#U.S. Core Banking Software Market Driver

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The “We are the 99%” Tumblr blog became the slogan for the Occupy Wall Street movement.

Text

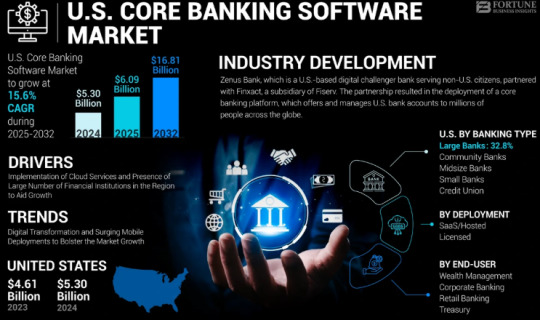

The U.S. Core Banking Software Market Size, Share | CAGR 15.6% during 2024-2030

The U.S. core banking software market Size was valued at USD 5.30 billion in 2024 and is projected to grow from USD 6.09 billion in 2025 to USD 16.81 billion by 2032, exhibiting a CAGR of 15.6% during the forecast period. Driven by the modernization of legacy banking systems, increasing customer demand for digital-first banking experiences, and adoption of cloud-native platforms, the U.S. banking industry is rapidly shifting toward agile, API-driven core banking systems.

Key Market Highlights:

2024 U.S. Market Size: USD 5.30 billion

2025 U.S. Market Size: USD 6.09 billion

2032 U.S. Market Size: USD 16.81 billion

CAGR (2025–2032): 15.6%

Market Outlook: Cloud-first transformation of retail and commercial banking infrastructure

Leading Players in the U.S. Market:

FIS (Fidelity National Information Services)

Finastra

Temenos USA

Oracle Financial Services Software

Jack Henry & Associates

SAP America

nCino

Infosys (EdgeVerve)

Thought Machine

Backbase

Mambu

Q2 Holdings

TCS BaNCS (U.S. operations)

Request Free Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-core-banking-software-market-107481

Market dynamics:

Growth Drivers:

Legacy System Modernization: Traditional banks are replacing decades-old core systems to enable agility, scalability, and faster innovation.

Rise of Digital-Only Banks & Neobanks: Challenger banks are opting for coreless and cloud-native platforms to deliver real-time banking experiences.

Regulatory Mandates: U.S. regulations increasingly demand transparency, real-time compliance, and modular tech stacks.

Omnichannel and Mobile Banking Boom: Surge in mobile-first customers is accelerating demand for flexible and API-driven core systems.

Adoption of BaaS & Embedded Finance: Banks are embedding financial services into non-banking platforms, requiring agile backend core systems.

Key Opportunities:

AI-Powered Core Modernization: Integration of AI for risk scoring, predictive analytics, and process automation

Cloud Migration Projects: Large-scale re-platforming from on-premise to cloud-native or hybrid models

Banking-as-a-Service (BaaS): U.S. institutions offering core services to fintechs and enterprises

Open Banking APIs: Ecosystem expansion through developer-friendly, regulatory-compliant APIs

Personalized Customer Experience Engines: Data-driven personalization built directly into core systems

Technology & Application Scope:

Deployment Models:

Cloud-native

On-premises

Hybrid (transitional)

Core Features:

Customer and account management

Payments and transaction processing

Lending and credit modules

Risk and compliance automation

Real-time reporting and dashboards

Target Users:

Retail banks

Credit unions

Community banks

Commercial and corporate banks

Neobanks and fintechs

Speak to Analysts: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-core-banking-software-market-107481

Recent Developments:

January 2024 – A top-10 U.S. bank announced a $700M multiyear plan to migrate its entire core system to a cloud-native microservices architecture with Temenos and AWS.

October 2023 – Jack Henry & Associates launched a new AI-powered fraud prevention module integrated into its core platform, reducing false positives by 45%.

July 2023 – A mid-sized credit union in the Midwest completed a legacy core banking system overhaul, leading to a 22% increase in customer satisfaction due to improved digital banking capabilities.

Trends Shaping the U.S. Core Banking Market:

Composable Banking Architecture: Shift toward modular, plug-and-play architecture

AI & Machine Learning in Core: Real-time fraud detection, dynamic credit risk models, and intelligent automation

Blockchain Integration: Experiments in real-time settlement, decentralized identity, and smart contracts

Low-Code/No-Code Customization: Democratization of development within banking teams

Cybersecurity Embedded in Core: Zero-trust frameworks and secure-by-design approaches

Conclusion:

The U.S. core banking software market is undergoing a significant transformation, driven by rising customer expectations, digital competition, and the imperative to stay compliant and resilient. The future belongs to banks that embrace modular, cloud-native, and API-driven core platforms—designed to scale, personalize, and evolve. As the market accelerates toward modernization, technology vendors and banks alike are finding immense value in flexible ecosystems, open banking capabilities, and real-time innovation.

Frequently Asked Questions: 1. What is the projected value of the global market by 2032?

2. What was the total market value in 2024?

3. What is the expected compound annual growth rate (CAGR) for the market during the forecast period of 2025 to 2032?

4. Which industry segment dominated market in 2023?

5. Who are the major companies?

6. Which region held the largest market share in 2023?

#U.S. Core Banking Software Market Share#U.S. Core Banking Software Market Size#U.S. Core Banking Software Market Industry#U.S. Core Banking Software Market Driver#U.S. Core Banking Software Market Growth#U.S. Core Banking Software Market Analysis#U.S. Core Banking Software Market Trends

0 notes

Text

Exploring Key Trends and Market Drivers in Point-of-Care Testing Through 2033

Astute Analytica stands out as a premier provider of comprehensive Point-of-Care Testing Market research reports specifically tailored for the healthcare sector. Our commitment lies in delivering valuable insights and research that empower healthcare organizations to navigate the complexities of this rapidly evolving industry.

By understanding the trends and opportunities within the healthcare Point-of-Care Testing market, businesses can strategically position themselves for success in an increasingly competitive environment. The integration of digital solutions, a focus on sustainability, and the adaptation to new care delivery models are essential components for enhancing patient care and ensuring the long-term viability of healthcare systems.

Point-of-care testing market was valued at US$ 46.48 billion in 2024 and is projected to hit the market valuation of US$ 85.55 billion by 2033 at a CAGR of 7.33% during the forecast period 2025–2033.

A Request of this Sample PDF File@- https://www.astuteanalytica.com/request-sample/point-of-care-testing-market

The Essential Path of Digital Transformation in Healthcare

As we approach 2025, health system leaders across the globe are prioritizing efforts to drive efficiencies, boost productivity, and improve patient engagement. A significant factor influencing these initiatives is the accelerated digital transformation within healthcare, which has been identified as the most impactful issue for global health systems in the coming years. This emphasis on digitalization is not surprising, considering that healthcare has lagged behind other industries, such as retail and finance, in adopting advanced digital technologies.

According to recent surveys, approximately 70% of respondents believe that investing in technology platforms for digital tools and services will be crucial for their organizations. Furthermore, 60% of leaders highlighted the necessity of investing in core technologies, including electronic medical records (EMRs) and enterprise resource planning (ERP) software. Notably, around 90% of C-suite executives anticipate a significant acceleration in the use of digital technologies by 2025, with half expecting a profound impact on their operations.

The Rise of Consumer-Driven Digital Health Tools

The growing adoption of connected monitoring devices and digital tools among consumers is reshaping the healthcare landscape. In 2024, 43% of consumers are expected to utilize these technologies, up from 34% in 2022. This shift aligns with the highly personalized experiences that consumers have come to expect from industries such as banking, retail, and entertainment. Digital monitoring tools empower consumers by providing trending data that supports their health concerns, thereby enhancing their agency during patient-clinician interactions. This increased control and confidence is particularly vital in areas like maternal health, where timely and informed interactions can prevent adverse outcomes.

Mergers and Acquisitions in Healthcare Technology

The healthcare technology sector is poised for a surge in mergers and acquisitions (M&A) as we move into 2024. The COVID-19 pandemic has underscored the importance of health technology and healthcare delivery systems, prompting a renewed focus on consolidation within the industry. In 2023, biopharma M&A experienced a remarkable rebound, with an aggregate deal value increasing by 79% compared to 2022, reaching approximately $152 billion—the highest level since 2019. The average deal size has also shown an upward trend, approaching levels not seen since 2020. Several positive catalysts are expected to support this momentum in 2024, including emerging threats to growth, a fear of missing out on opportunities, and a resurgence of high-prevalence conditions that necessitate innovative solutions.

The U.S. Healthcare Point-of-Care Testing Market Landscape

The United States remains the world's largest healthcare Point-of-Care Testing market, with healthcare spending reaching $4.3 trillion in 2021, translating to about $12,900 per person. However, as consolidation continues and exposure to government payers increases, healthcare markets in other regions are anticipated to grow at a faster pace. Despite the substantial investment in healthcare, the outcomes do not always reflect this high expenditure, leading to significant disparities in access and quality of care. The U.S. healthcare system is evolving in response to these challenges, particularly the pressures of rising costs and an increasing number of uninsured individuals.

Navigating Political Changes and Regulatory Shifts

As the healthcare industry prepares for 2025, potential changes in political leadership could usher in new policy directions and regulatory shifts. Leaders within the healthcare space must remain agile, anticipating policy reforms that could reshape operational priorities, including resource allocation and shifts in care delivery models. Building collaborative ecosystems and staying informed about legislative developments will be crucial for organizations aiming to thrive in this dynamic environment.

For Purchase Enquiry: https://www.astuteanalytica.com/industry-report/point-of-care-testing-market

Market Segmentation and Analysis

In its quest for a granular understanding of the Point-of-Care Testing market, the report segments the industry into various categories. This segmentation facilitates a more detailed analysis of the dynamics within each segment, allowing stakeholders to identify specific growth opportunities and challenges. By breaking down the market, the report aids in crafting targeted strategies tailored to the unique characteristics of each segment.

By Product

Devices & Instruments

Diagnostic Analyzers & Testing Devices

Blood Gas & Electrolyte Analyzers

Cardiac Biomarker Analyzers

Glucose Monitoring Devices

Coagulation Testing Analyzers

Urinalysis Analyzers

Routine Clinical Chemistry Analyzers

Others

Monitoring Devices

Blood Pressure Monitors

Thermometers

Pulse Oximeters

Others

Testing Kits & Consumables

Blood Gas & Electrolyte Test Kits

Cardiac Biomarker Test Kits

Routine Clinical Chemistry Test Kits

Hematology Test Kits Coagulation Testing Kits

Urinalysis Test Strips & Kits

Cholesterol Test Strips

Drugs Abuse Testing Kits

Pregnancy And Fertility Testing Kits

Others

By Test Type

Immunological PoC Tests

Nucleic Acid-Based PoC Tests

Biomarker-Based PoC Tests

By Indication

Infectious Diseases

HIV

COVID-19

Others

Oncology

Cardiovascular Diseases

Metabolic Disorders

Respiratory Diseases

Neurological Disorders

Gastrointestinal Disorders

Others

By Technology

Biosensor Technology

Microfluidic Lab-On-A-Chip Technology

Molecular Diagnostics

Immunoassays

Others

By Sample Type

Blood

Urine

Saliva

Others

By Mode Of Purchase

Prescription-based Testing

Over the Counter (OTC) Testing

By End User

Hospitals & Clinics

Diagnostic Centers

Homecare Settings

Research Laboratories

Others

By Distribution Channel

Direct Distribution

Retail Pharmacies

Online Pharmacies

Others

By Region

North America

The U.S.

Canada

Mexico

Europe

Western Europe

The UK

Germany

France

Italy

Spain

Rest of Western Europe

Eastern Europe

Poland

Russia

Hungary

Rest of Eastern Europe

Asia Pacific

China

India

Japan

South Korea

Australia & New Zealand

ASEAN

Rest of Asia Pacific

Middle East

UAE

Saudi Arabia

Bahrain

Kuwait

Qatar

Rest of Middle East

Africa

Morocco

Egypt

Nigeria

South Africa

Rest of Africa

South America

Argentina

Brazil

Rest of South America

Geographical Segmentation

The report further segments the market into geographical regions, including North America, South America, Asia, Europe, Africa, and Others. Each region is examined with a focus on key countries, providing insights into the current market size and forecasts extending until 2033. This geographical breakdown is critical for understanding regional market dynamics and tailoring strategies to meet local demands effectively.

Competitive Landscape

A significant portion of the report is dedicated to analyzing the competitive landscape within the Point-of-Care Testing market. This includes a comprehensive examination of leading Point-of-Care Testing product vendors, highlighting their latest developments and market shares in terms of shipment and revenue. By profiling these major players, the report offers valuable insights into their product portfolios, technological capabilities, and overall market positioning.

The report identifies key players in the Point-of-Care Testing market, providing a closer look at their contributions to the industry. This competitive profiling is essential for understanding the strengths and weaknesses of various companies, enabling stakeholders to make informed decisions and devise effective strategies in a crowded marketplace.

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Danaher Corporation

Becton, Dickinson and Company (BD)

bioMérieux SA

Bio-Rad Laboratories, Inc.

Other Prominent Players

Download Sample PDF Report@- https://www.astuteanalytica.com/request-sample/point-of-care-testing-market

About Astute Analytica:

Astute Analytica is a global analytics and advisory company that has built a solid reputation in a short period, thanks to the tangible outcomes we have delivered to our clients. We pride ourselves in generating unparalleled, in-depth, and uncannily accurate estimates and projections for our very demanding clients spread across different verticals. We have a long list of satisfied and repeat clients from a wide spectrum including technology, healthcare, chemicals, semiconductors, FMCG, and many more. These happy customers come to us from all across the globe.

They are able to make well-calibrated decisions and leverage highly lucrative opportunities while surmounting the fierce challenges all because we analyse for them the complex business environment, segment-wise existing and emerging possibilities, technology formations, growth estimates, and even the strategic choices available. In short, a complete package. All this is possible because we have a highly qualified, competent, and experienced team of professionals comprising business analysts, economists, consultants, and technology experts. In our list of priorities, you-our patron-come at the top. You can be sure of the best cost-effective, value-added package from us, should you decide to engage with us.

Get in touch with us

Phone number: +18884296757

Email: [email protected]

Visit our website: https://www.astuteanalytica.com/

0 notes

Text

Core Banking Software Market - Industry Dynamics, Market Size

According to Market Statistix, the Core Banking Software Market revenue and growth prospects are expected to grow at a significant rate during the analysis period of 2024-2032, with 2023 as the base year. Core Banking Software Market research is an ongoing process. Regularly monitor and evaluate market dynamics to stay informed and adapt your strategies accordingly. As a market research and consulting firm, we offer market research reports that focus on major parameters, including Target Market Identification, Customer Needs and Preferences, Thorough Competitor Analysis, Market Size and market Analysis, and other major factors. In the end, we provide meaningful insights and actionable recommendations that inform decision-making and strategy development.

The Core Banking Software Market is projected to experience steady growth, expanding at a CAGR of 17.5% over the forecast period.

Who are the key players operating in the industry?

Oracle Corporation (U.S.), SAP SE (Germany), Tata Consultancy Services Limited (India), Finastra International Limited (U.K.), Capital Banking Solutions (U.S.), EdgeVerve Systems Limited (India), Fidelity National Information Services, Inc. (U.S.), Fiserv, Inc. (U.S.), Mambu GmbH (Germany), Temenos AG (Switzerland)

Request a sample on this latest research report Core Banking Software Market spread across 100+ pages and supported with tables and figures is now available @ https://www.marketstatistix.com/sample-report/global-core-banking-software-market

Core Banking Software Market Overview and Insights:

Market Statistix is solidifying its reputation as a leading market research and consulting service provider, delivering data-driven insights that help businesses make informed strategic decisions. By focusing on detailed demand analysis, accurate market forecasts, and competitive evaluations, we equip companies with the essential tools to succeed in an increasingly competitive landscape. This comprehensive Core Banking Software market analysis offers a detailed overview of the current environment and forecasts growth trends through 2032. Our expertise enables clients to stay ahead of the curve, providing actionable insights and competitive intelligence tailored to their industries.

What is included in Core Banking Software market segmentation?

The report has segmented the market into the following categories:

Segment by Type: Large Banks (Greater than USD 30 Billion in Assets), Midsize Banks (USD 10 billion to USD 30 Billion in Assets), Small Banks (USD 5 billion to USD 10 Billion in Assets), Community Banks (Less than USD 5 Billion in Assets), Credit Unions

Segment by Application: Retail Banks, Corporate Banks, Treasury, Wealth Management, Others

Core Banking Software market is segmented by company, region (country), by Type, and by Application. Players, stakeholders, and other participants in the Core Banking Software market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on revenue and forecast by Type and by Application in terms of revenue and forecast for the period 2019-2032.

Have a query? Market an enquiry before purchase @ https://www.marketstatistix.com/enquiry-before-buy/global-core-banking-software-market

Competitive Analysis of the market in the report identifies various key manufacturers of the market. We do company profiling for major key players. The research report includes Competitive Positioning, Investment Analysis, BCG Matrix, Heat Map Analysis, and Mergers & Acquisitions. It helps the reader understand the strategies and collaborations that players are targeting to combat competition in the market. The comprehensive report offers a significant microscopic look at the market. The reader can identify the footprints of the manufacturers by knowing about the product portfolio, the global price of manufacturers, and production by producers during the forecast period.

As market research and consulting firm we offer market research report which is focusing on major parameters including Target Market Identification, Customer Needs and Preferences, Thorough Competitor Analysis, Market Size & Market Analysis, and other major factors.

Purchase the latest edition of the Core Banking Software market report now @ https://www.marketstatistix.com/buy-now?format=1&report=42

The Core Banking Software market research study ensures the highest level of accuracy and reliability as we precisely examine the overall industry, covering all the market fundamentals. By leveraging a wide range of primary and secondary sources, we establish a strong foundation for our findings. Industry-standard tools like Porter's Five Forces Analysis, SWOT Analysis, and Price Trend Analysis further enhance the comprehensiveness of our evaluation.

A Comprehensive analysis of consumption, revenue, market share, and growth rate is provided for the following regions:

-The Middle East and Africa region, including countries such as South Africa, Saudi Arabia, UAE, Israel, Egypt, and others.

-North America, comprising the United States, Mexico, and Canada.

-South America, including countries such as Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, and others.

-Europe (including Turkey, Spain, the Netherlands, Denmark, Belgium, Switzerland, Germany, Russia, the UK, Italy, France, and others)

-The Asia-Pacific region includes Taiwan, Hong Kong, Singapore, Vietnam, China, Malaysia, Japan, the Philippines, South Korea, Thailand, India, Indonesia, and Australia.

Browse Executive Summary and Complete Table of Content @ https://www.marketstatistix.com/report/global-core-banking-software-market

Table of Contents for the Core Banking Software Market includes the following points:

Chapter 01 - Core Banking Software Executive Summary

Chapter 02 - Market Overview

Chapter 03 - Key Success Factors

Chapter 04 - Core Banking Software Market – Pricing Analysis Overview

Chapter 05 - Overview of the History of the Core Banking Software Market

Chapter 06 - Core Banking Software Market Segmentation [e.g. Type (Large Banks (Greater than USD 30 Billion in Assets), Midsize Banks (USD 10 billion to USD 30 Billion in Assets), Small Banks (USD 5 billion to USD 10 Billion in Assets), Community Banks (Less than USD 5 Billion in Assets), Credit Unions), Application (Retail Banks, Corporate Banks, Treasury, Wealth Management, Others)]

Chapter 07 - Analysis of Key and Emerging Countries in the Core Banking Software

Chapter 08 - Core Banking Software Market Structure and Value Analysis

Chapter 09 - Competitive Landscape and Key Challenges in the Core Banking Software Market

Chapter 10 - Assumptions and Abbreviations

Chapter 11 - Market Research Approach for Core Banking Software

About Market Statistix:

Market Statistix is an expert in the area of global market research consulting. With the aid of our ingenious database built by experts, we offer our clients a broad range of tailored Marketing and Business Research Solutions to choose from. We assist our clients in gaining a better understanding of the strengths and weaknesses of various markets, as well as how to capitalize on opportunities. Covering a wide variety of market applications, We are your one-stop solution for anything from data collection to investment advice, covering a wide variety of market scopes from digital goods to the food industry.

Contact Information:

Market Statistix

Media & Marketing Manager

Call: +91 9067 785 685

Email: [email protected]

Website: www.marketstatistix.com

#Core Banking Software Market#Core Banking Software Market Share#Core Banking Software Market Size#Core Banking Software Market Trends#Core Banking Software Market Growth#Core Banking Software Market Forecast Analysis

0 notes

Text

Performance Overview Of The S&P Composite Index Across Key Sectors

Highlights:

The S&P Composite Index includes a diversified mix of companies across major U.S. sectors.

Regular fluctuations in the index reflect broader economic activity and sector-specific shifts.

The index is tracked by market participants as a gauge of U.S. equity market health.

The S&P Composite Index represents a wide spectrum of public companies traded primarily on U.S. exchanges. It encompasses sectors such as technology, energy, consumer goods, industrials, healthcare, financials, and utilities. Its composition reflects broad equity market behavior and acts as a market performance indicator.

The companies listed under this index are selected from major U.S. exchanges including the NYSE and NASDAQ. The structure of the index ensures that it captures a wide-ranging view of business activity across different segments of the economy.

Technology Sector

Technology continues to remain a core driver of movement within the S&P Composite Index. Companies in software, hardware, semiconductors, and IT services contribute significantly to the weight of the index. Changes in consumer behavior and enterprise needs influence this sector's performance within the index.

Frequent advancements in cloud infrastructure, artificial intelligence, and automation technologies impact the relative standing of technology-focused components within the index. These shifts also mirror broader industry developments and influence sectoral dynamics in the index.

Healthcare Sector

Healthcare is another foundational pillar of the S&P Composite Index, consisting of firms in pharmaceuticals, biotechnology, and medical equipment. This sector often displays resilience during periods of economic uncertainty due to continuous demand for essential services and treatments.

Drug manufacturers and diagnostics companies play a notable role in the index's sectoral breakdown. Market responses to new product developments and regulatory decisions often coincide with changes in this sector’s contribution to the index.

Energy Sector

The energy segment within the S&P Composite Index includes companies involved in oil, natural gas, and renewable sources. These entities respond to variations in global supply conditions, environmental initiatives, and geopolitical events.

Shifts in the energy market landscape can affect sector representation within the index, especially as alternative energy sources gain traction alongside traditional resources.

Consumer Goods and Services

The S&P Composite Index includes businesses in apparel, food, electronics, and retail. These companies reflect shifting trends in consumer demand and preferences. Retailers and manufacturers adapt operations in response to changes in supply chains, seasonal consumption, and product innovations.

Brand performance, pricing adjustments, and external influences such as trade agreements often affect this sector’s influence on the index. Consumer behavior trends can significantly impact daily trading volumes and sector weight in the index.

Financial Sector

Banks, insurance firms, and asset management companies form a large portion of the S&P Composite Index. Their performance is often associated with regulatory frameworks, interest rate environments, and broader capital movement.

Credit services and payment networks are also included within this group, reflecting ongoing transformations in digital finance and commercial banking practices.

Industrial Sector

Industrial companies within the S&P Composite Index focus on manufacturing, aerospace, logistics, and construction. This sector often reflects activity levels tied to domestic and international infrastructure developments.

Shipping trends, equipment production, and large-scale project implementation influence the industrial sector’s overall positioning in the index.

Utilities and Infrastructure

The utilities segment in the S&P Composite Index features providers of electricity, water, and gas. These firms are often included due to their consistent operational nature and essential role in daily functioning.

Public infrastructure upgrades, environmental regulations, and energy transitions often impact the utilities portion of the index. Seasonal consumption patterns and maintenance schedules can also influence index metrics for this segment.

Communication Services

This sector includes broadband, entertainment, and wireless communication providers within the S&P Composite Index. It has grown in relevance with the expansion of digital streaming, mobile data usage, and online services.

Consumer engagement with content and telecommunications services plays a role in shaping this sector’s influence on the overall index movement.

Real Estate Sector

Real estate within the S&P Composite Index covers both commercial and residential segments, with firms involved in property development, leasing, and management.

Urbanization, construction activity, and space utilization trends are factors that drive movements within this segment of the index. Retail and office space adjustments post-pandemic have also influenced representation within the index.

0 notes

Text

AI Model Risk Management Market to See 9.8% CAGR, Growing to $16.2B by 2034

AI Model Risk Management Market is entering a transformative era. Projected to surge from $6.2 billion in 2024 to an impressive $16.2 billion by 2034, the market is set to grow at a compelling CAGR of 9.8%.

This boom is driven by the rapid proliferation of artificial intelligence across industries and the increasing demand for tools that ensure AI systems operate responsibly, ethically, and within the boundaries of regulatory standards. As companies lean into AI to boost productivity and innovation, they’re simultaneously investing in frameworks and platforms that identify, assess, and mitigate risks tied to these intelligent models.

Market Dynamics

At the core of the market’s growth are robust software solutions and critical services that manage AI-related risk. The software segment dominates, commanding about 55% of the market thanks to real-time monitoring, analytics, and transparency tools. Meanwhile, services like consulting, training, and implementation take up the remaining 45%, supporting businesses in understanding and integrating risk protocols.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS32156

Key drivers include increased regulatory scrutiny, the complexity of AI models, and rising concerns around AI ethics, bias, and transparency. On the flip side, high costs, integration challenges, and a shortage of AI-savvy professionals remain notable restraints. Yet, the opportunities are vast — particularly for firms innovating in real-time risk assessment, bias detection, and governance tools.

Key Players Analysis

The market is populated by both legacy giants and emerging innovators. Notable players like DataRobot, SAS Institute, C3.ai, FICO, and Alteryx provide end-to-end risk management platforms tailored for complex AI ecosystems. Emerging disruptors such as Model Wise Analytics, AI Compliance Systems, and Risk Mind AI are gaining traction with specialized tools focused on compliance, model integrity, and explainability.

These companies are engaging in strategic collaborations and R&D investments to offer solutions that blend AI governance, transparency, and operational excellence. Their platforms often cater to mission-critical industries like banking, insurance, healthcare, and government — sectors where failure to manage AI risk can lead to serious legal or financial repercussions.

Regional Analysis

North America leads the global market, primarily due to the U.S.’s strong AI regulatory environment and its push for AI transparency. Here, companies are increasingly aligning with standards from the National Institute of Standards and Technology (NIST) and other federal bodies.

Europe follows closely, driven by countries like the U.K., Germany, and France, all of which emphasize AI ethics and compliance. The region’s focus on human-centered AI and data protection (such as GDPR) is accelerating demand for risk frameworks.

Asia-Pacific, with its tech-forward economies like China, Japan, and South Korea, is experiencing rapid market growth. Governments and enterprises alike are recognizing the need for structured AI oversight amid increasing adoption.

Meanwhile, Latin America, the Middle East, and Africa are emerging markets. Brazil, Mexico, UAE, and Saudi Arabia are taking early steps with infrastructure investments and policy initiatives to harness AI responsibly.

Recent News & Developments

The market is buzzing with activity as organizations adapt to evolving global AI regulations. Investment in AI risk tools now often ranges from $100,000 to over $1 million annually, reflecting the value companies place on trustworthy AI.

Recent trends include the integration of AI explainability tools, bias mitigation frameworks, and end-to-end model monitoring platforms. Strategic partnerships between tech companies and academic institutions are also playing a critical role in developing best-in-class risk management technologies.

Notably, regulatory bodies like the European Central Bank and Federal Reserve have issued frameworks demanding greater transparency and accountability in AI applications. These developments are forcing even traditional firms to ramp up their investments in AI risk management systems.

Browse Full Report : https://www.globalinsightservices.com/reports/ai-model-risk-management-market/

Scope of the Report

This comprehensive report offers a full-spectrum analysis of the AI Model Risk Management Market, with forecasts from 2025 to 2034. It covers key market segments — by type, product, services, technology, component, deployment, and end user — highlighting growth trends and sector-specific dynamics. The research identifies major drivers, restraints, and emerging opportunities, as well as the strategic moves of top players in this space.

From localized insights to global outlooks, this study also evaluates regulatory impacts, competitive benchmarking, and innovation pipelines shaping the future of AI governance. Whether you’re a stakeholder in finance, healthcare, or public policy, understanding the AI Model Risk Management Market is now essential.

Discover Additional Market Insights from Global Insight Services:

Multicarrier Parcel Management Solutions Software Market : https://www.globalinsightservices.com/reports/multicarrier-parcel-management-solutions-software-market/

Building Energy Simulation Software Market : https://www.globalinsightservices.com/reports/building-energy-simulation-software-market/

Dealer Management System Market : https://www.globalinsightservices.com/reports/dealer-management-system-market/

Mobile Phone Insurance Market : https://www.globalinsightservices.com/reports/mobile-phone-insurance-market/

#ai #aigovernance #aimodelrisk #modelriskmanagement #ethicalai #transparency #compliance #aiexplainability #regtech #aiethics #machinelearning #deeplearning #nlp #aiinhealthcare #aiinfinance #fintech #aioversight #biasmitigation #accountableai #responsibleai #modelvalidation #riskmanagement #aitools #aiops #secureai #aiinbanking #aicompliance #aiforethics #aiindustry #modelintegrity #aiinbusiness #cyberrisk #dataprivacy #artificialintelligence #aiinretail #aiaudit #techregulation #aimonitoring #aigovernanceframework #aiinnovation #ai2025Top of Form

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

FinTech Mobile App Development Service: Transforming the Financial Landscape

The financial industry has undergone a massive transformation with the rise of FinTech mobile applications Service. These digital solutions have made banking, payments, and financial management more accessible, secure, and efficient. Today, consumers expect seamless, fast, and personalized financial services — driving the demand for innovative FinTech applications.

At Mobiloitte, we understand the importance of cutting-edge technology in shaping the future of finance. Our expertise in FinTech mobile app development helps businesses create secure, scalable, and user-friendly applications that cater to evolving customer needs.

The Growth of FinTech Mobile Apps

FinTech applications have eliminated the limitations of traditional banking. Earlier, financial services were only available to select groups through physical banking institutions. Now, anyone with a smartphone can access banking, lending, investment, and payment services instantly.

One of the key drivers behind this shift is user convenience. FinTech applications offer 24/7 access to financial tools, replacing time-consuming visits to physical banks. Recognizing this trend, many financial institutions are partnering with leading FinTech app development companies like Mobiloitte to create innovative solutions that enhance customer engagement and loyalty.

The Rise of Mobile Payments

The digital revolution has significantly impacted the way we conduct financial transactions. The adoption of mobile payments has surged, especially post-pandemic, as businesses and consumers move towards cashless transactions.

According to a report by Ernst & Young, 46% of U.S. consumers now rely on FinTech applications for various financial activities. Mobile wallets, peer-to-peer (P2P) payments, and real-time transactions have become the new norm.

Many traditional banks are responding by either developing their own mobile payment solutions or collaborating with FinTech companies like Mobiloitte to integrate advanced payment technologies.

Why FinTech Mobile App DevelopmentService is Essential

1. The Shift to Mobile Banking

Millennials and Gen Z users increasingly depend on mobile apps for their financial needs. From managing bank accounts to investing in stocks, consumers expect a seamless digital experience.

Financial institutions that fail to prioritize mobile-first strategies risk losing customers to agile FinTech startups that offer intuitive, personalized financial services.

2. Expanding Financial Inclusion

FinTech mobile apps have played a crucial role in making financial services more inclusive. With a mobile-first approach, businesses can reach a wider audience, including underserved and remote populations.

By partnering with trusted enterprise software development companies like Mobiloitte, FinTech businesses can expand their market reach and generate higher revenue while empowering users with financial independence.

3. Contactless Payments as the Norm

Contactless payment technology has revolutionized transactions. QR codes, NFC payments, and biometric authentication are now standard features in mobile banking apps.

Today, people don’t need to carry wallets — a smartphone with a secure FinTech app is enough to handle daily transactions. At Mobiloitte, we focus on integrating secure and seamless contactless payment solutions into FinTech applications to enhance the user experience.

4. Enhancing User Experience

User experience (UX) is at the core of every successful FinTech application. Consumers expect: ✅ Intuitive interfaces✅ Fast transaction processing✅ Secure authentication✅ AI-driven financial insights

FinTech companies must analyze user behavior and engagement patterns to design apps that are both functional and enjoyable to use. A seamless UX increases customer satisfaction and brand loyalty.

5. The Power of an Omnichannel Experience

Modern consumers interact with financial services across multiple touchpoints — mobile apps, websites, smart devices, and even social media. An omnichannel strategy ensures a consistent and connected experience across all platforms.

According to Google, the average consumer switches between 3–4 screens before completing a financial transaction. FinTech companies that implement omnichannel strategies will see higher engagement and better customer retention rates.

Conclusion

The future of finance is mobile-first. As FinTech applications continue to evolve, businesses must invest in scalable, secure, and user-centric mobile solutions to stay ahead in the digital financial revolution.

At Mobiloitte, we specialize in developing cutting-edge FinTech mobile applications that prioritize security, convenience, and innovation. Whether you’re a startup or an established financial institution, we can help you navigate the digital transformation and unlock new growth opportunities.

Are you ready to revolutionize financial services with a powerful FinTech mobile app? Contact Mobiloitte today!

#Mobile application service provider#Mobile application development services#Native app development services#Hybrid app development services#Android app development#iOS mobile app development#Cross-platform mobile development#Mobile game development company#Mobile Application Development#Custom Mobile Apps#Mobile App Development Services#Professional Mobile Development#Custom Mobile Solutions#Expert Mobile App Development.

0 notes

Text

Voice And Speech Recognition Market Outlook, Competitive Strategies And Forecast

The global voice and speech recognition market size is anticipated to reach USD 53.67 billion by 2030, registering a CAGR of 14.6% from 2024 to 2030, according to a new report by Grand View Research, Inc. The market is anticipated to witness an upsurge in the adoption of voice-activated systems, voice-enabled devices, and voice-enabled virtual assistant systems owing to the rising applications in the banking and automobile sectors. The escalating need to counter fraudulent activities and enhance security in the banking sector is boosting the adoption of voice biometrics for the authentication of users. The automobile sector is expected to gain momentum owing to advances in technology & emergence of innovative concepts, such as autonomous and connected cars.

The integration of the voice-activated software in future cars is anticipated to adopt technologies, such as noise abatement for selectively ignoring driving & passenger noises for providing an error-free and seamless experience to the operator. Voice recognition is also a core technology that is widely used in the healthcare sector to enhance the Electronic Health Record (HER) systems by providing an ease to the doctor to speak and keep the records instead of manual typing or writing. In 2018, the healthcare vertical held the largest market share and it is expected to grow significantly over the forecast period. AI-based voice and speech recognition software is expected to grow at the fastest CAGR from 2023 to 2030.

This is due to the continuous development of machine learning techniques and the integration of connected devices with personal assistants. For instance, Dragon Drive is a personal assistant developed by Nuance Communication Inc. that integrates various household appliances, cars, and smartphones that can be connected to a hub through the internet. Thus, an individual can get alerts about daily chores, work schedules, traffic updates, and many more alerts through the Dragon Drive. In addition, sentiment analysis using the changes in the pitch of the voice is anticipated to provide an opportunity to the market. However, the lack of accuracy of these technologies in recognizing the regional accents and dialects is expected to limit the market growth.

Gather more insights about the market drivers, restrains and growth of the Voice And Speech Recognition Market

Voice And Speech Recognition Market Report Highlights

• A rising trend in the development of Artificial Intelligence (AI)-based systems is expected to be the key factor driving the market growth over the forecast period

• Leveraging deep learning algorithms in voice & speech solutions for better search results is expected to be the key factor for the growth of the AI-based technology segment

• The deployment of speech recognition solutions in consumer and retail verticals is anticipated to lead to the high market growth

• This can be attributed to the changing lifestyles in countries, such as the U.S., Germany, and the U.K.

• Moreover, the growing adoption of smart electronics in India, China, Japan, and Brazil is likely to drive the market growth in the consumer vertical

• North America and the Asia Pacific are anticipated to witness considerable growth owing to the presence of several U.S.- and China-based players, such as Apple, Inc., Facebook, Inc., Baidu, Inc., Amazon.com, Inc., and Alphabet, Inc., working toward the development of this technology

• Key industry participants are focusing on integrating the AI technology in speech & voice recognition software to build superior products that would increase their user customer base

Voice And Speech Recognition Market Segmentation

Grand View Research has segmented the global voice and speech recognition market on the basis of function, technology, vertical, and region:

Voice & Speech Recognition Function Outlook (Revenue, USD Million, 2017 - 2030)

• Voice Recognition

o Speaker Identification

o Speaker Verification

• Speech Recognition

o Automatic Speech Recognition

o Text-to-Speech

Voice & Speech Recognition Technology Outlook (Revenue, USD Million, 2017 - 2030)

• AI-based

• Non-AI-based

Voice & Speech Recognition Vertical Outlook (Revenue, USD Million, 2017 - 2030)

• Automotive

• Enterprise

• Consumer

• BFSI

• Government

• Retail

• Healthcare

• Military

• Legal

• Education

• Others

Voice & Speech Recognition Regional Outlook (Revenue, USD Million, 2017 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Italy

o Spain

o The Netherlands

o Switzerland

o Poland

• Asia Pacific

o China

o Japan

o India

o South Korea

o Singapore

o Pakistan

o Malaysia

o Australia

o Hong Kong

o Vietnam

• South America

o Brazil

o Argentina

o Chile

• Middle East & Africa

o UAE

o Saudi Arabia

o Israel

o South Africa

o Nigeria

Order a free sample PDF of the Voice And Speech Recognition Market Intelligence Study, published by Grand View Research.

#Voice And Speech Recognition Market#Voice And Speech Recognition Market Size#Voice And Speech Recognition Market Share#Voice And Speech Recognition Market Analysis#Voice And Speech Recognition Market Growth

0 notes

Text

"Empowering Energy: Key Players and Trends in the Battery Monitoring Industry

Battery monitoring systems are designed to inform users about the real-time status and health of batteries or battery banks, providing alerts on battery failures and the net charge available. These systems play a crucial role in preventing severe damage, prolonging battery life, and ensuring efficiency. Monitoring charging, discharging, load, AC mains frequency and voltage, ambient temperature, and battery temperature are key functions of a battery monitoring system. Additionally, these systems generate live reports on battery performance and trigger alarms in case of any faults.

Request 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 : https://www.alliedmarketresearch.com/request-toc-and-sample/16324

COVID-19 Impact Analysis

The global effects of the COVID-19 pandemic have significantly impacted the battery monitoring system market. Disruptions in exports, imports, manufacturing, and changes in consumer consumption patterns have led to challenges and a shift in demand during the pandemic.

Top Impacting Factors

The increasing adoption of battery monitoring systems in electric vehicles (EVs) is a major driver for market demand. Governments globally support battery manufacturers for EVs, aligning with the transition to renewable energy sources. Additionally, the need to prevent unplanned outages, the rise in demand for electric vehicles, and improved operational efficiency contribute to the growing demand for battery monitoring systems.

Market Trends

Growing Demands for Electricity at Various End-Use Industries: The necessity to prevent unplanned outages, coupled with the increased demand for electric vehicles and improved battery operational efficiency, drives the demand for battery monitoring systems. The rise in renewable power generation and the use of these systems in data center applications further boost market growth.

Increased Usage in Data Centers: Data centers, critical for organizations' core applications, rely on batteries for uninterrupted power supply. Integrating battery monitoring systems enhances operations and safety in data centers, where battery failures can disrupt operations and result in financial losses.

Focus on Environmental Safety Concerns: The growing demand for clean energy and concerns about global warming have led to a shift towards environmentally friendly solutions. Battery monitoring systems play a crucial role in ensuring the proper functioning of clean technologies and applications dependent on batteries, thereby supporting environmental safety initiatives.

𝐄𝐧𝐪𝐮𝐢𝐫𝐲 𝐁𝐞𝐟𝐨𝐫𝐞 𝐁𝐮𝐲𝐢𝐧𝐠 : https://www.alliedmarketresearch.com/purchase-enquiry/16324

Key Benefits of Report

The report provides an analytical overview of the battery monitoring system market, offering insights into current trends and future estimations to identify potential investment opportunities. It covers key drivers, restraints, and opportunities, along with a detailed analysis of market share. The quantitative analysis highlights the growth scenario, while Porter's five forces analysis illustrates buyer and supplier potency. The report offers a comprehensive analysis of the battery monitoring system market based on competitive intensity and future competition dynamics.

Battery Monitoring System Market Report Highlights

Aspects Details

By Type

Wired

Wireless

By Component

Hardware

Software

𝐆𝐞𝐭 𝐚 𝐂𝐮𝐬𝐭𝐨𝐦𝐢𝐳𝐞𝐝 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 𝐑𝐞𝐩𝐨𝐫𝐭 @ : https://www.alliedmarketresearch.com/request-for-customization/16324

By Application

Telecommunication

Automotive

Energy

Industries

Others

By Battery Type

Lithium-ion

Lead Acid

Others

By Energy Storage

Batteries

Thermal

Mechanical

By Region

North America (U.S., Canada, Mexico)

Europe (France, Germany, Italy, Spain, United Kingdom, Rest of Europe)

Asia-Pacific (China, Japan, India, South Korea, Australia, Rest of Asia Pacific)

LAMEA (Brazil, South Africa, Saudi Arabia, Rest of LAMEA)

Key Market Players ABB, BatteryDAQ, Schneider Electric, Hbl Power Systems, Eagle Eye Power Solutions, LLC, Btech Inc, Socomec, Powershield, Canara, Texas Instrument

0 notes

Text

Software Testing Market To Witness Accelerated Growth by 2030

Software Testing Market To Hit USD 70 Bn By 2030. The rising demand for autonomous driving systems will outline global software testing market growth. Electric vehicles (EVs) are seeing a major increase in production volume as customers are becoming aware of the harmful effects of driving fossil-fueled vehicles.

EVs run on cutting-edge software that gives the driver vital information on the performance of their vehicle. For example, the motor controller is dependent on the embedded software to regulate and supervise the functioning of various components in an electric car, such as the accelerator and battery.

Get sample copy of this research report @

https://www.gminsights.com/request-sample/detail/3382

Software testing is an integral part of sectors that use advanced technologies to carry out their daily operations. According to some reports, organizations across the U.S. incurred costs worth USD 1.56 trillion in 2020 alone due to operational software failures, thereby augmenting the need for tougher software testing standards.

The COVID-19 pandemic period witnessed a worrying rise in cybersecurity issues, such as virtual hacking due to lack of proper software testing or poor software quality. As per the European Union Agency for Cybersecurity, in 2020, there was a 47% growth in cyberattacks on healthcare networks and hospitals across Europe. This scenario will accelerate the need for stringent software testing methods to mitigate the risk of losing confidential data.

1. Pure play software testing offers customized solutions:

Pure play software testing market size will expand at a notable pace over the coming years. The main role of this type of testing is to help product developers enhance the performance of their programs. Pure play testing will assist developers in identifying and solving various defects before making their products available for public use.

Many organizations outsource these services to external agencies who then work closely with the onshore teams. They can fast-track the software development processes because of their flexibility and ability to offer solutions that are tailor-made for the needs of the clients.

2. Professional services gain significant momentum:

The professional services segment will capture a sizeable share of global software testing market in the future. Software testing processes are quite tedious and time-consuming due to the complexities associated with them. They can take up a company’s valuable time who can instead focus on other core activities to boost its performance.

Professional services are helpful in such cases as consultants from external agencies can be hired to take on the cumbersome task of testing different types of software. They can also provide in-depth and personalized guidance to their clients on improving the software quality through timely checks.

Request for customization @ https://www.gminsights.com/roc/3382

3. BFSI sector undergoes large-scale digitization:

Global software testing market revenue from the BFSI sector application will increase considerably in the future as this industry vertical is strengthening its reliance on digital technologies. Many banks and financial institutions are launching online platforms to boost their efficiency and enhance their customers’ banking experience.

For instance, in June 2022, Canada-based fintech organization Nuula declared the launch of its app version in the country. The application will enable small business owners to keep a real-time track of their cashflows, while also alerting them of cash shortage beforehand.

It will also help them monitor their customers’ sentiments through online reviews and ratings. Such innovations will amplify the need for software testing solutions to ensure the seamless functioning of these apps. Fast-growing economies in Asia Pacific also represent key markets for software testing solutions. In India, mobile payments skyrocketed during the period of 2020-21. The number of transactions done through payment applications went up from 1.12 billion in April 2020 to 3.7 billion in June 2021. Similar trends will fuel the need for constant software testing to enhance an app’s performance.

About Global Market Insights:

Global Market Insights, Inc., headquartered in Delaware, U.S., is a global market research and consulting service provider; offering syndicated and custom research reports along with growth consulting services. Our business intelligence and industry research reports offer clients with penetrative insights and actionable market data specially designed and presented to aid strategic decision making. These exhaustive reports are designed via a proprietary research methodology and are available for key industries such as chemicals, advanced materials, technology, renewable energy and biotechnology.

Contact US:

Aashit Tiwari Corporate Sales, USA Global Market Insights Inc. Toll Free: +1-888-689-0688 USA: +1-302-846-7766 Europe: +44-742-759-8484 APAC: +65-3129-7718 Email: [email protected] Social Media: Google+ | LinkedIn | Twitter | Facebook

0 notes

Text

Robotic Process Automation Market Is Expected To Boost, Due To Increased Need Of Automate Workflow During The Covid-19 Pandemic

Robotic Process Automation Industry Overview

The global robotic process automation market size was valued at USD 1.89 billion in 2021 and is projected to expand at a compound annual growth rate (CAGR) of 38.2% from 2022 to 2030.

Factors such as the need to optimize operations to gain improved productivity and generate maximum return, integration of the latest technologies, and changing business processes across enterprises is expected to boost the market growth. Furthermore, during the COVID-19 pandemic, businesses switched to remote work culture, and the need to automate workflow was also increased thus this factor accelerated the market growth. As RPA is becoming mature, it is anticipated to grow increasingly more sophisticated during the forecasted period. Technological advancement such as machine learning, Optical Character Recognition (OCR), and analytics within the RPA domain is potentially creating a demand for intelligent automation systems.

As a result, intelligent automation is anticipated to eliminate more than 40% of service desk interactions by 2025. The combination of cognitive RPA and various chatbot technologies would enable unattended modes of automation at the services desk, thereby reducing human interventions and improving operational productivity.

Gather more insights about the market drivers, restrains and growth of the Global Robotic Process Automation Market

The growing demand for automation of business processes is one of the significant factors influencing the increasing adoption of RPA technology. The core purpose of RPA is to document the activities of an organization for efficient management. Moreover, automated data collection provides seamless data entry & storage and eliminates errors and repetitions. Such practices reduce the time and cost required to rectify the mistakes in data gathering and processing. According to a survey conducted by UiPath (U.S.) in 2020, a global software company for robotic process automation, and The Economist Intelligence Unit (U.K.), a research and analysis division of the Economist Group, 90% of the organizations adopted RPA for automating business processes. In comparison, 73% of the surveyed agreed to be completely satisfied with the benefits resulting from automation.

Further, the increased demand to simplify the complex handling process is expected to augment the industry growth. Organizations across several verticals are deploying RPA and AI to increase productivity and efficiency. In a highly competitive market, it has become essential to improve work agility and deliver enhanced customer experiences. RPA robots can perform tasks across different legacy systems to get information on the digital platform. For instance, bank customers can check their account details online and process KYC verification and automatic bill payment along with other functions through the internet. These services have minimized manual involvement and are guiding in delivering a better customer experience.

Even though the market is anticipated to grow steadily due to the benefits mentioned above, the reluctance of companies to switch from manual to automated processes is expected to restrain the market growth. Organizations around the globe are looking at deploying RPA solutions to improve business processes. However, lack of understanding about the technology pose a barrier to the adoption of this software. Professional service providers are planning to implement RPA solutions in their organizations within the next two to three years.

During the COVID-19 pandemic, businesses switched to remote work culture and increased the need to automate workflow. Thus, significant adoption of RPA for maintaining and automating workflow was witnessed in the year 2020 - 2021. Also, the growing interest of companies in no-code automation platforms has fueled the adoption rate for RPA and has become a part of the automation process for businesses. Furthermore, cloud-based solutions have gained tremendous demand during the pandemic. The cloud automation solutions deliver excellent business value inconsistent deployment, operational cost reductions, and overall resilience and security. It also improves the backend processes in the enterprise workflows.

Browse through Grand View Research's IT Services & Applications Industry Research Reports.

Artificial Intelligence Market - The global artificial intelligence market size was valued at USD 93.5 billion in 2021 and is projected to expand at a compound annual growth rate (CAGR) of 38.1% from 2022 to 2030. The continuous research and innovation directed by the tech giants are driving the adoption of advanced technologies in industry verticals, such as automotive, healthcare, retail, finance, and manufacturing.

Multiexperience Development Platforms Market - The global multiexperience development platforms market size was valued at USD 6.52 billion in 2019 and is expected to grow at a compound annual growth rate (CAGR) of 18.2% from 2020 to 2027.

Robotic Process Automation Market Segmentation

Grand View Research has segmented the global robotic process automation market based on type, deployment, organization, application, and region:

Robotic Process Automation Type Outlook (Revenue, USD Million, 2018 - 2030)

Software

Service

Consulting

Implementing

Training

Robotic Process Automation Deployment Outlook (Revenue, USD Million, 2018 - 2030)

Cloud

On-premise

Robotic Process Automation Organization Outlook (Revenue, USD Million, 2018 - 2030)

Large Enterprises

Small & Medium Enterprises

Robotic Process Automation Application Outlook (Revenue, USD Million, 2018 - 2030)

BFSI

Pharma & Healthcare

Retail & Consumer Goods

Information Technology (IT) & Telecom

Communication and Media & Education

Manufacturing

Logistics and Energy & Utilities

Others

Robotic Process Automation Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Market Share Insights

October 2021: Walmart uses over 500 bots not only to automate duties like answering employee inquiries or collecting helpful information from audit papers but also to track inventory flow and identify slow-moving commodities and headstock.

June 2021: Kofax Inc. a U.S. based company acquired PSIGEN Software, Inc., a leading provider of content management, document capture, and workflow automation software and solutions, providing a wide range of solutions and software in the marketplace and augmenting the intelligent automation platform of the company.

Key Companies profiled:

Some prominent players in the global robotic process automation market include

Automation Anywhere

Blue Prism

EdgeVerve Systems Ltd.

FPT Software

KOFAX, Inc.

NICE

NTT Advanced Technology Corp.

OnviSource, Inc.

Pegasystems

UiPath

Order a free sample PDF of the Robotic Process Automation Market Intelligence Study, published by Grand View Research.

About Grand View Research

Grand View Research, U.S.-based market research and consulting company, provides syndicated as well as customized research reports and consulting services. Registered in California and headquartered in San Francisco, the company comprises over 425 analysts and consultants, adding more than 1200 market research reports to its vast database each year. These reports offer in-depth analysis on 46 industries across 25 major countries worldwide. With the help of an interactive market intelligence platform, Grand View Research Helps Fortune 500 companies and renowned academic institutes understand the global and regional business environment and gauge the opportunities that lie ahead.

#Robotic Process Automation Market#Robotic Process Automation#Robotic Process Automation Market Analysis

0 notes

Text

Voice and Speech Recognition Market Is Projected To Reach USD 31.82 Billion By 2025

The global voice and speech recognition software market size is anticipated to reach USD 31.82 billion by 2025, according to a new report by Grand View Research, Inc. It is anticipated to register a CAGR of 17.5% during the forecast period. The market is anticipated to witness an upsurge in the adoption of voice activated systems, voice-enabled devices, and voice-enabled virtual assistant systems owing to the rising application in the banking and automobile sectors. The escalating need to counter fraudulent activities and to enhance security in the banking sector is projected to boost the adoption of voice biometrics for user authentication.

Automobile sector is expected to gain momentum owing to advancements in technology and emergence of innovative concepts such as autonomous and connected cars. Integration of voice-activated software in future cars is anticipated to drive demand for technologies such as noise abatement for selectively ignoring driving and passenger noises for providing an error-free and seamless experience to the operator.

Voice recognition is also a core technology widely used in healthcare sector to enhance the Electronic Health Record (EHR) systems by providing an ease to the doctor to speak and keep the records instead of manual typing or writing. In 2018, the healthcare vertical held the largest market share and is expected to grow significantly over the forecast period.

Artificial Intelligence (AI)-based voice and speech recognition software is expected to expand at a high CAGR owing to the continuous development of machine learning techniques and integration of connected devices with personal assistants. For instance, Dragon Drive is a personal assistant developed by Nuance Communication Inc. that integrates various household appliances, cars, and smartphones that can be connected to a hub through the internet. Thus, an individual can get alerts about daily chores, work schedules, traffic updates, and many more alerts through the Dragon Drive.

However, the lack of accuracy of these technologies in recognizing the regional accents and dialects is expected to limit the growth of the voice and speech recognition software market. Additionally, sentiment analysis using the changes in the pitch of the voice is anticipated to provide growth opportunity to the market in the forthcoming years.

Request a free sample copy or view report summary: Voice & Speech Recognition Software Market Report

Voice & Speech Recognition Software Market Report Highlights

Rising trend in development of artificial intelligence-based system is expected to be the key factor driving the market over the forecast period. Leveraging deep learning algorithm in voice and speech solutions for better search results is expected to be the key growth driver for AI-based technology segment

Deployment of speech recognition solutions in consumer and retail verticals is anticipated to lead to the high market growth, attributed to the changing lifestyle in several countries including U.S., Germany, and U.K. Growing adoption of smart electronics in India, China, Japan, and Brazil is also likely to drive growth in consumer vertical

North America led the market, in terms of revenue, representing over 36% of the total market share in 2018. Additionally, North America and Asia Pacific are anticipated to witness a considerable growth owing to the presence of several U.S.- and China-based players, such as Apple, Inc.; Facebook, Inc.; Baidu, Inc.; Amazon.com, Inc.; and Alphabet, Inc.; working toward the development of this technology

Key companies operating in the voice and speech recognition software market include Advanced Voice Recognition Systems, Inc.; Agnitio S.L.; Amazon.com, Inc.; Api.ai; Apple, Inc.; Anhui USTC iFlytek o., Ltd.; Baidu, Inc.; BioTrust ID B.V.; CastleOS Software, LLC; Facebook, Inc.; Google, Inc.; International Business Machines Corporation; JStar; LumenVox LLC; M2SYSLLC; Microsoft Corporation; MModal, Inc.; Nortek Holdings, Inc.; Nuance Communications, Inc.; Raytheon Company; SemVox GmbH; Sensory, Inc.; ValidSoft UK Limited; VoiceBox Technologies Corporation; and VoiceVault, Inc. These players focus on integrating the artificial intelligence technology, to build superior products that would increase their user customer base.

Voice & Speech Recognition Software Market Segmentation

Grand View Research has segmented the global voice and speech recognition software market report based on function, technology, vertical, and region.

Voice and Speech Recognition Software Function Outlook (Revenue, USD Million, 2014 - 2025)

Voice Recognition

Speaker Identification

Speaker Verification

Speech Recognition

Automatic Speech Recognition

Text to Speech

Voice and Speech Recognition Software Technology Outlook (Revenue, USD Million, 2014 - 2025)

AI-based

Non-AI based

Voice and Speech Recognition Software Vertical Outlook (Revenue, USD Million, 2014 - 2025)

Automotive

BFSI

Consumer

Education

Enterprise

Government

Healthcare

Legal

Military

Retail

Others

Regional Outlook (Revenue, USD Million, 2014 - 2025)

North America

Europe

Asia Pacific

South America

Middle East and Africa

U.S.

Canada

Mexico

Germany

U.K.

France

Italy

Spain

Netherlands

Switzerland

Poland

China

Japan

India

South Korea

Singapore

Pakistan

Malaysia

Australia

Hong Kong

Vietnam

Brazil

Argentina

Chile

UAE

Saudi Arabia

Israel

South Africa

Nigeria

About Grand View Research

Grand View Research, Inc. is a U.S. based market research and consulting company, registered in the State of California and headquartered in San Francisco. The company provides syndicated research reports, customized research reports, and consulting services. To help clients make informed business decisions, we offer market intelligence studies ensuring relevant and fact-based research across a range of industries, from technology to chemicals, materials and healthcare.

0 notes

Text

Global Serverless Computing Market

Global Serverless Computing Market Size, Share, Application Analysis, Regional Outlook, Growth Trends, Key Players, Competitive Strategies and Forecasts to 2030

In Serverless Computing Methodology, the management of server is handled by the cloud provider and provides the dynamic allocation of machine resources. Therefore, serverless architecture eliminates the requirement for server software and hardware management by the developer. In recent years, some of the major innovations in IT industry enabled business agility, and enhanced resilience. In such scenario, serverless computing was introduced as a major element for the deployment of cloud services and applications. As for instance, utilization of conventional cloud infrastructure to develop an application that checks the credit score using mobile phones for mobile banking, could take days and weeks for development and testing of the application. With the utilization of serverless computing such as AWS Lamba, similar application can be developed in hours. Global Serverless Computing market size accounted 6361.54 million in 2020 is estimated to reach 69438.3 million by 2030 growing with a CAGR of 27% during the forecast period.

Download Sample Copy of the Report to understand the structure of the complete report (Including Full TOC, Table & Figures) @ https://www.decisionforesight.com/request-sample/DFS020230

Market Dynamics and Factors:

The serverless computing market is anticipated to grow with a CAGR of 26.2% during the forecast period from 2020-2028 owing to the reduced operational cost and increased process agility provided by the technology. Furthermore, serverless architecture provides benefits such as easier operational management, faster set up, and zero system administration which attract customers to the serverless computing market. Due to the rapid evolution of artificial intelligence, internet of things, and machine learning companies are pressurized to release innovative products and features that meets the growing consumer expectations. Increasing importance of these trends is expected to propel the serverless computing market growth. Furthermore, serverless computing exploits cloud based computing to their full potential and allows the companies to concentrate on their core products and services instead of handling the traffic load on their IT infrastructure. Hence, the user can run the application on a third party server thereby reducing the deployment time. However, as the organization lack control over the infrastructure, addition of multiple customers to the same platform causes security threats and it is estimated to pose a threat to the serverless computing market progression.

Market Segmentation:

Global Serverless Computing Market – By Services

Automation & Integration

API (Application Programming Interface)

Management

Monitoring

Security

Support & Maintenance

Training & Consulting

Global Serverless Computing Market – By Enterprise

SME

Large Enterprise

Global Serverless Computing Market – By End-User

Telecom & IT

BFSI (Banking, Financial Services, And Insurance)

Government & Public

Health Care & Life Science

Media And Entertainment

Manufacturing

Retail & E-Commerce

Others

Global Serverless Computing Market – By Geography

North America

U.S.

Canada

Mexico

Europe

U.K.

France

Germany

Italy

Rest of Europe

Asia-Pacific

Japan

China

India

Australia

Rest of Asia Pacific

ROW

Latin America

Middle East

Africa

New Business Strategies, Challenges & Policies are mentioned in Table of Content, Request TOC at @ https://www.decisionforesight.com/toc-request/DFS020230

Geographic Analysis:

North America dominates the market by contributing the largest serverless computing market share of 42.09% attributed to the presence of prominent players in the U.S such as Amazon Web Services, Inc., Google LLC, and CA Technologies. Large number of industries such as BFSI, manufacturing, healthcare, and retail boosts the user base in this region. Therefore, the competitive dynamic market compels the enterprises to deliver new products with innovative features thus leading to the adoption of new technologies. This in turn helped North American region to dominate in the serverless computing market.

Competitive Scenario:

Some of the major key players in the serverless computing industry are Alibaba Cloud, Amazon Web Services, Inc., CA Technologies, Google LLC, and IBM Corporation, Microsoft Corporation, Oracle Corporation, Dynatrace, Fiorano Software, Inc., Joyent Inc., ModuBiz Ltd, NTT Data Corporation, Rackspace Inc., TIBCO Software Inc., and Twistlock Inc.

Connect to Analyst @ https://www.decisionforesight.com/speak-analyst/DFS020230

How will this Market Intelligence Report Benefit You?

The report offers statistical data in terms of value (US$) as well as Volume (units) till 2030.

Exclusive insight into the key trends affecting the Global Serverless Computing industry, although key threats, opportunities and disruptive technologies that could shape the Global Serverless Computing Market supply and demand.

The report tracks the leading market players that will shape and impact the Global Serverless Computing Market most.

The data analysis present in the Global Serverless Computing Market report is based on the combination of both primary and secondary resources.

The report helps you to understand the real effects of key market drivers or retainers on Global Serverless Computing Market business.

The 2021 Annual Global Serverless Computing Market offers:

100+ charts exploring and analysing the Global Serverless Computing Market from critical angles including retail forecasts, consumer demand, production and more

15+ profiles of top producing states, with highlights of market conditions and retail trends