump, and the actuator that switched between samples to all talk to each other so I could set up my solutions, automatically flow the thiol solution for an appropriate time and flow rate to modify the surface, then automatically flow a bio fluid sample (or rather in the beginning, pure samples of specific isolated biomarkers, tho their tendency to aggregate in aqueous solution may have changed the way they would interact with the sensor from how they would in a native environment, stabilized in blood or urine) over the electrode and cue the potentiostat for multiple measurements, and then flow cleaning solutions to clean out the tubings and renew the electrode. This involved transistor level logic (pain) and working with the potentiostat company to interact with their proprietary software language (pain) and so much dicking around with the physical components.

2) coming up with new cyclodextrin variants to test, and optimizing the parameters for surface functionalization. What concentrations and times and flow rates to use? How do different groups around the edge of the cyclodextrin affect the ability to capture distinct classes of neurotransmitters? I wasn't working with specific sensors, I was trying to get cross reactivity for the purpose of constructing nonspecific sensor arrays (less akin to antibody/antigen binding of ELISAs and more like the nonspecific combinatorial assaying you do with receptors in your tongue or nose to identify "taste profiles" or "smell profiles"), so I wanted diverse responses to diverse assortments of molecules.

Idk where I'm going with this. Mostly reminiscing. I don't miss the math or programming or the physical experience of being at the bench (I find chemistry more "fun") but I liked the ultimate goal more. I think cross reactive sensor arrays and principle component analysis could really change how we do biosample testing, and could potentially be useful for defining biochemical subtypes of subjectively defined mental illnesses.... I think that could (maybe, possibly, if things all work and are sufficiently capturing relevant variance in biochemistry from blood or piss or sweat or what have you) be a more useful way to diagnose mental illness and correlate to possible responses to medications than phenotypic analysis/interviews/questionnaires/trial and error pill prescribing.

4 notes

·

View notes

Text

H.M. The Queen's speech at Goodes Prize Science Day, Alzheimer’s Drug Discovery Foundation

Distinguished guests, researchers, ladies and gentlemen,

It is a true pleasure to be here today with you to open this important scientific event.

I would like to extend my gratitude to the Alzheimer’s Drug Discovery Foundation (ADDF) for organising the Science Day, in collaboration with Professor Kivipelto’s team at Karolinska Institutet and the FINGERS Brain Health Institute.

Sweden is honoured to host this gathering as we celebrate the 10th Anniversary of the Melvin R. Goodes Prize and recognise the outstanding accomplishments of the remarkable scientists who have received this prestigious award.

It is wonderful to see so many leading researchers from around the world come together to discuss the latest breakthroughs in the field. I sincerely hope that this meeting will inspire further innovation and global collaboration in our efforts to find more effective ways to prevent and treat Alzheimer’s disease and other dementias.

Thanks to greater prosperity and advances in medicine, people are now living longer than before - a positive development for all of us. However, this increased longevity has also led to a sharp rise in the number of people living with Alzheimer’s disease and other forms of dementia. Advanced age remains the primary risk factor for dementia, making it especially valuable that the Alzheimer’s Drug Discovery Foundation is placing significant emphasis on the ‘biology of aging’.

This focus is essential for identifying new ways to prevent and treat these diseases. In the fight against dementia, there are many reasons to prioritise preventive measures. Any efforts to prevent or delay the onset of dementia can have a significant impact on individuals and the society. In Sweden, we have seen a great deal of innovation in this field.

The FINGER model, developed by Professor Kivipelto and her team, has gained global recognition and now includes trials that combine lifestyle interventions with pharmacological treatments, thanks to the support of the ADDF. It is encouraging to see progress in the development of new treatments, and continued support for clinical trials is crucial to this advancement.

New advancements in early detection and diagnosis will be a key focus during this science day. The introduction of new blood-based biomarkers promises to significantly enhance early detection and treatment, potentially transforming both research and patient care. I am delighted to be here for this special occasion, as Professor Henrik Zetterberg from Gothenburg, Sweden, receives the 10th Goodes Prize for his groundbreaking work in this field. Warm congratulations to him on this well-deserved recognition.

It is wonderful to see all the previous Goodes Prize winners gathered here as well. Each of these scientists represents the very best minds in Alzheimer’s research. By fostering communication and exchanging ideas across borders, programmes and research areas, they are paving the way toward the future of dementia prevention and treatment.

As everyone here knows, dementia does not discriminate – it can affect anyone, no matter where they are from – so global collaboration among scientists is essential to deliver effective solutions to patients.

While there are many opportunities ahead, there are also several challenges. I am deeply grateful for the work you are all doing to advance this critical field. I have seen firsthand the profound impact of Alzheimer’s disease. Questions related to dementia research and care have been close to my heart for many years. This commitment inspired me to establish the Silviahemmet foundation in 1996, with a mission to provide education in dementia care, and to offer tailored care options focusing on enhancing quality of life.

Over the years I have had the pleasure of attending several Alzheimer’s conferences here at Karolinska, and I look forward to hosting the eleventh Queen Silvia Nursing Award Grand Ceremony later this week.

I firmly believe that by working together and sharing knowledge, we can build a dementia-friendly society and ensure that research findings are translated into real-world applications. Alzheimer’s disease challenges us to think creatively and act collectively.

Once again, I extend my deepest gratitude to the ADDF for organising this vital event together with Karolinska Institutet and the FINGERS Brain Health Institute. Thank you all for being here and for your dedication and work in this crucial field.

I wish you a productive and inspiring conference, and a wonderful stay in Stockholm!

Speech held by Queen Silvia at Karolinska Institutet, Stockholm, on September 9, 2024.

#swedish royal family#speeches#queen silvia#silvia's dementia work#karolinska institutet#stockholm#240909

2 notes

·

View notes

Text

Investment Surge in GLP-1 Drugs Market: Trends and Future Prospects

Market Growth and Investment Trends

The GLP-1 drugs market has seen substantial investment from pharmaceutical companies and venture capitalists. This is driven by the increasing prevalence of type 2 diabetes and obesity, coupled with the efficacy of GLP-1 drugs in managing these conditions. Key trends include:

Rising Prevalence of Diabetes and Obesity: The global rise in lifestyle-related health issues is fueling demand for effective treatments.

Innovative Drug Development: Companies are investing heavily in R&D to develop next-generation GLP-1 drugs with improved efficacy and fewer side effects.

Strategic Collaborations and Partnerships: Collaborations between pharmaceutical giants and biotech firms are accelerating innovation and market entry of new drugs.

Recent Developments

Several notable developments have occurred in the GLP-1 drugs market:

New Drug Approvals: Regulatory bodies like the FDA and EMA have recently approved several new GLP-1 receptor agonists, expanding treatment options.

Clinical Trials and Research: Ongoing clinical trials are investigating the broader therapeutic potential of GLP-1 drugs, including their effects on cardiovascular health and non-alcoholic fatty liver disease (NAFLD).

Technological Advancements: Innovations in drug delivery systems, such as oral formulations and long-acting injectables, are enhancing patient compliance and convenience.

Browse Press Release

Future Opportunities

The future of the GLP-1 drugs market holds numerous opportunities for growth and innovation:

Expansion into New Therapeutic Areas: Research suggests potential applications of GLP-1 drugs in conditions beyond diabetes and obesity, such as neurodegenerative diseases and inflammation.

Personalized Medicine: Advances in genomics and biomarkers may enable personalized GLP-1 therapies tailored to individual patient profiles, improving outcomes.

Emerging Markets: Increasing healthcare access and rising diabetes prevalence in emerging markets present significant growth opportunities for GLP-1 drugs.

Conclusion

The GLP-1 drugs market is poised for remarkable growth, driven by robust investment, innovative developments, and expanding therapeutic applications. As research progresses and new technologies emerge, GLP-1 receptor agonists will play a crucial role in addressing the global burden of diabetes, obesity, and potentially other diseases, offering improved health outcomes for millions.

About iDataAcumen

iDataAcumen is a global business intelligence and management consulting firm providing data driven solutions to a wide array of business challenges. Our clients are present across major geographies globally and belong to industries ranging mainly from healthcare, pharmaceuticals, life science, biotechnology, medical devices, food industry, chemicals, among others. We have catered to more than 500 clients across these industries.

We aspire to help our clients build a sustainable business by providing them robust business insights that are derived from sound data driven analysis. In today’s ever changing business environment, its become important to look objectively at your own business just as it is important to look at the competition. Technological advancement including but not limited to big data, artificial intelligence, and machine learning are helping industries worldwide to make informed business decisions. Our research process also makes use of some of these advanced tools to uncover valuable insights from vast amount of data to arrive at logical conclusions.

2 notes

·

View notes

Text

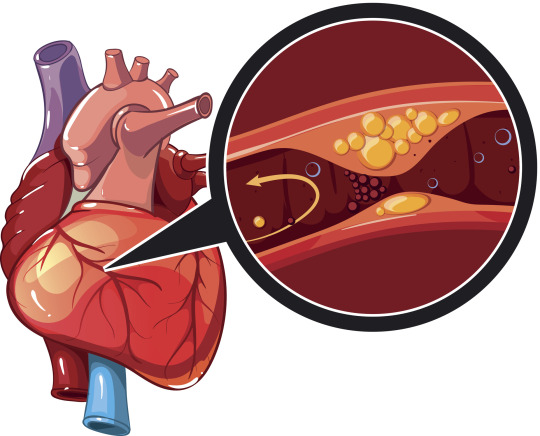

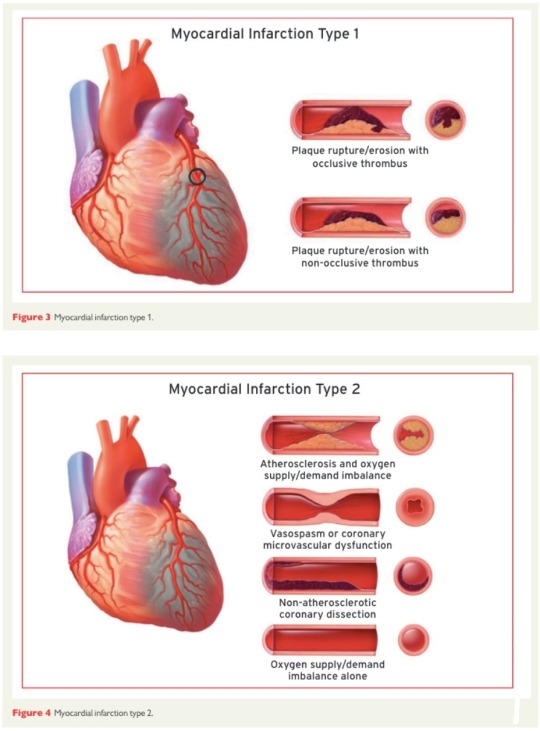

Myocardial Infarction Epidemiology: Prevalence and Risk Factors

Myocardial Infarction Disease

Myocardial Infarction Disease Overview:

Myocardial Infarction Disease, commonly known as a heart attack, is a life-threatening condition that occurs when blood flow to the heart muscle is severely reduced or completely blocked, typically due to the narrowing or blockage of coronary arteries. This article delves into various aspects of myocardial infarction, including diagnostic analysis, treatment, regulatory frameworks, clinical trials, pricing, market access, and epidemiological studies.

About 22,200 people had an acute myocardial infarction (AMI) in 2020, and approximately 5,000 of those cases resulted in death. This global health risk is defined by the sudden cessation of blood supply to a specific area of the heart muscle, typically due to a blockage in the coronary artery. The heart muscle deteriorates in the absence of a consistent supply of oxygen-rich blood, which might have dangerous consequences.

Price and Market Access

Myocardial Infarction Disease Market Competitors Listed Below are Revolutionizing Healthcare with Innovative Diagnostic Inventions:

Imaging Studies:

Siemens Healthineers

GE Healthcare

Philips Healthcare

Hitachi Healthcare

Canon Medical System

CTA, PET & SPECT Scan:

Siemens Healthineers

Beckman Coulter

Toshiba Medical Systems

Bruker

Philips Healthcare

GE Healthcare

Laboratory Tests:

Abbott Laboratories

Roche Diagnostics

Siemens Healthineers

Beckman Coulter

Bio-Rad Laboratories

Sysmex Corporation

Browse In-depth Research Report on Myocardial Infarction Disease:https://www.diseaselandscape.com/cardiovascular/myocardial-infarction-market-entry-solutions

Myocardial Infarction Disease Diagnostic Analysis:

Accurate and timely diagnosis is crucial in managing myocardial infarction. Physicians employ a combination of clinical evaluation, medical history assessment, and various diagnostic tools, including:

Electrocardiogram (ECG): An ECG records the heart's electrical activity and helps identify irregularities in heart rhythm or the presence of a heart attack.

Blood Tests: Biomarkers like troponin and creatine kinase-MB are measured in blood to confirm myocardial infarction.

Angiography: Coronary angiography involves injecting contrast dye into the coronary arteries to visualize blockages via X-ray, facilitating the assessment of the extent and location of the blockage.

Echocardiography: This imaging technique uses ultrasound to assess the heart's structure and function, helping diagnose damage to the heart muscle.

Myocardial Infarction Disease Treatment Analysis:

Treatment of myocardial infarction aims to restore blood flow to the affected area, minimize heart damage, and prevent future occurrences. The key components of treatment include:

Medications: Patients receive antiplatelet drugs, anticoagulants, pain relievers, and medications to manage blood pressure and cholesterol levels.

Angioplasty and Stent Placement: In many cases, a percutaneous coronary intervention (PCI) is performed to open blocked arteries using a balloon and place a stent to keep the vessel open.

Coronary Artery Bypass Grafting (CABG): For more severe cases, coronary artery bypass surgery is necessary to bypass blocked arteries using healthy vessels from other parts of the body.

Lifestyle Changes: Patients are advised to make lifestyle modifications, including dietary changes, exercise, and quitting smoking, to reduce the risk of future heart attacks.

Regulatory Framework for Myocardial Infarction Disease:

The regulatory landscape for myocardial infarction treatment is rigorous, with government agencies such as the U.S. Food and Drug Administration (FDA) playing a critical role in approving and monitoring medications and medical devices. Rigorous clinical trials are necessary for drug and treatment approvals to ensure safety and efficacy.

Emerging Detection Methods:

Liquid Biopsies: Liquid biopsies are revolutionizing cancer diagnosis and monitoring. These tests analyze tiny fragments of DNA and other molecules circulating in the bloodstream. They enable the early detection of cancer, tracking of disease progression, and assessment of treatment response without the need for invasive tissue biopsies.

Artificial Intelligence (AI) in Medical Imaging: AI-driven algorithms are significantly improving the accuracy of medical imaging, such as X-rays, CT scans, and MRIs. AI can identify subtle anomalies that may escape human eyes, enabling earlier and more precise diagnosis of conditions like cancer, cardiovascular diseases, and neurological disorders.

CRISPR-Based Diagnostics: Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR) technology is being adapted for diagnostics. CRISPR-based tests can identify specific genetic sequences, allowing for the rapid detection of pathogens, mutations, and diseases with high accuracy and speed.

Nanotechnology: Nanoscale materials and devices are being used to develop highly sensitive sensors for detecting molecules, viruses, and even individual cells. These nanosensors have applications in disease diagnosis, environmental monitoring, and drug testing.

Telemedicine and Wearable Devices: The integration of wearable health monitoring devices and telemedicine platforms is allowing for continuous health monitoring. These technologies can detect irregularities in real-time and transmit data to healthcare professionals, providing early warnings and better management of chronic diseases.

Blockchain for Disease Tracking: Blockchain technology is being employed for secure and transparent disease tracking. It can streamline the tracking of epidemics, ensure data accuracy, and improve collaboration among healthcare organizations, government agencies, and researchers.

Clinical Trial Assessment:

Clinical trials are the foundation of medical advancements in myocardial infarction treatment. These trials evaluate new drugs, devices, or procedures to determine their effectiveness and safety. Participants are closely monitored, and results are scrutinized to ensure the treatment's benefits outweigh its risks.

Price and Market Access:

The cost of treating myocardial infarction can be significant due to hospitalization, surgical procedures, and long-term medication. Access to affordable healthcare is crucial to ensure that patients receive the best care without incurring financial hardship. Government programs, insurance plans, and pharmaceutical assistance programs play a vital role in ensuring market access and affordability.

Epidemiology Study:

Epidemiological studies provide essential insights into the prevalence, incidence, and risk factors of myocardial infarction. These studies help healthcare providers and policymakers understand the disease's burden on a population and develop targeted prevention and intervention strategies.

Conclusion:

Myocardial infarction, a severe and life-threatening condition, requires accurate diagnosis and prompt treatment to minimize heart damage. The regulatory framework, clinical trials, pricing, and epidemiological studies play pivotal roles in addressing this disease effectively. Ongoing research and advances in treatment options continue to improve the prognosis for individuals at risk of myocardial infarction, ensuring better outcomes and a higher quality of life.

Browse Through More Cardiovascular Diseases Research Reports:

For More Related Reports:

Unlocking the Most Recent Advances in Alzheimer's Disease research: a glimmer of hope

Global Insights on Multiple System Atrophy (MSA) Disease: Rising Against the Odds

Understanding Crohn's Disease: Its Causes, Signs, and Treatment

Demystifying Parkinson's Disease: A Closer Look at its Complex Nature

Cardiomyopathy Disease Research Trends and Clinical Trials

#health news#healthcare#medicalupdates#medicaleducation#medicalnews#trending#health#medicare#Myocardial Infarction#hearthealth#heartdisease#irregular heartbeat#heartcare#heartattack

1 note

·

View note

Text

Just to be clear here: neither the linked article nor the study are claiming that butyrylcholinesterase deficiency is the cause of SIDS - I assume the above post is an old excerpt, as the article has been amended to conclude with

Now that this biomarker has been further confirmed, researchers can turn their attention to a solution. In the next few years, those in the medical community who have studied SIDS will likely work on a screening test to identify babies who are at risk for SIDS and hopefully prevent it altogether.

What the study did find is that butyrylcholinesterase can serve as a biomarker for elevated risk of SIDS, meaning that doctors can test for it and use it to determine which patients might be at an elevated risk - and in turn use that to make recommendations.

This is still a significant development in understanding and hopefully preventing deaths from SIDS, but it's not a cause. Causal relationships are extremely difficult to determine in any science, especially medicine, and doubly especially with postmortem studies.

They’ve found the cause of Sudden Infant Death Syndrome. Babies who die of SIDS have a significantly lower level of an enzyme, the purpose of which is to rouse the baby from sleep if necessary (such as the baby stops breathing). This is extremely huge science and medicine news. There is a biological reason. It’s not random.

120K notes

·

View notes

Text

Strategic Imperatives for the HIV Diagnostics Market

As healthcare systems across the globe pursue digital transformation and patient-centric delivery models, HIV diagnostics is emerging as a critical inflection point. The convergence of technology, policy, and personalized medicine is reshaping the HIV diagnostics market, positioning it as a cornerstone of global public health strategies and commercial healthcare innovation. For senior executives and industry leaders, this sector represents not just a public health mandate, but a high-impact opportunity for strategic differentiation, sustainable growth, and value-driven transformation.

Download PDF Brochure

The Evolving Landscape of HIV Diagnostics: A Strategic Overview

The HIV diagnostics market has undergone a seismic shift over the past decade, transitioning from reactive testing protocols to proactive, integrated screening strategies. This evolution is being driven by multiple high-level forces:

Heightened global awareness and funding initiatives aimed at early detection and prevention.

Integration of diagnostics into primary care and telehealth ecosystems, facilitating decentralized access.

Advances in biomarker science and AI-powered diagnostics, enabling greater precision and speed.

Emergence of regulatory frameworks that support innovation while ensuring compliance and patient safety.

For stakeholders across healthcare delivery, biotechnology, and diagnostics manufacturing, these changes offer fertile ground for scalable innovation and cross-sector collaboration.

Real-World Applications: Where Innovation Meets Impact

Senior decision-makers are increasingly recognizing that HIV diagnostics is no longer a siloed function within infectious disease management. Instead, it is a vital enabler of broader clinical, operational, and population health goals. Here are key areas where real-world applications are transforming outcomes and driving new value:

1. Point-of-Care (POC) Testing Integration

The push toward decentralized care has made point-of-care HIV diagnostics a business-critical priority. Modern POC solutions are compact, user-friendly, and capable of delivering results in under 20 minutes. This dramatically shortens the diagnosis-to-treatment window, particularly in low-resource and rural environments. For healthcare providers and diagnostic firms, this opens avenues for:

New service delivery models (e.g., mobile clinics, remote testing).

Expansion into underserved geographies.

Value-based care contracting based on improved patient outcomes.

2. Digital Diagnostics and AI-Driven Interpretation

Artificial Intelligence is redefining how HIV test data is captured, analyzed, and acted upon. AI-driven diagnostics reduce error margins, increase throughput, and support clinicians with predictive insights that go beyond binary results. Enterprises investing in digital diagnostics platforms are gaining:

Competitive advantages in test accuracy and efficiency.

Data monetization pathways via anonymized population health insights.

Strategic positioning as enablers of intelligent, integrated care.

3. Self-Testing and Consumer Empowerment

With regulatory approvals expanding, self-administered HIV tests are gaining mainstream traction. This marks a fundamental shift in patient behavior, placing diagnostics into the hands of the end user. For diagnostics companies and retail health networks, this opens up:

New direct-to-consumer (DTC) revenue channels.

Brand engagement and loyalty through education-driven platforms.

Product development insights drawn from real-world user data.

Emerging Trends Reshaping the Market Trajectory

Understanding where the HIV diagnostics market is headed requires looking beyond current tools and metrics. Senior executives must anticipate the next wave of transformation. Key trends on the horizon include:

1. Multiplex Testing Platforms

The future of HIV diagnostics is integrated, not isolated. Multiplex platforms that can test for HIV alongside other infections (e.g., Hepatitis B/C, syphilis, HPV) are gaining momentum. These platforms streamline workflows, reduce costs, and provide a more holistic view of patient health—making them highly attractive to health systems seeking efficiency and comprehensiveness.

2. Biomarker-Based Personalized Testing

Precision medicine is making its way into infectious disease diagnostics. Next-generation HIV tests that incorporate individual genetic, immunological, or behavioral risk factors are poised to change how risk is assessed and interventions are prioritized. This personalization enhances clinical decision-making and aligns with the broader trend of tailored therapeutics.

3. Integration with Health Information Systems (HIS)

As electronic health records (EHRs) and health information exchanges (HIEs) become more interoperable, HIV diagnostics are being embedded directly into care workflows. Seamless data integration allows for real-time alerts, automated follow-ups, and longitudinal patient tracking—key enablers of chronic disease management models.

Business Opportunities and Strategic Leverage Points

The confluence of innovation, regulation, and public health urgency has created a dynamic environment ripe for investment and transformation. Here are strategic entry points and business opportunities for organizations seeking leadership in the HIV diagnostics ecosystem:

1. Private-Public Partnerships (PPPs)

Governments and NGOs are actively seeking private-sector partners to scale diagnostics access. By co-developing testing infrastructure or contributing proprietary platforms, companies can secure long-term contracts, enhance global brand presence, and fulfill ESG mandates.

2. M&A and Strategic Collaborations

Consolidation is a growing theme in the diagnostics market. Larger players are acquiring specialized HIV diagnostics firms to bolster their infectious disease portfolios. Conversely, nimble startups with proprietary technologies are entering strategic alliances to accelerate go-to-market strategies. Executives should explore both vertical integration and lateral expansion to gain speed and scale.

3. Expansion into Emerging Economies

Asia, Sub-Saharan Africa, and parts of Latin America present significant untapped potential for HIV diagnostics, driven by large at-risk populations and improving healthcare infrastructures. Companies that can tailor offerings to local contexts—regulatory, cultural, and economic—will gain a strong first-mover advantage.

4. Data-as-a-Service (DaaS) Models

The data generated by modern diagnostics is a strategic asset. Forward-thinking firms are developing DaaS models that provide anonymized epidemiological data to governments, payers, and research institutions. This not only creates new monetization channels but positions diagnostics providers as indispensable intelligence partners.

Long-Term Industry Shifts: The Road to 2030

As we look toward 2030, the HIV diagnostics market is set to be redefined by a series of long-term shifts that will reshape how care is delivered, how value is measured, and how innovation is scaled:

Diagnostics-as-a-Platform (DaaP): Moving beyond individual tests to platforms that support multiple conditions, use cases, and settings.

Sustainability and ESG Integration: Environmental impact and social equity will become key differentiators in procurement and investment decisions.

Next-Gen Workforce Enablement: Diagnostics firms must invest in training healthcare workers—both human and digital (e.g., AI agents)—to interpret and act on test results effectively.

Regulatory Harmonization: Efforts to streamline international regulatory pathways will accelerate global market entry and reduce time-to-impact.

Final Thoughts: A Call to Strategic Action

The HIV diagnostics market is no longer defined by incremental progress—it is being propelled by exponential innovation and systemic convergence. For C-suite leaders, this is a time for bold vision and decisive execution. Organizations that embrace the strategic imperatives outlined here—digital transformation, precision testing, cross-sector collaboration, and data-driven value creation—will not only capture market share but help reshape the global health narrative.

The future of HIV diagnostics lies not just in better tests, but in smarter ecosystems. Stakeholders who recognize and act on this reality will lead the next chapter of healthcare evolution.

For more information, Inquire Now!

0 notes

Text

Clinical Trials Market Size & Share: Analysis & Key Drivers

Executive Summary

The global clinical trials market is poised for substantial growth, driven by increasing demand for innovative drug development, rising investments in pharmaceutical and biotechnology research, and technological advancements. By 2025, the market is projected to reach USD 79.7 billion, with a compound annual growth rate (CAGR) of 5.8%. This growth is attributed to multiple factors, including the rising prevalence of chronic diseases, advancements in precision medicine, and the widespread adoption of decentralized and virtual clinical trials.

As we move towards 2032, the market is expected to surpass USD 94 billion. This article provides a comprehensive analysis of the global clinical trials market, exploring key trends, challenges, and opportunities shaping the industry. It also covers market segmentation, regional dynamics, and an in-depth competitive landscape, offering valuable insights into this dynamic sector.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40622-global-clinical-trials-market

Clinical Trials Market Overview

The clinical trials market represents a critical aspect of the pharmaceutical and biotechnology sectors, where new drugs and therapies are rigorously tested for safety and efficacy. The increasing complexity of diseases, particularly chronic conditions such as cancer, diabetes, and neurological disorders, is driving demand for more specialized and targeted clinical trials.

Key Drivers of Growth

Rising Prevalence of Chronic Diseases: The global increase in chronic diseases is placing immense pressure on healthcare systems, necessitating the development of novel therapeutic solutions. This trend is particularly evident in oncology, cardiology, and neurology, where clinical trials are essential for advancing treatment options.