#Containerized Data Center Market Driver

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

US Tumblr user growth rate is estimated to slow down to 4.1%.

Text

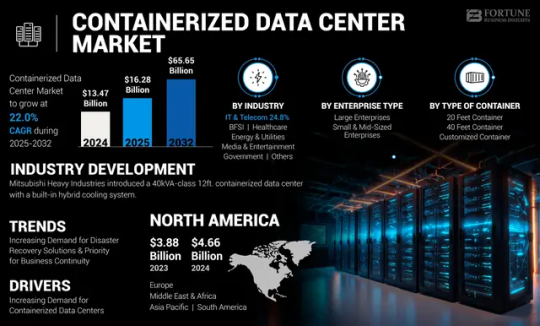

Containerized Data Center Market Size Expected to Reach USD 65.65 Bn By 2032

The global Containerized Data Center Market Industry was valued at USD 13.47 billion in 2024 and is projected to grow to USD 65.65 billion by 2032, exhibiting a CAGR of 22.0% during the forecast period (2025–2032). As organizations worldwide seek scalable, portable, and energy-efficient IT infrastructure, containerized solutions are rapidly transforming the data center landscape.

Key Market Highlights:

2024 Global Market Size: USD 13.47 billion

2025 Forecast Start: USD 16.28 billion

2032 Global Market Size: USD 65.65 billion

CAGR (2025–2032): 22.0%

U.S. Forecast (2032): USD 16.81 billion

Primary Growth Drivers: Surge in edge computing, need for rapid deployment, and energy-efficient infrastructure

U.S. Market Outlook:

The U.S. containerized data center market is forecasted to reach USD 16.81 billion by 2032, supported by:

Strong demand for modular, energy-efficient, and scalable data center infrastructure

Federal and enterprise initiatives to reduce carbon footprints

Rising IT workloads across cloud, AI, 5G, and IoT ecosystems

Data center growth in underserved and remote regions via mobile and edge deployments

Top Players in the Containerized Data Center Market:

IBM Corporation

Hewlett Packard Enterprise (HPE)

Huawei Technologies Co., Ltd.

Dell Technologies Inc.

Schneider Electric SE

Cisco Systems, Inc.

Rittal GmbH & Co. KG

Eaton Corporation

Vertiv Group Corp.

ZTE Corporation

Cannon Technologies Ltd.

Request Free Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/containerized-data-center-market-108571

Market Dynamics:

Key Growth Drivers:

Rapid Deployment Needs: Prefabricated modules allow setup in weeks vs. months

Energy Efficiency Focus: High demand for sustainable and lower-PUE designs

Edge Computing Expansion: Mobile and edge data centers enabling low-latency processing

Disaster Recovery & Military Use: Ruggedized units for defense, healthcare, and emergencies

Space and Cost Constraints: Containerized systems reduce facility footprint and CAPEX

Key Opportunities:

5G Rollouts: Driving demand for local data processing units

Smart City Infrastructure: Scalable data solutions for urban connectivity and automation

Emerging Markets: Modular systems supporting digital transformation in APAC, MEA, and LATAM

AI & ML Workloads: On-premise processing power in controlled and scalable containers

Data Sovereignty Requirements: Countries preferring in-region containerized solutions.

Emerging Trends:

Integration with renewable energy systems (solar-powered containers)

AI-enhanced cooling and remote management

Smart grid support and edge-data aggregation

Containerized HPC (High Performance Computing) for research and genomics

Use of circular economy principles in materials and design

Speak to Analysts: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/containerized-data-center-market-108571

Technology & Application Scope:

Deployment Types:

All-in-one (IT, power, cooling pre-integrated)

Customized (user-defined IT + cooling)

Container Sizes: 20-ft, 40-ft ISO containers

Cooling Systems: Integrated HVAC, in-row cooling, liquid cooling options

End Users:

Cloud service providers

Telecom operators

Military & defense

BFSI

Government & public sector

Healthcare providers

Recent Developments:

March 2024 – Vertiv unveiled its SmartMod Max containerized data center solution tailored for the U.S. telecom sector, integrating AI-powered cooling and real-time monitoring.

July 2023 – Schneider Electric partnered with a major U.S. energy provider to deploy modular edge data centers powered entirely by renewable sources in rural communities.

Conclusion:

Containerized data centers are reshaping global IT infrastructure with agility, sustainability, and scalability at the core. The U.S. market is particularly poised for robust growth through 2032, as organizations move to meet data demand while reducing environmental impact. With modularity becoming the new normal, players who combine efficiency, customization, and reliability will define the future of modern infrastructure deployment.

Frequently Asked Questions:

What is the projected value of the global containerized data center market by 2032?

What was the total market value of containerized data centers in 2024?

What is the expected compound annual growth rate (CAGR) for the market during the forecast period of 2025 to 2032?

Which industry segment dominated the containerized data center market in 2023?

Who are the major companies operating in the containerized data center space?

Which region held the largest market share in 2023?

#Containerized Data Center Market Share#Containerized Data Center Market Size#Containerized Data Center Market Industry#Containerized Data Center Market Driver#Containerized Data Center Market Analysis#Containerized Data Center Market Growth

0 notes

Text

Top Trends Reshaping the GCC Data Centre Landscape This Year

Unraveling the Exponential Rise of the GCC Data Center Market Ecosystem

The Gulf Cooperation Council data center market stands at the forefront of regional digital transformation, propelled by surging demand for resilient IT infrastructure, AI integration, and edge computing capabilities. As we project forward, the GCC data center market-valued at USD 5.87 billion in 2024—is set to experience a seismic expansion, reaching an anticipated USD 33.05 billion by 2031, growing at a CAGR of 12.3%. This trajectory is underpinned by high-performance computing demands, smart city initiatives, sovereign digital strategies, and the accelerated adoption of hybrid cloud frameworks.

Request Sample Report PDF (including TOC, Graphs & Tables): https://www.statsandresearch.com/request-sample/40593-data-center-industry-analysis

Technological Drivers Reshaping GCC’s Digital Backbone

Edge Computing and AI: Catalysts of Infrastructure Evolution

The fusion of edge computing and artificial intelligence is redefining the physical and operational contours of data center infrastructure. These technologies enable real-time data processing, lower latency, and enhanced bandwidth efficiency—essentials in a region increasingly reliant on IoT, autonomous systems, and immersive media.

Edge Data Centers are proliferating across urban and remote industrial zones to reduce network latency and support mission-critical applications in telecom, logistics, and smart utilities.

AI-powered infrastructure management enables predictive maintenance, workload optimization, and autonomous scalability, aligning with sustainability goals and uptime assurance.

Cloud-Native Transformation and Multi-Cloud Adoption

Enterprise and government adoption of hybrid and multi-cloud ecosystems is fueling demand for flexible, modular, and scalable data centers. Organizations are rapidly transitioning from legacy systems to cloud-native architectures that support containerization, orchestration (e.g., Kubernetes), and zero-trust security postures.

Get up to 30%-40% Discount: https://www.statsandresearch.com/check-discount/40593-data-center-industry-analysis

Key GCC Data Center Market Segments and Growth Benchmarks:

Data Center Types: Segment-Wise Expansion

Enterprise Data Centers dominate current deployment, with projections reaching USD 12.69 billion by 2031. These are favored by banks, government entities, and large corporations for security, compliance, and customization.

Edge Data Centers, expected to grow at a CAGR of 13.3%, are essential for latency-sensitive operations—especially in retail, telecom, and autonomous industries.

By Component: IT Infrastructure Leads the Stack

IT Infrastructure, valued at USD 7.27 billion in 2024, comprises compute, storage, and networking units. The sector will nearly double by 2031, reaching over USD 16 billion.

Management Software emerges as the fastest-growing component (13.9% CAGR), driven by demand for automated orchestration, resource analytics, and energy optimization.

Tier Standards: Reliability as a Strategic Differentiator

Tier III Data Centers remain the enterprise standard for redundancy and availability, offering a balance between cost-efficiency and resilience.

Tier IV Data Centers are witnessing increased adoption in financial and defense sectors due to their fault-tolerant architectures and unmatched uptime assurance.

Enterprise Demand: SME Acceleration and Enterprise Stability

Large Enterprises will remain dominant consumers, owing to vast operational scale and stringent compliance requirements.

SMEs, however, will outpace in growth (12.8% CAGR), increasingly leveraging colocation and cloud-managed data services to fuel innovation and agility.

Industry Verticals: IT and Telecom Anchor Growth

IT & Telecom, accounting for USD 3.83 billion in 2024, drive GCC data center market dominance through robust connectivity and digital service demand.

Retail, with the highest CAGR of 13.3%, is expanding rapidly due to rising e-commerce penetration and digital payment infrastructure.

Geographic Landscape: Market Expansion Across the GCC

United Arab Emirates: The Regional Nucleus of Digital Infrastructure

With a GCC data center market value of USD 4.91 billion in 2024, the UAE leads in regional data center development. Its progressive regulatory landscape, free zones (like Dubai Internet City), and focus on AI strategy and cloud governance position it as the premier data hub.

Saudi Arabia: Hyper-Scaling Through Vision 2030

Saudi Arabia's Vision 2030 initiatives are accelerating digital infrastructure deployment. Projected to grow at a CAGR of 12.7%, the Kingdom is investing in hyperscale facilities and AI-integrated networks to empower its Smart Nation ambitions and government digital services.

GCC Data Center Market Forces and Challenges

GCC Data Center Market Growth Drivers

Proliferation of smart city initiatives, such as NEOM and Masdar.

National cloud-first policies and rising government investments.

Accelerated digital adoption across BFSI, healthcare, and manufacturing.

Constraints and Strategic Hurdles

Acute skills shortage in high-density data center operations.

Escalating OPEX due to cooling and power requirements in desert climates.

Regulatory complexities and varying data sovereignty frameworks across GCC nations.

Key Players and Strategic Developments

Major incumbents and rising challengers are reshaping the competitive landscape through aggressive capital expenditures, greenfield projects, and regional collaborations.

Major Developments

Batelco’s White Space Data Center in Bahrain, developed with Almoayyed Contracting Group, introduces a high-density, energy-efficient facility adjacent to a solar farm—marking a regional milestone in sustainable infrastructure.

Ooredoo’s USD 1 billion investment, backed by QAR 2 billion in financing, aims to scale their data center capacity beyond 120MW, with AI and cloud infrastructure at the core.

GCC Data Center Market Leaders

Equinix – Expanding interconnection hubs and hybrid cloud onramps.

Khazna Data Centers – Driving hyperscale growth with government-backed investment.

STC Solutions and Mobily – Enhancing regional content delivery and 5G edge integration.

Microsoft Azure – Strengthening sovereign cloud services and AI deployment.

Strategic Outlook and Market Forecast

The GCC data center market is rapidly transitioning from traditional IT support roles to becoming central to digital economic competitiveness. As sovereign data strategies, AI integration, and decentralized architectures take hold, the region’s data center industry is set to become one of the fastest-growing globally.

By 2031, Tier IV and Edge Data Centers will define market leadership.

Public-private partnerships, sovereign fund allocations, and energy innovations will drive infrastructure resilience and global competitiveness.

Green data centers, leveraging renewable energy and liquid cooling technologies, will gain prominence amid growing environmental mandates.

Purchase Exclusive Report: https://www.statsandresearch.com/enquire-before/40593-data-center-industry-analysis

Final Word

We are entering a transformative era in the GCC’s digital infrastructure ecosystem. The convergence of policy, technology, and private capital is accelerating the rise of a hyperconnected, data-driven Gulf economy. Those who invest now in future-ready, AI-integrated, edge-enabled data center architecture will lead the next chapter of the region’s digital revolution.

Our Services:

On-Demand Reports: https://www.statsandresearch.com/on-demand-reports

Subscription Plans: https://www.statsandresearch.com/subscription-plans

Consulting Services: https://www.statsandresearch.com/consulting-services

ESG Solutions: https://www.statsandresearch.com/esg-solutions

Contact Us:

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

1 note

·

View note

Text

DDR4 RAM Market to reach US$ 18,600 million by 2032, at a CAGR of -3.24%

Global DDR4 RAM Market size was valued at US$ 23,800 million in 2024 and is projected to reach US$ 18,600 million by 2032, at a CAGR of -3.24% during the forecast period 2025-2032.

DDR4 RAM (Double Data Rate 4 Synchronous Dynamic Random-Access Memory) represents the fourth generation of DDR memory technology. These high-speed memory modules deliver improved performance, lower power consumption (1.2V operating voltage), and higher data transfer rates (up to 3200 MT/s) compared to previous DDR3 standards. Key variants include 4GB, 8GB, 16GB and 32GB modules catering to different computing requirements.

While enterprise server upgrades continue driving bulk demand, the consumer segment shows strong growth due to gaming PCs and high-performance workstations. The 32GB module segment is projected to grow at 8.2% CAGR through 2032 as applications demand higher memory capacities. However, supply chain constraints and the gradual transition to DDR5 present challenges. Major manufacturers like Samsung (holding 42% market share) and SK Hynix are investing in production capacity expansions to meet growing demand across data center and automotive applications.

Get Full Report : https://semiconductorinsight.com/report/ddr4-ram-market/

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of High-Performance Computing to Fuel DDR4 Demand

The global DDR4 RAM market is experiencing robust growth, driven by accelerating adoption across data centers, cloud computing, and enterprise applications. Modern workloads in artificial intelligence, machine learning, and big data analytics demand faster memory bandwidth and lower power consumption – capabilities where DDR4 excels over previous generations. The technology’s 50% higher bandwidth efficiency and 20% lower operating voltage compared to DDR3 make it indispensable for performance-intensive scenarios. Enterprise server deployments continue to favor DDR4 modules, with average per-server memory capacity growing 15-20% annually to handle virtualization and containerization requirements.

5G Infrastructure Rollout Accelerating Memory Requirements

Telecommunications infrastructure upgrades represent another significant growth vector. As 5G networks achieve broader deployment globally, base stations and edge computing nodes require high-density DDR4 solutions to manage increased data throughput. Network function virtualization (NFV) implementations particularly benefit from DDR4’s 3200 Mbps transfer rates when processing real-time analytics. The technology’s superior signal integrity also makes it ideal for the low-latency requirements of next-generation networks. Memory manufacturers report that 5G-related orders now account for over 30% of industrial DDR4 shipments, a figure projected to increase as standalone 5G cores become standard.

➤ Major hyperscale data centers are now standardizing on 64GB DDR4 RDIMMs as baseline memory configuration, driving double-digit year-over-year growth in enterprise segment.

Consumer electronics remain a vital market driver, with gaming PCs and workstations adopting higher-capacity DDR4 configurations. The shift toward hybrid work models has sustained demand for performance-optimized systems, where DDR4’s balance of speed and efficiency delivers tangible user benefits. This segment demonstrates particular elasticity, with premium configurations frequently outperforming market forecasts.

MARKET RESTRAINTS

DDR5 Transition Creating Market Uncertainty

While DDR4 maintains strong market positioning, the accelerating adoption of DDR5 technology introduces competitive pressures. Next-generation platforms from major CPU vendors now natively support DDR5, offering 50% greater bandwidth and improved power efficiency. This transition has created bifurcation in procurement strategies, particularly in the enterprise segment where long-term infrastructure planning must balance current DDR4 availability against future DDR5 roadmaps. Industry analysis suggests that while DDR4 will remain relevant through 2026, its share of new system deployments could decrease by 15-20% annually as DDR5 achieves price parity.

Other Restraints

Geopolitical Factors Affecting Supply Chains Trade restrictions and semiconductor export controls continue disrupting memory supply chains. Certain regional markets face 8-12 week lead times for specialty DDR4 products, forcing OEMs to maintain elevated inventory levels. These constraints particularly impact industrial and medical applications where component qualification processes limit supplier flexibility.

Pricing Volatility in Commodity Segments Standard DDR4 modules experience price sensitivity in consumer channels, with 10-15% quarterly fluctuations based on wafer allocation decisions. This volatility complicates inventory management for system integrators and distributors operating with narrow margins.

MARKET CHALLENGES

Thermal and Power Constraints in High-Density Configurations

As DDR4 implementations push density boundaries with 32GB and 64GB modules, thermal management becomes increasingly complex. Server deployments utilizing eight or more DIMMs per CPU socket must carefully balance performance targets with power budgets. Signal integrity challenges escalate at higher frequencies, requiring sophisticated PCB designs and voltage regulation modules that add 10-15% to bill of materials costs. These engineering constraints limit adoption in price-sensitive edge computing applications where simpler DDR3 solutions often remain technically adequate.

Manufacturers face additional validation challenges when supporting legacy platforms. With DDR4 specifications spanning multiple JEDEC standards and vendor-specific implementations, ensuring compatibility across generations of host controllers demands extensive qualification testing. This complexity particularly affects industrial applications requiring decade-long component availability guarantees.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and IoT Ecosystems

Automotive computing architectures present significant untapped potential for DDR4 adoption. Advanced driver assistance systems (ADAS) and in-vehicle infotainment platforms increasingly require the reliability and bandwidth that DDR4 provides. With automotive memory markets projected to grow at 12% CAGR, suppliers are developing ruggedized modules meeting AEC-Q100 qualification standards. These solutions address the harsh operating environments of electric and autonomous vehicles while providing the deterministic latency required for safety-critical systems.

The proliferation of industrial IoT gateways creates adjacent opportunities. Smart manufacturing implementations utilize DDR4 in edge computing nodes that aggregate sensor data and run predictive analytics. Unlike consumer applications, these deployments prioritize longevity and stability over peak performance – characteristics aligning well with DDR4’s mature ecosystem. Suppliers now offer extended lifecycle versions with 7-10 year availability guarantees to meet industrial procurement requirements.

Memory technology transitions always create nuanced market dynamics. While DDR5 represents the future, DDR4’s cost-performance balance and extensive qualification base ensure its relevance across multiple industries for years to come. Strategic focus on high-value applications rather than broad commoditization will define supplier success during this transitional period.

DDR4 RAM MARKET TRENDS

Growing Demand for High-performance Computing Drives DDR4 Adoption

The global DDR4 RAM market continues to experience robust growth, driven by increasing demand for high-performance computing across multiple industries. DDR4 technology, offering superior bandwidth (up to 3200 Mbps) and lower power consumption (1.2V compared to DDR3’s 1.5V), has become the standard for modern computing systems. Recent market analyses indicate that the 32GB module segment shows the fastest growth, projected to expand at a compound annual growth rate exceeding 15% through 2032. This trend aligns with the requirements of data-intensive applications in AI, machine learning, and cloud computing sectors.

Other Trends

Consumer Electronics Miniaturization

The ongoing miniaturization of consumer electronics coupled with performance demands is reshaping DDR4 implementation strategies. Manufacturers are developing low-profile DDR4 modules with capacities reaching 16GB in single-die packages for ultra-thin laptops and IoT devices. The consumer electronics segment accounted for approximately 42% of total DDR4 shipments last year as premium smartphones increasingly incorporate LPDDR4X variants. This specialization enables 30% power reduction while maintaining performance benchmarks critical for battery-powered devices.

Automotive Sector Emerges as Strategic Growth Area

Automotive applications present a significant growth opportunity as vehicle architectures evolve toward connected and autonomous platforms. The automotive DDR4 market is projected to triple by 2028 as advanced driver assistance systems (ADAS) and in-vehicle infotainment require reliable, high-bandwidth memory solutions. These specialized automotive-grade modules feature extended temperature ranges (-40°C to 105°C) and enhanced error correction capabilities. Leading manufacturers have formed partnerships with Tier 1 automotive suppliers to develop customized solutions meeting stringent AEC-Q100 qualification standards.

Supply Chain Diversification

Recent geopolitical tensions have accelerated supply chain restructuring in the memory sector. While Samsung and SK Hynix maintain approximately 68% combined market share, regional players like China’s CXMT and Taiwan’s Nanya Technology are expanding production capacities. Industry reports indicate over $25 billion in new fabrication investments announced across Asia through 2026, targeting both mainstream DDR4 and next-generation technologies. This geographic diversification aims to mitigate risks while meeting growing demand, particularly in emerging markets where local sourcing requirements are becoming more prevalent.

COMPETITIVE LANDSCAPE

Key Industry Players

Memory Giants Compete Through Innovation and Strategic Capacity Expansions

The global DDR4 RAM market is dominated by a handful of memory semiconductor heavyweights, creating an oligopolistic competitive environment. As of 2024, the top five manufacturers collectively held approximately 78% of global revenue share, with Samsung Electronics maintaining its pole position through technological leadership in high-density modules and superior manufacturing yields. The South Korean giant’s market dominance stems from its vertical integration capabilities and continuous R&D investments exceeding $15 billion annually in semiconductor development.

SK Hynix and Micron Technology follow closely, leveraging their advanced fabrication facilities and patented memory architectures. These players are aggressively transitioning production to more advanced nodes (1α nm and below) to improve power efficiency and density – critical factors driving adoption in data center and mobile applications. Both companies recently announced billion-dollar expansions of their DRAM fab capacities in response to growing cloud infrastructure demand.

Meanwhile, emerging Chinese players like CXMT (ChangXin Memory Technologies) are disrupting the market through aggressive pricing and government-backed capacity expansions. While currently holding single-digit market share, these domestic champions are rapidly closing the technology gap through licensing agreements and reverse engineering.

List of Key DDR4 RAM Manufacturers

Samsung Electronics (South Korea)

SK Hynix (South Korea)

Micron Technology (U.S.)

Nanya Technology (Taiwan)

Winbond Electronics (Taiwan)

Powerchip Semiconductor Manufacturing Corp. (Taiwan)

ChangXin Memory Technologies (China)

Shenzhen Longsys Electronics (China)

Segment Analysis:

By Type

32G Segment Leads Growth Due to High-Performance Computing Demands

The market is segmented based on type into:

32G

16G

8G

4G

By Application

Consumer Electronics Dominates Market Share Owing to Proliferation of Smart Devices

The market is segmented based on application into:

Industrial Computers

Medical

Automotive

Consumer Electronics

Regional Analysis: DDR4 RAM Market

North America The North American DDR4 RAM market is characterized by strong demand from enterprise data centers, gaming industries, and high-performance computing applications. The U.S. dominates regional consumption, driven by technological advancements and significant investments in IT infrastructure. However, the gradual transition to DDR5 in premium segments is creating pricing pressures on DDR4 products. Major manufacturers like Micron Technology and Intel continue to innovate with higher-density modules (32G/16G) to meet data center needs. While commercial adoption remains steady, consumer demand is slowing due to market saturation and longer upgrade cycles.

Europe Europe’s DDR4 RAM market relies heavily on automotive electronics and industrial computing applications, where reliability and mid-range performance are prioritized. Germany and France lead in automotive semiconductor consumption, with DDR4 being integral to advanced driver-assistance systems (ADAS). However, strict EU regulations on energy efficiency and e-waste recycling are pushing manufacturers toward eco-design principles. The competitive landscape features strong local procurement policies, with companies like SK Hynix expanding production facilities in Eastern Europe. The region also sees steady demand from medical imaging systems, which require stable, high-bandwidth memory solutions.

Asia-Pacific As the largest regional market, Asia-Pacific benefits from massive electronics manufacturing hubs in China, South Korea, and Taiwan. Samsung and SK Hynix control significant market shares, benefiting from vertical integration with local OEMs. China’s push for semiconductor self-sufficiency has led to increased DDR4 production by domestic players like CXMT, though quality gaps remain compared to global leaders. The 16G segment dominates due to balanced cost-performance ratios favored by smartphone and PC manufacturers. Despite growing DDR5 adoption in flagship devices, DDR4 maintains strong demand across mid-tier consumer electronics and IoT devices.

South America The South American DDR4 RAM market faces constraints from currency volatility and reliance on imports, with Brazil being the primary consumption center. Local assembly of computers and servers creates consistent demand, but infrastructure limitations hinder large-scale data center growth. Price sensitivity leads to higher sales of 4G-8G modules for entry-level devices. Political instability in key markets occasionally disrupts supply chains, forcing distributors to maintain higher inventory buffers. Nonetheless, increasing digitization in banking and public sectors offers stable opportunities for industrial-grade memory solutions.

Middle East & Africa This emerging market shows fragmented growth patterns, with UAE and Saudi Arabia driving demand through smart city initiatives and data center construction. The lack of local semiconductor manufacturing results in complete dependence on imports, primarily from Asian suppliers. Government IT modernization projects sustain steady demand for server-grade DDR4, while consumer markets lag due to low disposable incomes. The region also serves as a secondary market for refurbished DDR4 modules from Europe and North America, creating price competition for new products. Long-term growth potential exists in 5G infrastructure deployments, which will require compatible memory solutions.

Download a Sample Report : https://semiconductorinsight.com/download-sample-report/?product_id=97961

Report Scope

This market research report provides a comprehensive analysis of the global and regional DDR4 RAM markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global DDR4 RAM market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (32G, 16G, 8G, 4G), technology, application (Industrial Computer, Medical, Automotive, Consumer Electronics), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market size is estimated at USD million in 2024, while China is expected to reach USD million.

Competitive Landscape: Profiles of leading market participants including Samsung, SK Hynix, Intel, Micron Technology, and Nanya Technology, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

Technology Trends & Innovation: Assessment of emerging memory technologies, integration with next-gen computing platforms, semiconductor design trends, and evolving industry standards.

Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

Customisation of the Report In case of any queries or customisation requirements, please connect with our sales team, who will ensure that your requirements are met.

Contact us:

+91 8087992013

0 notes

Text

Chile Data Center Cooling Market Size, Drivers, Opportunities & Market Trends

Chile Data Center Cooling Market Overview The Chile data center cooling market is experiencing significant growth, driven by the rapid expansion of cloud computing, big data analytics, and digital transformation across various industries. As of 2025, the market size is estimated to be valued at approximately USD 120 million, with a robust compound annual growth rate (CAGR) projected between 8% to 10% over the next 5 to 10 years. This growth is underpinned by increasing demand for energy-efficient cooling solutions to manage the escalating heat loads from high-density data center deployments. Key factors propelling the market include Chile’s growing investment in IT infrastructure, rising internet penetration, and governmental initiatives promoting smart city projects and digital economies. Additionally, the trend towards modular and scalable data centers necessitates advanced cooling systems such as liquid cooling, free cooling, and AI-powered thermal management. The surge in hyperscale data centers by cloud service providers and colocation facilities is further accelerating the adoption of innovative cooling technologies. Chile Data Center Cooling Market Dynamics Drivers: The primary growth drivers in the Chile market include increasing digitalization, rising demand for cloud services, and the imperative to reduce operational costs through energy-efficient cooling technologies. Environmental concerns and government mandates on carbon footprint reduction are also fostering the adoption of green cooling solutions such as evaporative cooling and geothermal systems. Restraints: Despite growth prospects, the market faces challenges including high initial capital expenditure for advanced cooling infrastructure, fluctuating electricity costs, and limited skilled labor for installation and maintenance of sophisticated systems. Additionally, the intermittency of renewable energy sources poses challenges for integrating sustainable cooling solutions consistently. Opportunities: Chile’s strategic location and increasing foreign direct investment in technology sectors present opportunities for expanding data center infrastructure. Furthermore, emerging technologies such as AI-based predictive cooling, edge computing, and integration of renewable energy sources can redefine market potential. Regulatory frameworks encouraging sustainability and energy efficiency also open avenues for innovation and collaboration among vendors and operators. Download Full PDF Sample Copy of Chile Data Center Cooling Market Report @ https://www.verifiedmarketresearch.com/download-sample?rid=503224&utm_source=PR-News&utm_medium=361 Chile Data Center Cooling Market Trends and Innovations The market is witnessing a paradigm shift towards eco-friendly and energy-optimized cooling solutions. Key trends include the rise of liquid cooling technologies that offer superior thermal management for high-performance computing equipment. Immersion cooling is gaining traction as it reduces energy consumption and increases hardware longevity. Another significant innovation is the incorporation of AI and IoT-driven cooling systems that enable real-time monitoring and dynamic adjustment of cooling loads, enhancing efficiency and minimizing downtime. Collaborative ventures between data center operators, cooling technology providers, and energy companies are fostering the development of hybrid cooling systems combining traditional HVAC with renewable energy-driven solutions. Furthermore, the adoption of modular and containerized cooling units allows for scalable and flexible deployments, aligning with the growing demand for edge data centers in remote and industrial locations across Chile. Chile Data Center Cooling Market Challenges and Solutions Supply chain disruptions, particularly in sourcing specialized cooling components, have been a notable hurdle, exacerbated by global logistics constraints and fluctuating raw material costs. Pricing pressures due to competition and the high costs of cutting-edge cooling technologies also pose challenges for market players.

Regulatory complexity, especially concerning environmental compliance and energy usage standards, can delay project approvals and increase operational burdens. To address these challenges, stakeholders are focusing on diversifying supplier bases, investing in local manufacturing capabilities, and leveraging government incentives for sustainable infrastructure development. Enhanced collaboration with technology partners and adopting modular, scalable cooling designs can reduce upfront costs and improve time-to-market. Training programs aimed at building a skilled workforce for advanced cooling system maintenance are also vital for overcoming operational challenges. Chile Data Center Cooling Market Future Outlook Looking ahead, the Chile data center cooling market is poised for sustained expansion driven by continuous digital transformation, increasing cloud adoption, and rising data center capacities. The integration of renewable energy sources and the transition to zero-carbon cooling technologies will be critical factors shaping future market dynamics. Advancements in AI-driven predictive maintenance, thermal analytics, and adaptive cooling architectures will enhance operational efficiency and reduce total cost of ownership, making data centers more sustainable and resilient. The government’s commitment to sustainability and digital infrastructure modernization will further catalyze investments and innovation. Overall, the market is expected to evolve with a greater focus on energy efficiency, environmental compliance, and scalability, positioning Chile as a strategic hub for data center operations in Latin America. Chile Data Center Cooling Market Competitive Landscape The Chile Data Center Cooling Market competitive landscape is characterized by intense rivalry among key players striving to gain market share through innovation, strategic partnerships, and expansion initiatives. Companies in this market vary from established global leaders to emerging regional firms, all competing on parameters such as product quality, pricing, technology, and customer service. Continuous investments in research and development, along with a focus on sustainability and digital transformation, are common strategies. Mergers and acquisitions further intensify the competition, allowing companies to broaden their portfolios and geographic presence. Market dynamics are influenced by evolving consumer preferences, regulatory frameworks, and technological advancements. Overall, the competitive environment fosters innovation and drives continuous improvement across the Chile Data Center Cooling Market ecosystem. Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount?rid=503224&utm_source=PR-News&utm_medium=361 Chile Data Center Cooling Market Segmentation Analysis The Chile Data Center Cooling Market segmentation analysis categorizes the market based on key parameters such as product type, application, end-user, and region. This approach helps identify specific consumer needs, preferences, and purchasing behavior across different segments. By analyzing each segment, companies can tailor their strategies to target high-growth areas, optimize resource allocation, and improve customer engagement. Product-based segmentation highlights variations in offerings, while application and end-user segmentation reveal usage patterns across industries or demographics. Regional segmentation uncovers geographical trends and market potential in emerging and developed areas. Chile Data Center Cooling Market, By Type Chile Data Center Cooling Market, By Application Chile Data Center Cooling Market, By End User Chile Data Center Cooling Market, By Geography • North America• Europe• Asia Pacific• Latin America• Middle East and Africa For More Information or Query, Visit @ https://www.verifiedmarketresearch.com/product/chile-data-center-cooling-market/ About Us: Verified Market Research Verified Market Research is a leading Global Research and Consulting firm servicing over 5000+ global clients.

We provide advanced analytical research solutions while offering information-enriched research studies. We also offer insights into strategic and growth analyses and data necessary to achieve corporate goals and critical revenue decisions. Our 250 Analysts and SMEs offer a high level of expertise in data collection and governance using industrial techniques to collect and analyze data on more than 25,000 high-impact and niche markets. Our analysts are trained to combine modern data collection techniques, superior research methodology, expertise, and years of collective experience to produce informative and accurate research. Contact us: Mr. Edwyne Fernandes US: +1 (650)-781-4080 US Toll-Free: +1 (800)-782-1768 Website: https://www.verifiedmarketresearch.com/ Top Trending Reports https://www.verifiedmarketresearch.com/ko/product/laser-interferometer-market/ https://www.verifiedmarketresearch.com/ko/product/hybrid-printing-market/ https://www.verifiedmarketresearch.com/ko/product/interposer-and-fan-out-wafer-level-packaging-market/ https://www.verifiedmarketresearch.com/ko/product/russia-automotive-glass-fiber-composites-market/ https://www.verifiedmarketresearch.com/ko/product/united-states-contraceptive-devices-market/

0 notes

Text

Car Carrier Market to Surpass $27.9B by 2034 | 7.1% CAGR

Car Carrier Market Set to Soar from $14.1B in 2024 to $27.9B by 2034! 🌍Growing at a CAGR of 7.1%, the global car carrier market is shifting into high gear, fueled by the rise in automotive production, international trade, and increasing consumer demand for secure and efficient vehicle transport. This dynamic industry includes specialized marine vessels, trucks, rail systems, and even air transport designed to move cars safely and quickly across vast distances. In 2024, the market handled an impressive 180 million metric tons, with volumes expected to surge through 2034.

To Request Sample Report : https://www.globalinsightservices.com/request-sample/?id=GIS32212 &utm_source=SnehaPatil&utm_medium=Article

🚢 The roll-on/roll-off (RoRo) segment leads the market with a 45% share, renowned for its speed, efficiency, and cost-effectiveness in loading and unloading vehicles. 📦 Containerized car carriers follow at 30%, providing added protection and versatility during long hauls. 📊 Regionally, Asia-Pacific holds the top spot, thanks to rapid urbanization and booming auto exports from China and India. 🇺🇸 The United States and Europe trail close behind, supported by strong manufacturing bases and advanced logistics networks.

🌱 Sustainability is taking center stage, with eco-friendly transport solutions, digital tracking, and IoT integration enhancing operational efficiency and reducing emissions.

As auto demand surges globally, stakeholders in the car logistics space have an exciting road ahead.

#carcarrier #vehicletransport #automotivelogistics #roro #containertransport #fleetmanagement #globaltrade #smartlogistics #cargomovement #vehicledistribution #autotransport #supplychaininnovation #marinetransport #trucktransport #railtransport #automotiveindustry #infrastructuregrowth #freightservices #gpsfleettracking #iotinlogistics #telematics #smartshipping #logisticstechnology #customlogistics #fleetexpansion #dealershiplogistics #vehicletracking #automatedloading #urbanmobility #evlogistics #sustainablelogistics #multilevelcarriers #carhaulage #auctiontransport #industriallogistics #militarylogistics #digitalfreight #logisticsoptimization #logisticsfuture #transportautomation #automobility

Research Scope:

· Estimates and forecast the overall market size for the total market, across type, application, and region

· Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling

· Identify factors influencing market growth and challenges, opportunities, drivers, and restraints

· Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates

· Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

0 notes

Text

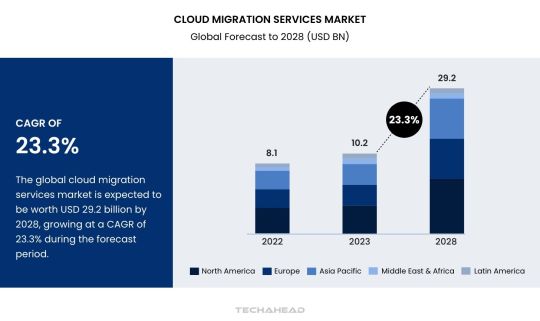

Explore the growth and trends in the cloud computing market, including key drivers, technologies, and industry applications. Understand the future of cloud computing and its impact on businesses globally.

Key Drivers of the Cloud Computing Market

1. Digital Transformation and Technological Advancements

The ongoing digital transformation in businesses worldwide has been one of the biggest catalysts for cloud adoption. As companies strive to remain competitive in an increasingly digital world, cloud computing offers them a way to innovate, improve operational efficiency, and enhance their service offerings.

Cloud technologies such as Artificial Intelligence (AI), Machine Learning (ML), the Internet of Things (IoT), and Big Data analytics have become more integrated into cloud platforms. These technologies enable businesses to harness the full potential of their data, deliver enhanced customer experiences, and automate critical processes—all of which are essential to the digitalization of industries across the globe.

The development of cloud-native technologies and containerization (e.g., Kubernetes) has further accelerated the adoption of cloud computing, allowing businesses to modernize their applications and infrastructure with greater flexibility and scalability.

2. Cost Efficiency and Scalability

One of the most compelling advantages of cloud computing is its ability to provide businesses with the scalability they need without the upfront capital expenditure required for traditional on-premise infrastructure. Cloud services allow organizations to pay only for the resources they use, enabling them to scale up or down based on demand.

This pay-as-you-go model provides significant cost savings for businesses, particularly small and medium-sized enterprises (SMEs) that may not have the resources to invest in their own data centers. The cloud eliminates the need for expensive hardware, software, and IT maintenance costs, making it an attractive solution for businesses seeking to optimize their budgets.

Furthermore, the ability to scale quickly and efficiently has made cloud computing the preferred solution for companies experiencing growth or those with fluctuating demands. Whether it's expanding server capacity for a short-term project or increasing storage space to accommodate new data, cloud platforms offer an unmatched level of flexibility.

3. Business Continuity and Disaster Recovery

Cloud computing has revolutionized how organizations approach business continuity and disaster recovery. Storing data and applications in the cloud ensures that businesses can access critical information in the event of a natural disaster, power outage, or hardware failure. Cloud service providers often have multiple data centers located in different regions, which ensures high availability and the redundancy of data storage.

Many cloud providers offer built-in disaster recovery capabilities, which reduce the need for businesses to maintain expensive disaster recovery infrastructure in-house. This is particularly beneficial for organizations operating in industries where downtime is costly or where data loss can result in significant financial or reputational damage.

4. Collaboration and Remote Work Solutions

The rise of remote work has further driven the adoption of cloud computing, as businesses require solutions that facilitate collaboration and communication between employees, regardless of their location. Cloud-based collaboration tools such as Google Workspace, Microsoft 365, and Slack have become essential for teams that need to work together in real-time, sharing documents, data, and files securely.

Cloud computing has empowered businesses to continue operations during the COVID-19 pandemic, with remote work becoming the norm for many industries. As hybrid and remote work models continue to gain popularity, the demand for cloud-based collaboration and productivity tools will continue to rise.

5. Security and Compliance

While security remains a concern for some organizations, cloud service providers have made significant advancements in cybersecurity to address these concerns. Leading cloud providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud offer robust security frameworks, including encryption, multi-factor authentication, and identity access management tools to protect sensitive data.

Moreover, cloud computing providers are also investing heavily in compliance with industry-specific regulations such as General Data Protection Regulation (GDPR), Health Insurance Portability and Accountability Act (HIPAA), and Payment Card Industry Data Security Standard (PCI DSS). These certifications ensure that organizations using the cloud can meet legal and regulatory requirements regarding data privacy and security.

0 notes

Text

"Power in a Box: Containerized Data Center Market Insights 2025–2033 📦⚡"

Containerized Data Center Market is at the forefront of revolutionizing data storage and management. These portable, modular solutions, housed in shipping containers, integrate power, cooling, and IT infrastructure, offering unmatched scalability and mobility. As the demand for energy-efficient and cost-effective solutions rises, this market is poised for robust growth.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS32243 &utm_source=SnehaPatil&utm_medium=Article

Key drivers include the expansion of cloud and edge computing and the growing need for disaster recovery solutions. The IT and telecom sector dominates the market with a 45% share, fueled by surging data traffic and increasing reliance on cloud services. The BFSI sector follows with a 30% share, leveraging containerized data centers for secure and rapid deployments.

Geographically, North America leads the market, benefiting from advanced IT infrastructure and early adoption of innovative technologies. Europe follows closely, with a focus on green data initiatives and modernization of data centers. The Asia-Pacific region is emerging as a high-growth area, driven by digital transformation and expanding internet penetration in developing economies.

Market segmentation highlights diverse offerings, including all-in-one, stand-alone, and customized containers. Key components such as servers, storage, and cooling systems are tailored to various applications, from BFSI and healthcare to telecommunications and energy.

The competitive landscape features prominent players like IBM, HPE, and Cisco, each shaping the industry with modular designs and energy-efficient solutions. Regulatory frameworks, such as GDPR and cybersecurity policies, significantly influence market dynamics. Despite challenges like high initial costs and evolving security threats, the integration of AI and IoT in data management presents exciting growth opportunities.

Future projections indicate a 15% rise in capital expenditure by 2033, spurred by investments in edge computing and advanced cooling technologies, ensuring a promising outlook for the containerized data center market.

#DataCenters #ModularSolutions #CloudComputing #EdgeComputing #ContainerizedDataCenters #ITInfrastructure #GreenDataCenters #DigitalTransformation #DataStorage #AIIntegration #IoTInnovation #BFSISolutions #EnergyEfficiency #DataManagement #FutureOfData

0 notes

Text

AWS Cloud Migration: Benefits, Strategies, and Phases Simplified

Many businesses embark on their cloud migration journey with a strategy known as “lift and shift.” This approach involves relocating existing applications from on-premises environments to the cloud without altering their architecture. It’s an efficient and straightforward starting point, often appealing due to its simplicity and speed.

However, as companies dive deeper into the cloud ecosystem, they uncover a broader spectrum of possibilities. Lift and shift, though effective initially, is only the foundation of cloud migration. Businesses quickly realize that cloud computing offers far more than just infrastructure relocation.

To unlock its true potential, modernization becomes essential. Modernization transforms applications to align with cloud-native architectures. This ensures businesses can harness advanced features like scalability, resilience, and cost efficiency. It’s no longer about merely shifting workloads; it’s about reimagining them for the future.

This evolution in approach is also reflected in the market’s staggering growth. According to Gartner, Inc., global end-user spending on public cloud services is projected to grow by 20.4% in 2024, reaching $675.4 billion from $561 billion in 2023. Generative AI (GenAI) and application modernization are major drivers of this surge. This data underscores the strategic importance of not just migrating to the cloud but modernizing applications to stay competitive in an evolving landscape.

For instance, early adopters of cloud migration often struggled with limited performance gains post-migration. They soon discovered that while lift and shift addressed immediate needs, it didn’t optimize long-term efficiency. Modernization solved this challenge by enabling applications to utilize the dynamic capabilities of cloud platforms.

This shift in approach isn’t just about technology—it’s about competitiveness. Businesses that embrace modernization gain agility and faster time-to-market, giving them a significant edge. They leverage tools like containerization and serverless computing, allowing seamless adaptation to evolving customer demands.

In this blog, we’ll delve into the reasons why lift and shift is just the starting line. We’ll also explore how modernization drives real value and share best practices for ensuring a smooth transition. By the end, you’ll understand why adapting to the evolving cloud landscape is not just a choice—it’s a necessity.

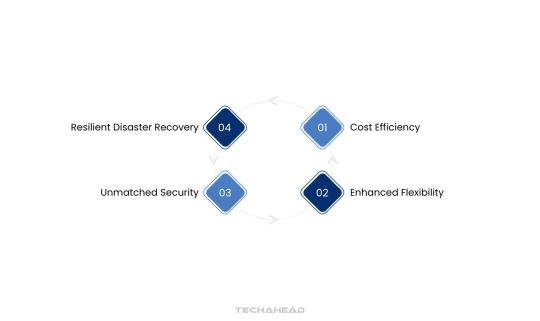

Benefits of AWS Migration

Transitioning your cloud infrastructure to the AWS cloud unlocks unparalleled scalability and efficiency. AWS provides a suite of advanced computing resources tailored to manage IT operations seamlessly. This enables your business to channel its efforts, resources, and investments into core activities that drive growth and profitability.

By adopting AWS cloud infrastructure, you eliminate the constraints of physical data centers and gain unrestricted, anytime-anywhere access to your data. Global giants like Netflix, Facebook and the BBC leverage AWS for its unmatched reliability and innovation. Let’s explore how AWS helps streamline IT operations while ensuring cost-effectiveness and agility.

Cost Efficiency

Expanding cloud infrastructure typically requires significant investment in hardware and administrative overhead. AWS eliminates these costs with a pay-as-you-go model.

Zero Upfront Investment: Run enterprise applications and systems without the need for large initial capital.

Flexible Scaling: AWS enables businesses to upscale or downscale resources instantly, ensuring that you never pay for unused capacity. This dynamic scaling matches your operational demands and avoids the waste associated with overprovisioning.

Advanced Cost Control: AWS provides tools like Cost Explorer and AWS Budgets, helping businesses track, forecast, and optimize cloud expenses. By analyzing consumption patterns, organizations can minimize waste and ensure maximum return on investment (ROI).

Reduced Maintenance Overheads: Without the need to maintain physical servers, businesses save on administrative and repair costs, redirecting budgets to strategic growth areas.

Enhanced Flexibility

AWS offers unparalleled adaptability, making it suitable for businesses of all sizes, whether they are start-ups, enterprises, or global businesses. Its integration capabilities enable smooth migrations and rapid scaling.

Seamless Compatibility: AWS supports a vast number of programming languages, operating systems, and database types. This ensures that existing applications or software frameworks can integrate effortlessly, eliminating time-consuming reconfigurations.

Rapid Provisioning of Resources: Whether migrating applications, launching new services, or preparing for DevOps, AWS provides the agility to provision resources instantly. For instance, during seasonal demand spikes, businesses can quickly allocate additional capacity and scale back during off-peak times.

Developer Productivity: Developers save time as they don’t need to rewrite codebases or adopt new frameworks. This allows them to focus on building innovative applications rather than troubleshooting compatibility issues.

Unmatched Security

Security is a cornerstone of AWS’s offerings, ensuring that your data remains protected against internal and external threats. AWS combines global infrastructure standards with customizable tools to meet unique security needs.

Shared Responsibility Model: AWS takes care of the underlying infrastructure, including physical security and global compliance. Customers are responsible for managing access, configuring permissions, and securing their data.

Data Encryption: AWS allows businesses to encrypt data both at rest and in transit, ensuring end-to-end protection. Businesses can leverage services like AWS Key Management Service (KMS) for robust encryption.

Compliance and Governance: AWS adheres to internationally recognized standards, including ISO 27001, GDPR, and SOC. This helps businesses meet legal and regulatory requirements with ease.

Threat Mitigation: AWS offers tools like AWS Shield and GuardDuty to detect and mitigate cybersecurity threats in real time, providing peace of mind in a rapidly evolving threat landscape.

Resilient Disaster Recovery

Disruption like power outages, data corruption, or natural disasters can cripple traditional IT systems. AWS AWS equips businesses with robust disaster recovery solutions to maintain operational continuity.

Automated Recovery Processes: AWS simplified disaster recovery through services like AWS Elastic Disaster Recovery, which automates recovery workflows and reduces downtime significantly.

Global Redundancy: Data is stored across multiple geographic locations, ensuring that even if one region experiences issues, operations can seamlessly shift to another. This minimizes disruptions and maintains business continuity.

Cost-Efficient Solutions: Unlike traditional disaster recovery setups that duplicate hardware, AWS’s cloud-based approach uses on-demand resources. This reduces capital investments while delivering the same level of protection.

Faster Recovery Times: With AWS, businesses can restore systems and data within minutes, ensuring minimal impact on operations and customer experiences.

Cloud migration with AWS is more than just a technological upgrade; it’s a strategic move that empowers businesses to innovate, scale, and thrive in a competitive market. By leveraging AWS, organizations can reduce costs, enhance flexibility, strengthen security, and ensure resilience.

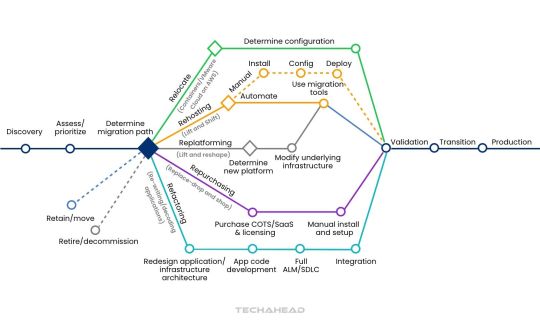

7 Cloud Migration Strategies for AWS

AWS’s updated 7 Rs model for cloud migration builds on Gartner’s original 5 Rs framework. Each strategy caters to unique workloads and business needs, offering a tailored approach for moving to the cloud. Let’s explore these strategies in detail.

Rehost (Lift and Shift)

The rehost strategy involves moving workloads to the cloud with minimal changes using Infrastructure-as-a-Service (IaaS). Enterprises migrate applications and dependencies as they are, retaining the existing configurations. This approach ensures operational consistency and reduces downtime during migration. It is an easy-to-perform option, especially for businesses with limited in-house cloud expertise. Additionally, rehosting helps businesses avoid extensive re-architecting, making it a cost-effective and efficient solution.

Relocate (Hypervision-Level Lift and Shift)

Relocating shifts workloads to a cloud-based platform without altering source code or disrupting ongoing operations. Organizations can transition from on-premises platforms like VMware to cloud services such as Amazon Elastic Kubernetes Service (EKS). This strategy minimizes downtime and ensures seamless business operations during migration. Relocating maintains existing configurations, eliminating the need for staff retraining or new hardware. It also offers predictable migration costs, with clear scalability limits to control expenses.

Replatform (Lift and Reshape)

The replatform approach optimizes workloads by introducing cloud-native features while maintaining the core application architecture. Applications are modernized to leverage automation, scalability, and cloud compliance without rewriting the source code. This strategy enhances resilience and flexibility while preserving legacy functionality. Partial modernization reduces migration costs and time while ensuring minimal disruptions. Teams can manage re-platformed workloads with ease since the fundamental application structure remains intact.

Refactor (Re-architect)

Refactoring involves redesigning workloads from scratch to utilize cloud-native technologies and features fully. This strategy supports advanced capabilities like serverless computing, autoscaling, and enhanced automation.

Refactored workloads are highly scalable and can adapt to changing demands efficiently. Applications are often broken into microservices, improving availability and operational efficiency. Although refactoring requires significant initial investment, it reduces long-term operational costs by optimizing the cloud framework.

Repurchase (Drop and Shop)

Repurchasing replaces existing systems with third-party solutions available on the cloud marketplace. Organizations adopt a Software-as-a-Service (SaaS) model, eliminating the need for infrastructure management. This approach reduces operational efforts and simplifies regulatory compliance, ensuring efficient governance. Repurchasing aligns IT costs with revenue through consumption-based pricing models. It also accelerates migration timelines, enhancing user experience and performance with minimal downtime.

Retire

The retirement strategy focuses on decommissioning applications that no longer hold business value. Inefficient legacy systems are terminated or downsized to free up resources for more critical functions. Retiring outdated workloads reduces operational costs and simplifies IT management. This strategy also allows businesses to streamline their application portfolio, focusing efforts on modernizing essential systems.

Retain (Revisit)

The retain strategy is used for applications that cannot yet be migrated to the cloud. Some workloads rely on systems that need to be transitioned first, making retention a temporary solution. Businesses may also retain applications while waiting for SaaS versions from third-party providers. Retaining workloads provides flexibility, allowing organizations to revisit migration strategies and align them with long-term objectives.

Cloud Transformation Phases

Cloud transformation is a comprehensive process where businesses transition from traditional IT infrastructure to a modern, cloud-centric framework. Below is an in-depth exploration of its critical phases.

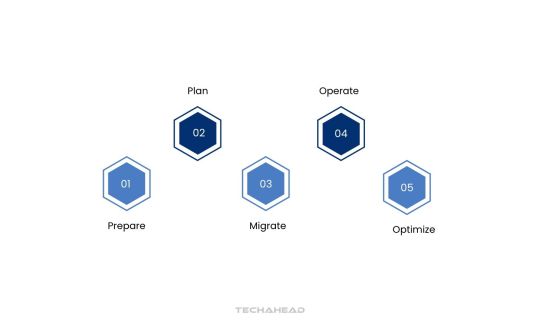

Prepare

The preparation phase sets the foundation for a successful migration by assessing feasibility and identity benefits.

Evaluate current IT infrastructure: Audit existing hardware, software, and networks to confirm if the cloud aligns with organizational goals. This step ensures clarity about readiness.

Identify potential risks: Analyze risks like data loss, downtime, or security threats. A detailed mitigation strategy ensures minimized disruptions.

Analyze interdependencies: Understand how applications, databases, and systems interact to prevent issues during migration. Dependency mapping is vital for seamless transitions.

Select a migration strategy: Choose from approaches such as rehosting, refactoring, or rebuilding. Tailor the strategy to meet specific organizational needs and ensure efficiency.

Plan

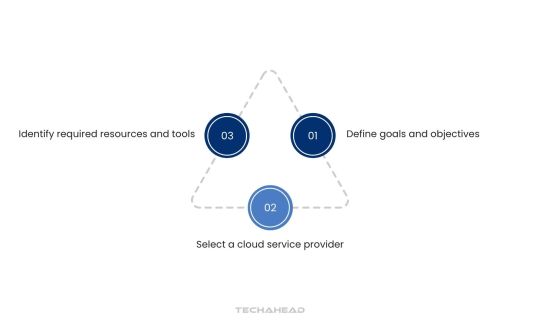

The planning phase involves creating a structured roadmap for the migration process, ensuring alignment with business objectives.

Define goals and objectives: Establish specific goals like cost reduction, scalability improvement, or enhanced security. This clarity drives project focus.

Select a cloud service provider: Choose a provider that matches your organization’s priorities. Evaluate cost, performance, security, and customer support before finalizing.

Identify required resources and tools: Determine essential resources such as migration tools, management software development, and skilled personnel to execute the project effectively.

Migrate

Migration focuses on the actual transfer of IT infrastructure, applications, and data to the cloud.

Configure and deploy cloud resources: Set up virtual machines, storage, and networking components to create a robust cloud environment for workloads.

Migrate data securely: Use data migration tools or replication techniques to ensure secure and accurate data transfer with minimal disruptions.

Test applications in the cloud: Run performance tests to verify that applications meet operational requirements. Address issues before full-scale deployment.

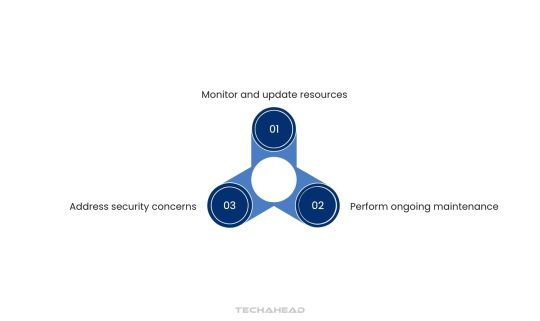

Operate

The operation phase emphasizes managing and maintaining the cloud environment for optimal performance.

Monitor and update resources: Continuously monitor cloud infrastructure to identify bottlenecks and ensure resources align with evolving organizational needs.

Perform ongoing maintenance: Proactively resolve infrastructure or application issues to prevent service interruptions and maintain system integrity.

Address security concerns: Implement robust security measures, including encryption, access controls, and regular log reviews, to safeguard data and applications.

Optimize

Optimization ensures that cloud resources are fine-tuned for maximum performance and cost efficiency.

Monitor performance metrics: Use advanced monitoring tools to track application performance and identify improvement opportunities in real time.

Adjust and fine-tune resources: Scale resources dynamically based on demand to maintain performance without unnecessary cost overheads.

Leverage cost-saving features: Use provider offerings like auto-scaling, reserved instances, and spot instances to minimize operational costs while maintaining quality.

By thoroughly understanding and executing each phase of cloud transformation, organizations can achieve a seamless transition to a modern, efficient cloud environment. This structured approach ensures scalability, performance, and long-term success.

Conclusion

Cloud migration is a multifaceted process that demands in-depth analysis of existing challenges and aligning them with strategic changes to meet business objectives. Selecting the right migration strategy depends on workload complexities, associated costs, and potential disruption to current systems. Each organization must evaluate these factors to ensure a smooth transition while minimizing impact.

While the benefits of a well-planned migration are significant, organizations must address the ongoing risks and effort required for maintenance. Ensuring compatibility and performance in the cloud environment demands continuous oversight and optimization.

For a deeper understanding of how TechAhead can streamline your cloud migration journey, explore our comprehensive guide on migrating enterprise workloads. Our cloud migration case studies also provide insights into the transformative advantages of moving critical business operations to the cloud. Partnering with experts ensures a seamless transition, unlocking agility, scalability, and innovation for your business.

Source URL: https://www.techaheadcorp.com/blog/aws-cloud-migration-benefits-strategies-and-phases-simplified/

#AWS Cloud Services#Cloud Transformation#AWS Cloud Migration#Lift and Shift Cloud Migration#Cloud Migration Strategies

0 notes

Text

Containerized Data Center Market Poised to Expand from $15.6 Billion in 2023 to $38.3 Billion by 2033!

Containerized Data Center Market is at the forefront of revolutionizing data storage and management. These portable, modular solutions, housed in shipping containers, integrate power, cooling, and IT infrastructure, offering unmatched scalability and mobility. As the demand for energy-efficient and cost-effective solutions rises, this market is poised for robust growth.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS32243 &utm_source=SnehaPatil&utm_medium=Article

Key drivers include the expansion of cloud and edge computing and the growing need for disaster recovery solutions. The IT and telecom sector dominates the market with a 45% share, fueled by surging data traffic and increasing reliance on cloud services. The BFSI sector follows with a 30% share, leveraging containerized data centers for secure and rapid deployments.

Geographically, North America leads the market, benefiting from advanced IT infrastructure and early adoption of innovative technologies. Europe follows closely, with a focus on green data initiatives and modernization of data centers. The Asia-Pacific region is emerging as a high-growth area, driven by digital transformation and expanding internet penetration in developing economies.

Market segmentation highlights diverse offerings, including all-in-one, stand-alone, and customized containers. Key components such as servers, storage, and cooling systems are tailored to various applications, from BFSI and healthcare to telecommunications and energy.

The competitive landscape features prominent players like IBM, HPE, and Cisco, each shaping the industry with modular designs and energy-efficient solutions. Regulatory frameworks, such as GDPR and cybersecurity policies, significantly influence market dynamics. Despite challenges like high initial costs and evolving security threats, the integration of AI and IoT in data management presents exciting growth opportunities.

Future projections indicate a 15% rise in capital expenditure by 2033, spurred by investments in edge computing and advanced cooling technologies, ensuring a promising outlook for the containerized data center market.

#DataCenters #ModularSolutions #CloudComputing #EdgeComputing #ContainerizedDataCenters #ITInfrastructure #GreenDataCenters #DigitalTransformation #DataStorage #AIIntegration #IoTInnovation #BFSISolutions #EnergyEfficiency #DataManagement #FutureOfData

0 notes

Text

Micro Data Center Market: Forthcoming Trends and Share Analysis by 2030

Micro Data Center Market Size Was Valued at USD 5.7 Billion in 2023, and is Projected to Reach USD 55.3 Billion by 2032, Growing at a CAGR of 28.8% From 2024-2032.

A mini data center is a secure, self-contained device that has all the electricity, ventilation, rack space, and uninterruptible power supply needed to house all of the essential IT components plus management and monitoring software. Micro data centers allow companies to reduce their energy, footprint, and capital costs while also speeding up deployment. Organizations are motivated to implement micro data solutions at peripheral locations by the many advantages offered by micro facilities, including mobility, cost-effectiveness, enhanced networking and connectivity, and power economy. Moreover, the capacity to quickly deploy these tiny data centers or containerized (modular) buildings allows businesses to increase their operational activity in reaction to surges in computing demand.

While the construction of micro data center facilities at the necessary sites takes about one week, the deployment of conventional IT facilities at network locations usually takes more than a month. These factors encourage the market for mini data centers to grow.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://introspectivemarketresearch.com/request/4919

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Leading players involved in the Micro Data Center Market include:

Vertiv Co, Schneider Electric SE, IBM Corporation, Dell Inc, Huawei Technologies Co. Ltd, Hewlett Packard Enterprise Company, Eaton Corporation,and Other Key Players

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

If You Have Any Query Micro Data Center Market Report, Visit:

https://introspectivemarketresearch.com/inquiry/4919

Segmentation of Micro Data Center Market:

By Component

Solutions

Service

By Application

BFSI

Energy

Government

Healthcare

Industrial

IT & Telecom

Others

Market Segment by Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

Key Benefits of Micro Data Center Market Research:

Research Report covers the Industry drivers, restraints, opportunities and challenges

Competitive landscape & strategies of leading key players

Potential & niche segments and regional analysis exhibiting promising growth covered in the study

Recent industry trends and market developments

Research provides historical, current, and projected market size & share, in terms of value

Market intelligence to enable effective decision making

Growth opportunities and trend analysis

Covid-19 Impact analysis and analysis to Micro Data Center market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=4919

About us:

Introspective Market Research (introspectivemarketresearch.com) is a visionary research consulting firm dedicated to assist our clients grow and have a successful impact on the market. Our team at IMR is ready to assist our clients flourish their business by offering strategies to gain success and monopoly in their respective fields. We are a global market research company, specialized in using big data and advanced analytics to show the bigger picture of the market trends. We help our clients to think differently and build better tomorrow for all of us. We are a technology-driven research company, we analyze extremely large sets of data to discover deeper insights and provide conclusive consulting. We not only provide intelligence solutions, but we help our clients in how they can achieve their goals.

Contact us:

Introspective Market Research

3001 S King Drive,

Chicago, Illinois

60616 USA

Ph no: +1 773 382 1049

Email: [email protected]

#Micro Data Center#Micro Data Center Market#Micro Data Center Market Size#Micro Data Center Market Share#Micro Data Center Market Growth#Micro Data Center Market Trend#Micro Data Center Market segment#Micro Data Center Market Opportunity#Micro Data Center Market Analysis 2024

0 notes

Text

Hybrid Cloud Market Size, Growth Forecast & Trends 2032